THE ROLE OF ADVANCE PAYMENTS IN WORKING CAPITAL

63

LAPPEENRANTA UNIVERSITY OF TECHNOLOGY Faculty of Technology Management Department of Industrial Management THE ROLE OF ADVANCE PAYMENTS IN WORKING CAPITAL MANAGEMENT AND PROFITABILITY Instructors: Miia Pirttilä & Sari Viskari Examiners: Professor Timo Kärri & Professor Hannu Rantanen Lappeenranta, October 31 st , 2012 Anna-Maria Talonpoika

Transcript of THE ROLE OF ADVANCE PAYMENTS IN WORKING CAPITAL

LAPPEENRANTA UNIVERSITY OF TECHNOLOGY

Faculty of Technology Management

Department of Industrial Management

THE ROLE OF ADVANCE PAYMENTS IN WORKING

CAPITAL MANAGEMENT AND PROFITABILITY

Instructors: Miia Pirttilä & Sari Viskari

Examiners: Professor Timo Kärri & Professor Hannu Rantanen

Lappeenranta, October 31st, 2012

Anna-Maria Talonpoika

ABSTRACT

Author: Anna-Maria Talonpoika

Title: The role of advance payments in working capital management and

profitability

Year: 2012 Place: Lappeenranta

Master’s thesis. Lappeenranta University of Technology, Industrial Management.

51 pages, 9 figures, 3 tables and 2 appendices.

Examiners: Professor Timo Kärri and professor Hannu Rantanen

Keywords: advance payments, working capital, working capital management,

profitability, cycle time, CCC, mCCC, DIO, DSO, DPO, DAO

The objective of this thesis is to study the role of received advance payments in

working capital management by creating a new measurement and to study the

relationship between advance payments and profitability. The study has been

conducted using narrative literature review and quantitative research methods.

The research was made analyzing 108 companies listed in Helsinki Stock

Exchange.

The results indicate that 68 % of the studied companies are receiving advance

payments and the average cycle time for received advance payments is 13 days.

A new key figure is created to include received advance payments into the

calculation of working capital. Received advance payments shorten the working

capital cycle, by 13 days, when they are used in the calculation. The role of

advance payments is not as significant as the role of receivables and inventories

but advance payments may have a larger role than payables if the company is

receiving noticeable amounts of advance payments. There are three branches

where companies are receiving more advance payments than average companies.

The branches are project business and ICT and publishing sectors. There is a

negative correlation between profitability and advance payments based on the

results of this study.

TIIVISTELMÄ

Tekijä: Anna-Maria Talonpoika

Työn nimi: Saatujen ennakoiden merkitys käyttöpääoman hallinnassa ja

yrityksen kannattavuudessa

Vuosi: 2012 Paikka: Lappeenranta

Diplomityö. Lappeenrannan teknillinen yliopisto, tuotantotalous.

51 sivua, 9 kuvaa, 3 taulukkoa ja 2 liitettä.

Tarkastajat: professori Timo Kärri ja professori Hannu Rantanen

Hakusanat: ennakkomaksut, käyttöpääoma, käyttöpääoman hallinta,

kannattavuus, kiertoaika, CCC, mCCC, DIO, DSO, DPO, DAO

Tämän työn tarkoituksena on selvittää saatujen ennakkomaksujen roolia

käyttöpääoman hallinnassa työssä luotavan tunnusluvun avulla. Tämän lisäksi

tutkitaan saatujen ennakkomaksujen suhdetta yrityksen kannattavuuteen.

Tutkimuksen tekemiseen käytetään kuvailevaa kirjallisuuskatsausta sekä

kvantitatiivisia tutkimusmenetelmiä. Tutkimus toteutetaan analysoimalla 108

Helsingin pörssissä listattua yritystä.

Tulosten perusteella 68 % tutkituista yrityksistä saa ennakkomaksuja ja saatujen

ennakkomaksujen keskimääräinen kiertoaika on 13 päivää. Saatujen

ennakkomaksujen huomioimiseksi käyttöpääoman laskennassa, luotiin uusi

tunnusluku. Saadut ennakkomaksut lyhentävät käyttöpääoman kiertoaikaa

keskimäärin 13 päivällä, kun ne huomioidaan laskennassa. Saatujen

ennakkomaksujen rooli ei ole yhtä merkittävät kuin myyntisaamisten ja

varastojen, mutta ne voivat nousta ostovelkoja merkittävämpään asemaan, mikäli

yritys saa ennakkomaksuja huomattavia määriä. Kolmella eri toimialalla yritykset

saavat ennakkomaksuja keskimääräisiä yrityksiä enemmän. Nämä toimialat ovat

projekti-, ICT- ja kustannustoimiala. Saatujen ennakkomaksujen ja

kannattavuuden väliltä on löydettävissä negatiivinen korrelaatio tämän työn

tulosten pohjalta.

ACKNOWLEDGEMENTS

I am thankful to Professor Timo Kärri for giving this subject for my master’s

thesis. I want to thank Professor Timo Kärri as well as Miia Pirttilä and Sari

Viskari for patient guidance and excellent advices that made it possible for me to

finish this thesis.

I am also grateful to my family and to my friends for support during my studies

and especially during the thesis project. Special thanks go to my dog that keeps

me going.

Lappeenranta, October 31st, 2012

Anna-Maria Talonpoika

TABLE OF CONTENTS

1 INTRODUCTION ........................................................................................... 1

1.1 Background ............................................................................................... 1

1.2 Research questions .................................................................................... 2

1.3 Research methods ..................................................................................... 3

1.4 Structure .................................................................................................... 4

2 LITERATURE REVIEW ................................................................................ 6

2.1 Working capital ......................................................................................... 6

2.2 Optimal levels of working capital ............................................................. 8

2.3 Working capital management ................................................................... 9

2.4 Working capital management policies .................................................... 13

2.5 Challenges of working capital management ........................................... 14

2.6 Measures of working capital management ............................................. 17

2.7 Working capital management and profitability ...................................... 19

2.8 Advance payments .................................................................................. 21

2.9 Summary of the literature review............................................................ 23

3 ANALYSIS OF THE ADVANCE PAYMENTS ......................................... 25

3.1 Modified Cash Conversion Cycle ........................................................... 25

3.2 Research design and procedure ............................................................... 26

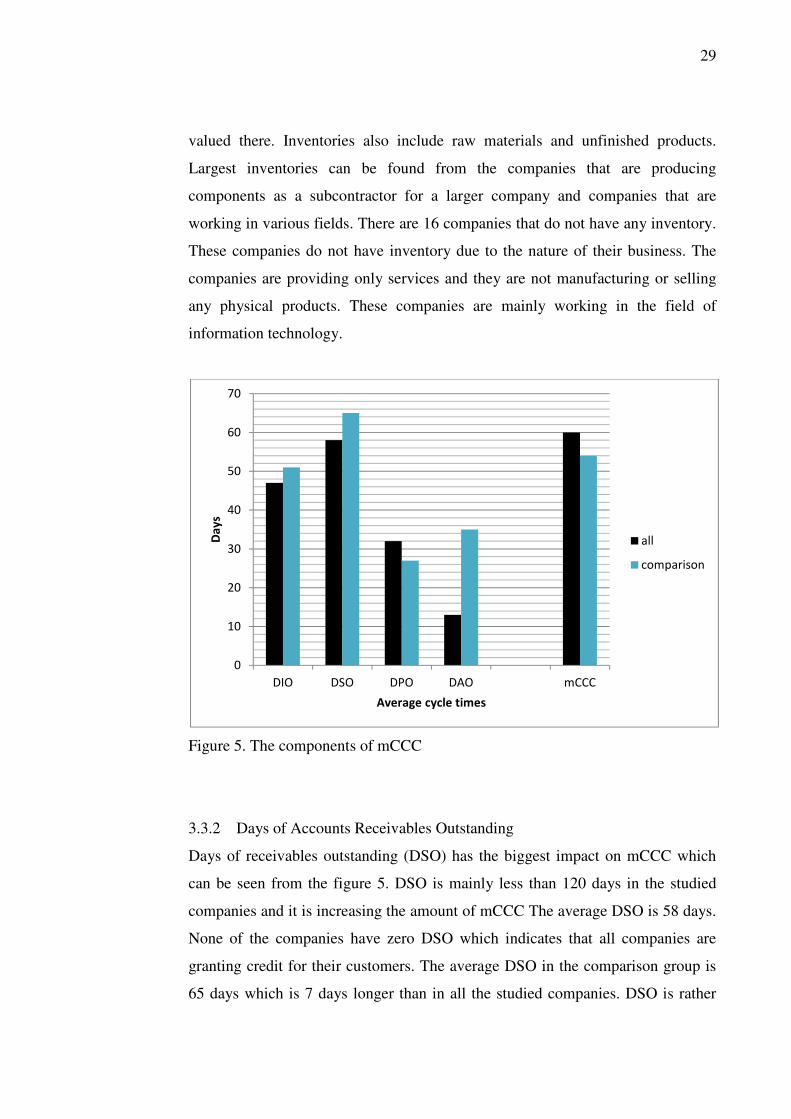

3.3 The components of modified Cash Conversion Cycle ........................... 28

3.3.1 Days of Inventory Outstanding ........................................................ 28

3.3.2 Days of Accounts Receivables Outstanding .................................... 29

3.3.3 Days of Accounts Payables Outstanding ......................................... 31

3.3.4 Days of Advance Payments Outstanding ........................................ 31

3.4 The difference between CCC and mCCC ............................................... 32

3.5 Branches with advance payments ........................................................... 35

3.6 Profitability and advance payments ........................................................ 37

3.7 Future research ........................................................................................ 40

4 CONCLUSIONS ........................................................................................... 42

REFERENCES ...................................................................................................... 44

APPENDIXES

Appendix I / All studied companies

Appendix II / Companies in the comparison group

FIGURES

Figure 1. The working capital cycle ........................................................................ 6

Figure 2. Cycle times of working capital and profitability .................................... 23

Figure 3. Modified Cash Conversion Cycle .......................................................... 26

Figure 4. Distribution of the companies ................................................................ 28

Figure 5. The components of mCCC ..................................................................... 29

Figure 6. The difference between CCC and mCCC .............................................. 33

Figure 7. CCC and mCCC ..................................................................................... 35

Figure 8. The relationship between advance payments and profitability .............. 38

Figure 9. The relationship between advance payments and profitability in the

comparison group .................................................................................................. 39

TABLES

Table 1. Research questions .................................................................................... 3

Table 2. Structure of the thesis ................................................................................ 5

Table 3. Balance sheet ........................................................................................... 22

ABBREVIATIONS

CCC Cash Conversion Cycle

mCCC modified Cash Conversion Cycle

DIO Days of Inventory Outstanding

DSO Days of Receivables Outstanding

DPO Days of Payables Outstanding

DAO Days of Advance Payments Outstanding

ROI Return on Investment

1

1 INTRODUCTION

1.1 Background

Working capital management has been studied all over the world. Most of these

studies are made through a practical setting and not scientific (Tahir & Anuar

2011, 366-371). There are also few scientific researches about working capital

management according to Viskari et al. (2011a, 9). These researches are often

made using listed companies from a selected stock exchange. Most research

projects have connected working capital management to profitability of a

company. This master’s thesis will also connect those two.

There are two commonly used definitions for working capital. Companies often

use the operational view of working capital but the financial view is often

observed in the literature. The financial view considers the working capital to be

the value of current assets less the value of current liabilities. This view can also

be defined as net working capital. The working capital can be calculated in an

operational view which uses three specific components. The components are

inventories, accounts receivables and accounts payable. (Hampton 1983, 220;

Proctor 2006, 62)

Most companies calculate profitability for their investors but not working capital.

Working capital is sometimes calculated for the investors through the financial

view. Cash Conversion Cycle (CCC) is the most used tool for working capital

management research in academic world but there is almost no information about

working capital management procedures in business life. CCC takes into account

only inventories, accounts receivable and accounts payable but not advance

payments which are also sometimes used when working capital is defined, for

example Corporate Analysis Association in Finland includes advance payments

on calculation of CCC. This thesis creates a new key figure for operative working

capital management, modified Cash Conversion Cycle (mCCC), which also takes

advance payments into account. There are no published working capital

2

researches with the connection to advance payments. This thesis will connect

received advance payments to working capital management.

Advance payments can be divided into received advance payments and paid

advance payments. Received advance payments are payments that the company

has received from its customers before the company has delivered the goods. Paid

advance payments are the opposite side. The company pays to its suppliers

beforehand in order to receive the product or service later. This research is

concentrated in received advance payments. Therefore only advance payments are

mentioned and they are referred to as received advance payments.

Working capital management is currently researched in Lappeenranta University

of Technology by the Capital, Capacity and Cost Management (C3M) research

group. The research is made with a broad scale concerning all aspects of working

capital management. Most research subjects are studied through a value chain

perspective. The linkage between working capital management and profitability is

also part of the research project. This master’s thesis is partly connected to the

current research project in Lappeenranta University of Technology.

1.2 Research questions

Advance payments are in the center of this research and they are studied in two

different ways: working capital management and profitability. The profitability is

studied through the working capital management view. There are two main

research questions that are divided into sub questions. The research questions are

presented in table 1.

3

Table 1. Research questions

Research questions The purpose of a research question

What is the role of advance payments in

working capital management?

The main purpose of this thesis is to study

changes in working capital management

caused by advance payments.

How does CCC change when the

advance payments are calculated

into it?

The purpose is to create a new key figure

which includes advance payments.

What is the cycle time for advance

payments?

The purpose is to calculate advance

payments in to the operational working

capital and determine cycle times for

advance payments in different branches.

Have companies with advance

payments centered in some

particular branches?

The purpose is to detect the branches and

discover reasons for the concentration.

Do advance payments affect profitability? The purpose is to find changes in

profitability caused by advance payments.

1.3 Research methods

This thesis has two parts: theoretical and empirical. Theoretical part is executed as

a narrative literature review. Salminen (2011, 7) classifies it a descriptive research

method and it is often used to give theoretical guidelines to a study. General

overview of the previous research is one type of narrative literature review and

that is the type used in this thesis. The empirical part of this thesis contains the

research of advance payments. The research is conducted using statistical methods

as a part of quantitative methods. The statistical methods are used to conduct

financial statement analysis. Creswell (2003, 18-19) describes quantitative

approach in three different ways. Developing knowledge by postpositivist claims,

using surveys and collecting data through predetermined instruments are all

indications of quantitative approach. The statistical data for this research is

collected using predetermined instruments but specific surveys have not been

4

used. Postpositivist claims like hypothesis testing have not been used either but

numerical information measurements have been widely executed in this research.

Data used in the empirical part is collected from financial statements of

companies. This sort of data is called secondary data. Zikmund et al. (2010, 161)

describes the secondary data as data that has been previously collected for some

other purpose. The advantages of this type of data collection are availability and

resources saving. These are also the reasons why secondary data was used in this

study. Secondary data was the only available data for this study and it also enables

the publicity of this thesis. The possible problems of secondary data are outdated

information, variation in definition of terms, variations in units of measurement

and data accuracy. The collected data was from the year 2010 so it is still fairly

new and this sort of study can only be made from historical data. All listed

companies in Finland have to make their financial statements according to IFRS

(International Financial Reporting Standards) standard so the terms and units are

invariable. The data is also accurate and it is verified by auditing.

1.4 Structure

There are four chapters in this thesis. The first chapter will introduce the reader to

the study and give some background information. The second chapter presents the

current state of working capital research by written articles. The third chapter

introduces a new figure that is then used to analyze advance payments. The results

are also explained in this chapter. Recommendations for future research are also

included in this chapter. The fourth chapter will summarize the results of this

thesis.

5

Table 2. Structure of the thesis

Input Chapter Output

The reason for this thesis. 1 Introduction

Background, research

questions, methods and

structure of the study.

Literature about working capital

management chosen by using

guidelines defined in the

chapter 1.

2 Literature review

Short review of previous

literature written about

working capital management

and profitability.

Literature review from the

chapter 2 and collected data. 3 Analysis

Definition and usage of a new

figure. Results and analysis

of the research conducted in

this thesis. Recommendations

for future research.

Literature review from chapter

2 and results from chapter 3. 4 Conclusions

The summary of the research

in this thesis.

6

2 LITERATURE REVIEW

2.1 Working capital

Working capital is needed every day until the on-going project is completed

(Kumar et al. 2002, 100). Richards & Laughlin (1980, 34-35) discovered that

working capital is needed in every step of the process but it changes after certain

steps. The working capital cycle can be seen from the figure 1. The basic activities

for companies are purchasing, production, sales and collection of payments. The

cash is invested to the production cycle when resources are purchased. The tied up

cash is back to use after the company has collected its payments. The cash that is

invested in working capital cannot be invested to some profitable targets.

Figure 1. The working capital cycle (Mott 2008, 232)

7

Mullins (2009, 5) considers that working capital is cash that a company needs to

stay in business. The cash needs to be available in short terms so the company can

pay to its employees and suppliers. The company will go out of business very fast

if it cannot keep up the constant cash flow. Profitability is held very important but

it does not help the company if it does not have any cash to pay its suppliers.

Companies should therefore consider a suitable working capital policy that can be

implemented to the company.

The study of Filbeck & Krueger (2005, 17-18) indicates that working capital

measures are not stable and they can change dramatically. The changes can be

explained by macroeconomics. The most important macroeconomic factors for

working capital are interest rate, rate of innovation and competition. The company

also has to ensure excess liquidity to balance unexpected changes in amount of

working capital (Richards & Laughlin 1980, 35). Kumar et al. (2002, 103) have

introduced a fuzzy set theory which can be helpful for companies in order to

improve cost allocation and financial planning. The theory can help managers

understand the effects of qualitative factors in the assessment of the required

amount of working capital.

The research of Padachi et al. (2008, 58) indicates that working capital is financed

mainly with short-term assets like trade credit and other payables. Short-term

bank credits are the most used external source of financing working capital. Small

companies are trying to avoid external financing as long as they can so they would

not get any financial troubles paying back the credits. García-Teruel & Martínez-

Solano (2007, 175) discovered in their research that working capital is also

especially important in small and medium- sized companies because most of their

assets are in the form of current assets. Current liabilities are also the main source

of external finance. Steyn et al. (2002, 47) considers that there are risks for

companies that have large amounts of non-cash working capital and that are

growing at a high rate. The companies that are growing too fast will not have the

sufficient amount of cash needed for working capital. These companies will

probably be liquidated or be combined with some larger companies.

8

Mullins (2009, 5) has found that a company should always aim to negative

working capital which means that the company receives cash from the product

before they have to pay from it. Retail and manufacturing companies can both get

into this ideal situation. One of the key elements on negative working capital is

advance payments. Company can receive cash from the customer before the

product is delivered.

2.2 Optimal levels of working capital

The research of Hill et al. (2010, 27) indicates that optimal levels of working

capital depend on the industry. There are several internal and external factors that

are affecting the optimal level of working capital and every company should

recognize them. Companies in concentrated industries do not need working

capital as much than companies in competitive industries. Companies should also

check the internal factors not only industry benchmarking when considering the

optimal levels of working capital. Chiou et al. (2006, 155) have discovered that

the factors affecting the optimal level are not only internal but also external. The

most important internal factors are operating cash flow, growth rate, company

performance and the size of the company. Industry is the most meaningful

external factor.

Chiou et al. (2006, 155) considers that the optimal level of working capital is

somewhere between meeting unexpected capital requirements and avoiding

inefficient working capital management. Working capital levels might be too low

and as a result of that company may miss profitable investment opportunities and

suffer liquidity crises. The research of Appuhami (2008, 22) indicates that most

important factors are capital, operating and finance expenditures as well as

leverage, performance and operating cash flow. Capital expenditure and operating

cash flow have the largest effect in working capital management. The research

indicates that companies are changing their working capital management policies

according to these factors.

9

Optimal levels for all parts of working capital and profitability can be calculated

by the optimal cash conversion cycle introduced by Nobanee & AlHajjar (2010a,

6-11). This function is similar to cash conversion cycle except it will be calculated

with optimal levels of inventory conversion, receivable collection and payable

deferral period. The optimal inventory level can be calculated with Economic

Order Quantity model (EOQ) where total costs are combined costs of carrying and

shortage costs. This is not the only possible model to calculate optimal inventory

levels and there are several models presented in the literature. Optimal amount of

granted credit can be calculated with the same method as inventory levels. The

optimal amount is the sum of carrying and opportunity costs. The optimal amount

of accounts payables is the sum of carrying costs and opportunity costs of short-

term borrowings.

2.3 Working capital management

Working capital management is a vital part of every company. Noreen et al.

(2009, 169) discovered it is conducted at the corporate level as opposed to local

and regional levels. This indicates that working capital management is considered

important. Sharma & Kumar (2011, 171) as well as Chiou et al. (2006, 155)

consider working capital management to be very important part of financial

management and therefore it should be the backbone for financial decisions of a

company; unfortunately that is not the case in real life. Working capital

management is basically balancing between liquidity and profitability as well as

between financial and managerial decisions. Dramatic changes into one way or

another will cause the finance of the company to go in wrong tracks.

Michalski (2008, 132-133) considers that the goal of working capital management

is to create value for the company. The value creation is considered successful if

the cost of tied up working capital is less than the cost of a debt. Working capital

ties up cash that cannot be used for profitable investments. Increase in the amount

of working capital ties up more cash and therefore reduces the free cash flow to

the company. According to Chiou et al. (2006, 155) working capital management

is basically finding short-term capital and implementing it properly. Working

10

capital management will be ineffective if too much cash is tied up in the working

capital. This will reduce the benefits of short-term investments. The research of

Hutchison et al. (2007, 43-44) as well as Strischek (2001, 34-40) indicate that

effective management of a company needs both profit and cash management.

Efficient working capital management also implicates larger cash flow which ends

up increasing shareholder value. The company will have numerous benefits if it

will have more cash available. Short cash conversion cycle also generates a better

net present value and therefore higher value for the business.

Appuhami (2008, 22) discovered that working capital management is especially

efficient when the company has growth opportunities and they can ensure the

required capital expenditure to expand their business. Strischek (2001, 38-40)

claims that working capital management is one of the things that banks check

when they are allowing credit to their customers. Companies that have efficient

working capital management will easily get external financing with low interest

rate. The cost of capital is therefore lower for these companies and they are

assumed to be more profitable.

The research of Howorth & Westhead (2003, 106-109) indicates that companies

which do not manage their working capital as much as most of the companies will

get a higher profitability. The companies with less working capital management

will also have less interest in growth as well as less external finance. They do not

usually buy in credit and they have short production cycles. The companies also

have several on-time paying customers and they do not normally have cash flow

problems. These companies are not smaller or younger than the average

companies. Companies focus their working capital management only in one area

because they have limited resources for working capital management. Companies

with limited resources are not the smallest ones but these companies do not

usually have advanced financial skills. These companies also need to be

convinced that proper working capital management will improve their

performance.

11

Hutchison et al. (2007, 42-43) have found that a cash conversion cycle can be

positive or negative. A positive cycle means that the company has to tie up

working capital before it gets payment from the customer. Negative cycle means

that the company gets cash from the customer before it has to pay its suppliers.

Essentially every company should have as short cash conversion cycle as possible.

Shorter CCC indicates that the company manages its cash flows efficiently.

Therefore it will have more cash cycles during a year and an invested dollar will

generate more sales. Managers have in recent years noticed the importance of

working capital management. The reduction in CCC will almost automatically

lead to improvements in operational and financial management.

According to Strischek (2001, 38-40) the company can have numerous positive

effects by improving its working capital management practices. Hutchison et al.

(2007, 43-44) found that the improvements depend on which variable will be

improved. Ongoing expenses and inventory carrying costs are examples of these.

Payne (2002, 41-42) considers that the improvements usually start at the financial

department but they will affect the whole company. Changes in financial

operations do not usually remove the problem. The problems are hidden in the

processes. The ordering system might be ineffective or the sales personnel might

be offering too long payment times. The improvements will be effective after the

root of the problems is found. All the companies should consider the optimization

of working capital management even though the company would not be in crisis.

The changes in working capital management will end up showing as larger

revenue for the company. The research of Richards & Laughlin (1980, 35)

indicates that a company can shorten the cash conversion cycle with a few

implementations. Payables will decrease the length of cycle time for working

capital. The company should therefore use the offered credit. The different

inventory managing techniques will also decrease the cycle time by ensuring the

appropriate inventory levels. The company should also decide the right credit

times for its customers.

12

Hill et al. (2010, 27) discovered that working capital (CCC) has a positive

relationship with operating cash flow and company size. There is also a negative

relationship between working capital and financial distress as well as between

working capital and market share. Essentially companies with weak internal

financing abilities, limited access to capital markets and greater costs of external

financing will more likely use payables than receivables or inventory in order to

adjust the working capital.

Howorth & Westhead (2003, 106-107) discovered in their research that

companies that have focused on cash management are usually larger and younger

than average companies. They do not have that much cash sales and they work in

seasons. These companies have more cash flow problems and they have more

external financing. Companies that have focused on stock management are

smaller and younger. They do not usually have that much external finance and

they also have long production cycles. Companies with focus on credit

management are not that profitable but they have an interest to grow. They usually

do purchases on credit and their customers do not pay on time.

The research of Uyar (2009, 192) was conducted by analyzing companies listed in

the Istanbul Stock Exchange. The research indicates that smaller firms have

longer cash conversion cycles. The research also indicates that retail industry has

a shorter cash conversion cycle than manufacturing industry. Textile industry has

the longest cash conversion cycle in the manufacturing industry. The reason for

shorter CCC is the fact that retail industry does not manufacture goods so

therefore it does not need that much inventory. The retail industry also pays bills

slowly and accepts only cash payments so it has optimized the cash conversion

cycle.

The research of Filbeck & Krueger (2005, 13-14) was conducted by analyzing

1 000 U.S. companies during a five year period from 1996 to 2000. The results

show that the average CCE was nine percent and it fluctuated between six and ten

percent. The average CCC was 51.8 days and it fluctuated between 46 and 59

13

days. The average rates for components of CCC were 50.6 days for DSO, 32 days

for DIO and 32.4 days for DPO. Wang (2002, 168) has found evidence that

Japanese companies have shorter cash conversion cycles than companies in

Taiwan. The average cash conversion cycle length on Japanese companies is 87

days and 219 days in Taiwanese companies. The shortest cash conversion cycles

are found (calculated from mean values) from food industry in Japan and

transportation industry in Taiwan.

2.4 Working capital management policies

Meszek & Polewski (2006, 226) discovered that working capital management of a

company depends on the management policy or the lack of it. Different

companies have variable approaches to working capital management. There are

companies that do not control all components of working capital and therefore

they do not have a holistic view over it but there are three policies that are widely

used: aggressive, moderate and conservative. According to Kaur (2010, 13-14)

companies should choose a policy that fits into their needs and financing

capabilities. Yadav et al. (2009, 34) have found that working capital management

policies of the companies are not static. They change over time. The changes in

economy have the biggest effect on working capital management policy.

Aggressive policy is according to Michalski (2009, 132-133) financing the

changes in working capital with short-term assets and conservative policy with

long-term assets. Aggressive policy has been proved efficient when working

capital management needs to be refined and it will bring most value for the

company but it has also most risks. Hill et al. (2010, 27) claim that companies are

using an aggressive policy if their sales are volatile and the company is growing.

Yadav et al. (2009, 34) on the other hand considers that companies use the

conservative approach when the volatility of the business is high and aggressive

approach when the volatility is low.

There are few things that need to be considered when planning working capital

management policy for a company referred to Kaiser & Young (2009, 67).

14

Companies should not use income statements as the primary source of financial

information. Inventories and accounts receivables are tying up cash even though it

cannot be seen on the income statement. The rewarding systems of the companies

can also be the reason for problems in working capital management. Sales persons

should not be rewarded only for completed sales because they will concentrate

only to selling and not keeping up accounts receivables. Production quality is a

good thing but if quality is emphasized it will lead to a slow-down of the

production. Keeping the production in satisfying level and keeping up the speed

will free some cash from the working capital. Companies sometimes connect

accounts receivables and accounts payable. They are not related to each other so

they should be handled separately. Current and quick ratios are measurements to

calculate liquidity of the company. They do not give any information about

working capital. Working capital management is balancing between liquidity and

profitability. If they are not in balance the company will suffer. Benchmarking is a

good way to recover information about the practices inside the industry.

Benchmarking does not tell the right levels of working capital and it should not be

used that way.

2.5 Challenges of working capital management

The problem of working capital management according to Richards & Laughlin

(1980, 35) is to find the ideal level of working capital so the company can have

enough cash as well as money to invest. The key issue is to find a balance

between resources tied up in working capital and in capital investments.

Appuhami (2008, 22) has discovered that working capital management needs to

be done efficiently or the company will invest too much money on working

capital and profitability of the company will be reduced. Inefficient working

capital management might also lead to situation where the company does not have

enough working capital and it will cause the company some financial difficulties.

The risk of the company develops between these two situations. According to

Hutchison et al. (2007, 43) the problem to find the balance can be divided into

operational and financial decisions. The operational management wants to

15

lengthen the CCC to increase liquidity and financial management wants to shorten

the CCC to release cash for capital investments.

The research of Nobanee & AlHajjar (2010b, 15-19) indicates that working

capital has a significantly negative relationship on performance of the company.

There are several factors in this relationship that affect the impact. The indication

is that reduction of working capital does not increase profitability in every

situation. Shortening of CCC may lead into trouble because the shortage costs will

increase if the inventory is kept on a too low level. The reduction of receivable

collection periods will louse the company some credit customers and lengthening

of payable period will cause the company a bad reputation in the eyes of other

companies. The most important piece of working capital management is therefore

to find an optimal level of working capital which maximizes the profitability.

Payne (2002, 40) believes that working capital management can be a key to a

better functioning company. The shortening of cash conversion cycle can free

large amounts of cash for the company. Hard times in the economy can increase

the need of cash in a company. Several companies issue short or long-term debts

to cover the cash demand. The cost of debts is increasing rapidly and therefore it

is not very wise to use a debt to pay another one. Companies should improve their

working capital practices so they could get the needed amount of cash from inside

the company. The improvement takes more time than negotiations at the bank but

they are free of charge. Reilly & Reilly (2002, 15-18) introduces accounts

receivable as one of the elements companies could improve most. Companies

should do more effective evaluation of companies they are granting credit. Bad

debts are costing the company a lot. Companies should also set policies for

granting credit. Every salesperson should know the principles for granting credit.

Flexibility of payment methods is also one way of improving the accounts

receivable. Company could offer several different ways to pay the bill and this

way make sure the bill gets paid.

16

Reilly & Reilly (2002, 13-14) consider that working capital management is these

days financially oriented and it is conducted by financial managers. The

measurements for working capital are traditionally financial ratios. These ratios

do not tell where the origin of the problem is. The problems should be detected

before they end up in financial statements. These situations require the company

to focus its actions into reducing the inventory levels and accounts receivable as

well as prolonging the accounts payable.

Molina & Preve (2009, 684) discovered that companies that have problems with

profitability are more likely to increase the level of accounts receivables. This

procedure is done in order to gain more market share. Companies that are in

financial distress are doing the other way around and they reduce the level of

accounts receivables. This way more working capital is released for other use.

Companies in competitive industries face difficulties when they reduce the

accounts receivables because customers can easily choose another supplier.

Companies in concentrated industries do not face same sort of problem.

According to Bougheas et al. (2009, 306) companies can use accounts payables to

finance the changes in inventories. The companies also have to find a balance

between accounts payables and accounts receivables in order to run the business

effectively.

The research of Long et al. (1993, 126-127) presents that small companies with

unique products usually grant longer credit periods so the customers can verify the

product quality before payment. Large companies with less unique products and

high turnover do not need to grant trade credit. The companies that are granting

trade credit do not usually buy on credit. Large and creditworthy companies are

most likely to extend their trade credits. Extension of trade credit is also used by

companies that have variable demand. Small companies with long production

times are very likely to extend their trade credits in order to finance their

receivables.

17

Late payments are a common problem among small companies in UK according

to Peel et al. (2000, 33). The companies have recognized the problem and are

supporting the legislation for late payments. The companies also consider that the

most helpful way to reduce late payments is interest. Almost all small companies

have at least once paid late to their suppliers and about 15 percent do it regularly.

Small companies still are not the worst type of companies to pay late. Large

companies pay late almost every time then the small companies and the medium

sized companies pay on time.

2.6 Measures of working capital management

Working capital management efficiency can be measured with several different

ways. The calculation methods can be divided into financial and operational

methods. Financial methods include for example Quick Ratio and Current Ratio.

Operational methods are for example Cash-to-Cash method and Cash Conversion

Cycle (CCC). CCC is the most used measurement and there are few variations of

it. Most commonly known versions are Cash Conversion Efficiency (CCE), Net

Trade Cycle (NTC) and Weighted Cash Conversion Cycle (WCCC). All of these

measurements are used in the business life and they might be used together

because they measure working capital management in a different perspective.

(Farris & Hutchison 2003, 83; Filbeck & Krueger 2005, 12; Shin & Soenen 1998,

38)

Cash conversion cycle developed by Richards & Laughlin (1980, 34) is an

important measurement in financial management. It measures liquidity of the

company. The cash conversion cycle reflects the time between the moments when

resources are purchased and the cash is recovered from sales. Basically it

establishes the period of time needed to convert cash disbursements back to cash

inflow. Cycle times for inventory and receivables are calculated to find out the

liquidity of the company. Cash conversion cycle also adds cycle times for

payables into this calculation. This calculation shows that when inventories and

receivables increase the amount of working capital increases and it has to be

therefore financed. The increase in payables in the other hand indicates that

18

spontaneous working capital will accumulate during a longer period of time.

According to Farris & Hutchison (2003, 90) the management needs to understand

the calculation of CCC in order to use it as a tool. Effective use of CCC requires

information about the working capital from a longer period of time.

Shin & Soenen (1998, 38, 43) have developed net trade cycle (NTC) that can be

easily used to check the efficiency of working capital management. NTC is a

more simplified version of cash conversion cycle where the three components of

cash conversion cycle are expressed as percentage of sales. The main goal of the

NTC is to show the number of day’s sales the company needs to finance the

needed working capital. NTC can be easily used when evaluating the required

amount of working capital. A short NTC implicates that the company is managing

its working capital efficiently and therefore the company does not need external

financing for working capital. Reductions in the NTC are one option to create

shareholder value and therefore working capital management should be done

efficiently.

Gentry et al. (1990, 98-99) have developed a weighted cash conversion cycle that

provides more accurate information than the traditional cash conversion cycle.

WCCC is a good measurement for short-term financial management. It focuses

the management to the real engagement of resources in the working capital

process. The WCCC describes of the amount and speed the working capital is

changing in the company. Accounts payable is the factor that is causing the gap

between CCC and WCCC.

CCC is calculated in this thesis using the equation 1 which is based on the

calculation method of Shin & Soenen (1998, 38).

��� = ��� + ��� − �� (1)

19

Where,

CCC = Cash Conversion Cycle

DIO = Days of Inventory Outstanding

DSO = Days of Accounts Receivables Outstanding

DPO = Days of Accounts Payables Outstanding

��� =��� ����� × 365

� ���� � (2)

��� =��������� � ����� × 365

� ���� � (3)

�� =������������� × 365

� ���� � (4)

2.7 Working capital management and profitability

According to Raheman & Nasr (2007, 294) companies have invested large

amounts of money into working capital. Working capital management has

therefore a substantial effect on profitability of the companies. Several studies (for

example Mojtahedzadeh (2011, 165), Lazaridis & Tryfonidis (2006, 34-35),

Dong & Su (2010, 66), Eljelly (2004, 59)) indicate a significant negative

relationship between the cash conversion cycle and profitability of the company.

A long cash conversion cycle is reducing the profitability and vice versa. Deloof

(2003, 585) has found a relationship between profitability and all three aspects of

cash conversion cycle. So there is a relationship between accounts payable and

profitability as well as between account receivable and profitability. The research

of Raheman & Nasr (2007, 294) indicates that the reduction of length of cash

conversion cycle should be done reducing accounts receivables and inventories.

Basically the company will have a better profitability if it pays its bills more

slowly. The payables deferral period has to be appropriate or otherwise the

company will harm its own credit reputation.

Working capital management procedures in a company are affected by the

operational profitability according to Lazaridis & Tryfonidis (2006, 34-35). Talha

et al. (2010, 226) discovered that maintaining the acquired level of profitability

20

requires companies to have the optimum amount of current assets needed in daily

use. The companies also have to take care of their short-term maturities in order to

survive. The basic rule is to have low liquidity and high profitability. Companies

should efficiently use the working capital resources in order to increase

profitability and the values of the company. Mathuva (2010, 10) considers that a

company can increase profitability by decreasing the cash conversion cycle. The

decrease needs efficient use of working capital management resources.

Lazaridis & Tryfonidis (2006, 35) found a significant relationship between gross

operating profit and DPO in their research. DPO will increase when the gross

operating profit is decreasing. This means that less profitable companies are

paying their bills slower to take advantage of the credit period granted to them.

DSO and gross operating profit also has a negative relationship. The companies

that are not so profitable are trying to decrease the accounts receivable in order to

gain more cash. There is a negative relationship between DIO and gross operating

profit. The relationship indicates that if sales are decreasing and the inventories

are not managed properly the company will have lots of capital tied up in

inventories and not available for investments.

There is a negative relationship between the measures of profitability and

aggressiveness of working capital management according to Nazir & Afta (2009,

27-28). The companies will most likely have negative return if they have very

aggressive working capital management policy. On the other hand companies that

have aggressive management policy will get more investors because the

aggressiveness is highly valued by them. Most investors believe that companies

that have less equity and less long-term loans will perform better than other

companies. Filbeck et al. (2007, 20) discovered that also companies that are

ranked high in the CFO Magazine’s working capital survey are doing more return.

This indicates that there is a positive relationship between efficient working

capital management and profitability. Investors also find companies with efficient

working capital management policies interesting.

21

Kieschnick et al. (2011, 12) finds working capital management to be important for

the value of the company. The shareholder value can simply be increased by

optimizing the cash conversion cycle and especially all its parts according to

Deloof (2003, 585). The importance is understandable because significant amount

of company assets are tied up in working capital in most companies. On the other

hand outside investments to working capital are reducing the value of the

company. The invested value is decreasing at the same pace than the invested

amount is increasing. The reductions are not so dramatic if the company has an

easy access to public capital markets. The research of Kieschnick et al. (2011, 19)

indicates that the outside investments into the working capital of a company are

not profitable. The value of the investment will be negative. Basically the investor

will save his money by keeping it on cash than investing it to the working capital.

The research indicates that the pattern is similar in all industries.

Raheman et al. (2010, 426-427) have been analyzing 204 companies listed in

Karachi Stock Exchange in the period 1998-2007. The results indicate that there is

sectoral deviance between the different measures of working capital management.

The results vary significantly between the sectors. The measures may predict the

profitability in some sectors but in others it has no role. Several researches on the

other hand have indicated that there is a negative relationship between liquidity

and profitability. This particular study shows that there might be a positive

relationship as well as negative. There is also evidence that CCC and NTC

measures liquidity differently than Current Ratio.

2.8 Advance payments

Advance payments are one part of current liabilities. Their position in the balance

sheet can be seen from the table 3. Leppiniemi (2002) considers that advance

payments are liabilities from the moment they are received until the finished

goods are delivered. Yritystutkimus (2011, 48) on the other hand does not see

advance payments as liabilities when the goods are still work-in-progress.

Advance payments can also be part of long-term liabilities but the ones in current

liabilities are studied in this thesis.

22

Table 3. Balance sheet (modified from Yritystutkimus 2011, 28-29)

ASSETS LIABILITIES

Fixed assets Shareholder’s equity

Intangible assets Share capital

Tangible assets Retained earnings

Investments Profit for the period

Funds

Current assets Minority interest

Inventories Capital loans

Receivables

Current financial assets Liabilities

Cash and cash equivalents Long-term liabilities

Current liabilities

Advance payments

Advance payments are considered as a part of working capital according to

Yritystutkimus (2011, 68-69). Advance payments are reducing the amount of

working capital needed. Advance payments are therefore one form of financing to

the companies. Companies do not necessarily need to take any other liabilities to

finance their working capital. Advance payments are also affecting profitability

not only working capital. Advance payments can be considered as a one

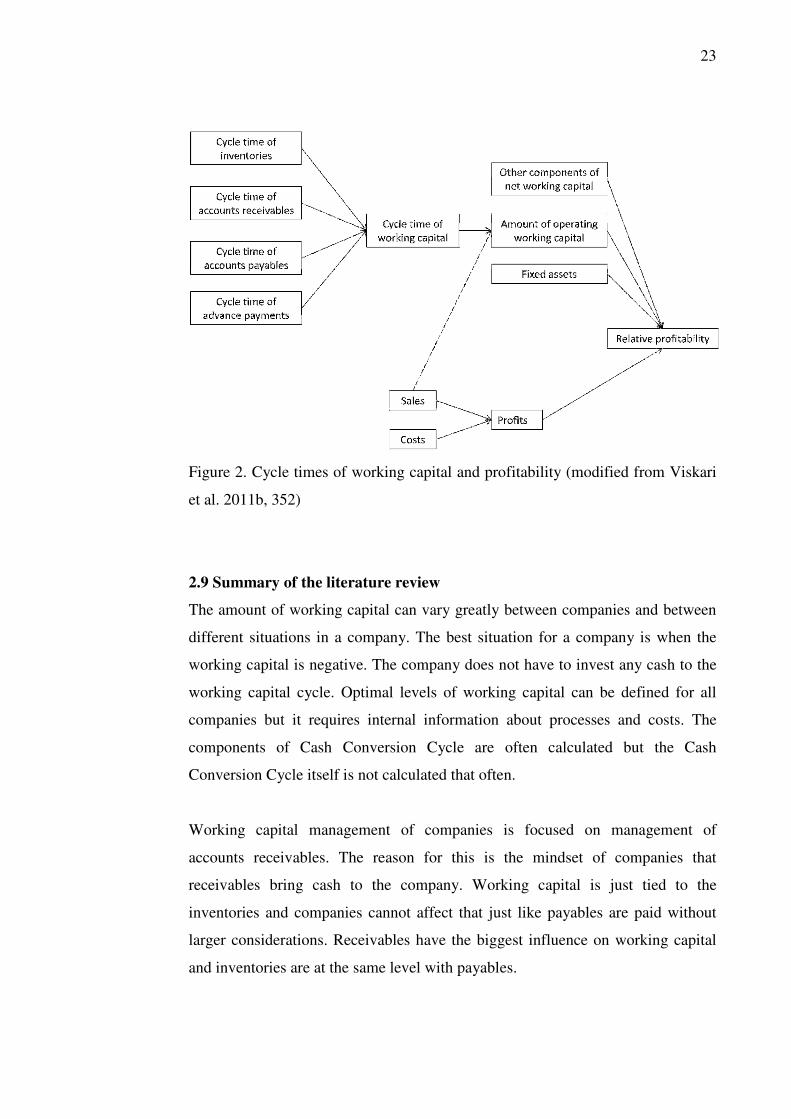

component of working capital and thus figure 2 can be drawn.

23

Figure 2. Cycle times of working capital and profitability (modified from Viskari

et al. 2011b, 352)

2.9 Summary of the literature review

The amount of working capital can vary greatly between companies and between

different situations in a company. The best situation for a company is when the

working capital is negative. The company does not have to invest any cash to the

working capital cycle. Optimal levels of working capital can be defined for all

companies but it requires internal information about processes and costs. The

components of Cash Conversion Cycle are often calculated but the Cash

Conversion Cycle itself is not calculated that often.

Working capital management of companies is focused on management of

accounts receivables. The reason for this is the mindset of companies that

receivables bring cash to the company. Working capital is just tied to the

inventories and companies cannot affect that just like payables are paid without

larger considerations. Receivables have the biggest influence on working capital

and inventories are at the same level with payables.

24

Reductions of working capital can increase profitability of a company. There are

results from several researches that working capital and profitability are linked

together. The results indicate that efficient working capital management can

increase profitability and add a larger cash flow to the company. Companies have

to ensure the liquidity and not only profitability by reasonable working capital

management in order to keep the company running. The company may fall in to

problems if they do not have enough cash and they have poor profitability.

25

3 ANALYSIS OF THE ADVANCE PAYMENTS

3.1 Modified Cash Conversion Cycle

Modified Cash Conversion Cycle (mCCC) is an advanced version from the Cash

Conversion Cycle. mCCC takes into consideration also the received advance

payments which are normally left out from the calculation of working capital. The

reason why they are not used is the fact that they were not included in the first

research conducted by Richards and Laughlin. The CCC was originally used in

scientific research to calculate long stock exchange lists during a longer time

period. These days CCC is widely used in business life to evaluate the levels of

working capital. Therefore companies should calculate DAO and mCCC instead

of CCC because many companies have significant amounts of advance payments.

Advance payments, one part of the short time assets, can shorten the cycle time

many days because the company will receive cash earlier than in the usual cycle.

The needed amount of working capital will be then reduced and it might

sometimes even turn negative. The mCCC will therefore give a more accurate

view of the working capital for the companies. mCCC can be seen from the figure

3.

mCCC is calculated through the same pattern than CCC. First all the components

of mCCC are calculated. The components DIO, DSO and DPO are calculated

similarly than in CCC. Days of Advance Payments Outstanding (DAO) is the only

new component. DAO is calculated by dividing the amount of advance payments

in a year with the same year’s turnover. The plain number is then multiplied with

365 days. DAO is then reduced from the CCC. The equation is presented below.

��� = ��� + ��� − �� − ��� (5)

��� = �!���� �� ��� × 365

� ���� � (6)

26

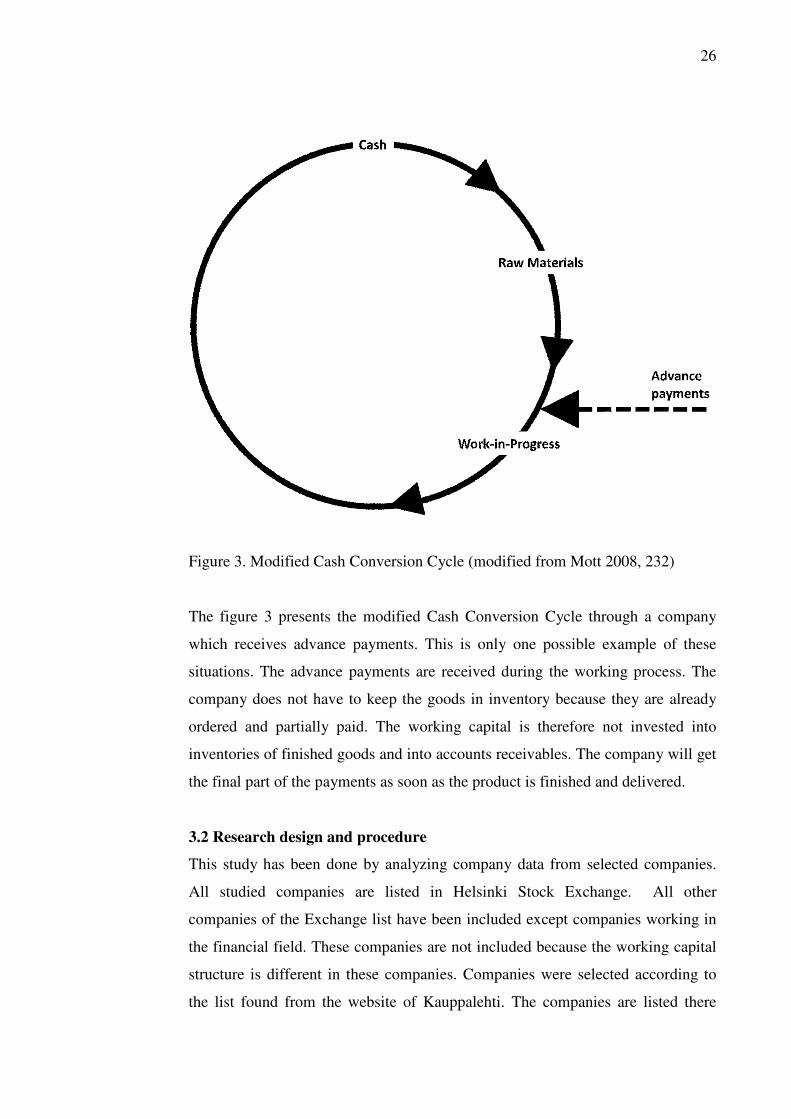

Figure 3. Modified Cash Conversion Cycle (modified from Mott 2008, 232)

The figure 3 presents the modified Cash Conversion Cycle through a company

which receives advance payments. This is only one possible example of these

situations. The advance payments are received during the working process. The

company does not have to keep the goods in inventory because they are already

ordered and partially paid. The working capital is therefore not invested into

inventories of finished goods and into accounts receivables. The company will get

the final part of the payments as soon as the product is finished and delivered.

3.2 Research design and procedure

This study has been done by analyzing company data from selected companies.

All studied companies are listed in Helsinki Stock Exchange. All other

companies of the Exchange list have been included except companies working in

the financial field. These companies are not included because the working capital

structure is different in these companies. Companies were selected according to

the list found from the website of Kauppalehti. The companies are listed there

27

according to the branches. There are two companies that were left out because of

various reasons. TeliaSonera was left out because it does not produce its financial

statements in Euros and SieviCapital is also left out because it was in 2010 still

called Scanfil. Scanfil is among the studied companies.

The data required for the study was collected from two different sources.

Information about ROI and sales were collected from the website of Kauppalehti.

Kauppalehti calculates ROI for every company the same way unlike companies

which can calculate ROI differently. This way it was ensured that the data was

comparable. All other data was recovered from the annual reports of the

companies. The reports were found in their websites. The data was collected

during January 2012. The website of Kauppalehti was at that point free of

registration and fees. The used data is from the year 2010 because the annual

reports of 2011 were not published at that point. Information used for this thesis is

public and everyone can use it. All of the studied companies have made their

financial statements according to the IFRS standard. Companies may assess their

belongings differently but the basic principles are always the same. Therefore all

collected data is equal.

The research was executed in two stages. The first stage was data collection and

calculation. Data was collected from previously presented sources. Calculation

was conducted after the data was collected. Calculation changed the raw data into

figures. The second stage is analyzing. The results of calculation were analyzed.

The findings were described and they were compared to the previous researches

presented in the beginning of this thesis.

The companies in this research were divided into two groups. The allocation was

made by checking the amount of received advance payments. Histogram in the

figure 4, which has been drawn from the data, shows that about 65 percent of the

companies have DAO less than five days. The limit was then put into the five

days. A closer look was taken to a comparison group which consists of companies

that have their DAO more than five days. It can be said that these companies have

28

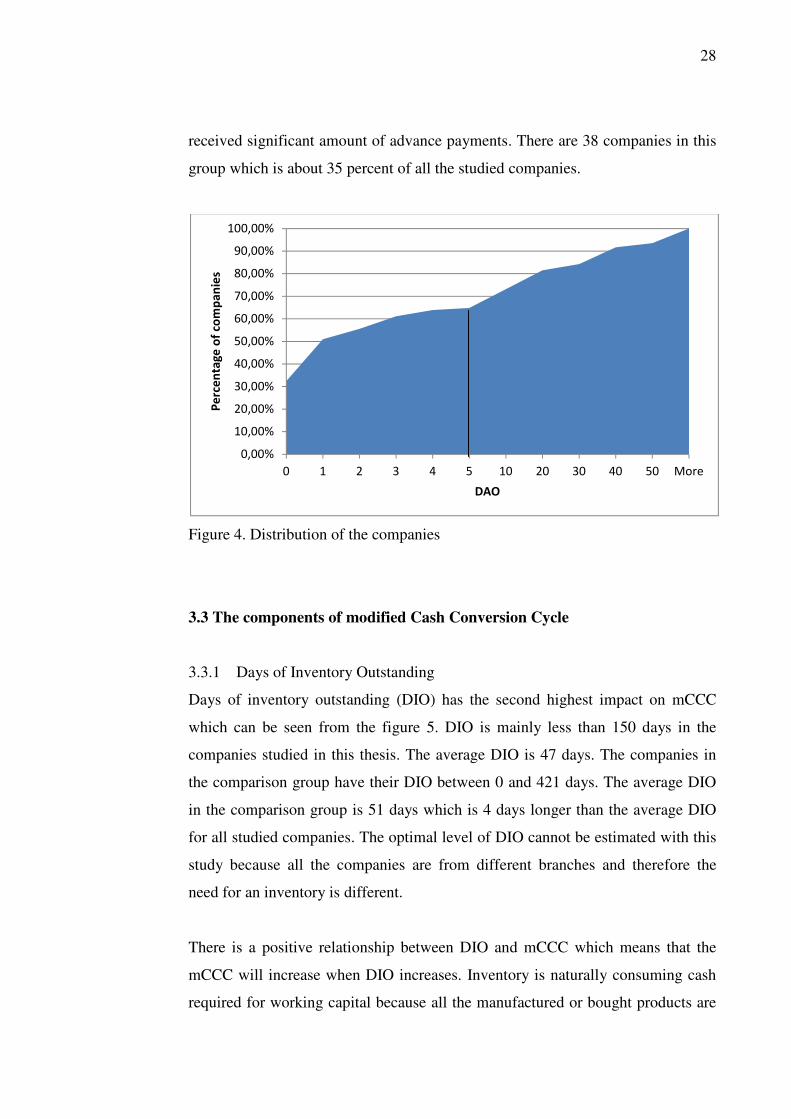

received significant amount of advance payments. There are 38 companies in this

group which is about 35 percent of all the studied companies.

Figure 4. Distribution of the companies

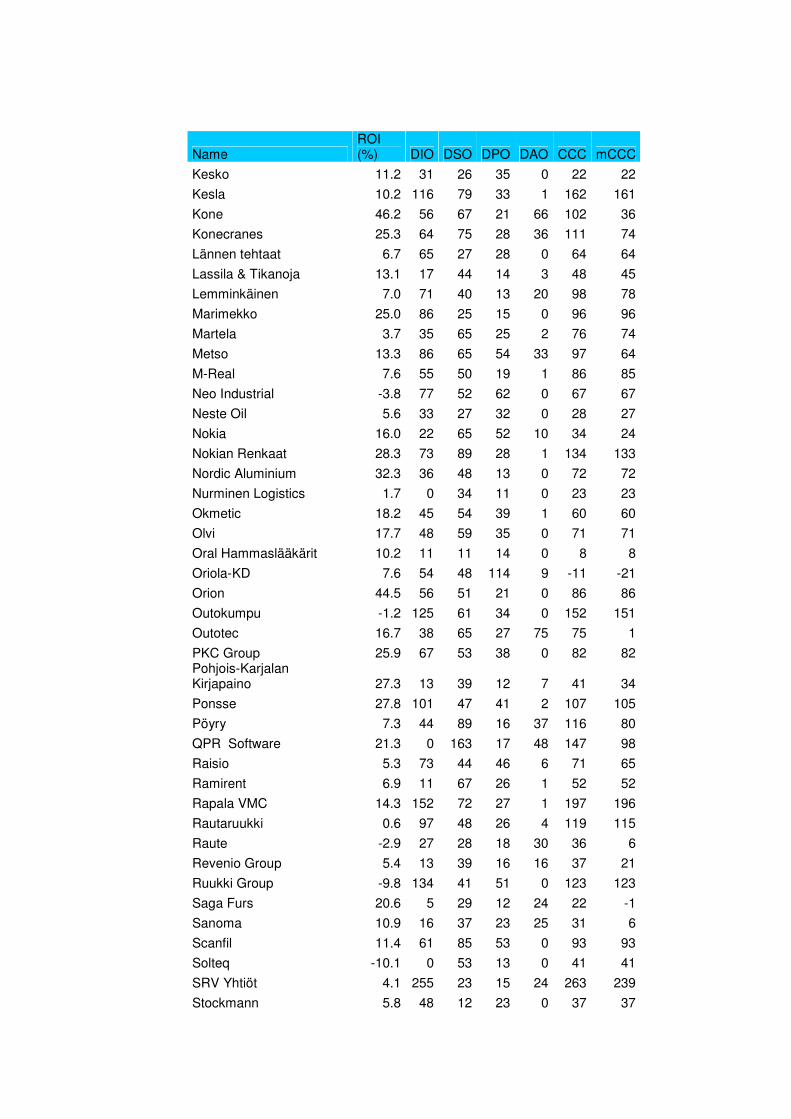

3.3 The components of modified Cash Conversion Cycle

3.3.1 Days of Inventory Outstanding

Days of inventory outstanding (DIO) has the second highest impact on mCCC

which can be seen from the figure 5. DIO is mainly less than 150 days in the

companies studied in this thesis. The average DIO is 47 days. The companies in

the comparison group have their DIO between 0 and 421 days. The average DIO

in the comparison group is 51 days which is 4 days longer than the average DIO

for all studied companies. The optimal level of DIO cannot be estimated with this

study because all the companies are from different branches and therefore the

need for an inventory is different.

There is a positive relationship between DIO and mCCC which means that the

mCCC will increase when DIO increases. Inventory is naturally consuming cash

required for working capital because all the manufactured or bought products are

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%

80,00%

90,00%

100,00%

0 1 2 3 4 5 10 20 30 40 50 More

Pe

rce

nta

ge

of

com

pa

nie

s

DAO

29

valued there. Inventories also include raw materials and unfinished products.

Largest inventories can be found from the companies that are producing

components as a subcontractor for a larger company and companies that are

working in various fields. There are 16 companies that do not have any inventory.

These companies do not have inventory due to the nature of their business. The

companies are providing only services and they are not manufacturing or selling

any physical products. These companies are mainly working in the field of

information technology.

Figure 5. The components of mCCC

3.3.2 Days of Accounts Receivables Outstanding

Days of receivables outstanding (DSO) has the biggest impact on mCCC which

can be seen from the figure 5. DSO is mainly less than 120 days in the studied

companies and it is increasing the amount of mCCC The average DSO is 58 days.

None of the companies have zero DSO which indicates that all companies are

granting credit for their customers. The average DSO in the comparison group is

65 days which is 7 days longer than in all the studied companies. DSO is rather

0

10

20

30

40

50

60

70

DIO DSO DPO DAO mCCC

Da

ys

Average cycle times

all

comparison

30

long because the average credit time in Finland varies between 7 and 28 days. The

shortest receivables collection times can be found from companies that are

working close to consumers and longest receivable collection times can be found

from companies that are doing business in the information technology sector.

The long DSO indicates that companies have difficulties to collect their

receivables in time. Some of the long credit times can be explained with foreign

sales. There are several countries where companies are used to get longer credit

times and therefore they are not paying their bills on time. Companies may also

grant longer credit times for these companies. One of the reasons for receivable

collecting times is the current economic situation. There are companies that do not

have any cash to pay the products or services they are bought. They will not get

any credit from financial institutions so their only change is to use credit granted

by their suppliers. This way they will ensure their working capital levels. The

companies might also have difficulties to collect cash payments and therefore they

will end up having receivables. Companies used to grant cash discounts to their

buyers if they pay their purchase immediately or within the next seven days. It

used be very profitable for the buyer the use this discount but these days only few

companies can take advantage of the discounts. This is an effect caused by the

financial crisis.

Previous researches indicate that companies concentrate on managing receivables

even they would not otherwise manage working capital at all. Receivables bring

cash to the companies and the concentration can be therefore easily explained.

This study shows that receivables are the most significant factor in working

capital. The company has to manage them properly in order to minimize the

working capital. Holistic view over working capital is still the best approach to

working capital management because all components of working capital needs to

be considered.

31

3.3.3 Days of Accounts Payables Outstanding

Days of payables outstanding (DPO) has the third highest impact on mCCC

among all companies and the fourth highest impact on comparison group. The

difference can be seen from the figure 5. DPO is less than 60 days in most of the

companies studied in this thesis. The average DPO is 32 days. The average DPO

in the comparison group is 27 days which is 5 days shorter than the average DPO

for all companies. These days a normal credit time is somewhere between 7 and

28 days so the average time is a bit long. Most of the companies are granting 28

days for their customers to pay their bills. But it is not by any means a standard.

This credit time is shortening all the time and the financial crisis decreased it even

more. 14 days is probably the most popular credit time in the business-to-business

environment. There same reasons for the behavior of accounts payables than

accounts receivables because they are the same payment only looked from

different sides of the coin. Companies that work closer to consumers have also

shorter DPO.

mCCC and DPO has positive relationship which means that mCCC is increasing

when DPO is increasing. This is controversial to the previous researches that

indicate that mCCC will decrease when DPO is increasing. The definition of

mCCC, as well as CCC, indicates that payables are subtracted from inventories

and receivables. Companies should always use the longest possible payment times

if the cash discounts are not significant. The company can ensure better liquidity

if the payables are extended.

3.3.4 Days of Advance Payments Outstanding

Days of advance payments outstanding (DAO) has a higher impact on comparison

group than among all studied companies. This can be seen from the figure 5.

DAOis less than 50 days among most of the companies that are receiving advance

payments and that are studied in this thesis. The average DAO is 13 days. mCCC

and DAO has a negative relationship which means that mCCC is reducing when

DAO is increasing The average DAO in the comparison group is 35 days which is

22 days longer than within all the studied companies. There are 73 companies that

32

are receiving advance payments of some sort which is 68 percent of all the studied

companies. Most of the companies do not receive large amounts of advance

payments because the focus of cash transactions is still after the product has

changed its owner. The longest DAO can be found from the companies that are

working in the project business.

There are various reasons for receiving advance payments. Smoothing of the cash

flow can be seen as a one major factor for advance payments. Advance payments

are helping both the producer as well as the customer to keep their finance in

balance. Customers do not have to pay enormous amount of cash at once instead

they can pay the cash in small portions. The advance payments are beneficial for

the receiver as well because they are reducing the need of working capital.

Basically the producer does not need as much cash of their own as they would

without the advance payments. The advance payments are a necessity in situations

where the company just does not have enough working capital to start with. The

companies that are working with private customers are using advance payments to

secure the cash flow. Airline tickets for example are bought before the flight so

that the company can make sure they get cash from all the customers on board.

3.4 The difference between CCC and mCCC

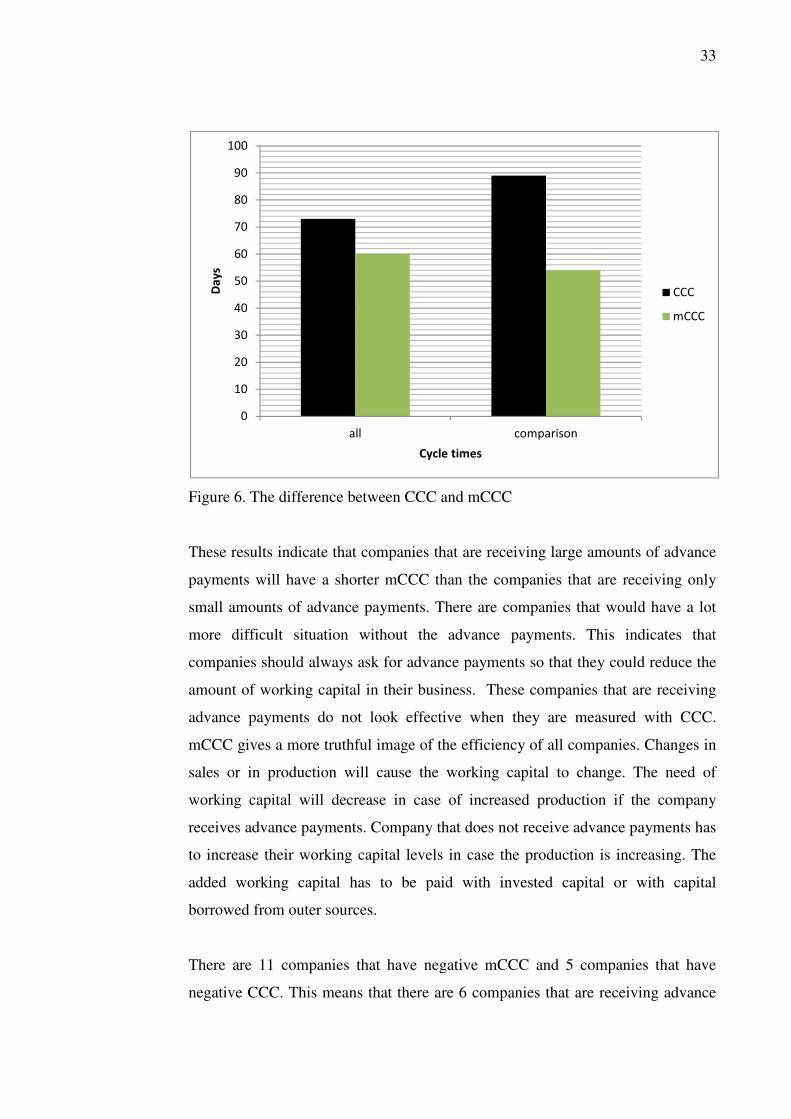

Average CCC in this studied data is 73 days and the average mCCC is 60 days.

Average mCCC is 82 percent of CCC. These findings indicate that advance

payments really help companies with working capital. The advanced payments are

dropping the need of working capital by 13 days. The companies need almost a

fortnight’s amount of less working capital to run their businesses. There is also a

difference between CCC and mCCC in the comparison group. The average CCC

in the comparison group is 89 days and the average mCCC is 54 days. mCCC is

60 percent out of CCC and the difference between these two is 35 days. The

relationship of CCC and mCCC can be seen from the figure 6.

33

Figure 6. The difference between CCC and mCCC

These results indicate that companies that are receiving large amounts of advance

payments will have a shorter mCCC than the companies that are receiving only

small amounts of advance payments. There are companies that would have a lot

more difficult situation without the advance payments. This indicates that

companies should always ask for advance payments so that they could reduce the

amount of working capital in their business. These companies that are receiving

advance payments do not look effective when they are measured with CCC.

mCCC gives a more truthful image of the efficiency of all companies. Changes in

sales or in production will cause the working capital to change. The need of

working capital will decrease in case of increased production if the company

receives advance payments. Company that does not receive advance payments has

to increase their working capital levels in case the production is increasing. The

added working capital has to be paid with invested capital or with capital

borrowed from outer sources.

There are 11 companies that have negative mCCC and 5 companies that have

negative CCC. This means that there are 6 companies that are receiving advance

0

10

20

30

40

50

60

70

80

90

100

all comparison

Da

ys

Cycle times

CCC

mCCC

34

payments so much that their need for working capital is negative. These 11

companies do not need any working capital because their customers and suppliers

are paying for them. Negative cycle time is a good thing because companies do

not need any working capital. It has usually been considered that if companies

have negative CCC they get longer period to pay their bills than they request from

their customers. Advance payments change this setting. Company can receive

advance payments before the capital is contracted into the inventories. They do

not need long period to pay their bills because they already have sufficient amount

of cash to conduct their work.

REL has made working capital benchmarking for one thousand largest companies

in United States of America. Cycle times for working capital were calculated

using data from the years 2008 and 2009. The average CCC for all industries was

35.4 days in 2008 and 38.3 days in 2009. (The Controller’s Report 2010, 5-6)

These cycle times are significantly lower than cycle times discovered in this

study. The difference might be explained by the varying working capital

structures in different countries and with the smaller sample size. There are

researches that present that the average CCC in pulp and paper industry is 63 days

and in automotive industry 67 days (Pirttilä et al. 2010, 9; Lind et al. 2012, 8).

These figures are close to the figures discovered in this study. The discovered

CCC is a bit longer than these and mCCC is a bit shorter than the CCC indicated

in these studies. Figure 7 gives more information about the differences between

CCC and mCCC. The figures are average figures among all studied companies.

This comparison reflects that working capital structures are variable in different

branches.

35

Figure 7. CCC and mCCC

3.5 Branches with advance payments

Companies that have DAO more than five days mainly work in the project

business but there is also remarkable amount of companies from the ICT and

publishing industries. This group also includes companies from the manufacturing

industry as well as mining and service industries. The companies are divided into

two categories for further research; project companies and other companies. There

are 13 project companies and 25 other companies. This research concentrates to

project companies but there are also closer looks to ICT and publishing

companies.

All these three industries; project, ICT and publishing, receive a lot advance

payments. There are different and similar reasons for receiving advance payments

in all these industries. There are similarities in project and ICT industries because

some ICT companies conduct only projects. Most ICT companies provide only

services, not products and sometimes the services are done project based.

-60

-40

-20

0

20

40

60

80

100

120

CCC CCC mCCC mCCC

Da

ys

Average cycle times

mCCC

CCC

DAO

DPO

DSO

DIO

36

Publishing companies are different because they do not do projects. Book

publishing could be considered as projects but for the companies it is just regular

continuous business. They are printing books all the time, only the book title

changes.

Project companies do not necessarily have enough equity to finance different

steps of the project. Construction companies for example need a lot of money to

buy the materials for the project. They do not necessarily have enough working

capital to cover the expenses so they need the customer to pay advance payments.

The companies also need less working capital which is good because they can

invest the money to get more profit. The amount of advance payments is not

constant. Companies negotiate with customers about the needed level of advance

payments. Advance payments are usually some percentage of the total price of the

project. Advance payments might also be paid in several steps of the project.

One reason for the advance payments is commitment. Large scale projects take

several years to finish and they require huge amounts of money and working

hours. Project companies need to commit the customer to the project so the

customer will not change the company providing the project. Customers may find

a cheaper option to carry out the project. Project companies cannot sell the

finished product or service to the next client unlike production companies can.

Project company has then made redundant work that will affect their financial

status. Customers that pay advance payments will be more committed to the

project because they already have invested money to the project.

Publishing is the only branch with advance payments that is close to consumers.

They are publishing almost exclusively to consumers. Magazines and newspapers

are usually paid in advance in order to get it delivered at home. Annual

subscriptions are also often cheaper than single copies. Books are usually paid

when they are purchased from the bookstore or from the Internet. One of the

biggest reasons for this advance payment system is custom. People are used to pay

in advance and they do not see it strange. Individual consumers also do not have

37

any influence in large publishing companies in order to change the system. The

system is very affordable for publishing companies because they get the cash in

advance. They will easily achieve negative cycle times which are always good for

the companies.

The reason why advance payments concentrate into particular branches is not

clear. Project companies in ICT and construction branches receive a lot of them

but why not wholesale traders? They have to purchase the products with their own

capital and they will get cash from the products after they have sold them. The

branches where there is no custom for advance payments will have difficulties in

asking for advance payments because the customers are not used to them.

Competition in a branch is also one determining factor for advance payments.