The Latest M&A Outlook & Business Value Drivers · Type of Business Industry Segment Service...

72

The Latest M&A Outlook & Business Value Drivers Anthony M. Giordano BKD Corporate Finance [email protected] Daniel A. Boarder BKD, LLP [email protected]

Transcript of The Latest M&A Outlook & Business Value Drivers · Type of Business Industry Segment Service...

The Latest M&A Outlook & Business Value Drivers

Anthony M. Giordano

BKD Corporate Finance

Daniel A. Boarder

BKD, LLP

• Participate in entire webinar • Answer polls when they are provided

• If you are viewing this webinar in a group o Complete group attendance form with

Title & date of live webinar Your company name Your printed name, signature & email address

o All group attendance sheets must be submitted to [email protected] within 24 hours of live webinar

o Answer polls when they are provided

• If all eligibility requirements are met, each participant will be emailed their CPE certificates within 15 business days of live webinar

To Receive CPE Credit

The Latest M&A Outlook & Business Value Drivers

Anthony M. Giordano

BKD Corporate Finance

Daniel A. Boarder

BKD, LLP

• Subsidiary of BKD, LLP

• 17-year history

• Member of FINRA & SIPC

• Professional team includes

o Investment bankers

o Financial analysts

o Market analysts

BKD Corporate Finance Profile

BKD, LLP–Breadth & Depth of Resources

• 30 offices in 12 states

• Approximately 250 partners

• More than 2,000 employees

• Six industry niche groups

o Health Care, Financial Services, Construction & Real Estate, Manufacturing & Distribution, Not-for-Profit, and Energy

• Clients in all 50 states & internationally

• End-to-end client service proposition

Services

• Joined BKDCF in 2007

• More than 25 years of financial advisory services experience

• Managed investment & commercial banking transactions totaling over $1 billion

• Experience in many industries, including M&D, food & beverage, technology, telecom, media, retail, hospitality, construction, real estate, health care & insurance

Tony Giordano Biography

• More than 15 years of professional experience in variety of industries & roles

• Member of BKD’s transaction services team

• Provides essential consulting service by assisting private equity firms & corporate buyers in evaluating potential acquisition targets

• Provides consulting services to sellers looking to improve value through the due diligence process

• In charge of over 100 engagements with transaction values ranging from $7 million to over $750 million

• Consulting experience includes providing evaluations of post-transaction matters such as purchase accounting, working capital analysis & related negotiations to variety of industries

Daniel Boarder Biography

Completed Engagements Since May 2009

• 33 client engagements closed since May ’09

Type of Business Industry Segment Service ProvidedEnviromental Consulting Firm Con/Eng Sell-sideQuarry & Landfill Con/Eng Sell-side

Commerical Bank FS Sell-sideTrust Company FS Sell-sideCommunity Bank FS Sell-side

Skilled Nursing & Assisted Living HC Sell-sideSkilled Nursing Facility HC Sell-sideOpen MRI Facility HC Sell-sideSkilled Nursing & Assisted Living HC Sell-sideMedical Laboratory HC Sell-sideDME Store HC Buy-sideHospital / DME Store HC ConsultingLong Term Acute Care Hospital HC ConsultingCritical Access Hospital HC ConsultingLong Term Acute Care Hospital HC FinancingMedical Supplies Distributor HC Financing/Consulting

Explosives Components M&D Sell-sideChemical Distribution M&D Sell-sideBankruptcy Software Developer M&D Sell-sideIndustrial Equipment & Supplies M&D Sell-sideMachine Tool Manufacturer M&D Sell-sideMfg. of School Supplies M&D Buy-sideWireless Electronics Company M&D ConsultingHealthcare Supply Chain Management M&D ConsultingMfg. of Pressure Vessels M&D ConsultingMfg of Welded Stainless Steel Tubing M&D ConsultingMfg of Water Control Values M&D ConsultingMfg. of Light Metal Products M&D ConsultingProduct Marking Company M&D FinancingSteel Service Center M&D FinancingFull Service Steel Products Manufacturer M&D Financing

Presort Mail Service Other Sell-sideSEO / Internet Marketing Other Consulting

CURRENT M&A & CAPITAL MARKET CONDITIONS

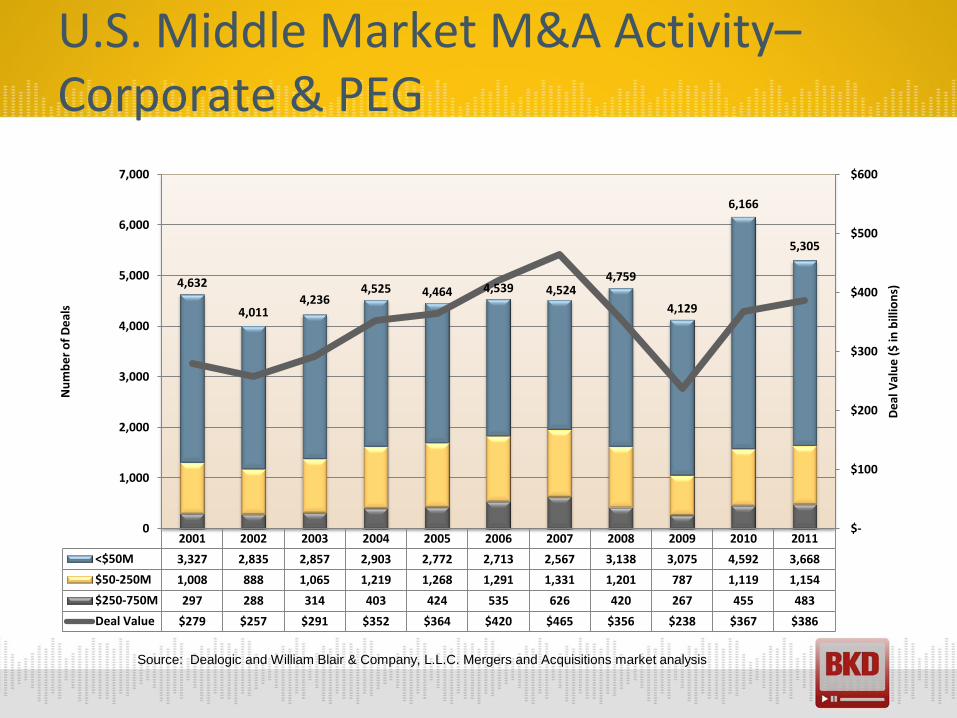

U.S. Middle Market M&A Activity– Corporate & PEG

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

<$50M 3,327 2,835 2,857 2,903 2,772 2,713 2,567 3,138 3,075 4,592 3,668

$50-250M 1,008 888 1,065 1,219 1,268 1,291 1,331 1,201 787 1,119 1,154

$250-750M 297 288 314 403 424 535 626 420 267 455 483

Deal Value $279 $257 $291 $352 $364 $420 $465 $356 $238 $367 $386

4,632

4,011 4,236

4,525 4,464 4,539 4,524 4,759

4,129

6,166

5,305

$-

$100

$200

$300

$400

$500

$600

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

De

al V

alu

e (

$ in

bill

ion

s)

Nu

mb

er

of

De

als

Source: Dealogic and William Blair & Company, L.L.C. Mergers and Acquisitions market analysis

M&A Deal Volume

Total middle market deal value for 2011 was approximately $386B

Number of Deals Deal Value

2009 2010 2011 % Chg. '11

vs. '10 2009 2010 2011 % Chg. '11

vs. '10

< $50M 3,075 4,592 3,668 -20% $ 38,357 $ 45,922 $ 44,830 -2.4%

$50M-$250M

787 1,119 1,154 3% $ 89,582 $ 128,704 $ 135,499 5.3%

$250M-$750M

267

455

483 6% $ 109,644 $ 192,284 $ 205,436 6.8%

Total Middle Market 4,129 6,166 5,305 -14% $ 237,583 $ 366,910 $ 385,765 5.1%

> $750M

156

285

269 -6% $ 647,486 $ 674,147 $ 818,823 21.5%

Undisclosed 5,024 6,108 7,561 24% - - - -

Total Deals 9,309 12,559 13,135 5% $ 885,069 $ 1,041,056 $ 1,204,588 15.7%

Source: Dealogic and William Blair & Company, L.L.C. Mergers and Acquisitions market analysis

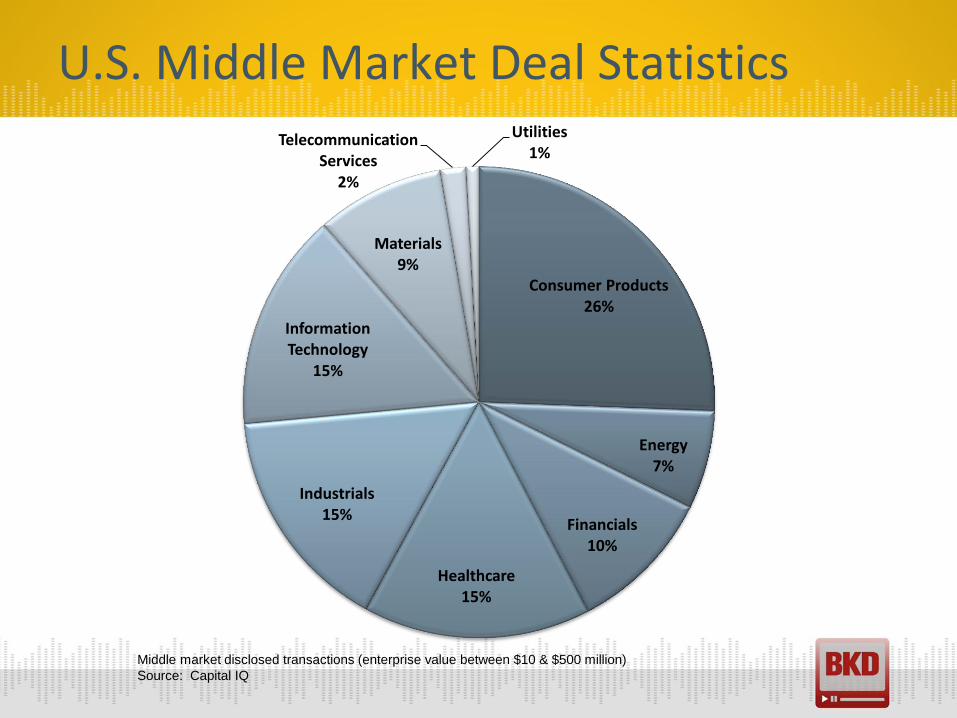

Consumer Products 26%

Energy 7%

Financials 10%

Healthcare 15%

Industrials 15%

Information Technology

15%

Materials 9%

Telecommunication Services

2%

Utilities 1%

U.S. Middle Market Deal Statistics

Middle market disclosed transactions (enterprise value between $10 & $500 million)

Source: Capital IQ

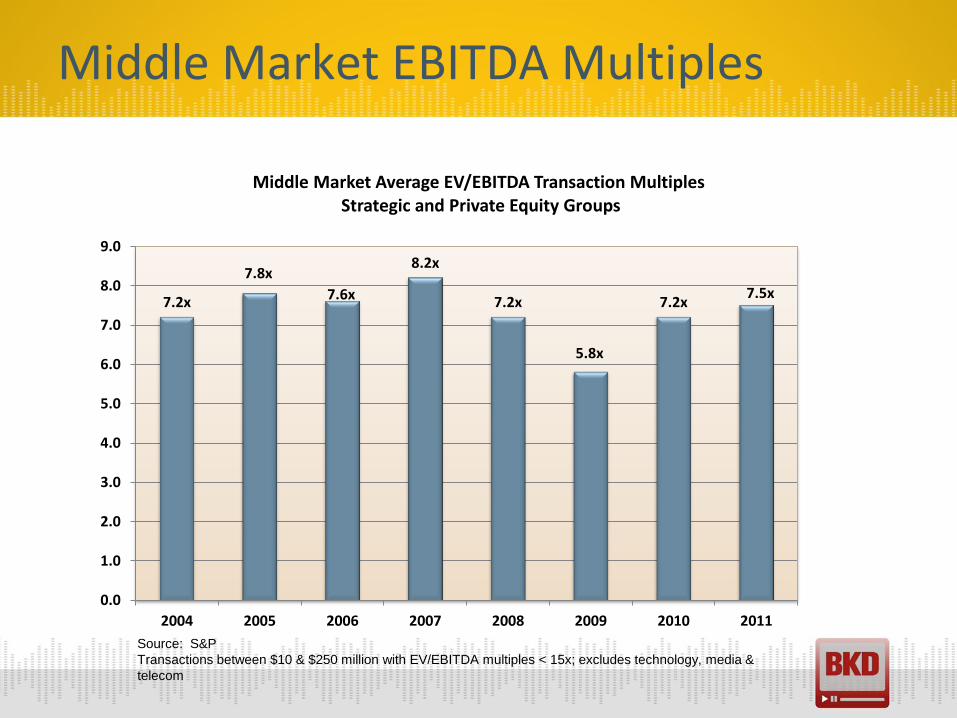

Middle Market EBITDA Multiples

7.2x

7.8x

7.6x

8.2x

7.2x

5.8x

7.2x 7.5x

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2004 2005 2006 2007 2008 2009 2010 2011

Middle Market Average EV/EBITDA Transaction Multiples Strategic and Private Equity Groups

Source: S&P

Transactions between $10 & $250 million with EV/EBITDA multiples < 15x; excludes technology, media &

telecom

Private Equity EBITDA Multiples

Source: GF Data Resources

5.9x

6.0x 6.0x

6.2x 6.2x

6.0x

5.9x 5.9x

6.1x

5.0

5.5

6.0

6.5

2003 2004 2005 2006 2007 2008 2009 2010 2011

U.S. PEG Middle Market Deal Statistics

GF Data Resources is subscription database that tracks deal activity for

approximately 185 middle market private equity firms

U.S. PEG Middle Market Deal Statistics

Source: GF Data Resources

5.4x 5.5x 4.7x

5.5x 5.5x

6.3x 6.0x 6.3x 6.4x 6.1x

6.8x

6.5x 6.5x 6.7x

7.4x 7.4x

5.6x

8.8x

5.2x

8.2x

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011

U.S. PEG Middle Market Deal Statistics

$10 - $25 MM $25 - $50 MM $50 - $100 MM $100 - $250 MM

GF Data Market Update–TEV/EBITDA

INDUSTRY 2003-06 2007 2008 2009 2010 2011 Total N =

Manufacturing 5.8 6.2 5.9 5.8 5.9 6.0 5.9 575

Business Services 6.1 6.3 6.2 5.9 5.9 6.6 6.1 234

Health Care Services 6.7 6.6 6.8 6.3 6.6 7.3 6.7 125

Retail 6.5 6.6 6.4 5.2 6.1 6.7 6.5 44

Distribution 5.8 6.0 6.3 5.5 5.3 6.0 5.9 135

Publishing/Media 7.4 7.7 6.1 7.4 4.2 6.1 7.2 31

Technology 5.6 5.2 6.5 6.6 5.7 4.6 5.9 25

Other 5.9 5.7 5.4 6.4 5.6 5.0 5.7 163

N = 553 218 160 87 169 145 1332

Source: GF Data Resources

M&D Market Update

• GDP grew at 3% annual rate in Q4 of 2011, fastest growth since Q2 of 2010

• According to Manufacturing ISM Report On Business:

o Economic activity in manufacturing sector expanded in January for 30th consecutive month

o Overall economy grew for 32nd consecutive month

o New Orders Index increased in January, reflecting 33rd consecutive month of growth in new orders

Historical Manufacturing Valuations

TOTAL ENTERPRISE VALUE (TEV)/EBITDA—Manufacturing

TEV 2003-06 2007 2008 2009 2010 2011 Total N =

10-25 5.3 5.7 5.4 5.7 5.4 5.5 5.5 231

25-50 6.1 6.1 5.6 5.8 5.9 5.1 5.9 182

50-100 6.3 6.5 6.6 5.2 6.5 6.8 6.4 122

100-250 N/A N/A 6.6 7.4 6.0 8.7 7.2 40

Total 5.8 6.2 5.9 5.8 5.9 6 5.9

N = 263 89 73 30 61 59 575

Source: GF Data Resources

* Based on Private Equity transactions

TOTAL ENTERPRISE VALUE (TEV)/EBITDA—DISTRIBUTION

TEV 2003-06 2007 2008 2009 2010 2011 Total N =

10-25 5.5 5.6 5.4 5.3 4.9 5.0 5.3 49

25-50 5.9 6.2 6.9 5.8 5.1 6.1 6.1 51

50-100 5.8 6.5 5.9 N/A 6.4 6.2 6.0 26

100-250 7.1 6.3 N/A N/A 6.8 8.7 7.3 9

Total 5.8 6 6.3 5.5 5.3 6 5.9

N = 58 21 13 4 19 19 135

Historical Distribution Valuations

Source: GF Data Resources

* Based on Private Equity transactions

CAPITAL MARKETS

Financing Sources & Transaction Structures

• Cash on balance sheets of nonfinancial S&P 500 companies ($1.1 trillion)

• Private equity capital

• Debt financing (senior & subordinated)

• Alternative funding sources

o BDCs, SBICs, hedge funds, etc.

• Other financing structures

o Earn-outs

o Seller notes

o Royalties

Private Equity Group Fundraising

$137,973

$215,854

$307,188 $311,122

$142,401

$88,763 $102,928

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

2005 2006 2007 2008 2009 2010 2011

$ in

mill

ion

s

Source: Pitchbook, 2012 Report

PE Investors Sitting on $425B of Dry Powder

$24.22

$77.64

$114.98

$67.80 $63.46

$76.11

$0

$100

$200

$300

$400

$500

$600

$0

$20

$40

$60

$80

$100

$120

$140

2006 2007 2008 2009 2010 2011

$ in

bill

ion

s

Cumulative Overhang Under $100M $100M-$250M $250M-$500M $500M-$1B $1B-$5B $5B+

$425 Billion

Source: Pitchbook, 2012 Report

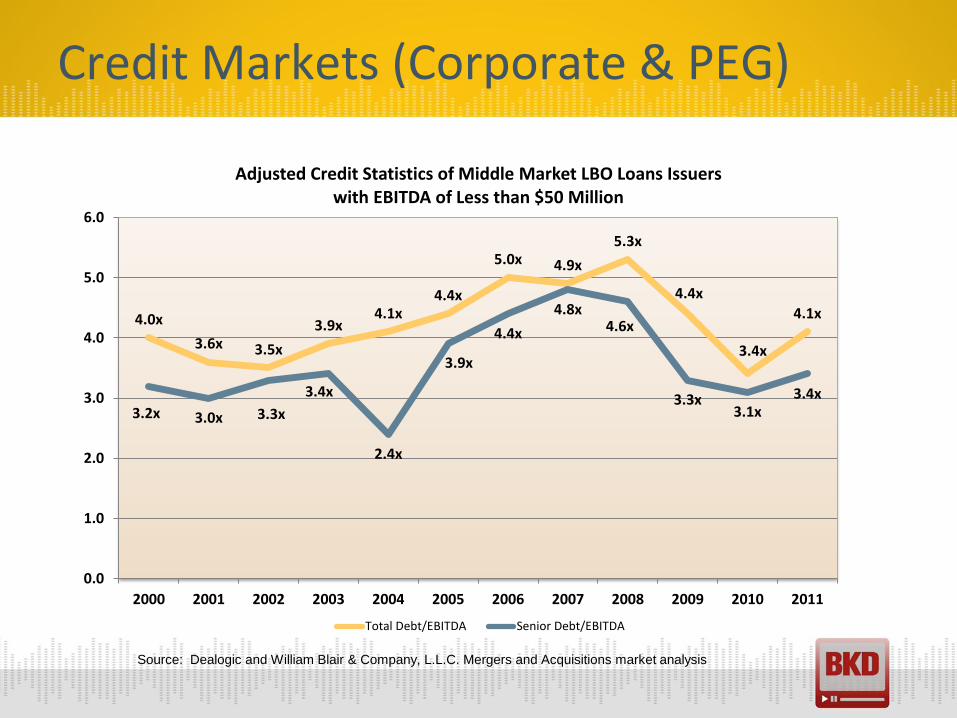

Credit Markets (Corporate & PEG)

4.0x

3.6x 3.5x

3.9x 4.1x

4.4x

5.0x 4.9x

5.3x

4.4x

3.4x

4.1x

3.2x 3.0x 3.3x

3.4x

2.4x

3.9x

4.4x

4.8x 4.6x

3.3x 3.1x

3.4x

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Adjusted Credit Statistics of Middle Market LBO Loans Issuers with EBITDA of Less than $50 Million

Total Debt/EBITDA Senior Debt/EBITDA

Source: Dealogic and William Blair & Company, L.L.C. Mergers and Acquisitions market analysis

Source: GF Data Resources

0.9x 1.0x 1.0x 0.7x

0.9x

2.8x 2.3x

1.8x 2.2x

2.4x

3.7x

3.3x

2.8x 2.9x

3.3x

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2007 2008 2009 2010 2011

Historical Leverage Multiples

Sub Debt/EBITDA Sr Debt/EBITDA

Credit Markets (PEG only)

Credit Markets (PEG only)

13.6% 16.6% 17.4% 12.1% 14.5%

43.9% 37.5% 29.4% 36.8% 37.4%

42.1% 46.0% 53.1% 51.1% 48.2%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2007 2008 2009 2010 2011

Equity & Debt Contributions

Sub Debt Senior Debt Equity

Source: GF Data Resources

Bank Term Sheet Comparison (Oct. ‘11)

Bank 1 Bank 2 Bank 3 Bank 4

CREDIT FACILITY

REVOLVER 25,000,000$ 25,000,000$ 30,000,000$ 1,500,000$

TERM -$ -$ -$ 12,000,000$

TOTAL 25,000,000$ 25,000,000$ 30,000,000$ 13,500,000$

Estimated Borrowing Base at Close 15,900,000$ 16,500,000$ 17,000,000$ 13,500,000$

INTEREST RATES Various

LIBOR LIBOR LIBOR LIBOR No

RATE PLUS (LIBOR) 2.75% 4.00% 2.75% 0.00%

Base Rate Prime Prime NA PRIME

RATE PLUS 1.50% 3.00% NA 0.00%

TERM/AMORT. (IN MONTHS)

REVOLVER 36 36 48 Annual

BORROWING BASE %

A/R 85.00% 85.00% 85.00% 80.00%

INVENTORY 65.00% Various 65.00% NA

OTHER

PREPAYMENT PENALTY (%) 3%-2%-1% 1% None 3%-2%-1%-0.5%-

CLOSING FEES -

CLOSING FEE % of Revolver Commitment 1.00% 1.50% 0.75% 1.00%

COVENANTS

MINIMUN NET WORTH UNKNOWN NO NO YES

MINIMUN DEBT SERVICE COVERAGE UNKNOWN YES YES YES

SENIOR FUNDED DEBT TO EBITDA No 3.00 No 2.75

Total FUNDED DEBT TO EBITDA No 0.00 No 3.50

DEBT SERVICE (INT & PRINC) 1.1-1.00 1.1-1.00 1.125-1.0 1.25-1.00

Manufacturing Company Term Sheet

Bank Term Sheet Comparison (July ’11)

Bank 1 Bank 2

CREDIT FACILITY

REVOLVER 3,000,000$ 3,000,000$

LETTER OF CREDIT -$ -$

ENTERPRISE VALUE TERM LOAN 1,500,000$ 1,500,000$

REAL ESTATE 200,000$ -$

EQUIP & REAL ESTATE 1,500,000$ 1,500,000$

CAP EXP - EQUIP -$ -$

TOTAL 6,200,000$ 6,000,000$

INTEREST RATES

REVOLVER - LIBOR LIBOR LIBOR

RATE PLUS (LIBOR) 0.00% 0.00%

REVOLVER - BEGIN. RATE (LIBOR) 0.00% 0.00%

Base Rate Prime Prime

RATE PLUS 0.50% 1.25%

RATE PLUS (Floor) Prime 4.50% NA

EV - Term Loan

Term-Loan - LIBOR LIBOR Prime

RATE PLUS (LIBOR) 5.50% 3.00%

FLOOR 6.50% No

FIXED RATE OPTION-TERM Yes No

Fixed Rate 7.00% 0.00%

Metal & Plastics Fabrication - Term Sheet Summary

Bank Term Sheet Comparison

Bank 1 Bank 2

TERM/AMORT. (IN MONTHS)

REVOLVER 36 36

TERM (ENTERPRISE VALUE LOAN) 48 36

BORROWING BASE %

A/R 85.00% 85.00%

INVENTORY 60.00% 60.00%

OTHER

PREPAYMENT PENALTY (%) 2%-1%-0.5% 3%-2%-1.0%

CLOSING FEES

CLOSING FEE 15,000$ 45,000

COVENANTS

MINIMUN NET WORTH TBD TBD

MINIMUM TANGIBLE CAPITAL FUNDS UNKNOWN TBD

MINIMUN DEBT SERVICE COVERAGE UNKNOWN YES

SENIOR FUNDED DEBT TO EBITDA 4.00 TBD

DEBT SERVICE (INT & PRINC) 1.25-1.00 TBD

CAPITAL EXPENDITURES LIMIT Yes Yes

Excess Cash Flow recapture No Yes

Metal & Plastics Fabrication - Term Sheet Summary

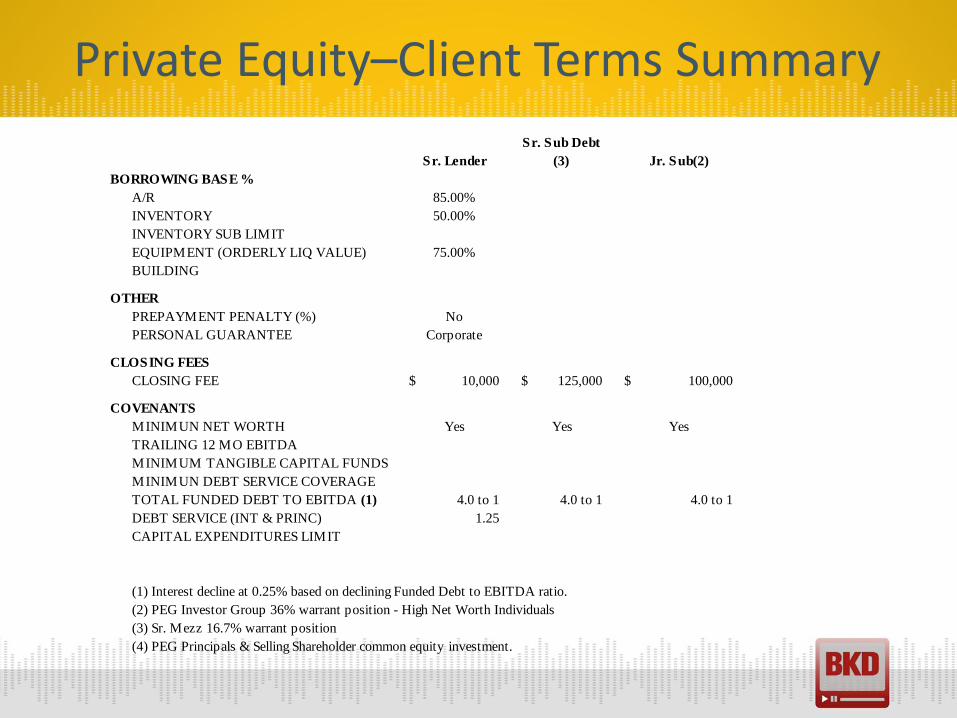

Private Equity–Client Terms Summary (Sept ‘11)

Sr. Lender

Sr. Sub Debt

(3) Jr. Sub(2) Equity (4)

CREDIT FACILITY

REVOLVER 2,000,000$

Term Loan 5,000,000$ 2,373,000$

CAP EXP - EQUIP

Common Equity 51,665$

Security Senior 2nd Lien Unsecured

TOTAL

INTEREST RATES

LIBOR OR PRIME Prime

RATE PLUS (LIBOR-PRIME)* 0.50%

REVOLVER - BEGIN. RATE 4.00%

Mezz Lenders 13.00% 10.00%

UNUSED LINE FEE (%) 0.25%

DEFAULT RATE 2.00% 5.00%

TERM/AMORT. (IN MONTHS)

MATURITY DATE

REVOLVER/Mezz 3 Year

Term Mezz 5 Year 7 Year

Sr. Lender

Sr. Sub Debt

(3) Jr. Sub(2)

BORROWING BASE %

A/R 85.00%

INVENTORY 50.00%

INVENTORY SUB LIMIT

EQUIPMENT (ORDERLY LIQ VALUE) 75.00%

BUILDING

OTHER

PREPAYMENT PENALTY (%) No

PERSONAL GUARANTEE Corporate

CLOSING FEES

CLOSING FEE 10,000$ 125,000$ 100,000$

COVENANTS

MINIMUN NET WORTH Yes Yes Yes

TRAILING 12 MO EBITDA

MINIMUM TANGIBLE CAPITAL FUNDS

MINIMUN DEBT SERVICE COVERAGE

TOTAL FUNDED DEBT TO EBITDA (1) 4.0 to 1 4.0 to 1 4.0 to 1

DEBT SERVICE (INT & PRINC) 1.25

CAPITAL EXPENDITURES LIMIT

(1) Interest decline at 0.25% based on declining Funded Debt to EBITDA ratio.

(2) PEG Investor Group 36% warrant position - High Net Worth Individuals

(3) Sr. Mezz 16.7% warrant position

(4) PEG Principals & Selling Shareholder common equity investment.

Private Equity–Client Terms Summary

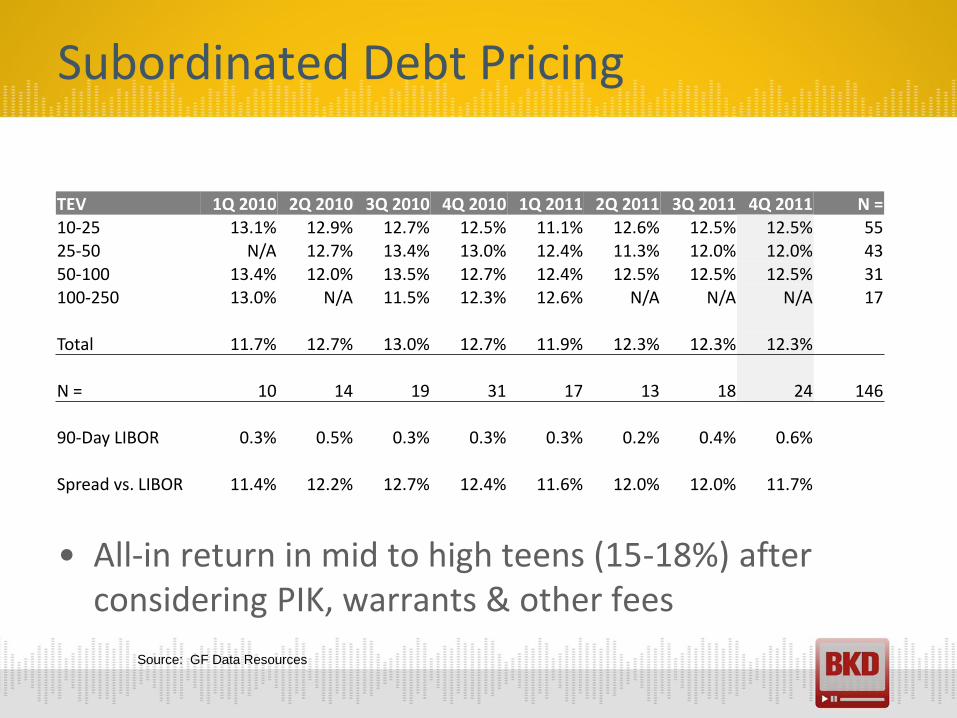

Subordinated Debt Pricing

• All-in return in mid to high teens (15-18%) after considering PIK, warrants & other fees

TEV 1Q 2010 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 N = 10-25 13.1% 12.9% 12.7% 12.5% 11.1% 12.6% 12.5% 12.5% 55 25-50 N/A 12.7% 13.4% 13.0% 12.4% 11.3% 12.0% 12.0% 43

50-100 13.4% 12.0% 13.5% 12.7% 12.4% 12.5% 12.5% 12.5% 31 100-250 13.0% N/A 11.5% 12.3% 12.6% N/A N/A N/A 17

Total 11.7% 12.7% 13.0% 12.7% 11.9% 12.3% 12.3% 12.3%

N = 10 14 19 31 17 13 18 24 146

90-Day LIBOR 0.3% 0.5% 0.3% 0.3% 0.3% 0.2% 0.4% 0.6%

Spread vs. LIBOR 11.4% 12.2% 12.7% 12.4% 11.6% 12.0% 12.0% 11.7%

Source: GF Data Resources

Summary

• Deal activity intensified in second half of 2010 & early 2011 with some slow down in second half of 2011

o Interest rates remain low & credit markets active

o Excess growth & buyout capital is available & needs to be invested

• Deals are taking longer to close–everything from due diligence to financing

o M&A: six- to nine-month process

o Financing: three- to six-month process

• Baby boomer-owned companies are coming to market in increasing numbers–estimated 8.4 million in next 10-15 years

• Improving U.S. market conditions should continue to support stronger business operating results & corporate valuations

• How will M&A & credit markets react to global economic & political uncertainty?

• Extension of Bush tax laws gave owners two year window to plan & complete sale or recap (sell minority or majority stake, dividend recap)

o Still nine months to complete transaction

• Excess investment capital will support active M&A market & attractive valuations for remainder of 2012 & into 2013

• Downside risk in forefront of buyers’ minds—attempting to alleviate downside risk through

o More meticulous due diligence

o Structuring of deals—more recaps, earn-outs, seller notes & other deferred comp.

• Credit markets could potentially tighten due to global uncertainly, impacting number of transactions & their valuations

What to Expect

TOOLS FOR BUILDING VALUE

• Identify goals of ownership, management &/or corporate board

o Retain some ownership while having continued involvement in business operations–majority sale/recap

o Sell 100% & help assist with ownership transition

o No involvement after sale

o Transition company to family members or employees

Identify Stakeholder Goals

• How seller participates will typically determine potential buyer/investor & deal structure

o Outright sale (strategic or financial)

o Sale of majority interest or recap (financial)–most likely require seller involvement post transaction

o Growth capital–minority interest (financial)–require seller involvement post transaction

o Management/employees (MBO/ESOP)

o Transfer ownership to family members

Company M&A Options

• CPA, financial planner, M&A experienced attorney, investment banker, business consultant

• Help minimize taxes, ensure coverage of legal & transaction issues

• A competitive process can lead to higher valuation, favorable deal structure & terms

• Sell on your terms, not buyer’s terms

• Net proceeds from transaction that meets your objectives

• Early planning with your advisors can cover all your bases

Team of Advisors

• Mold strong management team

• Business plan

• Financial statements

• Invest in the future

• Improve margins & profitability

• Customer concentration

• Balance sheet

• Controlled ownership

• Pre-due diligence/ sell-side diligence

• Timing

Tools for Building Value–Plans to Accelerate Value

* See appendix for additional information on the above

IMPROVING COMPANY VALUE

• Assess quality of company’s earnings

o What portion of company’s earnings are repeatable post-transaction?

o Identify potential earnings adjustments

o Gather back-up documentation to support adjustments

o Identify potential earnings issues & remedies to correct issues prior to potential buyer finding them

Identify Value Drivers

• With increase in deal activity

o Buyers are putting more of their own capital into deals

o Greater risk that small issues can turn into big problems

o Lenders are less tolerant of potential issues

• Being prepared for buy-side diligence process is best way to ensure successful transaction

Intensifying Buyer Scrutiny

• Could impact deal EBITDA

• Could impact deal multiple

• Could reduce deal fatigue by shortening buyer’s due diligence process

• Could attract more/different types of potential buyers

• Could identify tax strategies that are mutually beneficial

• Could support internal resources so they can focus on running business

Seller Benefits

• Drafting Letter of Intent

• Deal Structure–Asset vs. Stock, etc.

• Working Capital Trends

• Income Statement

o Revenue trends

o Margin trends

o Gaining new or losing customers–earnings impact?

o Vendor accessibility & availability

o Related-party transactions

Other Important Due Diligence Focus Points

• Balance sheet exposure areas

o Assets included/excluded

o Appropriateness of reserves

o Inventory requirements

o Liabilities assumed/excluded

• Tax exposure areas

o State & local taxes

o Federal tax successor liability

Other Important Due Diligence Focus Points

• Information Technology

o Does it produce reliable data?

o Is it compatible?

o Is it scalable?

• Operations

o What efficiencies can be developed?

o What synergies can be leveraged?

Other Important Due Diligence Focus Points

• Smooth out deal process

• Prepares buyer for “what’s to come” with buy-side diligence

• Reduce number of “surprises” at negotiation table

• Lower hold-backs

• Gives sense of security, credibility

Overall Benefits We Have Seen

Recent Examples

• Identified risks relating to budgeting process of target company in construction industry

• Budgets provided by management included

o Numerous clerical errors

o Aggressive bookings assumptions

o Assumptions that recent unfavorable trends would somehow “be recovered” with no supporting detail

• Takeaway–Get in front of issue & take time to complete accurate & reasonable budgets

Recent Examples

• Identified risks related to lack of reporting accuracy

• Target was very profitable & had numerous “nonrecurring” expenses

• Due diligence resulted in Adjusted EBITDA $1.5 million higher than Reported EBITDA

• Takeaway–We were able to show potential buyers issues prior to LOI stage so they did not become reasons to renegotiate deal

Recent Examples

• Identified risks related to seasonality of target company in manufacturing industry

• Target experienced high volumes during summer months & low volumes during winter months

• NWC target was based on TTM average & closing was expected during down time, resulting in reduced purchase price

• Takeaway–Utilize clear wording in purchase agreement & consider all factors that may influence purchase price

• Multidisciplinary buy-side diligence

o Financial

o Federal, state & local tax

o Information technology

o Operational

o Incentives

• Sell-side diligence preparation

• Business & tax structuring

• Working capital reviews

• Audits of beginning & ending balance sheets

BKD Transaction Services Overview

POLLING QUESTIONS

Polling Question 1

• Example? *Note: questions can only have 126 total characters in them

o Yes *Note: answers can only have 60 total characters

o No

o Unsure

54

Polling Question 2

55

• Example? *Note: questions can only have 126 total characters in them

o Yes *Note: answers can only have 60 total characters

o No

o Unsure

Polling Question 3

56

• Example? *Note: questions can only have 126 total characters in them

o Yes *Note: answers can only have 60 total characters

o No

o Unsure

Polling Question 4

57

• Example? *Note: questions can only have 126 total characters in them

o Yes *Note: answers can only have 60 total characters

o No

o Unsure

58 58

• Up to 1 CPE credit will be awarded upon verification of participant attendance; however, credits may vary depending on state guidelines

• For questions, complaints or comments regarding CPE credit, please email BKD Learning & Development department at [email protected]

CPE Credit

APPENDIX

• Success of company should depend on entire organization, not a few people

• Loss of one or two key personnel should not negatively affect company

• Need strong second-in-command & junior-level management

Mold a Strong Management Team

• Develop business plan–reasonable & attainable assumptions

• Clearly define internal & external growth opportunities

• Identify & explain operation or margin improvements (investment in technology, improved supplier terms)

• Identify capital expenditures

• Capital requirement (internal CF, outside capital)

• Hit your numbers

Business Plan

• Effective financial controls

o Audited or reviewed financial statements

o GAAP internal financial statements

o Dependable accounting department

• Gives sense of security, credibility

• Lowers due diligence costs

• Lowers holdbacks

Financial Statements

• Putting off needed expenses may not add value

• Review & address operational processes

• Ensure systems & controls are in place

• Investment in technology or equipment

• Give best appearance possible

• Also applies to investment in human capital

o Management

o Other personnel

Invest in the Future

• Eliminate unprofitable products &/or customers

• Examine expenses (excessive, personal/family related, nonrecurring expenses)

• Review & improve supplier contracts

• Sell divisions or locations if they significantly lower earnings & are not strategic

• Manage working capital

Improve Margins & Profitability

• Too much revenue with too few customers can give appearance that business may be risky

• Improve quality (profitability) & diversification of customers

• Attempt to get sales contracts or agreements

• Be prepared for holdbacks in transaction

Customer Concentration

• Clean up

o Manage working capital

o Obsolete inventory

o Loans to shareholders

• Will clarify assets & liabilities in transaction

Balance Sheet

• Different owners = different objectives

• Beneficial to buy out minority shareholders

• Can ensure smoother transaction & may increase value

Controlled Ownership

• Litigation

• Corporate records

• Contracts

• Financial records

• Allow time to fix what might impact value

Pre-Due Diligence

• If selling your company is your exit plan, timing can be single most important factor to consider

• Buy low, sell high applies to business sales as well

• Sell on your own terms

• In difficult market, deal structure & partner going forward critical

• Don’t be a Lone Ranger

Timing

Anthony Giordano | Vice President | 303.837.3562 | [email protected]

Daniel Boarder | Supervising Consultant | 816.221.6300 or 972.702.8262 |

71 71

Continuing Professional Education (CPE) Credits

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org.

The information in BKD webinars is presented by BKD professionals, but applying specific information to your

situation requires careful consideration of facts & circumstances. Consult your BKD advisor before acting

on any matters covered in these webinars.

72 72

CPE Credit

• Up to 1 CPE credit will be awarded upon verification of participant attendance; however, credits may vary depending on state guidelines

• For questions, complaints or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected]