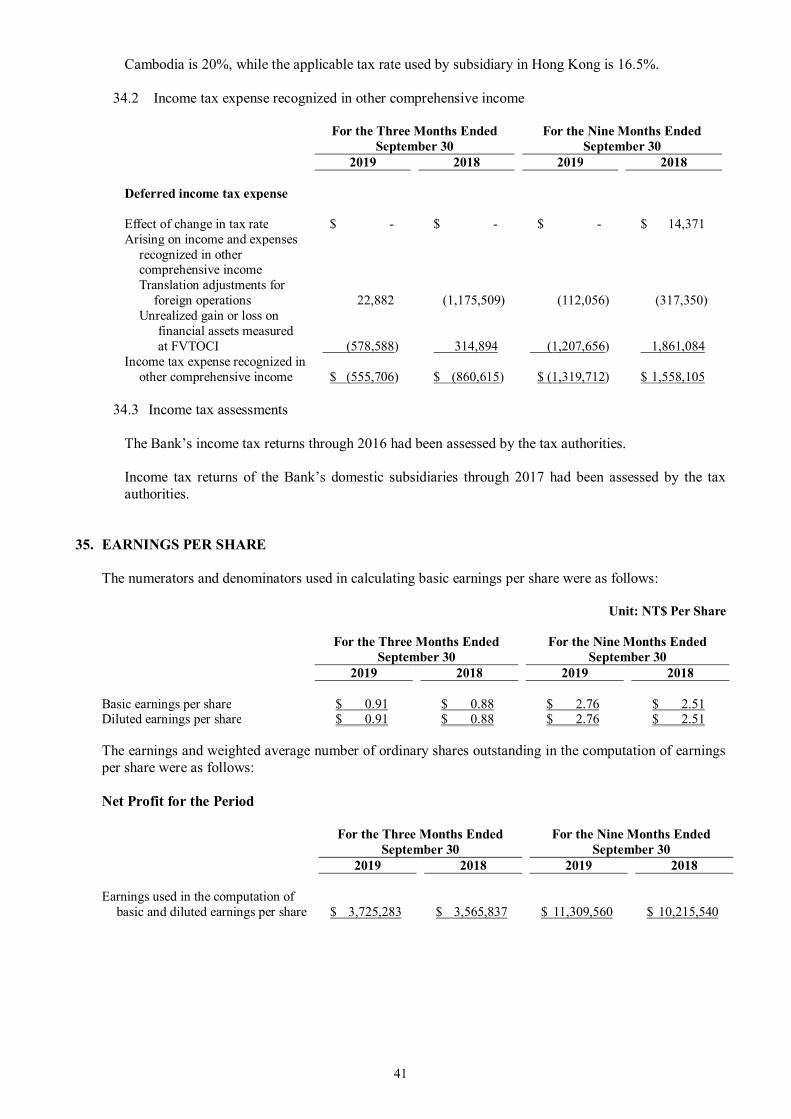

The Shanghai Commercial & Savings Bank, Ltd. and Subsidiaries Financial... · -5- THE SHANGHAI...

92

The Shanghai Commercial & Savings Bank, Ltd. and Subsidiaries Consolidated Financial Statements for the Nine Months Ended September 30, 2019 and 2018 and Independent Auditors’ Review Report Stock code: 5876 Taiwan Stock Exchange Address: No. 2, Sec.1 Min Chuan E. Rd., Taipei, Taiwan Telephone: 886-2-2581-7111

Transcript of The Shanghai Commercial & Savings Bank, Ltd. and Subsidiaries Financial... · -5- THE SHANGHAI...

The Shanghai Commercial & Savings Bank, Ltd. and Subsidiaries Consolidated Financial Statements for the Nine Months Ended September 30, 2019 and 2018 and Independent Auditors’ Review Report

Stock code: 5876 Taiwan Stock Exchange

Address: No. 2, Sec.1 Min Chuan E. Rd., Taipei, Taiwan Telephone: 886-2-2581-7111

-1-

Table of Contents

Contents Page Notes

1. Table of Contents 1 -

2. Independent Auditors’ Review Report 2~3 -

3. Balance Sheets 4 -

4. Statements of Comprehensive Income 5~6 -

5. Statements of Changes in Stockholders’ Equity 7 -

6. Statements of Cash Flows 8~9 -

7. Notes to Financial Statements

(1) Organization and Operations 10 1

(2) Authorization of Financial Statements 10 2

(3) Application of New, Amended and Revised Standards and Interpretations 10~12 3

(4) Summary of Significant Accounting Policies 12~15 4

(5) Critical Accounting Judgments and Key Sources of Estimation Uncertainty 15 5

(6) Summary of Major Accounts 15~45 6~38

(7) Related-Party Transactions 45~48 39

(8) Pledged Assets 48 40

(9) Significant Contingent Liabilities and Unrecognized Commitments 48~50 41

(10) Significant Catastrophic Losses - -

(11) Significant Subsequent Events - -

(12) Others 50~79 42~48

(13) Disclosure Required

(a) Related Information on Significant Transactions 79~80 82~86

49

(b) Related Information on Investee Companies 80 49

(c) Related Information on Investments in Mainland China 80.87 49

(d) Related Information on Intercompany Relationships and Significant Intercompany Transactions

80 88~91

49

(14) Segment Information 81 50

-2-

INDEPENDENT AUDITORS’ REVIEW REPORT The Board of Directors and Shareholders The Shanghai Commercial & Savings Bank, Ltd. Taipei, Taiwan Introduction We have reviewed the accompanying consolidated balance sheets of The Shanghai Commercial & Savings Bank, Ltd. (the “Bank”) and its subsidiaries (collectively, the “Group”) as of September 30, 2019 and 2018, the related consolidated statements of comprehensive income for the three months ended September 30, 2019 and 2018 and the nine months ended September 30, 2019 and 2018, the consolidated statements of changes in equity and cash flows for the nine months ended September 30, 2019 and 2018, and the related notes to the consolidated financial statements, including a summary of significant accounting policies (collectively referred to as the consolidated financial statements). Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with the Regulations Governing the Preparation of Financial Reports by Public Banks, and International Accounting Standard 34 “Interim Financial Reporting” endorsed and issued into effect by the Financial Supervisory Commission of Taiwan (R.O.C). Our responsibility is to express a conclusion on the consolidated financial statements based on our reviews. Scope of Review We conducted our reviews in accordance with Statement of Auditing Standards No. 65 “Review of Financial Information Performed by the Independent Auditor of the Entity”. A review of consolidated financial statements consists of making inquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion. Conclusion Based on our reviews, nothing has come to our attention that caused us to believe that the accompanying consolidated financial statements do not present fairly, in all material respects, the consolidated financial position of the Group as of September 30, 2019 and 2018, and of its consolidated financial performance for the three months ended September 30, 2019 and 2018, and its consolidated financial performance and its consolidated cash flows for the nine months ended September 30, 2019 and 2018 in accordance with the Regulations Governing the Preparation of Financial Reports by Public Banks, and International Accounting Standard 34 “Interim Financial Reporting” endorsed and issued into effect by the Financial Supervisory Commission of Taiwan (R.O.C).

-3-

Emphasis of Matter As stated in Note 37 to the consolidated financial statements, the Group had not completed the acquisition purchase price allocation report when submitted to the board of directors in the third quarter of 2018, and the relevant accounting treatment was only tentative. The purchase price allocation report was completed in March, 2019.Therefore, the financial statements of the comparative period was retrospectively reviewed in accordance with the provisions of the IFRS 3 Business Combination. The accountant did not correct the review conclusions as a result. The engagement partners on the reviews resulting in this independent auditors’ reviews report are Chun-Hung Chen and Tzu-Jung Kuo. Deloitte & Touche Taipei, Taiwan Republic of China November 8, 2019

Notice to Readers The accompanying consolidated financial statements are intended only to present the consolidated financial position, financial performance and cash flows in accordance with accounting principles and practices generally accepted in Taiwan (R.O.C) and not those of any other jurisdictions. The standards, procedures and practices to review audit such consolidated financial statements are those generally applied in Taiwan (R.O.C). For the convenience of readers, the independent auditors’ review report and the accompanying consolidated financial statements have been translated into English from the original Chinese version prepared and used in Taiwan (R.O.C). If there is any conflict between the English version and the original Chinese version or any difference in the interpretation of the two versions, the Chinese-language independent auditors’ review report and consolidated financial statements shall prevail.

-4-

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES Consolidated Balance Sheets

September 30, 2019, December 31, 2018 and September 30, 2018 (Expressed in Thousands of New Taiwan Dollars)

September 30, 2019 (Reviewed)

December 31, 2018 (Audited)

September 30, 2018 (Restatement and Reviewed)

Codes ASSETS Amount % Amount % Amount % 11000 Cash and cash equivalents (Note 6) $49,330,482 3 $60,496,417 3 $70,365,291 4 11500 Due from the Central Bank and call loans to banks (Note 7) 215,997,804 11 191,069,205 10 211,840,511 12 12000 Financial assets measured at fair value through profit or loss (Note 8) 11,567,168 1 13,580,032 1 14,198,240 1 12100 Financial assets measured at fair value through other comprehensive income (Notes 9, 11 and 40) 466,674,454 23 436,008,517 23 401,643,697 22 12200 Investments in debt instruments measured at amortized cost (Notes 10, 11 and 40) 110,456,425 5 106,071,194 6 95,868,572 5 12500 Securities purchased under resale agreements (Note 12) 1,337,883 - 438,017 - 144,875 - 13000 Receivables, net (Notes 13 and 39) 18,015,451 1 16,993,738 1 20,895,984 1 13200 Current income tax assets (Note 34) 171,312 - 89,235 - 197,906 - 13500 Discounts and loans, net (Notes 14 and 39) 1,122,778,206 55 1,029,803,185 55 1,005,598,124 54 15000 Investments under the equity method, net (Note 16) 1,898,927 - 1,738,636 - 1,573,700 - 15500 Other financial assets, net (Note 17) 5,659,144 - 2,461,333 - 860 - 18500 Properties, net (Note 18) 21,390,471 1 21,546,669 1 21,489,205 1 18600 Right-of-use assets, net (Note 19) 2,453,841 - - - - - 18700 Investment properties, net (Note 20) 5,775,231 - 5,661,390 - 5,457,708 - 19000 Intangible assets, net (Note 21) 1,864,894 - 1,837,331 - 1,820,970 - 19300 Deferred income tax assets (Note 34) 767,667 - 1,325,996 - 1,192,611 - 19500 Other assets, net (Note 22) 3,553,151 - 3,288,862 - 3,313,570 - 10000 Total assets $2,039,692,511 100 $1,892,409,757 100 $1,855,601,824 100 Codes LIABILITIES AND EQUITY 21000 Due to the Central Bank and banks (Note 23) $82,990,566 4 $60,263,330 3 $57,422,943 3 22000 Financial liabilities measured at fair value through profit or loss (Note 8) 4,023,657 - 3,781,474 - 2,062,314 - 22500 Securities sold under repurchase agreements (Note 24) 12,808,245 1 14,629,530 1 25,306,706 2 23000 Payables (Notes 25 and 39) 31,417,900 2 30,113,575 2 31,552,165 2 23200 Current income tax liabilities (Note 34) 2,007,679 - 1,168,875 - 2,375,139 - 23500 Deposits and remittances (Notes 26 and 39) 1,610,210,195 79 1,520,625,615 80 1,486,492,676 80 24000 Bank debentures (Note 27) 79,114,628 4 64,785,252 4 57,723,924 3 25500 Other financial liabilities (Note 28) 3,664,819 - 4,211,038 - 4,099,869 - 25600 Provisions (Note 29) 2,585,046 - 2,385,217 - 2,312,427 - 26000 Lease liabilities (Note 19) 2,521,803 - - - - - 29300 Deferred income tax liabilities (Note 34) 10,031,136 - 9,411,303 1 9,087,094 1 29500 Other liabilities (Notes 30 and 39) 3,871,778 - 3,012,622 - 3,868,985 - 20000 Total liabilities 1,845,247,452 90 1,714,387,831 91 1,682,304,242 91 Equity (Note 32) Equity attributable to owners of the Bank

Share capital 31101 Ordinary shares 41,016,031 2 41,016,031 2 40,791,031 2 31111 Capital collected in advance 1,643,259 - - - - - 31500 Capital surplus 10,624,510 1 5,893,238 1 5,351,666 -

Retained earnings 32001 Legal reserve 51,946,585 3 47,832,994 3 47,832,994 3 32003 Special reserve 7,669,374 - 7,600,814 - 7,600,814 - 32005 Unappropriated earnings 22,312,022 1 23,499,036 1 20,126,458 1 32000 Total retained earnings 81,927,981 4 78,932,844 4 75,560,266 4 32500 Other equity 8,869,606 - 5,396,978 - 5,850,614 1 32600 Treasury shares (83,144 ) - (83,144 ) - (83,144 ) - 31000 Total equity attributable to owners of the Bank 143,998,243 7 131,155,947 7 127,470,433 7 38000 Non-controlling interests 50,446,816 3 46,865,979 2 45,827,149 2 30000 Total equity 194,445,059 10 178,021,926 9 173,297,582 9 Total liabilities and equity 2,039,692,511 100 1,892,409,757 100 1,855,601,824 100

The accompanying notes are an integral part of the consolidated financial statements.

-5-

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES Consolidated Statements of Comprehensive Income

For the nine months ended September 30, 2019 and 2018(Reviewed, Not Audited) (Expressed in Thousands of New Taiwan Dollars, Except Earnings Per Share)

For the Three Months Ended September 30 For the Nine Months Ended September 30 2019(Reviewed) 2018(Restatement) 2019(Reviewed) 2018(Restatement) Codes Amount % Amount % Amount % Amount % 41000 Interest revenue $13,188,618 121 $10,954,440 116 $37,817,885 120 $30,391,712 110 51000 Interest expenses 5,404,852 49 3,871,979 41 15,550,972 49 10,257,258 37 49010 Net interest (Notes 33 and 39) 7,783,766 72 7,082,461 75 22,266,913 71 20,134,454 73 Non-interest revenue 49100 Service fee income, net (Note 33) 1,741,887 16 1,200,785 13 5,330,391 17 4,071,198 15 49200 Gain on financial assets and liabilities measured at

fair value through profit or loss (Note 33) 166,326 1 90,700 1 579,267 2 (12,432) - 49310 Realized gain on financial assets measured at fair

value through other comprehensive income (Note 33) 420,161 4 398,999 4 1,286,759 4 1,034,613 4 49450 Loss on financial assets measured at amortized cost (215) - (138) - (215) - (1,807) - 49600 Foreign exchange gain, net 499,464 5 324,563 3 1,207,199 4 1,195,447 4 49700 Impairment gain(loss) on assets (Note 11) 9,503 - (14,402) - 5,376 - (22,237) - 49750 Proportionate share of profit of subsidiaries,

associates and joint ventures under the equity method, net (Note 16) (8,884) - (808) - 99,505 - 124,823 -

49800 Other non-interest revenue (Note 39) 269,331 2 394,289 4 754,463 2 994,305 4 49020 Total non-interest revenue 3,097,573 28 2,393,988 25 9,262,745 29 7,383,910 27 4xxxx Consolidated net revenue 10,881,339 100 9,476,449 100 31,529,658 100 27,518,364 100 58200 Provisions for bad-debt expense, commitment and

guarantee liability (Note 14) 275,228 3 151,876 1 852,705 3 517,510 2

Operating expenses 58500 Employee benefits (Notes 31, 33 and 39) 2,708,642 25 2,090,042 22 7,175,552 23 5,864,278 21 59000 Depreciation and amortization (Note 33) 413,470 4 203,105 2 1,235,242 4 606,397 2 59500 Other general and administrative 1,161,544 10 1,187,433 13 3,294,672 10 3,447,158 13 58400 Total operating expenses 4,283,656 39 3,480,580 37 11,705,466 37 9,917,833 36 61001 Profit before income tax 6,322,455 58 5,843,993 62 18,971,487 60 17,083,021 62 61003 Income tax expense (Note 34) (1,248,679) (11) (1,078,720) (12) (3,702,310) (12) (3,469,687) (13) 64000 Consolidated net income 5,073,776 47 4,765,273 50 15,269,177 48 13,613,334 49 Other comprehensive income (loss) Items that will not be reclassified subsequently to

profit or loss: 65204 Gain on investments in equity instruments measured at fair value through other comprehensive income $277,959 2 $1,146,923 12 $860,874 3 $1,943,620 7 65205 Financial liabilities designated at FVTPL which the amount of change derived from credit risk (Note 8) (15,796) - - - (26,112) - - -

-6-

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES Consolidated Statements of Comprehensive Income

For the nine months ended September 30, 2019 and 2018(Reviewed, Not Audited) (Expressed in Thousands of New Taiwan Dollars, Except Earnings Per Share)

The accompanying notes are an integral part of the consolidated financial statements. (Concluded)

For the Three Months Ended September 30 For the Nine Months Ended September 30 2019(Reviewed) 2018(Restatement) 2019(Reviewed) 2018(Restatement) Codes Amount % Amount % Amount % Amount % 65206 Proportionate share of other comprehensive income

of associates and joint ventures under the equity method 1 - (42) - (51) - (31) -

65220 Income tax relating to items that may not be reclassified subsequently to profit or loss (Note 34) 7,186 - 37,704 1 (21,665) - 1,601,464 6

65200 Subtotal of items that will not be reclassified subsequently to profit or loss 269,350 2 1,184,585 13 813,046 3 3,545,053 13

Items that may be reclassified subsequently to profit

or loss: 65301 Exchange differences on translating foreign operations (109,542) (1) 587,048 6 1,139,464 4 2,813,582 10

65306 Share of the other comprehensive income of associates and joint ventures accounted for using the equity method 18,476 - 834 - 64,187 - (35,159) -

65309 Gain(loss) on debt instruments measured at fair value through other comprehensive income 287,793 3 101,544 1 3,972,569 12 (1,727,515) (6) 65310 Loss allowance on debt instruments measured at fair value through other comprehensive income (Note 11) (9,416) - 14,962 - (4,705) - 22,174 -

65320 Income tax relating to items that may be reclassified subsequently to profit or loss (Note 34) (562,892) (5) (898,319) (9) (1,298,047) (4) (43,359) -

65300 Subtotal of items that may be reclassified subsequently to profit or loss (375,581) (3) (193,931) (2) 3,873,468 12 1,029,723 4

65000 Other comprehensive income (loss) for the period, net of income tax (106,231) (1) 990,654 11 4,686,514 15 4,574,776 17

66000 Total comprehensive income for the period $4,967,545 46 $5,755,927 61 $19,955,691 63 $18,188,110 66 Net profit attributable to: 67101 Owners of the Bank $3,725,283 34 $3,565,837 37 $11,309,560 36 $10,215,540 37 67111 Non-controlling interests 1,348,493 13 1,199,436 13 3,959,617 12 3,397,794 12 67100 $5,073,776 47 $4,765,273 50 $15,269,177 48 $13,613,334 49 Total comprehensive income attributable to: 67301 Owners of the Bank $3,845,796 36 $4,020,811 43 $14,693,768 46 $12,086,174 44 67311 Non-controlling interests 1,121,749 10 1,735,116 18 5,261,923 17 6,101,936 22 67300 $4,967,545 46 $5,755,927 61 $19,955,691 63 $18,188,110 66 Earnings per share (Note 35) 67500 Basic $0.91 $0.88 $2.76 $2.51 67700 Diluted $0.91 $0.88 $2.76 $2.51

-7-

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES Consolidated Statements of Changes in Equity

For the nine months ended September 30, 2019 and 2018(Reviewed, Not Audited) (Expressed in Thousands of New Taiwan Dollars)

Equity Attributable to Owners of the Bank (Note 3 and Note 32) Codes Share Capital Retained Earnings Other Equity

Change in Change in

Exchange

Differences on Unrealized Gain

(Loss) on Financial Assets at

Fair Value Credit Risk From

Financial Total Equity Capital Translating Available-for- Through Other Liabilities Attributable to Non-controlling Ordinary Collected Unappropriated Foreign sale Financial Comprehensive Designated at Owners of the Interests Shares in Advance Capital Surplus Legal Reserve Special Reserve Earnings Operations Assets Income FVTPL Treasury Shares Bank (Note 32) Total Equity

A1 Balance at January 1, 2018 $ 40,791,031 $ - $ 4,655,555 $ 44,117,426 $ 7,538,888 $ 21,066,873 $ (1,564,469) $ 5,887,639 $ - $ - $ (83,144) $ 122,409,799 $ 40,623,295 $ 163,033,094 A3 Effect of retrospective application and retrospective restatement - - - - - 55,374 - (5,887,639) 5,453,000 - - (379,265) (16,386) (395,651) A5 Balance at January 1, 2018 as restated 40,791,031 - 4,655,555 44,117,426 7,538,888 21,122,247 (1,564,469) - 5,453,000 - (83,144) 122,030,534 40,606,909 162,637,443 Appropriation of 2017 earnings B1 Legal reserve - - - 3,715,568 - (3,715,568) - - - - - - - - B3 Special reserve - - - - 61,926 (61,926) - - - - - - - - B5 Cash dividends - - - - - (7,342,386) - - - - - (7,342,386) - (7,342,386) C7 Changes in capital surplus from investments in associates and

joint ventures accounted for using the equity method - - 9,480 - - - - - - - - 9,480 - 9,480

C17 Dividends not yet collected - - 686,631 - - - - - - - - 686,631 - 686,631 D1 Net profit for the nine months ended September 30, 2018 - - - - - 10,215,540 - - - - - 10,215,540 3,397,794 13,613,334 D3 Other comprehensive income for the nine months ended

September 30, 2018, net of income tax - - - - - 10,843 957,909 - 901,882 - - 1,870,634 2,704,142 4,574,776

D5 Total comprehensive income for the nine months ended

September 30, 2018 - - - - - 10,226,383 957,909 - 901,882 - - 12,086,174 6,101,936 18,188,110

Q1 Disposal of equity instruments at fair value through other

comprehensive income - - - - - (102,292) - - 102,292 - - - - -

O1 Changes in non-controlling interests - - - - - - - - - - - - (881,696) (881,696) Z1 Balance at September 30, 2018 $ 40,791,031 $ - $ 5,351,666 $ 47,832,994 $ 7,600,814 $ 20,126,458 $ (606,560) $ - $ 6,457,174 $ - $ (83,144) $ 127,470,433 $ 45,827,149 $ 173,297,582 A1 Balance at January 1, 2019 $ 41,016,031 $ - $ 5,893,238 $ 47,832,994 $ 7,600,814 $ 23,499,036 $ (165,709) $ - $ 5,562,687 $ - $ (83,144) $ 131,155,947 $ 46,865,979 $ 178,021,926 A3 Effect of retrospective application and retrospective restatement - - - - - (22,797) - - - - - (22,797) (15,229) (38,026) A5 Balance at January 1, 2019 as restated 41,016,031 - 5,893,238 47,832,994 7,600,814 23,476,239 (165,709) - 5,562,687 - (83,144) 131,133,150 46,850,750 177,983,900 Appropriation of 2018 earnings B1 Legal reserve - - - 4,113,591 - (4,113,591) - - - - - - - - B3 Cash dividends - - - - 68,560 (68,560) - - - - - - - - B5 Share dividends - - - - - (8,203,206) - - - - - (8,203,206) - (8,203,206) C7 Changes in capital surplus from investments in associates and

joint ventures accounted for using the equity method - - 10,534 - - - - - - - - 10,534 - 10,534

M7 Changes in equity of subsidiaries - - 85,518 - - - - - - - - 85,518 (85,518) - D1 Net profit for the nine months ended September 30, 2019 - - - - - 11,309,560 - - - - - 11,309,560 3,959,617 15,269,177 D3 Other comprehensive income (loss) for the nine months ended

September 30, 2019, net of income tax - - - - - - 289,123 - 3,121,197 (26,112) - 3,384,208 1,302,306 4,686,514

D5 Total comprehensive income (loss) for the nine months ended

September 30, 2019 - - - - - 11,309,560 289,123 - 3,121,197 (26,112) - 14,693,768 5,261,923 19,955,691

E1 Issue of ordinary shares for capital increase by cash - 1,643,259 4,635,220 - - - - - - - - 6,278,479 - 6,278,479 Q1 Disposal of equity instruments at fair value through other

comprehensive income - - - - - (88,420) - - 88,420 - - - - -

O1 Changes in non-controlling interests - - - - - - - - - - - - (1,580,339) (1,580,339) Z1 Balance at September 30, 2019 $ 41,016,031 $ 1,643,259 $ 10,624,510 $ 51,946,585 $ 7,669,374 $ 22,312,022 $ 123,414 $ - $ 8,772,304 $ (26,112) $ (83,144) $ 143,998,243 $ 50,446,816 $ 194,445,059 The accompanying notes are an integral part of the consolidated financial statements.

-8-

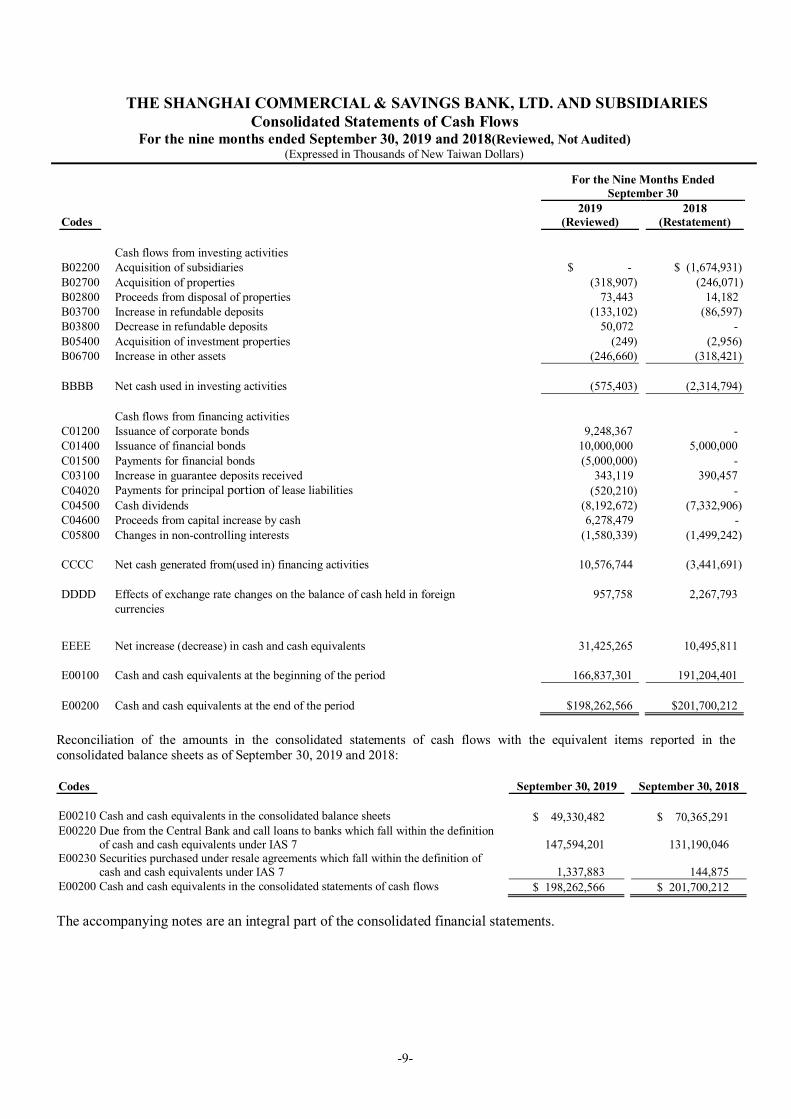

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES

Consolidated Statements of Cash Flows For the nine months ended September 30, 2019 and 2018(Reviewed, Not Audited)

(Expressed in Thousands of New Taiwan Dollars)

(Continued)

For the Nine Months Ended September 30

Codes 2019

(Reviewed) 2018

(Restatement)

Cash flows from operating activities A00010 Consolidated net profit before income tax $18,971,487 $17,083,021 A20010 Adjustments to reconcile net profit to net cash provided by operating activities A20100 Depreciation expenses 1,074,837 445,906 A20200 Amortization expenses 160,405 160,491 A20300 Bad debt expense, commitment and guarantee liability provisions 852,705 517,510 A21400 Loss(gain) on expected credit impairment (5,376) 22,237 A20400 Loss(gain) on financial assets and liabilities at fair value through profit or loss (255,211) 365,429 A20900 Interest expenses 15,550,972 10,257,258 A21200 Interest revenue (37,817,885) (30,391,711) A21300 Dividend income (981,124) (593,391) A22400 Proportionate share of profit of associates and joint ventures (99,505) (124,823) A22500 Loss(gain) on disposal of properties and equipment, net (18,768) 8,014 A29900 Other adjustments (326,709) (447,686) A40000 Changes in operating assets and liabilities A41110 Decrease in due from the Central Bank and call loans to banks 17,424,710 9,476,553 A41120 Decrease(increase) in financial assets measured at fair value through profit or loss 2,369,040 (998,790) A41123 Increase in financial assets measured at fair value through other comprehensive

income (28,397,803) (50,906,936) A41125 (Increase) decrease in investments in debt instrument measured at amortized cost (1,132,095) 16,103,181

A41150 Increase in receivables (1,515,473) (3,894,561) A41160 Increase in discounts and loans (91,009,417) (72,484,221) A41190 (Increase)decrease in other financial assets (3,197,787) 4,954 A42110 Increase in due to the Central Bank and banks 22,295,122 21,700,905 A42120 Increase in financial liabilities at fair value through profit or loss 173,720 1,201,151 A42140 Decrease in securities sold under repurchase agreements (1,821,285) (4,485,361) A42150 (Decrease) increase in payables (129,013) 2,301,702 A42160 Increase in deposits and remittances 84,876,482 78,658,185 A42170 (Decrease) increase in other financial liabilities (950,393) 850,063 A42180 Increase in employee benefit provisions 111,067 78,131 A42990 Increase in other liabilities 1,008,400 125,725

A33000 Cash used in operations (2,788,897) (4,967,064)

A33100 Interest received 38,495,149 30,320,761 A33200 Dividends received 981,124 593,391 A33300 Interest paid (14,199,879) (9,184,325) A33500 Income tax paid (2,021,331) (2,778,260)

AAAA Net cash generated from operating activities 20,466,166 13,984,503

-9-

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES Consolidated Statements of Cash Flows

For the nine months ended September 30, 2019 and 2018(Reviewed, Not Audited) (Expressed in Thousands of New Taiwan Dollars)

Reconciliation of the amounts in the consolidated statements of cash flows with the equivalent items reported in the consolidated balance sheets as of September 30, 2019 and 2018: Codes September 30, 2019 September 30, 2018

E00210 Cash and cash equivalents in the consolidated balance sheets $ 49,330,482 $ 70,365,291 E00220 Due from the Central Bank and call loans to banks which fall within the definition

of cash and cash equivalents under IAS 7

147,594,201 131,190,046 E00230 Securities purchased under resale agreements which fall within the definition of

cash and cash equivalents under IAS 7

1,337,883 144,875 E00200 Cash and cash equivalents in the consolidated statements of cash flows $ 198,262,566 $ 201,700,212

The accompanying notes are an integral part of the consolidated financial statements.

For the Nine Months Ended September 30

Codes 2019

(Reviewed) 2018

(Restatement)

Cash flows from investing activities B02200 Acquisition of subsidiaries $ - $ (1,674,931) B02700 Acquisition of properties (318,907) (246,071) B02800 Proceeds from disposal of properties 73,443 14,182 B03700 Increase in refundable deposits (133,102) (86,597) B03800 Decrease in refundable deposits 50,072 - B05400 Acquisition of investment properties (249) (2,956) B06700 Increase in other assets (246,660) (318,421) BBBB Net cash used in investing activities (575,403) (2,314,794) Cash flows from financing activities C01200 Issuance of corporate bonds 9,248,367 - C01400 Issuance of financial bonds 10,000,000 5,000,000 C01500 Payments for financial bonds (5,000,000) - C03100 Increase in guarantee deposits received 343,119 390,457 C04020 Payments for principal portion of lease liabilities (520,210) - C04500 Cash dividends (8,192,672) (7,332,906) C04600 Proceeds from capital increase by cash 6,278,479 - C05800 Changes in non-controlling interests (1,580,339) (1,499,242) CCCC Net cash generated from(used in) financing activities 10,576,744 (3,441,691) DDDD Effects of exchange rate changes on the balance of cash held in foreign 957,758 2,267,793 currencies

EEEE Net increase (decrease) in cash and cash equivalents 31,425,265 10,495,811 E00100 Cash and cash equivalents at the beginning of the period 166,837,301 191,204,401 E00200 Cash and cash equivalents at the end of the period $198,262,566 $201,700,212

10

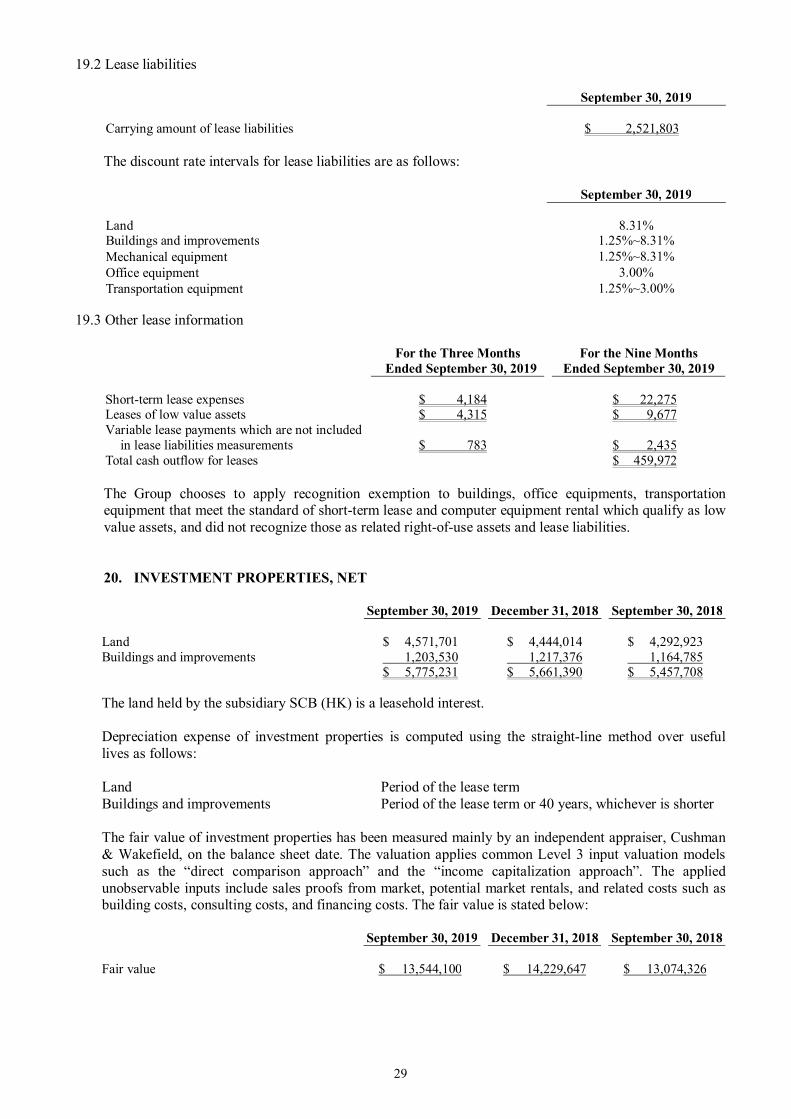

THE SHANGHAI COMMERCIAL & SAVINGS BANK, LTD. AND SUBSIDIARIES Notes to Consolidated Financial Statements

For the nine months ended September 30, 2019 and 2018(Reviewed, Not Audited) (Expressed in thousands of New Taiwan Dollars, unless otherwise stated)

1. ORGANIZATION AND OPERATIONS

The Shanghai Commercial & Savings Bank (the “Bank”) was incorporated in Taiwan and engaged in the commercial banking businesses under related laws and regulations. The Bank has a head office in Taipei, 71 domestic branches, 3 foreign branches located in Hong Kong, Vietnam and Singapore, and 3 representative offices located in Thailand, Cambodia and Indonesia. The operations of the Bank’s trust department include services related to planning, managing and operating a trust business under the Banking Act and Trust Enterprise Act. The shares of the Bank have been listed and traded on the Taiwan Stock Exchange since October 19, 2018. The consolidated financial statements are presented in the Bank’s functional currency, the New Taiwan dollar. In order to integrate the use of resources and achieve operating synergy, the Bank merged SCSB Life Insurance Agency and SCSB Property Insurance Agency on May 6, 2019, which were both 100% owned by the Bank. The shareholder’s equity would not be affected after the merger, refer to Note 48.

2. AUTHORIZATION OF CONSOLIDATED FINANCIAL STATEMENTS On November 8, 2019, the consolidated financial statements were approved by the board of directors and issued afterward.

3. APPLICATION OF NEW, AMENDED AND REVISED STANDARDS AND INTERPRETATIONS 3.1 Initial application of the amendments to the Regulations Governing the Preparation of Financial

Reports by Securities Issuers and the International Financial Reporting Standards (IFRS), International Accounting Standards (IAS), IFRIC Interpretations (IFRIC), and SIC Interpretations (SIC) (collectively, the “IFRSs”) endorsed and issued into effect by the Financial Supervisory Commission (FSC). Aside from the following explanations, the applicable amendments to the Regulations Governing the Preparation of Financial Reports by Public Banks and the IFRSs approved and issued by the FSC will not result in significant changes to the Bank's accounting policies: IFRS 16 “Lease” IFRS 16 sets out the identification of lease agreements and the accounting standards for lessor and lessee that will supersede IAS 17 and a number of related interpretations. For the related accounting policy, see Note 4. Definition of Lease When applying IFRS 16 for the first time, the Bank will choose whether a contract signed or changed on or after January 1, 2019 will be assessed as a lease according to IFRS 16. Currently, lease contracts under IAS 17 and IFRIC 4 are not allowed to be reassessed, which should be processed in accordance with the transitional provisions of IFRS 16.

11

The Bank as lessee

When IFRS 16 is applied, leases are recognized as the right-of-use assets and lease liabilities in the consolidated balance sheets, except for the low value underlying asset leases and short-term leases, which are recognized under a straight-line basis. However, assets, which are eligible for use under the definition of investment real estate, will be presented as investments in real estate.

The consolidated comprehensive income statements will represent the depreciation expense of the right-of-use assets and the interest expense arising from the effective interest method on the lease liabilities separately.

In the consolidated cash flow statements, the principal amount of lease liabilities is expressed as financing activities, and the interest payment portion is classified as operating activities. Prior to the application of IFRS 16, the operating leases were recognized as expenses on a straight-line basis. Operating lease cash flows are expressed in operating activities in the consolidated cash flow statements. Contracts classified as finance leases are recognized in the consolidated balance sheets as lease assets and lease payables. The Group elects to apply IFRS 16 retrospectively with the cumulative effect of the initial application of this standard recognized in retained earnings on January 1, 2019. Comparative information is not restated. In accordance with the agreement of IAS 17 for operating leases, the measurement of lease liabilities on January 1, 2019 had been discounted by the remaining lease payments at the incremental borrowing rate of the lessee at that date. Parts of right-of-use assets were measured at the amount of lease liabilities on that date. Parts of the right-of-use assets were discounted at the aforementioned interest rate and measured as if IFRS 16 had been applied at the commencement date of the lease. The identified right-of-use assets will be subject to an IAS 36 impairment assessment. For the leases classified as financing leases under IAS 17, the carrying amount of the lease assets and lease liabilities on January 1, 2019 was the same as those on December 31, 2018.

The Bank as lessor

No adjustments were made to the lessor's lease during the transition and IFRS 16 was applied from January 1, 2019. The adjustments of assets, liabilities and equities accounts that applied IFRS 16 for the first time are summarized as follows:

Carrying Amount as of

December 31, 2018

Adjustments Arising from Initial Application

Adjusted Carrying Amount as of

January 1, 2019 Other assets, net $ 3,288,862 $ (17,368) $ 3,271,494 Right-of-use assets - 2,092,410 2,092,410 Total effect on assets $ 3,288,862 $ 2,075,042 $ 5,363,904 Accounts payable $ 30,113,575 $ (3,121) $ 30,110,454 Liabilities provisions 2,385,217 2,748 2,387,965 Deferred income tax liabilities 9,411,303 (5,699) 9,405,604 Lease liabilities - 2,119,140 2,119,140 Total effect on liabilities $ 41,910,095 $ 2,113,068 $ 44,023,163 Retained earnings $ 78,932,844 $ (22,797) $ 78,910,047 Non-controlling interests 46,865,979 (15,229) 46,850,750 Total effect on equities $ 125,798,823 $ (38,026) $ 125,760,797

12

3.2 IFRSs approved by the FSC for application starting from 2020

New IFRSs Effective Date

Announced by IASB Amendments to IFRS 3 “Definition of a Business” January 1, 2020 (Note 1) Amendments to IAS 1 and IAS 8 “Definition of Material” January 1, 2020 (Note 2)

Note 1: The Group shall apply these amendments to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after January 1, 2020 and to asset acquisitions that occur on or after the beginning of that period.

Note 2: The Group shall apply these amendments prospectively for annual reporting periods

beginning on or after January 1, 2020. As of the date the consolidated financial statements were authorized for issue, the Group is continuously assessing the possible impact that the application of other standards and interpretations will have on the Group’s financial position and financial performance and will disclose the relevant impact when the assessment is completed.

3.3 New IFRSs in issue but not yet endorsed and issued into effect by the FSC

New IFRSs Effective Date

Announced by IASB (Note 1) Amendments to IFRS 9, IAS39 and IFRS 7 “Inter Bank Offered Rate Change” January 1, 2020 Amendments to IFRS 10 and IAS 28 “Sale or Contribution of Assets between an Investor and its Associate or Joint Venture”

To be determined by IASB

IFRS 17 “Insurance Contracts” January 1, 2021

Note 1: Unless stated otherwise, the above New IFRSs are effective for annual periods beginning on or after their respective effective dates.

As of the date the consolidated financial statements were authorized for issue, the Group is continuously assessing the possible impact that the application of other standards and interpretations will have on the Group’s financial position and financial performance and will disclose the relevant impact when the assessment is completed.

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

4.1 Statement of Compliance

The consolidated financial statements have been prepared in accordance with the Regulations Governing the Preparation of Financial Reports by Public Banks, and IAS 34 “Interim Financial Reporting” as endorsed and issued into effect by the FSC. Under IFRSs, disclosure information included in these interim consolidated financial statements is less than the disclosure information required in a complete set of annual consolidated financial statements.

4.2 Basis of Preparation

The consolidated financial statements have been prepared on the historical cost basis except for financial instruments which are measured at fair value. The fair value measurements are grouped into Levels 1 to 3 based on the degree to which the fair value measurement inputs are observable and the significance of the inputs to the fair value measurement in its entirety, which are described as follows: 4.2.1 Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities;

13

4.2.2 Level 2 inputs are observable parameters other than quoted prices included within Level 1,

either directly (i.e. as prices) or indirectly (i.e. derived from prices); 4.2.3 Level 3 inputs are unobservable inputs for an asset or liability.

4.3 Basis of Consolidation

The consolidated financial statements contain the financial statements of the Bank and the subsidiaries controlled by the Bank. The consolidated statements of comprehensive income have included the operating gains and losses of acquired or divested companies in the current period from the date of acquisition or to the date of disposal. The financial statements of subsidiaries have been adjusted to align their accounting policies with the Bank's accounting policies. In the preparation of the consolidated financial statements, all intra-company transactions, account balances, income and losses have been eliminated. The comprehensive income of the subsidiaries is attributed to the owner of the Bank and non-controlling interests, even if the non-controlling interests have negative balance. For details on subsidiaries, shareholding ratios and business items, refer to Note 15.

4.4 Other Significant Accounting Policies

Except for lease related accounting policies and the following the accounting policies applied in these consolidated financial statements are consistent with those applied in the consolidated financial statements for the year ended December 31, 2018. For the summary of other significant accounting policies, refer to the consolidated financial statements for the year ended December 31, 2018.

4.4.1 Retirement benefits Pension cost for an interim period is calculated on a year-to-date basis by using the actuarially determined annual pension cost rate at the end of the prior financial year, adjusted for significant market fluctuations since that time and for significant plan amendments, settlements, or other significant one-off events. 4.4.2 Taxation Income tax expense represents the sum of the tax currently payable and deferred tax. Interim period income taxes are assessed on an annual basis and calculated by applying to an interim period's pre-tax income the tax rate that would be applicable to expected total annual earnings. 4.4.3 Properties In order to cope with the redevelopment of the head office building, the original building is expected to be demolished in January 2020. Based on this actual situation, the Group re-evaluated the durability period of the accounting items “ Properties –Buildings” of the original building, and proposed to change its estimated useful life by amortizing the unreduced book value of $159,069 thousand from the original accounting item of the building before end of 2019. This matter was approved by the competent authority and applied on October 17, 2019. 4.4.4 Leases

2019 The Group assesses whether the contract is (or includes) the lease on the contract establishment date. For contracts that include the lease and non-lease components, the Group distributes the consideration in the contract on a relatively separate price basis and deals with them separately.

14

(1) The Group as lessor

When the lease terms transfer almost all the risks and rewards attached to the ownership of the assets to the lessee, they are classified as finance leases. All other leases are classified as operating leases. Under finance leases, lease payments include fixed payments, substantially fixed payments, variable lease payments which depend on an index or a rate, guaranteed residual values, and the exercise price of the purchase option that is reasonably certain to be exercised, and the rental termination penalties reflected in the lease term, less the incentives for the lease to be paid. The net amount of the leased investment is measured as the sum of the present value of both the lease receivable and the unguaranteed residual value plus the original direct costs and expressed as a finance lease receivable. The financing income is apportioned to each accounting period so as to reflect a periodic fixed rate of return that the Group's unexpired net lease investment is available for each period. Under operating leases, the lease payments deducted from the lease incentives are recognized as income on a straight-line basis over the relevant lease periods. The original direct costs incurred in obtaining the operating leases are added to the carrying amount of the underlying assets and recognized as an expense on a straight-line basis over the lease terms.

(2) The Group as lessee

The Group recognizes right-of-use assets and lease liabilities for all leases at the commencement date of a lease, except for short-term leases and low value asset leases accounted for applying a recognition exemption where lease payments are recognized as expenses on a straight line basis over the lease terms. Right-of-use assets are initially measured at cost, which comprises the initial measurement of lease liabilities adjusted for lease payments made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs needed to restore the underlying assets, and less any lease incentives received. Right-of-use assets are subsequently measured at cost less accumulated depreciation and impairment losses and adjusted for any remeasurement of the lease liabilities.

Right-of-use assets are depreciated using the straight-line basis from the commencement dates of the lease to the earlier of the end of the useful lives of the right-of-use assets or the end of the lease terms. Lease liabilities are initially measured at the present value of the lease payments, which comprise fixed payments, substantially fixed payments, variable lease payments which depend on an index or a rate, residual value guarantees, the exercise price of a purchase option if the Group is reasonably certain to exercise that option, and payments of penalties for terminating a lease if the lease term reflects such termination, less any lease incentives receivable. The lease payments are discounted using the interest rate implicit in a lease, if that rate can be readily determined. If that rate cannot be readily determined, the Group uses the lessee’s incremental borrowing rate. Subsequently, lease liabilities are measured at amortized cost using the effective interest method, with interest expense recognized over the lease terms. When there is a change in the amounts expected to be payable under a residual value guarantee, a change in the assessment of an option to purchase an underlying asset, or a change in future lease payments resulting from a change in an index or a rate used to determine those payments, the Group remeasures the lease liabilities with a corresponding adjustment to the right-of-use assets. However, if the carrying amount of the right-of-use asset has been reduced to zero, the remaining amount of remeasurement is recognized in profit or loss. Lease liabilities are presented separately in the consolidated balance sheets.

15

2018

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases. (1) The Group as lessor

Rental income from operating leases is recognized on a straight-line basis over the term of the relevant lease.

(2) The Group as lessee

Operating lease payments are recognized as an expense on a straight-line basis over the lease term.

5. CRITICAL ACCOUNTING JUDGMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY In the application of the Bank's accounting policies, the management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

Estimated impairment of financial assets Estimates of impairment on loans and receivables are based on management’s assumptions about default rates and expected loss rates. The Bank considers historical experience, current market conditions and forward-looking information to make assumptions and select input values for impairment assessments. Refer to Note 42 for the important assumptions and input values used. If the actual cash flows in the future are less than expected, significant impairment losses may occur.

6. CASH AND CASH EQUIVALENTS

September 30, 2019 December 31, 2018 September 30, 2018 Cash on hand and working fund $ 8,734,127 $ 8,598,419 $ 8,512,794 Notes and checks in clearing 1,926,741 3,105,616 3,354,229 Due from other banks 38,669,614 48,792,382 58,498,268 $ 49,330,482 $ 60,496,417 $ 70,365,291 The reconciliation of the amounts of cash and cash equivalents reported in the consolidated statements of cash flows and consolidated balance sheets as of December 31, 2018 is shown below. For the reconciliation of the period ended September 30, 2019 and 2018, refer to the consolidated statements of cash flows.

16

December 31, 2018 Cash and cash equivalents in consolidated balance sheets $ 60,496,417 Due from the Central Bank and call loans to banks which are categorized as cash and cash

equivalents under IAS 7 105,902,867 Securities purchased under resale agreements which are categorized as cash and cash

equivalents under IAS 7 438,017 Cash and cash equivalents $ 166,837,301 The Group assesses the allowance for cash and cash equivalents based on the expected credit loss model. Due to the low credit risk of cash and cash equivalents, allowance losses are recognized based on the 12-month expected credit losses. On September 30, 2019, December 31 and September 30, 2018, cash and cash equivalents recognized as allowances were in the amounts of $1,869 thousand, $1,505 thousand and $254 thousand, respectively.

7. DUE FROM THE CENTRAL BANK AND CALL LOANS TO BANKS, NET

September 30, 2019 December 31, 2018 September 30, 2018 Call loans to banks $ 182,031,562 $ 162,795,368 $ 181,994,658 Deposit reserves - I 10,051,606 5,825,635 9,008,937 Deposit reserves - II 21,209,002 19,651,176 18,527,161 Deposit reserves - foreign 160,689 158,795 158,389 Due from foreign central banks 2,544,945 2,638,231 2,151,366 $ 215,997,804 $ 191,069,205 $ 211,840,511 Deposit reserves are statutory reserves and determined monthly at prescribed rates based on average balances of customers’ deposits. The entire balance of deposit reserves - II is subject to withdrawal restrictions while no restrictions are placed on other deposit reserves. The Group assesses the allowance for due from the Central Bank and call loans to banks in accordance with the expected credit loss model. Due to the low credit risk of due from the Central Bank and call loans to banks, the loss allowance is recognized as 12-month expected credit losses. On September 30, 2019, December 31 and September 30, 2018, the allowances recognized for the due from the Central Bank and call loans to banks were in the amounts of $1,373 thousand, 2,253 thousand and 10,431 thousand, respectively.

17

8. FINANCIAL INSTRUMENTS AT FAIR VALUE THROUGH PROFIT OR LOSS

September 30, 2019 December 31, 2018 September 30, 2018 Financial assets at fair value through profit

or loss Financial assets measured at fair value

through profit or loss Corporate bonds $ 7,872,706 $ 8,294,566 $ 8,040,206 Forward contracts 1,356,223 1,245,817 1,759,313 Shares 965,735 891,791 808,354 Beneficiary securities 503,849 2,630,218 3,027,662 Interest rate swap contracts 394,476 140,200 48,963 Government bonds 182,744 - 136,955 Option contracts 204,517 284,402 314,266 Others 86,918 93,038 62,521 $ 11,567,168 $ 13,580,032 $ 14,198,240 Financial liabilities at fair value through profit or loss Held-for-trading financial liabilities Forward contracts $ 1,258,976 $ 1,171,737 $ 1,684,052 Option contracts 225,775 319,039 346,459 Others 50,923 48,177 31,803 1,535,674 1,538,953 2,062,314 Financial liabilities designated at fair value through profit or loss Bank debentures 2,487,983 2,242,521 - $ 4,023,657 $ 3,781,474 $ 2,062,314 The Group engages in derivative transactions mainly to accommodate customers’ needs and manage its exposure positions. The financial assets and liabilities at FVTPL contract (nominal) amounts of derivative transactions were as follows: September 30, 2019 December 31, 2018 September 30, 2018 Option contracts $ 286,481,302 $ 212,466,269 $ 223,466,795 Forward contracts 224,211,378 137,644,001 197,733,765 Currency swap contracts 19,950,330 19,892,282 17,353,082 Interest rate swap contracts 2,608,020 2,258,760 266,650 Asset exchange transactions 558,468 1,014,354 854,000 Future contracts 10,176 54,209 11,039

Information for financial liabilities designated by the Bank at FVTPL is as follows (September 30, 2018:

None):

September 30, 2019 December 31, 2018

The difference between the fair value and the maturity value -Fair value $ 2,487,983 $ 2,242,521 -Maturity value 2,550,401 2,250,590 $ (62,418) $ (8,069)

18

Effects of changes in credit risk Current amount of change From January1, 2019 to September 30, 2019 $(26,112) Cumulative amount of change Up to September 30, 2019 $(26,112) The financial liabilities designated by the Bank at FVTPL were the second issuance of unsecured debentures amounting to US$70,000 thousand with a 30-year maturity and a fixed interest rate of 0% on October 29, 2018. On the expiration of 5 years and every subsequent year, the Bank may exercise the option at the agreed redemption price. If the option is not exercised during the period, the payment will be made on the expiration date.

The Bank arranged an interest rate swap contract to reduce the interest rate risk of the aforementioned financial bonds. The interest rate swap contract was measured at fair value and the fair value changes were included in profit or loss. The Bank designated the aforementioned financial bonds as financial liabilities measured at FVTPL for consistencies. The amount of change in the fair value of financial bonds and the combination of financial assets attributable to the changes in the fair value of financial liabilities and the combination of the fair value of financial assets is calculated as the difference between the changes in the fair value of market risk factor. The amount of change in fair value attributable to the market risk factor is calculated using the benchmark yield curve at the balance sheet date. Fair value of financial bonds and combined commodities is based on the benchmark yield curve on the balance sheet date and the estimated credit risk spread by the creditor's interest rate quote on the similar maturity date of the combined company, such that the estimated future cash flow is discounted.

9. FINANCIAL ASSETS AT FAIR VALUE THROUGH OTHER COMPREHENSIVE INCOME

September 30, 2019 December 31, 2018 September 30, 2018 Financial assets at fair value through

other comprehensive income Investments in equity instruments measured

at FVTOCI Shares $ 20,526,185 $ 19,245,827 $ 20,868,009 Investments in debt instruments measured at

FVTOCI Bank debentures 163,630,242 186,430,516 185,737,697 Corporate bonds 143,638,928 103,366,162 90,901,887 Government bonds 105,555,261 81,577,905 60,191,756 Commercial papers 31,794,046 43,122,083 38,181,426 Asset backed securities 1,529,792 274,292 278,708 Treasury bonds - 1,991,732 5,484,214 446,148,269 416,762,690 380,775,688 $ 466,674,454 $ 436,008,517 $ 401,643,697

The Bank invests in ordinary shares for medium- and long-term strategic purposes and expects to make a profit through long-term investments. The management of the Bank considers that if the short-term fair value fluctuations of these investments are included in profit or loss, they are inconsistent with the aforementioned long-term investment plans. Therefore, the designated investments are selected to be measured at FVTOCI.

For the information on credit risk management and impairment assessment of investments in debt instruments at FVTOCI, refer to Note 11. Parts of the aforementioned financial assets at FVTOCI were sold under repurchase agreements as of September 30, 2019, December 31 and September 30, 2018. The par value of bonds and commercial

19

papers sold under repurchase agreements were $12,071,796 thousand, $14,450,800 thousand and $25,104,500 thousand, respectively. For the information on financial assets pledged at FVTOCI, refer to Note 40.

10. INVESTMENTS IN DEBT INSTRUMENTS MEASURED AT AMORTIZED COST

September 30, 2019 December 31, 2018 September 30, 2018 Negotiable certificates of deposit $ 94,830,000 $ 88,165,000 $ 74,175,000 Government bonds 11,894,377 12,534,538 15,617,080 Corporate bonds 2,648,768 3,148,504 3,102,160 Bank debentures 1,084,732 1,228,948 1,281,875 Treasury bonds - 995,971 1,694,126 Less: Loss allowance (1,452) (1,767) (1,669) $ 110,456,425 $ 106,071,194 $ 95,868,572

For the information on financial assets’ related credit risk management and impairment at amortized cost, refer to Note 11. For the information on related financial assets at amortized cost pledged as collateral, refer to Note 40.

11. CREDIT RISK MANAGEMENT OF INVESTMENTS IN DEBT INSTRUMENTS

The investments in debt instruments are classified as financial assets at FVTOCI and financial assets at amortized cost.

September 30, 2019

At FVTOCI At Amortized Cost Total Total carrying amount $ 443,911,256 $ 110,457,877 $ 554,369,133 Allowance loss (96,024) (1,452) (97,476) Amortized cost 443,815,232 $ 110,456,425 554,271,657 Fair value adjustment 2,333,037 2,333,037 $ 446,148,269 $ 556,604,694

December 31, 2018

At FVTOCI At Amortized Cost Total Total carrying amount $ 418,496,103 $ 106,072,961 $ 524,569,064 Allowance loss (100,729) (1,767) (102,496) Amortized cost 418,395,374 $ 106,071,194 524,466,568 Fair value adjustment (1,632,684) (1,632,684) $ 416,762,690 $ 522,833,884

September 30, 2018

At FVTOCI At Amortized Cost Total Total carrying amount $ 381,710,900 $ 95,870,241 $ 477,581,141 Allowance loss (94,710) (1,669) (96,379) Amortized cost 381,616,190 $ 95,868,572 477,484,762 Fair value adjustment (840,502) (840,502) $ 380,775,688 $ 476,644,260

The Group implements a policy of only investing in debt instruments with investment grade and have low credit risk for the purpose of impairment assessment. The Group continues to track external rating information and monitor changes in credit risk of the investments of debt instruments and to review

20

other information such as the bond yield curve and the debtor’s material information to assess whether the credit risk of investments in debt instrument has increased significantly since the initial recognition. The Bank considers the historical default loss rate provided by the independent rating agencies, the debtor’s current financial status and the industry’s forward-looking forecast to measure the 12-month expected credit loss or full-lifetime expected credit loss of the investments in debt instruments. The Bank’s current credit risk rating mechanism and the total carrying amount of each credit rating investment in debt instruments are as follows: September 30, 2019

Credit Rating

Definitions

Expected Credit Loss

Recognition Base

Expected Credit Loss Rate

September 30, 2019

Total Carrying Amount

Normal The debtor has a low credit risk and is fully capable of paying off contractual cash flows

12-month expected credit loss

0.000%~0.880% $ 554,206,057

Abnormal Overdue for more than 30 days or credit risk has increased significantly since the initial recognition

Expected credit loss during the period of existence (no credit impairment)

1.633%~8.522% 163,076

December 31, 2018

Credit Rating

Definitions

Expected Credit Loss

Recognition Base

Expected Credit

Loss Rate

December 31, 2018 Total Carrying

Amount Normal The debtor has a low credit risk and

is fully capable of paying off contractual cash flows

12-month expected credit loss

0.000%~1.096% $ 524,448,188

Abnormal Overdue for more than 30 days or credit risk has increased significantly since the initial recognition

Expected credit loss during the period of existence (no credit impairment)

2.859%~9.960% 120,876

September 30, 2018

Credit Rating

Definitions

Expected Credit Loss

Recognition Base

Expected Credit Loss Rate

September 30, 2018

Total Carrying Amount

Normal The debtor has a low credit risk and is fully capable of paying off contractual cash flows

12-month expected credit loss

0.000%~0.470 % $ 477,581,141

21

The information of changes in allowance for loss under the normal credit rating (12-month expected credit loss) assessment of investments in debt instruments at FVTOCI and at amortized cost is summarized as follows:

At FVTOCI At Amortized Cost Total

Balance at January 1, 2019 $ 100,729 $ 1,767 $ 102,496 Purchase of new debt instruments 40,341 188 40,529 Derecognition (36,642) (486) (37,128) )Model/risk parameter changes (8,761) (16) (8,777) )Exchange rate and other changes 357 (1) 356 Balance at September 30, 2019 $ 96,024 $ 1,452 $ 97,476 Balance on January 1, 2018 (IAS 39) $ - $ - $ - Retrospective application of the impact of IFRS 9 72,536 1,406 73,942 Balance at January 1, 2018 (IFRS 9) 72,536 1,406 73,942 Purchase of new debt instruments 39,600 439 40,039 Derecognition (20,793) (117) (20,910) )Model/risk parameter changes 3,096 12 3,108 Exchange rate and other changes 271 (71) 200 Balance at September 30, 2018 $ 94,710 $ 1,669 $ 96,379

12. SECURITIES PURCHASED UNDER RESALE AGREEMENTS Securities purchased under resale agreements as of September 30, 2019, December 31, 2018 and September 30, 2018 were $1,337,883 thousand, $438,017 thousand and $144,875 thousand, respectively. The aforementioned securities will be bought back one after another before November 20, 2019, January 14, 2019 and October 19, 2020 at $1,340,353 thousand, $439,091 thousand and $144,951 thousand, respectively.

13. RECEIVABLES, NET

September 30, 2019 December 31, 2018 September 30, 2018 Accrued interest $ 5,576,661 $ 5,931,285 $ 5,233,679 Acceptances 3,477,478 4,001,533 4,185,740 Credit cards receivable 3,186,284 2,894,491 2,884,268 Accounts receivable due from sales of securities 2,038,064 1,000,414 3,781,599 Accounts receivable - factoring 992,213 811,314 919,664 Others 3,206,114 2,838,463 4,381,360 18,476,814 17,477,500 21,386,310 Less allowance for credit losses (461,363) (483,762) (490,326) $ 18,015,451 $ 16,993,738 $ 20,895,984

22

The changes in total carrying amount and the allowance of receivables and other financial assets for the nine months ended September 30, 2019 and 2018 (including collections not included in loans and purchase of remittance, refer to Note 17) are as follows:

For the Nine Months Ended September 30, 2019

12-Month ECLs Lifetime

ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs

(Non-Purchase or Original Credit Impairment on

Financial Assets)

Total

Receivables and other financial assets Beginning on January 1, 2019 $ 16,228,239 $ 246,377 $ 355,156 $ 651,093 $ 17,480,865 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (92,381) 21,857 59,000 (510) (12,034) Transfer to ECLs on financial assets (16,829) (7,588) (4,343) 42,965 14,205 Transfer to 12-month ECLs 67,270 (214,544) (59,209) (23,074) (229,557) Financial assets derecognized in the

current period (3,970,172) (86,920) (224,082) (4,613) (4,285,787) Purchased or original financial assets 4,650,757 17,530 121,741 6,225 4,796,253 Write-offs (148) (2,585) - (54,216) (56,949) Exchange rate and other changes 678,164 93,669 2,701 590 775,124 Balance on September 30, 2019 $ 17,544,900 $ 67,796 $ 250,964 $ 618,460 $ 18,482,120

12-Month Expected

Credit Loss

Lifetime ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs (Non-Purchase

or Original Credit

Impairment on Financial

Assets)

Impairment Under the

Guidelines of IFRS 9

The Difference of Impairment Under the

Decree Regulation

Total

Allowance January 1, 2019 $ 63,747 $ 47,499 $ 6,018 $ 338,807 $ 456,071 $ 30,863 $ 486,934 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (935) 10,034 2,179 (385) 10,893 - 10,893 Transfer to ECLs on financial assets (285) (2,122) (399) 32,263 29,457 - 29,457 Transfer to 12-month ECLs 2,562 (27,162) (2,053) (22,457) (49,110) - (49,110) Financial assets derecognized in the

current period (8,897) (9,977) (225) (1,683) (20,782) - (20,782) Purchased or original financial assets 10,581 10,354 241 1,744 22,920 - 22,920 The difference of impairment under the decree

regulation - - - - - 3,284 3,284 Write-offs (148) (2,585) - (54,216) (56,949) - (56,949) Recoveries after write-off - - - 24,156 24,156 - 24,156 Exchange rate and other changes 12,257 85 14 3,007 15,363 - 15,363 Balance on September 30, 2019 $ 78,882 $ 26,126 $ 5,775 $ 321,236 $ 432,019 $ 34,147 $ 466,166

For the Nine Months Ended September, 2018

12-Month ECLs Lifetime

ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs

(Non-Purchase or Original Credit Impairment on

Financial Assets)

Total

Receivables and other financial assets Beginning on January 1, 2018 $ 15,794,845 $ 415,848 $ 431,783 $ 546,774 $ 17,189,250 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (76,269) 32,119 30,307 (348) (14,191) Transfer to ECLs on financial assets (14,454) (10,879) (5,237) 57,063 26,493 Transfer to 12-month ECLs 965,819 (343,725) (69,569) (4,370) 548,155 Financial assets derecognized in the

current period (2,519,827) (107,864) (253,614) (8,493) (2,889,798) Purchased or original financial assets 3,047,202 23,785 13,662 66,565 3,151,214 Write-offs (2,853) (6,324) - (59,078) (68,255) Exchange rate and other changes 3,347,944 26,942 25,142 48,834 3,448,862 Balance on September 30, 2018 $ 20,542,407 $ 29,902 $ 172,474 $ 646,947 $ 21,391,730

23

12-Month Expected

Credit Loss

Lifetime ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs (Non-Purchase

or Original Credit

Impairment on Financial

Assets)

Impairment Under the

Guidelines of IFRS 9

The Difference of Impairment Under the

Decree Regulation

Total

Allowance January 1, 2018 $ 60,993 $ 46,673 $ 8,152 $ 363,619 $ 479,437 $ 24,479 $ 503,916 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (864) 11,205 1,649 (2,120) 9,870 - 9,870 Transfer to ECLs on financial assets (247) (753) (410) 35,069 33,659 - 33,659 Transfer to 12-month ECLs 6,681 (20,819) (3,504) (1,092) (18,734) - (18,734) Financial assets derecognized in the

current period (11,891) (5,110) (313) (7,827) (25,141) - (25,141) Purchased or original financial assets 5,674 5,824 272 5,058 16,828 - 16,828 The difference of impairment under the decree

regulation - - - - - 7,650 7,650 Write-offs (2,853) (6,324) - (59,078) (68,255) - (68,255) Recoveries after write-off - - - 24,146 24,146 - 24,146 Exchange rate and other changes 4,849 2,429 403 3,266 10,947 - 10,947 Balance on September 30, 2018 $ 62,342 $ 33,125 $ 6,249 $ 361,041 $ 462,757 $ 32,129 $ 494,886

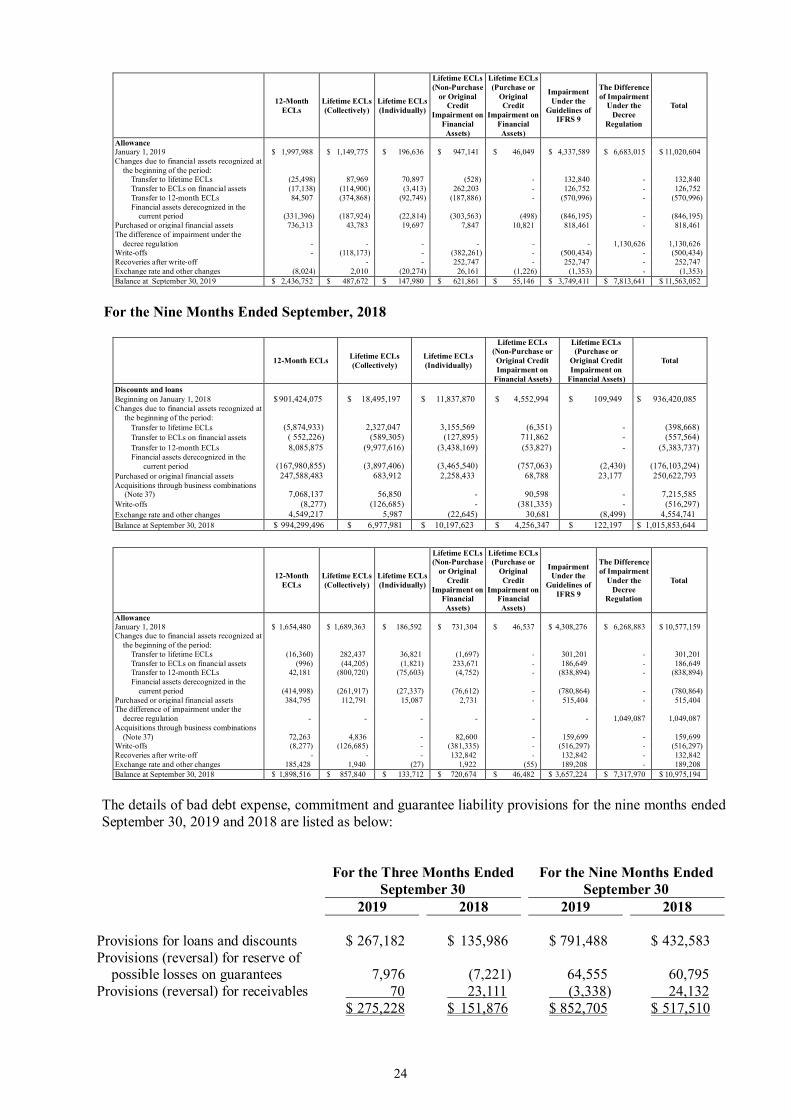

14. DISCOUNTS AND LOANS, NET

September 30, 2019 December 31, 2018 September 30, 2018 Loans $ 1,110,978,275 $ 1,014,096,799 $ 991,520,171 Inward/outward documentary bills 19,829,992 22,782,139 21,107,869 Non-performing loans 3,141,046 3,384,938 3,225,604 1,133,949,313 1,040,263,876 1,015,853,644 Discount and premium adjustments 391,945 559,913 719,674 Allowance for credit losses (11,563,052) (11,020,604) (10,975,194) $ 1,122,778,206 $ 1,029,803,185 $ 1,005,598,124

The Bank discontinues accruing interest when loans are deemed non-performing. For the nine months ended September 30, 2019 and 2018, the unrecognized interest revenue on the non-performing loans amounted to $29,075 thousand and $34,481 thousand, respectively. For the nine months ended September 30, 2019 and 2018, the Group only had written off certain credits after completing the required legal procedures.

The changes in carrying amount and allowance for discounts and loans for the nine months ended September 30, 2019 and 2018 are as follows: For the Nine Months Ended September, 2019

12-Month ECLs Lifetime ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs (Non-Purchase or Original Credit Impairment on

Financial Assets)

Lifetime ECLs (Purchase or

Original Credit Impairment on

Financial Assets)

Total

Discounts and loans Beginning on January 1, 2019 $ 1,011,099,721 $ 10,788,122 $ 13,707,860 $ 4,563,914 $ 104,259 $ 1,040,263,876 Changes due to financial assets recognized at the

beginning of the period: Transfer to lifetime ECLs (12,177,569) 3,296,251 8,826,280 (12,059) - (67,097) Transfer to ECLs on financial assets (802,407) (744,222) (79,832) 1,772,877 - 146,416 Transfer to 12-month ECLs 11,016,719 (3,993,714) (4,146,158) (458,241) - 2,418,606 Financial assets derecognized in the current

period (201,369,750) (2,556,057) (5,046,385) (1,375,587) (39,857) (210,387,636) Purchased or original financial assets 291,332,416 612,123 3,606,365 103,118 64,636 295,718,658 Write-offs - (118,173) - (382,261) - (500,434) Exchange rate and other changes 6,190,435 16,933 82,024 66,629 903 6,356,924 Balance at September 30, 2019 $ 1,105,289,565 $ 7,301,263 $ 16,950,154 $ 4,278,390 $ 129,941 $ 1,133,949,313

24

12-Month ECLs

Lifetime ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs (Non-Purchase

or Original Credit

Impairment on Financial Assets)

Lifetime ECLs (Purchase or

Original Credit

Impairment on Financial Assets)

Impairment Under the

Guidelines of IFRS 9

The Difference of Impairment

Under the Decree

Regulation

Total

Allowance January 1, 2019 $ 1,997,988 $ 1,149,775 $ 196,636 $ 947,141 $ 46,049 $ 4,337,589 $ 6,683,015 $ 11,020,604 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (25,498) 87,969 70,897 (528) - 132,840 - 132,840 Transfer to ECLs on financial assets (17,138) (114,900) (3,413) 262,203 - 126,752 - 126,752 Transfer to 12-month ECLs 84,507 (374,868) (92,749) (187,886) - (570,996) - (570,996) Financial assets derecognized in the

current period (331,396) (187,924) (22,814) (303,563) (498) (846,195) - (846,195) Purchased or original financial assets 736,313 43,783 19,697 7,847 10,821 818,461 - 818,461 The difference of impairment under the

decree regulation - - - - - - 1,130,626 1,130,626 Write-offs - (118,173) - (382,261) - (500,434) - (500,434) Recoveries after write-off - - 252,747 - 252,747 - 252,747 Exchange rate and other changes (8,024) 2,010 (20,274) 26,161 (1,226) (1,353) - (1,353) Balance at September 30, 2019 $ 2,436,752 $ 487,672 $ 147,980 $ 621,861 $ 55,146 $ 3,749,411 $ 7,813,641 $ 11,563,052

For the Nine Months Ended September, 2018

12-Month ECLs Lifetime ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs (Non-Purchase or Original Credit Impairment on

Financial Assets)

Lifetime ECLs (Purchase or

Original Credit Impairment on

Financial Assets)

Total

Discounts and loans Beginning on January 1, 2018 $ 901,424,075 $ 18,495,197 $ 11,837,870 $ 4,552,994 $ 109,949 $ 936,420,085 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (5,874,933) 2,327,047 3,155,569 (6,351) - (398,668) Transfer to ECLs on financial assets ( 552,226) (589,305) (127,895) 711,862 - (557,564) Transfer to 12-month ECLs 8,085,875 (9,977,616) (3,438,169) (53,827) - (5,383,737) Financial assets derecognized in the

current period (167,980,855) (3,897,406) (3,465,540) (757,063) (2,430) (176,103,294) Purchased or original financial assets 247,588,483 683,912 2,258,433 68,788 23,177 250,622,793 Acquisitions through business combinations

(Note 37) 7,068,137 56,850 - 90,598 - 7,215,585 Write-offs (8,277) (126,685) - (381,335) - (516,297) Exchange rate and other changes 4,549,217 5,987 (22,645) 30,681 (8,499) 4,554,741 Balance at September 30, 2018 $ 994,299,496 $ 6,977,981 $ 10,197,623 $ 4,256,347 $ 122,197 $ 1,015,853,644

12-Month ECLs

Lifetime ECLs (Collectively)

Lifetime ECLs (Individually)

Lifetime ECLs (Non-Purchase

or Original Credit

Impairment on Financial Assets)

Lifetime ECLs (Purchase or

Original Credit

Impairment on Financial Assets)

Impairment Under the

Guidelines of IFRS 9

The Difference of Impairment

Under the Decree

Regulation

Total

Allowance January 1, 2018 $ 1,654,480 $ 1,689,363 $ 186,592 $ 731,304 $ 46,537 $ 4,308,276 $ 6,268,883 $ 10,577,159 Changes due to financial assets recognized at

the beginning of the period: Transfer to lifetime ECLs (16,360) 282,437 36,821 (1,697) - 301,201 - 301,201 Transfer to ECLs on financial assets (996) (44,205) (1,821) 233,671 - 186,649 - 186,649 Transfer to 12-month ECLs 42,181 (800,720) (75,603) (4,752) - (838,894) - (838,894) Financial assets derecognized in the

current period (414,998) (261,917) (27,337) (76,612) - (780,864) - (780,864) Purchased or original financial assets 384,795 112,791 15,087 2,731 - 515,404 - 515,404 The difference of impairment under the

decree regulation - - - - - - 1,049,087 1,049,087 Acquisitions through business combinations

(Note 37) 72,263 4,836 - 82,600 - 159,699 - 159,699 Write-offs (8,277) (126,685) - (381,335) - (516,297) - (516,297) Recoveries after write-off - - - 132,842 - 132,842 - 132,842 Exchange rate and other changes 185,428 1,940 (27) 1,922 (55) 189,208 - 189,208 Balance at September 30, 2018 $ 1,898,516 $ 857,840 $ 133,712 $ 720,674 $ 46,482 $ 3,657,224 $ 7,317,970 $ 10,975,194

The details of bad debt expense, commitment and guarantee liability provisions for the nine months ended September 30, 2019 and 2018 are listed as below:

For the Three Months Ended

September 30 For the Nine Months Ended

September 30 2019 2018 2019 2018 Provisions for loans and discounts $ 267,182 $ 135,986 $ 791,488 $ 432,583 Provisions (reversal) for reserve of

possible losses on guarantees 7,976 (7,221) 64,555 60,795 Provisions (reversal) for receivables 70 23,111 (3,338) 24,132 $ 275,228 $ 151,876 $ 852,705 $ 517,510

25

15. SUBSIDIARIES 15.1 Subsidiaries included in the consolidated financial statements

The consolidated financial statements include the Bank and entities controlled by the Bank (i.e. subsidiaries).

Proportion of Ownership (%)

Investor Investee Nature of Activities September

30, 2019 December 31, 2018

September 30, 2018

Remark

Domestic subsidiaries The Bank China Travel Service (Taiwan) Travel agency 99.99 99.99 99.99 1. The Bank SCSB Marketing Ltd. Human resource services 100.00 100.00 100.00 1.

The Bank SCSB Asset Management Ltd.

Purchase, evaluation, auction and management of creditor’s right of financial institutions

100.00 100.00 100.00

1.

China Travel Service (Taiwan) CTS Travel International Ltd. Travel agency 100.00 100.00 100.00 1. Foreign subsidiaries The Bank Shancom Reconstruction Inc. Investment holding 100.00 100.00 100.00 The Bank Wresqueue Limitada Investment holding 100.00 100.00 100.00 1. The Bank Paofoong Insurance Company Ltd. Insurance 40.00 40.00 40.00 1. The Bank AMK Microfinance Institution Plc. Microfinance 84.89 80.01 80.01 1. SCSB Asset Management Ltd. SCSB Leasing (China) Co., Ltd. Leasing operation 100.00 100.00 100.00 1. Wresqueue Limitada Prosperity Realty Inc. Real estate service 100.00 100.00 100.00 Shancom Reconstruction Inc. Empresa Inversiones Generales, S.A. Investment holding 100.00 100.00 100.00 Shancom Reconstruction Inc. Krinein Company Investment holding 100.00 100.00 100.00 Shancom Reconstruction Inc. Safehaven Investment Corporation Investment holding 100.00 100.00 100.00 Empresa Inversiones Generales, S.A. Shanghai Commercial Bank (HK) Banking 48.00 48.00 48.00 2. Krinein Company Shanghai Commercial Bank (HK) Banking 9.60 9.60 9.60 2.

Shanghai Commercial Bank (HK) Shanghai Commercial Bank (Nominees) Ltd. Nominee services 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Shanghai Commercial Bank Trustee Ltd. Trustee services 60.00 60.00 60.00 1.

Shanghai Commercial Bank (HK) Shacom Futures Ltd. Commodities trading 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Shacom Investment Ltd. Investment in exchange fund bills and notes 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Shacom Property Holdings (BVI) Limited Property holding 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Shacom Property (NY) Inc. Property holding 100.00 100.00 100.00 1. Shanghai Commercial Bank (HK) Shacom Property (CA) Inc. Property holding 100.00 100.00 100.00 1. Shanghai Commercial Bank (HK) Shacom Assets Investment Ltd. Investment in bonds 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Infinite Financial Solutions Limited I.T. application services provider 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Shacom Insurance Brokers Ltd. Insurance broker 100.00 100.00 100.00 1. Shanghai Commercial Bank (HK) Shacom Securities Ltd. Securities brokerage services 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Hai Kwang Property Management Co., Ltd. Property management 100.00 100.00 100.00 1.

Shanghai Commercial Bank (HK) Paofoong Insurance Company Ltd. Insurance 60.00 60.00 60.00 1. Shanghai Commercial Bank (HK) Right Honour Investments Limited Property holding 100.00 100.00 100.00 1. Shanghai Commercial Bank (HK) KCC 23F Limited Property holding 100.00 100.00 100.00 1. Shanghai Commercial Bank (HK) KCC 25F Limited Property holding 100.00 100.00 100.00 1. Shanghai Commercial Bank (HK) KCC 26F Limited Property holding 100.00 100.00 100.00 1.

Right Honour Investments Limited Glory Step Westpoint Investment Limited Property holding 100.00 100.00 100.00 1.

Right Honour Investments Limited Silver Wisdom Westpoint Investment Limited Property holding 100.00 100.00 100.00 1.

Remark 1: The entity is an immaterial subsidiary; its financial statements have not been reviewed. Remark 2: This entity is a subsidiary with material non-controlling interests. On September 18, 2017, the board made a resolution to purchase 80.01% of the shares of AMK Microfinance (AMK). The resolution was approved by the FSC and MOEAIC of Taiwan in November 2017 and January 2018, respectively. It was approved by the Cambodian authorities on July 9, 2018. The Group acquired 80.01% equity of AMK for US$80,103 thousand (equivalent to NT$2,457,470 thousand) on August 28, 2018, refer to Note 37. In addition, on November 10, 2018, the Bank’s board approved to purchase additional 1,560 thousand shares of AMK. The additional investment was US$15,300 thousand, and the number of shares obtained through capital increase was 1,554 thousand shares. The case was approved by the FSC and Cambodian authorities on January 19, 2019 and July 16, 2019, respectively. The shareholding ratio increased from 80.01% to 84.89% on July 29, 2019. Refer to Note 38.

26

15.2 Details of subsidiaries that have material non-controlling interests (“NCI”)

Principal Place of Proportion of Ownership and Voting Rights Held by Non-controlling Interests Name of Subsidiary Business September 30, 2019 December 31, 2018 September 30, 2018

Shanghai Commercial Bank (H.K.) Hong Kong 42.4% 42.4% 42.4%

Profit Allocated to Non-controlling Interests For the Three Months Ended For the Nine Months Ended Accumulated Non-controlling September 30 September 30 September 30, December 31, September 30,

Name of Subsidiary 2019 2018 2019 2018 2019 2018 2018 Shanghai Commercial Bank (H.K.) (excluding NCI in its subsidiaries) $ 1,343,427 $ 1,195,141 $ 3,946,789 $ 3,393,453 $ 49,863,694 $ 46,198,858 $ 45,119,683

Summarized financial information in respect of the Group’s subsidiary that has material non-controlling interests is set out below. The summarized financial information below represents amounts before intragroup eliminations. Shanghai Commercial Bank (H.K.) and its subsidiaries

September 30, 2019 December 31, 2018 September 30, 2018 Assets $ 852,359,094 $ 776,338,670 $ 753,584,511 Liabilities (734,418,414) (666,920,867) (646,860,600) Non-controlling interests of Shanghai

Commercial Bank (H.K.)

(337,629)

(317,413) (309,564) Equity $ 117,603,051 $ 109,100,390 $ 106,414,347 Owners of Shanghai Commercial Bank (H.K.) Non-controlling interests of Shanghai

Commercial Bank (H.K.)

$ 67,739,357

$ 62,901,532 $ 61,294,664 Non-controlling interests of Shanghai

Commercial Bank (H.K.)

49,863,694

46,198,858 45,119,683 $ 117,603,051 $ 109,100,390 $ 106,414,347

For the Three Months Ended

September 30 For the Nine Months Ended

September 30 2019 2018 2019 2018 Revenue $ 5,558,252 $ 4,765,594 $ 16,633,544 $ 14,444,845 Net profit for the period $ 3,172,006 $ 2,828,722 $ 9,325,986 $ 8,026,984 Allocated to NCI in subsidiaries of

Shanghai Commercial Bank (H.K.) (3,545) (2,794) (17,521) (16,357)

3,168,461 2,825,928 9,308,465 8,010,627 Other comprehensive income for the

period 1,218,207 651,088 2,939,088 5,762,459

Other comprehensive income (loss) allocated to NCI in subsidiaries of Shanghai Commercial Bank (H.K.) 27 (12)

(91) 484 Total comprehensive income for the period $ 4,386,695 $ 3,477,004 $ 12,247,462 $ 13,773,570 Profit attributable to:

Owners of Shanghai Commercial Bank (H.K.) $ 1,825,034 $ 1,630,787

$ 5,361,676 $ 4,617,174

Non-controlling interests in Shanghai Commercial Bank (H.K.) 1,343,427 1,195,141

3,946,789 3,393,453

$ 3,168,461 $ 2,825,928 $ 9,308,465 $ 8,010,627 Total comprehensive income attributable

to: Owners of Shanghai Commercial Bank

(H.K.) $ 2,526,736 $ 2,005,807 $ 7,054,538 $ 7,936,629

Non-controlling interests of Shanghai Commercial Bank (H.K.) 1,859,959 1,471,197

5,192,924 5,836,941

$ 4,386,695 $ 3,477,004 $ 12,247,462 $ 13,773,570

27

For the Nine Months Ended September 30 2019 2018 Net cash inflow (outflow) from: