THE RELATIONSHIP BETWEEN FREE CASH FLOWS …chss.uonbi.ac.ke/sites/default/files/chss/KINYANJUI...

62

THE RELATIONSHIP BETWEEN FREE CASH FLOWS AND INVESTMENTS OF FIRMS QUOTED AT THE NAIROBI SECURITIES EXCHANGE BY KINYANJUI MICHAEL M. D63/60249/2013 A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE IN FINANCE OF THE UNIVERSITY OF NAIROBI 2014

Transcript of THE RELATIONSHIP BETWEEN FREE CASH FLOWS …chss.uonbi.ac.ke/sites/default/files/chss/KINYANJUI...

THE RELATIONSHIP BETWEEN FREE CASH FLOWS AND

INVESTMENTS OF FIRMS QUOTED AT THE NAIROBI

SECURITIES EXCHANGE

BY

KINYANJUI MICHAEL M.

D63/60249/2013

A RESEARCH PROJECT SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE IN FINANCE OF THE UNIVERSITY OF

NAIROBI

2014

ii

DECLARATION

This research project is my original work and has not been presented in any other

examination body. No part of this research project should be produced without my

consent or that of the University of Nairobi.

Signature………………………..………. Date:…………………………………

Name: Kinyanjui Michael M.

REG: D63/60249/2013

DECLARATION

This research project has been submitted with the approval of the University of Nairobi

SUPERVISOR

Signature………………………………… Date…………………………………….…

Name: Mr. James M. Karanja

Lecturer, Department of Finance and Accounting

School of Business, University of Nairobi

iii

ACKNOWLEDGMENT

I would like to first and foremost thank God for sustaining me in the course of my studies

and enabling me complete this research project.

I would like to thank my entire family for their encouragement and being there for me

during this period. To also my friends and classmates for supporting me throughout the

course especially where matters of group work and revision were concerned.

I give special thanks to my supervisor Mr. James M. Karanja who worked closely with

me in developing this research project. I also wish to thank my lecturers and the whole

staff of the University of Nairobi for enriching my academic life.

May the Almighty God bless you all greatly!

iv

DEDICATION

This paper is dedicated to my Mother Mrs Lucy Kinyanjui for her support and

encouragement, and to my whole entire family for their support throughout the course.

To my nephew Andrew and nieces Nichole and Kimberly I encourage them to work hard

in school.

v

TABLE OF CONTENTS DECLARATION........................................................................................................................... ii

ACKNOWLEDGMENT ............................................................................................................. iii

DEDICATION.............................................................................................................................. iv

LIST OF TABLES ...................................................................................................................... vii

LIST OF CHARTS .................................................................................................................... viii

LIST OF ABBREVIATIONS ..................................................................................................... ix

ABSTRACT ................................................................................................................................... x

CHAPTER ONE: INTRODUCTION ..........................................................................................1

1.1 Background Information ........................................................................................................... 1

1.1.1 Free cash flows .................................................................................................................2

1.1.2 Investment decisions .........................................................................................................3

1.1.3 Effect of free cash flows on investments ..........................................................................4

1.1.4 Nairobi Securities Exchange (NSE) ..................................................................................4

1.2 Problem Statement .................................................................................................................... 5

1.3 Research Objective ................................................................................................................... 6

1.4 Value of the Study .................................................................................................................... 6

CHAPTER TWO: LITERATURE REVIEW .............................................................................8

2.0 Introduction ............................................................................................................................... 8

2.1 Theoretical Review ................................................................................................................... 8

2.1.1 Dividend policy related theories .......................................................................................8

2.1.2 Pecking order theory .........................................................................................................9

2.1.3 Agency Costs Based Theory .............................................................................................9

2.2 Determinants of investments of listed firms ........................................................................... 10

2.2.1 Real interest rates ............................................................................................................11

2.2.2 Exchange rate ..................................................................................................................11

2.2.3 Capital Stock ...................................................................................................................11

2.2.4 Dividend policy and Retention policy ............................................................................12

2.3 Empirical Review .................................................................................................................... 14

2.4 Summary of the Literature Review ......................................................................................... 22

vi

CHAPTER THREE: RESEARCH METHODOLOGY ..........................................................24

3.1 Introduction ............................................................................................................................. 24

3.2 Research Design...................................................................................................................... 24

3.3 The Population ........................................................................................................................ 24

3.4 Sampling Method .................................................................................................................... 24

3.5 Data Collection ....................................................................................................................... 25

3.6 Data Analysis .......................................................................................................................... 25

3.6.1 Research Model ....................................................................................................................25

CHAPTER FOUR: DATA ANALYSIS, RESULTS AND DISCUSSION .............................29

4.1 Introduction ............................................................................................................................. 29

4.2 General Findings ..................................................................................................................... 29

4.2.1 Net Capital Expenditure ..................................................................................................29

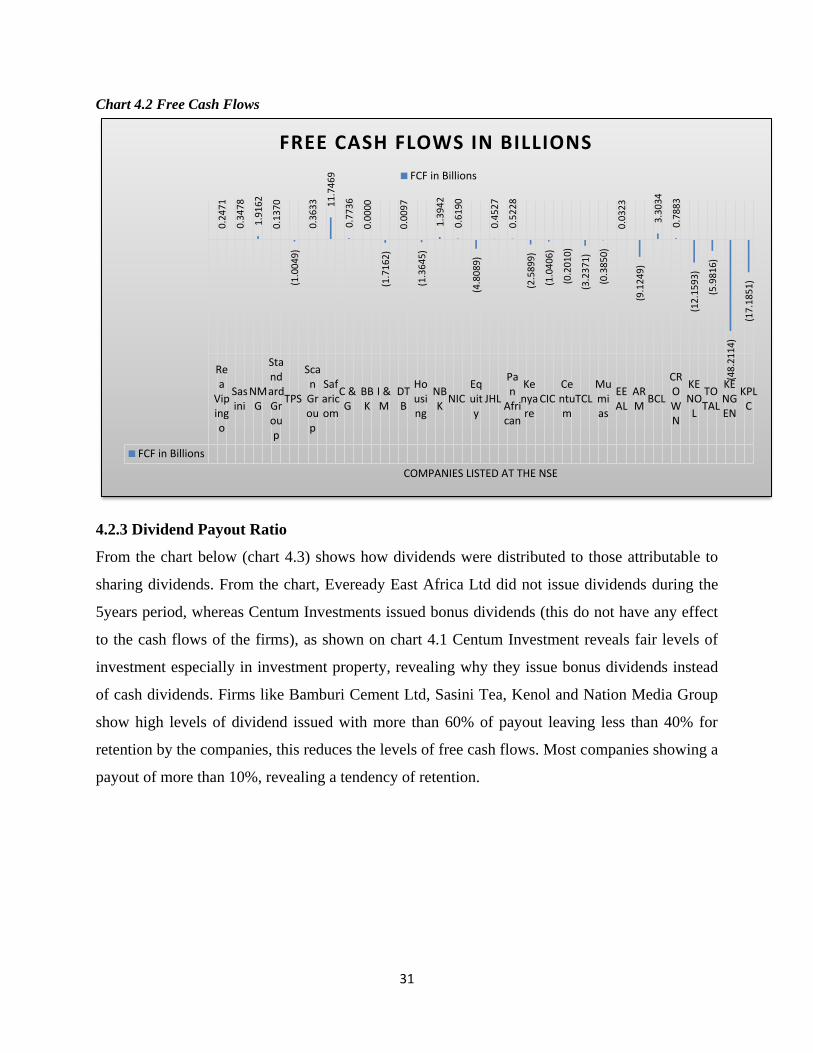

4.2.2 Free Cash Flows ..............................................................................................................30

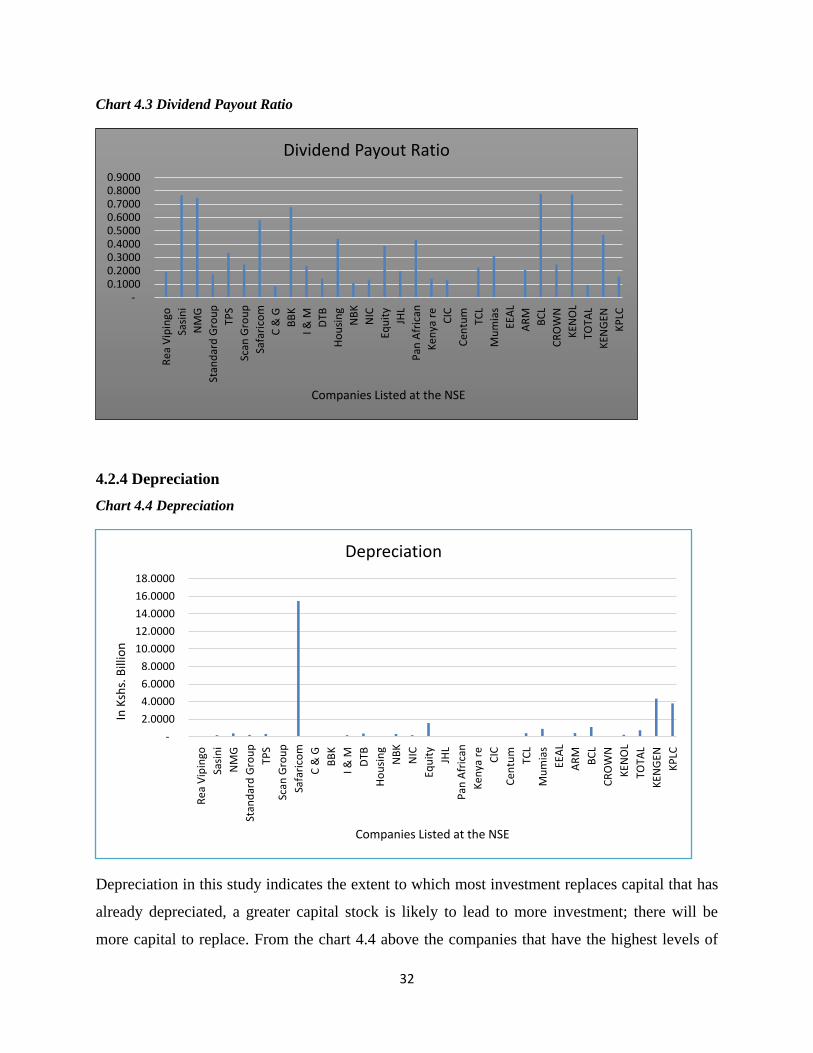

4.2.3 Dividend Payout Ratio ....................................................................................................31

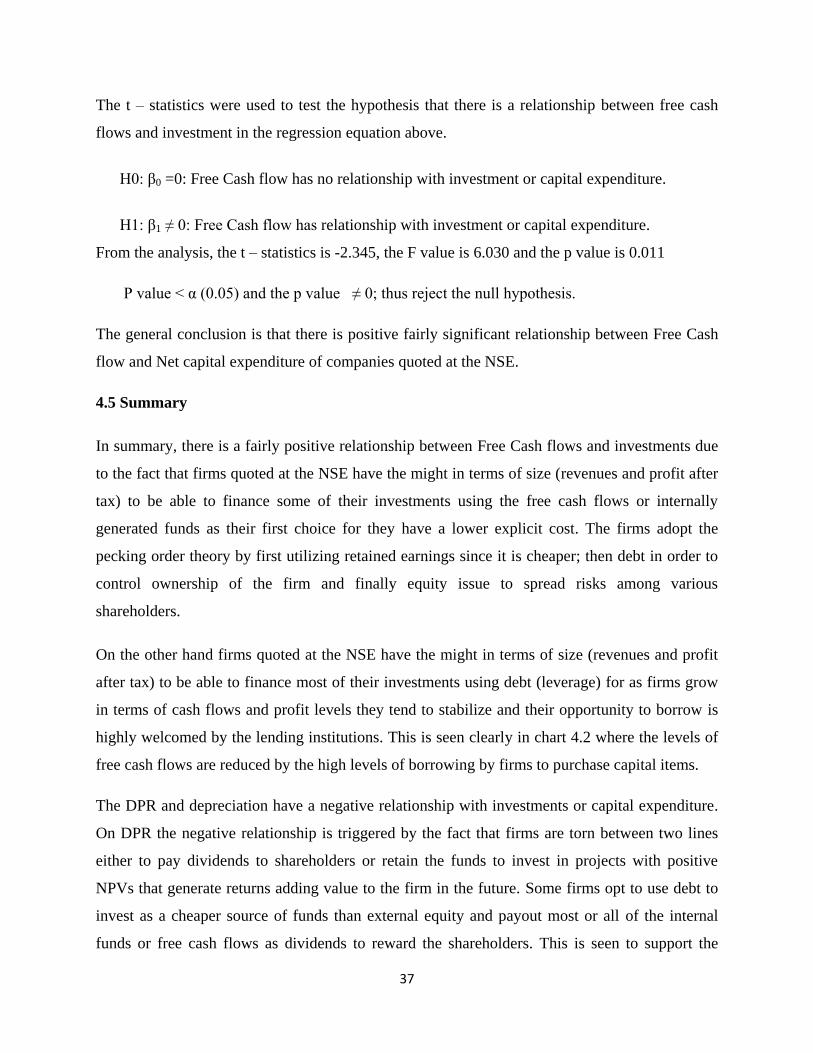

4.2.4 Depreciation ....................................................................................................................32

4.3 Correlation Analysis ............................................................................................................... 33

4.4 Regression Analysis and Hypothesis testing ......................................................................... 34

4.5 Summary ................................................................................................................................. 37

CHAPTER FIVE: SUMMARY, CONCLUSION AND RECOMMENDATIONS ...............39

5.1 Introduction ............................................................................................................................. 39

5.2 Summary ................................................................................................................................. 39

5.3 Conclusions ............................................................................................................................. 39

5.4 Recommendations ................................................................................................................... 40

5.5 Limitations of the Study.......................................................................................................... 41

5.6 Suggestions for Further Research ........................................................................................... 41

REFERENCES .............................................................................................................................42

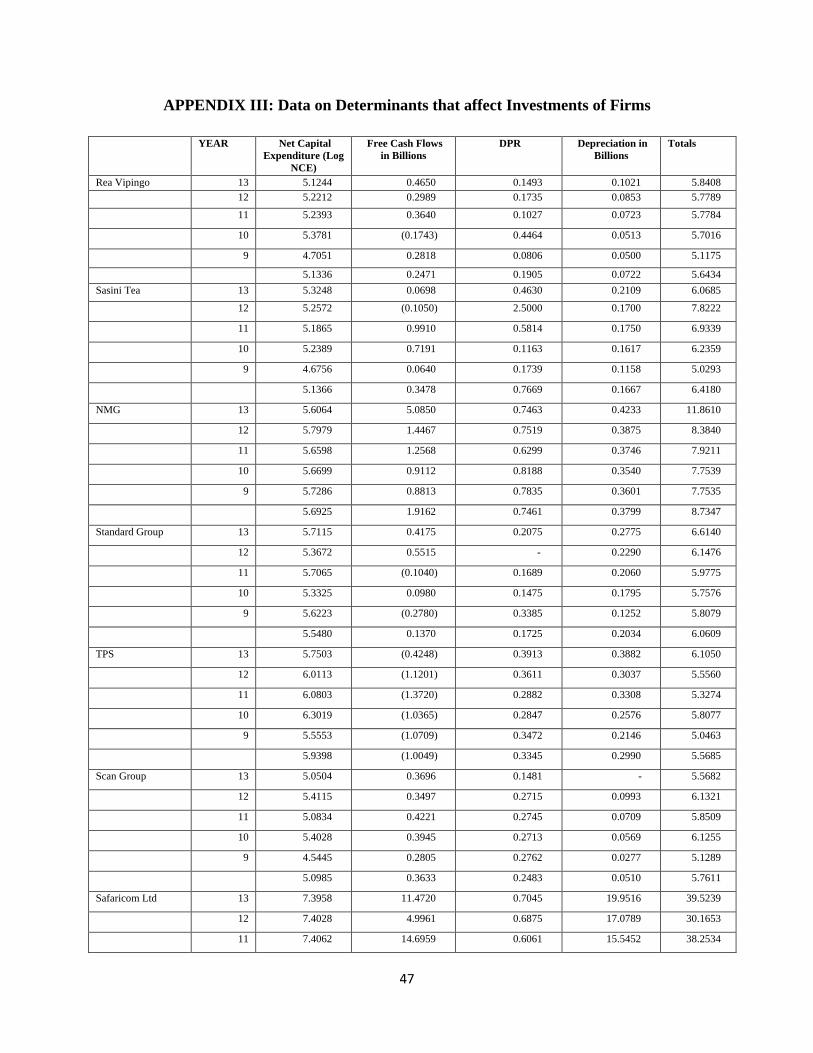

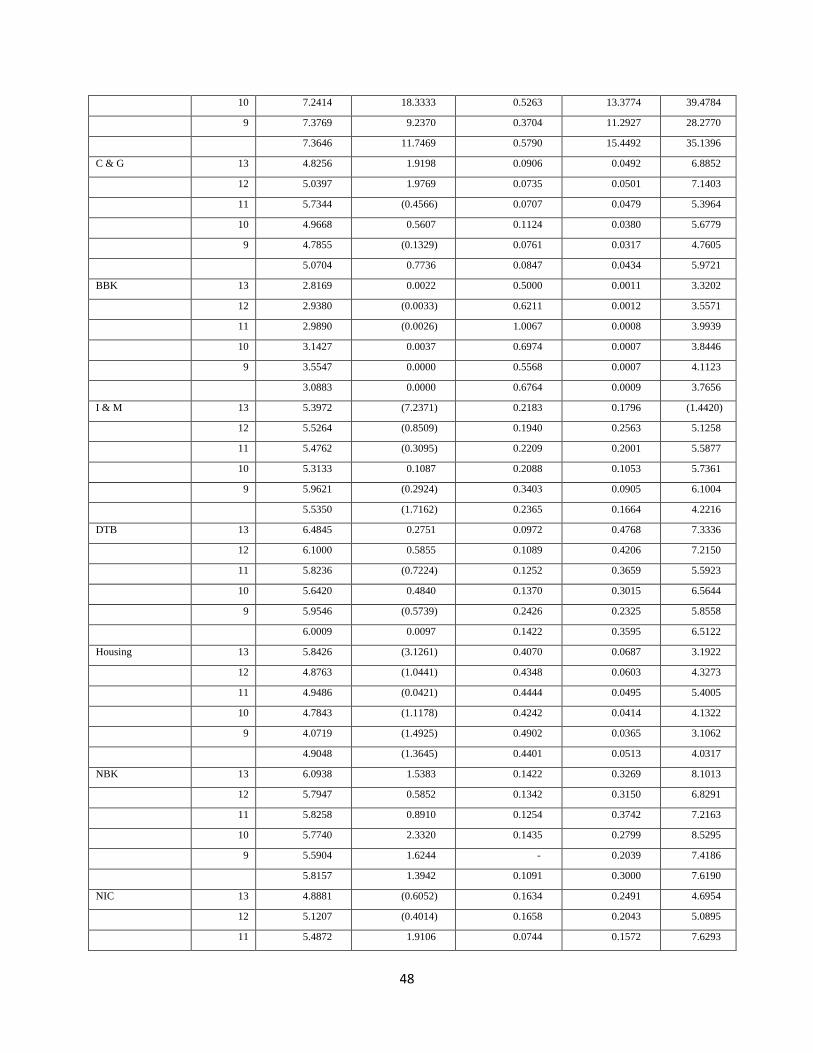

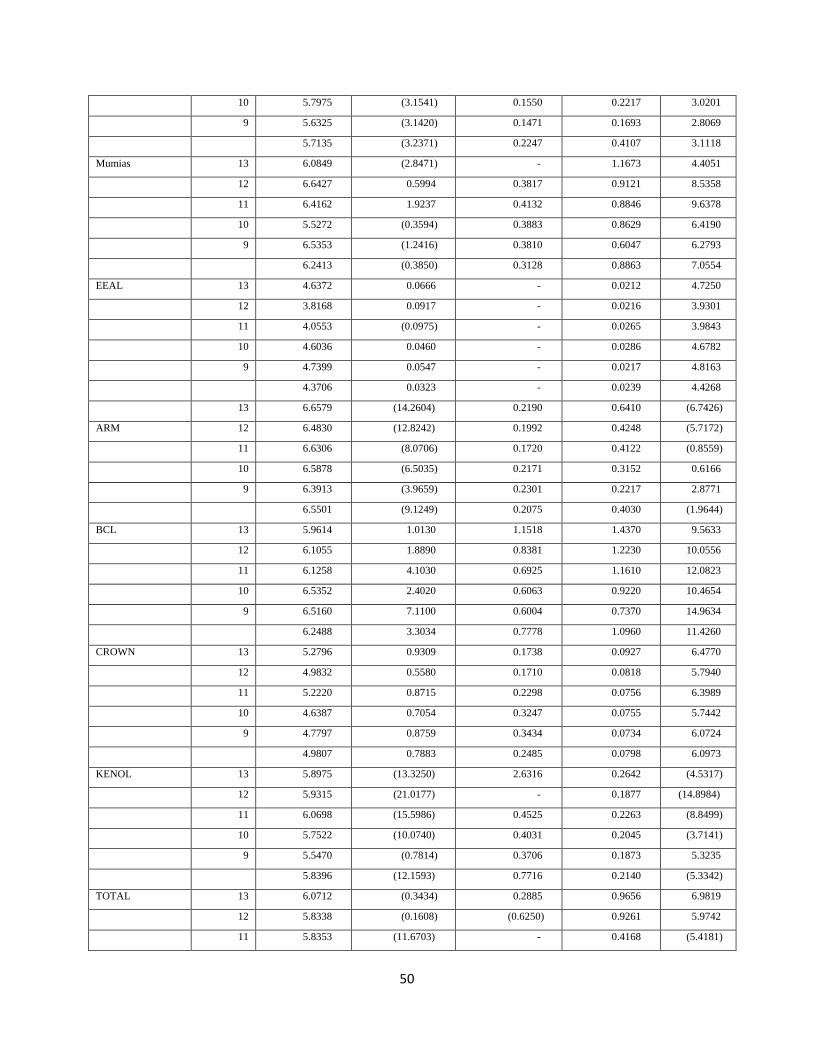

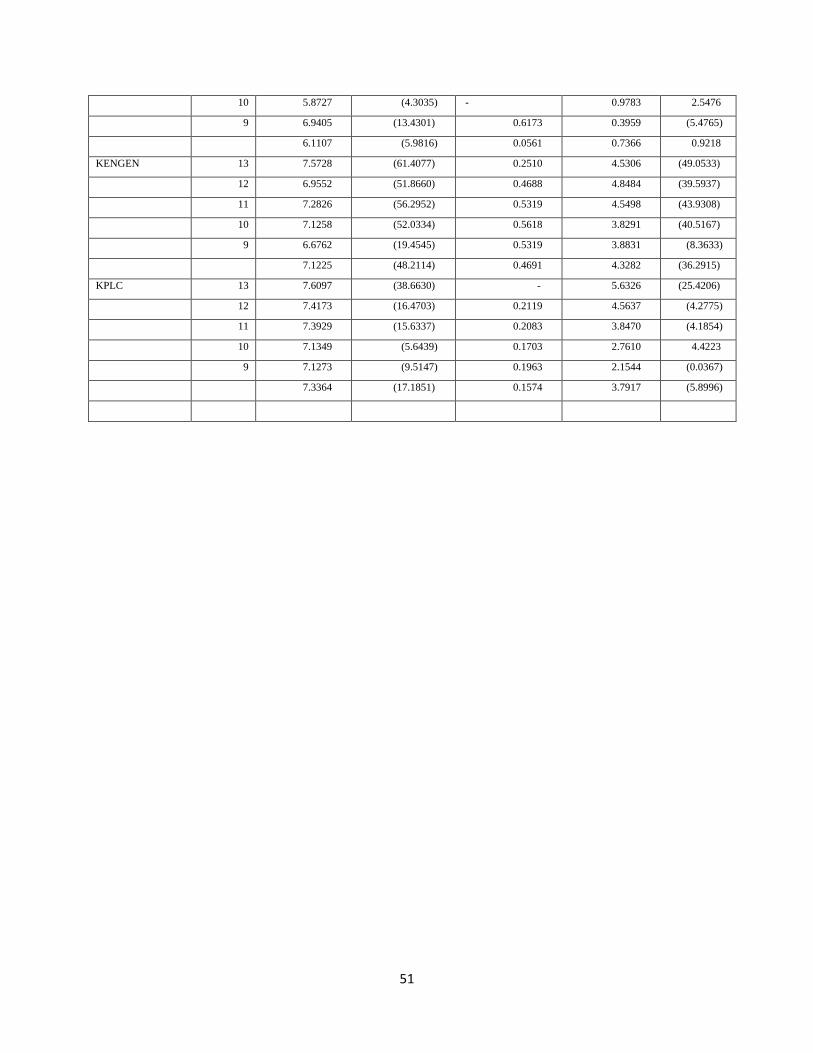

APPENDIX 1 .................................................................................................................................45

APPENDIX II ................................................................................................................................46

APPENDIX III ...............................................................................................................................47

vii

LIST OF TABLES

Table 4.1: Correlation Matrix…………………………………………………….…..33

Table 4.2: Model Summary……………………………………………………….….34

Table 4.3: Analysis of Variance (ANOVA)…………………………………….……35

Table 4.4: Coefficients of Determination…………………………………………....35

viii

LIST OF CHARTS

Chart 4.1: Net Capital Expenditure …………………………………………………30

Chart 4.2: Free Cash Flows ………………………………………...………….……31

Chart 4.3: Dividend Payout Ratio …………………………………………..……....32

Chart 4.4: Depreciation……………………………………………………...……....32

ix

LIST OF ABBREVIATIONS

ANOVA - Analysis of Variance

CMA - Capital Markets Authority

DPR - Dividend Payout Ratio

FCF - Free Cash Flows

IMF - International Monetary Fund

MM - Modigliani and Miller

NCE - Net Capital Expenditure

NPV - Net Present Value

NSE - Nairobi Securities Exchange

RD - Research and Development

SPSS - Software Package for Statistical Analysis

x

ABSTRACT

The aim of this study was to establish the relationship between free cash flow and investments of

companies listed at the Nairobi Stock Exchange. Companies engage in various ways to finance

their investments, including equity financing (internally generated funds and externally raised

funds) and or debt. Free cash flow tempts managers to expand the scope of operations and the

size of the firm, these spending is seen as unprofitable especially to the shareholders, who see it

worthwhile for the firm to issue dividends instead of retaining the funds to invest. Capital

expenditure is strongly and positively associated to the level of free cash flow (the more free

cash flows a firm has, the more investments the firm can engage in. The study aimed at

determining the relationship between the level of free cash flow and the amount of extra cash

that can be committed on investment decisions by companies that are listed at the Nairobi Stock

Exchange. Data was obtained from annual statements of listed companies. The study covered a

five year period from 2009 to 2013. Multiple linear regression method was used to identify the

existence of the relationship. The regression model results point out that FCF have a positive

impact on Net Capital Expenditure. From the organizations considered, it was established that

there is a positive fairly significant relationship between free cash flows and investment that is as

the level of free cash flows increase, the level of investments increases. This study used only

three variables as the measures of the relationship between free cash flows and investments,

hence there is need to carry out the study with other different factors in order to be able to

establish whether there are other major factors that have a relationship with investments at the

NSE and in companies not listed at the NSE.

1

CHAPTER ONE:

INTRODUCTION

1.1 Background Information

The main objective of the firm is to maximize the shareholders wealth. In relation to financial

management this objective can be achieved by analyzing the two sides of the statement of

financial position. On the assets side, the focus is on adding value to the shareholders wealth by

taking advantage of investment opportunities that is projects that generate positive NPVs.

On the liability and capital side, the focus is maximizing value by reducing the cost of financing

the investments of the firm. Companies engage in various ways to finance their investments,

including equity financing (internally generated funds and externally raised funds) and or debt.

Internally generated funds refer to the retained earnings, which in relation to various factors

among them stage in the firm‟s life cycle (which depicts the dividend policy applied) determine

whether the retained earnings will be wholly distributed as dividends to shareholders, partly

distributed to the shareholders and partly utilized to investment or capital expenditure and or

wholly retained to be invested in projects that generate positive NPVs.

External equity financing or new equity unlike internally generated funds, attract a higher cost in

raising the funds (flotation costs), thus most firms first use the internal funds to finance firms

investments because its much cheaper, this is well explained by Myers, (1984) who states that

the pecking order theory maintains that businesses adhere to a hierarchy of fin

ancing sources and prefer internal financing when available, and debt is preferred over equity

if external financing is required (equity would mean issuing shares which meant 'bringing

external ownership' into the company). This clearly illustrates that the free internal funds can

first be used to finance the investment needs of the firm.

It should also be noted that, these internal funds can be prone to abuse by the managers who are

the custodians or agents of the shareholders, giving rise to the basic conflict of interest between

owners and managers that is the agency theory problem Jensen (1986) adds that free cash flow as

a cash in surplus of that necessary to fund all positive net present value projects. Free cash flow

2

tempts managers to expand the scope of operations and the size of the firm, thus increasing

managers' control and personal compensation, by investing free resources in projects that have

zero or negative net present values. These spending is seen as unprofitable especially to the

shareholders, who see it worthwhile for the firm to issue dividends instead of retaining the funds

to invest.

Modigliani and Miller (1958, 1961), hereafter referred to as MM, put forward the irrelevance

theorems, more commonly known as the MM theorems and these form the foundation of modern

corporate finance theory. The two main conclusions that are drawn from the MM theorems are

that firm value is dependent on its current and future free cash flow. Secondly, the level of

dividends (or dividend policy) does not affect firm value given that firms maximize their value

through investment. Whilst investment increases the value of future cash flows. The difference

between equity issued and payouts of the firm is equal to its free cash flow. Hence, dividend

policy is irrelevant when it comes to affecting firm value.

Free cash flow has always been a subject of great debate especially in the literature on the

determinants of investment.

1.1.1 Free cash flows

Richardson (2006) defines free cash flows as cash flows beyond what is necessary to maintain

assets in place and to finance expected new investments.

Subramanyam & John (2009) states that free cash flows also can be defined for the entire firm.

Specifically, free cash flows to the firm or simply free cash flows equal operating cash flows

(adjusted for interest expense and revenue) less investments in operating assets. They continue to

say that free cash flows to the firm reflects the added effects of investments and divestments in

operating assets. The appeal of the free cash flows to the firm concept is that it represents cash

that is free to be paid to both debt and equity holders.

Vogt (1997) expounds free cash flows as operating income before depreciation, less interest

expense on debt, less income taxes, less preferred and common dividends. FCF is a coverage

ratio representing the amount to which current period generated free cash flow is sufficient to

cover next period's capital expenditures.

3

Vogt (1997) continues to explain that free cash flow is the amount of cash that a company has

left over after it pays all of its expenses, including investments. Negative free cash flow is not

inevitably an indication of a bad company, however, since many young companies put a lot of

their cash into capital expenditure, which diminishes their free cash flow. Although if a company

is spending so much FCF, it should have a good grounds for doing so and it should be earning

high rate of return on its investments. While free cash flow doesn't receive as much attention as

earnings do, it is considered by some experts to be a better indicator of a company's financial

health.

Poulsen (1989) states that free cash flow is a cash flow in hand for giving out among all the

securities holders of an organization. They include: equity holders, debt holders, preferred stock

holders and convertible security holders.

Jensen (1986) tries to suggest that free cash flow is a cash flow in surplus of that necessary to

fund all projects that have positive net present value when discounted at the appropriate cost of

capital. When FCF is present and shareholder monitoring is imperfect, the typical manager-

shareholder agency problem arises. Managers have a tendency to overinvest (that is, invest in

negative-NPV projects) in order to capture the financial and non-financial benefits of increased

firm size.

1.1.2 Investment decisions

Investment decision refers to the process of determining which investment projects result in

maximization of shareholders value (Hermes et al., 2007). Several techniques have been

designed by researchers to aid in the calculation of expected return from promising investment

projects these are selected of potential investment. The commonly used technique is the Net

Present Value (NPV).

Investment decisions of a firm are generally known as the capital budgeting, or capital

expenditure decision. It is defined as the firm‟s decision to invest its current funds most in the

long-term assets in anticipation of an expected flow of benefits over a series of years it includes

expansion, acquisition, modernization and replacement of the long-term assets, sale of a division

or business (divestment), change in the methods of sales distribution, an advertisement

4

campaign, research and development programme and employee training, shares (tangible and

intangible assets that create value) (Pandey, 2005).

According to Modigliani (1958), investment in perfect capital markets decisions are independent

of financing decisions and, hence, investment policy only depends on the availability of

investment opportunities with a positive net present value. In the neoclassical model, companies

have unlimited access to sources of finance and investment, so firms with opportunities for

profitable investment that exceed their available cash flow would not be expected to invest any

less than firms with the same opportunities and higher cash flow, because external funds provide

a perfect substitute for internal resources.

1.1.3 Effect of free cash flows on investments

Capital expenditure is strongly and positively associated to the level of free cash flow (the more

free cash flows a firm has, the more investments the firm can engage in, also according to Vogt

(1997) the more a firm has free cash flows, the more the profitable capital expenditure projects

the firm can undertake), and free cash flow's influence on capital expenditure increases as firm

size decreases, (in that small firms gear towards rampant growth thereby using most or all their

free cash flows to invest in value adding projects) and as insider ownership increases.

Firms maximize their value through investment and this therefore is a motivation to the

managers who own shares of the company (as a measure to tame the agency problem) to invest

in projects that add value to the firm, which has a long-term or future perspective unlike issuing

dividends to shareholders which motivates for now but if invested in positive NPV projects can

increase the value of the firm and the shareholders wealth.

1.1.4 Nairobi Securities Exchange (NSE)

NSE is a market established in 1953 and licensed by the CMA with the main mandate of

regulating the security market and ensuring exchange of ownership of securities by bringing

borrowers and investors together at low cost. Regulation of the quoted firms is achieved by

ensuring that firms abide by the rules and regulations set by submitting their periodic

performance reports. Also, the NSE educates the general public on investment issues. The

products traded are securities which consist of shares/equities and bonds/debt investments.

5

The shares of sixty one companies listed at the NSE trade in the eleven sectors namely: -

agriculture, automobiles & accessories, banking, commercial, construction, energy & petroleum,

insurance, manufacturing & allied, telecommunication & technology industry, investment and

growth enterprise market segment (NSE, 2014).

1.2 Problem Statement

Some observers have pointed out that there exists a relationship between free cash flow and

investment. Hovakimian and Hovakimian (2005) observed that there is a positive relationship

between internal funds and investment decisions due to the liquidity constraints faced by firms as

a result of the gap between the cost of external financing and internal financing. In relation to

this, Alti (2003) showed that the relationship between cash flow and investments is stronger in

companies that are in growth stage, which is likely to experience financial difficulties because

the companies have to make adjustments between the investments made with generated cash

flow. Moreover it reflects the company's growth opportunities.

In contrast to the above, Bo Becker (2006) research explains that in frictionless financial

markets, investment does not depend on internal cash flows. In a large European data set, the

researcher finds that firms invest more on average when they have higher cash flow.

In relation to previous studies, investment and free cash flow are significantly related, though

both the strength of the relationship and its cause are the subject of much debate. There still

remains disagreement whether free cash flows and investment decisions are related, therefore,

this study intends to answer the research question, does the relationship exists between free cash

flows and investment made by the companies at the Nairobi Securities Exchange (NSE) in

Kenya?

According to Vogt (1997) the more a firm has free cash flows, the more the profitable capital

expenditure projects the firm can undertake. Consequently, capital expenditure is met with

positive shareholder reactions, particularly when spending is dependent on cash flow, mostly to

those who aspire for higher dividend in the future than those who want free cash flows

distributed as dividends now. He continues to explain that Negative free cash flow is not

inevitably an indication of a bad company, however, since many young companies put a lot of

their cash into capital spending, which diminishes their free cash flow. Although if a company is

6

spending so much FCF, it should have good grounds for doing so and it should be earning high

rate of return on its investments. While free cash flow doesn't receive as much attention as

earnings do, it is considered by some experts to be a better indicator of a company's financial

health.

Vogt (1994) explains FCF assumption that cash flow should influence capital spending. The

firms not paying dividends should demonstrate the strongest relationship between cash flow and

capital spending, while those paying high dividends should show the weakest relationship. With

this it‟s important to have a look at the relationship between free cash flows and investment of

the firms, whether positive or negative, and more so to do this study on publicly listed firms in

Kenya.

1.3 Research Objective

To establish the relationship between free cash flows and the investments made by the listed

companies at the Nairobi Securities Exchange (NSE).

1.4 Value of the Study

Firms will be able to know whether investment decisions wholly rely on the free cash flows of

the firm or not.

The research study will add to the field of knowledge and also the scholars will also benefit from

this study in their research process, to either fill the research gaps or contribute in their learning

process.

The paper will enable the investors to know the kind of information to be disclosed by firms on

the financial statements pertaining to free cash flows and investing decisions.

The conclusions will also bridge the knowledge gap that exists in the Finance field on free cash

flows and investing decisions.

It will also bridge the knowledge gap about the correlation between free cash flows and

investments made by the companies in the Nairobi Securities Exchange (NSE) in Kenya and add

7

to the literature on prior studies done on the concepts of free cash flows and investment decisions

made by the companies at the Nairobi Securities Exchange (NSE).

8

CHAPTER TWO:

LITERATURE REVIEW

2.0 Introduction

This chapter examines the literature relevant to the study. It follows the conceptual framework,

incorporate scholarly works that is the empirical evidence and theories. The rationale of the

study is to ascertain the relationship between free cash flows and investments. The literature

under review is obtained from journal articles, text books and websites.

2.1 Theoretical Review

2.1.1 Dividend policy related theories

The initial theory relating to Dividend policy was developed in 1958 by economists Franco

Modigliani and Merton Miller known as MM Theory. The Modigliani and Miller (1961) and

Miller (1977) result that firm value is independent of dividend policy has also been examined

extensively. Bhattacharya (1979) and others show that firm dividend policy can be a costly

device to signal a firm‟s state, and hence relevant, in a class of models, firstly, asymmetric

information about stochastic firm earnings, secondly, shareholder liquidity (a need to sell makes

firm valuation relevant), and thirdly deadweight costs (to pay dividends, refinance cash flow

shocks or cover under-investment). In a separating equilibrium, only firms with high anticipated

earning pay high dividends, thus signaling their prospects to the stock market. As in other costly

signaling models, why a firm would use financial decisions to reveal information, rather than

direct disclosure, must be addressed. As previously, taxes are another important friction which

affects dividend policy

Modigliani and Miller (1958, 1961), hereafter referred to as MM, put forward the irrelevance

theorems, more commonly known as the MM theorems and these form the foundation of modern

corporate finance theory. The two main conclusions that are drawn from the MM theorems are

that firm value is dependent on its current and future free cash flow. Secondly, the level of

dividends (or dividend policy) does not affect firm value given that firms maximize their value

through investment. Whilst investment increases the value of future cash flows. The difference

9

between equity issued and payouts of the firm is equal to its free cash flow. Hence, dividend

policy is irrelevant when it comes to affecting firm value.

Regarding the impact of dividend policy decision on investment, it is understood that firms

should take all projects with a positive Net Present Value (NPV). However, the issue is that if

management put more emphasis on dividend policy to such an extent that it eventually dominates

investment policy decisions, it could be argued that NPV projects or projects creating firm value

be cancelled or delayed for a later time. By cancelling or delaying positive NPV projects, this

will obviously have an adverse effect on the future expected profits of the company. Although

Fama (1974) carried out a research on the relationship between investment decisions and

dividend decisions. His findings revealed that investment decisions and dividend decisions are

not correlated; that these two types of decision making do not affect each other.

2.1.2 Pecking order theory

Pecking Order theory popularized by Myers (1984) tries to capture the costs of asymmetric

information. It states that companies prioritize their sources of financing (from internal

financing to equity) according to the law of least effort, or of least resistance, preferring to

raise equity as a financing means “of last resort”. Hence, internal financing is used first; when

that is depleted, then debt is issued; and when it is no longer sensible to issue any more debt,

equity is issued. This theory maintains that businesses adhere to a hierarchy of financing

sources and prefer internal financing when available, and debt is preferred over equity if

external financing is required (equity would mean issuing shares which meant 'bringing

external ownership' into the company). This clearly illustrates that the free internal funds can

first be used to finance the investment needs of the firm.

2.1.3 Agency Costs Based Theory

This is a kind of conflict that comes about when the owners of the business are separated from

the control of the business. Managers of firms may diverge from the goal of the owners which is

the maximization of the firm value. Instead, managers may choose to behave in way that will

satisfy their interest. This can be in the form of luxuriant office and cars, expensive travels,

extravagant benefits etc. (Jensen and Meckling, (1976))

10

The way to mitigate the chances of this kind of behavior from managers is by giving and or

increasing the ownership of managers in the firm they manage. Additionally, increasing the

debt level also helps to mitigate the loss of conflicts between owners/shareholders and

managers. Since debt forces managers to pay out cash, reducing the free cash. If the manager

has ownership in the firm, it puts her/him in a position of unwillingness to loosely spend the

firm‟s money. With this step (s)he will recognize and beware that the firm money (partly his

money) should be carefully managed. Free cash flow managers can waste on the perquisites.

(Jensen and Meckling, 1979; Niu, 2008) From other perspectives, this conflict arises because

managers may prefer short-term projects, which produce results early and enhance their

reputation quickly, rather than more profitable long-term projects. Managers may prefer less

risky investments and lower leverage to reduce the probability of bankruptcy.

Jensen (1986) adds that free cash flow as a cash in surplus of that necessary to fund all positive

net present value projects. Free cash flow tempts managers to expand the scope of operations and

the size of the firm, thus increasing managers' control and personal compensation, by investing

free resources in projects that have zero or negative net present values. These spending is seen as

unprofitable especially to the shareholders, therefore, an aspect of the basic conflict of interest

between owners and managers that is the agency theory problem. To mitigate this conflict the

manager should have ownership in the firm, it puts her/him in a position of unwillingness to

loosely spend the firm‟s money. With this step (s)he will recognize and beware that the firm

money (partly his money) should be carefully managed, therefore will invest this free cash

flows in projects with positive NPVs.

2.2 Determinants of investments of listed firms

The most important determinant of capital expenditure is cash flow. Capital expenditure is

strongly and positively associated to the level of free cash flow (the more free cash flows a firm

has, the more investments the firm can engage in, also according to Vogt 1997 the more a firm

has free cash flows, the more the profitable capital expenditure projects the firm can undertake),

and free cash flow's influence on capital expenditure increases as firm size decreases, in that

small firms gear towards rampant growth thereby using most or all their free cash flows to invest

in value adding projects.

11

In the IMF working paper Geng and N‟diaye (2012), the empirical analysis of the determinants

of investment indicates that financial variables such as interest rates and the exchange rate are

important determinants of corporate investment, others include: capital stock and dividend policy

or retention policy (not included in the paper).

2.2.1 Real interest rates

Rittenberg and Tregarthen (2014) state that real interest rates have a negative impact on

investment that is higher interest rates increase the cost of the borrowing used to finance most

types of investment expenditures this tends to reduce the quantity of investment, while lower

interest rates increase quantity of investment. According to Geng and N‟diaye (2012) at the

aggregate level, a 100 basis points increase in real interest rates reduces corporate investment in

China by about ½ percent of GDP. Based on these estimates, raising real interest rates to the

level of the marginal product of capital net of depreciation would probably lower investment by

about 3 percent of GDP. The estimated effect for China of real interest rates on investment is

much larger than the average of the other 52 economies in the panel. The estimated impact of

interest rates changes on corporate investment is about half as big when estimated based on the

firm-level data. This could possibly reflect the smaller reliance of this sample (which are large,

listed enterprises) on bank-intermediated financing.

2.2.2 Exchange rate

An exchange rate appreciation lowers investment and vice versa as the exchange rate depreciates

there is a corresponding increase in investments. As observed by Geng and N‟diaye (2012) a

10% percent appreciation would reduce total investment by around 1 percent of GDP. The large

concentration of manufacturing companies in the firm-level sample means that the estimated

impact of exchange rate appreciation from the firm-level data is much larger.

2.2.3 Capital Stock

According to Rittenberg and Tregarthen (2014) the quantity of capital already in use affects the

level of investment in two ways. First, because most investment replaces capital that has

depreciated, a greater capital stock is likely to lead to more investment; there will be more capital

to replace. But second, a greater capital stock can tend to reduce investment. That is because

12

investment occurs to adjust the stock of capital to its desired level. Given that desired level, the

amount of investment needed to reach it will be lower when the current capital stock is higher.

2.2.4 Dividend policy and Retention policy

Modigliani and Miller (1961), in which they challenged the common belief that payment of

dividend increases firm‟s value and argued that in perfect capital market a firm‟s dividend

decision does not affect its value. But on the other hand, Lintner (1962) and Gordon (1963)

supported “Bird-in-the-hand” theory and argued that in the world of uncertainty and imperfect

information, high dividend payment is associated with high firm value.

Miller and Modigliani (1961) presented the irrelevance proposition and proved that in a perfect

capital market firm‟s dividend decision is not a thing of value at all. During the last fifty years,

the enduring nature of debate on dividend policy has generated a rich body of literature in

which the majority of the researchers support that the payment of dividends has a positive

impact on firms‟ value but on the other hand many researchers have argued that payment of

dividends affect the firm‟s value negatively, still many others believe that dividend decisions is

not a thing of value and have no significant impact on firms‟ perceived financial position .

Firms with high cash flow volatility are also those with the greatest potential agency costs. When

cash flows are variable, it is difficult for investors to accurately attribute deviations in cash flows

to the actions of corporate managers or to factors beyond management‟s control. Thus, the higher

the expected variance in cash flows, the greater the potential agency costs, and the greater the

reliance on dividend distributions. The value of dividend payout as a guarantee against non-value

maximizing investments should be greatest for those firms with the greatest cash flow

uncertainty. Therefore, the agency cost theory predicts that firms with volatile cash flows would,

on average, pay out a greater proportion of their cash flows in the form of a dividend (Bradley et

al, 1998).

According to Jensen‟s (1986) Free Cash Flow Hypothesis, companies prefer to use their cash

resources to invest in profitable projects first and dividends are paid out of residual. Berle and

Means (1932), who first time introduced the concept of separation of ownership and

management, argued that the inefficient use of cash resources, in excess of profitable

13

investment opportunities by management, causes conflict of interest between ownership and

management. Dividend and interest payment reduces the free cash flow available to

management, hence reducing the chance of using it in less profitable projects or on managers‟

prerequisites. From companies‟ point of view, cash generated from operations plays an

important role in deciding the amount of payout, companies having greater cash flow generated

from operations are expected to be in a better position to pay cash dividends rather than

companies having negative operating cash flows.

In relation to the above, Mizuno (2007) agrees to the fact that a firm ought to pay dividends to

shareholders if it cannot identify suitable investments which would bring higher returns than

those expected by the shareholders.

From cash flow sensitivity point of view prior studies reported that financially constrained

firms accumulate higher cash holdings and retain greater portion of the cash earned during the

period, which means that liquidity is more important when firms cannot raise funds from

external market and liquid resources are required for investment in future profitable projects

(Khurana et. al., 2006). Almeida et. al. (2004) points out that firms facing financial constraints

will save more cash today to fund future investment opportunities. Intuitively, increasing

tendency of saving cash out of free cash flows will indicate the availability of profitable

projects and financial constraints and hence will reduce the payout ratio of the firm, provided

that firms‟ access to external finance is limited to a certain level.

The payment of cash dividends to shareholders now is the opportunity cost of retaining the

internal funds and investing the same in projects that have positive NPV that have greater

returns to the shareholders in the future. This is influenced by the shareholders view that is

largely explained by the „bird in hand‟ theory, where the shareholder perceives the uncertainty

of the future cash flows, which have a risk aspect in them. According to Amidu (2007) the bird

in hand theory proposes that a relationship exists between firm value and dividend payout. It

states that dividends are less risky than capital gains since they are more certain. Investors

would therefore prefer dividends to capital gains.

According to Farsio et al. (2004) firms that pay high dividends without considering investment

needs may therefore experience lower future earnings, also firms that consider investment

14

needs that have prospects of maximizing the shareholders wealth, either retain all internally

generated funds or issue low dividends. This shows that there is a negative relationship

between dividend payout and future earnings.

2.3 Empirical Review

This section discusses studies which have been conducted locally and internationally, which

examines the relationship between free cash flows and investments.

Financing capital expenditure by utilizing the internally generated cash flow is highly

recognized. According to Myers (1984) states that companies prioritize their sources of

financing (from internal financing to equity) according to the law of least effort, or of least

resistance, preferring to raise equity as the last financing means. Hence, internal financing is

used first; when that is depleted, then debt is issued; and when it is no longer sensible to issue

any more debt, equity is issued.

Modigliani and Miller‟s (1958) insignificance suggestion asserts firms to carry out all positive

net present value (NPV) investments regardless of the financing source. Jensen (1986) adds that

free cash flow as a cash in surplus of that necessary to fund all positive net present value

projects. Free cash flow tempts managers to expand the scope of operations and the size of the

firm, thus increasing managers' control and personal compensation, by investing free resources

in projects that have zero or negative net present values. These spending is seen as unprofitable

especially to the shareholders, therefore, an aspect of the basic conflict of interest between

owners and managers that is the agency theory problem.

Free cash flow is inconsistent with the goal of owner to maximize their wealth. Expansions

wasted by administration instead could have been distributed to the owners or stock holders as

cash dividends or to the policyholders of mutual or stock firms in the form of lower premiums,

higher policy dividends, or higher investment returns. The existence of free cash flow provides

managers with an opportunity to waste cash on unprofitable capital spending. These unprofitable

capital expenditure represents an incremental cost of the owner-manager conflict (Jensen, 1986).

15

With the previous paragraphs raising the issue of abuse of free cash flows, Jensen (1986) gives a

remedy stating that the majority of existing evidence on the free cash flow hypothesis focuses on

changes in financial structure. Leveraged buyout activities are one way of controlling free cash

flow because the debt incurred in such transactions forces managers to pour out excess cash. It

examines the cross-sectional relation between free cash flow and ownership structure and finds

some evidence that organizational forms specific to the oil industry (corporations, limited

partnerships, and royalty trusts) have different agency costs of free cash flow. Specifically, the

Capital spending of free cash flow is lower in royalty trusts and limited partnerships than in

corporations.

Vogt (1994) explains important implications for both investors and managers. While the study

shows that cash flow-financed capital expenditure is marginally unproductive for some firms, the

potential sources of this inefficiency have also been identified. Cash flow-financed growth by

large, low-dividend firms tends to be value-destroying, while cash flow-financed growth is

value-creating for small, low-dividend firms. The importance of dividends as a method of

mitigating agency costs of free cash flow, moreover, is confirmed. Managers of free cash flow-

rich companies may consider increasing dividend payouts as a method of increasing the

efficiency of their capital spending decisions. A continued high-dividend-payout policy may also

signal to shareholders that additional and costly monitoring of capital expenditure decisions is

unnecessary.

Jensen's (1986) theory predicts that capital spending of equity is partly driven by free cash flow.

Previous research indicates that the agency problems between owners and managers are greater

in mutual organizations than in stock organizations, which leads to the expectation that the free

cash flow problem will be greater in mutual insurers than in stock insurers. (Jensen, 1986)

Jensen‟s (1986) observations test for differences in free cash flow in capital spending automobile

insurance industry. The purpose is to examine whether organizational form affects managerial

behavior with respect to the holding of free cash flow rather distributing or investing.

Gentry (1990) analyzed capital spending with total cash outflow and found out that the

percentage of cash outflows going to capital investment ranged from an outflow of 60 per cent or

16

more. The giant companies invested a higher percentage of their total outflow in plant and

equipment than companies in the other size categories. The small companies invested the lowest

percentage of their total outflows in capital.

Research was applied to agricultural firms by Farrell E. Jensen (1993) which showed that results

are consistent with previous studies for non-agricultural firms which show that internal cash flow

variables are important in explaining investment. Result indicate that internal cash flow variables

are important and that the addition of internal cash flow variables can improve the explanatory

power of agricultural investment models. In terms of elasticity, investment was more responsive

to internal cash flow variables.

Vogt (1994) explains the relationship of cash flow and capital expenditure by analyzing the free

cash flow theory of Jensen‟s (1986) and find outs that, since monitoring is costly, and managers

can benefit from over investment, cash flow will significantly influence capital spending after

controlling for the cost of capital. Capital expenditure of firms not paying dividends will be more

influenced by cash flows than investment spending of firms that pay dividends. This follows

because no-dividend firms are able to retain all cash flow and still not reach the retention

constraint.

Vogt (1994) explains free cash flow assumption that cash flows should influence capital

spending. The firms not paying dividends should demonstrate the strongest relationship between

cash flow and capital expenditure, while those paying high dividends should show the weakest

relationship.

Vogt (1994) explains the case of capital expenditure, the observed results tend to support the free

cash flow description of the cash flow/capital expenditure relationship. Actions that supports the

free cash flow assumption, however, it is found in small firms paying low dividends. In the case

of Research and development expenditure, results are more reliable with the free cash flow

assumption. These results together suggest that the effect that cash flow-financed investment has

on firm value depends on asset size, dividend behavior, and the type of capital expenditure.

Vogt (1997) explains the strong influence that free cash flow has on capital expenditure is well

documented. On the free-cash-flow hypothesis of Jensen (1986) as explanations for the

17

importance of free cash flow on capital expenditure. Initial results expose relations similar to

those uncovered in previous studies. Capital expenditure is associated with positive and

statistically significant with free cash flow. Firms with favorable investment opportunities are

responsible for much of the positive, excess returns. Also, for firms announcing spending

increases, the level of announced capital expenditure is positively and strongly related to the

level of cash flow. The power of this relation increases for firms with profitable capital

expenditure opportunities, as firm size declines, and as the proportion of insider ownership

increases. Further analysis suggests that considerable diversity exists in the capital market's

response to cash-flow-financed capital expenditure.

Vogt (1997) research‟s result indicate a positive and significant excess returns found in the

sample announcing increases is concentrated in the smallest of the sample firms, in firms with

low cash flow relative to capital expenditure, and, to a lesser extent, in firms with high levels of

insider stock ownership. Tests elaborating the cross-sectional variation in returns disclose that

excess returns for medium and small firms in the sample are positively associated with

unexpected increases in planned spending. These tests also recommend that the market reacts

more favorably to announced capital expenditure by small firms when the planned spending is

more dependent on free cash flow. Conversely, excess returns for the largest firms in the sample

are negative, though not statistically significant. Cross-sectional regressions specify that large

firms have, excess returns and are negatively related to the extent that undistributed free cash

flow is available to finance planned capital spending, and positively related to their capital

spending opportunities.

These results are consistent with the hypothesis that small firms follow a free cash flow model

like the one described by (Myers, 1984; Myers and Majluf, 1984). Because small firms and large

firms are the most likely to face the liquidity constraints associated with asymmetric information,

they are also the most likely to forgo profitable investment expenditure in times of cash-flow

shortages. As free cash flow rises, the set of profitable capital expenditure projects the firm can

undertake also increases. Consequently, capital expenditure is met with positive shareholder

reactions, particularly when spending is dependent on cash flow.

18

Vogt (1997) finds some indication that is reliable with the free- cash-flow hypothesis. Excess

returns are negatively related to large firm‟s ability to cover capital spending with cash flow.

This is consistent with the FCF hypotheses. This apparent diversity in the market's response to

capital spending decisions suggests different capital-spending financing policies for firms that

seek to enhance shareholder value. Small firms with sizeable insider ownership and firms that

are generally cash-flow constrained appear to be enhanced, on average, by financing capital

spending with free cash flow. These firms might consider policies of conserving undistributed

cash flow through low payout and leverage policies, thus encouraging new capital spending from

internally generated funds. No evidence that free cash flow financed capital spending improves

these firms' market values, on average. Furthermore, limited indication exists that such a

financing strategy could reduce market value for large, low insider owned, and cash flow rich

firms.

Vogt (1994) suggests that cash flow-financed capital spending is marginally inefficient and

provides primary evidence in support of the FCF hypothesis. The negative relationship found in

the aggregate data is concentrated in firms paying low dividends over the sample period, in large

firms, and most strongly in large firms paying low dividends.

According to Worthington (1995) cash flows measures enter industry level investment equations

positively and significantly, even after investment opportunities are proxied by capacity

utilization variables. The effect of cash flow is greater in durable goods industries than in non-

durable goods industries.

Klaus et al. (2004) tested the following hypothesis first asymmetric information (AI) hypothesis

which predicted that firms underinvest and have returns on investment greater than their costs of

capital, and second the managerial discretion (MD) hypothesis which predicts overinvestment

and returns on investment less than the costs of capital, using the ratio of returns on investment

to costs of capital for each firm is a natural way to make this identification.

Moyen (2004) explained the fact that the cash flow sensitivity of firms described by the

constrained model is lower than the cash flow sensitivity of firms described by the unconstrained

model can be easily explained. In both models, cash flow is highly correlated with investment

19

opportunities. With more favorable opportunities, both constrained and unconstrained firms

invest more.

Aggarwal (2005) started a study on four controlling for the investment opportunity set, and he

concluded investment levels are significantly positively influenced by levels of internal cash

flows. The strength of this association generally increases with the level of financial constraints

faced by firms. Overall, these findings seem strong to the nature of the financial system and

indicate that most firms operate in financially incomplete and imperfect markets and find

external finance to be less attractive than internal finance.

Becker and Sivadasan (2006) concluded for their research paper that in frictionless financial

markets, investment does not depend on internal cash flows. In a large European data set, results

indicate that firms invest more on average when they have higher cash flow. Contribution to the

literature is being made by testing formally if the coefficient on internal resources (cash flow) is

related to a country‟s financial development. Comparing countries, it is further discovered the

cash flow effect is indeed stronger in countries with weaker financial development. This suggests

that financial constraints are strongest when financial development is low.

Vogt (1994) gives an explanation on free cash flow, however, is still a significant variable in the

capital expenditure behavior of small, low-payout firms. The constraint predicts, less than those

associated with the larger firms in the low-payout group, is still highly significant. Consequently,

the asymmetric information induced free cash flow assumption explanation cannot be dismissed.

The most reasonable argument is that both free cash flow and asymmetric information are

important factors contributing to the influence of cash flow on capital spending.

Vogt (1994) explains different incentives that Research and development and capital expenditure

may generate for managers over time. Research and development represents an expenditure on

intangible assets whose impact on the asset size and future cash flows of the firm is extremely

uncertain and secondly not likely to be realized in the near future. Fixed plant and equipment

expenditure is likely to produce more certain cash flows in the near future (in part because of

accelerated depreciation allowances) as well as increase the tangible asset base of the firm. The

effect of plant and equipment expenditure is to generate free cash flow that can be used in the

20

next period. Consequently, capital expenditure may be more susceptible to free cash flow

problems than research and development expenditure.

According to Mizen (2005) the relationship between cash low and investment are based on

sample-splitting between constrained and unconstrained firms taken from a single country. The

degree of sensitivity appears to be greater. It extends the literature by examining from a number

of perspectives the behavior of firms. The research article proposes a number of hypotheses that

are explored in turn. A first possible reason is that firms in market-oriented financial systems

show greater sensitivity to cash flow because borrowers and lenders operate at arms-length

compared to those in relationship-oriented systems. A second possible cause for differences in

response to cash flow across countries is that the samples of firms taken from each country might

differ in composition with respect to particular characteristics, for instance size. Equally, the

industrial type may be an important determinant of investment sensitivity to cash flow since

industries differ considerably in terms of the size of firms, capital-intensity, borrowing capacity,

openness and the durability of their output.

Whilst investment is measured by capital expenditure, the same is deflated by the capital stock.

Investment cash flow sensitivity is defined as the level of the company's financial constraints.

Cash flow sensitivity of investment reflects higher cost of external financing relative to internal

financing due to asymmetric information or agency problem. Other studies show a relationship

between cash flow sensitivity and financing constraints are sensitive to how the company is

classified into two groups who are financially constrained and non-financially constrained.

Fazzari et al (1998) stated that in addition to the opportunity to grow, investment by companies

as well affect the company's cash flow and more will further reduce the company's dividend

payment.

Hovakimian and Hovakimian (2005) concluded that there is a positive relationship between

internal funds and investment decisions due to the liquidity constraints faced by firms as a result

of the gap between the cost of external financing and internal financing. The results Alti (2003)

showed that the relationship between investment and cash flow is stronger in companies that are

in growth stage, which is likely to experience financial difficulties because the companies have

21

to make adjustments between the investments made with generated cash flow. Moreover it

reflects the company's growth opportunities.

Alti (2003) continues to expound that investment is sensitive to cash flow, even after controlling

for its link to profitability by conditioning market. Furthermore, the sensitivity is substantially

higher for young, small firms with high growth rates and low dividend payout ratios, as it is in

the data. The uncertainty these firms face about their growth prospects amplifies the investment-

cash flow sensitivity in that, the uncertainty is resolved in time as cash flow realizations provide

new information about investment opportunities. This makes capital expenditure highly sensitive

to free cash flow surprises.

Gentry (1990) tells about free cash flow analysis shows that the financial health of a company

depends upon its ability to generate net operating cash flows that are sufficient to cover a

hierarchy of cash outflows. The profiles generated from a large sample of companies show that

relative cash flow components vary across company size and across industry groups. The

researcher hopes that these profiles will serve as benchmarks for comparing cash flow

components and encourage financial analysts to use cash flow analysis.

Bo Becker (2006) research explains that in frictionless financial markets, investment does not

depend on internal cash flows. In a large European data set, the researcher finds that firms invest

more on average when they have higher cash flow. The researcher contributes to the literature by

testing formally if the coefficient on internal resources that is cash flow is related to a country‟s

financial development. Comparing with different countries, the researcher finds that the cash

flow effect is indeed stronger in countries with weaker financial development. This suggests that

financial constraints are strongest when financial development is low. The effect is weaker inside

conglomerates and is probably not driven by the East-West difference. This is consistent with the

idea that conglomerates ease internal financial constraints. Industries with few low liquid assets

may experience bigger benefits of financial development (i.e. the cash flow coefficient is

reduced more by financial development in low liquidity industries). However, the proof for this

is diverse. Our findings suggest that financial frictions operate in Europe. They suggest that

financial development is beneficial because it reduces financial constraints at the firm level and

therefore relaxes the correlation between internal resources and investment.

22

An important implication of adverse selection is that firms with positive NPV investment

opportunities will forgo profitable projects to avoid the excessive cost of external financing. This

implication has been explored in detail by Fazzari et al. (1998) for capital spending and

Himmelberg and Peterson (1994) for research and development spending. These authors show

formally that the excess cost of external finance causes some firms to be liquidity constrained, so

that cash flow becomes an important determinant of investment spending.

In an in depth study of 25 large firms, Gordon Donaldson (1961) concludes that management

strongly favored internal generation as a source of new funds even to the exclusion of external

funds except for occasional unavoidable „bulges‟ in the need for new funds. A more recent

survey of 176 corporate managers by Pinegar and Wilbricht (1989) also finds that managers

prefer cash flow over external sources to finance new investment; 84.3 percent of sample

respondents indicate a preference for financing investment with cash flow.

2.4 Summary of the Literature Review

The two main conclusions that are drawn from the MM theorems are that firm value is dependent

on its current and future free cash flow. Secondly, the level of dividends (or dividend policy)

does not affect firm value given that firms maximize their value through investment. Whilst

investment increases the value of future cash flows. With regards to the impact of dividend

policy decision on investment, it is understood that firms should take all projects with a positive

Net Present Value (NPV). However, the issue is that if management put more emphasis on

dividend policy to such an extent that it eventually dominates investment policy decisions, it

could be argued that NPV projects or projects creating firm value be cancelled or delayed for a

later time. By cancelling or delaying positive NPV projects, this will obviously have an adverse

effect on the future expected profits of the company.

In relation to the agency theory problem and its relevance to free cash flow-investment

relationship Jensen and Meckling (1976) suggests the way to mitigate the chances of this kind

of behavior from managers is by giving and or increasing the ownership of managers in the

firm they manage. If the manager has ownership in the firm, it puts her/him in a position of

unwillingness to loosely spend the firm‟s money. With this step (s)he will recognize and

beware that the firm money (partly his money) should be carefully managed. Therefore

23

managers will see to it that they utilize the free cash flows by investing in positive NPV

projects that maximize the firm‟s value.

The Pecking Order theory popularized by Myers (1984) tries to capture the costs of

asymmetric information. It states that companies prioritize their sources of financing (from

internal financing to equity) the theory maintains that businesses adhere to a hierarchy of

financing sources and prefer internal financing when available, and debt is preferred over

equity if external financing is required (equity would mean issuing shares which meant

'bringing external ownership' into the company). This clearly illustrates that the free internal

funds can first be used to finance the investment needs of the firm.

The kind of conflict that comes about when the owners of the business are separated from the

control of the business. Managers of firms may diverge from the goal of the owners which is the

maximization of the firm value. Instead, managers may choose to behave in a way that will

satisfy their interest. This can be in the form of luxuriant office and cars, expensive travels,

extravagant benefits etc. (Jensen and Meckling, 1976). The way to mitigate the chances of this

kind of behavior from managers is by giving and or increasing the ownership of managers in

the firm they manage. If the manager has ownership in the firm, it puts her/him in a position of

unwillingness to loosely spend the firm‟s money. With this step (s)he will recognize and

beware that the firm money (partly his money) should be carefully managed. Therefore the

managers will faithfully utilize the free cash flows by investing in projects that add value to the

portfolio of the shareholders.

In Kenya, few research studies relating to investment decisions have been done, but clear

research study on the relationship between free cash flows and investments has not been carried

out in Kenya, therefore this research seeks to fill this gap by doing this research study on firms

listed at the Nairobi Securities Exchange. The focus is on free cash flows although they have not

receive as much attention as earnings do, they are considered by some experts to be a better

indicator of a company's financial health.

24

CHAPTER THREE:

RESEARCH METHODOLOGY

3.1 Introduction

The main purpose of the study was to find out the relationship between free cash flows and

investment decisions of quoted companies at the NSE. This chapter discusses the research

design, population of the study, sampling design, data collection, research models and data

analysis.

3.2 Research Design

This research study adopted the descriptive research design. This design gives a description of

phenomenon, characteristics and association of the research variables. It is appropriate for the

study as it will enable high level analysis such as correlation and regression analysis that will

allow to establish the nature and the extent of the relationship between free cash flows and

investment decisions of quoted companies at the NSE. Quantifiable data was collected to

determine the current status of the relationship. The research design employed secondary

quantitative data. The data was obtained from the current financial reports of the companies

listed at the NSE.

3.3 The Population

The population of the study covered companies listed at the NSE (See Appendix I). NSE (2014)

provided that there are a total of sixty one companies listed, therefore our population size will be

these sixty one listed companies.

3.4 Sampling Method

A sample of thirty companies (See Appendix I) that have been quoted for the five years (2009 –

2013) will be considered from the population. The sample was selected by randomly picking a

company from each sector or industry of firms listed in the NSE.

Simple random sampling will be used to select the sample from the population, for the technique

minimizes bias and increases the chances of representativeness. Mugenda & Mugenda (2003)

suggested that for correlation research, 30 cases or more are required. Since this study involved

25

determining the relationship between free cash flows and investments, a sample of 30 firms

listed at the NSE was considered sufficient.

3.5 Data Collection

The secondary data was extracted from the audited annual reports and financial statements of

individual companies sourced from the NSE and the CMA. In order to determine the relationship

that exists between free cash flows and investment decisions of companies quoted at the NSE, a

period of five years (2009 – 2013) was considered. Data collected was classified as per sectors of

the individual sampled companies. Group consolidated annual reports and financial statements

were considered since they portrayed overall performance of a firm unlike the company‟s

financial statements which show part performance of a company in a given region. The annual

financial statements included the statements of comprehensive income, financial position, cash

flows, changes in equity and the notes to the financial statements.

3.6 Data Analysis

The data collected for this study was cleaned, edited and tested for completeness. This was done

to ensure that the data used was adequately reflective, accurate and reliable for conclusion and

realization of the research objective of this study. SPSS software was used to carry out the

analysis of the data obtained. The researcher used the multiple linear regression analysis

technique, a statistical tool that was used to analyze the association between a dependent variable

and several independent variables. According to Hair (2006) the objective of multiple linear

regression analysis is to use the independent variables whose values are known to forecast the

single dependent value selected by the researcher.

The data was presented in form of tables and charts where appropriate. The study used three

independent variables. The researcher constructed a regression model to analyze the reliance

investments (the dependent variables) on the independent variable outlined below.

3.6.1 Research Model

The model adopted by this study was the multiple linear regression model. This is a technique

that allows many factors to enter the analysis separately so that the effect of each can be

26

estimated. It is valuable for quantifying the impact of various simultaneous influences upon a

single dependent variable.

Data collected on the variable of interest within the period of study were analyzed through

descriptive statistics. Further multiple regressions and correlation analysis will be used to explain

the nature and significance of relationship between changes in the response variables

(investments) and change in the prediction variables (determinants) identified in the study. The

regression model used is shown below:

Y =B0 +B1X1 +B2X2 +B3X3 + et

Where:

Y = NCE - Net Capital Expenditure

B0 – constant

B1, B2, B3, – regression coefficients

X1 = Free Cash Flows (FCF)

X2 = Dividends Payout Ratio

X3 = Depreciation

et = Error term/Disturbance term

The hypothesis of the study:

H0: Free Cash flow has no relationship with investment or capital expenditure.

H1: Free Cash flow has relationship with investment or capital expenditure.

27

Measurement of variables

The equation:

Dependent Variable = Independent Variable, that is a change in Fixed Assets is equal to Free

Cash Flow. The control variables in this case include: dividends payout and capital stock or

depreciation. Where the:

i) Independent Variable = Free Cash Flow (FCF)

ii) Dependent Variable = Net investment or Net capital expenditure

Vogt, 1997 explains free cash flow, as operating income before depreciation, less interest

expense on debt, less income taxes, less preferred and common dividends. FCF is a coverage

ratio representing the amount to which current period generated free cash flow is sufficient to

cover next period's capital expenditures. Free cash flow was determined as follows:

FCF = Operating Income + Depreciation – Interest Expense – Income Taxes – Expected loan

(less repayment) – Dividends

Dividends payout = Dividend per Share / Earnings per Share

Depreciation = ((Initial asset cost-terminal value)/economic useful life)

Capital expenditure was considered as funds spent by a company to buy or upgrade fixed

assets, such as equipment, during the year and acquiring subsidiaries. It was also considered

as a payment by a business for basic assets such as property, fixtures, or machinery, that is an

increase in the value of company assets and is usually intended to improve productivity but

not for day-to-day operations such as payroll, inventory, maintenance and advertising.

Net Capital Expenditure = (Current Year – Previous Year)

The greatest advantage with regression analysis was that the parameters were estimated to

show causality between explanatory variables and regressors. Parameters estimated suggest

magnitude and direction the independent variables have on the explanatory variables. In

order to test the significance of the model in measuring the relationship between independent

and dependent variable, this study conducted an Analysis of Variance (ANOVA). On

28

extracting the ANOVA statistics, the researcher looked at the significance value. The study

was tested at 95% confidence level and 5% significant level. If the significance number was

found to be less than the critical value set, then the conclusion will be that the model is

significant in explaining the relationship.

29

CHAPTER FOUR:

DATA ANALYSIS, RESULTS AND DISCUSSION

4.1 Introduction

This chapter presents the findings derived from data collected and further analyzed. The

analyzed data is presented in tables and charts in terms of derived means, frequencies,

percentages and proportions where necessary. Explanations of the findings are discussed after

each table. The chapter constitute of the general findings of various variables on free cash flows

and investments, the relationship between free cash flows and investments of companies quoted

at the NSE and finally the overall summary of the findings.

4.2 General Findings

This section details the findings of various variables analyzed. Descriptive statistics was used to

analyze the data collected and presented in tabular form (See Appendices II). A sample of thirty

companies quoted at the Nairobi securities exchange (NSE) was used.

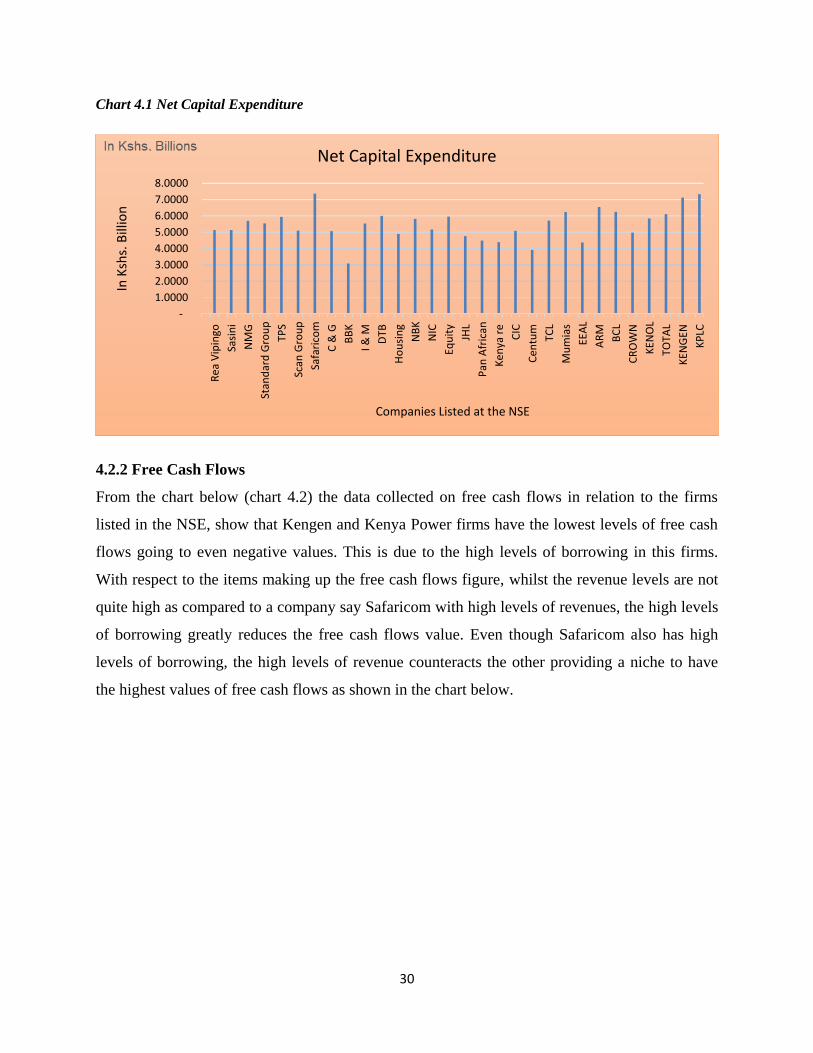

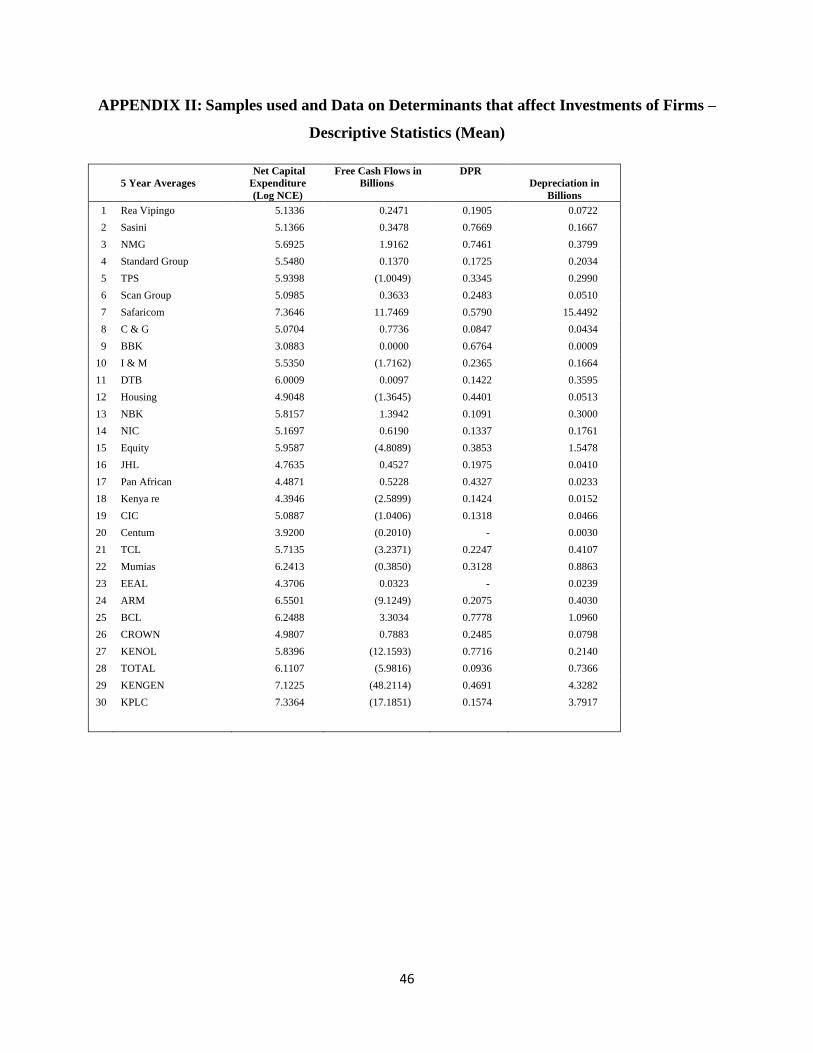

4.2.1 Net Capital Expenditure

The summary of the data collected on Net Capital Expenditure is represented in the chart below

(chart 4.1) in relation to the companies quoted in the NSE. From the sample of thirty companies,

it shows that safaricom has the highest values of net capital expenditure. This is due to the high

investment in property plant and equipment, and other telecommunication items, the same case

goes to Kengen and Kenya power companies. The chart shows that Barclays bank has the lowest

values of net capital expenditure, although the bank did acquire assets but not as much as the

other companies. It is clear that investments, which in this case are represented by net capital

expenditure differs from company to company depending on the nature of business and sector

under operations. It also depends on the stage in company cycle for example at start up and

growth stages companies tend to engage in vigorous investment activities unlike at maturity and

post maturity stages where companies do not necessarily engage in extensive investment

projects.

30