The Pinnacle Fund - Scotiabank Pinnacle Fund Simplified Prospectus September 10, 2010 Class A, Class...

25

The Pinnacle Fund Simplified Prospectus September 10, 2010 Class A, Class I and Manager Class units Pinnacle Emerging Markets Equity Fund No securities regulatory authority has expressed an opinion about these units. It is an offence to claim otherwise. The Fund and the units it offers under this simplified prospectus are not registered with the U.S. Securities and Exchange Commission. Units of the Fund may be offered and sold in the United States only in reliance on exemptions from registration.

Transcript of The Pinnacle Fund - Scotiabank Pinnacle Fund Simplified Prospectus September 10, 2010 Class A, Class...

The Pinnacle Fund Simplified Prospectus

September 10, 2010

Class A, Class I and Manager Class units

Pinnacle Emerging Markets Equity Fund No securities regulatory authority has expressed an opinion about these units. It is an offence to claim otherwise.

The Fund and the units it offers under this simplified prospectus are not registered with the U.S. Securities and Exchange Commission. Units of the Fund may be offered and sold in the United States only in reliance on exemptions from registration.

i

Table of Contents

INTRODUCTION....................................................................................................................................................... 2 SPECIFIC INFORMATION ABOUT THE MUTUAL FUND DESCRIBED IN THIS DOCUMENT..................... 3 ABOUT THE FUND DESCRIPTION........................................................................................................................ 3

Pinnacle Emerging Markets Equity Fund ........................................................................................................... 6 WHAT IS A MUTUAL FUND AND WHAT ARE THE RISKS OF INVESTING IN A MUTUAL FUND?.......... 8 ORGANIZATION AND MANAGEMENT OF THE FUND................................................................................... 12 PURCHASES, SWITCHES AND REDEMPTIONS................................................................................................ 14

About the Classes of Units.................................................................................................................................. 14 How to Buy the Fund.......................................................................................................................................... 14 How We Calculate Net Asset Value Per Unit..................................................................................................... 14 How to Place Orders for the Fund ...................................................................................................................... 15 How to Switch the Fund ..................................................................................................................................... 15 How to Switch between Classes of the Fund...................................................................................................... 15 How to Redeem the Fund ................................................................................................................................... 15

OPTIONAL SERVICES ........................................................................................................................................... 16 Tax-Deferred Plans............................................................................................................................................. 16 Optimized Portfolios (Class A Units) ................................................................................................................. 16 Custom Portfolios (Class A Units) ..................................................................................................................... 17 Automatic Rebalancing (Class A Units)............................................................................................................. 17 Pre-Authorized Chequing Plan (Class A Units) ................................................................................................. 17 Automatic Withdrawal Plan................................................................................................................................ 17

FEES AND EXPENSES ........................................................................................................................................... 18 DEALER COMPENSATION ................................................................................................................................... 20 DEALER COMPENSATION FROM MANAGEMENT FEES ............................................................................... 21 INCOME TAX CONSIDERATIONS FOR INVESTORS ....................................................................................... 21 WHAT ARE YOUR LEGAL RIGHTS?................................................................................................................... 23

2

Introduction

In this document, the Manager, we, us, and our refer to Scotia Asset Management L.P. and ScotiaMcLeod refers to ScotiaMcLeod, a division of Scotia Capital Inc.

This simplified prospectus contains selected important information to help you make an informed decision about the Pinnacle Emerging Markets Equity Fund (the “Fund”), and to understand your rights as an investor.

Additional information about the Fund is available in the Fund’s annual information form, their most recently filed annual and interim financial statements and their most recently filed annual and interim management reports of fund performance. These documents are incorporated by reference into this simplified prospectus. This means they legally form part of this simplified prospectus just as if they were printed in it.

You can get a copy of the Fund’s annual information form, financial statements and management reports of fund performance at no cost by asking your dealer, or by calling toll free at 1-800-268-9269 (416-750-3863 in Toronto), or by email through our website at www.scotiabank.com/pinnaclefunds.

These documents and other information about the Fund are also available at www.sedar.com, or on our website at www.scotiabank.com/pinnaclefunds.

3

Specific Information About the Mutual Fund Described in This Document

The Fund is part of the Pinnacle family of mutual funds. The Fund offered for sale under this simplified prospectus offers Class A, Class I and Manager Class units.

The classes have different fees and are intended for different investors. Class A units are only available to investors who participate in the Pinnacle Program through ScotiaMcLeod advisors or as otherwise permitted by the Manager. Class I units are available only to eligible institutional investors and other qualified investors and are currently only available through Scotia Asset Management L.P. Manager Class units are available to investors who have signed a discretionary investment management agreement with Scotia Asset Management L.P. or Scotiatrust. You’ll find more information about the Classes of units on page 14.

About the Fund Description

On the following pages, you will find detailed descriptions of the Fund to help you make your investment decisions. Here is what each section of the Fund descriptions tells you.

Fund Details

This section gives you some basic information about the Fund, including what kind of Fund it is, when it was established and its eligibility for registered plans. See the Fund description on page 6 for details.

What Does the Fund Invest In?

This section includes the Fund's fundamental investment objectives and the strategies it uses in trying to achieve those objectives. Any change to the fundamental investment objectives must be approved by a majority of votes cast at a meeting of unitholders held for that reason.

Portfolio Advisor Selection and Monitoring

The Manager has retained the services of an independent investment consulting firm, NT Global Advisors, Inc. (“NTGA”), a wholly owned subsidiary of Northern Trust Corporation, to assist in the selection and monitoring of portfolio advisors (the “Portfolio Advisors”). Based on consultation with and research on prospective portfolio advisors, NTGA evaluates and recommends a group of qualified portfolio advisors who, in the opinion of NTGA, are best able to carry out the investment objectives and strategies of the Fund. Portfolio Advisors are then chosen by the Manager from this group based on each Portfolio Advisor’s specialized expertise, performance, consistency, investment philosophy or style, investment disciplines and quality of service. Each Portfolio Advisor is required to operate within the limits of the investment objectives, restrictions and any supplemental guidelines developed from time to time by the Manager.

On an ongoing basis, NTGA will monitor the performance of the Portfolio Advisors and report to us.

4

About Derivatives

What is a derivative? It is a contract between two parties whose value is based on, or derived from, an underlying asset, such as a stock, a market index such as the S&P/TSX Composite Index or the securities of another mutual fund. It is not a direct investment in the underlying asset itself. Examples of derivatives are options and forward contracts.

• Options generally give holders the right, but not the obligation, to buy or sell an asset such as a security or currency at a set price and at a set time. Option holders normally pay the other party a cash payment, called a premium, for agreeing to give them the option.

• Forward contracts are agreements to buy or sell an asset, such as a security or currency, at a set price and at a set time. The parties have to complete the deal, or sometimes make or receive a cash payment, even if the price has changed by the time the deal closes.

Generally, derivative investments can be designed to create an obligation on either contractual party to deliver cash or securities on the occurrence of a specific future event. Canadian securities laws prohibit the Fund from investing in derivatives (other than where the derivative is for hedging purposes) unless the Fund retains sufficient cash or cash equivalents to cover the exposure created by the derivative investment. As a result, it is not possible for the Fund to leverage its investment in derivatives. The Fund must maintain sufficient cash or highly liquid cash equivalents such as treasury bills or bankers acceptances to cover its obligations under the derivative instruments.

There may be a number of reasons why the Fund may use derivatives. Derivatives can:

• be structured to protect an investor if a particular asset denominated in a foreign currency declines in value (called “hedging”)

• reduce transaction costs

• provide more effective exposure to foreign markets than direct investments.

About Securities Lending

The Fund may enter into securities lending transactions to generate additional income from securities held in the Fund's portfolio. A mutual fund may lend securities held in its portfolio to qualified borrowers who provide adequate collateral. For a description of the strategies the Fund uses to minimize the risks associated with these transactions, see ‘Securities Lending Risk’ under ‘What are the risks of investing in a mutual fund?’.

About Repurchase and Reverse Repurchase Transactions

The Fund may enter into repurchase or reverse repurchase agreements to generate additional income from securities held in the Fund’s portfolio. When a mutual fund simultaneously agrees to sell a security at one price and buy it back on a specified date at a lower price, it is entering into a repurchase transaction. When a mutual fund simultaneously agrees to buy a security at one price and sell it back on a specified later date at a higher price, it is entering into a reverse repurchase

5

transaction. For a description of the strategies the Fund uses to minimize the risks associated with these transactions, see ‘Repurchase and Reverse Repurchase Transaction Risk’ under 'What are the risks of investing in a mutual fund?'.

About Purchasing Debt from Related Parties

The Fund may purchase or sell non-government and government debt securities in the secondary market from, or to, Scotia Capital Inc. or one of our affiliates. The Fund may only do so in reliance upon an exemption from the Canadian Securities Administrators and provided that such transactions are done in accordance with certain conditions.

What are the Risks of Investing in the Fund?

This section shows the specific risks associated with the Fund. For an explanation of these risks, see ‘What are the risks of investing in a mutual fund?’.

Who Should Invest in this Fund?

This section tells you the type of portfolio or investor the Fund may be suitable for. This is meant as a general guide only. For advice about your portfolio, you should consult your dealer or advisor.

Distribution Policy

This section tells you when the Fund usually distributes any income and capital gains to unitholders. The Fund may also make distributions at other times. Each class of units will share distributions. See ‘Income Tax Considerations for Investors’ for more information about how distributions are taxed.

Fund Expenses Indirectly Borne by Investors

As the Fund is new, fund expense information is not available. See ‘Fees and Expenses’ for more information about the costs of investing in the Fund.

6

Pinnacle Emerging Markets Equity Fund Fund Details

Type of Fund Emerging Markets Equity Fund Date Established September 8, 2010 Type of Securities Class A: September 8, 2010

Class I: September 8, 2010 Manager Class: September 8, 2010

Eligible for Registered Plans?

Yes

Portfolio Advisor Trilogy Global Advisors, LLC New York, New York

What does the Fund invest in?

Investment Objectives

The Fund’s objective is to achieve long term returns through capital growth by investing primarily in equity and equity-related securities of companies located in emerging markets and emerging industries of any market.

Any change to the investment objectives must be approved by a majority of votes cast at a meeting of unitholders held for that purpose.

Investment Strategies

The Fund uses a growth-oriented investment style to achieve its investment objectives.

The portfolio advisor analyzes the global economy and the economies and industries of various emerging markets. Based on this analysis, it identifies the countries and then the companies that it believes offer the potential for growth. The portfolio advisor uses techniques such as fundamental analysis to assess growth potential. This means evaluating the financial condition and management of a company, its industry and the overall economy through due diligence, including meetings with companies' management, financial statement analysis and modeling. The portfolio advisor also focuses on the upside potential versus the downside risk of each security.

The Fund may temporarily hold cash or fixed income securities for strategic reasons.

The Fund may use derivatives for foreign currency hedging purposes and to provide more effective exposure while reducing transaction costs.

The Fund may participate in securities lending, repurchase and reverse repurchase transactions to achieve its investment objectives and to enhance returns. You’ll find more information on securities lending, repurchase and reverse repurchase transactions and how the Fund limits the risks associated with them under ‘What are the risks of investing in a mutual fund?’.

Pinnacle Emerging Markets Equity Fund

7

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greater price fluctuations than would be expected of a money market or bond funds.

See ‘What are the risks of investing in a mutual fund? — General Investment Risk, Class Risk, Derivatives Risk, Emerging Markets Risk, Foreign Exchange Risk, Foreign Securities Risk, Interest Rate Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk and Significant Unitholder Risk’.

Who should invest in this Fund?

This Fund may be suitable for you if:

• You're seeking exposure to emerging market equities

• you’re investing for at least five years

• you can accept moderate to high risk.

Distribution Policy

The Fund will distribute sufficient net income and net taxable capital gains in the year they are earned to ensure that the Fund does not have to pay ordinary income tax. Distributions on units are reinvested in additional units of the Fund unless you tell us in writing that you want to receive cash distributions.

Income Distributions Annually in December of each year

Capital Gains Distributions Annually in December of each year

Fund expenses indirectly borne by investors Fund expense information is not available because the Fund is new.

8

What is a Mutual Fund and What are the Risks of Investing in a Mutual Fund?

What is a mutual fund?

A mutual fund is a pool of money contributed by people with similar investment objectives. A professional investment advisor — called a Portfolio Advisor — takes that large pool of cash and invests it for the whole group. These investments could be shares, bonds, money market instruments or a combination of these. When you invest in a mutual fund, you receive units of the mutual fund. Unitholders share the mutual fund’s income, expenses, and any gains and losses from the mutual fund’s investments, generally in proportion to the units they own. The price of a unit, also described as the net asset value of the unit, changes every day, depending on how well the investments are performing.

Mutual funds may issue one or more classes of units which may be purchased by investors. The Fund offers Class A, Class I and Manager Class units.

When the investments rise in value, the price of a unit goes up. When the investments drop in value, the price of a unit goes down. The value of an investment in a mutual fund is realized by redeeming the units held. You make money on mutual funds if you buy your units at one price and sell them later at a higher price. Of course, you lose money if you sell your units for less than you paid. You can also make money when the mutual fund pays you your share of the income and capital gains it has earned on its investments. This is called a distribution.

Your investment in a mutual fund is not guaranteed. Unlike bank accounts or guaranteed investment certificates, units of a mutual fund are not covered by Canada Deposit Insurance Corporation (CDIC) or any other government deposit insurer is not guaranteed by The Bank of Nova Scotia (“Scotiabank”), Montreal Trust or National Trust Company.

WHAT ARE THE RISKS OF INVESTING IN A MUTUAL FUND?

There are many factors that can affect the value of a mutual fund investment. The most common ones are:

General Investment Risk

Different kinds of securities held in a mutual fund carry varying amounts of risk. The value of those securities may fluctuate from day to day in response to changes in interest rates, economic conditions and market and company news. This means that the units of the Fund held by an investor may be worth more or less than their original purchase price.

If the price of a mutual fund declines from the price at which units were purchased and units are subsequently sold, the investor will lose money. History has shown that the longer a mutual fund investment is held, the greater the chance that the value of the investment will increase above the original purchase price.

9

Class Risk

Some mutual funds offer two or more classes of units of the same fund. Although the value of each class is calculated separately, there’s a risk that the expenses or liabilities of one class of units may affect the value of the other classes. If one class is unable to cover its liabilities, the other classes are legally responsible for covering the difference. We believe that this risk is very low.

Credit Risk

A fixed income security, such as a bond, is a promise to pay interest and repay the principal on the maturity date. There is always a risk that the issuer will fail to honour that promise. This is called credit risk. Credit risk is lowest among issuers that have a high credit rating from a credit rating agency. It is highest among issuers that have a low credit rating or no credit rating. Issuers with a low credit rating usually offer higher interest rates to make up for the higher risk.

Derivatives Risk

Some mutual funds may use derivatives, but only in ways allowed by Canadian securities regulators. While derivatives are useful investment tools, they also have the following risks:

• there is no guarantee that hedging will be effective

• some derivative instruments may lack liquidity and there is no guarantee a secondary market will exist

• investment exchange markets can impose trading limits that could prevent the carrying out of the derivative contract

• derivatives based on a stock market index could be adversely affected if trading is halted on a number of stocks in the index

• the other party to a derivative contract may not be able to honour its obligations under the contract

• money or other forms of collateral deposited with a derivatives dealer may be lost if the dealer experiences financial difficulties or goes bankrupt

• increased risks are associated with foreign derivative instruments, including less liquidity and greater credit risk.

Emerging Markets Risk

Some mutual funds may invest in foreign companies or governments (other than the U.S.) which may be located in, or operate, in developing countries. Companies in these markets may have limited product lines, markets or resources, making it difficult to measure the value of the company. Political instability, possible corruption, as well as lower standards of business regulation increase the risk of fraud and other legal issues. In addition to foreign securities risk described above, these mutual funds may be exposed to greater volatility as a result of such issues.

10

Foreign Exchange Risk

Investments in foreign securities carry the risk of fluctuations in the value of foreign currency in relation to the Canadian dollar. If a foreign currency appreciates in relation to the Canadian dollar and the mutual fund holds securities denominated in that currency, the market value of that portion of the mutual fund’s portfolio may tend to increase. The opposite is true if the foreign currency depreciates in value relative to the Canadian dollar.

A mutual fund may attempt to hedge the currency exposure of its foreign portfolio positions by using derivatives.

Foreign Securities Risk

Mutual funds that hold foreign securities can offer benefits such as increased diversification and potentially higher returns, but there are also additional risks. These are known as foreign securities risks.

Political, economic or social instability can also impact the value of foreign investments. Foreign stock exchanges may be smaller and less strictly regulated, resulting in decreased liquidity. Likewise, the rules for accounting, financial reporting and securities may not be as strict as they are in Canada, and access to information may be less readily available.

Interest Rate Risk

To the extent that a mutual fund invests in money market or fixed income securities (such as bonds), its value is affected by changes in the general level of interest rates. When interest rates fall, bond prices rise. That’s because existing bonds pay higher rates than newly issued ones, and are worth more. Conversely, when interest rates rise, bond prices fall, and so will the unit value of Fund that hold them.

The income earned by the mutual fund — and the income paid by the mutual fund to unitholders — is also affected by changes in interest rates.

Repurchase and Reverse Repurchase Transaction Risk

When a mutual fund agrees to sell a security at one price and buy it back on a specified later date from the same party with the expectation of profit, it is entering into a repurchase agreement. When a mutual fund agrees to buy a security at one price and sell it back on a specified later date to the same party with the expectation of a profit, it is entering into a reverse repurchase agreement.

Mutual funds engaging in repurchase and reverse repurchase transactions are exposed to the risk that the other party to the transaction may become insolvent and unable to complete the transaction. In those circumstances, there is a risk that the value of the securities bought may drop or the value of the securities sold may rise between the time the other party becomes insolvent and the time the Fund recovers its investment. Mutual funds that engage in these transactions reduce this risk by holding as collateral enough of the other party’s cash or securities to cover that party’s repurchase or reverse repurchase obligations.

11

To limit the risks associated with repurchase and reverse repurchase transactions, the collateral held in respect of the repurchase or reverse repurchase obligations must be marked to market on each business day and be fully collateralized at all times with acceptable collateral which has a value at least equal to 102% of the sold securities or cash paid for the securities by the mutual fund.

Prior to entering into a repurchase or reverse repurchase agreement, a mutual fund must ensure that the aggregate value of the securities of the mutual fund that have been sold pursuant to repurchase transactions, together with securities loaned, does not exceed 50% of its total asset value at the time the mutual fund enters into the transaction.

Securities Lending Risk

A mutual fund may lend securities held in its portfolio to qualified borrowers who provide adequate collateral. In lending its securities, a mutual fund is exposed to the risk that the borrower may not be able to satisfy its obligations under the securities lending agreement and the mutual fund would be forced to take possession of the collateral held. Losses could result if the collateral held by the mutual fund does not have a value, at the time the remedy is exercised, which is sufficient to replace the securities borrowed.

Mutual funds must receive collateral worth no less than 102% of the value of the loaned securities and borrowers must adjust that collateral daily to ensure this level is maintained. Prior to entering into a securities lending agreement, a mutual fund must ensure that the aggregate value of the securities loaned together with those that have been sold pursuant to repurchase transactions does not exceed 50% of its total asset value.

Significant unitholder risk

The purchase or redemption of a significant number of units of a fund may require the portfolio advisor to change the composition of the fund’s portfolio significantly or may force the portfolio advisor to buy or sell investments at unfavourable prices, which can affect the fund’s performance.

12

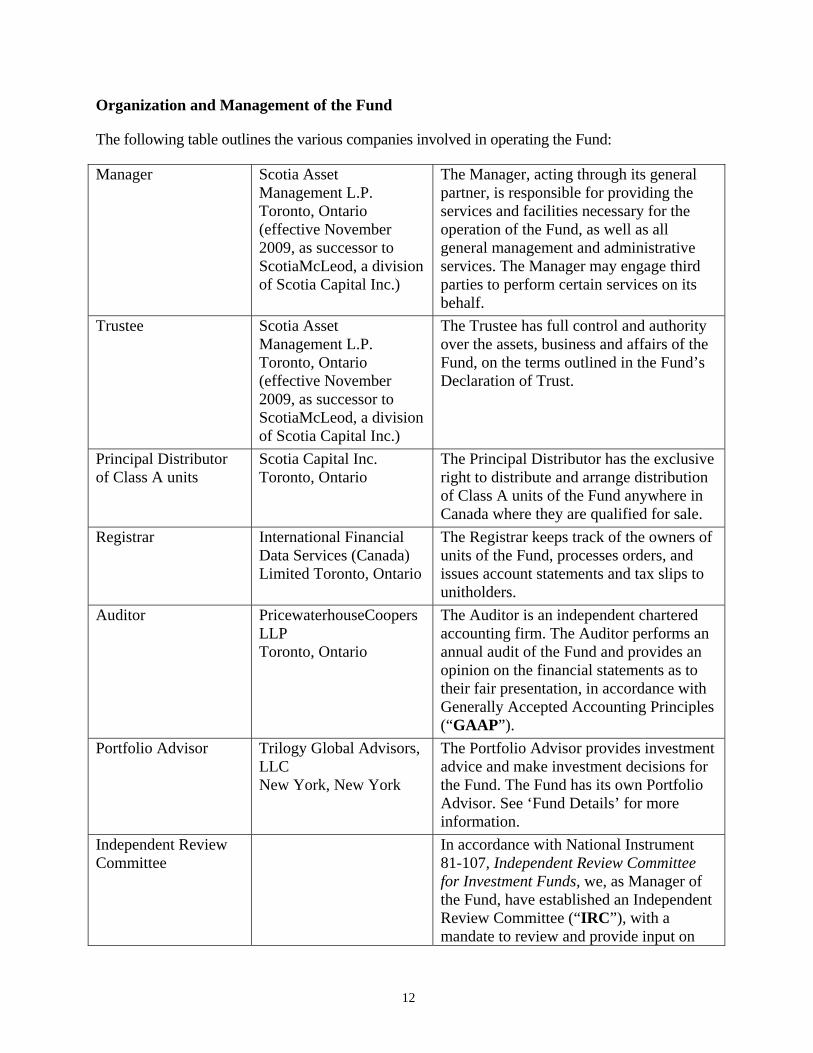

Organization and Management of the Fund

The following table outlines the various companies involved in operating the Fund:

Manager Scotia Asset Management L.P. Toronto, Ontario (effective November 2009, as successor to ScotiaMcLeod, a division of Scotia Capital Inc.)

The Manager, acting through its general partner, is responsible for providing the services and facilities necessary for the operation of the Fund, as well as all general management and administrative services. The Manager may engage third parties to perform certain services on its behalf.

Trustee Scotia Asset Management L.P. Toronto, Ontario (effective November 2009, as successor to ScotiaMcLeod, a division of Scotia Capital Inc.)

The Trustee has full control and authority over the assets, business and affairs of the Fund, on the terms outlined in the Fund’s Declaration of Trust.

Principal Distributor of Class A units

Scotia Capital Inc. Toronto, Ontario

The Principal Distributor has the exclusive right to distribute and arrange distribution of Class A units of the Fund anywhere in Canada where they are qualified for sale.

Registrar International Financial Data Services (Canada) Limited Toronto, Ontario

The Registrar keeps track of the owners of units of the Fund, processes orders, and issues account statements and tax slips to unitholders.

Auditor PricewaterhouseCoopers LLP Toronto, Ontario

The Auditor is an independent chartered accounting firm. The Auditor performs an annual audit of the Fund and provides an opinion on the financial statements as to their fair presentation, in accordance with Generally Accepted Accounting Principles (“GAAP”).

Portfolio Advisor Trilogy Global Advisors, LLC New York, New York

The Portfolio Advisor provides investment advice and make investment decisions for the Fund. The Fund has its own Portfolio Advisor. See ‘Fund Details’ for more information.

Independent Review Committee

In accordance with National Instrument 81-107, Independent Review Committee for Investment Funds, we, as Manager of the Fund, have established an Independent Review Committee (“IRC”), with a mandate to review and provide input on

13

our policies and procedures dealing with conflicts of interest in respect of the Fund, and to review conflict of interest matters that we present to the IRC. The IRC currently has three members, each of whom is independent of the Manager and any party related to the Manager. The IRC will prepare, at least annually, a report of its activities for unitholders. The current report is available at no charge on the internet at www.scotiabank.com/pinnaclefunds. Additional information about the IRC, including the names of its members, is available in the Fund’s annual information form.

In certain circumstances, your approval may not be required under securities legislation to effect a fund merger or a change in the auditor of the Fund. In these circumstances, the IRC must approve the proposal and you will receive at least 60 days written notice before the change takes effect.

The Fund has received an exemption from the Canadian Securities Administrators allowing it to purchase equity securities of a Canadian reporting issuer during the period of distribution of the securities and for the 60-day period following the period of distribution pursuant to a private placement notwithstanding that a related underwriter, such as ScotiaMcLeod, participates in offering the securities of such issuer. Any such purchase must be consistent with the investment objective of the Fund. Further, the Independent Review Committee of the Fund must approve the investment and such purchase can only be carried out if it is in compliance with certain other conditions.

Trilogy Global Advisors LLC relies on the international advisor exemption. The name and address of the agent for the service for this Portfolio Advisor is available from the Ontario Securities Commission. The Portfolio Advisor is located outside of Canada and all or a substantial portion of its assets may be situated outside of Canada, which may make it difficult for investors to enforce their legal rights against the Portfolio Advisor.

The Custodian for the Fund is The Bank of Nova Scotia, Toronto, Ontario.

The Custodian is responsible for the safekeeping of the securities and cash in the Fund's portfolio.

14

Purchases, Switches and Redemptions

About the Classes of Units The Fund is available in three classes of units: Class A units, Class I units and Manager Class units. The classes have different fees and are intended for different investors:

• Class A units are only available to investors who participate in the Pinnacle Program, through ScotiaMcLeod advisors or as otherwise permitted by the Manager.

• Class I units are available to eligible institutional investors and other qualified investors. Class I units are currently only available through Scotia Asset Management L.P. If an investor is no longer eligible to hold Class I units, the Manager may reclassify the Class I units as Class A units.

• Manager Class units are available to investors who have signed a discretionary investment management agreement with Scotia Asset Management L.P. or Scotiatrust.

How to Buy the Fund The minimum initial investment for Class A units is $1,000 and the minimum subsequent investment is $500. For Class I units, the minimum initial investment is generally $1,000,000. The minimum initial investment in Manager Class units of the Fund is generally $250,000. At the discretion of the Manager these minimums may be reduced. When the initial investment is made, your dealer will send you a confirmation that summarizes the details of the purchase. The Fund does not issue unit certificates; the Manager arranges to keep records of unit ownership.

For Class A units, if the value of the investment(s) in your account falls below $100, we may sell your units and send you the proceeds. For Class I units and Manager class units, if the value of the investment(s) in your account falls below the minimum initial investment, we may sell your units and send you the proceeds.

We will give you 30 days written notice before selling your units.

Units are non-transferable except with the written consent of the Manager for the sole purpose of granting a security interest therein.

How We Calculate Net Asset Value Per Unit Separate net asset values are calculated for each class of a Fund at the end of each day based on each class’s share of the Fund's net asset value as determined in accordance with the Fund's declaration of trust. The class net asset value per unit is calculated daily by dividing (1) the amount equal to the value of that class’s share of assets of a Fund, less that class’s share of the common expenses of the Fund and less that class’s specific expenses by (2) the total number of units of that class outstanding at such time.

The net asset value per unit is determined daily, at the close of regular trading on the Toronto Stock Exchange, normally 4:00 p.m. Toronto time. In unusual circumstances, we may suspend the calculation of the net asset value per unit of each class, subject to obtaining any necessary regulatory

15

approval. The unit price of a class usually varies day to day in response to changes in the value of the Fund's portfolio’s securities.

Units are purchased, distributions reinvested and redemptions implemented for the Fund on the basis of the class net asset value per unit applicable to the transactions.

How to Place Orders for the Fund Your request to purchase units must be received before 3:00 p.m. Toronto time in order for the purchase to be priced at the class net asset value per unit determined at 4:00 p.m. on such day. If the order is received after 3:00 p.m., units will be issued at the class net asset value calculated at 4:00 p.m. on the next business day. If the cash required to complete the transaction is not received within three trading days of receipt of the purchase order, the same number of units purchased will be redeemed. If the Fund's redemption price is less than the purchase price, your dealer will pay the difference to the Fund and collect that amount from you. If the redemption price is greater than the purchase price for the units, the Fund will keep the difference.

The Manager has the right to reject any order within one business day after it has been received. If an application is rejected, the purchase price paid by you will be refunded immediately. We may reject your order if you’ve made several purchases and sales of the Fund within a short period of time, usually 31 days.

If you purchase units of a Fund at a time when the Fund has a significant amount of undistributed income and gains, the net asset value of the Fund and therefore the purchase price paid by you for the units will reflect the amount of the undistributed income and gains. Upon the subsequent distribution by the Fund of such income and gains, you may be subject to tax on your share of the distribution, notwithstanding that the distribution may reflect part of the purchase price paid by you for the units.

How to Switch the Fund Switches are permitted from units of one Fund into units of another Fund, provided that the minimum investment requirements are met. The rules applicable to purchases and redemptions also apply to switches. If you switch units within 31 days of buying them, you may have to pay a short-term trading fee. In a non-registered account, switching may result in a capital gain or loss for tax purposes. See ‘Income Tax Considerations for Investors’.

How to Switch between Classes of the Fund

Reclassifications are permitted from one class of a Fund into another class of the same Fund if you are eligible for that class. The number of units you receive upon reclassification depends upon the relative net asset value per unit of the class of units being exchanged to the class of units being received. The rules applicable to purchases and redemption also apply to reclassifications. A reclassification from one class of a Fund to another class of the same Fund is not considered a disposition for tax purposes.

How to Redeem Units of the Fund All or some of the units held by you can be redeemed on any business day. Your request to redeem units of the Fund must be received before 3:00 p.m. Toronto time in order for the redemption to be

16

priced at the net asset value per unit determined at 4:00 p.m. on such date. If the redemption request is received after 3:00 p.m., units will be redeemed at the net asset value per unit calculated at 4:00 p.m. on the next business day.

If any documents which may be required by the Manager to complete the sale are not received within ten business days of the redemption request, the Manager will buy the same number of units sold. If the purchase price is less than the sale price of the units, the Fund will keep the difference. If the purchase price is greater than the sale price for the units, your dealer is required to pay the Fund the difference. This amount will be collected from you.

Redemption proceeds will be paid within three business days after the documents required to complete the sale are received. Upon request, the Manager will mail you a cheque for the proceeds of the sale, or will deposit the proceeds into an account designated by you, provided your cheque for the purchase of any of the units being redeemed has cleared. If you sell units within 31 days of buying them, you may have to pay a short-term trading fee. See ‘Fees and Expenses Payable by You — Short-Term Trading Fee’ for details.

Under extraordinary circumstances, the rights of investors to redeem units may be suspended by a Fund. A Fund may suspend the right to sell units if normal trading is suspended in any market where more than fifty percent of that Fund's assets are traded.

Optional Services

Tax-Deferred Plans The Fund is an eligible investment for all registered accounts.

This means you can hold units of the Fund in the following registered accounts (collectively referred to as “tax deferred plans”):

• registered retirement savings plans (“RRSPs”), including group RRSPs

• locked-in RRSPs and locked-in retirement accounts (“LIRAs”)

• registered retirement income funds (“RRIFs”)

• life income funds (“LIFs”) and life registered income funds (“LRIFs”)

• deferred profit sharing plans (“DPSPs”)

• registered pension plans (“RPPs”), including defined contribution pension plans (“DCPPs”)

• registered education savings plans (“RESPs”)

• registered disability savings plans (“RDSPs”)

• tax-free savings accounts (“TFSAs”).

Optimized Portfolios (Class A Units) You have the option of choosing from several optimized portfolios, professionally designed with the assistance of NTGA. Each of the optimized portfolios consists of various funds as well as cash and

17

cash equivalent securities. You can choose an optimized portfolio with the help of your ScotiaMcLeod advisor. You can also set the target weighting for each fund within your portfolio if you wish to use the automatic rebalancing as described below. If NTGA recommends a change in weighting in a particular optimized portfolio or a change in fund comprising the particular optimized portfolio, such change in weighting or change in the fund comprising the particular optimized portfolio will not be made unless you agree with your ScotiaMcLeod advisor to make the change.

Custom Portfolios (Class A Units) You also have the option of designing a custom portfolio with the help of your ScotiaMcLeod advisor. You can generally choose as many or as few funds as you wish to include in the custom portfolio. You can also set the target weighting for each fund within your portfolio if you wish to use the automatic rebalancing as described below.

Automatic Rebalancing (Class A Units) At your request, your optimized or custom portfolio can be automatically rebalanced to the set fund target weightings in each portfolio. The rebalancing will take place on or about the 15th day of the month following the end of each calendar quarter. The short-term trading fee doesn’t apply to rebalancing that is offered in connection with an optimized or custom portfolio.

If you hold your funds in a non-registered account, you may realize a capital gain or loss when your account is rebalanced. Capital gains are taxable.

Pre-Authorized Chequing Plan Regular investing is an effective way to build wealth. In order to facilitate regular investing, the Manager has established a Pre-Authorized Chequing Plan. Once the minimum initial investment in a fund has been made, you can authorize regular deductions from your bank account to buy units. The minimum amount per authorized deduction is $500. You can suspend this authorization at any time.

If you make a purchase under a Pre-Authorized Chequing Plan, you will receive a renewal simplified prospectus for the fund only if you request it. If you would like to receive a copy of a renewal prospectus along with any amendment, please contact us at 1-800-268-9269 (416-750-3863 in Toronto) or contact your dealer. The current simplified prospectus and any amendments may be found at www.sedar.com or at www.scotiabank.com/pinnaclefunds. Although you do not have a statutory right to withdraw from a purchase of units made under a Pre-Authorized Chequing Plan, you will continue to have a right of action for damages or rescission in the event a renewal prospectus contains a misrepresentation, whether or not you request a renewal prospectus.

Automatic Withdrawal Plan

If you have a minimum of $50,000 in your fund account, you may establish an automatic withdrawal account to provide predetermined cash payments through automatic redemption of units. You may suspend this authorization at any time. The Manager reserves the right to terminate this arrangement for accounts that fall below a market value of $25,000.

18

Fees and Expenses

This table lists the fees and expenses that you may have to pay if you invest in the Fund. You may have to pay some of these fees and expenses directly, or the Fund may have to pay some of these fees and expenses, which will therefore reduce the value of your investment in the Fund. Fees and operating expenses paid by the Fund and fees paid by the investors in the Fund are subject to applicable goods and services taxes. As a result of recent changes, including the harmonization of Ontario's and British Columbia's respective provincial sales taxes with the federal goods and services tax, effective July 1, 2010, such fees and expenses borne by a Fund and fees borne by investors in certain provinces will increase.

Fees and Expenses Payable by the Fund

Management Fees

Class A No management fees are charged by the Manager in respect of the Class A units of the Fund. If you have a Pinnacle Program Agreement with ScotiaMcLeod, you will agree to pay an asset based fee for the services offered under that Agreement. You will pay the fees on a quarterly basis and the payment can only be made through the redemption of Class A units held in the Fund, unless otherwise permitted by ScotiaMcLeod. The maximum annual fee charged is 2.5% of the value of the units held in the Fund by the investor. ScotiaMcLeod will pay the Manager up to the rate of fees it receives in respect of Class A units of the Fund. ScotiaMcLeod also reimburses the Manager for that portion of the fees of the portfolio advisors and NGTA attributable to the Class A units and may reimburse the Manager for certain other expenses. Any fee for purchases of Class A units outside the Pinnacle Program are negotiated separately with your dealer and the Manager.

Class I Fees for services of the Manager payable by Class I investors are negotiable by the investor and are payable directly to the Manager. The maximum amount will not exceed the Class A annual rate.

Manager Class In addition to any fees paid directly to Scotia Asset Management under a discretionary investment management agreement, each Fund pays us a management fee with respect to Manager Class Units for providing general management services. The fee is calculated and accrued daily and paid monthly. The maximum annual management fee for Manager Class units of the Fund is 0.70%.

Operating Expenses

Class A: The Class A units of the Fund bear their proportionate share of the common expenses relating to the operation of the Fund and the carrying on of their business, including legal and audit fees, taxes, interest, administrative costs relating to the issue and redemption of units, brokerage commissions, as well as the cost of financial and other reports

19

and complying with all applicable laws, regulations and policies. These expenses also include the annual fee paid to each IRC member, fees for each meeting he or she attends, and the reasonable expenses associated with the performance of his or her duties as an IRC member. In addition, there are class specific expenses such as the costs of holding a unitholder meeting specific to members of the class. The amount of expenses will not exceed 0.50% of the Class A net assets of the Fund. Class specific expenses such as the costs of holding a unitholder meeting specific to members of the class, brokerage commissions, interest charges and taxes of all types, including goods and services taxes are not included in the 0.50% cap on expenses. ScotiaMcLeod is responsible for reimbursing the Manager for expenses in excess of 0.50%. Class I: The Class I units of the Fund bear their proportionate share of the common expenses relating to the operation of the Fund and the carrying on of their business, including legal and audit fees, taxes, interest, administrative costs relating to the issue and redemption of units, brokerage commissions, as well as the cost of financial and other reports and complying with all applicable laws, regulations and policies. These expenses also include the annual fee paid to each IRC member, fees for each meeting he or she attends, and the reasonable expenses associated with the performance of his or her duties as an IRC member. In addition, there are class specific expenses such as the costs of holding a unitholder meeting specific to members of the class. Manager Class: The Manager Class units of the Fund bear their proportionate share of the common expenses relating to the operation of the Fund and the carrying on of their business, including legal and audit fees, taxes, interest, administrative costs relating to the issue and redemption of units, brokerage commissions, as well as the cost of financial and other reports and complying with all applicable laws, regulations and policies. These expenses also include the annual fee paid to each IRC member, fees for each meeting he or she attends, and the reasonable expenses associated with the performance of his or her duties as an IRC member. In addition, there are class specific expenses such as the costs of holding a unitholder meeting specific to members of the class. General: We may choose to absorb any of these expenses. Currently, each member of the IRC is entitled to an annual retainer of $35,000 ($47,000 for the Chair), and a per meeting fee of $1,500 for attending each IRC meeting. The Fund pays a proportionate share of the total compensation paid to the IRC each year and reimburses members of the IRC for expenses incurred by them in connection with their services as members of the IRC. The Fund’s share of the IRC’s compensation will be disclosed in the Fund’s financial statements.

20

Fees and Expenses Payable by You

Sales Charges No sales commission or other sales charge is payable for any purchase, switch or redemption of the Fund.

Short-Term Trading Fee

Short-term trading by investors can increase the Fund's expenses, which impacts all investors in the Fund, and can affect the economic interest of long-term investors. Short-term trading can affect the Fund's performance by forcing the portfolio advisor to keep more cash in the Fund than would otherwise be required. To discourage short-term trading, the Fund may charge a fee of 2% of the amount you sell or switch, if you sell or switch your units within 31 days of buying them. The fee does not apply to Class I units and may not apply to:

• automatic rebalancing that is part of the service offered by the Manager;

• transactions not exceeding a certain minimum dollar amount, as determined by the Manager from time to time;

• trade corrections or any other action initiated by the Manager or the applicable portfolio advisor;

• transfers of units of the Fund between two accounts belonging to the same unitholder; and

• regularly scheduled RIF or LIF payments.

Any formal or informal arrangements to permit short-term trading are described in the Fund’s annual information form. If securities regulations mandate the adoption of specified policies relating to short-term trading, the Fund will adopt such policies if and when implemented by the securities regulators. If required, these policies will be adopted without amendment to this simplified prospectus or the Fund’s annual information form and without notice to you, unless otherwise required by such regulations.

1 The 0.50% cap excludes class specific expenses, brokerage commissions, interest charges and taxes of all types, including goods and services taxes.

Dealer Compensation

Although ScotiaMcLeod advisors receive no up-front sales commissions in connection with the sale of Class A units of the Fund, they are compensated in connection with certain ongoing services they provide to investors in the Pinnacle Program. Currently, ScotiaMcLeod pays no more frequently than monthly, a service fee to ScotiaMcLeod advisors in an amount up to 72% of the fee paid by each Class A investor to ScotiaMcLeod.

For the sale of units of the Fund to investors outside of the Pinnacle Program, ScotiaMcLeod also pays, no more frequently than monthly, a service fee to ScotiaMcLeod advisors in an amount up to 72% of the fee paid by each Class A investor to ScotiaMcLeod.

No service fee is payable in respect of Class I units or Manager Class units.

A ScotiaMcLeod advisor may also receive sales incentives based on his or her overall performance.

21

The Manager may participate in co-operative marketing programs with dealers to help them market the Fund. We may pay up to 50% of the cost of these co-operative marketing programs in accordance with the rules set out in National Instrument 81-105 Mutual Fund Sales Practices.

The Bank of Nova Scotia owns, directly or indirectly, 100% of Scotia Asset Management L.P. and ScotiaMcLeod, a division of Scotia Capital Inc.

Dealer Compensation from Management Fees

Prior to the date of this simplified prospectus, no management fees have been payable by the Fund.

Income Tax Considerations for Investors

This section is a summary of how investing in the Fund can affect your taxes. It assumes that you’re an individual other than a trust, a Canadian resident and deal at arm’s length with the Fund and you hold your units as capital property.

More detailed information is provided in the Fund’s annual information form. Because tax laws vary by province and every investor’s situation is different, we recommend you get advice from a tax expert.

How your Investment Can Earn Money

Funds earn money in the form of income and capital gains. Income includes the interest and dividends the Fund earns on its investments and gains on certain derivatives. Capital gains are earned when the Fund sells investments for a profit.

You earn money in the form of distributions when the Fund pays you your share of the income and capital gains it has earned. In general, the Fund will distribute enough of its net income and net realized capital gains each year to unitholders so it won’t have to pay income tax.

You can also earn money in the form of a capital gain when you sell or switch your units for a profit. You can realize a capital loss if you sell or switch your units at a loss.

How Earnings are Taxed

The tax you pay depends on whether you hold your units in a tax-deferred plan or in a non-registered account.

Units Held Outside a Tax-Deferred Plan

For units of the Fund which are held outside a tax-deferred plan, you must include in your income each year the amount of distributions of income and taxable capital gains paid or payable to you in the year by the Fund, whether you receive these amounts in cash or in additional units. The higher the Fund's portfolio turnover rate, the greater the chance the Fund will make taxable distributions.

The price of a unit of the Fund may include income and/or capital gains that the Fund has earned, but not yet realized and/or distributed. If you buy units of the Fund before it makes a distribution,

22

you will be taxed on that distribution, even though the Fund earned the amount before you owned it. For example, many Funds make their only, or most significant, distribution of capital gains in December. If you buy units late in the year, you may have to pay tax on the income and capital gains the Fund earned for the whole year. That will mean that you will pay tax on Fund earnings that you had no benefit from. Distributions by the Fund that are a return of capital are not taxable but will generally reduce the adjusted cost base of your units of that Fund.

When you redeem or switch your units of the Fund to units of another fund, you may realize a capital gain or loss. Your capital gain (or loss) will be equal to the difference between the amount you receive on the redemption or switch (net of any reasonable disposition costs such as deferred sales charges) and your adjusted cost base of the units redeemed or switched. You must calculate your adjusted cost base separately for each class of units of each Fund that you own. In general, the aggregate adjusted cost base of your units equals:

• your initial investment, plus

• additional investments, plus

• reinvested distributions, minus

• any return of capital distributions, minus

• the adjusted cost base of any previous redemptions.

You should keep detailed records of the purchase cost of your investments and distributions you receive on those units so you can calculate their adjusted cost base. You may want to get advice from a tax expert.

Individuals, including certain trusts and estates, are subject to an alternative minimum tax. If you are an individual, you may be liable for this alternative minimum tax in respect of realized capital gains and/or dividends in respect of your units of the Fund.

The fees paid by unitholders to ScotiaMcLeod in respect of Class A and Class I units and to Scotia Asset Management L.P. or Scotiatrust in respect of Manager Class units may not be deductible by unitholders. Unitholders should consult their own tax advisors. Unitholders should consult their own tax advisors.

Units Held in a Tax-Deferred Plan

Where you hold your units in a tax-deferred plan, you do not pay any tax on distributions from the Fund or any capital gains realized from redeeming or switching units inside the plan. See ‘Optional Services — Tax Deferred Plans’. Withdrawals from a tax-deferred plan are generally taxable. However, withdrawals from TFSAs are not subject to tax, and RESPs and RDSPs are subject to special rules.

So long as the Fund is a mutual fund trust or registered investment for tax purposes, units of the Fund are “qualified investments” for RRSPs, RRIFs, RESPs, DPSPs, RDSPs and TFSAs.

23

What are Your Legal Rights?

Securities legislation in certain provinces gives you the right to withdraw from an agreement to purchase mutual fund securities within two business days of receiving a simplified prospectus, or within forty-eight hours after receiving confirmation of your purchase. If the agreement is to purchase such securities under a contractual plan, the time period during which withdrawal may be made may be longer.

In several of the provinces and territories, securities legislation also allows you to cancel an agreement to buy units and get your money back, or in some cases to make a claim for damages if the simplified prospectus, annual information form or financial statements (including any amendments) contain a misrepresentation. These rights must usually be exercised within certain time limits. You should refer to any applicable provisions of the securities legislation of your province or territory for the particulars of these rights or consult with a legal advisor.

24

The Pinnacle Fund Class A units, Class I units and Manager Class units

Pinnacle Emerging Markets Equity Fund

Managed by:

Scotia Asset Management L.P. Scotia Plaza 52nd Floor 40 King Street West Toronto, Ontario M5H 1H1 Toll Free: 1-800-268-9269 (416-750-3863 in Toronto)

Additional information about the Fund is available in the Fund’s annual information form, their most recently filed annual and interim management reports of fund performance and their most recently filed annual and interim financial statements. These documents are incorporated by reference into this simplified prospectus which means they legally form part of this document just as if they were printed in it.

You can get a copy of the Fund’s annual information form, management reports of fund performance, and financial statements at your request, and at no cost, by calling toll free 1-800-268-9269 (416-750-3863 in Toronto), or by email or through the Pinnacle website at www.scotiabank.com/pinnaclefunds.

These documents and other information about the Fund such as information circulars and material contracts, are also available on the SEDAR website at www.sedar.com, or on the Pinnacle website at www.scotiabank.com/pinnaclefunds.

EACH OF SCOTIA ASSET MANAGEMENT L.P. AND SCOTIA CAPITAL INC. IS A CORPORATE ENTITY SEPARATE FROM, ALTHOUGH WHOLLY-OWNED BY, THE BANK OF NOVA SCOTIA