The ROI of the PA Dutch Convention & Visitors Bureau ... Economics... · 2.6 Perishability of the...

40

May 28, 2014 The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities

Transcript of The ROI of the PA Dutch Convention & Visitors Bureau ... Economics... · 2.6 Perishability of the...

May 28, 2014

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

2

Contents

1. Executive Summary ........................................................................ 3

2. Vital Role of Destination Promotion ............................................... 4

2.1 Tourism as a fragmented sector ................................................................. 5

2.2 Efficiencies of scale and stable, sustained operations ............................... 6

2.3 Essence of the tourism product .................................................................. 7

2.4 Competitive market ..................................................................................... 7

2.5 Global market opportunity ........................................................................... 8

2.6 Perishability of the tourism product and seasonality of demand ..............10

3. Key Performance Indicator Analysis ........................................... 11

4. Market Share Analysis .................................................................. 15

4.1 Visitor spending.........................................................................................16

4.2 Tourism employment ................................................................................18

4.3 Room revenue based on bed tax receipts ................................................19

4.4 Hotel performance as measured by STR .................................................21

5. Case Study Review........................................................................ 24

5.1 Destination marketing ROI matrix .............................................................24

5.2 Case studies in which destination marketing spending was reduced.......28

5.3 Brand USA and the effectiveness of destination marketing .....................29

6. Economic Impact Analysis ........................................................... 32

6.1 Economic impact of travel and tourism in Lancaster County ....................32

6.2 Economic impact of PDCVB .....................................................................36

7. About Tourism Economics ........................................................... 39

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

3

1. Executive Summary

Destination marketing is a proven driver of economic development and is

particularly important due to the unique characteristics of the tourism sector. To

document the important role of Pennsylvania Dutch Convention and Visitors Bureau

(PDCVB) promotional activities, Tourism Economics has conducted a multi-layered

analysis.

The analysis begins with an explanation of the vital role that destination promotion

plays in Lancaster County. Given the characteristics of the tourism sector, including

its fragmented structure and prevalence of small businesses, individual businesses

lack the economic incentives and financial wherewithal to independently conduct

true destination marketing. As a destination marketing organization (DMO), the

PDCVB communicates a coordinated, sustained message to potential travelers that

conveys important aspects of Lancaster County as a destination. These activities

help Lancaster County stay relevant and visible in the eyes of potential travelers, to

maintain relationships with tour operators, and keep a current online presence that

is useful to households whether they are in the Mid-Atlantic region, or across the

globe.

Tourism Economics’ analysis of key performance indicators shows an organization

that continues to succeed at not only creating brand awareness through advertising,

but also driving interest among potential visitors that results in interaction with the

PDCVB as a source of information on the destination.

To assess changes in Lancaster County’s tourism market share over recent years,

Tourism Economics conducted a market share analysis across four measures of

tourism activity. The results show that Lancaster County has grown its market share

as measured by visitor spending and accommodations revenue as tracked by room

rental taxes, and maintained its share of employment. The analysis also shows that

Lancaster County hotels have posted stronger occupancy and RevPAR gains than

comparable regions. In dollar terms, market share improvements between 2007 and

2012 translated into $51.5 million of additional visitor spending and $7.9 million of

additional room rental revenue.

The analysis concludes with two final sections. The first is a case study review that

documents the importance of destination marketing based on typical ranges of

estimated marketing returns that are realized by DMOs, and by considering case

study examples in which marketing funding reductions have resulted in substantial

declines in visitation. The second is an analysis of the economic impacts of tourism

in Lancaster County updated on a preliminary basis for 2013, and the estimated

PDCVB contribution to these impacts. In total, $1.9 billion of direct visitor spending

in Lancaster County by 7.9 million visitors helps support almost 23,700 tourism

economy jobs and generate $184.7 million of state and local taxes. Of this, the

PDCVB contribution represents approximately $120.9 million of visitor spending,

supporting almost 1,600 jobs and $10.2 million of state and local taxes.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

4

2. Vital Role of Destination Promotion

The case for destination marketing is broad and compelling. Indeed, across the US,

there are more than 500 destination marketing organizations (DMOs) with a

combined budget of $1.5 billion in the 2011/12 fiscal year. This chapter briefly

outlines the rationale for destination marketing and the particular importance of the

Pennsylvania Dutch Convention and Visitors Bureau (PDCVB) in fostering the

economic value for Lancaster County of the tourism sector.

In summary, destination marketing is vital because:

The tourism sector is fragmented across various industries and is

made up of smaller companies. Individual businesses lack the

capacity to conduct certain types of marketing effectively, and certain

benefits accrue across the economy rather to just an individual

business.

Scale supports marketing efficiencies, leveraging the impact of each

marketing dollar. DMOs provide a stable base for coordinated

marketing over time.

The destination and overall experience of an area is a fundamental

motivator of tourism. As a result, the message to a potential traveler

extends beyond the offerings of a single business.

Competing destinations are actively marketing and a failure to

engage with travel markets results in lost market share.

The global market opportunity is vast, presenting attractive growth

prospects for domestic destinations that can present a coordinated

message to potential visitors.

Destination marketing helps address challenges presented by the

perishability of tourism products and the seasonality of demand.

Lastly, as discussed in case studies in Section 2, destination marketing has been

proven to be historically effective, producing returns in excess of investments and

greater than many other sectors.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

5

Other transport25%

Lodging20%

Food & beverage

16%

Air transport16%

Shopping13%

Recreation and Ent.

10%

Distribution of tourism spending in the US2012, Share of total spending

Source: BEA Travel & Tourism Satellite Account

2.1 Tourism as a fragmented sector

The tourism sector faces two natural disadvantages that impact destination

marketing. The first is that tourism is not represented by a single industry, the

second is that many tourism sector businesses are small establishments. As a

result, relying on individual businesses to conduct independent destination

marketing would leave a destination short of its potential. Collaborative destination

marketing effectively deals with this challenge by representing a fragmented tourism

industry as a single product to a common customer. Destination marketing

represents all of these disparate businesses to origin markets in a way that no

single business or industry segment could.

The following provides a more thorough discussion of these

points.

- Tourism spending is spread across multiple

industries. As with the national view of the

distribution of tourism spending presented in an

accompanying graph, visitors are customers to

Lancaster County businesses across numerous

industries, including hotels, restaurants, shops, rental

car companies, taxi services, museums, and

theaters. As a result, a visitor benefits multiple

segments of the Lancaster County economy.

- Tourism-related businesses tend to be smaller

than in other sectors. Similar to national norms, the

tourism sector in Lancaster County is comprised of

small and medium sized businesses, and many

businesses have fewer than 50 employees. Of the

110 lodging establishments in the County listed by STR at year-end 2013,

the average room count was 63 rooms per property and the largest hotel

had a roughly 5% share of total room supply in the County. At the level of an

individual destination, this implies that very few of these organizations would

have the resources needed for concerted investments in destination

marketing.

- Coordinated destination marketing addresses the challenges posed by

the tourism industry structure. As a result of the industry structure,

independent marketing of the destination by individual businesses can be

far less compelling than coordinated destination marketing. Because a

visitor’s spending is spread across businesses, any single business may not

capture sufficient share of a visitor’s spending to justify marketing to attract

visitors to a destination. For example, an individual hotel could market the

attractiveness of a destination, but it would only benefit from those

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

6

additional visitors who not only choose the destination, but also choose that

particular hotel; and the hotel would only benefit directly from the visitor’s

spending at the hotel and not other businesses in the area. In other words,

at the level of an individual business, the returns on independent marketing

to attract visitors to a destination can be less compelling. However, when

viewed at the level of the destination, there is a more direct connection. The

destination captures a substantial dollar amount per visitor, and in

aggregate there are compelling returns on effective destination marketing.

The fragmented nature of the sector, and the prominence of small businesses in the

Lancaster County tourism industry, implies that no one business entity would have

the resources to adequately fund the promotion activities conducted by PDCVB in a

way that would generate meaningful returns in the form of increased visitation.

Hence, collaborative destination marketing by PDCVB plays a vital role, and yields

results that benefit the Lancaster County economy, including its businesses and

other stakeholders.

2.2 Efficiencies of scale and stable, sustained operations

Effective destination marketing requires significant and consistent funding with the

aim of gaining a sufficient “share of voice” to be heard and make an impact. While

the cost of media purchases is expensive, per unit advertising costs go down as the

volume of purchases goes up. Further, scale produces efficiencies that reduce

overhead and maximize the share of funding that goes to actual marketing and

advertising. As a result, the larger scale of collaborative destination marketing is

more effective than what individual businesses could accomplish. Simply put, the

whole of destination marketing is greater than the sum of individual parts.

One of the benefits of coordinated marketing facilitated by a DMO such as PDCVB

is the ability to have a stable organization and funding base to support destination

marketing. For example, this allows a DMO to build the infrastructure, brand

awareness, and relationships that yield results over time.

As a result, PDCVB is at the point at which it is effectively using annual funds to

leverage a brand, infrastructure and relationships that have been built up over time.

For example, in terms of marketing, because a base level of awareness of the

destination has already been established with some target customers, additional

annual marketing spend can be more effective at activating and reinforcing key

messages. Infrastructure, such as the website, and the processes around

maintaining and updating material such as the Lancaster County Getaway Guide, as

well as current staff of the organization, represent key resources, allowing PDCVB

to accomplish more with its marketing budget than it could without such resources.

Also, PDCVB supports market research, such as visitor profile studies, that help

individual businesses better target market opportunities, but which would likely not

be economical for individual businesses to support independently. Lastly, PDCVB

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

7

leverages established relationships with local tourism-sector businesses and

marketing service providers that enable it to better promote Lancaster County as a

destination.

2.3 Essence of the tourism product

The fundamental motivation driving a visit to Lancaster County is not a single

business—it is the destination and the overall experience the area has to offer. This

experience is comprised of a visitor’s interaction with and patronage of numerous

businesses and local experiences: hotels and other accommodations; restaurants;

shopping and galleries; conferences; performances and other events; family

activities; sports and other recreation; and cultural sites and attractions. In many

cases, the choice of a hotel, for example, is not the primary decision for potential

visitors choosing between Lancaster County and another destination.

Instead, for many visitors the destination is the primary decision and as a result,

destination marketing is an essential driver of demand for tourism-related goods.

Marketing efforts that focus on only one segment of the tourism market, such as

communicating the offering of a specific hotel or other business, do not also

adequately address the core motivation for potential visitors. The activities of

PDCVB recognize that fact. By banding together, the members of the County’s

tourism industry are able to represent the destination collectively, and in doing so

drive demand for all segments of the tourism industry. Stand-alone marketing efforts

would almost certainly be less effective than a collective destination marketing

campaign.

As an example, packages that are offered by partnerships of local businesses, or in

conjunction with events held throughout the year, are also part of the vital role of

destination marketing. Coordination and marketing of such packages may be more

effective when the package offers the potential visitor the option of several hotels or

dining choices as a part of the package.

2.4 Competitive market

To lack destination promotion is to lose market share. This is partly evident by the

sheer number of DMOs in the US and the amount invested annually. One oft-cited

example of what happens when destination promotion is defunded comes from

Colorado. Prior to 1993, Colorado had a $12 million marketing budget, funded by a

0.2% tax on travel-related goods and services. Voters struck down the tax,

effectively eliminating the marketing and promotion budget. The effect of the abrupt

stop to marketing was significant and swift: Colorado lost 30% of its market share of

US tourism within two years and more than $1.4 billion annually in visitor spending.

When a new Colorado Tourism office opened and the budget was expanded,

spending recovered.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

8

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

1996 1998 2000 2002 2004 2006 2008 2010 2012

US Share of North American Outbound% out-of-region travel by source

Source: Tourism Economics

Mexico

Canada

Another example has played out on a national level, as the US competes to attract

visitors from other countries. Similar to the regional destination level, the absence of

destination marketing at the national level can lead to a lack of competitiveness and

declines in market share. Global competition for such international travelers is

steep, with tourism offices around the world devoting significant resources to

destination marketing. Oxford Economics, the parent company of Tourism

Economics, estimates that $4.3 billion was spent on national level tourism promotion

in 2012; primarily by European ($1.7 billion) and Asia Pacific destinations ($1.2

billion). Although the United States remains a top destination among worldwide

travelers, during a 15 year period, beginning in 1996 and 1997 (depending on the

market), the United States lost market share to destinations with consistently funded

destination marketing programs (see accompanying graphs).

Tourism Economics works with national tourism offices around the world and

regularly observes the positive effects of tourism campaigns sponsored by these

organizations. Implicitly, these activities result in lost market share among

destinations that are not investing in destination promotion. And this is one of the

reasons that the United States has lost global market share.

2.5 Global market opportunity

The sheer size of the global travel market also makes a compelling case for

destination marketing. Since 1990, growth in international travel has averaged 4%

per annum and has expanded a cumulative 62% since 2000. In 2013, international

tourist arrivals reached 1.1 billion. Many of these travelers have limited, or no, initial

familiarity with the offerings of Lancaster County as a destination. By working with

tour group leads, and providing resources such as its website, PDCVB helps

promote Lancaster County to visitors from these growing markets in ways that

extend beyond the capabilities of many small or medium-sized tourism businesses.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1996 1998 2000 2002 2004 2006 2008 2010 2012

US Share of Long Haul Outbound Travel% out-of-region travel by source

Source: Tourism Economics

South America

Europe

Asia

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

9

This rate of global travel growth is expected to persist as the global middle class

continues to expand (see accompanying graphs). By 2020, the global market for

international travel is expected to reach 1.5 billion annual tourist arrivals.

The growth of the US tourism industry, in all of its parts, depends largely on its

success in attracting international visitors. International markets represent the

highest growth area of business for the tourism sector in the United States. In 2007,

international visitor spending on US trips represented 16% of all travel spending in

the United States. In 2013, this is estimated to have reached 20% and is expected

to continue to rise based on Oxford Economics latest econometric forecasts.

0 5 10 15 20

China

India

Indonesia

Malaysia

Thailand

New "Middle-Class" Households 2013-23millions

Source: Oxford Economics

75 mn

9 mn

7 mn

2 mn

1 mn

0

200

400

600

800

1,000

1,200

1,400

1,600

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

International tourist arrivals by regionMillions

Source: Tourism Economics

Americas

Europe

Asia Pacific

Mideast & Africa

50

100

150

200

250

2007 2009 2011 2013 2015 2017 2019

US visitor spending by type2007=100

Source: U.S. Travel Association, BEA, Tourism Economics

International travel spending

Domestic travel spending

15%

16%

17%

18%

19%

20%

21%

22%

23%

2007 2009 2011 2013 2015 2017 2019

International visitor spendingShare of total visitor spending (including domestic and international)

Source: U.S. Travel Association, BEA, Tourism Economics

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

10

2.6 Perishability of the tourism product and seasonality of demand

In manufacturing, inventory can be stored or redistributed to markets where demand

is stronger, and seasonal fluctuations in demand can be managed effectively. This

same degree of flexibility doesn’t exist for many tourism-dependent businesses, the

product of which is perishable, fixed in one market, and typically under more heavy

demand during some seasons and days of the week than others.

For example, in the lodging sector, the product sold is a room night, which cannot

be held over to another day. If a room goes unoccupied, the potential room night

sale and associated revenue are lost. The hotel product depends heavily on

infrastructure, which cannot be picked up and moved to another location. Also, the

upfront investment of capital required in lodging, and the fixed nature of many

operating costs, results in a situation in which successful ongoing operations are

frequently heavily dependent on demand reaching a “break even” level of

operations. Restaurant and retail products are less perishable in a direct sense,

however management of inventory and staffing for these industries is also

challenging, particularly for the types of small businesses that make up Lancaster

County’s tourism industry. In situations in which demand is concentrated in peak

periods, staffing can be challenging for employers and employees alike due to

season duration.

Effective destination marketing helps address these challenges. By broadening

potential visitors’ understanding of a destination’s offering, destination marketing is

frequently designed to boost demand during shoulder periods. This helps

businesses make use of resources that would otherwise be idle, extends the

duration of seasonal employment, and supports a better base for year-round jobs.

This incremental activity supported by destination marketing can be critically

important to successful and profitable operations in the tourism sector. The end

result is a level of market demand that benefits local businesses, employees and

other stakeholders and expands the tax base.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

11

3. Key Performance Indicator Analysis

As a window to recent PDCVB promotional activities, Tourism Economics analyzed

information provided by PDCVB and selected a set of key performance indicators.

These measures track advertising exposure, as well as interactions with the

PDCVB, such as through the website and room bookings.

To document the advertising activities of PDCVB, Tourism Economics relied on an

analysis presented by Harmelin Media and marketing budget information provided

by PDCVB.1 Key aspects of PDCVB’s 2013 advertising are summarized as follows:

- Marketing activities were focused on reaching specific target markets. For

example, a condensed list of geographic markets was used, and media mix

was selected to reach women ages 25-54 with families, and couples/empty

nesters ages 45-64 in particular. Also, digital marketing was introduced to

extend PDCVB’s reach to targets with active, evolving lifestyles.

- Television advertising was targeted to Harrisburg/Lancaster/Lebanon/York

(HLLY), Philadelphia and New York (Long Island and Northern NJ). The

advertising delivered 1,933 target rating points (TRPs).2

- The digital campaign was targeted to the same markets as the television

marketing, plus Washington DC. The display and online video campaigns

combined generated over 27,000 clicks and over 3.3 million completed

video views (81.4% video completion rate, above industry benchmarks) on

nearly 12 million impressions. Search engine marketing resulted in 1.8

million impressions through the end of October 2013, with a click-through-

rate of 5.1%.

- Out of home advertising, including billboards, generated 42.6 million gross

impressions.

Such advertising is designed to influence the trip planning process of a potential

visitor. In many cases, these households take an intermediate step in the trip

planning process to learn more about Lancaster County by interacting with the

PDCVB in some way. To document such interactions, and to provide a view to

various other marketing conducted by PDCVB beyond the advertising described

1 Harmelin Media (2013, November) PA Dutch Convention & Visitors Bureau 2013

Media Recap & Post Analysis.

2 TRPs is a measure of the number of ad impressions delivered to the target group

population. For example, if 50% of a target population sees an ad spot four times a

week for 10 weeks, that is equivalent to 2,000 TRPs (50 x 4 x 10).

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

12

above, Tourism Economics selected a set of PDCVB metrics for further

consideration, and noted the following observations.

- Potential visitors are interacting with PDCVB through a variety of means.

These activities include online means, extending from the website, which

received 2.3 million visits and generated over 33,000 sign-ups for email

communications, to Facebook, where the PDCVB recorded over 26,000

measures of engagement such as likes and shares. Offline interactions

were also substantial, with over 106,000 visitors recorded at the two visitor

centers combined, and distribution of over 755,000 copies of the Getaway

Guide

- While some activities decreased in 2013, many of the key measures

increased. Some of these shifts appear consistent with a transition to online

mediums. For example, while distributions of the Getaway Guide and visits

to the visitors centers decreased, online and other types of offline activities

increased, such as website visits, public relations stories, and room nights

booked.

Overall, the metrics support the picture of a DMO that continues to succeed at not

only creating brand awareness through advertising, but also driving interest among

potential visitors that results in interaction with the PDCVB as a source of

information on the destination.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

13

Metric 2012 2013 Change

Website

Visits 2,165,661 2,333,793 8%

Page views 10,768,992 10,538,248 -2%

Unique visitors 1,473,609 1,636,698 11%

Website Visits From Top Feeder Markets

Philadelphia 390,252 380,903 -2%

New York 386,381 367,263 -5%

Harrisburg/Lancaster/

Lebanon/York (HLLY) 343,240 360,618 5%

Washington D.C. 155,774 150,923 -3%

Baltimore 83,950 85,530 2%

Website Conversion Rate

Email sign-ups 38,393 33,159 -14%

Clicks to member websites 1,155,126 1,282,140 11%

Reservation inquiries 214,175 143,351 -33%

Getaway Guide requests 47,124 40,776 -13%

Consumer e-Marketing

Number of emails opened 499,688 749,111 50%

Advertiser click thru 9,541 9,867 3%

Total click thru 182,121 182,401 0.2%

Site visits 141,108 128,636 -9%

Engagement (likes, shares,

comments) 13,253 26,199 98%

Website visits 8,631 29,734 245%

Source: PDCVB

PDCVB Online Activity

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

14

Metric 2012 2013 Change

Getaway Guide Distribution

Total 793,558 755,279 -5%

Visitor Center Traffic

Greenfield Visitors Center 106,977 79,550 -26%

Downtown Visitors Center 31,445 26,978 -14%

Total 138,422 106,528 -23%

PR Activity

Number of stories 1,038 1,738 67%

Audience impressions (in

billions) 1.1 2.0 82%

Ad value (in millions) $8.5 $12.2 44%

Reservation Center

Leisure room nights 3,186 1,617 -49%

Sports & convention room

nights 11,645 23,130 99%

Sales Activity

Lead room nights 146,839 120,137 -18%

Room nights booked 45,974 52,240 14%

Source: PDCVB

PDCVB Offline Activity

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

15

4. Market Share Analysis

Recent years have witnessed substantial shifts in travel activity across the country,

initially as travelers responded to the national recession that extended from

December 2007 to June 2009 by pulling back on trips and spending, and more

recently as travel activity has resumed. To understand the recent performance of

the tourism sector in Lancaster County, and to understand how Lancaster County’s

market share has weathered these changes, it is useful to consider several sets of

comparable markets in the region. It is also useful to consider several sets of

indicators to help form a holistic understanding of relative performance trends.

The overall message from the discussion that follows is that Lancaster County has

improved its tourism market share slightly in recent years, and is emerging from the

recession well-positioned to further grow tourism as a key industry in the local

economy. The following key points are noted:

- In terms of visitor spending, Lancaster County tourism has grown at a

slightly faster pace than the state (in this case, the state total adjusted to

remove Philadelphia and Pittsburgh). Overall, this indicates that Lancaster

County is improving its market share and attractiveness in the eyes of

visitors. With national and regional economies that are gradually recovering

from the recession, and visitor spending volumes that are expanding,

Lancaster County is a competitive destination that is positioned to continue

to retain and grow its market share.

- In terms of tourism employment, Lancaster County tourism has expanded,

exceeding the pace of growth in some comparable regions, but has grown

at a slower pace than the adjusted state total. Given the favorable

indications on the other market share measures, there is potential for

Lancaster County tourism employment to continue to grow in future years.

- In terms of accommodations revenue as tracked by room rental taxes,

which provides a broad measure of hotel, motel, and B&B performance,

Lancaster County accommodations establishments have out-performed

peers in comparable regions.

- In terms of lodging performance as tracked STR, a firm that aggregates

hotel and motel performance data, Lancaster County hotels have out-

performed peers in comparable regions as measured by strong occupancy

and RevPAR gains.

The following provides a more detailed discussion of the market share analysis

across four measures of tourism activity: visitor spending, tourism employment,

estimated room revenue based on bed tax receipts, and hotel performance as

measured by STR.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

16

4.1 Visitor spending

As part of its annual analysis for the Commonwealth of Pennsylvania, Tourism

Economics estimates visitor spending in each county.3 These estimates show a total

of $1.8 billion of tourism sector spending by visitors to Lancaster County during

2012, an increase of 26.5% from the level of $1.4 billion in 2005 (reflects rounding).4

These estimates are based on visitor spending surveys and industry data.

Tourism Economics analyzed visitor spending in Lancaster County in relation to the

following areas:

- Dutch Country Roads region, of which Lancaster County is one of nine

counties (Adams, Berks, Cumberland, Dauphin, Franklin, Lancaster,

Lebanon, Perry, and York counties);

- Valleys of the Susquehanna, a five-county region (Columbia, Montour,

Northumberland, Snyder, and Union counties);

- The Alleghenies, an eight-county region (Bedford, Blair, Cambria, Centre,

Fulton, Huntingdon, Juniata, and Mifflin counties); and,

- The state, adjusted to exclude the counties that are part of the Philadelphia

and Pittsburgh metropolitan statistical areas (for Philadelphia this includes

five Pennsylvanian counties, and for Pittsburgh this includes seven).

The Lehigh Valley region was excluded from the comparisons, as the opening of a

casino in Bethlehem, PA in 2009 impacts the visitor spending growth in a way that is

not comparable with Lancaster County.

To support comparability across the regions, Tourism Economics indexed the

spending levels such that spending in each region was equal to 100 in 2005. In the

accompanying graph, the index value of 126.5 for Lancaster County shows that the

26.5% increase since 2005 trails only the Valleys of the Susquehanna region, and

slightly outpaces the Dutch Country Roads and The Alleghenies regions and the

state.

3 Tourism Economics (2013, December). The Economic Impact of Travel and

Tourism in Pennsylvania, Tourism Satellite Account Calendar Year 2012.

4 The economic analysis section of this report includes a preliminary estimate of

2013 visitor spending in Lancaster County for the purpose of estimating economic

impacts of travel and tourism during 2013. For the purpose of the market share

analysis, discussion is limited to the period through 2012, as that is the period with

comparable information across regions.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

17

To take a closer look at the more recent performance in Lancaster County, Tourism

Economics calculated the change in market share from 2007 to 2012. As shown in

the adjacent table, Lancaster County improved from a 7.9% share of state visitor

spending in 2007 (excluding Philadelphia and Pittsburgh) to a 8.2% share in 2012,

representing a market share increase of 20 basis points (reflects rounding). As

shown in the accompanying table, a comparison of actual 2012 visitor spending in

Lancaster County to the hypothetical level of spending that would have occurred

without an increase in market share (i.e. remaining at 7.9%), shows that the market

share increase resulted in a gain of $51.5 million of additional visitor spending,

equivalent to a 2.9% increase of visitor spending relative to the hypothetical

alternative.

95

100

105

110

115

120

125

130

2005 2006 2007 2008 2009 2010 2011 2012

Valleys of the Susquehanna (128.1) Lancaster County (126.5)

State (excluding Phila. and Pitt.) (126) Dutch Country Roads (126.1)

The Alleghenies (124.6)

Visitor Spending

Index (2005=100)

Source: Tourism Economics

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

18

4.2 Tourism employment

Tourism Economics’ analysis for the Commonwealth also includes estimates of

tourism sector employment in Lancaster County, such as is supported by visitor

spending on lodging, retail, food and beverage, and other services. As a

supplemental measure of market share trends, an accompanying graph shows

tourism employment in Lancaster County as compared to selected comparable

regions. On the basis of employment, Lancaster County’s tourism sector has

expanded each year, with the exception of 2009 (due to the national recession). As

a result, tourism employment in 2012 in Lancaster County was 7.9% higher than in

2005. However, growth in Lancaster County has been somewhat slower than at the

state level. Despite this slower growth, there is still potential for Lancaster County to

continue to grow tourism sector employment in future years, especially because

other measures of market share and performance appear favorable.

Tourism spending analysis

Lancaster County market share (ratio to State excluding

Philadelphia and Pittsburgh)

7.9% 2007

8.2% 2012

20 Market share increase (in basis points, reflects rounding)

$1,817.5 Lancaster County tourism spending in 2012 (in millions)

$1,766.0 Hypothetical Lancaster County tourism spending in 2012 if market

share had remained at 2007 level (in millions)

$51.5 Gain attributable to improved market share (in millions)

2.9% Percentage increase attributable to improved market share

Source: Tourism Economics

Tourism Spending Market Share Change ('07 to '12)

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

19

4.3 Room revenue based on bed tax receipts

Lancaster County collects an excise tax of 1.1% on room rental revenue at all

hotels, motels and bed and breakfasts. Additionally, Lancaster County collects an

additional 3.9% room rental tax on hotels, motels and bed and breakfasts that have

greater than ten rooms. Information on the 1.1% excise tax can be used to estimate

total room revenue of accommodation establishments in Lancaster County, and

trends in these estimates are comparable across regions. Since bed tax receipt

information is available for Lancaster County for 2013, but was not yet obtainable for

the other regions, Tourism Economics has used hotel performance data from STR

to estimate 2013 performance for the comparable regions.

95

100

105

110

115

2005 2006 2007 2008 2009 2010 2011 2012

State (excluding Phila. and Pitt.) (111.6) Valleys of the Susquehanna (110.4)

Lancaster County (107.9) Dutch Country Roads (104.2)

The Alleghenies (102.1)

Tourism Employment

Index (2005=100)

Source: Tourism Economics

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

20

Based on this analysis, room revenue in Lancaster County has expanded more

quickly than the adjusted state total, as well as the estimates for two of the three

comparable regions. Lancaster County growth has been similar to the Dutch

Country Roads region overall, increasing 38.7% between 2007 and 2012, as

compared to a gain of 38.1% for Dutch Country Roads overall. Based on estimated

performance for 2013, Dutch Country Roads room revenue appears to have grown

slightly faster than that of Lancaster County, with both continuing to outperform the

comparable regions.

To take a closer look at the more recent performance in Lancaster County, Tourism

Economics calculated the change in room revenue market share from 2007 to 2012

based on the bed tax estimates. As shown in the adjacent table, Lancaster County

improved from a 9.3% share of state room revenue in 2007 (excluding Philadelphia

and Pittsburgh) to a 9.9% share in 2012, a market share increase of 60 basis points.

As shown in the accompanying table, a comparison of estimated 2012 room

revenue in Lancaster County to the hypothetical level of room revenue that would

have occurred without an increase in market share (i.e. remaining at 9.3%), shows

that the market share increase resulted in a gain of $7.9 million of additional room

revenue, equivalent to a 6.2% increase of room revenue relative to the hypothetical

alternative.

90

100

110

120

130

140

150

2007 2008 2009 2010 2011 2012 2013

Lancaster County (138.7) Dutch Country Roads (138.1)

State without Philadelphia and Pittsburgh (130.7) The Alleghenies (114.6)

Valleys of the Susquehanna (112.9)

Room Revenue Based on Bed Tax

Index (2007=100)

Sources: Tourism Economics; state and local sources

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

21

4.4 Hotel performance as measured by STR

The hotel performance statistics aggregated from individual hotel properties by STR,

formerly Smith Travel Research, provides a timely measure of hotel performance.

Based on this information, we observe that lodging supply as measured by the STR

census of lodging properties has expanded more slowly in Lancaster County than in

comparable regions, but that performance levels of existing hotels have shown

stronger than average improvement.

Occupancy levels at Lancaster County hotels have improved substantially from

2008 levels, surpassing the gains achieved by the Dutch Country Roads region

more broadly and the adjusted state total (see accompanying graph).

Lodging analysis

Lancaster County market share (ratio to State excluding

Philadelphia and Pittsburgh)

9.3% 2007

9.9% 2012

60 Market share increase (in basis points, reflects rounding)

$136.8 Lancaster County room revenue in 2012 (in millions)

$128.8 Hypothetical Lancaster County room revenue in 2012 if market

share had remained at 2007 level (in millions)

$7.9 Gain attributable to improved market share (in millions)

6.2% Percentage increase attributable to improved market share

Source: Tourism Economics, state and local tax records

Lodging Market Share Change ('07 to '12)

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

22

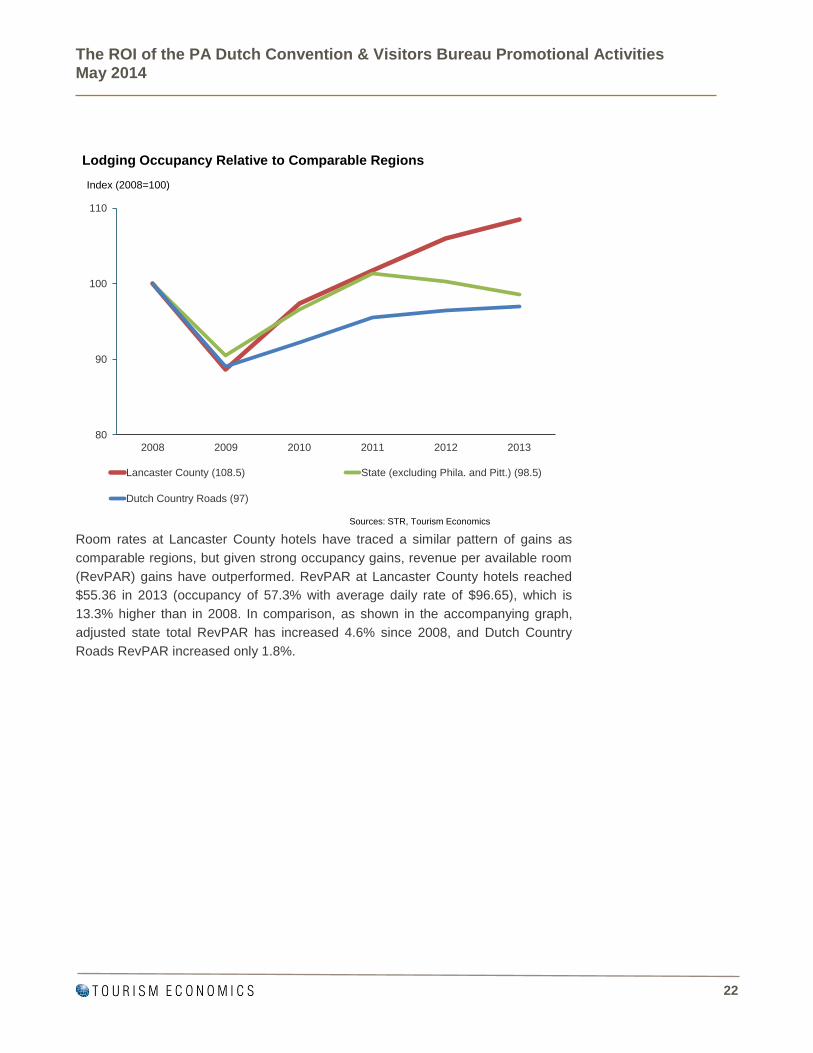

Room rates at Lancaster County hotels have traced a similar pattern of gains as

comparable regions, but given strong occupancy gains, revenue per available room

(RevPAR) gains have outperformed. RevPAR at Lancaster County hotels reached

$55.36 in 2013 (occupancy of 57.3% with average daily rate of $96.65), which is

13.3% higher than in 2008. In comparison, as shown in the accompanying graph,

adjusted state total RevPAR has increased 4.6% since 2008, and Dutch Country

Roads RevPAR increased only 1.8%.

80

90

100

110

2008 2009 2010 2011 2012 2013

Lancaster County (108.5) State (excluding Phila. and Pitt.) (98.5)

Dutch Country Roads (97)

Lodging Occupancy Relative to Comparable Regions

Index (2008=100)

Sources: STR, Tourism Economics

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

23

80

90

100

110

120

2008 2009 2010 2011 2012 2013

Lancaster County (113.3) State (excluding Phila. and Pitt.) (104.6)

Dutch Country Roads (101.8)

Lodging RevPAR Relative to Comparable Regions

Index (2008=100)

Sources: STR, Tourism Economics

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

24

5. Case Study Review

Given the important role of destination marketing, and the spending that is

undertaken every year across the US by local and regional destination marketing

groups in carrying out that role, understanding the connection between marketing

spend and corresponding destination impacts is an important topic. To that end,

Tourism Economics has compiled a repository of case studies of destination

promotion effectiveness. To communicate key findings, we have summarized three

aspects of this research. First, we present a return-on-investment (“ROI”) matrix that

summarizes destination marketing ROI estimates prepared through research in a

variety of US destinations. Second, we present several case studies of situations in

which destination marketing amounts have been reduced and discuss the resulting

effects on visitation and spending. Third, we discuss marketing of the US as a

destination for international travelers, and the returns that have been realized in

recent years.

5.1 Destination marketing ROI matrix

Many DMOs conduct periodic assessments of marketing effectiveness. There are

several goals of these studies, including understanding how specific marketing

campaigns were perceived by households, how effective the campaigns were in

having an impact on households’ intent to travel to a given destination, and which

target markets are showing differing level of responsiveness to marketing. Many of

these studies also include a specific analysis of the ROI of marketing spending in

the form of a quantitative assessment of the level of incremental visitor spending

and tax revenues that are attributable to the destination marketing being analyzed.

These studies use a variety of methodologies, and are measuring the impact of a

range of different campaigns used by destinations in a variety of situations. For

example, a specific study may look at incremental visitors attracted by a state-level

marketing campaign conducted by a state that attracts travelers from a range of

national markets, while another study may focus on the results of a more targeted

regional campaign carried out by a city-level CVB. While the results of a specific

study pertain most directly to the situation that was analyzed, and the corresponding

assumptions, it is appropriate to consider broader inferences from the research.

For the purpose of this report, Tourism Economics analyzed 16 recent studies that

included an estimate of the incremental visitor spending attributable to marketing

spending. For example, in a fairly typical approach, a study would:

- use a survey to analyze the effect of a specific advertising campaign on

households’ travel to a given destination, such as by analyzing the impact

on actual travel among those that had observed the advertising or by

analyzing the impact on households’ intentions to travel;

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

25

- project that effect to the broader set of households in the marketing area to

estimate the number of incremental visits attributable to the campaign;

- apply typical levels of spending per visitor to estimate incremental visitor

spending; and,

- compare incremental visitor spending to the level of marketing spending to

estimate the ROI.

Tourism Economics has summarized the estimates of incremental visitor spending

per dollar of marketing spend from these studies in the accompanying table. The

results range from as low as $12 for an analysis conducted for Syracuse, NY to as

high as $200 for an analysis conducted for Colorado. However, for the most part,

visitor spending per dollar of marketing spend ranges between $50 and $100, with

an average for state studies of $116 and an average of metro and regional studies

of $54. In other words, in general, recent marketing campaigns by destination

marketing organizations at the metro and regional level in the US have generated

approximately $54 of incremental visitor spending for each dollar of destination

marketing spending.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

26

As it relates to Lancaster County, it is useful to consider several selected regions

covered in the marketing impact research.

- Finger Lakes Wine Country consists of four counties. In economic impact

analysis for the State of New York, Tourism Economics estimated visitor

spending in this region totaled $328.0 million in 2012.5 Based on marketing

5 Tourism Economics (2013). The Economic Impact of Travel and Tourism in New

York, Calendar Year 2012, Finger Lakes Focus.

Marketing ROI Matrix

Region Timing

Visitor

Spending Per

Ad Dollar

States

Colorado 2012 200

Florida 2011 177

Maryland 2012 160

Wyoming 2013 134

Missouri 2013 131

North Dakota 2010 91

Virginia 2006 71

Michigan 2009/10 54

New Mexico 2012 29

Metros and regions

Philadelphia, PA 2009/10 100

Branson, MO 2012 79

Kansas City, MO 2013 65

Springfield, MO 2011 61

Finger Lakes Wine Country, NY 2012 44

San Diego, CA 2013 19

Syracuse, NY 2008 12

Average of all studies $89

Median of all studies $75

Average of states $116

Average of metros and regions $54

Sources: Local studies compiled by Tourism Economics

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

27

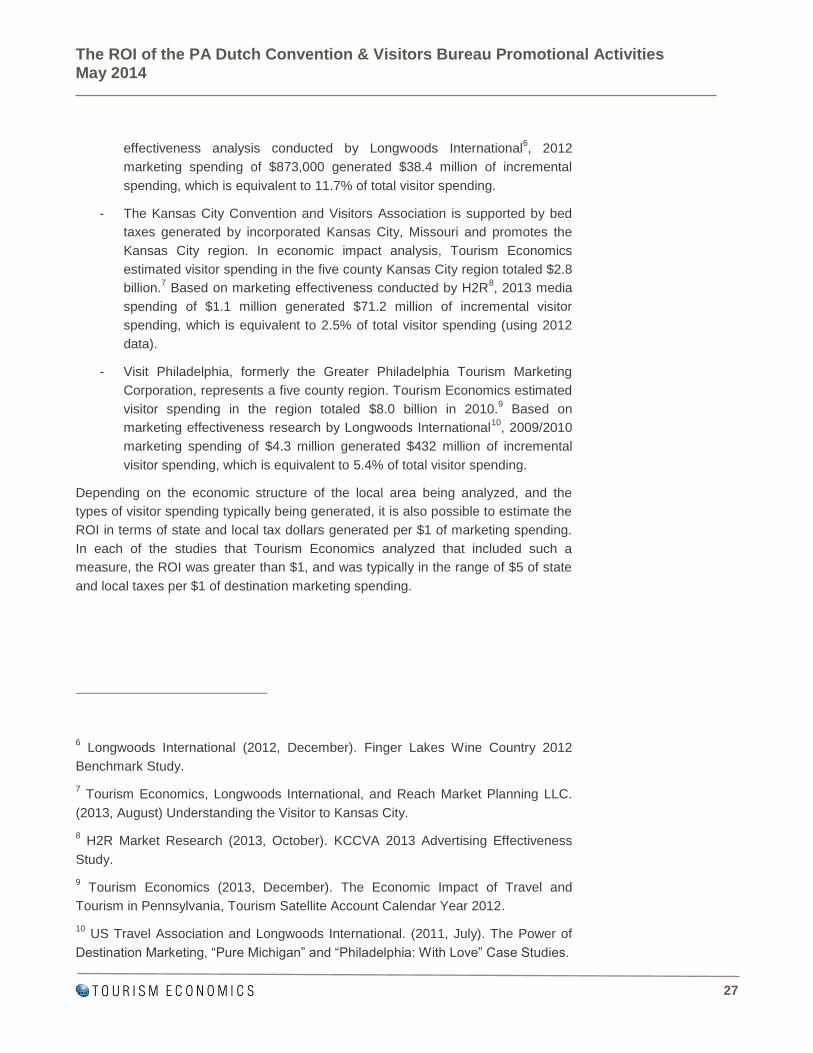

effectiveness analysis conducted by Longwoods International6, 2012

marketing spending of $873,000 generated $38.4 million of incremental

spending, which is equivalent to 11.7% of total visitor spending.

- The Kansas City Convention and Visitors Association is supported by bed

taxes generated by incorporated Kansas City, Missouri and promotes the

Kansas City region. In economic impact analysis, Tourism Economics

estimated visitor spending in the five county Kansas City region totaled $2.8

billion.7 Based on marketing effectiveness conducted by H2R

8, 2013 media

spending of $1.1 million generated $71.2 million of incremental visitor

spending, which is equivalent to 2.5% of total visitor spending (using 2012

data).

- Visit Philadelphia, formerly the Greater Philadelphia Tourism Marketing

Corporation, represents a five county region. Tourism Economics estimated

visitor spending in the region totaled $8.0 billion in 2010.9 Based on

marketing effectiveness research by Longwoods International10

, 2009/2010

marketing spending of $4.3 million generated $432 million of incremental

visitor spending, which is equivalent to 5.4% of total visitor spending.

Depending on the economic structure of the local area being analyzed, and the

types of visitor spending typically being generated, it is also possible to estimate the

ROI in terms of state and local tax dollars generated per $1 of marketing spending.

In each of the studies that Tourism Economics analyzed that included such a

measure, the ROI was greater than $1, and was typically in the range of $5 of state

and local taxes per $1 of destination marketing spending.

6 Longwoods International (2012, December). Finger Lakes Wine Country 2012

Benchmark Study.

7 Tourism Economics, Longwoods International, and Reach Market Planning LLC.

(2013, August) Understanding the Visitor to Kansas City.

8 H2R Market Research (2013, October). KCCVA 2013 Advertising Effectiveness

Study.

9 Tourism Economics (2013, December). The Economic Impact of Travel and

Tourism in Pennsylvania, Tourism Satellite Account Calendar Year 2012.

10 US Travel Association and Longwoods International. (2011, July). The Power of

Destination Marketing, “Pure Michigan” and “Philadelphia: With Love” Case Studies.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

28

5.2 Case studies in which destination marketing spending was

reduced

Colorado

Colorado provides an example of the impact of a dramatic reduction in destination

marketing spending.

- Prior to 1993 the Colorado Tourism Board (CTB) had a $12 million

marketing budget, funded by a 0.2% tax on most tourism spend.

- Within two years of the 1993 repeal of funding, Colorado lost 30% of its US

visitor market share, which translated into the equivalent of over $1.4 billion

annually in lost revenues. By the late 1990s, this had escalated to $2.4

billion a year.

- After having moved from 14th to 1st position in the states’ summer resorts

category, Colorado slipped to 17th in 1994. It also shifted back to being

more of a regional drive destination opposed to being a national fly-in venue

and attracting fewer international visitors.

- The subsequent establishment of the Colorado Travel & Tourism Authority,

which was an attempt to market the state with private sector funding in co-

operation with the CTB, failed miserably. This was attributed to the fact that

private sector companies had separate priorities.

- The new Colorado Tourism Office opened with a $5 million budget and in

2003, $9 million was approved for tourism promotion. A campaign

conducted from October 2003 through December 2004 resulted in 5.3

million incremental visits (or 17% of total visitation to the state). In 2004, this

generated $1.4 billion of additional spend and $89.5 million in state and

local taxes.

- These estimates are equivalent to an implied visitor spending ROI per

marketing dollar of $140 (i.e. each dollar change in marketing spending

resulted in a change in visitor spending of $140).

San Diego

A series of events in San Diego recently resulted in a reduction in tourism marketing

spending, providing a case study for consideration. Tourism Economics has studied

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

29

the situation in San Diego and recently published a report quantifying the impact of

reduced marketing.11

- In recent years, the San Diego Tourism Marketing District (SDTDM) had a

budget ranging from $21 million to $27 million. As a result of litigation, funds

intended for the SDTDM were held in limbo starting January 1, 2013.

SDTDM funding in the second half of fiscal 2013 was reduced to a 61%

funding level, and at the point of Tourism Economics’ analysis, funding for

FY 2014 was anticipated to be 16% of what would normally be expected.

- As a result, over the course of FY 2013 and FY 2014, there was an

expected $30 million reduction in marketing activities relative to the level of

spending likely under normal funding conditions. The impact of the reduced

funding was reflected in the performance of the San Diego hotel industry, as

room demand leveled off in 2013, and occupancy rates and prices levels

increased more slowly than in competing markets. The city’s performance

trailed other regional and national destinations that maintained funding

levels and marketing programs.

- Tourism Economics analyzed the impacts of reduced marketing through two

independent methods and estimated the total amount of losses experienced

by San Diego’s hotel sector over 2013 and 2014 would sum to over $200

million in room revenues and 1.2 million room nights. In total, the impacts

were expected to result in a loss of total visitor spending of $560 million,

reduced city tax revenues of $22.3 million, and total reduced business sales

in the San Diego economy of $1.3 billion (including indirect and induced

impacts).

- These estimates are equivalent to a $19 decrease in visitor spending per

dollar of marketing spend (i.e. each dollar decrease in marketing spending

resulted in an expected reduction in visitor spending of $19).

5.3 Brand USA and the effectiveness of destination marketing

In addition to a role at the state and local level, destination marketing also plays an

important part in economic development strategy for countries around the world as

they seek to increase exports generated by international tourists. For the US, Brand

USA was established as the sole organization with the mandate to promote the

country globally to increase international visitation and spending in the US.

11 Tourism Economics (2013, November) The Impact of Reduced Funding for the

San Diego Tourism Marketing District.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

30

Oxford Economics, in coordination with its Tourism Economics subsidiary company,

recently conducted a detailed analysis of the return on investment of Brand USA’s

marketing in its 2013 fiscal year (October 1, 2012-September 30, 2013).12

Overall,

this analysis documented the impact of Brand USA in supporting incremental visits

to the US by international travelers, helping draw a more complete picture of the

effectiveness of destination marketing and the importance of international travel as a

growth market for US destinations.

- This analysis was based on an econometric model of how the eight markets

in which Brand USA was fully active would have performed without its

investments in marketing compared with actual performance. These

markets include Canada, Mexico, Japan, South Korea, the United Kingdom,

Germany, Brazil and Australia.

- The model indicated that Brand USA marketing generated 1.1 million

incremental trips to the United States—a 2.3% increase over the growth that

would have occurred without Brand USA’s activities.

- These incremental visitors spent $3.4 billion in the US, including both travel

and U.S. carrier airfare receipts. The results equate to a marketing ROI

equivalent to $47 dollars of incremental visitor spending per dollar of

marketing spending based on Brand USA’s marketing expenses of $72

million (a ratio of 47:1). The total budget ROI, including overhead ($9.6

million), startup expenses (e.g. new website development), and expenses

from partially deployed markets is estimated at 34:1.

- A parallel analysis was conducted to validate the model results based on

advertising tracking surveys conducted by Ipsos in Brazil and Mexico in

2013. With an average ROI of 49:1, these surveys confirm the range of

impact indicated by the econometric analysis.

- A secondary validation was conducted based on an analysis of US market

share for each of the eight markets where Brand USA’s marketing was fully

deployed. During fiscal year 2013, US market share of the key origin

markets increased 0.5 percentage points over FY 2012 against a

competitive set of destinations.

- Across the markets, a consistent trend of either an increase in share, or a

slowdown in the rate of share losses, is evident. This indicates a

strengthening of competitiveness that coincided with Brand USA’s

marketing investments, providing a confirmation of the returns indicated by

the econometric model.

12 Oxford Economics (2014, February) The Return on Investment of Brand USA

Marketing, 2013 Fiscal Year Analysis.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

31

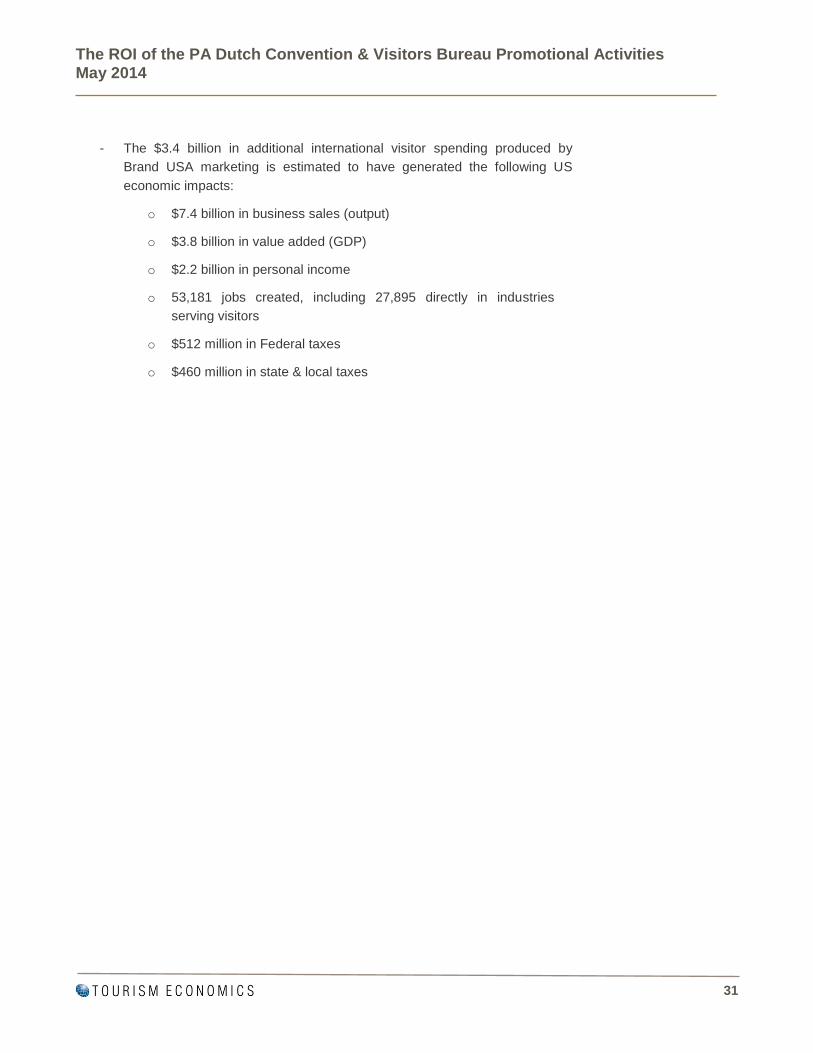

- The $3.4 billion in additional international visitor spending produced by

Brand USA marketing is estimated to have generated the following US

economic impacts:

o $7.4 billion in business sales (output)

o $3.8 billion in value added (GDP)

o $2.2 billion in personal income

o 53,181 jobs created, including 27,895 directly in industries

serving visitors

o $512 million in Federal taxes

o $460 million in state & local taxes

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

32

6. Economic Impact Analysis

6.1 Economic impact of travel and tourism in Lancaster County

As part of its analysis for the Commonwealth of Pennsylvania, Tourism Economics

analyzes the economic impact of travel and tourism in Lancaster County on an

annual basis.13

For the purpose of this analysis, Tourism Economics updated the

most recent calculation of 2012 impacts to provide a preliminary assessment of the

economic contribution of travel and tourism in Lancaster County in 2013, and

analyzed the portion of the impacts that represent the contribution of the ongoing

activities of the PDCVB.

Key points of background on economic impact

analysis of travel and tourism are summarized as

follows.

Travelers create direct economic value within

a discreet group of sectors (e.g. recreation,

transportation). This supports a relative

proportion of jobs, wages, taxes, and GDP

within each sector.

Each directly affected sector also purchases

goods and services as inputs (e.g. food

wholesalers, utilities) into production. These

impacts are called indirect impacts.

Lastly, the induced impact is generated when

employees whose incomes are generated

either directly or indirectly by tourism, spend

those incomes in the state economy.

Specific terms are used in the economic impact

analysis.

- Traveler: Includes both leisure and business travelers.

- Travel and tourism industry: The value of traveler activity within “travel

characteristic industries.” This concept measures only the direct impact of

the travel industry from the sales made to travelers.

13 Tourism Economics (2013, December). The Economic Impact of Travel and

Tourism in Pennsylvania, Tourism Satellite Account Calendar Year 2012.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

33

- Travel and tourism economy: This expands the focus to measure the

overall impact of tourism on all sectors of the economy. The value of

traveler activity plus government spending and capital investment in support

of travel and tourism and certain personal consumption expenditures. This

is the basis of the total economic impact analysis, including the direct impact

and the downstream indirect and induced impacts.

Tourism Economics used the IMPLAN modeling system, a well-respected economic

impact analysis tool, to quantify key relationships in the Lancaster County economy.

The IMPLAN model traces the flow of visitor-related expenditures through the local

economy and their effects on employment, wages, and taxes. IMPLAN also

quantifies the indirect (supplier) and induced (income) impacts of tourism. For

example, when a visitor purchases a meal at a local restaurant, a portion of the sale

supports wages for restaurant employees, while a portion of the sale may consist of

locally produced food and beverages. The IMPLAN model captures these types of

relationships based on a structured analysis of economic statistics. Tourism

Economics’ annual report for the Commonwealth provides further discussion of the

economic impact methodology.

Overall, Tourism Economics estimates that Lancaster County visitor spending

totaled $1.9 billion in 2013. For the purpose of this preliminary analysis of 2013

impacts, this represents an increase of 2.5% from the prior year, which is an

estimate generated by Tourism Economics using the annual increase in lodging

revenue as reported by STR as a proxy for overall spending growth. Based on

analysis of the number of visitors to the Dutch Country Roads region as part of the

annual analysis for the Commonwealth, Tourism Economics estimates there were

7.9 million visitors to Lancaster County in 2012, including day and overnight

visitors.14

Applying STR data that shows an increase in hotel room nights of 0.4%

during 2013, Tourism Economics estimates that 2013 visitor volume increased from

2012, but that the total still rounds to approximately 7.9 million visitors. Overall, the

average spend per visitor is estimated at $235, which includes some visitors who

stay one or more nights, as well as day visitors.

The estimated $1.9 billion of direct visitor spending, plus corresponding impacts of

more than $600 million of indirect and induced business sales, is estimated to have

supported $2.5 billion in total visitor-generated sales in Lancaster County. For

example, direct spending by visitors on food and beverages results in additional

demand in industries that supply the restaurants, such as food inputs, energy,

capital equipment and professional services such as legal and accounting services.

Additionally, induced impacts are produced as incomes earned through visitor

14 The definition of day visitors includes visitors who traveled outside of their normal

pattern to spend time in Lancaster County.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

34

spending are spent in Lancaster County. To a degree, such impacts tend to leak out

of the area in which the direct spending occurs, for example as local businesses

purchase inputs that are produced outside of Lancaster County. However, there are

also some tourism-related impacts that relate to spending by visitors to other

Pennsylvania counties but that accrue to businesses and households in Lancaster

County, and these are included.

This annual level of spending activity is estimated to support 23,694 total jobs in

Lancaster County, including 15,617 direct tourism industry jobs. Total employee

wages and other labor income are estimated at almost $755.9 million, including

$384.7 million of direct labor income.

Tourism Economics’ estimate of direct tourism

sector employment is also useful in considering

the importance of tourism in the Lancaster

County economy relative to other sectors. As

shown in the accompanying table, we have

summarized employment levels for sectors as

reported by the Bureau of Labor Statistics

(BLS), and consolidated our estimate of direct

tourism employment, moving direct tourism jobs

from the sector in which they were originally

reported to the tourism sector row. Based on

this analysis, tourism ranks as the fifth largest

employer in Lancaster County, ahead of mining

and construction. Overall, the tourism industry

directly accounts for 1 out of every 15 non-

agriculture private sector jobs in Lancaster

County. Several additional comments are also

relevant:

- This analysis shows employment as tracked using standard BLS categories,

adjusted to reclassify tourism sector employment as its own sector. For

example, this moves almost 8,500 tourism jobs from the accommodation

and food service sector to the tourism sector, leaving approximately 10,100

non-tourism food service and other accommodation jobs (e.g. dormitories).

- This analysis only includes direct tourism employment, and does not include

jobs in other sectors of the economy that are indirectly supported.

- Tourism is also important as an industry because it represents an “export

sector”, in which services are provided to visitors from other regions,

representing a source of revenue and income that can be spent on services

from local businesses, such as at local retail establishments.

- The ranking analysis is prepared using 2012 employment levels, the most

recent consistent basis for such a ranking. The 2013 analysis of the tourism

Rank Industry 20121 Manufacturing 36,100

2 Health Care and Social Assistance 35,200

3 Retail Trade 25,794

4 Professional and Business Services 21,700

5 Tourism 15,2396 Mining, Logging, and Construction 14,800

7 Wholesale Trade 12,900

8 Other Services 10,752

9 Food Services and Other Accommodations 10,054

10 Transportation and Utilities 8,597

11 Financial Activities 8,400

12 Arts, Entertainment, and Recreation 3,600

13 Educational Services 3,365

14 Information (e.g. publishing, telecom) 3,100

Source: Bureau of Labor Statistics, Tourism Economics

Private-Sector Employment Ranking

Lancaster County

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

35

sector shows 15,617 direct tourism jobs, up from approximately 15,239 in

2012.

The following recaps the 2013 economic impact of tourism in Lancaster County:

$2.5 billion in business sales (output), including $1.9 billion in direct

visitor spending

$755.9 million in labor income

23,694 jobs, including 15,617 directly in industries serving visitors

(one out of every 15 jobs)

$178.8 million in Federal taxes

$184.7 million in state and local taxes

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

36

6.2 Economic impact of PDCVB

To provide perspective, we have estimated the portion of the total tourism economy

impact that represents a contribution of PDCVB. For the purpose of this analysis, we

estimated that PDCVB contributed to approximately $120.9 million of the almost

$1.9 billion in total tourism direct sales in 2013. This estimate is based on the

assumption that PDCVB generates incremental visitor spending that represents a

similar order of magnitude marketing return as the average of $54 dollars of visitor

spending per dollar of marketing spending observed for metro and regional

destinations in the case studies. Based on financial information provided by PDCVB,

we calculated average annual PDCVB marketing spend of $2.2 million during the

last two years.15

Thus, we estimated that $2.2 million of annual marketing spending

supported approximately $120.9 million of annual visitor spending in 2013.

We considered several additional perspectives to assess the reasonability of the

estimated PDCVB contribution of $120.9 million in visitor spending, which is

equivalent to approximately 515,000 visitors (assuming spending per visitor of $235

consistent with the Lancaster County average). One was to consider a

representative “funnel” from a wide number of marketing and public relations

impressions, to a moderate set of interested “potential” travelers, and finally to a

more narrow set of visitors influenced by PDCVB marketing to visit Lancaster

County, to extend their stay, or to make additional purchases while visiting.

For example, at the marketing and public relations stage of the funnel, we

considered measures such as the number of audience impressions from media

coverage supported by PDCVB PR activity (2.0 billion audience impressions), out of

home advertising including billboards (42.6 million gross impressions), and

completed video views (3.3 million). At the next stage of the funnel, we considered

website visit activity as demonstrating interest by potential visitors (1.6 million

unique website visitors). Understandably, many of these PR and advertising

impressions and even website visits do not result in incremental visits to Lancaster

County, and as expected, the PDCVB contribution of spending equivalent to that of

515,000 visitors represents a small fraction of the aforementioned impression

metrics.

Secondly, we considered the aspects of PDCVB activities that extend beyond

marketing spending. For example, by maintaining its website and providing visitors

information through the Getaway Guide and visitor centers, PDCVB supports

15 Includes co-op advertising in 2012. We used a two-year average to reflect the

expectation that visitor spending depends on spending over time, not just the

current year.

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

37

opportunities for travelers to extend the length of their trip or experience a greater

range of area activities. This helps both with influencing the initial trip, and by

supporting reasons for repeat visits or word of mouth referrals. While difficult to

quantify directly, one can consider the incremental spending and return trip impacts

of the distribution of over 700,000 Getaway Guides, reception of over 100,000

visitors at visitor centers, and impressions through 750,000 opened emails.

Third, we considered the role of PDCVB in helping secure bookings for local hotels.

This includes sales activity of the PDCVB sales team (over 52,000 room nights

booked in 2013), and the reservation center (over 24,000 room nights booked).

Using an approximate average visitor spending per room night associated with

meetings and group business in the region of $250, the room nights sold by PDCVB

would represent approximately $13.1 million of visitor spending.

Fourth, we considered the estimated level of PDCVB contribution of $120.9 million

as representing 6.5% of total direct visitor spending in Lancaster County. This

compares to estimates based on marketing

effectiveness studies of 2.5% for the Kansas City

region, 5.4% for the Philadelphia region, and 11.7%

for the Finger Lakes Wine Country region as noted in

Destination marketing ROI matrix.

In aggregate, considering the activities of PDCVB as

we understand them, the KPI’s as reported by

PDCVB, and the level of marketing spend and the

impact of such marketing spend estimated in other

regional and metro-level markets, we believe the

estimate of PDCVB-contributed visitor spending of

$120.9 million is a reasonable estimate of the

PDCVB contribution. This estimate supports

economic impact calculations that set the return on

investment on PDCVB activities in the context of the

Lancaster County tourism economy and the broader

economy in the county.

Based on this analysis, Tourism Economics

estimates that PDCVB activities supported, on

average during 2013, approximately 1,554 total jobs

in Lancaster County, including 1,195 in the tourism

sector. These jobs generated approximately $42.8

million of wages and other labor income. PDCVB

activities supported an estimated $10.2 million of

state and local taxes, including a substantial level of

Lancaster County bed taxes. Overall, this

contribution in terms of visitor spending, jobs, and

state and local tax revenue represents a substantial

Lancaster

County

PDCVB

Contribution

In millions, except

employment

Tourism direct sales

Lodging $248.6

Food & beverage 383.5

Retail 377.2

Recreation 338.2

Transport 515.0

Total $1,862.5

Tourism industry

Direct sales $1,862.5 $120.9

Employment 15,617 1,195

Labor income $384.7 $28.3

Taxes

State and local $106.3 $7.9

Federal $88.8 $6.4

Total tourism economy

Business sales $2,482.2 $161.1

Employment 23,694 1,554

Labor income $755.9 $42.8

Taxes

State and local $184.7 $10.2

Federal $178.8 $9.7

Source: Tourism Economics

Economic Impact Analysis (2013)

Not separately

analyzed

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

38

return on the marketing spending coordinated through the PDCVB and supported by

the local tourism sector.

The following recaps the contribution of the PDCVB to the economic impact of

tourism in Lancaster County in 2013:

$161.1 million in business sales (output), including $120.9 million in direct

visitor spending

$42.8 million in labor income

1,554 jobs, including 1,195 directly in industries serving visitors

$9.7 million in Federal taxes

$10.2 million in state and local taxes

The ROI of the PA Dutch Convention & Visitors Bureau Promotional Activities May 2014

39

7. About Tourism Economics

Tourism Economics is an Oxford Economics company with a singular objective:

combine an understanding of tourism dynamics with rigorous economics in order to

answer the most important questions facing destinations, developers, and strategic