The Long-Term Squeeze on Municipal Finances Massachusetts Association of School Business Officials...

28

The Long-Term Squeeze on Municipal Finances Massachusetts Association of School Business Officials Michael J. Widmer, President Massachusetts Taxpayers Foundation February 10, 2014

-

Upload

eden-thornbrugh -

Category

Documents

-

view

214 -

download

0

Transcript of The Long-Term Squeeze on Municipal Finances Massachusetts Association of School Business Officials...

The Long-Term Squeeze on Municipal Finances

Massachusetts Association of School Business Officials

Michael J. Widmer, PresidentMassachusetts Taxpayers Foundation

February 10, 2014

Economic Context

2

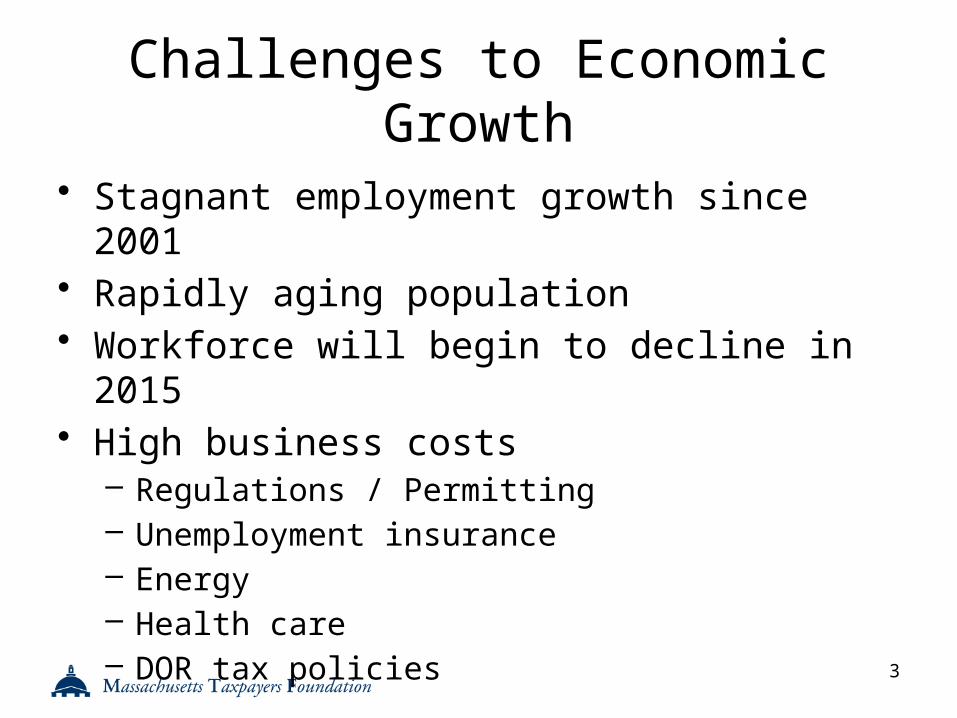

Challenges to Economic Growth

• Stagnant employment growth since 2001• Rapidly aging population• Workforce will begin to decline in 2015• High business costs

– Regulations / Permitting– Unemployment insurance– Energy– Health care– DOR tax policies

3

2001

Q1

2001

Q3

2002

Q1

2002

Q3

2003

Q1

2003

Q3

2004

Q1

2004

Q3

2005

Q1

2005

Q3

2006

Q1

2006

Q3

2007

Q1

2007

Q3

2008

Q1

2008

Q3

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q33,000

3,100

3,200

3,300

3,400

3,500

3,600

Actual US Average

In T

hou

san

ds

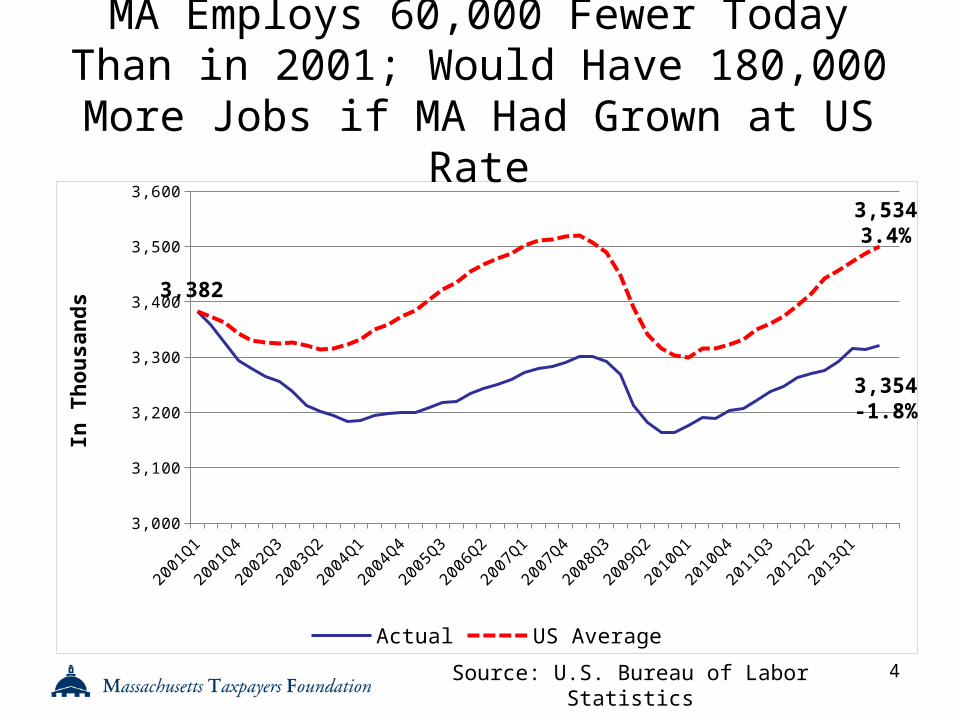

MA Employs 60,000 Fewer Today Than in 2001; Would Have 180,000 More Jobs if MA Had Grown at US

Rate

4

3,382

3,354-1.8%

Source: U.S. Bureau of Labor Statistics

3,5343.4%

180,000 More Jobs Would Have Generated $700 Million in

Additional Income Tax Revenues in FY 13

5

Avg. Income Tax / Employee

Additional Employees

Additional Income Taxes

FY 13 3,942 180,000 709,631,935

1980Q11983Q11986Q11989Q11992Q11995Q11998Q12001Q12004Q12007Q12010Q12013Q1200

250

300

350

400

450

500

550

600

650

700

Actual US Average

In T

hou

san

ds

MA Manufacturing Employment Declines 60 Percent; Difference Has

Cost MA 150,000 Jobs

6

Down 60% since 1980

Source: Moody’s Analytics, January 6, 2014

Down 37.8% since 1980

Percent of MA Population 65+ Soars Starting in 2012

7Source: Moody’s Analytics

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

2033

2036

2039

2042

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

MA U.S.

Massachusetts’ Work Age Population (15 – 64) Peaks in

2015

8

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

2033

2036

2039

2042

3,500

3,700

3,900

4,100

4,300

4,500

4,700

Th

ou

san

ds

Source: Moody’s Analytics

U.S. Work Age Population (15 – 64) Continues to Grow

9Source: Moody’s Analytics

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

2033

2036

2039

2042

120

140

160

180

200

220

240

260

Mil

lion

s

State Finances Will Continue to Challenge Lawmakers

Tight Budgets for the Foreseeable Future

• Revenue growth less than 5 percent annually over the next decade

• Growth in major obligations exceeds revenue growth– Medicaid– Debt service– Employee benefits

• Curtailed federal spending over the next 10 years through ACA and sequestration (recently postponed by the budget agreement for two years until 2016)– Medicare ~ $7.3 billion– NIH ~ $1 billion– Defense ~ $6 billion 11

State Facing Sustained Period of Slower Revenue Growth

12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Health Care and Employee Benefits Consume 85 Percent of Increased

Spending Since 2008

13

Hea

lth C

are

Empl

oyee

Ben

efits

Capita

l Sup

port

Trans

portat

ion

Hum

an S

ervice

s

Local

Gov

ernm

ent S

uppo

rt

Other

Edu

catio

n

Public

Saf

ety

Econo

mic D

evelop

men

t

Other

/Gen

eral

Gov

ernm

ent

CPI-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

The Long-Term Squeeze in Municipal Finances

Municipalities in Longest Period of Slow Growth in Prop

2 ½ Era

15

-2%

0%

2%

4%

6%

8%

10%

12% Average Annual Growth:

4.8%

Annual Municipal Revenue Growth(all sources)

Annual Revenue GrowthAverage Annual Growth FY1983 - FY2013

Fiscal Year

Property Taxes Grew at Slowest Rate Since 1985

• Property taxes account for half of all municipal revenues and increased by just 3.6 percent in 2013, from $13 billion to $13.4 billion.

16

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0% Annual Property Tax Growth, 1985 to 2013

From 1993 to 1997, state aid grew an average of 8.3% annually

In contrast, from 2009 to 2013, state aid dropped an aver-age of -0.4% annually

Average Annual Property Tax Growth, 1985 – 2012: 5.4%

Note: Proposition 2 ½ was not fully implemented until 1984, so growth for 1982 to 1984 is excluded for the graph.

Slow Recovery Is Limiting Increases in State Aid

• After years of cuts, the rebound in state aid lags that of other economic recoveries.

17

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%Annual Change in State Aid, 1985 to 2014

After 3 years of cuts, state aid rebounded with 6.5% growth in 1993

After 2 years of cuts state aid grew by 4.4% in 2005

After 3 years of cuts state aid grew by 3.0% in 2012

Municipalities Face Enormous Unfunded Retiree Liabilities

18

2012 Unfunded Liability

($ billions)

2012 Total

Liability($ billions)

Funded Ratio

Municipal Pensions $13.2 $32.0 58.5%

Municipal Retiree Health Care $30.0 $30.0 <1.0%

Total, Retiree Benefits $43.2 $62.0 30.2%

Spending on Benefits and Debt is Crowding Out Basic

Services• Municipalities find themselves in a long-term

budget squeeze because the costs for pensions, employee and retiree health care, and debt service are rising faster than revenues.

19

Growth, 2007 to 2012

Revenues, 13.1%

All Other Health Care Debt Service Pension0%

5%

10%

15%

20%

25%

30%

35%

10.1%

18.5%

23.3%

29.8%

Debt Service Costs Grew Twice as Fast as Other

Spending• Debt service costs grew by 23

percent between fiscal 2007 and 2012, totaling $2.26 billion in 2012.

• Municipalities hold more than $12.7 billion in outstanding debt—almost as much as their unfunded pension liabilities. This is principal only and does not include interest costs.

20

Municipal Workforce Is Shrinking

• Municipalities have eliminated more than 15,500 full time positions, or six percent, since 2007.

21

FYTotal Municipal

FTEs2007 265,042

2008 261,835

2009 258,971

2010 252,613

2011 250,894

2012 249,472

Change -15,570

Source: Massachusetts Division of Local Services data

Despite Billions in Contributions, Little Progress in Funding Pensions

• In 2012, the state’s 99 local pension systems had approximately $13.2 billion in unfunded liabilities, compared to $13.5 billion in 2000.

• Municipal pensions were just 58.5 percent funded in 2012, compared to 59 percent in 2000. Of the 99 systems, 97 are below 80 percent funded and 26 are less than 50 percent funded.

• The lack of progress can be attributed to several factors:– Benefit enhancements– Weak investment returns– Extending funding schedules– Minimal savings from 2011 pension reform

22

23

2011 Pension Reforms Apply Only toNew Hires; Provide Minimal Savings• Pension reforms (in present value terms) will

save municipalities only $500 million out of a total liability of $35 billion, or roughly 1.5 percent.

• Savings are small because the pension reforms apply only to new hires (beginning April 2012):– Raises the minimum retirement age from 55 to 60 and

the full retirement age from 65 to 67 for most employees.

– Lengthens the period for calculating the pension benefit from three years to five years.

– Reduces the incentive to retire early by adjusting the benefit scale so that it mirrors Social Security’s benefit neutrality.

The Retiree Health Care Challenge

• Municipalities have $30 billion in retiree health care liabilities—99 percent unfunded.– This is what cities and towns must

pay in today’s dollars for the lifetime health care benefits already earned by current employees and retirees.

24

The Retiree Health Care Challenge

• Rather than paying down liabilities as they are doing with pensions, municipalities have opted to pay-as-you-go.

• Cities and towns spent an estimated $800 million on retiree health care benefits in fiscal 2012, almost equal to unrestricted (general government) aid.

• Without change, spending is expected to grow to $1.5 billion in 10 years.

25

Huge Increase in Property Taxes Required to Fund Retiree Health

Care(single family homes)

26

Municipality

ARC Shortfall($1,000s)

Total Residential

Share of ARC

Shortfall($1,000s)

Single Family Property Share

of Shortfall($1,000s)

Tax Bill Increase

Per Single Family

PropertyAverage Tax Bill

Tax Bill Increase

Brockton $36,983 $24,179 $17,332 $1,057 $2,954 36%Fitchburg 8,243 6,186 3,812 591 2,820 21%Haverhill 4,947 3,691 2,279 223 3,648 6%Holyoke 13,015 6,558 4,208 793 2,915 27%Lawrence 25,011 14,875 5,155 1,209 2,397 50%Lowell 23,261 16,106 8,407 714 3,205 22%New Bedford 21,352 14,468 7,805 633 2,762 23%Pittsfield 7,975 5,162 3,961 351 2,795 13%Springfield 18,551 11,197 7,655 294 2,638 11%Worcester 32,362 20,229 12,167 490 3,307 15%Total $191,699 $122,649 $72,781 $565 N/A N/A

Huge Increase in Property Taxes Required to Fund Retiree Health

Care(businesses, thousands of dollars)

Municipality

ARC Shortfall

(A)

Business Share of Shortfall

(B)

Total Business Property Tax Levy, FY 2011

(C)

Percent Increase in

Business Tax Levy (D)

Brockton $36,983 $12,804 $35,776 36%

Fitchburg 8,243 2,057 9,811 21%

Haverhill 4,947 1,256 20,546 6%

Holyoke 13,015 6,458 23,728 27%

Lawrence 25,011 10,136 20,101 50%

Lowell 23,261 7,154 32,132 22%

New Bedford 21,352 6,884 30,036 23%

Pittsfield 7,975 2,813 22,479 13%

Springfield 18,551 7,354 66,000 11%

Worcester 32,362 12,133 81,832 15%

Total $191,699 $69,050 $342,440 20%27

The Need for Urgent Action

• The longer that retiree health care obligations go unaddressed, the more severe the consequences for retirees.

• As with municipal health reform, even with changes in eligibility and benefits, retirees would still receive a very generous benefit.

28