The Securities Industry

46

Chapter 3 The Securities Industry

Transcript of The Securities Industry

Chapter 3

The Securities Industry

Contents

PageStructure of the Securities Industry . . . . . . . . . . . . . . . . . . . . ... , . . . . . . . . 51

The Development of the Securities Industry in the United States . . . . . . 51Organizations Composing the Securities Industry . . . . . . . . . . . . . . . . . . . 52Industry Users.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57The Regulatory Structure of the Securities Industry . . . . . . . . . . . . . . . . . 59Characteristics of the Securities Industry . . . . . . . . . . . . . . . . . . . . . . . . . . 62New Entrants to the Securities Industry. . . . . . . . . . . . . . . . . . . . . . . . . . . 63The Securities Industry and the International Market . . . . . . . . . . . . . . . 64The Effects of Information Technology on the Structure of the

Securities Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

The Functions of the Securities Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64The Securities Industry as an Advisor.. . . . . . . . . . . . . . . . . . . . . . . . . . . . 65Acceptance of Risk by the Securities Industry . . . . . . . . . . . . . . . . . . . . . . 67Marketing by the Securities Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69Technology and the Functions of the Securities Industry . . . . . . . . . . . . 75

The Effects of Information Technology insecurities Instruments . . . . . . . 75

Appendix 3A: Securities Instruments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76Corporate Capital Structure: Debt and Equity Issues . . . . . . . . . . . . . . . . 76Short-Term Debt–Money Market Securities.. . . . . . . . . . . . . . . . . . . . . . . 83Options and Futures Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

Appendix 3B: Capital Formation and the Functions of theSecurities Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

Private Sources of Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92Venture Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92Public Offerings of Securities of a Corporation . . . . . . . . . . . . . . . . . . . . . . 93

Tables

Table No. Page2. Contracts Traded-Futures Exchanges: A Comparison of

1983 and 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563A-1. Meet Active Venture Capitalists, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . 93

Figures

Figure No. Page3. Average Daily Share Volume New York Stock Exchange

1963 to 1983 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 544. Volume of Futures Trading, 1958-83 (millions of contracts traded) . . . . . 585. Overview of SIAC Facility Management for NSCC Services . . . . . . . . . . 74

Chapter 3

The Securities Industry

The securities industry in the United States,which developed to help young American busi-ness gain financing from European investors,continues to bring together those who needcapital and those wishing to invest. The indus-try directs its concentrated expertise on finan-cial markets toward its intermediary role offacilitating the development of capital. It pro-vides advice, accepts risk, and offers market-ing services to ensure that an orderly marketfor the issuing and trading of securities* ismaintained.

XFO~ PUW{)=S of this study, securities include debt and equityissues used to develop capital (stocks and bonds, money-marketsecurities, and instruments which have been developed to allowhedging and speculation in securities and commoditymarket s—i. e., options and futures contracts). These instru-ments, as well as investment tools which developed from thepackaging of securities instruments, such as mutual funds andcentral asset accounts, are described in app. 3A.

Since the introduction of the telegraph 140years ago, communications technologies havebeen used by the industry to convey informa-tion on which the operations of securities in-dustry depend. However, while the securitiesindustry has always applied state-of-the-arttechnology to its operations, the level of tech-nology used today and likely to be availabletomorrow is beyond what could have beendreamed of when the telegraph was applied in1844.

In this chapter, the structure, functions, andinstruments of the securities industry are de-scribed. The impact that the application ofcomputer and communications technologieshas had in these areas is reviewedble future effects are discussed.

Structure of the Securities Industry

The structure of the securities industry hasbeen shaped by the demands of users, nationalpolicy objectives regarding the financial serv-ice industry, practical operational concerns,and competitive market forces. In this section,a brief overview of the development of the cur-rent structure of the securities industry anda description of the organizations and compet-itive forces comprising the industry will beprovided. Present and future effects of infor-mation technology on the structure of the in-dustry will be discussed.

The Development of the SecuritiesIndustry in the United States

The securities industry in the United Statesdeveloped to meet the capital demands of thenew Nation. One side effect of the independ-ence won in the Revolutionary War was wardebt. This was funded by the issuance of in-terest-paying bonds, for which a secondary

market shortly developed.1 At the

and possi-

same timethe need to finance development in the newNation was recognized. The burgeoning secu-rities industry provided a vital link to Euro-pean capital markets and also a means oftransferring capital within the United States.The basic role filled by the securities indus-try in the late 1700’s is still a driving forcebehind its operations today: to provide a meansof interaction for those seeking capital andthose wishing to invest.

Two factors which quickly emerged as essen-tial to the operation of the securities industrywere the maintenance of an orderly marketand the availability of trading information.Twenty-four brokers, conducting trading undera buttonwood tree, subscribed to a brokers’agreement that formed the first stock market

IMarketpIace-A Brief History of the New York Stock Ex-change (New York: New York Stock Exchange, Inc., 1982).

51

52 ● Effects of Information Technology on Financial Services Systems—

in New York on May 17, 1792.2 This marketbecame the New York Stock Exchange. Inwhat is now known as the “ButtonwoodAgreement, ” the brokers focused on workingtogether to assure they would be able to tradesecurities smoothly and fairly.

Information on trading and prices has al-ways been essential to trading decisions. Se-curities firms and exchanges clustered (as onWall Street) to facilitate the communicationsneeded for the operation of the market. Anewspaper first published stock prices in 1815.Prior to the introduction of the industry’s firsttechnology-based information system, theelectric stock ticker (in 1867), messengersliterally ran from the trading floor to brokers’offices with information.

Early refinement and expansion of securitiestrading can be related to three communica-tions technologies: the telegraph, the trans-atlantic cable, and the telephone.3 These tech-nologies improved information flows on whichthe markets are dependent. The telegraphlinked exchanges, brokers, and investorsthroughout the country and made decision-making on investments by someone not onWall Street practical for the first time. Thistechnology offered the first hope of a national,noncentralized market. The transatlanticcable, completed in 1866, made an interna-tional market feasible at a time when Ameri-can industry was still very much dependenton financing from European investors. Tele-phones were first used to convey orders frombrokers to the floor of the New York Stock Ex-change in 1878, 2 years after the first suc-cessful test of that technology.

The adoption of these communications tech-nologies and the stock ticker were based onthe recognition that the faster and more ac-curately information flows, the better securi-ties markets function. The introduction of newtechnologies today is largely based on thisassumption.

Organizations Composing theSecurities Industry

Three types of organizations traditionallycompose the securities industry: investmentbanks perform the services surrounding a pub-lic offering of the stocks and bonds of a cor-poration; brokers manage the buying and sell-ing of securities; and exchanges provide avehicle for setting prices and actually conduct-ing transactions.

Investment Banks

The activities of investment banks are cen-tered on the development of capital. The Bank-ing Act of 1933, commonly called “Glass-Stea-gall, ” required that investment banking beseparated from commercial banking becauseof the sometimes incongruent objectives andthe different levels of risk associated withthese kinds of organizations. Investmentbanks fall into two categories: originatingfirms and distribution firms. Originating firmsdeveloped largely as intermediaries betweenEuropean financiers and young American in-dustry, and they remain major players in thedevelopment of securities offerings. Distribu-tion firms come together in syndication, underthe guidance of an originating firm, to guar-antee and sell the securities of an issuer.4

The four leading investment banks in bothdomestic and foreign financing are SalomonBrothers, Inc.; Morgan Stanley Inc.; FirstBoston Inc.; and Goldman Sachs & Co. Mer-rill Lynch, Pierce, Fenner, & Smith Inc. (Mer-rill Lynch) and Paine, Webber, Jackson, &Curtis (Paine Webber) have a significant shareof the domestic market. Three levels of pur-chasers and sellers are reached through invest-ment bank activities: first, the issuers of secu-rities, those corporations and governmentsthat purchase investment bank services; sec-ond, the investors in new issues; and third, theintermediaries who bring these two partiestogether—other investment bankers, distri-

‘New York Stock Exchange 1983 Fact Book (New York: NewYork Stock Exchange, June 1983), p. 66.

‘Marketplace-A Bn”ef History of the New York Stock Ex-change, op. cit.

4Sarnuel L. Hayes III, “The Transformation of InvestmentBanking, ” Harvard Busines 12ew”ew, January-February 1979,pp. 153-170.

—

Ch. 3—The Securities Industry ● 5 3

buting underwriters, and commercial banks.Investment banks assume the risk of a pub-lic offering of investments by guaranteeingtheir purchase—i.e., underwriting them.

The nature of competition within invest-ment banking is changing. Price competitionis cutting fees for underwriting to new lows.In addition, simplification of securities regis-tration requirements could make underwritersunnecessary. Nevertheless, the need to trans-fer risk continues to provide a strong incen-tive for utilizing the services of investmentbanks.

Brokerage Houses

Full-service brokerage houses perform tradesin securities and commodities and provide fi-nancial counseling services supported by in-depth research and analysis of markets andindustries. This segment of the industry isdominated by firms which are subsidiaries ofcompanies that offer a range of financial man-agement services. Six national brokeragehouses lead the industry. They are: MerrillLynch; E. F. Hutton & Co.; Shearson/Ameri-can Express; Prudential Bache; Dean WitterReynolds; and Paine Webber. There are alsomany regional firms, such as Alex Brown &Sons, which play major roles in trading eithernationwide or regionally.

This portion of the industry has been af-fected by the abolition of fixed commissionrates in 1975. While brokerage houses in thepast competed on the reputation of their re-search and the quality of their service, pricecompetition has also become a factor. Dis-counters, who concentrate on the transactionside of the business, have entered the marketand have attracted a significant portion ofboth institutional and individual trading. Inresponse to this market entrance, many full-service brokerage houses are taking steps todistinguish their services and to increase cli-ent loyalty. Increased efforts are being di-rected toward product development and pro-motion.

Exchanges

The fundamental role of all exchanges in thesecurities industry is to provide an orderlymarketplace for trading. Exchanges providea central location and a structure in whichbuyers and sellers can conduct trades. Ex-changes are operated on a membership basis.“Seats,” memberships that carry the right totrade on an exchange, are purchased by firmsor individuals desiring access to its market.Members agree to direct all trades on listedsecurities through the exchange floor. Thisallows the exchanges to manage the marketsbetter–for example, to halt trading on a se-curity, if necessary, with the assurance thatmember firms will not trade off-market.Stocks and bonds, options, and futures con-tracts are usually traded on separate ex-changes. This specialization is a carry-overfrom the separate formation of capital andcommodity markets.

Stock Exchanges.– Stock exchanges are in-dependent players in the securities industryand have two functions: performing transac-tions and accepting risk. Stock exchanges actas a secondary securities market for both debtand equity issues, providing flexibility andchoice for investors. Potential investors in newissues can evaluate the desirability of the in-strument in light of their ability to sell it, andtherefore may recognize a lower opportunitycost. The existence of secondary markets alsoincreases the available investment choicessince securities other than new issues are madeavailable.

There are seven major stock exchanges:New York, American, Boston, Cincinnati, Mid-west, Pacific, and Philadelphia. In 1982, 80.8percent of the total share volume of registeredexchanges was traded on the New York StockExchange (NYSE). The National Associationof Securities Dealers, Inc. (NASD) operates aquotation system and clearing facility for theover-the-counter market. The automated quo-tation system, NASDAQ,5 has been responsi-

5National Association of %curities Dealers Automatic Quota-tion System.

54 • Effects of Information Technology on Financial Services Systems

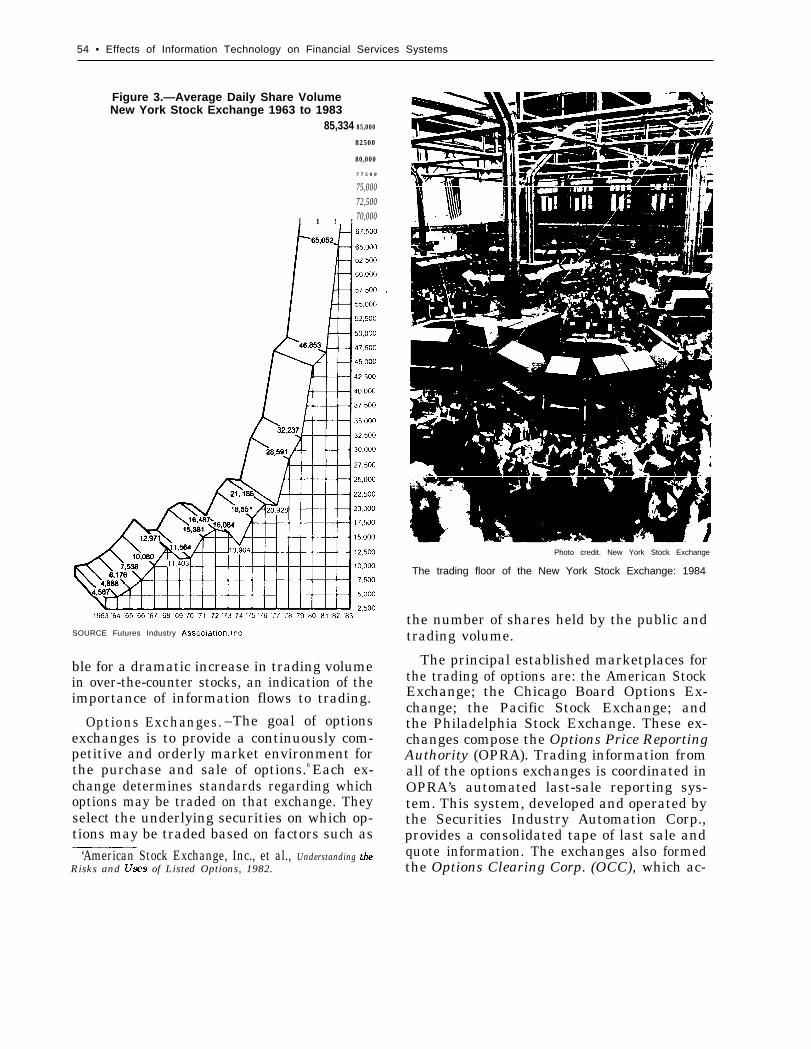

Figure 3.—Average Daily Share VolumeNew York Stock Exchange 1963 to 1983

85,334 85,000

[ 1 ! !

82500

80,000

7 7 5 0 0

75,00072,50070,000

SOURCE Futures Industry Assoclatlon, Inc

ble for a dramatic increase in trading volumein over-the-counter stocks, an indication of theimportance of information flows to trading.

Options Exchanges.–The goal of optionsexchanges is to provide a continuously com-petitive and orderly market environment forthe purchase and sale of options.6 Each ex-change determines standards regarding whichoptions may be traded on that exchange. Theyselect the underlying securities on which op-tions may be traded based on factors such as

‘American Stock Exchange, Inc., et al., Understanding theRisks and U=s of Listed Options, 1982.

Photo credit. New York Stock Exchange

The trading floor of the New York Stock Exchange: 1984

the number of shares held by the public andtrading volume.

The principal established marketplaces forthe trading of options are: the American StockExchange; the Chicago Board Options Ex-change; the Pacific Stock Exchange; andthe Philadelphia Stock Exchange. These ex-changes compose the Options Price ReportingAuthority (OPRA). Trading information fromall of the options exchanges is coordinated inOPRA’s automated last-sale reporting sys-tem. This system, developed and operated bythe Securities Industry Automation Corp.,provides a consolidated tape of last sale andquote information. The exchanges also formedthe Options Clearing Corp. (OCC), which ac-

Ch. 3—The Securities Industry • 55

;red/t New York Stock Exchange

The trading floor of the New York Stock Exchange: 1930

tually issues the exchange-traded options and futures contracts.7 Futures trading is con-assigns exercises. ducted in price auctions on the trading floor.

Options exchanges aid in industry self-reg-ulation by developing and enforcing rules con-cerning the handling of accounts by brokers,trading hours, and position and exercise limits.Options exchanges and the OCC are regulatedby the Securities and Exchange Commission(SEC).

Futures Exchanges.—The principal respon-sibility of a commodity futures exchange is toensure the existence of competitive marketsfree of price manipulation for the trading of

The exchanges are operated on a membershipbasis, and exchange regulations and policiesare set by their boards of directors and sub-ject to approval of the Commodity FuturesTrading Commission (CFTC). There are manyfutures exchanges in the United States. Thelargest is the Chicago Board of Trade, whichin 1983 handled 44.89 percent of total tradingvolume (see table 2.)

‘Futures Industry Associates, Inc., “Roles Played by EachParticipant, ” Futures Trading Course and Handbook, Wash-ington, D. C., 1983, p. I I-4.

35-505 0 - 84 - 5 : QL 3

56 ● Effects of /formation Technology on Financial Services Systems

Exchange

1. Chicago Board of Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2. Chicago Mercantile Exchange. . . . . . . . . . . . . . . . . . . . . . . .3. Commodity Exchange, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . .4. Coffee, Sugar & Cocoa Exchange5. New York Mercantile Exchange . . . . . . . . . . . . . . . . . . . .6. New York Futures Exchange . . . . . . . . . . . . . . . . . . . . . . . . .7. MidAmerica Commodity Exchange . . . . . . . . . . . . . . . . . . .8. New York Cotton Exchange. . . . . . . . . . . . . . . . . . . . . . . . . .9. Kansas City Board of Trade. . . . . . . . . . . . . . . . . . . . . . . . . .

10. Minneapolis Grain Exchange. . . . . . . . . . . . . . . . . . . . . . . . .11. New Orleans Commodity Exchange . . . . . . . . . . . . . . . . . . .

1983

Contracts

62,811,52337,830,04420,014,5974,876,0693,926,5893,510,2853,166,5371,703,1051,693,042

379,60713,542

139,924,940

Percent

44.8927.0414.303.482.812.512.261.221.210.270.01

100.00

1982

Contracts Percent Rank

48,206,790 42,89 (1)33,574,286 29.87 (2)17,520,712 15.59 (3)3,252,512 2.89 (4)2,649,941 2.36 (5)1,451,442 1.29 (9)2,397,721 2.13 (6)1,479,781 1.32 (8)

1,493,558 1,33 (7)346,264 0.31 (lo)

27,872 0.02 (11)

112.400.879 100.00, .SOURCE: Futures Industry Association.

, ,

Ch. 3—The Securities Industry ● 57— — — — —

The exchanges play a major role in self-reg-ulation of the futures industry. In this rolethey are required to perform four activities:surveillance of market activity to detect andprevent situations conducive to price distor-tion; surveillance of trading practices to detectand prevent trading abuses; investigation ofrule violations and customer complaints; andexamination of members’ books and records.8

The introduction of new investment products,such as stock futures, indicates that activityon futures exchanges may be expected to growover the next several years. The regulatoryand operational role of the exchanges will be-come more complex. Information technologyis being applied to facilitate the operations ofthe exchanges and will play an increasinglyimportant role in their activities.

Industry Users

The demands and characteristics of users ofthe industry are major determinants of indus-try structure. The organizations of the secu-rities industry serve as intermediaries betweentwo sets of users: capital seekers and in-vestors.

Organizations Seeking Capital

While the focus of much of the activity ofsecurities industry is on secondary markets,the underlying demand for capital is the rea-son the industry exists. In 1982, the value ofnew issues of common stock publicly offeredwas $23.4 billion; new, publicly offered debtobligations totaled $45.2 billion. Private place-ments of debt and equity totaled $22.3 billion.As the U.S. economy completes its evolutionto an information economy, it may be expectedthat a great number of both new firms and ex-isting corporations with growing operationswill be seeking capital through both privateand public sources.

Corporations will demand more rapid accessto their capital than ever before because of theeffect of information technology on the over-

8U. S. General Accounting Office, Survey of Investor Protec-tion and the Regulation of Financial Intermediaries, 1983, pp.28-29.

all economy. Business decisions are beingmade more quickly, and delays in financingwill not be tolerated.

Institutional Investors

Institutional investors include special-in-terest funds and companies such as pensionfunds, mutual funds, insurance companies,and private foundations that have a goal ofproducing income for a specific organizationaluse and deal in large blocks of securities. Theydemand prompt, efficient transactions and ex-tensive information.

Since the passage of the Employee Retire-ment Income Security Act (ERISA), the im-pact of these investors on the total market hasincreased substantially. Trades in 10,000 -share blocks, a measure of institutional in-volvement, have increased to over 44 percentof total share volume. g The broker must alsobe willing to assume risk by buying from theinstitutional investor because he demands ahigh level of liquidity. At the same time, theimportance of this segment of the market hasled to price competition following the deregula-tion of commission rates in 1975.

The demands of institutional investors havebeen, in large part, responsible for much of theautomation of trading and clearing by the se-curities industry. Exchanges need to attractinstitutional capital to maintain the market-place, yet information technology, combinedwith institutional traders’ level of market ex-pertise, makes off-market trading a viable al-ternative for these traders. The volume oftrading conducted by institutional investorsmakes those investors valuable clients forboth brokers and exchanges.

Pension funds are the most significant insti-tutional investors in capital markets. In 1980,these funds held 13.4 percent of the total mar-ket value of NYSE listed stocks.10 Two factorsthat have contributed to the growing impor-tance of pension funds, both as savings vehi-cles and institutional investors, are the aging

‘Securities Industry Association data.IONew York Stock Exchange 1983 Fact Book, op. cit., P. 52.

58 . Effects of Information Technology on Financial Services Systems

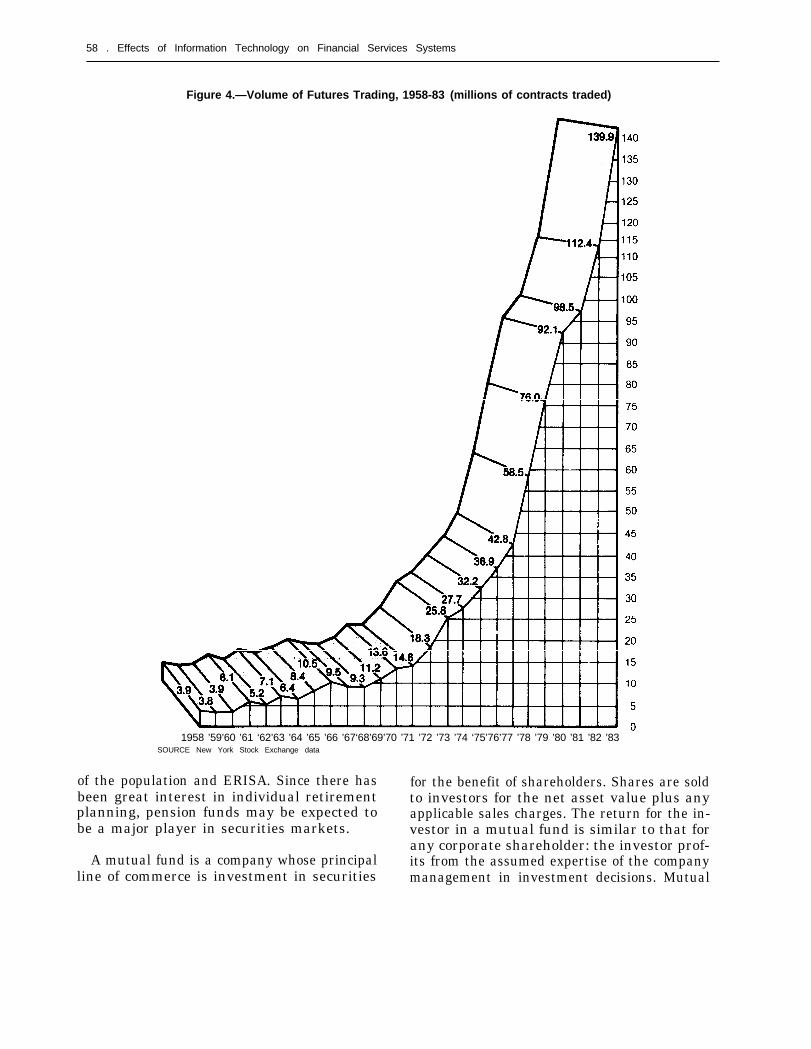

Figure 4.—Volume of Futures Trading, 1958-83 (millions of contracts traded)

1958 ’59’60 ’61 ‘62’63 ’64 ’65 ’66 ’67‘68’69’70 ’71 ’72 ’73 ’74 ‘75’76’77 ’78 ’79 ’80 ’81 ’82 ’83SOURCE New York Stock Exchange data

of the population and ERISA. Since there has for the benefit of shareholders. Shares are soldbeen great interest in individual retirement to investors for the net asset value plus anyplanning, pension funds may be expected to applicable sales charges. The return for the in-be a major player in securities markets. vestor in a mutual fund is similar to that for

any corporate shareholder: the investor prof-A mutual fund is a company whose principal its from the assumed expertise of the company

line of commerce is investment in securities management in investment decisions. Mutual

Ch. 3—The Securities Industry ● 5 9

funds are significant as institutional investorsbecause they usually trade in large volumes.

Funds are classified by investment strategyand fall into three categories: income funds,which strive to provide a current income forinvestors; growth funds, which focus on long-term appreciation; and income and growthfunds, which try to be all things to all people.Generally, funds that seek a higher return forinvestors are more risky. For example, somefunds, such as the Phoenix Fund of MerrillLynch, are composed of securities of failingcompanies that are believed to have the po-tential to rebound. While the risk level ishigher than average, shareholders in this typeof fund have less exposure to risk than if theywere to invest in individual securities, andthey benefit from high yield.

Mutual funds frequently specialize in spe-cific types of securities, such as governmentbonds, or in securities from a particular typeof industry. Money market mutual funds in-vest only in money market securities, whichare by definition short term. For this reason,money market mutual funds are consideredless risky and are more liquid than the tradi-tional mutual funds. Money market fundshave three basic objectives: to preserve share-holder capital; to maintain liquidity; and, inlight of these two objectives, to achieve thehighest possible current income.” Money mar-ket instruments are generally written in highdenominations and are only accessible to manyinvestors because they are able to pool theirinvestment dollars in the funds. The moneymarket benefits from the funds because a largequantity of capital not otherwise available isattracted.

Individual Investors

The typical individual investor in securitiesis an affluent consumer who demands infor-mation and advice geared toward his require-ments. The sales of mutual funds, a proxy in-dicator of the level of individual involvementin the securities market, are rebounding aftera period of decline. This upswing, plus recog-

“U.S. General Accounting Office, op. cit., p. 60.

nized opportunity to market new investmentproducts, has generated renewed interest inindividual investors by the securities industry.

There has been tremendous growth in thenumber of stockholders. NYSE reports that42.36 million Americans own shares of U.S.corporations or stock mutual funds, an in-crease of 10.1 million since 1981. ]2 Of particu-lar significance to the securities industry is thetremendous growth in the number of first-timeinvestors, 7.3 million since 1981. This growthma-y be attributable to several factors, includ-ing the strength of the stock market duringthe early 1980’s, corporate employee stockpurchase plans, and most notably, changingdemographics.

The “aging” baby-boom generation, now ap-proaching peak investment years, may causean increase in the number of people investing.People are waiting longer to get married forthe first time and have families and thereforeare likely to be able to invest at a younger age.While securities firms once targeted their serv-ices towards a small portion of the population,their market has become more diverse in termsof both age and income.

Securities firms have been expanding theirproduct lines and the scope of financial serv-ices they provide to meet the demands of theindividual investor. Movement by firms intoother areas, such as insurance and real estate,is an attempt to draw clients at an earlierstage in their financial lifecycle and to fill allof their financial needs.

The Regulatory Structure of theSecurities Industry

Federal regulations enacted in the 1930’sdisallowed involvement by depository institu-tions in securities activities because of con-cerns about the effects of risk associated withthese transactions on the stability and sound-ness of banks. Such restrictions separated cap-ital creation from the banking activities of cor-porations, such as the extension of operating

‘zJon Friedman and Tom Petruno, “Record 42M of Us AreWall Street Investors, ” USA Today, Dec. 1, 1983, sec. A, p. 1.

60 • Effects of /formation Technology on Financial Services Systems—

credit and transaction accounts. These restric-tions were intended to assure that depositoryinstitutions acted in the best interests ofdepositors.

The regulatory structure of the securities in-dustry recognizes that capital and money mar-kets are essential to the health of all sectorsof the national economy. Legislation concern-ing the securities industry has focused onthree areas: providing for disclosure to in-vestors, promoting self-regulation by the in-dustry, and facilitating the development of anational market for securities. Federal regu-lation that is focused directly on the commodi-ties futures segment of the industry is simi-larly designed and seeks to protect marketsand individual traders.

Securities and commodities trading is over-seen by a two-tier regulatory system: Federaland State government and industry. Federalregulation is focused on the oversight of mar-kets and investor protection. State regulationof securities, commonly called “blue skylaws,” since they were designed to prevent thesale of securities with the investment poten-tial of the blue sky, preceded Federal regula-tion, and the right of States to regulate waspreserved when the first major legislation con-cerning the operation of the securities indus-try, the Securities Act of 1933, was passed.

While Federal regulation focuses on dis-closure without value judgment on the worthof the securities, State laws may actually in-volve licensing. Registration of an issue maybe refused by a State authority, which wouldprohibit sale in that State.13 State laws differ,but efforts to develop uniform laws are beingled by the North American Securities Admin-istrators Association.

Self-regulation is imposed and enforced bythe exchanges and by industry associations.While the industry began formally supervis-ing its own operations with the developmentof the Buttonwood Agreement, the self-regu-latory system was first recognized by Con-gress and subject to Federal Government

13U.S. General Accounting Office, op. cit., p. 22.

supervision with the passage of the SecuritiesExchange Act of 1934.

Federal Regulatory Agencies

Several Federal agencies play roles in theactivities of the securities industry. The SmallBusiness Administration licenses and regu-lates Small Business Investment Corpora-tions, a type of venture capital firm. TheBoard of Governors of the Federal Reserveregulates the extension of credit by brokers,as mandated in the Securities Exchange Actof 1934, and has a major impact on the in-dustry by regulating the activities of banks.However, responsibility for regulating thesecurities industry is held by SEC, and respon-sibility for the futures industry, by CFTC.

SEC was established by the Securities Ex-change Act of 1934. Its regulatory activitiesare based on the belief that disclosure is thepreferable means of assuring the smooth oper-ation of securities markets; it is not invasiveto the operations of industry players, and itretains investor choice. SEC also acts to pre-vent price manipulation of securities and reg-ulates the the practices of exchanges, brokers,and dealers. It acts in conjunction with the in-dustry self-regulatory agencies and overseestheir activities.

While not a regulatory agency, the Securi-ties Investor Protection Corp. (SIPC), a quasi-governmental organization, has brought a uni-form investor protection policy to the securi-ties industry. SIPC operates as a private non-profit membership corporation whose primaryfunction is to provide financial protection forthe clients of failed securities firms. The cor-poration was mandated by the Securities In-vestor Protection Act of 1970 in response toproblems that occurred in the late 1960’sthroughout the brokerage industry as stockprices fluctuated widely and volume on the ex-changes increased dramatically.

The only function of SIPC is to insure ac-counts. It covers shortages in accounts of upto $500,000, including coverage for as muchas $100,000 in cash, for each account. Sinceit began operation in December 1970, it has

Ch. 3—The Securities Industry . 61

paid out more than $133 million in claims. ’4SIPC assesses an annual fee on each of the7,000 brokerage houses in the United States,which are required to be members of the cor-poration, to maintain the $150 million level itis required by law to keep available to satisfyclaims. At times, SIPC has acted as trusteein cases of brokerage house liquidations andas such has distributed payments to custom-ers as accounts were settled.

The corporation relies on SEC and the se-curities industry’s self-regulating organiza-tions for notification that a member firm is indanger of collapse. If SIPC determines thatthe customers of the brokerage house are inneed of its protection, it begins what is termeda “customer protection proceeding, ” which isa liquidation procedure. SEC is the only orga-nization that can sue SIPC to force it to beginliquidation proceedings.

CFTC is responsible for regulating com-modity futures trading on organized ex-changes. It acts to prevent price manipulation,attempts to corner market dissemination offalse or misleading information, and mishan-dling of traders’ margin money and equity.15

It reviews and approves the instrumentstraded on the futures exchanges-i. e., futurescontracts. CFTC oversees the activities of ex-changes and other self-regulatory associations.

Disclosure for the futures industry involvesnot only the characteristics of specific con-tracts, but also the level of risk involved in thistype of investment. All potential investors infutures markets are informed that they mayexperience large losses as well as gains andthat it maybe difficult to liquidate a position.

Industry Self-Regulatory Agencies

Industry associations and exchanges estab-lish and enforce rules concerning the opera-tions of the securities industry, rules that areoften more stringent than Federal regulations.An implicit objective of self-regulatory agen-cies is to maintain the autonomy of the indus-

14 Christine Davies, “Brokerage Failures Bring Agency toLife, ” USA Today, Mar. 9, 1983.

“U.S. General Accounting Office, op. cit., p. 26.

try. To meet this goal, these organizations tryto ensure that the behavior of the industry isabove reproach. They play a major role in over-seeing the markets, market systems, and theindividuals active in the industry. Self-regu-latory agencies also have an educational rolein dealing with both members of the industryand the public.

The two most significant securities indus-try self-regulatory organizations are NASDand NYSE. Their roles may be expected togrow as they continue to carry a great portionof all securities trading. The National FuturesAssociation (NFA) is the self-regulatory orga-nization of the futures industry.

NASD is a self-regulatory agency responsi-ble for regulating the over-the-counter secu-rities market and for promoting high stand-ards of operation throughout the industry. Italso establishes standards of professional com-petence. NASD was empowered through theMaloney Act of 1938 amendments to the Se-curities Exchange Act of 1934. Its central pur-pose—to promote high standards of commer-cial honor and just and equitable principles oftrade throughout the industry—has becomeeven more important to the industry as tech-nology is applied.

NYSE oversees the operation of the ex-change marketplace and administers rules andregulations related to the maintenance of or-derly markets and the standards of profession-al competence. ” NYSE is also a major sourceof information concerning the industry as awhole.

In 1981 NFA was designated a “registeredfutures association” by CFTC, which overseesits activities, with congressional endorsement.It began operating on October 1, 1982. NFAwas formed in recognition of the continuinggrowth of futures trading to bring a uniformsystem of self-regulation to its activities.

NFA works toward four fundamental pur-poses: strengthening industry self-regulationby regulating those segments of the futures

“U.S. General Accounting Office, op. cit., p. 24.

62 ● Effects of Information Technology on Financial Services Systems

industry that were previously outside thescope of self-regulatory organizations; elim-inating duplication in self-regulation, therebycontrolling expenses; eliminating overlap andconflicts in self-regulation of the industry byproviding uniform standards; and aiding ef-fective regulation by removing unnecessaryregulatory constraints.17

Trends in Industry Regulation

Trading volume and the number of types ofsecurities instruments have been increasing.The securities industry is being entered byplayers from other sectors of the financialservices industry and by outside industries.It is likely that more demands will be placedon the oversight functions of the regulatorysystem. However, while the importance of thisrole is increasing, technology will facilitate thisfunction by improving information flows onthe operations of the industry.

While the oversight role may be stream-lined, standards and education will requiremore attention. Changes in industry functionsand the introduction of new products (facili-tated by the application of information tech-nology) will require an expansion of the educa-tional role of the regulatory agencies. Thecontinuing development of technology-basedsystems necessitates coordination of stand-ards to ensure that different markets, both do-mestically and internationally, can interact.

Characteristics of the Securities Industry

Concentration

The securities industry is heavily concen-trated. In 1982, the 25 largest firms, out ofnearly 550 Securities Industry Associationmember firms, controlled nearly 75 percent ofthe total capital of the industry. The 10 largestinvestment banks controlled two-thirds of theprofits for that segment. This high level of con-centration results, in part, from the large num-ber of mergers, reorganizations, and liquida-tions that occurred during the 1970’s. The

l~NatiOn~ FUtUreS Association, A %rtnership Between thePublic and the Industry, Chicago, 1983, p. 11.

consolidation activity was spawned by risingbusiness costs for the industry and the weightof transaction processing, as the volume oftrade had increased throughout the 1960’s.

Throughout the 1970’s several verticalmergers between brokers and investmentbanks occurred-most notably the acquisitionof Reynolds Securities by broker Dean Wit-ter & Co. and the purchase of White Weld byMerrill Lynch. These mergers integrated newissue management with the distribution of se-curities and may be considered an early movetoward consolidation throughout the financialservices industry.

Recent acquisitions and mergers seen in thesecurities industry have frequently involvedplayers from other financial services indus-tries. The product lines of firms are becomingboth horizontally and vertically integratedwith lines previously only offered outside ofthe securities industry.

Movement Toward a NationalSecurities Market

The Securities Acts Amendments of 1975directed SEC and the securities industry tocreate a national market system for bothtransacting and clearance. Movement in thisdirection is having a profound effect on thestructure of the securities industry. Ex-changes have been linked to a degree not pre-viously seen, through development of technol-ogy-based information systems such as theIntermarket Trading System. Clearing sys-tems involving the National Securities Clear-ing Corp. have made same-day settlement apossibility.

The driving force in developing systems thatmake a national market possible is the Securi-ties Industry Automation Corp. (SIAC). Thegreat increase in the volume of trading on themajor exchanges in the late 1960’s made it evi-dent that the securities market needs the ca-pability to deal with extensive volume. SIACwas organized both to operate and to developmore efficient and effective ways of dealingwith the transaction process. SIAC systemssupport order processing, trading, and report-

3333333333. —

Ch. 3—The Securities Industry ● 6 3— — —— ———- — — . ——— . —

ing functions, as well as clearance and settle-ment for stocks, bonds, options, and financialfutures. The corporation is owned by the NewYork and American Stock Exchanges,

One of the major impacts of SIAC on thesecurities industry is that it makes the devel-opment and refinement of technological sys-tems a continual process. This should preventor at least limit the lag between the identifica-tion of a need that could be best addressedwith a technology-based system and the appli-cation of a solution.

New Entrants to the Securities Industry

Entrance by Depository Institutions

An amendment, effective September 9,1983, to Regulation Y of the Federal ReserveBoard has added securities brokerage andrelated margin lending to the list of activitiespermissible for bank holding companies. Thisaction, which extends from previous approvalby the Government for the acquisition of retaildiscount brokers by bank holding companies(notably the BankAmerica Corp. acquisitionof Charles Schwab), may increase the interestamong bank holding companies in entering thesecurities industry. ]8

The motivation of banks for providing dis-count brokerage services may be seen as eithera reaction to market conditions or an attemptto protect market shares. Since many broker-age houses are offering investment opportu-nities that serve functions similiar to depos-itory accounts, often with more flexibility andhigher rates of return, the consumer’s per-ceived need for a bank may be decreased. Onemotivation for providing brokerage servicesmay be to prevent the potential luring awayof other portions of a depositor’s business.

While acquisition of a discount broker pro-vides one method of expansion into securitiesfor depository institutions, economies in op-erations made possible by the application in-formation technology have made other meansof market entrance possible. Twenty-five sav-—-————

‘“Federal Reserve Press Release, Aug. 11, 1983.

ings and loan associations and savings banksown ISFA Holding Co., Ltd., which operatesINVEST, a brokerage service, through awholly owned subsidiary. Thrift institutions,which would not be able to enter the brokeragebusiness independently, can offer transactionand advice investment services to their cus-tomers by subscribing to INVEST.

Special INVEST centers are placed inbranches where they are accessible and evi-dent to customers, yet remain separate anddistinct, by order of SEC and the FederalHome Loan Bank Board, from the other opera-tions of the thrift. Just as the securities indus-try is developing and offering new productsto retain clients, this is also a basic motiva-tion behind INVEST. Thrifts are thus able toexpand the services they can offer their cus-tomers.

Trades conducted through new alternativebrokerage services are executed through theexchanges, usually by way of a clearing bro-ker. The securities industry finds itself in theposition of servicing competitors, a situationthat is quite common throughout the financialservice industry. As capabilities and econ-omies found in information technology con-tinue to grow, more entrants maybe expectedand the wholesale portion of the securities in-dustry will probably grow.

Possible Entrants to the Securities Industry

Players throughout the financial service in-dustry, including the securities industry, havebeen expanding their product lines to fill asmany of their clients’ needs as possible. Rec-ognized economies of scope usually underliethis expansion of distribution systems, bothfor information and for community presence,and in terms of complementing current prod-uct lines. Providers often feel they can retaintheir customer base by entering other lines offinancial services.

The entrance of other financial service play-ers into the securities industry is already oc-curring. Several insurance companies havepurchased regional brokers, and some depos-itories have acquired discount brokers. Shear-

64 ● Effects of Information Technology on Financial Services Systems

son/American Express and Prudential Bacheare both results of mergers between playersin different sections of the financial servicesindustry. Consolidation within the financialservice industry is likely to continue.

Others, not traditionally thought of as pro-viders of financial services, have also enteredthe securities industry. The most widely citedexample is Sears’ entrance through the acqui-sition of Dean Witter.

Other players who may recognize significanteconomies of scope in entering the securitiesindustry are firms in the communications andcomputer industries. These firms might be inan especially strong position to enter thewholesale side for the securities industry. Bar-riers to entry, such as exchange membership,may be overcome by technology. Computerand communications technologies allow for thecreation of information and transacting sys-tems not dependent on the current industrystructure.

The Securities Industry and theInternational Market

The securities industry has its roots in theneed for the American economy to interact inthe international capital markets. However,prior to the completion of the transatlanticcable in 1866, a real international market couldnot exist because it was impossible to conveyinformation in any meaningful time frame. In-formation technology has made it possible forthe American securities industry to interactin the international market, while economicforces have made it essential.

Information technology has allowed a globalcapital market to develop, resulting in in-

creased opportunities both for investors andcapital seekers. Foreign individuals and insti-tutions made purchases and sales of $79.8 bil-lion of domestic corporate stock in 1982, andtransactions in all securities resulted in a netinflow of $14.3 billion in capital to the UnitedStates. ’g

Communications technologies are so ad-vanced that a market anywhere in the worldcan be selected for trading. This could havesignificant impacts on the stability of the econ-omies of nations. For example, the halting oftrading on an exchange in one country couldsimply result in new trade in another nation.It is not clear what impact large differencesin the valuation of a security by different coun-tries could have on capital markets. Interna-tional issues in the development of capitalmarkets are being considered by various or-ganizations. One such organization is theFederation Internationale des Bourses de Va-leurs, an association of 30 stock exchanges in20 countries.

The Effects of Information Technology onthe Structure of the Securities Industry

The application of information technologyin the securities industry affects its structureby facilitating the flow of information to suchan extent that it removes geographic con-straints on market participants and allows fordevelopment of international capital markets.It may also place additional barriers to entryto the securities industry. Without adequateaccess to telecommunication services, for ex-ample, a securities firm cannot function.

1’New York Stock Exchange 1983 Fact Book, op. cit., p. 63.

The Functions of the Securities Industry

The most significant role of the securitiesindustry is in the development of capital. Theinstitutions and players of the securities in-dustry facilitate the development of capital

structures of organizations and corporations.While it would be possible for organizationsin search of financing and potential investorsto interact directly, the market structure that

Ch. 3—The Securities industry ● 6 5

has developed provides needed services moreefficiently. Since most corporations and orga-nizations do not approach capital markets fre-quently, financing with the aid of the securi-ties industry is usually more cost effectivethan direct attempts because of the expertisesecurities institutions have in analyzing secu-rities markets and in locating potential inves-tors, and because of the ability of the securi-ties industry to accept risk.

The use of information and communicationtechnologies by the industry is nearly univer-sal, and adjustments may be expected in op-erations as the value of technology is realized.However, while information technology maychange the way in which the securities indus-try performs its activities, and may even fa-cilitate attempts by investors to act on theirown behalf, it is expected that the basic func-tions of the securities industry will remain anessential part of the development of capital.In this section, an overview of the functionsof the industry and the emerging effect of theapplication of information technology on theseroles will be described. The significance of theadvisory, risk-accepting, and marketing func-tions of the securities industry to the processof gathering capital will be outlined, and theeffect of information technology on this proc-ess will be summarized. Specific approachesto capital formation are discussed in appen-dix 3B.

The Securities Industry as an Advisor

In its advisory role, the securities industryprovides information and offers guidance toits clients. It is able to advise organizationsseeking capital on the type of financing mostdesirable, whether through private or publicmeans, and, perhaps most significantly, whatthe timing for entering the capital marketshould be. These decisions are based on the ob-jectives of the firm. Factors to be consideredinclude the risk and return associated withvarious issuing organizations and instru-ments. Timing of buy and sell decisions is alsopart of this advice function.

Information Dissemination

Information technology affects informationdissemination by the securities industry inseveral ways. Information is now less costlyto gather, store, and access than it was inlargely manual systems. Therefore, not onlyis it likely that the quantity and quality ofavailable information will increase, but alsothat more information will be sought. Inves-tors and other parties interacting with thesecurities industry may be expected to makebetter and more satisfying decisions becauseof the increased availability of information.

Technology has already had a major impacton information flows throughout the securitiesindustry, and it appears that the resultantchanges may have major impacts on the oper-ation and, in time, the structure of the securi-ties industry. Information technology en-hances the reporting of securities trades. TheConsolidated Quotation System, which wentonline in 1978, collects and disseminates quo-tation information from exchanges across theNation and calculates and appends the na-tional Best Bid and Offer to the quotation in-formation. 20 Communication technologymakes it possible to transmit this informationin real time to system subscribers nationwide.A similar system is in place on the NYSE fordebt issues. The Automated Bond System pro-vides current quotation and trade informationfor more than 80 percent of the exchange-listedbonds.21 This system has improved the qualityof information available on bond trading.

Information technology may increase theindependent role investors assume as infor-mation monitors, particularly the individualinvestors. Although massive quantities of fi-nancial information are currently availablethrough a variety of media, such as news-papers, radio, and television, and through pub-licly available consolidated tapes, individualinvestors may expect to have even more in-

‘“Securities Industry Automation Corp., Annual Report, NewYork, 1982.

21 New York Stock Exchange, Amual Report 1982, New York.

66 . Effects of Information Technology on financial Services Systems

formation at their disposal. While a “more isbetter” philosophy is usually applied to infor-mation, the result can be confusing, deceptive,and frustrating to users. Moreover, informa-tion gathered by intermediaries within thesecurities industry may require translation toa form that can be used by clients.

The adoption of home information systems,particularly interactive cable and personalcomputer systems, may change the way inwhich this information is gathered and used.E. F. Hutton and Dean Witter provide cus-tomers with securities research that can be ac-cessed via home computers.22 It is not clearhow investors will use this information. Thecontinual availability of new information mayresult in more frequent trading; however,home systems may just be, in the aggregate,a new medium. Investors may evaluate nomore information than they did in the past.

Computer and communication technologieshave increased the speed with which informa-tion is available to the mass market. With thesystems now available, investors may becomeless dependent on a broker or dealer for up-dated information. An example of this type ofsystem is Pocket Quote, produced by TelemetAmerica, Inc. The basis of Pocket Quote is an1 l-ounce programmable receiver, which lookslike a calculator and can be used to monitorthe New York and American Stock Exchangesas well as option exchanges. Information, in-cluding price and trade volume, on up to 20securities specified by the user is transmitted,subject to a 15-minute delay. The data arebroadcast in a scrambled form on FM sidebands, using a digital signal. Not only is theinformation readily available to the investor,but the system can be programed to page theuser automatically at any time there is “news”about any investment instrument in which he/she is interested.

The potential for investors to act immedi-ately on information continually updated andtransmitted via such systems may affect thestability of securities markets. The ability of

“Tim Barrington, “Stock Trading by Computer EntersHomes, ” The Wall Street Journal, Oct. 6, 1983.

the market to correct itself in unusual situa-tions may be destroyed. In the long run, thismay be a severe disadvantage for the investor,particularly the small investor, who may findhimself bearing both transaction and lost op-portunity costs because of action taken because of basically meaningless market fluc-tuations.

Counseling

The nature of counseling may be changedby the amount and type of information andsupporting analytical tools available. Researchis expected to become pivotal rather than pas-sive in the investment advisory function.23

Analysis and recommendations presented bysecurities industry intermediaries to clientsconcerning potential investments may be moredetailed and, to complement this process, anal-ysis of the financial needs of the individualmay also improve.

Increased availability of information tech-nology has changed the nature of counselingby placing more sophisticated analytical toolsin the hands of both advisors and investorswho may not have had access to these toolsin the past. This change may affect the wayin which investment decisions are made andthe quality of these decisions.24

The reliance on information technology foranalysis of personal investment needs, objec-tives, and choices may indicate an initial movein the industry to reemphasize individual hu-man judgment and perhaps a reemphasis ofthe client/broker relationship. It is not clearwhat the impact of this change will be; how-ever, a decline in personalized service, basedon the evaluation by the broker of the client’sfinancial objectives, may occur.

While counseling may be displaced in someareas within the securities industry, its impor-tance as a separate and unique service of theindustry has been highlighted in some cases.

“Thomas Moore, “Ball Takes Bache and Runs With It, ” For-tune, Jan. 24, 1983, pp. 97-98.

24 Lee B. Spencer, “The Electric Library, ” remarks to theAmerican Bar Association, Federal Regulation of SecuritiesCommittee, Nov. 19, 1982.

Ch. 3—The Securities Industry ● 6 7

Advice, particularly counseling, has been un-bundled from the total package of services of-fered in a new service supplied by MerrillLynch, called “Pathfinder.” For a set fee, theclient receives what amounts to a financialcheckup. The evaluation provides guidance tothe investor in a somewhat objective frame-work. The success of this product may be anindication of the future role of advice withinthe securities industry.

Acceptance of Risk by theSecurities Industry

The securities industry accepts risk thatmight otherwise be experienced by individualsor organizations seeking investment. It doesthis in two ways: through underwriting andby the extension of credit through margin.Underwriting refers to the assumption of riskby an investment bank or other third partyat the time of a public offering. The extensionof credit by brokerage houses is referred to asmargin.

Underwriting New Issues

Underwriting involves the purchase of se-curities from the issuing company and thesubsequent resale of the instruments to thepublic. This service, which is usually per-formed by investment bankers, is essential tofirms in need of capital that are not in the busi-ness of marketing securities. It allows themto receive the funds they need while transfer-ring the marketing function to an expert whomay be expected to be more effective in reach-ing prospective investors.

The underwriter accepts some of the riskassociated with a public offering. He preventslag time by assuring that the issuing corpora-tion has access to the funds it is attemptingto raise when needed. By buying the public of-fering from the firm in search of financing, theunderwriter makes it easier for the manage-ment of the firm to plan the use of the fundsgenerated. The issuing organization may beless concerned about the flow of cash the saleproduces because it is usually guaranteed afixed price and can use those funds when the

agreement with the investment bank or otherunderwriter is closed.

In most cases, the underwriter also assumesrisk by assuring that the issue will be sold, andhe accepts the risk that market fluctuationsor initial pricing mistakes may influence thesuccess of the issue. Offerings underwrittenon a “best efforts” basis, where the under-writer does not bear the risk of an unsuccessfuloffering, permit those issuers in a startup ordevelopmental stage, whose issues may beconsidered to be more risky, to have access tothe public capital markets.

Underwriters earn money by buying secu-rities at a lower price than they resell them forto investors. The difference in price, or spread,is a major consideration in the selection of aninvestment bank by a firm. A prospective cli-ent for an underwriter may choose an invest-ment bank through two methods: competitivebidding or negotiation. Both systems have ad-vantages, and experts disagree on which pro-vides the best price for the capital seeker. Theadvantage of the negotiated system is that theissuing firm and the underwriter work to-gether to make decisions about the pricing andtiming of the issue.

The company using a competitive biddingsystem invites offers from investment bank-ers. This process is required for many publicutilities and most municipal offerings. Butwhile some experts believe it results in highernet proceeds for the issuing organization (be-cause of the forces of competition), it has dis-advantages. Much of the benefit of the advi-sory function that the issuing company wouldenjoy in a negotiated situation is lost. A higherprice may be received, but this largely dependson the health of the market at the time of theoffering. In a depressed market, investmentbankers are less likely to compete for a pub-lic offering, and therefore the price receivedmay be lower.

It is also typical for investment banks tominimize their risk by forming syndicates.This spreads risk and benefit because of theirpooled sales force and allows a number ofunderwriting firms to participate together in

68 • Effects of Information Technology on Financial Services Systems

large public offerings. Changes in industrystructure, particularly consolidation among in-vestment banks, may affect this operation.

The presence of an underwriter provides avaluable service for the prospective investor.Investment bankers are expected to examinethe corporate records with due diligence andare liable to defrauded investors if they failtheir due-diligence obligations and miss anymisstatement or omission of material fact bythe issuer in the prospectus. Therefore, notonly does an underwriter assure that the issuewill be sold in a “firm commitment” offering,but it also provides an oversight function ofthe issuer on behalf of prospective investors.

The underwriter also frequently accepts riskthrough providing a secondary market for se-curities by maintaining a position in the stock.This activity, called “making a market, ” issimilar to the role played by securities special-ists, which is discussed in a later section. Theunderwriter quotes “bid” and “asked” pricesfor the security based on market supply anddemand and intervenes as a buyer or seller,when necessary. The original offering of a debtor equity issue may be expected to be moresuccessful when the potential investors knowthat the existence of a secondary market isguaranteed.

Information technology may affect theunderwriting function by decreasing the timebetween the initial development of a securitiesissue and its sale, lessening the need of capi-tal seekers to be protected against this lag.Pricing decisions and market evaluations maybe more certain if the time frame in which thesecurity is offered is lessened.

Price competition has been increasing in thearea of underwriting. Since the use of syndi-cates is decreasing, there is a greater need forindividual firms to have substantial capital ifthey are to continue functioning as underwrit-ers.25 Information technology may be a con-tributing factor in the advent of bought dealsthat involve the purchase of an entire issue,

usually by a single underwriter who has notlined up buyers in advance. While informationtechnology may allow underwriters to locatebuyers quickly, more risk is involved in thismethod than with a traditional syndicate.

The emphasis on price competition maybea disadvantage for corporations entering cap-ital markets because the benefits of advice onpricing and timing of an issue is sacrificed.While sophisticated analytical tools, which in-formation technology may enhance, may as-sist corporations seeking financing in evalu-ating various possibilities, this type ofanalysis may not be tailored to the needs andobjectives of corporations to the same extentas the information and counseling services pro-vided by an underwriter.

Margin

“Margin” refers to the amount of moneypaid by an investor to acquire a securitythrough credit instead of cash. At the end of1982, the securities industry held nearly $13billion ($12.98 million) in margin debt securedby nearly $39 billion ($38.88 million) worth ofcollateral. 26

The Securities Exchange Act of 1934 em-powers the Federal Reserve Board to regulatethis extension of credit. Brokers are permittedto extend regulated credit on stocks and con-vertible bonds traded on registered exchangesas well as some select over-the-counter stocks.Initial margin requirements, set by the Fed-eral Reserve Board, currently call for a depositequal to 50 percent of the total value for bothstocks and convertible bonds. Stock ex-changes and other self-regulatory agencies ofthe industry have individual requirements forthe opening and maintenance of margin ac-counts. For example, the NYSE requires aninitial deposit of at least $2,000 and the main-tenance of equity of the customer at 25 per-cent of the value of securities carried.

The advent of home equity access accounts,encouraged by advances in information tech-nology, may increase the amount of margin

25A. F. Ehrbar, “Upheaval in Investment Banking, ” Fortune,Aug. 23, 1982, pp. 90-95, Z6New york Stock Exchange 1963 Fact Book, OP. cit., Il. 46.

-..

Ch. 3—The Securities Industry ● 6 9— —

debt and change the nature of collateral. Whilesome accounts restrict this use of credit drawnfrom home equity for the purchase of securi-ties, in many situations this is acceptable.

Margin takes on a different meaning in op-tion and futures contract trading. In futurestrading, margin refers to the amount of moneyor collateral which a client is required to de-posit with his broker to insure the brokeragainst losses on open futures contracts. Op-tion writers must, similarly, deposit cash orsecurities with their brokers so that the bro-kers are covered in case of an assignment.

Margin plays an important role in specula-tion in securities markets. A frequently usedstrategy in the buying and selling of securi-ties is the “short” position. In this case, aninvestor sells securities he does not own, buthas borrowed, to make delivery in the hopesthat the price will decline before it is neces-sary for him to return the security. This activ-ity can be extremely risky. However, it ac-counts for a significant amount of marketactivity. In 1982, 1.5 billion shares, in roundlots, were sold short, an amount that was 9.3percent of all reported securities sales.27

Information technology may decrease thesignificance of margin as a convenience forbrokerage customers because it eases accessto assets and facilitates funds transfers. Cus-tomers may be able to finance securities pur-chases using other assets whose liquidity hasincreased as a result of increased use of infor-mation technology. It is not clear what the neteffect will be; however, the use of electronicfunds transfers may largely eliminate the useof margin by brokerage houses to providefloat.

Marketing by the Securities Industry

For purposes of discussing the securities in-dustry, “marketing” is defined as those activ-ities designed to identify and meet the needsof clients; i.e., both seekers of capital and in-vestors. It is assumed that these clients do notdemand a specific product or type of service,

but rather, that the clients recognize an un-filled need and seek a way to meet it.

At one time the operations of the securitiesindustry were centered on what was possible,given the regulatory framework and its busi-ness concerns. Now, a new awareness of theimportance of basic marketing to retain anddevelop business is evident, resulting in re-search to support activities in product devel-opment and promotion and the targeting ofspecific segments of the population for special-ized products. Given the competition the in-dustry faces in its traditional and new prod-uct lines, especially from new entrants into thefinancial service industry, the marketing func-tion may be expected to continue to grow inimportance for the foreseeable future.

Information technology may affect thosemarketing functions of the securities industrythat comprise product development, sales orbrokerage, and pricing.

Product Development

In recent years, the regulatory restraints onthe financial service industry have decreased,and the securities industry has found competi-tors in what at one time were strictly separatebusinesses. These developments have occurredwhen the securities industry was observing acontinual demographic and psychographicchange among its potential retail clients, agrowing institutional market, and more com-plex financial needs among organizations seek-ing capital.

Shifts in the area of product developmentare seen mainly in the way products are pack-aged, specifically in the variety of mutualfunds and money market mutual funds thathave been developed. It is not yet clear howpatent and copyright laws will affect the de-velopment of information technology-based fi-nancial services products. If financial serviceproducts become patentable, some securitiesindustry experts believe that competitioncould be stifled.28 Many financial service prod-ucts are similar in both character and features,

“New York Stock Exchange 1983 Fact Book, op. cit., p. 48.“’’Merrill Lynch Wins Cash Account Row With Dean Wit-

ter, ” The Wall Street Journal, Dec. 29, 1983, sec. 1, p. 2.

70 • Effects of Information Technology on Financial Services Systems

and therefore, there is an inherent possibilityof patent infringement. Differentiating prod-ucts by attribute has not been of great interestto the financial service industry, which hascompeted by geographic market and compara-tive return and cost.

Information technology has created interestin patenting financial service products becausecommunications and computer technologieshave broadened markets. Products that at onetime may have been offered locally now com-pete nationally. Therefore, protection of prod-uct may become as necessary as the position-ing of the product.

The patentability of financial products isnow being tested in cases involving the cen-tral-asset account. In response to perceivedconsumer demand, most major firms in thesecurities industry, including Dean Witter,Paine Webber, Shearson/American Express,and Prudential Bache, have introduced theseaccounts, which are combination margin ac-counts and investment funds. Merrill Lynchled the development of asset managementaccounts with its introduction of the cashmanagement account in 1977, for which it re-ceived patents in August 1982 and March1983, and, with over 1 million accounts, is themarket leader. Following the receipt of its pat-ent, Merrill Lynch notified competitors thatit was imposing an annual licensing fee of $10on all asset management accounts. Initially,this levy was not taken seriously throughoutthe industry; however, without admitting anypatent infringement, Dean Witter resolved itsdispute with Merrill Lynch about the accountsin late December 1983 for $1 million. The firmsagreed to “grant each other a nonexclusive,royalty-free license to use any improvementsor changes either might make relating to cen-tral-asset accounts. ”29

If financial service accounts are routinelypatented, investors may find that their choicesare limited, since the patent may be a barrierto entry into some product lines for some serv-ice providers. Since players within the securi-

29Ibid.

ties industry may be expected to make effortsto distinguish similar products legally, patent-ing may also increase consumer confusionabout product features and attributes.

Brokerage

Brokerage involves bringing together buy-ers and sellers, facilitating trades through themaintenance of a marketplace, and assuringthat the trade is complete. The significance ofthis activity as part of the operations of thesecurities industry cannot be overestimated.Traditionally, all of the costs of supporting aninvestment bank or brokerage house were re-covered through this portion of the business.The services provided to clients, such as re-search support and advice, were bundled intothe commission rate for purchasers of securi-ties and into the spread on new issues for in-vestment banks.

The heart of brokerage with retail clients hasbeen personal selling. The relationship be-tween the investor and the individual brokerhas been fairly constant, and typically, the ac-counts a registered representative developswhile with a particular brokerage house movewith him if he/she switches firms. Firms withinthe industry have expended great effort in at-tempts to retain clients. The development ofnew products unique to particular houses mayencourage a loyalty to the company ratherthan to the broker. It is not yet clear how thismight change the character of the industry.

Most technology-encouraged competition isoccurring within the selling function of retailand institutional brokerage. The end of stand-ardized commissions on the sale of securities(1975) has encouraged the entrance of dis-counters into this market. Discount brokerscomplete trades for investors at prices that aregenerally lower than the commission chargedby full-service brokers. Usually, the serviceprovided by discounters is limited; e.g., thesefirms usually do not support extensive re-search and advice operations. However, theydo fill the needs of a portion of the market.About 15 percent of trading by individual in-vestors is handled by discounters.

Ch. 3—The Securities Industry ● 7 1

Access to information technology for indi-viduals will facilitate direct selling of securi-ties to investors without the interaction of abroker. This type of system is particularlyadaptable for discount brokers whose serviceis basically order-taking. C. D. Anderson &Go., a small discount broker, developed thefirst home brokerage system, and other bro-kerage houses are expected to enter this mar-ket. 30 C. D. Anderson’s system allows clients,who pay a hook-up charge and a usage charge,to enter buy and sell orders at their conven-ience, without dealing with a broker.

Transactions

Congress mandated the development of acomputerized national stock market systemin 1975, believing that by linking all marketcenters, such a market would expose securi-ties to a greater number of buyers and sellers,and an investor would have the chance to ob-tain the best price available. This system wasalso expected to provide competition toNYSE, which dominated the market with 80to 90 percent of the trading volume.

The Cincinnati Stock Exchange was ex-pected by many industry experts to becomethe basis of an automated national stock ex-change. The exchange was supported by Mer-rill Lynch, the largest firm within the securi-ties industry. In July 1983 Merrill Lynchwithdrew a large portion of its business fromthe Cincinnati Stock Exchange and returnedit to the floor of NYSE, noting that not onlyhad the Cincinnati Stock Exchange failed togain the volume anticipated, but that NYSEhad improved.

While NYSE is still largely based on a sys-tem of auction pricing and securities special-ists, the adoption of systems made feasible bythe application of information technology hasallowed it largely to eliminate problems asso-ciated with high volume. In addition, commu-nications systems have been developed thatallow users of NYSE to enjoy many of thebenefits of a national system by providing in-formation on the activities of regional ex-

‘°Carrington, op. cit.

●

35-505 0 - 84 - 6 : QL 3

changes. One such system, the IntermarketTrading System (ITS), may be seen as beingindicative of a trend toward a national mar-ket for securities trading.

ITS allows brokers, specialists, and marketmakers to interact with their counterparts atother markets. The system, maintained bySIAC, currently involves eight stock ex-changes: New York, American, Boston, Phila-delphia, Cincinnati, Midwest, Pacific, and, toa limited extent, NASDAQ.

ITS provides a mechanism through whichthe most favorable exchange setting can bechosen for a transaction. * At NYSE, the bestprice from any member of ITS, as well as theNYSE floor price, is displayed. If it is advis-able for a trader to deal on an exchange otherthan the one at which he is operating, he canenter his order by contacting his counterpartthere. At the end of 1982, 1,039 issues wereeligible for trading on ITS. NYSE reports thatthis represents most of the stocks traded onmore than one exchange.

The Designated Order Turnaround (DOT)system was introduced in 1973 to route smallorders (599 shares or less). It reports elec-tronically between NYSE and member firms.DOT bypasses floor brokers by routing ordersdirectly to the appropriate trading post on thefloor of the exchange and, following execution,back to the member firm on the same elec-tronic circuit. Over 80 percent of the 5.7 mil-lion market orders processed through DOT in1982 were executed and reported back to themember firm within 2 minutes.31 This systemminimizes the cost to member firms of han-dling small transactions while giving small in-vestors the benefit of timely execution of theirtrades. DOT may also provide a better pricethan would normally be received by a smallinvestor. A trade made through DOT ismatched by computer for price with the mostrecent trade of that issue. The investor bene-fits because the price he receives may have

*For Purpows of this discussion, “transacting” is defined asthe physical execution of trades.

“New York Stock Exchange 1983 Fact Book, op. cit.

72 . Effects of Information Technology on Financial Services Systems

resulted from price negotiation on a muchlarger order.32

Another technology-dependent system thatfacilitates transacting is the Opening Auto-mated Report Service (OARS). OARS makesefficient and accurate processing of marketorders, that are received at NYSE prior to thestart of daily trading, possible without caus-ing unnecessary delays in the opening of trad-ing, and transmits computer-generated reportsto the originating member firm.33 This systemis especially valuable to specialists on dayswith high trading volume, which have recentlybeen occurring with great regularity.

Future developments in transacting en-hanced by information technology may includethe bypassing of intermediaries in the proc-ess of selling. Some experts believe that theadoption of home information systems maymake it more common for investors to com-plete transactions between themselves pri-vately or to gain direct access to exchangefloors. While it does not appear that the pos-sibility of off-market trading is having a ma-jor impact on the individual investor at thistime, institutional investors have at timesfound it advantageous to trade off-market.

About 500 brokerage houses, pension funds,insurance companies, and other institutionalinvestors are linked through AutEx Systems,a nationwide computer network. The potentialof this system for trading was demonstratedby its use in creating a market in a stock forwhich trading had been closed by NYSE. Jef-feries & Co. is a discount broker specializingin institutional trading. It is not a member ofany major exchange and therefore is able tomake a market in an exchange-listed stockwithout going through the exchange. Follow-ing a request by a client, Jefferies announcedover the AutEx System that it was makinga market in the closed stock. The companytraded a total of about 8 million shares of thestock off-market.34

3’Desmond Smith, “The Wiring of Wall Street, ” The NewYork Times Magazine, Oct. 23, 1983, p. 109.

33New York Stock Exchange, Annual Report 1982, New York,p. 33.

“Smith, op. cit., p. 73.

Given that the primary responsibility of se-curities exchanges is to maintain an orderlymarket, technology, the great facilitator oftheir operations, could also be a major under-mining force for the exchanges. It is basicallymeaningless to stop trading for a security onan exchange if the end result is simply thattrading is moved off of the exchange and con-ducted without the prudent management ofthe specialist. It may be essential for ex-changes to continue trading a given securityin all but the most unusual situations.

Clearance and Settlement of Securities