THE INSURANCE BILL 2014/15 - Chartered Insurance … · THE INSURANCE BILL 2014/15 ... remedied...

18

THE INSURANCE BILL 2014/15 CII NORTHERN IRELAND PRESENTATION 11 th December 2014 Alison Cassidy Aine Tyrrell Partners 028 90327388 [email protected] [email protected]

Transcript of THE INSURANCE BILL 2014/15 - Chartered Insurance … · THE INSURANCE BILL 2014/15 ... remedied...

THE INSURANCE BILL 2014/15

CII NORTHERN IRELAND

PRESENTATION 11th December 2014

Alison Cassidy

Aine Tyrrell

Partners

028 90327388

DISCUSSION POINTS

To outline the critical changes to the law for insurers:

(i) Pre-contractual duty of disclosure / fair

presentation

(ii) Proportionate remedies for breach

(iii) Effect of warranties

(iv) Insurer’s remedies for fraudulent claims

21ST CENTURY SOLUTIONS

‣ Existing regime founded on Marine Insurance Act 1906

‣ Judicial interpretation gave insured some “latitude”

“New” Regime

‣ Third Party (Rights Against Insurers) Act 2010

‣ Consumer Insurance (Disclosure & Representations) Act 2012 (CIDRA)

‣ Insurance Bill 2014/15

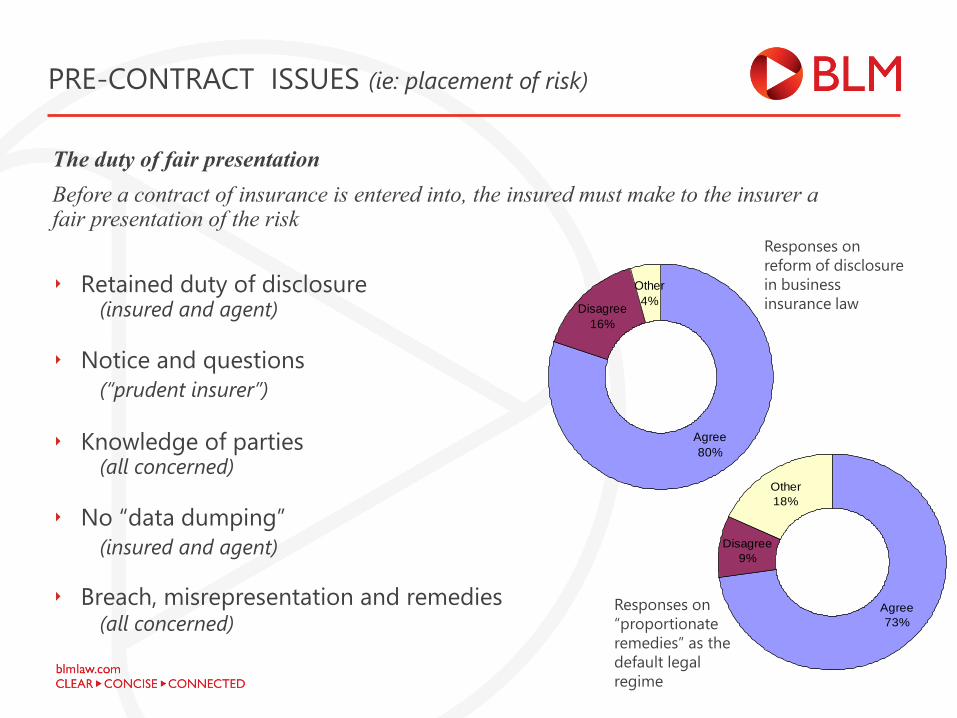

PRE-CONTRACT ISSUES (ie: placement of risk)

The duty of fair presentation

Before a contract of insurance is entered into, the insured must make to the insurer a fair presentation of the risk

‣ Retained duty of disclosure (insured and agent)

‣ Notice and questions (“prudent insurer”)

‣ Knowledge of parties (all concerned)

‣ No “data dumping” (insured and agent)

‣ Breach, misrepresentation and remedies (all concerned)

Agree

80%

Disagree

16%

Other

4%

Responses on

reform of disclosure

in business

insurance law

Agree

73%

Disagree

9%

Other

18%

Responses on

“proportionate

remedies” as the

default legal

regime

PROPORTIONATE REMEDIES (breach of “fair presentation”)

‣ Deliberate or reckless breach

‣ Breach neither deliberate nor

reckless, and if known:

• Insurer would not have

contracted

• Insurer would have contracted,

but on different terms

• Insurer would have contracted,

but at higher premium

‣ Avoidance (no need to return premium)

• Avoidance (must return premium)

• Apply relevant terms retrospectively

• Reduce claim proportionately

(averaging)

Remedy available Type of breach

ONCE COVER IS IN PLACE - WARRANTIES

CURRENT POSITION

‣ s33 and s34 of 1906 Act

‣ Express or implied

‣ Basis of contract clause – turn any representation made into a warranty

‣ Demand absolute compliance – even minor breaches which do not affect the risk or temporary breaches remedied before loss.

‣ Unpopular with courts

‣ Doctrine of “suspensive condition”

‣ Kler Knitwear v Lomnard General Insurance Co Ltd (2000)

Support for warranty reforms

Agree

88%

Other

7%

Disagree

5%

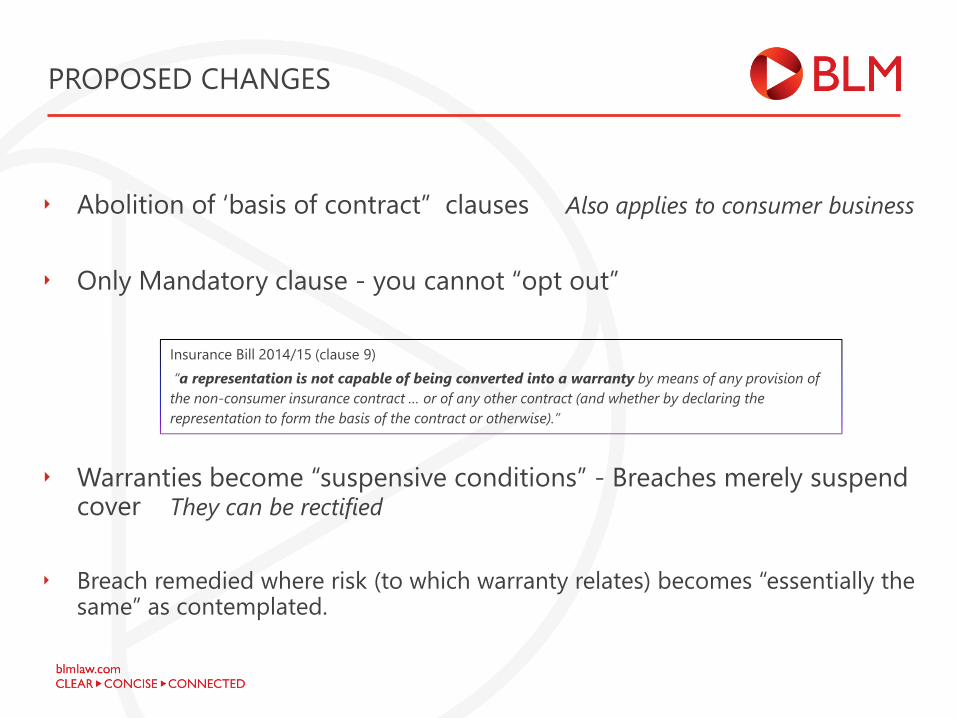

PROPOSED CHANGES

‣ Abolition of ‘basis of contract” clauses Also applies to consumer business

‣ Only Mandatory clause - you cannot “opt out”

‣ Warranties become “suspensive conditions” - Breaches merely suspend cover They can be rectified

‣ Breach remedied where risk (to which warranty relates) becomes “essentially the same” as contemplated.

Insurance Bill 2014/15 (clause 9)

“a representation is not capable of being converted into a warranty by means of any provision of

the non-consumer insurance contract … or of any other contract (and whether by declaring the

representation to form the basis of the contract or otherwise).”

LATE OMISSIONS? (for the time being, at least)

‣ Further restrictions on warranties

• Terms designed to reduce particular types of loss (e.g. burglar alarm)

• Evidence gathering in House of Lords completed 9TH December 2014

• Committee interested in “irrelevant warranties”

• May see a proposed amendment but will it be adopted?

“Controversial” issue among parts of the market:

INSURERS REMEDIES FOR FRAUDULENT CLAIMS

Current Position

‣ All encompassing fraud clause s 17 MIA

‣ Void policy from outset

‣ Unpopular with courts – reluctance to apply in practice

‣ Apply “contractual remedy” – no liability from date of fraudulent claim

‣ Uncertainty in approach to fraud claims

INSURERS REMEDIES FOR FRAUDULENT CLAIMS

New Proposals – Part 4 of Insurance Bill

‣ No definition of fraudulent claim

‣ Remedies are universal – apply to consumer and non-consumer

‣ Fraud – no liability to pay

‣ Codification of established legal principle that fraud taints entire claim

‣ May recover sums paid to insured

‣ Option to terminate policy from date of fraud, and

• Refuse claims from subsequent events

• Retain premium

• But claims from previous “genuine” events remain valid

‣ May “opt out” in favour of robust fraud policies

‣ Subject to “transparency” conditions of the Bill

THE FUTURE

A new statutory default (i.e. opt out) regime for all business insurance

‣ Reform will happen

‣ First & second reading in Lords in July 2014

‣ Lord Woolf chairs Special Public Bill Committee

‣ Written evidence to Lords by 27 November

‣ Evidence gathering completed 9thDecember

‣ Expected to complete by March 2015

‣ Likely commencement in q3 2016

‣ Effects, implications and reactions?

DEVELOPMENTS IN THE LEGAL LANDSCAPE FOR 2015

FUNDAMENTAL DISHONESTY

‣ Not an entirely new concept

‣ CPR r44.16 – “Orders for costs made against the claimant may be enforced to the full extent of such orders with the permission of the court where the claim is found on the balance of probabilities to be fundamentally dishonest”.

‣ Gosling v Screw Fix Direct Ltd (unreported, Cambridge County Court 29th March 2014)

‣ First finding of fundamental dishonesty

‣ Distinction between dishonesty that is fundamental to the claim, and dishonesty that is collateral or incidental

‣ Effect was that Claimant lost costs protection

‣ Criminal Justice and Courts Bill 2014-2015

IMPLICATIONS IN NORTHERN IRELAND?

‣ Hazlett v Robinson, Loughrey & Ussher [2014] QB NIQB 17

‣ Can claims be struck out for abuse of process?

‣ Discretion as to costs - Order 62 rule 3(3) of the Rules of the Court of Judicature (Northern Ireland) 1980

‣ Effect of Fairclough v Summers [2012] UKSC 26

‣ Possibility of future legislation in NI?

ASBESTOSIS CLAIMS UPDATE

‣ Carol McAuley as personal representative of the estate of William McCauley deceased v Harland & Wolff & Royal Mail [2014] NIQB 91 –

‣ First judgment from Mr Justice O’Hara on valuation of pleural plaques claims in NI since introduction of the Damages (Asbestos-Related Conditions) Act (NI) 2011

‣ £10,000 awarded

‣ Possibility of appeal?

RECENT SUPREME COURT DECISION

‣ McDonald (deceased)v National Grid Electricity plc [2014] UKSC 53 –

‣ Deceased employed as a lorry driver and was a ‘casual visitor’ to Battersea power station.

‣ Visited areas where lagging work was being done around twice a month.

‣ Diagnosed with mesothelioma and died in February 2014.

‣ Case dismissed at first instance, allowed in Court of Appeal. This judgment was upheld by the Supreme Court.

‣ No logical reason to exclude persons who were liable to exposure despite not working directly with asbestos.

![Insurance Bill [HL] · Insurance Bill [HL] Bill No 39 ... ‘warranties’ in an insurance contract, to avoid paying a claim. Under the current law, breach ... Chief amongst these](https://static.fdocuments.us/doc/165x107/5e9f687c807cb83220581c2e/insurance-bill-hl-insurance-bill-hl-bill-no-39-awarrantiesa-in-an-insurance.jpg)