The New Financial Statements: What the FASB and IASB are Considering Presented November 16, 2010 at...

74

The New Financial Statements: What the FASB and IASB are Considering Presented November 16, 2010 at the North Penn Chapter of the Institute of Management Accountants by Joel Wagoner, MBA, CPA, CMA, CFM Assistant Professor of Accounting Arcadia University

Transcript of The New Financial Statements: What the FASB and IASB are Considering Presented November 16, 2010 at...

The New Financial Statements:What the FASB and IASB are Considering

Presented November 16, 2010 at the

North Penn Chapter of the

Institute of Management Accountants

by

Joel Wagoner, MBA, CPA, CMA, CFM

Assistant Professor of Accounting

Arcadia University

The New Financial Statements

• Purpose: “The purpose of this joint project is to establish a standard that will guide the organization and presentation of information in the financial statements.”

(continued on next slide)

The New Financial Statements

“The results of this project will directly affect how the management of an entity communicates financial statement information to users of financial statements, such as present and potential equity investors, lenders, and other creditors.”

The New Financial Statements

“The boards’ goal is to improve the usefulness of the information provided in an entity’s financial statements to help users make decisions in their capacity as capital providers.”

The Staff Draft of an Exposure Draft

•On July 1, the FASB and IASB jointly released a staff draft of an exposure draft on the new financial statement presentation.

•(This is literally a draft of a draft.)

The Staff Draft of an Exposure Draft

•Originally, the two boards had intended to release an exposure draft by the end of 2010.

•The date was later moved to the first quarter of 2011.

The Staff Draft of an Exposure Draft

•On November 1, the boards announced that “[A]t their October 2010 joint meeting, the Boards acknowledged that they do not have the capacity currently to devote the time necessary to consider the information learned during outreach activities and modify their tentative decisions.”

The Staff Draft of an Exposure Draft

•“Consequently, the Boards decided to not issue an Exposure Draft in the first quarter 2011 as originally planned.”

The Staff Draft of an Exposure Draft

"The Boards will return to this project when they have the requisite capacity. This is expected to be after June 2011.”

The New Financial Statements

•What follows are the major aspects and features of the financial statements that are proposed in the staff draft of July 1, 2010.

The New Financial Statements

•These are an indication of the future of financial reporting, as currently envisioned by the FASB and IASB.

The New Financial Statements

Two main themes of the staff draft on financial statements are

• Cohesiveness

• Disaggregation

Cohesiveness

“The aim. . .is to clarify the relationship between items across financial statements and to have an entity’s financial statements complement each other as much as possible.” [74]

Cohesiveness

“Financial statements that are [cohesive] will display data in a way that clearly associates related information across the statements.” [74]

The New Financial Statements

An entity’s financial statements shall include the following sections, categories, and subcategories, as appropriate:a. A business section, containing:

1. An operating categoryi. An operating finance subcategory

2. An investing category. [62]

The New Financial Statements

An entity’s financial statements shall include:

b. A financing section, containing:

1. A debt category

2. An equity category.

[62]

The New Financial Statements

An entity’s financial statements shall include:

c. An income tax section.

d. A discontinued operation section.

e. A multicategory transaction section. [62]

The Operating Category of the Business Section

•The operating category of the business section will include:

–Assets used in the entity’s day-to-day business and all changes in those assets;– Liabilities that arise from the entity’s day-to-day business and all changes in those liabilities. [72]

The Operating Finance Category

The operating finance subcategory includes liabilities that “are directly related to an entity’s operating activities; however, they also provide a source of long-term financing for the entity.” [74]

The Operating Finance Category

• Liabilities are included in the operating finance subcategory if they meet (all) three conditions:

The Operating Finance Category

Condition 1: “The liability is incurred in exchange for a service, a right of use, or a good, or is incurred directly as a result of an operating activity (rather than a capital-raising activity that funds general business activities, capital expenditures, or acquisitionactivities); [75]

The Operating Finance Category

•Condition 2: “The liability is initially long term”; [75]

The Operating Finance Category

Condition 3: “The liability has a time value of money component that is evidenced by either interest or an accretion of the liability

attributable to the passage of time (that is, the accounting for the liability requires the calculation of an interest component).” [75]

The Operating Finance Category

• The staff draft offers the following examples of liabilities that would be presented in the operating finance subcategory:

a. A net postemployment benefit obligation;b. A lease obligation;c. Vendor financing; [76]

The Operating Finance Category

“If an entity enters into a borrowing arrangement with its own suppliers primarily to acquire a specific good used in production or to procure a specific service, that borrowing arrangement, if initially long term, is classified in the operating finance subcategory of the operating category. If such a borrowing arrangement is not initially long term it is classified in the operating category.” [89]

The Operating Finance Category

•Assets restricted for the purpose of satisfying liabilities reported in the operating finance subcategory will also be presented in the operating finance subcategory. [77]

The Investing Category of the Business Section

The investing category of the business section will include “an asset or a liability that an entity uses to generate a return and any change in that asset or liability”. [81]

The Investing Category of the Business Section

“No significant synergies are created for the entity by combining an asset or a liability classified in the investing category with other resources of the entity.” [81]

The Investing Category of the Business Section

“An asset or a liability classified in the investing category may yield a return for the entity in the form of, for example, interest, dividends, royalties, equity income, gains, or losses.” [81]

The Investing Category of the Business Section

“Examples of investing activities and related items include:

a. The purchase and sale of investments, unless the transaction is part of the business in which the entity is engaged (for example, financial services entities)”

b. Dividends received on equity investments”[82]

The Investing Category of the Business Section

“Examples of investing activities and related items include:

c. Interest earned on debt investmentsd. The purchase and sale of nonfinancial

assets, such as a real estate investmente. Distributions of nonfinancial investments

such as rents, royalties, fees, and commissions

f. Equity method investments and investments in fixed-income securities and equity securities.” [82]

The Financing Section

The financing section shall include items that are part of an entity’s activities to obtain (or repay) capital. [83]

Two categories in the financing section:

Debt

Equity

The Financing Section

Although the statement of comprehensive income and statement of financial position will present debt-related and equity-related activities separately, “The statement of cash

flows shall not include separate categories for debt or equity.” [85]

The Financing Section

“Assets and liabilities and the related income effects that arise from transactions involving an entity’s own equity shall be classified in the debt category and presented separately from borrowing arrangements within the debt category.” [93]

The Financing Section

“Examples of assets and liabilities that arise from transactions involving an entity’s own equity include:

a. A dividend payable

b. A written put option on the entity’s own shares

c. A prepaid forward purchase contract for the entity’s own shares.” [94]

The Financing Section

“Examples of activities or items that may be classified in the equity category in the statement of financial position or the financing section in the statement of cash flows include:a. Issuing shares or other equity instrumentsb. Common, preferred, and treasury sharesc. Cash payments to owners to acquire or redeem the entity’s sharesd. Distributions to owners.” [96]

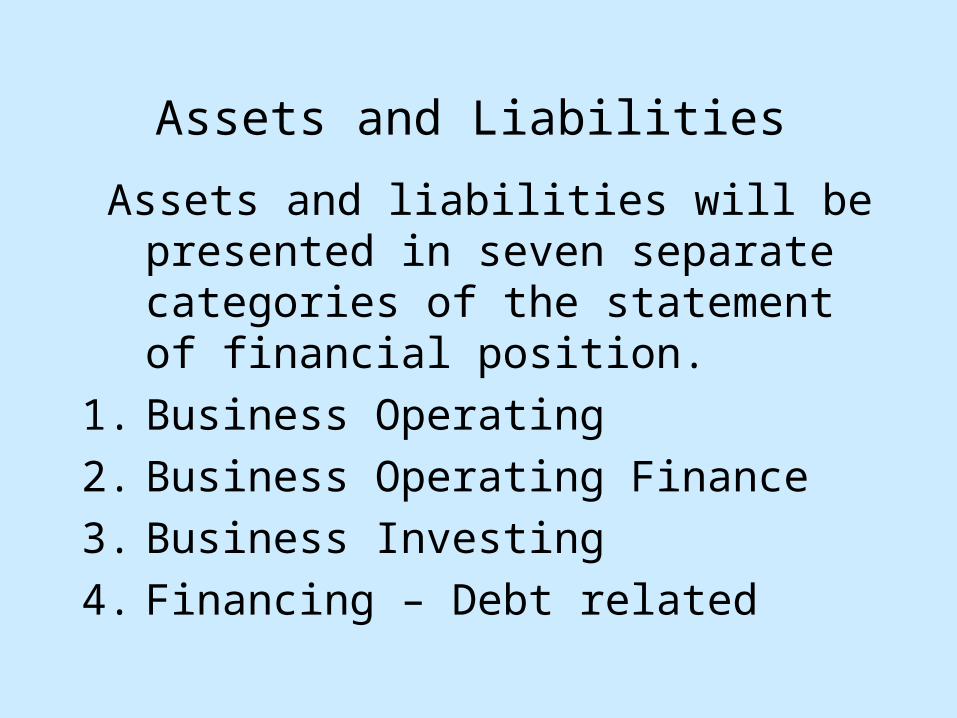

Assets and Liabilities

Assets and liabilities will be presented in seven separate categories of the statement of financial position.

1. Business Operating

2. Business Operating Finance

3. Business Investing

4. Financing – Debt related

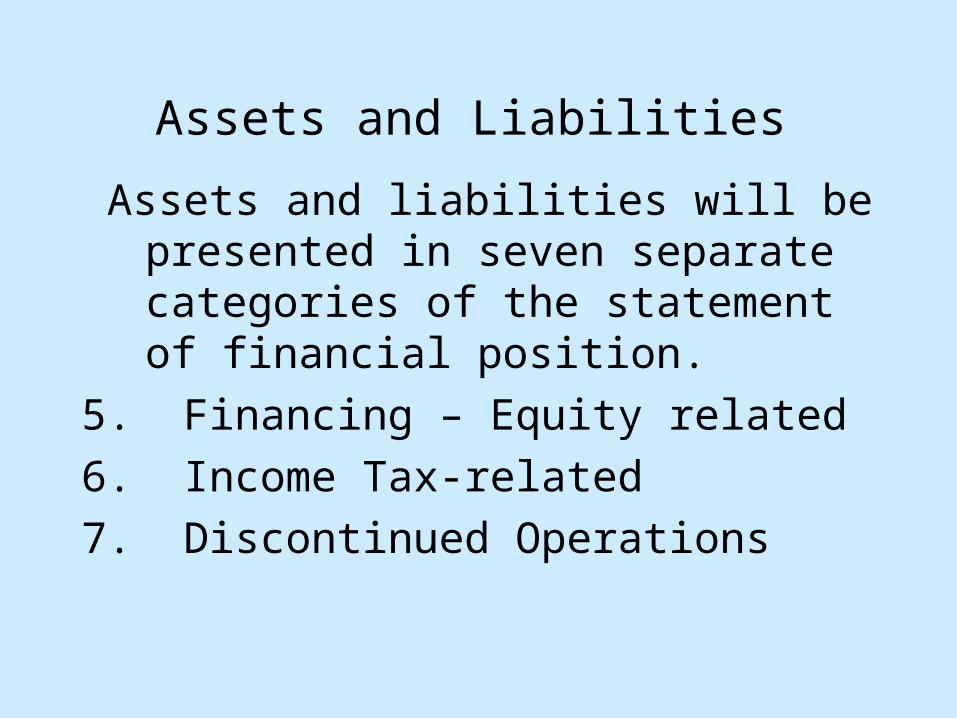

Assets and Liabilities

Assets and liabilities will be presented in seven separate categories of the statement of financial position.

5. Financing – Equity related

6. Income Tax-related

7. Discontinued Operations

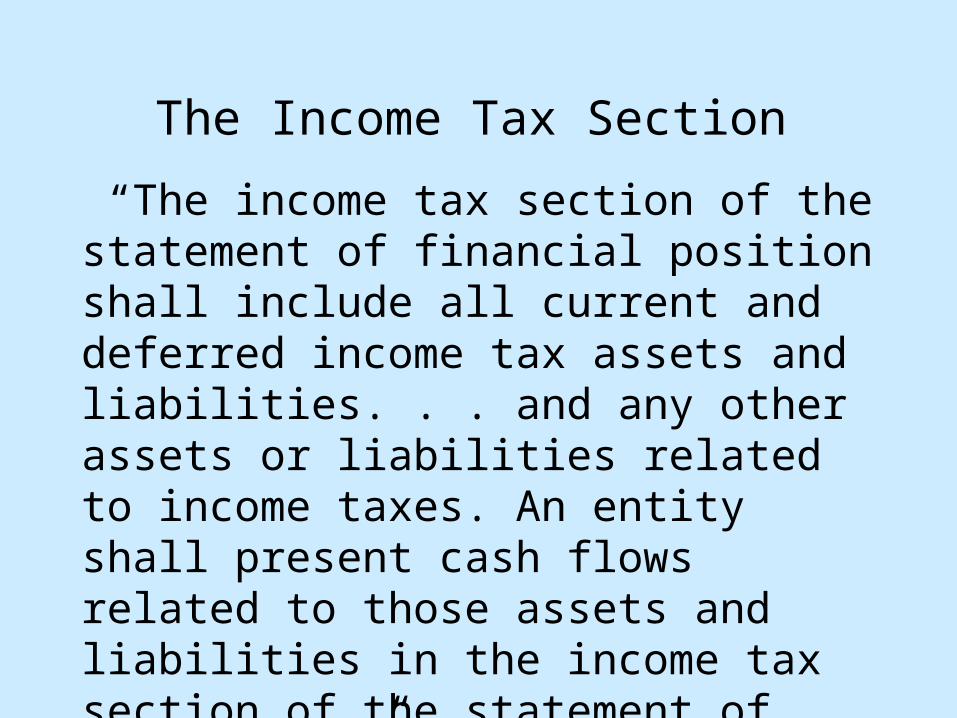

The Income Tax Section

“The income tax section of the statement of financial position shall include all current and deferred income tax assets and liabilities. . . and any other assets or liabilities related to income taxes. An entity shall present cash flows related to those assets and liabilities in the income tax section of the statement of cash flows.” [97]

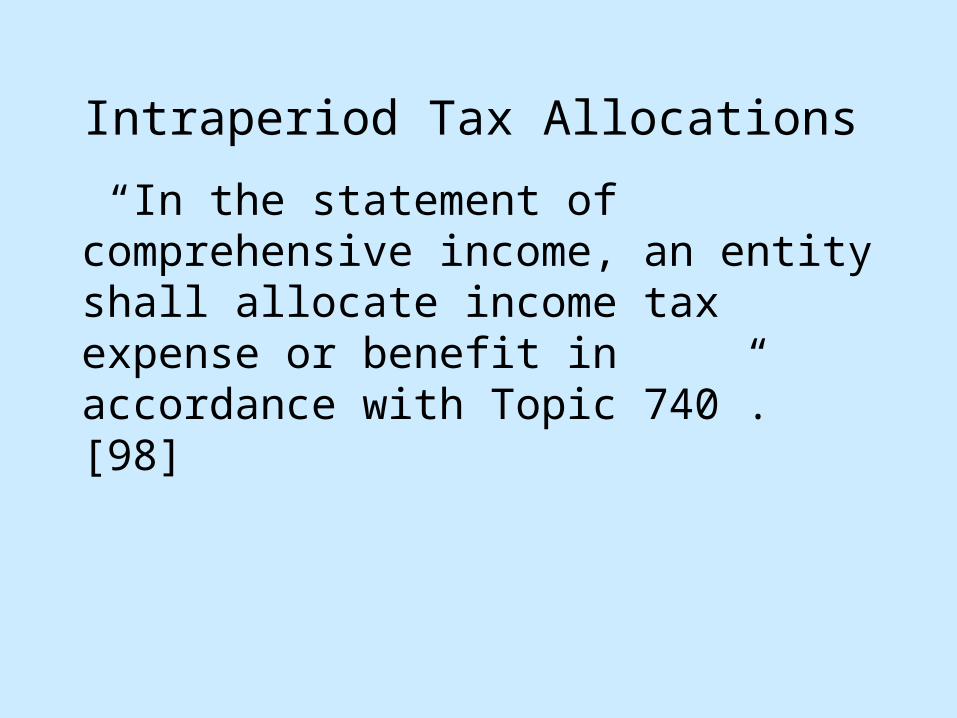

Intraperiod Tax Allocations

“In the statement of comprehensive income, an entity shall allocate income tax expense or benefit in accordance with Topic 740”. [98]

Intraperiod Tax Allocations

“Consequently, an entity may be required to present amounts of income tax expense or benefit in the discontinued operation section and in the other comprehensive income part of the statement of comprehensive income rather than in the income tax section of the statement of comprehensive income.” [98]

Discontinued Operations

“All assets and liabilities related to a discontinued operation shall be classified in the discontinued operation section of the statement of financial position.” [99]

Discontinued Operations

• “All changes in the assets and liabilities of a discontinued operation shall be presented in the discontinued operation section of the statements of comprehensive income and cash flows.” [99]

Multicategory Transactions

“The net effects on comprehensive income and cash flows of an acquisition (or disposal) that results in the recognition of assets and liabilities in more than one section or category in the statement of financial position shall be

classified in the multicategory transaction section of the statements of comprehensive income and cash flows.” [100]

The New Financial Statements

“An entity shall classify an asset or a liability used for more than one function in the

section or category of predominant use.” [106]

Interest Expense

“Interest expense and cash paid for interest shall be presented in the same section, category, or subcategory as the liability giving rise to the interest.” [107]

Classification of Assets and Liabilities

“An entity shall present short-term assets, long-term assets, short-term liabilities, and long-term liabilities separately in each category within its statement of financial position unless a presentation based on liquidity provides information that is more relevant.” [115]

Classification of Assets and Liabilities

• Note: No more “current” and “non-current” assets and liabilities. “Short-term” if within one year, “long-term” if more than one year. [124]

Classification of Assets and Liabilities

If a presentation based on liquidity is more relevant, “an entity shall present all assets and liabilities within each category in order of

liquidity.” [115]

Classification of Assets and Liabilities

“[A]n entity may present some of its assets and liabilities using a short-term/long-term classification and others in order of liquidity

if that presentation provides information that is relevant. The need for a mixed basis of presentation may arise when an entity has diverse operations.” [116]

Disaggregation

Disaggregation: “[D]isaggregate assets and liabilities and present them separately in the statement of financial position when the function, nature, or measurement basis of an item or aggregation of similar items is such

that separate presentation is relevant to an understanding of the entity’s financial position.” [119]

Disaggregation

“Assets or liabilities that do not respond similarly to similar economic events shall

be presented separately in the statement of financial position.” [120]

Classification of Income and Expense

“An entity shall classify items of income and expense that comprise net income into the section, category, and subcategory that are consistent with the classification of the related asset or liability in the statement of financial position and consistent with the related cash flows in the statement of cash flows.” [137]

Classification of Income and Expense

“An item of income or expense that is not related to an asset or a liability in the statement of financial position shall be

classified consistent with the activity generating the income, expense, or cash flow.” [137]

Disaggregation

• The rationale for disaggregating:

“Disaggregation of income and expense items by function is useful in understanding the various activities required to convert an entity’s resources into cash.” [149]

Disaggregation

“An entity shall disaggregate and present its income and expense items by function within each section and category in the statement of

comprehensive income so that the information is useful in understanding the activities of the entity and in assessing the amount, timing, and uncertainty of future cash flows.” [140]

Disaggregation

“An entity shall disaggregate its income and expense items by their nature within the related functional grouping to the extent that the information is useful in assessing the amount, timing, and uncertainty of future cash flows.” [142]

Disaggregation

“Disaggregation by nature within a functional grouping may include, for example, disaggregating total cost of sales into materials, labor, transportation, and energy costs. Disaggregation by nature within a functional grouping may also include, for example, disaggregating revenue from selling goods into wholesale and retail components.” [143]

Disaggregation

“An entity that does not provide a segment disclosure. . . may disclose its income and expense items disaggregated by nature in the notes to financial statements rather than present that information in the statement of comprehensive income.” [146]

Disaggregation

“An entity may choose not to disaggregate. . .by function if (doing so) is not useful to users of financial statements in understanding the entity’s activities and the amount, timing, and uncertainty of future cash flows. (In that case), an entity shall disaggregate its income and expense items by nature and present that information in the statement of comprehensive income.” [148]

The New Financial Statements

“Understanding those activities is particularly useful in assessing the amount, timing, and uncertainty of future cash flows for an entity that develops and produces tangible products.” [149]

The New Financial Statements

“[F]or entities that provide services rather

than. . .products, the conversion of resources into cash happens almost simultaneously. Therefore, for those entities disaggregation of income and expense items by function often does not provide any incremental

information about the amount, timing, and uncertainty of future cash flows.” [149]

Statement of Cash Flows

• The statement of cash flows will be prepared on the direct basis.

• To the extent practical, the activities will align with the sections in the Statement of Financial Position and the Statement of Comprehensive Income.

Statement of Cash Flows

“[D]isaggregate cash flows in the statement of cash flows by classes of cash receipts and payments so that the statement of cash flows provides a meaningful depiction of how the entity generates and uses cash.” [177]

Cash and Cash Equivalents

• “Cash Equivalents” will no longer be presented on the same line of the balance sheet as “Cash”.

Other Comprehensive Income

“In the statement of comprehensive income, an entity shall indicate for each item of other comprehensive income, except for a foreign currency translation adjustment of a consolidated subsidiary, whether the item

relates to an operating activity, investing activity, financing activity, or a discontinued operation.” [139]

So, how does this affect us?

What does this mean for Accountants working in private industry?

So, how does this affect us?

Obviously, accountants who work in reporting functions will have much to learn, and will see their job requirements become more complex.

So, how does this affect us?

What about accountants in other functions?

So, how does this affect us?

Accountants (and consultants) whose responsibilities are related to the development of accounting systems can expect to be very busy as organizations retool their accounting systems to comply with the new requirements.

So, how does this affect us?

Cost accountants will possibly see more information available as a result of the retooling of accounting systems.

So, how does this affect us?

Financial analysts will have much more information on competitors available.

Might we see an increased for accountants in competitive intelligence?

The New Financial Statements

• The staff draft of the exposure draft on Financial Statement Presentation, and additional information, are available on the FASB’s website:

– www.fasb.org

(follow the links)

The New Financial Statements

• The staff draft of the exposure draft on Financial Statement Presentation, and additional information, are available on the FASB’s website:

– www.fasb.org

(follow the links)