The Litigation Risk Transfer Market..The Lord Justice Jackson effect James Delaney .

12

The Litigation Risk Transfer Market ..The Lord Justice Jackson effect James Delaney www.thejudge.co.uk

-

Upload

christina-edwards -

Category

Documents

-

view

216 -

download

1

Transcript of The Litigation Risk Transfer Market..The Lord Justice Jackson effect James Delaney .

The Litigation Risk Transfer Market

..The Lord Justice Jackson effect

James Delaney

www.thejudge.co.uk

BTE Legal Expenses Insurance• Pre-paid (traditional) insurance to cover legal expenses in the event

that a dispute occurs (i.e. not applicable for existing disputes).

• Sold as an add-on to household/motor

• Jackson recommends greater take-up – Is it realistic?

• Limited cover/indemnity e.g. pi, clinical negligence, employment

• Commercial BTE - take up is nominal.

• Access to Justice – Different mindset of BTE v ATE underwriters.

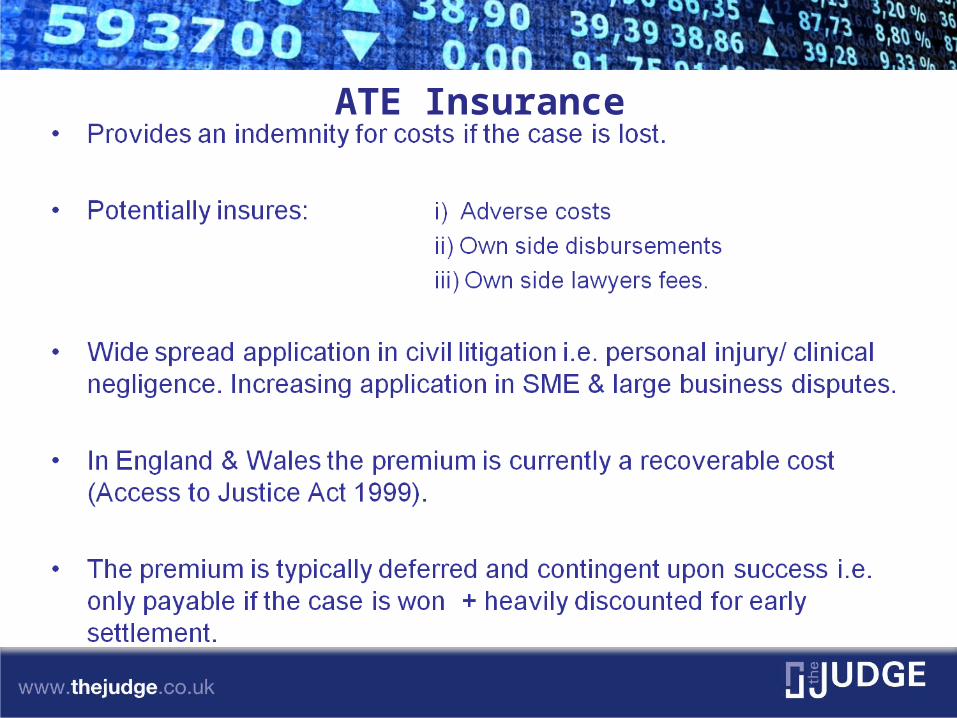

ATE Insurance

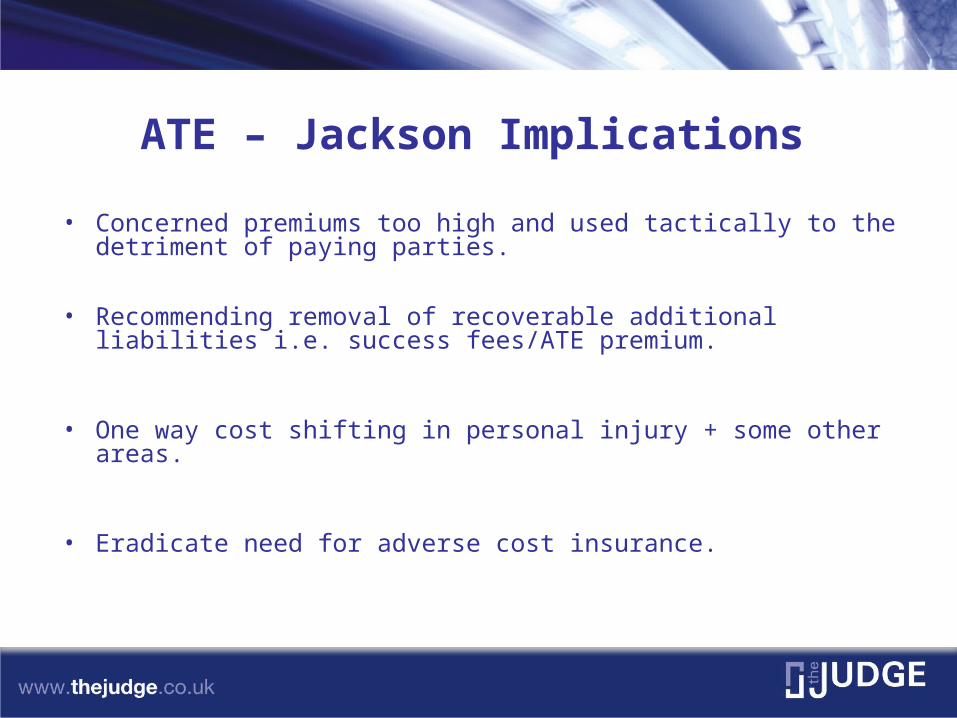

ATE – Jackson Implications

• Concerned premiums too high and used tactically to the detriment of paying parties.

• Recommending removal of recoverable additional liabilities i.e. success fees/ATE premium.

• One way cost shifting in personal injury + some other areas.

• Eradicate need for adverse cost insurance.

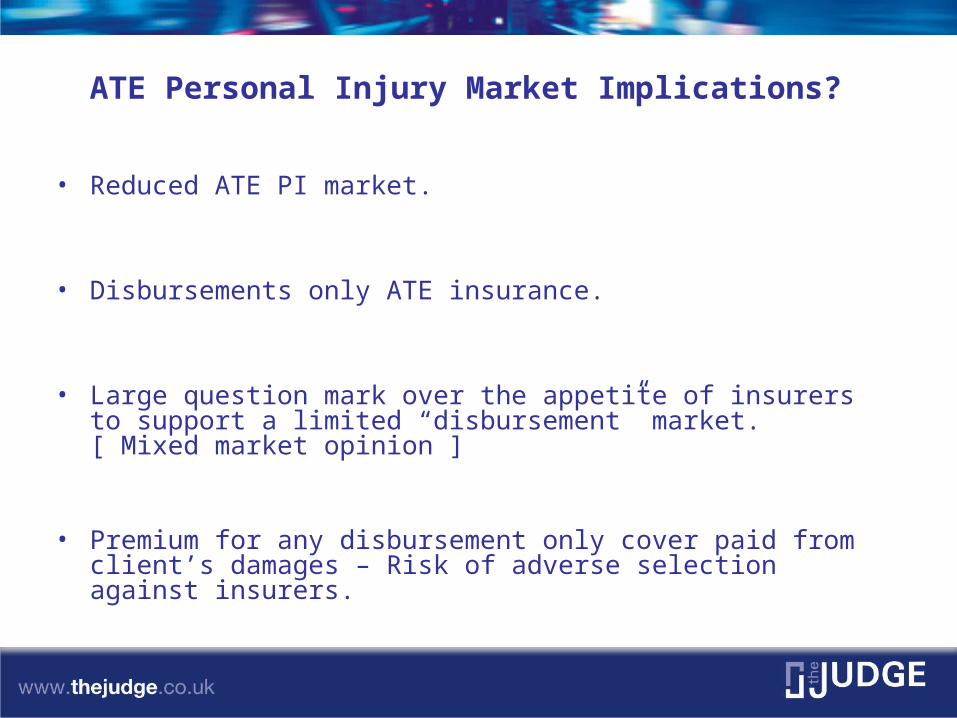

ATE Personal Injury Market Implications?

• Reduced ATE PI market.

• Disbursements only ATE insurance.

• Large question mark over the appetite of insurers to support a limited “disbursement” market. [ Mixed market opinion ]

• Premium for any disbursement only cover paid from client’s damages – Risk of adverse selection against insurers.

Commercial/Non PI ATE Insurance

• Eradicating recoverability of premiums will prohibit clients’ ability to insure and thereby pursue their cases - Why?

• Small business disputes – Proportionality Issues

• The Asia experience - Cost v Damages Ratio (good cases uninsurable)

• Cases with non monetary remedies won’t be insurable e.g. IP infringement proceedings etc…

• David v Goliath - Goliath can force a settlement at undervalue

Jackson ATE Impact Big Ticket Cases

• Concerned that big business can utilise a system intended for impecunious clients. Is the concern misguided?

• Greater propensity for global settlements inclusive of costs.

• Keeping recoverability for some but not others requires - means testing but how?

Would commercial ATE survive without premium recoverability?

• Yes but with a more restrictive qualifying pool of insurable cases + increased adverse selection risk.

Third Party Funding What is it?

– Professional Funder with no prior interest in case– Provides cash flow for legal costs– Share of proceeds

Cost to the client – 20-40% of damages?– 200-400% min return on investment?

– Typically works best in large disputes with a large damages v cost ratio.

Third Party Funding – Jackson Implications

• Generally a thumbs up endorsement by Lord Justice Jackson.

• Removal of Arkin cap could prohibit funders.

• Funders are unlikely to be interested in bridging any gap for small business disputes left by eradication of recoverability.

• Funders in UK need buoyant ATE market to mitigate their adverse cost exposure.

• Restricting ATE market growth could inhibit the growth of the funding market.

Litigation Buyout Insurance (AKA Outcome Hedging / Stop Loss Policy)

What is it?• Defendant client facing actual or possible litigation• Policy providing hedge on risk by capping potential liability at

a certain level• Insured’s retained element of risk (retention/excess)

Jackson implications? None.

The Future of the Market? • Hedging legal costs is here to stay both in the UK and

internationally.

• Individuals, SMEs and large blue chip clients – Continual education/promotion of “hedging risk” by lawyers/funders/insurers

• Huge international growth ahead with litigation insurance being applied in Asia, Australia, Canada, Europe and US.

• Insuring attorney fees in the States provides an economic alternative to contingency fees.

• Continued growth of litigation funding – albeit restrictive market in comparison to the size of the litigation insurance market.