The Roadmap to an Electrified Car Market - lbma.org.uk 2017/S5_AB.pdf · The Roadmap to an...

30

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. The Roadmap to an Electrified Car Market How will Targets for the End of the Combustion Engine be Met? Al Bedwell, LMC Automotive LBMA/LPPM Precious Metals Conference Barcelona, October 16, 2017

Transcript of The Roadmap to an Electrified Car Market - lbma.org.uk 2017/S5_AB.pdf · The Roadmap to an...

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved.

The Roadmap to an Electrified Car Market How will Targets for the End of the Combustion Engine be Met?

Al Bedwell, LMC Automotive LBMA/LPPM Precious Metals Conference Barcelona, October 16, 2017

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 2

• European Electrification in a Global Context

• What’s Driving Change in Europe

• Update on Current Situation

• Outlook

• Wrapping Up

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 3

0

10

20

30

China Japan USA Europe

BEV xHEV1,154,000 Battery Electric Vehicle

% o

f N

ew C

ar &

US

Ligh

t Tr

uck

Sal

es

Source: LMC Automotive Global Hybrid & EV Forecast

Regional Electrification 2016 Passenger Car and US Light Truck Market

• BEVs in use were just 0.1% of pass cars & US light in 2016 (1mn of 1bn)

• After 10+ years of sales, only Japan has really embraced electrification

• China is unique due to 50% BEV share of electrified sales

World: Hybrid & EV Market 2016

440,000 512,000 500,000

All Hybrid Types

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 4

• European Electrification in a Global Context

• What’s Driving Change in Europe

• Update on Current Situation

• Outlook

• Wrapping Up

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 5

Europe • UK: 2040, no IC-only car sales; Oxford 2020?

• France: 2040, no IC car sales (?); Paris 2030

• Germany: No date; says UK/FR approach is ‘right’

• Norway: No ban, but sales by 2025 ‘should be ZEV’

• Austria, Denmark, Ireland, Netherlands, Portugal, Spain: EV targets

Elsewhere • India: 2030, all passenger cars to be battery electric (!?)

• Japan, Korea: No ban, EV targets set

• China: Studying timeline to IC ban

• US: No nationwide target, some states have EV targets

World: Targets for Removal of IC Vehicles

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 6

0%

1%

2%

3%

4%

5%

6%

40

60

80

100

120

140

160

180

20019

95

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

2018

201

9

202

0

202

1

202

2

202

3

202

4

2025

202

6

202

7

202

8

202

9

203

0

• CO2 fell less sharply in 2016: SUV boom & falling diesel share?

• Post-2021 target announcement may be imminent

Fle

et C

O2 (

gm/k

m)

YoY

CO

2 R

ed

uct

ion

Rat

e

Source: European Environment Agency, CCFA, JATO

118.1 (2016)

EU28 Passenger Car CO2 Emission Trend

95

50?

130

73?

annual achievement

YoY

CO2 achieved Annual change Target (set)

International comparison: China 2025 gm/km CO2: 93 US 2025 gm/km CO2: 100

super credits

Target (likely)

Europe: Update on CO2: Achievements & Targets

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 7

0

1

2

3

4

5

42

46

50

54

58

Au

g-1

2

No

v-1

2

Feb

-13

May

-13

Au

g-1

3

No

v-1

3

Feb

-14

May

-14

Au

g-1

4

No

v-1

4

Feb

-15

May

-15

Au

g-1

5

No

v-1

5

Feb

-16

May

-16

Au

g-1

6

No

v-1

6

Feb

-17

May

-17

Au

g-1

7

Max diesel >55%, now 43%

W. Europe Passenger Cars: Diesel versus Electrification

• Diesel decline started in 2011 but accelerated after the VW problems

• Much diesel is being substituted by gasoline, but also by HEV (not by BEV)

• Share of all electrified types reached 5.7% in July of this year

Die

sel %

of

New

Car

Sal

es

Source: National Sources

Hyb

rid

/EV

% o

f N

ew C

ar S

ale

s

VW dieselgate

BEV

xHEV

Diesel

Europe: A Move from Diesel to Electric?

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 8

Paris to phase out diesel cars

by 2024 Olympics 12/10/17

Madrid vows to ban diesel-

fuelled cars by 2025 2/12/16

Europe: The Pressure on Diesel Keeps Building

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 9

30

35

40

45

50

55

60

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Diesel Market Evolution: W. Europe Cars, Base Case

Great Recession, scrappage incentives

• Nervousness about investing in diesel is growing (for OEM and car buyer)

• But core strengths of diesel mean it will endure at least in some segments

Die

sel %

of

New

Car

Sal

es

Source: LMC Automotive European LV Diesel Forecast. Includes DHEV 32.6%

RDE, Increasing after-treatment costs

Substitution by gasoline MHEV, pre-EU6 city bans

Urban diesel- free zones?

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

6.45 6.85 6.91 6.43 6.02 5.89 5.72 5.38 5.24 5.13 4.89

Better gasoline engines, worse fiscal situation for diesel

Dieselgate, image problems, falling residuals

Europe: More Pain for the Diesel Car Market

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 10

0

5

10

15

20

25

30

35

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

W. Europe Passenger Cars: Share of SUV/Crossovers

• The shift to crossover types seems relentless and has an impact on CO2

• Example: Kia Stonic 1.4 gas MT has FE/CO2 10% worse than Rio 1.4L MT

SUV

% o

f N

ew C

ar S

ale

s

Source: LMC Automotive

Europe: Those Pesky Car Buyers Keep Choosing SUVs

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 11

• European Electrification in a Global Context

• What’s Driving Change in Europe

• Update on Current Situation

• Outlook

• Wrapping Up

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 12

-20

0

20

40

60

80

100

120

140

160

180

0

1

2

3

4

5

6

7BEV EREV FCEV FHEV MHEV PHEV

• Share reached a new peak in recent times on strong FHEV demand

• But for most car buyers the plug-in offer simply isn’t compelling (yet)

Source: LMC Automotive Global Hybrid & EV Forecast

5-year Monthly Hybrid & EV Share

Sales pulled forward W. Europe Passenger Car Market

Ele

ctri

fie

d %

of

New

Car

Sal

es

An

nu

alis

ed

Mo

nth

ly G

row

th (

%)

YoY (right axis)

Europe: Hybrid & EV Market - Share

5.7%

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 13

0

1

2

3

4

5

6

7

8

9

10

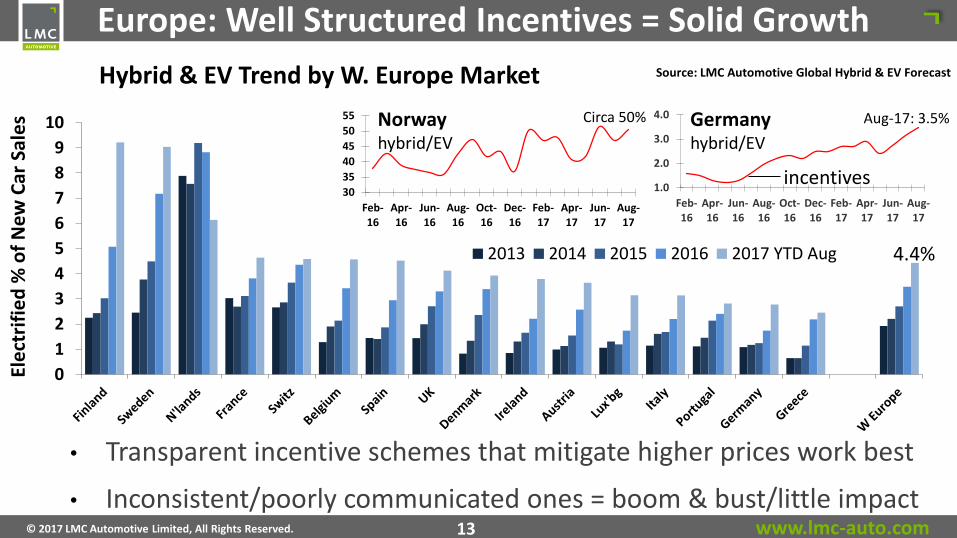

2013 2014 2015 2016 2017 YTD Aug

30

35

40

45

50

55

Feb-16

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

Jun-17

Aug-17

• Transparent incentive schemes that mitigate higher prices work best

• Inconsistent/poorly communicated ones = boom & bust/little impact

Ele

ctri

fie

d %

of

New

Car

Sal

es

Source: LMC Automotive Global Hybrid & EV Forecast

Norway hybrid/EV

Circa 50%

4.4%

1.0

2.0

3.0

4.0

Feb-16

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

Jun-17

Aug-17

Germany hybrid/EV

Hybrid & EV Trend by W. Europe Market

Aug-17: 3.5%

incentives

Europe: Well Structured Incentives = Solid Growth

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 14

0

10

20

30

40

50

60

70

80

non plug-in plug-in

• SP + IT: Weak infrastructure, unstable incentives = low plug-in sales

• Norway’s big incentives lead, but only ZEV schemes will endure

Ele

ctri

fie

d N

ew C

ar S

ale

s (‘

00

0s)

Source: LMC Automotive Global Hybrid & EV Forecast

Electrified Sales by Market & Macro-Type, YTD Aug 2017

Europe: Support for Plug-ins Varies Hugely

Strong support

Weak support

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 15

0

1

2

3

4

5

6

7

Hyundai BMW Geely R-N Daimler VW PSA Honda Tata Ford

2016h1 2017h1

• Hyundai has hits with the Niro & Ioniq (but hard to make money)

• VW has seen its electrified share fall further this year

Ele

ctri

fie

d %

of

New

Car

Sal

es

Source: LMC Automotive Global Hybrid & EV Forecast

Hybrid & EV Trend by OEM, W. Europe Car Sales

0

20

40

60

ToyotaEle

ctri

fie

d %

of

Ne

w C

ar S

ale

s

Europe: OEM Hybrid & EV Profile has a Big Range

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 16

Europe: Few new BEVs, but Current ones Improving

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 17

• European Electrification in a Global Context

• What’s Driving Change in Europe

• Update on Current Situation

• Outlook

• Wrapping Up

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 18

Europe: OEMs are Racing to Meet Expected Demand

OEM Strategy Overview HEV + BEV BEV

BMW group 15-25% of sales electrified by 2025. Mix of standalone & bespoke BEVs ?? 12 by 2025

Daimler Electrified versions of all M-B range by 2022, Smart all BEV 'at some point' 50 by 2022 >10 by 2022

FCA Half of FCA fleet electrified by 2022 50% by 2022 ??

Ford 13 new electrified vehicles globally in next 5 years 13 by 2022 1st dedicated BEV 2020

Hyundai-Kia Electrify core models, plus standalone BEVs 31 by 2020 8 by 2020

JLR New models all hybrid or EV from 2020 At least 1 by 2020

PSA Electrify core models, no standalone BEVs 11 by 2023 4 by 2023

R-N New common electrified electrified platforms 12 ZEV by 2022

Toyota Hybrid remains core tech, BEV mass production from 2020 Several by 2020

Volvo All new models hybrid or EV from 2019, no IC-only by circa 2024 5 by 2021

VW At least 1 electrified version of all models by 2030 80 by 2025 50 by 2025

Minimum 100 new BEVs by 2025

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 19

Europe: ….and so are Others

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 20

0

100

200

300

400

500

600

700

140

180

220

260

300

340

380

420

460

500claimed

real world

0

100

200

300

400

500

600 all

fast

e-R

ange

(km

)

e-Range: average max e-Range of mass-market EV

• Claimed range of mass market cars rose by average 40% for 2017MY

• Battery pack wholesale cost is reckoned to be circa $200/kWh in 2017

• Battery cost dropped 80% over 6 years, $100/kWh possible by 2020?

• Charge point infrastructure problems include investment & grid issues

390km

430Km

Typical BEV battery pack cost ($/kWh)

W. Europe public charge points (‘000s)

640

70 Ch

arge

rs (

‘00

0s)

Bat

tery

pac

k ($

/kW

h)

lift-off?

lift-off?

lift-off?

Europe: Evolution of Key BEV Enablers

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 21

0

10

20

30

40

50

60

2015 2018 2021 2024 2027

BEV EREV FCEV FHEV MHEV PHEV PFCEV MHEV (48V)

% o

f C

ar S

ale

s

Source: LMC Automotive Global Hybrid & EV Forecast

Outlook for Electrification by Technology Europe + CIS Passenger Cars 12.4mn sales

60%!

• New generation hybrids start to achieve real volume from 2018

• BEVs accelerate from mid-2020s, reaching 15% of market by 2027

• Fuel cells remain niche over this time period

Europe: Hybrid & EV Base Case Forecast (July 2017)

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 22

0

10

20

30

40

50

60

70

80

90

100W. Europe Car Market

IC-only (gasoline)

• IC-only disappears well before 2040!

• FCEV gets in to the picture

% o

f N

ew C

ar S

ale

s

Source: LMC Automotive Forecast

28%

IC-only (diesel)

BEV

PHEV

MHEV+FHEV

FCEV

5%

50%

15% 0% IC-only (CNG/LPG)

MHEV(48V)

2%

Europe: 50-Year Fuel & Technology Picture

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 23

• Europe Electrification in a Global Context

• What’s Driving Change in Europe

• Update on Current Situation

• Outlook

• Wrapping Up

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 24

Source: LMC Automotive

0

1

2

3

4

5

62

01

4

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

BEV car sales (mn)

Jan-17 8%

Jul-17 16%

0.0

0.5

1.0

1.5

2.0

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

PHEV car sales (mn) Jan-17 5.6%

Jul-17 3.9%

• NEV ‘cap and trade’ scheme will be introduced from 2019 after a 1 year delay

• OEMs will have to achieve a NEV score of 10 points in 2019, 12 in 2020

• OEMS selling at least 30,000 cars will have to comply, buy credits or face fines

China: NEV Quotas will Push Global EV Spend

LMC Automotive China NEV Forecast Revisions

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 25

BMW, 15k/Y

Mercedes, 8k/Y

Changan, 80k/Y

SAIC, 140k/Y

BYD: 250k/Y

China OEM: • Geely • BYD • BAIC • SAIC • JAC & JMC

GAC: 140k/Y

Toyota: 15k/Y

Geely, 200k/Y Lynk, 15k/Y Volvo, 15k/Y Global OEM:

• VW • GM • Renault-Nissan • Volvo • Mercedes-Benz & BMW

VW, 15k/Y

VW, 50k/Y

GM, 50k/Y

Hyundai, 15k/Y

BAIC, 240K/Y

Toyota: 8k/Y

• Traditional giants continue to lead the market, and occupy more than 90% market share • China OEM vs. Global OEM

China: NEV - Traditional OEMs

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 26

Shijiazhuang: Chery, ¥3 (Bn.), ? k/Y

Hangzhou: Wanxiang, ¥2.75 (Bn.), 50k/Y

Beijing: BJ EV, ¥1.15 (Bn.), 20k/Y

Tianjin: NEVS, ¥4.27(Bn.), 50k/Y

Sanmenxia: Suda, ¥2.65 (Bn.), 100k/Y

Qingdao: BJ EV, ¥1.15 (Bn.), 50k/Y

Chongqing: Jinkang, ¥2.51(Bn.), 50k/Y

Wuhu: Chery, ¥2.05 (Bn.), 85k/Y

Suzhou: Qiantu, ¥2.02 (Bn.), 50k/Y

Changzhou: BJ EV, ¥10(Bn.), 400k/Y

Huai’an: Min’an, ¥2.50 (Bn.), 50k/Y

Hangzhou: Changjiang, ¥0.80 (Bn.), 50k/Y

Jiaxing: Hozon, ¥0.97 (Bn.), 50k/Y

Nanchang: Jiangling, ¥1.33 (Bn.), 50k/Y

Putian: Yudo, ¥1.89 (Bn.), 65k/Y

Lanzhou: Zhidou, ¥0.89(Bn.), 40k/Y

Jiujiang: BJ EV, ¥14.0 (Bn.), 10k/Y

- In construction or in planning

China: NEV - New Players (Qualified)

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 27

Wuhan: NextEV, ¥30 (Bn.), 200k/Y

Zhaoqing: Xpeng, ¥10 (Bn.), 10k/Y

Wuhu: Zhiche, ¥3 (Bn.), 100k/Y

Nanjing: FMC, ¥11.6 (Bn.), 300k/Y

Changzhou: Chehejia, ¥5(Bn.), 300k/Y

Nanjing: Bordrin, ¥10 (Bn.), 100k/Y

Wenzhou: VM Motor, ¥6.7 (Bn.), 200k/Y

Huzhou: Youxia, ¥11.5 (Bn.), 200k/Y

Deqing: LeSee, ¥20 (Bn.), 400k/Y

Ganzhou: Sinomach, ¥8.0 (Bn.), 100k/Y

Shangrao: AICEV, ¥13.3 (Bn.), 150k/Y

Wuxi: Yogomo, ¥3(Bn.), 150k/Y

Jinhua: Leap Motor, ¥2.5 (Bn.), 50k/Y

China: NEV - New Players (Applying)

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 28

0

10

20

30

40

2015 2018 2021 2024 2027

BEV EREV FCEV FHEV MHEV PHEV PFCEV MHEV (48V)

% o

f C

ar +

US

LT S

ale

s

Source: LMC Automotive Global Hybrid & EV Forecast

Outlook for Electrification by Technology World Passenger Cars & US Light Trucks

36.3mn sales 35.0%

• Mild hybrid with 48V becomes the leading electrified technology

• 10% of global car sales are BEV in 2027: 10mn vehicles

• We think FCEV is coming but remains is a technology for the 2030s

World: Hybrid & EV Base Case Forecast (July 2017)

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 29

Expectation Risk

Battery EVs will be a viable mass market alternative to conventional IC by mid- next decade

MH

EV

PH

EV

BEV

s Wrapping Up

New generation gasoline mild hybrids with 48V will proliferate, plugging the CO2 gap left by declining diesel

BEV cost reduction, incentive taper & worse WLTP rating result in PHEV losing out to true ZEV solutions

Ener

gy

Charging infrastructure does not roll out as expected – home charging will dominate, but public network needed

There are still some cost questions to be answered but pressure to find solutions may override these

Incentives support PHEV to a greater degree than expected, cost of PHEV falls faster than anticipated

Policy does not support this – green levies and feed-in tariffs to support transition phase are withdrawn

Cost of renewable energy continues to fall significantly, enabling low well-to-wheel emissions and ultimately FCEV

For any further questions, please contact: [email protected]

www.lmc-auto.com © 2017 LMC Automotive Limited, All Rights Reserved. 30

Focused › Smart Responsive Flexible › ›