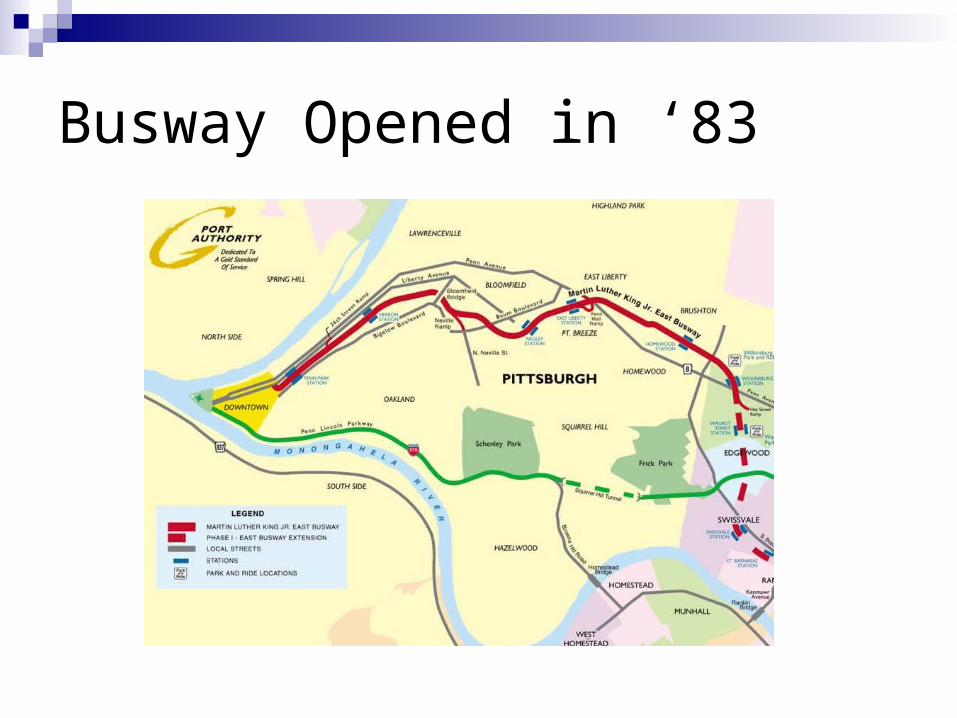

The Martin Luther King Jr. East Busway

46

The Martin Luther The Martin Luther King Jr. East Busway King Jr. East Busway A Cost-Benefit A Cost-Benefit Analysis Analysis

-

Upload

lewis-glass -

Category

Documents

-

view

38 -

download

3

description

The Martin Luther King Jr. East Busway. A Cost-Benefit Analysis. Overview. Pre-1978 History Port Authority’s CBA (1978) Revising Port Authority’s CBA Actual Results. The busway was part of the Early Action Plan (EAP) EAP consisted of 3 other projects. - PowerPoint PPT Presentation

Transcript of The Martin Luther King Jr. East Busway

The Martin Luther King Jr. The Martin Luther King Jr. East BuswayEast Busway

A Cost-Benefit AnalysisA Cost-Benefit Analysis

Overview

Pre-1978 History Port Authority’s CBA (1978) Revising Port Authority’s CBA Actual Results

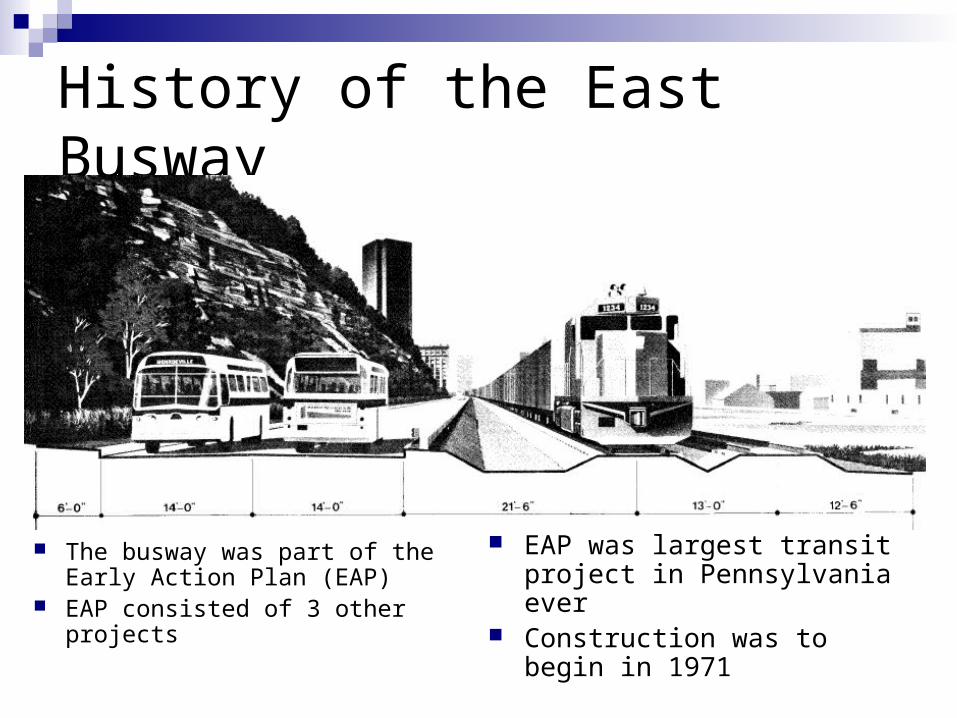

History of the East Busway

The busway was part of the Early Action Plan (EAP)

EAP consisted of 3 other projects

EAP was largest transit project in Pennsylvania ever

Construction was to begin in 1971

Delay of the East Busway

Lawsuit delayed the project 6 years until 1978

Factors that increased project costs:Oil crisesSpiraling inflationRight of way dispute with railroads

Construction was completed in 1983

Port Authority’s ’78 CBA

Capital Costs Operating Costs Benefits Benefit Cost Ratio

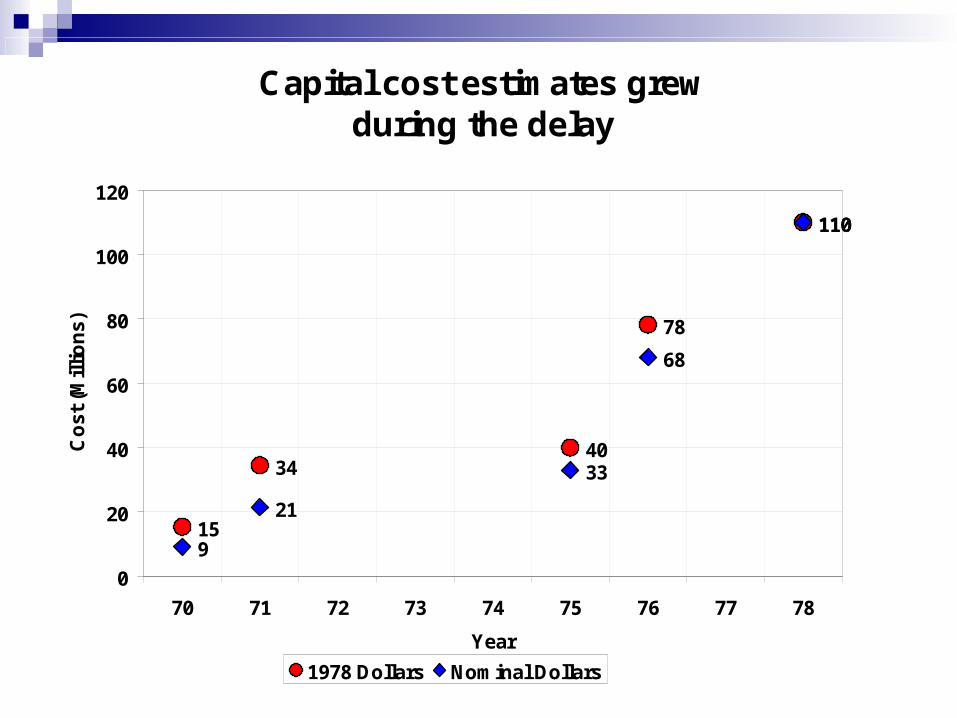

Capital cost estimates grew during the delay

15

3440

78

110

9

21

33

68

110

0

20

40

60

80

100

120

70 71 72 73 74 75 76 77 78

Year

Co

st (

Mil

lio

ns)

1978 Dollars Nominal Dollars

Port Authority’s Capital Costs

Project Costs

Original Project $20,000,000

Cost of Delay (from inflation) $20,000,000

Additional Cost of Property Over Estimate $6,800,000

Costs for Adjustments to Conrail

Cost to Accommodate Conrail $36,900,000

Vertical Separation $6,000,000

Improvement Costs

Neville Ramp Addition $10,600,000

East Liberty Station Improvements $3,200,000

Additional Changes $6,500,000

Capital Costs Total $110,000,000

Port Authority’s Operating Costs

Per Year

Maintenance Costs $700,000

Total Operating Costs $700,000

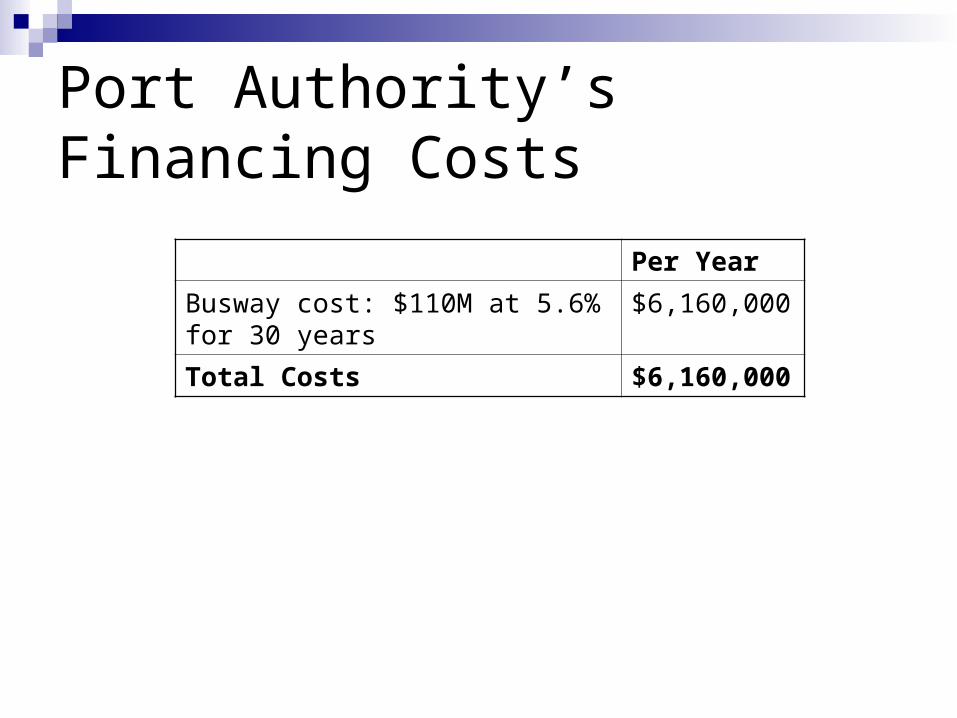

Port Authority’s Financing Costs

Per Year

Busway cost: $110M at 5.6% for 30 years

$6,160,000

Total Costs $6,160,000

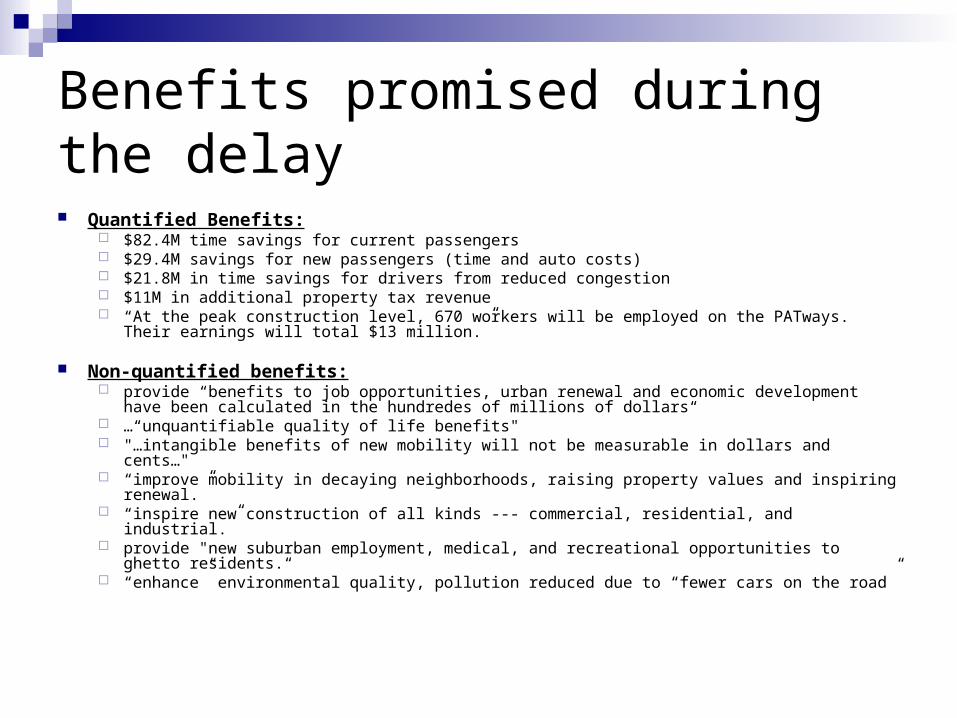

Benefits promised during the delay

Quantified Benefits: $82.4M time savings for current passengers $29.4M savings for new passengers (time and auto costs) $21.8M in time savings for drivers from reduced congestion $11M in additional property tax revenue “At the peak construction level, 670 workers will be employed on the PATways. Their

earnings will total $13 million.”

Non-quantified benefits: provide “benefits to job opportunities, urban renewal and economic development have been

calculated in the hundredes of millions of dollars“ …“unquantifiable quality of life benefits" "…intangible benefits of new mobility will not be measurable in dollars and cents…" “improve mobility in decaying neighborhoods, raising property values and inspiring renewal.” “inspire new construction of all kinds --- commercial, residential, and industrial.” provide "new suburban employment, medical, and recreational opportunities to ghetto

residents.“ “enhance” environmental quality, pollution reduced due to “fewer cars on the road”

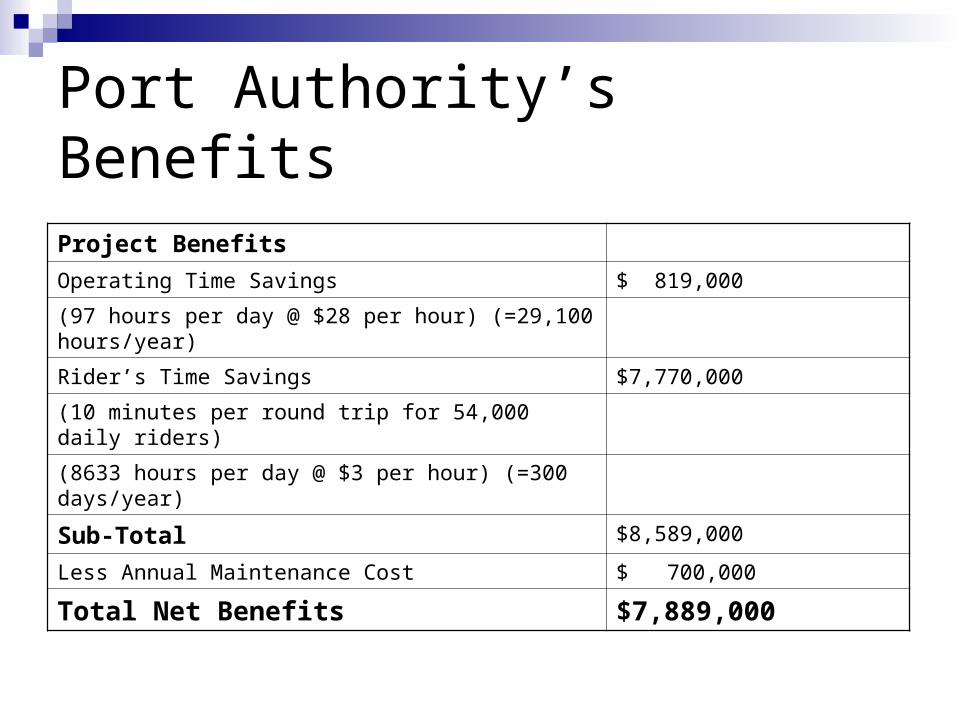

Port Authority’s Benefits

Project Benefits

Operating Time Savings $ 819,000

(97 hours per day @ $28 per hour) (=29,100 hours/year)

Rider’s Time Savings $7,770,000

(10 minutes per round trip for 54,000 daily riders)

(8633 hours per day @ $3 per hour) (=300 days/year)

Sub-Total $8,589,000

Less Annual Maintenance Cost $ 700,000

Total Net Benefits $7,889,000

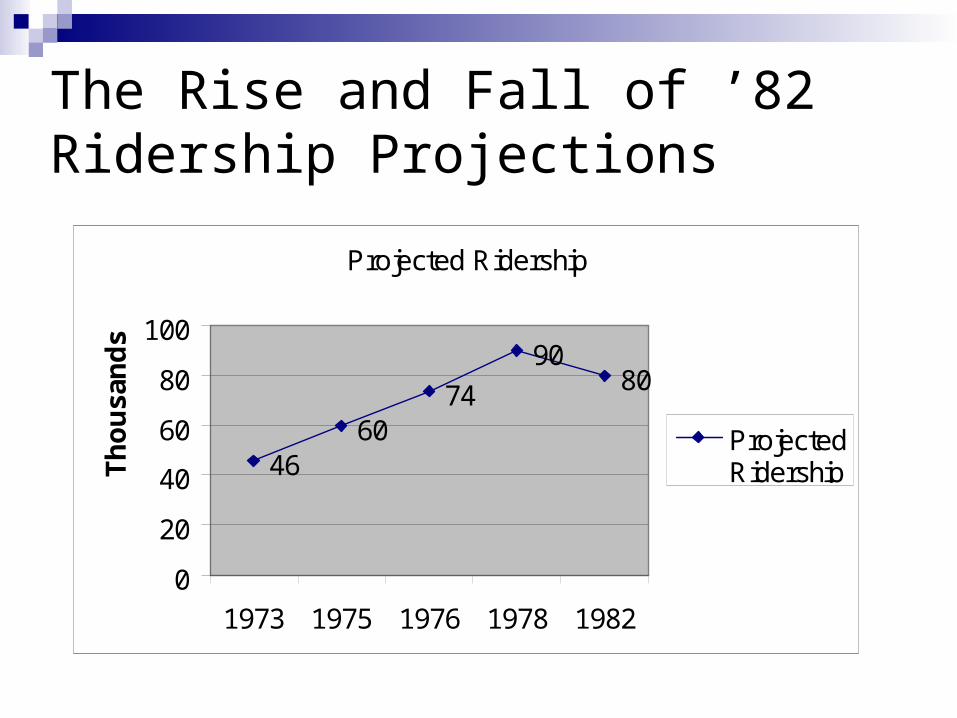

The Rise and Fall of ’82 Ridership Projections

Projected Ridership

4660

74

9080

0

20

40

60

80

100

1973 1975 1976 1978 1982

Th

ou

san

ds

ProjectedRidership

Port Authority’s “CBA”

What’s missing from Port Authority’s analysis?

Missing benefits No loan principal No NPV No discount rate The benefit-cost ratio

may be inflated

Port Authority’s Benefit Problems

’78 analysis indicates many potential benefits without any attempt at measurement: Vehicle Emissions Safety

’78 analysis points to future benefits ($10 million/yr) for future riders without analyzing associated costs: Service Expansion Unidentified Improvements

Previously mentioned benefits gone!

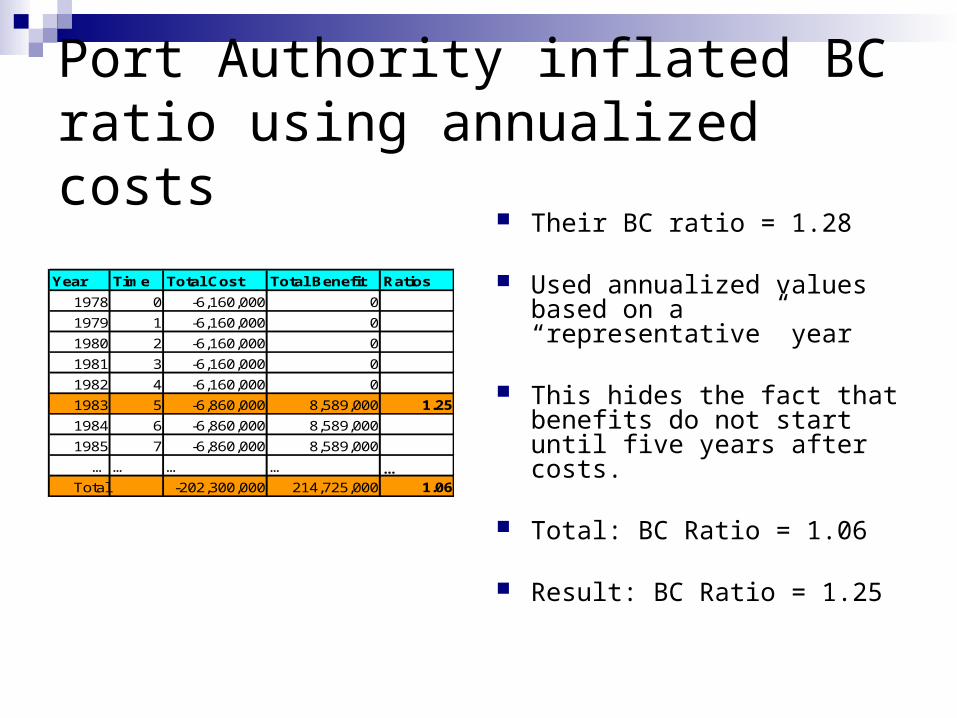

Port Authority inflated BC ratio using annualized costs

Their BC ratio = 1.28

Used annualized values based on a “representative” year

This hides the fact that benefits do not start until five years after costs.

Total: BC Ratio = 1.06

Result: BC Ratio = 1.25

Year Time Total Cost Total Benefit Ratios

1978 0 -6,160,000 0

1979 1 -6,160,000 0

1980 2 -6,160,000 0

1981 3 -6,160,000 0

1982 4 -6,160,000 0

1983 5 -6,860,000 8,589,000 1.25

1984 6 -6,860,000 8,589,000

1985 7 -6,860,000 8,589,000

… … … … …Total -202,300,000 214,725,000 1.06

Their Way

Time Savings 7,770,000

Operating Savings 819,000

Maintenance Cost -700,000

Annualized Benefits 7,889,000

Finance Cost -6,160,000

Annualized Costs -6,160,000

Annualized BC Ratio 1.28

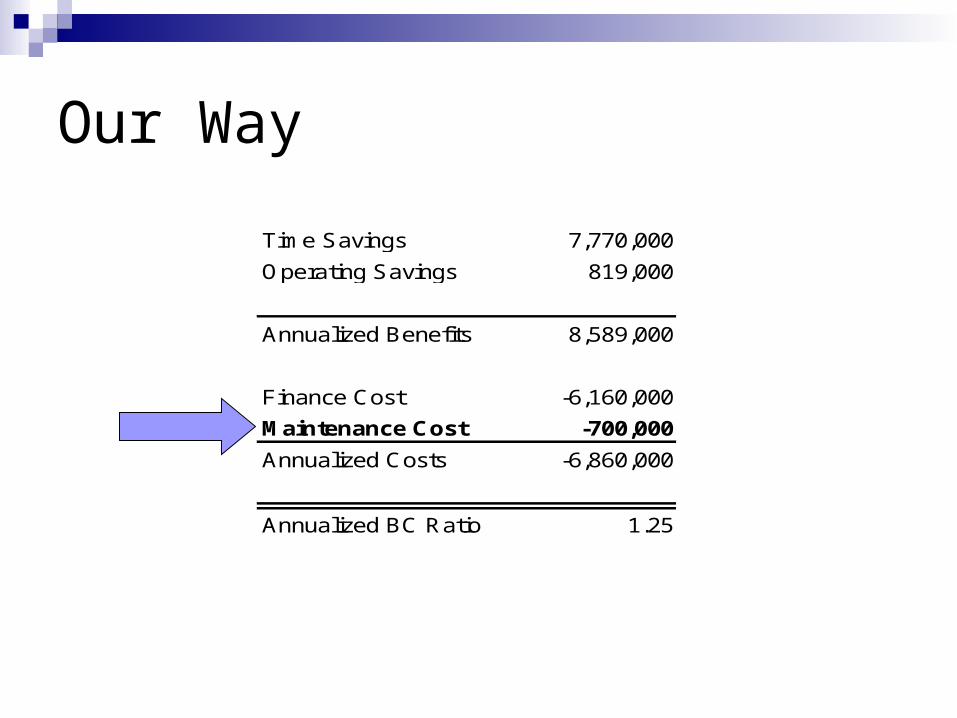

Our Way

Time Savings 7,770,000

Operating Savings 819,000

Annualized Benefits 8,589,000

Finance Cost -6,160,000

Maintenance Cost -700,000

Annualized Costs -6,860,000

Annualized BC Ratio 1.25

Adding the loan principal makes a difference

No principal payments:

NPV = 12,425,000

With principal payments:

NPV = -32,346,343

Assumes 0% discount rate over 30 years. Thus NPV = net benefits

Estimating a discount rate for 1978

Nominal yields on corporate AAA bonds 8% Nominal T-bill rates 7.57% Inflation 7.6% Corporate tax est.40% Individual tax est. 20%

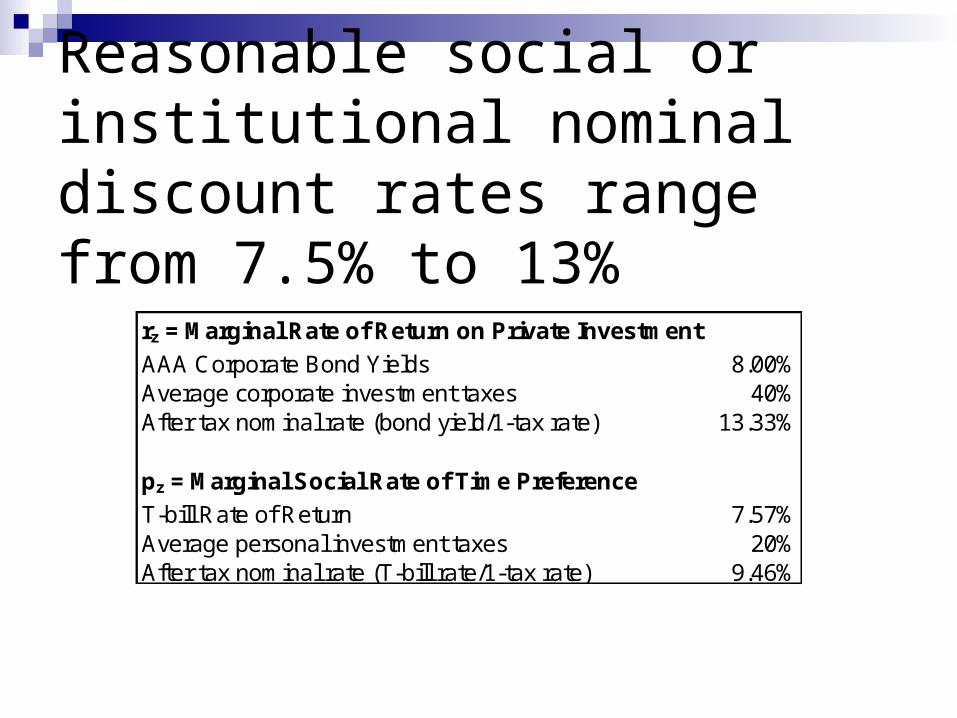

Reasonable social or institutional nominal discount rates range from 7.5% to 13%

rz = Marginal Rate of Return on Private Investment

AAA Corporate Bond Yields 8.00%Average corporate investment taxes 40%After tax nominal rate (bond yield/1-tax rate) 13.33%

pz = Marginal Social Rate of Time Preference

T-bill Rate of Return 7.57%Average personal investment taxes 20%After tax nominal rate (T-bill rate/1-tax rate) 9.46%

Discounting actually improves NPV

Rate NPV

Undiscounted 0% -32,346,344

Untaxed Rz 7.57% -31,284,651

Aftertax Rz 8.00% -31,141,424

Untaxed Pz 9.46% -30,635,167

Aftertax Pz 13.33% -29,230,007

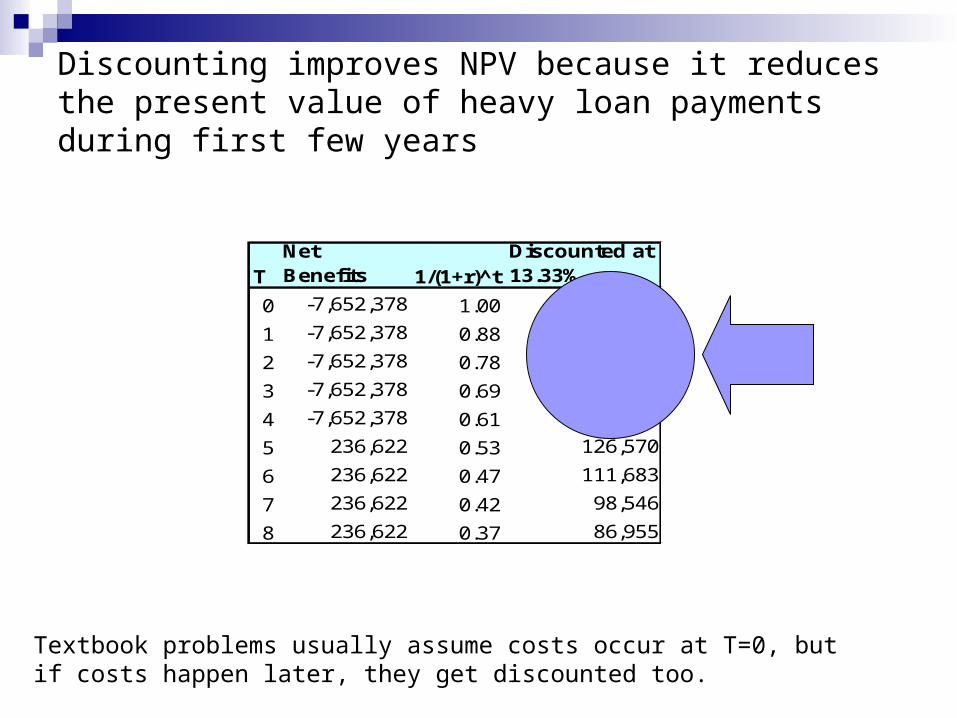

Discounting improves NPV because it reduces the present value of heavy loan payments during first few years

TNet Benefits 1/(1+r)^t

Discounted at 13.33%

0 -7,652,378 1.00 -7,652,378

1 -7,652,378 0.88 -6,752,297

2 -7,652,378 0.78 -5,958,084

3 -7,652,378 0.69 -5,257,288

4 -7,652,378 0.61 -4,638,920

5 236,622 0.53 126,570

6 236,622 0.47 111,683

7 236,622 0.42 98,546

8 236,622 0.37 86,955

Textbook problems usually assume costs occur at T=0, but if costs happen later, they get discounted too.

Additional problems with Port Authority’s analysis Funding too aggregated Economic impact of taxes ignored Time savings understated Option value ignored Accounting for future inflation ignored No recognition of uncertainty

Funding was more complicated than a single bond issue

$88M federal grants

$11M in state contributions

$11M local funding

10%

10%

80%

Federal

State

Local

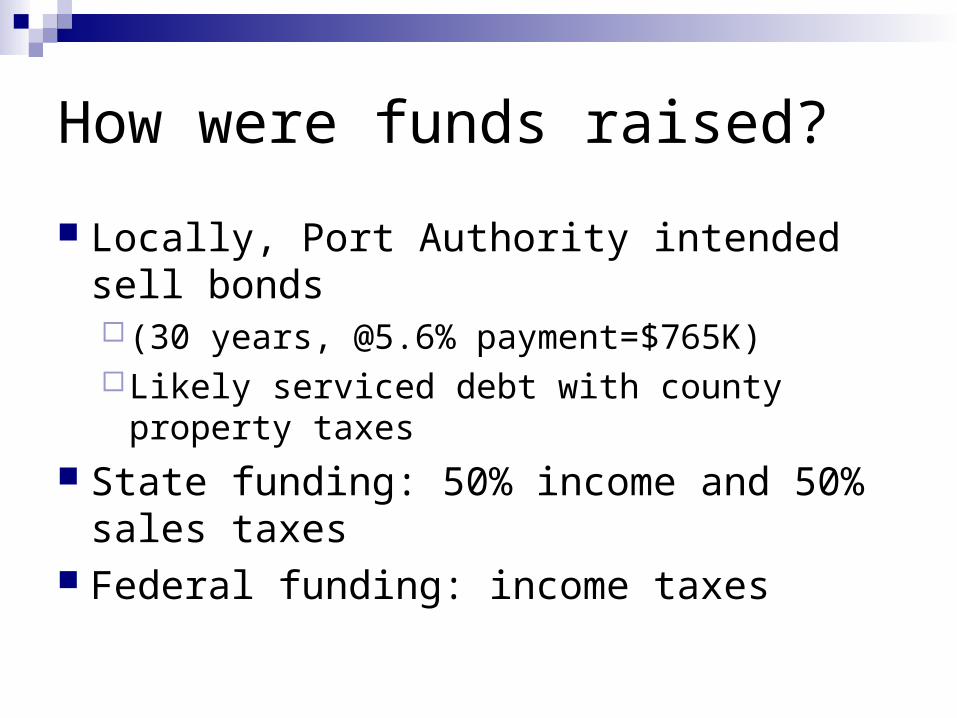

How were funds raised?

Locally, Port Authority intended sell bonds (30 years, @5.6% payment=$765K)Likely serviced debt with county property

taxes State funding: 50% income and 50% sales

taxes Federal funding: income taxes

When were the funds raised?

State and federal funding to be appropriated each year over the construction project (4-5yrs)

Local funding serviced over 30 years

Distribution of Funding

18%21% 22% 21%

18%

0%

5%

10%

15%

20%

25%

Y1 Y2 Y3 Y4 Y5

Construction Year

How much did they cost to raise?

Amount Rate METB

Local property taxes 22,957,134 17.0% 3,902,713

State income taxes 5,500,000 25.0% 1,375,000

State sales taxes 5,500,000 43.5% 2,392,500

Federal income taxes 88,000,000 43.5% 38,280,000

Total 45,950,213

With METB and more realistic funding assumptions NPV gets worse, except for undiscounted case

Rate NPV

Undiscounted 0% -32,346,344

Untaxed Rz 7.57% -31,284,651

Aftertax Rz 8.00% -31,141,424

Untaxed Pz 9.46% -30,635,167

Aftertax Pz 13.33% -29,230,007

Rate NPV

Undiscounted 0% 29,317,653

Untaxed Rz 7.57% -68,520,605

Aftertax Rz 8.00% -70,579,163

Untaxed Pz 9.46% -76,261,658

Aftertax Pz 13.33% -84,552,731

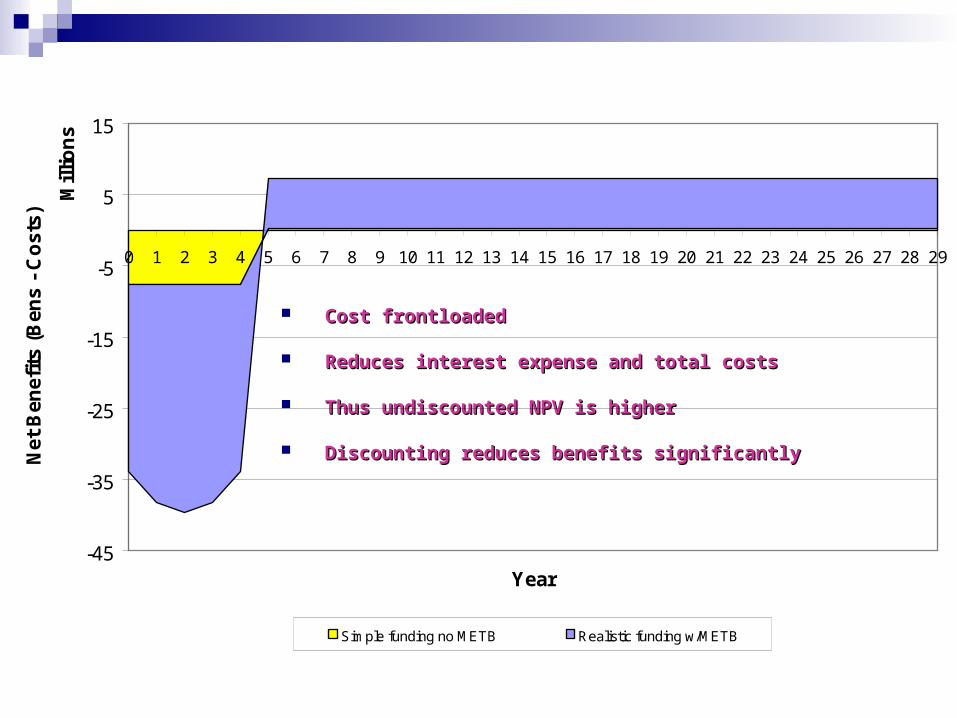

Previous Assumptions With realistic funding and METB

Cost frontloadedCost frontloaded

Reduces interest expense and total costsReduces interest expense and total costs

Thus undiscounted NPV is higherThus undiscounted NPV is higher

Discounting reduces benefits significantlyDiscounting reduces benefits significantly

-45

-35

-25

-15

-5

5

15

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29

Mil

lio

ns

Year

Net

Ben

efit

s (B

ens

- C

ost

s)

Simple funding no METB Realistic funding w/METB

Port Authority’s benefits could have been higherProject Benefits

Operating Time Savings $ 819,000

(97 hours per day @ $28.00 / hour) (29,100 hours/year)

Rider’s Time Savings $8,100,000

18.5 minutes per round trip for 34,300 daily riders

10,617 hours per day @ $3 per hour, 256 days/year

Sub-Total $8,919,000

Option Value

(Assumes Bus Commuters to Car Commuters 1:1)

(6 trips per driver a year @ $0.57/trip) $ 184,700

Total Measurable Benefits $9,103,700

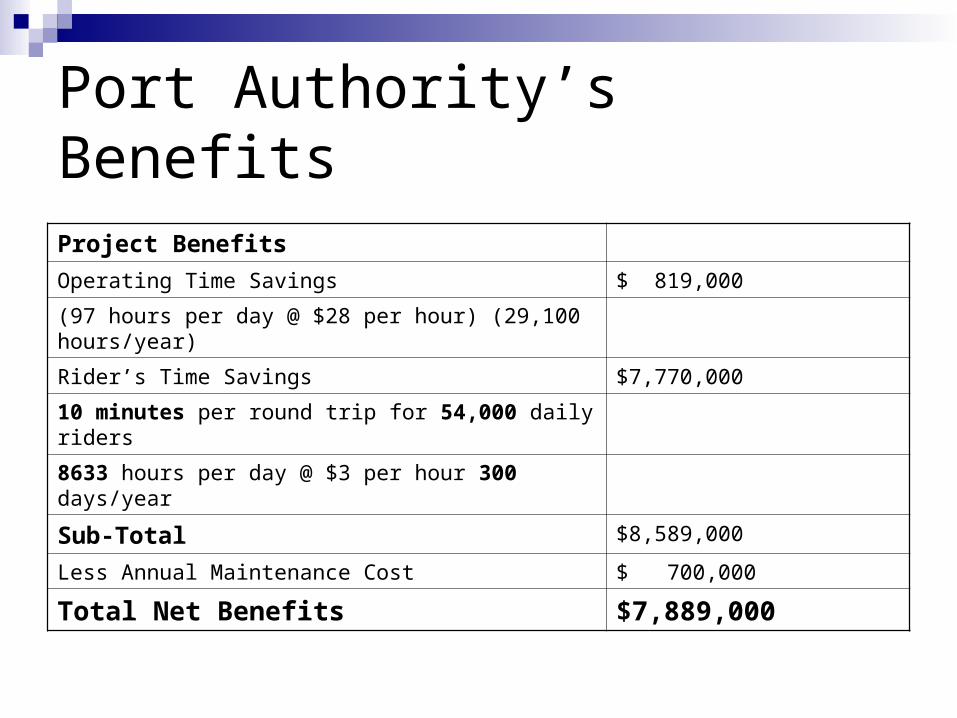

Port Authority’s Benefits

Project Benefits

Operating Time Savings $ 819,000

(97 hours per day @ $28 per hour) (29,100 hours/year)

Rider’s Time Savings $7,770,000

10 minutes per round trip for 54,000 daily riders

8633 hours per day @ $3 per hour 300 days/year

Sub-Total $8,589,000

Less Annual Maintenance Cost $ 700,000

Total Net Benefits $7,889,000

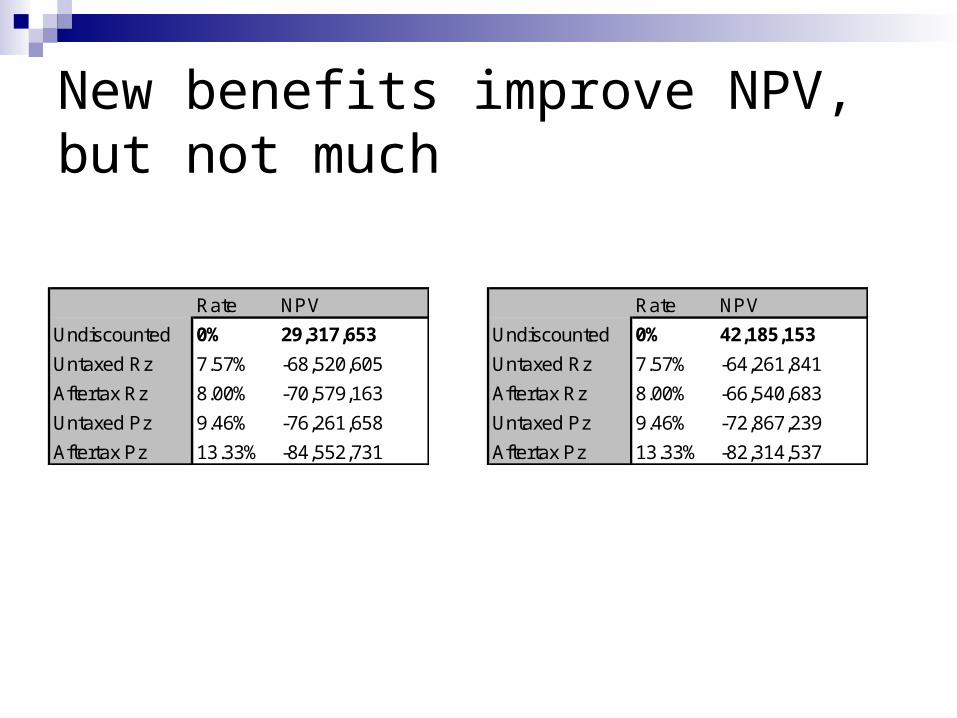

New benefits improve NPV, but not much

Rate NPV

Undiscounted 0% 29,317,653

Untaxed Rz 7.57% -68,520,605

Aftertax Rz 8.00% -70,579,163

Untaxed Pz 9.46% -76,261,658

Aftertax Pz 13.33% -84,552,731

Rate NPV

Undiscounted 0% 42,185,153

Untaxed Rz 7.57% -64,261,841

Aftertax Rz 8.00% -66,540,683

Untaxed Pz 9.46% -72,867,239

Aftertax Pz 13.33% -82,314,537

Inflation/Uncertainty

-64 -82M NPV? Why bother!

Busway Opened in ‘83

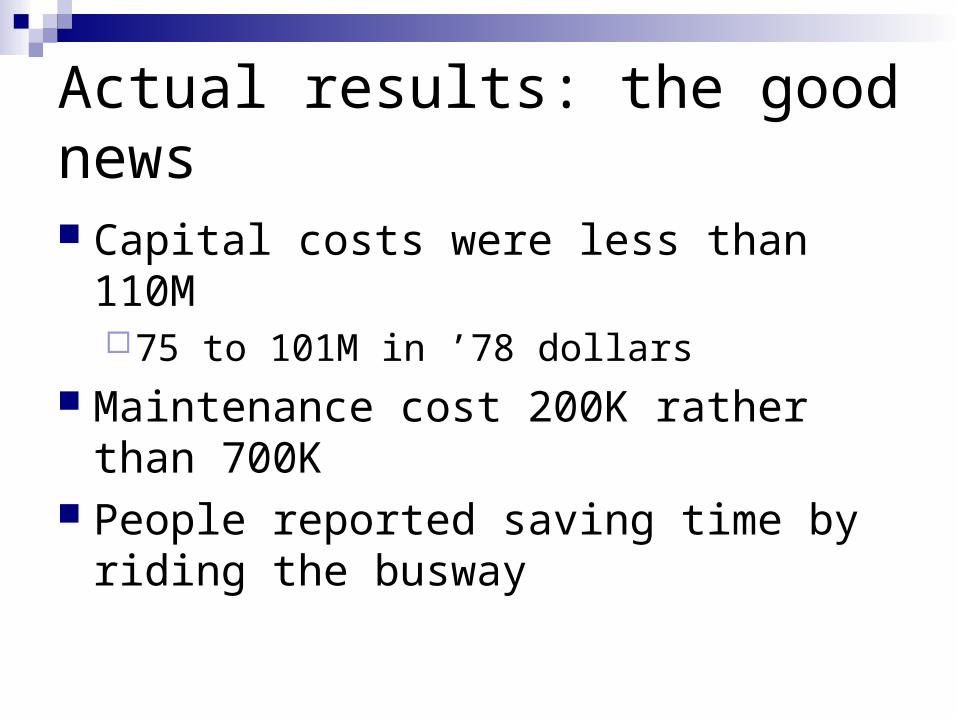

Actual results: the good news

Capital costs were less than 110M75 to 101M in ’78 dollars

Maintenance cost 200K rather than 700K People reported saving time by riding the

busway

Projections Performance

010000

20000

30000

40000

50000

60000

70000

80000

90000

100000

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

Rid

ersh

ip/

Wee

kday

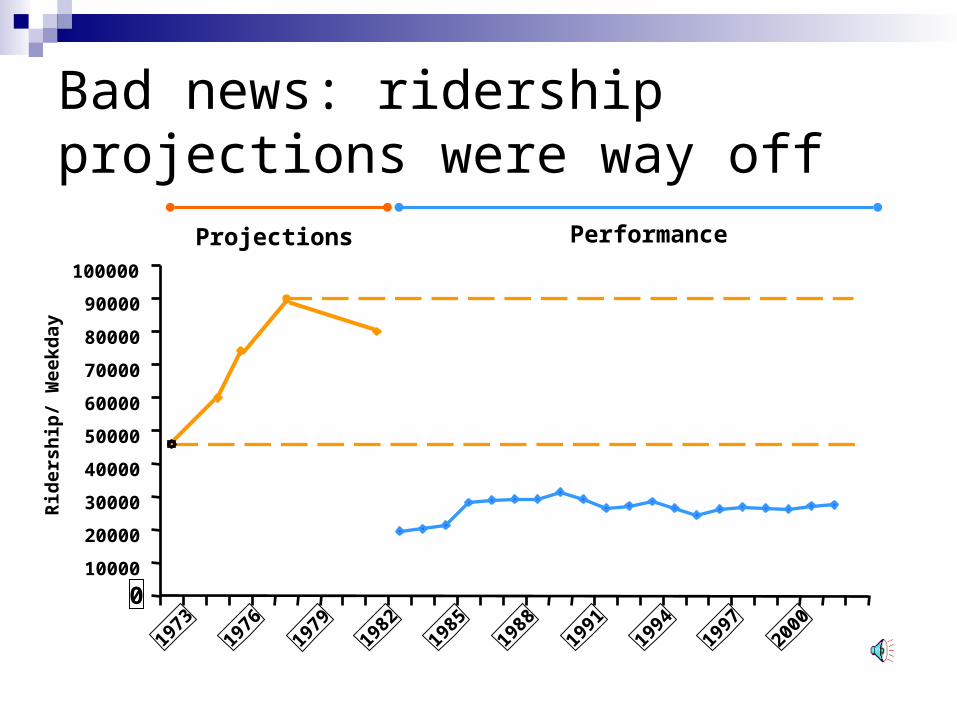

Bad news: ridership projections were way off

Thus ridership benefits were overstated by about 3.6M a year Assuming Port Authority’s assumptions

about time savings were true except for ridership, having 30,000/week rather than 54,000 per week cuts time savings in half!

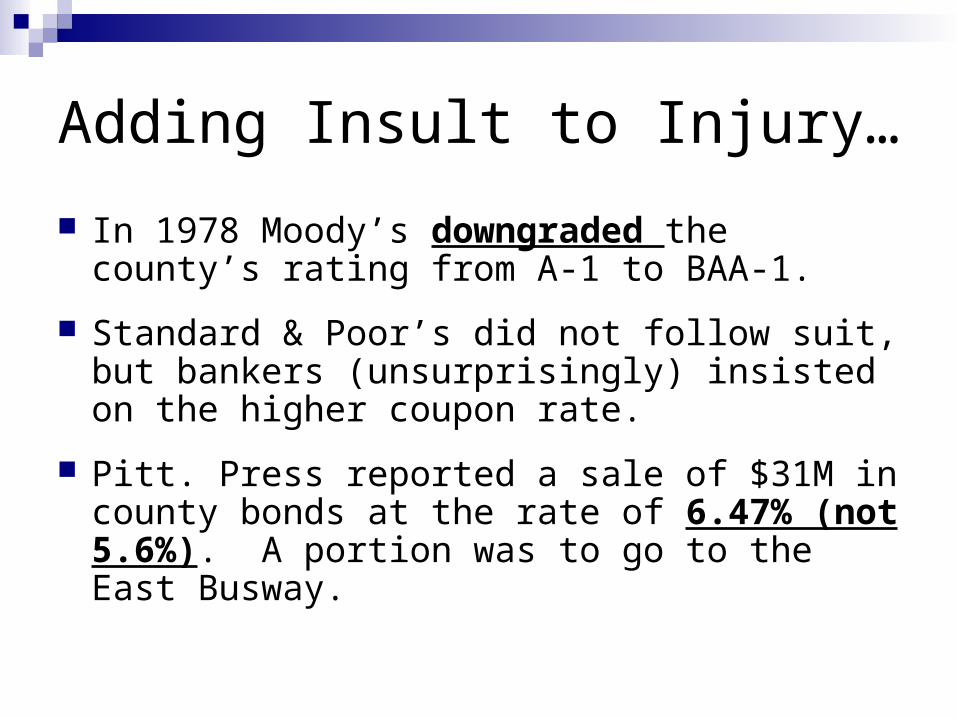

Adding Insult to Injury…

In 1978 Moody’s downgraded the county’s rating from A-1 to BAA-1.

Standard & Poor’s did not follow suit, but bankers (unsurprisingly) insisted on the higher coupon rate.

Pitt. Press reported a sale of $31M in county bonds at the rate of 6.47% (not 5.6%). A portion was to go to the East Busway.

Conclusions

Promises change when you ask for money Port Authority CBA wholly inadequate Even w/ other benefits, hard to say the

busway was worth it In ’78 inertia won again Still going however

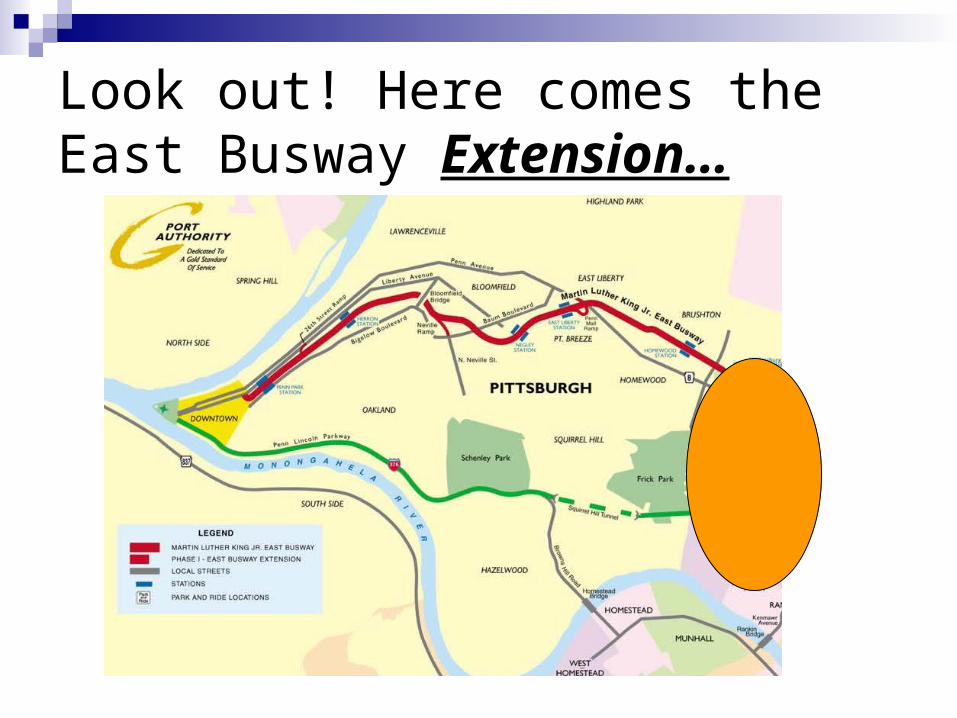

Look out! Here comes the East Busway Extension…

Look at these great benefits!

“The extension will attract new customers to the system”

13,000 riders (4,000 new) “Environmental benefits” “Decreases travel times” “Eases traffic congestion”

“Adds a decorative green space along most of the Busway corridor”

“Construction… is rehabilitating desolate and deserted areas.”

“Provides, at no cost to community residents, various neighborhood enhancements, such as the rehabilitation of the historic Edgewood Train Station…among many other improvements.”

Cost:$62M

Thank You!Thank You!

The busway did save time for those who rode it: Routes diverted to the busway routes saved 8 minutes travel time

during the morning, 3.5 minutes during the evening.

EBA Passengers (main new route) reduced travel time by 21-24 minutes.

On board survey showed that both new and diverted route passengers perceive large travel times savings since they started using the busway.

Transferring perceived to be easier, bus service deemed more reliable

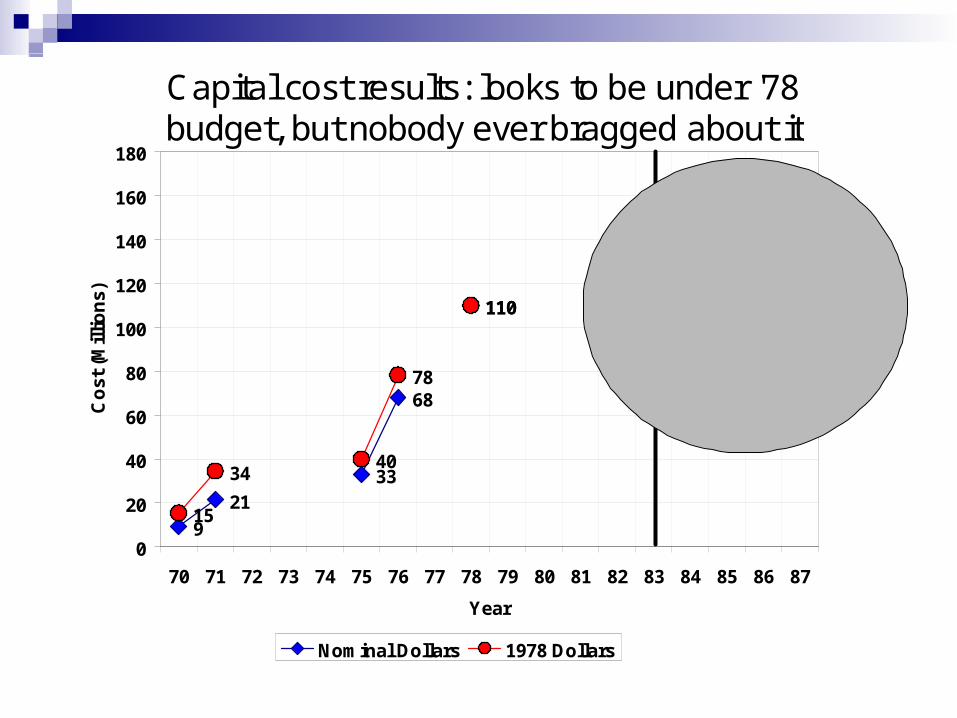

Capital cost results: looks to be under '78 budget, but nobody ever bragged about it

9

2133

68

110115

156

15

3440

78

110

75

101

0

20

40

60

80

100

120

140

160

180

70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87

Year

Co

st (

Mil

lio

ns)

Nominal Dollars 1978 Dollars