The phases of customer management in distressed portfolios

37

Enabling Intelligent Action

Transcript of The phases of customer management in distressed portfolios

Enabling Intelligent Action

30/10/2014 "First Annual Middle East Retail Banking Summit” 2

The Phases of Customer Management in distressed portfolios

Manos Margaritis

Deputy CEO

30/10/2014 "First Annual Middle East Retail Banking Summit” 3

Customer Management

origination servicing collection

30/10/2014 "First Annual Middle East Retail Banking Summit” 4

Customer Management

Macro- framework Change in GDP

% unemployment

Loans/GDP

NPL

Regulation

Credit Culture

origination servicing collection

30/10/2014 "First Annual Middle East Retail Banking Summit” 5

Customer Management

Credit Expansion SE ASIA

Parts of Africa

origination servicing collection origination servicing

30/10/2014 "First Annual Middle East Retail Banking Summit” 6

30/10/2014 "First Annual Middle East Retail Banking Summit” 7

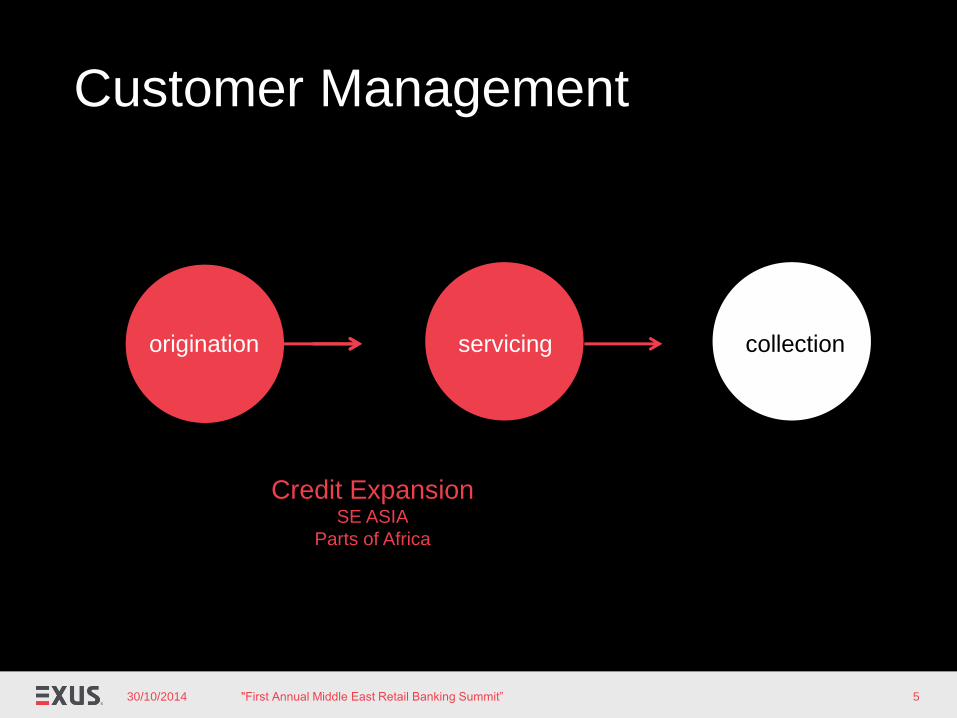

41.7%

30/10/2014 "First Annual Middle East Retail Banking Summit” 8

The objectives

Cross-sell

Minimize churn

Maximize profit

Increase market share

Manage risk

30/10/2014 "First Annual Middle East Retail Banking Summit” 9

Customer Management

Distressed Europe

origination servicing collection origination servicing

30/10/2014 "First Annual Middle East Retail Banking Summit” 10

The European Landscape

European Banking Federation, 2012 report

Cyprus 2013: 39% Spain 2013: 17%

30/10/2014 "First Annual Middle East Retail Banking Summit” 11

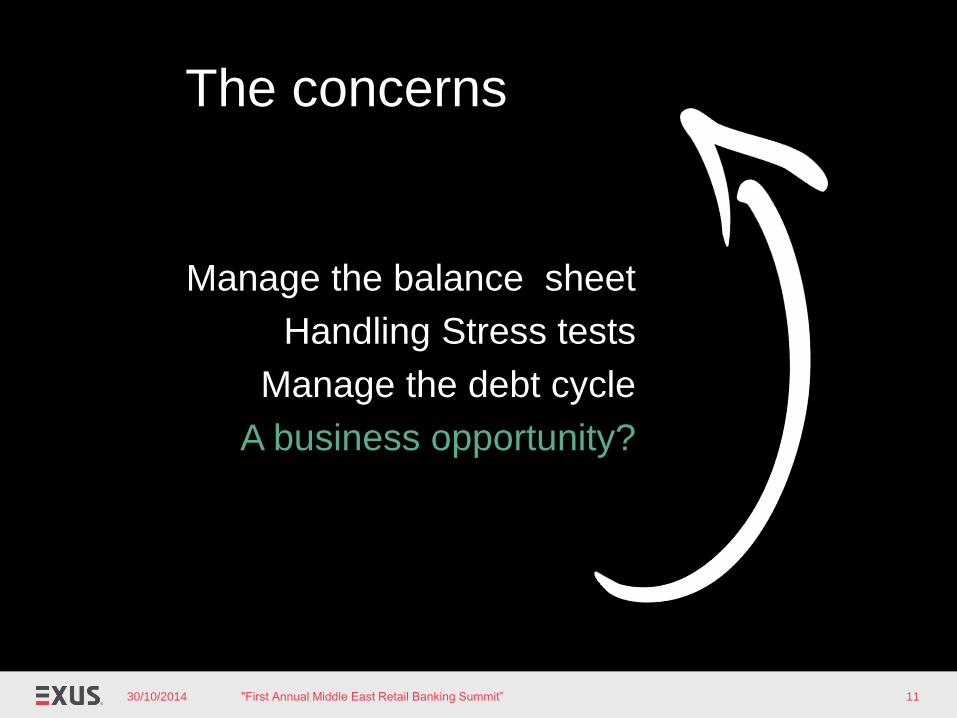

The concerns

Manage the balance sheet

Handling Stress tests

Manage the debt cycle

A business opportunity?

30/10/2014 "First Annual Middle East Retail Banking Summit” 12

Customer Management

origination servicing collection Pre-collection

30/10/2014 "First Annual Middle East Retail Banking Summit” 13

Short term

settlements

Grace period

Capitalization of

delinquencies

Extension

Medium term

settlements Final settlements

Not just a matter of banks: A new agent in the relation to the client Central Bank directive example (European example) , 22 ways for settlements

Interests reduction Interest type change

Partial write-off Split to securitized /

non securitized fractions

Liquidation of securities legal actions ..

Voluntary securities handover ..

30/10/2014 "First Annual Middle East Retail Banking Summit” 14

Not just a matter of the banks: A new agent in the relation to the

client Central Bank directive example The collaborative customer (as per prescription on behavioral patterns)

Contact

information

update

Available to

communicate

Gives info re:

his financial

situation

Collaborates

for new

settlements

30/10/2014 "First Annual Middle East Retail Banking Summit” 15

In the words of a senior Retail Manager:

The development and deployment or settlement

policies is nowadays the most important Marketing

process for every financial institution.

The success of this process will influence : financial results (short and medium term)

reputation and position in future competition landscape

30/10/2014 "First Annual Middle East Retail Banking Summit” 16

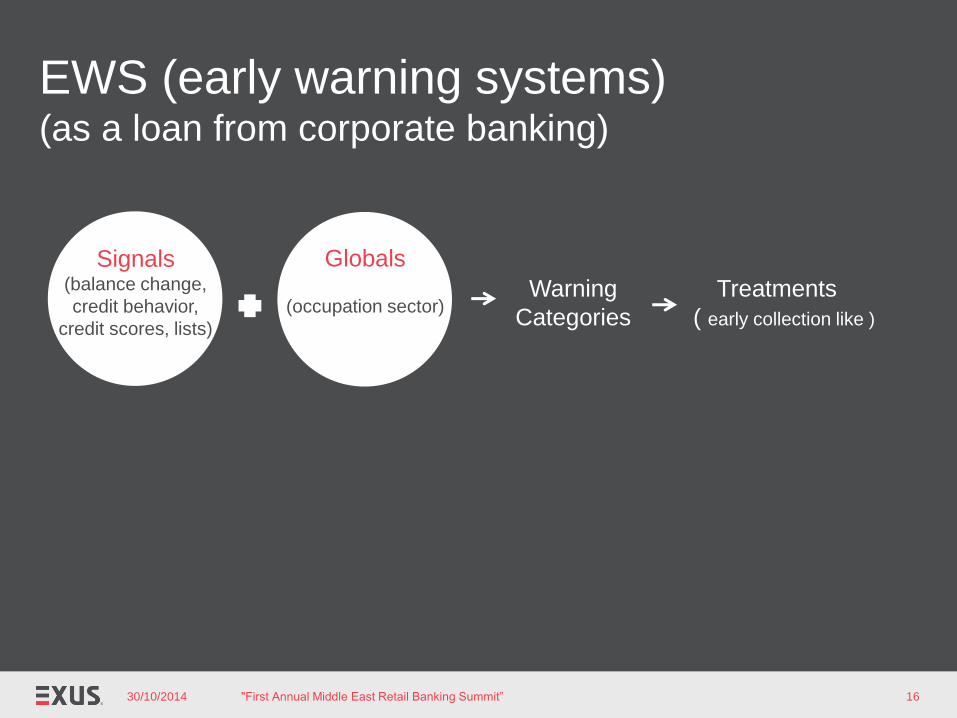

EWS (early warning systems) (as a loan from corporate banking)

Signals (balance change,

credit behavior,

credit scores, lists)

Globals

(occupation sector)

Warning

Categories

Treatments (

( early collection like )

30/10/2014 "First Annual Middle East Retail Banking Summit” 17

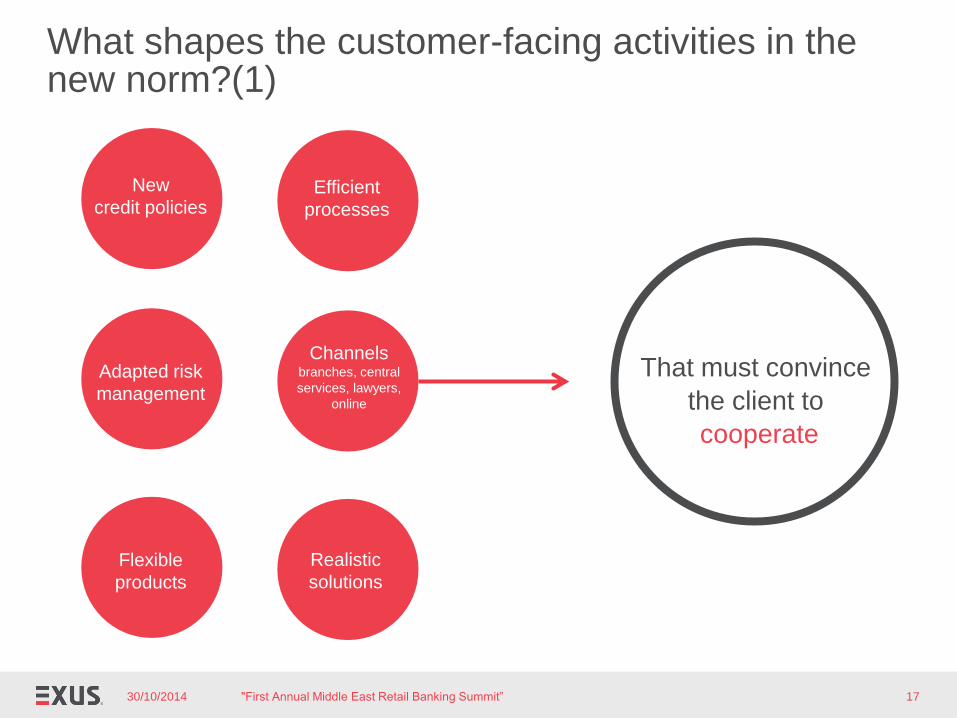

New

credit policies

Adapted risk

management

Flexible

products

That must convince

the client to

cooperate

Efficient

processes

Realistic

solutions

Channels branches, central

services, lawyers,

online

What shapes the customer-facing activities in the new norm?(1)

30/10/2014 "First Annual Middle East Retail Banking Summit” 18

The new KnowYourCustomer (consider what you can)

What is the

economy cycle?

What is the

(un)employment

cycle? What is the lender

economic prospect?

What about the lifestyle?

Can the lender pay?

When?

What is the lender’s attitude?

30/10/2014 "First Annual Middle East Retail Banking Summit” 19

Target:

Social considerations Maximize

NPV*(1-PD)

30/10/2014 "First Annual Middle East Retail Banking Summit” 20

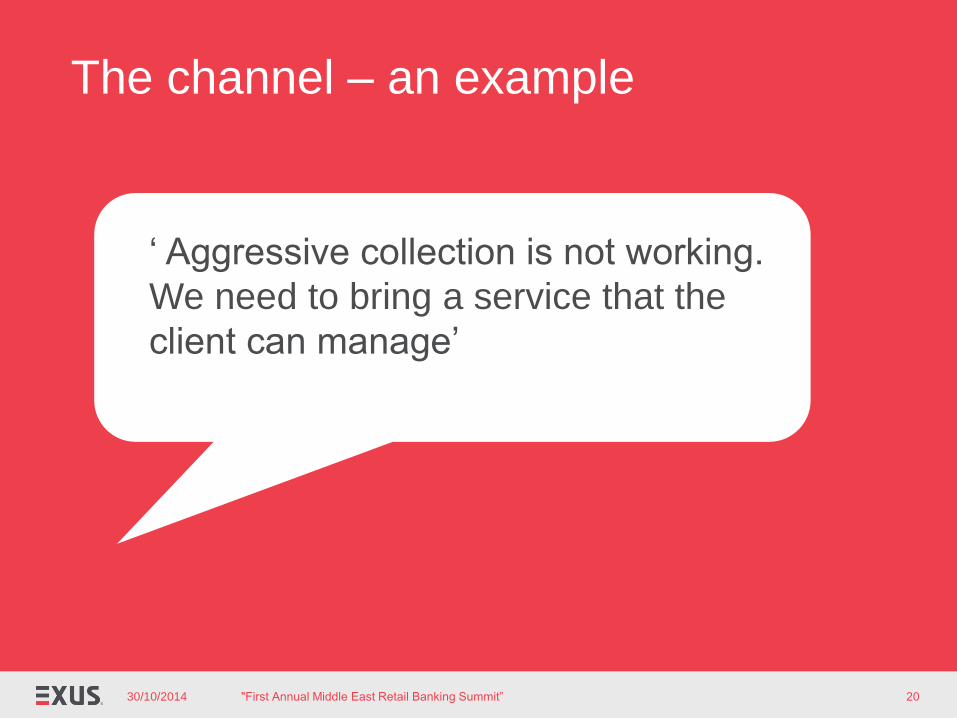

The channel – an example

‘ Aggressive collection is not working.

We need to bring a service that the

client can manage’

30/10/2014 "First Annual Middle East Retail Banking Summit” 21

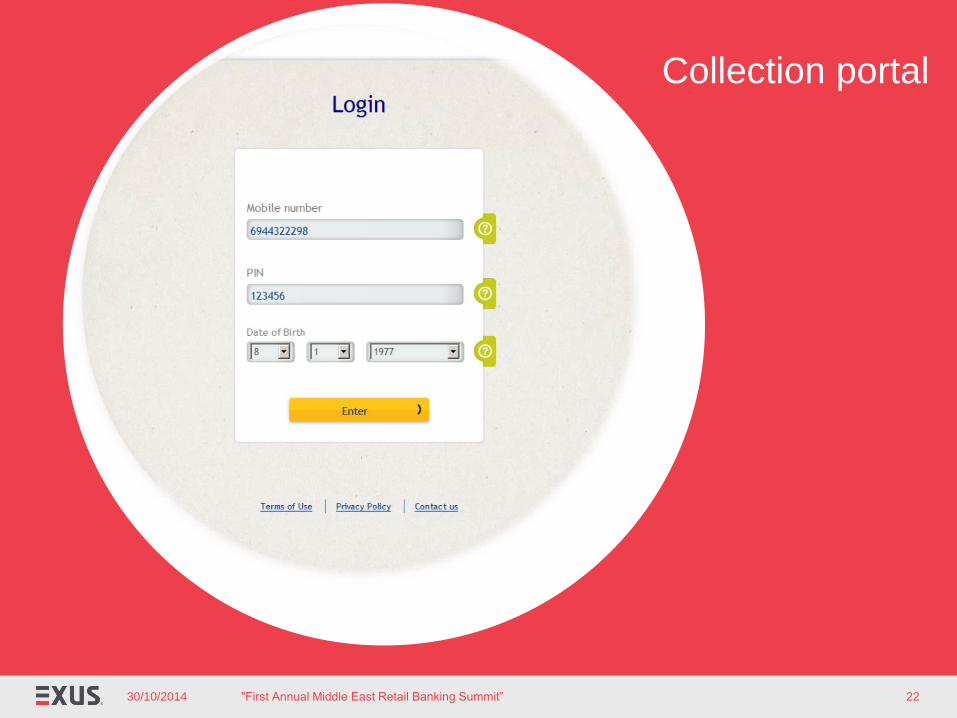

Collection portal

Self-service

Access 24x7

No regulatory limitations

30/10/2014 "First Annual Middle East Retail Banking Summit” 22

Collection portal

30/10/2014 "First Annual Middle East Retail Banking Summit” 23

Collection portal

30/10/2014 "First Annual Middle East Retail Banking Summit” 24

Collection portal

30/10/2014 "First Annual Middle East Retail Banking Summit” 25

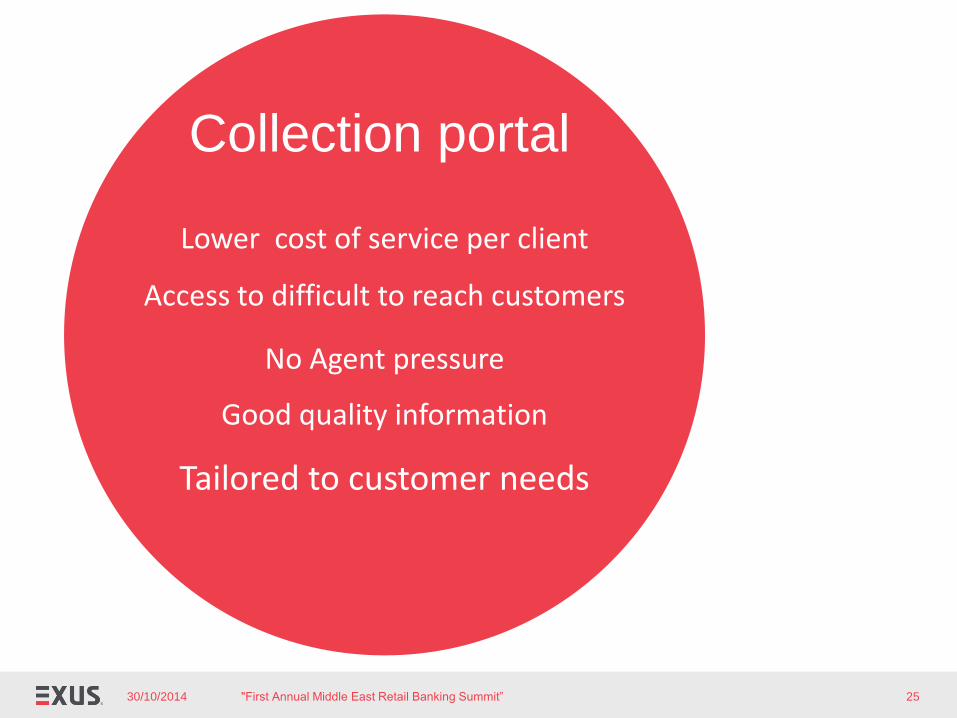

Collection portal

Lower cost of service per client

Access to difficult to reach customers

No Agent pressure

Good quality information

Tailored to customer needs

30/10/2014 "First Annual Middle East Retail Banking Summit” 26

Customer management

is the result of a plethora

of sub-processes that

must be identified and

managed

The customers is

unaware of the

sub- processes

Rethink the processes

30/10/2014 "First Annual Middle East Retail Banking Summit” 27

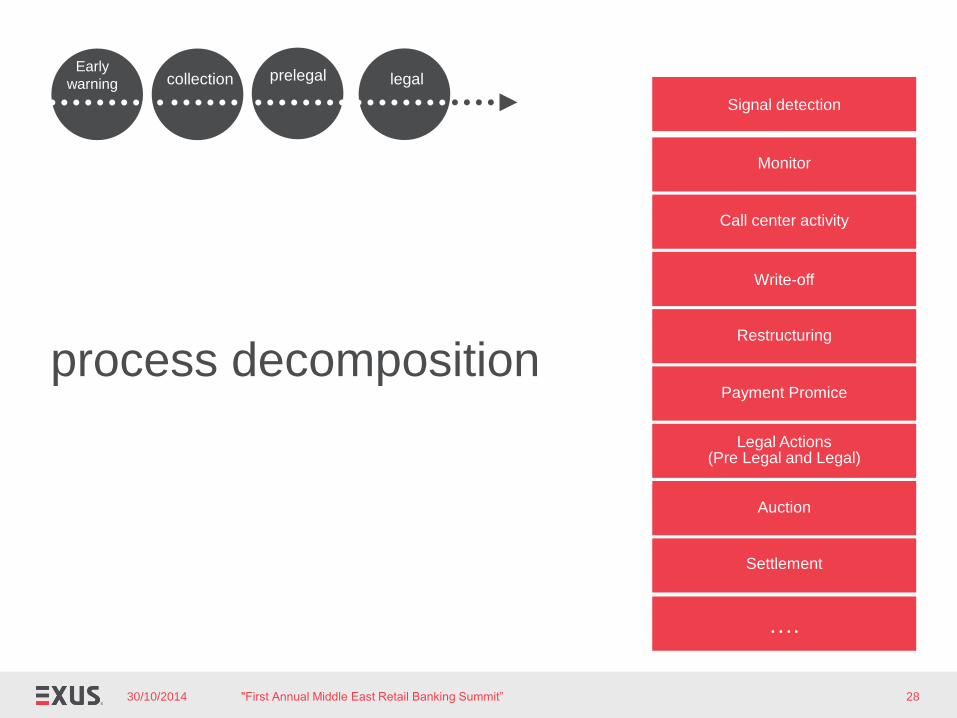

Phases*

collection

prelegal

legal

Early

warning

*segments #1: securities

Write-off

….

30/10/2014 "First Annual Middle East Retail Banking Summit” 28

process decomposition

collection prelegal legal Early

warning

Call center activity

Monitor

Payment Promice

Settlement

Auction

Legal Actions (Pre Legal and Legal)

Restructuring

Signal detection

30/10/2014 "First Annual Middle East Retail Banking Summit” 29

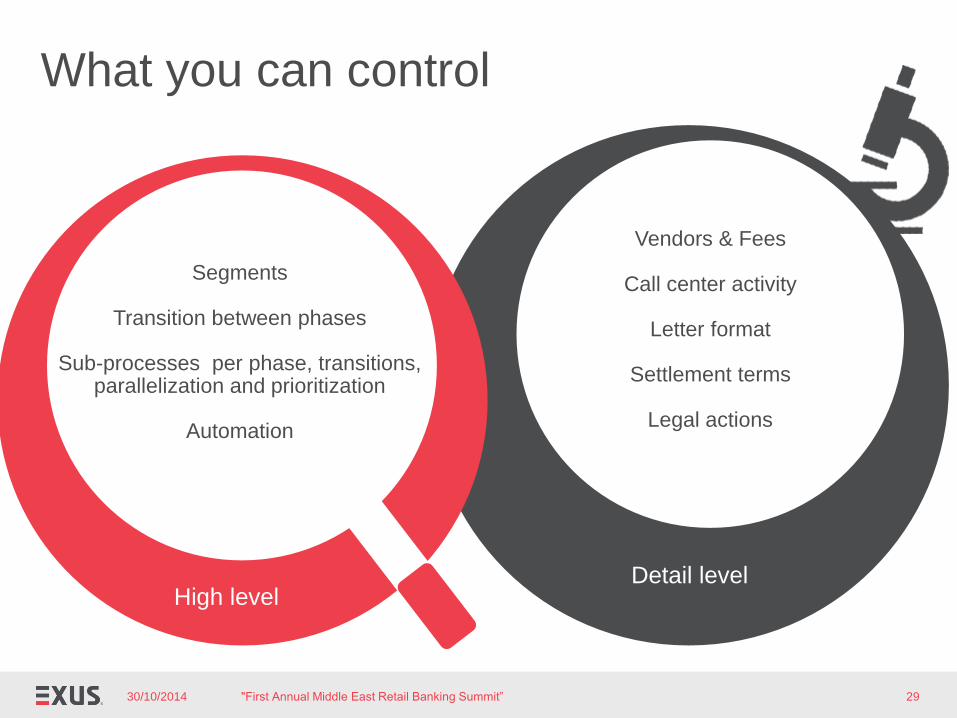

Vendors & Fees

Call center activity

Letter format

Settlement terms

Legal actions

Segments

Transition between phases

Sub-processes per phase, transitions, parallelization and prioritization

Automation

High level Detail level

What you can control

30/10/2014 "First Annual Middle East Retail Banking Summit” 30

Social Considerations Maximize

NPV*(1-PD)

KPIs

Process metrics

30/10/2014 "First Annual Middle East Retail Banking Summit” 31

collection

prelegal

legal precollection

Risk-Related

Exposures back to performing

Coverage Ratio

RAC (part)

Process–related

Cost/Collections

Closing Rate

Self-Cured

Collection – Related

Time in current NPL status

Average Age

Gross collection

Total recovery

Roll rale (upshifts – downshifts)

Legal expenditures/ Recoveries

KPIs

Social

Performance

30/10/2014 "First Annual Middle East Retail Banking Summit” 32

Segment

Sub-process

Phase

Dials per hour

Contacts Per Hour

Collections per Contact

Promise kept rate

Delinquent amount

Total Balance

Cured

Promises

Payments on Promises Amount

Actions

Agent performance

Right Party contacts

Restructuring rate

Restructuring kept

Value managed per account manager

Auctions

Duration of legal actions

Duration of Asset retrieval

(K) PIS

Breakdown

to metrics

30/10/2014 "First Annual Middle East Retail Banking Summit” 33

10

segments X 4

(phases) X 3

process = 120

Different

Approaches,

Heterogeneous

systems

Δ

Different units

Δ

Competitive

objectives

Challenge

30/10/2014 "First Annual Middle East Retail Banking Summit” 34

Champion

Challenger

Portfolio

Level of trials: Per segment

Dependent of

previous phase

2 Χ10=20

Se

gm

ent

Sub-process

Phase

30/10/2014 "First Annual Middle East Retail Banking Summit” 35

That must convince

the client to

cooperate

We are working on new ecosystem to face the client

New

credit policies

Adapted risk

management

Flexible

products

Efficient

processes

Realistic

solutions

Channels branches, central

services, lawyers,

online

30/10/2014 "First Annual Middle East Retail Banking Summit” 36

Helping banks:

Social Considerations Maximize

NPV*(1-PD)

30/10/2014 37

END

END

"First Annual Middle East Retail Banking Summit”