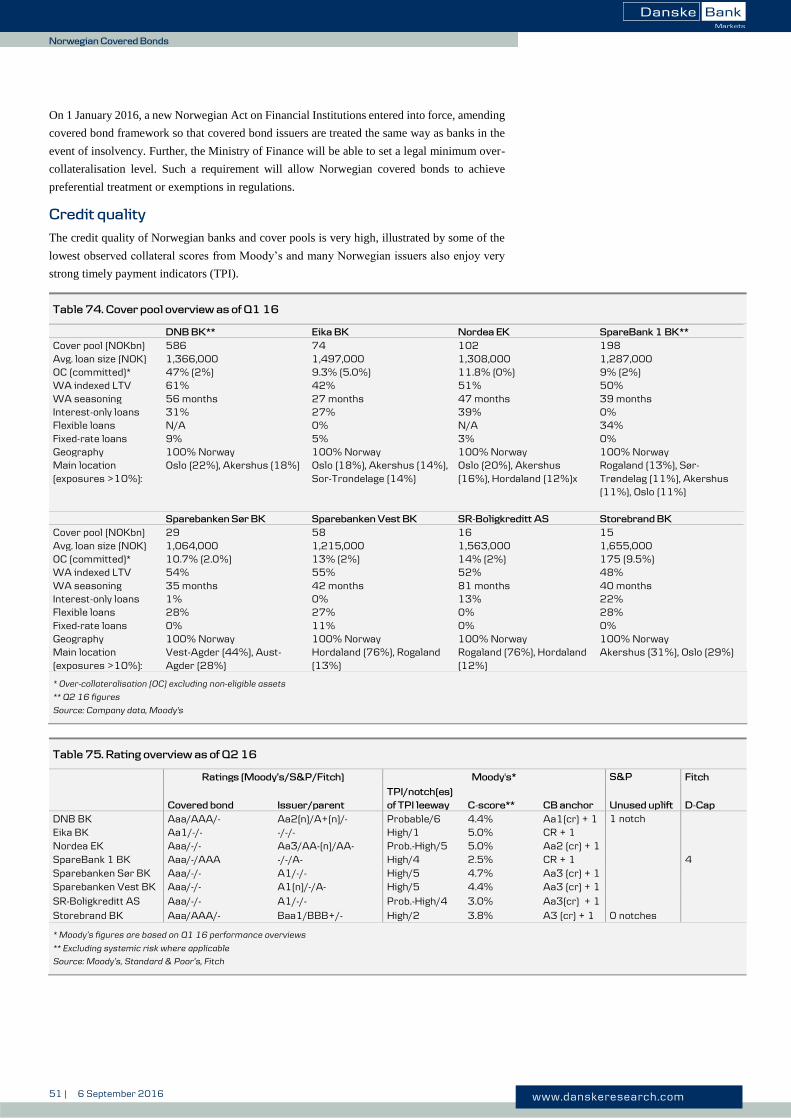

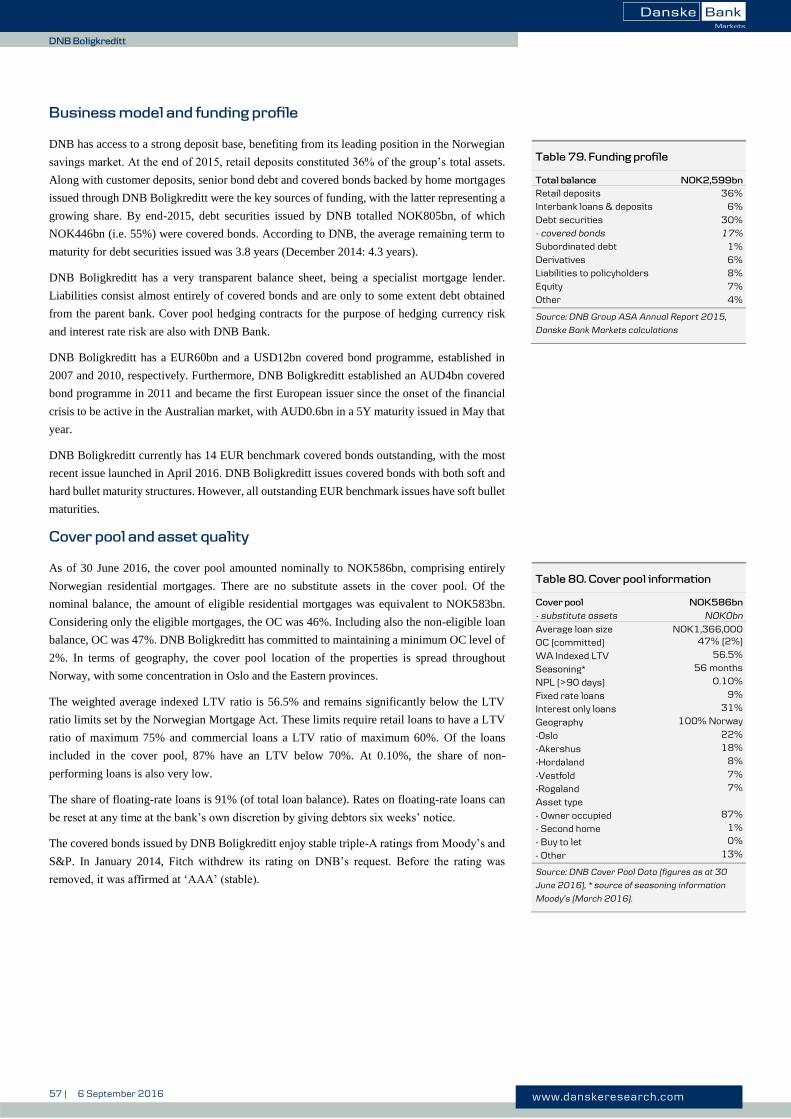

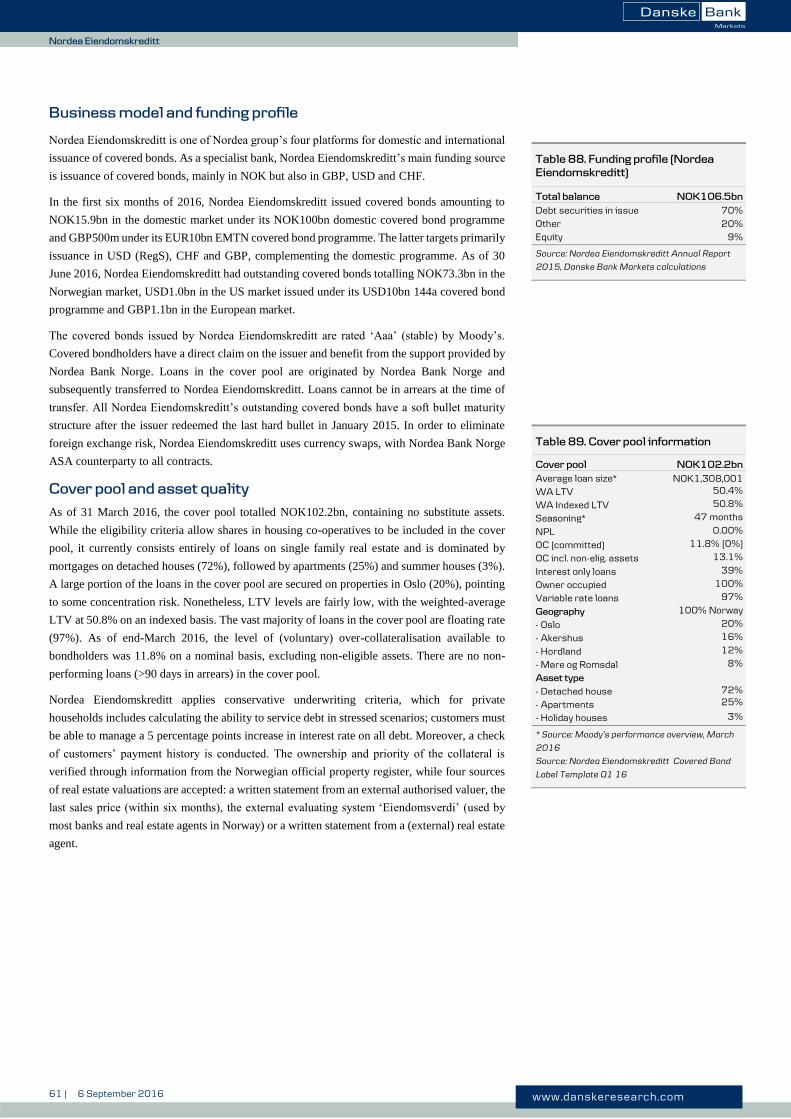

The Nordic Covered Bond Handbook (2016-17) - Danske...

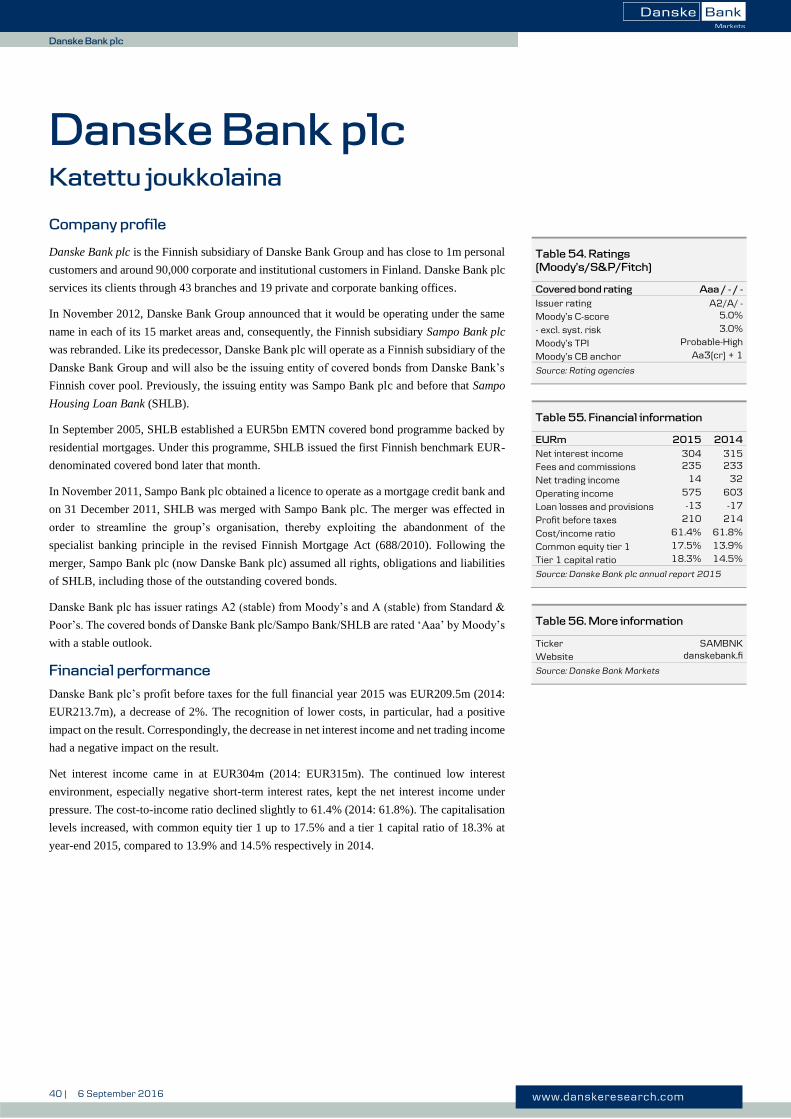

100

www.danskeresearch.com Investment Research 6 September 2016 Nordic Covered Bond Handbook The handbook of the Nordic covered bond markets and issuers Markets Senior Analyst Lukas Platzer +45 45 12 84 30 [email protected] This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research reports prepared for retail investors. Important disclosures and certif ications are contained from page 97 of this report. Senior Analyst Sverre Holbek +45 45 14 88 82 [email protected]

Transcript of The Nordic Covered Bond Handbook (2016-17) - Danske...

www.danskeresearch.com

Investment Research

6 September 2016

Nordic Covered Bond HandbookThe handbook of the Nordic covered bond markets and issuers

Markets

Senior AnalystLukas Platzer+45 45 12 84 [email protected]

This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Important disclosures and certifications are contained from page 97 of this report.

Senior AnalystSverre Holbek+45 45 14 88 [email protected]

Important disclosures and certifications are contained from page 97 of this report. www.danskeresearch.com

Investment Research — General Market Conditions

Welcome to the 12th edition of the Nordic Covered Bond Handbook from the Covered Bond

Research team at Danske Bank Markets.

This publication is intended to act as a quick reference guide to the Nordic covered bond

markets, providing an overview of covered bond issuers in Denmark, Finland, Norway and

Sweden. Further, we provide an overview of the legislative framework in each of the four

markets, as well as updates on housing market developments and the macroeconomic backdrop.

Table 1. Issuers included in this edition

Denmark Finland Norway Sweden

BRFkredit Aktia Bank plc DnB BK Landshypotek Danske Bank Bank of Åland Eika BK LF Hypotek DLR Kredit Danske Bank plc Nordea EK Nordea Hypotek Nordea Kredit Mortg. Society of Finl. SpareBank 1 BK SCBC/SBAB Nykredit/Totalkredit Nordea Finland Sparebanken Sør BK SEB Realkredit Danmark OP MB Sparebanken Vest BK Stadshypotek

SR-Boligkreditt AS Swedbank Hypotek Storeband KF

Most covered bond issuers are subsidiaries of larger, universal banks. The specialist banking

principle is applied in Norway and partly in Denmark, while there is no such requirement in

Sweden and Finland. Parent banks are covered only briefly in this handbook.

Issuer profiles of Danish specialist mortgage banks are included in this handbook, drawing on

the Danish Covered Bond Handbook. We refer readers to the latter for an in-depth description

of this unique market.

6 September 2016

Senior Analyst Lukas Platzer +45 45 12 84 30 [email protected]

Senior Analyst Sverre Holbek +45 45 14 88 82 [email protected]

Nordic Covered Bond

Handbook

12th edition

2 | 6 September 2016 www.danskeresearch.com

No

rdic C

overed

Bo

nd

Ha

nd

bo

ok

Nordic Covered Bond Handbook

3 | 6 September 2016 www.danskeresearch.com

No

rdic C

overed

Bo

nd

Ha

nd

bo

ok

Nordic Covered Bond Handbook

Contents

Introduction ..................................................................................................................... 5

Danish Covered Bonds ............................................................................................. 9

BRFkredit ............................................................................................................................................................................ 16

Danske Bank ..................................................................................................................................................................... 18

DLR Kredit .......................................................................................................................................................................... 20

Nordea Kredit .................................................................................................................................................................. 22

Nykredit/Totalkredit .................................................................................................................................................... 24

Realkredit Danmark..................................................................................................................................................... 26

Finnish Covered Bonds ......................................................................................... 29

Aktia Bank plc .................................................................................................................................................................. 36

Bank of Åland plc ........................................................................................................................................................... 38

Danske Bank plc ............................................................................................................................................................. 40

Mortgage Society of Finland .................................................................................................................................. 42

Nordea Bank Finland ................................................................................................................................................... 44

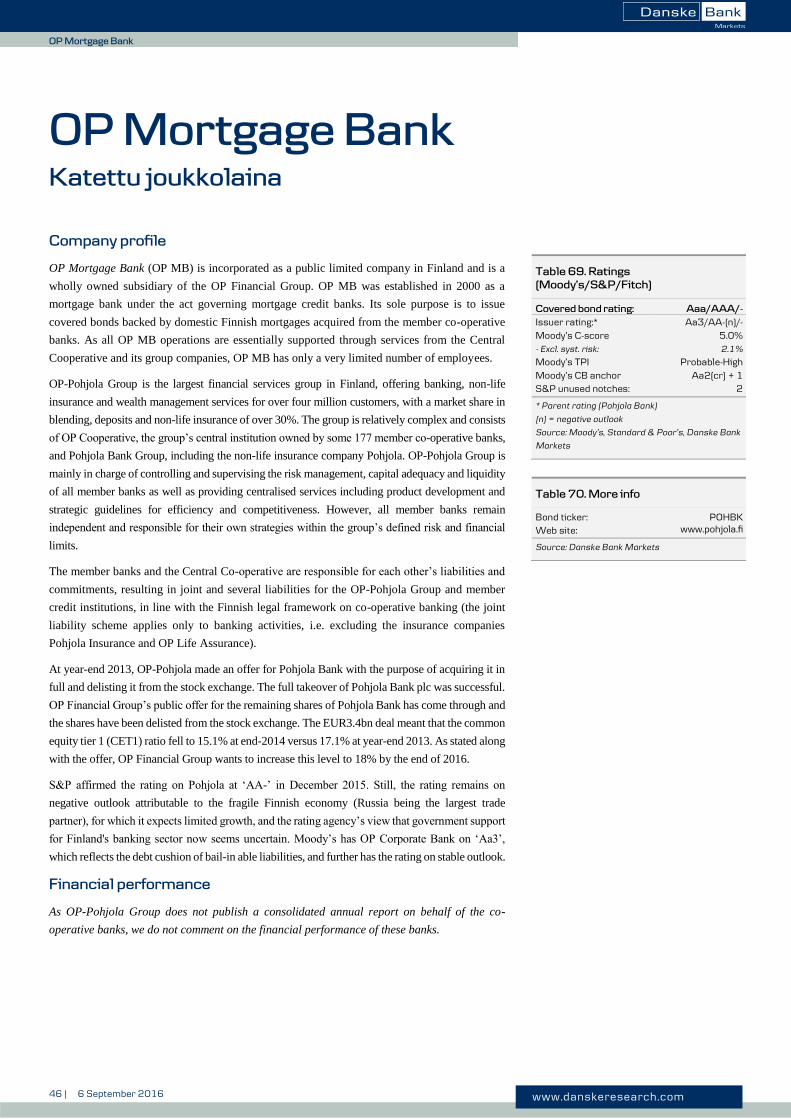

OP Mortgage Bank ....................................................................................................................................................... 46

Norwegian Covered Bonds ................................................................................. 49

DNB Boligkreditt ............................................................................................................................................................ 56

Eika Boligkreditt ............................................................................................................................................................. 58

Nordea Eiendomskreditt .......................................................................................................................................... 60

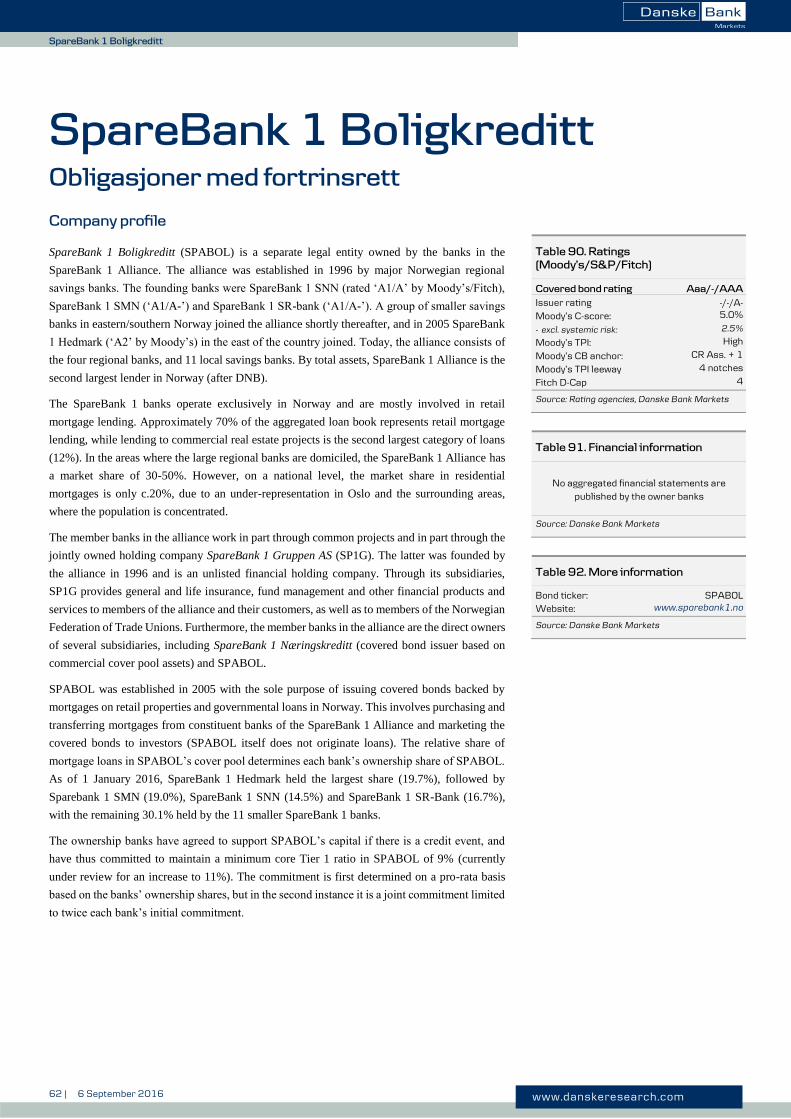

SpareBank 1 Boligkreditt ........................................................................................................................................ 62

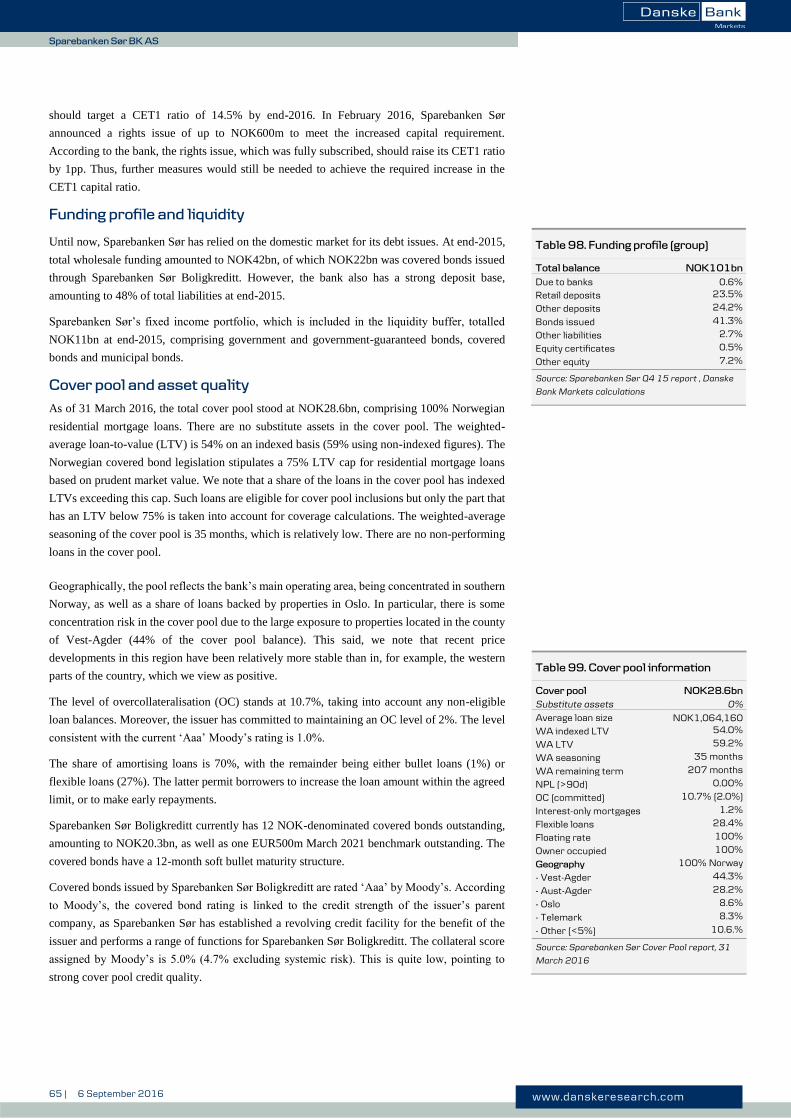

Sparebanken Sør BK AS .......................................................................................................................................... 64

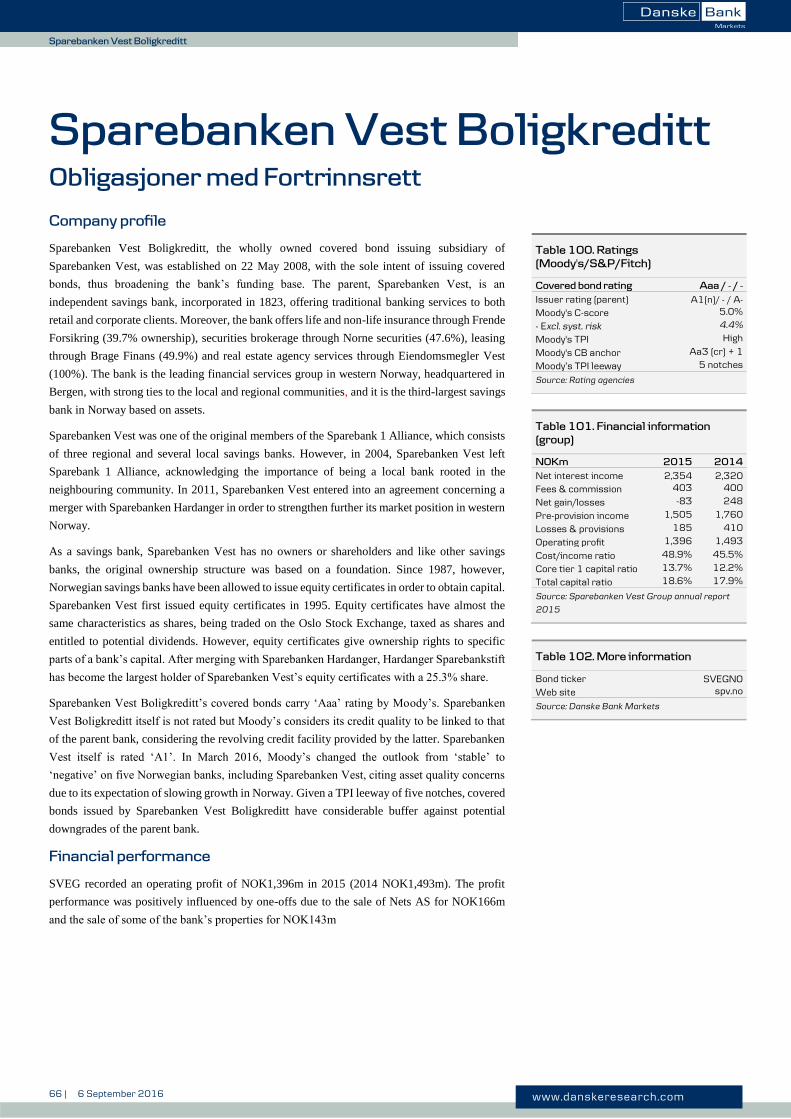

Sparebanken Vest Boligkreditt ............................................................................................................................ 66

SR-Boligkreditt AS ........................................................................................................................................................ 68

Storebrand Boligkreditt ............................................................................................................................................ 70

Swedish Covered Bonds ...................................................................................... 73

Landshypotek Bank AB ............................................................................................................................................. 78

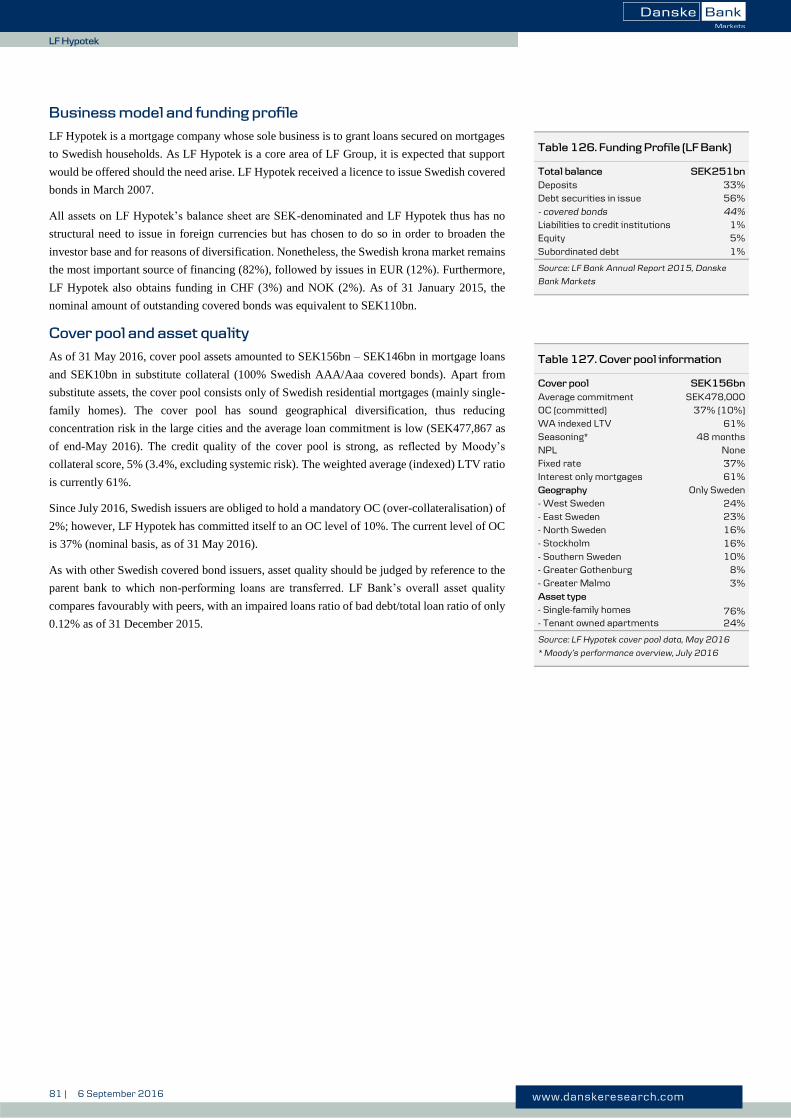

LF Hypotek.......................................................................................................................................................................... 80

Nordea Hypotek ............................................................................................................................................................. 82

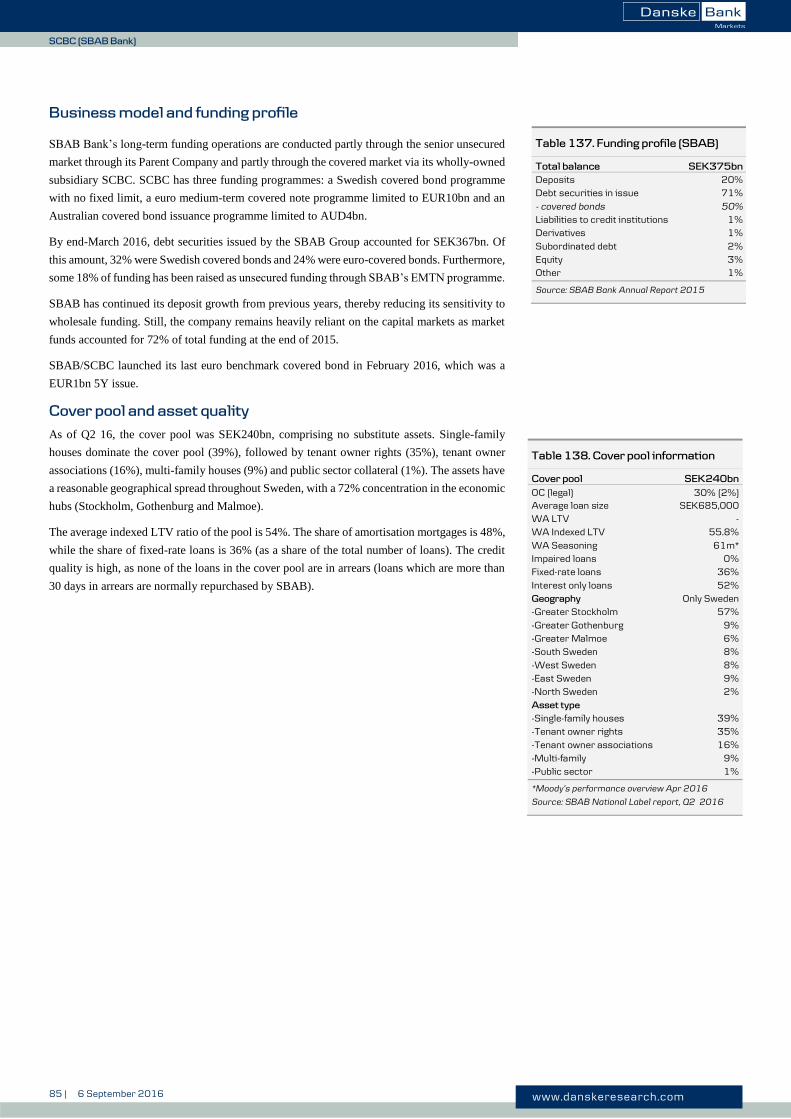

SCBC (SBAB Bank) ...................................................................................................................................................... 84

SEB .......................................................................................................................................................................................... 86

Stadshypotek AB ........................................................................................................................................................... 88

Swedbank Hypotek ....................................................................................................................................................... 90

Covered Bonds Regulatory Framework and Treatment .................. 93

4 | 6 September 2016 www.danskeresearch.com

No

rdic C

overed

Bo

nd

Ha

nd

bo

ok

Nordic Covered Bond Handbook

5 | 6 September 2016 www.danskeresearch.com

Intro

du

ction

Introduction

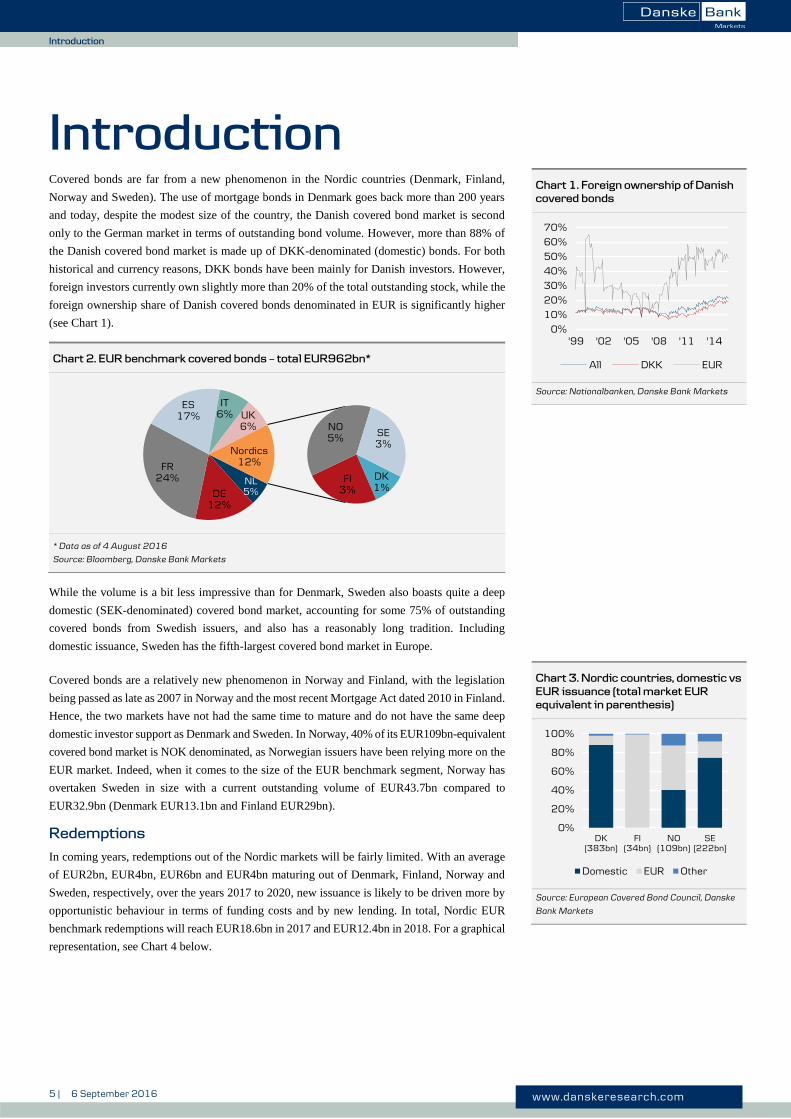

Introduction Covered bonds are far from a new phenomenon in the Nordic countries (Denmark, Finland,

Norway and Sweden). The use of mortgage bonds in Denmark goes back more than 200 years

and today, despite the modest size of the country, the Danish covered bond market is second

only to the German market in terms of outstanding bond volume. However, more than 88% of

the Danish covered bond market is made up of DKK-denominated (domestic) bonds. For both

historical and currency reasons, DKK bonds have been mainly for Danish investors. However,

foreign investors currently own slightly more than 20% of the total outstanding stock, while the

foreign ownership share of Danish covered bonds denominated in EUR is significantly higher

(see Chart 1).

Chart 2. EUR benchmark covered bonds – total EUR962bn*

* Data as of 4 August 2016

Source: Bloomberg, Danske Bank Markets

While the volume is a bit less impressive than for Denmark, Sweden also boasts quite a deep

domestic (SEK-denominated) covered bond market, accounting for some 75% of outstanding

covered bonds from Swedish issuers, and also has a reasonably long tradition. Including

domestic issuance, Sweden has the fifth-largest covered bond market in Europe.

Covered bonds are a relatively new phenomenon in Norway and Finland, with the legislation

being passed as late as 2007 in Norway and the most recent Mortgage Act dated 2010 in Finland.

Hence, the two markets have not had the same time to mature and do not have the same deep

domestic investor support as Denmark and Sweden. In Norway, 40% of its EUR109bn-equivalent

covered bond market is NOK denominated, as Norwegian issuers have been relying more on the

EUR market. Indeed, when it comes to the size of the EUR benchmark segment, Norway has

overtaken Sweden in size with a current outstanding volume of EUR43.7bn compared to

EUR32.9bn (Denmark EUR13.1bn and Finland EUR29bn).

Redemptions

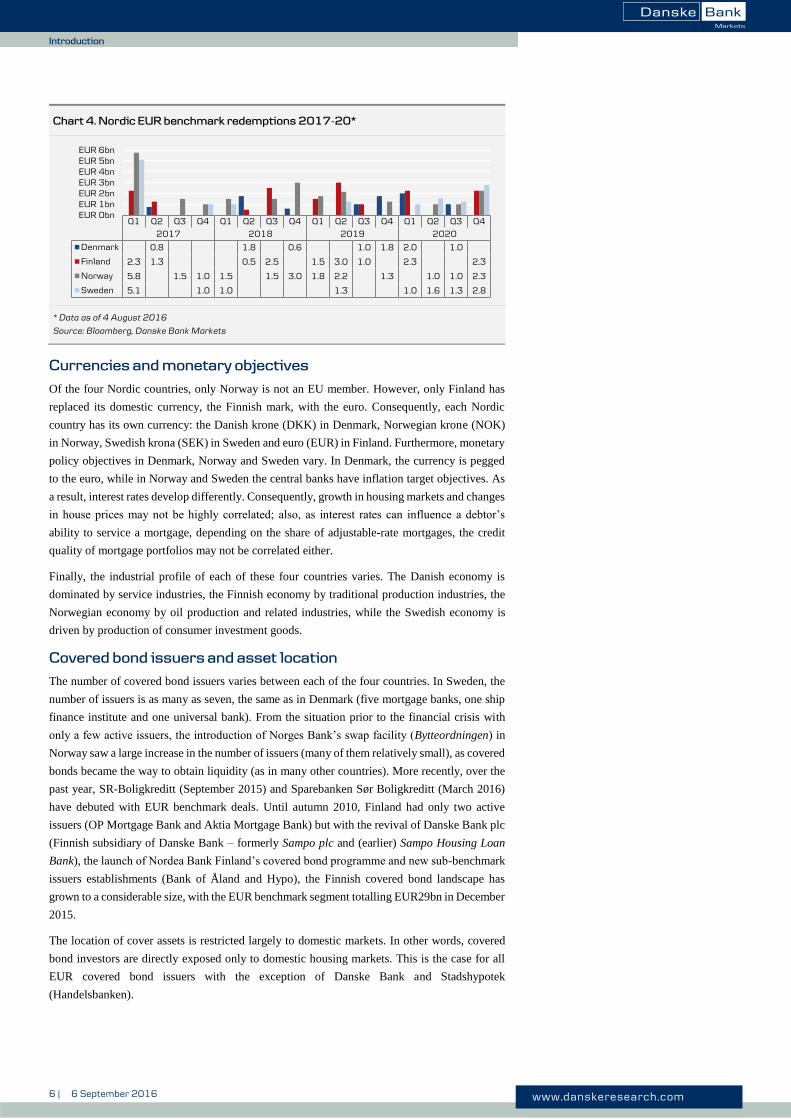

In coming years, redemptions out of the Nordic markets will be fairly limited. With an average

of EUR2bn, EUR4bn, EUR6bn and EUR4bn maturing out of Denmark, Finland, Norway and

Sweden, respectively, over the years 2017 to 2020, new issuance is likely to be driven more by

opportunistic behaviour in terms of funding costs and by new lending. In total, Nordic EUR

benchmark redemptions will reach EUR18.6bn in 2017 and EUR12.4bn in 2018. For a graphical

representation, see Chart 4 below.

NL5%DE

12%

FR24%

ES17%

IT6% UK

6%

DK1%

FI3%

NO5% SE

3%Nordics

12%

Chart 1. Foreign ownership of Danish

covered bonds

Source: Nationalbanken, Danske Bank Markets

Chart 3. Nordic countries, domestic vs

EUR issuance (total market EUR

equivalent in parenthesis)

Source: European Covered Bond Council, Danske

Bank Markets

0%

10%

20%

30%

40%

50%

60%

70%

'99 '02 '05 '08 '11 '14

All DKK EUR

0%

20%

40%

60%

80%

100%

DK(383bn)

FI(34bn)

NO(109bn)

SE(222bn)

Domestic EUR Other

6 | 6 September 2016 www.danskeresearch.com

Intro

du

ction

Introduction

Chart 4. Nordic EUR benchmark redemptions 2017-20*

* Data as of 4 August 2016

Source: Bloomberg, Danske Bank Markets

Currencies and monetary objectives

Of the four Nordic countries, only Norway is not an EU member. However, only Finland has

replaced its domestic currency, the Finnish mark, with the euro. Consequently, each Nordic

country has its own currency: the Danish krone (DKK) in Denmark, Norwegian krone (NOK)

in Norway, Swedish krona (SEK) in Sweden and euro (EUR) in Finland. Furthermore, monetary

policy objectives in Denmark, Norway and Sweden vary. In Denmark, the currency is pegged

to the euro, while in Norway and Sweden the central banks have inflation target objectives. As

a result, interest rates develop differently. Consequently, growth in housing markets and changes

in house prices may not be highly correlated; also, as interest rates can influence a debtor’s

ability to service a mortgage, depending on the share of adjustable-rate mortgages, the credit

quality of mortgage portfolios may not be correlated either.

Finally, the industrial profile of each of these four countries varies. The Danish economy is

dominated by service industries, the Finnish economy by traditional production industries, the

Norwegian economy by oil production and related industries, while the Swedish economy is

driven by production of consumer investment goods.

Covered bond issuers and asset location

The number of covered bond issuers varies between each of the four countries. In Sweden, the

number of issuers is as many as seven, the same as in Denmark (five mortgage banks, one ship

finance institute and one universal bank). From the situation prior to the financial crisis with

only a few active issuers, the introduction of Norges Bank’s swap facility (Bytteordningen) in

Norway saw a large increase in the number of issuers (many of them relatively small), as covered

bonds became the way to obtain liquidity (as in many other countries). More recently, over the

past year, SR-Boligkreditt (September 2015) and Sparebanken Sør Boligkreditt (March 2016)

have debuted with EUR benchmark deals. Until autumn 2010, Finland had only two active

issuers (OP Mortgage Bank and Aktia Mortgage Bank) but with the revival of Danske Bank plc

(Finnish subsidiary of Danske Bank – formerly Sampo plc and (earlier) Sampo Housing Loan

Bank), the launch of Nordea Bank Finland’s covered bond programme and new sub-benchmark

issuers establishments (Bank of Åland and Hypo), the Finnish covered bond landscape has

grown to a considerable size, with the EUR benchmark segment totalling EUR29bn in December

2015.

The location of cover assets is restricted largely to domestic markets. In other words, covered

bond investors are directly exposed only to domestic housing markets. This is the case for all

EUR covered bond issuers with the exception of Danske Bank and Stadshypotek

(Handelsbanken).

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2017 2018 2019 2020

Denmark 0.8 1.8 0.6 1.0 1.8 2.0 1.0

Finland 2.3 1.3 0.5 2.5 1.5 3.0 1.0 2.3 2.3

Norway 5.8 1.5 1.0 1.5 1.5 3.0 1.8 2.2 1.3 1.0 1.0 2.3

Sweden 5.1 1.0 1.0 1.3 1.0 1.6 1.3 2.8

EUR 0bnEUR 1bnEUR 2bnEUR 3bnEUR 4bnEUR 5bnEUR 6bn

7 | 6 September 2016 www.danskeresearch.com

Intro

du

ction

Introduction

Danske Bank includes two non-domestic cover pools in its covered bond programme. The

international cover pool (I) can comprise mortgages from all countries other than Denmark in

which the bank operates. Currently, only mortgages from Norway and Sweden are included in

this pool. In 2010, Danske Bank also launched a combined cover pool – Cover Pool C – currently

containing both residential and commercial mortgages from Norway and Sweden. However,

Danske Bank is in the process of restructuring its covered bond programmes – please see issuer

profile for details.

In late 2011, Stadshypotek added a second cover pool to its covered bond programme. While

the original cover pool remains solely Swedish in its asset composition, the new cover pool

comprises solely Norwegian assets and will be used to obtain NOK funding. However, the

Norwegian pool is very small relative to the Swedish pool, making up only NOK29bn compared

with the SEK641bn Swedish pool (as of June 2016). Furthermore, in 2016, Stadshypotek

announced that it would establish a third cover pool consisting entirely of Finnish residential

collateral.

Nordic housing markets

The large majority of collateral backing Nordic covered bonds is residential mortgages.

Regardless of the unique features of covered bonds, collateral is ring-fenced with the investor

enjoying a dual recourse: firstly to the issuer and secondly to the collateral pool.

Ultimately, regulatory frameworks and housing traditions in the Nordic countries supporting the

credit quality of cover pools become at least as important as specific covered bond acts. In the

(theoretical) case of default by the homeowner as well as the covered bond issuer, payments to

bondholders depend on foreclosure procedures in the country in which the collateral is located.

Based on data from the European Banking Industry Committee, the average duration for the

entire foreclosure procedure in European countries is six to 12 months, although in Italy the

average duration is, exceptionally, five to seven years. As the following table shows, foreclosure

proceedings in the Nordic countries can be carried out relatively quickly compared with in other

European countries.

Table 2. Foreclosure period in housing markets

Finland Sweden Denmark Spain Germany France

3 months 6 months 6 months 9 months 12 months 25 months

Source: European Banking Industry Committee

Finally, should the foreclosure price on a property prove insufficient to cover the outstanding

mortgage debt and additional costs, the mortgage provider has a claim on the borrower. In other

words, borrowers are personally liable for their mortgage loans.

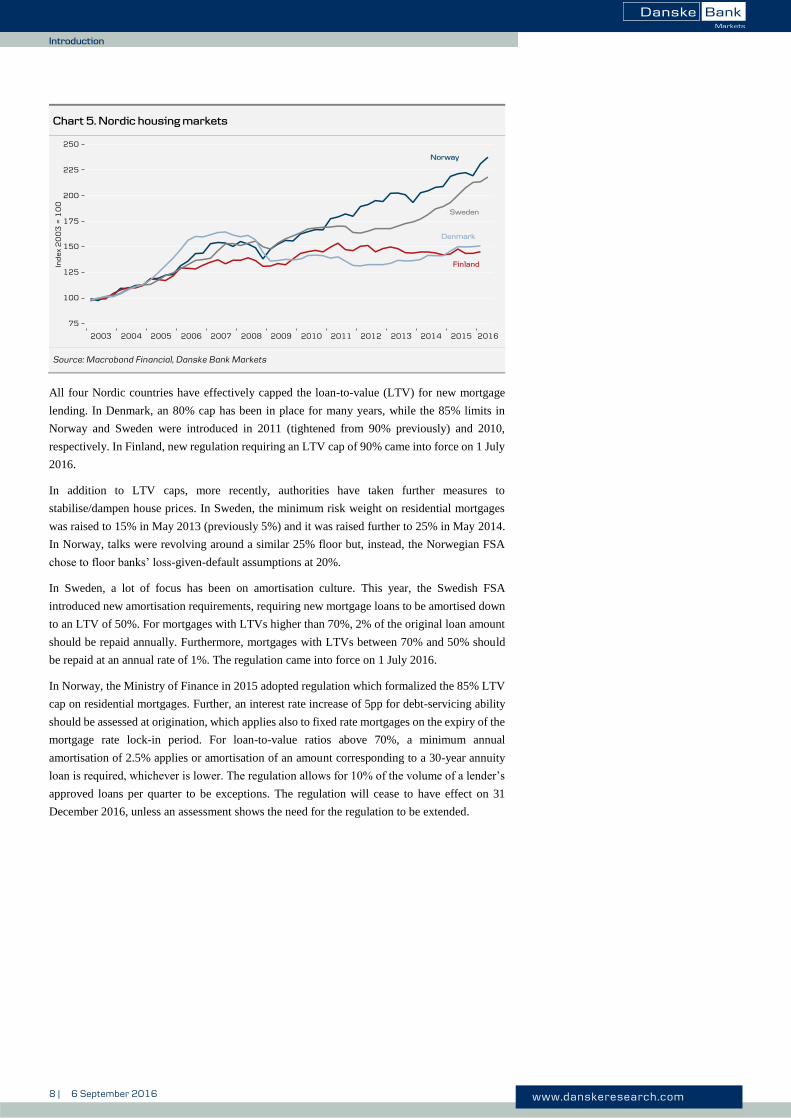

Nordic authorities minding their housing markets

In general, with the exception of Denmark, the Nordic housing markets have all fared fairly well

over the course of the financial crisis. In order to maintain stability, the financial authorities in

the Nordic countries have adopted several measures over the past few years.

8 | 6 September 2016 www.danskeresearch.com

Intro

du

ction

Introduction

Chart 5. Nordic housing markets

Source: Macrobond Financial, Danske Bank Markets

All four Nordic countries have effectively capped the loan-to-value (LTV) for new mortgage

lending. In Denmark, an 80% cap has been in place for many years, while the 85% limits in

Norway and Sweden were introduced in 2011 (tightened from 90% previously) and 2010,

respectively. In Finland, new regulation requiring an LTV cap of 90% came into force on 1 July

2016.

In addition to LTV caps, more recently, authorities have taken further measures to

stabilise/dampen house prices. In Sweden, the minimum risk weight on residential mortgages

was raised to 15% in May 2013 (previously 5%) and it was raised further to 25% in May 2014.

In Norway, talks were revolving around a similar 25% floor but, instead, the Norwegian FSA

chose to floor banks’ loss-given-default assumptions at 20%.

In Sweden, a lot of focus has been on amortisation culture. This year, the Swedish FSA

introduced new amortisation requirements, requiring new mortgage loans to be amortised down

to an LTV of 50%. For mortgages with LTVs higher than 70%, 2% of the original loan amount

should be repaid annually. Furthermore, mortgages with LTVs between 70% and 50% should

be repaid at an annual rate of 1%. The regulation came into force on 1 July 2016.

In Norway, the Ministry of Finance in 2015 adopted regulation which formalized the 85% LTV

cap on residential mortgages. Further, an interest rate increase of 5pp for debt-servicing ability

should be assessed at origination, which applies also to fixed rate mortgages on the expiry of the

mortgage rate lock-in period. For loan-to-value ratios above 70%, a minimum annual

amortisation of 2.5% applies or amortisation of an amount corresponding to a 30-year annuity

loan is required, whichever is lower. The regulation allows for 10% of the volume of a lender’s

approved loans per quarter to be exceptions. The regulation will cease to have effect on 31

December 2016, unless an assessment shows the need for the regulation to be extended.

9 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

Særligt dækkede obligationer and realkreditobligationer

Background

Despite Denmark having a long and internationally recognised tradition of funding residential

and commercial properties by issuing mortgage bonds, in May 2007, a proposal for a new

Mortgage Act was passed, which became effective on 1 July 2007. Executive orders concerning

the Mortgage Act were passed shortly afterwards.

The main reasons for amending the Danish Mortgage Act were to ensure that Danish covered

bonds complied with the EU Capital Requirement Directive (CRD) – and therefore qualified for

preferential risk weighting – and to abandon the specialist banking principle. This enabled

Danish universal banks to access attractive covered bond funding.

Traditionally, Danish mortgage bonds are tapped into the market on a daily basis. Mortgage

bonds are matched with mortgages in order to ensure that mortgage banks are not exposed to

any kind of interest, currency, option or liquidity risk. Furthermore, the Danish mortgage market

is the only one (besides the US) where 30-year, fixed-rate, callable loans remain the predominant

mortgage type. See our Danish Covered Bond Handbook for a more in-depth description of the

traditional Danish mortgage market.

Key elements of the Covered Bond Act

Danish covered bonds fall into three categories.

Særligt dækkede obligationer (SDOs).

Særligt dækkede realkreditobligationer (SDROs).

Realkreditobligationer and Skibskreditobligationer (ROs).

The legal framework for ROs is almost unchanged compared with the previous Mortgage Act.

We expect the market for ROs to be insignificant, as they do not comply with the CRD. Besides

issuer privileges related to SDROs, the primary difference between SDOs and SDROs concerns

the types of substitution assets allowed in the cover pool. However, in both cases eligible

substitution assets must comprise safe and liquid securities, in accordance with the CRD.

The specialist banking principle, allowing only specialised institutions restricted in their

business to issue covered bonds, has been abandoned. This is also the case in Germany, Sweden

and Finland. Specialist mortgage banks still enjoy the privilege of issuing realkreditobligationer

(ROs) and SDROs, while Danmarks Skibskredit has the privilege of issuing

Skibskreditobligationer (ROs).

Danish Covered Bonds

10 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

Universal banks, specialist mortgage banks and Danmarks Skibskredit can apply for the right to

issue SDOs.

In accordance with UCITS 52(4) requirements, the issuer is subject to special public

supervision. The issuer must keep a cover register of collateral (including open hedge

positions) and bonds issued. Collateral assets may include residential and commercial

mortgages, public loans, derivatives and substitute assets. Universal banks issuing SDOs may

also include ships as collateral assets. LTV ratio limits are 80% and 60% for mortgage and

commercial loans, respectively. The LTV ratio is limited to 75% for 30Y interest-only

mortgages. Regarding substitution assets in the form of short-term guarantees from loan-

providing banks or SDOs issued by another credit institution (only when issuing SDOs), the

15% limit on exposure to other credit institutions (according to the CRD) has been abandoned

in the Danish Covered Bond Act. The valuation of cover assets must be carried out in a prudent

manner and not exceed the market value and the assessment must be on an individual basis. If

approved by the Danish FSA, statistical models can be used. Properties in the cover asset pool

must be valued on an ongoing basis, i.e. commercial properties annually and residential

properties every third year. If LTV ratio limits are breached, the issuer is obliged to include

substitution assets in the cover asset pool. Specialist mortgage banks can issue senior debt

secured on the cover pool (ranking second to covered bonds) to fund such assets.

Mandatory minimum over-collateralisation (OC) is fixed at 8% of risk-weighted assets for

specialist mortgage banks, regardless of the type of covered bond issued. There is no legal

minimum OC requirement for universal banks issuing SDOs. Asset segregation and

bankruptcy proceedings concerning bondholders are unchanged in the new legislation but, in

line with other European covered bond acts, the revised act specifies that derivatives

counterparties rank pari passu with bondholders. Lenders of senior debt rank second to covered

bondholders regarding claims for cover assets but rank above lenders of subordinated debt or

hybrid core capital. There is no acceleration of payment following bankruptcy of the issuer.

As regards ALM requirements, the executive order sets strict limits for interest rate risk, currency

risk, option risk and liquidity requirements. We consider Danish ALM requirements to be the strictest

in Europe. Issuers can choose to adhere to one of two different balance principles: the general balance

principle (illustrated below) or the specific balance principle. Regarding liquidity risk, the executive

order states that interest payable to bondholders in any given 12-month period must not exceed interest

received from assets, according to the specific balance principle. Furthermore, NPV coverage is

required.

Table 3. General balance principle

Requirement Universal banks Specialist banks

Interest rate risk - scenario 1 (+/-100bp change in ir. curve)

10% of OC 1% of capital requirement + 2% of voluntary OC

Interest rate risk - scenario 2 (+/-250bp change in ir. curve)

100% of OC 5% of capital requirement + 10% of voluntary OC

Currency risk (+/-10%/50% change in ex. rate)

5% of OC 10% of capital requirement + 10% of voluntary OC

Option risk (+/-100% change in vol. curve)

5% of OC 0.5% of capital requirement + 1% of voluntary OC

Source: Danske Bank Markets

With regard to exposure of cross currencies other than EUR/DKK, the currency risk limit for

specialist mortgage banks is 1% of the capital requirement plus 1% of voluntary OC.

11 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

Below, we show how issuers in the Danish market have positioned themselves regarding the

type of covered bond and type of balance principle. Nordea Kredit and Realkredit Danmark,

owned by the two large banks Nordea and Danske Bank, respectively, are the only ones to issue

covered bonds in the SDRO format and adhere to the specific balance principle. DLR Kredit

also adheres to the specific balance principle. Danmarks Skibskredit is the only issuer that does

not issue CRD-compliant covered bonds. In the case of Danmarks Skibskredit, these non-

compliant bonds are so-called skibskreditobligationer (ROs).

Table 4. Covered bond positions

Issuer Covered bond type Balance principle Issuing principle

BRFkredit SDO & RO General principle Pass-through Danmarks Skibskredit RO Specific principle - Danske Bank SDO General principle Euro style DLR Kredit SDO Specific principle Pass-through Nordea Kredit SDRO Specific principle Pass-through Nykredit/Totalkredit SDO & RO General principle Pass-through Realkredit Danmark SDRO Specific principle Pass-through

Source: Danske Bank Markets

BRFkredit and Nykredit/Totalkredit have opted for the general balance principle and (like DLR

Kredit) issue covered bonds in the SDO format. The main reasons for doing so are to have the

option of carrying out joint funding, to benefit from a slightly more flexible balance principle

and to have the choice of including a broader range of collateral in the cover pool.

Not being a specialised mortgage bank, Danske Bank is allowed to issue covered bonds in the

SDO format only. Obviously, the general balance principle within the ALM suits it best as a

universal bank. So far, Danske Bank has been the only Danish bank to issue covered bonds in a

euro benchmark style.

FSA supervision

The risk profile of mortgage banks is closely monitored by the Danish FSA.

Property valuations are reported directly to the FSA for control purposes. If the value of a

pledged property is set too high, the FSA will carry out a second valuation. If the second

valuation confirms that the value is set too high, the FSA will instruct the mortgage bank to

reduce the size of the loan to observe the maximum LTV ratio.

Reports to the FSA are prepared on a quarterly basis on the following.

Credit risk exposures.

Market risk exposures.

Solvency.

Inspections of mortgage banks by the FSA are performed on a regular basis. During inspections

the FSA will monitor to ensure that risk mitigating procedures are sufficient and adhered to.

On 2 December 2014, the Danish FSA published the final version1 of a ‘Supervisory Diamond’

for mortgage-credit institutions (MCIs). The Supervisory Diamond contains five indicators with

corresponding limits on risk of the mortgage banks. The five indicators are listed on the next

page.

1 A proposal was published on 11 September 2014.

12 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

Chart 6. Supervisory Diamond for Danish mortgage-credit institutions

Source: Danske Bank Markets

1. Lending growth. Growth in lending to individual customer segments should not exceed

15% per year. The four customer segments are private homeowners, rental property,

agriculture and other corporates.

2. Borrower interest-rate risk. Share of lending where Loan-to-Value (LTV) exceeds 75%

of the lending limit for MCIs and where the interest rate is only fixed for up to two years, it

should be less than 25%. Applies only to loans to private homeowners and rental property.

Loans hedged by interest rate swaps and the like are excluded.

3. Interest-only lending to personal borrowers. The share of interest-only loans in the LTV

band above 75% of the lending limit should not exceed 10% of total lending. Interest-only

loans are included regardless of position in order of priority.

4. Loans with short-term funding. The share of lending to be refinanced should be less than

12.5% of the total loan portfolio per quarter and less than 25% of the loan portfolio annually.

5. Large exposures: Sum of the 20 largest exposures should be less than the institution’s CET

1 (core equity tier 1 capital).

The benchmarks for interest-only lending (point 3) and loans with short-term funding (point 4)

are set to apply from 2020, while the other benchmarks are set to apply from 2018.

Our general assessment is that the coming Supervisory Diamond will prompt the mortgage-

credit institutions to maintain their focus on reducing the proportion of interest-only loans and

loans with annual refinancing and on spreading out the auctions.

Along with the Supervisory Diamond, the FSA will launch two initiatives intended to counter

the risk of price bubbles in the real estate market. These initiatives will be implemented via

changes to existing executive orders.

Requirement that private homebuyers should in general provide a 5% deposit.

Rental properties should generally be able to generate positive liquidity before they can be

mortgaged.

Further requirements apply for borrowers seeking a mortgage in so-called growth areas. The

guidance defines growth areas as the largest cities and towns with more significantly

1. Lending growth

2. Borrower

interest-rate risk

3. Interest-only lending

to personal borrowers

4. Loans with short-

term funding

Supervisory

Diamond

5. Large

exposures

13 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

appreciating prices on owner-occupied property and where the price level for apartments and

single-family homes is considerably higher than in the rest of the country. Currently, this applies

to Copenhagen and surrounding districts and Aarhus.

A key point in this guidance applies to mortgages on residential property in growth areas where

the customer opts for an adjustable rate loan. In this instance, the mortgage bank’s assessment

of whether disposable income is sufficient at the time of granting the loan should generally be

based on a fixed interest rate that is 1 percentage point higher than the current fixed interest rate,

though at least 4%, and with a repayment period of maximum 30 years.

Issuers and credit quality

The Danish covered bond set-up is recognised as one of the strongest in the world, with high

systemic support. In particular, the almost non-existent market risk, eliminated by the balance

principle, is a major advantage for traditional Danish covered bonds.

Until June 2011, Danish covered bonds issued by mortgage banks enjoyed the best timely

payment indicator (TPI) possible at Moody’s (‘Very High’). However, for most Danish

mortgage banks, Moody’s changed this one step down to ‘High’ due to the increased use of

loans with embedded refinancing (in contrast to loans where the maturity of the loan is exactly

matched by the maturity of the bond). For specialist lender DLRkredit, this was further reduced

to ‘Probable High’ in July 2011. Covered bonds issued by universal bank Danske Bank were

not affected as they already had a lower TPI score of ‘Probable’.

Besides the TPI revision, Moody’s, in particular, was quite active regarding Danish issuers in 2011.

Issuer ratings came under pressure mainly as a result of Moody’s changed view on the Danish

banking sector and the systemic support expected to be available for banks. The agency

consequently reclassified Denmark from a ‘High’ support country to a ‘Low’ support country in

terms of expected systemic support.

In 2012, in addition to taking action on ratings and rating outlooks, Moody’s raised its OC

requirements for the various mortgage banks. Most Danish mortgage banks decided to end their

collaboration with Moody’s following these events. This means that Nordea Kredit is now the

only Danish covered bond issuer to have its bonds rated by Moody’s. Instead, S&P has become

the main rating agency of Danish mortgage banks.

14 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

Table 5. Capital centres and cover pool overview as of Q1 16

Issuer (capital centre) BRFkredit (E) Danske Bank (C) Danske Bank (D) Danske Bank (I) DLR Kredit

Cover pool (DKKbn) 226 53.9 38.8 120.7 127 OC 6.5% 19.6% 14.9% 13.3% 15.8% WA indexed LTV 63% 55.9% 57.8% 57.3% 58% Interest-only loans 49% 31% 89% 58% 48% Fixed-rate loans 32% 0% 0% 0% 17% Geography (main) 99% DK 69% SE & 21% NO 100% DK 51% NO & 49% SE 99% DK

Issuer (capital centre) Nykredit (E) Nykredit (H) Nordea Kredit Realkredit (S) Realkredit (T)

Cover pool (DKKbn) 341 589 375 222 465 OC 4.3%* 5.2%* 9.8% 8.4% 8.3% WA indexed LTV 64% 62% 64% 61% 63% Interest-only loans 38% 69% 49% 28% 59% Fixed-rate loans 88% 0% 39% 88% 0%

Geography (main) 99% DK 82% DK DK DK DK

*S&P available credit enhancment

Source: Company data, Moody's

Table 6. Rating overview as of Q2 16

Ratings (Moody’s/S&P/Fitch) Moody’s S&P Fitch

Covered bond Issuer/parent C-score/TPI leeway Unused uplift D-Cap/IDR uplift

BRFkredit (E) - /AAA/- -/A-/- 2 notches Danske Bank (C) -/AAA/AAA -A2/A/A N/A 3/2 notches Danske Bank (D) -/AAA/AAA -A2/A/A N/A 3/2 notches Danske Bank (I) -/AAA/AAA -A2/A/A 0 notches 3/2 notches DLR Kredit (B) -/AAA/- -/BBB+/- 0 notches Nykredit (E) -/AAA/- Baa1u/A/A 2 notches Nykredit (H) -/AAA/- Baa1u/A/A 2 notches Nordea Kredit Aaa/AAA/- Aa3/AA-/AA- 13.6%/6 4 notches Realkredit (S) -/AAA/AAA -/-/A 4/N/A Realkredit (T) -/AAA/AA+ -/-/A 2/N/A

Source: Moody’s, Standard & Poor’s, Fitch

15 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danish Covered Bonds

Outlook for the Danish economy

After a very disappointing H2 15, GDP surprised on the upside in Q1 16, growing 0.7% q/q.

Overall, GDP has grown steadily since 2013 but the pace has been quite slow. Progress in the

Danish economy is clearer in the labour market, where employment is up 4% since the low in

Q3 12. Given that Denmark has a small, open economy, it relies on foreign economic conditions

and a positive trend in economic growth in the EU area is of the essence. In the wake of the

Brexit vote, the outlook for the Danish economy has worsened, as the heightened uncertainty

about the future relationship between the UK and the EU may postpone many business

investments in Denmark as well as in Europe in general. GDP growth might be weak in H2 16

but we still expect moderate economic growth in 2016. Our forecasts suggest GDP growth will

be 0.7% in 2016 and 1.0% in 2017. The continued improvement in the Danish economy is

supported by low interest rates and low inflation, which boost purchasing power domestically

as well as abroad.

In 2016 so far, we have seen progress in the housing market. It is driven by increasing income

and employment and low interest rates but not by credit growth, which is still very low. We

expect progress in the housing market to continue over the rest of the year and in 2017. We

expect Brexit to have a negative impact on the labour market but we still forecast an increase in

employment and, as interest rates have gone even lower, we expect this to keep supporting the

housing market. We expect house prices to appreciate by 4.0% in 2016 and 3.2% in 2017.

Apartment prices have appreciated by around 10% across Denmark over the past year. This is

very much a city phenomenon, with the steepest price rises in Copenhagen and Aarhus, which

is also where most apartments are located. Prices here have been given a further boost in recent

years by the large influx of people attracted to the larger cities. While the price increases can be

explained largely by fundamental economic factors, this does not mean prices cannot fall again,

for example if interest rates rise.

Consumer price inflation was very low in the first half of 2016. We still expect inflation to rise

in H2, as the impact of cheaper oil disappears from the figures, although our headline inflation

expectation stands at just 0.5% for 2016. For next year, we expect inflation to increase to 1.3%,

affected by the plans to abolish the so-called Public Service Obligations (PSO) charge on

electricity (however, the government has decided nothing yet). The current low level of inflation

is very much imported. Danish wages and the prices that reflect them are continuing to rise by

almost 2% a year.

In terms of official policy rates, the rate spread between Denmark and the euro area has been

reduced by 0.2 percentage points this year, although the Danish rate is still 0.25 percentage

points below the euro area rate. The previous currency outflow from Denmark reversed to

become a relatively strong inflow in Q2 16. However, this was due not only to the reduced policy

rate spread. The situation in the Danish money market has been another contributing factor,

although that Danmarks Nationalbank is buying foreign currency and selling Danish krone

(DKK) may reduce the pressure on the money market. This has a similar effect to an interest

rate cut, which is why we do not expect an official rate cut any time soon, despite the large FX

inflows. This said, we would not rule out a rate cut entirely, as there has already been some safe-

haven traffic in the direction of Denmark.

Chart 7. Danish economy set to grow

at moderate pace

Source: Statistics Denmark, Danske Bank

Markets

Chart 8. Housing market improving

Source: Statistics Denmark, Danske Bank

Markets

Chart 9. Inflation set to remain low in

2016

Source: Statistics Denmark, Danske Bank

Markets

Chart 10. Extremely low deposit rate

Source: Danmarks Nationalbank, Danske Bank

Markets

Economist Bjørn Tangaa Sillemann +45 45 12 82 29 [email protected]

16 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

BRFkredit

BRFkredit

Company profile

BRFkredit (BRF) was established in 1959 as an independent business foundation authorised to

grant third-lien mortgages. Originally, it was intended that BRFkredit grants mortgage loans for

specific purposes. Until 30 April 2014 BRFkredit was an independent specialist mortgage bank

providing customers with financial solutions and other services connected with real estate and

was wholly owned by BRFfonden, an independent business foundation, through the holding

company BRFholding. On 30. April 2014 a merger between BRFkredit and Jyske Bank A/S

came into effect, and today BRFkredit is owned by Jyske Bank A/S through the holding

company BRFholding A/S. BRFkredit continues as a subsidiary subject to Danish mortgage

finance legislation.

The merger between BRFkredit and Jyske Bank A/S is expected to strengthen the distribution

of banking and mortgage products through an extended base of approx. 900.000 clients, 149

branches, approx. 4,600 employees and a balance sheet of approx. 480bn.

Less than 10 years ago, BRFkredit was the third-largest mortgage bank in Denmark but over the

past couple of years it has lost market share due to weak distribution. Today, Jyske Bank and

BRFkredit is the fourth largest financial institution in Denmark, and BRFkredit has a 9.7%

market share of the total Danish mortgage market.

BRFkredit issues SDO covered bonds in the form of traditional pass-through callable bonds and

bullet bonds. In addition, BRFkredit adheres to the general balance principle.

In December 2012 BRF established an EMTN (Euro Medium Term Notes) programme listed

on Bourse de Luxembourg. Under the EMTN programme, BRF can issue bonds pursuant to §15

of the Danish Mortgage-Credit Act (Senior Secured Notes) and senior debt (Senior Unsecured

Notes) equivalent to up to EUR4bn.

In October 2011 S&P assigned BRFkredit a long-term issuer rating of A- and AAA for covered

bonds issued out of Capital Centres B and E. BRFkredit’s covered bonds issued out of the

General Capital Centre received an AAA rating from S&P in December 2013. For more rating

details, see Chapter 4.

Financial performance

BRFkredit Group reported an operating profit of DKK909m in 2015, an increase from the 2014

level of DKK-348m. Net interest income decreased from DKK2.12bn to DKK1.98bn. Loan

losses and provisions decreased from DKK1.1bn to DKK103m. The core capital ratio increased

from 17.5% as of 31 December 2014 to 18.9% as of 31 December 2015.

The arrears rate (90 days) was 0.3% as at end-September 2015, down from 0.5% in 2014. The

number of repossessed properties decreased from 50 to 41.

Table 7. Ratings (M/S/F)

Covered bond rating WR/AAA/-

Issuer rating WR/A-/-

Source: Rating agencies, Danske Bank Markets

Table 8. Financial information - BRF

DKKm 2015 2014 2009

Net interest income 1,979 2,116 1,730

Fees and commissions 256 185 114

Net gain/losses -354 -636 351

Pre-provision income 1,012 721

Loan losses & provisions 103 1,069 2,125

Operating profit 909 -348 -858

Core capital ratio 18.9% 17.5% 13.3%

Total capital ratio 19.1% 17.7% 13.0%

Arrears rate 0.3% 0.5%

Repossessed properties 41 50

Source: BRFkredit, Danske Bank Markets

Table 9. More info

Bond ticker BRF

Website www.brf.dk

Source: Danske Bank Markets

17 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

BRFkredit

Business model and funding profile

BRFkredit is a specialist mortgage bank subject to supervision by the Danish FSA. BRFkredit

offers mortgages through Jyske Bank A/S and several partnerships. For example, BRFkredit has

entered into agreements with a range of independent real estate agencies and financial

institutions. In 2012 BRFkredit entered into a range of referral agreements with enterprises that

meet the customers before a financing requirement arises, for instance estate agents and

companies operating in energy renovation and large consumer durables. BRFkredit also

distributes mortgages through its website (www.brf.dk) and directly from its headquarters.

BRFkredit primarily offers mortgages secured on properties in Denmark, specialising in those

used for residential properties and office and shop premises. Loans for residential properties,

including owner-occupied homes, co-operative homes, rental homes and publicly subsidised

housing projects, comprise most of the total mortgage book. BRFkredit’s main lending segment

are owner-occupied dwellings and vacation homes (51%), private rentals (18%) and subsidised

housing (18%). BRFkredit offers interest-reset loans (55%), fixed rate callable loans (29%),

floaters 11% and a small share of other types of loans (5%).

Mortgage-backed covered bonds issued by BRFkredit are divided into different cover registers

(capital centres). Bonds issued prior to 31 December 2007 are issued out of capital centre B and

are grandfathered to the CRD. New ROs (Realkreditobligationer) are also issued from Capital

Centre B but they do not comply with the CRD and hence do not get preferential treatment in

terms of risk weighting. According to the revised Mortgage Act, any new SDOs must be issued

out of separate capital centres and new SDOs are issued out of Capital Centre E.

BRFkredit first entered into a joint funding agreement with Jyske Bank and Sydbank in February

2012. Since then, two more banks (Arbejdernes Landsbank and Ringkjøbing Landbobank) have

joined. Furthermore, in October 2013, BRFkredit began funding fixed rate mortgages through the

joint funding agreement. Following the merger in April 2014, the joint funding agreements with

Jyske Bank and Ringkjøbing Landbobank have continued.

The Danish FSA approved the joint funding model in 2012 and it enables financial institutions

to fund private residential mortgage loans through BRFkredit for a fee. The mortgages are

funded through BRFkredit’s SDO covered bond programme and must comply with the

requirements of Danish mortgage finance legislation. Furthermore, the underwriting standards

must comply with BRFkredit’s policies.

The portfolio of jointly funded loans has increased steadily, from DKK5bn at end-2013 to

DKK42bn at end-2015, fuelled primarily by Jyske Bank's focus on the housing area, with loans

jointly funded at BRFkredit. Since the accounts were finalised, the portfolio recorded a further

increase of DKK5bn on 1 January 2016.

BRFkredit announced in February 2016, that it will finance part of the mortgage loans under the

joint funding agreements with bonds denominated in EUR. Since the announcement, BRF has

issued two EUR denominated SDO bonds: EUR 500m in BRF 0.25% Apr-2021 (ISIN

XS1385173734) and EUR 750m in BRF 0.25% Jul-23 (ISIN XS1435774903).

Cover pool and asset quality

At end of Q1 2016, BRFkredit’s cover pool E stood at DKK226bn, made up of 99% Danish-

based loans. The average LTV ratio is 63%. Loans are well diversified; however, the majority

of the properties (46%) are located in the Copenhagen area. Of the cover pool, 55% is residential

property and 11% is commercial. Fixed-rate assets constitute 32% of the pool.

Table 10. Funding profile

Market funds (match-funded) 93%

Other 3%

Equity 4%

Source: BRF, Danske Bank Markets

Table 11. Cover pool info – CC E

Capital Centre E DKK226bn

Junior covered bonds DKK1bnx

WA LTV 63%

OC 6.5%

Fixed-rate loans 32%

IO loans 49%

Geography 99% Denmark

-Copenhagen area 46%

-Zealand & Bornholm 12%

-Northern Jutland

-Eastern Jutland

-Southern Jutland & Funen

7%

19%

15%

Asset type

-Residential 55%

-Subsidised 16%

-Private rental housing 16%

-Commercial 11%

-Other 2%

Source: Investor Report Q1 2016 from BRF and

Danske Bank Markets.

18 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danske Bank

Danske Bank

Company profile

Danske Bank A/S (Danske Bank) is part of the Danske Bank Group, which also includes the

wholly-owned subsidiaries Realkredit Danmark (one of the largest Danish mortgage credit

institutions) and Danica Pension (a leading Danish life insurance company). Danske Bank is the

largest bank in Denmark, where it operates 128 branches and holds market shares in deposits

and lending (excluding mortgage loans issued by Realkredit Danmark) of around 28% and 26%.

However, the group also has a significant international presence, operating in 15 countries. In

addition to Denmark, Danske Bank is one of the largest banks in Northern Ireland and Finland,

and has challenger positions in Sweden, Norway, Estonia, Lithuania and Latvia.

Danske Bank provides a wide range of banking products and services to retail, corporate and

institutional clients. It has three main operating units (Personal Banking, Business Banking,

Corporates & Institutions), as well as Danske Capital (asset management) and Danica Pension.

The group also reports a non-core division (consisting mainly of the portfolio of non-core Irish

exposures, which are being wound up), and other activities (encompassing Group Treasury,

Group IT, Group Services and eliminations).

Danske Bank’s issuer ratings from Moody’s, S&P and Fitch are ‘A2’, ‘A’ and ‘A’, respectively.

The most recent rating action was by Moody’s which lifted its rating by one notch in June 2015,

reflecting the progressive strengthening of the bank's performance in recent years, including

improvements in asset quality and capitalisation. S&P has affirmed the ratings and changed the

outlook to stable reflecting the expectations of stable capital ratios and further earnings

improvements. Danske Bank’s covered bonds issued out of cover pools D, I and C are rated

AAA by S&P and Fitch.

Financial performance

Group net profit for 2015 was DKK13.1bn. The result was affected by goodwill impairments of

DKK4.6bn. Net profit before goodwill impairments rose 36% to DKK17.7bn. Net interest

income was down 4%. The negative short-term interest rates continued to put pressure on deposit

margins and net interest income. Lending volume growth and lower funding costs partly offset

this pressure.

Operating expenses fell 4% to DKK21.8bn, and the cost/income ratio before goodwill

impairments improved 2.1 percentage points to 49.4%. At the end of 2015, the total capital ratio

was 21.0% (2014: 19.3%) and the CET 1 capital ratio was 16.1% (2014: 15.1%). Danske Bank

has set two capital targets: a total capital ratio of at least 17% and a CET1 capital ratio of at least

13%. Danske Bank has met the targets since the end of 2012.

Business model and funding profile

Danske Bank is a universal bank subject to supervision by the Danish FSA. The group has a

well-diversified funding platform including a solid deposit base. Much of the lending consists

of Danish mortgages, financed by Realkredit Danmark (RD) mortgage bonds. However, the

group also issues covered bonds under the Danske Bank name in a SDO format, under the

general balance principle (cf. the Danish Covered Bond Act).

Table 12. Ratings

(Moody’s/S&P/Fitch)

Covered bond rating -/AAA /AAA (D/I/C)

Issuer rating A2 / A / A Fitch D-Cap 3 (D/I/C)

Fitch IDR uplift 2 notches

S&P unused notches: N/A/0/N/A (D/I/C)

Source: Rating agencies, Danske Bank Markets

Table 13. Financial information

DKKm 2015 2014

Net interest income 33,333 34,607

Fees & commissions 10,679 9,814 Net gain/losses 6,908 9,720 Pre-provision income 17,701 11,553

Losses & provisions -61 3,718 Profit before tax 17,762 7,969 Cost/income ratio 59.8% 72.1%

CET 1 capital ratio 16.1% 15.1% Total capital ratio 21.0% 19.3%

Source: Danske Bank Annual Report 2015

Table 14. More information

Bond ticker DANBNK Website www.danskebank.com

Source: Danske Bank Markets

19 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Danske Bank

Danske Bank has established three active cover pools within its EUR30bn covered bond

programme. Cover Pool D comprises 100% domestic mortgages while Cover Pool I and C

include international mortgages originated by Danske Bank, stemming from Norway and

Sweden. Cover Pool C is made up of a diverse combination of loan types, while the I pool is

purely residential, and they are both used for issuance of EUR benchmark covered bonds.

In 2016, Danske Bank announced changes to its cover pool setup. This entails establishing a

new mortgage institution under Swedish law (Danske Hypotek), as well as separating the

Swedish and Norwegian assets contained in cover pool I, and possibly also to some extent cover

pool C, by removing Swedish ‘residential-like’ assets from the latter. When the changes have

been fully implemented, in addition to its existing D-pool, Danske Bank should thus have a new,

purely residential Swedish cover pool in Danske Hypotek, a purely residential Norwegian cover

pool (cover pool I), as well as a combined cover pool of both Norwegian and Swedish assets (C-

pool). The timing for these changes are dependent on the establishment of the new Swedish

mortgage subsidiary. According to Danske Bank, cover pool I will be partly dedicated to NOK

funding. However, regarding both cover pools C and I, the bank states that it will continue to

issue EUR benchmark covered bonds on a regular basis. There is also a Cover Pool R, which

consisted of Irish residential mortgages. The cover pool is inactive, containing no assets, having

been moved to the bank’s non-core business unit.

Danske Bank’s outstanding EUR benchmark covered bonds all have soft bullet maturities,

allowing for a 12-month extension period. Covered bonds secured by Danish cover assets issued

after 1 January 2015, i.e. Cover Pool D, are affected by the new legislation on maturity extension

for Danish covered bonds. According to the legislation, an administrator will have the possibility

of extending the maturity of the covered bonds in the cover pools by up to one year at a time to

avoid temporary shortfalls of liquidity, but only after other refinancing options have been

exhausted. If there is a maturity extension, the interest rate will be fixed at a reference rate plus

a maximum of 5pp. The maturity of new issues will be limited to a minimum of two years.

Cover pool and asset quality

As of 31 March 2016, Cover Pool D totalled DKK38.8bn and consisted exclusively of Prioritet

Plus mortgage loans, which offer the borrower the flexibility to partially draw down or repay

amounts held in a dedicated savings account. In a bank’s default scenario, the borrower cannot

set off the deposit account against its loan account, thus protecting bondholders against set-off

risk. The underlying assets are residential properties in Denmark (92% primary homes, 8%

secondary homes). All the mortgages in Cover Pool D are floating rate. The average indexed

LTV ratio in Cover Pool D is 57.8%. The pool is well seasoned (91 months) and has an OC of

14.9% (of which 2% is committed).

Cover Pool I – the main cover pool – amounted to DKK120.7bn and comprised 51% Norwegian

and 49% Swedish mortgages. Of the mortgages in Cover Pool I, 100% are floating rate. The

average indexed LTV ratio in Cover Pool I is 57.3%. The pool has an overall weighted seasoning

of 49 months. OC stood at 13.3%, of which 2% is committed.

Cover Pool C stood at DKK55.6bn and comprised Swedish and Norwegian floating-rate assets

– mainly offices (42%), rental housing (23%) and manufacturing industries (16%). The average

indexed LTV ratio in Cover Pool C is 55.9%. The 6,436 loans in cover Pool C reflect the more

business-oriented nature of the pool.

Loans in arrears (over 90 days) are not allowed in any of the cover pools. Furthermore, Danske

Bank commits to a voluntary minimum OC of 2% (agreed with the Danish FSA). Approval of

mortgages by Danske Bank is based on a strict credit policy, identical to that of Realkredit

Danmark.

Table 15. Funding profile

Total balance DKK3,293bn

Retail deposits 25% Due to credit & central Inst. 10% Bonds issued by RD 21% Other debt issued 11% Trading portfolio liabilities 14% Liab. (insurance contracts) 9% Subordinated debt 1% Equity 5% Other 5%

Source: Danske Bank Annual Report 2015

Table 16. Cover pool information (D)

Cover Pool D DKK 38.8bn

Number of loans 68,345 OC (committed) 14.9% (2%) WA Indexed LTV 57.8% Seasoning 91 months Arrears (> 90 days) None Floating rate 100% Geography 100% Denmark -Greater Copenhagen 37% -South Denmark 24% -Eastern Jutland 20% -Remaining Zealand 13% -North Jutland 6% Asset type 100% residential -Primary home 92% -Secondary home 8%

Source: Danske Bank ECBC template, Mar 2016

Table 17. Cover pool information (I)

Cover Pool I DKK 120.7bn

Number of loans 128,704 OC (committed) 13.3% (2%)

WA Indexed LTV 57.3%

Seasoning

Arrears (> 90 days)

49 months None

Floating rate 100%

Geography

-Norway 51%

-Sweden 49%

Asset type

-Owner-occupied 79%

-Cooperative housing -Holiday homes

21% 5%

Source: Danske Bank ECBC template, Mar 2016

Table 18. Cover pool information (C)

Cover Pool C DKK53.9bn

Number of loans 6,436 OC (committed) 19.6% (2%) WA Indexed LTV 55.9% Seasoning Arrears (> 90 days)

23 months None

Floating rate 100% Geography -Sweden 69% -Norway 21% Property type -Private rental 23% -Agricultural properties 10% -Cooperative housing 5% -Offices and businesses 42% -Manufacturing industries 16% -Other 4%

Source: Danske Bank ECBC template, Mar 2016

20 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

DLR Kredit

DLR Kredit

Company profile

Dansk Landbrugs Realkreditfond (DLR) is a Danish mortgage lender, specialised in agricultural

and commercial mortgages. DLR was founded in 1960 on the initiative of the banks and savings

banks associations (now the Danish Bankers Association). DLR’s formation was driven by

farmers’ requirements for long-term capital in the 1950s, which were covered only partially by

first- and second-lien mortgage banks. Lack of funding resulting from hesitant lending policies

of first- and second-lien mortgage banks led in part to the establishment of DLR, which was

allowed to operate with a loan-to-value ratio of 70% of DLR’s valuation of the mortgaged

property.

Between its establishment in 1960 and 1 July 2000, DLR operated on its own individual legal

basis pursuant to the DLR Act. DLR’s exclusive right to grant loans based on a LTV ratio of 45-

70% was abandoned from 1 January 1999. DLR became subject to the Mortgage Credit Act as

of 1 July 2000 and in 2001 it became a company limited by shares. Shares in DLR are held by

65 local and regional banks and savings banks. The shareholders are members of Local Banks

in Denmark (39%), members of the Association of Regional Banks (34%), Nykredit (11%),

PRAS A/S (6%), DLR (5%), the Danish centralbank (4%) and other shareholders (0.3%). As

well as providing mortgage loans, DLR has managed the loan portfolio of LR Realkredit

(majority owned by Nordea, Danske Bank, Jyske Bank, SEB and Arbejdernes Landsbank) since

1994. DLR takes no credit risk on this portfolio.

DLR’s market share was 5.2% as at the end of 2015. If we look at DLR’s main lending areas

(agriculture, office and business properties, private rental housing properties and private co-

operative housing properties), the market share was 15.2%.

DLR has a BBB+ issuer-rating from Standard & Poor’s and a AAA covered bond rating (Capital

Centre B and “General Capital Centre”).

Financial performance

DLR Kredit A/S reported operating profit of DKK875m in 2015 – a decrease from the 2014

level of DKK933m. Net interest income increased from DKK1.680bn to DKK1.724bn. Loan

losses and provisions decreased from DKK191m to DKK94m. The core capital ratio increased

from 12.3% to 12.9%.

The arrears rate (3.5 months) as of mid-January 2016 was 1.24%, up from 1.15% as at mid-

January 2015. The number of repossessed properties decreased from 30 as of end 2014 to 26 as

of end 2015.

Table 19. Ratings (M/S/F)

Covered bond rating: WR/AAA/- Issuer rating: WR/BBB+/-

Source: Rating agencies, Danske Bank Markets.

Table 20. Financial info

DKKm 2015 2014 2009

Net interest income 1,724 1,680 1,047

Fees and commissions -217 -172 -240

Net gain/losses -330 -188 -14

Pre-provision income 969 1,124

Loan losses & provisions 94 191 159

Operating profit 875 933 450

Cost/income ratio 27% 30% 45%

Core capital ratio 12.9% 12.3% 11.6%

Total capital ratio 12.9% 12.3% 11.7%

Arrears rate 1.24% 1.15%

Repossessed properties 26 30

Source: DLR Kredit, Danske Bank Markets

Table 21. More info

Bond ticker LANDBR

Website www.dlr.dk

Source: Danske Bank Markets

21 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

DLR Kredit

Business model and funding profile

DLR is a specialist mortgage bank subject to supervision by the Danish FSA. DLR provides

mortgages through the branch networks of its shareholder banks. In order to support the

customer advisory services of the banks in connection with mortgage loans DLR has developed

an electronic communications system – DLRxperten. DLR has no branches itself.

DLR only offers mortgages secured on properties in Denmark. It focuses on mortgages on

agricultural and commercial properties as well as co-operative homes, rental homes and publicly

subsidised housing projects. The bank offers interest-reset loans (52%), fixed rate callable loans

(17%) and floating rate loans (31%). All mortgages are based on the pass-through principle,

meaning that consumers have a delivery option on underlying bonds. Interest-reset loans are

funded by issuing a portfolio of fixed rate, non-callable bonds, while other types of mortgages

are funded individually by issuing bonds with exactly the same characteristics as the mortgages.

DLR has a management agreement with all shareholder banks, which requires loan-providing

banks to put up an individual loan loss guarantee covering the most risky part of each mortgage.

The agreement includes all commercial properties.

As a result, DLR’s risk of losses arising from the granting of loans for the property types

mentioned is very limited. Loans for agricultural properties are also protected by a collective

guarantee scheme set up between DLR and the loan-providing banks, which comes into force in

the event that the losses suffered by DLR within a given financial year exceed a given level. The

guarantee scheme means that DLR’s risk of losses arising from the granting of loans for

agricultural properties is relatively limited. As at the end of Q1 2016, the guarantee scheme

covered 90% of DLR’s total loan portfolio; the remaining loans often have a very low LTV.

Mortgage-backed covered bonds issued by DLR are divided into different cover registers

(capital centres). According to the revised Mortgage Act, any new SDOs must be issued out of

separate capital centres. By the end of 2007 DLR closed and subsequently grandfathered the

existing series in General Capital Centre, according to the Capital Requirement Directive

(CRD), with new SDOs issued out of Capital Centre B.

Cover pool and asset quality

As of Q1 2016 DLR’s capital centre B totalled DKK127bn and consisted mainly of Danish-

based assets, distributed as 62% in agricultural assets and 18% in commercial assets. All assets

are geographically well diversified with a slight tendency to be concentrated in Jutland.

Approval of mortgages by DLR is based on a strict credit policy. Only mortgages on properties

stated in the Mortgage Act are allowed in the cover pool. The LTV ratio on each mortgage is

monitored on an ongoing basis while the borrower’s ability to pay is reviewed each month.

Table 22. Funding profile

Market funds (match-funded) 91%

Equity 8%

Other 1%

Source: DLR, Danske Markets

Table 23. Cover pool info – CC B

DLR Kredit DKK127bn

WA LTV 58%

OC 15.8%

Fixed rate loans 17%

IO-loans 48%

Geography 99% Denmark

-Copenhagen area 6%

-Zealand 13%

-South Denmark 28%

-Jutland 51%

-International 1%

Asset type

-Owner-occupied 5%

-Agricultural 62%

-Commercial 18%

-Rental housing 11%

-Co-operative housing 2%

Source: Cover pool report Q1 2016 from DLR and

Danske Bank Markets

22 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Nordea Kredit

Nordea Kredit

Company profile

Nordea Kredit Realkreditaktieselskab (NOR) is a wholly-owned subsidiary of Nordea Bank

Danmark, which is part of the Nordea Group. In 1997 Swedish Nordbanken merged with Finnish

Merita Bank to form MeritaNordbanken. In 2000 Danish Unibank merged with

MeritaNordbanken, which, at the same time, changed its name to Nordea. Later in 2000 the

Norway-based Christiania Bank joined the newly formed Scandinavian banking group. Today

Nordea is the largest bank in Scandinavia with activities in Scandinavia, the Baltic region and

Russia.

Nordea’s main business areas include retail banking, corporate banking, asset management, life

insurance and pensions and mortgage finance.

NOR began its mortgage activities in September 1993. Initially, it provided only lending for

residential properties and holiday homes. Currently, however, mortgage loans are offered for

most types of property. NOR’s share of the domestic mortgage market as at Q1 2016 was 15.0%

(mortgage loans at nominal value as a share of all Danish mortgage bank loans).

Nordea’s long-term issuer ratings by Moody’s, S&P and Fitch are A1, AA- (negative outlook)

and AA-, respectively. Covered bonds issued by NOR have Aaa and AAA ratings from Moody’s

and S&P, respectively. For more rating details, see Chapter 4.

Financial performance

Nordea Kredit reported operating profit of DKK1.9bn for 2015, an increase from the 2014 level

of DKK1.8bn. Net interest income increased from DKK2.7bn to EUR2.8bn and loan losses and

provisions decreased from DKK366m to DKK114m. The core capital ratio and the total capital

ratio increased from 28.6% as of 31 December 2014 to 29.7% as of 31 December 2015.

The arrears rate (3.5 months) for residential properties and holiday homes for Nordea Kredit was

0.17% as at end-2015, down from 0.24% as at end-2014. The number of repossessed properties

fell from 41 to 35.

Business model and funding profile

NOR is a specialist mortgage bank subject to supervision by the Danish FSA. The objective of

NOR is to carry on business as a mortgage bank, including any kind of business permitted

pursuant to the Danish Mortgage Act. NOR only has mortgage credit activities in Denmark,

while all mortgages in the cover pool are secured on properties situated in Denmark. All

mortgages included in the cover pool are distributed through Nordea’s branch network and that

of the real estate chain, DanBolig.

A management agreement exists between NOR and Nordea Bank Danmark. It states the

following: Nordea Bank Danmark A/S provides a guarantee for the upper 25% of mortgage

loans originated by the bank. For loans granted for non-profit housing, youth housing and

housing for the elderly, there is only a 10% guarantee. For loans for all-year dwellings, co-

operative housing, private rental housing, non-profit rental housing and properties for social,

cultural and educational purposes, the guarantee covers that part of the mortgage loan that

exceeds 60% of the valuation made in conjunction with the loan origination process. For loans

granted to agricultural properties, the guarantee covers that part of the mortgage loan that

exceeds 55% of the valuation made in conjunction with the loan origination process.

Table 24. Ratings (M/S/F)

Covered bond rating Aaa/AAA/-

Issuer rating Aa3/AA-/AA-

Source: Rating agencies, Danske Bank Markets

Table 25. Financial info

DKKm 2015 2014 2009

Net interest income 2,791 2,679 5,281

Fees and commissions 2,135 2,066 1,693

Net gain/losses 124 274 1,946

Pre-provision income 2,027 2,141 4,513

Loan losses & provisions 114 366 1,486

Operating profit 1,913 1,775 3,027

Cost/income ratio 10.6% 8.6% 50%

Core capital ratio* 29.7% 28.6% 10.2%

Total capital ratio* 29.7% 28.6% 11.9%

Arrears rate** 0.17% 0.24%

Repossessed properties 35 41

*Excluding Basel I floor

**Residential properties and holiday homes

Source: Nordea, Danske Bank Markets

Table 26. More info

Bond ticker: NDASS

Website www.nordea.com

Source: Danske Bank Markets

23 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Nordea Kredit

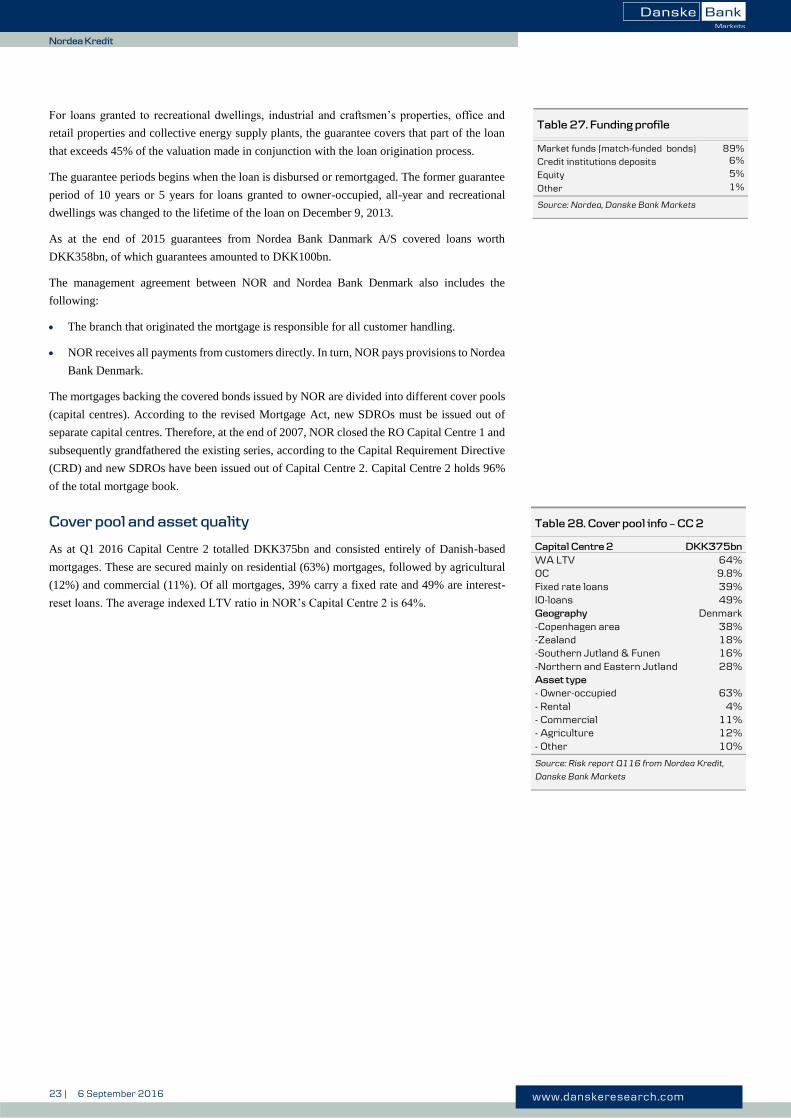

For loans granted to recreational dwellings, industrial and craftsmen’s properties, office and

retail properties and collective energy supply plants, the guarantee covers that part of the loan

that exceeds 45% of the valuation made in conjunction with the loan origination process.

The guarantee periods begins when the loan is disbursed or remortgaged. The former guarantee

period of 10 years or 5 years for loans granted to owner-occupied, all-year and recreational

dwellings was changed to the lifetime of the loan on December 9, 2013.

As at the end of 2015 guarantees from Nordea Bank Danmark A/S covered loans worth

DKK358bn, of which guarantees amounted to DKK100bn.

The management agreement between NOR and Nordea Bank Denmark also includes the

following:

The branch that originated the mortgage is responsible for all customer handling.

NOR receives all payments from customers directly. In turn, NOR pays provisions to Nordea

Bank Denmark.

The mortgages backing the covered bonds issued by NOR are divided into different cover pools

(capital centres). According to the revised Mortgage Act, new SDROs must be issued out of

separate capital centres. Therefore, at the end of 2007, NOR closed the RO Capital Centre 1 and

subsequently grandfathered the existing series, according to the Capital Requirement Directive

(CRD) and new SDROs have been issued out of Capital Centre 2. Capital Centre 2 holds 96%

of the total mortgage book.

Cover pool and asset quality

As at Q1 2016 Capital Centre 2 totalled DKK375bn and consisted entirely of Danish-based

mortgages. These are secured mainly on residential (63%) mortgages, followed by agricultural

(12%) and commercial (11%). Of all mortgages, 39% carry a fixed rate and 49% are interest-

reset loans. The average indexed LTV ratio in NOR’s Capital Centre 2 is 64%.

Table 27. Funding profile

Market funds (match-funded bonds) 89% Credit institutions deposits 6%

Equity 5%

Other 1%

Source: Nordea, Danske Bank Markets

Table 28. Cover pool info – CC 2

Capital Centre 2 DKK375bn

WA LTV 64% OC 9.8% Fixed rate loans 39% IO-loans 49% Geography Denmark -Copenhagen area 38% -Zealand 18% -Southern Jutland & Funen 16% -Northern and Eastern Jutland 28% Asset type - Owner-occupied 63% - Rental 4% - Commercial 11% - Agriculture 12% - Other 10%

Source: Risk report Q116 from Nordea Kredit,

Danske Bank Markets

24 | 6 September 2016 www.danskeresearch.com

Da

nish

Co

vered B

on

ds

Nykredit/Totalkredit

Nykredit/Totalkredit

Company profile

Nykredit Realkredit (NYK) is a wholly-owned subsidiary of Nykredit Holding. Nykredit

Holding is an unlisted holding company owned by Foreningen Nykredit (90%), Industriens

Realkreditfond (5%), Foreningen Østifterne (3%) and PRAS (2%). As a mortgage association,

NYK originated in 1851. Today, besides mortgage finance, NYK is active in retail and corporate

banking, asset management, insurance and real estate. Mortgage finance is the most important

business area. Nykredit announced in February 2016 that it is planning a stock exchange listning

which is expected to be ready within a period of 12-24 months.

In 2003 NYK acquired Totalkredit (TOT), which is currently a wholly-owned subsidiary of

NYK. Following the acquisition of TOT, NYK became the largest specialist mortgage bank in

Denmark with a current market share based on outstanding mortgages of 41.3%. There are nearly

60 partner banks in the TOT corporation network, making it crucial for the distribution of NYK

mortgages. NYK and both local and regional banks are competitors in agricultural mortgage and

non-mortgage markets. In 2008 NYK acquired Forstædernes Bank, which increased NYK’s

market share within banking to 5.2%. Forstædernes Bank has subsequently been merged with

Nykredit Bank.

Nykredit’s covered bonds issued out of Capital Centre E and H are rated AAA by S&P. Nykredit

has a A long-term rating from S&P and Fitch. For more rating details, see Chapter 4.

Financial performance

Nykredit Group reported operating profit of DKK4.7bn in 2015 – a significant increase from the

2014 level of DKK-186m. Net interest income increased from DKK11.4bn to DKK11.9bn and

loan losses and provisions decreased from DKK2.4bn to DKK0.9bn.

The core capital ratio increased from 15.4% as of end-2015 to 19.4% as of end and the total

capital ratio increased to 18.2% from 23.9%. The arrears rate (75 days) as of September 2015

was 0.39% – a fall from the 2014 level. The number of repossessed properties decreased from

356 to 159.

Business model and funding profile

NYK is a specialist mortgage bank subject to supervision by the Danish FSA. Banking, asset

management and insurance activities are carried out by wholly-owned separate subsidiaries of

NYK. As mentioned above, TOT is also a wholly-owned subsidiary of NYK. Retail and

commercial customers are offered mortgages through Nykredit’s distribution channels, which

include 54 customer centres, Nykredit.dk, mobile app downloads, a central customer services

centre and the real estate agencies of the Nybolig and Estate chains. Like NYK, TOT is a

specialist mortgage bank under the supervision of the Danish FSA.