The Kroger Co. 2014 Proxy Statement and 2013 Annual Report

152

N OTICE OF A NNUAL M EETING OF S HAREHOLDERS P ROXY S TATEMENT AND 2013 A NNUAL R EPORT

Transcript of The Kroger Co. 2014 Proxy Statement and 2013 Annual Report

N o t i c e o f A N N u A l M e e t i N g o f S h A r e h o l d e r S

P r o x y S t A t e M e N t

A N d

2 0 1 3 A N N u A l r e P o r t

Kroger

Convenience Stores

Jewelry Stores

Services

Bring it all home.

COVER PRINTED ON RECYCLED PAPER

1

F e l l o w S h a r e h o l d e r S :

Kroger achieved another outstanding year of performance for shareholders in 2013.

We are a company with many strengths, among them:

• Strongandconsistentreturnstoshareholders,

• Anaggressivestrategicplanthatdeliversreliablegrowthandfinancialperformance,and

• Deeplyloyalcustomerswhoarethebasisforourbroadandgrowingmarketshare.

Our Company’s most enduring strength is our people — our more than 375,000 associates who strive tomakeeverycustomer’sdayalittlebettereachtimetheyvisitoneofourstores.

Our foundational approach is called Customer 1st. It simply means that the needs and wants of our customersareattheheartofeverydecisionwemake—inourstores,plants,offices,andfacilities.ItisourassociateswhobringCustomer1st to life. From product and technology innovation to improvements in the shoppingexperience,weare inspiredby theever-changingneedsandwantsofcustomers.Our greatest strategic advantage is our Customer 1st culture.

Weareproudtobebothlargeandsmall.Asoneoftheworld’slargestretailers,weleverageeconomiesofscaleinwaysthatmakeadifferenceforourcustomersintheirdailylives.Forexample,weimplementedaninnovative,fastercheckoutapproachthatsavesminutesforeachcustomereverytimetheyshop.Wealsoleverageoursizetooffergreatvalueoneverydayitemsandweeklyspecials,andthenprovideapersonalizedmobile app—one of themost popular in that crowded space—that highlights the deals thatmatch eachshopper’s list.

Inthisletter,Iwillprovidemoredetailbehindouroutstandingresultsin2013andexplainthebasisofour firm conviction that there is much more to come for shareholders, associates and customers.

Fiscal 2013 Results – Delivering Growth That Investors Can Count On

At our October 2012 investor meeting, we announced aggressive growth plans that expand our Customer 1st Strategybyacceleratinggrowth inourcorebusinessand improvingourconnectionwithallcustomers,expandingourpresenceinnewandexistingmarkets,andinvestingtocreateuniquecompetitivepositioningfortodayandthefuture.Asaresult,weexpecttoachievealong-term,net-earnings-per-diluted-sharegrowthrateof8-11%andanincreasingdividendovertime.

We committed to four key performance indicators to measure our progress at that meeting as well:

• Positiveidenticalsupermarketsales;

• SlightlyexpandingFIFOoperatingmarginonarollingfourquartersbasis,excludingfuel;

• Improvingreturnoninvestedcapital;and

• Growingmarketshare.

In 2013, the first full fiscal year executing our aggressive growth plan, Kroger delivered on all four indicators. We achieved an unparalleled 41st consecutive quarter of positive identical supermarket sales;expanded FIFOoperatingmargin on a rolling four quarters and adjusted basis, excluding fuel; improvedreturnoninvestedcapital,evenasweincreasedcapital investments;andgrewmarketsharefortheninthconsecutive year.

Kroger’s consistent and reliable performancedeliverslong-termgrowth investors can count on. And2013wasanotheryearofsteadygrowth.Totalsaleswere$98.4billioninfiscal2013,anincreaseof3.9%afteradjustingforthe53rdweekinfiscal2012.Netearningswere$1.52billion,or$2.90perdilutedshare.Onanadjustedbasis,netearningsgrew13percentoverlastyear’sadjustedamount.WecontinuetolowerKroger’scostsofdoingbusiness–achievingourninthconsecutiveyearofreducingoperatingexpensesasarateofsales–andtoreinvestthesesavingsinlowerpricesforourcustomers.

2

We are using free cash flow to reward shareholders. Since January 2000,Kroger has returnednearly$10billiontoshareholdersthroughsharerepurchases.Since2006,Krogerhaspaidnearly$1.9billionindividendstoshareholders,whilemaintainingourinvestment-gradecreditrating.In2013,weincreasedourannual dividend for the seventh consecutive year and returned more than $928 million to shareholders through dividendsandstockbuybacks.Ifyouhadinvested$100inKrogerstockonJanuary31,2000,andreinvestedalldividendsissued,yourinvestmentwouldhavebeenworth$235onJanuary31,2014,andKroger’sTotalShareholderReturninthatsameperiodis125.8%.InMarch2014,Kroger’sBoardofDirectorsapproveda$1billionsharerepurchaseprogram,underscoringourcommitmenttodelivercashtoshareholders.

Welcoming Harris Teeter to the Kroger family

Oneofourplatformsforgrowthisexpandingintonewmarkets.Weareproudandexcitedtowarmly welcome Harris Teeter to the Kroger family of stores.WecompletedourmergerinJanuary2014andintegrationiswellunderway.Thisexceptional54-year-oldregionalchainreceivesveryhighmarksfromtheircustomersforservice,selection,meal-timesolutions,andfreshness.The230HarrisTeeterstoresarelocatedinthehighlyattractivemid-AtlanticmarketsandexpandKroger’snationalfootprint.WehavelongrespectedtheHarrisTeetermanagementteamandtheiroperations,andwelookforwardtobringingthebestofHarrisTeeter and Kroger to our customers and shareholders.

Deeply loyal customers, creating strong market share

We have the privilege of serving eight million customers each day.Everyoneofthemhasuniqueinterestsandcomestoourstoreswiththebeliefwewillbothmeettheirneeds–theirtastes,budget,andlifestyle–and delight them with the unexpected.

Wecontinuetocreateinnovativewaysthatallowustoknowourcustomersbetterthananyoneelseandtopersonalizetheirexperiencewithus.We’vebeenmining“bigdata”foralongtime,alwayswiththesinglefocus on Customer 1st–bringingtoeachcustomerwhatismostrelevanttothem.

Wehaveinvestedinpriceeveryyearfortenconsecutiveyears,savingourcustomersmorethan$3billionannually in the process.

We have rewarded customers with fuel savings through our popular fuel rewards program at more than 1,240convenient supermarket fuel center locations in 2013.And, customerswith aKrogerRewardsVisacredit card earned more than $33 million in free groceries last year.

We have partneredwith customers to support the community organizations they care aboutmost,returning$46millionannuallytolocalorganizationsthatcustomersselectthroughourCommunityRewardsprogram.

Ourapproachhasresultedingrowingbothmarketshareandshareofloyalty.

And we are not done!

Customer 1st innovation is giving us new and varied ways of connecting with and deepening our relationship with our customers. We are growing our digital offering to deliver value to our customers through the communication channels they prefer, and customers are responding. In fact, our customers have downloadedmorethan1billiondigitalcouponssincewebeganofferingtheminlate2009.

WeareinnovatingupanddownoursupplychainsothatKrogermilkstaysfresher,longerincustomers’refrigerators.Throughprocessimprovements,ourdairysuppliers,milkplants,logisticsoperation,andstoresworkedtogethersothatwecanpromiseourcustomersthatKroger’s milk is among the freshest in the industry.

Andwecontinuetobuildourbest-in-class Corporate Brands portfoliobyprovidingchoicestoourcustomersthroughamulti-tierofferingofpricepointsandproductexperiences.WeexpectSimple Truth and Simple Truth Organictojoinourpremiumtier,Private Selection,asa“BillionDollarBrand”bytheendoffiscal2014asthosebrandsareincreasinglysoughtbyshoppersfocusedonnaturalandorganicfoods.OurBanner Brand continuestoprovidegreatqualitywithawidebreadthofproducts,andourValuebrandofferscustomersthechoiceofqualityproductsthatarepricedtofittheirbudget.

3

The Kroger Difference

Kroger’scultureanddeeply-rootedvaluesarealsoreflectedinhowweserveourfriendsandneighborsinlocalcommunities,andhowwetakecareofeachother.

Westrivetobeconnectedtoandresponsivetothelocalcommunitiesweserveby:

• Deliveringtheequivalentofmore than 200 million meals to more than 100 local Feeding America foodbanksin2013.

• Engagingvendorsandcustomerstodonatemore than $6 million in 2013 in support of women’s health and breast cancer awareness programs.

• Contributing$3.3 million to the USO in2013tohelpsupportthemilitaryandtheirfamilies.Since2010,Krogerhasdonated$8.5milliontotheUSO–thelargest cumulative gift to the USO in that organization’s history.

•Hiring more than 22,456 veterans since 2009,andhelpingthe“100,000JobsMission”–acoalitionof more than 130 companies with the common goal of hiring more than 100,000 transitioning service membersandmilitaryveteransby2020–surpassitsoriginalgoalinJanuary,sevenyearsearly.

• Supportingmore than30,000 schools and local organizationswith $46million in 2013 throughour Community Rewards program that delivers personalized, customer-driven donations based ontotal purchases.

• Contributinganadditional$9.1milliontolocalorganizationsin2013throughTheKrogerCo.Foundation.In the past five years, our foundation has donated nearly $40 million.

Let’srememberthatwemaketheseinvestmentsbecauseourcustomerstellusthesecausesareimportanttothem,andbecausetheystrengthenthecommunitieswecallhome.Whenyoucombinethecash,foodandproduct we donate to a variety of causes and programs, Kroger contributed more than $250 million to our local communities in 2013.

We also make a difference in the lives of our associates, customers and communities through ourcommitmentstosafety,sustainability,supplierdiversityandjobgrowth.

Kroger is one of the safest companies in our industry. Associate engagement in innovative safety programshasreducedaccidentrates inourstoresandmanufacturingplantsby77percentsince1995. In2013,831retail locations, threemanufacturingplants,and threedistributioncenterswent theentireyearwithoutarecordableaccident.

One of Kroger’s key sustainability priorities is moving our retail stores and facilities toward “zerowaste”.Ourstoresaresendinglesswastetolandfillsandincineratorsthroughavarietyofefforts,includingcomposting and our innovative Perishable Donations Program – aprocess to rescue safe, edible freshproductsanddonatethemquicklytolocalfoodbanks.ThissystemhasbeenreplicatedbyotherretailersandtodayfreshproductsmakeupmorethanhalfofthefooddistributednationwidebyFeedingAmerica.Ourmanufacturing facilities continue to lead waste reduction. Today, 26 of our 38 manufacturing plants are designated as “zero waste” facilities.

You can learn more about our sustainability initiatives by reading our annual sustainability report,availableonourwebsitesustainability.kroger.com.

Kroger is a leader in supplier diversity, spending nearly $2 billion annually with women- andminority-ownedbusinesses.WeproudlyremainamemberoftheBillionDollarRoundtableandtheUnitedStatesHispanicChamberofCommerceMillionDollarClub.

Kroger is doing our part to create jobs and opportunity.Weemploy7,000moreassociatestodaythanwedidlastyear,andnearly90percentofthosenewjobsareinoursupermarketdivisions.Overthelastsixyears,Krogerhascreatedmorethan40,000newjobsinthelocalcommunitiesweserve.

4

Leadership

Webelievewehaveoneof thestrongestmanagement teams in theretail industry.For tenyearsourCompanyhasbeenledbyDaveDillon,whohasbeencalled“thegrocers’grocer.”Dave’sknowledgeofthebusiness,passionforcustomersandassociates,andprincipledanddisciplinedapproachtorunningaworld-classcompanyhasrewardedshareholders,associates,customers,andcommunities.Wethankhimfor thestrong foundationhebuilt and thatwe are inspired tocontinue toexpand.Daveoften refers to retailingasateamsport.Everygreatteam,includingours,needsagreatcoachandleader.Thankyou,Dave,fortenremarkableyearsasChairmanandCEO.

In Memoriam and Retirements

Weweresaddenedbythelossofourfriendandcolleague,JonC.Flora,whopassedawayunexpectedlyinSeptember2013.HewaspresidentofFry’sFoodStoresinArizona.Jonwasacompassionateandhands-onleader. We all miss him deeply.

We extend our appreciation to John LaMacchia, who retired from Kroger’s Board of Directors inDecember2013after24yearsofservice;toPaulHeldman,executivevicepresident,secretaryandgeneralcounsel,whoretiresinMayafter32yearsofservice;andtoRobert“Pete”Williams,seniorvicepresident,whoretiresinMayafter37yearswiththeCompany.OnbehalfofourentireCompany,wethankeachoftheseindividuals for their service and leadership.

Bright Future – More to Come

Kroger’sfutureisbright.WearedifferentiatingourCompanyinthecrowdedfieldofretailersinwaysthatleadtosustainable,reliablegrowth.Andthereisalotmoretocomeforshareholders,associatesandcustomers.

OnbehalfoftheentireKrogerfamily,wethankyouforyourcontinuedsupportandtrust.

W.RodneyMcMullen Chief Executive Officer

5

CongratulationstothewinnersofTheKrogerCo.CommunityServiceAwardfor2013:

2013 Community Service Award Winners

Division RecipientAtlanta EmilyMayCentral SherryMillerCincinnati JeanettaSteelyCityMarket Adilia AsplundColumbus MartiKingDelta DianneScallionsDillonStores JamieTietgenFood 4 Less MarisaRobertsFredMeyer Tracy NicholsFry’s BryanSeppalaJayCStores DonnieRoarkKingSoopers LindaHutsellLouisville JohnOwensMichigan RachelMasonMid-Atlantic RachelStrattonNashville BrysonHigginsQFC KathyButcherRalphs MichaelVuSmith’s April WilsonSouthwest Aaron Calvert / Phillip Ingram______

Tara Foods MonaMcCoyKBSpecialtyFoods Laurie FosterPace Crawfordsville Kevin FroedgeWinchester Farms Dairy RitaAkersLaHabraBakery BerthaGuzman______

CStores Aiesha Little______

Corporate Tricia FettersLogistics Patty Freeman

6

N o t i c e o F a N N u a l M e e t i N g o F S h a r e h o l d e r S

Cincinnati,Ohio,May14,2014

ToAllShareholdersofTheKrogerCo.:

YouareinvitedtoourannualmeetingofshareholdersofTheKrogerCo.whichwillbeheldattheMUSICHALLBALLROOM,MUSICHALL,1241ElmStreet,Cincinnati,Ohio45202,onJune26,2014,at11a.m.,easterntime, for the following purposes:

1. Toelectthirteendirectorsfortheensuingyear;

2. Toconsiderandactuponaproposaltoapprovethe2014Long-TermIncentiveandCashBonusPlan;

3. Toconsiderandactuponanadvisoryvotetoapproveexecutivecompensation;

4. To consider and act upon a proposal to ratify the selection of independent registered publicaccountantsfortheyear2014;

5. Toactupontwoshareholderproposals,ifproperlypresentedattheannualmeeting;and

6. Totransactsuchotherbusinessasmayproperlybebroughtbeforethemeeting;

HoldersofcommonsharesofrecordatthecloseofbusinessonApril29,2014,willbeentitledtonoticeof and to vote at the meeting.

a t t e N d a N c e

Only shareholders and persons holding proxies from shareholders may attend the meeting. If you are attending the meeting, please bring the notice of the meeting that was separately mailed to you or the top portion of your proxy card, either of which will serve as your admission ticket.

YOUR MANAGEMENT DESIRES TO HAVE A LARGE NUMBER OF SHAREHOLDERS REPRESENTEDATTHEMEETING, INPERSONORBYPROXY.PLEASEVOTEYOURPROXYELECTRONICALLYVIATHEINTERNETORBYTELEPHONE.IFYOUHAVEELECTEDTORECEIVEPRINTEDMATERIALS,YOUMAYSIGNANDDATETHEPROXYANDMAILITINTHESELF-ADDRESSEDENVELOPEPROVIDED.NOPOSTAGEISREQUIREDIFMAILEDWITHINTHEUNITEDSTATES.

Ifyouareunabletoattendtheannualmeeting,youmaylistentoalivewebcastofthemeeting,whichwillbeaccessiblethroughourwebsite,ir.kroger.com,at11a.m.,easterntime.

ByorderoftheBoardofDirectors,PaulW.Heldman,Secretary

7

P r o x y S t a t e M e N t

Cincinnati,Ohio,May14,2014

ThisCombinedNotice,ProxyStatementandAnnualReportisbeingfurnishedtotheshareholdersofTheKrogerCo.inconnectionwiththesolicitationofproxiesbytheBoardofDirectorsforuseattheAnnualMeetingofShareholderstobeheldonJune26,2014,at11a.m.,easterntime,attheMUSICHALLBALLROOM,MUSICHALL,1241ElmStreet,Cincinnati,Ohio45202andatanyadjournmentsthereof.

The principal executive offices of TheKroger Co. are located at 1014Vine Street, Cincinnati,Ohio45202-1100. Our telephone number is 513-762-4000. This Proxy Statement and Annual Report, and theaccompanyingproxy,werefirstfurnishedtoshareholdersonMay14,2014.

Yourproxy issolicitedby theBoardofDirectorsofTheKrogerCo.,and thecostofsolicitationwillbe borne byKroger.Wewill reimburse banks, brokers, nominees, and other fiduciaries for postage andreasonable expenses incurred by them in forwarding the proxymaterial to their principals. Kroger hasretainedD.F.King&Co.,Inc.,48WallStreet,NewYork,NewYork,toassistinthesolicitationofproxiesandwillpaythatfirmafeeestimatedatpresentnottoexceed$15,000.Proxiesmaybesolicitedpersonally,bytelephone,electronicallyviatheInternet,orbymail.

RobertD.Beyer,W.RodneyMcMullen,andRonaldL.Sargent,allofwhomareKrogerdirectors,havebeennamedmembersoftheProxyCommittee.

AsofthecloseofbusinessonApril29,2014,therecorddate,ouroutstandingvotingsecuritiesconsistedof 509,553,233commonshares, theholdersofwhichwillbeentitled toonevoteper shareat theannualmeeting.Thesharesrepresentedbyeachproxywillbevotedunlesstheproxyisrevokedbeforeitisexercised.Revocationmaybe inwriting toKroger’s Secretary, or inperson at themeeting,orby appointmentof asubsequentproxy.Shareholdersmaynotcumulatevotesintheelectionofdirectors.

Ifyouholdsharesinstreetnameanddonotprovideyourbrokerwithspecificvotinginstructionsonproposals1,2,3,5and6,yourbrokerdoesnothavetheauthoritytovoteonthoseproposals.Thisisgenerallyreferredtoasa“brokernon-vote.”Proposal4isconsideredaroutinematterand,therefore,yourbrokermayvote your shares according to your broker’s discretion. The vote required, including the effect of brokernon-votesandabstentionsforeachofthematterspresentedforshareholdervote,issetforthbelow.

Item No. 1, Election of Directors–Anaffirmativevoteofthemajorityofthetotalnumberofvotescast“for”or“against”adirectornomineeisrequiredfortheelectionofadirectorinanuncontestedelection.Accordingly,brokernon-votesandabstentionswillhavenoeffectonthisproposal. Amajorityofvotescastmeansthatthenumberofsharesvoted“for”adirectornomineemustexceedthenumberofvotes“against”such director.

Item No. 2, Approval of 2014 Long-Term Incentive and Cash Bonus Plan – ApprovalbyshareholdersofthePlanrequirestheaffirmativevoteofthemajorityofsharesentitledtovoteonthematter.Accordingly,brokernon-votesandabstentionswillhavenoeffectonthisproposal.

Item No. 3, Advisory Vote to Approve Executive Compensation – Approval by shareholders ofexecutivecompensationrequirestheaffirmativevoteofthemajorityofsharesentitledtovoteonthematter.Accordingly,brokernon-votesandabstentionswillhavenoeffectonthisproposal.

Item No. 4, Selection of Auditors–Ratificationbyshareholdersoftheselectionofindependentpublicaccountantsrequirestheaffirmativevoteofthemajorityofsharesentitledtovoteonthematter.Accordingly,abstentionswillhavenoeffectonthisproposal.

Item Nos. 5 and 6, Shareholder Proposals –Theaffirmativevoteofamajorityofsharesparticipatinginthevotingonashareholderproposal isrequiredfor itsadoption.ProxieswillbevotedAGAINSTtheseproposals unless the Proxy Committee is otherwise instructed on a proxy properly executed and returned. Brokernon-votesandabstentionswillhavenoeffectontheseproposals.

8

Important Notice Regarding the Availability of Proxy Materials for the Shareholder Meeting to be Held on June 26, 2014.

UndertherulesadoptedbytheSEC,wearefurnishingproxymaterialstoourshareholdersprimarilyontheInternet.Webelievethatthisprocessshouldexpediteshareholders’receiptofproxymaterials,lowerthecostofourannualmeetingandhelptoconservenaturalresources.OnoraboutMay14,2014,wemailedtoeachofourshareholders(otherthanthosewhopreviouslyrequestedelectronicorpaperdelivery),aNoticeof InternetAvailabilityofProxyMaterialscontaining instructionsonhowtoaccessandreviewtheproxymaterialsontheInternetandinstructionsonhowtovoteyourshares.TheNoticeofInternetAvailabilityofProxyMaterialsalsocontainsinstructionsonhowtoreceiveapaperore-mailcopyoftheproxymaterials.IfyoureceiveaNoticeofInternetAvailabilityofProxyMaterials,youwillnotreceiveaprintedcopyoftheproxymaterialsunlessyourequestone.Ifyoureceivepapercopiesofourproxymaterials,youmayalsoviewthesematerials at http://www.proxyvote.com. If you receive paper copies of our proxy materials and wish to receive thembyelectronicdeliveryinthefuture,pleaserequestelectronicdeliveryathttp://www.proxyvote.com.

9

P r o P o S a l S t o S h a r e h o l d e r S

e l e c t i o N o F d i r e c t o r S ( i t e M N o . 1)

TheBoardofDirectors,asnowauthorized,consistsofthirteenmembers.Allmembersaretobeelectedattheannualmeetingtoserveuntiltheannualmeetingin2015,oruntiltheirsuccessorshavebeenelectedbytheshareholdersorbytheBoardofDirectorspursuanttoKroger’sRegulations,andqualified.Kroger’sArticlesofIncorporationprovidethatthevoterequiredforelectionofadirectorbytheshareholders,exceptinacontestedelectionorwhencumulativevotingisineffect,willbetheaffirmativevoteofamajorityofthevotes cast for or against the election of a nominee.

Theexperience,qualifications,attributes,andskillsthatledtheCorporateGovernanceCommitteeandtheBoard toconclude that the following individualsshouldserveasdirectorsareset forthoppositeeachindividual’sname.Thecommitteemembershipsstatedbelowarethoseineffectasofthedateofthisproxystatement.Itisintendedthat,excepttotheextentthatauthorityiswithheld,proxiesbytheProxyCommitteewillbevotedfortheelectionofthefollowingpersons:

NameProfessional

Occupation (1) AgeDirector

Since

N o M i N e e S F o r d i r e c t o r F o r t e r M S o F o F F i c e c o N t i N u i N g u N t i l 2 015

Reuben V. Anderson Mr. Anderson is a Senior Partner in the Jackson, Mississippi officeof Phelps Dunbar, a regional law firm based in NewOrleans. Priorto joining this law firm, he was a justice of the Supreme Court ofMississippi.Mr.Anderson iscurrentlyservingas the leaddirectorofAT&TInc.,andduringthepastfiveyearswasadirectorofTrustmarkCorporation.HeisamemberoftheCorporateGovernanceandPublicResponsibilitiesCommittees.

Mr.Andersonhasextensivelitigationexperience,andheservedasthefirstAfrican-American Justiceon theMississippi SupremeCourt.HisknowledgeandjudgmentgainedthroughyearsoflegalpracticeareofgreatvaluetotheBoard.Inaddition,asformerChairmanoftheBoardofTrusteesofTougalooCollegeandaresidentofMississippi,hebringsto the Board his insights into the African-American community andthesouthernregionoftheUnitedStates.Mr.Andersonhasservedonnumerousboardcommittees, including audit,publicpolicy, finance,executive, and nominating committees.

71 1991

10

NameProfessional

Occupation (1) AgeDirector

Since

Robert D. Beyer Mr.BeyerisChairmanofChaparalInvestmentsLLC,aprivateinvestmentfirmandholdingcompanythathefoundedin2009.From2005to2009,Mr.BeyerservedasChiefExecutiveOfficerofTheTCWGroup,Inc.,aglobalinvestmentmanagementfirm.From2000to2005,heservedasPresident and Chief Investment Officer of Trust Company of the West, theprincipaloperatingsubsidiaryofTCW.Mr.BeyerisamemberoftheBoardofDirectorsofTheAllstateCorporationandLeucadiaNationalCorporation.He ischairof theCorporateGovernanceCommittee, amemberoftheFinancialPolicyCommittee,andourLeadDirector.

Mr.Beyerbrings toKrogerhis experience asCEOofTCW, a globalinvestment management firm serving many of the largest institutional investorsintheU.S.HehasexceptionalinsightintoKroger’sfinancialstrategy, and his experience qualifies him to serve as a member ofthe Financial Policy Committee. While at TCW, he also conceived and developed the firm’s riskmanagement infrastructure, an experiencethatisusefultotheKrogerBoardinperformingitsriskmanagementoversight functions. His abilities and service as a director wererecognized by his peers,who selectedMr. Beyer as anOutstandingDirector in 2008 as part of the Outstanding Directors Program of the Financial Times.His strong insights into corporate governance formthefoundationofhisleadershiproleasLeadDirectorontheBoard.

54 1999

David B. Dillon Mr.DillonwaselectedChiefExecutiveOfficerin2003andChairmanoftheBoardofKrogerin2004.Mr.DillonretiredasChiefExecutiveOfficer at the end of calendar year 2013 and will continue to serve as ChairmanoftheBoarduntiltheendofcalendaryear2014.Mr.Dillonserved as President and Chief Operating Officer in 2000, as President in 1999, and as President andChiefOperatingOfficer from1995 to1999. Mr. Dillonwas elected Executive Vice President of Kroger in1990andPresidentofDillonCompanies,Inc.in1986.HeisadirectorofDIRECTVandUnionPacificCorporation,andduringthepastfiveyears was a director of Convergys Corporation.

Mr.DillonbringstoKrogerhisextensiveknowledgeofthesupermarketbusiness,havingover38yearsofexperiencewithKrogerandDillonCompanies.InadditiontohisdepthofknowledgeofKrogerandthefiercely competitive industry in which Kroger operates, he has gained awealthofexperiencebyservingonaudit,compensation,finance,andgovernancecommitteesofotherboards.

63 1995

11

NameProfessional

Occupation (1) AgeDirector

Since

Susan J. Kropf Ms.KropfwasPresidentandChiefOperatingOfficerofAvonProductsInc., a manufacturer and marketer of beauty care products, from2001until her retirement in January2007. She joinedAvon in1970.Prior to hermost recent assignment,Ms.Kropf had been ExecutiveVice President and Chief Operating Officer, Avon North America and GlobalBusinessOperationsfrom1998to2000.From1997to1998shewasPresident,AvonU.S.Ms.KropfwasamemberofAvon’sBoardofDirectorsfrom1998to2006.ShecurrentlyisamemberoftheBoardofDirectorsofCoach,Inc.,MeadWestvacoCorporation,andSherwinWilliams Company. She is a member of the Audit and FinancialPolicy Committees.

Ms.Kropfhasgainedauniqueconsumer insight,having ledamajorbeautycarecompany.Shehasextensiveexperienceinmanufacturing,marketing, supply chain operations, customer service, and productdevelopment,allofwhichassistherinherroleasamemberofKroger’sBoard.Ms.Kropfhasastrongfinancialbackground,andhasservedoncompensation, audit, and corporate governance committees of other boards.ShewasinductedintotheYWCAAcademyofWomenAchievers.

65 2007

David B. Lewis Mr.LewisisashareholderanddirectorofLewis&Munday,aDetroitbased lawfirmwithoffices inWashington,D.C.andNewYorkCity.He isadirectorofH&RBlock, Inc.andSTERISCorporation.He isamemberoftheFinancialPolicyCommitteeandvicechairofthePublicResponsibilitiesCommittee.

Inaddition tohisbackgroundasapracticingattorneyandexpertisein bond financing,Mr. Lewis brings to Kroger’s Board his financialexpertise gained while earning his MBA in Finance as well as hisservice and leadership on Kroger’s audit committee and the boardcommitteesofotherpubliclytradedcompanies.Mr.Lewishasservedon theBoardofDirectorsofConrail, Inc.,LG&EEnergyCorp.,M.A.Hanna,TRW,Inc.,andComerica,Inc.HeisaformerchairmanoftheNationalAssociationofSecuritiesProfessionals.

69 2002

12

NameProfessional

Occupation (1) AgeDirector

Since

W. Rodney McMullen Mr.McMullenwaselectedChiefExecutiveOfficerofKrogerinJanuary2014. Prior to this, he served as President and Chief Operating Officer fromAugust2009toDecember2013.Priortothat,Mr.McMullenwaselected Vice Chairman in 2003, Executive Vice President in 1999, and SeniorVicePresidentin1997.Mr.McMullenisadirectorofCincinnatiFinancial Corporation.

Mr. McMullen has broad experience in the supermarket business,having spenthiscareer spanningover35yearswithKroger.Hehasastrongfinancialbackground,havingservedasourCFO,andplayedamajorroleasarchitectofKroger’sstrategicplan.Hisserviceonthecompensation, executive, and investment committees of Cincinnati Financial Corporation adds depth to his extensive retail experience.

53 2003

Jorge P. Montoya

Mr.MontoyawasPresidentofTheProcter&GambleCompany’sGlobalSnacks&Beveragedivision,andPresidentofProcter&GambleLatinAmerica, from 1999 until his retirement in 2004. Prior to that, he was anExecutiveVicePresidentofProcter&Gamble,aproviderofbrandedconsumerpackagedgoods,from1995to1999.Mr.MontoyaisadirectorofTheGap,Inc.HeischairofthePublicResponsibilitiesCommitteeandamemberoftheCompensationCommittee.

Mr. Montoya brings to Kroger’s Board over 30 years of leadershipexperienceatapremierconsumerproductscompany.HehasadeepknowledgeoftheHispanicmarket,aswellasconsumerproductsandretailoperations.Mr.Montoyahasvastexperience inmarketingandgeneralmanagement,includinginternationalbusiness.Hewasnamedamongthe50mostimportantHispanicsinBusiness&Technology,inHispanic Engineer & Information Technology Magazine.

67 2007

Clyde R. Moore Mr.MooreistheChairmanandChiefExecutiveOfficerofFirstServiceNetworks, a national provider of facility and maintenance repairservices.HeisadirectorofFirstServiceNetworks.Mr.Mooreischairof the Compensation Committee and a member of the CorporateGovernanceCommittee.

Mr. Moore has over 25 years of general management experience inpublicandprivatecompanies.Hehassoundexperienceasacorporateleader overseeing all aspects of a facilities management firm and a manufacturingconcern.Mr.Moore’sexpertisebroadensthescopeoftheBoard’sexperiencetoprovideoversighttoKroger’sfacilitiesandmanufacturingbusinesses.

60 1997

13

NameProfessional

Occupation (1) AgeDirector

Since

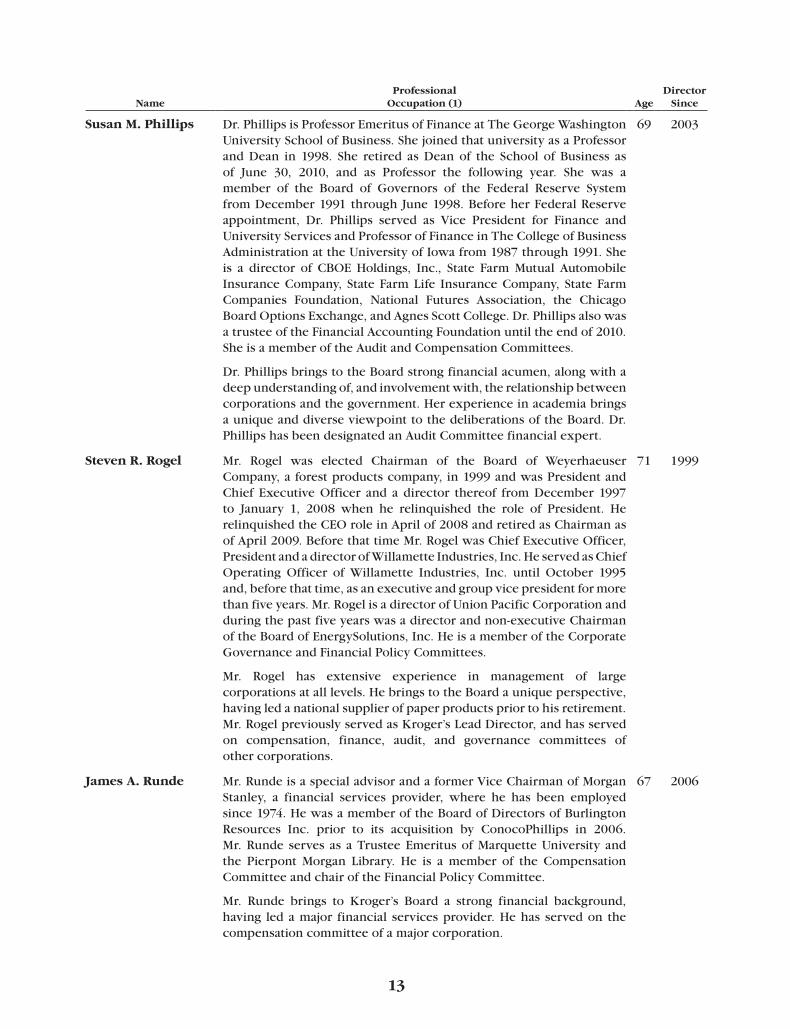

Susan M. Phillips Dr.PhillipsisProfessorEmeritusofFinanceatTheGeorgeWashingtonUniversitySchoolofBusiness.ShejoinedthatuniversityasaProfessorandDean in 1998. She retired asDeanof the School of Business asof June 30, 2010, and as Professor the following year. She was amember of the Board of Governors of the Federal Reserve SystemfromDecember1991throughJune1998.BeforeherFederalReserveappointment, Dr. Phillips served as Vice President for Finance and UniversityServicesandProfessorofFinanceinTheCollegeofBusinessAdministrationattheUniversityofIowafrom1987through1991.Sheis a director of CBOEHoldings, Inc., State FarmMutual AutomobileInsuranceCompany, StateFarmLife InsuranceCompany, StateFarmCompanies Foundation, National Futures Association, the Chicago BoardOptionsExchange,andAgnesScottCollege.Dr.Phillipsalsowasa trustee of the Financial Accounting Foundation until the end of 2010. SheisamemberoftheAuditandCompensationCommittees.

Dr.PhillipsbringstotheBoardstrongfinancialacumen,alongwithadeepunderstandingof,andinvolvementwith,therelationshipbetweencorporationsandthegovernment.HerexperienceinacademiabringsauniqueanddiverseviewpointtothedeliberationsoftheBoard.Dr.PhillipshasbeendesignatedanAuditCommitteefinancialexpert.

69 2003

Steven R. Rogel Mr. Rogel was elected Chairman of the Board of WeyerhaeuserCompany, a forest products company, in 1999 and was President and Chief ExecutiveOfficer and a director thereof fromDecember 1997to January 1, 2008 when he relinquished the role of President. HerelinquishedtheCEOroleinAprilof2008andretiredasChairmanasofApril2009.BeforethattimeMr.RogelwasChiefExecutiveOfficer,PresidentandadirectorofWillametteIndustries,Inc.HeservedasChiefOperating Officer ofWillamette Industries, Inc. until October 1995and,beforethattime,asanexecutiveandgroupvicepresidentformorethanfiveyears.Mr.RogelisadirectorofUnionPacificCorporationandduringthepastfiveyearswasadirectorandnon-executiveChairmanoftheBoardofEnergySolutions,Inc.HeisamemberoftheCorporateGovernanceandFinancialPolicyCommittees.

Mr. Rogel has extensive experience in management of largecorporationsatalllevels.HebringstotheBoardauniqueperspective,having led a national supplier of paper products prior to his retirement. Mr.RogelpreviouslyservedasKroger’sLeadDirector,andhasservedon compensation, finance, audit, and governance committees of other corporations.

71 1999

James A. Runde Mr.RundeisaspecialadvisorandaformerViceChairmanofMorganStanley, a financial services provider, where he has been employedsince1974.HewasamemberoftheBoardofDirectorsofBurlingtonResources Inc. prior to its acquisition by ConocoPhillips in 2006.Mr.Runde serves as aTrusteeEmeritusofMarquetteUniversity andthe PierpontMorgan Library. He is amember of the CompensationCommittee and chair of the Financial Policy Committee.

Mr. Runde brings to Kroger’s Board a strong financial background,having ledamajor financial servicesprovider.Hehas servedon thecompensationcommitteeofamajorcorporation.

67 2006

14

NameProfessional

Occupation (1) AgeDirector

Since

Ronald L. Sargent Mr.SargentisChairmanandChiefExecutiveOfficerofStaples,Inc.,aconsumerproductsretailer,wherehehasbeenemployedsince1989.PriortojoiningStaples,Mr.Sargentspent10yearswithKrogerinvariouspositions.InadditiontoservingasadirectorofStaples,Mr.SargentisadirectorofFiveBelow,Inc.Duringthepastfiveyears,hewasadirectorofMattel,Inc.andTheHomeDepot,Inc.Mr.SargentischairoftheAuditCommitteeandamemberofthePublicResponsibilitiesCommittee.

Mr. Sargenthasover30yearsof retail experience, firstwithKrogerand then with increasing levels of responsibility and leadershipat Staples, Inc.His efforts helped carve out a newmarket niche forthe international retailer that he leads. His understanding of retailoperationsandconsumerinsightsareofparticularvaluetotheBoard.Mr.SargenthasbeendesignatedanAuditCommitteefinancialexpert.

58 2006

Bobby S. Shackouls Until the merger of Burlington Resources Inc. and ConocoPhillips,which became effective in 2006, Mr. Shackouls was Chairman oftheBoardofBurlingtonResourcesInc.,anaturalresourcesbusiness,since July 1997 and its President and Chief Executive Officer sinceDecember1995.Hehadbeenadirectorof thatcompanysince1995and President and Chief Executive Officer of Burlington ResourcesOilandGasCompany(formerlyknownasMeridianOilInc.),awholly-ownedsubsidiaryofBurlingtonResources,since1994.Mr.ShackoulsisadirectorofPlainsGPHoldings,L.P.andOasisPetroleumInc.Duringthepastfiveyears,Mr.ShackoulswasadirectorofConocoPhillipsandPNGSGP LLC, the general partner of PAANatural Gas Storage, L.P.Mr. Shackouls is amember of the Audit and Corporate GovernanceCommittees.Mr.ShackoulspreviouslyservedasKroger’sLeadDirector.

Mr. Shackouls brings to the Board the critical thinking that comeswith a chemical engineering background, aswell as his experienceleadingamajornaturalresourcescompany,coupledwithhiscorporategovernance expertise.

63 1999

(1) Exceptasnoted,eachofthedirectorshasbeenemployedbyhisorherpresentemployer(orasubsidiary)in an executive capacity for at least five years.

15

i N F o r M a t i o N c o N c e r N i N g t h e B o a r d o F d i r e c t o r S

c o M M i t t e e S o F t h e B o a r d

The Board of Directors has a number of standing committees including Audit, Compensation andCorporateGovernance.Allstandingcommitteesarecomposedexclusivelyofindependentdirectors.AllBoardcommitteeshavechartersthatcanbefoundonourcorporatewebsiteatir.kroger.comunderGuidelines on Issues of Corporate Governance.

ThetablebelowprovidesthecurrentmembershipofourindependentdirectorsoneachofthestandingcommitteesofourBoardofDirectors.

NameAudit

CommitteeCompensation

Committee

Corporate Governance Committee

Financial Policy

Committee

Public Responsibilities

Committee

ReubenV.Anderson x xRobertD.Beyer Chair xSusanJ.Kropf x xDavidB.Lewis x xJorgeP.Montoya x ChairClydeR.Moore Chair xSusanM.Phillips x xStevenR.Rogel x xJamesA.Runde x ChairRonaldL.Sargent Chair xBobbyS.Shackouls x x

During 2013, the Audit Committee met five times, the Compensation Committee met four times, and the Corporate Governance Committeemet two times. The Audit Committee reviews financial reportingand accounting matters pursuant to its charter and selects our independent accountants. The Compensation CommitteerecommendsfordeterminationbytheindependentmembersofourBoardthecompensationoftheChief Executive Officer, determines the compensation of Kroger’s other senior management, and administers some of our incentive programs. Additional information on the Compensation Committee’s processes and procedures for consideration of executive compensation are addressed in the Compensation Discussion and Analysisbelow.TheCorporateGovernanceCommitteedevelopscriteriaforselectingandretainingmembersoftheBoard,seeksoutqualifiedcandidatesfortheBoard,andreviewstheperformanceoftheBoardand,alongwiththeotherindependentboardmembers,theCEO.

d i r e c t o r N o M i N a t i o N S

TheCorporateGovernanceCommitteewillconsidershareholder recommendations fornominees formembershipontheBoardofDirectors. IfshareholderswishtonominateapersonorpersonsforelectiontotheBoardofDirectorsatour2015annualmeeting,writtennoticemustbesubmittedtotheCompany’sSecretary,andreceivedatourexecutiveofficesnotlaterthanJanuary14,2015.Suchnoticeshouldincludethename,age,businessaddressandresidenceaddressofsuchperson,theprincipaloccupationoremploymentofsuchperson,thenumberofsharesoftheCompanyownedofrecordorbeneficiallybysuchperson,andanyother information relating to theperson thatwouldbe required tobe included inaproxy statementrelatingtotheelectionofdirectors.TheSecretarywillforwardtheinformationtotheCorporateGovernanceCommitteeforitsconsideration.TheCommitteewillusethesamecriteriainevaluatingcandidatessubmittedbyshareholdersasitusesinevaluatingcandidatesidentifiedbytheCommittee.Thesecriteriaare:

• Demonstrated ability in fields considered tobeof value in thedeliberationsof theBoard, includingbusinessmanagement,publicservice,education,science,law,andgovernment;

• Higheststandardsofpersonalcharacterandconduct;

16

• Willingnesstofulfilltheobligationsofdirectorsandtomakethecontributionofwhichheorsheiscapable,includingregularattendanceandparticipationatBoardandcommitteemeetings,andpreparationforallmeetings,includingreviewofallmeetingmaterialsprovidedinadvanceofthemeeting;and

• AbilitytounderstandtheperspectivesofKroger’scustomers,takingintoconsiderationthediversityofour customers, including regional and geographic differences.

Racial, ethnic, and gender diversity is an important element in promoting full, open, and balanceddeliberationsofissuespresentedtotheBoard,andisconsideredbytheCorporateGovernanceCommittee.Some consideration also is given to the geographic location of director candidates in order to provide areasonabledistributionofmembersfromtheoperatingareasoftheCompany.

TheCorporateGovernanceCommitteetypicallyrecruitscandidatesforBoardmembershipthroughitsown efforts and through suggestions from other directors and shareholders. The Committee on occasion has retainedanoutsidesearchfirmtoassistinidentifyingandrecruitingBoardcandidateswhomeetthecriteriaestablishedbytheCommittee.

c o r P o r a t e g o v e r N a N c e

TheBoardofDirectorshasadoptedGuidelines on Issues of Corporate Governance. These Guidelines, which include copies of the current charters for the Audit, Compensation, and Corporate GovernanceCommittees,andtheothercommitteesoftheBoardofDirectors,areavailableonourcorporatewebsiteatir.kroger.com.Shareholdersmayobtainacopyof theGuidelinesbymakingawrittenrequest toKroger’sSecretaryatourexecutiveoffices.

i N d e P e N d e N c e

TheBoardofDirectorshasdeterminedthatallofthedirectors,withtheexceptionofMessrs.DillonandMcMullen,havenomaterialrelationshipswithKrogerand,therefore,areindependentforpurposesoftheNewYork StockExchange listing standards.TheBoardmade its determinationbasedon informationfurnishedbyallmembersregardingtheirrelationshipswithKrogeranditsmanagement,andotherrelevantinformation.Afterreviewingtheinformation,theBoarddeterminedthatallofthenon-employeedirectorswere independentbecause (i) theyall satisfied the independencestandardsset forth inRule10A-3of theSecuritiesExchangeActof1934,(ii)theyallsatisfiedthecriteriaforindependencesetforthinRule303A.02oftheNewYorkStockExchangeListedCompanyManual,(iii)anybusinesstransactionsbetweenKrogerandentitieswithwhichthedirectorsareaffiliated,thevalueofwhichfallsbelowthethresholdsidentifiedbytheNewYorkStockExchangelistingstandards,and(iv)nonehadanymaterialrelationshipswithusexceptforthose arising directly from their performance of services as a director for Kroger.

a u d i t c o M M i t t e e e x P e r t i S e

The Board of Directors has determined that Susan M. Phillips and Ronald L. Sargent, independentdirectorswhoaremembersoftheAuditCommittee,are“auditcommitteefinancialexperts”asdefinedbyapplicableSECregulationsandthatallmembersoftheAuditCommitteeare“financiallyliterate”asthattermisusedintheNYSElistingstandards.

c o d e o F e t h i c S

TheBoardofDirectorshasadoptedThe Kroger Co. Policy on Business Ethics,applicabletoallofficers,employees andmembers of theBoard ofDirectors, includingKroger’s principal executive, financial, andaccounting officers. The Policy is available on our corporatewebsite at ir.kroger.com. ShareholdersmayobtainacopyofthePolicybymakingawrittenrequesttoKroger’sSecretaryatourexecutiveoffices.Weintendtosatisfythedisclosurerequirementregardinganyamendmentto,orawaiverfrom,aprovisionofthe Policyforourprincipalexecutive,financialandaccountingofficersbypostingthatinformationonourwebsiteatir.kroger.com.

17

c o M M u N i c a t i o N S w i t h t h e B o a r d

The Board has established two separate mechanisms for shareholders and interested parties tocommunicatewiththeBoard.Anyshareholderorinterestedpartywhohasconcernsregardingaccounting,improperuseofKrogerassets,orethical improprietiesmayreporttheseconcernsviathetoll-freehotline(800-689-4609)oremail address ([email protected])establishedby theBoard’sAuditCommittee.Theconcerns are investigatedbyKroger’sVicePresidentofAuditingand reported to theAuditCommitteeasdeemedappropriatebytheVicePresidentofAuditing.

ShareholdersorinterestedpartiesalsomaycommunicatewiththeBoardinwritingdirectedtoKroger’sSecretaryatourexecutiveoffices.TheSecretarywillconsiderthenatureofthecommunicationanddeterminewhethertoforwardthecommunicationtothechairoftheCorporateGovernanceCommittee.Communicationsrelatingtopersonnelissuesorourordinarybusinessoperations,orseekingtodobusinesswithus,willbeforwardedtothebusinessunitofKrogerthattheSecretarydeemsappropriate.AllothercommunicationswillbeforwardedtothechairoftheCorporateGovernanceCommitteeforfurtherconsideration.ThechairoftheCorporateGovernanceCommitteewilltakesuchactionasheorshedeemsappropriate,whichmayincludereferraltotheCorporateGovernanceCommitteeortheentireBoard.

a t t e N d a N c e

TheBoardofDirectorsheldsevenmeetingsin2013.During2013,allincumbentdirectorsattendedatleast75%oftheaggregatenumberofmeetingsoftheBoardandcommitteesonwhichthatdirectorserved.MembersoftheBoardareexpectedtousetheirbesteffortstoattendallannualmeetingsofshareholders.Allfourteen membersthenservingontheBoardattendedlastyear’sannualmeeting.

c o M P e N S a t i o N c o N S u l t a N t S

TheCompensationCommitteedirectlyengagesacompensationconsultantfromMercerHumanResourceConsulting to advise the Committee in the design of compensation for executive officers. In 2013, Kroger paid thatconsultant$375,944forworkperformedfortheCommittee.Kroger,onmanagement’srecommendation,retainedtheparentandaffiliatedcompaniesofMercerHumanResourceConsultingtoprovideotherservicesforKroger in2013, forwhichKrogerpaid$4,743,100.Theseotherservicesprimarilyrelatedto insuranceclaims(forwhichKrogerwasreimbursedbyinsurancecarriersasclaimswereadjusted),insurancebrokerageandbondingcommissions,andpensionconsulting.Krogeralsomadepaymentstoaffiliatedcompaniesforinsurancepremiumsthatwerecollectedbytheaffiliatedcompaniesonbehalfofinsurancecarriers,buttheseamountsarenotincludedinthetotalsreferencedabove,astheamountswerepaidovertoinsurancecarriersforservicesprovidedbythosecarriers.AlthoughneithertheCommitteenortheBoardexpresslyapprovedtheother services, after taking intoconsideration theNYSE’s independence standards and the SEC rules,theCommitteedeterminedthattheconsultant is independentandhisworkhasnotraisedanyconflictofinterestbecause(a)hewasfirstengagedbytheCommitteebeforehebecameassociatedwithMercer;(b)heworksexclusivelyfortheCommitteeandnot forourmanagement;(c)hedoesnotbenefit fromtheotherworkthatMercer’sparentandaffiliatedcompaniesperformforKroger;and(d)neithertheconsultantnortheconsultant’steamperformanyotherservicesonbehalfofKroger.

NomemberoftheCompensationCommitteewasanofficeroremployeeoftheCompanyduringfiscalyear2013,andnomemberoftheCompensationCommitteewasformerlyanofficeroftheCompanyorwasapartytoanydisclosablerelatedpersontransactioninvolvingtheCompany.Duringfiscalyear2013,noneoftheexecutiveofficersoftheCompanyservedontheboardofdirectorsoronthecompensationcommitteeof any other entity that has or had executive officers serving as amember of the Board of Directors orCompensation Committee of the Company.

18

B o a r d o v e r S i g h t o F e N t e r P r i S e r i S k

While riskmanagement is primarily the responsibility of Kroger’s management team, the Board ofDirectorsisresponsiblefortheoverallsupervisionofourriskmanagementactivities.TheBoard’soversightofthematerialrisksfacedbyKrogeroccursatboththefullBoardlevelandatthecommitteelevel.

TheBoard’sAuditCommitteehasoversightresponsibilitynotonlyforfinancialreportingofKroger’smajor financial exposures and the stepsmanagement has taken tomonitor and control those exposures,butalsofortheeffectivenessofmanagement’sprocessesthatmonitorandmanagekeybusinessrisksfacingKroger,aswellas themajorareasof riskexposureandmanagement’sefforts tomonitorandcontrol thatexposure.TheAuditCommitteealsodiscusseswithmanagementitspolicieswithrespecttoriskassessmentandriskmanagement.

Management, including Kroger’s Chief Ethics and Compliance Officer, provides regular updatesthroughouttheyeartotherespectivecommitteesregardingthemanagementoftheriskstheyoversee,andeachofthesecommitteesreportsonrisktothefullBoardateachregularmeetingoftheBoard.

Inadditiontothereportsfromthecommittees,theBoardreceivespresentationsthroughouttheyearfromvariousdepartmentandbusinessunitleadersthatincludediscussionofsignificantrisksasnecessary.AteachBoardmeeting,theChairmanandtheCEOaddressmattersofparticularimportanceorconcern,includinganysignificantareasofriskthatrequireBoardattention.Additionally,throughdedicatedsessionsfocusingentirelyon corporate strategy, the full Board reviews in detail Kroger’s short- and long-term strategies, includingconsiderationof significant risks facingKroger and theirpotential impact. The independentdirectors, inexecutivesessionsledbytheLeadDirector,addressmattersofparticularconcern,includingsignificantareasofrisk,thatwarrantfurtherdiscussionorconsiderationoutsidethepresenceofKrogeremployees.

We believe that our approach to risk oversight, as described above, optimizes our ability to assessinter-relationshipsamong thevarious risks,make informedcost-benefitdecisions,andapproachemergingrisks in aproactivemanner forKroger.We alsobelieve that our risk structure complements our currentBoardleadershipstructure,asitallowsourindependentdirectors,throughthefivefullyindependentBoardcommittees, and in executive sessions of independent directors led by an independent LeadDirector, toexerciseeffectiveoversightoftheactionsofmanagement,ledbyMr.McMullenasCEO,inidentifyingrisksandimplementingeffectiveriskmanagementpoliciesandcontrols.

B o a r d l e a d e r S h i P S t r u c t u r e a N d l e a d d i r e c t o r

OurBoardiscomposedofelevenindependentnon-employeedirectors,andtwomanagementdirectors,Mr.Dillon,theChairmanoftheBoardandourformerChiefExecutiveOfficer,andMr.McMullen,ourChiefExecutive Officer. In addition, as provided in our Guidelines on Issues of Corporate Governance,theBoardhasdesignatedoneoftheindependentdirectorsasLeadDirector.TheBoardhasestablishedfivestandingcommittees—audit,compensation,corporategovernance,financialpolicy,andpublicresponsibilities.EachBoardcommitteeiscomposedsolelyof independentdirectors,eachwithadifferentindependentdirectorservingascommitteechair.ThemixofexperiencedindependentandmanagementdirectorsthatmakeupourBoard,alongwiththe independentroleofourLeadDirectorandour independentBoardcommittees,benefitsKrogeranditsshareholders.

TheBoarddesignatesoneof the independentdirectorsasaLeadDirector.TheLeadDirectorservesa variety of roles, including reviewing and approvingBoard agendas,meetingmaterials and schedules toconfirmtheappropriatetopicsarereviewedandsufficienttimeisallocatedtoeach;servingasliaisonbetweenthe Chairman of the Board,management, and the non-management directors; presiding at the executivesessionsofindependentdirectorsandatallothermeetingsoftheBoardofDirectorsatwhichtheChairmanoftheBoardisnotpresent;callinganexecutivesessionofindependentdirectorsatanytimeandservingastheBoard’srepresentativeforanyconsultationanddirectcommunication,followingarequest,withmajorshareholders.UnlessotherwisedeterminedbytheBoard,thechairoftheCorporateGovernanceCommitteeisdesignatedas theLeadDirector.RobertBeyer, an independentdirector and thechairof theCorporateGovernanceCommittee, iscurrentlyourLeadDirector.Mr.Beyer isaneffectiveLeadDirector forKrogerdue to, among other things, his independence, his deep strategic and operational understanding of Kroger obtainedwhileservingasaKrogerdirector,his insight intocorporategovernanceandhisexperienceonotherboards.

19

With respect to the roles of Chairman and CEO, the GuidelinesprovidethattheBoardwilldeterminewhenitisinthebestinterestsofKrogeranditsshareholdersfortherolestobeseparatedorcombined,andtheBoardexercises itsdiscretion as it deemsappropriate in lightofprevailingcircumstances.Aspartofthe succession planning process, the Guidelines provide that upon the selection of a new Chief Executive Officer,theBoardwilldeterminewhetheraseparationoftheofficesisappropriate.TheBoardbelievesthatthecombinationorseparationofthesepositionsshouldcontinuetobeconsideredaspartofthesuccessionplanning process, as was the case in 2003, and again in 2014, when the roles were separated.

OurBoardandeachof its committeesconduct an annual evaluation todeterminewhether they arefunctioningeffectively.Aspartofthisannualself-evaluation,theBoardassesseswhetherthecurrentleadershipstructurecontinuestobeappropriateforKrogeranditsshareholders.OurGuidelinesprovidetheflexibilityforourBoardtomodifyourleadershipstructureinthefutureasappropriate.WebelievethatKroger,likemanyU.S.companies,hasbeenwell-servedbythisflexibleleadershipstructure.

20

c o M P e N S a t i o N d i S c u S S i o N a N d a N a l y S i S

e x e c u t i v e c o M P e N S a t i o N – o v e r v i e w

As one of the largest retailers in the world, our executive compensation philosophy remains to attract andretainthebestmanagementtalentandtomotivatetheseemployeestoachieveourbusinessandfinancialgoals.Webelieveourstrategycreatesvalueforshareholdersinamannerconsistentwithourfocusonourcorevalues: honesty, integrity, respect, inclusion, diversity, and safety.

Toachieveourobjectives,ourCompensationCommitteeseekstoensurethatcompensationiscompetitiveandthatthereisadirectlinkbetweenpayandperformance.Todoso,itisguidedbythefollowingprinciples:

• Asignificantportionofpayshouldbeperformance-based,increasingproportionallywithanexecutive’slevelofresponsibility;

• Compensation should include incentive-based pay to drive performance, providing superior pay forsuperiorperformance,includingbothashort-andlong-termfocus;

• Compensationpoliciesshouldincludeanopportunityfor,andarequirementof,equityownership;and

• Componentsofcompensationshouldbetiedtoanevaluationofbusinessandindividualperformancemeasuredagainstmetricsthatalignwithourbusinessstrategy.

The compensation of our senior executives in fiscal year 2013 reflects these principles. Total compensation fortheyearisanindicatorofhowwellKrogerperformedcomparedtoourbusinessplan,reflectinghowourcompensationprogramrespondstobusinesschallengesandthemarketplace.Wecontinuetodeliversalesgrowth and positive earnings results.

• Akeymetric,identicalsupermarketsales,excludingthe53rdweekin2012andfuel,increased3.6%from2012.Throughfiscal2013,wehaveachieved41consecutivequartersofpositiveidenticalsalesgrowth.

• Netearningsperdilutedsharewere$2.90,andevenafter taking intoaccount several items thatwebelievearenecessary tomake these resultscomparable to fiscal2012,our results still exceededourguidance range.

• InSeptember2013,theBoardofDirectorsraisedthequarterlycashdividendby10%,to$0.165pershare.

• Kroger’sstockpriceincreased29.4%infiscalyear2013.

The Committee believes our management produced outstanding results in 2013, measured againstincreasinglyaggressivebusinessplanobjectivesforsales,earnings,andourstrategicplan.Thecompensationpaidtoournamedexecutiveofficersreflectedthisfactastheannualperformance-basedcashbonuspaidoutat104.949%ofbonuspotentials.Thestronglinkbetweenpayandperformanceisillustratedbyacomparisonofthe2012annualcashbonus,withan85.881%payout.In2012,weperformedwellbutdidnotachieveallofourbusinessplanobjectives.In2013,allofourbusinessplangoalswereexceeded(withtheexceptionofoursalesgoal,whichfellslightlyshort),resultinginanannualbonuspayoutthatexceeded100%ofpotentials.

Inkeepingwithouroverallcompensationphilosophy,weendeavortoensurethatourcompensationpracticesconformtobestpractices.Inparticular,overthepastseveralyearswehave:

• putinplacesignificantstockownershipguidelinelevelstoreinforcethelinkbetweentheinterestsofournamedexecutiveofficersandthoseofourshareholders;

• adopted claw-back policies under which the repayment of bonuses may be required incertaincircumstances;

• eliminatedtaxgross-ups;

• adoptedtherecommendationofshareholdersthattheybepermittedannually,onanadvisorybasis,tovoteonexecutivecompensation;and

• adoptedapolicyprohibitinghedgingandshortsales,andrestrictingpledging,ofKrogercommonsharesbyourofficersanddirectors.

21

Inaddition,beginningin2010,fiftypercentofthetime-basedequityawardsthatotherwisewouldhavebeengrantedtothenamedexecutiveofficersasrestrictedstockhavebeenreplacedwithperformanceunitsthatareearnedonlytotheextent thatperformanceobjectivesareachieved.Equitycompensationawardscontinuetoplayanimportantroleinrewardingnamedexecutiveofficersfortheachievementoflong-termbusinessobjectivesandprovidingincentivesforthecreationofshareholdervalue.

The following discussion and analysis addresses the compensation of the named executive officers, and thefactorsconsideredbytheCommitteeinsettingcompensationforthenamedexecutiveofficersandmakingrecommendations to the independentBoardmembers in the case of theCEO’s compensation.Additionaldetail isprovided in thecompensation tablesand theaccompanyingnarrativedisclosures that followthisdiscussion and analysis.

e x e c u t i v e c o M P e N S a t i o N – o B j e c t i v e S

TheCommitteehasseveral relatedobjectives regardingcompensation.First, theCommitteebelievesthatcompensationmustbedesignedtoattractandretain thosebestsuitedto fulfill thechallengingrolesthatexecutiveofficersplayatKroger.Second,someelementsofcompensationshouldhelpaligntheinterestsof the officers with your interests as shareholders. Third, compensation should create strong incentives for the officers (a) to achieve the annual business plan targets established by the Board, and (b) to achieveKroger’s long-termstrategicobjectives. Indevelopingcompensationprogramsandamounts tomeet theseobjectives,theCommitteeexercisesjudgmenttoensurethatexecutiveofficercompensationisappropriateandcompetitiveinlightofKroger’sperformanceandtheneedsofthebusiness.

S h a r e o w N e r S h i P g u i d e l i N e S

Tomore closely align the interests of the officerswith your interests as shareholders, the Board ofDirectorshasadoptedstockownershipguidelines.Theseguidelinesrequirenon-employeedirectors,officersandsomeotherkeyexecutivestoacquireandholdaminimumdollarvalueofKrogercommonshares.Theguidelines require the CEO to acquire andmaintain ownership of Kroger shares equal to five times hisbasesalary;theChiefOperatingOfficeratfourtimeshisbasesalary;ExecutiveVicePresidents,SeniorVicePresidentsandnon-employeedirectorsatthreetimestheirbasesalariesorannualbasecashretainers;andotherofficersandkeyexecutivesattwotimestheirbasesalaries.Coveredindividualsareexpectedtoachievethetarget levelwithinfiveyearsofappointmenttotheirposition.Krogershares, includingequityawardsfromKroger,maynotbesoldbycoveredindividualspriortoachievingholdingsrequiredbytheguidelines(otherthantopayfortheexercisepriceofoptionsandthetaxesassociatedwithequityawards),withouttheapproval of Kroger’s CEO.

r e S u l t S o F 2 0 1 3 a d v i S o r y v o t e t o a P P r o v e e x e c u t i v e c o M P e N S a t i o N

At the 2013 Annual Meeting of Shareholders, we held our third annual advisory vote on executivecompensation.Over97%ofthevotescastwereinfavoroftheadvisoryproposal in2013.TheCommitteeconsideredthisoverwhelminglyfavorableoutcomeandbelievesitconveysourshareholders’supportoftheCommittee’s decisions and the existing executive compensation programs. As a result, the Committee made no material changes in the structure of our compensation programs or pay for performance philosophy. At the 2014AnnualMeetingofShareholders,inkeepingwithourshareholders’requestforanannualadvisoryvote,we will again hold a vote to approve executive compensation (see page 55).TheCommitteewillcontinuetoconsider the results from this year’s and future advisory votes on executive compensation.

r o l e o F c o M P e N S a t i o N c o M M i t t e e

The Compensation Committee of the Board has the primary responsibility for establishing thecompensation of Kroger’s executive officers, including the named executive officers, with the exception of the Chief Executive Officer. The Committee’s role regarding the CEO’s compensation is to makerecommendationstotheindependentmembersoftheBoard;thoseindependentBoardmembersestablishthe CEO’s compensation.

22

e S t a B l i S h i N g e x e c u t i v e c o M P e N S a t i o N

TheindependentmembersoftheBoardhavetheexclusiveauthoritytodeterminetheamountoftheCEO’s salary; thebonuspotential for theCEO; thenature and amountof anyequity awardsmade to theCEO;andanyothercompensationquestionsrelatedto theCEO. Insetting theannualbonuspotential fortheCEO,theindependentdirectorsdeterminethedollaramountthatwillbemultipliedbythepercentagepayoutundertheannualbonusplangenerallyapplicabletoallcorporatemanagement,includingthenamedexecutive officers. The independent directors retain discretion to reduce the percentage payout the CEO wouldotherwisereceive.TheindependentdirectorsthusmakeaseparatedeterminationannuallyconcerningboththeCEO’sbonuspotentialandthepercentageofbonuspaid.

The Committee performs the same function and exercises the same authority as to the other named executive officers. The Committee’s annual review of compensation for the named executive officers includes the following:

• Conductsanannualreviewofallcomponentsofcompensation,quantifyingtotalcompensationforthenamed executive officers on tally sheets. The review includes a summary for each named executive officer ofsalary;annualperformance-basedcashbonus;long-termperformance-basedcashandperformanceunitcompensation;equity;accumulatedrealizedandunrealizedstockoptiongainsandrestrictedstockand performance unit values; the value of any perquisites; retirement benefits; severance benefitsavailableunderTheKrogerCo.EmployeeProtectionPlan;andearningsandpayoutsavailableunderKroger’snonqualifieddeferredcompensationprogram.

• ConsidersinternalpayequityatKrogertoensurethattheCEOisnotcompensateddisproportionately.The Committee has assured itself that the compensation of Kroger’s CEO and that of the other named executiveofficersbearsareasonablerelationshiptothecompensationlevelsofotherexecutivepositionsatKrogertakingintoconsiderationperformanceanddifferencesinresponsibilities.

• ReviewsareportfromtheCommittee’scompensationconsultants(describedbelow)comparingnamedexecutive officer and other senior executive compensation with that of other companies, primarily our competitors,toensurethattheCommittee’sobjectivesofcompetitivenessaremet.

• TakesintoaccountarecommendationfromtheCEO(exceptinthecaseofhisowncompensation)forsalary,bonuspotential, andequity awards foreachof the seniorofficers including theothernamedexecutiveofficers.TheCEO’srecommendation takes intoconsiderationtheobjectivesestablishedbyandthereportsreceivedbytheCommitteeaswellashisassessmentofindividualjobperformanceandcontributiontoourmanagementteam.

• Looksathistoricalinformationregardingsalary,bonus,andequitycompensationfora3-yearperiod.

Inconsideringeachof the factorsabove, theCommitteedoesnotmakeuseofa formula,but rathersubjectivelyreviewseachinsettingcompensation.

t h e c o M M i t t e e ’ S c o M P e N S a t i o N c o N S u l t a N t S a N d B e N c h M a r k i N g

As referenced earlier in this compensation discussion and analysis, the Committee directly engages a compensationconsultantfromMercerHumanResourceConsultingtoadvisetheCommitteeinthedesignofcompensation for executive officers.

TheMercer consultant conducts an annual competitive assessment of executive positions atKrogerfor theCommittee.Theassessment isoneof severalbases, asdescribedabove,onwhich theCommitteedetermines compensation. The consultant assesses:

• Basesalary;

• Targetannualperformance-basedbonus;

• Targetannualcashcompensation(thesumofsalaryandannualbonus);

• Annualizedlong-termincentiveawards,suchasstockoptions,restrictedshares,andperformance-basedlong-termcashbonusesandperformance-basedequityawards;and

• Totaldirectcompensation(thesumofalltheseelements).

23

Theconsultantcomparestheseelementsagainstthoseofothercompaniesinagroupofpublicly-tradedfood and drug retailers. For 2013, the group consisted of:

Costco Wholesale SupervaluCVS/Caremark TargetRite Aid Wal-MartSafeway Walgreens

Thispeergroupisthesamegroupaswasusedin2012.Themake-upofthecompensationpeergroupis reviewed annually and modified as circumstances warrant. Industry consolidation and other competitive forces will change the peer group used over time. The consultant also provides the Committee data from companiesin“generalindustry,”arepresentationofmajorpublicly-tradedcompanies.Thesedataarereferencepoints,particularlyforseniorstaffpositionswherecompetitionfortalentextendsbeyondtheretailsector.

In 2009, the Committee directly engaged an additional compensation consultant to conduct a review of Kroger’s executive compensation. This consultant, from FredericW. Cook & Co., Inc., examined thecompensationphilosophy,peergroupcomposition,annualcashbonus,andlong-termincentivecompensationincludingequityawards.TheconsultantconcludedthatKroger’sexecutivecompensationprogrammettheCommittee’sobjectives,andthatitprovidesastronglinkagebetweenpayandperformance.TheCommitteeexpectstoengageanadditionalcompensationconsultantfromtimetotimeasitdeemsadvisable.

ConsideringthesizeofKrogerinrelationtootherpeergroupcompanies,theCommitteebelievesthatsalariespaidtoourexecutiveofficersshouldbeatorabovethemedianpaidbycompetitorsforcomparablepositions.Thecommitteealsoaimstoprovideanannualbonuspotential toourexecutiveofficers that, ifthe increasingly more challenging annual business plan objectives are achieved, would cause total cashcompensationtobemeaningfullyabovethemedian.

c o M P o N e N t S o F e x e c u t i v e c o M P e N S a t i o N a t k r o g e r

Compensation for our named executive officers is comprised of the following:

• Salary;

• Performance-BasedAnnualCashBonus(annual,non-equityincentivepay);

• Performance-Based Long-Term Compensation (long-term, cash and performance unitincentivecompensation);

• OtherEquity(non-qualifiedstockoptionsandrestrictedstock);

• Retirementandotherbenefits;and

• Perquisites.

S a l a r y

Weprovideournamedexecutiveofficersandotheremployeesafixedamountofcashcompensation–salary–fortheirwork.Salariesfornamedexecutiveofficers(withtheexceptionoftheCEO)areestablishedeachyearbytheCommittee,inconsultationwiththeCEO.TheCEO’ssalaryisestablishedbytheindependentdirectors.SalariesforthenamedexecutiveofficerswerereviewedinJune2013.

Theamountofeachexecutive’ssalaryisinfluencedbynumerousfactorsincluding:

• AnassessmentofindividualcontributioninthejudgmentoftheCEOandtheCommittee(or,inthecaseoftheCEO,oftheCommitteeandtherestoftheindependentdirectors);

• Benchmarkingwithcomparablepositionsatpeergroupcompanies;

• Tenure;and

• RelationshipwiththesalariesofotherexecutivesatKroger.

24

Theassessmentof individualcontribution isbasedonasubjectivedetermination,without theuseofperformance targets, in the following areas:

• Leadership;

• Contributiontotheofficergroup;

• Achievementofestablishedobjectives,totheextentapplicable;

• Decision-makingabilities;

• Performanceoftheareasorgroupsdirectlyreportingtotheofficer;

• Increasedresponsibilities;

• Strategicthinking;and

• FurtheranceofKroger’scorevalues.

TheamountsshownbelowreflectthesalariesofthenamedexecutiveofficersineffectfollowingtheannualreviewoftheircompensationinJune.

Salaries

2011 2012 2013

DavidB.Dillon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,290,000 $1,330,000 $1,370,000W.RodneyMcMullen* . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 910,000 $ 939,600 $ 968,600J.MichaelSchlotman . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 650,000 $ 671,100 $ 704,655KathleenS.Barclay** . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — $ 677,300 $ 700,000PaulW.Heldman . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 739,000 $ 763,000 $ 786,000MichaelL.Ellis*** . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — $ 527,360

* Mr.McMullen’ssalaryincreasedto$1,100,000effectivewithhispromotiontoCEOonJanuary1,2014.

** Ms.Barclaybecameanamedexecutiveofficerin2012.

*** Mr.Ellisbecameanamedexecutiveofficerin2013.Hissalaryincreasedto$775,000effectivewithhispromotiontoPresidentandCOOonJanuary1,2014.

P e r F o r M a N c e - B a S e d a N N u a l c a S h B o N u S

Alargepercentageofouremployeesatalllevels,includingthenamedexecutiveofficers,areeligibletoreceiveaperformance-basedannualcashbonusbasedontheperformanceofKroger(inthecaseofthenamedexecutiveofficers)orbusinessunit(inthecaseofemployeesinourbusinessunits).TheCommitteeestablishesbonuspotentialsforeachexecutiveofficer,otherthantheCEOwhosebonuspotentialisestablishedbytheindependentdirectors.Actualpayouts,whichcanexceed100%ofthepotentialamountsbutmaynotexceed200%ofthepotentialamounts,representtheextenttowhichperformancemeetsorexceedsthethresholdsestablishedbytheCommittee.

TheCommitteeconsidersseveralfactorsinmakingitsdeterminationorrecommendationastobonuspotentials. First, the individual’s levelwithin the organization is a factor in that the Committee believesthatmoreseniorexecutivesshouldhaveasubstantialpartoftheircompensationdependentuponKroger’sperformance.Second, the individual’s salary isa factorso thatasubstantialportionofanamedexecutiveofficer’s total cash compensation is dependent upon Kroger’s performance. Finally, the Committee considers thereportsofitscompensationconsultantstoassessthebonuspotentialofthenamedexecutiveofficersinlightoftotalcompensationpaidtocomparableexecutivepositionsintheindustry.

25

TheannualcashbonuspotentialineffectfollowingtheannualreviewofcompensationinJuneforeachnamedexecutiveofficerisshownbelow.Actualbonuspayoutsareproratedtoreflectchanges,ifany,tobonuspotentials during the year.

Annual Bonus Potential

2011 2012 2013

DavidB.Dillon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,500,000 $1,500,000 $1,500,000W.RodneyMcMullen* . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,000,000 $1,000,000 $1,000,000J.MichaelSchlotman . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 525,000 $ 550,000 $ 550,000KathleenS.Barclay** . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — $ 550,000 $ 550,000PaulW.Heldman . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 550,000 $ 550,000 $ 550,000MichaelL.Ellis*** . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — $ — $ 375,000

* Mr.McMullen’sannualbonuspotentialincreasedto$1,500,000effectivewithhispromotiontoCEOonJanuary1,2014.

** Ms.Barclaybecameanamedexecutiveofficerin2012.

*** Mr.Ellisbecameanamedexecutiveofficerin2013.Hisannualbonuspotentialincreasedto$750,000effectivewithhispromotiontoPresidentandCOOonJanuary1,2014.

Over time the Committee and our independent directors have placed an increased emphasis on our strategic plan bymaking the targetmore difficult to achieve. The bonus plan allows forminimal bonustobeearnedat relatively low levelsofperformance toprovide incentive for achievingevenhigher levelsof performance.

The amount of bonus that the named executive officers earn each year is determined by Kroger’sperformance compared to targets establishedby theCommittee andour independent directors basedonthebusinessplanadoptedbytheBoardofDirectors.In2013,one-thirdofthebonuswasbasedonatargetforidenticalsaleswithoutfuel;one-thirdwasbasedonatargetforEBITDAwithoutfuel;andone-thirdwasbasedonimplementationandresultsofasetofmeasuresunderourstrategicplan.Anadditional5%wouldbeearnedifKrogerachievedthreegoalswithrespecttoitssupermarketfueloperations:achievementofthetargetedfuelEBITDA,increaseofatleast3%intotalgallonssold, andachievementoftheplannednumberoffuel centers placed in service.

Following the close of the year, the Committee reviewed Kroger’s performance against the identical sales withoutfuel,EBITDAwithoutfuel,andstrategicplanobjectivesanddeterminedtheextenttowhichKrogerachievedthoseobjectives. Kroger’sEBITDAwithoutfuelfor2013was$4.245billionandKroger’sidenticalsaleswithout fuel for2013were3.5%. In2013,Kroger’s supermarket fuel EBITDAwas$232.990million,whichexceededthegoalof$184.875millionnecessarytoearnabonusforthefuelcomponent.Kroger’sfuelgallonsalesinsupermarketfuelcenterswere4.431billiongallons,or6.6%overtheprioryear.Weoperated1,240supermarketfuelcentersasoftheendof2013,exceedingourgoalof1,235centers.Asaresult,thepayoutpercentageincludedtheadditional5%fuelbonus.Duetoourperformancewhencomparedtothetargetsestablishedby theCommittee,andbasedon thebusinessplanadoptedby theBoardofDirectors,thenamedexecutiveofficersearned104.949%oftheirbonuspotentials.Thisisthesamebonuspercentagepayoutreceivedbyallotherparticipantsintheannualcorporatebonusplan.

26

The 2013 targets established by the Committee for annual bonus amounts based on identical saleswithoutfuelandEBITDAwithoutfuelresults,theactual2013results,andthebonuspercentageearnedineachofthecomponentsofnamedexecutiveofficerbonus,wereasfollows:

Targets

Component Minimum 100% Result Amount Earned

IdenticalSaleswithoutfuel . . . . . . . . . 1.6% 3.6% 3.5% 31.679%EBITDAwithoutfuel . . . . . . . . . . . . . . $3.583Billion $4.216Billion* $4.245Billion 34.474%StrategicPlan. . . . . . . . . . . . . . . . . . . . ** ** ** 33.796%FuelBonus . . . . . . . . . . . . . . . . . . . . . . [asdescribedinthetextabove] 5.000%Total Earned . . . . . . . . . . . . . . . . . . . . . 104.949%

* Payoutisat125%ifidenticalsalesgoalisachieved.

** The Strategic Plan component also was established by the Committee, but is not disclosed as it iscompetitively sensitive.

In2013,asinallyears,theCommitteeretaineddiscretiontoreducethebonuspayoutforallexecutiveofficers,includingthenamedexecutiveofficers,iftheCommitteedeterminedforanyreasonthatthebonuspayoutswerenotappropriate.TheindependentdirectorsretainedthatdiscretionfortheCEO’sbonus.Thosebodiesalsoretaineddiscretiontoadjustthetargetsundertheplanshouldunanticipateddevelopmentsariseduring theyear.Noadjustmentsweremade to the targets in2013.TheCommittee, and the independentdirectorsinthecaseoftheCEO,determinedthatthebonuspayoutsforthenamedexecutiveofficersshouldremain the same as other participants.

The percentage paid for 2013 represented excellent performance that exceeded our business planobjectives.Acomparisonofbonuspercentagesforthenamedexecutiveofficersinprioryearsdemonstratesthevariabilityofannualcashbonusincentivecompensation:

Fiscal Year Annual Cash Bonus

Percentage

2013 104.949%2012 85.881%2011 138.666%2010 53.868%2009 38.450%2008 104.948%2007 128.104%2006 141.118%2005 132.094%2004 55.174%

Theactualamountsofannualperformance-basedcashbonusespaidtothenamedexecutiveofficersfor2013arereported in theSummaryCompensationTableunder theheading“Non-Equity IncentivePlanCompensation” and footnote 4. These amounts represent the bonus potentials for each named executiveofficermultipliedbythe104.949%payoutpercentageearnedin2013.Innoeventcananyparticipantreceiveaperformance-basedannualcashbonusinexcessof$5,000,000.Themaximumamountthataparticipant,including each named executive officer, can earn is further limited to 200% of the participant’s bonuspotential amount.

Theperformance-basedannualcashbonusfor2014willbedeterminedbasedonKroger’sperformanceagainsttheidenticalsaleswithoutfuel,EBITDAwithoutfuel,strategicplan,andoperatingcostsasapercentageofsalesobjectivesestablishedbytheCommittee.Thefirstthreemetricswillbeweightedat30%eachandthefinalmetricwillbeweightedat10%.Theunderlyingstrategymetricshavebeenrevisedfromprioryearstofocusonshorter-termmeasures,asthelong-termbonusemphasizeslong-termperformance.The2014planalsoprovidesforanadditional5%payoutifourgoalsforsupermarketfuelEBITDA,supermarketfuelgallonssold,andtargetednumberoffuelcentersinoperationatthefiscalyearendareachieved.

27

l o N g -t e r M i N c e N t i v e S

TheCommitteebelievesintheimportanceofprovidinganincentivetothenamedexecutiveofficerstoachievethelong-termgoalsestablishedbytheBoardofDirectorsbyconditioningasignificantportionofcompensation on the achievement of those goals.

In 2006, theCommittee adopted the first in a series of long-termperformancebased compensationplansdesignedtorewardparticipantsfortheircontributiontothelong-termperformanceofKroger.Theseearlierplansprovidedforoverlappingfouryearperformanceperiodsthatallowedfortheearningofalong-termcashbonus.In2010,Kroger’slong-termincentiveprogramwasredesignedtocombinethetotalvalueofourlong-termcashbonusandequityprogramsintoacohesive,strategicrewardforeligibleexecutivesattheVicePresidentlevelandabove.Approximatelyfiftypercentoftheplanvalueisperformance-based,deliveredin cash and performance units, contingent on the achievement of certain strategic performance measures. Theotherfiftypercentofthevalueistime-basedanddeliveredinstockoptionsandrestrictedshares.Eachcomponentisdescribedinmoredetailbelow.

P e r F o r M a N c e B a S e d l o N g -t e r M c o M P e N S a t i o N

Thelong-termincentiveplanadoptedin2010(andearnedin2012)providesthemodelforourcombinedplan structure. Subsequent plans have been adopted each year thereafter. Each of these plans has thefollowing characteristics:

• Performanceismeasuredoverathreeyearperiod.

• Between130and170executives,includingthenamedexecutiveofficers,participateineachplan.

• Awardsincludebothcashandperformanceunits.

Ø Thecashbonusbaseequalstheexecutive’ssalaryattheendofthefiscalyearprecedingtheplanadoption date (or for those participants entering the plan after the commencement date, as of the dateofcommencingparticipationintheplan).

Ø A fixednumberofperformanceunits is awarded to eachparticipant. The awards arepaidoutin Kroger common shares, along with a cash amount equal to the dividends paid during theperformanceperiodonthenumberofissuedcommonshares.

• CompensationundertheplansisearnedbasedonourperformanceagainstmetricsestablishedbytheCommitteeatthebeginningoftheperformanceperiod.

• Thepayoutpercentage,basedontheextenttowhichtheperformancemetricsareachieved,isappliedtoboththebonusbaseandthenumberofperformanceunitsawarded.

• Actualpayoutscannotexceed100%of thecashbonusbaseor100%of thenumberofperformanceunits awarded.

• Innoeventcanacashbonusawardexceed$5,000,000.

28

Thefollowingtablesummarizeseachofthelong-termperformancebasedplansfortheyearsshown:

2011 Plan 2012 Plan 2013 Plan 2014 Plan

Performance Period 2011 to 2013 2012 to 2014 2013to2015 2014to2016

Payout Date March2014 March2015 March2016 March2017

Cash Bonus Base Salaryatendoffiscalyear2010*

Salaryatendoffiscalyear2011*

Salaryatendoffiscalyear2012*

Salaryatendoffiscalyear2013*

Performance Metrics

Strategic Plan 2%payoutperunitimprovement

2%payoutperunitimprovement

2%payoutperunitimprovement

2%payoutperunitimprovement

Reduction in Operating Cost as a Percentage of Sales, Excluding Fuel

0.50%payoutper0.01%reductioninoperating costsBaseline:27.60%

0.50%payoutper0.01%reductioninoperating costsBaseline:27.09%

0.50%payoutper0.01%reductioninoperating costsBaseline:26.69%

0.50%payoutper0.01%reductioninoperating costsBaseline:26.61%

Improvement in Associate Engagement

2%payoutperunitimprovement

4%payoutperunitimprovement

4%payoutperunitimprovement

4%payoutperunitimprovement

Return on Invested Capital

N/A N/A 1%payoutper0.01%improvement in ROIC Baseline:13.41%

1%payoutper0.01%improvement in ROICBaseline:13.43%

* Ordateofplanentry,iflater.

Atthetimeofadoptingnewlong-termplans,theCommitteehasmadeadjustmentstothepercentagepayouts for the components of the long-term plans to account for the increasing difficulty of achievingcompounded improvement.

The Committee anticipates adopting a new plan each year, measuring improvement over successive three-yearperiods.

Thelong-termperformancebasedplanadoptedin2011,whichmeasuredimprovementsthroughfiscalyear2013,paidoutinMarch2014andwascalculatedasfollows:

Component Baseline Result Improvement Multiplier Percentage

Earned

StrategicPlan. . . . . . . . . . . . . . . . . . . . . * * 6unitsofimprovement 2% 12.00%Associate Engagement . . . . . . . . . . . . . * * 8 units of improvement 2% 6.00%Operating Costs, as a Percentage of Sales,ExcludingFuel . . . . . . . . . . . . 27.60% 26.76% 84basispointimprovement 0.50% 42.00%

Total Earned . . . . . . . . . . . . . . . . . . . . . . 70.00%

* TheStrategicPlanandAssociateEngagementcomponentswereestablishedbytheCommitteebutarenot disclosed as they are competitively sensitive.

Accordingly,eachnamedexecutiveofficerreceivedcashinanamountequalto70.00%ofthatexecutive’slong-termcashbonusbase,andwas issued thenumberofKrogercommonsharesequal to70.00%of thenumberofperformanceunitsawardedtothatexecutive,alongwithacashamountequaltothedividendspaidonthatnumberofcommonsharesduringthethreeyearperformanceperiod.Payoutforthecashcomponentsofthe2011planarereportedinthe“Non-EquityIncentivePlanCompensation”and“AllOtherCompensation”columnsoftheSummaryCompensationTableandfootnotes4and6tothattable,andthecommonsharesissuedundertheplanarereportedintheOptionsExercisedandStockVestedTableandfootnote2tothattable.

29

Equity Awards