THE OECD BEPS ACTION PLAN - Copenhagen … Questions & Answers. 1 ... a transaction between...

34

THE OECD BEPS ACTION PLAN Intangibles and Services 28-03-2017 Seminar

Transcript of THE OECD BEPS ACTION PLAN - Copenhagen … Questions & Answers. 1 ... a transaction between...

THE OECD BEPS

ACTION PLANIntangibles and Services

28-03-2017Seminar

INTRODUCTION TO

COPENHAGEN ECONOMICS

TRANSFER PRICING

Transfer pricing valuations and documentation related to…

• TP systems upon business re-structuring efforts

• I/co license rates for brand, technologies, know-how…

• Determination of economic benefits from centrally provided services and functions

• Implementation of global transfer pricing documentation (master file, local file, CbC)

• Local tax audit support

3

IP Valuation & Transfer Pricing

We help our clients by quantifying the economic value of various kinds of

intellectual property and intangible assets, employing state-of-the art

economic models. This can be for transfer pricing, dispute, or strategic and

monetization purposes.

DISPUTES & LICENSING

• Calculation of damages in e.g. infringement cases and loss of patenting

• Support settlements and settlement negotiations with economic analysis

• Determine license rates for commercialization purposes

HENDRIK FÜGEMANN

Partner

VINCENZO ZURZOLO

Senior Economist

KATHARINA HUHN

EconomistMORITZ LUBCZYK

AnalystHENRIK KARLSSON

Analyst

KATRINE

VESTERGAARD

Assistant

STRATEGY

• Economic evaluation of early-stage technology

• Market assessments to determine the market potential for a (to-be-developed) technology and patents

• Policy-related questions on e.g. the design of licensing, IP and related frameworks

CONTACT INFORMATION

www.copenhageneconomics.com

Hendrik Fügemann

+46 76 1872 665

• Established year 2000

• Offices in Copenhagen, Stockholm and Brussels

• Single expertise: Economics

• 70 employees, Ph.D. or M.Sc. in Economics

• Multiple nationalities: Danish, Swedish, Finnish, German, Italian, Lithuanian, Romanian, American

• Partner-owned, six partners

Hard Facts about Copenhagen

Economics

4

1 2

3 4

Evolvement of TP Regulations Intangibles

Services Questions & Answers

1

EVOLVEMENT OF TRANSFER PRICING REGULATIONS

• FROM CUP TO VALUATION TECHNIQUES

From CUP to Valuation Techniques

Number of OECD publications on TP Topics. DD: Discussion Draft. CCA: Cost Contribution Arrangement. 7

20152008 2010 2012

•Value creation

•Control over functions & risks

•Use of valuation techniques

DD Business Restruct.

•Cross-border services

•Most appropriate TP method

•CCA

DD on Intangibles

•Important functions (DEMPE)•Unique & Valuable contributions•Opening to Safe Harbours

2010 TP Guidelines

Attribution of profits to

PE

Attribution of profits to

PE

1995

1st OECD TP

Guidelines

• Cross-border transfers of valuable intangibles

• Significant People Functions

2011

•Differentia-tion between intangible transfers and services

•Marketing intangibles

Scoping doc. on

Intangibles

DD on Safe Harbours

BEPS Actions

8-10

• The CUP method as the best method in hierarchy

2015=19

Year = #

1999=1

2

INTANGIBLES

• DISENTANGLING DIFFERENT CATEGORIES OF INTANGIBLES

• DIFFERENT WAYS TO EXPLOIT INTANGIBLES

• ESTABLISHING THE ARM’S LENGTH PRICE FOR INTANGIBLES

• VALUE OF CONTRIBUTIONS TO INTANGIBLES

• TRANSFER PRICING METHODS APPROPRIATE FOR INTANGIBLES

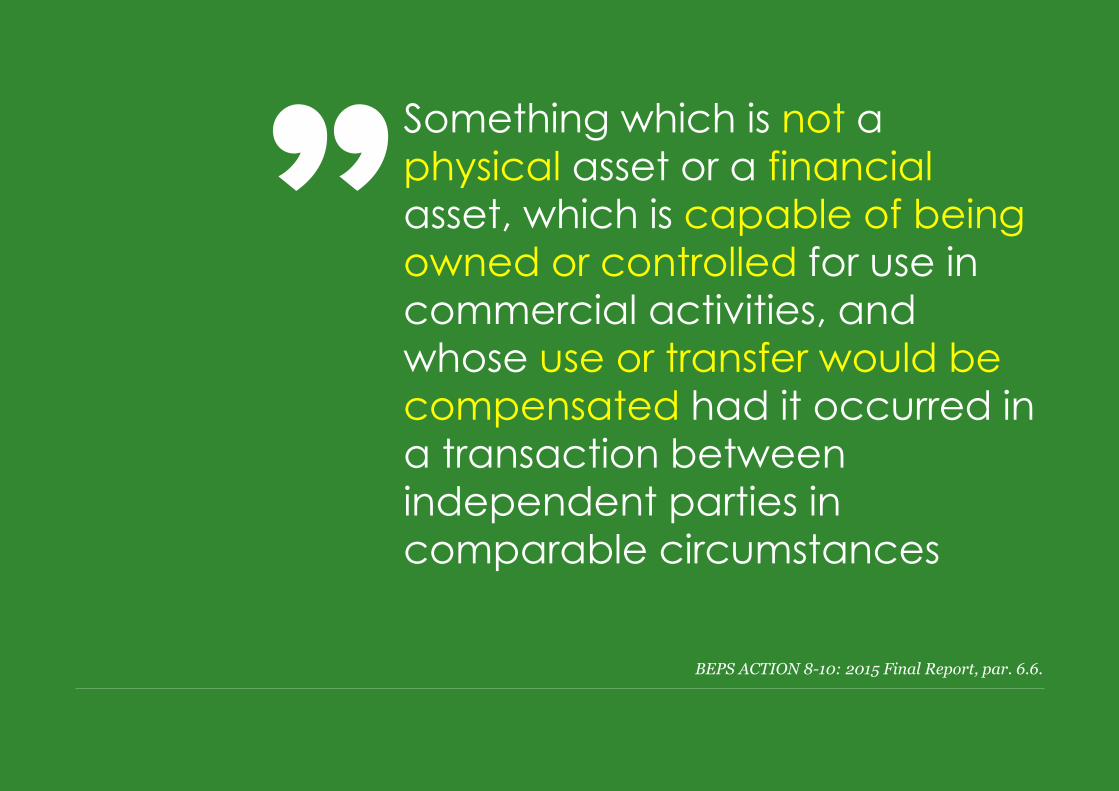

Something which is not a

physical asset or a financial

asset, which is capable of being

owned or controlled for use in

commercial activities, and

whose use or transfer would be

compensated had it occurred in

a transaction between

independent parties in

comparable circumstances

BEPS ACTION 8-10: 2015 Final Report, par. 6.6.

10

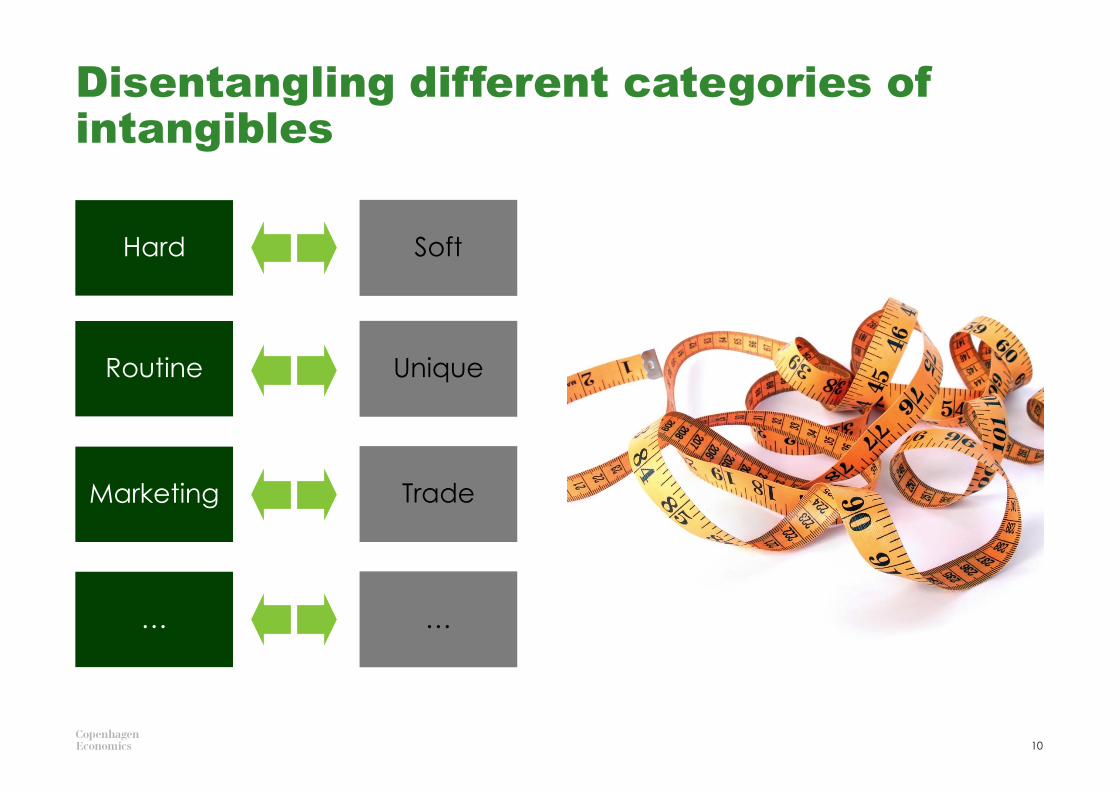

Disentangling different categories of

intangibles

Hard Soft

Routine Unique

Marketing Trade

… …

1 BEPS ACTION 8-10: 2015 Final Report, par. 6.30-6.31. 11

Hard intangiblesAn intangible characterized by legal, contractual, or other forms of protection (local or worldwide)

Soft intangiblesAn intangible not protected/ registered under international or local law. Taken into account, but not considered intangibles for TP purposes1

Hard vs. Soft Intangibles

Trademarks Patents

Government

Licenses &

Concessions

Software /

Copyrights

Group

Synergies

Location

Savings

Skilled

Workforce

Access to

market

Know-how

Customer

List

1 BEPS Action 8-10: par. 6.10. 2 Ibidem, par. 6.116. 12

Routine intangiblesAn intangible commonly available on the marketplace. Does not justify the allocation of premium return, over and above normal returns earned by comparable enterprises1

Unique intangiblesAn intangible with unique characteristics having the potential for generating returns and creating future benefits that could differ widely2

Routine vs. Unique Intangibles

Non unique Know-how

Retail customer list

(e.g. tobacconists)

Open-source software

Commercial Licenses

Trademarks Patents

Proprietary market and

customer data

Government Licenses &

Concessions

1 BEPS Action 8-10: Section A. 3 Amendment to Glossary. 2 OECD TP GL 2010: Glossary. 3 UN Practical Manual on Transfer Pricing, par. 1.6.5. 13

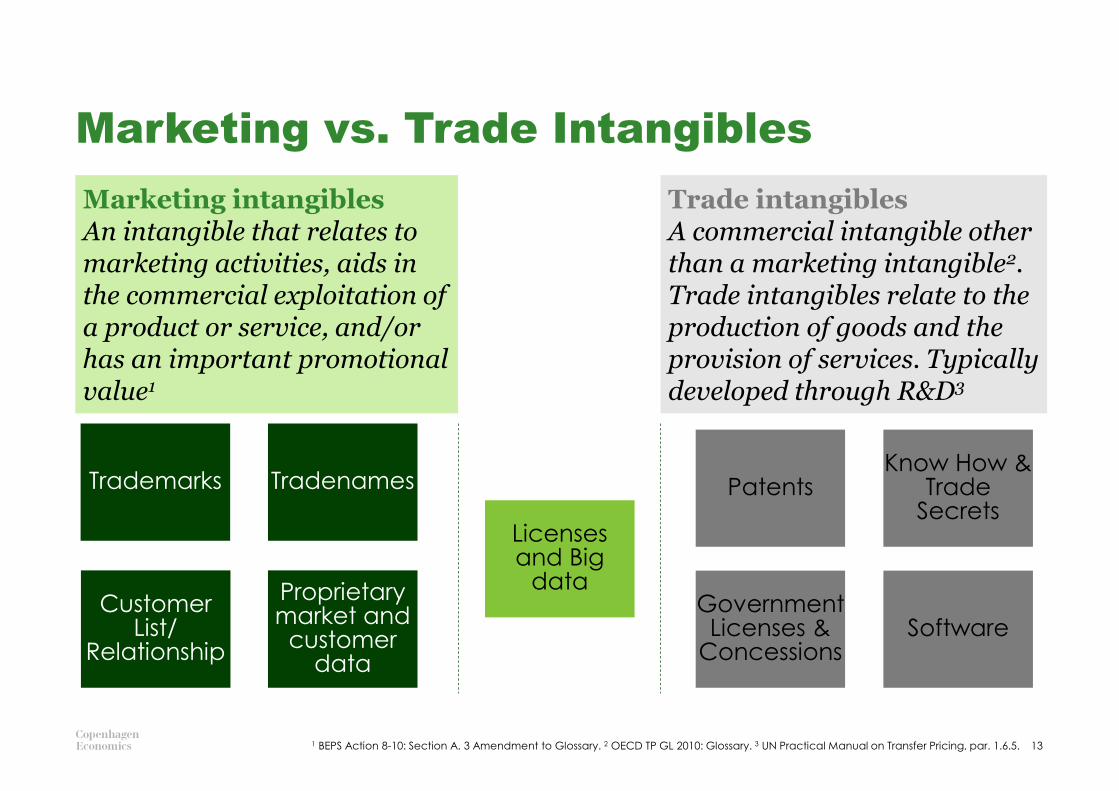

Marketing intangiblesAn intangible that relates to marketing activities, aids in the commercial exploitation of a product or service, and/or has an important promotional value1

Trade intangiblesA commercial intangible other than a marketing intangible2. Trade intangibles relate to the production of goods and the provision of services. Typically developed through R&D3

Marketing vs. Trade Intangibles

Trademarks Tradenames

Customer List/

Relationship

Proprietary market and

customer data

PatentsKnow How &

Trade Secrets

Government Licenses &

ConcessionsSoftware

Licenses and Big

data

14

Combination of

intangibles

Intangibles &

Services

Goodwill

Different ways to exploit intangibles

Trademark Patent Tangibles GW

On a stand-alone

basis

1 BEPS Action 8-10: par. 6.94. 15

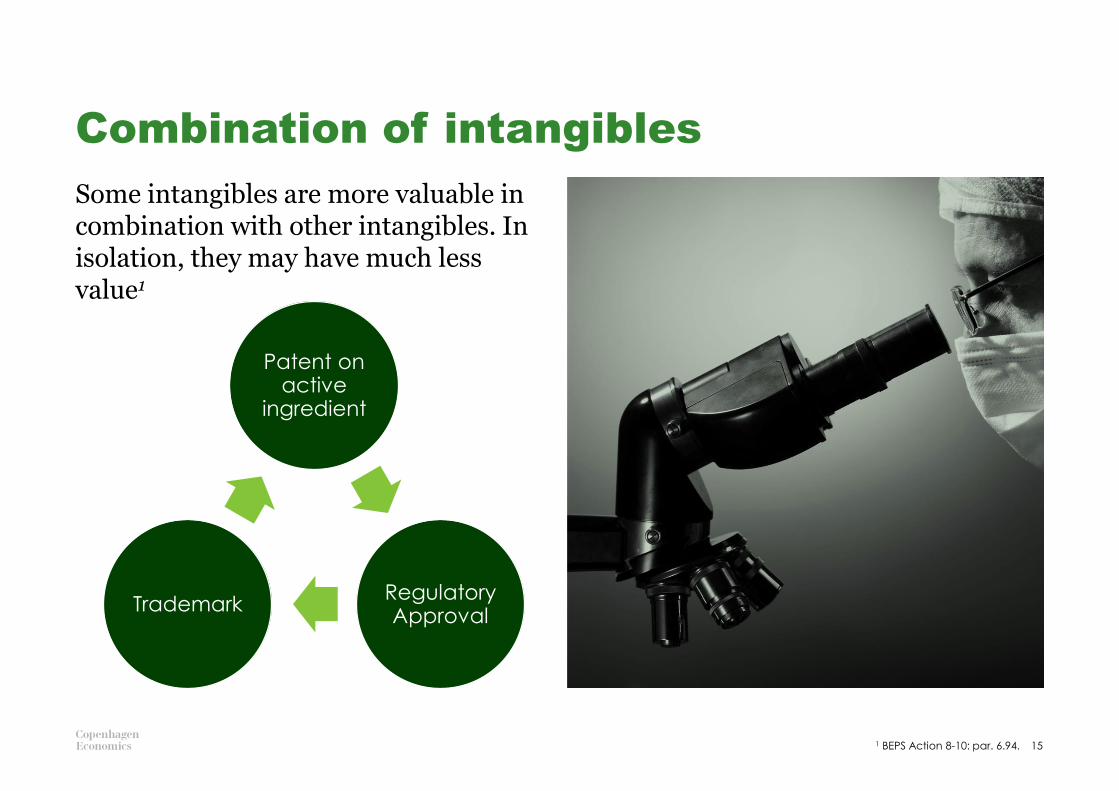

Combination of intangibles

Some intangibles are more valuable in combination with other intangibles. In isolation, they may have much less value1

Patent on active

ingredient

Regulatory Approval

Trademark

Service

1 BEPS Action 8-10: para. 6.99 - 6.101. 2 TP: Transfer Price. 16

Intangibles may also be transferred in combination with services1

Intangibles & Services

Where comparable arrangements are

not available, it may be possible and

appropriate to separate services from

the transfer of intangibles (e.g.

franchising agreements)

In other situations, the provision of

services and the transfer of intangible

may be so intertwined that is difficult

to separate the transactions (e.g.

brand, software)

Service

Intangible

Testing TP2 for the provision of service

Testing TP for the transfer of rights in the intangible

Intangible

Testing TP on an aggregate basis for the provision of services and the transfer of rights in the intangible

17

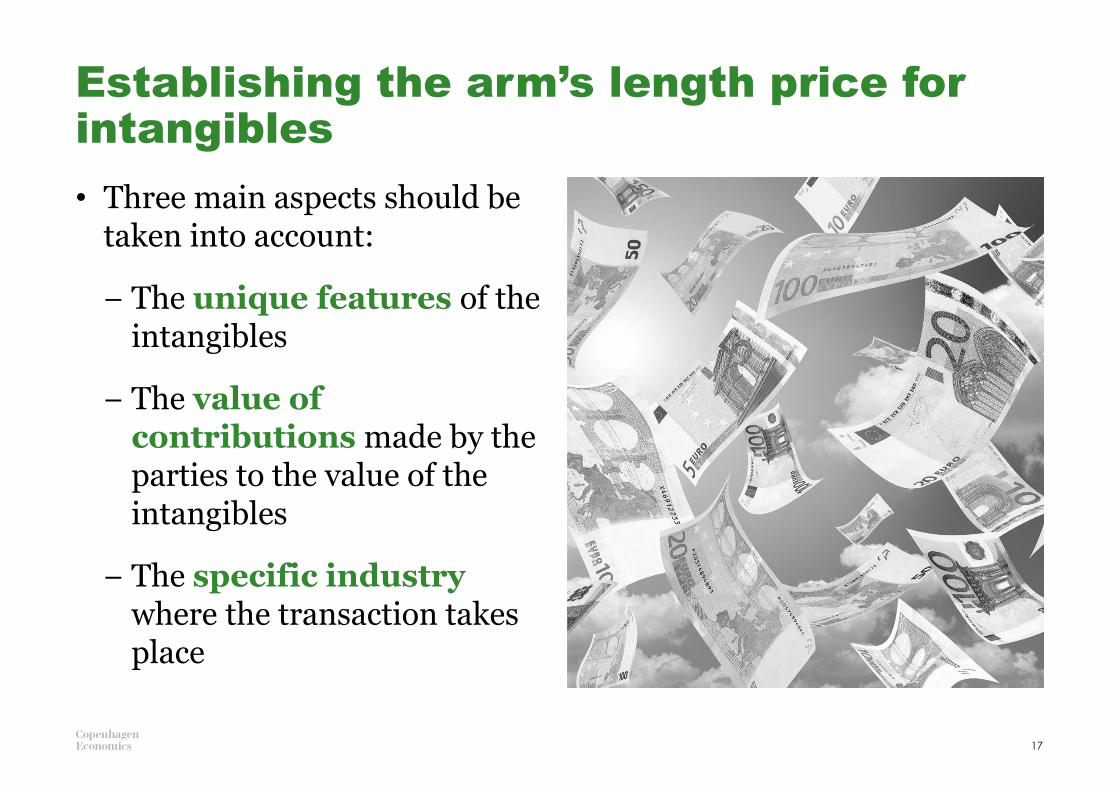

• Three main aspects should be taken into account:

− The unique features of the intangibles

− The value of contributions made by the parties to the value of the intangibles

− The specific industry where the transaction takes place

Establishing the arm’s length price for

intangibles

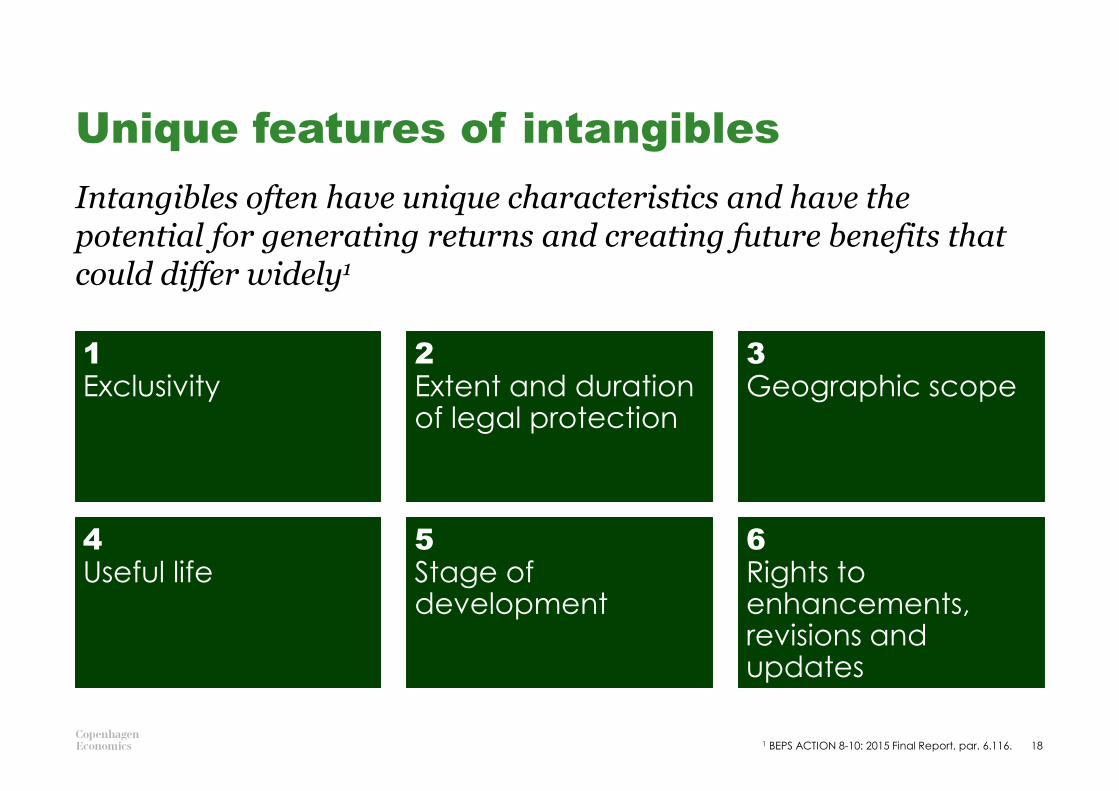

Intangibles often have unique characteristics and have the potential for generating returns and creating future benefits that could differ widely1

Unique features of intangibles

18

1

Exclusivity2

Extent and duration of legal protection

3

Geographic scope

4

Useful life 5

Stage of development

6

Rights to enhancements, revisions and updates

1 BEPS ACTION 8-10: 2015 Final Report, par. 6.116.

1 BEPS ACTION 8-10: 2015 Final Report, par. 6.48. 2 BEPS ACTION 8-10: 2015 Final Report, par. 6.42. 19

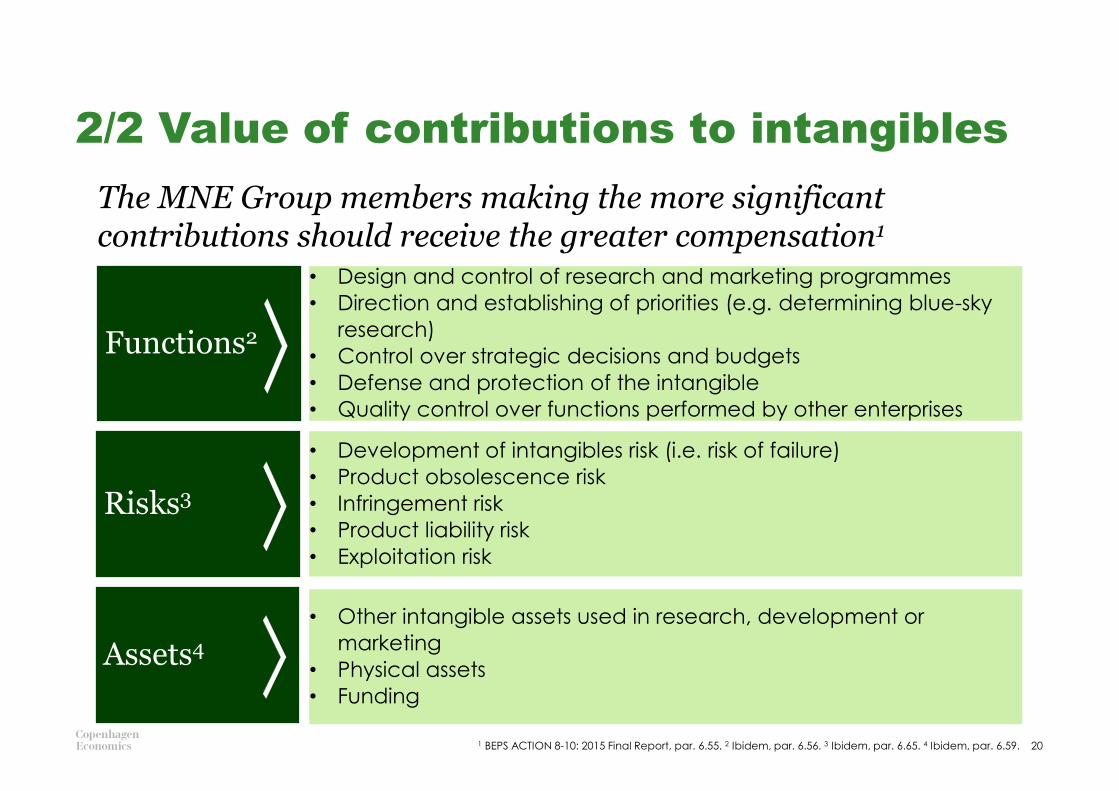

• Under the arm’s length principle, members of a MNE Group must be compensated for their contribution to the value of the intangible, in terms of functions, risks, and assets related to the Development, Enhancement, Maintenance, Protection, and Exploitation of the intangible1

• Legal ownership of intangibles, by itself, does not confer any returns derived by the MNE Group from exploiting the intangible2

1/2 Value of contributions to intangibles

2/2 Value of contributions to intangibles

1 BEPS ACTION 8-10: 2015 Final Report, par. 6.55. 2 Ibidem, par. 6.56. 3 Ibidem, par. 6.65. 4 Ibidem, par. 6.59. 20

Risks3

Assets4

• Design and control of research and marketing programmes

• Direction and establishing of priorities (e.g. determining blue-sky

research)

• Control over strategic decisions and budgets

• Defense and protection of the intangible

• Quality control over functions performed by other enterprises

Functions2

The MNE Group members making the more significant contributions should receive the greater compensation1

• Development of intangibles risk (i.e. risk of failure)

• Product obsolescence risk

• Infringement risk

• Product liability risk

• Exploitation risk

• Other intangible assets used in research, development or

marketing

• Physical assets

• Funding

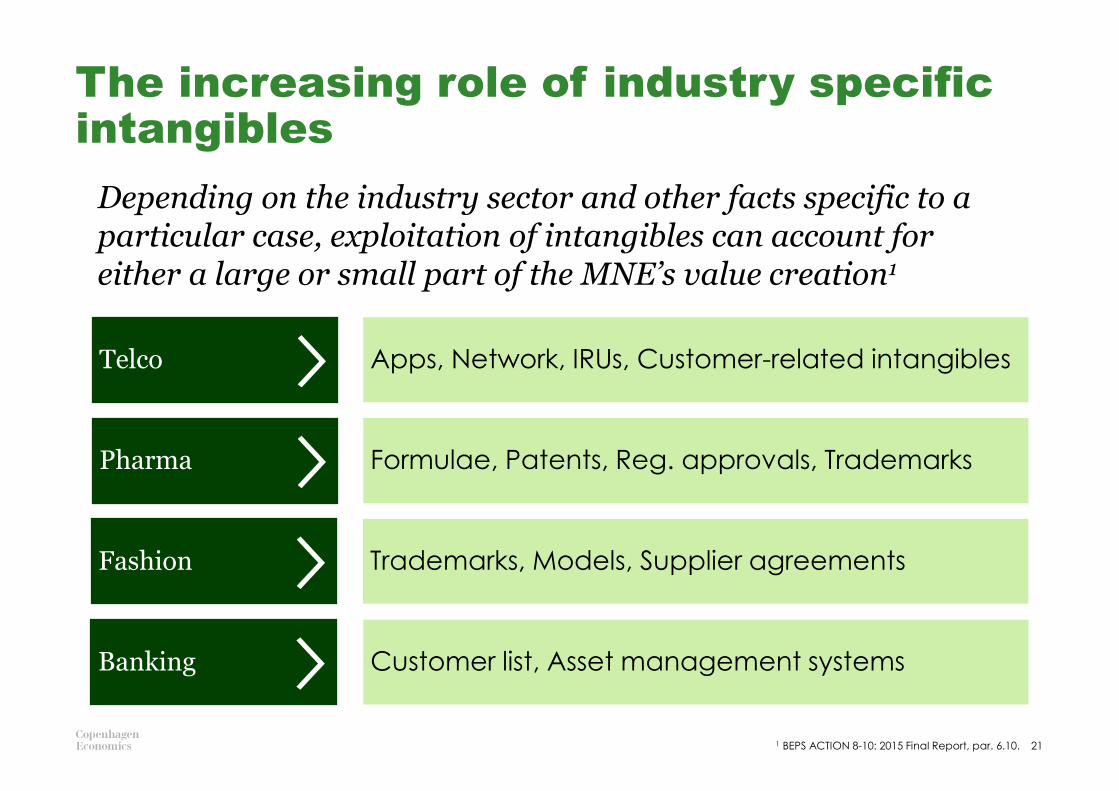

The increasing role of industry specific

intangibles

1 BEPS ACTION 8-10: 2015 Final Report, par. 6.10. 21

Fashion

Banking

Formulae, Patents, Reg. approvals, TrademarksPharma

Trademarks, Models, Supplier agreements

Customer list, Asset management systems

Apps, Network, IRUs, Customer-related intangiblesTelco

Depending on the industry sector and other facts specific to a particular case, exploitation of intangibles can account for either a large or small part of the MNE’s value creation1

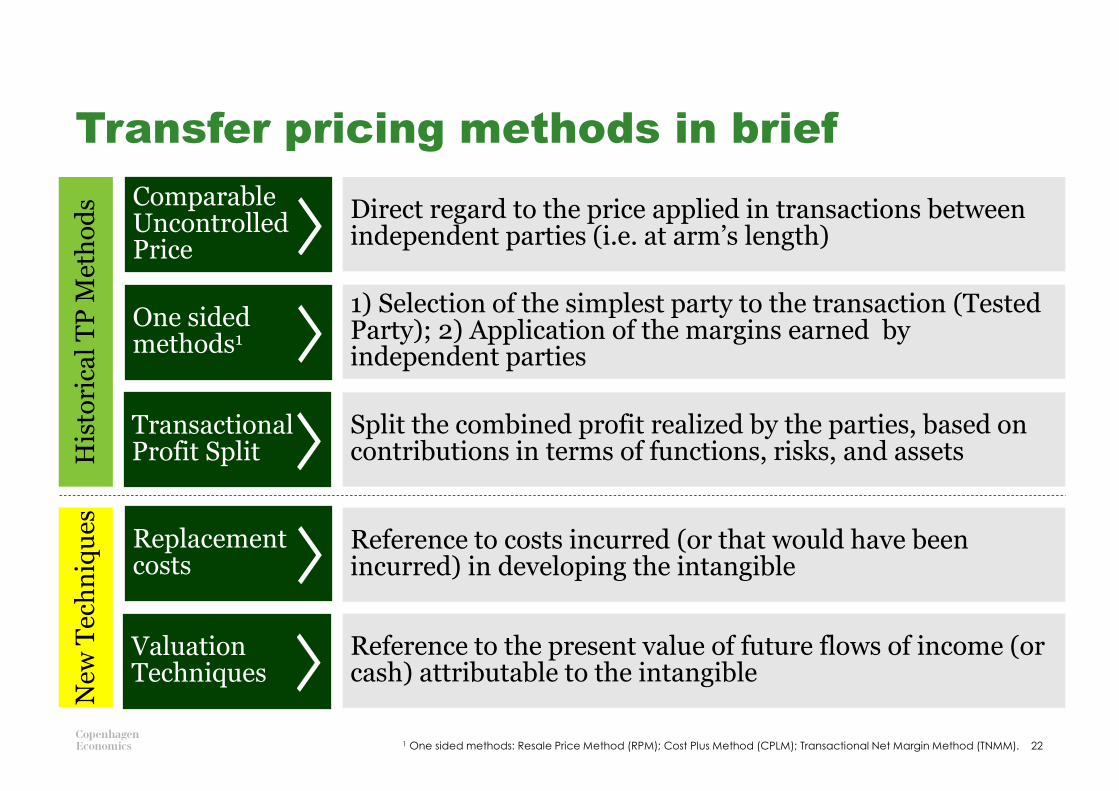

1 One sided methods: Resale Price Method (RPM); Cost Plus Method (CPLM); Transactional Net Margin Method (TNMM). 22

Transfer pricing methods in brief

Transactional Profit Split

Valuation Techniques

Direct regard to the price applied in transactions between independent parties (i.e. at arm’s length)

Comparable Uncontrolled Price

One sided methods1

Replacement costs

1) Selection of the simplest party to the transaction (Tested Party); 2) Application of the margins earned by independent parties

Split the combined profit realized by the parties, based on contributions in terms of functions, risks, and assets

Reference to costs incurred (or that would have been incurred) in developing the intangible

Reference to the present value of future flows of income (or cash) attributable to the intangible

His

tori

cal

TP

Met

ho

ds

New

Tec

hn

iqu

es

1 BEPS ACTION 8-10: 2015 Final Report, para. 6.131 – 6.157. 23

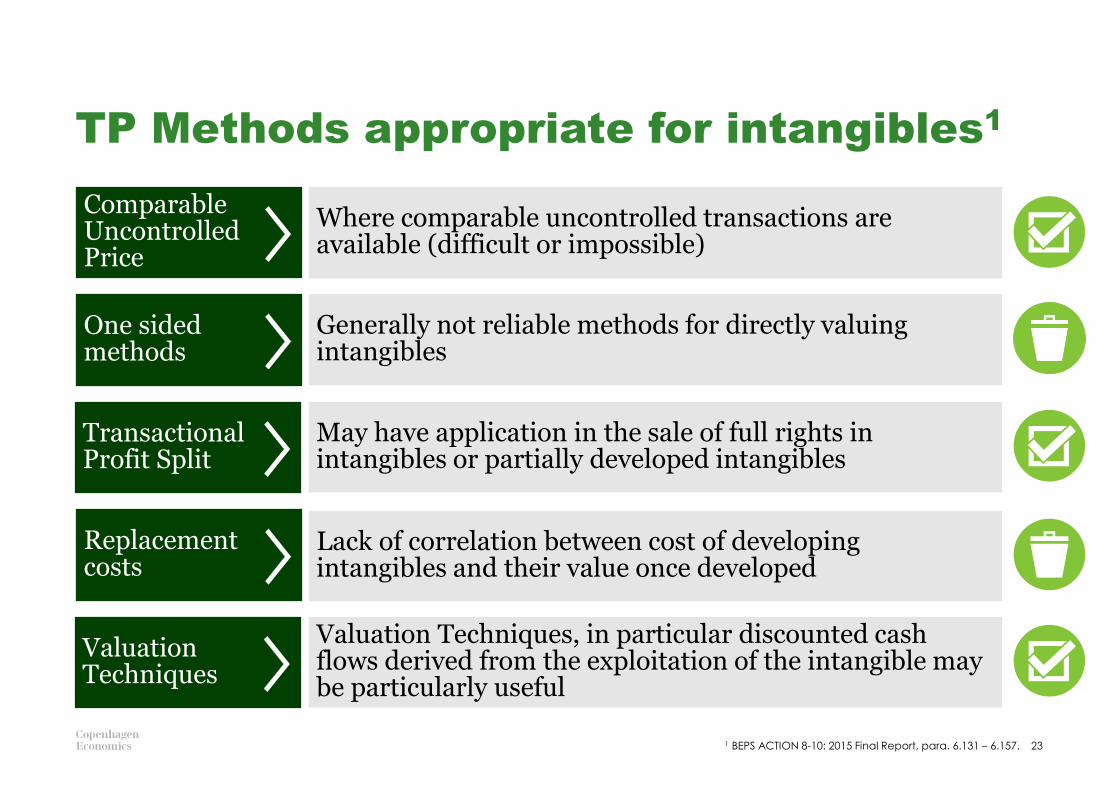

TP Methods appropriate for intangibles1

Where comparable uncontrolled transactions are available (difficult or impossible)

Transactional Profit Split

Valuation Techniques

Comparable Uncontrolled Price

One sided methods

Replacement costs

Generally not reliable methods for directly valuing intangibles

May have application in the sale of full rights in intangibles or partially developed intangibles

Lack of correlation between cost of developing intangibles and their value once developed

Valuation Techniques, in particular discounted cash flows derived from the exploitation of the intangible may be particularly useful

3

SERVICES

• CENTRALIZATION OF SERVICES

• DUPLICATION OF SERVICES

• EXEMPLARY UNIVERSE OF SERVICES

• EVOLUTION OF TP METHODS FOR SERVICES

Whether an activity provides a

respective Group member with

economic and commercial

value to enhance or maintain its

business position and […] an

independent enterprise would

have been willing to pay for the

activity or would have

performed the activity in-house

BEPS ACTION 8-10: 2015 Final Report, par. 7.6.

Centralization of services

26

HQ

Op. Co 1 Op. Co 2 Op. Co N

Sales

Marketing

R&D

Finance/HR

IT

HQ

Op. Co 1 Op. Co 2 Op. Co N

Monitoring

Sales

IT Local

MarketingR&D

IT Global

Sales

IT Local

Sales

IT Local

Regional Office 1

Regional Office 2

Decentralized Centralized

Finance/HR

Sales

Marketing

R&D

Finance/HR

IT

Sales

Marketing

R&D

Finance/HR

IT

1 BEPS ACTION 8-10: 2015 Final Report, par. 7.11. 2 Ibidem. 27

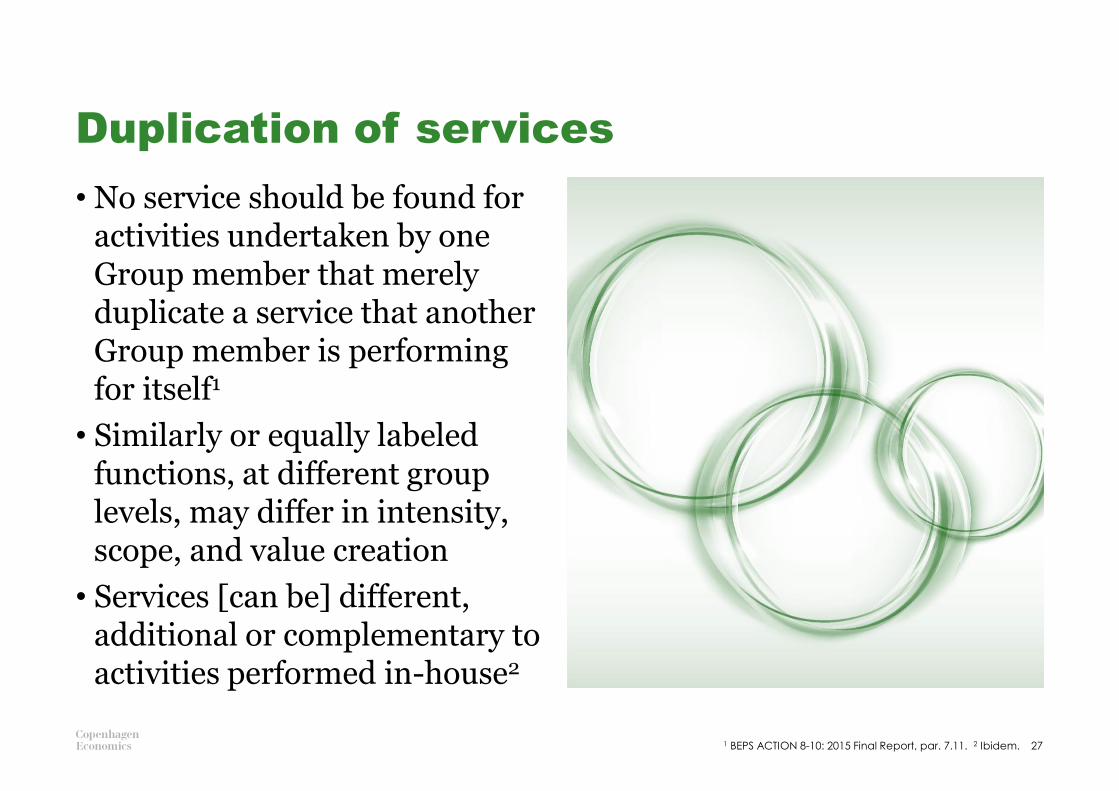

• No service should be found for activities undertaken by one Group member that merely duplicate a service that another Group member is performing for itself1

• Similarly or equally labeled functions, at different group levels, may differ in intensity, scope, and value creation

• Services [can be] different, additional or complementary to activities performed in-house2

Duplication of services

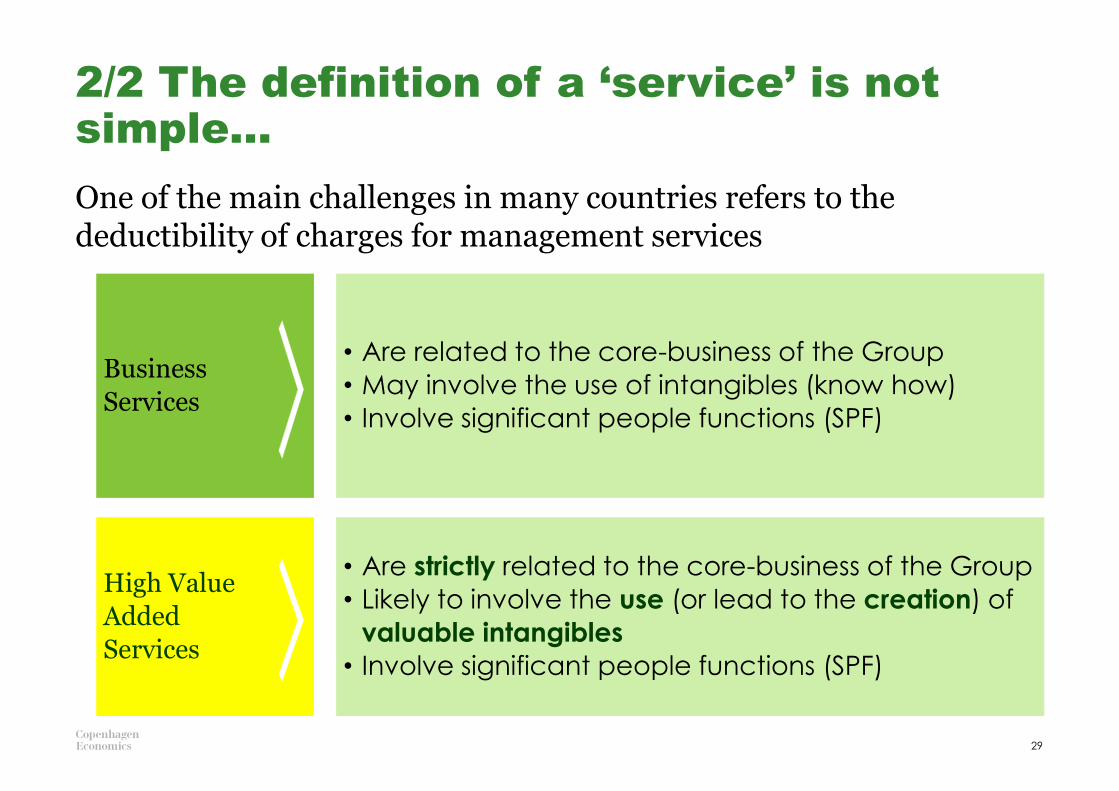

One of the main challenges in many countries refers to the deductibility of charges for management services

1/2 The definition of a ‘service’ is not

simple…

28

Low Value

Added

Services

• Activities performed by one Group member solely

because of its ownership interest in one or more

group members

• Independent enterprises would not be willing to pay

• Not considered intra-group services

Shareholder

activities

• Are supportive in nature and not part of the core-

business of the Group

• Do not require the use of unique and valuable

intangibles and do not involve significant risks

• The arm’s length price is closely related to costs

One of the main challenges in many countries refers to the deductibility of charges for management services

2/2 The definition of a ‘service’ is not

simple…

29

Business

Services

• Are related to the core-business of the Group

• May involve the use of intangibles (know how)

• Involve significant people functions (SPF)

High Value

Added

Services

• Are strictly related to the core-business of the Group

• Likely to involve the use (or lead to the creation) of

valuable intangibles

• Involve significant people functions (SPF)

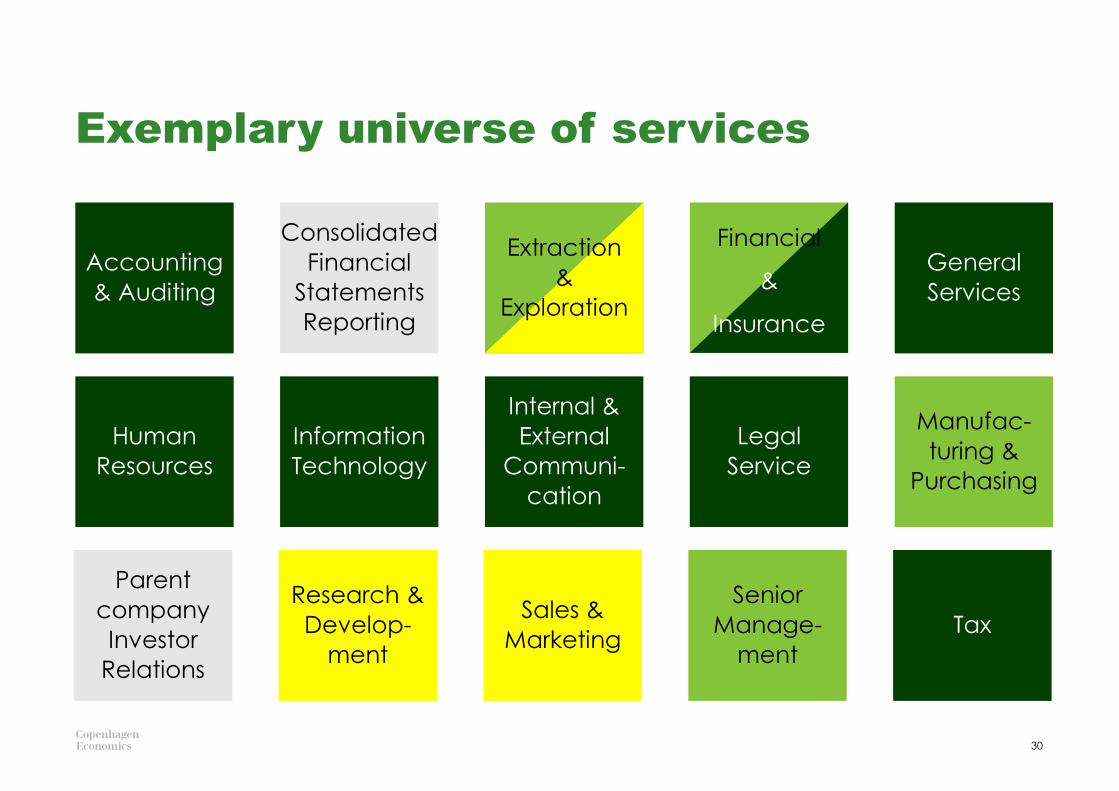

Exemplary universe of services

30

Accounting

& Auditing

Consolidated

Financial

Statements

Reporting

Human

Resources

Information

Technology

Internal &

External

Communi-

cation

Legal

Service

Tax

General

Services

Sales &

Marketing

Senior

Manage-

ment

Manufac-

turing &

Purchasing

Parent

company

Investor

Relations

Research &

Develop-

ment

Financial

&

Insurance

Extraction

&

Exploration

Evolution of TP Methods for services

LVAS: Low value added services. HVAS: Low value added services. GL: Guidelines. EUJTP: European Joint Transfer Pricing. 31

OECD Developments

Supplementary Developments

20152008 2010

2008 Attribution of profit to PE:Significant People Functions

2010 TP GL:Economic Substance, Cross-border services

BEPS 8-10:Value creation,Unique & valuable contributions

US Regs. §1.482:Service Cost Method

TP Methods Cost+At cost /Cost+ Cost+

LVAS:E.g. HR, LegalC+ [Safe Harbour]

Business Services:E.g. ProductionC+ [Benchmark]

HVAS:Val. TechniquesE.g. R&D, Mktg

General functional

comparability

Comparability requirements

Value creation

EUJTP Forum:Low Value Added Services

How to clear the dust …

32

Value

Creation

IntangiblesIntragroup

Services

LVAS

BS

Routine

Soft

Hard

Unique

HVAS

33

Hard facts. Clear Stories.

ABOUT COPENHAGEN ECONOMICS

Copenhagen Economics is the leading economic consultancy in the Nordic region. Founded in2000, the firm counts more than 70 people and operates across the world. Global CompetitionReview (CGR) lists Copenhagen Economics as one of the top 20 economic consultancies in theworld.

We provide independent advice based on recognised research methods, and our experts havein-depth sector knowledge.

www.copenhageneconomics.com