THE NEW MORTGAGE - National Consumer Law Center · THE NEW MORTGAGE RULES A seven course tasting...

60

11/12/2013 1 THE NEW MORTGAGE RULES A seven course tasting menu Alys Cohen & Nina Simon NCLC Conference 2013 November 9, 2013 The Menu • Amuse bouche: Remedies • Starters: Mandatory arbitration, waiver of statutory claims, credit insurance • Soup: – HOEPA points & fees as the foundation for everything else • Main courses: – QM – Qualified mortgage – ATR – ability to repay – LO – Loan originator compensation – New HOEPA • Dessert: ATR rules for Open end HOEPA

Transcript of THE NEW MORTGAGE - National Consumer Law Center · THE NEW MORTGAGE RULES A seven course tasting...

11/12/2013

1

THE NEW MORTGAGE RULES

A seven course tasting menuAlys Cohen & Nina SimonNCLC Conference 2013November 9, 2013

The Menu

• Amuse bouche: Remedies • Starters: Mandatory arbitration, waiver of statutory claims,

credit insurance• Soup:

– HOEPA points & fees as the foundation for everything else

• Main courses: – QM – Qualified mortgage– ATR – ability to repay– LO – Loan originator compensation– New HOEPA

• Dessert: ATR rules for Open end HOEPA

11/12/2013

2

What’s not on the menu

• Old rules including anti‐steering and HPML rules on ATR, PPPs, escrow and evasion.

• Disclosure

• Servicing rules in Reg Z

• LO qualification, registration and licensing

• HPML Appraisal rule

• Counseling

• Dodd‐Frank steering (15 USC 1639b(c)(3)) (no regs yet, no deadline)

Federally Sourced Menu

• Statute

• Regulation

• Commentary

• Supplementary Information

• CFPB Compliance Guides, Manuals

• CFPB charts

• Chapter 9, NCLC TILA Manual

• Caselaw (as it develops)

11/12/2013

3

Amuse bouche: remedies

• Remedies for ATR/LO against creditors & assignees:– Regular TILA remedies: actual, statutory damages; attorneys fees

– Enhanced (HOEPA) damages: sum of all finance charges and fees paid by consumers (for material violations).

• Remedies for LO violations against LO*: – Regular TILA remedies– Enhanced damages – BUT damages capped at greater of actual damages or 3x direct and indirect compensation to the LO (in connection with the loan) plus attorneys fees

• *D‐F says “mortgage originators,” rule says LO

Amuse bouche: remedies

• Assignee liability‐15 USC 1640(k),1641;TILA manual Ch. 12– Absolute when jud or non‐jud foreclosure initiated.

• Available only in recoupment or set‐off. • 3 year cap on damages.

– Otherwise depends on “apparent on the face of the disclosure statement”

• Did disclosures include income verification, ATR review, application with relevant income data?

• What do disclosures say about how brokers were paid?

• Statute of limitations beyond regular TILA – LO (both types) or ATR claim when jud. or non‐jud. foreclosure

initiated.– Claims against creditor, assignee or holder (or originator)– 3‐yr cap on damages applies– Recoupment or set‐off.

11/12/2013

4

Amuse bouche: remedies

• Record retention: – 3 years after consummation

• General TILA rule is 2 years

– Retain “evidence of compliance” with mortgage‐related obligations under §1026.43

• Evidence goes beyond TILA documents to underwriting documentation.

– Problem of ARMs, etc. adjusting at or after 3 years

• Policies and procedures requirement: Creditors must maintain policies and procedures to monitor compliance with the loan originator and steering provisions. (Discovery) §1026.36(j)

Starters: demise of mandatory arbitration, waiver of federal statutory claims or upfront credit insurance

• §1026.26(h)(1)—no mandatory pre‐dispute arbitration clauses– for applications after 6/1/13

– for closed end loans secured by a dwelling,&

– for open end loans secured by principal dwelling

11/12/2013

5

Federal statutory claims

NO pre‐dispute waiver of federal claims or right to pursue these claims in court, §1026.36(h)(2)

–for applications on or after 6/1/13 –for closed end loans secured by a dwelling &

–for open end loans secured by principal dwelling

Credit insurance & the like

• NO financing single premium credit insurance §1026.36(i) – closed end loans secured by a dwelling &– open end loans secured by principal dwelling– N/A if credit insurance calculated and fully paid monthly– Includes

• credit life, disability, unemployment, or property insurance &

• any other accident, loss of income, life or health insurance & payments directly or indirectly for debt cancellation or suspension

– Excludes credit unemployment insurance meeting specific requirements, §1026.36(i)(2)(ii)

11/12/2013

6

Soup: Points and fees What’s new?

• Now applies to nearly ALL dwelling‐secured mortgage loans

• Is basic to assessing status as: – Closed‐end QM & HOEPA – And open‐end HOEPA

• Closed‐ & open‐end rules essentially the same • C‐E applies to charges payable at or before consummation

• O‐E applies to charges known at or before account opening

• Additional rules for open‐end

Points and fees

• Same basic model as before:

• Start with finance charges

• Subtract some types of charges

• Exclude other types of charges

• Add some types of charges

11/12/2013

7

Requirements for Points and Fees§1026.32(b)(1)—what’s always out

• Interest and time price differential

• Premiums for federal or state mortgage insurance

• Private mortgage insurance (PMI) paid after consummation, typically monthly

• Escrows for future taxes

• Credit unemployment insurance if premiums are reasonable, no direct or indirect $$ to creditor or affiliate and creditor not beneficiary

Points and Fees—what’s squishy (sometimes in and sometimes out)

• Private Mortgage Insurance (PMI):

– If payable at or before consummation, e.g. upfront premium, exclude the portion that is = to federal/state premium

– Except, do not exclude any of the premium unless it is refundable pro‐rata! (this may swallow the rule and effectively require inclusion of all upfront PMI at least for now)

11/12/2013

8

More Squishy Points and Fees§1026.32(b)(1)

• Bona fide 3d party charge not retained by creditor, loan originator (LO) or affiliate of creditor or LO is out unless:– §1026.32(b)(1)(i)(C)—addressing PMI premiums (see earlier slide)

– §1026.32(b)(1)(iii)– addressing real estate related charges (§1026.4(c)(7)) or

– §1026.32(b)(1)(iv) addressing credit insurance

• provide otherwise

More Squishy Points and Fees‐‐real estate related charges‐§1026.32(b)(1)(iii)

• §1026.4(c)(7) charges are generally excluded if

– reasonable,

– no direct or indirect comp to the creditor &

– not paid to an affiliate of creditor

• Example: Hazard insurance premiums payable to an affiliate of the creditor and escrowed at closing are included in p&f even if not due until after consummation

11/12/2013

9

More squishy points & fees: bona fide discount points

• Points = 1% of the loan amount (closed‐end) or 1% credit limit (open‐end)

• Discount points are in but

• May excludemaximum of 1 or 2 bona fide discount points paid by the consumer– §1026.32(b)(1)(i)(E),(F)(closed)

– §1026.32(b)(2)(i)(E),(F) (open)

• if meet specified conditions

More squishy points & fees: 2 bona fide discount points

• May deduct from points and fees, up to 2bona fide discount points if:

– Interest rate w/o discount is < APOR + 1; or

– Interest rate w/o discount is < average rate for Title I loans (for personal property secured transactions) + 1

11/12/2013

10

More squishy points & fees: 1 bona fide discount point

• May deduct up to one bona fide discount point if:

– Interest rate w/o discount is < APOR + 2; or

– Interest rate w/o discount is < average rate for Title I loans (for personal property secured transactions) + 2.

More squishy points & fees: more bona fide discount points

• What makes points bona fide?

• They reduce the interest rate or time price differential consistent with established industry practices ‐‐§1026.32(b)(3)

11/12/2013

11

Points and fees: what’s always in

• LO comp, including ysps

• Two types of prepayment penalty (PPP)

• Open‐end PPP

• Open‐end participation fees

• Open‐end minimum or per transaction fee for taking a draw on credit line

Points and fees—more what’s in

• LO comp‐– All compensation

– paid directly or indirectly

– by a consumer or creditor

– to a LO

– that can be attributed to a transaction

– at the time the interest rate is set

– §1026.32(b)(1)(ii)—closed‐end; (b)(2)(ii)—open‐end

11/12/2013

12

Points & fees—more what’s in—LO comp

• Includes YSPs

• No double counting‐‐if LO comp is already included in finance charge don’t count again‐‐excludes:– Consumer paid mortgage broker fee (already in FC)

– Compensation paid by mortgage broker to its LO employee

– Compensation paid by creditor to its LO employee

Points & fees—what’s in‐‐credit insurance/debt cancel‐‐.32(b)(1,2)(iv)

• Premiums or other charges payable at or before consummation (or known at or before account opening) for any: – credit life, credit disability, credit unemployment, or credit property insurance, or

– any other life, accident, health, or loss‐of‐income insurance for which the creditor is a beneficiary, or

– any payments directly or indirectly for any debt cancellation or suspension agreement or contract

11/12/2013

13

Points and fees—what’s in‐‐ppp

• 2 types of PPP are points & fees for closed‐end loan:

–maximum ppp payable under the new loan—§1026.32(b)(1)(v); and

– total ppp paid by the consumer in refinancing with its current loan holder or servicer or affiliate of either—§1026.32(b)(1)(vi)

Points & fees—what’s in—open‐end PPP

• Slightly different definition of PPP for o‐e:

– “charge imposed by the creditor if the consumer terminates the open‐end credit plan prior to the end of its term”‐‐§1026.32(b)(6)(ii)

• Count 2 types of PPP:

–maximum ppp that may be collected under terms of the o‐e plan‐‐ §1026.32(b)(2)(v)

11/12/2013

14

Points & fees—more what’s in—open‐end PPP

• total ppp incurred if consumer refis‐‐§1026.32(b)(2)(vi)):

– with same holder or servicer of existing plan, or affiliate of either;

– From closed to open OR

– From open to open OR

– From open to closed‐end

NOT a PPP so not a point & fee

• NOTE for both closed and open: NEW definition of ppp allows creditor to recover certain waived closing costs without treating them as ppp‐‐ §1026.32(b)(6)(i)—

• waived bona fide third party closing cost can be charged if loan prepaid w/in 36 mos of consummation and is not a ppp

11/12/2013

15

Points & fees—what’s in—open‐end only

• Any fee charged for participation in open‐end loan at or before account opening‐‐§1026.32(b)(2)(vii)

• Any transaction fee or minimum fee for drawing on credit line—must assume at least one‐‐§1026.32(b)(2)(viii)

Total Loan Amount (TLA)

• §1026.32(b)(4)(i)—closed end credit:– Start with amount financed AF)‐‐§1026.18(b)– Subtract from AF the following if both included in p & f and financed by the creditor:

• 1026.32(b)(1)(iii)—(4)(c)(7) charges• 1026.32(b)(1)(iv)—credit insurance premiums/debt cancellation or suspension charges

• 1026.32(b)(1)(vi)—total ppp paid—same lender/servicer/affiliate refi

• But not LO comp paid by creditor to LO and not YSP

– Result is total loan amount—TLA

11/12/2013

16

TLA—open‐end

• TLA for open end

• §1026.32(b)(4)(ii)

• TLA= the credit limit for the plan when the plan is opened

Main Courses

• Ability to Repay (“ATR”)

• Qualified Mortgage (“QM”)

• Loan Originator Compensation (“LO”)

• New HOEPA rules (with more coverage)(“high‐cost”)

11/12/2013

17

Main Course: Ability to Repay and QM15 U.S.C. 1639c and 12 CFR 1026.43

• Ability to Repay—general requirements

• Qualified Mortgage—rebuttable presumption (for higher‐priced loans) or safe harbor? – Private label

– GSE

– Gov’t Agency (insured or guaranteed by FHA, USDA, VA)

• Small Creditor Qualified Mortgage

• Sm Cr Balloon Qualified Mortgage

• Prepayment Penalty Qualified Mortgage

• Refi Exemption

Main Course: Ability to Repay and QM

• Effective Date: Jan. 10, 2014 (earlier as “existing industry standards”)

• COVERAGE: §1026.43(a) & (b) • “residential mortgage loans”

– Not “residential mortgage transactions”– Closed‐end, dwelling‐secured

• Applies to manufactured housing • Applies to multiple loans where creditor knows or has reason to know more than one covered loan is being made to same consumer

• Does not include: HELOCs, time shares, reverse mortgages or bridge or construction loans

• Note reverse mortgages only exempt if meet TILA definition: non‐recourse and secured by principal dwelling

• Note exemption for certain non‐profit and government‐supported lenders (1026.43(a)(3)(iv)&(v).

11/12/2013

18

Ability to Repay and QM: First Questions

• Where to start—Did the lender make a reasonable and good faith determination that the loan was affordable to the consumer at the time of the transaction

• Can show not reasonable or not good faith

• Based on common underwriting factors (discovery)

• Difficult claims—do your homework first.

Ability to Repay and QM: First Questions

• Questions:– Reasonable and good faith determination?

– If the loan was an ARM or subject to reset, did lender reasonably conclude reset payments were affordable based on financial picture at closing?

– Did consumer share information with lender that should have alerted lender to affordability problem?

• Imminent retirement, expected job loss, ongoing high medical bills, etc.?

11/12/2013

19

Ability to Repay and QM: First Questions

• YES TO ALLLook elsewhere for solutions (does this person need a modification?).

• NOWhat is the timing/circumstances of the delinquency?

– Shortly after closing? (within 6‐12 months)

– Shortly after reset?

– Shortly after known event? (retirement, job loss)

Ability to Repay and QM: First Questions

• If delinquency was delayed, what are mitigating factors?

– Used funds from previous refi cashout?

– Overdrafted accounts/cards to pay mortgage until sources ran out?

– Borrowed from family/friends?

11/12/2013

20

Ability to repay and QM: Building your Case

• Identify which set of ATR and QM rules applies

• Determine if this is a QM or non QM loan

• If QM, safe harbor or rebuttable presumption?

• If QM rp loan, can you rebut presumption?

• If non‐QM, what are general ATR requirements?

• Note: only QMs have presumption of affordability; non‐QMs do NOT.

• Alternatives include UDAP, unconscionability, bankruptcy, etc.

Building your Case: Which set of QM rules applies?

• Investor type

– Gov’t insured or guaranteed?

– GSE loan?

– Private label security or portfolio loan?

• Lender type—small creditor?

• Product type—sm cr balloon? Ppp? Refi of nonstandard loan?

11/12/2013

21

Building your case: Determine if this is a QM loan

• Private label/general QM rules:– Loan terms (these are common to all QMs):

• No neg am or interest only• Points and fees maximum of 3% (but loans under $100K have separate caps)

• Loan term of no more than 30 years

– Underwriting payments: maximum rate for first 5 years after first payment based on fully amortizing schedule

– No more than 43% DTI (Appendix Q, which formally applies only to QM analysis but may have other applications)

Building your case: Determine if this is a QM loan

• Appendix Q for checking the 43% DTI is very detailed. Guidelines include:– Seasonal and self‐employment

– Reliance on bonuses/overtime for income

– Alimony, child support, maintenance income

– Rental income

– Projected income (verified and within 60 days) and obligations (only if begins within 12 mos)

– Exclusions from “debt” include open accounts with zero balance

11/12/2013

22

Building your case: Determine if this is a QM loan

• GSE or Agency “Temporary QM” §1026.43(e)(4)– Common loan term restrictions on neg am, IO, balloons, 30‐year term and pts and fees.

– Plus eligible for purchase or guarantee by GSEs, to be insured by FHA, guaranteed by VA, guaranteed by USDA or insured by RHS

– Sunset: expires earlier of 1/10/2021 or agency regulation defining QM or if conservatorship ends

– HUD has proposed FHA QM effective January 2014.

– New leverage to enforce GSE/agency underwriting rules

Building your case: Determine if this is a QM loan

• How to establish eligibility for purchase, guarantee or insurance: (Commentary 43(e)(4)‐4– Valid “approve/eligible” from GSE automated underwriting program, and compliance with any conditions

– Compliance with GSE or agency guidelines

– Written agreement between GSE or agency and creditor

– Individual loan waivers from GSE or agency

11/12/2013

23

Building your case: Determine if this is a QM loan

• Small Creditor QM

– Part 1: Definition of small creditor

• Assets less than $2 billion(not including affiliates) AND

• Creditor and affiliates combined originated no more than 500 first‐lien, closed‐end residential mortgages subject to ATR in prior calendar year (not including subordinate liens or mortgages excluded from ATR)

Building your case: Determine if this is a QM loan

• Small Creditor QM is more flexible• Part 2: Loan/underwriting rules

– Common loan term restrictions:» No neg am or interest only» Points and fees maximum of 3% (but loans under $100K have

separate caps)» Loan term of no more than 30 years

– Points and fees cap– Underwrite to maximum rate for 5 years– Consider and verify income or assets, and debts, alimony, and child

support– Consider DTI or residual income, but no numbers required. – Loan not subject to forward commitment (agreement made at or

prior to consummation to sell the loan after consummation, other than to a creditor that itself is eligible to make Small Creditor QMs).

11/12/2013

24

Building your case: Determine if this is a QM loan

• A small creditor QM can lose its status if it sells or transfers the loan.– Part 3: Small creditor QM status retained if:

• It is sold more than three years after consummation.

• It is sold to another creditor that meets the criteria regarding number of originations and asset size, at any time.

• It is sold pursuant to a supervisory action or agreement, at any time.

• It is transferred as part of a merger or acquisition of or by the creditor, at any time.

Building your case: Determine if this is a QM loan

• Small Creditor Balloon QM– Creditor requirements—

• Until 1/9/2016 all small creditors • After 1/10/16 only small creditors operating predominantly in rural and underserved

areas (special definition)

– Loan criteria• No neg am or IO• Points and fees cap• 30 years amortization and fixed interest payments (other than balloon)• Loan term of at least 5 years• Held in portfolio (not subject to forward commitment)• Determine affordability of regular periodic payments OTHER THAN balloon (contrast with

balloon ATR rule)• Consider and verify income/assets/debts• Consider DTI or residual income (but no number required)

– Same restrictions on sale or transfer as small cred QM

11/12/2013

25

Building your case: Determine if this is a QM loan

• QMs with PPPs

– Only on fixed rate or step rate loans

– Not on higher‐priced QM loans

– Otherwise permitted by applicable (state) law

– If maximum ppp pushes loan above points and fees threshold then not QM

– No PPP after first 3 years of loan

Building your case: Determine if this is a QM loan

• More on PPP QMs

– PPP definition does not include certain bona fide third party fees if waived at closing (in exchange for earning through interest rate), even if must be repaid upon prepayment in first three years

– Maximum PPP is 2% of UPB for year 1 and 2 and 1% for year 3.

– Must also have offered similar loan without PPP (bait and switch opportunity?)

11/12/2013

26

Building your case: Determine if this is a QM loan

• What does the offer of a similar loan without PPP have to look like?– Consumer must also qualify for other option offered.– No PPP– Fixed rate or step‐rate with same rate type– Same term as PPP loan – No deferred principal, balloon or interest‐only payments, or negative

amortization

• If creditor is brokering or table‐funding, then additional requirements if offer also used to comply with anti‐steering rules for loan originators under § 1026.36(e):– loan with the lowest interest rate overall; – loan with the lowest interest rate with a PPP; and – the loan with the lowest total origination points or fee and discount

points

Certain Refis are Exempt from ATR/QM§1026.43(d)

• ATR/QM does not apply to refinancing of “non‐standard” mortgage by creditor holding or servicing the non‐standard mortgage.

• Not available to subservicers or third parties.

• Meant to help avoid impending payment shock.

• FHA Streamline Refi subject to FHA QM

• Modifications already exempt because not new credit.

11/12/2013

27

Certain Refis are Exempt from ATR/QM §1026.43(d)

• Eligible non‐standard loans:– ARM fixed for at least one year; IO or Neg Am

– Current on loan• Maximum 1 30‐day late in 12 months; no lates in prior 6 mos. (See details in Commentary)

– Written app. no later than 2 mos. after recast

– New loan likely to prevent default on non‐standard loan after recast

– Non‐standard loan made after 1/10/14 must comply with ATR/QM.

Certain Refis are Exempt from ATR/QM §1026.43(d)

• Standard loan requirements– No increase in principal balance

– No cash out (except closing costs and escrow)

– Monthly payment after recast materially lower‐‐reduced by more than 10% (not necessarily affordable long‐term)

– No IO, neg am or balloon

– Meets points and fees cap for QM

– Loan term not greater than 40 years

– Fixed rate for first 5 years

11/12/2013

28

What’s Next if it is a QM?

• Qualified Mortgages have two levels of presumption:

– Conclusive presumption/safe harbor IF QM

– Rebuttable presumption for “higher‐priced” mortgages

A word about this dichotomy

QM Levels of Presumption

• In order to show you are entitled to the rebuttable presumption, you have to show it is a higher‐priced mortgage loan.

• Higher‐priced QM loans:– Loans with APR >1.5 + APOR (1st lien)

– Loans with APR >3.5 + APOR (sub liens)

– Loans with APR>3.5 + APOR (small creditor QM loans—all liens)

Remember HPMLs have already been subject to the FRB ability to repay rule

11/12/2013

29

QM Levels of Presumption

• What’s APOR?

– The Average Prime Offer Rate

– APOR is published by the FFIEC on behalf of the FRB.

– http://www.ffiec.gov and choose Rate Spread Calculator from Consumer Compliance menu on homepage.

– http://www.ffiec.gov/ratespread/newcalc.aspx.

Rebutting the QM Presumption

• Rebut by showing that a) income, debts, alimony, child support and PITI (including simultaneous loans of which creditor was aware) b) leave consumer with insufficient residual income or assets other than equity c)for meeting living expenses, d) including any recurring and material non‐debt obligations of which the creditor was aware at consummation

11/12/2013

30

QM or non QM

• Non‐compliance with QM standard may be easier to show than rebutting QM presumption

• Unclear how courts will interpret standard for rebuttal

• And many loans get the safe harbor (despite lack of Congressional intent)

• General ATR standard has more prongs to challenge than the rebuttal

Whither Non‐QM Loans?: General ATR

• All loans must comply with the general Ability to Repay (ATR) requirements. A reasonable, good‐faith ATR evaluation must include eight underwriting factors:

– 1. Current or reasonably expected income or assets (other than value of secured property)

– 2. Current employment status (if employment income used to assess ability to repay)

– 3. Monthly mortgage payment—fully indexed rate for ARMs (but may use lifetime max rate); max rate for fixed and step‐rate loans; special rules for IO, neg am and balloon loans

– 4. Monthly payment on any simultaneous loans secured by the same property about which creditor knows or has reason to know

– 5. Taxes and insurance required by creditor, plus association fees/ground

– 6. Debts, alimony and child support obligations (Appendix Q??)

– 7. Monthly back‐end debt‐to‐income ratio (based on mortgage payment(s), current debts, alimony, and child support) or residual income (remaining income after subtracting total monthly debts from total monthly income). May consider both and may use compensating factors (and residual income may be a comp. factor).

– 8. Credit history

11/12/2013

31

Whither Non‐QM Loans?: General ATR

• Special monthly payment calculations include:– Balloons: maximum payment first five years except use maximum payment in

life of loan if loan is HPML– Neg Am: assume amortizing payments after recast and assume recast is based

on minimum payments prior to recast with interest rate rising as quickly as possible after consummation (note this is not worst case scenario because repayment has more time since interest is assumed to increase quickly)

• Creditor must verify information, including income and assets, using “reasonably reliable third‐party records”– Employment status can be orally verified.– Credit lines not reflected on a credit report used as a source need not be

further verified.– Third party sources can include: tax return or transcript, W‐2s, payroll

statements, bank records, employer records or third party with employer information, public benefit documentation , check cashing receipts, funds transfer receipts.

– Records can be obtained from the consumer

Whither Non‐QM Loans?: General ATR

• Comment 43(c)(2)(i)‐1

• Any current or reasonably expected income for ATR analysis includes:– Salary/wages/self‐empl. Income

– Military/reserve duty income

– Bonuses/tips/commissions

– Interest/dividends/retirement benefits or entitlements

– Rental income

– Royalties/trust income

– Public assistance

– Alimony/child support/maintenance

11/12/2013

32

Whither Non‐QM Loans?: General ATR

• Comment 43(c)(2)(vi)‐1&2

• Consider current debt of ALL applicants

• Examples of current debt include– Student/car loans

– Credit cards/revolving debt

– Existing mortgages not paid off at consummation (unless contract for sale)

– Debt where forbearance or deferral expires soon (but remember 12 month rule from App. Q)

Whither Non‐QM Loans?: General ATR

• Credit History, Comment 43(c)(2)(viii) No minimum score or specific take on how to evaluate credit history– Creditor may use rental or utility payment history where traditional credit history is scarce (note problems with this)

– Consider credit history of all applicants

• Credit report as reasonably reliable third‐party record: sufficient but not where creditor knows or has reason to know it is inaccurate in whole or in part.– Fraud or similar alert; statement of dispute; other record that contradicts

– Inaccuratecan disregard without additional records but OK to get additional records

11/12/2013

33

No waiver of ATR claims

• Comment 1026.43(c)(1)‐1(i)

– “A consumer’s statement or attestation that the consumer has the ability to repay the loan is not indicative of whether the creditor’s determination was reasonable and in good faith.”

ATR analysis is individual

• Comment 1026.43(c)(1)‐1(i)

– Question of whether ATR determination is reasonable and in good faith “depends not only on the underwriting standards adopted by the creditor, but on the facts and circumstances of an individual extension of credit and how a creditor’s underwriting standards were applied to those facts and circumstances.”

11/12/2013

34

Evidence that ATR determination not reasonable/good faith

• Comment 1026.43(c)(1)(ii)(B): Evidence, but not elements of a claim.

– 1. Default shortly after consummation or recast– 2. Use of underwriting standards that have historically resulted in

relatively high delinquency and default rates in adverse economic conditions

– 3. Underwriting standards applied inconsistently or used standard different from those of similar loans without reasonable justification

– 4. Disregard of evidence that underwriting standards not effective at determining ATR

– 5. Disregard of evidence of insufficient residual income– 6. Disregard of evidence that ATR relies on refinance of loan or sale of

secured property– (These are not requirements or prohibitions, nor elements of a claim)

Evidence of ATR: Facts on Continuum

• Comment 43(c)(1)‐1(ii)(C)• The longer payments were made, the less likely it is ATR assessment was unreasonable

• Inconsistent underwriting could make a difference or just be bad training with no impact

• Early payment default “may even be sufficient to establish a prima facie case” but may be caused by subsequent change of circumstances.

• Lack of early default may not preclude ATR claim if early payments were made by foregoing necessities such as food and heat

11/12/2013

35

Main course: Loan originator compensation‐‐§1026.36 (a), (b), (d)

• Effective 1/1/14

• Applies to closed‐end consumer credit secured by a dwelling, including closed‐end reverse mortgages

• Compensation – broad definition §1026.36(a)(3)—any $$ or incentive (Rule is simple, Comments are detailed and complex)

• Loan originators subject to restrictions on compensation include loan originator organizations and individual LO/natural person (Comment §1026.36(a)‐1.i.D) (generally excludes creditors except in table‐funded transactions)

Who is a loan originator (LO) subject to the rule?

• Broad definition includes an individual or organization that for $ or expectation of $:

– takes application,

– arranges credit transaction,

– assists in applying for credit,

– presents credit terms to consumer,

– offers or negotiates credit terms,

– extends credit,

– makes a referral to a LO or creditor, OR

– advertises any of the above services

11/12/2013

36

More on who is LO

• LO definition includes creditor in table‐funded transaction

• Comment §1026.36(a)‐1.ii—solely for purposes of the LO rule, a table‐funding creditor is also an LO;

• Creditormust both fund the loan from its own resources & not assign the loan at closing to avoid treatment as LO

More on who is LO

• LO definition:

• Includes employees, agents and contractors of creditor that meet any prong of the definition

• Includes employees, agents and contractors of mortgage broker that meet any prong of the definition

11/12/2013

37

Who is excluded as LO?

• Person who performs clerical duties only and none of LO functions/prongs (including manager)– except “producing manager,” i.e. who also performs LO functions is LO

– Comment §1026.36(a)‐4, details activities that do not count as LO activities

– loan processor/underwriter is not LO • as long as doesn’t communicate credit terms/decisions to consumer

More exclusions from LO

Not an LO:

• a licensed real estate broker who is paid only for real estate brokerage services,

• servicer or servicer employee unless performs any of the LO functions

– refi is covered transaction making servicer employee LO

– but loan mod is not LO function

11/12/2013

38

More on who is not LO

• bona fide 3d party advisor including accountants, attorneys, registered financial advisors, housing counselors are generally excluded

– Needs to take care not to advise on credit terms

– Comment §1026.36(a)‐1.v discusses when 3d party advisor crosses over to LO

– Special rules for HUD approved housing counselors

More on who is not LO

• Employee of manufactured housing retailer unless performs LO functions

• Seller financers who meet specified requirements:

– sellers of 3 or fewer properties/12 mos., including loan terms and ATR, §1026.36(a)(4)

– sellers of 1 or fewer properties/12 mos – less stringent restrictions on loan terms & no ATR, §1026.36(a)(5)

11/12/2013

39

WHAT is compensation subject to LO comp rule and what restrictions apply?

• §1026.36(d) “prohibited payments to loan originators”

• In thinking about LO comp it’s important to distinguish between:

– LO comp that counts as points and fees for QM and HOEPA, that is, tied to the transaction; and

– LO comp that is or may be prohibited and gives rise to claims under 15 USC §1639b

Prohibited payment to LO, §1026.36(d)

• Except for the exceptions:– no LO shall receive &

– no person shall pay to a LO

– directly or indirectly

– $$ that is based on

• a term of a transaction;

• the terms of multiple transactions by an individual LO; OR

• the terms of multiple transactions by multiple individual LOs.

11/12/2013

40

LO comp tied to loan terms‐‐prohibited

• For this rule only “term” has an expansive definition:

– Term = any right or obligation of the parties to the credit transaction.

• Except $ amount of loan does not generally = term for this rule

– Term can include:

• the rights and obligations, or part of any rights or obligations, memorialized in (1) a promissory note or other credit contract, (2) the security interest created and (3) any docs incorporated into the note and/or security interest.

More on expansive definition of “term” for LO comp rule

• “Term” includes fees and charges:

– Any LO or creditor fees/charges imposed on the consumer, including fees/charges financed through the interest rate

– Any fees/charges imposed on the consumer, including any fees/charges financed through the interest rate, for any product or service required to be obtained or performed as a condition of the extension of credit.

– Limitation: only fees and charges required to be disclosed in the GFE and/or HUD‐1 or future TILA/RESPA integrated disclosures are fees that can be considered a “term.”

11/12/2013

41

LO comp‐‐proxies for loan terms

• Proxies – also prohibits comp/$$ based in whole or in part on a factor that is a proxy for a term.

• Two part definition:

– The factor must consistently vary with a term over a significant number of transactions AND [so need lots of data—enforcement/class action v. individual case]

– The LO must have control – must be able to directly or indirectly add drop or change the factor in originating loans.

LO comp—Proxies—Examples

• CFPB says geography (the state, county, census tract etc) where the property is locatedis not typically a proxy for a loan term since LO cannot change it,§1026.36(d)(1)‐2.ii.A

– but what if LO targets homeowners in certain areas because lenders pay more there?

– CFPB does recognize that where LO has ability to affect location—e.g. in a purchase transaction in a multi‐state area, location can be a proxy http://www.mba.org/Compliance/cfpbrecordings.htm

11/12/2013

42

LO Comp—more proxies‐‐examples

• LO can manipulate DTI and LTV so they can be proxies depending on facts

(http://www.mba.org/Compliance/cfpbrecordings.htm, Oct. 17, 2013)

• Whether a loan is held in portfolio or sold could be a proxy – e.g. where loans in portfolio are short term balloons and loans sold are 30 year terms, and LO gets more $ for portfolio, LO can control by steering customers to balloon loans. §1026.36(d)(1)‐2.ii.A

LO Comp Not Based On Loan Terms—Comp Insulated From Proxy Analysis §1026.36(d)(1)‐2.i

• LO Comp is permissible if based on:

–Overall $$ volume

– Long term performance of loans

– Hourly rate for hours actually worked and paid to LO, but

• Rejected industry proposal to have specified comp for products based on average hours to do the work—quite concerned about steering

– Existing v. new customers

11/12/2013

43

More LO Comp Insulated From Proxy Analysis §1026.36(d)(1)‐2.i

• LO Comp is permissible if based on:– Payment fixed in advance for all loans for the creditor

– Quality of loan files

– % of loan apps that result in closed loans

• Removed overhead or other legitimate business expense from list because there could be steering of loans to offices with more overhead and therefore higher fees—want to retain option of proxy analysis for this

LO Comp—shared or pooled compensation

• Shared Compensation—compensation based on terms of multiple transactions by multiple LOs

–General Rule: No sharing of pooled compensation if LOs originate transactions w/different terms and are compensated differently

–§1026.36(d)(1)‐2.iii.

11/12/2013

44

LO Comp—exceptions to prohibition onpooled compensation

• Exceptions to rule v. pooled compensation:

– Designated tax advantaged plans – 2 types:

• Comp to individual LO is permitted in the form of benefits under a defined benefit plan

• Comp to individual LO is permitted in the form of contribution to a defined contribution plan so long as the $$ is not based on the terms of the individual LO’s loans

LO Comp—more exceptions to prohibition on pooled compensation

• Comp based on profits from mortgage related business—“non‐deferred profits‐based comp plan”—not allowed:

– Exceptmay pay up to 10% of LO’s total comp through profits: 10% rule

– Except if individual was LO for 10 or fewer covered loans in 12 months: 10 loan rule

11/12/2013

45

LO Comp—excluded from prohibition on pooled compensation

• NOT comp based on multiple LO transactions so not subject to §1026.36(d)(1)‐3.iii:– If LO organization’s revenues come exclusively from transactions subject to §1026.36(d); and

– If LO org otherwise complies with §1026.36(d)(1),

– Then LO org can pay bonuses to its individual LOs

– And those bonuses are not directly or indirectly based on the terms of multiple transactions of multiple loan originators

• Brain twister

LO Comp—dual compensation, §1026.36(d)(2)

• Payments by person other than the consumer

– Dual compensation:

– If any LO receives compensation directly from a consumer then

• No LO may receive comp directly or indirectly from any other person, and

• No person shall pay $$ to the LO directly or indirectly

• Comp received directly from a consumer includes $$ from another person not the creditor or its affiliates pursuant to an agmt btw consumer and person

11/12/2013

46

LO Comp—dual compensation, §1026.36(d)(2)‐‐exceptions

• EXCEPT and this is a big change from current rule

– LO organization that receives $$ directly from consumer MAY:• Pay comp to individual LO, and

• Individual LO may receive comp from LO org

• So long as $$ is not based on term of the transaction, terms of the LO’s multiple transactions or terms of multiple LOs’ multiple transactions – that is must comply with §1026.36(d)(1)

LO Comp—dual compensation, §1026.36(d)(2)—more exceptions

• More Exceptions—– NO prohibition on dual compensation where consumer pays upfront points and fees to creditor

– And – LO does not receive any comp directly from consumer

• The prohibition on dual comp applies only to LO comp paid directly by the consumer to the LO. The interpretation of what it means to pay directly is so narrow that it eviscerates the prohibition on dual compensation.

11/12/2013

47

LO Comp—dual compensation

• What does comp received directly by LO from consumer mean? §1026.36(d)(2)(i)‐2

• It includes: – “Payments by a consumer to a LO from loan proceeds”

• but payments by consumer to creditor are never payments directly to LO whether paid by consumer upfront or from proceeds

• so doesn’t this exception swallow the rule? §1026.36(d)(2)(i)‐2.i.

– Payments to LO pursuant to an agreement btw consumer & entity other than creditor (or affil) e.g seller, builder, etc ‐§1026.36(d)(2)(i)‐2.iii

• BUT what happens if entity pays creditor instead of LO???

LO Comp received directly by LO from consumer

• Does not include: – pmts derived from increased interest rate ‐2.i or – pmts by consumer to creditor by check or from loan proceeds ‐2.i or

– funds from creditor to reduce consumer’s settlement charges including origination charges to LO; credit on HUD ‐1—how is this different from 1st point? ‐2.ii

– Pmts to creditor pursuant to an agmt btw consumer & entity other than creditor (or affil) e.gseller, builder, etc ‐2.iii

11/12/2013

48

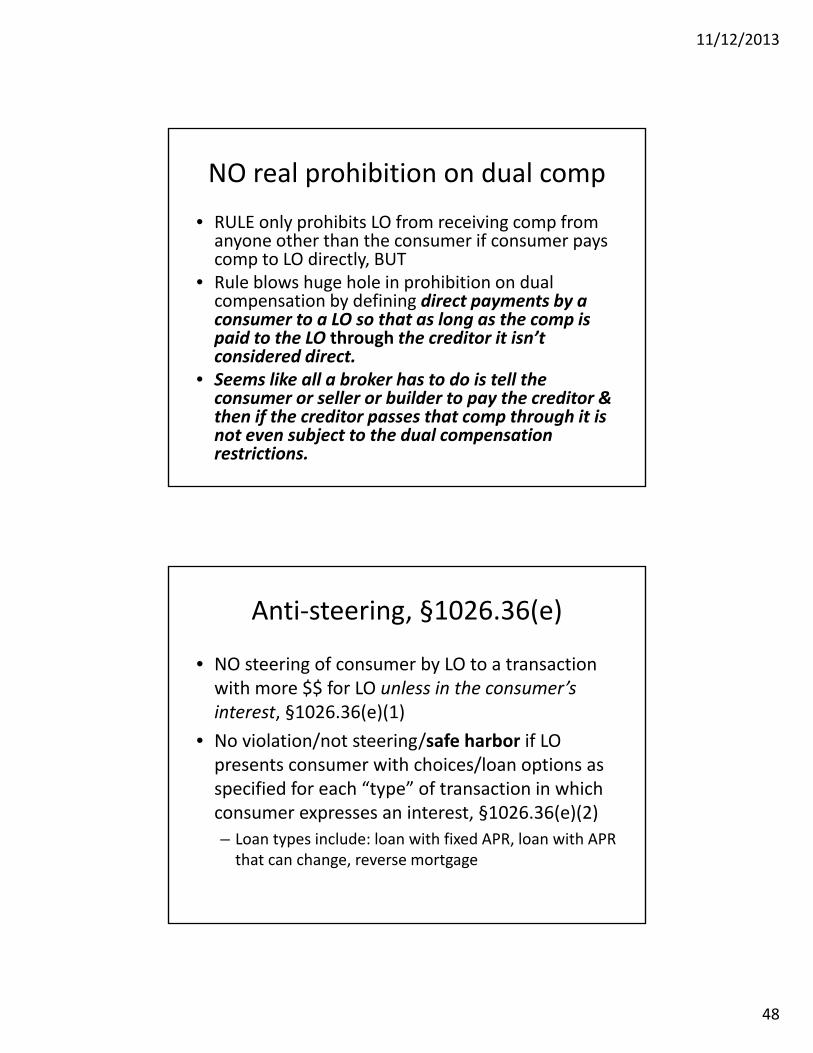

NO real prohibition on dual comp

• RULE only prohibits LO from receiving comp from anyone other than the consumer if consumer pays comp to LO directly, BUT

• Rule blows huge hole in prohibition on dual compensation by defining direct payments by a consumer to a LO so that as long as the comp is paid to the LO through the creditor it isn’t considered direct.

• Seems like all a broker has to do is tell the consumer or seller or builder to pay the creditor & then if the creditor passes that comp through it is not even subject to the dual compensation restrictions.

Anti‐steering, §1026.36(e)

• NO steering of consumer by LO to a transaction with more $$ for LO unless in the consumer’s interest, §1026.36(e)(1)

• No violation/not steering/safe harbor if LO presents consumer with choices/loan options as specified for each “type” of transaction in which consumer expresses an interest, §1026.36(e)(2)

– Loan types include: loan with fixed APR, loan with APR that can change, reverse mortgage

11/12/2013

49

Anti‐steering—loan options‐‐§1026.36(e)(3)

• For each loan “type” LO must present these loan options to avoid steering violation & must have good faith belief that consumer likely qualifies for options:– Lowest interest rate

– Lowest interest rate without nasty loan terms such as PPP, neg am, IO, demand feature, < 7 year balloon, shared equity or shared appreciation, or if reverse mortgage, w/o PPP, shared equity or shared appreciation

– Lowest total $$ discount points, orig points/fees

– If multiple loans with same total $$ points/fees, loan with lowest interest rate and lowest p/f

• Then, LO is free to originate loan with highest comp.

HOEPA—what’s new and what’s substantive

• HOEPA coverage

– Effective for loan apps on or after 1/10/2014

– Covers loans secured by the principal dwellingincluding:• Purchase loans• Refis• Closed‐end home equity loans

• HELOCs (open‐end credit)• Includes manufactured housing, RV or boat if principal dwelling

11/12/2013

50

HOEPA—what’s covered & what’s not

• Exempt from HOEPA coverage: –Reverse mortgage subject to §1026.33

»Must be non‐recourse, payable only after HO’s death, move out or transfers property to be exempt

»Means any reverse mortgage not meeting this definition is covered

–Financing of initial construction of dwelling

–HFA is creditor and originates OR–USDA rural §502 loan

HOEPA triggers

• Loan is subject to HOEPA, a/k/a high‐cost, if meets any one of 3 alternative triggers

• 3 triggers –APR–Points and fees–PPPs (NEW trigger)

11/12/2013

51

HOEPA‐‐APR trigger

• Loan is subject to HOEPA if:–APR is > APOR + 6.5 for 1st lien–APR is > APOR + 8.5 for 1st lien if dwelling is personal property + loan is < $50,000

–APR is > APOR + 8.5 for subordinate lien

– details on interest rate for APR calculation in §1026.32(a)(3)

HOEPA—Points and fees trigger

• Loan is subject to HOEPA if:

–Points & fees are > 5% of TLA

• For loans of $20,000 or more

–Points & fees are > the lesser of 8% or $1,000

• for loans < $20,000

• CFPB to make adjustments in $20k and $1k

11/12/2013

52

HOEPA –PPP trigger

• Loan is subject to HOEPA if loan terms permit PPP:– after 3 years OR– > 2% of principal prepaid (at anytime)

• NOTE: if loan is HOEPA based on PPP, then PPP is illegal loan term (belt and suspenders)

HOEPA—new creditor defense‐‐corrections & unintentional violations

• 15 USC §1639(v)—HOEPA corrections/unintentional violations; §1026.31(h)

• §1639(v) is new and different from existing rule for TILA correction of errors generally; compare 15 USC §1640(b) and (c)

• For HOEPA loans only– Gives creditors & assignees the right to make restitution and offer corrected or modified loans to avoid liability.

– Burden of proof on creditor/assignee

11/12/2013

53

Corrections & unintentional violations—HOEPA only

• Correction of errors made “in good faith:”– Within 30 days after consummation or account opening & before lawsuit

– Creditor/assignee provides written notice to consumer of error &

– Offers restitution &

– Offers consumer a choice between (1) making the loan compliant with HOEPA or (2) modifying the loan so that it is both not high‐cost & benefits the consumer

• §1026.31(h) & §1026.31(h)‐1

Unintentional violations—HOEPA only

• Creditor/assignee may avoid liability if within 60 days after discovery of bona fide error or unintentional violation & before lawsuit it:

• Provides written notice to consumer of violation &

• Offers restitution &

• Offers consumer the choice between: (1) a compliant HOEPA loan, or (2) a modified loan that benefits consumer & is no longer HOEPA

• §1026.31(h) & §1026.31(h)‐1

11/12/2013

54

HOEPA – new prohibited loan terms

• §1026.32(d)—prohibited terms for high cost closed‐end & open‐end loans

–Balloons

–Prepayment penalties

–Acceleration of debt

HOEPA‐‐prohibited terms—balloons, §1026.32(d)(1)

• NO balloon payment loans—except:– if payment schedule is adjusted to seasonal or irregular income of consumer,

– bridge construction loan < 1 year or – a balloon payment QM loan (that’s right folks, you can have a HOEPA balloon payment QM!)

–Open‐end credit loan permitted in which regular payment increases at the end of the draw period

11/12/2013

55

HOEPA – prohibited terms ‐‐ PPPs

• Prepayment penalties are prohibited terms for both closed‐end and open‐end loans

• §1026.32(d)(6)

HOEPA – prohibited terms –acceleration, §1026.32(d)(8)

• No acceleration of debt ‐‐ In general, HOEPA loan may not contain demand feature that allows creditor to accelerate & demand repayment

• EXCEPT if there is:– Fraud or misrepresentation by the consumer in

connection with the loan OR– Default by the consumer– Consumer action/inaction impairs security

interest» Troubling Comment §1026.32(d)(8)‐2.ii allows

acceleration “if one of two consumers obligated on a loan dies . . . if the security is adversely affected.”

11/12/2013

56

HOEPA – new prohibited acts/practices for high‐cost loans, §1026.34

• Home improvement contractor ‐‐may not directly pay/disburse to home improvement Ker

‐‐Old rule now covers more loans: purchase, open end

• NOTICE ‐‐ Failure to include notice that loan is high‐cost when selling loan

• NO same creditor/assignee refi to a new high cost loan w/in 1 year

– Unless in consumer’s interest

– NO evasion

HOEPA –more new prohibited acts/practices for high‐cost loans,

§1026.34• Ability to repay high‐cost, open‐end credit

• Prohibition on making loans without regard to consumer’s repayment ability applies to high‐cost‐open‐end credit §1026.34(a)(4)—

• this seems to be the only place where ATR is considered for open‐end credit which is excluded from ATR/QM rule;

• closed‐end loans follow§1026.43 &

• bridge loans < 1 year are exempt

11/12/2013

57

HOEPA—new prohibited practices—ATR for open‐end loans

• Creditor may not open an open‐end high‐cost mortgage without regard to repayment ability as of account opening.

• Creditor must consider and verify consumer’sreasonably expected income, employment, other assets & current obligations, including prior or simultaneous mortgage secured by same home

HOEPA—new prohibited practices—ATR presumptions for open‐end

• Rebuttable presumption of compliance if creditor:

– Determines repayment ability by:

• Verifying income, assets and obligations, including other loans secured by the home, (mandatory)

• Considers repayment ability based on largest minimum payment assuming

– Full draw at account opening

– Minimum payment throughout draw and repayment period, and

– Maximum APR chargeable under the contract, and

• Considers DTI or residual income

11/12/2013

58

HOEPA—new prohibited practices—ATR presumptions for open‐end

• BUT if:– Creditor follows mandated procedures for verifying income, assets and obligations

– But not optional procedures for determining payment amount and considering DTI and residual income

THEN THERE IS NO presumption of compliance or violation §______

• NO rebuttable presumption of compliance available for balloon loans – except high‐cost open‐end balloon QM

HOEPA‐‐prohibited practices‐‐mandatory pre‐loan counseling,§1026.34(a)(5)

• Pre‐loan counseling—no high‐cost credit w/o counseling certificate– Counseling must occur after consumer has received either the GFE or o‐e TILA disclosures

– Counselor has no affiliation with creditor

– Certificate must include specified content

– Creditor may pay counseling fees but may not condition on completing loan

– No steering by creditor to particular counselor or counseling organization

– Creditor may finance if bona fide 3d party fee

11/12/2013

59

HOEPA—more new prohibited practices

• No creditor or mortgage broker may recommend default §1026.34(a)(6)

• No fee to modify, renew, extend or amend a high‐cost mortgage or to defer payment §1026.34(a)(7)

• No late fee UNLESS– Authorized by K and

– < 4% of past due payment;

– only 1 late fee/missed payment

– Other late fee rules/prohibitions §1026.34(a)(8)

HOEPA—more new prohibited practices

• No charge for payoff statement except:– to cover fax or courier cost (but must be available some way for free),

– Except may charge after more than 4 requests/calendar year

– Payoff stmt must be provided w/in 5 business days

– §1026.34(a)(9)

• No financing of points and fees, §1026.34(a)(10)—including through a separate note

11/12/2013

60

Prohibited practices for dwelling secured loans, §1026.34(b)

• No structuring of high‐cost loan to evade high‐cost mortgage requirements, e.g. by dividing loan into separate parts

– E.g. if creditor structures loan as multiple loans to evade the points and fees trigger

– Loan documented as open‐end , but not meeting the definition of open‐end must be treated as closed‐end and the TLA calculated under closed‐end rules