THE RELATIONSHIP BETWEEN OWNERSHIP GOVERNANCE … · survival issue of firms affected all aspects...

28

The 14 th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013 1 THE RELATIONSHIP BETWEEN OWNERSHIP GOVERNANCE AND FIRMS’ PERFORMANCE AMONG SURVIVING LISTED FIRMS IN MALAYSIA Zaleha Abdul Shukor 1 , Romlah Jaffar 2 , Khalijah Ahmad 3 , Ruhanita Maelah 4 , and Aini Aman 5 1 Universiti Kebangsaan Malaysia, Malaysia, [email protected] 2 Universiti Kebangsaan Malaysia, Malaysia, [email protected] 3 Universiti Kebangsaan Malaysia, Malaysia, [email protected] 4 Universiti Kebangsaan Malaysia, Malaysia, [email protected] 5 Universiti Kebangsaan Malaysia, Malaysia, [email protected] ABSTRACT Ownership structure is pertinent in the management of shareholders and stakeholders’ interests. Many develop countries have dispersed ownership whereas many developing countries have concentrated ownership. It is a question whether ownership structure influence firms’ performance which could reflect stakeholders’ interests. Prior studies found majority concentrated shareholders tend to ignore the interests of minority shareholders. Prior studies also found that listed firms in Malaysia, a developing country, tend to show low survival rates, only about 20% survive more than 10 years in listing. The aim of this study is to investigate the type of ownership structure that influence firms performance amongst surviving listed firms in Malaysia. This study focused on four types of ownership: institutional ownership, managerial ownership, board of directors’ (BOD) ownership and individual ownership. Institutional ownership with substantial shareholdings is expected to be positively associated with firms’ performance. Managerial and BOD ownership should be able to reduce agency conflict between management and owners. However, managerial ownership could be contaminated with entrenchment effect, preferring short-term rather than long-term profits. Prior studies were not conclusive about both managerial and BOD ownership effect, hence we only expect a significant association with firms’ performance. Individual ownership, lacking control in firms’ decision-making should not be associated with firms’ performance. Based on a 904 firm-years data, for the period of 2007 through 2011, from firms that survived more than 10 years of listing, findings show that, as expected, institutional ownership has a positively significant association with firms’ performance. Managerial ownership show tendency of a negative association with firms’ performance. BOD ownership and individual ownership show insignificant association with firms’ performance. Findings suggest that the ownership component in a corporate governance setting should be seriously considered by investors and stakeholders home and abroad when evaluating on potential long-term investments among listed firms in Malaysia. Keywords: Ownership structure, majority ownership, minority ownership, corporate governance, surviving firms, firm performance

Transcript of THE RELATIONSHIP BETWEEN OWNERSHIP GOVERNANCE … · survival issue of firms affected all aspects...

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

1

THE RELATIONSHIP BETWEEN OWNERSHIP GOVERNANCE AND FIRMS’ PERFORMANCE AMONG SURVIVING LISTED FIRMS IN MALAYSIA

Zaleha Abdul Shukor1, Romlah Jaffar2, Khalijah Ahmad3, Ruhanita Maelah4, and Aini Aman5

1Universiti Kebangsaan Malaysia, Malaysia, [email protected]

2Universiti Kebangsaan Malaysia, Malaysia, [email protected]

3Universiti Kebangsaan Malaysia, Malaysia, [email protected]

4Universiti Kebangsaan Malaysia, Malaysia, [email protected]

5Universiti Kebangsaan Malaysia, Malaysia, [email protected]

ABSTRACT Ownership structure is pertinent in the management of shareholders and stakeholders’ interests. Many develop countries have dispersed ownership whereas many developing countries have concentrated ownership. It is a question whether ownership structure influence firms’ performance which could reflect stakeholders’ interests. Prior studies found majority concentrated shareholders tend to ignore the interests of minority shareholders. Prior studies also found that listed firms in Malaysia, a developing country, tend to show low survival rates, only about 20% survive more than 10 years in listing. The aim of this study is to investigate the type of ownership structure that influence firms performance amongst surviving listed firms in Malaysia. This study focused on four types of ownership: institutional ownership, managerial ownership, board of directors’ (BOD) ownership and individual ownership. Institutional ownership with substantial shareholdings is expected to be positively associated with firms’ performance. Managerial and BOD ownership should be able to reduce agency conflict between management and owners. However, managerial ownership could be contaminated with entrenchment effect, preferring short-term rather than long-term profits. Prior studies were not conclusive about both managerial and BOD ownership effect, hence we only expect a significant association with firms’ performance. Individual ownership, lacking control in firms’ decision-making should not be associated with firms’ performance. Based on a 904 firm-years data, for the period of 2007 through 2011, from firms that survived more than 10 years of listing, findings show that, as expected, institutional ownership has a positively significant association with firms’ performance. Managerial ownership show tendency of a negative association with firms’ performance. BOD ownership and individual ownership show insignificant association with firms’ performance. Findings suggest that the ownership component in a corporate governance setting should be seriously considered by investors and stakeholders home and abroad when evaluating on potential long-term investments among listed firms in Malaysia. Keywords: Ownership structure, majority ownership, minority ownership, corporate governance, surviving firms, firm performance

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

2

1. INTRODUCTION

The multiple economic downturns occurring at least in the last few decades demand

firms to be equipped with survival strategies. These include strategies for firms to

continue as going concern as well as searching and exploring opportunities and avenues

to continuously strengthen and enhance themselves. In order to implement any survival

strategies, firms need owners that can appreciate and provide appropriate compensation

to management effort (Zhang, Venus & Wang, 2012). Hence, this could reduce

significantly the conflict of agency costs between firms’ management and stakeholders

(including owners and investors).

The ability for firms to survive and grow in the long run is important to investors

searching for potential new investments during economic crisis period. Survival and

growth of firms promised long-term employments to the current employees and creation

of new employment to others. Stable firms create more businesses allowing continuation

of activities among creditors and debtors. Firms that survived promised continuous tax to

the government apart from creating more business activities in the market. Hence,

survival issue of firms affected all aspects of social environment whether directly or

indirectly involved with those firms.

Firms’ survival is critical to a country business environment, which could strongly

influence the country’s gross domestic product (Tsoukas, 2011). Firms listed on stock

exchanges obtain their capital from investment activities within the capital market they

are listed on. Capital market activities have a strong influence on a country’s economy

because their performances affect potential foreign investment. The better the

performance of the stock exchanges, the better will be potential for a country to attract

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

3

high foreign investment. Hence, the main contributor towards an increase in foreign

investments will be based on listed firms’ growth and solvency.

Issue of ownership structure among surviving firms is important to all stakeholders

related to the firms’ business activities including investors, financial providers,

employees, customers and the authority. This is because ownership with control can

seriously influence the governance of decision making for the firms. This study focus on

the issue of ownership structure since one of the uniqueness of ownership structure in

Malaysia typical among Asian countries is control by only among a few shareholders

(Claessens et al., 2000; Yen & Andre, 2007). Prior literature found that active venture

capitalist can influence the degree of firms’ success (Bottazzi, Da Rin & Hellmann,

2008), hence leading to firms’ survival. Additionally, firms having succession of family

members’ ownership show higher potential of survival in the long run (Achleitner et al.,

2012). Extant studies however lack information on whether ownership structure

influences firms’ survival after going through multiple economic downturns. Hence the

aim of this study is to investigate the association between ownership structure and firm

performance among surviving listed firms in Malaysia after going through several

economic downturns, specifically the 1997-1998 Asian financial crisis and the 2008-2009

sub-prime crisis.

Financial data from firms’ annual reports was collected for years 2007 until 2011. Based

on a 904 firm-years data for firms that survived more than 10 years of listing, findings

show that, as expected, institutional ownership has a positively significant association

with firms’ performance. Managerial ownership show tendency of a negative association

with firms’ performance but not BOD ownership. This finding could be due to the agency

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

4

conflict argued in prior studies that managers generally prefer short-term profits rather

than long term profits, hence their ownership constitute ownership within the short-term

category, subsequently result in negative association with the performance of long term

surviving firms. As expected, individual ownership did not show any significant

association with firms’ performance. Findings suggest that the ownership component in

a corporate governance setting should be seriously considered by investors and

stakeholders home and abroad when evaluating on potential long-term investments

among listed firms in Malaysia. In addition, this study is expected to provide critical

evidence to investors and the various stakeholders on the type of ownership structure

they should be alert with when firms they invest in faced poor economic conditions.

This paper proceeds with section two discussing relevant literature review and

hypotheses development. Section three present the methodology of this study. Section

four presents results and discussion on findings. Finally section five concludes this

paper.

2. LITERATURE AND HYPOTHESES DEVELOPMENT

2.1 Firms’ Survival Strategies

Firms’ ownership in general would only create agency issues if owners are not involved

in the day to day running of firms. Issue might arise if managers are not compensated

well which might affect firms’ performance since managers manage the firms but

ultimate power on compensation is in the hands of controlling owners. As such, owners

must have the appropriate contract with managers to ensure the long-term survival and

going concern of the firms. Nevertheless, firms’ survivorship normally depends on many

factors and not just the interaction between managers and owners. Prior studies

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

5

generally found large firms survived many turbulent times better than small firms (Knox

et al., 2008) due to the existence of various and multiple resources within the firms that

can be utilized.

However, all firms must start with being small and start-ups before they can expand and

eventually become large to survive any economic downturns. During the early

establishment of Bursa Malaysia in late 1970s and early 1980s, most listed firms were

presumably young and growing. Young and growing firms’ survival strategies will be

different from mature firms (Zahra et al., 2008). Firms listed on Bursa Malaysia during

the 1990s era will mostly be at their professional management stage of their

organizational life cycle (Zahra et al., 2008) should they survive the 1980s economic

downturn. Whereas firms still listed after year 2000 are expected to be at their mature

stage since they survive both the economic crisis during early 1980s and end of 1990s.

Some survival strategies involved the need for serious intervention from certain parties

such as the regulators and government to ensure stable social economy is maintain

throughout the country. For example, firms in the financial sector must adhere to many

strict rules and regulations mainly because their actions on loan interest, among others,

will create a chain reaction to all economic activities in the whole country no matter what

their ownership structure will be. Hence, survival strategies of such groups are not within

the scope of this study since their survival strategy is too much dependent on formal

country ruling and regulations.

Firms in economic sectors other than the financial sector will depend more on their own

initiatives to survive turbulent times. Hence, the focused of this study as well as the

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

6

focused of our literature review will be more on survival strategy of firms other than the

financial sector. The extractive industry (with raw materials such as oil, gas, silver, gold

and the like) is also another specialized industry that depends upon availability or

alternatively the lack of raw materials in determining their future existence (Cortese et

al., 2009). For as long as their raw material is available, their survival might be intact.

However, since the establishment of Bursa Malaysia, most listed firms do not focused on

one type of economic activity only in order to ensure their survivorship. Acquiring or

entering into multiple economic activities or commonly known as diversification has been

one of the strategies for survival among firms all over the world (Nachum, 1999; Kim &

Mathur, 2008). This highlights the importance of relevant networking intra-firms and

inter-firms where diversification is rampant.

Prior studies always found that firms’ strong and reliable networking contribute seriously

towards firms’ survival and continuous performance (Manolova et al., 2010; Pananond,

2007; Plehn-Dujowich, 2009). Networking not only involved business networking among

firms but also all entities important to the business community for future survival, which

include legal networking with the government and business regulators. Prior studies also

found that having corporate entrepreneurship (Ritchie, 2004; Zahra et al., 2008) which

include the ability to utilize existing intellectual capital (Euh & Rhee, 2007) and other

abilities firms have in control strongly assist in bringing firms out of problematic

situations. Always looking forward based on global perspectives has also been found to

contribute strongly towards firms’ future survival (Almeida & Fernando, 2008). Firms’

survival strategy is therefore multifaceted in nature. Having internal strength is expected

to be as important as having external assistance, such as from the government and

regulators in order for firms to survive.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

7

Provided that firms have all tangible and intangible resources available to assist in their

survival mission, owners’ intention to allow firms to grow and stay as a going concern is

very critical towards firms’ future endeavor. Even though staying as a going concern

could be achieved through many actions including mergers and acquisition (Khalijah et

al., 2011), however it all depends upon owners to propose the final decision (Kam et al.,

2008). If owners do not intend to continue growing for whatever reason, firms on their

own could not proceed with any mission or vision because owners are the ultimate

decision maker of firms (George & Kabir, 2012; Zahra, 2003). As such, understanding

ownership issue among surviving firms are critical to investors in making investment

decisions.

2.2 Ownership and Performance of Surviving Firms

There are two main types of ownership typical among firms all over the world, that is,

either concentrated or dispersed ownership. Previously firms in developed markets are

more typical of having dispersed ownership as compared to concentrated ownership

(Gugler et al., 2008; Thomsen et al., 2006). On the other hand firms in developing or

emerging markets including Malaysia have always been referred to constitute

concentrated ownership (Claessens et al., 2000; Polsiri & Jiraporn, 2012). Common

within the concentrated ownership is the institutional ownership, which may also comes

from government institutions and/or family owned (Thomsen et al., 2006). Common

within the dispersed ownership is the individual ownership, which can also include or

separated from insider ownership such as management ownership as long as their

ownership is less than a certain level of influence (Gugler et al., 2008).

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

8

This study investigates on both the concentrated and dispersed ownerships. The

concentrated ownership focused on institutional ownership in general. The dispersed

ownership focused on potential controlling ownerships hence include, managerial

ownership, BOD ownership and all other individuals ownership. Therefore, there are four

types of ownership being investigated in this study. Among the four types, institutional

ownership is the most commonly found to have control in firms (Polsiri & Jiraporn, 2012).

Furthermore, institutional ownership is also most commonly found to be associated with

firms’ performance (Gugler et al., 2008). As to which type of ownership has significant

influence towards performance of surviving firms in facing economic downturns is a

question not yet concrete in the literature. Understanding ownership influence toward

firm performance among surviving firms is not just important toward potential investors

but also other parties intended to form business relationships with the firms or having to

develop regulations on economic policies and corporate governance.

2.2.1 Institutional Ownership and Firms’ Performance

Organizations being owners to other institutions commonly referred to as institutional

owners or investors, usually hold substantial percentage of ownership in firms that they

own (Elyasiani & Jia, 2010). These institutional investors could be holding companies to

the firms they own or venture capitalists or owners in their own right (Bottazzi et al.,

2008). Since institutional investors have substantial ownership, they usually have a

strong voice in firms’ decision-making (Margaritis & Psillaki, 2010). Furthermore, since

these institutional owners invest highly in firms, they will ensure that their investments

will continuously be fruitful and survive in the long run utilizing whatever means possible

(Bottazzi et al., 2008). Among others, institutional owners can utilize internal funds

among firms that they own to assist subsidiaries or associates firms having cash flow

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

9

problems (Margaritis & Psillaki, 2010). The lower need for external funds can reduce

cost of capital, hence better firm performance.

Institutional owners are normally entities having strong networking which can also assist

their firms in securing more contracts and opportunities for business activities. The

lower risks and the higher potential to survive suggest institutional owners would have

higher association with performance of firms surviving economic problems. Hence it is

expected that the higher the institutional ownership in firms would be associated with

high performance especially among firms’ surviving multiple economic downturns.

Therefore, our first hypothesis is stated as follows:

H1: Institutional ownership is positively associated with performance of firms’

surviving multiple economic downturns.

2.2.2 Individual Ownership and Firms’ Performance

Organizations having many individual owners are commonly known as having dispersed

ownership (Gugler et al., 2008). Disperse investors do not have the capacity to be in

control in firms’ decision making because they normally do not know each other to be

able to organize a group decision. As such these owners could become the component

that increase agency cost in companies (Jensen & Meckling, 1976). The higher the

individual ownership in firms, the higher will be the risks for firms’ survival due to higher

agency costs. Managers will tend to make decisions more in favor of their own benefits

rather than the owners benefit due to lack of control from the owners (Bunkanwanicha et

al., 2008). Opportunistic behavior among managers normally does not favor firms’

performance in the long run and subsequently affected firms’ survival (Gugler et al.,

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

10

2008). Hence, firms having higher individual ownership are not expected to influence

performance of firms’ surviving multiple economic downturns.

Findings from studies on firms in developed countries where most of their companies

have dispersed ownership show that even in developed countries, individual ownership

per se do not influence firms’ performance and survival (Gadhoum, 1999; Richter &

Weiss, 2013). Firms’ survival and performances in developed countries were influence

by other factors such as firms’ size and management expertise but not by any specific

ownership such as individual or managerial ownerships. Only lately, when firms in

developed countries also being owned more by concentrated ownership that the

ownership structure show influence towards firms’ performance (Elyasiani & Jia, 2010;

Florackis et al., 2009). Therefore, based on findings in prior studies, we believe

individual ownership on their own would not affect performance of surviving firms due to

individual ownership lack of control on firms’ operations. Hence, our second hypothesis

is therefore stated as follows:

H2: Individual ownership is not associated with performance of firms’ surviving

multiple economic downturns.

2.2.3 Management Ownership and Firms’ Performance

When firms have management who are at the same time also owners to the firm, it is

expected that information asymmetry issue will reduce (Florackis et al., 2009; Rose,

2005). Consequently agency cost will also reduce. In such a case, when management

makes decisions, they are at the same time making decisions on their own behalf. It is

therefore expected that management being owners of firms will ensure that their

investments will prosper and beneficial. However, there is also wide prior literature

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

11

evidence that found managerial ownership related to entrenchment effect (Florackis et

al., 2009; Ryu & Yoo, 2011). Entrenchment effect normally assumed that management

owners only protect themselves and do not protect other shareholders. In a normal

situation, management would usually be given ownership due to the position they hold

and not necessarily due to being part of the founder family (Gadhoum, 1999). If

management is part of the founder family, they might be interested to ensure future

survival of the companies they own. However if they were given ownership only after

they join the companies and probably due to compensation, they might be interested

only to ensure firm performance is high during their tenure-ship.

Prior studies generally found that managerial ownership do not show positive

association with firm performance (Florackis et al., 2009; Gadhoum 1999). As such,

firms having management being owners will not necessarily care for firms’ long term

survival. Therefore, it is expected that managerial ownership will not be associated with

the performance of firms’ surviving multiple economic downturns. Furthermore, the

entrenchment effect where management can take advantage of their position to

expropriate firms’ resources (Chen & Yu, 2012) could end up with negative performance

among firms’ surviving multiple economic crises. Nevertheless, due to many prior

studies found both negative and positive associations between managerial ownership

with firms’ performance, we stated our third hypothesis as follows:

H3: Management ownership is associated with performance of firms’ surviving

multiple economic downturns.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

12

2.2.4 Board of Directors’ Ownership and Firms’ Performance

Board of directors (BOD) being the supreme decision maker in firms is expected to

create the smallest information asymmetry gap between management and owners

(MCCG, 2012). Within a typical corporate governance setting, BOD is the supreme

decision maker, acting on behalf of firms’ owners (shareholders). BOD is expected to act

not only on behalf of majority but also especially to minority shareholders. This is

because the minority shareholders are within the group of dispersed shareholders which

generally depend extremely upon firms’ management to provide them with results on

their investments. Minority shareholders do not only faced with agency conflict with firms’

management but much more with majority shareholders who have tendency for power

and control over firms’ management. Therefore, within a good corporate governance

environment, BOD is expected to act on behalf of all shareholders.

Having BOD ownership in firms would mean BOD decisions will tend to benefit all

owners generally. There will be as little conflict of interest between what management

decides and what BOD endorsed concerning ownership interests. This is because in the

current corporate governance setting, firms’ top management members will have as little

overlapping with the BOD members (MCCG, 2012). Hence, BOD ownership could

monitor top management actions better. As such, it is expected that if BOD has

ownership in the firms, the BOD will ensure that firms perform well throughout the firms’

lifetime regardless of whether the firms exist for a short or long time.

However, prior studies investigate BOD ownership as a reflection of managerial

ownership. As such, in the case of BOD ownership, it is expected that the issue of

entrenchment effect also exist similar to the concept of other managerial ownership

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

13

problems. This is because even though BOD should act on behalf of shareholders and

all other stakeholders, several of their members are directly involve in management of

the firms. Furthermore, many times BOD members are chosen based on their

networking with other prior BOD members of the firms or with the top management of

the firms (Florackis et al., 2009; Gadhoum, 1999; Gugler et al., 2008). Hence, it is

expected that BOD ownership association with firms’ performance would be similar to

the managerial ownership association with firms’ performance, that is, could be either

positive or negative. Therefore, our final hypothesis is stated as follows:

H4: Board of directors’ ownership is associated with performance of firms’

surviving multiple economic downturns.

3. METHODOLOGY

The aim of this study is to investigate whether ownership structure of listed firms in

Malaysia has any relationship with firm performance among firms surviving several

economic downturns. Data was collected from Annual Reports of sample firms. Our

sample is firms listed on the Main Market of Bursa Malaysia with three specific criteria.

The first criteria is that the firms must have survived since listed on Bursa Malaysia

(previously known as the Kuala Lumpur Stock Exchange, KLSE) until year 2012. The

second criterion is that the firms must start being listed at least prior to the 1997-1998

Asian financial crises. This will allow our sample to represent firms that survived at least

two major economic crisis periods, specifically the 1997-1998 Asian financial crisis and

the 2008-2009 global sub-prime crises. Finally the firms must still be listed on the stock

exchange in the year we collect our data which is year 2012.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

14

Financial firms (such as banks, insurance companies, financial institutions and

brokerage firms) are excluded from our analysis because their survival relates to the

existence of many regulations and government’s policies, which are compulsory for

them. Hence, their survival issue should be examined separately from non-financial

firms. Our data was collected for a 5 years period, 2007 through 2011. We do not

include year 2012 data because many firms have not yet uploaded their 2012 annual

reports on Bursa Malaysia website during the time period of our study.

3.1 Empirical Model

In order to find evidence to support our hypotheses, we utilized the performance model

commonly used in prior studies (O’Connell & Cramer, 2010; Omran et al., 2008;

Pangarkar & Wu, 2012) where we measure performance based on three situations:

Earnings per share (EARN), Return on Assets (ROA) and Market Capitalization

(MKTCAP). We utilize three performance measurements to investigate the internal and

external performances of the surviving firms in order to provide robust findings for our

analysis. We utilize external performance to be Market Capitalization (MKTCAP) based

on the conceptual issue of this measurement being a reflection of firms’ value at risk

(Dias, 2013; Narayan et al., 2011). Our internal and external performance empirical

models are as shown below:

- Internal Performance Model

PERFORMit = Β0 + β1InstOWNit + β2IndOWNit + β3MgmtOWNit

+ β4BODOWNit + β5SURVIVEit + β6SIZEit + β7LEVit + eit

Where:

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

15

Dependent variable

PERFORMit = (1) ROA – Return on Asset (Net Income / Total Assets) of firm i at time t

(2) EARN - Earnings per share of firm i at time t

Independent variables

SURVIVEit = Number of years firm exist since listed on the stock exchange for firm i at time t

InstOWNit = % of institutional ownership among 30 major shareholders of firm i at time t

IndOWNit = % of individual ownership among 30 major shareholders of firm i at time t

MgmtOWNit = % of top management ownership of firm i at time t

BODOWNit = % of board of directors (BOD) ownership of firm i at time t

Control variables

SIZEit = Log of Total Assets of firm i at time t

LEV(A)it = Ratio of Total Liability over Total Assets of firm i at time t

LEV(E)it = Ratio of Total Liability over Equity of firm i at time t

eit = Error term for this regression

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

16

- External Performance Model

PERFORMit = Β0 + β1InstOWNit + β2IndOWNit + β3MgmtOWNit + β4BODOWNit + β5SURVIVEit + β6ROAit + β7SIZEit +

β8LEVit + eit

Where:

Dependent variable

PERFORMit = MKTCAP – Share price multiply by number of outstanding shares for firm i at time t

Independent variables

SURVIVEit = Number of years firm exist since listed on the stock exchange for firm i at time t

InstOWNit = % of institutional ownership among 30 major shareholders of firm i at time t

IndOWNit = % of individual ownership among 30 major shareholders of firm i at time t

MgmtOWNit = % of top management ownership of firm i at time t

BODOWNit = % of board of directors (BOD) ownership of firm i at time t

Control variables

ROAit = ROA – Return on Asset (Net Income / Total Assets) of firm i at time t

SIZEit = Log of Total Assets of firm i at time t

LEVit = Ratio of Total Liability over Total Assets of firm i at time t

eit = Error term for this regression

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

17

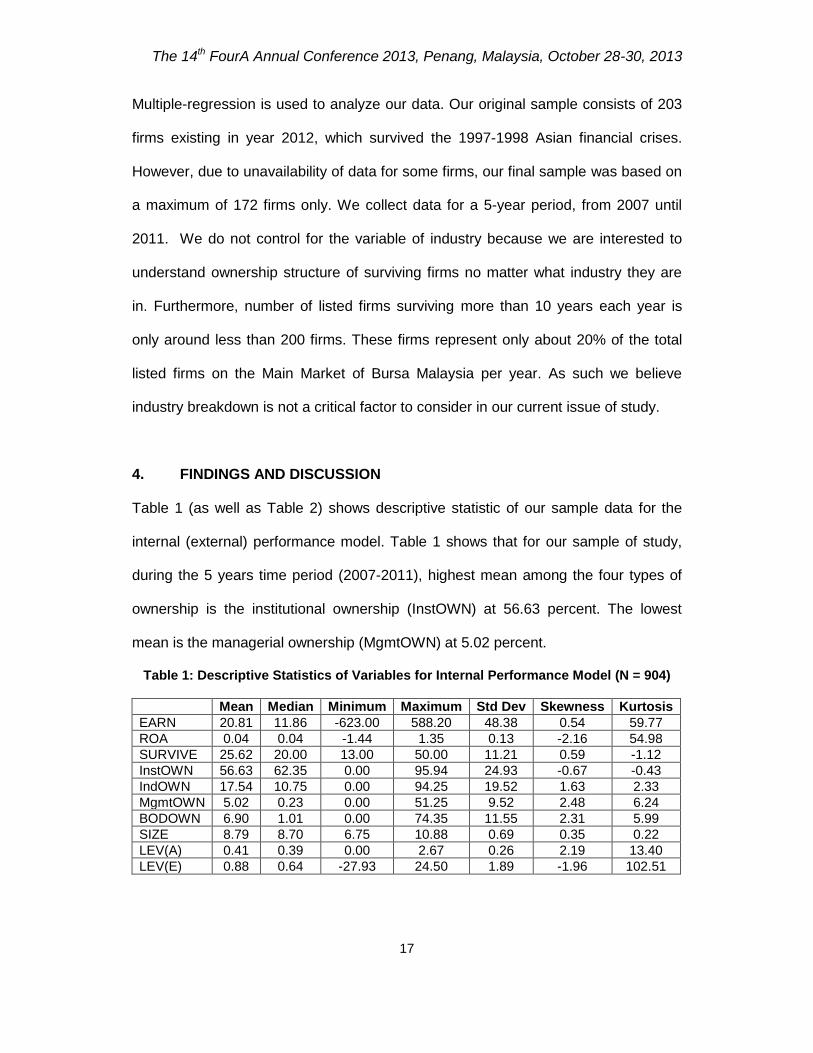

Multiple-regression is used to analyze our data. Our original sample consists of 203

firms existing in year 2012, which survived the 1997-1998 Asian financial crises.

However, due to unavailability of data for some firms, our final sample was based on

a maximum of 172 firms only. We collect data for a 5-year period, from 2007 until

2011. We do not control for the variable of industry because we are interested to

understand ownership structure of surviving firms no matter what industry they are

in. Furthermore, number of listed firms surviving more than 10 years each year is

only around less than 200 firms. These firms represent only about 20% of the total

listed firms on the Main Market of Bursa Malaysia per year. As such we believe

industry breakdown is not a critical factor to consider in our current issue of study.

4. FINDINGS AND DISCUSSION

Table 1 (as well as Table 2) shows descriptive statistic of our sample data for the

internal (external) performance model. Table 1 shows that for our sample of study,

during the 5 years time period (2007-2011), highest mean among the four types of

ownership is the institutional ownership (InstOWN) at 56.63 percent. The lowest

mean is the managerial ownership (MgmtOWN) at 5.02 percent.

Table 1: Descriptive Statistics of Variables for Internal Performance Model (N = 904)

Mean Median Minimum Maximum Std Dev Skewness Kurtosis

EARN 20.81 11.86 -623.00 588.20 48.38 0.54 59.77

ROA 0.04 0.04 -1.44 1.35 0.13 -2.16 54.98

SURVIVE 25.62 20.00 13.00 50.00 11.21 0.59 -1.12

InstOWN 56.63 62.35 0.00 95.94 24.93 -0.67 -0.43

IndOWN 17.54 10.75 0.00 94.25 19.52 1.63 2.33

MgmtOWN 5.02 0.23 0.00 51.25 9.52 2.48 6.24

BODOWN 6.90 1.01 0.00 74.35 11.55 2.31 5.99

SIZE 8.79 8.70 6.75 10.88 0.69 0.35 0.22

LEV(A) 0.41 0.39 0.00 2.67 0.26 2.19 13.40

LEV(E) 0.88 0.64 -27.93 24.50 1.89 -1.96 102.51

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

18

When examining our sample firms in more detail, maximum InstOWN at 95.94

percent belongs to Tasek Corporation Berhad for year 2010, a company focused on

operation of producing cement products. Maximum individual ownership (IndOWN)

at 94.25 percent belongs to Goh Ban Huat Berhad for year 2011, a company

focused on operation of producing tiling products. Maximum management ownership

(MgmtOWN) at 51.25 percent belongs to Seni Jaya Corporation Berhad for year

2010, a company focused on providing media services for outdoor and indoor

advertising. Maximum board of directors’ ownership (BODOWN) at 74.35 percent

belongs to Goh Ban Huat Berhad for year 2010. Data suggest that in year 2011,

many directors in Goh Ban Huat Berhad cease to become directors after 2010 but

still hold majority ownership together as individuals.

Table 2: Descriptive Statistics Of Variables for External Performance Model (N = 817)

Mean Median Minimum Maximum Std Dev Skewness Kurtosis

MKTCAP 8.45 8.30 6.47 11.39 0.81 0.55 -0.09

ROA 0.05 0.04 -1.44 0.67 0.11 -2.72 52.53

SURVIVE 25.85 20.00 13.00 50.00 11.18 0.56 -1.15

InstOWN 56.62 62.37 0.00 95.94 24.74 -0.72 -0.30

IndOWN 17.42 10.65 0.00 94.25 19.58 1.64 2.39

MgmtOWN 4.99 0.18 0.00 51.25 9.33 2.43 5.92

BODOWN 7.01 1.07 0.00 74.35 11.56 2.28 5.91

SIZE 8.81 8.71 6.95 10.88 0.67 0.49 0.17

LEV 0.39 0.39 0.00 2.27 0.23 1.24 6.53

Table 3 shows Pearson correlation of variables for our sample data with regards to

our internal performance model. Table 3 shows that two types of ownership; that is,

institutional (InstOWN) and individual (IndOWN) consistently show significant

association with firms’ performance, measured either based on ROA or earnings per

share (EARN). Where InstOWN show positive association, on the other hand

IndOWN show negative association. However, managerial (MgmtOWN) and board of

directors (BODOWN) ownerships only show significant association with firm

performance measured based on EARN (see Table 4 for details). Findings in Table 3

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

19

and Table 4 provide initial evidence of potential association between categories of

ownerships and firms’ performance.

Table 3: Pearson Correlation of Variables for Internal Performance Model (N = 904)

Dependent = ROA

SURVIVE InstOWN IndOWN MgmtOWN BODOWN SIZE LEV(A)

ROA 0.14*** 0.18*** -0.12*** -0.02 -0.05 0.18*** -0.23***

SURVIVE 0.26*** -0.34*** -0.24*** -0.24*** 0.26*** -0.17***

InstOWN -0.83*** -0.54*** -0.64*** 0.49*** -0.07**

IndOWN 0.62*** 0.78*** -0.49*** -0.06

MgmtOWN 0.83*** -0.19*** -0.04

BODOWN -0.22*** -0.06

SIZE 0.10***

Dependent = EARN

SURVIVE InstOWN IndOWN MgmtOWN BODOWN SIZE LEV(E)

EARN 0.20*** 0.28*** -0.22*** -0.11*** -0.14*** 0.34*** -0.07**

SURVIVE -0.04

InstOWN -0.01

IndOWN -0.07**

MgmtOWN 0.02

BODOWN 0.01

SIZE 0.15***

Note: *, **, *** represent significance level at <0.10, <0.05, <0.01 respectively.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

20

Table 4: Pearson Correlation of Variables for External Performance Model (N = 817)

(1) (2) (3) (4) (5) (6) (7) LEV

MKTCAP 0.36*** 0.34*** 0.55*** -0.53*** -0.25*** -0.28*** 0.87*** -0.00

ROA (1) 0.19*** 0.20*** -0.15*** -0.05 -0.08** 0.19*** -0.20***

SURVIVE (2) 0.26*** -0.34*** -0.23*** -0.24*** 0.28*** -0.14***

InstOWN (3) -0.85*** -0.54*** -0.65*** 0.50*** -0.05

IndOWN (4) 0.61*** 0.78*** -0.52*** -0.07*

MgmtOWN (5) 0.82*** -0.21*** -0.02

BODOWN (6) -0.25*** -0.04

SIZE (7) 0.17***

Note: *, **, *** represent significance level at <0.10, <0.05, <0.01 respectively.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

21

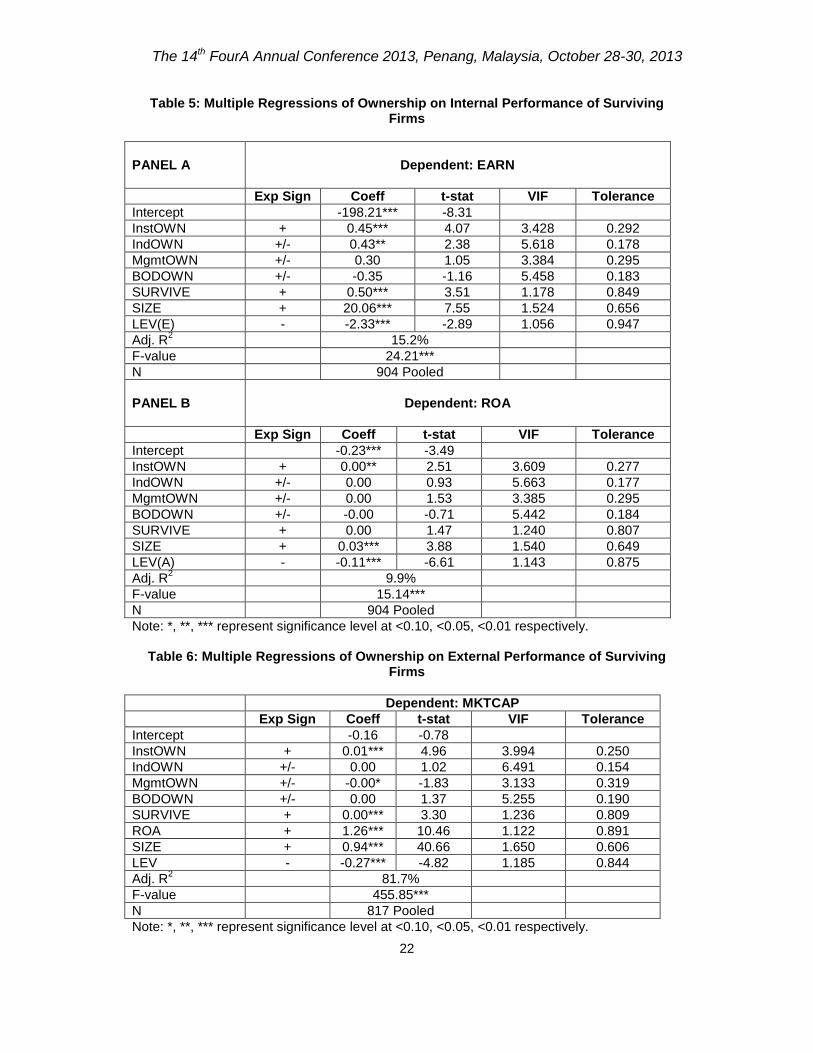

With respect to the issue of multicollinearity, Table 3 (and Table 4) also shows that

high positive collinearity is between MgmtOWN and BODOWN at 83% or 0.83 (at

85% in Table 4). In multiple regression analysis, when either one of the variable is

taken out from the analysis, findings remain conceptually the same throughout.

Similarly in the case of correlation between InstOWN and IndOWN which is negative

at 83% in Table 3 (and negative but at 82% in Table 4), when either one of the

variable is taken out from the analysis, findings remain conceptually the same

throughout. We also test for multicollinearity issue based on absence of problem if

VIF is less than 10 and Tolerance is more than 0.1 (Meyers et al., 2006) in multiple

regressions. We do not find any problem of multicollinearity among independent

variables in all three-performance models. Therefore, we present our findings based

on inclusion of all variables as originally proposed.

Findings in Table 5 and Table 6 support extant research findings on the association

between institutional ownership and firm performance (Elyasiani & Jia, 2010; Tsai &

Gu, 2007). Findings on the association between the other three categories of

ownerships also conceptually support prior findings in terms of being not clear on the

contribution of ownerships to firm performance. Ownership effect was suggested to

be investigated in more detail in terms of specific factors that influence each

category of ownership (Gugler et al., 2008).

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

22

Table 5: Multiple Regressions of Ownership on Internal Performance of Surviving Firms

PANEL A

Dependent: EARN

Exp Sign Coeff t-stat VIF Tolerance

Intercept -198.21*** -8.31

InstOWN + 0.45*** 4.07 3.428 0.292

IndOWN +/- 0.43** 2.38 5.618 0.178

MgmtOWN +/- 0.30 1.05 3.384 0.295

BODOWN +/- -0.35 -1.16 5.458 0.183

SURVIVE + 0.50*** 3.51 1.178 0.849

SIZE + 20.06*** 7.55 1.524 0.656

LEV(E) - -2.33*** -2.89 1.056 0.947

Adj. R2

15.2%

F-value 24.21***

N 904 Pooled

PANEL B

Dependent: ROA

Exp Sign Coeff t-stat VIF Tolerance

Intercept -0.23*** -3.49

InstOWN + 0.00** 2.51 3.609 0.277

IndOWN +/- 0.00 0.93 5.663 0.177

MgmtOWN +/- 0.00 1.53 3.385 0.295

BODOWN +/- -0.00 -0.71 5.442 0.184

SURVIVE + 0.00 1.47 1.240 0.807

SIZE + 0.03*** 3.88 1.540 0.649

LEV(A) - -0.11*** -6.61 1.143 0.875

Adj. R2

9.9%

F-value 15.14***

N 904 Pooled

Note: *, **, *** represent significance level at <0.10, <0.05, <0.01 respectively.

Table 6: Multiple Regressions of Ownership on External Performance of Surviving Firms

Dependent: MKTCAP

Exp Sign Coeff t-stat VIF Tolerance

Intercept -0.16 -0.78

InstOWN + 0.01*** 4.96 3.994 0.250

IndOWN +/- 0.00 1.02 6.491 0.154

MgmtOWN +/- -0.00* -1.83 3.133 0.319

BODOWN +/- 0.00 1.37 5.255 0.190

SURVIVE + 0.00*** 3.30 1.236 0.809

ROA + 1.26*** 10.46 1.122 0.891

SIZE + 0.94*** 40.66 1.650 0.606

LEV - -0.27*** -4.82 1.185 0.844

Adj. R2

81.7%

F-value 455.85***

N 817 Pooled

Note: *, **, *** represent significance level at <0.10, <0.05, <0.01 respectively.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

23

5. CONCLUSION

This paper investigates the relationship between ownership structure and

performance of listed firms’ surviving multiple economic crises in Malaysia. Findings

suggest that surviving firms show better performance if they have higher level of

institutional ownership only. Findings also suggest that surviving firms tend to show

poor performance if they have higher level of management ownership. However, it is

unclear in the case of board of directors’ (BOD) ownership. As for individual

ownership, findings might actually reflect the situation of dispersed ownership

whereby they generally do not have any effect on firms’ performance. Findings from

this study could provide input to potential long-term investors for their investments

decision making in Malaysian firms. Existence of high institutional ownership in firms

seems to reflect a good choice for long-term investments. On the other hand,

existence of high managerial ownership could reflect otherwise.

Even though this study finds a significant association between institutional ownership

and firm performance, our investigation assume only the existence of a linear

relationship between the two. Therefore, we would like to caution generalization of

our findings to other settings. Prior studies have suggested that there might be a

non-linear relationship between certain types of ownership with firm performance.

Therefore, further investigation need to be done to examine the non-linear issue.

Additionally, the latest improvements to the Malaysian Code of Corporate

Governance in year 2012 (MCCG, 2012) might change the distribution of

management and BOD membership after the period of our study. This change could

affect the ownership structure involving management and BOD members. As such, a

more detail investigation on composition of managerial and BOD ownership could be

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

24

undertaken to understand their latest influence towards firms’ performance.

Similarly, further investigation on the composition of institutional ownership could

also be done such as in the case of government institution versus private institution

ownership influence on firm performance.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

25

REFERENCES

Achleitner, A.K., Kaserer, C. & Kauf, T. (2012). The dynamics of voting ownership in lone-founder, family-founder, and heir firms. Journal of Family Business Strategy, xxx, xxx–xxx.

Almeida, S., & Fernando, M. (2008). Survival strategies and characteristics of start-

ups: an empirical study from New Zealand IT industry. Technovision, 28, 161-169.

Bottazzi, L., Da Rin, M. & Hellmann, T. (2008). Who are the active investors?

Evidence from venture capital. Journal of Financial Economics, 89, 488–512. Bunkanwanicha, P., Gupta, J. & Rokhim, R. (2008). Debt and entrenchment:

Evidence from Thailand and Indonesia. European Journal of Operational Research, 185, 1578–1595.

Chen, C-J. & Yu, C-M.J. (2012). Managerial ownership, diversification, and firm

performance: Evidence from an emerging market. International Business Review, 21, 518–534.

Claessens, S., Djankov, S. & Lang, L.H.P. (2000). The separation of ownership and

control in East Asian Corporations. Journal of Financial Economics, 58, 81-112.

Cortese, C.L., Irvine, H.J., & Kaidonis, M.A. (2009). Extractive industries accounting

and economic consequences: past, present and future. Accounting Forum, 33, 27-37.

Dias, A. (2013). Market capitalization and Value-at-Risk. Journal of Banking &

Finance, xxx, xxx–xxx. Elyasiani, E. & Jia, J. (2010). Distribution of institutional ownership and corporate

firm performance. Journal of Banking & Finance, 34, 606–620. Euh, Y.D., & Rhee, J.H. (2007). Lessons from the Korean crisis: policy and

managerial implications. Long Range Planning, 40, 431-445. Florackis, C., Kostakis, A. & Ozkan, A. (2009). Managerial ownership and

performance. Journal of Business Research, 62, 1350–1357. Gadhoum, Y. (1999). Potential effects of managers' entrenchment and

shareholdings on competitiveness. European Journal of Operational Research, 118, 332-349.

George, R. & Kabir, R. (2012). Heterogeneity in business groups and the corporate

diversification–firm performance relationship. Journal of Business Research, 65, 412–420.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

26

Gugler, K., Mueller, D.C. & Yurtoglu, B.B. (2008). Insider ownership, ownership concentration and investment performance: An international comparison. Journal of Corporate Finance, 14, 688–705.

Jensen, M. & Meckling, W. (1976). Theory of the firm: managerial behavior, agency

costs and ownership structure. Journal of Financial Economics, 3, 305–360. Kam, A., Citron, D. & Muradoglu, G. (2008). Distress and restructuring in China:

Does ownership matter? China Economic Review, 19, 567–579. Khalijah, A., Romlah, J., Zaleha, A.S., Aini, A. & Ruhanita, M. (2011). The use of

legal protection under section 176 of Companies Act 1965 for survival during economic crisis. Proceedings of the 1st International Conference on Accounting, Business and Economics.

Kim, Y.S. & Mathur, I. (2008). The impact of geographic diversification on firm

performance. International Review of Financial Analysis, 17, 747–766. Knox, K.J., Blankmeyer, E.C., Trinidad, J.A., & Stutzman, J.R. (2008). Predicting

bankruptcy in the Texas nursing facility industry. The Quarterly Review of Economics and Finance, doi:10.1016/j.qref.2008.08.004.

Manolova, T.S., Manev, I.M. & Gyoshev, B.S. (2010). In good company: The role of

personal and inter-firm networks for new-venture internationalization in a transition economy. Journal of World Business, 45, 257–265.

Margaritis, D. & Psillaki, M. (2010). Capital structure, equity ownership and firm

performance. Journal of Banking & Finance, 34, 621–632. Malaysian Code on Corporate Governance (MCCG). (2012). Securities Commission

Malaysia: Kuala Lumpur. Meyers, L.S., Gamst, G. & Guarino, A.J. (2006). Applied Multivariate Research.

Sage Publications: Thousand Oaks, California. Nachum, L. (1999). Diversification strategies of developing country firms. Journal of

International Management, 5, 115–140. Narayan, P.K., Mishra, S. & Narayan, S. (2011). Do market capitalization and stocks

traded converge? New global evidence. Journal of Banking & Finance, 35, 2771–2781.

O’Connell, V. & Cramer, N. (2010). The relationship between firm performance and

board characteristics in Ireland. European Management Journal, 28, 387– 399.

Omran, M.M., Bolbol, A. & Fatheldin, A. (2008). Corporate governance and firm

performance in Arab equity markets: Does ownership concentration matter? International Review of Law and Economics, 28, 32–45.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

27

Pananond, P. (2007). The changing dynamics of Thai multinationals after the Asian economic crisis. Journal of International Management, 13, 356-375.

Pangarkar, N. & Wu, J. (2012). Industry globalization and the performance of

emerging market firms: Evidence from China. International Business Review, 21, 196–209.

Plehn-Dujowich, J. (2009). A theory of serial entrepreneurship. Small Business

Economics, DOI 10.1007/s11187-008-9171-5. Polsiri, P. & Jiraporn, P. (2012). Political connections, ownership structure, and

financial institution failure. Journal of Multinational Financial Management, 22, 39– 53.

Richter, A. & Weiss, C. (2013). Determinants of ownership concentration in public

firms: The importance of firm-, industry- and country-level factors. International Review of Law and Economics, 33, 1–14.

Ritchie, B.W. (2004). Chaos, crises and distress: a strategic approach to crisis

management in the tourism industry. Tourism Management, 25, 669-683. Rose, C. (2005). Managerial Ownership and Firm Performance in Listed Danish

Firms: In Search of the Missing Link. European Management Journal, 23, 5, 542–553.

Ryu, K. & Yoo, J. (2011). Relationship between management ownership and firm

value among the business group affiliated firms in Korea. Journal of Comparative Economics, 39, 557–576.

Thomsen, S., Pedersen, T. & Kvist, H.K. (2006). Blockholder ownership: Effects on

firm value in market and control based governance systems. Journal of Corporate Finance, 12, 246– 269.

Tsai, H. & Gu, Z. (2007). The relationship between institutional ownership and casino

firm performance. Hospitality Management, 26, 517–530. Tsoukas, S. (2011). Firm survival and financial development: Evidence from a panel

of emerging Asian economies. Journal of Banking & Finance, 35, 1736–1752. Yen, T.Y. & Andre, P. (2007). Ownership structure and operating performance of

acquiring firms: The case of English-origin countries. Journal of Economics and Business, 59, 380–405.

Zahra, S.A. (2003). International expansion of U.S. manufacturing family businesses:

the effect of ownership and involvement. Journal of Business Venturing, 18, 495–512.

The 14th FourA Annual Conference 2013, Penang, Malaysia, October 28-30, 2013

28

Zahra, S.A., Filatotchev, I., & Wright, M. (2008). How do threshold firms sustain corporate entrepreneurship? The role of boards and absorptive capacity. Journal of Business Venturing, doi:101016/j.jbusvebt.2008.09.001.

Zhang, X., Venus, J. & Wang, Y. (2012). Family ownership and business expansion

of small- and medium-sized Chinese family businesses: The mediating role of financing preference. Journal of Family Business Strategy, 3, 97-105.