The New Revenue Recognition Rules - Systems, Data, Reporting and Creating a Transparent Audit Trail

54

The New Revenue Recognition Rules: Systems, Data, Reporting and Creating a Transparent Audit Trail May 21, 2015

Transcript of The New Revenue Recognition Rules - Systems, Data, Reporting and Creating a Transparent Audit Trail

The New Revenue Recognition Rules:

Systems, Data, Reporting and Creating a Transparent Audit Trail

May 21, 2015

2 © 2015 Protiviti Inc.

You can download a copy of the presentation via the Resources Area on your screen. Following

the webinar, all attendees will receive a link to a copy of the presentation and recording.

During the webinar you can ask questions by clicking on the Questions Area on your screen. Please

provide your e-mail address for a swift reply.

There will be a Q&A session at the end of the webinar.

If you are having trouble hearing the audio through the computer, a separate phone line is available.

US/Canada Line +1 (855) 707-0664

International Line +1 (734) 385-2579

Conference ID 28330988

A Reminder…

3 © 2015 Protiviti Inc.

• We are offering 1.5 CPE credits for this webinar

• To be eligible to receive these credits, please ensure you answer at least four (4) out

of the five (5) polling questions

• You will receive the CPE certificate via e-mail approximately 2-4 weeks after the

webinar date

• In the Resources Area, you can:

− Save/Print copy of today’s presentation

− Download Protiviti's Revenue Recognition Flash Reports

CPE Credits and Supplemental Information

If you are having trouble hearing the audio through the computer, a separate phone line is available.

US/Canada Line +1 (855) 707-0664

International Line +1 (734) 385-2579

Conference ID 28330988

4 © 2015 Protiviti Inc.

Find additional resources on revenue recognition, including webcasts and more at:

www.financialexecutives.org/revrec

FEI Resources on Revenue Recognition

5 © 2015 Protiviti Inc.

Kevin Swartzendruber is vice president and corporate controller

for Flextronics International Ltd., a leading end-to-end supply

chain solutions company with $26 billion in sales generated a

through a network of facilities and innovations centers in

approximately 30 countries and across four continents, and

employing approximately 200,000 globally. During his almost ten

year tenure with Flextronics, Kevin has also served as an

assistant corporate treasurer and director of SEC reporting and

technical accounting. Prior to joining Flextronics Kevin was a

director of SEC reporting and technical accounting with EchoStar

(Dish Network) and was also with Deloitte first in its Denver

practice’s audit group and later in mergers and acquisitions in

San Francisco. Kevin is a Certified Public Accountant and

received his Bachelors of Business Administration in accounting

and finance, with honors, from the University of Cincinnati. To

learn more about Flextronics, visit www.flextronics.com.

E-mail: [email protected]

Speakers

Trouble hearing the audio through the computer? Dial in! Phone: (855) 707-0664; International (734) 385-2579,

Conference ID: 28330988

6 © 2015 Protiviti Inc.

Raji Gunasekera is Senior Director, Assistant Corporate

Controller at Flextronics. Raji joined Flextronics as a Director in

the Corporate Accounting group four years ago to oversee the

Company’s SEC reporting and technical accounting functions.

He has expanded his responsibilities in to consolidations, month

end close processes and other core accounting and finance

functions within the Corporate Accounting group. Prior to joining

Flextronics, Raji was with PwC for almost 9 years, of which 3

years with their firm in Botswana and 6 years in their technology

audit practice in San Jose. Raji is a Certified Public Accountant

holding a license in California and also a Chartered Accountant

from Sri Lanka. To learn more about Flextronics, visit

www.flextronics.com.

E-mail: [email protected]

Speakers

Trouble hearing the audio through the computer? Dial in! Phone: (855) 707-0664; International (734) 385-2579,

Conference ID: 28330988

7 © 2015 Protiviti Inc.

Chris Wright, from Protiviti’s New York office, is the firm-wide

Managing Director of our Finance Remediation and Reporting

Compliance group. Chris is also the Regional Managing Director

for Protiviti’s Eastern Region in the United States. He has over

twenty-five years of experience serving clients as an external

auditor, including 6 years as a partner at two global accounting

firms (Arthur Andersen and KPMG), and as an internal auditor and

financial reporting risk consultant.

E-mail: [email protected]

Speakers

Trouble hearing the audio through the computer? Dial in! Phone: (855) 707-0664; International (734) 385-2579,

Conference ID: 28330988

8 © 2015 Protiviti Inc.

Steve Hobbs is a Managing Director in the San Francisco office

of Protiviti and is the global leader of the firm’s Public Company

Transformation solution. He has over 30 years of experience

providing business consulting and financial reporting services to

clients in various industries, primarily technology and consumer

products entities. Prior to joining Protiviti in 2006, Steve was a

partner at KPMG for three years and spent nearly 20 years at

Arthur Andersen, where he was also a partner. He has served on

the board of directors at three companies, one as Chairman and

two as Audit Committee Chair. Steve has served over 100 public

companies during his career with assistance in corporate

governance, financial reporting, and numerous business

transformation issues.

E-mail: [email protected]

Speakers

Trouble hearing the audio through the computer? Dial in! Phone: (855) 707-0664; International (734) 385-2579,

Conference ID: 28330988

9 © 2015 Protiviti Inc.

Siamak Razmazma has over 25 years of experience in enterprise

systems and business process automation. He provides advisory

and assurance services to executive management and process

leads assisting them with defining the business systems strategy

and selecting the appropriate solutions. Siamak is a thought

leader in designing solutions supporting ERP and enterprise

system strategies that help organizations achieve measurable

return on their investment. He has played a leading role in the

conception of an innovative and holistic approach to optimize and

automate business processes centered on enterprise systems

such as SAP, Oracle, Microsoft, NetSuite, Hyperion, and Revenue

Recognition Automation tools.

E-mail: [email protected]

Speakers

Trouble hearing the audio through the computer? Dial in! Phone: (855) 707-0664; International (734) 385-2579,

Conference ID: 28330988

Webinar Agenda

11 © 2015 Protiviti Inc.

Future Revenue Recognition Webinars

Protiviti and FEI are please to offer a five-part webinar series on the new Revenue

Recognition Standard, recently issued by the Financial Accounting Standards Board

(FASB). Participants will learn how to implement an appropriate transition plan to the

new standard and why this plan must be cross-functional in nature. Webinars will occur

approximately every 60 days following the prior webinar, ending in mid-2015.

Webinar Series

• Listen to the recorded version of our November 20th, January 20th and March18th

webinars: http://www.protiviti.com/en-US/Pages/Webinars.aspx

• Next webinar: July 23, 2015

- An invitation will follow this event

• Future webinar topics:

- More transition considerations

- Industry implications

Future Revenue Recognition Webinars

12 © 2015 Protiviti Inc.

Today We Will Cover…

Transition Strategy and the Six Elements of

Infrastructure

Overview of the New Standard

Impact on Systems and Data

Reporting Considerations

13 © 2015 Protiviti Inc.

Six Elements of Infrastructure

About the Six Elements

• The six elements of infrastructure (six elements) is a useful tool for categorizing issues,

understanding where problems are occurring within the organization, and drawing conclusions to

form the basis for recommendations.

• In Protiviti’s view, the elements of infrastructure should be considered when designing a new process

or assessing an existing process. Also, the six elements are common to each process or function.

• These elements represent the capabilities that each process or function should possess; and they

provide a comprehensive and consistent framework to communicate the requirements for the

appropriate operation of a process or function.

• While these elements are not necessarily intended to be a strictly linear process, the components of

the framework are generally designed from left to right. The use of this structure helps organize the

otherwise complex network of risk management activities into a comprehensive and consistent

framework. In particular, it ensures that all key components are appropriately considered.

• In planning to adopt the new revenue standard, companies would benefit from considering the six

elements of infrastructure.

Key elements of infrastructure must be linked by design:

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

14 © 2015 Protiviti Inc.

PCAOB Issues Practice Alert

Related to Auditing Revenue

FASB Considering Revenue Recognition Delay to Reduce Uncertainty

15 © 2015 Protiviti Inc.

Effective Date of Revenue Recognition Standard to be Deferred

• The Financial Accounting Standards Board (FASB)

voted to defer, by one year, the effective date of its

new revenue recognition standard

• Issued almost a year ago, this new guidance

resulted from a collaborative effort by the FASB

and International Accounting Standards Board to

agree on a global standard based on common

principles that can be applied across industries and

regions

• The FASB voted for a one-year deferral of the

effective date of the new standard and has issued

an exposure draft proposing the deferral, with a

30-day comment period

• We anticipate there will be an impact on public and

nonpublic entities

Source: Protiviti Flash Report – Effective Date of Revenue Recognition Standard to

be Deferred

16 © 2015 Protiviti Inc.

Impact on Public and Private Companies

• The standard, as originally issued, is expected to be effective for fiscal years beginning

after December 15, 2017, and interim periods thereafter

• The proposal would now require application of the new standard no later than annual

reporting periods beginning after December 15, 2018, including interim reporting periods

therein

For example, a calendar year reporting company would be required to apply the new standard

during 2019, including the interim periods therein

Private Companies

• In the original release, the new standard is expected to be effective for fiscal years

including interim periods beginning after December 15, 2016

• The proposal would now require application of the new standard no later than annual

reporting periods beginning after December 15, 2017, including interim reporting periods

therein

For example, a calendar year reporting company would now be required to apply the new

standard during 2018, including the interim periods therein

Public Companies

17 © 2015 Protiviti Inc.

The FASB’s Proposal…

• Public companies would be permitted to elect to

early adopt the new standard as the original

effective date – in effect, a year earlier than the

proposed new effective date

• Nonpublic entities may elect to apply the

amendments as part of the original effective date

for public companies

• The proposal is based on FASB’s outreach to

various stakeholders

• Determined that a deferral is necessary to provide

companies adequate time to effectively implement the

new standard

• The IASB has not provided a specific timeline to

make a decision regarding a potential delay in its

original effective date.

18 © 2015 Protiviti Inc.

What Does the Deferral Mean?

Not a Surprise1

Not only was it expected, but it has been an assumption baked into the planning and

implementation practices among many companies that have started the transition to the new

standard in earnest

“Full Steam Ahead”2

Public companies should continue to work on transitioning to the standard, especially for those

who many not have begun working on the transition process

Nearly Half of the Year is Gone3

The only delay is in the effective date of the standard; there should be no delay in management’s

efforts to position the organization in a prudent state of readiness

19 © 2015 Protiviti Inc.

Early Adoption Option

Presents an opportunity for those who have started, were focused on the new

standard and now are, or will be, ready to adopt early

Another choice to add to the list of decisions for companies when determining

whether to adopt prospectively or retrospectively

Include your audit committee and external auditor when making this decision

Analysts, regulators, lenders and other stakeholders may have an interest in

this aspect of the organization’s decision

20 © 2015 Protiviti Inc.

Use this time wisely Don’t take your foot off of the gas1 2

Keep working through an

adoption plan rather than

deferring preparations

There is not a lot of time to waste3 4

Don’t stop and continue

waiting

Other uncertainties still loom over

adoption efforts (e.g. IASB)5 6

Recommendations

21 © 2015 Protiviti Inc.

A. Yes

B. No, but it is on my to-do list

Have you read the new Financial Accounting Standards Board (FASB)

Accounting Standards Update No. 2014-09, Revenue from Contracts with

Customers (new revenue recognition standard), issued on May 28, 2014?

Reminder: Answer 4 out of 5 questions to qualify for CPE credit.

Poll Question #1

Overview of the New Standard

23 © 2015 Protiviti Inc.

New Revenue Recognition Standard – Overview

Final Standard Released May 28, 2014

Transition Approaches

• Retrospective, or

• Cumulative effect at the date of adoption

Objective of project

• Achieve a single, comprehensive revenue recognition

model

Removes existing industry specific guidance

Expands qualitative and quantitative disclosures

Still a lot of uncertainty on the impact of this new standard

Core Principle: Revenue recognition depicts transfer of promised goods or services to customer

in an amount that reflects the consideration to which the entity expects to be entitled in

exchange for those goods or services

24 © 2015 Protiviti Inc.

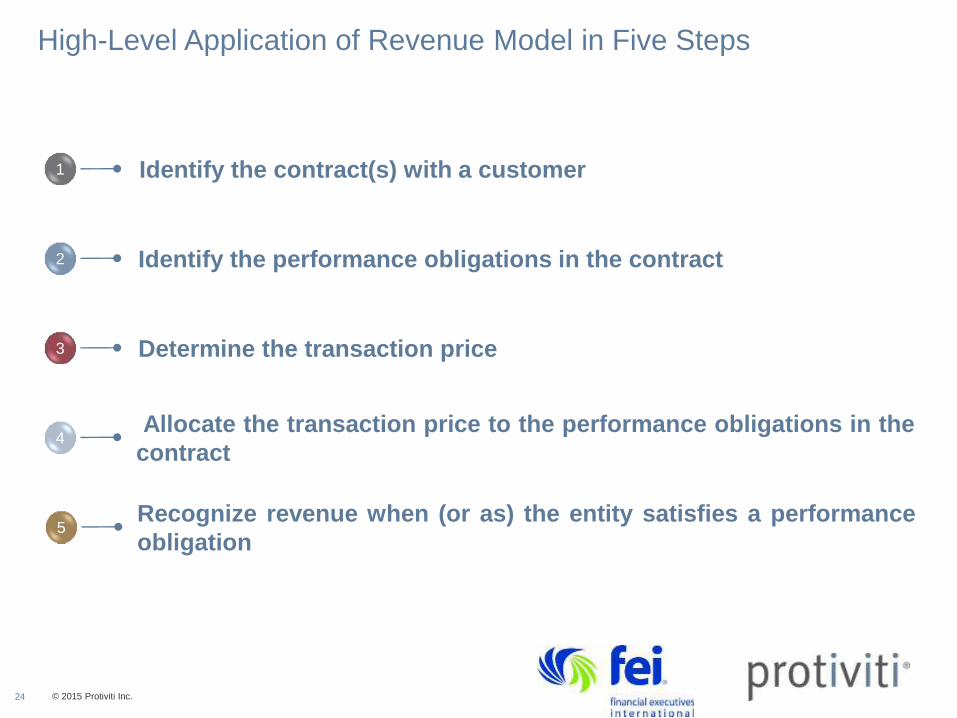

High-Level Application of Revenue Model in Five Steps

Identify the contract(s) with a customer1

Identify the performance obligations in the contract 2

Determine the transaction price3

Allocate the transaction price to the performance obligations in the

contract4

Recognize revenue when (or as) the entity satisfies a performance

obligation5

25 © 2015 Protiviti Inc.

Multiple Element

Arrangements

• Entities that enter into contracts with customers to provide a series of promised goods or

services delivered consecutively will need to assess whether the contract is a single

performance obligation or contains multiple separate performance obligations

Estimated

Selling Price

• Use of observable inputs should be maximized, but if the stand alone selling price of a good

or service is variable or uncertain, the residual approach would be allowed

Variable

Consideration

• Variable consideration is reasonably assured if BOTH of the following criteria are met: (i) The

entity has experience with similar types of performance obligations and (ii) the entity's

experience is predictive of the amount of consideration to which the entity will be entitled in

satisfaction

Time Value

of Money

• The transaction price should reflect the time value of money when the contract includes a

significant financing component; a practical expedient allows entities to disregard the time

value of money for short-term contracts

Timing of Revenue

Recognition

• Each performance obligation would be evaluated to determine whether it is satisfied (a) over

time or (b) at a point in time; might lead to more “over time” recognition

New Revenue Model – Potential Significant Accounting and

Reporting Changes

26 © 2015 Protiviti Inc.

Construction-Type

Contracts

• Recognition of contract revenue and contract cost would be separated from each another.

Predictive margins would only be possible if a company uses a cost-to-cost method of measuring

progress towards satisfaction of the performance obligations

Construction-Type

Contract Costs

• Contract costs not eligible for capitalization (e.g., as inventory or direct fulfillment costs) would be

expensed as incurred

Software

Subscription

Accounting

• Further guidance is expected to help determine whether a license transfers a right or provides

access

Separation Criteria for

Elements in Software

Arrangements

• VSOE of the FV of the undelivered items would no longer be required to separately account for

elements in a software arrangement

Disclosures

• The standard includes a number of disclosure requirements intended to enable users of financial

statements to understand the amount, timing, and judgments related to revenue recognition and

cash flows

Contract Costs • Certain contract acquisition costs would need to be capitalized

New Revenue Model – Potential Significant Accounting and

Reporting Changes (Cont’d)

27 © 2015 Protiviti Inc.

Notable Implications

1

2

4

Industries that are likely to experience the most significant changes include software, telecommunications, asset management, airlines, real estate, aerospace and construction

Changes won’t be limited to these industries, of course, so all

companies should consider the need to assess the

implications of the new standard and develop implementation

plans to address those implications of the new standard and

develop implementation plans to address those implications

Companies with longer delivery cycles, or those with nonstandard and

complex contract terms, will be the most affected

• These organizations will require greater resources from systems or

process to provide the necessary information to meet the data

requirements to account for and describe revenue recognition

3The new guidance may enable some companies to recognize revenue sooner than they typically do under existing accounting standards

While no

industry will be

exempt…

28 © 2015 Protiviti Inc.

A. Yes

B. No

C. Don’t know

If the effective dates for the new revenue recognition standard are extended

beyond the current requirements, does your organization plan on moving

ahead with a transition strategy in 2015?

Reminder: Answer 4 out of 5 questions to qualify for CPE credit.

Poll Question #2

Transition Strategy and the Six

Elements of Infrastructure

30 © 2015 Protiviti Inc.

Phase I – Preliminary Diagnostic Phase II – Project Implementation Phase III – Embedding

Revenue Recognition – Transition Strategy Roadmap

Step I – Preliminary Diagnostic

Step II – Develop Project

Management

Step VI –Integrate Change &

Ongoing Compliance

Step V –Transition Year 1

Reporting

Step IV – Detailed Gap

Analysis/Transition Method

Step III – Detailed Project Set

Up

Deliverables

Each conversion project is a change management process that runs through multiple

phases. Every phase can be addressed in a structured way.

31 © 2015 Protiviti Inc.

What Does This Mean to Me?

Scope &

Analyze

Methodology

Business Policies

Business Processes

Systems and Data

Reporting

People

During the Scope and Analyze Phase, it is important to consider the implications to your

organization’s infrastructure. You can do this by using the Protiviti Six Elements of

Infrastructure Model.

32 © 2015 Protiviti Inc.

Revenue Recognition – Impact on Six Elements of Infrastructure

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

• Gap analysis

• 5 step analysis

framework

• Transition strategy

– PMO

• Update risk

assessment and/or

control framework

• Cross functional

awareness,

training and

deployment

• Multiple-

performance

obligations

revenue allocation

• Consistent

performance

measures/metrics

• Transition -

retrospective vs

cumulative effect

• Impact on

contracting,

pricing,

performance

obligations

• Update

documented

policies and

guidelines

• Judgment

considerations –

evidence of an

arrangement,

collectability

• Established

materiality

thresholds

• Transition timeline

defined and

monitored

• Identify processes

impacted –

contracting, order

entry, deal desk,

revenue

allocation,

reporting,

forecasting

• Identify

performance

metrics to

track/control the

Rev Rec process

• IA/SOX program

modifications

• Clearly-defined

review/approval

processes

• Determine data

elements allowing

systems to

process automatic

and judgmental

rules differently

• Define integration

points between

contracts T&Cs/

sales orders

• Define revenue

allocation rules

based on contract

groupings

• Design solutions

to rebuild the

current systems

and support

multiple/ parallel

rev rec principles

• Significant new

disclosures –

quantitative and

qualitative

• Updated

executive level

dashboards and

performance

metrics

• Revenue

allocation drill-

down capabilities

that enable quick

reference to

supporting detail

• Transparent audit

trail

• Identify cross-

functional

collaboration team

• Appropriate

segregation of

duties for key

revenue/issue

resolution

• Clearly defined

responsibility and

accountability

framework linked to

periodic

performance

evaluations

• Training on

policies,

procedures, and

enabling tools

33 © 2015 Protiviti Inc.

A Cross-Functional Impact

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

HR Accounting/Finance Internal Audit Treasury

• Metrics for measuring

performance

• Sales commission,

compensation and bonus

plans

• Resources required by all

areas to ensure compliance

during transition

• Training

• Target staffing operating

model (ongoing)

• Accounting policies and

procedures

• Forecasts, budgeting and

financial metrics

• Analytical reviews

• Data accuracy

• Financial reporting of results

and associated disclosures

(reconciliation of contract

balances, disaggregation of

performance obligations,

qualitative disclosures,

interim period disclosures

• Accounting deviations

• Increased judgment and

estimates (allocation of

transaction price, variable

considerations, discounts)

• Revenue process

• Capitalizing contract costs

• Margin

• Net income

• Bonuses and other key

performance metrics

• Investor relations

• Impact on systems and controls

due to changes in policies and

processes

• Controls and processes

surrounding additional estimates

and required disclosures

• Awareness of fraud indicators

• Audit skills enhancement

• ERM augmentation

• Change management

• Controls adjusted (real-time)

• Debt covenants (potential

modification to maintain

original intent)

• Cash flow

projections/analysis

• Foreign currency

• Provisions for significant

financing component

• Hedging/Derivative

considerations on long-

term contracts with interest

• Contract review

(embedded features)

34 © 2015 Protiviti Inc.

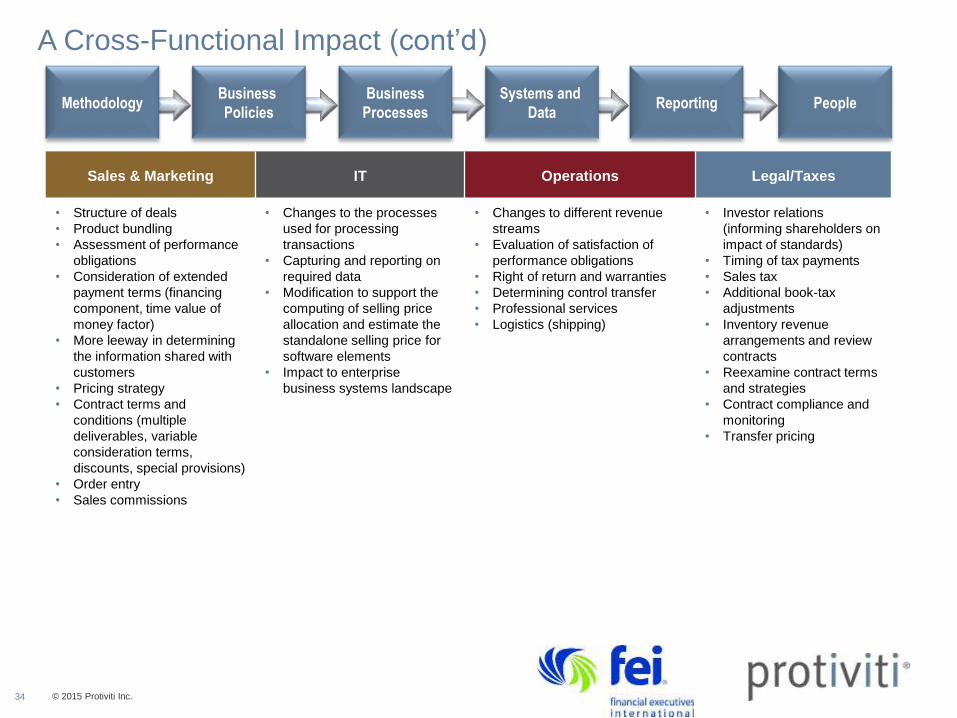

A Cross-Functional Impact (cont’d)

Sales & Marketing IT Operations Legal/Taxes

• Structure of deals

• Product bundling

• Assessment of performance

obligations

• Consideration of extended

payment terms (financing

component, time value of

money factor)

• More leeway in determining

the information shared with

customers

• Pricing strategy

• Contract terms and

conditions (multiple

deliverables, variable

consideration terms,

discounts, special provisions)

• Order entry

• Sales commissions

• Changes to the processes

used for processing

transactions

• Capturing and reporting on

required data

• Modification to support the

computing of selling price

allocation and estimate the

standalone selling price for

software elements

• Impact to enterprise

business systems landscape

• Changes to different revenue

streams

• Evaluation of satisfaction of

performance obligations

• Right of return and warranties

• Determining control transfer

• Professional services

• Logistics (shipping)

• Investor relations

(informing shareholders on

impact of standards)

• Timing of tax payments

• Sales tax

• Additional book-tax

adjustments

• Inventory revenue

arrangements and review

contracts

• Reexamine contract terms

and strategies

• Contract compliance and

monitoring

• Transfer pricing

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

35 © 2015 Protiviti Inc.

The Revenue Recognition Diagnostic Process

Item Element Background

Diagnostic Question

Applicable to the Organization

Current State

Recommendation Estimated EffortEstimated Urgency

36 © 2015 Protiviti Inc.

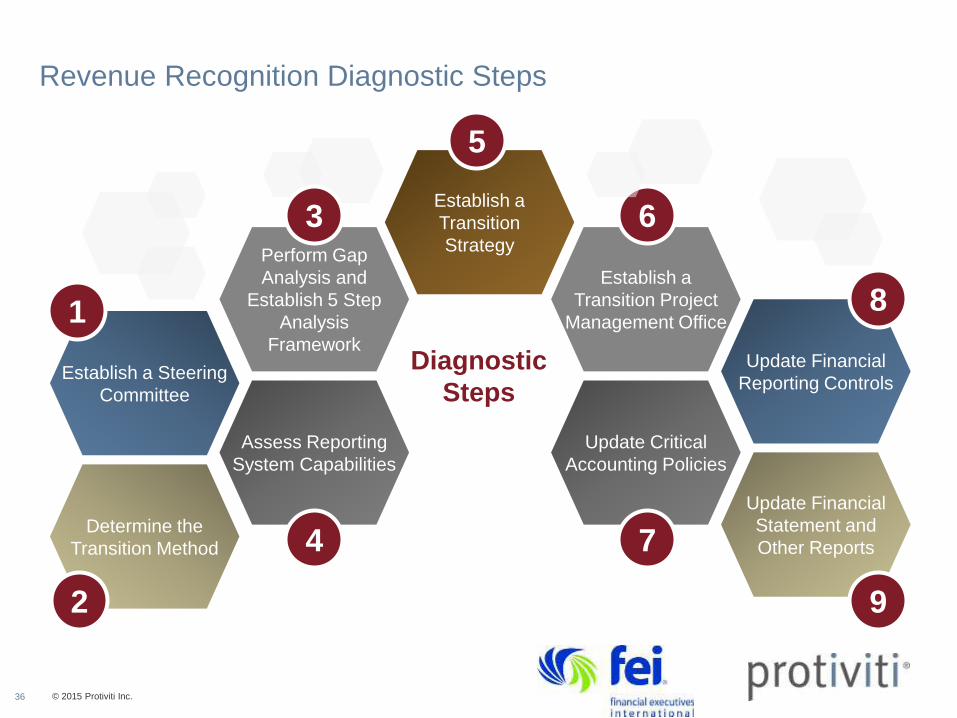

Revenue Recognition Diagnostic Steps

Assess Reporting

System Capabilities

Update Critical

Accounting Policies

Perform Gap

Analysis and

Establish 5 Step

Analysis

Framework

Establish a

Transition Project

Management Office

Update Financial

Statement and

Other Reports

Update Financial

Reporting Controls

Establish a

Transition

Strategy

Determine the

Transition Method

Establish a Steering

Committee

3

1

2

4

6

7

8

9

5

Diagnostic

Steps

37 © 2015 Protiviti Inc.

Example Diagnostic – Establish a Steering Committee

Ref

#Item Element Background Sub Ref Diagnostic Question

1

Establish a

Steering

Committee

Business

Process

A dedicated task force

should be established to

provide oversight to the

transition process. The

task force should include

resources from areas likely

to be impacted by the

transition, including

accounting, financial

reporting, tax, internal

audit, sales operations, IT,

legal and human

resources.

1a

Has the company's functional

framework been evaluated to identify

which processes will be impacted by

transition and to what extent?

People 1b

Has a transition steering committee

been formed? Does the committee

include resources from each critical

process impacted by the transition?

People 1c

Have all members of the transition

steering committee been provided

sufficient training on the new revenue

recognition standard?

38 © 2015 Protiviti Inc.

Six Elements of Infrastructure

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

• Gap analysis

• 5 step analysis

framework

• Transition strategy –

PMO

• Update risk

assessment and/or

control framework

• Cross functional

awareness, training

and deployment

• Multiple-

performance

obligations revenue

allocation

• Consistent

performance

measures/metrics

• Transition -

retrospective vs

cumulative effect

• Impact on

contracting, pricing,

performance

obligations

• Update documented

policies and

guidelines

• Judgment

considerations –

evidence of an

arrangement,

collectability

• Established

materiality

thresholds

• Transition timeline

defined and

monitored

• Identify processes

impacted –

contracting, order

entry, deal desk,

revenue allocation,

reporting,

forecasting

• Identify

performance

metrics to

track/control the

Rev Rec process

• IA/SOX program

modifications

• Clearly-defined

review/approval

processes

• Determine data

elements allowing

systems to process

automatic and

judgmental rules

differently

• Define integration

points between

contracts T&Cs/

sales orders

• Define revenue

allocation rules

based on contract

groupings

• Design solutions to

rebuild the current

systems and

support multiple/

parallel rev rec

principles

• Significant new

disclosures –

quantitative and

qualitative

• Updated executive

level dashboards

and performance

metrics

• Revenue allocation

drill-down

capabilities that

enable quick

reference to

supporting detail

• Transparent audit

trail

• Identify cross-

functional

collaboration team

• Appropriate

segregation of duties

for key revenue/issue

resolution

• Clearly defined

responsibility and

accountability

framework linked to

periodic performance

evaluations

• Training on policies,

procedures, and

enabling tools

39 © 2015 Protiviti Inc.

A. Yes

B. No

C. Don’t know

Has your organization established a steering committee to provide oversight of

the transition to the new revenue recognition standard?

Reminder: Answer 4 out of 5 questions to qualify for CPE credit.

Poll Question #3

Impact on Systems and Data

41 © 2015 Protiviti Inc.

Six Elements of Infrastructure – Systems and Data

Systems and Data

• Support the modeling and reporting that are integral to risk management capabilities

• Provide relevant, accurate, and on-time information

• Should meet the company’s business requirements, and be flexible enough to allow for future

enhancement, scalability and integration with other systems

• Typically include:

Transaction systems and analytical software

Systems that identify and capture risk drivers

Systems and databases that warehouse key data elements relating to specific tasks

Special-purpose systems that quantify individual risks and aggregate portfolios of risks

Database systems that support the management of individual risks and risk portfolios

Risk analytics programmed into decision-support systems

This risk element is deficient if: Information is not available for analysis and reporting

Key elements of infrastructure must be linked by design:

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

42 © 2015 Protiviti Inc.

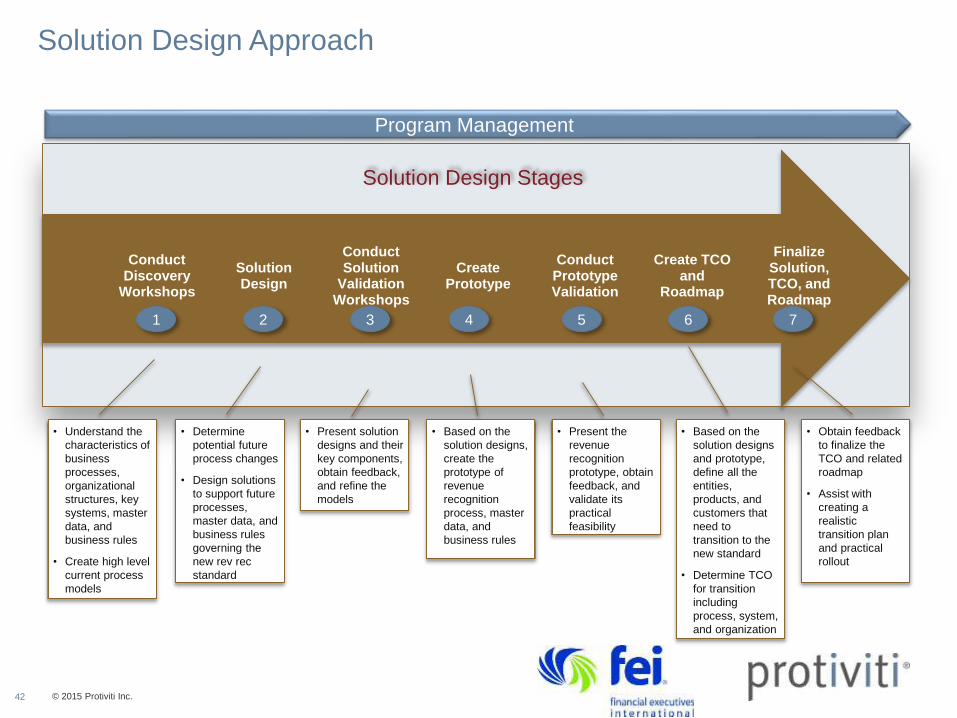

Solution Design Approach

Finalize Solution, TCO, and Roadmap

Create TCO and

Roadmap

Conduct Prototype Validation

Create Prototype

Conduct Solution

Validation Workshops

Solution Design

Conduct Discovery

Workshops

Solution Design Stages

Program Management

• Understand the

characteristics of

business

processes,

organizational

structures, key

systems, master

data, and

business rules

• Create high level

current process

models

• Determine

potential future

process changes

• Design solutions

to support future

processes,

master data, and

business rules

governing the

new rev rec

standard

• Present solution

designs and their

key components,

obtain feedback,

and refine the

models

• Based on the

solution designs,

create the

prototype of

revenue

recognition

process, master

data, and

business rules

• Present the

revenue

recognition

prototype, obtain

feedback, and

validate its

practical

feasibility

• Based on the

solution designs

and prototype,

define all the

entities,

products, and

customers that

need to

transition to the

new standard

• Determine TCO

for transition

including

process, system,

and organization

• Obtain feedback

to finalize the

TCO and related

roadmap

• Assist with

creating a

realistic

transition plan

and practical

rollout

2 3 4 5 6 71

43 © 2015 Protiviti Inc.

New Revenue Recognition Principle System Components

Most of revenue-generating arrangements are contractual arrangements of some form between two parties

Revenue would be earned and recognized as the reporting organization satisfies performance obligations or

promises within the contractual arrangement

Timing of revenue recognition may vary depending on whether the contract is for the delivery of goods or for the

performance of a service

Contract management

system providing structured

data to order fulfillment and

accounting systems

Pricing master data

categorized and classified to

support different price types

Rule-based component to

pick the right transaction

price automatically

Rule-based engine to

compute and allocate

revenue using a decision

tree which translates the

policy principles

Automatic event manager

component to capture

revenue recognition

triggering events

Revenue recognition sub-

ledger allowing automatic

reconciliation and detailed

reporting

(4) Allocate the

transaction price to

separate contract

performance

obligations

(3) Determine

the transaction

price

(5) Recognize

revenue when (or

as) entity satisfies

a performance

obligation

(2) Identify the

separate

performance

obligations in the

contract

(1) Identify the

customer

contract(s)

Consistent application of the new standard will be achieved through the use of a contract-based model

Five steps to

achieve the

core principle

of the new

standard

44 © 2015 Protiviti Inc.

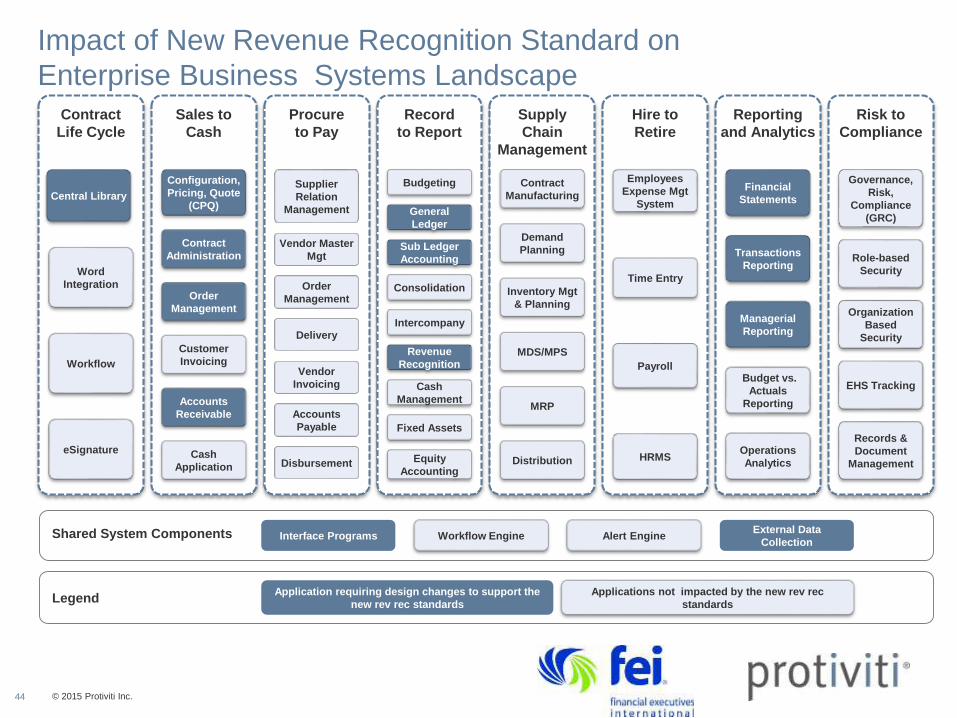

Impact of New Revenue Recognition Standard on

Enterprise Business Systems Landscape

Legend

Contract

Life Cycle

Central Library

Word

Integration

Workflow

eSignature

Sales to

Cash

Configuration,

Pricing, Quote

(CPQ)

Contract

Administration

Order

Management

Customer

Invoicing

Accounts

Receivable

Cash

Application

Procure

to Pay

Supplier

Relation

Management

Vendor Master

Mgt

Order

Management

Delivery

Vendor

Invoicing

Accounts

Payable

Disbursement

Record

to Report

Budgeting

General

Ledger

Sub Ledger

Accounting

Consolidation

Intercompany

Revenue

Recognition

Cash

Management

Fixed Assets

Equity

Accounting

Supply

Chain

Management

Contract

Manufacturing

Demand

Planning

Inventory Mgt

& Planning

MDS/MPS

MRP

Distribution

Hire to

Retire

Employees

Expense Mgt

System

Time Entry

Payroll

HRMS

Reporting

and Analytics

Financial

Statements

Transactions

Reporting

Managerial

Reporting

Budget vs.

Actuals

Reporting

Operations

Analytics

Risk to

Compliance

Governance,

Risk,

Compliance

(GRC)

Role-based

Security

Organization

Based

Security

EHS Tracking

Records &

Document

Management

Shared System Components

Application requiring design changes to support the

new rev rec standards

Applications not impacted by the new rev rec

standards

Interface Programs Workflow Engine Alert EngineExternal Data

Collection

45 © 2015 Protiviti Inc.

Revenue Recognition – System Redesign

The new revenue recognition standard impacts all the systems and interfaces related to the revenue reallocation

computation rules. The following chart depicts a typical revenue recognition engine used for the high technology industry.

This engine requires a comprehensive redesign to support the new revenue recognition principle.

Transactions

Sales Data Billing Data

Receivable Data Contract Data

Arrangements DataDiscounts

(basic, additional)

POS Data

Rev Rec Data

Staging

Component

ERP

Master Data

Category Type

PriceList

Discount

Product

ERP

SKU

Pricing

OrganizationCustomers

BESP

VSOE

List Price

Update

BSEP Price

Calculation

VSOE Price

Calculation

Periodic

Automated Process

Business rule

Rebate is an “additional

discount“ which is claimed

by the channel partner

based on the realization of

the sales to the end

customer (sell-in) and

linked at the serial

number/contract number

level

For Non Reporting

Partner

Determine Arrangements

Using Customer Purchase

Orders

1 Determine Arrangements

Using End User Names

1

Only For Reporting

Partner

Determine Channel

Rebates corresponding to

Arrangements

1.1

Exceptions Exceptions

No Exceptions

Determine Arrangement

Revenue Recognition

Principle

Resolve

Arrangements

Exceptions

Exception

Management

Application

Business Rule

Decision tree to determine which

revenue recognition is used

Rev Rec Data Staging Component

Determine Arrangement

Revenue Allocation, Amount,

and Timing based on customer

registration which occurs at

some point after invoicing

32Store Arrangement

Details for Tracking and

Analytical Purposes

4

Calculation of VSOE of FV

and BESP achievement

percentage quarterly

START

Rebate Data

Cleared

Exceptions

46 © 2015 Protiviti Inc.

A. Yes

B. No

Has your organization started to assess the impact of the new revenue

recognition standard on data requirements and related IT systems?

Reminder: Answer 4 out of 5 questions to qualify for CPE credit.

Poll Question #4

Reporting Considerations

48 © 2015 Protiviti Inc.

Six Elements of Infrastructure – Reporting

Reporting

• Reports should be actionable, easy to use and linked to well-defined accountabilities

Are designed according to the information needs of people who are responsible for executing

processes in accordance with the risk strategy

• Personnel with risk management responsibilities use reports to monitor achievement of objectives,

execution of strategies, and compliance with policies

• Management reports include position reports, transaction reports, management and board reports,

valuation/scenario analyses and comprehensive reports

• Factors to consider when reporting on frequency include the volatility or severity of the risks, the

needs for the user and the dynamics of the underlying business activities

• Reporting on risks is integral to an organization’s success as reporting on quality, costs, and time

• In order for management to make informed decisions, management reports should:

Be prepared with appropriate frequency

Be easy to use

Capture information succinctly and highlight key points for decision-making

• This risk element is deficient if: Reports do not provide enough information for management

Key elements of infrastructure must be linked by design:

MethodologyBusiness

Policies

Business

Processes

Systems and

DataReporting People

49 © 2015 Protiviti Inc.

Financial Reporting Disclosures

Transaction price allocation

Methods and assumptions

Remaining performance obligations

50 © 2015 Protiviti Inc.

Management Reports

Commissions, Bonus and

Compensation Structure

ExecutiveDashboards

ForecastingReports

Internal Controlsand SOX Compliance

Loan Financial

Covenant Compliance

M&A (Working capital adjustments, revenue projections, post-deal multiple earnout

provisions, etc.)

Impact on Internal Reports and External Reports

Partnerships, Alliance and Joint Ventures

The are numerous implications to the internal reporting and external reporting processes. These reports

should always be right and create a transparent audit trail.

Budget Reports Key Financial Performance Metrics

Financial

Reporting

51 © 2015 Protiviti Inc.

A. Yes

B. No

Have you started to assess the impact of the new revenue recognition standard

on your organization’s revenue reporting and related processes?

Reminder: Answer 4 out of 5 questions to qualify for CPE credit.

Poll Question #5

52 © 2015 Protiviti Inc.

Q & A

Let us know how we did on this webinar. Click on the

Survey icon to give us feedback.

Submit Your Questions

53 © 2015 Protiviti Inc.

New Revenue Model – The Next Steps?

Take Time to Learn,

Diagnose and

Assess Now…..

1. Education: Review final standard and implementation guidance

2. Analyze current revenue policy vs. the proposed standard to identify expected changes:

− Customer contracts with unique terms

− Changes to cost recognition policies

3. Depending on significance of accounting policy gaps, consider extent of tax (or legal)

involvement that may be required

4. Perform a high level analysis of data gaps:

− Will required information be available from your existing processes?

− Will system changes be required?

5. Develop high level approach regarding transition method:

− Retrospective versus cumulative effect

− Consider complexity of performing the transition and whether specific tools/systems may be

required

6. Identify and assess additional resource needs; internal / external; temporary or permanent

7. Educate senior management team, key stakeholders and board of directors

54 © 2015 Protiviti Inc.

Thank

You