The Quarter Close- Q2 2016

16

www.pwc.com/cfodirect . June 13, 2016 What’s inside Accounting hot topics ...... 2 Hot off the press ...............5 Regulatory update .......... 6 Corporate governance .... 8 Appendix……………………..10 The quarter close A look at this quarter’s financial reporting issues

Transcript of The Quarter Close- Q2 2016

www.pwc.com/cfodirect

.

June 13, 2016

What’s inside

Accounting hot topics ...... 2

Hot off the press ............... 5

Regulatory update .......... 6

Corporate governance .... 8

Appendix……………………..10

The quarter close A look at this quarter’s financial reporting issues

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 1

What you need to know—Q2–2016

Welcome to the second quarter edition of The quarter close. As you sprint towards second quarter reporting, we share the information you need to know to get to the finish line. Accounting hot topics. Stakeholders should be able to see the potential impact of new standards on your financial statements from a mile away. We focus on what you should be disclosing when it comes to new accounting standards. We also discuss the hurdles associated with changing accounting policies, and their interplay with new standards. Lastly, we discuss accounting considerations for accelerated share repurchases. Hot off the press. We anchor you in the basics of the PCAOB’s proposed changes to the auditor’s report.

Regulatory update. Stay on track when disclosing non-GAAP measures: we provide reminders of the fundamentals, and our point of view on best practices. We also provide you with the latest in the disclosure effectiveness marathon to keep you ahead of the pack. Corporate governance. We relay insights on disclosing forward-looking information, undertaking share repurchases or dividends, and assessing board composition.

Video perspectives Spotlight on the hot topic videos included this quarter

Volatility and accounting impacts

Click on the pictures or titles to launch the videos.

Leasing: Build to suit and sale leaseback

Segment changes impact on goodwill allocation

Financial instruments: Recognition and measurement

Held for sale accounting

Equity method: Basis differences

Check out our new webpage pwc.com/fasbeffectivedates

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 2

Accounting hot topics

Disclosures for recently issued accounting standards—avoiding a false start

Companies are required to disclose the impact that recently issued accounting standards will have on the financial statements when adopted (commonly called SAB 74 disclosures after an SEC Staff Accounting Bulletin). When the effective date of a new accounting standard is off in the distance, companies often disclose that they are still assessing whether the impact of adopting the new standard will be material. However, in some instances, the reasonableness of such a disclosure may come into question.

Information on the sidelines

In Q1, the FASB issued two new pieces of guidance—on leases and share-based payment accounting—that will impact most companies’ financial statements. Historically, aspects of accounting for both leases and share-based payments were tracked off-balance sheet but there was footnote disclosure. This disclosure, coupled with considerations of how the guidance has changed, can provide an indication of whether the impact of the new guidance will be material. Companies should consider this interplay when determining the timing and nature of their SAB 74 disclosures.

Closing in fast on effective dates

Certain new standards are issued with effective dates that may be two or more years away. Often, the long runway to the effective date correlates to the expected significance of the adoption effort, and/or the expected magnitude of change that companies may experience when adopting the new guidance. In these instances, it’s often reasonable for a company to initially indicate that it is still assessing the potential impact of adopting the standard on its financial statements. However, the closer adoption gets, the more such an assertion may be scrutinized.

The new revenue guidance is a good example. The standard was initially issued in 2014, and is effective for calendar year-end public companies in 2018. Now at the mid-point of the pre-adoption window, the SEC has indicated that it senses many companies are behind in their assessment of the impact of the new revenue standard, and that it is closely monitoring companies’ disclosures about the potential impact of adoption. If a company is still assessing the potential impact, the SEC has suggested that it should consider indicating when it expects to complete the assessment. Given this enhanced scrutiny, companies should challenge themselves each reporting period as to whether it is still reasonable to assert that they are still assessing the potential impact of adoption, and what further information they can provide in the interim.

This quarter’s hot topics:

Disclosing the potential impact of new standards

Change in accounting policies

Accelerated Share Repurchase considerations

Investors should expect the level of disclosures to increase as companies make further progress in their implementation plans for adopting the new standards... Source: Wesley Bricker, Deputy Chief Accountant, SEC Office of the Chief Accountant (May 2016)

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 3

For more information

For additional considerations with regard to SAB 74 disclosures, see chapter 30 of our Financial statement presentation guide. In addition, our podcast FASB Standard setting update, First quarter 2016 shares information on some of the new standards for which SAB 74 disclosures should be considered.

Preferability as it relates to new standards

Companies may wish to voluntarily change from one generally accepted accounting principle to another when more than one principle is considered generally accepted. For example, a company may decide to change its inventory method from FIFO to LIFO. To make this change, a company must demonstrate that the change is preferable. The FASB has issued several significant new standards, which has prompted some companies to consider whether an accounting principle that is required under the new standard could serve as evidence that changing to that accounting principle now (prior to adopting the new standard) is preferable. For example, a company that is currently expensing sales commissions may want to change to a policy of deferring sales commissions prior to adoption of the new revenue standard. The company may believe the deferral method is preferable because it will be required by the new standard. The fact that an accounting principle will be required once a new standard is adopted does not, in and of itself, justify a change in accounting principle prior to the period of adoption. Companies must be able to relay that the change is preferable for other reasons—for example, that the change improves financial reporting or that the business has changed and the new accounting principle better reflects the economics of the business. Otherwise, the change in accounting principle is essentially early-adopting portions of the new standard, which is prohibited (unless the standard explicitly says otherwise). This guidance on changes in accounting principles applies to both public and private companies. Emphasis of material changes are required in the auditor’s report for all entities, and preferability letters are required for material accounting changes made by public companies.

For more information

For additional considerations with regard to changes in accounting policy, see chapter 30 of our Financial statement presentation guide.

Accelerated share repurchases make a comeback

When companies have excess cash, they may pay dividends to shareholders or engage in share buyback programs. There are various ways a company can buy back shares, including open market purchases or accelerated share repurchase (ASR) programs. Generally, companies use investment banks to structure and execute ASR programs, repurchasing a large number of shares at a purchase price determined by an average market price over a period of time.

Among the perceived benefits of an ASR program are the company’s ability to remove shares delivered to it from the investment bank on Day 1 from the EPS computation, and the avoidance of certain regulatory considerations (e.g., no blackout periods and no limit on the number of shares that can be purchased). In addition, the investment bank that’s involved often guarantees a discount from the average price of the company’s stock over the contract period.

Click here to learn more about accounting changes and preferability.

http://www.pwc.com/us/en/cfodirect/multimedia/podcasts/fasb-standard-setting-first-quarter-2016.html

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 4

Accounting implications

On Day 1, an ASR is accounted for as two transactions: a treasury stock purchase and a forward sale contract. The treasury stock purchase is straightforward, but the forward contract generally meets the definition of a derivative. As such, the company must consider whether the forward contract should be classified in equity or as a liability. Equity classification does not require subsequent remeasurement, while liability classification requires remeasurement at fair value, with changes in fair value reported through earnings.

In order to be classified in equity, the forward contract must qualify for the derivative scope exception. Typically the scope exception is available only if the contract is indexed to the company’s own stock and the ASR contract is classified as equity. The analysis required to determine if the scope exception applies involves understanding the economics behind all adjustments that can be made to the settlement value.

Companies should also consider the impact of the ASR on basic and diluted EPS. For instance, a company should assess all dividend provisions in the contract in order to ensure that the contract is not considered a participating security, which would require the use of the two class method for purposes of computing EPS. In addition, the contract will likely require the use of the treasury stock method for purposes of computing diluted EPS.

For more information

For help navigating the complexities of share repurchase contracts, see chapter 6 of our Guide to accounting for financing transactions: debt, equity and the instruments in between.

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 5

Hot off the press

PCAOB issues second proposal on changing the content of the auditor’s report

The PCAOB’s 2013 proposal to revise the content in the auditor’s report received significant feedback from auditors, companies, and other stakeholders. The new proposal would retain the existing “pass/fail” opinion and the basic elements of the auditor’s report, but would require the auditor to report a wider range of information specific to the particular audit and auditor.

Communicating critical audit matters (CAM)

The auditor would be required to communicate in the audit report CAM arising from the audit of the current period’s financial statements. The source of potential CAM are limited to any matters arising from the audit of the financial statements that are communicated or are required to be communicated to the audit committee, and that:

relate to accounts or disclosures that are material to the financial statements, and

involve especially challenging, subjective, or complex auditor judgment.

The auditor’s report would (1) identify the CAM; (2) describe the principal considerations that led the auditor to determine the

matter is a CAM; (3) describe how it was addressed in the audit; and (4) refer to the relevant financial statement accounts and disclosures.

Other aspects of the proposal

Under the proposed standard, the auditor’s report would indicate what year the auditor began serving consecutively as the company’s auditor, require the opinion to be the first section of the auditor’s report, and prescribe several other format and wording enhancements. The 2013 proposal also included proposed changes related to the auditor’s responsibilities for other information outside the financial statements. The PCAOB is not reproposing these changes at this time, but plans to determine next steps at a later date.

What’s next?

The proposed standard includes significant changes that would result in auditors reporting on certain facts and circumstances specific to a company’s audit. Companies may want to weigh in on the proposal. Comments on the proposal are due by August 15, 2016.

Comment letter deadlines:

Out for comment Comments due

Restricted cash on cash flow statement (FASB)

June 27

Technical corrections – revenue (FASB)

July 2

Technical corrections (FASB)

July 5

International Valuation Standards (IVSC)

July 7

Simplifying goodwill impairment (FASB)

July 11

Regulation S-K and disclosure requirements (SEC)

July 21

Clarifying scope of asset derecognition guidance (FASB)

August 5

Auditors report and responsibility regarding other information (PCAOB)

August 15

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 6

Regulatory update

Stay in the lane when communicating non-GAAP measures

Non-GAAP financial measures continue to be popular with companies looking to provide additional insights and information to users of their financial statements.

Together with the increased popularity of non-GAAP measures comes increased regulatory scrutiny. The SEC staff recently updated its interpretive guidance on non-GAAP measures. The SEC Division of Corporation Finance also continues to issue comments concerning non-GAAP measures, and in some cases, has objected to certain measures. The comments have focused on a company’s disclosure as to why its non-GAAP measures are useful; selective adjustments within a non-GAAP measure; and adjustments to remove normal cash operating expenses in liquidity measures.

Given the increased regulatory focus, management should review the relevant SEC rules and interpretive guidance, and make sure the non-GAAP measures disclosed comply with the requirements.

Non-GAAP measures are governed by three different regulations:

Regardless which regulation a particular non-GAAP disclosure falls under, it cannot be misleading and is prohibited from being included in financial statements or the accompanying notes. Companies must also reconcile the non-GAAP measure to its most directly comparable GAAP measure. Companies may be subject to express prohibitions or be required to disclose additional information depending on which regulation governs a particular non-GAAP disclosure. For example, adjusting a non-GAAP performance measure to eliminate or smooth items identified as non-recurring, infrequent, or unusual when such items are likely to recur or have occurred over a two-year period is expressly prohibited under Item 10(e). In addition, non-GAAP measures disclosed under Item 2.02 or Item 10(e) require the GAAP measure to be disclosed with equal or greater prominence, among other requirements.

For more information

For insights on steps companies can take to build confidence in their non-GAAP measures and other key performance indicators, read our Point of view, Building confidence in non-GAAP measures and other KPIs. For information on the SEC’s updated interpretive guidance on non-GAAP measures, read In brief US2016-22, SEC updates interpretive guidance on non-GAAP financial measures.

Regulation G Item 2.02 Form 8-K Item 10(e) Reg S-K

Covers public statements made by the company, such as:

Earnings webcasts

Media interviews

Industry conference slides

Non-earnings press releases (including earnings guidance)

Covers press releases or other public announcements of results of operations and financial conditions for completed quarterly or annual periods that are required to be furnished with the SEC.

Applies whenever non-GAAP measures are included in a filing with the SEC, such as:

Form 10-K

Form 10-Q

Proxy statements

Registration statements

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 7

Second heat starts for SEC’s disclosure effectiveness project

In April 2016, the SEC published a concept release to solicit stakeholder input on whether the business and financial disclosure requirements in Regulation S-K continue to provide important information for investors, and how that information can be presented most effectively. The concept release is the second release in the SEC’s disclosure effectiveness initiative, which was mandated by the Jumpstart Our Business Startups Act of 2012. The concept release focuses primarily on the non-financial statement portions of disclosures registrants provide in their periodic and current reports (e.g., Form 10-K, Form 10Q, Form 8-K) and registration statements (e.g., Form 10, Form S1, Form S3). The release excludes the required disclosures for foreign private issuers, business development companies, and certain other categories of registrants. The SEC is seeking comment on questions such as:

● whether registrants should be permitted to omit the earliest period in the three-year results of operations comparison when the earliest of the three years does not provide information that is important to investors;

● whether registrants should be required to discuss the probability of a risk occurrence and the effect on performance for each risk factor; and

● whether larger companies, such as companies with a longer reporting history or more readily available public information, should be allowed to benefit from scaled disclosure requirements as a means of reducing compliance costs.

Although the concept release’s length may be intimidating, it presents an excellent opportunity for investors, companies, audit committees, and other stakeholders to provide input on financial reporting requirements—even if they only provide comments on the aspects that are of most interest to them. Comments are due by July 21, 2016.

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 8

Corporate governance

Navigating the risks of forward-looking guidance

The vast majority of public companies provide forward-looking guidance, although it is not required. Analysts commonly consider this guidance in their financial models, most often in revenue and earnings per share forecasts. Many investors then use the analysts’ estimates to make investment decisions. Securities regulators also monitor this information—in fact, the SEC staff has recently renewed its focus on companies’ use of non-GAAP measures, which are often provided as part of forward-looking guidance. How useful forward-looking guidance is continues to be debated: Some companies view it as a market necessity, while others believe earnings guidance provides little benefit and can present greater risk than reward. When forward-looking guidance is provided, audit committee members should consider the legal, market, and reputational risks. In addition, some believe that forward-looking guidance could create a management bias to meet analysts’ estimates. Audit committees should consider that possibility when overseeing the integrity of the company’s financial reporting. They should also consider performing the following:

Understand management’s philosophy and assess whether sharing forward-looking guidance supports management’s focus on the long-term value drivers, and whether it is consistent with compensation incentives

Evaluate management’s rationale for providing guidance and periodically revisit company policy as trends evolve, market views fluctuate, and related risks change

Understand management’s processes for developing assumptions and estimates and accumulating guidance information, and consider whether the process is robust and management’s judgments are reasonable

Benchmark peer and competitor practices to evaluate whether the company is an outlier

For more information

Our latest edition of the Audit Committee Excellence Series, Forward-looking guidance, provides additional practical insights, the pros and cons of providing forward-looking guidance, and other key actions for audit committees to consider when forward-looking guidance is provided.

Is cash burning a hole in your pocket? Considering the impact of share repurchases and dividends

US companies are sitting on record levels of cash. While this phenomenon indicates robust balance sheet health, it also raises questions about the best way to use this liquidity. These situations stimulate provocative discussions about the most prudent use of company resources–taking into account different stakeholders’ expectations, the company’s individual circumstances, and the overall economic environment. Activists’ strategies layer on additional considerations: They may involve pressuring companies to return cash to shareholders through share repurchases or dividends.

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 9

Ultimately, companies need an effective capital allocation strategy that is well thought-out, linked to their overall strategy, and clearly communicated. Whether, and/or how, cash is returned to shareholders is a key element of this capital allocation strategy.

Companies may adopt share repurchase plans for a variety of reasons. For example, they may think their shares are undervalued by the market and want to signal confidence in the company’s future prospects. Similarly, companies may choose to pay dividends to their shareholders to signal management’s confidence in the company and its financial liquidity.

Directors and investors should be sure to understand the effect share repurchases and dividends might have on some of the company’s key performance metrics and potential effects on executive compensation. They should also consider the company’s equity and debt structure, as well as the potentially adverse accounting and tax impact of returning cash to shareholders that would have to be repatriated from foreign jurisdictions.

For more information

Refer to the first edition of our Director-Shareholder Insights series, Is cash burning a hole in your pocket? Thinking through share repurchases and dividends, for more information.

Board composition: Key trends and developments

With the numerous challenges companies face, the expertise, experience, and diversity of perspective in the boardroom play a more critical role than ever in ensuring effective oversight. At the same time, many investors and other stakeholders, including activist investors, are seeking influence on board composition. They want more information about a company’s director nominees, and want to know that boards are appropriately considering director tenure, board diversity, and the results of board self-evaluations when making director nominations.

Within this context, directors can proactively address board refreshment by:

acting on the results of board assessments;

taking a strategic approach to director succession planning; and

broadening the pool of candidates when recruiting directors.

For more information

Read our Point of view, Board composition: Maintaining high performance, and Board composition – Key trends and developments, an edition of our Director-Shareholder Insights series, for additional steps directors can take to enhance board composition.

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 10

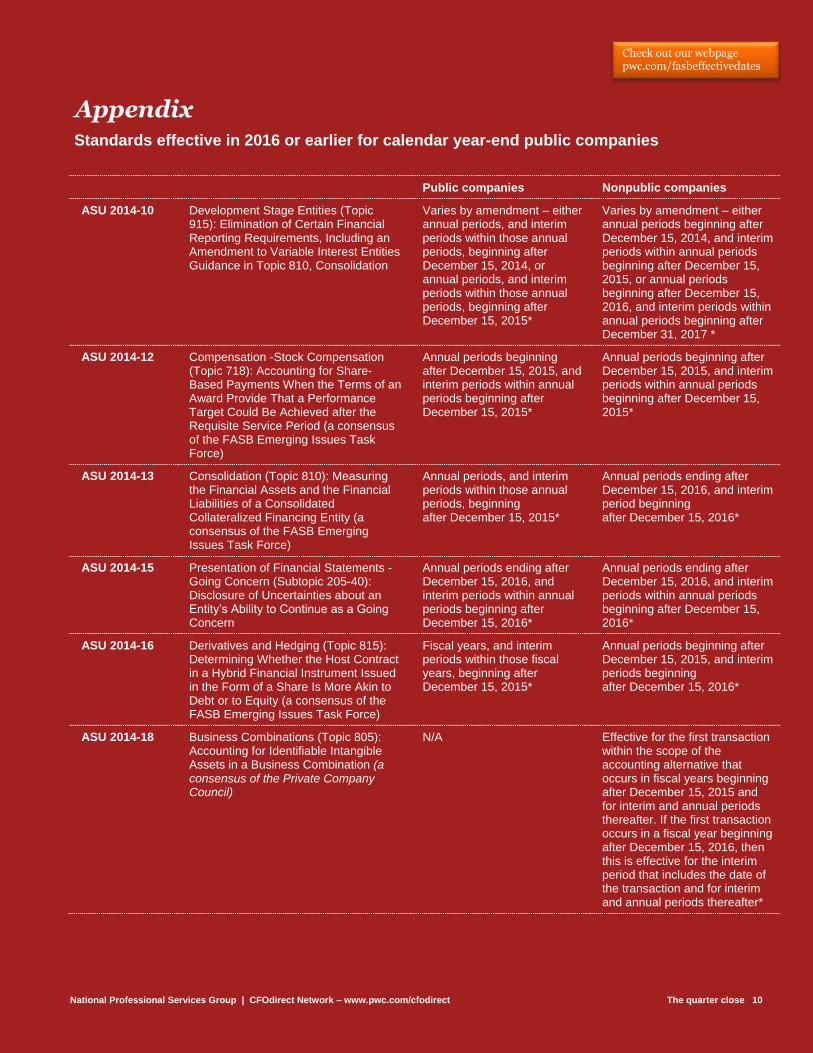

Appendix Standards effective in 2016 or earlier for calendar year-end public companies

Public companies Nonpublic companies

ASU 2014-10 Development Stage Entities (Topic 915): Elimination of Certain Financial Reporting Requirements, Including an Amendment to Variable Interest Entities Guidance in Topic 810, Consolidation

Varies by amendment – either annual periods, and interim periods within those annual periods, beginning after December 15, 2014, or annual periods, and interim periods within those annual periods, beginning after December 15, 2015*

Varies by amendment – either annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015, or annual periods beginning after December 15, 2016, and interim periods within annual periods beginning after December 31, 2017 *

ASU 2014-12 Compensation -Stock Compensation (Topic 718): Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period (a consensus of the FASB Emerging Issues Task Force)

Annual periods beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2015*

Annual periods beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2015*

ASU 2014-13 Consolidation (Topic 810): Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity (a consensus of the FASB Emerging Issues Task Force)

Annual periods, and interim periods within those annual periods, beginning after December 15, 2015*

Annual periods ending after December 15, 2016, and interim period beginning after December 15, 2016*

ASU 2014-15 Presentation of Financial Statements -Going Concern (Subtopic 205-40): Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Annual periods ending after December 15, 2016, and interim periods within annual periods beginning after December 15, 2016*

Annual periods ending after December 15, 2016, and interim periods within annual periods beginning after December 15, 2016*

ASU 2014-16 Derivatives and Hedging (Topic 815): Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity (a consensus of the FASB Emerging Issues Task Force)

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

Annual periods beginning after December 15, 2015, and interim periods beginning after December 15, 2016*

ASU 2014-18 Business Combinations (Topic 805): Accounting for Identifiable Intangible Assets in a Business Combination (a consensus of the Private Company Council)

N/A Effective for the first transaction within the scope of the accounting alternative that occurs in fiscal years beginning after December 15, 2015 and for interim and annual periods thereafter. If the first transaction occurs in a fiscal year beginning after December 15, 2016, then this is effective for the interim period that includes the date of the transaction and for interim and annual periods thereafter*

Check out our webpage pwc.com/fasbeffectivedates

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 11

Public companies Nonpublic companies

ASU 2015-01 Income Statement—Extraordinary and Unusual Items (Subtopic 225-20): Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

ASU 2015-02 Consolidation (Topic 810): Amendments to the Consolidation Analysis

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016, and interim periods beginning after December 15, 2017*

ASU 2015-03 Interest-Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015, and interim periods beginning after December 15, 2016*

ASU 2015-15 Interest—Imputation of Interest (Subtopic 835-30): Presentation and Subsequent Measurement of Debt Issuance Costs Associated with Line-of-Credit Arrangements - Amendments to SEC Paragraphs Pursuant to Staff Announcement at June 18, 2015 EITF Meeting

Should be adopted concurrent with adoption of ASU 2015-03*

Should be adopted concurrent with adoption of ASU 2015-03*

ASU 2015-04 Compensation-Retirement Benefits (Topic 715): Practical Expedient for the Measurement Date of an Employer’s Defined Benefit Obligation and Plan Assets

Annual reporting periods beginning after December 15, 2015, and interim periods within those fiscal years*

Annual reporting periods beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017*

ASU 2015-05 Intangibles-Goodwill and Other-Internal-use software (Subtopic 350-40): Customer's Accounting for Fees Paid in a Cloud Computing Arrangement

Annual periods, including interim periods within those annual periods, beginning after December 15, 2015*

Annual periods beginning after December 15, 2015, and interim periods in annual periods beginning after December 15, 2016*

ASU 2015-06 Earnings per share (Topic 260): Earnings Per Share (Topic 260): Effects on Historical Earnings per Unit of Master Limited Partnership Dropdown Transactions (a consensus of the Emerging Issues Task Force)

Fiscal years beginning after December 15, 2015, and interim periods within those fiscal years*

Fiscal years beginning after December 15, 2015, and interim periods within those fiscal years*

ASU 2015-07 Fair Value Measurement (Topic 820): Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent) (a consensus of the Emerging Issues Task Force)

Fiscal years beginning after December 15, 2015, and interim periods within those fiscal years*

Fiscal years beginning after December 15, 2016, and interim periods within those fiscal years*

ASU 2015-09 Financial Services—Insurance (Topic 944): Disclosures about Short-Duration Contracts

Annual periods beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016*

Annual periods beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017*

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 12

Public companies Nonpublic companies

ASU 2015-10 Technical Corrections and Improvements

Transition guidance varies based on the amendments in this Update. The amendments in this Update that require transition guidance are effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

Transition guidance varies based on the amendments in this Update. The amendments in this Update that require transition guidance are effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015*

ASU 2015-12 Plan Accounting: Defined Benefit Pension Plans (Topic 960), Defined Contribution Pension Plans (Topic 962), Health and Welfare Benefit Plans (Topic 965): (Part I) Fully Benefit-Responsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient (consensuses of the Emerging Issues Task Force)

Fiscal years beginning after December 15, 2015*

Effective for fiscal years beginning after December 15, 2015*

ASU 2015-16 Business Combinations (Topic 805): Simplifying the Accounting for Measurement-Period Adjustments

Fiscal years beginning after December 15, 2015, including interim periods within those fiscal years. Apply prospectively to adjustments to provisional amounts that occur after the effective date*

Fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017. Apply prospectively to adjustments to provisional amounts that occur after the effective date*

ASU 2016-03 Intangibles—Goodwill and Other (Topic 350), Business Combinations (Topic 805), Consolidation (Topic 810), Derivatives and Hedging (Topic 815): Effective Date and Transition Guidance (PCC 15-01)

N/A Effective immediately

ASU 2016-11 Revenue Recognition (Topic 605) and Derivatives and Hedging (Topic 815): Rescission of SEC Guidance Because of Accounting Standards Updates 2014-09 and 2014-16 Pursuant to Staff Announcements at the March 3, 2016 EITF Meeting (SEC Update)

Effective immediately N/A

*early adoption permitted

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 13

Standards effective after 2016 for calendar year-end public companies

Public companies Nonpublic companies

ASU 2014-09 Revenue from Contracts with Customers (Topic 606), as amended by ASU 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date

Annual reporting periods beginning after December 15, 2017, including interim reporting periods within that reporting period*

Annual reporting periods beginning after December 15, 2018, and interim periods beginning after December 15,

2019*

Revenue from Contracts with Customers (Topic 606):

Should be adopted concurrent with adoption of ASU 2014-09

Should be adopted concurrent with adoption of ASU 2014-09

ASU 2016-08 Principal versus Agent Considerations (Reporting Revenue Gross versus Net)

ASU 2016-10 Identifying Performance Obligations and Licensing

ASU 2016-12 Narrow-Scope Improvements and Practical Expedients

ASU 2015-11 Inventory (Topic 330): Simplifying the Measurement of Inventory

Fiscal years beginning after December 15, 2016, including interim periods within those fiscal years*

Fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017*

ASU 2015-17 Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes

Annual periods beginning after December 15, 2016, and interim periods within those annual periods*

Fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018*

ASU 2016-01 Financial Instruments—Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities

Fiscal years beginning after December 15, 2017, including interim periods within those fiscal years*(for certain amendments)

Fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019*

ASU 2016-02 Leases (Topic 842) Fiscal years beginning after December 15, 2018, including interim periods within those fiscal years*

Fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020*

ASU 2016-04 Liabilities—Extinguishments of Liabilities (Subtopic 405-20): Recognition of Breakage for Certain Prepaid Stored-Value Products (a consensus of the EITF)

Financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years*

Financial statements issued for fiscal years beginning after December 15, 2018, and interim periods with fiscal years beginning after December 15, 2019*

ASU 2016-05 Derivatives and Hedging (Topic 815): Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships (a consensus of the Emerging Issues Task Force)

Financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years*

Financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018*

Check out our webpage pwc.com/fasbeffectivedates

National Professional Services Group | CFOdirect Network – www.pwc.com/cfodirect The quarter close 14

Public companies Nonpublic companies

ASU 2016-06 Derivatives and Hedging (Topic 815): Contingent Put and Call Options in Debt Instruments (a consensus of the Emerging Issues Task Force)

Financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years*

Financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018.*

ASU 2016-07 Investments—Equity Method and Joint Ventures (Topic 323): Simplifying the Transition to the Equity Method of Accounting

Effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016*

Effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016*

ASU 2016-09 Compensation—Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting

Annual periods beginning after December 15, 2016, and interim periods within those annual periods*

Annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018. *

*early adoption permitted

Edited by: Beth Paul Partner Phone: 1-973-236-7270 Email: [email protected]

Kassie Bauman Director Phone: 1-973-236-5118 Email: [email protected]

Becky Bisesar Senior Manager Phone: 1-973-236-5794 Email: [email protected]

The quarter close is prepared by the National Professional Services Group of PwC. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. To access additional content on accounting and reporting issues, visit CFOdirect Network (www.pwc.com/cfodirect), PwC’s online resource for financial executives. © 2016 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the United States member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.