THE ROLE OF SME BANK IN MEETING SPECIFIC FINANCIAL …

19

1 THE ROLE OF SME BANK IN MEETING SPECIFIC FINANCIAL NEEDS OF SMEs

Transcript of THE ROLE OF SME BANK IN MEETING SPECIFIC FINANCIAL …

1

THE ROLE OF SME BANK IN MEETING SPECIFIC FINANCIAL NEEDS OF SMEs

2

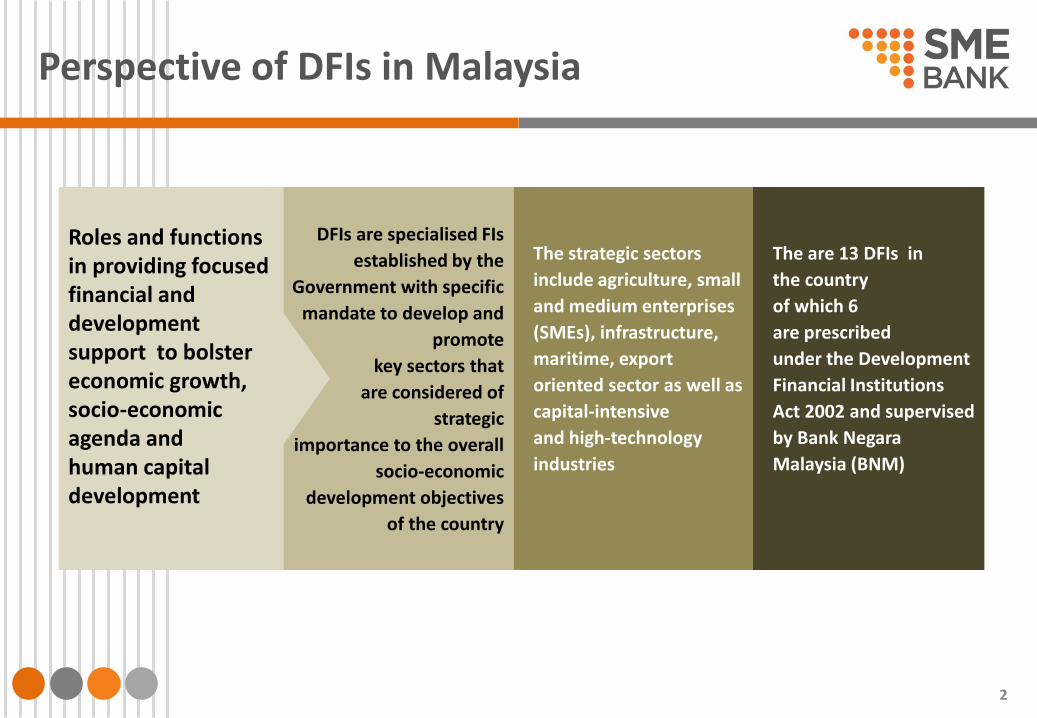

Perspective of DFIs in Malaysia

DFIs are specialised FIs

established by the

Government with specific

mandate to develop and

promote

key sectors that

are considered of

strategic

importance to the overall

socio-economic

development objectives

of the country

Roles and functions in providing focused financial and development support to bolster economic growth, socio-economic agenda and human capital development

The strategic sectors

include agriculture, small

and medium enterprises

(SMEs), infrastructure,

maritime, export

oriented sector as well as

capital-intensive

and high-technology

industries

The are 13 DFIs in

the country

of which 6

are prescribed

under the Development

Financial Institutions

Act 2002 and supervised

by Bank Negara

Malaysia (BNM)

3

SME Bank: An Overview

4

Ownership & Reporting

MOF Inc. Bank Negara

Malaysia MITI

SME Bank

Supervising Ministry

Shareholder 100% owned

Regulator Under DFIA 2002

Broad Focus on:

• Manufacturing sector • Services sector • Construction sector

• Authorized Capital RM5.0 billion

• Paid up Capital RM1.35 billion

5

Vision & Mission

A Full-Fledged

Specialised Financial

Institution With Global

Aspiration To Nurture

SMEs For Nation Building To Support

Government’s

Economic Agenda

In Developing SMEs

As An Engine Of

Growth

&

6

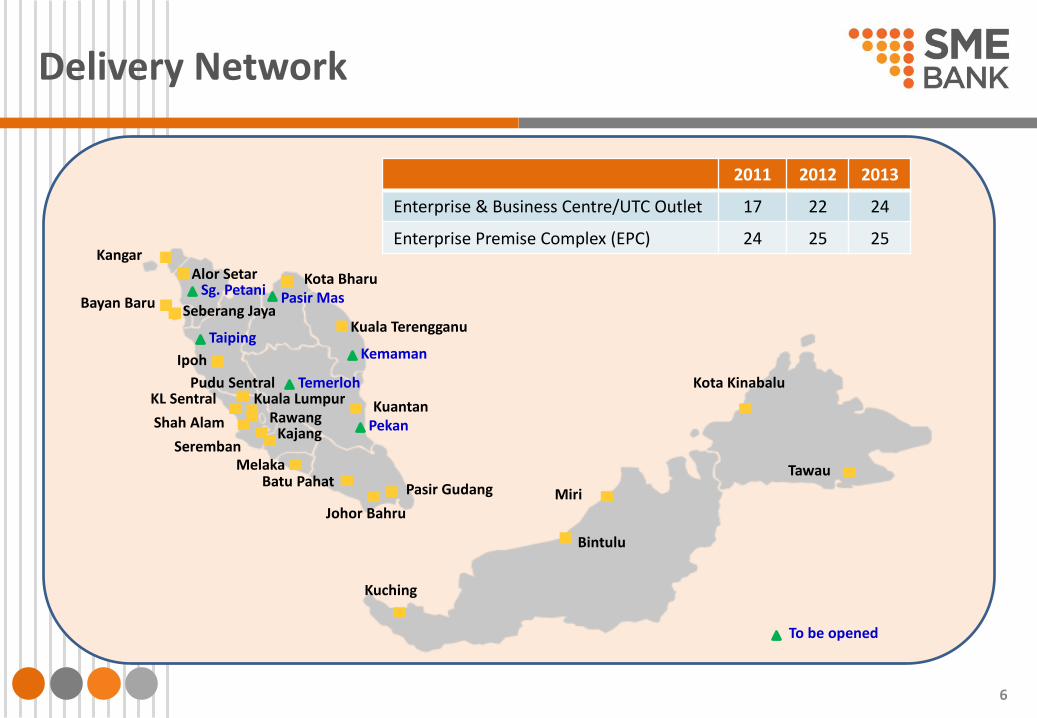

Delivery Network

Kuala Lumpur Kuantan

Johor Bahru Miri

Kota Kinabalu

Kuching

Melaka Seremban

Shah Alam

Ipoh

Kota Bharu

Kuala Terengganu

Bayan Baru Seberang Jaya

Alor Setar Kangar

Tawau

KL Sentral Rawang

Kajang

2011 2012 2013

Enterprise & Business Centre/UTC Outlet 17 22 24

Enterprise Premise Complex (EPC) 24 25 25

Sg. Petani

Taiping

Pudu Sentral

Pasir Mas

Pekan

Temerloh

Kemaman

Batu Pahat Pasir Gudang

Bintulu

To be opened

7

SME Bank: Major Roles

8

INNOVATION AND

TECHNOLOGY ADOPTION

- Encourage greater innovation and

technology adoption by SMEs

ACCESS TO FINANCING

- Ensure that

creditworthy SMEs have access to

financing for working capital and investment

LEGAL AND REGULATORY

ENVIRONMENT

- Ensure that legal and regulatory environment is

conducive for the formation and

growth of SMEs, while protecting the broader interest of

society.

HUMAN CAPITAL

DEVELOPMENT

- Enhance human capital and

entrepreneurship development among

SMEs

MARKET ACCESS

- Expand the

market access for goods and services produced by SMEs

INFRASTRUCTURE

- Improve the infrastructure for the

SMEs to operate effectively.

6 Focus Areas

41% share of GDP

(2010: 32%)

62% share of employment

(2010: 59%) 25% share of exports

(2010: 19%)

NATION

Our role in SME Master Plan 2012-2020

9

Government’s Economic Agenda - NKEAs

Islamic

10

SME Bank: Financing & Non financing activities

11

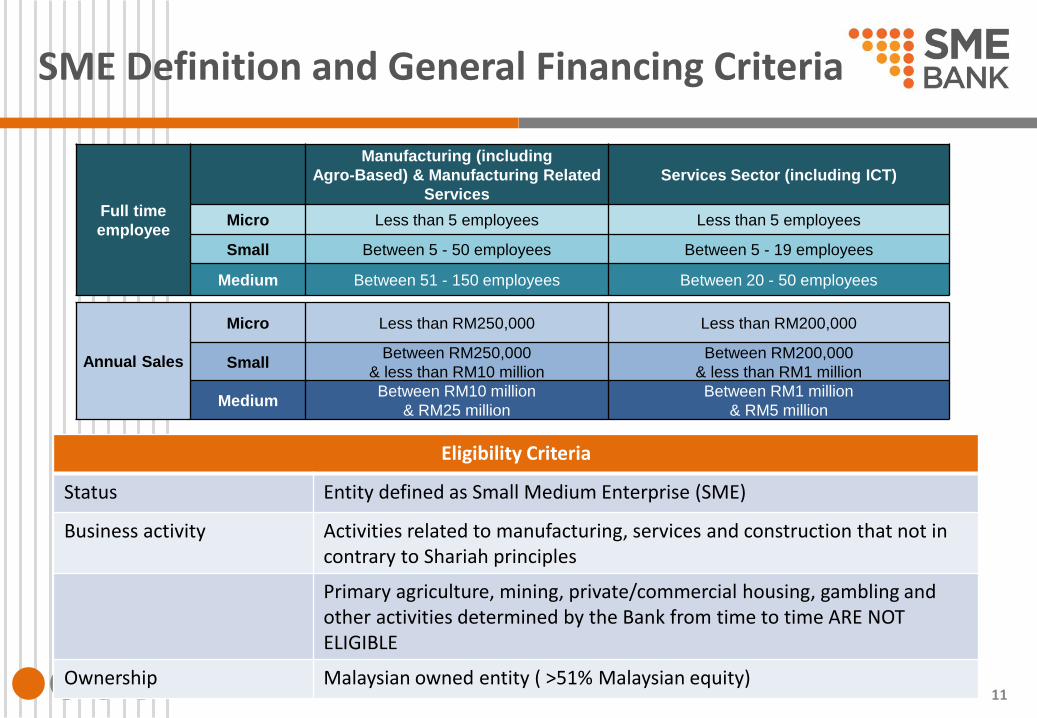

SME Definition and General Financing Criteria

Full time

employee

Manufacturing (including

Agro-Based) & Manufacturing Related

Services

Services Sector (including ICT)

Micro Less than 5 employees Less than 5 employees

Small Between 5 - 50 employees Between 5 - 19 employees

Medium Between 51 - 150 employees Between 20 - 50 employees

Annual Sales

Micro Less than RM250,000 Less than RM200,000

Small Between RM250,000

& less than RM10 million

Between RM200,000

& less than RM1 million

Medium Between RM10 million

& RM25 million

Between RM1 million

& RM5 million

Eligibility Criteria

Status Entity defined as Small Medium Enterprise (SME)

Business activity Activities related to manufacturing, services and construction that not in contrary to Shariah principles

Primary agriculture, mining, private/commercial housing, gambling and other activities determined by the Bank from time to time ARE NOT ELIGIBLE

Ownership Malaysian owned entity ( >51% Malaysian equity)

12

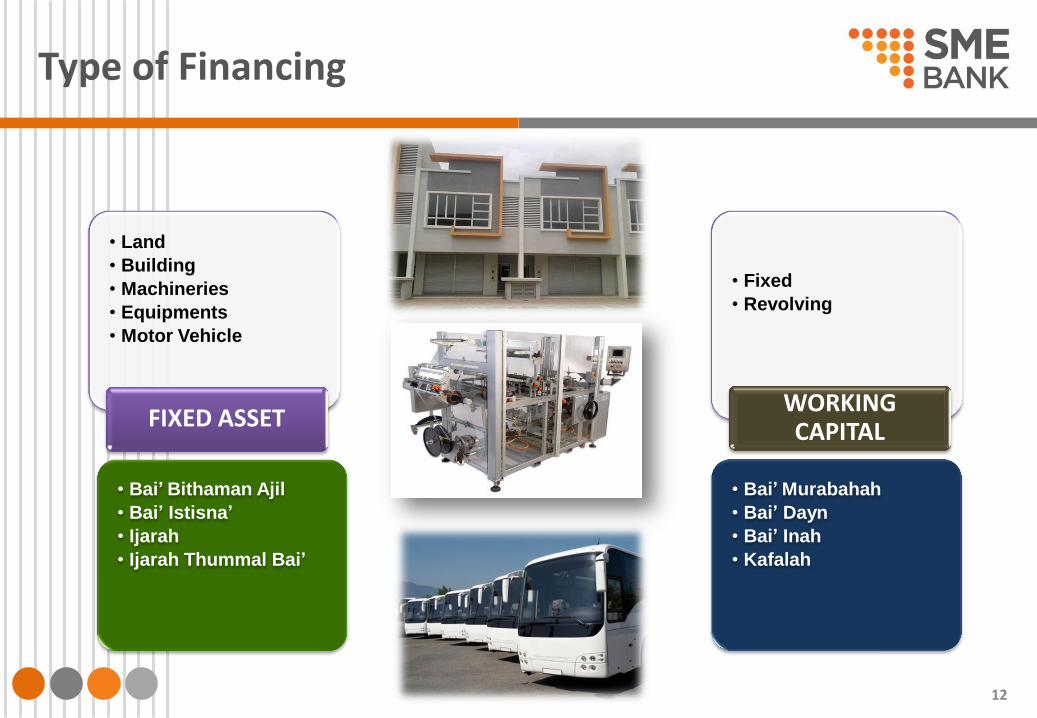

Type of Financing

• Bai’ Bithaman Ajil

• Bai’ Istisna’

• Ijarah

• Ijarah Thummal Bai’

• Land

• Building

• Machineries

• Equipments

• Motor Vehicle

FIXED ASSET

• Fixed

• Revolving

• Bai’ Murabahah

• Bai’ Dayn

• Bai’ Inah

• Kafalah

WORKING CAPITAL

13

Trade Services

Issuance of Letter of Credit

• Through Agent Bank

Shipping Guarantee

• Through Agent Bank

Issuance of Bank

Guarantee

14

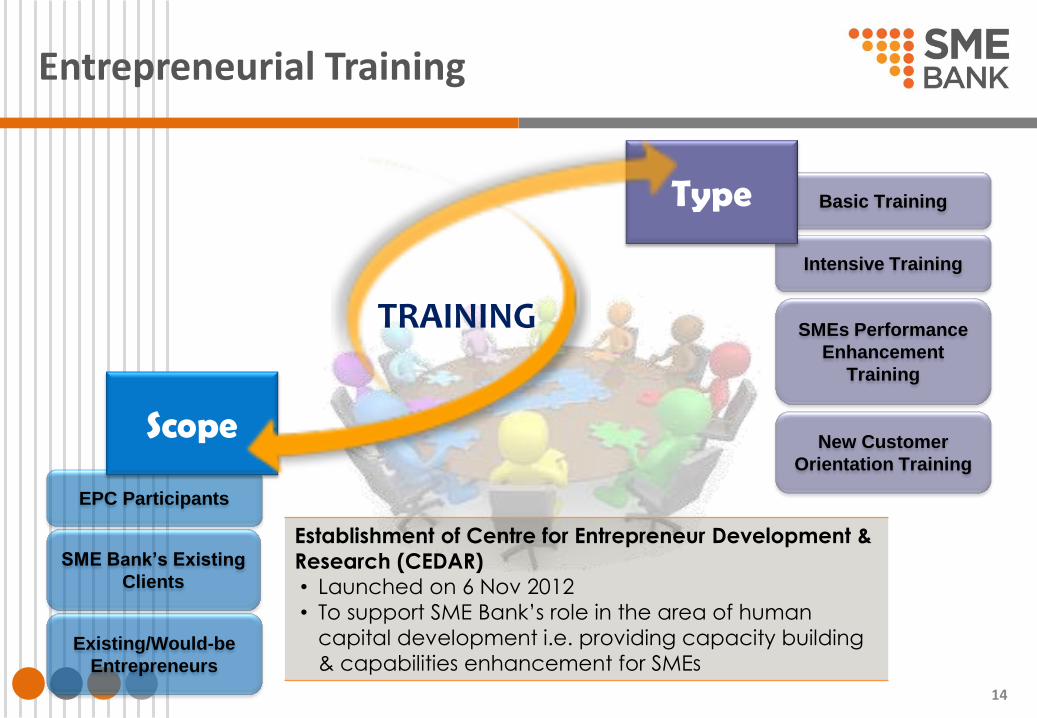

Entrepreneurial Training

SME Bank’s Existing

Clients

Existing/Would-be

Entrepreneurs

EPC Participants

Scope

Intensive Training

SMEs Performance

Enhancement

Training

Basic Training

New Customer

Orientation Training

Type

TRAINING

Establishment of Centre for Entrepreneur Development &

Research (CEDAR) • Launched on 6 Nov 2012

• To support SME Bank’s role in the area of human

capital development i.e. providing capacity building

& capabilities enhancement for SMEs

15

Entrepreneur Premise Program

25 Complexes/433 Lots

Financing Facilities

Matching Grant for Technical &

Training

Advisory Services

Entrepreneurship Training

16

i-Enterprise Premise Financing (i-EPF)

i-Enterprise Premise Financing is a financing package for the refinancing and purchase of shop-house, shop-lots, office spaces and factories. It also covers acquisition of completed or under construction properties. The package includes financing for working capital.

Margin of financing of up to 150% of Market Value (MV) of the property Longer tenure up to 30 years ; with grace period of up to 6 months (for completed

Property) and 24 to 36 months (for property under constriction) Stamp Duty, legal Fee, Mortgage Reducing term Takaful (MRTT) and Valuation Cost can be

included in the financing package Waiver for Fire & All Peril contribution (1st year only), actual cost of searches and actual cost

for Discharge of Charge (if any) No penalty for early settlement

Facility Eligibility Pricing

Islamic Bai Bithaman Ajil (BBA) Bai Istisna Bai Inah

Sole-proprietor and partnership Private Limited Co within the

National definition of SME Individual business owner

Up to BFR – 1.8%

17

Young Entrepreneur Fund (YEF) is a special fund allocated by the Government as part of its continuous strategy of acculturation and creation of new entrepreneurs among Malaysia youth. The purpose of this fund is to provide alternative access to the young entrepreneurs in obtaining financing to start their new business as well as for the needs of their existing business .

Financing Concept

Islamic Bai Bithaman Ajil (BBA) Bai Inah Ijarah, Ijarah Thummal Bai’, Bai’Istisna

Our Attractive pricing

5% per annum (Annuity Monthly rest)

Financing limit

Minimum : RM20,000 Maximum : RM100,000

Tenure

Up to 7 years including maximum 1 year grace period

Young Entrepreneur Fund (YEF)

18

Malaysian youth between 18 to 30 years of age, owning the business. The business is registered with Suruhanjaya Syarikat Malaysia (SSM) or other authorised registering

bodies under a sole-proprietorship or partnership firm, or a Sdn Bhd company. For a partnership firm or a Sdn Bhd Company, the youth applicant must hold majority shares of more

than 51% AND is the key decision maker. Minimum possession of entrepreneurship/vocational or at least 2 years experience in business to be

financed Those without entrepreneurship/vocational certificate could be considered through the acquisition

of entrepreneurship training from Centre for Entrepreneur Development and Research (CEDAR), SME Bank.

Start-up companies / firms may be considered

Young Entrepreneur Fund (YEF) ...(cont)

Working Capital Requirement Margin of Financing

Working Capital – Purchases of raw materials, stocks, overhead cost, renovation, advertising & promotion etc.

Up to 100%

Purchase of Assets for Business Operations Margin of Financing

Loose tools, machinery & equipment, office equipment, vehicle etc Brand New Used/Reconditioned

Up to 100% Up to 75%

19

Thank you

Follow us on:

Our Facebook facebook.com/smebank

Our Twitter twitter.com/sme_bank