The Rise of Resource Nationalism? - saimm

371

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism: A Resurgence of State Control in an Era of Free Markets Or the Legitimate Search for a New Equilibrium? A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining Compiled by Michael Solomon Cape Town, February, 2012

Transcript of The Rise of Resource Nationalism? - saimm

Southern African Institute of Mining and Metallurgy

The Rise of Resource Nationalism:

A Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

Compiled by Michael Solomon

Cape Town, February, 2012

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 2

Disclaimer

The Southern African Institute of Mining and Metallurgy, as a body, is not responsible for the statements

and opinions advanced in any of its publications.

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 3

Research Team Project Director Michael Solomon Chairman of the Mineral Economics Committee

Southern African Institute of Mining and Metallurgy

Project, Production Melanie Low Independent Researcher & Editorial Manager Research Director Dr Sue Cook Research + Planning Executive, Royal Bafokeng Nation Macro-economics Prof Stan Du Plessis Professor of Economics at Stellenbosch University.

Vice-Dean (Research) Faculty of Economics and Management Science at Stellenbosch University and President of the Economic Society of South Africa

Political Economics Michael Solomon Southern African Institute of Mining and Metallurgy Prof Anthony Butler Department of Political Science,

University of Cape Town Dr Michael Khan University of Stellenbosch

Fiscal Implications Prof Fred Cawood Head of School, School of Mining Engineering, University of the Witwatersrand, Johannesburg OP Oshokoya School of Mining Engineering, University of the Witwatersrand, Johannesburg Beneficiation Dr Marian Lydall Head: Regional Mineral Development, Mineral Economics &

Strategy Unit (MESU), Mintek, Randburg

Minerals Policy, SLPs Grant Mitchell Independent Researcher & Transformation State Capacity Dr Hudson Mtegha Senior Lecturer, Mineral Policy

School of Mining Engineering, University of the Witwatersrand, Johannesburg

Phillip Mogodi MSc candidate & Research Assistant School of Mining Engineering University of the Witwatersrand, Johannesburg

Legislative Environment Sivalingum Rungan Senior Lecturer, Minerals Law,

School of Mining Engineering, University of the Witwatersrand, Johannesburg

Mineral Economics Prof Magnus Ericsson Professor of Mineral Economics,

Luleå University of Technology, Sweden

Case Studies Luke Raffin Researchers, Kennedy School of Business, Kartik Akileswaran Harvard University

Melanie Low Independent Researcher Prof Magnus Ericsson Chief Executive Officer, Raw Materials Group, Sweden Barry Sergeant Freelance mining journalist/writer Country Risk Martin Bekker Manager, Information, Royal Bafokeng Nation Bilateral Treaties Martin Bekker Manager, Information, Royal Bafokeng Nation Economic Impacts Michael Solomon Southern African Institute of Mining and Metallurgy

Ogodiseng Letlape Research Officer, Royal Bafokeng Nation Editing & proof reading Cheryl Langbridge Independent Editor

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 4

Contents List of Acronyms .............................................................................................................................................. 14

List of Definitions .............................................................................................................................................. 17

SI Units ............................................................................................................................................................. 19

A Letter from His Majesty, Kgosi Leruo Moletlegi of the Royal Bafokeng Nation ........................................ 20

EXECUTIVE SUMMARY: PART 1 .......................................................................................................................... 22

Resource nationalism as a context for understanding the South African debate ................................... 23

Government response to resource nationalistic sentiment ...................................................................... 24

Political risk, investment returns and socio-economic contribution ......................................................... 25

Political elements of resource nationalism ................................................................................................ 25

Features of state ownership of global mineral production ....................................................................... 27

EXECUTIVE SUMMARY: PART 2 .......................................................................................................................... 30

South Africa: a case study .............................................................................................................................. 30

The stated objectives of calls for nationalisation ...................................................................................... 30

The economic and techno-legal realities of nationalisation ....................................................................... 31

Bilateral agreements ................................................................................................................................... 33

Market based institutions ........................................................................................................................... 33

The question of corruption ......................................................................................................................... 33

Achieving the objectives ............................................................................................................................. 33

Institutional capacity ................................................................................................................................... 35

Infrastructure ............................................................................................................................................... 36

Proposals ...................................................................................................................................................... 36

EXECUTIVE SUMMARY: PART 3 .......................................................................................................................... 38

Review of the ANC State Intervention in the Minerals Sector (SIMS) Report ............................................. 38

Critique ......................................................................................................................................................... 39

Overview ...................................................................................................................................................... 41

Structure of the report ................................................................................................................................ 44

Fiscal instruments ........................................................................................................................................ 45

The Brown Tax ............................................................................................................................................. 47

Resource rent tax (RRT) .............................................................................................................................. 47

Defining costs for resource rent taxes ....................................................................................................... 48

Excess profits tax ......................................................................................................................................... 48

Corporate income tax .................................................................................................................................. 48

Profit-based royalty ..................................................................................................................................... 48

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 5

Output-based royalties ................................................................................................................................ 48

Graduated price-based windfall tax ............................................................................................................ 48

Specific royalty tax ...................................................................................................................................... 49

State equity .................................................................................................................................................. 49

Existing fiscal instruments in the South African mining sector ................................................................. 49

Proposals for state intervention ..................................................................................................................... 50

Objectives .................................................................................................................................................... 50

Nationalisation as an option for state intervention ................................................................................... 50

The resource rent tax model ........................................................................................................................ 51

A state-owned mining company .................................................................................................................. 51

Strategic alignment of government departments ..................................................................................... 52

Granting of mineral rights ........................................................................................................................... 53

The Minerals Commission ........................................................................................................................... 54

Mineral rights conversion............................................................................................................................ 54

Capital gains tax on mineral rights.............................................................................................................. 54

Investment in state geo-knowledge ........................................................................................................... 54

Mining health and safety ............................................................................................................................. 55

Mining and the Environment-Monitoring and Compliance Agency .......................................................... 55

Minerals and environmental impacts research .......................................................................................... 55

Developing the mineral economic linkages ................................................................................................... 55

Establishing fiscal linkages .............................................................................................................................. 55

The capture of resource rents .................................................................................................................... 55

Mineral royalties .......................................................................................................................................... 56

Tax havens ................................................................................................................................................... 56

Carbon tax .................................................................................................................................................... 56

Deployment of resource rents .................................................................................................................... 57

Beneficiation and forward linkages ............................................................................................................ 58

Enhancing the strategic leverage of South Africa’s minerals .................................................................... 58

The formation of a Super Ministry .............................................................................................................. 58

Tariffs ........................................................................................................................................................... 58

Classification of strategic minerals ............................................................................................................. 59

Job creation strategies around strategic minerals .................................................................................... 59

Backward linkages: mining inputs .............................................................................................................. 62

Knowledge linkages .................................................................................................................................... 63

Mining-related infrastructure...................................................................................................................... 64

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 6

SECTION 1 RESOURCE NATIONALISM IN CONTEXT .......................................................................................... 68

Prologue .............................................................................................................................................................. 68

The WEF Responsible Mining Development Initiative (RMDI) ........................................................................ 69

Preface ................................................................................................................................................................. 70

Key questions about resource nationalism ..................................................................................................... 71

Chapter 1 Defining the issue ............................................................................................................................... 72

Defining resource nationalism ........................................................................................................................ 73

Key tenets of the argument for resource nationalism .................................................................................. 73

Chapter 2 Resource nationalism and state intervention in the mining sector ............................................... 75

Resource nationalism and nationalisation ..................................................................................................... 78

The cyclicity of nationalisation and privatisation ........................................................................................... 79

The economic theory and aspects of policy governing resource nationalism ............................................. 81

The strategic imperative for state control ..................................................................................................... 82

Differentiating ownership from control ..................................................................................................... 83

Nationalisation in market economies compared to centrally planned economies .................................. 83

Historical recap of nationalisation .............................................................................................................. 84

State ownership shares of global metal production ................................................................................. 85

State ownership in free market economies ............................................................................................... 87

The Chinese factor ....................................................................................................................................... 89

The political economics of resource nationalism ........................................................................................... 91

A summary of the economic factors to be considered in the nationalising of mines .................................. 92

Chapter 3 The mechanisms of state intervention in mining ............................................................................ 94

Nationalisation and economic development ................................................................................................. 94

State-owned mining companies: state participation or state intervention in the mining industry ............ 94

Chapter 4 The African experience of resource nationalism ............................................................................ 97

The nationalisation and reprivatisation of the Ashanti goldfields in Ghana ................................................. 97

Ashanti Goldfields during nationalisation .................................................................................................. 97

Re-privatisation ............................................................................................................................................ 98

The impact of re-privatisation reforms on the Ghanaian mining sector ................................................... 99

Lessons from Ghana .................................................................................................................................. 100

Ghana today ............................................................................................................................................... 100

Zambian nationalisation and subsequent privatisation of its copper mines: a stereotype of

nationalisation failure .................................................................................................................................... 100

Macro-economic performance under nationalisation .............................................................................. 102

Return to multi-party democracy and commitment to liberalisation of economy .................................103

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 7

ZCCM, Zambia’s greatest challenge...........................................................................................................103

Summary and lessons .................................................................................................................................103

Lessons from key drivers for nationalisation ............................................................................................103

Conclusion .................................................................................................................................................. 106

The liberalisation of state control over mines in Tanzania .......................................................................... 106

New legislation to liberalise the economy ................................................................................................ 107

Growth since liberalising economy ........................................................................................................... 108

Tanzania and resource nationalism .......................................................................................................... 108

State participation in the mining industry on Guinea Conakry .................................................................... 109

Interests in the mining sector .................................................................................................................... 110

Mismanagement of state-owned mines, abuse of resource rents and endemic corruption: Gécamines and

the DRC resource curse .................................................................................................................................. 112

Mobutu era and Gécamines ....................................................................................................................... 112

Civil war ....................................................................................................................................................... 113

New Mining Code, 2002 ............................................................................................................................. 113

The result as we know it by early 2012 ....................................................................................................... 115

Indigenisation - Zimbabwe's claim to majority ownership ........................................................................... 115

Ministry and state-owned mining companies ........................................................................................... 116

Indigenisation ............................................................................................................................................. 117

Marange diamond fields ............................................................................................................................ 119

Lessons from Zimbabwe ............................................................................................................................ 122

The importance of political leadership and effective institutional capacity: Botswana’s success with

diamonds......................................................................................................................................................... 123

Strategic negotiations over diamond partnerships .................................................................................. 124

World diamond market, economic management and beneficiation ....................................................... 124

Political leadership and institutions ........................................................................................................... 125

Integration with traditional authorities and openness to foreign support ............................................. 126

Chapter 5 The Latin American experience with nationalisation..................................................................... 127

Venezuela: socialist ideology and agenda driven resource nationalisation ................................................ 127

Progressive nationalisation ........................................................................................................................ 127

International arbitration against PDVSA ...................................................................................................130

The economic pragmatism of Brazil and the success of Vale and Petrobras ..............................................130

Privatisation of state-owned companies ...................................................................................................130

Vale .............................................................................................................................................................. 131

Petrobras .................................................................................................................................................... 132

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 8

Chile and the expedience of a nationalised Codelco through different political regimes .......................... 133

Codelco ....................................................................................................................................................... 133

Conclusion ................................................................................................................................................... 134

Peru: mining: socialist rhetoric and political compromise ............................................................................ 135

Bolivian nationalisation: the cyclicity of nationalisation, neo-liberalism and re-nationalisation ................ 137

Comibol ....................................................................................................................................................... 137

The brief rise of neoliberalism and the return of resource nationalism (1980s - today) .........................138

Chapter 6 Experiences from other countries – Europe and Asia................................................................... 140

The privatisation of the mining industry in Mongolia: Successes and subsequent mistakes .................... 140

Mongolia: 1997 to 2007 ............................................................................................................................. 140

External shock: 2008 to 2009 .................................................................................................................... 141

Oyu Tolgoi project ...................................................................................................................................... 142

Norway: a long history of state participation ............................................................................................... 143

The evolution of Statoil .............................................................................................................................. 143

Statoil today ............................................................................................................................................... 144

Some reasons why Norway has succeeded ............................................................................................. 144

Chapter 7 Resource rents, the Australian experience and SIMS proposals ................................................... 145

Australia and resource rent sharing: great economic theories and sobering political realities ................ 149

The impact of proposed resource rents on the competitiveness of South African mining projects ......... 151

Threshold IRR.............................................................................................................................................. 151

Impact on and influence of the Weighted Average Cost of Capital (WACC) in a competitive investment

situation ...................................................................................................................................................... 152

The proposed resource rent rate ............................................................................................................... 153

Summary of the comparative analysis exercise ........................................................................................154

Chapter 8 Lessons from the past, directions for the future ........................................................................... 156

Underperformance in nationalisation imperatives ....................................................................................... 157

Managing corruption .................................................................................................................................. 157

Workforce capacity and experience .......................................................................................................... 157

Inefficient state owned enterprises ......................................................................................................... 158

Inadequate foreign and domestic investment ......................................................................................... 159

Global economic and financial forces ....................................................................................................... 159

Achieving political objectives .................................................................................................................... 160

Private management of mining companies ............................................................................................. 160

Chapter 9 Resource nationalism and country risk ratings .............................................................................. 162

Comparisons of the impact on country risk ratings of previous nationalisation events ........................ 162

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 9

Country ratings .......................................................................................................................................... 164

Long term bond yields ............................................................................................................................... 166

Inbound FDI ................................................................................................................................................167

Portfolio investments ................................................................................................................................ 168

SECTION 2: CASE STUDY: THE SOUTH AFRICAN NATIONALISATION DEBATE............................................... 170

Chapter 10 The South Africa nationalisation debate in context ..................................................................... 170

Objectives of the case study .......................................................................................................................... 170

Context for the study ..................................................................................................................................... 170

Chapter 11 The political economy of the South African mining industry ....................................................... 172

Historical background to the current debate ............................................................................................... 172

Conclusion ................................................................................................................................................... 177

Chapter 12 The political dimensions of the debate .......................................................................................... 179

The Freedom Charter of 1955 and its relevance to mining ....................................................................... 179

Mine nationalisation and ANC factionalism ............................................................................................. 180

The position of the South African Communist Party (SACP) in the debate ................................................. 181

The Young Communist League (YCL) ........................................................................................................ 182

Labour’s position on nationalisation ............................................................................................................. 182

NUM’s proposals on state intervention in the mining sector ..................................................................183

The Cosatu position on state intervention in the mining industry .......................................................... 185

Tripartite Alliance divisions, factionalism and political vulnerability on the issue of nationalisation........ 186

An analysis of the ANC Youth League (ANCYL) proposals ....................................................................... 187

The political process ...................................................................................................................................... 189

The Economic Transformation Committee perspective on the question of nationalisation ................ 190

Potential outcomes of the process........................................................................................................... 190

Chapter 13 The economic dimensions of the nationalisation debate ............................................................. 192

The attractiveness of South Africa for local and international investors: economic development and the

role of the state .............................................................................................................................................. 192

The implications of corporate ownership as opposed to state ownership ................................................. 197

The track record of nationalisation .............................................................................................................. 198

Cost of nationalisation to South Africa......................................................................................................... 200

The implications of nationalisation for the fiscal capacity of the state ...................................................... 202

General principles ...................................................................................................................................... 203

The South African mining taxation regime .............................................................................................. 203

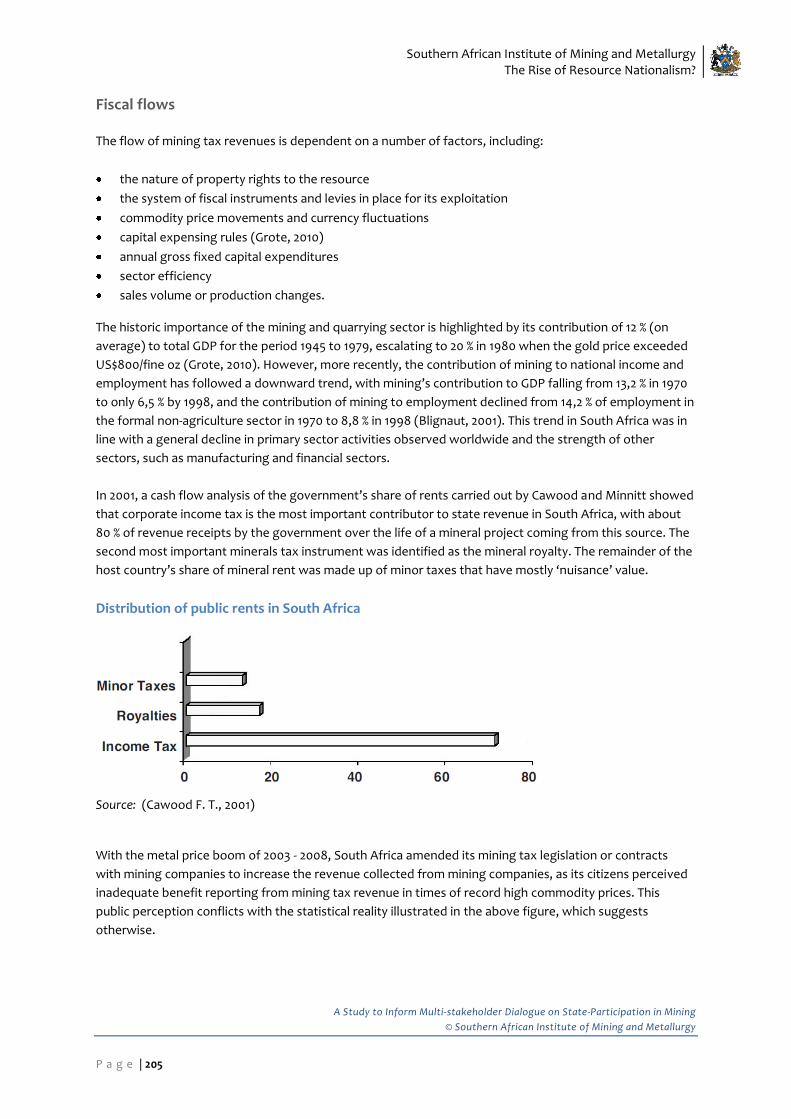

Fiscal flows ................................................................................................................................................. 205

Implications for the fiscal capacity of the state ....................................................................................... 207

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 10

Conclusions ................................................................................................................................................ 208

Chapter 14 The geopolitical issues around nationalisation in South Africa .................................................. 209

The rise of BITs ........................................................................................................................................... 209

Protection and restrictions under BITs .......................................................................................................... 210

Chapter 15 ANC Mining Policy, legislative framework and process ............................................................... 216

The Macro-Economic Research Group, the ANC Minerals and Energy Group and the development of

ANC Minerals Policy .................................................................................................................................... 216

The ANC Draft on a Mineral and Energy Policy (1990) .............................................................................. 217

The Minerals and Energy Policy Centre 1994 ............................................................................................ 219

The Kwagga Initiative 1994 ........................................................................................................................ 219

The Bakubung Initiative (2000)................................................................................................................. 220

SAMDA (2001) ............................................................................................................................................. 221

New Africa Mining Fund (NAMF) (2003) ...................................................................................................222

Support for small-scale mining (1999) .......................................................................................................222

The implications of the Polokwane Conference in 2007 ......................................................................... 224

Mining Industry Growth Development and Employment Task Team (MIGDETT) ................................. 224

The New Growth Path ............................................................................................................................... 225

The National Planning Commission diagnostic and the mining sector ................................................... 227

Chapter 16 Legislative environment and transformation .............................................................................. 228

Introduction to the MPRDA and Mining Charter ......................................................................................... 228

MPRDA (Mineral and Petroleum Resources Development Act 28 of 2002) ........................................... 228

The Mining Charter .................................................................................................................................... 229

Social and Labour Plans (SLPs) .................................................................................................................. 231

Overlaps between and implementation of the MPRDA, Mining Charter, and Social and Labour Plan . 231

Sector achievement of the requirements of the MPRDA and Charter ................................................... 235

Conclusions ................................................................................................................................................ 239

A techno-legal appraisal of the South African mining legislative regime and its implications for

nationalisation ............................................................................................................................................... 240

Applicable mining legislation .................................................................................................................... 240

Mineral and Petroleum Resources Royalty (Administration) Act 29 of 2008 ........................................ 248

Codes of Good Practice for the South African minerals industry ........................................................... 248

Stakeholders’ Declaration On Strategy For The Sustainable Growth And Meaningful Transformation of

South Africa’s mining industry .................................................................................................................. 250

Amendment of the Broad-Based Socio-Economic Empowerment Charter for the South African Mining

and Minerals Industry ................................................................................................................................. 251

The ANCYL Manifesto: Towards the Transfer of Mineral Wealth to the Ownership of the People as a

Whole: a perspective on the nationalisation of mines ............................................................................ 252

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 11

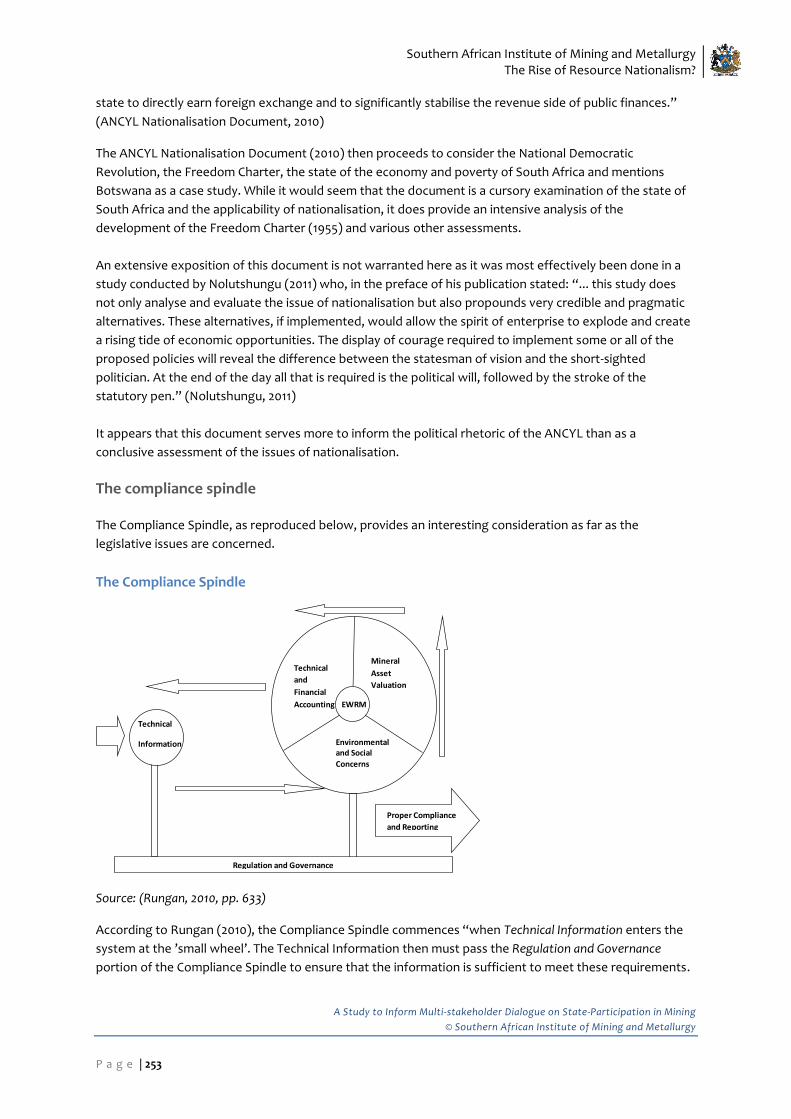

The compliance spindle ............................................................................................................................. 253

Conclusion .................................................................................................................................................. 254

Chapter 17 The economic reach of the South African mining industry: leveraging the minerals sector to

enhance the economic multipliers of mining ................................................................................................. 255

Catalysts for Dutch Disease and Resource Curse in emerging economies ................................................. 255

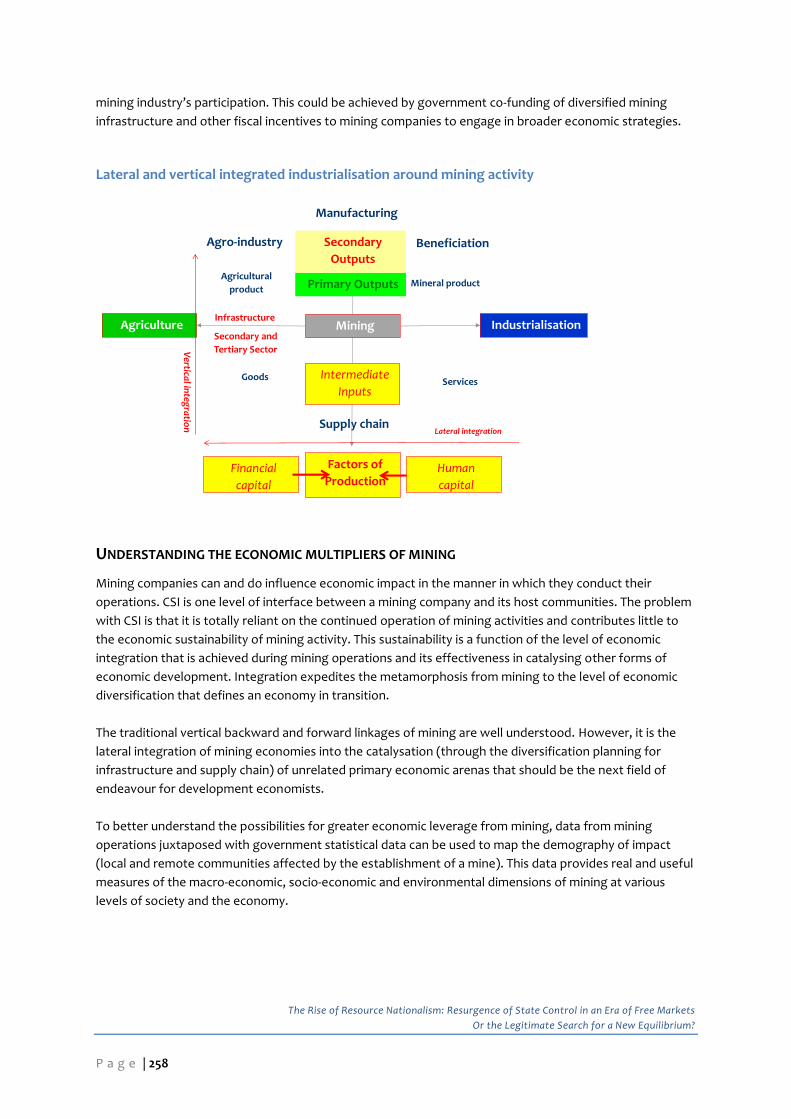

Industrialisation and economic diversification around mining ................................................................... 256

Understanding the economic multipliers of mining .................................................................................... 258

Mining and economic multipliers: examples from South Africa and Botswana ........................................ 259

Botswana ................................................................................................................................................... 259

Assessing the impact of the mining economy into the broader economy ................................................. 262

Cross sectoral spread of benefit ................................................................................................................... 265

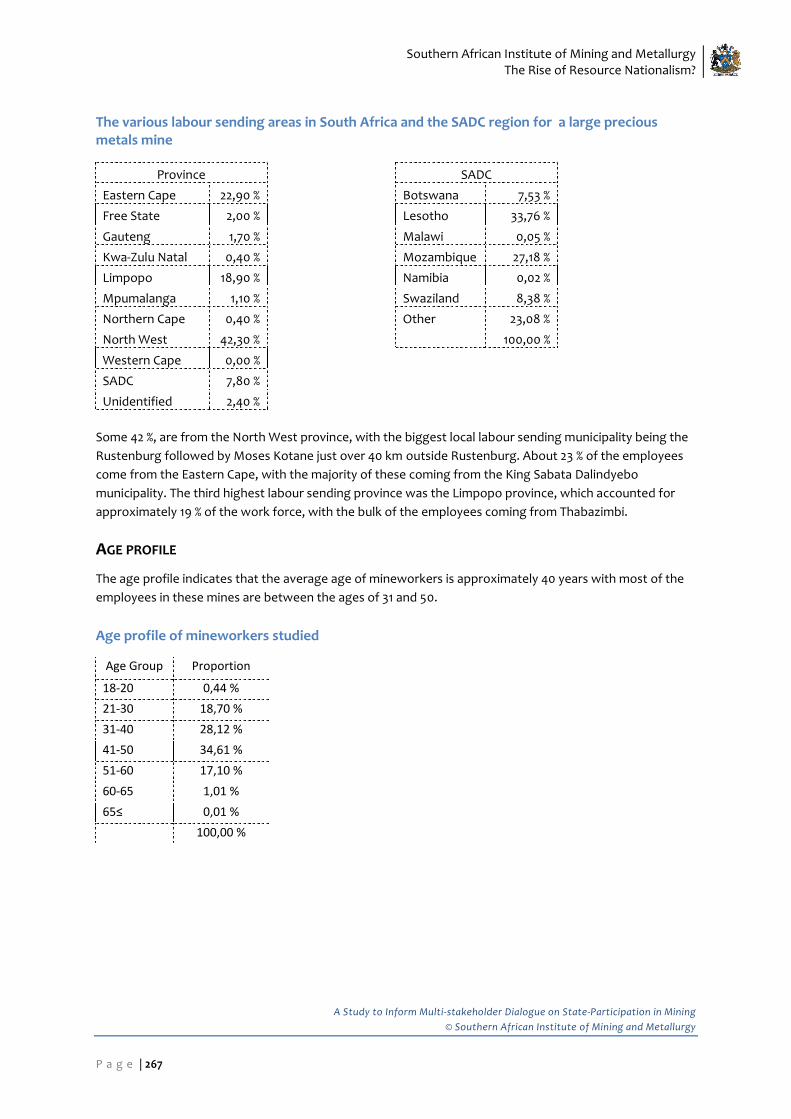

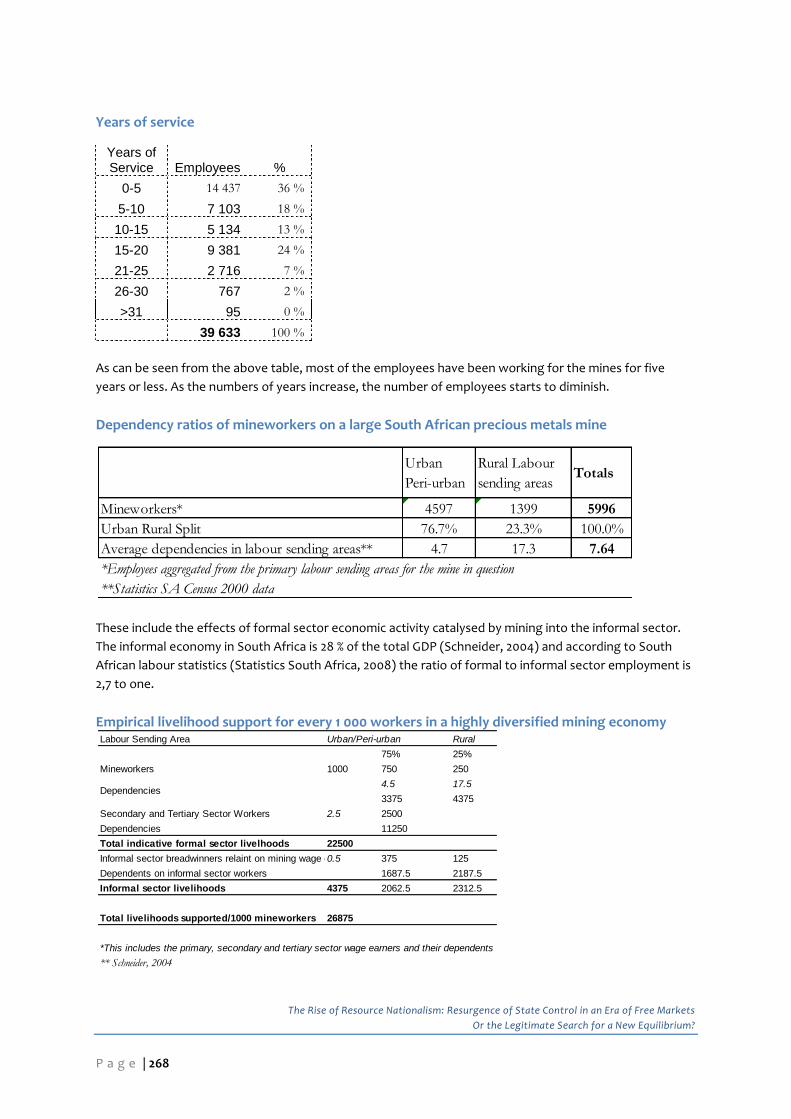

Mine wages and livelihood dependencies on mineworkers in South Africa .............................................. 266

Demography .................................................................................................................................................. 266

Age profile...................................................................................................................................................... 267

Conclusion ...................................................................................................................................................... 269

Chapter 18 Enhancing economically viable beneficiation in the South African mining sector ................... 270

South Africa’s comparative advantages in the global mineral sector ........................................................ 270

Towards a broader view of mineral beneficiation in South Africa .............................................................. 273

Downstream mineral beneficiation .............................................................................................................. 274

Sector-specific and macro-economic leverage ........................................................................................ 276

Upstream mineral beneficiation .................................................................................................................... 281

Sidestream mineral beneficiation ................................................................................................................. 282

Conclusion: optimising strengths, minimising weaknesses ........................................................................ 282

Chapter 19 The options for developmental state participation in the mining sector .................................. 285

Increasing the strategic capacity of the state to develop the mining sector ............................................. 287

Mineral-related science councils as a key contributor to national development strategy ........................ 289

Council for Geoscience .............................................................................................................................. 289

CSIR Mining Technology............................................................................................................................ 290

Mintek ......................................................................................................................................................... 291

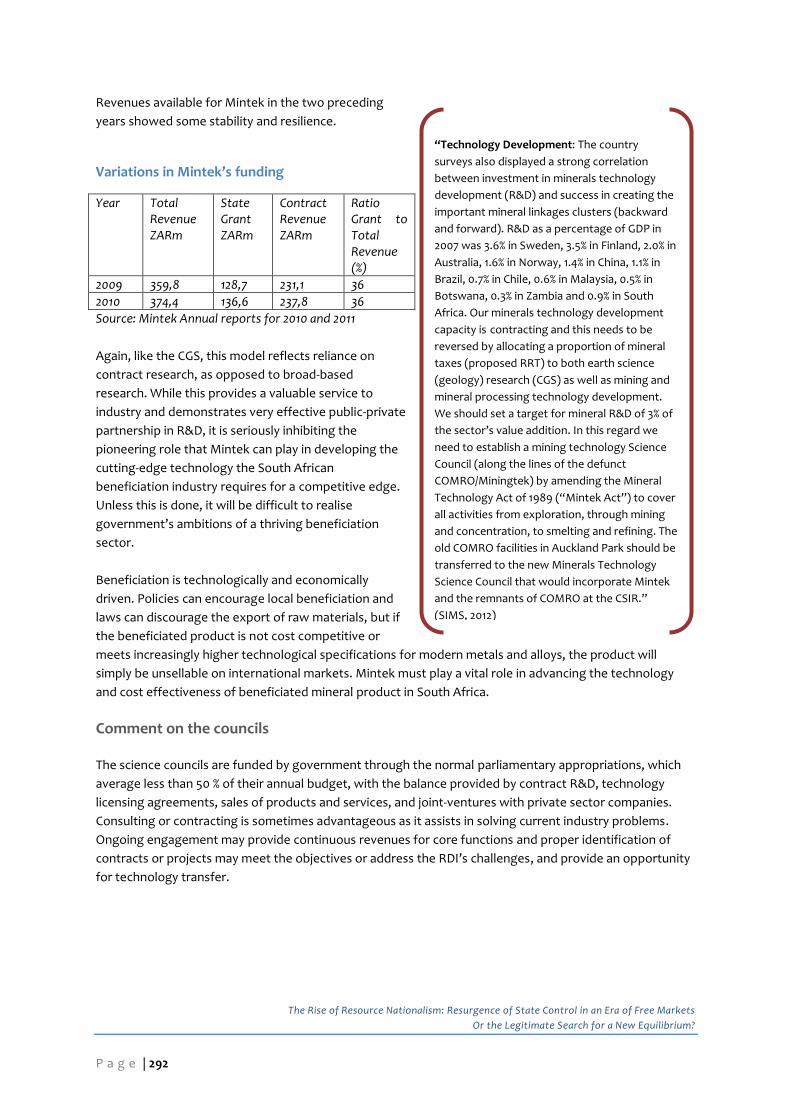

Comment on the councils ......................................................................................................................... 292

South African DFI involvement in the mining sector ................................................................................... 293

Industrial Development Corporation (IDC) .............................................................................................. 294

Development Bank of Southern Africa (DBSA)........................................................................................ 295

National Empowerment Forum (NEF) ...................................................................................................... 296

Comments on the DFIs .............................................................................................................................. 296

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 12

Enhancing the capacity and effectiveness of the human capital of the sector .......................................... 297

Challenges .................................................................................................................................................. 297

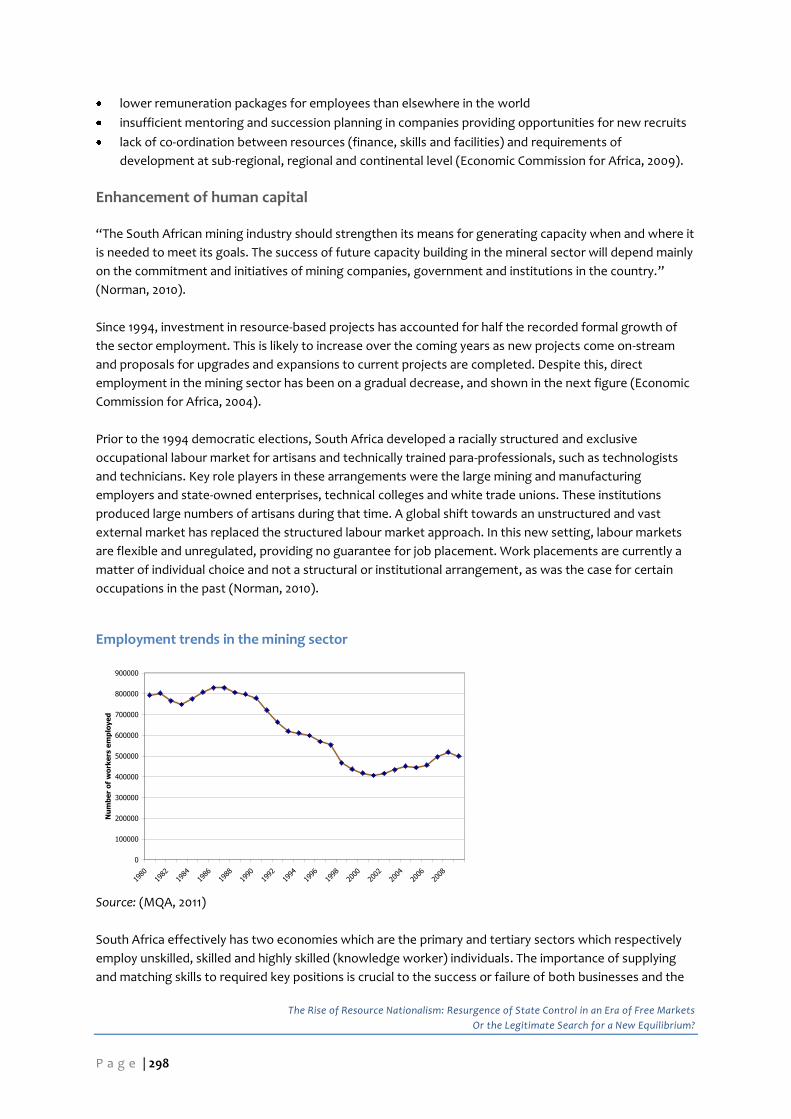

Enhancement of human capital ................................................................................................................ 298

Conclusion ...................................................................................................................................................301

Chapter 20 Community management of resources: the tension between state stewardship and

community ownership of mineral rights ........................................................................................................ 302

Historical background ............................................................................................................................... 303

The Bafokeng asset base........................................................................................................................... 305

Royal Bafokeng Holdings (RBH) and black empowerment .................................................................... 306

Leadership, governance, administration and service delivery ................................................................ 307

Building community capacity and economic opportunity ....................................................................... 309

Conclusion ...................................................................................................................................................310

SECTION 3 RESOURCE NATIONALISM AND COMPETITIVENESS ISSUES ....................................................... 312

Chapter 21 The relative competitiveness of the South African mining sector .............................................. 312

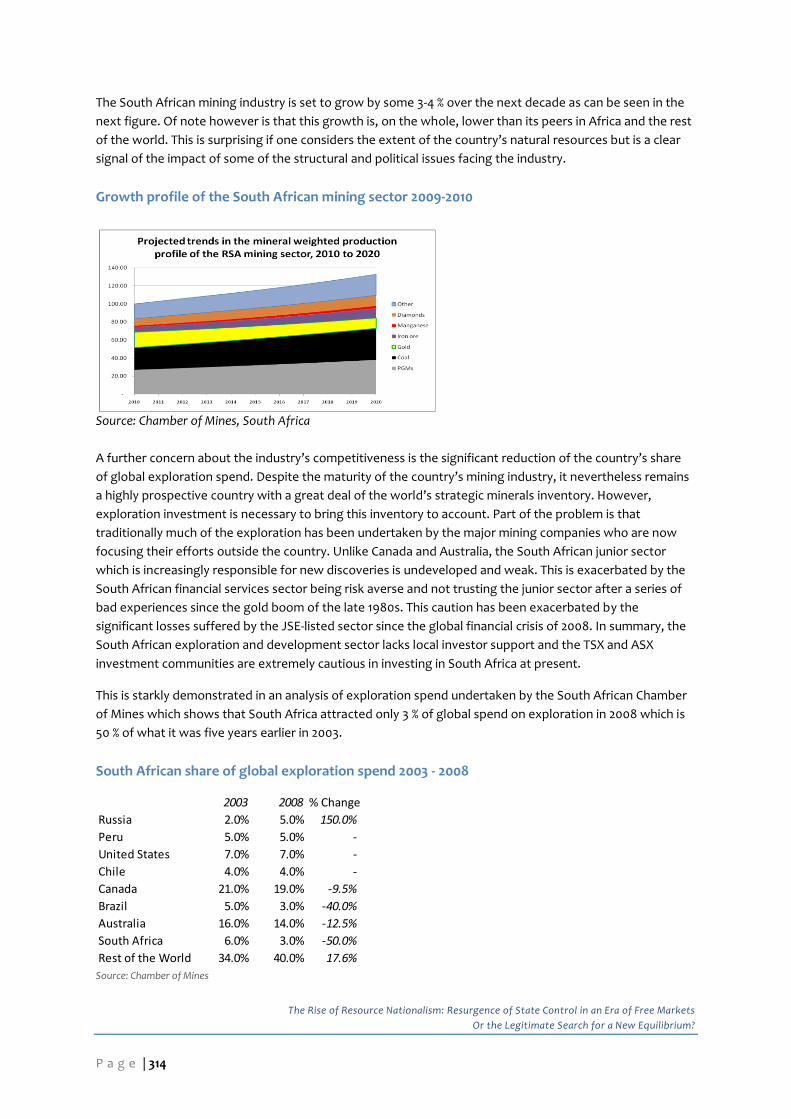

A profile of the South African mining industry ............................................................................................. 312

Prospectivity for new projects in South Africa ......................................................................................... 315

Iron ore and steel........................................................................................................................................ 315

Manganese.................................................................................................................................................. 315

Platinum ..................................................................................................................................................... 316

Nickel .......................................................................................................................................................... 316

Chrome ....................................................................................................................................................... 316

Gold ............................................................................................................................................................. 317

Beach sand ..................................................................................................................................................318

Regulatory environment ................................................................................................................................318

Mining Charter and Scorecard ...................................................................................................................319

The Charter and beneficiation .................................................................................................................. 320

Access to information on licencing ........................................................................................................... 320

Social and Labour Plans (SLP) ................................................................................................................... 320

Political economics ......................................................................................................................................... 321

Macro-economic issues .............................................................................................................................. 321

The South African mining industry in summary ....................................................................................... 322

Chapter 22 Case Studies of other main mining investment venues in SADC ................................................ 323

Botswana ....................................................................................................................................................... 323

Regulatory environment ........................................................................................................................... 323

Profile of the mineral industry .................................................................................................................. 324

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 13

Political economy....................................................................................................................................... 326

The Botswanan industry in summary ....................................................................................................... 327

Namibia .......................................................................................................................................................... 327

Regulation .................................................................................................................................................. 327

Tax regime ................................................................................................................................................. 328

Industry profile .......................................................................................................................................... 329

The political economy of the Namibian mining industry .......................................................................... 331

Zimbabwe ...................................................................................................................................................... 332

Regulation .................................................................................................................................................. 332

The political economy of the Zimbabwean mining industry ................................................................... 333

Industry profile .......................................................................................................................................... 334

The Zimbabwean industry in summary .................................................................................................... 337

Zambia ............................................................................................................................................................ 338

Regulatory regime ..................................................................................................................................... 338

Tax regime ................................................................................................................................................. 338

Industry profile .......................................................................................................................................... 339

Political economy....................................................................................................................................... 340

The Zambian mining industry in summary ............................................................................................... 342

Chapter 23 The relative competitiveness of the SADC countries on minerals investment ......................... 343

Rating agencies .......................................................................................................................................... 343

Conclusions on South Africa’s competitiveness in the SADC region ...................................................... 348

APPENDIX 1 ........................................................................................................................................................ 349

Bi-lateral agreements .................................................................................................................................... 349

Works Cited ....................................................................................................................................................... 353

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 14

LIST OF ACRONYMS

ABET: Adult Basic Education Training

AEMFC: African Exploration and Mining Finance Corporation

ALMP: Active Labour Market Policies

ANC: African National Congress

ANC MEG: ANC Minerals and Energy Group

ANCYL: ANC Youth League

AVR: Ad valorem royalty

BEE: Black Economic Empowerment

BBBEE: Broad-based Black Economic Empowerment

BBSEE: Broad-based Socio-economic Empowerment

BEE: Black Economic Empowerment

BIT: Bilateral Investment Treaty

BRIC: Brazil, Russia, India and China

BRICS Brazil, Russia, India, China and South Africa

CC: Central Committee (NUM)

CGS: South Africa Council of Geoscience

CIF: China International Fund

CITT: Coal Industry Task Team

Cosatu: Congress of South African Trade Unions

CSI: Corporate Social Investment

CSIR: Council for Scientific and Industrial Research

CMEA: Council for Mutual Economic Assistance

CNMC: China Nonferrous Metal Mining

DBSA: Development Bank of Southern Africa

DEP: Department of Economic Planning

DFI: Development Finance Institutions

DME: Department of Minerals and Energy

DMR: Department of Mineral Resources

DRC: Democratic Republic of the Congo

DST: Department of Science and Technology

DTI: Department of Trade and Industry

EBIT: Earnings Before Interest and Taxation

EDD: Economic Development Department

EEA: Europe Economic Area

EITI: Extractive Industries Transparency Initiative

EIU: Economist Intelligence Unit

EMPR: Environmental Management Programme Report

Eskom: Electricity Supply Commission

ESOP: Employee Share Ownership Plan

ETC: Economic Transformation Committee (South Africa)

EU: European Union

EWRM: Enterprise Wide Risk Management

FDI: Foreign Direct Investment

FET: Fair and Equal Treatment

GAC: Global Agenda Council

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 15

GCC: Government Certificate of Competency

GDP: Growth Domestic Product

GFCF: Gross Fixed Capital Formation

GNU: Government of National Unity (Zimbabwe)

HDSA: Historically Disadvantaged South African

HRD: Human Resource Development

ICCM: International Council on Mining and Metals

IDC: Industrial Development Corporation

IDZ: Industrial Development Zone

ILO: International Labour Organisation

IP: Indigenous Peoples

IPO: Intellectual Property Offering

IPP: Import Parity Pricing

IRR: Internal Rate of Return

ISCOR: Iron and Steel Corporation

JSE: Johannesburg Stock Exchange

JV: Joint Venture

KZN: KwaZulu–Natal

LED: Local Economic Development

LKAB: Luossavaara-Kiirunavaara Aktiebolag

MFN: Most Favoured Nation

MEPC: Minerals and Energy Policy Centre

MERG: Macro-economic Research Group

MHSA: Mine Health and Safety Act 29 of 1996

MIGDETT: Mining Industry Growth Development and Employment Task Team

MQA: Mining Qualifications Authority (South Africa)

MPRDA: Mineral and Petroleum Resources Development Act

MRRT: Minerals Resource Rent Tax

MWU: Mineworkers Union

NAMF: New Africa Mining Fund

NDC: Namdeb Diamond Corporation

NDP: National Development Plan

NDRC: National Development and Reform Commission

NEC: National Executive Committee (ANC)

NECSA: Nuclear Energy Council of South Africa

NEF: National Empowerment Forum

NEMA: Environmental Management Act 107 of 1998

NGC: National General Council (NUM)

NGO: Non-Governmental Organisation

NGP: New Growth Path

NPV: Net Present Value

NRC: Native Recruiting Organisation

NSC: National Steering Committee of Service Providers to the Small-scale Mining Sector

NUM: National Union of Mineworkers

NQF: National Qualifications Framework

OECD: Organisation for Economic Co-operation and Development

PACI: World Economic Forum Partnership against Corruption Initiative

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 16

PDAC: Canadian Prospectors and Developers Association

PDI: Previously Disadvantaged Individual

PIC: Public Investment Corporation

PPP: Public Private Partnership

PPs: State-equity Participation with Private Sector

RDI: Research, Development and Innovation

Research and Development Institutions

RDP: Reconstruction and Development Programme

RMDI: Responsible Mining Development Initiative

RSPT: Resources Super Profits Tax

S&P: Standard and Poor

SACP: South African Communist Party

SADC: Southern African Development Community

SAI: State Allocated Investment

SAIMM: Southern African Institute of Mining and Metallurgy

SAMDA: South African Mining Development Association

SAPPF: South African Preferential Procurement Forum

SAR&H: South African Railways and Harbours

SARS: South African Revenue Services

SIC: Standard Industrial Classification

SIMS: State Intervention in the Minerals Sector (report)

SLP: Social and Labour Plan

SMME: Small, Medium and Micro Enterprises

SNA System of National Accounts

SNIM: Société Nationale Industrielle et Minière

SOE State Owned Enterprise

SPV: Special Purpose Vehicle

SWF: Sovereign Wealth Fund

UASA: United Association of South Africa

UIF: Unemployment Insurance Fund

USPTO: United States Patent and Trademark Office

WEF: World Economic Forum

Wenela: Witwatersrand Native Labour Association

WACC: Weighted Average Cost of Capital

WIR: World Investment Report

WTO: World Trade Organisation

YCL: Young Communist League

ZCCM: Zambia Consolidated Copper Mines

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 17

LIST OF DEFINITIONS

Bilateral Investment Treaties (BITS): Legally binding contracts wherein two sovereign states agree on the

treatment of investors and investments across the borders of the contracting states, normally to be

adjudicated outside of the host country, should the terms be breached.

Bonds: Securities used by governments to raise funds to cover budget deficits or to fund extraordinary

capital expenditure large infrastructure projects. The bonds are vended to private individuals (retail bonds)

and corporate entities. The bonds are tradable and interest rates reflected on the bond coupons are

referred to as the “risk free” rate, are variable with changing market conditions and are quoted on a daily

basis in the financial press.

Developmental state: A state which leads and guides its economy and in which the state intervenes in the

interest of the people as a whole. The state establishes as its principle of legitimacy its ability to promote

and sustain development, understanding by development the combination of steady high rates of growth

and structural change in the productive system, both domestically and in its relationship to the

international economy. Ultimately for the developmental state, economic development is not a goal but a

means. (Fine B. , 2010)

Dutch Disease: The unintended adverse impact on the industrial sector of a country where a large

commodity boom causes the real exchange rate to appreciate, leaving the local industrial sector

uncompetitive internationally.

Foreign Direct Investment (FDI): Net inflows of investments which acquire sustained management interest

(conventionally, 10 % or more of voting shares) in an enterprise operating in a country other than that of

the investor.

Long-term bonds: More commonly referred to as long bonds, these bonds are promissory notes issued by

a national government carrying a coupon recoverable by the bearer on a certain date, as well as periodic

interest payments.

Nationalisation: One form of a range of ways in which the state can intervene in a sector or industry. It is

the transfer of ownership of an asset or industry from the private sector to the public sector.

Nationalised mining company: A mining company, expropriated by the state from the private sector, with

or without compensation. Usually, some measure of compensation is given to the mining company

furnishing the asset.

Ownership: A defined equity position in a company, which is easy to determine from the share register of

a company.

Portfolio flows: Financial investments into (or out of) an economy in instances where these investments

are lower than the minimum 10 % stake in the asset needed to classify the investment as a foreign direct

investment (FDI).

Privatisation: The transfer of such an asset from public to private ownership.

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 18

Resource Curse: The disadvantage experienced by a country that has a large amount of natural resources,

as a result of the resources not being properly utilised for the benefit of the citizens of the country

concerned. Instead of boosting the economy and the lives of the people, the people often find themselves

in a worse position than before, with little or no improvement in the economy. This occurs because the

income from these resources is often misappropriated by corrupt leaders and officials instead of being

used to support growth and development. Moreover, the wealth from the natural resources can fuel

internal grievances, creating stagnation and conflict, rather than economic growth and development.

Resource nationalism: The desire of the people of resource-rich countries to derive more economic benefit

from their natural resources and the resolution of their governments to concomitantly exercise greater

control of the country’s natural resource sectors. The forms in which these sentiments and control

mechanisms are manifested vary widely.

Resource rent: Surplus operating profits over and above a fair rate of return, which are required to

incentivise private investment in the high-risk exploration and development phases of mining after the

deduction from revenues of directly productive costs. A resource rent is calculated by adding the fiscal

flows and other statutory rents to the direct productive costs of the enterprise. The surplus (if it exists)

between this aggregated cost and the revenue is the resource rent, which is then split between the mining

company and the host government

State control: Comprises direct and decisive action on the part of the state on strategically important

imperatives and issues. These range from influencing or directly dictating industry and company policy to

interventions in large investments and even dictating management structures. Control does not necessarily

mean equity, direction or management. Control can be exercised indirectly through long-term contracts,

marketing regulations, proprietary technology developed by state research entities and with restrictions

on distribution, and state finance assistance through grants and subsidies.

State equity in mining projects: The state, through standing regulation, solicits a share of the company at

the inception of the project for which it may or may not pay.

State-owned mining company: A company that has been established and funded by the state to facilitate a

strategic involvement in the mining sector, with the state having a controlling interest in the company. The

company is managed by the state as a parastatal.

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 19

SI UNITS

bt billion tonnes

g/t grammes per tonne

kg kilogramme

km kilometres

kV kilovolts

m metres

moz million ounces

mt million tonnes

mtpa million tonnes per annum

MW megawatts

0z ounces

t tonnes

tpa tonnes per annum

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 20

A Letter from His Majesty, Kgosi Leruo Moletlegi of the Royal Bafokeng Nation

While diversification remains a key pillar of our economic development strategy, we must also recognise

the importance that mining plays in our local economy, and maximise the positive impact of mining on the

regional economy.

Few people know or appreciate that every mining job represents around 26 livelihoods. That means that

for every person who works on a mine in South Africa, about 26 other people benefit due to its economic

multiplier effect. This includes everything from secondary industries such as construction and catering, to

the tertiary sectors where the purchasing power of that miner is felt, to the money he remits to his home

community in the rural areas. If one then considers a typical local mine community such as my own

Community, the Bafokeng, about 50 % of adults are employed, and of those, almost 60 %, employed by

mines, we have some 62 000 people employed in the mining industry, it becomes clear how important

mining is not only to our local economy, but to the national economy. While mining represents 8 % of South

Africa’s GDP, it has a major identifiable impact on both rural and urban livelihoods not only in the local min

communities and labour sending areas, but also in the industrial areas such as Gauteng.

As a community so heavily involved with mining, we have undertaken to support study into the issues

related to state participation in the mining sector from a global and historical perspective. Our objective is

to inform the debate through rigorous and exhaustive research. We have partnered with the Southern

African Institute for Mining and Metallurgy and researchers from the Universities of Harvard, Lulea in

Sweden, Witwatersrand, Stellenbosch and Cape Town to compile a comprehensive suite of research to

create a better understanding of the social, economic and political impacts of state participation and

nationalisation policies, as they have been implemented in countries all over the world. This study also

considers the implications for the social and macro-economy and government capacity to directly assist the

country’s mineral economy to grow and yield maximum benefit to its people.

Although everyone agrees on the urgent need for greater economic justice in our country, a preliminary

analysis of our research suggests that nationalizing the mines in South Africa would not necessarily achieve

the desired impact. It is questionable whether the fiscal and strategic capacity of the state would

necessarily be strengthened by straightforward nationalisation or that there would be an increase mining-

related jobs and industrialisation. Notwithstanding this observation, there are many other ways in which

the State can indeed participate directly in the industry to ensure its development and maximise its benefit

while maintaining a critical and healthy investor interest.

As the Bafokeng we support and recognise the study as a non-partisan, ideologically neutral document

that seeks to provide all the stakeholders with a common information resource from which they can

develop their respective opinions and positions. However, this is not enough. It is imperative that these

opinions be aired and discussed in a constructive manner that is going to achieve a balanced outcome for

all stakeholder groupings. A neutrally facilitated multi-stakeholder dialogue needs to take place where

these groupings can express their opinions and solicit support for their interests without conflict or fear of

retribution. This process would include government, labour, industry, the investment community and civil

society.

We, as the Bafokeng, are highly sensitive to the fact that the call for nationalisation is being driven by a

sentiment that the distribution benefits of the mining industry are seen to be skewed and that there is little

tangible benefit to the greater population. In the first instance the study seeks to establish the real extent

and reach of economic benefit from the mines. In the second, we recognise that the Bafokeng model of

using dividends from platinum mining to support social and economic development in our 29 villages has

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 21

attracted increasing attention within southern Africa and the world. The Bafokeng have clearly

demonstrated that community participation in mining through the judicious management of community

resources is not only possible, but provides the direct benefit and tangibility that broader distribution of

benefit through government channels cannot achieve. It is an important qualification here that while there

is direct community benefit from a model such as ours, the nation still benefits from its share of economic

rents through the fiscal mechanisms employed by the state. We therefore contribute not only directly to

the quality of life of our own people, but to the broader social- and macro-economy of South Africa.

We are proud to be supporting an imperative that is in the national interests and will continue to strive

towards furthering the causes of social equity, economic justice and a healthy political economy in our

country.

(signed)

Kgosi Leruo Moletlegi

The Rise of Resource Nationalism: Resurgence of State Control in an Era of Free Markets

Or the Legitimate Search for a New Equilibrium?

P a g e | 22

EXECUTIVE SUMMARY: PART 1

South Africa has been in the grip of a critical political debate on the future of the mining industry for the

last eighteen months. This has resulted in an acrimonious stand-off between the ruling party, the African

National Congress and its youth wing, the ANC Youth League (ANCYL). The debate, at times, has

degenerated into an emotive and rhetoric driven public dialogue on the merits or otherwise of

nationalisation. It has been conducted primarily in the media between politicians either side of the party

divide with arbitrary commentary emanating from other quarters.

Of concern is that the argument has been unstructured and largely unqualified beyond the principal players

and industry representatives. More seriously, there has been little evidence of leadership in the debate

either from government or industry. South Africa’s political leadership demurred in taking a strong stand

against the ever vocal youth league while industry’s response can best be described as timid and

somewhat limp-wristed. The debate has been conducted within a vacuum of leadership.

As a point of departure, it is vital to appreciate that this debate is not about nationalisation. Rather,

nationalisation is a proxy for much more serious political economic and structural flaws in the South

African body politic. While populist rhetoric carries the torch of nationalisation as a placebo for the

economic ills facing the poor, White business tends to see the issue of nationalisation as being an election

ploy exploited to the limit by the ANCYL firebrand, Julius Malema. There is the naïve perception that since

he has been suspended the problem has been resolved. This has been confirmed by the pronouncements

at the South African Mining Indaba by the Minister of Mineral Resources, Susan Shabangu, that

nationalisation is not an option. Were it this simple it would be a much more manageable situation.

This study commenced in August 2011 at the height of the confrontation over the nationalisation issue.

Recognising that the debate lacked structure and that few people understood or appreciated the nature

and extent of the issues underlying the contretemps, the Southern African Institute of Mining and

Metallurgy (SAIMM) elected to deliver a report that would broaden the debate to other stakeholders. The

principal objective of the study was to facilitate and inform a rational, non-ideological dialogue to engender

an understanding of the real underlying issues to those South Africans who are materially affected by the

debate. This understanding could be used as a basis for qualified discussion directed towards reaching a

pragmatic and achievable outcome that will be in the broader national interest. It is an important

qualification that the study was undertaken prior to the release of the ANC State Intervention in the

Minerals Sector study (SIMS). The close correlation between the findings of this study and those of the

SIMS study are unsurprising given the respective closely aligned focuses of the studies. The primary

difference is however one of ideological interpretation. The ANC document provides the basis for policy

recommendations to the National Executive Committee (NEC) while the SAIMM study strives to inform

dialogue on the issues at hand and to equip those stakeholders who intend contributing to the debate to

make qualified decisions and inputs to the process.

Key objectives of this study were to:

develop an understanding of the concept of resource nationalism, its facets, related issues, and the

collateral forms of state intervention

interrogate the global repository of literature to establish best practice guidelines (what works and

what does not work)

Southern African Institute of Mining and Metallurgy The Rise of Resource Nationalism?

A Study to Inform Multi-stakeholder Dialogue on State-Participation in Mining

© Southern African Institute of Mining and Metallurgy

P a g e | 23