The Money Roller Livethemoneyroller.com/wp-content/uploads/2015/12/Astral-Pipes.pdf · 1961– Poly...

26

THE MONEY ROLLER The Money Roller Live Make your Money Work Sector Analysis on Plastic Pipes Latest trend is finding an innovative way for using Plastic Pipes An Initiative of “The Money Roller“ Mohit Ghai BITS PILANI Friday, 24 th July 2015

Transcript of The Money Roller Livethemoneyroller.com/wp-content/uploads/2015/12/Astral-Pipes.pdf · 1961– Poly...

THE MONEY ROLLER

The Money Roller Live Make your Money Work

Sector Analysis on Plastic Pipes

Latest trend is finding an innovative way

for using Plastic Pipes

An Initiative of “The Money Roller“

Mohit Ghai

BITS PILANI

Friday, 24th July 2015

Sunday, March 29,

2015

ABSTRACT

The Plastics Industry in India has made significant development since its inception in 1957 by

producing Polystyrene .The chronology polymer manufacture in India is as under:-

1957 – Polystyrene

1959 – Low Density Poly ethylene (LDPE)

1961– Poly Vinyl Chloride (PVC)

1968 – High Density Poly Ethylene (HDPE)

1978 – Polypropylene

The Indian plastic pipes market is growing at a healthy rate due to tremendous government

spending on commercial, agricultural, residential and sanitation, potable water, mining purpose,

municipal applications, Industrial Applications like transportation of chemicals, oil and gas

distribution, heavy electric wires, solar power. The durability of these pipes along with the various

applications makes it the preferred option over conventional pipes. Furthermore, the construction

sector and the agricultural sector are expected to boost demand for these pipes in the future.

It provides an insight into India’s position in the global market with regards to lower per capita

consumption creating strong opportunity in the domestic market. It also indicates the growing

usage of PVC for making plastic pipes. The market overview section estimates the market size of

the Indian plastic pipe market and also provides the growth rate. Segmented share of plastic pipes

in the total pipes market is highlighted. Porter’s analysis helps understand the dynamics in the

plastic pipes market in India.

Drivers identified include growing demand of the plastic pipes due to tremendous investment by

the government on infrastructure. Furthermore, growth in real estate also adds to the demand. It

has also been found that agricultural sector uses plastic pipes in a big way for all their agricultural

needs. The subsidies and investments doled out by the government should bolster the demand of

plastic pipes. The beneficial properties of plastic boosts the demand for plastic pipes compared to

other types of pipes which also gives rise to replacement demand. One of the challenges the plastic

pipe market is facing is the increasing trend of crude oil prices which squeezes the profit margin

of the manufacturers. The increase in price cannot be passed on to the customer due to tremendous

competition. As a result, low profit margins poses as a challenge to the organized sector. The

primary trends in the plastic pipes market include popularity of CPVC pipes as they have many

beneficial properties and find higher application in both industrial and household uses. Since

domestic demand is always very high, India has to import plastic pipes from other countries. In

addition, many players are increasing their plastic pipes production capacity to meet demand.

Contents

INTRODUCTION .......................................................................................................................... 4

TYPES OF PLASTIC PIPES APPLICATION .............................................................................. 6

MARKET SIZE OF PLASTIC PIPES AS PER APPLICATION .................................................. 7

Indian Scenario (2014) ................................................................................................................ 8

Global Scenario (2014) ............................................................................................................... 8

Product wise break up of plastic products exports in 2013-2014 ............................................... 9

INDUSTRY ANALYSIS WITH PORTER’S 5 FORCES MODEL ............................................ 10

BARGAINING POWER OF SUPPLIERS .............................................................................. 10

BARGAINING POWER OF BUYERS ................................................................................... 10

INTERNAL RIVALRY ............................................................................................................ 10

ENTRY ..................................................................................................................................... 11

THREAT OF SUBSTITUTES ................................................................................................. 11

GROWTH DRIVERS OF PLASTIC PIPES INDUSTRY ........................................................... 12

PLASTIC PIPES GROWTH IN INDIA IN LAST THREE YEARS AND FORTHCOMING

YEARS ......................................................................................................................................... 14

LIST OF PLAYERS INDIA (LISTED AND UNLISTED) ......................................................... 15

PLASTIC PIPES: GLOBAL DEMAND (TOTAL 7.5 BN METERS) ........................................ 16

SWOT ANALYSIS ...................................................................................................................... 17

COMPANY OVERVIEW ............................................................................................................ 22

Awards/ Recognition ................................................................................................................ 22

COMPANY”S HISTORY ............................................................................................................ 23

PRODUCTS OFFERED ............................................................................................................... 24

EQUITY PERFORMANCE OVER LAST 5 YEARS ................................................................. 24

FINANCIAL EVALUATION ...................................................................................................... 25

CONCLUSION ............................................................................................................................. 26

INTRODUCTION

Plastic pipe delivers exceptional value, unwavering reliability and remarkable advantages over

conventional types of piping. It's today's right choice for water service, drainage, fuel gas, conduit

and plumbing & heating.

Due to the advanced technology with superior customer service it has change the whole industry

and created the industry's most sophisticated and diverse products.

Plastic pipe industry is going to be one of the important sector where it will be the growing like

other sectors, continuing to steadily take share from competing materials in a range of markets.

Due to heavy investment in the infrastructure, demand of plastic pipe is going to be too high.

Polyvinyl chloride (PVC) will remain the leading resin used in plastic pipe through 2015, due to

its dominant position in small-diameter applications such as potable water distribution, sanitary

sewer and agricultural markets. While PVC pipe demand declined considerably during the 2005-

2010 period, the expected recovery in building construction activity will fuel strong gains through

2015. High density polyethylene (HDPE) pipe, however, has the best long-term growth prospects

among major plastic pipe resins. HDPE will continue to gain ground on concrete, steel, PVC and

other competing pipe materials.

The Indian plastic pipes market is growing at a healthy rate due to tremendous government

spending on commercial, agricultural, residential and sanitation, potable water, mining purpose,

municipal applications, Industrial Applications like transportation of chemicals, oil and gas

distribution, heavy electric wires, solar power. The durability of these pipes along with the various

applications makes it the preferred option over conventional pipes. Furthermore, the construction

sector and the agricultural sector are expected to boost demand for these pipes in the future.

It provides an insight into India’s position in the global market with regards to lower per capita

consumption creating strong opportunity in the domestic market. It also indicates the growing

usage of PVC for making plastic pipes. The market overview section estimates the market size of

the Indian plastic pipe market and also provides the growth rate. Segmented share of plastic pipes

in the total pipes market is highlighted. Porter’s analysis helps understand the dynamics in the

plastic pipes market in India.

Drivers identified include growing demand of the plastic pipes due to tremendous investment by

the government on infrastructure. Furthermore, growth in real estate also adds to the demand. It

has also been found that agricultural sector uses plastic pipes in a big way for all their agricultural

needs. The subsidies and investments doled out by the government should bolster the demand of

plastic pipes. The beneficial properties of plastic boosts the demand for plastic pipes compared to

other types of pipes which also gives rise to replacement demand. One of the challenges the plastic

pipe market is facing is the increasing trend of crude oil prices which squeezes the profit margin

of the manufacturers. The increase in price cannot be passed on to the customer due to tremendous

competition. As a result, low profit margins poses as a challenge to the organized sector. The

primary trends in the plastic pipes market include popularity of CPVC pipes as they have many

beneficial properties and find higher application in both industrial and household uses. Since

domestic demand is always very high, India has to import plastic pipes from other countries. In

addition, many players are increasing their plastic pipes production capacity to meet demand.

TYPES OF PLASTIC PIPES APPLICATION

We can majorly categorize application of plastic pipes into four parts:

Plastic Pipes that are used for commercial, agricultural, residential and sanitation. In short

these pipes manage storm water. For these purposes we use PVC pipes.

Plastic Pipes that are used for potable water, mining purpose, municipal applications like

waste water, sewer and for Industrial Applications like transportation of chemicals, etc. For

these purposes we use PVC pipes.

Plastic Pipes uses for oil and gas distribution. For these purposes we use HDPE conduits.

Plastic Pipes used for covering heavy electric wires, solar power, etc. For these purposes

we use PVC and HDPE conduits.

Note: In the following report we are using PVC and HDPE pipes instead of individual application.

Please refer this section for getting information regarding individual application.

MARKET SIZE OF PLASTIC PIPES AS PER APPLICATION

We can calculate the market size by calculating number of individuals who are potential buyers

and/or sellers of plastic pipes.

Estimated mean service lifetime of plastics products (Pipes and Conduits) in India is 35

years.

If we see the consumption of Plastic pipes raised to 2 MMT by 2012 due to massive

infrastructure development in the country during 2004 to 2012.

2014, Plastic Pipes consumption in India is about 2.3 MMT against domestic production

capacity of 1.3 MMT.

Plastic industry have already marked the history and also it will definitely have a bigger role to

play particularly because of its wide utilization areas and diverse applicability. Since

independence, plastic industry in India have been playing a predominant role in shaping our lives.

As it an indispensable item in our day to day activity, so its importance cannot be undermined.

Since last decade with the advent of new and improved technologies, the industry has gained

greater importance with the production of better and improved quality of polymers.

Indian Scenario (2014)

Global Scenario (2014)

Industry experts hold unwavering view that growth of the industry will be in double digits (CAGR

15%) with the investment in the irrigation sector. Piping Industry of India is approximately INR

215 billion consisting

69%

9%

6%4%

5% 3%1%3%

Consumption(%)

Pipes Calendering Fittings W&C Films Profiles Sheets Others

2% 3%

8%8%

43%

19%

17%

Bottles Floorings Others Wire&Cables Pipes&Fittings Profiles Films&Sheets

Irrigation: INR 33 billion, PVC Pipes: INR 165 billion, HDPE: INR 15 billion PPR etc: INR 2

billion.

India has irrigation potential of 140 million hectares. Out of this, only 40 per cent is under irrigation

hence there is huge potential for PVC pipes.

Product wise break up of plastic products exports in 2013-2014

33

165

15 20

20

40

60

80

100

120

140

160

180

Irrigation PVC Pipes HDPE PPR

Market Size(2014)

Amount(INR bn)

8%

10%

12%

29%

17%

4%

6%

6%8%

Woven Packaging Items Other Moulded Items

Film,Sheets&plates Others Pipes,Tubes&Fittings

Housewares Writing Instruments Optical Items

INDUSTRY ANALYSIS WITH PORTER’S 5 FORCES MODEL

Market is oligopoly in nature. Market shows significant growth of plastics pipes globally through

the massive investment in diverse industries like commercial, agricultural, sanitation and

residential. Amongst the individual Plastics Materials PVC accounted for 16.5% of the total

consumption.

BARGAINING POWER OF SUPPLIERS

If we see the bargaining of supplier is very high due to oligopoly market structure. There are many

factors which increases the supplier power like availability of only few suppliers, availability of

only many buyers, heavy cost incurred in switching suppliers. Supplier’s power is highly

reinforced when they have highly control over the prices. Due to the wide applicability nature of

plastic pipes in a variety of spheres, there is a great variety in demand also. To cater to this diverse

demands, there are some firms focusing on producing a single product with features making it

suitable for only a specific usage. Also there are some firms producing a product with wide

application areas. Last but not the least, there are also firms that are producing two or more related

products that serves as raw material to produce a finished product in another firm. The Indian

plastic industry is essentially an oligopolistic market. As regards to switching costs, the figures are

high for switching polymer manufacturers because of their small no but low in case of switching

equipment manufacturers due to the presence of small manufacturers in large numbers.

1. Number of Suppliers: The market is consolidated. The market contains few players in

plastic pipes relative to its size.

2. Availability of Substitutes: Products are standardized. Also market is continuously trying

to find the alternate of pipes like PVC, HDPE, etc.

3. High standardization leads to low level of price competition in the marketplace

4. Switching costs amongst suppliers is high

BARGAINING POWER OF BUYERS

Due to the wide applicability of plastic in every industry, it is evident that buyers in this industry

are huge and they range from small to big sized firms. The end user industries for plastic pipes are

Agriculture, Infrastructure, etc. Each of these is again a vast sector encompassing several areas

requiring plastic usage. In this case, buyer’s power is largely determined by firm size and its scale

of operation. Because if a firm is producing a standardized product, in that case it’s definitely

operating in volume so that per unit cost is low. In that sense, it can be said that Agriculture,

Infrastructure have low bargaining power.

1. Buyers are extremely concentrated with high collective buying power

2. Producers are free to set prices as they see fit. Piping industry is in emerging stage and in

coming years it is going to take a drastic change and as industry segment where pipes are

used is too diverse so manufacturers are free to set and change prices.

INTERNAL RIVALRY

Since a large number of plastic producers are lying in the small or medium scale range of

industries, hence internal rivalry is very high. Though it’s also a fact that there are wide variety of

plastic pipes that are produced, each one with a different feature and hence different application

oriented, still the variety is not sufficient to wipe out the competition and enable each producer to

cater to single variety having a single consumer. Though the industry is not stagnant but due to the

presence of large no of small players it becomes mandatory for bigger ones to steal business from

their smaller counter parts in order that the bigger ones wants to expand their output. Also due to

the divergent nature in the scale of operation, firms have different cost structures. Due to the

diverse nature of the industry itself, it often becomes difficult to match prices posed by small

players since they generally specializes on a particular variety, so they can adjust their prices

quickly and often lead to price wars in the industry and the big ones takes time due to their focus

on relatively greater variety.

1. India remains low to medium by the concentrated and standardized marketplace.

2. Solid industry concentration amongst leading firms.

3. Few numbers of players.

4. High levels of product differentiation meaning any new product cannot be easily copied or

updated by another. Specialized products do have proprietary methods for production or

features that separate one from another.

ENTRY

As the number of entrants grew in an industry the net market demand gets distributed among them

resulting in the eroding away of profits of the existing players in the concerned market. Due to the

fragmented nature of the plastic industry, sometimes new entrant faces difficulty in case that it

does not achieve a substantial market share to reach the minimum efficient scale, it usually stands

at a cost disadvantage. Due to the unorganized nature of the industry, many players will want to

enter the industry to enjoy the established market and reap advantages of economies of scope.

Another challenge foe a new entrant is the experience curve effect due to which existing players

enjoys significant cost advantage but the new entrant stands at a cost disadvantage.

Thus only big firms can enter this kind of market having sufficient capital at hand. As for the

existing small firms therefore the threat is high and might prove damaging to a large extent.

1. It’s difficult for a new entrant to penetrate into this market. It needs huge investment to set

up an organized sector.

2. Particular specifications.

3. Technical/proprietary knowledge needed is moderate to medium.

4. Economies of scale needed for competitiveness is medium

THREAT OF SUBSTITUTES

Substitution is driven by two factors: costs, and material properties.

Substitutes greatly disturbed the existing market. As Plastic Pipes industry has been growing since

independence substitutes is also growing. Heavily investment is in R&D for finding the optimum

substitutes to replace plastic pipes. For instance fiberglass.

GROWTH DRIVERS OF PLASTIC PIPES INDUSTRY

Industry is expected grow for the next decade mainly because of demand in agriculture pipes,

plumbing pipes and industrial pipes and change in the government. Prime Minister Narendra Modi

believes in creation of Infrastructure which needs different kind of pipes. Besides he has

announced that every Indian should be have a house by next decade which will create huge demand

of pipes for plumbing, sewerage, rain water etc.

Some key highlights of the budget 2015-2016 which greatly affects the growth of Plastic Pipe

Industry:

Housing for all - 2 cr. houses in Urban areas and 4 cr. houses in Rural areas.

Electrification of the remaining 20,000 villages including off-grid Solar Power- by 2020.

To strengthen rural economy - increase irrigated area, improve the efficiency of existing

irrigation systems, and ensure value addition and reasonable price for farm produce.

To meet these challenges public sector needs to step in to catalyze investment, “Make in

India” programme to create jobs in manufacturing, continue support to programs with

important national priorities such as agriculture, education, health, MGNREGA, rural

infrastructure including roads.

‘Paramparagat Krishi Vikas Yojana’ to be fully supported.

‘Pradhanmantri Gram Sinchai Yojana’ to provide ‘Per Drop More Crop’.

INR 5,300 crore to support micro-irrigation, watershed development and the ‘Pradhan

Mantri Krishi Sinchai Yojana’. States urged to chip in.

Target of INR 8.5 lakh crore of agricultural credit during the year 2015-16.

5 new Ultra Mega Power Projects, each of 4000 MW, in the Plug-and-Play mode

Target of renewable energy capacity revised to 175000 MW till 2022, comprising 100000

MW Solar, 60000 MW Wind, 10000 MW Biomass and 5000 MW Small Hydro.

Reduction in basic customs duty on Ethylene dichloride, vinyl chloride monomer and

styrene monomer from 2.5% to 2%. This will reduce the import price of these products

which is largely used in manufacturing of PVC. Such lower input costs would benefit the

manufacturers of PVC such as Reliance Industries, Finolex, Chemplast Sanmar, DCW

Limited, Supreme Industries, BASF, LG Polymers etc.

Reduction in basic customs duty on HDPE pipes for use in the manufacture of

telecommunication grade optical fiber cables from 7.5% to Nil. This will benefit the oil

and gas industry and in turn the demand for HDPE pipes will go up.

Other Measures like:

Like “Saurashtra Narmada Avataran Irrgiation yojana” has been launched to divert

excess over flowing flood water if narmada allocated to saurashtra region.This excess water

will distributed to 115 reservoirs of seven districts of saurashtra through total 1115 km

long pipelines.

Signed a Memorandum of Understanding (MoU) with Government of Andhra Pradesh

(GoAP) in Hyderabad for developing 1000 MW solar power project(s) in Andhra Pradesh.

Implementation of Govt. projects as per schedule Foreign funded infrastructure projects.

Countering the traditional material pipes. Stringent specifications to ensure quality

products.

Rural water management, which is one of the top priorities of this government, will be the key

demand driver for the industry along with expansion of housing sector and increasing demand for

oil and gas transportation. Around, 52% of the irrigation land is still rain fed. The launch of

”HarKhetKoPaani” & “Swach Bharat Abhiyan” initiatives will drive the growth further.

Infrastructure development, urbanization and the subsequent development of industrial

construction are also facilitating the growth of the pipe industry in India. Industry has been seeing

a very strong demand mainly from new construction in metro cities and last five years from the

Tier II and Tier III cities. Besides new construction demand, there is a huge demand for

replacement of metal pipes to plastic pipes mainly due to the corrosion, rusting, scaling etc.

Also, Indian piping market is still unorganized to the tune of 40 per cent to 50 per cent but with

growth of GDP and Per Capita Income – it will ultimately move to organized players. In last few

years, customers are moving from unbranded to branded quality pipes which are the key reasons

for growth of organized players.

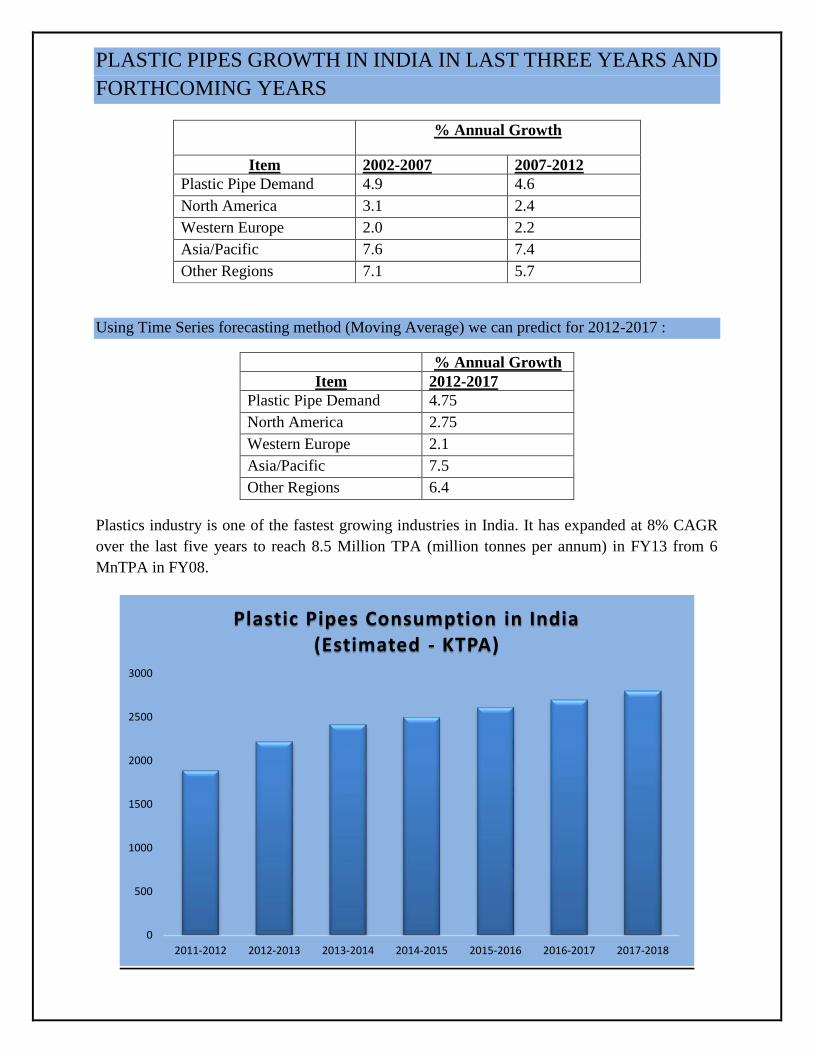

PLASTIC PIPES GROWTH IN INDIA IN LAST THREE YEARS AND

FORTHCOMING YEARS

% Annual Growth

Item 2002-2007 2007-2012

Plastic Pipe Demand 4.9 4.6

North America 3.1 2.4

Western Europe 2.0 2.2

Asia/Pacific 7.6 7.4

Other Regions 7.1 5.7

Using Time Series forecasting method (Moving Average) we can predict for 2012-2017 :

% Annual Growth

Item 2012-2017

Plastic Pipe Demand 4.75

North America 2.75

Western Europe 2.1

Asia/Pacific 7.5

Other Regions 6.4

Plastics industry is one of the fastest growing industries in India. It has expanded at 8% CAGR

over the last five years to reach 8.5 Million TPA (million tonnes per annum) in FY13 from 6

MnTPA in FY08.

0

500

1000

1500

2000

2500

3000

2011-2012 2012-2013 2013-2014 2014-2015 2015-2016 2016-2017 2017-2018

Plastic Pipes Consumption in India (Estimated - KTPA)

LIST OF PLAYERS INDIA (LISTED AND UNLISTED)

There are total 1431 players in Plastic pipes and PVC sector, only 4 are leading ones among

14 key ones.

Listed Unlisted

1. Supreme Ind Neeta Enterprises

2. Finolex Industries Limited Inseal International Pvt. Ltd.

3. Astral Poly Tec Aesteiron Steels Private Limited

4. Axel Polymers Digital Utilities

5. ChemPlast Sanmar Ltd Hiren Industrial Corporation

6. Responsive Ind Roechling Engineering Plastics (India) Pvt. Ltd

7. Nilkamal Pioneer Industries

8. Wimplast Dakle Industrial Plastics

9. PlastiBends Brass Copper & Alloy India Limited

10. Kalpena Ind

11. Jain Irrigation

PLASTIC PIPES: GLOBAL DEMAND (TOTAL 7.5 BN METERS)

As we can see that Budget 2015 is heavily impacting the plastic pipes industry. We are estimating

that demand of plastic pipes is going to climb 8.5% annually through 2017 reaching 11.7 billion.

Our study also shows that advances will come primarily due to increase in infrastructure

development. Due to cost and efficiency another important trend shows plastic pipe gaining market

share as it continues to replace other materials, such as copper, concrete, and steel, due to its low

cost, installation ease, and performance advantages.

Global demand for water pipe is forecast to increase 7.5 percent per year through 2017 to 10.9

billion meters. China alone will account for one-third of the increase, with other industrializing

countries in Asia -- such as India and Indonesia -- and in the Africa/Mideast region also driving

demand. Plastic pipe will be the fastest growing type.

6%7%

21%

21%

45%

Coverage

Central / South America Africa/Mideast North America Europe Asia pacific

SWOT ANALYSIS

STRENGTHS Micro, Small and Medium Enterprises are orienting themselves gradually towards export.

Continuously evolution of new companies with the help of foreign capital that can compete

successfully on third markets.

Emerging market is connecting to future investments in industries that need plastic Pipes

(building, transmission and service, sewer and drainage, irrigation).

WEAKNESSES

Most equipment is physically and morally obsolete, which limits the capacity of the sector

to apply new technologies and to obtain high technical products in conditions of

productivity and low costs

The former great state enterprises have been privatized and are still receiving limited

financing for investments. Most of the equipment is old, with medium productivity and

quality performance. Only some companies invested in new equipment with competitive

performance.

The polymer price fluctuation is strongly connected to the price of crude oil.

Low preoccupation for regaining past active traditional markets

High production costs in companies created from the former great state enterprises with

too much personnel, partially used production capacity, reduced productivity, high energy

consumption, and others.

Insufficient marketing on foreign markets

Incurred Very high production costs

OPPORTUNITIES

Plastic Pipes is a versatile material for piping and has replaced conventional pipes made

from conventional materials such as Galvanized Iron (GI), Cast Iron, Asbestos Cement and

Concrete Cement.

Its compatibility with most fluids, lower cost of material handling and installation, unique

combination of properties and availability of highly reliable jointing system makes it an

excellent competitor in the piping world.

Particularly PVC Pipes low cost, versatility, unique set of properties and performance

makes it the material of choice for dozens of industries such as Oil/gas, transmission, and

construction.

Increase of investments through national capital participation and by attracting foreign.

Companies to set up new companies in the country, or to cooperate with existing

companies.

Development of company activities in management, marketing, quality, research and

branding.

Orienting SMEs to accept contracts for complex products manufacturing meant for large

and multinational companies.

Important investments projects in infrastructure development.

Increase in domestic market demand of products for constructions and Oil/gas industry.

Increased price due to large indirect costs.

Cooperating with large companies that need plastics.

THREATS

The increase in price cannot be passed on to the customer due to the tremendous

competition. As a low profit margin possess a challenge to the organized sector.

The polymer price fluctuation is strongly connected to the price of Oil and gas industry.

Need high amount of investment as well as lots of rules and regulations constraints

available in India.

Cost of Capital is high as market economy is also growing heavily.

Insufficient foreign investment in the sector.

Need to import some types of raw materials necessary to manufacture products needed for

export. Due to heavy import of raw materials cost will increase and it’s difficult for SMEs

to survive and compete in the market.

Low interest in branding.

There is always so much difference in the prices of organized and unorganized sector due to

standardization. As we see the PVC and CPVC plastic pipes are dominating in the market. These

pipes are in the top position in respective consumption. Also demand is huge in the present market

and our study shows that CPVC pipes will register fastest growth in terms of production capacity

in the next five years from financial year 2014 to financial 2019. According to the given data we

can say CPVC pipes is available at very nominal charge and if we talk about the properties of this

plastic pipe it is going to highly available and highly preferred by the consumers in the coming

years as compare to the PVC pipes in the respective segments.

CPVC piping will not fail prematurely due to corrosion, electrolysis, or scale build-up in areas

where water, soil, and/or atmospheric conditions are aggressive. About 70 percent of Indian plastic

pipes products manufactured are in unorganized sector. At the same time organized sector is also

picking up at a rapid pace and this according to us will be the biggest advantage to your Company

because of the continuous efforts putting by the company.

On the basis of given data in above table we can infer that there is always lot much difference

remain of the organized segment of the market over the unorganized market and it is predicted to

grow at a faster rate in the coming years with shifting preferences towards branded and quality

products being witnessed in the domestic market.

According to key trends in the

market there are three

parameters which heavily

affecting the market

Capacity Expansion

Import of PVC Pipes

Popularity of CPVC pipes.

0

10

20

30

40

2014 2016 2018 2020

CPVC Plastic Pipes Consumption (Million Tonnes)

Million Tonnes

The rising demand for plastics in the Gulf Cooperation Council (GCC) and market is expanding

heavily and also increase in product diversification are encouraging theregional manufacturing

industry to ramp up their production capacity. This increasing the demand which results heavy

export of the plastic pipes results in economy growth.

Therefore, demand for plastics is rapidly increasing and soon India will emerge as one of the fastest

growing markets in the world. The next two decades are expected to offer unprecedented

opportunities for the plastic industry in India. This would necessitate industry initiatives to foster

investments, grow the market, upgrade quality standards, enhance global participation, encourage

Indian industry, to adopt and adapt to world class technology and manufacturing practices.

Sewer Ringfit Pipes and Sewer Selfit Pipes

Sewer Ringfit Pipes Sewer Selfit Pipes

One end of the pipe is plain and other end is self-socketed with an integral groove to hold the rubber gasket.

One end of the pipe is plain and the other end is self-socketed on sophisticated automatic machines for high degree of accurate dimension.

The use of these pipes is going to increase because if we see the usage of these pipes we can easily

infer about the market outlook of these pipes. Some of the usage of these pipes are as

Domestic Use – Drainage system for home, offices, hotels, residential & commercial complexes,

hospitals and Sanitation purposes.

Industrial – In Industries, chemical plant, power plants drain as chemical waste lines & overflow

Lines.

Other – Drainage system for public places such as airports, railway Stations, bus stands, hospitals

and theaters. In main vent lines in drainage schemes. Water harvesting systems.

If we talk about the investment in these sectors we can easily see the growth of these pipes.

4.3

6.4

8.9

12.1

0 2 4 6 8 10 12 14

FY05

FY10

FY15

FY20

% OF GDP

% OF GDP

We can infer from this figure that demand for plastics is rapidly increasing and soon India will

emerge as one of the fastest growing markets in the world. The next two decades are expected to

offer unprecedented opportunities for the plastic industry in India.

COMPANY OVERVIEW

Discover the world of superior designs and the marvel of engineering that keeps your home

seamlessly connected inside out.

Astral pipes bring to you the evolved form of crafting homes with the most reliable and state-of-

art pipes and plumbing systems.

With a drive to encompass purity, safety, reliability, flexibility in modern architecture, within 13

years Astral Pipes has more than 350 distributors and thousands of dealers in India penetrating the

plumbing market from metro cities to smaller towns.

Astral pipes are now also available in neighbouring countries like Nepal, Bhutan, Bangladesh and

Sri Lanka. Come be a part of our swift growing network

Astral Pipes specializes in manufacturing the best quality plumbing & drainage systems for both

residential and commercial applications, CPVC piping systems for industrial applications, column

and pressure piping system for agriculture applications and also conduit pipes for residential and

commercial applications.

Equipped with state-of-art production facilities, Astral pipes embraces latest international

technology and provides solutions made for the Indian markets.

Astral Pipes delivers consistent quality effortlessly with its robust facilities present in Ahmedabad

and Dholka (Gujarat), Baddi (Himachal Pradesh) and Hosur (Tamil Nadu) to manufacture

plumbing systems and drainage systems.

Astral pipes has its production facilities at Gujarat and Himachal Pradesh to manufacture plumbing

systems from ½" to 8" diameter. Astral pipes products include CPVC pipes and fittings for hot and

cold water plumbing systems, CPVC industrial piping system for transportation of hazardous and

highly corrosive chemicals, lead free PVC systems for cold water application.

Awards/ Recognition

In 2012 Astral Poly Technik bagged Power Brands Rising Stars India 2012 Award.

It was recognized with Rising Power brands of India in 2012.

For the year 2013 it has been recognized as the Indian Power brand.

Mr.Sandeep Engineer, Managing Director of the Company has been awarded

'PowerBrands Leadership Enterprising Entrepreneur 2012 Award'.

AMA (Ahmedabad Management Association) has conferred Mr. Sandeep Engineer as the

Outstanding Entrepreneur Award for the year 2012–13.

COMPANY”S HISTORY

Astral Poly Technik was established in the year 1999. It started its commercial production of

CPVC pipes and fittings at santej–15 Km from Ahmadabad.

Astral Poly Technik Limited is the first licensee of Lubrizol of USA (formerly known as BF

Goodrich a fortune 500 company) and has equity joint venture with Specialty Process LLC of USA

(manufacturing CPVC plumbing system since 25 years) to manufacture and market the most

advanced CPVC plumbing system for the first time in India.

Astral today manufactures CPVC plumbing systems for both residential and industrial

applications, and also ASTM solvent weld lead free PVC plumbing system.

It is equipped with state of art production facilities at Ahmadabad and Himachal Pradesh to

manufacture plumbing systems from ½ to 8 with all kinds of necessary fittings.

The company’s tie up with Specialty Process LLC of USA to incorporate latest technology and

quality control programs which are widely accepted at global level and to develop CPVC plumbing

systems as per Indian plumbing market.

The company has clients from various industries such as Hospitality which include companies

such as Krishna Heart Hospital Unity Hospital, Gokulam Medical Research ; Hotel & Restaurant

such as The Oberoi , Imperial , Hotel Claridges, Hotel Abbott; Government organizations such as

Canadian Embassy New Delhi, Embassy Of France New Delhi ,American Embassy New Delhi,

British High Commission New Delhi ; Technology parks such as Infocity – Ghandhinagar and

Silicon County – Hyderabad Resorts & clubs such as Nanu Resorts (Goa),Construction such as

Hiranandani construction,G.L Raheja group.

PRODUCTS OFFERED

Astral FlowGuard CPVC

Astral Corzan Aquarius

Astral Aquarius

Astral Underground

Astral Aquatek

Astral Blazemaster

Astral Ultradrain

Astral Flowguard bendable

EQUITY PERFORMANCE OVER LAST 5 YEARS

133.9

194.5

364.45

466.05 447.85

0

100

200

300

400

500

600

2011 2012 2013 2014 2015

Price Linear (Price)

FINANCIAL EVALUATION

Company has maintained healthy, cordial and harmonious industrial relations at all levels. The

enthusiasm and unstinted efforts of the employees have enabled company to remain at the forefront

of the industry. Directors place on record their sincere appreciation for significant contributions

made by the employees through their dedication, hard work and commitment towards the success

and growth of company. Directors take this opportunity to place on record their sense of gratitude

to the Banks, Financial Institutions, Central and State Government Departments, their Local

Authorities and other agencies working with the Company for their guidance and support.

INR in Cr. INR in Cr.

*Forecasted Revenue and PAT

INR in Cr. Growth Rate %

0

50

100

150

200

250

300

350

0

1000

2000

3000

4000

5000

6000

7000

8000

2013 2014 2015 2016* 2017* 2018* 2019* 2020* 2021* 2022* 2023* 2024* 2025*

Revenue (Cr.) PAT (Cr.)

0

5

10

15

20

25

30

35

40

45

0

100

200

300

400

500

600

700

800

2013 2014 2015 2016* 2017* 2018* 2019* 2020* 2021* 2022* 2023* 2024* 2025*

EBITDA Growth Rate

CONCLUSION

Infrastructure spending has begun to rebound from the financial crisis and is expected to grow

significantly over the coming decade. Therefore we can anticipate that market demand is going to

be heavily increase and it helps both the organized sector and unorganized sector available in the

market. This results heavy spending in managing the drainage system which shows growth of

sewer pipes.