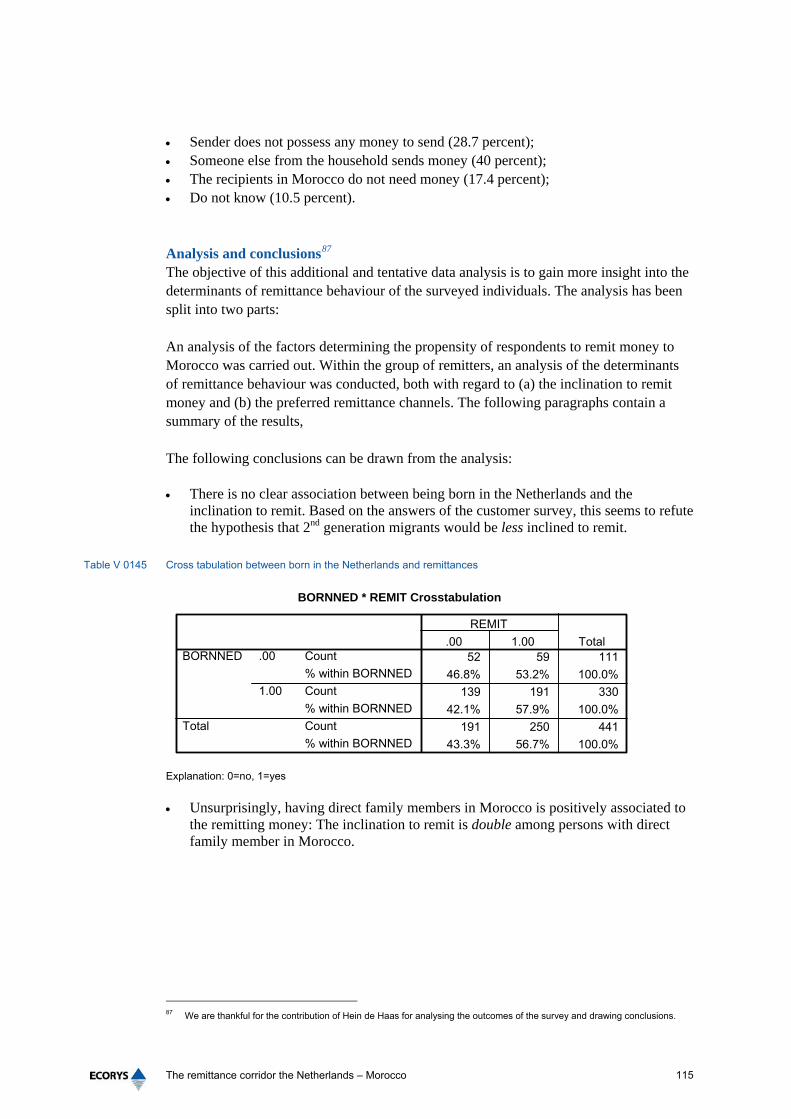

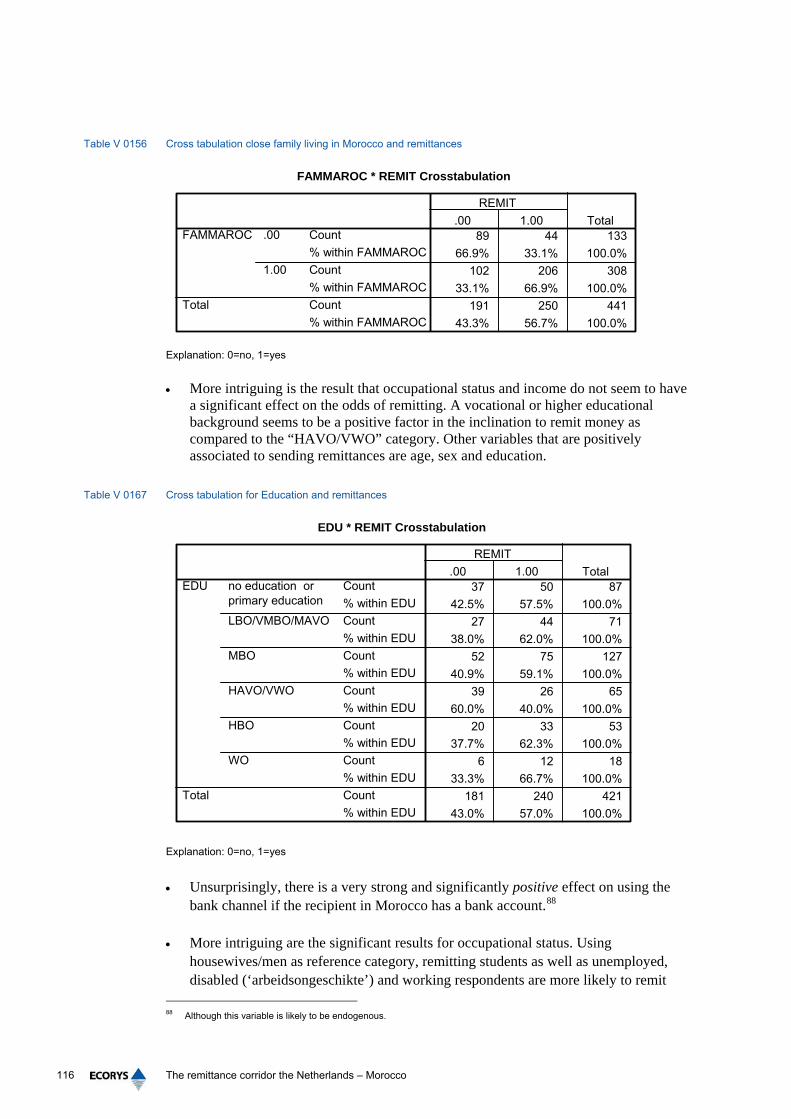

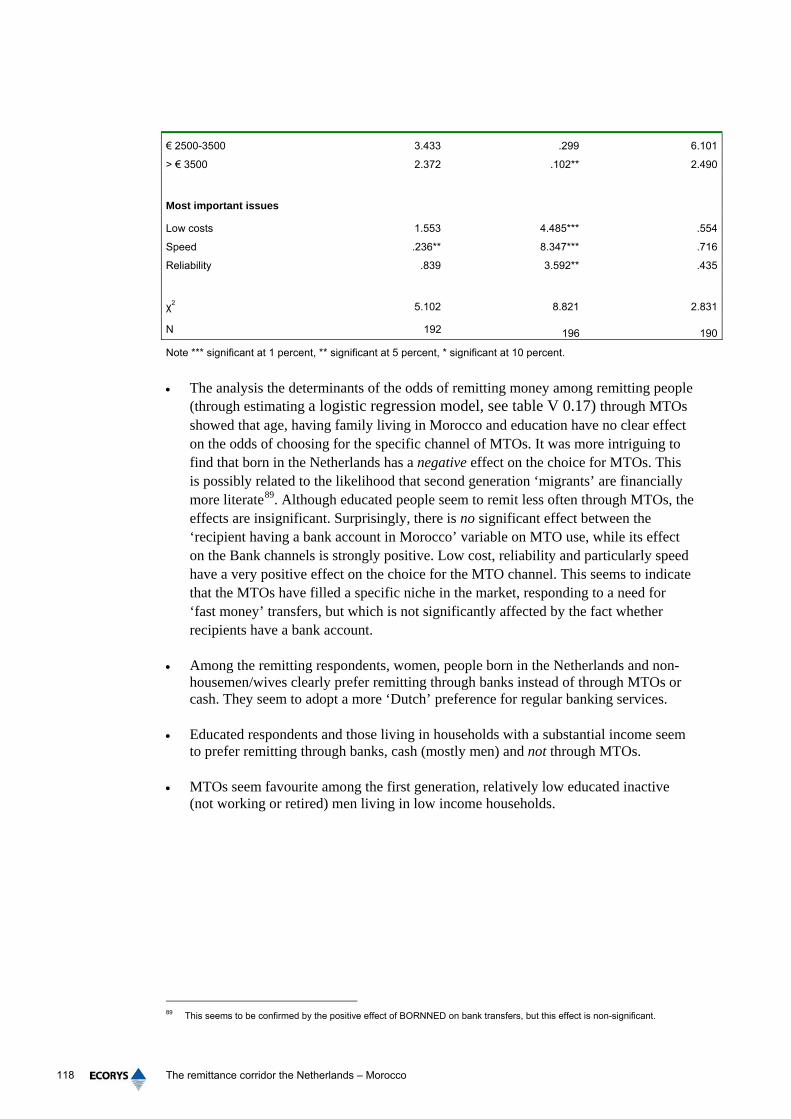

The Remittance Corridor of the...

119

Jacqueline Barendse, Christian Hiddink, Agnes Janszen, and Arjan Stavast The Remittance Corridor of the Netherlands–Morocco Review of obstacles and recommendations on how to increase use of the bank channel

Transcript of The Remittance Corridor of the...

Jacqueline Barendse, Christian Hiddink,Agnes Janszen, and Arjan Stavast

The Remittance Corridorof the Netherlands–Morocco

Review of obstacles and recommendationson how to increase use of the bank channel

The remittance corridor the Netherlands – Morocco Review of obstacles and recommendations on how to increase the use of the bank channel

Client: Netherlands Financial Sector Development Exchange (NFX)

ECORYS Nederland BV Jacqueline Barendse Christian Hiddink Agnes Janszen Arjan Stavast

Rotterdam, 27 October 2006

The authors take full responsibility for the contents of this report. The opinions expressed do not necessarily reflect the view of Netherlands Financial Development Exchange (NFX).

DS/AV14693

ECORYS Nederland BV

P.O. Box 4175

3006 AD Rotterdam

Watermanweg 44

3067 GG Rotterdam

The Netherlands

T +31 (0)10 453 88 00

F +31 (0)10 453 07 68

W www.ecorys.com

Registration no. 24316726

ECORYS Macro & Sector Policies

T +31 (0)31 (0)10 453 87 53

F +31 (0)10 452 36 60

DS/AV14693

Table of contents

List of abbreviations 9

Preface 11

Summary 13

1 Introduction 21 1.1 Introduction 21 1.2 Setting the scene 21 1.3 Why this study? 22 1.4 Objective of the study 23 1.5 Approach and methodology 24 1.6 Outline of this report 25

2 Migrants and remittances 27 2.1 Introduction 27 2.2 Moroccan migrants 27

2.2.1 Setting the scene 27 2.2.2 Moroccans in the Netherlands 28 2.2.3 Main facts 34

2.3 Remittances 34 2.3.1 Setting the scene 35 2.3.2 Remittances in the corridor the Netherlands – Morocco 36

2.4 Main facts and findings 40

3 First mile 41 3.1 Introduction 41 3.2 How to send money? 41 3.3 What are the formal channels in the Netherlands? 41

3.3.1 The banking sector in the Netherlands 41 3.3.2 Postbank 43 3.3.3 Money Transfer Organisations 44

3.4 How is the remittance market regulated? 45 3.4.1 Regulation in the European Union 45 3.4.2 Regulation in the Netherlands 46

3.5 Main findings for the first mile 48

4 Intermediate stage 51 4.1 Introduction 51

4.2 Who is remitting and what influences the choice of channel? 51 4.3 What are the market shares? 53

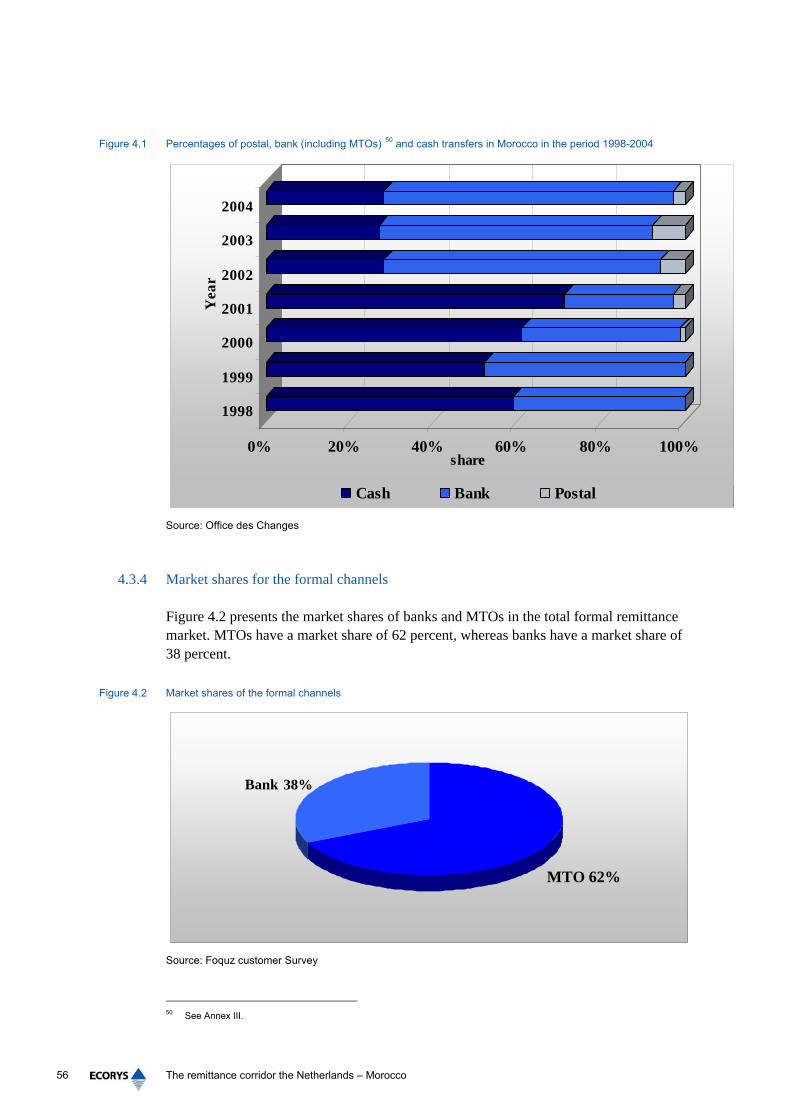

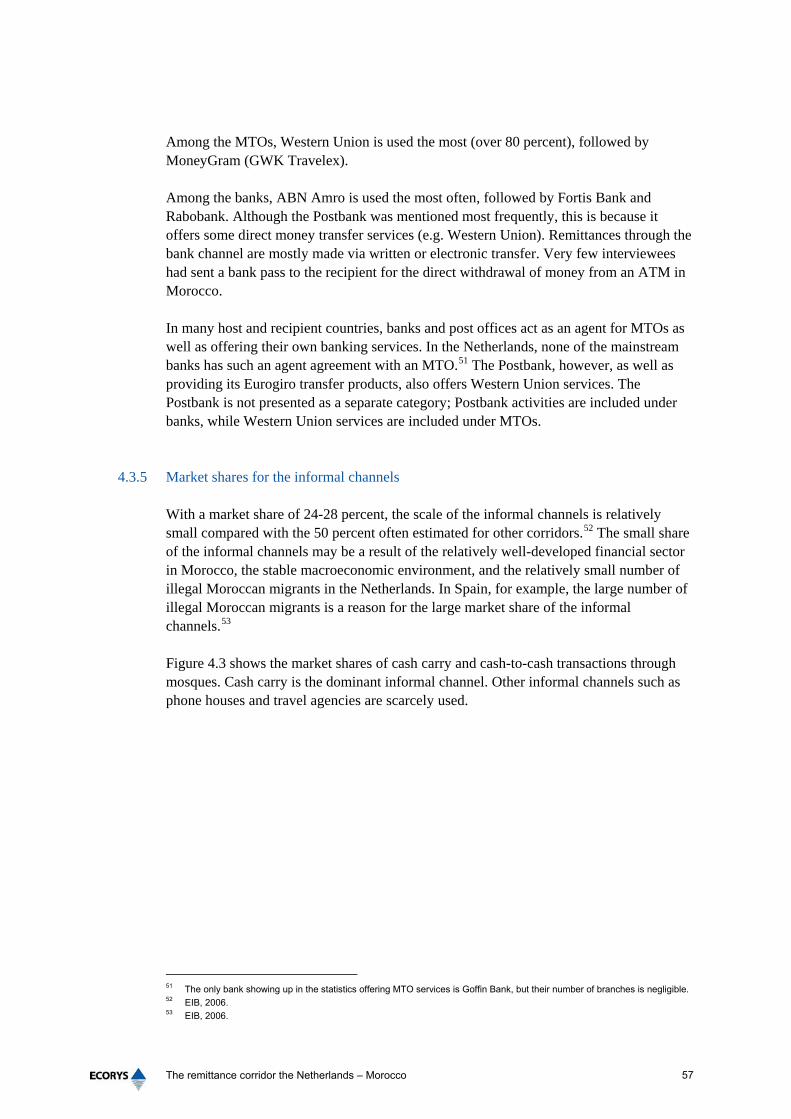

4.3.1 How much is remitted through which channel? 53 4.3.2 Different estimates of market shares 54 4.3.3 Cash-based remittances 55 4.3.4 Market shares for the formal channels 56 4.3.5 Market shares for the informal channels 57

4.4 Costs, speed, transparency and requirements of transfers 58 4.5 Main findings for the intermediate stage 60

5 Last mile 63 5.1 Introduction 63 5.2 Setting the scene 63 5.3 What are remittances used for and where are they sent to? 63 5.4 What are the formal channels in Morocco? 66

5.4.1 The banking sector in Morocco 67 5.4.2 The post office 68 5.4.3 Money Transfer Organisations 69

5.5 Support to Moroccan migrants 69 5.6 Main findings for the last mile 70

6 Factors hampering remittances through formal channels 71 6.1 Introduction 71 6.2 What is hampering the use of formal channels? 71 6.3 Inefficiency of formal systems 72

6.3.1 Transparency and customer protection 72 6.3.2 Payment system infrastructure 73 6.3.3 Legal and regulatory framework 74 6.3.4 Market structure and competition 75 6.3.5 Governance and risk management 77

6.4 Potential to further formalise remittance streams? 77

7 Increasing remittances through the bank channel 79 7.1 Introduction 79

7.1.1 Background and rationale 79 7.2 Factors hampering increased use of the bank channel 79

7.2.1 Preference for cash 80 7.2.2 Preference for counter transactions 80 7.2.3 Lack of adequate products offered by banks 81 7.2.4 Lack of transparency 83 7.2.5 Absence of a commercially beneficial business case 84

7.3 Is there potential to increase use of the bank channel? 85

Annex I References 89

Annex II Real money transfers 95

Annex III Definitions of migrants and remittances 101

DS/AV14693

Annex IV Remittances peak in 2001 105

Annex V Results of customer survey 107

The remittance corridor the Netherlands – Morocco 9

List of abbreviations

AMAP Accelerated Microenterprise Advancement Project ATM Automated Teller Machine BAM Barid-Al Maghrib (post office in Morocco) BIS Bank for International Settlements BP Banque Populaire BRCA Bilateral Remittances Corridor Analysis CBS Central Bureau of Statistics DFID Department for International Development DGIS Department for Development Cooperation of the Ministry of Foreign

Affairs DNB De Nederlandse Bank EIB European Investment Bank EIM Economisch Insituut voor het Midden- en kleinbedrijf EU European Union GDP Gross domestic product GEP Global Economic Prospects GWK Grens Wissel Kantoor IBAN International Bank Account Number IMF International Monetary Fund INSEA Institut National de Statistique et d’Economie Appliquée MRE Marocain résidant a l’étranger MTO Money Transfer Organisation NCDO Nationale Commissie voor internationale samenwerking en Duurzame

Ontwikkeling NFX Netherlands Financial Sector Development Exchange OdC Office des Changes RSP Remittance service provider RTGS Real-time Gross Settlement SEPA Single European Payment Area STP Straight-through processing SWIFT Society for Worldwide Interbank Financial Telecommunication TPG TNT Post Group UK United Kingdom Wgt Wet geldtransactiekantoren Wtk Wet Toezicht Kredietwezen WID Wet Identificatie bij Dienstverlening

The remittance corridor the Netherlands – Morocco 11

Preface

The Netherlands Financial Sector Development Exchange (NFX) has asked ECORYS to analyse the remittance corridor the Netherlands – Morocco and make recommendations leading to a further increase in the use of formal channels and to strengthen the role of banks in particular. A customer survey was also part of this study. This survey was conducted by Foquz Etnomarketing, a company specialising in research on ethnic groups. We are grateful for the pleasant cooperation with NFX and Jacco Knotnerus in particular. We like to thank Hans Boon (ING Bank) and Hein de Haas (University of Oxford) who provided valuable input. In addition, we thank Mohamed Khachani for his cooperation during our visit to Morocco. Furthermore, the project team would like to express its gratitude to representatives of Dutch and Moroccan banks, the Dutch Central Bank (DNB), Statistics Netherlands (CBS), Bank Al-Maghrib, King Hassan II foundation and Office des Changes. The (telephone) interviews with these organisations supported us to gain a good understanding of the remittance corridor the Netherlands - Morocco. We want to stress that the authors take full responsibility for the contents of this report and that the opinions expressed do not necessarily reflect the view of NFX. Jacqueline Barendse Christian Hiddink Agnes Janszen Arjan Stavast

The remittance corridor the Netherlands – Morocco 13

Summary

Objective of the study The Netherlands Financial Sector Development Exchange (NFX) has asked ECORYS to analyse the remittance corridor the Netherlands – Morocco and make recommendations leading to a further increase in the use of formal channels and to strengthen the role of banks in particular. The recommendations should be directed towards Dutch and Moroccan banks, governments and other players in both sending and receiving countries. The following five research questions were formulated in the Terms of Reference: 1. What is the size of formal and informal remittance flows from the Netherlands to

Morocco? 2. What are the main distribution channels? 3. What are the major factors that influence the choice between informal and formal

channels? 4. Is there potential to further formalise the remittance stream in the corridor the

Netherlands – Morocco? If there is such a potential, draft concrete and practical actions;

5. What is hampering the increase of remittance flows through the bank channel in the corridor the Netherlands – Morocco? If there are hampering factors, draft concrete and practical actions to address them.

The study should contribute to the body of knowledge on remittances and should allow for (future) comparisons between corridors. Working method We have used the Bilateral Remittances Corridor Analysis (BRCA) Methodology of the World Bank for this corridor study.1 The principle of this methodology is simple: it follows the money from sender to receiver and addresses all relevant aspects of the corridor. The five main research questions were analysed with the help of desk research, interviews in Morocco, expert feedback, a customer survey among Moroccan migrants in the Netherlands, and interviews with representatives of the Dutch bank sector. Moroccan migrants

1 World Bank, 2005.

The remittance corridor the Netherlands – Morocco 14

With about 325,000 migrants of Moroccan origin, the Moroccan community is the fourth largest non-Western migrant group in the Netherlands. The Moroccan migrant community is expected to grow by 11 percent (approximately 360,000) to 2010, mainly as a result of an increase in the number of second-generation Moroccans. After 2010, the growth rate is expected to decrease. Migrants of Moroccan origin predominantly live in the cities of Amsterdam, Utrecht, Rotterdam and The Hague. Size of the total remittances flow Remittance data for the corridor Netherlands – Morocco are ambiguous. There are considerable differences in how remittances are recorded in the Netherlands and Morocco, leading to different estimates of the size of the total remittance flow. Combined with information from customer surveys, we estimate that about EUR 93-132 million was remitted in 2004. Remittances have increased moderately over the last ten years. Based on historic trend analysis and the moderate growth of the migrant community, we expect that the volume of remittances will also grow moderately in the coming years. Use of remittances and regional destination The customer survey showed that remittances are mostly sent for food (23 percent), healthcare (16 percent) and housing (15 percent). The majority of recipients have other sources of income, but nearly 30 percent of senders stated that their recipients are completely dependent on the remittances they send. The most important destination regions are the Rif area and Great Casablanca. These percentages coincide with available information on the origin of Moroccans in the Netherlands. The largest group of Moroccan migrants (about 40 percent) originate from the northern part of Morocco (Rif mountains). Size of formal and informal remittance flows We estimate that around 71-76 percent of the remittances flow through formal channels (banks and Money Transfer Organisations). Approximately 24-28 percent of the remittances flow through informal channels, involving mainly cash carriage which constitutes more than 70 percent of the remittances though informal channels. International comparisons indicate that a fraction of more than 70 percent of remittances through formal channels to a developing country is rather high. Main distribution channels Around 70 percent of remittances turnover are cash-based, entailing cash handling in both Morocco and the Netherlands. The customer survey indicated that about 47 percent is remitted through Money Transfer Organisations (MTOs) involving cash transfers on both sides, 16 percent is cash carried by individuals and 6 percent is cash-based transfers

The remittance corridor the Netherlands – Morocco 15

through mosques. Given the advanced level of development of the Dutch financial system and the relatively high level of development of the financial sector in Morocco, it is striking to see such a high percentage of cash-based remittances. MTOs The most important MTOs in the corridor are Western Union and MoneyGram, which hold about 62 percent of the formal remittances market segment. In the Netherlands, Western Union seems to be the dominant player. The customer survey indicated that at least three-quarters of MTO transfers are conducted by Western Union; fewer than a quarter are through MoneyGram. Western Union uses the network of post offices in the Netherlands, while MoneyGram uses the GWK (Grens Wissel Kantoor) network. Banks The banks have approximately 38 percent of the market share within the formal channels. ABN Amro is most often used, followed by Fortis Bank and Rabobank. There are no Moroccan banks active in the Netherlands. In Morocco, the most important banks for remittance transfers are Banque Populaire (BP) and Banque Credit du Maroc. We expect that Bank Populaire channels the majority of remittances from the Netherlands, because it channels approximately 60 percent of all incoming remittances of both banks and MTO (MoneyGram). Banks and MTOs have in common that nearly all of their remittance transfers go over the counter: 100 percent of MTO transfers and about 60 percent of all bank transfers. Informal channels Cash carried by individuals is the most important informal transfer method, channelling 16 percent of the total remittance flow. In addition to carrying cash, informal transfers are made through mosques. Other informal channels such as phone houses and travel agencies are hardly used. Factors influencing the choice of informal and formal channels Factors influencing the choice of formal channels are listed below. We have not found clear factors determining the choice of informal channels. Occupational status Migrants’ occupational status seems to influence highly the choice of the bank sector. Remitters who are active in the labour market, unemployed or students are more likely to remit through the banks than retirees, housewives and others. In addition, the availability of a bank account for the recipient affects positively the choice of the bank channel. The combination of both factors significantly increases the propensity to choose the bank channel. Preferred frequency and speed of remittances The choice of a particular channel is also determined by how often remitters want to transfer money and the preferred speed of the transfer. Remitters use banks one to four times per year, whereas migrants using MTOs send money more often. When the speed

The remittance corridor the Netherlands – Morocco 16

of the transaction is important, MTOs are used. High-income earners seem to remit more often than low-income earners. However, well-educated high-income earners choose banks and carrying cash instead of MTOs, despite their higher remittance frequency. First or second-generation migrants Second (and subsequent) generations of migrants seem to have a higher tendency to use the bank channel, whereas the first generation seems to favour MTOs. If a first-generation migrant is also inactive (unemployed or retired) and has a lower educational background, the preference for MTOs increases. This difference between first and second-generation migrants could be explained by second (and subsequent) generation migrants probably being more financially literate. What are the hampering factors to formalise remittances? Factors hampering the use of formal channels are related to inefficiencies in the formal systems. Based on the General Principles for international remittance services,2 we located inefficiencies relating to transparency and the payment infrastructure. Furthermore, we also identified some deficiencies in the market structure and a lack of competition. Transparency The formal remittance market is not transparent. Product information can only be obtained through actual use of the different transfer services. MTOs are transparent on fee costs and speed prior to the transaction, but only provide exchange rate costs when the transaction takes place. The bank channel seems even less transparent. With the exception of Postbank, Dutch banks do not provide information on total fee costs prior to the transaction. Furthermore, banks do not provide information on exchange rates and only give an estimate of the transaction time. Fees charged by the correspondent bank are presented after the transaction. Payment system infrastructure The payment infrastructure is made up of the payment systems in both countries and cross-border payment and clearing systems. MTOs have dedicated payment infrastructures which are efficient. The banks rely on the correspondent banking system for their payments. However, the correspondent banking system seems to be inadequate for remittances, because it cannot supply exact information on speed and fee costs. Furthermore, the Moroccan giro system is still underdeveloped, despite financial sector reforms. This hampers further development of a more efficient payment infrastructure for the bank channel. Physical access points are part of the payment infrastructure. The customer survey indicated that Moroccan migrants still prefer to use counters for their transactions. The number of access points (banks and MTOs) has decreased rapidly in the Netherlands over the last ten years.

2 World Bank and BIS, 2006 and www.bis.org.

The remittance corridor the Netherlands – Morocco 17

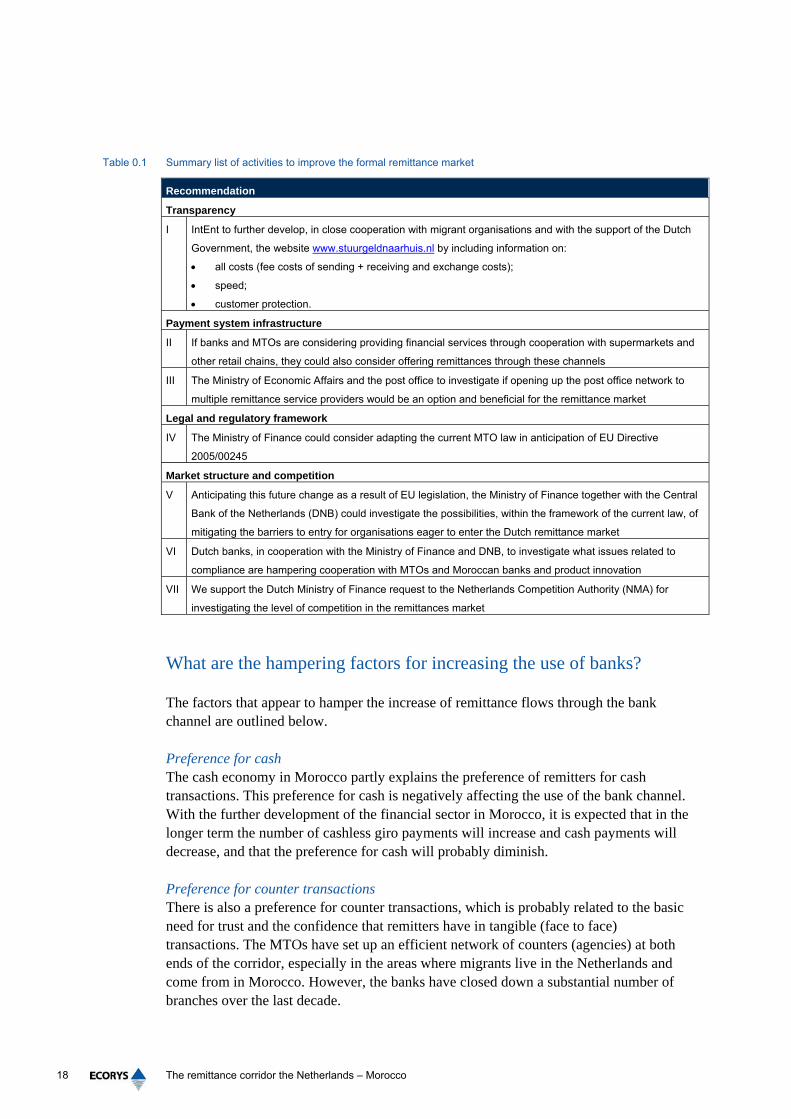

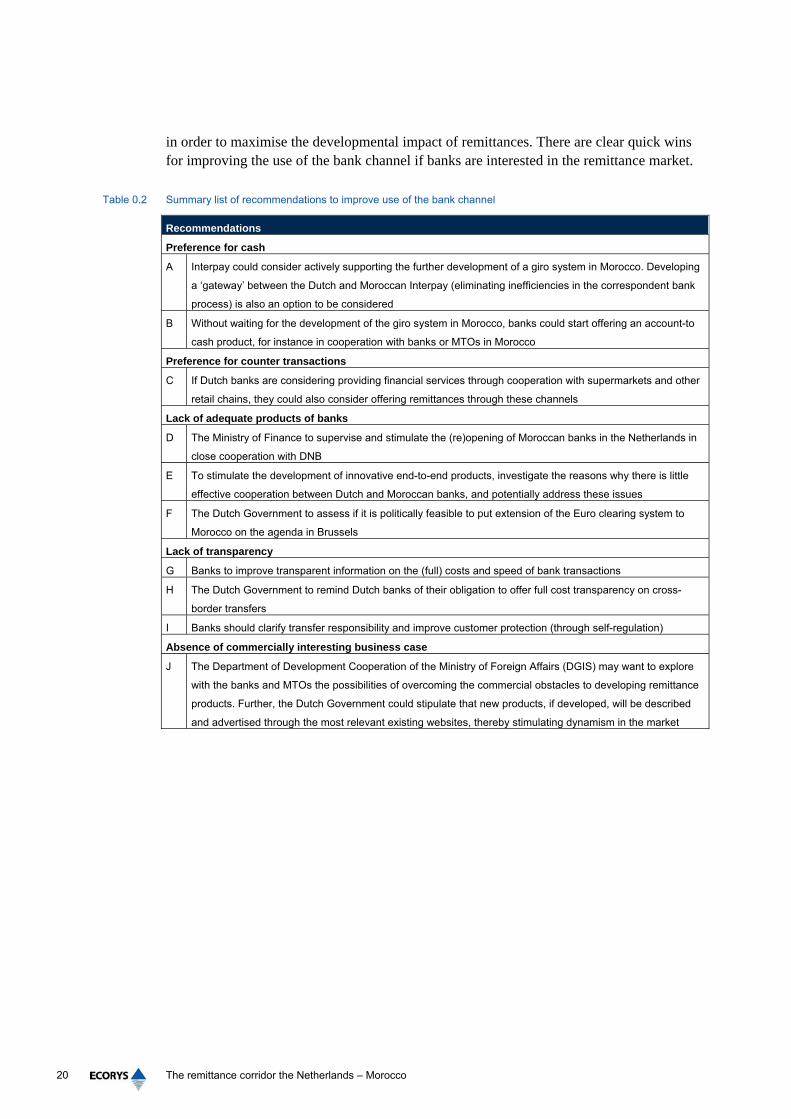

Market structure and competition Competition among service providers is not optimal, because transparency is lacking. Furthermore, there seem to be barriers for entry to the Dutch remittances market. Although the market for remittances is regarded as attractive by a number of Moroccan banks and foreign MTOs, no new players have entered the remittance market in the Netherlands recently. On the contrary, the Moroccan banks that were active in the Netherlands have left the market. The problems that these organisations have appear to be related to the Dutch law on MTOs and the fact that a Dutch banking licence is needed for Moroccan banks to offer remittance services. As both organisations have strong positions in other European Union (EU) countries, their absence from the Dutch market gives rise to the question: “Is the Dutch law and supervision (interpretation of the law) on banks and on MTOs stricter than similar laws in other EU countries?” This situation will change in the future, as a consequence of the further development of the Single European Payment Area and the adoption of the New Legal Framework. Furthermore, banks and MTOs will be allowed to offer their services in all EU countries once they have acquired a licence in one EU country. Interviews with representatives of the Dutch bank sector also made it clear that none of the Dutch banks cooperate with Moroccan banks and MTOs, because of a number of reasons e.g. (perceived) compliance costs and no possibilities for commercially interesting co-operation. A lack of cooperation hampers market innovations, such as the development of new end-to-end products. Is there potential to further formalise? Table 0.1 presents a summary list of activities that could be undertaken to make the remittance market more efficient. The potential for further formalising the remittance market lies mainly in eliminating inefficiencies in the formal market. However, the market share of the formal channels is already high, at over 70 percent. Therefore, in the short term these measures would be more likely to spark a shift of market shares within the formal channels than between the informal and formal channels. In the medium term, we expect that the market share of the informal channels could decrease further if Moroccan society becomes less cash oriented through the development of giro payment systems.

The remittance corridor the Netherlands – Morocco 18

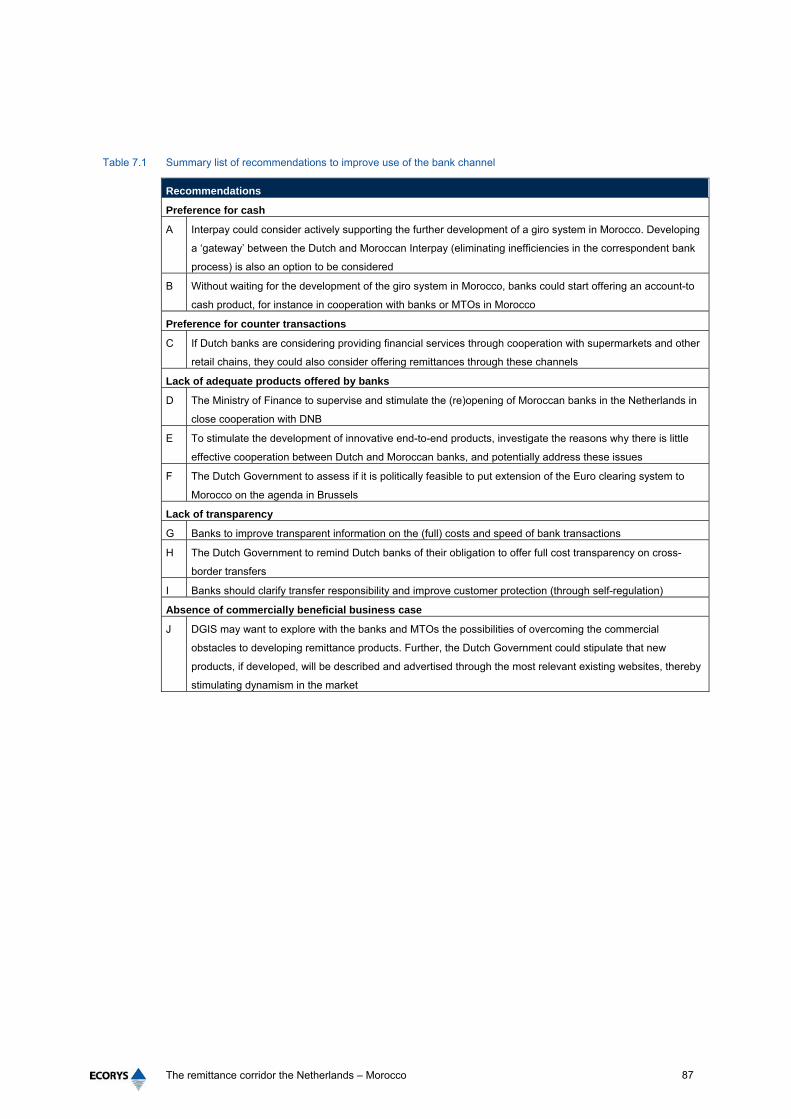

Table 0.1 Summary list of activities to improve the formal remittance market

Recommendation

Transparency

I IntEnt to further develop, in close cooperation with migrant organisations and with the support of the Dutch

Government, the website www.stuurgeldnaarhuis.nl by including information on:

• all costs (fee costs of sending + receiving and exchange costs);

• speed;

• customer protection.

Payment system infrastructure

II If banks and MTOs are considering providing financial services through cooperation with supermarkets and

other retail chains, they could also consider offering remittances through these channels

III The Ministry of Economic Affairs and the post office to investigate if opening up the post office network to

multiple remittance service providers would be an option and beneficial for the remittance market

Legal and regulatory framework

IV The Ministry of Finance could consider adapting the current MTO law in anticipation of EU Directive

2005/00245

Market structure and competition

V Anticipating this future change as a result of EU legislation, the Ministry of Finance together with the Central

Bank of the Netherlands (DNB) could investigate the possibilities, within the framework of the current law, of

mitigating the barriers to entry for organisations eager to enter the Dutch remittance market

VI Dutch banks, in cooperation with the Ministry of Finance and DNB, to investigate what issues related to

compliance are hampering cooperation with MTOs and Moroccan banks and product innovation

VII We support the Dutch Ministry of Finance request to the Netherlands Competition Authority (NMA) for

investigating the level of competition in the remittances market

What are the hampering factors for increasing the use of banks? The factors that appear to hamper the increase of remittance flows through the bank channel are outlined below. Preference for cash The cash economy in Morocco partly explains the preference of remitters for cash transactions. This preference for cash is negatively affecting the use of the bank channel. With the further development of the financial sector in Morocco, it is expected that in the longer term the number of cashless giro payments will increase and cash payments will decrease, and that the preference for cash will probably diminish. Preference for counter transactions There is also a preference for counter transactions, which is probably related to the basic need for trust and the confidence that remitters have in tangible (face to face) transactions. The MTOs have set up an efficient network of counters (agencies) at both ends of the corridor, especially in the areas where migrants live in the Netherlands and come from in Morocco. However, the banks have closed down a substantial number of branches over the last decade.

The remittance corridor the Netherlands – Morocco 19

Lack of adequate products offered by banks There is a lack of adequate remittance products offered by banks. This can be explained by a number of factors: 1. absence of competition by Moroccan banks in the Dutch market; 2. barriers in the correspondent banking system; 3. lack of cooperation between Dutch and Moroccan banks. The absence of Moroccan banks in the Netherlands is especially unfortunate as these banks have made it their business to offer attractive (remittance) services to migrants. The lack of adequate remittance products also lies in the cross-border payment system. Financial cross-border transactions are conducted using the correspondent banking system based on the SWIFT (Society for Worldwide Interbank Financial Telecommunication) transactions standards. The way that this system operates means that banks do not control the chain from end to end. In addition, it seems that Dutch banks are not cooperating effectively with Moroccan banks. This hampers the development of innovative end-to-end products. Lack of transparency Lack of transparency in the costs and speed of remittances, caused by the correspondent banking system, is also hampering the flow of remittances through banks. The correspondent banking system does not allow banks to provide their clients with the information needed to establish trust in the product. Most banks cannot give information on speed and price prior to the transaction. For information on costs (fee and exchange rate) and the speed of the transaction, the sending bank is dependent on the information provided and the fees charged by the correspondent banks in the chain. Another aspect of transparency is customer protection. It seems that most banks have less straightforward customer protection than MTOs. Absence of a commercially beneficial business case Dutch banks, with the exception of Rabobank, are not developing specific products for migrants and nor do they regard migrants as a specific target group. For two reasons, the commercial benefits for Dutch banks to (further) develop and introduce remittance products are not obvious. First, though the Netherlands is home to a large number of non-Western immigrants, each group in itself may be too small to justify the development of a dedicated product. Secondly, the banks that were interviewed often indicated that this product on its own is not commercially interesting. The driving factor for Rabobank is the philosophy that its customer base should be a reflection of society, probably using the remittance products to attract new Rabobank clients. Developing products targeting at the entire migrant community in the Netherlands is not a real alternative, as corridor studies on remittances clearly show that each corridor has specific issues which cannot be solved with general products. Is there potential to increase the use of the bank channel? Table 0.2 present a summary list of recommendations to improve the use of the bank channel. It is the challenge of the banking sector to turn cash transactions into giro flows

The remittance corridor the Netherlands – Morocco 20

in order to maximise the developmental impact of remittances. There are clear quick wins for improving the use of the bank channel if banks are interested in the remittance market.

Table 0.2 Summary list of recommendations to improve use of the bank channel

Recommendations

Preference for cash

A Interpay could consider actively supporting the further development of a giro system in Morocco. Developing

a ‘gateway’ between the Dutch and Moroccan Interpay (eliminating inefficiencies in the correspondent bank

process) is also an option to be considered

B Without waiting for the development of the giro system in Morocco, banks could start offering an account-to

cash product, for instance in cooperation with banks or MTOs in Morocco

Preference for counter transactions

C If Dutch banks are considering providing financial services through cooperation with supermarkets and other

retail chains, they could also consider offering remittances through these channels

Lack of adequate products of banks

D The Ministry of Finance to supervise and stimulate the (re)opening of Moroccan banks in the Netherlands in

close cooperation with DNB

E To stimulate the development of innovative end-to-end products, investigate the reasons why there is little

effective cooperation between Dutch and Moroccan banks, and potentially address these issues

F The Dutch Government to assess if it is politically feasible to put extension of the Euro clearing system to

Morocco on the agenda in Brussels

Lack of transparency

G Banks to improve transparent information on the (full) costs and speed of bank transactions

H The Dutch Government to remind Dutch banks of their obligation to offer full cost transparency on cross-

border transfers

I Banks should clarify transfer responsibility and improve customer protection (through self-regulation)

Absence of commercially interesting business case

J The Department of Development Cooperation of the Ministry of Foreign Affairs (DGIS) may want to explore

with the banks and MTOs the possibilities of overcoming the commercial obstacles to developing remittance

products. Further, the Dutch Government could stipulate that new products, if developed, will be described

and advertised through the most relevant existing websites, thereby stimulating dynamism in the market

The remittance corridor the Netherlands – Morocco 21

1 Introduction

1.1 Introduction

The Netherlands Financial Sector Development Exchange (NFX) has asked ECORYS to analyse the remittance corridor the Netherlands – Morocco and make recommendations leading to a further increase in the use of formal channels and to strengthen the role of banks in particular. These recommendations should contain actions for Dutch and Moroccan banks, governments and other players in both countries. Section 1.2 sets the scene for this corridor analysis. Section 1.3 elaborates on the objectives of this study, while section 1.4 presents the research approach. Section 1.5 then finishes with an outline of this report.

1.2 Setting the scene

What are remittances? Remittances are the money that migrants send to related people (family and friends) or into personal (bank) accounts from the migration destination (host country) to the place of origin (home country).3 The most important features of them are that: • remittances are cross-border transactions; • remittances are transactions from migrants to related people; • remittances usually involve the transfer of a relatively small sum of money. Global developments Remittance flows represent a major source of international finance. The World Bank estimated officially recorded remittance-related flows worldwide at $ 232 billion in 2005. This amount is equivalent to one third of the gross domestic product (GDP) of the Netherlands. Developing countries are the main beneficiary of remittances. More than 70 percent of all remittances sent last year were sent to developing countries. In 2000, the total recorded remittance flow was estimated to be $ 131 billion. So in the last five years, remittances have almost doubled.4 These estimates of the recorded remittances probably only form half of the actual flow or remittances, since it is estimated that informal (non-recorded) channels account for 50 percent of total remittances sent.

3 This definition is derived from the European Investment Bank (EIB) study (2006) on remittances, which reformulated the

International Monetary Fund (IMF) definition to a more operational level. 4 World Bank (2006) Global Economic Prospects (GEP).

The remittance corridor the Netherlands – Morocco 22

This impressive growth in remittances has given rise to the international interest of politicians, development organisations, private banks, other private financial organisations and researchers. Remittances from the Netherlands According to balance of payment statistics, migrants in the Netherlands sent ‘home’ approximately EUR 670 million in 2005.5 In 1995, this remittance flow was estimated at EUR 300 million. The Ministry of Finance states that this increase in remittances is caused by the increase of migrants in this period. In 2006, the Netherlands is home to about 3.2 million migrants, of whom about 1.7 million are non-Western migrants. Why are remittances important? Politicians and international financial institutions recognise the developmental impact of remittances for developing countries. For many developing countries, remittances are an important source of income (and foreign currencies) comparable or larger than foreign aid and foreign direct investments. The World Bank also points out that remittances can improve a country’s creditworthiness, as traditional indicators of vulnerability, such as debt to export ratios, would rise significantly in the absence of remittance inflows. Furthermore, the securitisation of remittance flows can raise a country’s external access to finance and reduce financing costs. On a micro level, household surveys and studies generally support the notion that remittances reduce poverty, smooth consumption when income is hit by shocks, and increase investment in education and health. Why is the bank channel important? Remittances through banks provide a potentially higher multiplier effect from remittance flows. Remittances through banks are more likely to stay within the domestic banking system (i.e. deposited in bank accounts), thus increasing the asset base of banks and allowing them to increase their on-lending activities. Furthermore, an increase in the use of the bank channel offers the opportunity to securitise future remittance flows by developing capital market instruments like, for example, remittance-backed bonds. These instruments will help in mobilising additional (domestic and foreign) savings for further on lending in Morocco.

1.3 Why this study?

The costs of remitting money (fees and exchange rate costs) were the subject of questions in Parliament in 2003 and 2005. In both cases, Members of Parliament asked the Minister of Finance for measures to reduce these costs. In 2003, the Minister of Finance answered that the remittance market in the Netherlands is open and that there is enough competition. The Minister further remarked that migrants have a choice of reducing the frequency of remittances and increasing the amounts, so that the costs can be reduced. In a letter to Parliament in 2006, the Minister confirmed his earlier standpoints, but promised to conduct further research.6 He refers to this study on the corridor Netherlands

5 Tweede Kamer, vergaderjaar 2005-2006, 26234 nr. 56. 6 Tweede Kamer, vergaderjaar 2005-2006, 26234 nr. 56.

The remittance corridor the Netherlands – Morocco 23

– Morocco commissioned by NFX and to a study on the corridor Netherlands – Suriname for which the Ministry of Finance is the commissioner. NFX acknowledges the possible contribution that remittances can make to the development of the financial sector in developing countries. NFX has chosen a corridor approach and selected the corridor Netherlands – Morocco. This corridor is of particular interest because: • Moroccan migrants are one of the most important migrant populations in the

Netherlands; • The level of formalisation of the remittance flow in the corridor Netherlands –

Morocco is unclear. There is a study indicating a low level of formality.7 However, the Moroccan economy has been stable for the last few years and the financial sector in Morocco is already relatively well developed and improving.8 This would indicate a high level of formality and/or prospects for increasing the use of formal channels.

1.4 Objective of the study

The objective of this study is to analyse the remittance corridor the Netherlands – Morocco. If there is potential to further increase the use of formal channels, then recommendations should be elaborated to increase the use of these channels. Furthermore, specific recommendations should be geared at strengthening the role of banks in particular. These recommendations should be directed towards Dutch and Moroccan banks, governments and other players in both countries. The objective has been translated into five research questions: 1. What is the size of formal and informal remittance flows from the Netherlands to

Morocco? 2. What are the main distribution channels? 3. What are the major factors that influence the choice between informal and formal

channels? 4. Is there potential to formalise the remittance stream in the corridor the Netherlands –

Morocco? If there is such a potential, draft concrete and practical actions. 5. What is hampering the increase of remittance flows through the bank channel in the

corridor the Netherlands – Morocco? If there are hampering factors, draft concrete and practical actions to address them.

NFX also required that the study should contribute to the body of knowledge on remittances, and should allow for future comparison between corridors.

7 NCDO, 2005. 8 The Terms of Reference mention a percentage of formal channels of 38 percent and an estimated remittance flow of

EUR200-300 million per year in the Netherlands – Morocco corridor.

The remittance corridor the Netherlands – Morocco 24

1.5 Approach and methodology

Methodology The Bilateral Remittances Corridor Analysis (BRCA) Methodology of the World Bank was chosen, as it provides a systematic method of comprehensive data collection and permits future comparison analysis, since it has also been used for other corridor studies.9 The principle of this methodology is simple: it follows the money from sender to receiver, and by doing so addresses all relevant aspects of the corridor. The methodology is based on three stages: • the first mile of the transfer; • the intermediary stage; • the last mile of the transfer. Data collection We have collected information from research on remittances, balance of payments, regulatory frameworks and governance procedures. In addition, we have implemented a customer survey, in particular targeting migrants of Moroccan origin in the Netherlands. This customer survey was conducted by Foquz Etnomarketing, a company specialising in research on ethnic groups.10 This survey provided us with valuable information on Moroccan migrants in the Netherlands, their remittance behaviour and their preferences. The survey results helped us to verify some of the findings of our desk research. But more importantly, it gave us information to answer the question of how the bank channel can be improved. A visit to Morocco was also part of our data-collection phase. We interviewed various relevant government bodies and financial institutions. Unfortunately, despite many attempts, banks in Morocco were not willing to discuss remittances. Therefore, only one bank was interviewed. Additionally, we interviewed key stakeholders in the Dutch banking sector. These interviews were used to verify our findings and our recommendations to improve the use of the bank channel. We also conducted own remittance transactions. These transactions not only led to a better understanding of remittance transfers in themselves – they also provided valuable information on real transaction costs, speed and procedures. Finally, expert reviews provided valuable inputs for our study. We are thankful for the inputs and suggestions of Hein de Haas, a renowned researcher on Morocco (with a focus on migration and remittances) at the University of Oxford, and Hans Boon, an expert in the field of (postal) banking and remittances. 9 World Bank, 2005. 10 www.foquz.nl.

The remittance corridor the Netherlands – Morocco 25

1.6 Outline of this report

Chapters 2, 3, 4 and 5 analyse the remittance corridor according to the BRCA methodology. Chapter 2 presents information on Moroccan migrants and remittances. The first section deals with the population of Moroccan origin. It answers the following questions: • What is the size of the Moroccan migrant population? • Is the population of Moroccan origin growing? • What are the characteristics of the Moroccan migrant population? The second section of Chapter 2 elaborates on remittances. It answers questions such as: • How much money is remitted in the corridor the Netherlands – Morocco? • Are remittances increasing in the corridor? Chapter 3 covers the first mile of the remittance transfer, and includes an overview of the remittance market in the Netherlands and the market regulations. Chapter 4 is dedicated to the intermediary stage and includes an overview of the type of providers of remittance services (both formal and informal), payment systems and the costs and characteristics of the remittance services offered. Also included is a description of the legal, regulatory and supervisory frameworks. Chapter 5 discusses the last mile of the transfer and includes a description of remittance recipients, a rough assessment of the impact of remittances on the macro and local economies, and the policy framework affecting remittances. Chapter 6 analyses the factors hampering further formalising of the remittance flow in the corridor. The first section presents an analytical framework, which is then applied to the corridor Netherlands – Morocco in the second section. This section also represents recommendations, which are summarised in the last section of the chapter. Chapter 7 analyses the possibility of extending the use of the bank channel and presents recommendations.

The remittance corridor the Netherlands – Morocco 27

2 Migrants and remittances

2.1 Introduction

This chapter elaborates on the size and main characteristics of the Moroccan migrant community in the Netherlands and the remittances they generate. Section 2.2 briefly analyses Moroccan migrants in Europe to set the scene. The characteristics of Moroccan migrants in the Netherlands are then described in more detail. Section 2.3 deals with remittances in the corridor the Netherlands – Morocco. Total amounts of remittances and trends are analysed, and indications of future developments given. Finally, in Section 2.4 the main findings are summarised. It is important to note that data on migrants and remittances should always be interpreted with great caution. Definitions of remittances and migrants are not always consistent across countries and recording methods differ. See Annex III for an explanation of definitions used for migrants and remittances, and background information on differences in registration methods for remittances.

2.2 Moroccan migrants

2.2.1 Setting the scene

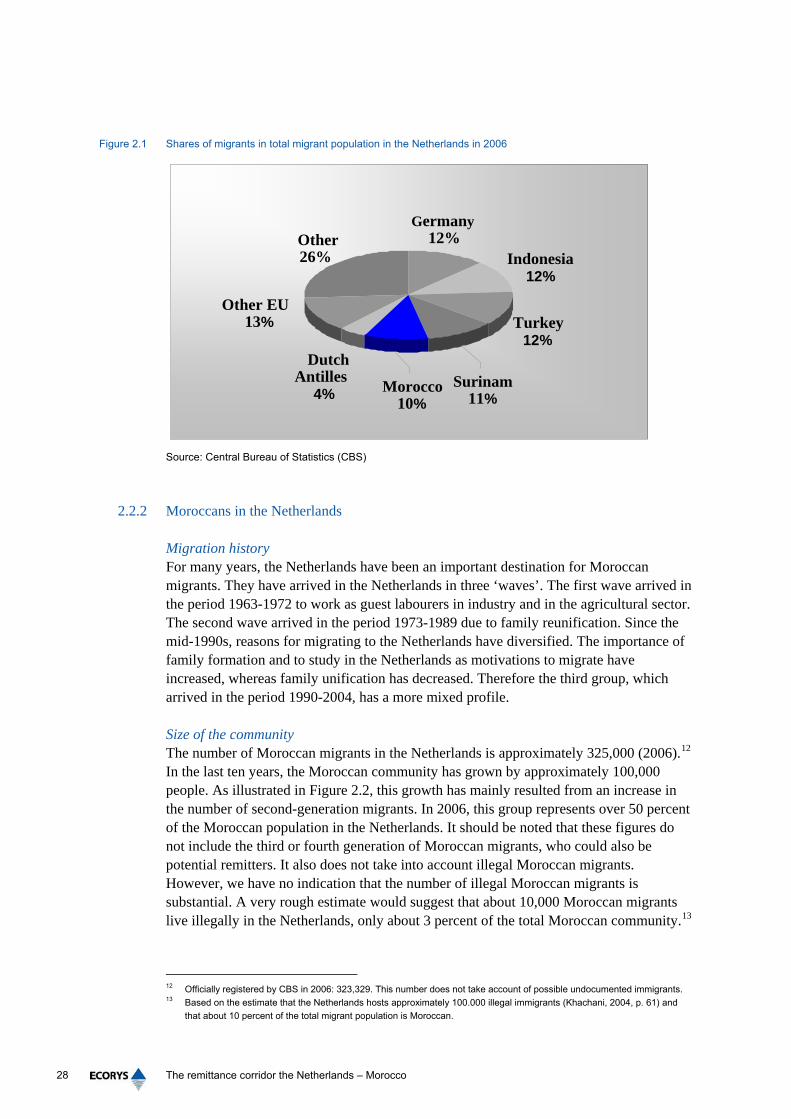

European context Around 85 percent of the persons migrating from Morocco have settled in Europe.11 Traditionally, most Moroccan migrants live in France, but in recent years Spain and Italy have become the most important new destinations. In 2003, the Netherlands housed the third largest community of Moroccans, after France and Spain. We expect that the Moroccan community in Italy will now have outgrown that in the Netherlands, moving the Netherlands to fourth place in Europe. Migrant communities in the Netherlands As illustrated by Figure 2.1, Moroccans constitute the fourth largest group of non-Western migrants in the Netherlands, after Indonesians, Turks and migrants from Surinam. As can be seen in Figure 2.1, the differences in size between these four groups are small. It is worth pointing out that the Netherlands is the only major EU migrant host country where there is no dominant migrant group.

11 EIB, 2006.

The remittance corridor the Netherlands – Morocco 28

Figure 2.1 Shares of migrants in total migrant population in the Netherlands in 2006

Source: Central Bureau of Statistics (CBS)

2.2.2 Moroccans in the Netherlands

Migration history For many years, the Netherlands have been an important destination for Moroccan migrants. They have arrived in the Netherlands in three ‘waves’. The first wave arrived in the period 1963-1972 to work as guest labourers in industry and in the agricultural sector. The second wave arrived in the period 1973-1989 due to family reunification. Since the mid-1990s, reasons for migrating to the Netherlands have diversified. The importance of family formation and to study in the Netherlands as motivations to migrate have increased, whereas family unification has decreased. Therefore the third group, which arrived in the period 1990-2004, has a more mixed profile. Size of the community The number of Moroccan migrants in the Netherlands is approximately 325,000 (2006).12 In the last ten years, the Moroccan community has grown by approximately 100,000 people. As illustrated in Figure 2.2, this growth has mainly resulted from an increase in the number of second-generation migrants. In 2006, this group represents over 50 percent of the Moroccan population in the Netherlands. It should be noted that these figures do not include the third or fourth generation of Moroccan migrants, who could also be potential remitters. It also does not take into account illegal Moroccan migrants. However, we have no indication that the number of illegal Moroccan migrants is substantial. A very rough estimate would suggest that about 10,000 Moroccan migrants live illegally in the Netherlands, only about 3 percent of the total Moroccan community.13

12 Officially registered by CBS in 2006: 323,329. This number does not take account of possible undocumented immigrants. 13 Based on the estimate that the Netherlands hosts approximately 100.000 illegal immigrants (Khachani, 2004, p. 61) and

that about 10 percent of the total migrant population is Moroccan.

Indonesia 12%

Turkey 12%

DutchAntilles

4%

Other26%

Other EU13%

Morocco10%

Surinam11%

Germany12%

The remittance corridor the Netherlands – Morocco 29

Figure 2.2 Number of first and second-generation Moroccans in the Netherlands from 1996 to 2006

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1996 1998 2000 2002 2004 2006

yearfirst generation second generation

Mor

roca

n m

igra

nts

Source: CBS

Is the migrant community growing? The Central Bureau of Statistics of the Netherlands expects a continued growth of the Moroccan population in the Netherlands, but the pace of the growth will slow down. The growth is mainly explained by an increase in the second generation of Moroccan migrants. The number of new Moroccan immigrants arriving in the Netherlands has been decreasing in the last few years. In 2001, the Netherlands received about 5,000 new Moroccan migrants. In 2005, the number of newcomers decreased to around 2,000. Figure 2.3 illustrates the projected growth of the Moroccan population up to 2050. Other researchers conclude that migration from Morocco will remain important over the next decades.14

14 Haas H de, 2006.

The remittance corridor the Netherlands – Morocco 30

Figure 2.3 Projections of number of Moroccan migrants (first and second generation) in the Netherlands up to 2050

0

100,000

200,000

300,000

400,000

500,000

600,000

Mor

roca

n M

igra

nts

1980 1990 2000 2010 2020 2030 2040 2050Year

Source: CBS

Is emigration an issue? As illustrated in Figure 2.4, the number of Moroccans emigrating from the Netherlands has been increasing since 2002. This increase is noticeable for both first and second generation migrants. Emigration is mostly back to Morocco – roughly half of Moroccan emigrants return there.15 It is of interest to note that retired migrants have a tendency to stay in the Netherlands. Emigrants from the first generation are predominantly relatively young Moroccan migrants in the 30-50 age group.

15 Based on historical migration data, CBS.

The remittance corridor the Netherlands – Morocco 31

Figure 2.4 Emigration from the Netherlands of Moroccan migrants in the period 1996 to 2005

0

500

1,000

1,500

2,000

2,500

1996 1998 2000 2002 2004

year

First Generation Second generation

Mor

roca

n M

igra

nts

Source: CBS

It must be borne in mind, however, that the numbers of emigrants are quite small in relation to the size of the total Moroccan population in the Netherlands. Furthermore, it is too early to conclude whether the recent increase in emigration is a structural break. It should also be noted that for Moroccans, the return migration rate is among the lowest of all immigrant groups in Europe.16 Where do Moroccan migrants live in the Netherlands? Figure 2.5 gives a breakdown of where Moroccan migrants live in the Netherlands. They live predominantly in the provinces of Noord Holland, Zuid Holland and Utrecht. In Noord Holland, Moroccans are concentrated in the city of Amsterdam. In Zuid Holland, they mainly live in Rotterdam and The Hague (see Figure 2.6). There is not a large difference in location preference between first-generation and second-generation Moroccan migrants. However, in the last few years the second generation seems to have a slight preference for Noord Brabant and Flevoland. The spatial planning bureau recently17 analysed the location preferences of the Moroccan community in the Netherlands up to 2025. They expect a growth of Moroccan migrants in Noord Holland, Zuid Holland and Flevoland. Although most other migrants will move out of the big cities and into smaller towns in these provinces, Moroccan migrants seem to prefer to stay in the big cities.

16 www.migrationinformation.org. 17 Ruimtelijk Planbureau, 2006.

The remittance corridor the Netherlands – Morocco 32

Figure 2.5 Moroccans in the Netherlands per province in 2005

Source: CBS

=10,000 Moroccans

Limburg

Gelderland

Overijssel

Drenthe

Groningen Friesland

Zuid - Holland

Noord - Holland

Noord - Brabant Zeeland

Utrecht

Flevoland

The remittance corridor the Netherlands – Morocco 33

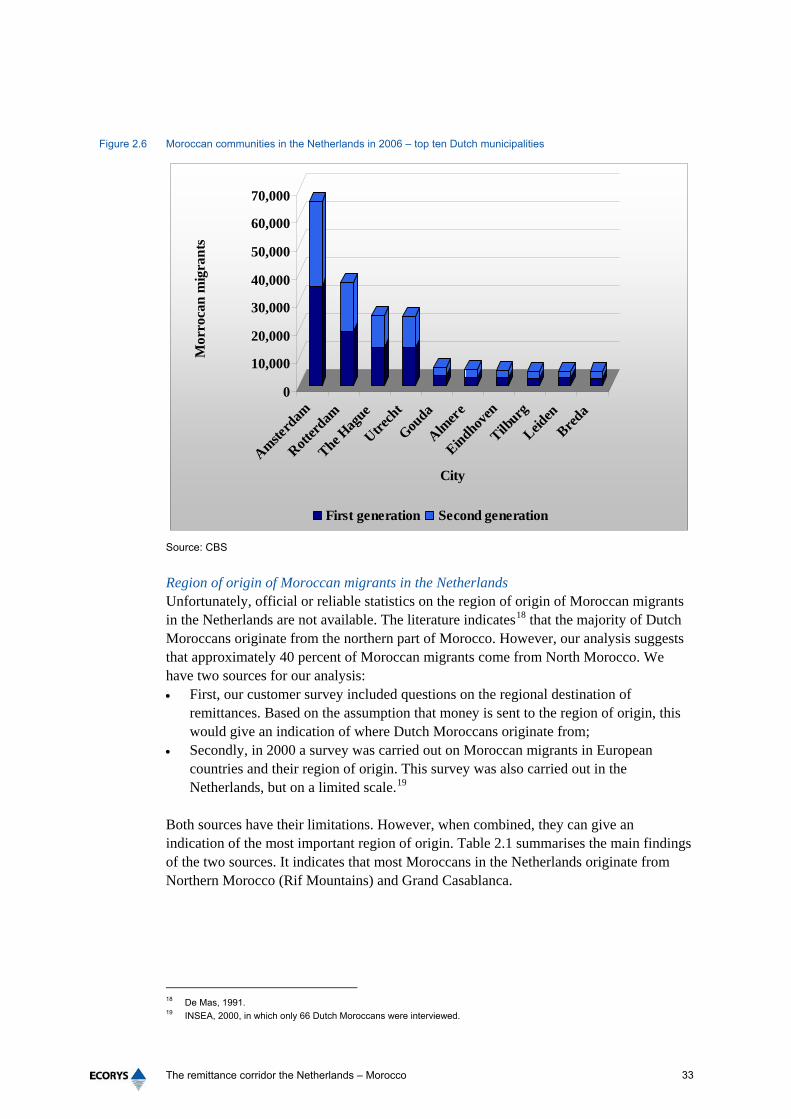

Figure 2.6 Moroccan communities in the Netherlands in 2006 – top ten Dutch municipalities

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Amsterd

am

Rotterd

am

The Hag

ue

Utrech

t

Gouda

Almer

e

Eindhoven

Tilburg

Leiden

Breda

City

First generation Second generation

Mor

roca

n m

igra

nts

Source: CBS

Region of origin of Moroccan migrants in the Netherlands Unfortunately, official or reliable statistics on the region of origin of Moroccan migrants in the Netherlands are not available. The literature indicates18 that the majority of Dutch Moroccans originate from the northern part of Morocco. However, our analysis suggests that approximately 40 percent of Moroccan migrants come from North Morocco. We have two sources for our analysis: • First, our customer survey included questions on the regional destination of

remittances. Based on the assumption that money is sent to the region of origin, this would give an indication of where Dutch Moroccans originate from;

• Secondly, in 2000 a survey was carried out on Moroccan migrants in European countries and their region of origin. This survey was also carried out in the Netherlands, but on a limited scale.19

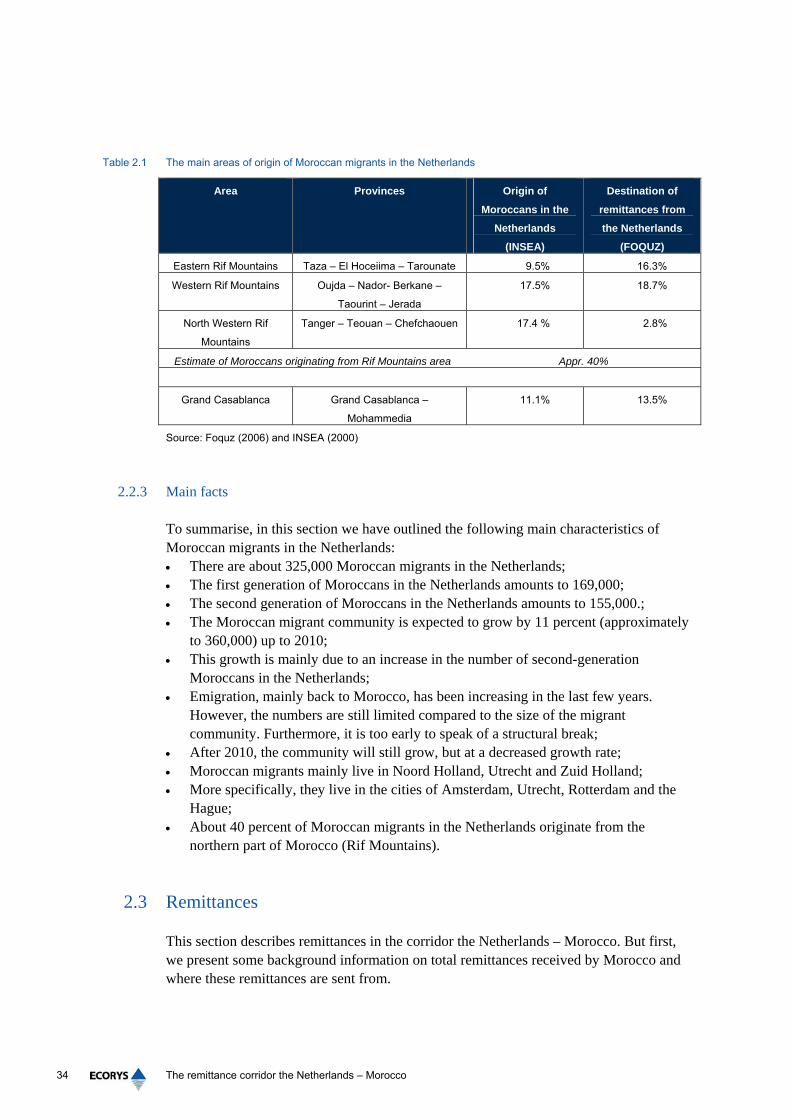

Both sources have their limitations. However, when combined, they can give an indication of the most important region of origin. Table 2.1 summarises the main findings of the two sources. It indicates that most Moroccans in the Netherlands originate from Northern Morocco (Rif Mountains) and Grand Casablanca.

18 De Mas, 1991. 19 INSEA, 2000, in which only 66 Dutch Moroccans were interviewed.

The remittance corridor the Netherlands – Morocco 34

Table 2.1 The main areas of origin of Moroccan migrants in the Netherlands

Area Provinces Origin of

Moroccans in the

Netherlands

(INSEA)

Destination of

remittances from

the Netherlands

(FOQUZ)

Eastern Rif Mountains Taza – El Hoceiima – Tarounate 9.5% 16.3%

Western Rif Mountains Oujda – Nador- Berkane –

Taourint – Jerada

17.5% 18.7%

North Western Rif

Mountains

Tanger – Teouan – Chefchaouen 17.4 % 2.8%

Estimate of Moroccans originating from Rif Mountains area Appr. 40%

Grand Casablanca Grand Casablanca –

Mohammedia

11.1% 13.5%

Source: Foquz (2006) and INSEA (2000)

2.2.3 Main facts

To summarise, in this section we have outlined the following main characteristics of Moroccan migrants in the Netherlands: • There are about 325,000 Moroccan migrants in the Netherlands; • The first generation of Moroccans in the Netherlands amounts to 169,000; • The second generation of Moroccans in the Netherlands amounts to 155,000.; • The Moroccan migrant community is expected to grow by 11 percent (approximately

to 360,000) up to 2010; • This growth is mainly due to an increase in the number of second-generation

Moroccans in the Netherlands; • Emigration, mainly back to Morocco, has been increasing in the last few years.

However, the numbers are still limited compared to the size of the migrant community. Furthermore, it is too early to speak of a structural break;

• After 2010, the community will still grow, but at a decreased growth rate; • Moroccan migrants mainly live in Noord Holland, Utrecht and Zuid Holland; • More specifically, they live in the cities of Amsterdam, Utrecht, Rotterdam and the

Hague; • About 40 percent of Moroccan migrants in the Netherlands originate from the

northern part of Morocco (Rif Mountains).

2.3 Remittances

This section describes remittances in the corridor the Netherlands – Morocco. But first, we present some background information on total remittances received by Morocco and where these remittances are sent from.

The remittance corridor the Netherlands – Morocco 35

2.3.1 Setting the scene

Development of received remittances Figure 2.7 illustrates the total remittances received in Morocco from 1982 to 2004 in Dirhams from different countries. In 2004, total remittances amounted to approximately 37 billion Dirham (EUR 3.4 billion). Remittance inflows are of considerable importance to the Moroccan economy as they account for 6-9 percent of GDP in Morocco. As the figure shows, remittances tripled in the period 1982-1990, then they more or less stabilised in the period 1990-2000. In the last five years, however, remittances have doubled again. This sharp increase in remittances over the last five years can partly be explained by an increase in migration to Spain, Italy and the USA. Migration to these countries started to increase in the mid-1990s, and remittances started to take off some years after this increase in migration. Nowadays, Spain and Italy are seen as the ‘new’ migrant countries, whereas France, Belgium and the Netherlands are characterised as the ‘old’ migrant countries. Note also the peak in 2001. This can partly be explained by the introduction of the Euro; Annex IV elaborates further on the occurrence of this peak.

Figure 2.7 Total remittances received in Morocco from 1982 to 2004 (in million Dirhams)

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Year

40,00035,000

30,00025,00020,000

15,000

10,000 5,000 0

In m

illlio

n D

irha

m

Source: Office des Changes, Morocco

Where do remittances come from? The countries of origination are diverse, but as would be expected those housing the largest migrant communities are the most important sources of remittances. Figure 2.8 illustrates recorded remittances from a selection of countries in 1999 and in 2004. It shows that remittance flows have increased from all these countries. France is the most important sending country, but its relative importance has decreased because of migration to Spain, Italy and the USA in the last five years. The relative importance of the Netherlands has also decreased. Up to 1992, the Netherlands was the second most important sending country after France, but it is now is the seventh most important sending country after France, Italy, Spain, the USA, Belgium/Luxemburg and the UK

The remittance corridor the Netherlands – Morocco 36

However, its importance should not be underestimated as the remittance flow from the Netherlands still constitutes about 0.5 percent of Morocco’s GDP. Based on this information, we conclude that the Netherlands has become less important for Morocco as a source of remittances. This can have an affect on the importance that Moroccan banks attach to cooperation with Dutch banks (see Chapter 6).

Figure 2.8 Remittances received in Morocco from selected countries in 1999 and 2004 (in million Dirhams)

Source: Office des Changes, Morocco

2.3.2 Remittances in the corridor the Netherlands – Morocco

An estimate for the corridor In the previous section, total received remittances in Morocco were presented. The Moroccan Office des Changes states that remittances amounted to about 37 billion Dirham (EUR 3.4 billion) in 2004. As will be further elaborated upon below, we estimate that in the corridor the Netherlands – Morocco, about EUR 93 million to EUR 132 million was remitted in 2004. Ambiguous remittances data This estimate represents a ‘best guess’ for the corridor, since actual remittance data are ambiguous. Table 2.2 presents remittance data recorded as received in Morocco (Office

0 5,000 10,000 15,000 20,000

Received Remittances in Morocco (in mln Dirham)

France

Italy

Netherlands

Belgium/Luxemburg

Germany

Spain

UK

USA

Middle East

Neighbours

Other

Country

1999 2004

The remittance corridor the Netherlands – Morocco 37

des Changes) and recorded as sent in the Netherlands (Central Bank of the Netherlands (DNB)). Ideally, the recorded sent remittances should be equal to the recorded received remittances. However, the table makes it clear that the Dutch and Moroccan figures do not coincide. Up to 2000, the Netherlands recorded more remittances sent than Morocco recorded as received. Then in 2001 to 2003 the situation was reversed: Morocco recorded more remittances received than the Netherlands recorded as sent. The picture changed again in 2004: the Netherlands recorded more sent than Morocco recorded as received.

Table 2.2 Recorded remittances in the corridor the Netherlands – Morocco (in million EUR)

1996 1997 1998 1999 2000 2001 2002 2003 2004

Received and recorded in

Morocco

91 80 123 103 163 343 201 187 132

Sent and recorded in the

Netherlands

106 117 124 151 169 180 191 172 182

Source: Office des Changes, Morocco and DNB

This variation in the level of recorded remittances can be explained by the different recording methods in Morocco and the Netherlands. In a nutshell, Morocco registers private bank transfers, post giro transfers and all money exchanges as remittances. The Netherlands uses the growth rates of the total migrant population as a proxy for growth in remittances. After total remittances are calculated, remittances per country are determined using a distribution formula. This distribution formula was constructed in 2002 and is based on the geographical breakdown of cash payments above ± EUR 11,000. Annex III explains the differences in recording remittances in more detail. Is one recording method better than the other? Both the Dutch and the Moroccan recording methods have their disadvantages, and it cannot be concluded that one method is better than the other. We need to take a closer look at both recording methods. If we take the definition of remittances as cross-border person-to-person transactions from sender to receiver as a starting point, the Moroccan data probably includes more than just remittances. This can be explained by the fact that the Office des Changes focuses on the transaction itself. The Office des Changes classifies all cash transfers as remittances, which probably also includes tourist expenditures by Moroccan migrants on holiday in Morocco. These expenditures are not remittances according to the definition stated earlier. We believe that subtracting these expenditures from remittance data can have a dramatic effect on recorded remittances. To illustrate: when Turkey classified money exchange in Turkey (Euro to Lira) as tourist expenditure instead of remittances, recorded remittances decreased from EUR 3.3 billion in 2001 to EUR 646 million in 2004.20 The Dutch data before 2003 probably also took more aspects into account than purely remittances. This can be explained by the fact that DNB only took account of the sender and not the receiver. Therefore, it is not clear if all transactions were person-to-person

20 EIB, 2006.

The remittance corridor the Netherlands – Morocco 38

transactions. All transactions smaller than EUR 11,000, be it payments for services or goods and small investments, were also seen as remittances. Therefore, the Dutch remittance data probably included other money flows than remittances. Since 2003, remittance estimates have been partly based on: • developments in the total migrant community in the Netherlands, to generate a gross

estimate for remittances; • a distribution formula based on the family name of the sender, to create a geographic

breakdown of the gross estimate of remittances. There are several disadvantages to this approach. First, this estimate does not take into account the fact that the growth in the migrant population is mostly second generation migrant growth, and this generation is less liable to remit. Secondly, the figures for 2003 do not take into account the third generation of Moroccan migrants. Although this group is even less liable to remit than the second generation, the number of third generation migrants is growing quickly and could be of importance. Thirdly, this estimate does not take account of the effects that economic development in the host country can have on the size of remittances. Based on these differences in definition, it is remarkable to see that for 2004 DNB recorded more remittances sent to Morocco than Morocco registered as received. What is the best estimate? Both the Dutch and the Moroccan data seem to overestimate remittances. The ‘real’ remittance figure should be lower than the Dutch and Moroccan data suggest. Fortunately, we have two additional sources of estimates for the remittance flow between the Netherlands and Morocco. In a recent parliamentary letter, the total remittance flow (recorded and unrecorded) from the Netherlands to Morocco was estimated at EUR 84 million for 2005.21 This estimate was based on a customer survey. In addition, the customer survey carried out for the underlying study has also generated an estimate of remittances for this corridor. Our survey focussed specifically on the corridor the Netherlands – Morocco and based on a larger sample. Therefore, we prefer to use the results of our survey in stead of the survey conducted in 2005. Based on the findings in our survey on numbers of migrants and size of remittance transfers, we estimate that EUR 97 million was sent to Morocco in 2006. Corrected for inflation, this would have been around EUR 93 million in 2004. Based on the data from the Office des Changes, DNB, the customer survey from 2005 and our own customer survey, we believe that total remittances in 2004 from the Netherlands to Morocco should be estimated in the range of EUR 93 million to EUR 132 million. The estimate of EUR 132 million should be seen as an upper bound, because, as indicated above, the Moroccan seem to overestimates the remittance flow.

21 Tweede Kamer, vergaderjaar 2005-2006, 26234 nr. 56. Numbers are based on the report of NCDO, 2005.

The remittance corridor the Netherlands – Morocco 39

Developments over the last 10 years Despite the differences in recording methods, both sources seem to indicate a similar trend over the last ten years. Figure 2.9 shows the development of recorded remittances in Morocco (in Dirhams and Euros) and in the Netherlands (in Euros).

Figure 2.9 Trends in remittances in the corridor the Netherlands – Morocco

Source: Office des Changes, DNB

The Dutch data seem to indicate a steady, moderate increase in remittances over the last ten years. This trend is the result of the estimation method. After all, DNB estimates remittances with the help of migrant data which grew with a steady pace. The Moroccan data is less clear as to trend. However, if we exclude the 2001-2002 peak in remittances (mainly resulting from an increase in cash remittances – see Annex IV), the Moroccan data also seem to suggest a moderate increase in remittances in the last ten years, although this increase has been more erratic. Unfortunately, the Office des Changes never answered the study team’s repeated question about how it has been able to register the country of origin since 2002, as the origin of cash Euros is difficult (if not impossible) to retrieve in comparison with the former country currencies. Future increase or decrease in remittances? If we simply extrapolate the remittances development from the last ten years, we assume a ‘moderate growth’ hypothesis for the coming years. Although the recent decrease in remittances received from the Netherlands in 2003 and 2004 seems to contradict the ‘moderate growth’ hypothesis, there is no indication yet of a structural break. A possible

0500

1,0001,5002,0002,5003,0003,5004,000

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004Year

050100150200250300350400

Recorded in Morocco from the Netherlands in DirhamsRecorded in Morocco from the Netherlands in Euros Recorded in Netherlands to Morocco in Euros

In m

illio

n E

uros

In m

illio

n D

irha

ms

The remittance corridor the Netherlands – Morocco 40

explanation for this decrease can be partly linked to the disappointing economic performance of the Netherlands.22 Extrapolation is a second best approach for trend analysis. First best is a more in-depth analysis of the causes underlying the trend. However, a full analysis is beyond the scope of this study. Nonetheless, we can say that the modest growth of the migrant population seems to confirm the moderate growth hypotheses. We have to take into account that this growth is mainly due to an increase of the number of second generation Moroccans. If we want to support the moderate growth hypotheses, we have to analyse remittance behaviour of the second generation and other factors which can explain remittance behaviour (sex, age, education, profession). This analysis is provided for in Chapter 4. For now we can say that the second generation migrants seem to have a similar likelihood of remitting as first generation migrants. Therefore, the growth of the second generation migrant population and its remittance behaviour seems to confirm our growth hypothesis.

2.4 Main facts and findings

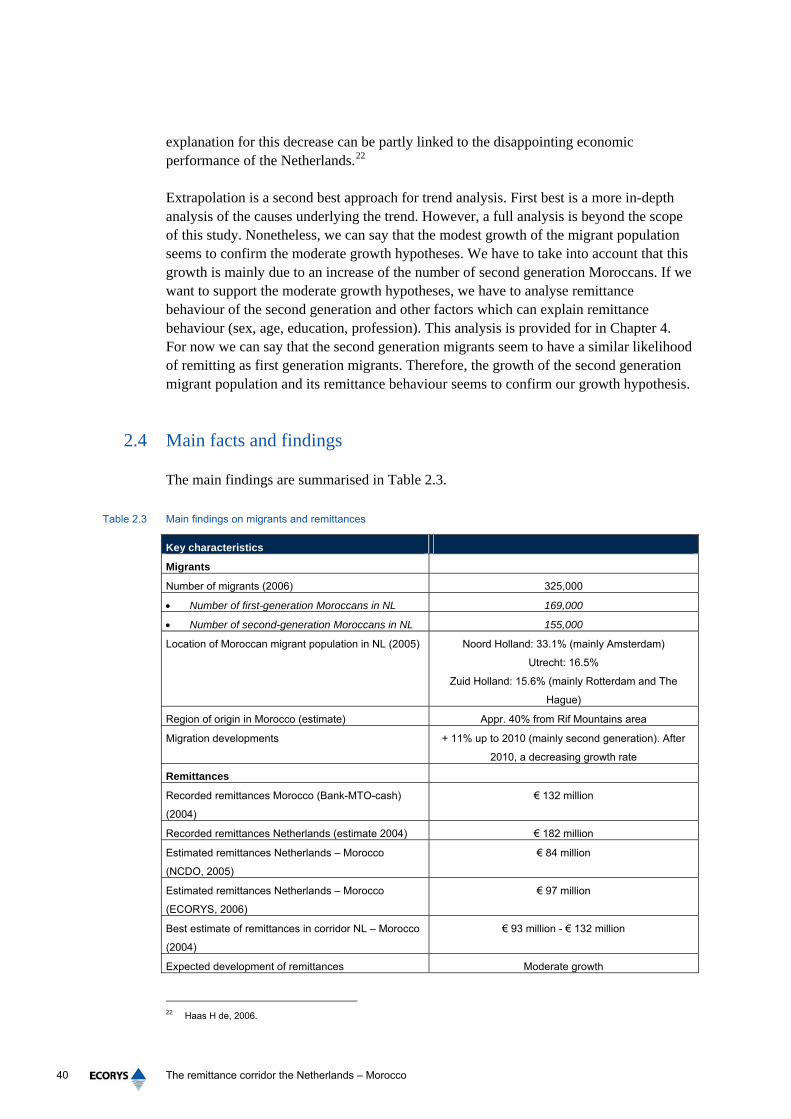

The main findings are summarised in Table 2.3.

Table 2.3 Main findings on migrants and remittances

Key characteristics

Migrants

Number of migrants (2006) 325,000

• Number of first-generation Moroccans in NL 169,000

• Number of second-generation Moroccans in NL 155,000

Location of Moroccan migrant population in NL (2005) Noord Holland: 33.1% (mainly Amsterdam)

Utrecht: 16.5%

Zuid Holland: 15.6% (mainly Rotterdam and The

Hague)

Region of origin in Morocco (estimate) Appr. 40% from Rif Mountains area

Migration developments + 11% up to 2010 (mainly second generation). After

2010, a decreasing growth rate

Remittances

Recorded remittances Morocco (Bank-MTO-cash)

(2004)

€ 132 million

Recorded remittances Netherlands (estimate 2004) € 182 million

Estimated remittances Netherlands – Morocco

(NCDO, 2005)

€ 84 million

Estimated remittances Netherlands – Morocco

(ECORYS, 2006)

€ 97 million

Best estimate of remittances in corridor NL – Morocco

(2004)

€ 93 million - € 132 million

Expected development of remittances Moderate growth

22 Haas H de, 2006.

The remittance corridor the Netherlands – Morocco 41

3 First mile

3.1 Introduction

This chapter starts with an overview of the remittance service providers (RSPs) in the Netherlands, followed by a description of the relevant regulatory framework. It concludes with an overview of the main facts and findings.

3.2 How to send money?

Money can be sent from the Netherlands to Morocco in several ways: through formal channels such as banks, post offices or Money Transfer Organisations (MTOs), or through informal channels such as carrying cash when visiting the home country, or by asking friends or family to carry the money. ‘Formal remittances’ are sent through formal channels, meaning that the remittance service provider has obtained a licence from the Central Bank of the Netherlands (DNB). Formal channels are monitored by DNB. ‘Informal remittances’ are sent through informal channels. Note that informal is not synonymous with ‘illegal’. Taking cash as a gift for family or friends when travelling to Morocco is a legal informal way of remitting.

3.3 What are the formal channels in the Netherlands?

The financial sector in the Netherlands is well developed. An account is needed for families to receive family allowance or child support, for workers to receive a salary, for anyone paying tax, for disabled or unemployed people receiving an allowance, and for students receiving a study or child allowance. Therefore, we assume that all Moroccan migrant families in the Netherlands have a bank account. The main remittance service providers in the Netherlands are banks and MTOs.

3.3.1 The banking sector in the Netherlands23

Dutch banks All Dutch banks offer international money transfers to their account holders. Dutch banks are part of international bank agreements and have correspondent banking relationships

23 CBS, Webmagazine, January 2003.

The remittance corridor the Netherlands – Morocco 42

with Morocco. The transfer itself is handled through the electronic wire transfer system SWIFT (Society for Worldwide Interbank Financial Telecommunication), to which all (international operating) banks are connected. To transfer via a bank, the remittance sender must have a current account with the bank in the host country and the recipient an account in the home country. Other than standard money transfer services, none of the banks in the Netherlands offer dedicated remittance services to migrants. However, they differ in their marketing efforts towards migrants. For example, the Rabobank ran a marketing campaign targeting third generation migrants during the Christmas holidays 2005. Rabobank indicated that this group of migrants is a potentially interesting clientele for the bank, as they are having better jobs and are well integrated. During the Rabobank campaign, every existing or new accountholder could transfer money for only EUR 1. After the campaign, on 10 January 2006, the normal costs for a transaction were reduced from EUR 20 to EUR 13.50.24 Compared with other European countries, Dutch customers visit their bank branch the least. One reason for this is the ample availability of alternative distribution channels like ATM machines, internet banking and telephone services. Rabobank, for example, noticed a fall in visits of 280 million in 1980 to five million in 2004 – a decline of 98 percent.25 Over the years, many bank branches have been closed, and as shown in Figure 3.1 the number of inhabitants per branch has risen in almost ten years from 2,500 inhabitants per bank branch in 1997 to about 4,400 inhabitants per branch in 2006, an increase of 75 percent. On the other hand, the numbers of ATM machines and ATM withdrawals have grown rapidly.

24 http://allochtonen.web-log.nl/allochtonen/arbeidsmarkteconomie/index.htm. 25 Minister Zalm, Toespraak Rabobank Noordwest Twente, ‘Het vliegen niet verleerd: over het belang van flexibiliteit’. March

2005.

The remittance corridor the Netherlands – Morocco 43

Figure 3.1 Indicators of the banking sector in the Netherlands

Source: Nederlandse Vereniging van Banken (NVB)

Moroccan banks in the Netherlands Many foreign banks have branches in the Netherlands. At present, however, there are no Moroccan banks offering banking services in the Netherlands. Banque Populaire and Wafa Bank26 used to offer bank products in the Netherlands, but they were closed about a year ago for “reasons concerning the bank licence”.27 The offices of these banks in Amsterdam, Rotterdam and The Hague now only operate as advisory organisations.28

3.3.2 Postbank

The Postbank occupies a special position in the banking sector as it both offers banking services and is an authorised agent of Western Union. Postbank, part of ING Bank, is the only mainstream bank in the Netherlands with such a liaison with a MTO. The main distribution channels for Postbank are mail, the internet and the post office network. Postbank is a member of Eurogiro/Worldgiro. Through alliance agreements and service-level agreements, the members of Eurogiro/Worldgiro aim to offer competitive cross-border payment products.29 Services offered include:

26 After a reorganisation in Morocco, Wafa Bank is now called Attijawafa Bank. 27 Statement, DNB. 28 The banks could not provide further information on the reasons for closure (telephone calls from ECORYS to the branches

in August 2006). 29 www.eurogiro.com.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1 2 3 4 0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Nr of bank branches Inhabitants per branch

1997 2000 2004 2006

Year

Ban

k br

anch

es

Inha

bita

nts p

er b

ranc

h

The remittance corridor the Netherlands – Morocco 44

• business day standard transfer – low-cost money orders in a maximum of five days; • semi-urgent cash payments in a maximum of two days; • urgent cash payments if the recipient needs the money within minutes; • bulk transactions, e.g. pensions. Postbank account holders can use the standard or semi-urgent transfer services by filling out paper or electronic transaction forms. For urgent cash transfers, Eurogiro/Worldgiro members cooperate with Western Union. In the Netherlands, the Postbank offers Western Union services through its daughter company Postkantoren BV. This organisation uses all post offices in the Netherlands and is a joint venture between Postbank and TPG Post. As with all MTO services, neither sender nor recipient needs to have a bank account.

3.3.3 Money Transfer Organisations

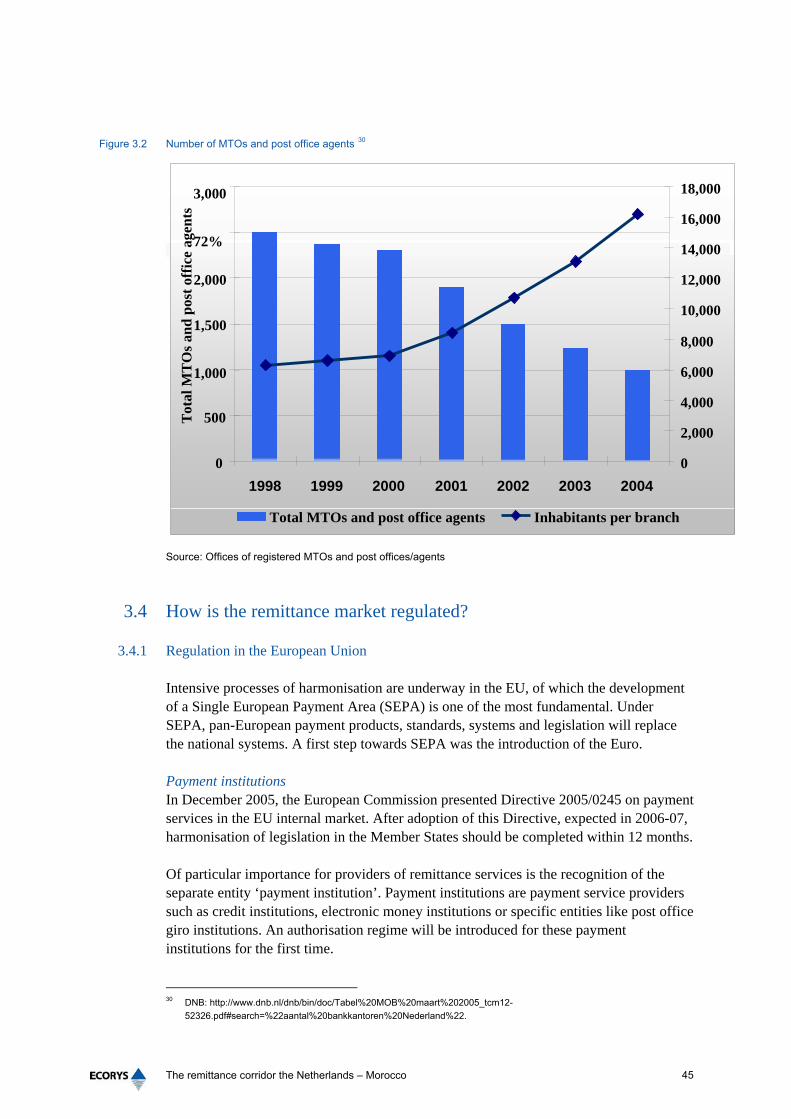

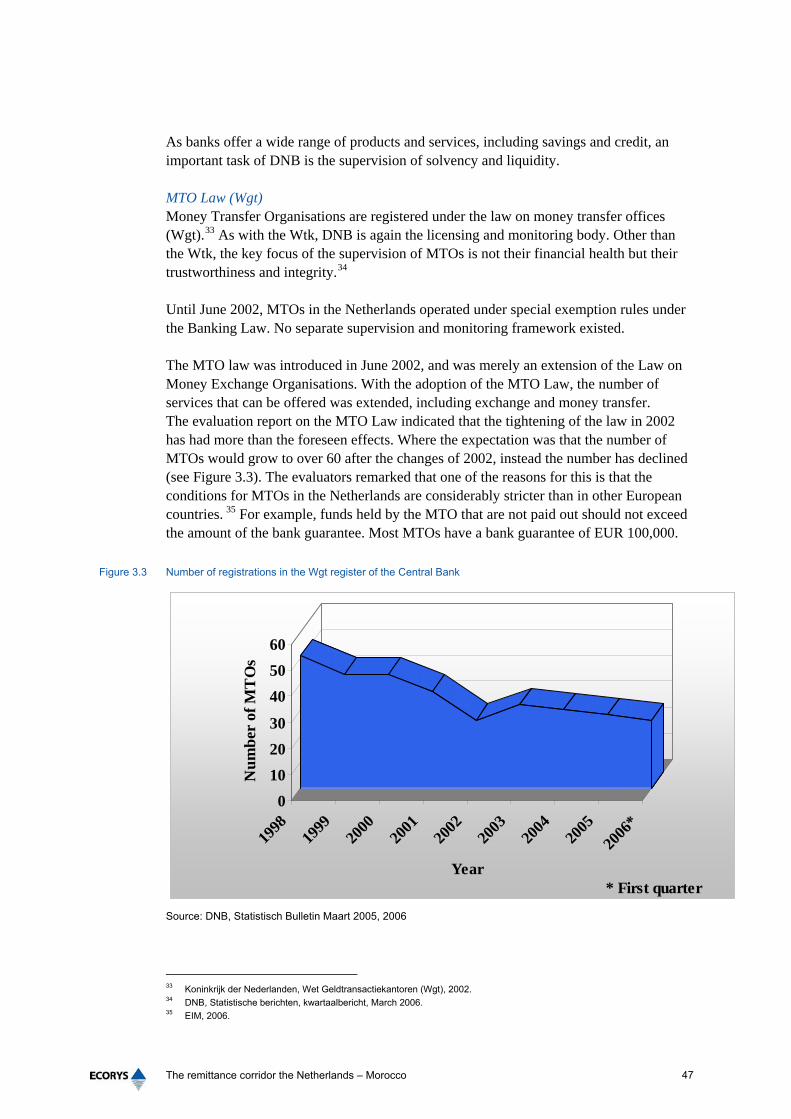

The major MTOs in the Netherlands are Western Union and MoneyGram. Currently, Western Union has 650 locations in the Netherlands. The Western Union agent with the largest network is the post office. Other agents of Western Union are Goffinbank, Cash Express, Does and Cadushi Travel. MoneyGram is part of Travelex and has a network of about 50 locations in the Netherlands. Travelex owns the distribution network GWK Travelex, with about 43 locations. Recently, Travelex bought the money transfer network of the German bank Reisebank, including seven offices in the Netherlands operating under the name Cash Express. As indicated in Figure 3.2, since 1998 the number of MTO counters has been declining. A major explanation for this decline is the decrease in the number of post offices over recent years, affecting the Western Union network. In addition, since the adaptation of the law on MTOs (Wgt) in 2002, the number of MTOs operating in the Netherlands has been considerably reduced. The Wgt is further discussed in the next section.

The remittance corridor the Netherlands – Morocco 45

Figure 3.2 Number of MTOs and post office agents 30

Source: Offices of registered MTOs and post offices/agents

3.4 How is the remittance market regulated?

3.4.1 Regulation in the European Union

Intensive processes of harmonisation are underway in the EU, of which the development of a Single European Payment Area (SEPA) is one of the most fundamental. Under SEPA, pan-European payment products, standards, systems and legislation will replace the national systems. A first step towards SEPA was the introduction of the Euro. Payment institutions In December 2005, the European Commission presented Directive 2005/0245 on payment services in the EU internal market. After adoption of this Directive, expected in 2006-07, harmonisation of legislation in the Member States should be completed within 12 months. Of particular importance for providers of remittance services is the recognition of the separate entity ‘payment institution’. Payment institutions are payment service providers such as credit institutions, electronic money institutions or specific entities like post office giro institutions. An authorisation regime will be introduced for these payment institutions for the first time. 30 DNB: http://www.dnb.nl/dnb/bin/doc/Tabel%20MOB%20maart%202005_tcm12-

52326.pdf#search=%22aantal%20bankkantoren%20Nederland%22.

0

500

1,000

1,500

2,000

72%

3,000

1998 1999 2000 2001 2002 2003 2004 0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Total MTOs and post office agents Inhabitants per branch

Tot

al M

TO

s and

pos

t off

ice

agen

ts

The remittance corridor the Netherlands – Morocco 46

In the draft Directive it is foreseen that authorised payment institutions will be restricted to rendering payment services and will not be allowed to take on deposits. The authorisation in one EU country to operate as a payment institution is valid for the entire EU.31 Transparency of conditions Under the Directive, clear transparency conditions are set. All payment service providers (including payment institutions, credit institutions, electronic money institutions etc.) are obliged to offer all services as transparently as possible. The Directive states that providers should supply information on: • charges and the reference exchange rate applied to payment transactions, prior to the

transaction (including the relevant date for determining such a rate and the way the rate is calculated). The scope is end to end – the party offering the service is obliged to disclose all information, including the costs charged to the recipient and the currency conversion rate used at the recipient’s end;

• identifiers of the transaction – remitter and recipient, transaction amount, amount of commission and charges and applied exchange rate, after executing the transaction.

Consequences for the Netherlands After approval of the Directive, national laws will have to be assessed as to their compliance with the New Legal Framework. The Directive’s conditions regarding transparency will not burden the banks offering remittance services, because in following the Cross-Border Credit Transfers Directive 97/5/EC they already comply with similar regulations regarding transparency. It is expected that most MTOs will welcome the Directive with respect to the legislation of payment institutions, as they will no longer be confronted with the different licensing regimes of individual EU countries. A licence obtained in one EU country will pave the way for the rest of the European Union.

3.4.2 Regulation in the Netherlands