The Rise of the Asian Giants: China and India compared Martin Wolf, Associate Editor & Chief...

44

The Rise of the Asian Giants: China and India compared Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times Leverhulme Centre for Research on Globalisation and School of Economics, Nottingham University March 15 th , 2007

-

Upload

phoebe-hudson -

Category

Documents

-

view

216 -

download

0

Transcript of The Rise of the Asian Giants: China and India compared Martin Wolf, Associate Editor & Chief...

The Rise of the Asian Giants: China and India comparedMartin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Leverhulme Centre for Research on Globalisationand School of Economics, Nottingham University

March 15th, 2007

2

China and India

“Let China sleep, for when she wakes, she will shake the world.” Napoleon Bonaparte

3

China and India

“China will again become a viable great power; India may become a great democracy.” Lord Meghnad Desai

4

China and India

• Potential

• Priorities

• Performance

• Prospects

5

1. Potential

• Asia’s rise is the third great transformation since the industrial revolution:

– Early 19th century: rise of the UK

– Late 19th and early 20th centuries: rise of US, Japan and Germany and Russia

– Post-second world war: from Japan’s surge to the rise of China and India

• East and south Asia contain more than half of humanity

• This is surely the end of the era of European dominance

6

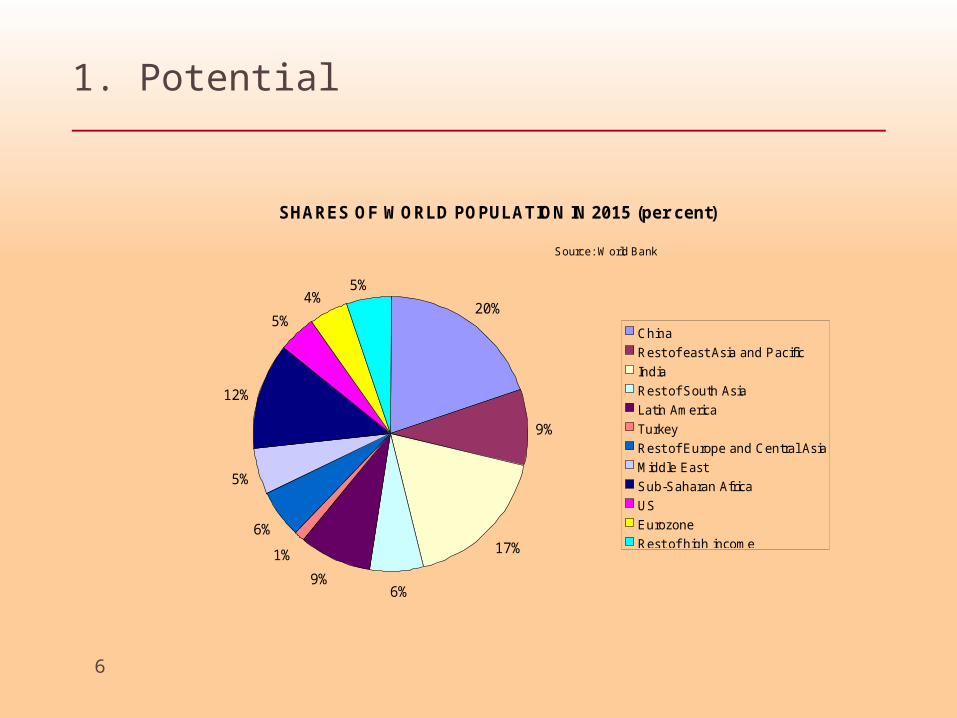

1. Potential

SHARES OF WORLD POPULATION IN 2015 (per cent)

20%

9%

17%

6%9%

1%

6%

5%

12%

5%

4%5%

China

Rest of east Asia and Pacific

India

Rest of South Asia

Latin America

Turkey

Rest of Europe and Central Asia

Middle East

Sub-Saharan Africa

US

Eurozone

Rest of high income

Source: World Bank

7

1. Potential

SHARES OF THE ASIAN GIANTS IN WORLD PRODUCT(per cent, at PPP)

22 23

33 33 3225 24

20 18

9

16 19

2522

2121

43

2

33 4

8

87

22

33

17

11 9 5 5 1115

24

1612 9 7

4 35 6

0

10

20

30

40

50

60

70

80

90

1700 1820 1870 1900 1913 1957 1973 1995 2003

EU-15 United States Japan China India

8

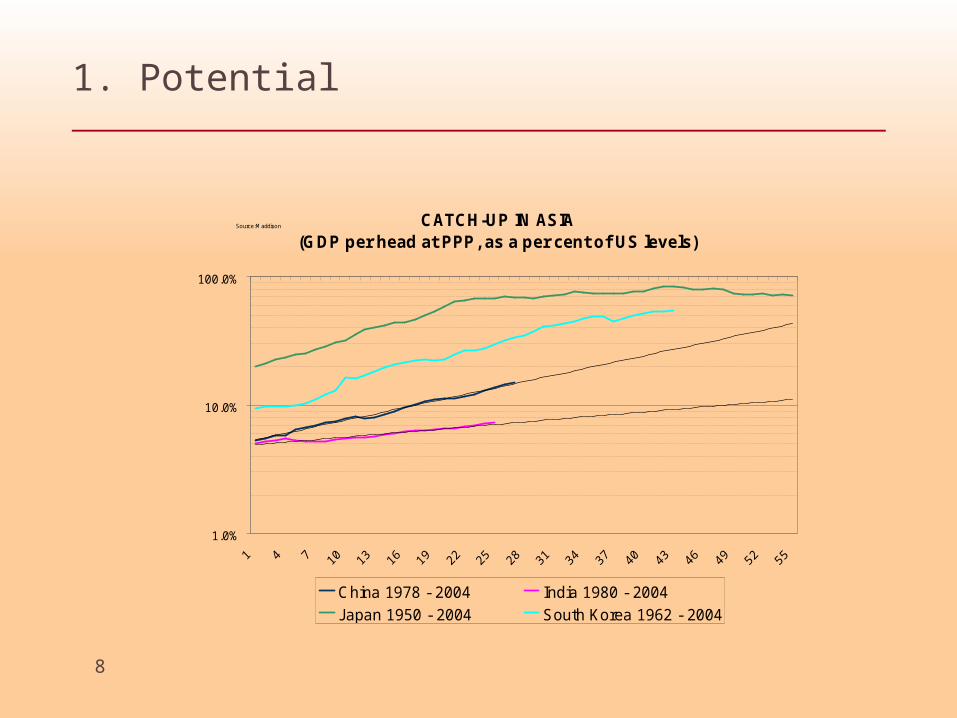

1. Potential

CATCH-UP IN ASIA(GDP per head at PPP, as a per cent of US levels)

1.0%

10.0%

100.0%

China 1978 - 2004 India 1980 - 2004

Japan 1950 - 2004 South Korea 1962 - 2004

Source: Maddison

9

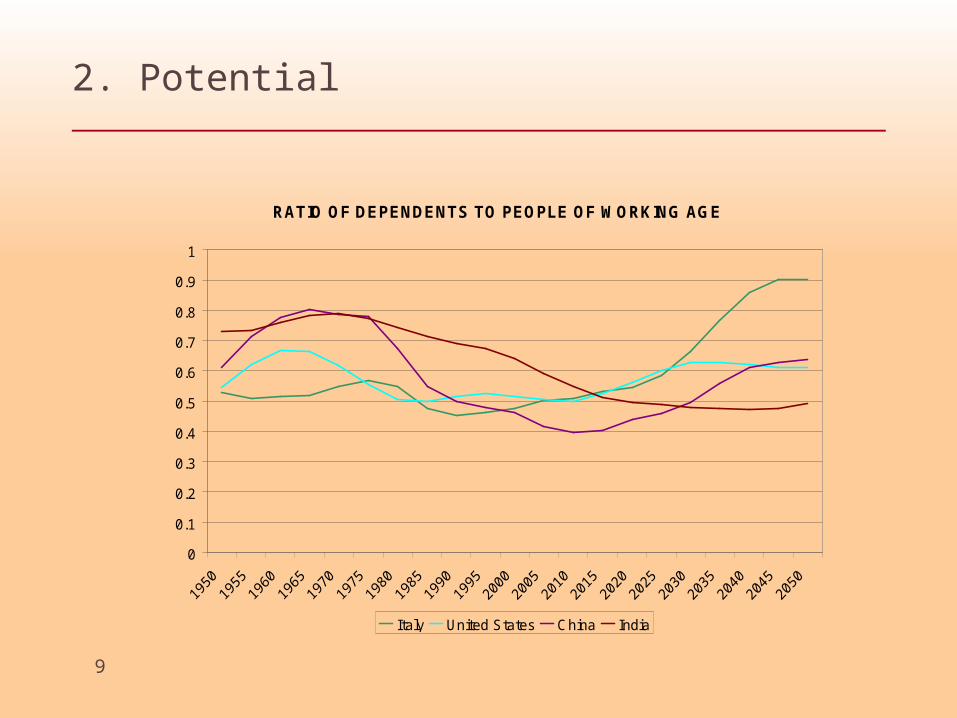

2. Potential

RATIO OF DEPENDENTS TO PEOPLE OF WORKING AGE

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Italy United States China India

10

1. Priorities

• The two countries are both enormous and homes to ancient and sophisticated civilisations.

• But they are also fundamentally different:

– China has been unified for at least half of the last 2,000 years, while India was never brought fully under a single centralised system of government.

– India was conquered by foreigners who brought their culture with them; China’s were “sinicised”.

11

1. Priorities

– China’s had an imperial system; India had dynasties.

– Chinese imperial dynasties endured; India’s were brief.

– China’s is an integrated society; India’s is pluralistic.

– China’s historic source of stability was political; India’s was social.

12

1. Priorities

• These differences help explain a number of contrasts between today’s China and India:

– China’s meritocracy; and India’s policy of reservations

– China’s ability to mobilise resources; and India’s weaker public sector

– China’s bureaucratic authoritarianism; and India’s democracy.

– Chinese elites think democracy is inefficient; without democracy, there would be no India.

• These differences also are reflected in growth strategy and performance.

13

1. Priorities

• China’s growth strategy is a hybrid:

– Like Japan and South Korea in the past, it relies on:

• Industrialisation through very high savings and investment; and;

• Trade as an engine of growth;

– But China is far more open to trade and foreign direct investment than its smaller predecessors; and so

– China is a vast combination of South Korea and Hong Kong.

14

1. Priorities

• China’s state plays a central role in development:

– As mobiliser of resources;

– As investor;

– As manager of political consequences.

• China’s aim is “development without political upheaval”.

15

1. Priorities

• India’s growth strategy has been unique:

– Growth without industrialisation;

– Driven by skill-intensive services;

– With low formal sector employment;

– Tyranny of interest groups;

– And relatively low trade and foreign investment.

• India’s aim is “growth without social upheaval”.

16

3. Performance

• Overview

• Openness

• Growth

• Contributions to growth

17

3. Performance: overview

Units China IndiaPopulation(2004) millions 1,296 1,080GNI (PPP) $bn $7,634 $3,369GDP per head growth 1970-2004 8.4% 3.4%GDP per head growth 1990-2004 8.9% 4.0%Share of industry in GDP 2004 46.0% 27.0%

ECONOMIC

Source: World Bank, World Development Indicators 2006 , UNDP, Human Development Report 2006

18

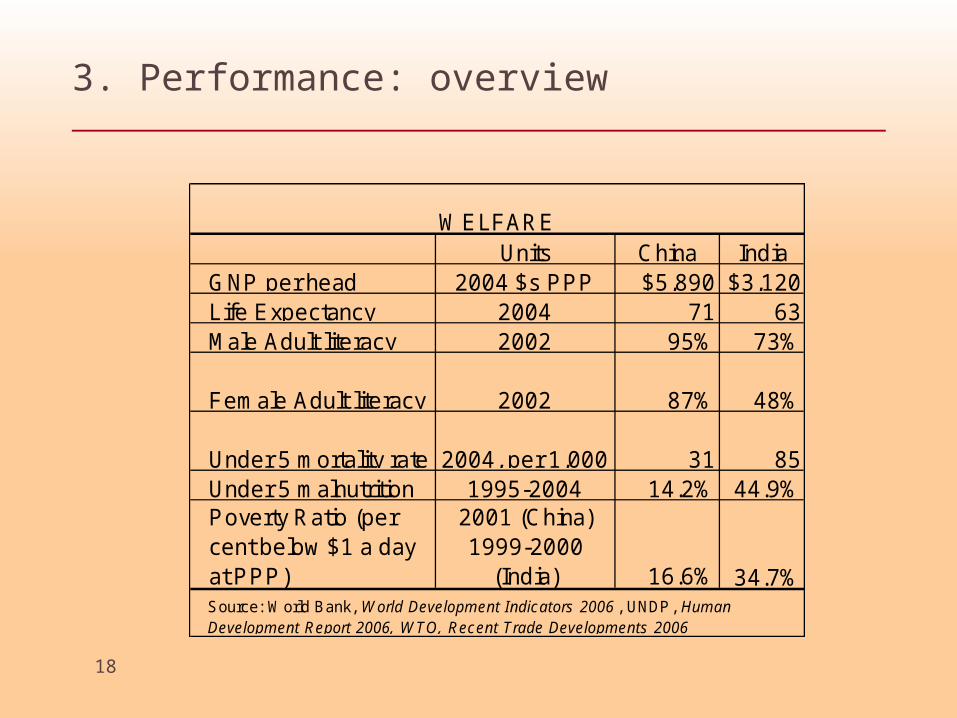

3. Performance: overview

Units China IndiaGNP per head 2004 $s PPP $5,890 $3,120Life Expectancy 2004 71 63Male Adult literacy 2002 95% 73%

Female Adult literacy 2002 87% 48%

Under 5 mortality rate 2004, per 1,000 31 85Under 5 malnutrition 1995-2004 14.2% 44.9%Poverty Ratio (per cent below $1 a day at PPP)

2001 (China) 1999-2000

(India) 16.6% 34.7%

WELFARE

Source: World Bank, World Development Indicators 2006 , UNDP, Human Development Report 2006, WTO, Recent Trade Developments 2006

19

3. Performance: overview

Units China India

Electricity Production KWHbn 2003 1,907 633Goods Hauled (railways)

2000-04 ton-km bn 1,829 381

Container traffic (ports)

2004 TEU million 75 4

Air freight2004 ton-km

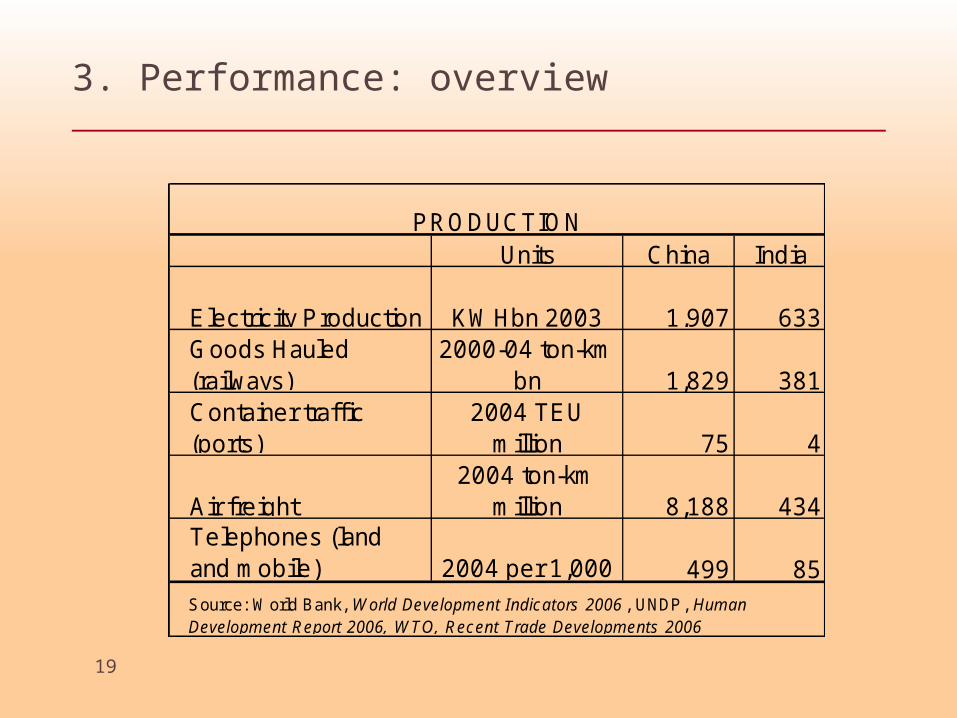

million 8,188 434Telephones (land and mobile) 2004 per 1,000 499 85Source: World Bank, World Development Indicators 2006 , UNDP, Human Development Report 2006, WTO, Recent Trade Developments 2006

PRODUCTION

20

3. Performance: overview

Units China India

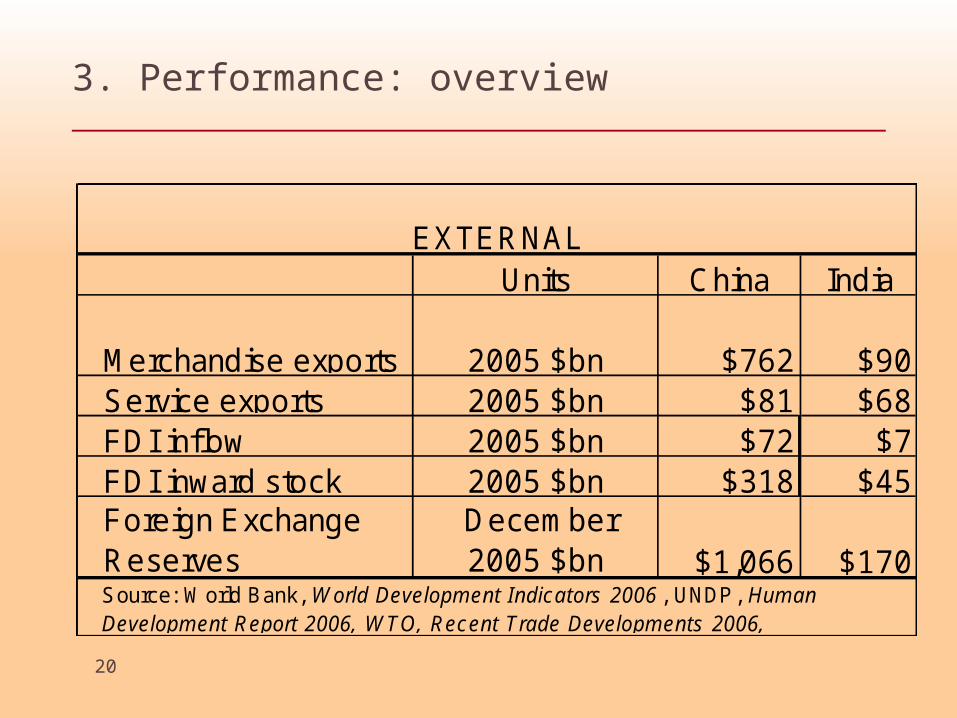

Merchandise exports 2005 $bn $762 $90Service exports 2005 $bn $81 $68FDI inflow 2005 $bn $72 $7FDI inward stock 2005 $bn $318 $45Foreign Exchange Reserves

December 2005 $bn $1,066 $170

Source: World Bank, World Development Indicators 2006 , UNDP, Human Development Report 2006, WTO, Recent Trade Developments 2006,

EXTERNAL

21

3. Performance: openness

TARIFF RATES IN 2004

9.6%

6.0%

9.6%

6.2%

9.5%

5.8%

28.1% 28.0%29.0%

36.9%

27.8%

25.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Simple mean Weighted mean Simple mean Weighted mean Simple mean Weighted mean

All Primary Manufactures

China India

Source: World Bank, World Development Indicators

22

3. Performance: openness

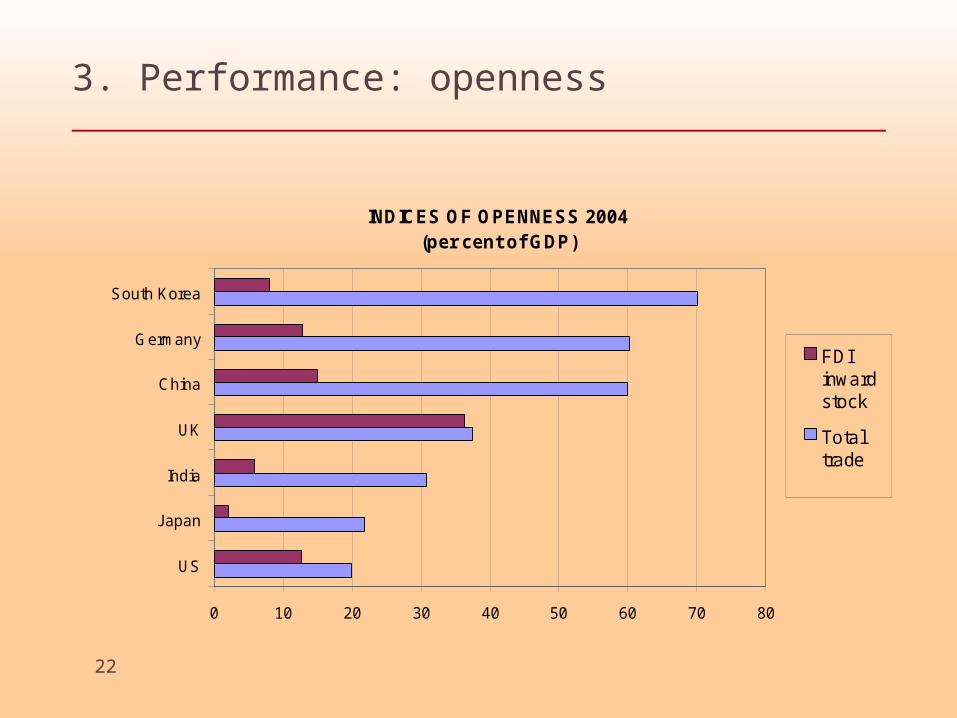

INDICES OF OPENNESS 2004(per cent of GDP)

0 10 20 30 40 50 60 70 80

US

Japan

India

UK

China

Germany

South Korea

FDIinwardstock

Totaltrade

23

3. Performance: openness

MERCHANDISE EXPORTS OVER GDP(per cent)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

China India

24

3. Performance: openness

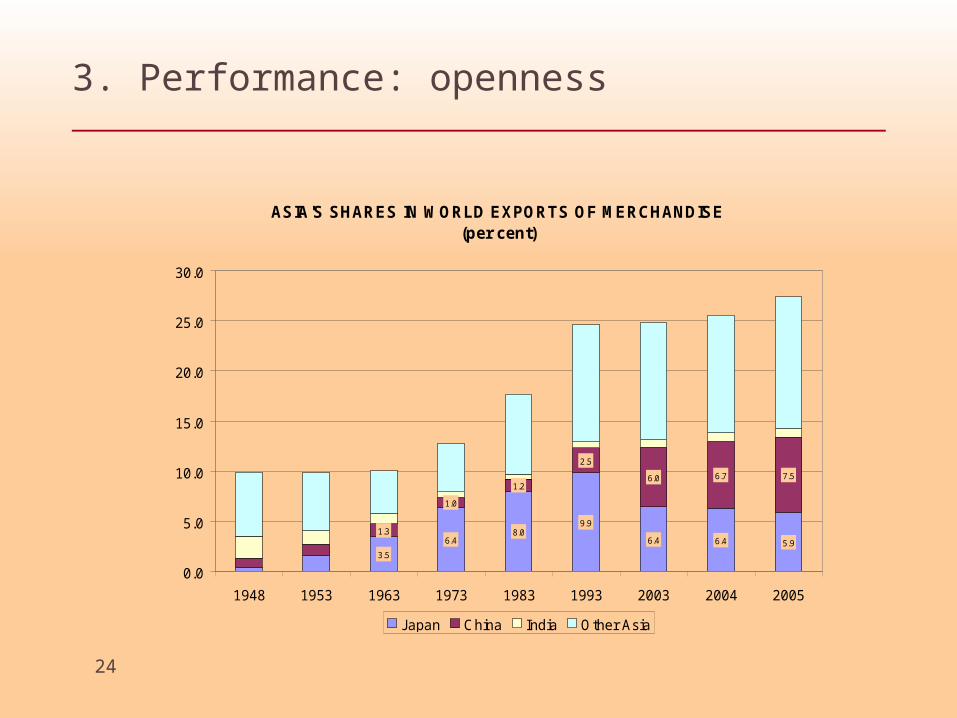

ASIA'S SHARES IN WORLD EXPORTS OF MERCHANDISE(per cent)

3.5

6.48.0

9.9

6.4 6.4 5.91.3

1.0

1.2

2.5

6.0 6.7 7.5

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1948 1953 1963 1973 1983 1993 2003 2004 2005

Japan China India Other Asia

25

3. Performance: openness

MERCHANDISE EXPORTS OF LEADING COUNTRIES($m, previous 12 months)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

Jan-

98

May

-98

Sep-9

8

Jan-

99

May

-99

Sep-9

9

Jan-

00

May

-00

Sep-0

0

Jan-

01

May

-01

Sep-0

1

Jan-

02

May

-02

Sep-0

2

Jan-

03

May

-03

Sep-0

3

Jan-

04

May

-04

Sep-0

4

Jan-

05

May

-05

Sep-0

5

Jan-

06

May

-06

Sep-0

6

China India US Japan Germany

26

3. Performance: openness

CURRENT ACCOUNT BALANCE(as per cent of GDP)

-6

-4

-2

0

2

4

6

8

10

China India

27

3. Performance: growth

A TALE OF TWO ASIAN GIANTS(GDP per head, at PPP)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

China IndiaSource: Maddison, IMF, World Economic Outlook

28

3. Performance: growth

GROWTH OF GDP IN INDIA AND CHINA(per cent)

0

2

4

6

8

10

12

14

16

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

China India

Source: EIU

29

3. Performance: growth

GROWTH OF GDP IN INDIA AND CHINA(5-year moving averages per cent)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

China India

Source: EIU

30

3. Performance: growth

STRUCTURE OF GROWTH COMPARED, 1990-2000(per cent a year)

10.4%

4.1%

13.7%

10.2%

6.0%

3.0%

6.3%

8.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

GDP Agriculture Industry Services

China India

Source: World Bank

31

3. Performance: growth

STRUCTURE OF GROWTH COMPARED 2000-04(per cent a year)

9.4%

3.4%

10.6%

9.8%

6.2%

2.0%

6.2%

8.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

GDP Agriculture Industry Services

China India

32

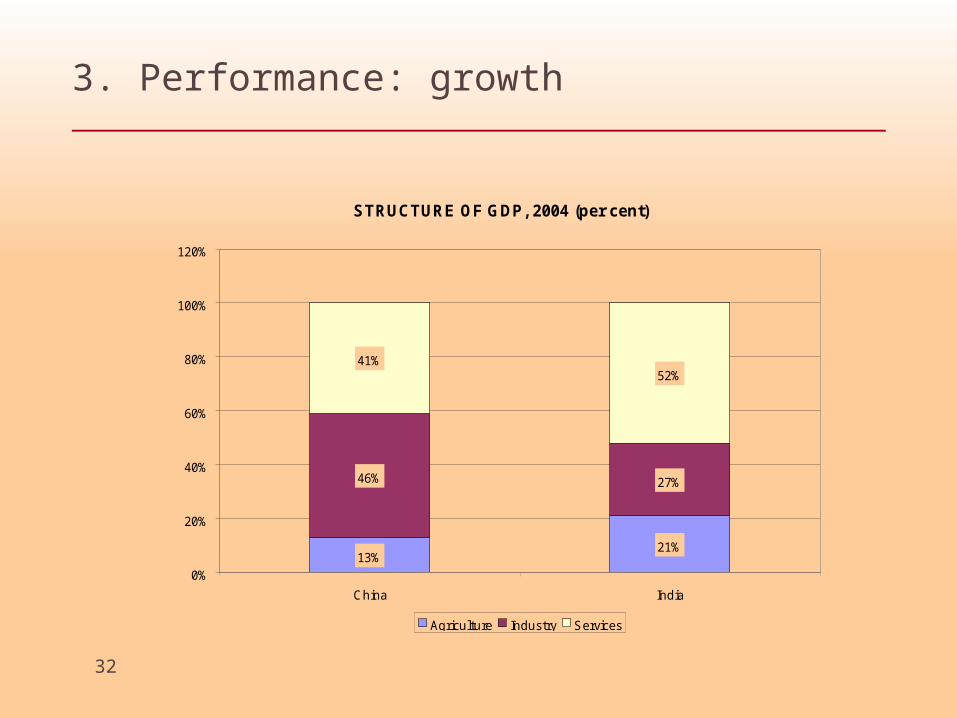

3. Performance: growth

STRUCTURE OF GDP, 2004 (per cent)

13%21%

46% 27%

41%52%

0%

20%

40%

60%

80%

100%

120%

China India

Agriculture Industry Services

33

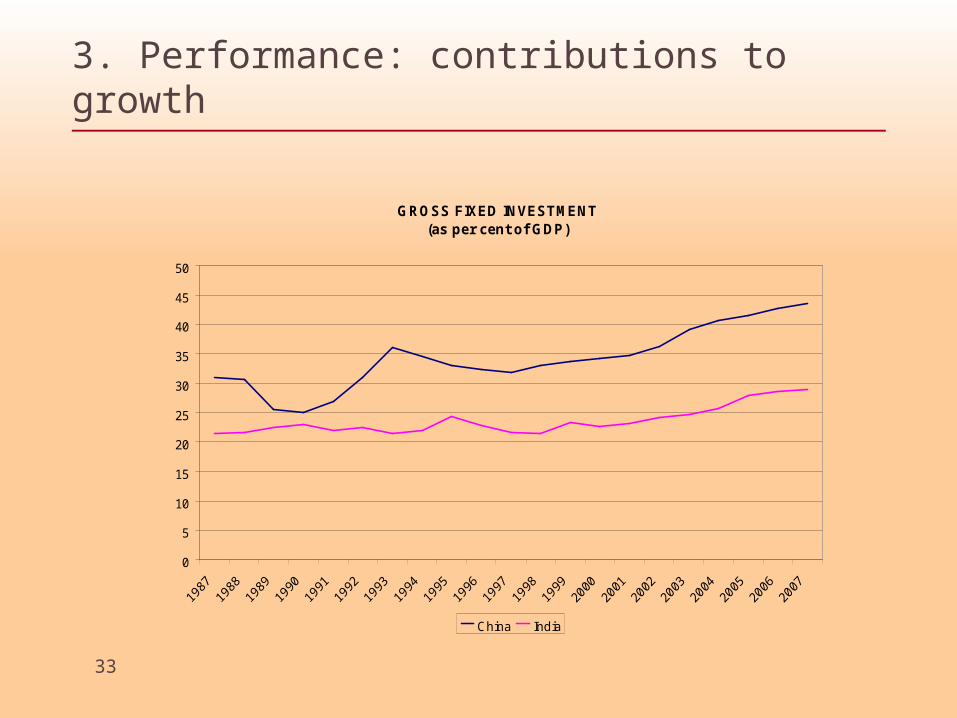

3. Performance: contributions to growth

GROSS FIXED INVESTMENT(as per cent of GDP)

0

5

10

15

20

25

30

35

40

45

50

China India

34

3. Performance: contributions to growth

DECOMPOSITION OF GROWTH, 1993-2004(percentage points)

1.2%1.9%

8.5%

4.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

China India

Employment Output per worker

Source: Barry Bosworth and Susan Collins, "Accounting for Growth: Comparing China and India", January 2007

35

3. Performance: contributions to growth

GROWTH OF TOTAL FACTOR PRODUCTIVITY (percentage points)

3.8%3.6%

4.0%

1.6%

1.1%

2.3%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

1978-2004 1978-93 1993-2004

China India

Source: Barry Bosworth and Susan Collins, "Accounting for Growth: Comparing China and India", January 2007

36

3. Performance: contributions to growth

CONTRIBUTIONS TO GROWTH OF OUTPUT PER WORKER,1993-2004 (percentage points)

4.2%

1.8%

4.0%

2.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

China India

Physical Capital Factor Productivity

Source: Barry Bosworth and Susan Collins, "Accounting for Growth: Comparing China and India", January 2007

37

3. Performance: contributions to growth

CONTRIBUTIONS TO GROWTH IN OUTPUT PER WORKER IN AGRICULTURE (1993-2004, percentage points)

2.1%

0.7%

1.8%

0.5%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

China India

Physical Capital Land Education Factor Productivity

Source: Barry Bosworth and Susan Collins, Accounting for Growth: Comparing China and India

38

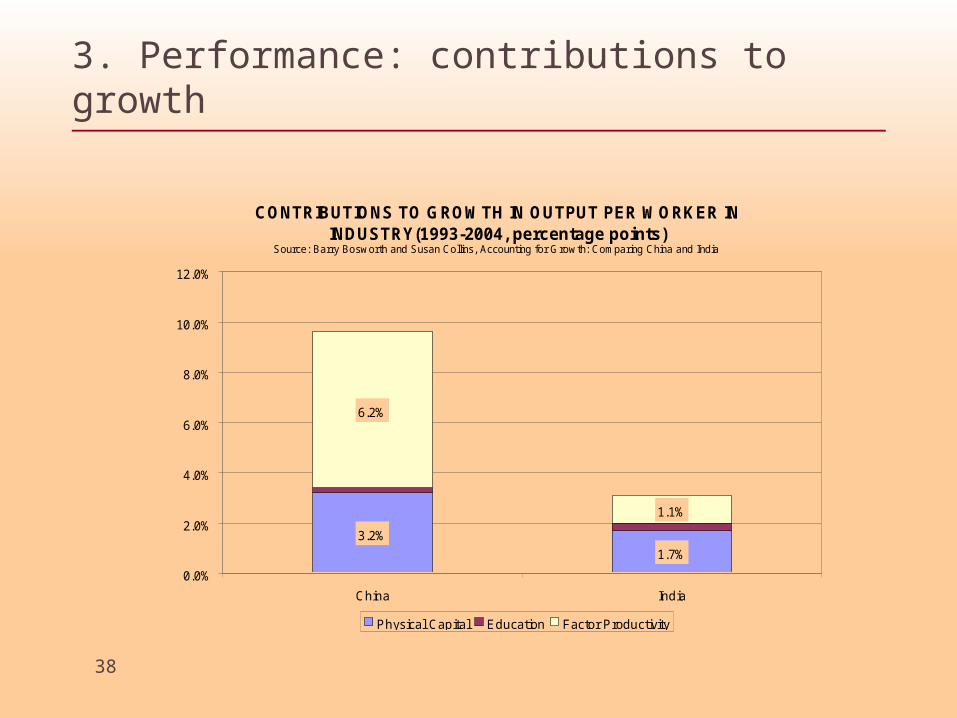

3. Performance: contributions to growth

CONTRIBUTIONS TO GROWTH IN OUTPUT PER WORKER IN INDUSTRY(1993-2004, percentage points)

3.2%

1.7%

6.2%

1.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

China India

Physical Capital Education Factor Productivity

Source: Barry Bosworth and Susan Collins, Accounting for Growth: Comparing China and India

39

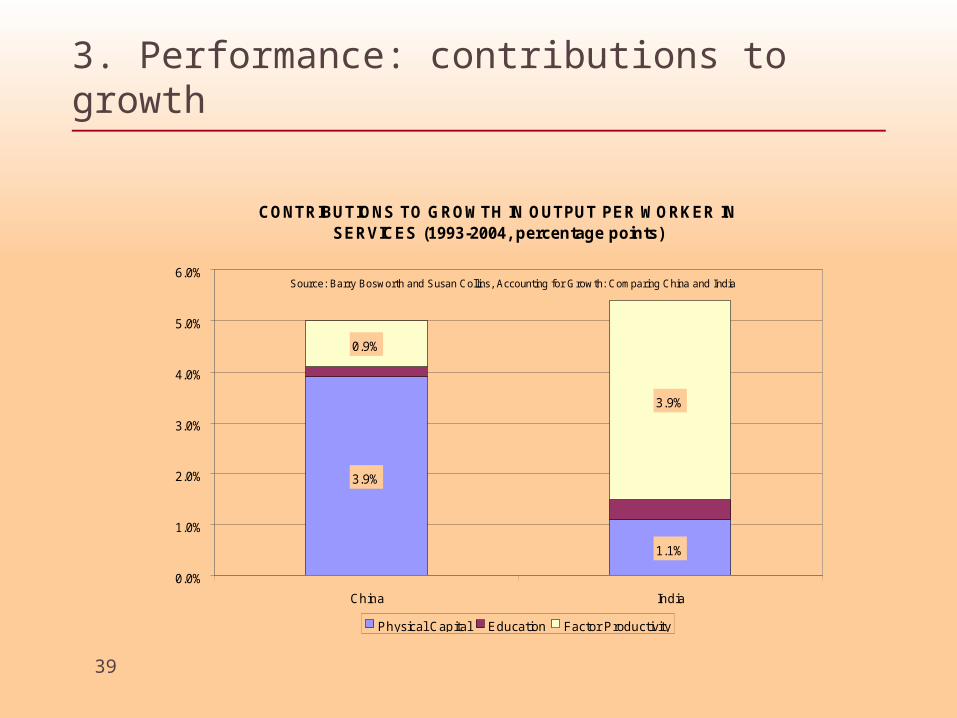

3. Performance: contributions to growth

CONTRIBUTIONS TO GROWTH IN OUTPUT PER WORKER IN SERVICES (1993-2004, percentage points)

3.9%

1.1%

0.9%

3.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

China India

Physical Capital Education Factor Productivity

Source: Barry Bosworth and Susan Collins, Accounting for Growth: Comparing China and India

40

4. Prospects

• China has outperformed India so far

• China does have weaknesses– A communist party-state

– Weak rule of law

• But also important strengths:– Open economy

– High saving and investment

– High literacy

– Classic east Asian export-oriented manufacturing

– Big investment in infrastructure

41

3. Prospects

• India does have strengths:– Stable political institutions

– A sophisticated legal system

– English as the business language

• But also weaknesses:– Lower investment;

– Failure to industrialise;

– Weaker integration into the world economy;

– Misallocation of public spending and worse infrastructure;

– Distorted labour markets; and

– Lower literacy.

42

3. Prospects

GDP AT MARKET PRICES ($bns)

$100

$1,000

$10,000

$100,000

2000 2010 2020 2030 2040 2050

China India Germany Japan UK US

Source: Goldman Sachs

43

3. Prospects

GDP PER HEAD AT CURRENT MARKET PRICES ($s)

$100.0

$1,000.0

$10,000.0

$100,000.0

2000 2010 2020 2030 2040 2050

China India Germany Japan UK US

Source: Goldman Sachs

44

3. Prospects

• India is in an excellent position to exploit the opportunities and, given its size, manage the risks

• Its performance has greatly improved over the past one and a half decades.

• But China’s performance shows India could do much better