The Predictive Power of the Yield Spread in Sub-Saharan and Northern Africa

50

1 The Predictive Power of the Yield Spread in Sub-Saharan and Northern Africa May 2008 By Oluwasegun Popoola

-

Upload

segunpopoola1849 -

Category

Documents

-

view

521 -

download

3

description

The predictive power of the yield spread has been widely studied and documented in the United States and a number of countries outside the United States. However, little or no studies have been conducted in Africa. This paper studies the predictive power of the yield spread and ascertains its usefulness for predicting real economic growth in Africa. It buttresses the predictive ability of the yield spread particularly in South Africa where the results suggest that the yield spread as a predictive indicator of future economic activities performs better at longer horizons.The paper further identifies the appropriate model for forecasting the yield spread in Morocco, Nigeria and South Africa.

Transcript of The Predictive Power of the Yield Spread in Sub-Saharan and Northern Africa

1

The Predictive Power of the

Yield Spread in Sub-Saharan and Northern Africa

May 2008

By Oluwasegun Popoola

2

Table of Contents

Abstract…………….………………………………………………………….……3

Section 1 Introduction……………………………………………………………...4

1.1 Background to the Study…………………………...4

1.2 Objectives of the Study..…………………………...6

1.3 Structure of the Study...…………………….……...6

Section 2 Literature Review and Theoretical Framework…………. ……………..7

2.1 Related Literature………………………..…………7

2.2 Theoretical Framework..…………………………....9

Section 3 Research Methodology, Empirical Analysis and Results……………...11

3.1 Data Description and Source(s)…………..….…….10

3.2 Predictive Power of the Yield Spread......................29

3.3 Forecasting Model Selection……............................44

Section 4 Summary of Research Findings, Recommendations and Conclusion…45

4.1 Summary of Research Findings……………………45

4.2 Conclusion..………………………………………..45

References…………………………………………………………………….…..48

3

Abstract

The predictive power of the yield spread has been widely studied and documented in the United States

and a number of countries outside the United States. However, little or no studies have been conducted in

Africa.

This paper studies the predictive power of the yield spread and ascertains its usefulness for predicting real

economic growth in Africa. It buttresses the predictive ability of the yield spread particularly in South

Africa where the results suggest that the yield spread as a predictive indicator of future economic

activities performs better at longer horizons.

The paper further identifies the appropriate model for forecasting the yield spread in Morocco, Nigeria

and South Africa.

4

SECTION 1

INTRODUCTION

1.1 Background to the Study

The use of financial variables to predict real economic activity only took a serious turn in the Nineties

when policymakers began to find alternative but more reliable ways of predicting economic conditions

having being previously been limited by the faulty macroeconomic models which are often characterized

by the lack of timely and accurate data and the complexity of the macroeconomic forecasting models.

The growing demand for such variables by policy makers fueled widening research into these variables

and their usefulness in predicting future economic conditions. One of such financial variables is the yield

spread, which is simply the difference between the long-term and short-term government instruments’

rates1.

Several studies have been conducted on the efficacy of the yield spread, which is often referred to as an

indicator of the future direction of the economy. Generally, a positive yield spread (i.e. higher long-term

interest rates than short-term rates) is associated with future economic expansion, while a negative yield

spread (i.e. lower long-term interest rates than short-term rates) is associated with future economic

contraction.

1 The widely used measure of the yield spread is the difference between the 10-year Treasury note and the 3-month

Treasury bill.

5

Harvey (1988) and several authors documented that there is information about future consumption and

output growth in the yield spread.

Bonser-Neal and Morley (1997) discovered that the predictive power of the yield spread is strongest in

Canada, Germany and the United States having taken the study of the efficacy of the yield spread further

by studying its implications in eleven OECD countries.

Perhaps, the closest semblance of a study of the yield spread and its predictive power in Africa was

conducted by Khomo and Aziakpono (2007) who both compared the efficacy of the yield curve and other

economic indicators as predictors of future economic activities (i.e. economic recessions and expansions)

in South Africa.

The seeming lack of studies on the yield spread in Africa is largely due to the nature of the African

monetary and financial markets which was largely seen as illiquid and sometimes not transparent because

of the level and size of government intervention and controls.

In addition, the institutional development frameworks for financial and monetary regulators and players

which were established about five decades ago in Sub-Saharan and Northern Africa (i.e. Morocco,

Nigeria and South Africa) only began to take strong roots in the last two decades. As a result, the use of

financial variables to forecast real economic activity was either absent or somewhat limited in most of the

countries studied.

This study is therefore is an attempt to ascertain the predictive power or otherwise of the yield spread in

three countries in Sub-Saharan and Northern Africa (i.e. Morocco, Nigeria and South Africa). The choice

of the countries was based on two criteria. First, only countries in the top five bracket of largest countries

6

in Africa in terms of real GDP were considered, Second, quarterly data on interest rates and (or) real

economic activity had to be available for at least the last ten years.

1.2 Objectives of the Study

The objectives of the study are:

Highlight the importance2 of the yield spread and determine the forecasting power

3 if any, of the

yield spread in Sub-Saharan and Northern Africa;

Appraise the theoretical underpinnings of the predictive capacity of the yield spread in Sub-

Saharan and Northern Africa; and

Consider the continued relevance of this financial variable in the light of constantly changing

economic conditions and circumstances.

1.3 Structure of the Study

The study covers the period 1963Q1 to 2006Q4. Section 2 contains a broad review of the existing and

relevant literature related to the study. A theoretical framework is also provided. Section 3 provides a

specification of the model, analysis of results obtained and the drawn generalizations from the findings.

Section 4 contains the summary of research findings, recommendations and conclusion.

2 Knowledge of the predictive ability of the yield spread enables businesses and policy makers to make better

forecasts of real economic activity in the light of unprecedented economic growth being recorded in Sub-Saharan

and Northern Africa in the last one decade. 3 As mentioned earlier, the yield spread is assumed to be a predictor of future economic conditions such as economic

expansion or contraction.

7

SECTION 2

RELATED LITERATURE AND THEORETICAL FRAMEWORK

2.1 Related Literature

Predictive role of the yield spread in industrial countries

Extensive studies on the predictive power of the yield spread and its predictive capacity began in the mid-

sixties when Kessel (1965) noted the existence of relationship between the yield curve and future real

economic activity. Ever since, researchers and analysts have continued to investigate the existence of a

relationship between these two economic variables.

In the late eighties and nineties, several studies including Harvey (1989) found that the yield spread

predicts real GDP growth in the United States. Stock and Watson (1989) empirically tested and

established a predictive relationship4 in macroeconomics that when the difference in yields between long

and short term interest rates in the United States is low or negative, future GDP growth tends to be slow

or negative. This view is also corroborated in Bernanke and Blinder (1992). Haubrich and Dombrosky

(1996) found that the yield spread is an excellent predictor of economic growth. Furthermore, Estrella and

Mishkin (1996), Dueker (1997) and Dotsey (1998) compare the yield curve with a few other variables5 as

a leading indicator of United States recessions and find generally supportive statistical evidence.

4 Recent findings however, indicate the relative weakness of the predictive power of yield curves and spreads to

forecast economic growth and future interest rates in the United States. For instance, the yield spread failed to

predict the 1990-1991 recession. Popoola (2007) 5 Alternative indicators are stock prices, stock returns, interest rates, dividend yields and exchange rates.

8

The early and mid-nineties also saw the emergence of a couple of studies on the predictive power of the

yield spread outside the United States. Estrella and Hardouvelis (1991) found that the yield spread

predicts real GDP growth in the United States and a number of European countries. Hu (1993), Caporale

(1994), Plosser and Rouwenhorst (1994) and Estrella and Mishkin (1995) all attempted to ascertain the

predictive power of the yield spread within and outside the United States. To the author’s best knowledge,

the most extensive multi-country analysis of the yield spread and its predictive capacity known to date

was conducted by Bonser-Neal and Morley (1997)6.

Predictive role of the yield spread in Africa

While extensive studies on the yield curve exist for the United States and a number of industrialized

countries, very little advancements have been made to study the yield curve and its predictive power in

other countries. Study on emerging economies let alone African countries are almost non-existent. This

view was buttressed by Mehl (2006).

Two works that specifically dwell on the yield spread and its predictive capacity relating to sub-Saharan

Africa were written by Mehl (2006) whose work was on the use of the slope of the yield curve to predict

domestic inflation and growth in South Africa among other emerging countries; while Khomo and

Aziakpono (2007) compared the efficacy of the yield curve and other economic indicators as predictors of

future economic activities (i.e. economic expansions or recessions) in South Africa.

Contribution

Interestingly, very few of the previous studies explored the possibility of appraising the theoretical

underpinnings of the predictive capacity of the yield spread in spite of the extensive literature available on

6 Bonser-Neal and Morley (1997) studied eleven OECD countries in their paper.

9

the subject matter. The only study known to the author was by Hamilton and Kim (2002) which attempted

to theoretically show evidence to buttress why the yield spread helps in forecasting the business cycle.

In addition, there has been no extensive work on the predictive capacity of the yield spread in African

countries except South Africa.

To the author’s best knowledge, this study is the first attempt to investigate and study the predictive

power of the yield spread in Morocco and Nigeria and provide an appropriate model for forecasting the

yield spread in Morocco, Nigeria and South Africa.

2.2 Theoretical Framework

The predictive capacity of the yield spread is embodied in an understanding of the relationship existing

between the yield curve, its movements and how it impacts economic conditions.7 A yield curve is the

graphical distribution of the yields of treasury securities with different maturities (i.e. 3-month, 6-month,

2, 3, 5, 10 and 20-year). The yield spread as described earlier is the difference between the long-term and

short-term government instruments’ rates. It is widely believed that the difference between the short and

long-term rates indicates the steepness or the slope of the yield curve.

A positive yield spread (i.e. long term rates are higher than short term rates; positively sloped yield curve)

is associated with a potential future increase in real economic activity while negative yield spread (i.e.

short term rates are higher than long term rates; negatively sloped or inverted yield curve) is associated

with a potential future decrease in real economic activity. Resultantly, the size of the yield spread

indicates the potential future increase or decline in real economic activity.

7 Guiding thoughts from Bonser-Neal and Morley (1997)

10

The following reasons have been adduced for the empirical relationship between the yield spread and its

predictive capacity:

The yield spread reflects the stance of monetary policy;

The yield spread reflects market expectations of future economic growth;

The yield spread reflects credit market conditions and in addition, reflects the changes in

expected inflation, fiscal situation and investors’ risk preferences.

Studies have consistently shown that all the theories listed above may have some merit. Estrella and

Hardovelis (1991) and Estrella and Mishkin (1995), for example, show that proxies for current monetary

policy do help forecast future real GDP growth; however, the inclusion of these proxies does not

eliminate the significance of the yield curve. These results suggest the yield curve reflects more than just

the effects of current monetary policy actions.

11

SECTION 3

RESEARCH METHODOLOGY, EMPIRICAL ANALYSIS AND

RESULTS

3.1 Data Description and Source(s)

The author studied three countries in Africa as previously documented in section one of the paper.

Real GDP is observed quarterly in South Africa and thus the sample is quarterly from 1963 through the

end of 2005 (i.e. 1963.01 to 2006.04). The author also obtained the 10-year government bond yield and 3-

month Treasury bill rate.

Quarterly real GDP for Morocco and Nigeria was unavailable. As a result, the author was unable to test

the predictive power of the yield spread. The author, however, obtained the quarterly 15-year Treasury

bond yield8 and 3-month Treasury bill rate for Morocco and deposit rate

9 and 3-month Treasury bill rate

for Nigeria in order to derive the yield spread.

All the data sets used for this study was sourced from the International Monetary Fund (IMF) data and

statistics electronic database.

8 15-year Treasury bond yield used in the absence of 10-year Treasury bond yield in Morocco.

9 The deposit rate was used as Nigeria discontinued the issuance of long term bonds only to have them re-introduced

about five years ago.

12

Figure 3.1 displays the time series plot of the annualized rate of growth of real GDP in South Africa over

the next four quarters which suggests that annualized growth rate in real GDP has been relatively unstable

over time.

Fig 3.1: Annualized Real GDP Growth Rates, 1963.01 – 2006.04 (South Africa)

-2

-1

0

1

2

3

4

5

65 70 75 80 85 90 95 00 05

GDP GROWTH RATE

Fig 3.2: Time series of T-bill rate and Government Bond Yield, 1963.01 – 2006.04 (South Africa)

0

4

8

12

16

20

24

65 70 75 80 85 90 95 00 05

TREASURY BILL RATE GOVERNMENT BOND YIELD

13

Fig 3.3: The Yield Spread and Real GDP growth rate, 1963.01 – 2006.04 (South Africa)

-6

-4

-2

0

2

4

6

8

65 70 75 80 85 90 95 00 05

GDP GROWTH RATE SPREAD

Fig 3.4: The Yield Spread, Real GDP growth rate and Periods of negative Real GDP growth rate, 1963.01 –

2006.04 (South Africa)

-6

-4

-2

0

2

4

6

8

65 70 75 80 85 90 95 00 05

GDP GROWTH RATE SPREAD

Figure 3.2 and 3.3 displays the time series of the T-bill rate and government bond yield rate and the yield

spread and real GDP respectively. Figure 3.4 displays the time series of the yield spread and real GDP.

14

The author observed that the yield spread declined into negative territory just before the real GDP turns

negative indicating the presence of predictive power in South Africa’s yield spread.

3.2 Predictive Power of the Yield Spread

The author followed the standard regression methodology adopted in previous studies, such as Estrella

and Hardouvelis (1991), Estrella and Mishkin (1997) and Bonser-Neal and Morley (1997).

Model Specification

(ΔY) t, t+k = α + β*spreadt + error,

Where ΔY is the change in real economic activity and defined as the annualized growth rate in real GDP.

The subscript k denotes the forecasting horizon in quarters and the spread is defined as the difference

between the long-term and short-term rates.

Results

The results reported in Table 3.1 indicates the yield spread explains roughly between 5% and 7% of the

variation in the following period’s real GDP (i.e. t + k). In addition, the results seem to support the

findings, in Khomo and Aziakpono (2007) that the yield spread as a predictive indicator of future

economic activities performs better at longer horizons compared to other leading indicators in South

Africa.

15

Table 3.1: Explanatory Power of the Yield Spread for Real GDP

Forecasting

Horizon;

Explanatory Power of the

Yield Spread for Real GDP

k Quarters

Ahead

1 5.66

2 6.10

3 6.23

4 6.27

5 6.27

6 6.27

7 6.30

8 6.37

12 6.47

16 6.60

20 6.74

3.3 Forecasting Model Selection

The author applied a number of models including trend, seasonality and ARMA regression models to

choose the best model to forecast yield spread from January to December 2006.

16

Trend Regression Model

Linear Trend Model

Yt = o + 1Timet + t

Table 3.2: Linear Trend Regression (South Africa)

Table 3.3: Linear Trend Regression (Morocco)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/04/08 Time: 23:29

Sample: 1963Q1 2005Q4

Included observations: 172

Variable Coefficient Std. Error t-Statistic Prob.

C 2.854042 0.357074 7.992849 0.0000

TIME -0.011156 0.003612 -3.089045 0.0023

R-squared 0.053147 Mean dependent var 1.900193

Adjusted R-squared 0.047578 S.D. dependent var 2.409735

S.E. of regression 2.351711 Akaike info criterion 4.559723

Sum squared resid 940.1927 Schwarz criterion 4.596322

Log likelihood -390.1362 F-statistic 9.542199

Durbin-Watson stat 0.159212 Prob(F-statistic) 0.002346

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 01:18

Sample: 1998Q1 2005Q4

Included observations: 32

Variable Coefficient Std. Error t-Statistic Prob.

C 1.442309 0.183345 7.866632 0.0000

TIME 0.027815 0.010162 2.737035 0.0103

R-squared 0.199816 Mean dependent var 1.873437

Adjusted R-squared 0.173143 S.D. dependent var 0.583715

S.E. of regression 0.530782 Akaike info criterion 1.631531

Sum squared resid 8.451888 Schwarz criterion 1.723139

Log likelihood -24.10450 F-statistic 7.491363

Durbin-Watson stat 0.488715 Prob(F-statistic) 0.010319

17

Table 3.4: Linear Trend Regression (Nigeria)

Quadratic Trend Model

Yt = o + 1Timet + 2Timet2 + t

Table 3.5: Quadratic Trend Regression (South Africa)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 02:54

Sample: 1992Q1 2005Q4

Included observations: 56

Variable Coefficient Std. Error t-Statistic Prob.

C 1.250543 0.690317 1.811548 0.0756

TIME 0.000645 0.021641 0.029795 0.9763

R-squared 0.000016 Mean dependent var 1.268275

Adjusted R-squared -0.018502 S.D. dependent var 2.593718

S.E. of regression 2.617602 Akaike info criterion 4.797456

Sum squared resid 369.9995 Schwarz criterion 4.869790

Log likelihood -132.3288 F-statistic 0.000888

Durbin-Watson stat 0.584429 Prob(F-statistic) 0.976341

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/04/08 Time: 23:36

Sample: 1963Q1 2005Q4

Included observations: 172

Variable Coefficient Std. Error t-Statistic Prob.

C 2.480436 0.531913 4.663240 0.0000

TIME 0.002030 0.014373 0.141239 0.8878

TIME^2 -7.71E-05 8.14E-05 -0.947883 0.3445

R-squared 0.058155 Mean dependent var 1.900193

Adjusted R-squared 0.047009 S.D. dependent var 2.409735

S.E. of regression 2.352414 Akaike info criterion 4.566049

Sum squared resid 935.2207 Schwarz criterion 4.620947

Log likelihood -389.6802 F-statistic 5.217491

Durbin-Watson stat 0.160069 Prob(F-statistic) 0.006328

18

Table 3.6: Quadratic Trend Regression (Morocco)

Table 3.7: Quadratic Trend Regression (Nigeria)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 01:19

Sample: 1998Q1 2005Q4

Included observations: 32

Variable Coefficient Std. Error t-Statistic Prob.

C 1.028893 0.247380 4.159157 0.0003

TIME 0.110498 0.036936 2.991644 0.0056

TIME^2 -0.002667 0.001151 -2.316430 0.0278

R-squared 0.324756 Mean dependent var 1.873437

Adjusted R-squared 0.278187 S.D. dependent var 0.583715

S.E. of regression 0.495922 Akaike info criterion 1.524263

Sum squared resid 7.132218 Schwarz criterion 1.661676

Log likelihood -21.38822 F-statistic 6.973708

Durbin-Watson stat 0.577224 Prob(F-statistic) 0.003367

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 02:54

Sample: 1992Q1 2005Q4

Included observations: 56

Variable Coefficient Std. Error t-Statistic Prob.

C -2.035820 0.815493 -2.496430 0.0157

TIME 0.365796 0.068563 5.335170 0.0000

TIME^2 -0.006639 0.001206 -5.506504 0.0000

R-squared 0.363921 Mean dependent var 1.268275

Adjusted R-squared 0.339918 S.D. dependent var 2.593718

S.E. of regression 2.107278 Akaike info criterion 4.380754

Sum squared resid 235.3529 Schwarz criterion 4.489255

Log likelihood -119.6611 F-statistic 15.16148

Durbin-Watson stat 0.915792 Prob(F-statistic) 0.000006

19

Exponential Trend Model

Yt = oe1Timet

+ t

Table 3.8: Exponential Trend Regression (South Africa)

Table 3.9: Exponential Trend Regression (Morocco)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 01:21

Sample: 1998Q1 2005Q4

Included observations: 32

Convergence achieved after 9 iterations

SPREAD=C(1)*EXP(C(2)*TIME) Coefficient Std. Error t-Statistic Prob.

C(1) 1.511348 0.167015 9.049159 0.0000

C(2) 0.013417 0.005542 2.420939 0.0217

R-squared 0.181001 Mean dependent var 1.873437

Adjusted R-squared 0.153701 S.D. dependent var 0.583715

S.E. of regression 0.536986 Akaike info criterion 1.654772

Sum squared resid 8.650618 Schwarz criterion 1.746380

Log likelihood -24.47635 Durbin-Watson stat 0.477824

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/04/08 Time: 23:40

Sample: 1963Q1 2005Q4

Included observations: 172

Convergence achieved after 6 iterations

SPREAD=C(1)*EXP(C(2)*TIME) Coefficient Std. Error t-Statistic Prob.

C(1) 2.893209 0.438064 6.604528 0.0000

C(2) -0.005262 0.001986 -2.649734 0.0088

R-squared 0.048053 Mean dependent var 1.900193

Adjusted R-squared 0.042454 S.D. dependent var 2.409735

S.E. of regression 2.358029 Akaike info criterion 4.565089

Sum squared resid 945.2509 Schwarz criterion 4.601688

Log likelihood -390.5976 Durbin-Watson stat 0.158361

20

Table 3.10: Exponential Trend Regression (Nigeria)

Table 3.11: Comparing AIC and SIC (South Africa)

Trend AIC SIC

Linear 4.5377 4.5737

Quadratic 4.5433 4.5974

Exponential 4.5439 4.5800

Table 3.12: Comparing AIC and SIC (Morocco)

Trend AIC SIC

Linear 1.6315 1.7231

Quadratic 1.5242 1.6617

Exponential 1.6548 1.7464

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 03:03

Sample: 1992Q1 2005Q4

Included observations: 56

Convergence achieved after 6 iterations

SPREAD=C(1)*EXP(C(2)*TIME) Coefficient Std. Error t-Statistic Prob.

C(1) -4.67E-13 5.30E-12 -0.088176 0.9301

C(2) 0.702880 2.95E-06 238064.3 0.0000

R-squared

-2959146.6

08949 Mean dependent var 1.268275

Adjusted R-squared

-3013945.6

38744 S.D. dependent var 2.593718

S.E. of regression 4502.882 Akaike info criterion 19.69788

Sum squared resid 1.09E+09 Schwarz criterion 19.77022

Log likelihood -549.5407 Durbin-Watson stat 0.255009

21

Table 3.13: Comparing AIC and SIC (Nigeria)

Trend AIC SIC

Linear 4.7975 4.8698

Quadratic 4.3808 4.4892

Exponential 19.6979 19.7702

Having considered the three models (i.e. linear, quadratic and exponential), we adopt the linear model for

South Africa and the quadratic model for Morocco and Nigeria10

.

A cursory look at the regression statistics produced by the linear trend model for South Africa and

quadratic model for Morocco and Nigeria reveal the following:

Linear Trend Model – South Africa

The linear term is significant11

.

R2

indicates that the trend is only responsible for about 5.3% of the variation in the yield

spread.

A Durbin-Watson statistic of 0.159 indicates the presence of positive serial correlation.

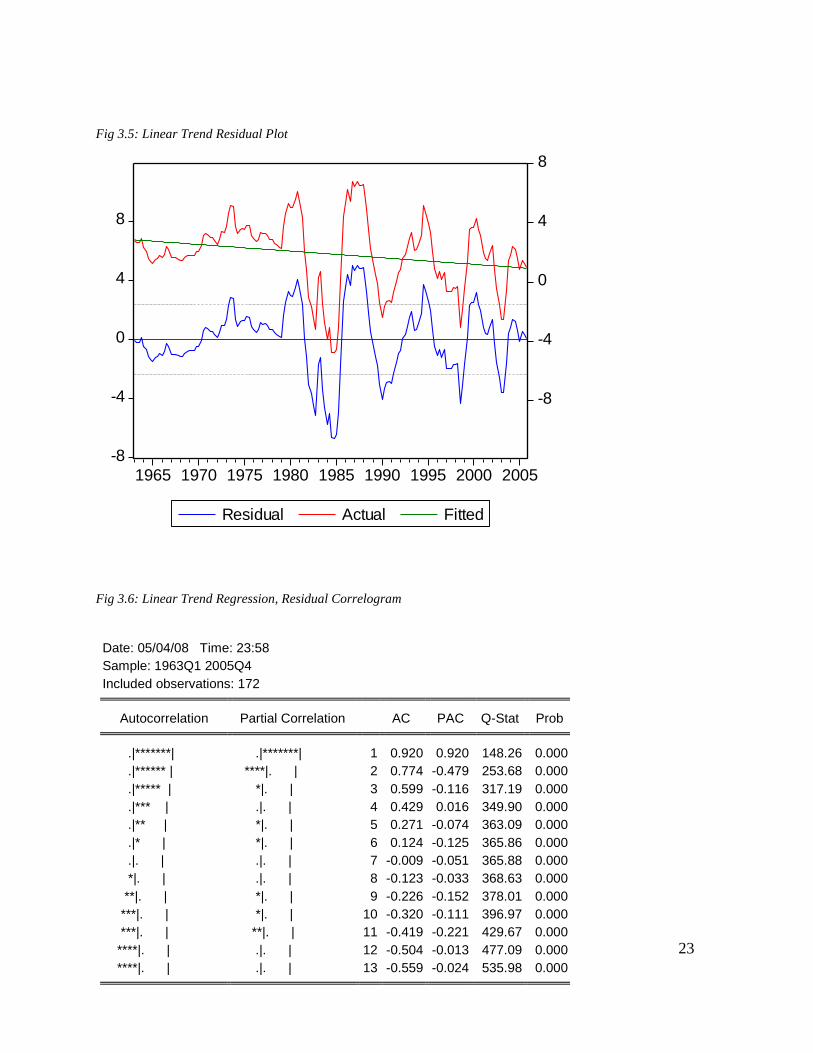

The linear trend regression residual plot in figure 3.5 reveals that the fitted trend remains relatively stable

throughout. As a result, it is difficult to notice any obvious seasonality or cyclical patterns.

Quadratic Model – Morocco

The linear and quadratic terms are significant.

10

The model with the lowest SIC and AIC for each country is selected in this instance. 11

Except otherwise stated, test of significance is at the 95% confidence interval.

22

R2 indicates that the trend is only responsible for about 32% of the variation in the yield

spread.

A Durbin-Watson statistic of 0.5772 indicates the presence of positive serial correlation.

The fitted trend remains stable throughout as can be seen from the quadratic trend regression residual plot

in figure 3.7. As a result, it is difficult to notice any obvious seasonality or cyclical patterns.

Quadratic Model – Nigeria

The linear and quadratic terms are significant.

R2 indicates that the trend is only responsible for about 36% of the variation in the yield

spread.

A Durbin-Watson statistic of 0.9158 indicates the presence of positive serial correlation.

The fitted trend remains stable as can be seen from the quadratic trend regression residual plot in figure

3.9. As a result, it is difficult to notice any obvious seasonality or cyclical patterns.

The residual correlograms and its graphs (i.e. figure 3.6, 3.7 and 3.8) reveal the residual sample

autocorrelation and partial autocorrelation function has spikes in the 1st, 2

nd, 9

th and 11

th lags for South

Africa; 1st and 2

nd lags for Morocco and 1

st, 2

nd, 9

th and 11

th lags for Nigeria. Additionally, it can been

seen that the Ljung-Box statistic rejects the white noise null hypothesis even at very small, non-seasonal

displacements which means there is still some useful information contained in the residuals which can be

extracted.

23

Fig 3.5: Linear Trend Residual Plot

-8

-4

0

4

8

-8

-4

0

4

8

1965 1970 1975 1980 1985 1990 1995 2000 2005

Residual Actual Fitted

Fig 3.6: Linear Trend Regression, Residual Correlogram

Date: 05/04/08 Time: 23:58

Sample: 1963Q1 2005Q4

Included observations: 172

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

.|*******| .|*******| 1 0.920 0.920 148.26 0.000

.|****** | ****|. | 2 0.774 -0.479 253.68 0.000

.|***** | *|. | 3 0.599 -0.116 317.19 0.000

.|*** | .|. | 4 0.429 0.016 349.90 0.000

.|** | *|. | 5 0.271 -0.074 363.09 0.000

.|* | *|. | 6 0.124 -0.125 365.86 0.000

.|. | .|. | 7 -0.009 -0.051 365.88 0.000

*|. | .|. | 8 -0.123 -0.033 368.63 0.000

**|. | *|. | 9 -0.226 -0.152 378.01 0.000

***|. | *|. | 10 -0.320 -0.111 396.97 0.000

***|. | **|. | 11 -0.419 -0.221 429.67 0.000

****|. | .|. | 12 -0.504 -0.013 477.09 0.000

****|. | .|. | 13 -0.559 -0.024 535.98 0.000

24

Fig 3.7: Quadratic Trend Residual Plot (Morocco)

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

0

1

2

3

1998 1999 2000 2001 2002 2003 2004 2005

Residual Actual Fitted

Fig 3.8: Quadratic Trend Regression, Residual Correlogram (Morocco)

Date: 05/06/08 Time: 01:31

Sample: 1998Q1 2005Q4

Included observations: 32

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

. |***** | . |***** | 1 0.693 0.693 16.871 0.000

. |**. | ****| . | 2 0.224 -0.493 18.699 0.000

. *| . | . |* . | 3 -0.069 0.103 18.878 0.000

.**| . | .**| . | 4 -0.241 -0.264 21.140 0.000

.**| . | . | . | 5 -0.308 0.010 24.965 0.000

25

Fig 3.9: Quadratic Trend Residual Plot

-8

-4

0

4

8

-8

-4

0

4

8

92 93 94 95 96 97 98 99 00 01 02 03 04 05

Residual Actual Fitted

Fig 3.10: Quadratic Trend Regression, Residual Correlogram

Date: 05/06/08 Time: 03:10

Sample: 1992Q1 2005Q4

Included observations: 56

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

. |**** | . |**** | 1 0.532 0.532 16.734 0.000

. |*. | .*| . | 2 0.165 -0.165 18.370 0.000

. | . | . | . | 3 0.044 0.043 18.490 0.000

. | . | . | . | 4 0.009 -0.014 18.495 0.001

. | . | . | . | 5 0.002 0.005 18.496 0.002

. | . | . | . | 6 -0.000 -0.002 18.496 0.005

. | . | . | . | 7 0.043 0.064 18.619 0.009

. | . | .*| . | 8 0.013 -0.061 18.630 0.017

.*| . | .*| . | 9 -0.064 -0.066 18.911 0.026

**| . | .*| . | 10 -0.197 -0.178 21.661 0.017

**| . | . | . | 11 -0.211 -0.018 24.862 0.010

.*| . | . | . | 12 -0.153 -0.035 26.601 0.009

.*| . | . | . | 13 -0.059 0.048 26.866 0.013

26

Modeling Seasonality

In order to test for seasonality, the author generated four dummy variables for the quarters in a year and

performed a regression using both the linear trend and seasonal dummies in the case of South Africa and

quadratic trend and seasonal dummies in the case of Morocco and Nigeria.

The results of the regression on seasonal dummies for South Afirca, Moroco and Nigeria are shown in

Tables 3.14, 3.15 and 3.16 respectively. The seasonal dummy model is

4

Yt = i Dit + t i=1

Table 3.14: Seasonal Dummy Variable Model (South Africa)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/05/08 Time: 00:38

Sample: 1963Q1 2005Q4

Included observations: 172

Variable Coefficient Std. Error t-Statistic Prob.

D1 1.811237 0.370623 4.887012 0.0000

D2 1.975157 0.370623 5.329295 0.0000

D3 1.876001 0.370623 5.061756 0.0000

D4 1.938377 0.370623 5.230057 0.0000

R-squared 0.000675 Mean dependent var 1.900193

Adjusted R-squared -0.017171 S.D. dependent var 2.409735

S.E. of regression 2.430335 Akaike info criterion 4.636916

Sum squared resid 992.2965 Schwarz criterion 4.710114

Log likelihood -394.7748 Durbin-Watson stat 0.147940

27

Table 3.15: Seasonal Dummy Variable Model (Morocco)

Table 3.16: Seasonal Dummy Variable Model (Nigeria)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 03:13

Sample: 1992Q1 2005Q4

Included observations: 56

Variable Coefficient Std. Error t-Statistic Prob.

D1 1.697393 0.703108 2.414127 0.0193

D2 1.585945 0.703108 2.255619 0.0283

D3 0.613574 0.703108 0.872658 0.3869

D4 1.176188 0.703108 1.672840 0.1004

R-squared 0.027325 Mean dependent var 1.268275

Adjusted R-squared -0.028791 S.D. dependent var 2.593718

S.E. of regression 2.630791 Akaike info criterion 4.841195

Sum squared resid 359.8952 Schwarz criterion 4.985863

Log likelihood -131.5535 Durbin-Watson stat 0.545425

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 01:36

Sample: 1998Q1 2005Q4

Included observations: 32

Variable Coefficient Std. Error t-Statistic Prob.

D1 1.974584 0.215272 9.172499 0.0000

D2 1.917082 0.215272 8.905389 0.0000

D3 1.793750 0.215272 8.332475 0.0000

D4 1.808333 0.215272 8.400215 0.0000

R-squared 0.017211 Mean dependent var 1.873437

Adjusted R-squared -0.088087 S.D. dependent var 0.583715

S.E. of regression 0.608882 Akaike info criterion 1.962083

Sum squared resid 10.38063 Schwarz criterion 2.145300

Log likelihood -27.39333 Durbin-Watson stat 0.351156

28

The dummies account for less than 1 percent of the variation in the yield spread for the three countries. As

a result, the author considered the linear trend model and the dummies below for South Africa and the

quadratic trend model and dummies below for Morocco and South Africa.

Yt = o + 1Timet + i Dit + t South Africa

Yt = o + 1Timet + 2Timet2 + i Dit + t Morocco and Nigeria

i=1

Table 3.17: Shows the Linear Trend and Seasonal Dummy Variable Regression Results (South Africa)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/05/08 Time: 00:44

Sample: 1963Q1 2005Q4

Included observations: 172

Variable Coefficient Std. Error t-Statistic Prob.

TIME -0.011176 0.003643 -3.067731 0.0025

D1 2.750030 0.473774 5.804524 0.0000

D2 2.925126 0.476135 6.143482 0.0000

D3 2.837146 0.478512 5.929098 0.0000

D4 2.910699 0.480906 6.052537 0.0000

R-squared 0.053985 Mean dependent var 1.900193

Adjusted R-squared 0.031326 S.D. dependent var 2.409735

S.E. of regression 2.371690 Akaike info criterion 4.593722

Sum squared resid 939.3606 Schwarz criterion 4.685219

Log likelihood -390.0601 Durbin-Watson stat 0.156185

29

Table 3.18: Shows the Quadratic Trend and Seasonal Dummy Variable Regression Results (Morocco)

Table 3.19: Shows the Quadratic Trend and Seasonal Dummy Variable Regression Results (Nigeria)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 01:38

Sample: 1998Q1 2005Q4

Included observations: 32

Variable Coefficient Std. Error t-Statistic Prob.

TIME 0.111948 0.038035 2.943313 0.0068

TIME^2 -0.002671 0.001185 -2.253588 0.0329

D1 1.155124 0.291318 3.965169 0.0005

D2 1.063127 0.297569 3.572709 0.0014

D3 0.910640 0.302575 3.009637 0.0057

D4 0.901410 0.306396 2.941973 0.0068

R-squared 0.358772 Mean dependent var 1.873437

Adjusted R-squared 0.235459 S.D. dependent var 0.583715

S.E. of regression 0.510389 Akaike info criterion 1.660074

Sum squared resid 6.772923 Schwarz criterion 1.934899

Log likelihood -20.56118 Durbin-Watson stat 0.535745

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 03:15

Sample: 1992Q1 2005Q4

Included observations: 56

Variable Coefficient Std. Error t-Statistic Prob.

TIME 0.367195 0.069042 5.318423 0.0000

TIME^2 -0.006642 0.001214 -5.471797 0.0000

D1 -1.632462 0.943469 -1.730276 0.0897

D2 -1.759062 0.953645 -1.844568 0.0710

D3 -2.733301 0.962518 -2.839738 0.0065

D4 -2.159269 0.970127 -2.225759 0.0306

R-squared 0.391712 Mean dependent var 1.268275

Adjusted R-squared 0.330883 S.D. dependent var 2.593718

S.E. of regression 2.121650 Akaike info criterion 4.443223

Sum squared resid 225.0700 Schwarz criterion 4.660225

Log likelihood -118.4102 Durbin-Watson stat 0.867988

30

From the foregoing results, the inclusion of the dummy variables provides little or no explanation for the

variation in the yield spread at least in the case of South Africa. The author therefore excludes the dummy

variables from the forecast model for South Africa but includes the dummy variables in the forecast

models for Morocco and Nigeria.

Incorporating the ARMA Model

AR (p) model

yt = c + 1yt-1 + 2yt-2 + …….. + pyt-p + t

MA (q) model

yt = + t + 1 t-1 + 2 t-2 + ………. + q t-q

Tables 3.20 to 3.26 provide the AIC and SIC estimates for various AR and MA processes.

Table 3.20: AIC Values, ARMA Models (South Africa)

MA Order

0 1 2 3 4

0 3.836832 3.213445 2.847858 2.666828

AR Order 1 2.696736 2.535904 2.478719 2.481130 2.492796

2 2.473483 2.479649 2.486647 2.498621 2.476628

3 2.484050 2.462456 2.474071 2.484896 2.495511

4 2.496814 2.477522 2.486658 2.511902 2.507652

Table 3.21: SIC Values, ARMA Models (South Africa)

MA Order

0 1 2 3 4

0 3.873431 3.268343 2.921056 2.758325

AR Order 1 2.733481 2.591021 2.552208 2.572992 2.603030

2 2.528821 2.553432 2.578876 2.609296 2.605750

3 2.558131 2.555057 2.585191 2.614537 2.643672

4 2.589789 2.589092 2.616823 2.660663 2.675007

31

Table 3.22: AIC Values, ARMA Models (Morocco)

MA Order

0 1 2 3 4

0 4.107412 4.096161 4.127168 4.161448

AR Order 1 4.102316 4.108774 3.975994 4.101645 4.125594

2 4.125950 3.986706 3.976569 3.991413 3.906611

3 4.172017 4.018662 4.131278 4.082619 4.123159

4 4.231887 4.038840 4.002267 4.061713 3.984842

Table 3.23: SIC Values, ARMA Models (Morocco)

MA Order

0 1 2 3 4

0 4.360581 4.385497 4.452671 4.523118

AR Order 1 4.357795 4.400750 4.304467 4.466615 4.527061

2 4.420615 4.318203 4.344900 4.396576 4.348607

3 4.506595 4.390415 4.540207 4.528722 4.606439

4 4.607126 4.451603 4.452554 4.549524 4.510177

Table 3.24: AIC Values, ARMA Models (Nigeria)

MA Order

0 1 2 3 4

0 4.107412 4.096161 4.127168 4.161448

AR Order 1 4.102316 4.108774 3.975994 4.101645 4.125594

2 4.125950 3.986706 3.976569 3.991413 3.906611

3 4.172017 4.018662 4.131278 4.082619 4.123159

4 4.231887 4.038840 4.002267 4.061713 3.984842

Table 3.25: SIC Values, ARMA Models (Nigeria)

MA Order

0 1 2 3 4

0 4.360581 4.385497 4.452671 4.523118

AR Order 1 4.357795 4.400750 4.304467 4.466615 4.527061

2 4.420615 4.318203 4.344900 4.396576 4.348607

3 4.506595 4.390415 4.540207 4.528722 4.606439

4 4.607126 4.451603 4.452554 4.549524 4.510177

32

Based on the results from the AIC and SIC, we select the ARMA (2, 0) for South Africa; ARMA (3, 2)

for Morocco and ARMA (1, 2) for Nigeria.

This suggests that the best model to regress yield spread is the ARMA (2, 0) model inclusive of the linear

trend but excluding the seasonal dummies for South Africa; ARMA (3, 2) and ARMA (1, 2) model

inclusive of the quadratic trend and seasonal dummies for Morocco and Nigeria respectively.

As such, the new model adopted is:

Yt = o + 1Timet + 2yt-2 + t South Africa i=1

Yt = o + 1Timet + 2Timet2 + i Dit + 2yt-2 + t Morocco and Nigeria

i=1

Table 3.26: Linear Trend Regression and ARMA (2, 0) Disturbances (South Africa)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/05/08 Time: 05:22

Sample (adjusted): 1963Q3 2005Q4

Included observations: 170 after adjustments

Convergence achieved after 4 iterations

Variable Coefficient Std. Error t-Statistic Prob.

TIME 0.012936 0.007089 1.824890 0.0698

AR(1) 1.375742 0.068624 20.04747 0.0000

AR(2) -0.461797 0.068463 -6.745181 0.0000

R-squared 0.885042 Mean dependent var 1.890489

Adjusted R-squared 0.883665 S.D. dependent var 2.422260

S.E. of regression 0.826181 Akaike info criterion 2.473483

Sum squared resid 113.9900 Schwarz criterion 2.528821

Log likelihood -207.2461 Durbin-Watson stat 2.074602

Inverted AR Roots .79 .58

33

Table 3.27: Quadratic Trend Regression, Seasonal Dummies and ARMA (3, 2) Disturbances (Morocco)

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 02:14

Sample (adjusted): 1998Q4 2005Q4

Included observations: 29 after adjustments

Convergence achieved after 108 iterations

Backcast: OFF (Roots of MA process too large)

Variable Coefficient Std. Error t-Statistic Prob.

TIME 0.226916 0.068170 3.328678 0.0037

TIME^2 -0.005621 0.001904 -2.951913 0.0085

D1 0.207156 0.525318 0.394343 0.6980

D2 0.116748 0.545711 0.213937 0.8330

D3 -0.099565 0.552776 -0.180118 0.8591

D4 0.001071 0.536030 0.001999 0.9984

AR(1) 0.940373 0.233439 4.028352 0.0008

AR(2) -0.070506 0.354592 -0.198838 0.8446

AR(3) -0.240043 0.231763 -1.035722 0.3140

MA(1) -0.099211 0.613869 -0.161617 0.8734

MA(2) -2.035910 0.656769 -3.099885 0.0062

R-squared 0.964129 Mean dependent var 1.897816

Adjusted R-squared 0.944201 S.D. dependent var 0.608116

S.E. of regression 0.143649 Akaike info criterion -0.761197

Sum squared resid 0.371428 Schwarz criterion -0.242568

Log likelihood 22.03736 Durbin-Watson stat 2.197198

Inverted AR Roots .67-.39i .67+.39i -.40

Inverted MA Roots 1.48 -1.38

Estimated MA process is noninvertible

34

Table 3.28: Quadratic Trend Regression, Seasonal Dummies and ARMA (1, 2) Disturbances (Nigeria)

Table 3.26 shows the regression results from the linear trend and ARMA (2, 0) model. Each of the

coefficients is significant. R2 for the model is now 88.37 percent. The Durbin-Watson statistic is now very

acceptable and the standard error of the regression is now reduced to 0.8262.

Table 3.27 shows the regression results from the quadratic trend and ARMA (3, 2) model. In spite of the

fact that some of the coefficients are insignificant, the R2

for the model is now 96 percent. The Durbin-

Watson statistic is now very acceptable and the standard error of the regression is now reduced to 0.1436.

Dependent Variable: SPREAD

Method: Least Squares

Date: 05/06/08 Time: 04:09

Sample (adjusted): 1992Q2 2005Q4

Included observations: 55 after adjustments

Convergence achieved after 20 iterations

Backcast: 1991Q4 1992Q1

Variable Coefficient Std. Error t-Statistic Prob.

TIME 0.791903 0.204280 3.876562 0.0003

TIME^2 -0.012240 0.002623 -4.665945 0.0000

D1 -8.977489 3.965062 -2.264148 0.0283

D2 -9.143115 4.000570 -2.285453 0.0269

D3 -10.05746 3.972891 -2.531523 0.0148

D4 -9.410579 3.927692 -2.395956 0.0207

AR(1) 0.850948 0.063813 13.33502 0.0000

MA(1) -0.441986 0.124828 -3.540754 0.0009

MA(2) -0.553947 0.127364 -4.349324 0.0001

R-squared 0.664313 Mean dependent var 1.289516

Adjusted R-squared 0.605933 S.D. dependent var 2.612704

S.E. of regression 1.640118 Akaike info criterion 3.975994

Sum squared resid 123.7394 Schwarz criterion 4.304467

Log likelihood -100.3398 Durbin-Watson stat 1.882480

Inverted AR Roots .85

Inverted MA Roots 1.00 -.56

35

Table 3.28 shows the regression results from the Linear Trend and ARMA (1, 2) model. Each of the

coefficients, except for the linear trend coefficients is significant. Even though the linear trend coefficient

is now insignificant, the adjusted R2

for the model is now 88.37 percent. The Durbin-Watson statistic is

now very acceptable and the standard error of the regression is now reduced to 0.8262.

Figures 3.11, 3.13 and 3.15 shows the residual plots for the selected models for South Africa, Morocco

and Nigeria, which looks like white noise and this is also confirmed by the residual correlograms (figures

3.12, 3.14 and 3.16). The sample autocorrelations and partial autocorrelations show no more patterns and

are mostly within the standard error bounds. Each of the Q-stats is insignificant thereby providing

evidence that white noise does exist. As such, the model is able to capture the elements explaining the

variation in the yield spread.

Fig 3.11: Linear Trend Regression and ARMA (2, 0) Residual Plot

-4

-2

0

2

4

-8

-4

0

4

8

1965 1970 1975 1980 1985 1990 1995 2000 2005

Residual Actual Fitted

36

Fig 3.12: Linear Trend Regression and ARMA (2, 0), Residual Correlogram

Date: 05/05/08 Time: 06:32

Sample: 1963Q3 2005Q4

Included observations: 170 Q-statistic

probabilities adjusted for 2 ARMA

term(s)

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

.|. | .|. | 1 -0.043 -0.043 0.3169

.|* | .|* | 2 0.081 0.079 1.4477

.|. | .|. | 3 -0.048 -0.042 1.8538 0.173

.|. | .|. | 4 -0.020 -0.030 1.9249 0.382

.|. | .|. | 5 0.038 0.044 2.1795 0.536

.|. | .|. | 6 0.017 0.022 2.2300 0.694

*|. | *|. | 7 -0.078 -0.086 3.3172 0.651

.|. | .|. | 8 0.048 0.043 3.7245 0.714

*|. | *|. | 9 -0.103 -0.084 5.6338 0.583

.|* | .|* | 10 0.146 0.128 9.5331 0.299

.|. | .|. | 11 -0.048 -0.029 9.9597 0.354

*|. | *|. | 12 -0.077 -0.104 11.050 0.354

*|. | *|. | 13 -0.142 -0.140 14.794 0.192

37

Fig 3.13: Quadratic Trend, Seasonality and ARMA (3, 2) Regression Residual Plot (Morocco)

-.4

-.3

-.2

-.1

.0

.1

.2

0

1

2

3

1999 2000 2001 2002 2003 2004 2005

Residual Actual Fitted

Fig 3.14: Quadratic Trend, Seasonality and ARMA (3, 2) Regression, Residual Correlogram (Morocco)

Date: 05/06/08 Time: 02:16

Sample: 1998Q4 2005Q4

Included observations: 29 Q-statistic

probabilities adjusted for 5 ARMA

term(s)

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

. *| . | . *| . | 1 -0.132 -0.132 0.5622

.**| . | .**| . | 2 -0.265 -0.288 2.9062

. *| . | . *| . | 3 -0.083 -0.184 3.1432

. *| . | .**| . | 4 -0.074 -0.232 3.3412

. |* . | . *| . | 5 0.078 -0.082 3.5716

38

Fig 3.15: Quadratic Trend, Seasonality and ARMA (1, 2) Regression Residual Plot (Nigeria)

-4

-2

0

2

4

6

-8

-4

0

4

8

92 93 94 95 96 97 98 99 00 01 02 03 04 05

Residual Actual Fitted

Fig 3.16: Quadratic Trend, Seasonality and ARMA (1, 2) Regression, Residual Correlogram (Nigeria)

Date: 05/06/08 Time: 04:16

Sample: 1992Q2 2005Q4

Included observations: 55 Q-statistic

probabilities adjusted for 3 ARMA

term(s)

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

. | . | . | . | 1 0.045 0.045 0.1186

. |*. | . |*. | 2 0.088 0.086 0.5769

.*| . | .*| . | 3 -0.136 -0.145 1.6942

.*| . | .*| . | 4 -0.088 -0.085 2.1702 0.141

.*| . | .*| . | 5 -0.109 -0.078 2.9142 0.233

.*| . | .*| . | 6 -0.079 -0.078 3.3096 0.346

. | . | . | . | 7 -0.032 -0.035 3.3757 0.497

. | . | . | . | 8 -0.011 -0.029 3.3832 0.641

. | . | .*| . | 9 -0.037 -0.071 3.4759 0.747

.*| . | .*| . | 10 -0.118 -0.151 4.4484 0.727

. | . | . | . | 11 -0.030 -0.047 4.5146 0.808

.*| . | .*| . | 12 -0.092 -0.112 5.1250 0.823

. |*. | . | . | 13 0.092 0.042 5.7546 0.835

39

The selected models for the respective countries in the earlier pages prove adequate to forecast the yield

spread. Figures 3.17, 3.18 and 3.19 show the history of the yield spread and the four quarters-ahead

forecast. It is apparent that the model forecasts well and adequately picks up all relevant elements in the

series as the realization fits within the confidence intervals shown by the lower and upper limits.

Fig 3.17: 4-Quarters Forecast (South Africa)

-3

-2

-1

0

1

2

3

4

5

6

2006Q1 2006Q2 2006Q3 2006Q4

SPREADF

Forecast: SPREADF

Actual: SPREAD

Forecast sample: 2006Q1 2006Q4

Included observations: 4

Root Mean Squared Error 0.865454

Mean Absolute Error 0.597711

Mean Abs. Percent Error 185.0955

Theil Inequality Coefficient 0.434289

Bias Proportion 0.476973

Variance Proportion 0.164668

Covariance Proportion 0.358359

40

Fig 3.18: History and 4-Quarters-Ahead Forecast

-4

-2

0

2

4

6

2002 2003 2004 2005 2006

FORECASTHISTORYLOWER

UPPERACTUAL

41

Fig 3.19: 4-Quarters Forecast (Morocco)

-1

0

1

2

3

4

2001 2002 2003 2004 2005 2006

SPREADF

Forecast: SPREADF

Actual: SPREAD

Forecast sample: 2001Q1 2006Q4

Included observations: 24

Root Mean Squared Error 0.477077

Mean Absolute Error 0.292781

Mean Abs. Percent Error 61.45160

Theil Inequality Coefficient 0.117914

Bias Proportion 0.094263

Variance Proportion 0.663533

Covariance Proportion 0.242204

42

Fig 3.20: History and 4-Quarters-Ahead Forecast (Morocco)

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

2002 2003 2004 2005 2006

ACTUALHISTORYLOWER

UPPERFORECAST

43

Fig 3.21: 4-Quarters Forecast (Nigeria)

-10

-8

-6

-4

-2

0

2

2006Q1 2006Q2 2006Q3 2006Q4

SPREADF

Forecast: SPREADF

Actual: SPREAD

Forecast sample: 2006Q1 2006Q4

Included observations: 4

Root Mean Squared Error 4.766529

Mean Absolute Error 4.211038

Mean Abs. Percent Error 453.0544

Theil Inequality Coefficient 0.623990

Bias Proportion 0.780502

Variance Proportion 0.186027

Covariance Proportion 0.033472

44

Fig 3.22: History and 4-Quarters-Ahead Forecast (Nigeria)

-12

-8

-4

0

4

8

2002 2003 2004 2005 2006

FORECASTACTUALUPPER

LOWERHISTORY

45

SECTION 4

SUMMARY OF RESEARCH FINDINGS, RECOMMENDATIONS

AND CONCLUSION

Summary of Research Findings

The author’s findings reveal the robustness of the yield spread and its predictive ability particularly in

South Africa where the results suggest that the yield spread as a predictive indicator of future economic

activities performs better at longer horizons.

In addition, the author’s attempt at determining the best forecasting model to explain the dynamics in the

yield spread provided a number of revelations on how the yield spread fluctuates rapidly as a result of

constantly changing economic conditions and circumstances.

Conclusion

The paper found evidence to suggest that the yield spread is a predictive indicator of future economic

activities in South Africa. Also, the paper reveals that the linear trend with ARMA (2, 0) is the best

model12

to forecast the yield spread in South Africa. In Morocco, the quadratic trend with seasonal

dummies and ARMA (3, 2) is the best model to forecast the yield spread and in Nigeria, the quadratic

trend with seasonal dummies and ARMA (1, 2) is the best model to forecast the yield spread.

12

The author has only employed trend, seasonality and ARMA regression models in this study.

46

However, a clear suggestion from the forecasting model results particularly for Morocco and Nigeria is

the possibility that there are other variables, which I have not considered in this study that may further

explain the variation in the yield spread.

This gives credence to the author’s views that several financial and non-financial variables may have a

strong influence on the yield spread. The author is also of the opinion that variables such as inflation

expectations via the consumer price index (CPI), money supply, exchange rate, monetary asset values and

consumer sentiment13

, may be very good determinants to consider in terms of their influence on the yield

spread.

While the African continent is particularly different from the United States, the continent is not entirely

insulated from the market and macroeconomic fundamentals from abroad. It is believed that the reliability

and predictive power of yield spreads in the United States has diminished significantly compared to the

past due to the following14

:

The determinants of the yield spread today are materially different from the determinants that

generated the yield spread during prior decades.

The impact of changes in international capital flows and inflation expectations have changed

considerably overtime.

Developments in the financial sector.

Reduction in the risk premiums of long term bonds caused by considerable improvement in the

fiscal balance may have distorted the predictive power of the yield spread of government bonds.

13

Consumer sentiment is presently not being measured in any of the three countries of focus 14

The listed factors were influenced by the Saito and Takeda paper. See reference section for further details.

47

In addition to the points listed above, there are arguments on the inappropriateness of using data before

1990 to measure the connection between the yield spread and future economic activities as some of the

countries in consideration particularly Morocco and Nigeria have not had a long history of accurate and

complete data collection.

Looking ahead, more work may be needed to understand how the yield spread is influenced by other

variables including the ones mentioned earlier. Further regressions on these variables and their

relationship with the yield spread may be advanced in the future.

While the author has attempted to provide interpretation for the results, the author suggests the results

should be treated with caution because of the obvious data limitations and sometimes small sample size.

As Alan Greenspan15

rightly suggested, yield curves should be interpreted carefully.

15

Source of the Greenspan quote is: Alan Greenspan, 2005. Letter to the Honorable Jim Saxson (Nov. 28).

48

References Bernanke, B. and A. Blinder 1992. “The Federal Funds Rate and the Channels of Monetary

Transmission”, American Economic Review, 82, 4, 901-921.

Bonser-Neal, Catherine and Timothy R. Morley., “Does the Yield Spread Predict Real Economic

Activity? A Multicountry Analysis,” “Federal Reserve Bank of Kansas City, Economic Review, (Third

Quarter 1997), 37-53.

Caporale, Guglielmo M. 1994. “The Term Structure as a Predictor of Real Economic Activity: Some

Empirical Evidence”, London Business School, Discussion Paper no. 4-94, February.

Dotsey, M., “The Predictive Content of the Interest Rate Term Spread for Future Economic Growth,”

“Federal Reserve Bank of Richmond, Economic Quarterly, Volume 84/3 Summer 1998.

Dueker, Michael. 1997. “Strenthening the Case for the Yield Curve as a Predictor of U.S. Recession,

“Federal Reserve Bank of St. Louis, Review, March/April, pp.41-50.

Estrella, Arturo, and Frederic Mishkin. 1995. “Predicting U.S. Recessions: Financial Varaibles as

Leading Indicators,” Federal Reserve Bank of New York, working paper no.5379, Dec.

Estrella, Arturo, and Frederic Mishkin. 1996. “Predicting U.S. Recessions: Financial Varaibles as

Leading Indicators,” Federal Reserve Bank of New York, working paper no. 9609, May.

49

Estrella, Arturo, and Gikas A. Hardouvelis. “The Term Structure as a Predictor of Real Economic

Activity,” Journal of Finance 46 (1991), 553-76.

Harvey, Campbell 1988. “The real term structure and Consumption Growth,” Journal of Financial

Economics, 22, Dec, 305-333

Haubrich, Joseph G., and Ann M. Dombrosky. 1996. “Predicting Real Growth Using the Yield Curve”,

Federal Reserve Bank of Cleveland, Economic Review, First Quarter, pp. 26-35.

Hu, Zuliu, 1993. “The Yield Curve and Real Activity,” IMF Staff Papers, 40, Dec, 781-806

Kessel, Reuben A. 1965. “The Cyclical Behavior of the Term Structure of Interest Rates,” National

Bureau of Economic Research, Occasional Paper 91.

Khomo Melvin and Aziapono Meshach. 2007. “Forecasting Recession in South Africa: A Comparison of

the Yield Curve and other Economic Indicators”. South African Journal of Economics, Volume 75.

Mehl, Arnaud, 2006. “The Yield Curve as a Predictor and Emerging Economies” European Central Bank

Working Paper Series, Paper 691.

Plosser, Charles I., and K. Geert Rouwenhorst, 1994. “International Term Structures and Real Economic

Growth”. Journal of Monetary Economics 33, Feb, 133-135.

50

Popoola, Oluwasegun, 2007. “The Yield Curve and the Economy”. Course Paper-Monetary Problems

and Policy Class, Feb, 1-5.

Saito, Yoshihito and Takeda, Yoko. 2000. “Predicting the US Real GDP Growth Using Yield Spreads of

Corporate Bonds”, Bank of Japan International Department Working Paper Series, Paper 00-J-2.

Stock, James H., and Mark W. Watson. 1989. “New Indexes of Coincident and Leading Indicators”, In

NBER Macroeconomic Annual, vol. 4, edited by Olivier Blanchard and Stanley Fischer. Cambridge,

Mass.: MIT Press, 1989.