THE INDIAN CEMENT INDUSTRY MYTHS VS. FACTS · THE INDIAN CEMENT INDUSTRY MYTHS VS. FACTS...

15

THE INDIAN CEMENT INDUSTRY MYTHS VS. FACTS Jagdeep Verma Holtec Consulting Pvt. Ltd., India

Transcript of THE INDIAN CEMENT INDUSTRY MYTHS VS. FACTS · THE INDIAN CEMENT INDUSTRY MYTHS VS. FACTS...

THE INDIAN CEMENT INDUSTRYMYTHS VS. FACTS

Jagdeep Verma

Holtec Consulting Pvt. Ltd., India

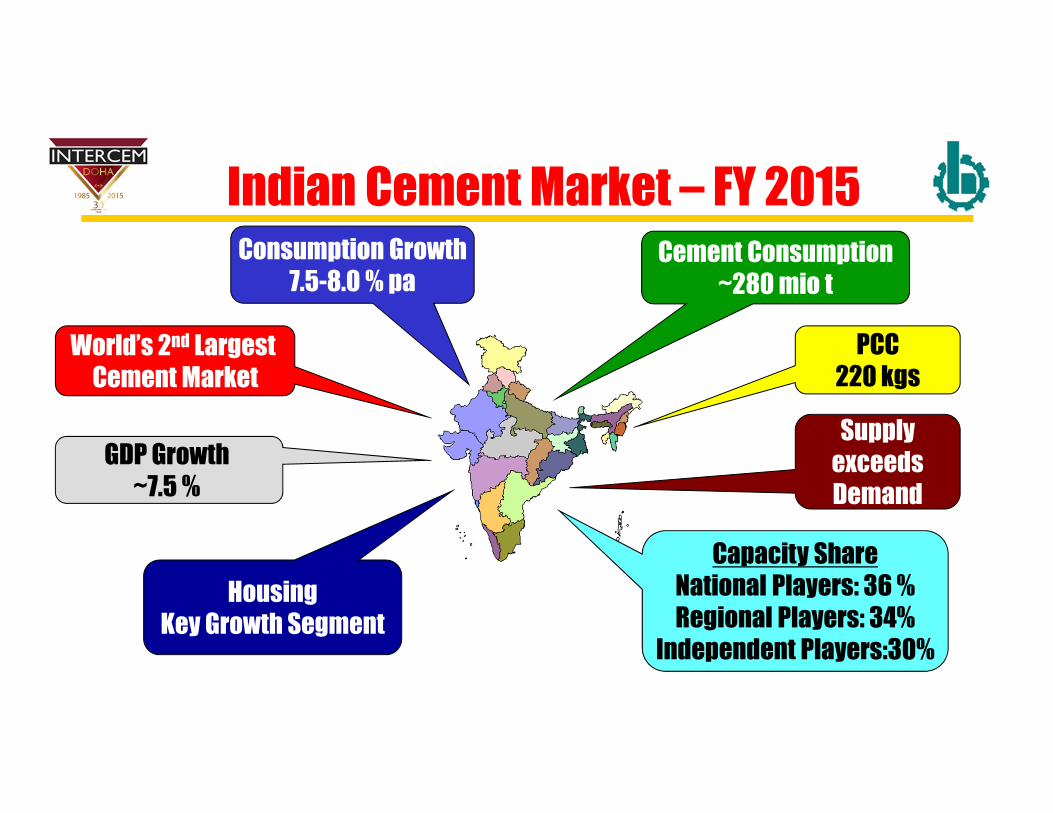

Indian Cement Market – FY 2015

World’s 2nd Largest Cement Market

Consumption Growth7.5-8.0 % pa

PCC220 kgs

Supply exceeds Demand

GDP Growth ~7.5 %

Housing Key Growth Segment

Capacity ShareNational Players: 36 %Regional Players: 34%

Independent Players:30%

Cement Consumption~280 mio t

200

250

300

350

400

450

500

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

Most Likely Pessimistic Optimistic

262

350

370

435 -485

208PCC 220 237 254 273 293 313 334

282

Demand

Over the period, we expect the CAGR of Demand to vary between 7.5 to 9.5 % between thePessimistic and Optimistic forecasts.

In theMost Likely case it is expected to be ~9%whichwould result in a PCC growth of 7 % pa.

mio t

262 282 307 335

365 398 432

468

337 358402

444 459 463 463 463

-

100

200

300

400

500

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

Demand Supply Capability

Demand & Supply Projectionsmio t Supply Capability assumed static at FY 19 level of 463 mio t

After trailing potential supply between FY 13-FY 20, demand could exceed supplybeyond FY 20, if fresh capacity expansion is not planned earlier.

*Refers to domestic supply (net of exports), assuming supply for any capacity added as 50% in Yr 1 & 100% from Yr2 onwards & 90% Cap. Util.Supply capability also accounts for possible plants’ closure – those that are very old, are not strategically located and have paucity of limestone.

*

0.077

0.072 0.070

0.063 0.063 0.063 0.062

0.050

0.055

0.060

0.065

0.070

0.075

0.080

FY 12 FY 13 FY 14 FY 15 FY 16 FY 17 FY 18

Myth 1: Industry Consolidation Herfindahl Index (HI) is a preferred metric to measure industry consolidation whenstudyingmarket price implications.

Herfindahl

Index

Our analysis shows, that if either of these three players desire to arrest the Index atits FY12 level, they would need to attain a capacity of ~ 245mio t by FY 18 (instead ofthe current estimated ~180mio t).

The index is seen to be fallingimplying a negative impact onprices.

To arrest this fall, the 3 largestplayers, singly or in tandem, haveto create/ acquiremore capacity.

6874

91111 108 101 106 116 111 104 113 121 130 139 150

106

109 113 115 117 119

-

2,500

5,000

7,500

10,000

0

50

100

150

200

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Prices in INR Past Price Optimistic Pessimistic Most Likely

US$/ t

Future Projections

9,000

7,000

INR/ t

� Fear that pricesmay fall due to prevalent demand-supply gap.

� Hypothesis tested by modeling and simulating the combined impact ofvarious variables on retail price. Over 40 variables evaluated.

� Prices in past have grown at 5-8% pa.

� Future prices likely to increase by around 6% pa.

Myth 2: Prices to Fall Sharply

After Demand -Supply, rising input materials’ prices have the most significant impact.

Myth 3: High Breakeven PointHypothesis tested by considering:

� Price points: US$ 106/ t (FY 2015 levels), US$ 112/ t (FY 2016 levels) & US$ 141 / t (FY 2020 levels).

� Specific Investing Cost/ t of OPC: US$ 130-135.

� Operational breakeven in 4th year of operations.

Price Breakeven

US$ 106/ t 48-50 %

US$ 112/ t 46-48 %

US$ 141/ t 43-45 %

In Case 3, after considering loan repayment, breakeven

seen to be ~ 70 %

Lower variable cost of production effected through improved,technologically-driven, energy efficiencies, falling cost of fuel and amuch higher volume of blended cement.

Myth 4: Imports to Reduce Prices

Cost of Production US$ 30-34 per t

900-1,300 NM

Cost of Production US$ 36-38 per t

2,000-4,000 NM

Landed Cost US$ 46-49/ t

Landed Cost US$ 59 -74/ t

Cost of Production in India US$ 35-37 per t

Bottlenecks hindering imports include ports infrastructure, domesticdistribution, market reach, competitiveness with domestic players, etc.

Low threat of imports and its impact on prices.

Myth 5: Blending Material ShortageFly ash

� Current flyash generation is around 100mio tpa.

� 45mio tpa of flyash is currently utilized by the cement industry.

� An additional 80 mio tpa could be available by FY 2016/2017 as against an

incremental requirement of 25mio tpa in next 4-5 years.

Slag

� Current slag generation is around 13mio tpa.

� 8-9mio tpa of slag is utilized by the cement industry.

� An additional 12 mio tpa could be available by FY 2016/ 2017 as against an

incremental requirement of 6-7 mio tpa in next 4-5 years.

Availability appears assured. Yet, advance booking of future strategically located sources being increasingly adopted.

-

10

20

30

40

2011

2016

2021

2026

2031

2033

2035

2036

2038

2041

2043

2045

2047

2049

Current product mix with current limestone

reserves

Increased exploitable limestone, 100 % blended

cement, lower growth rate

Myth 6: Limestone No Constraint

Need to secure deposits well in advance

Individual Deposit > 50 mio t

CaO > 42%45 bio t

Exploitable Reserves = 22 bio t

In Forest Land4 bio t

Statutorily Blocked19 bio t

Total Deposits = 50 bio t

Bn t

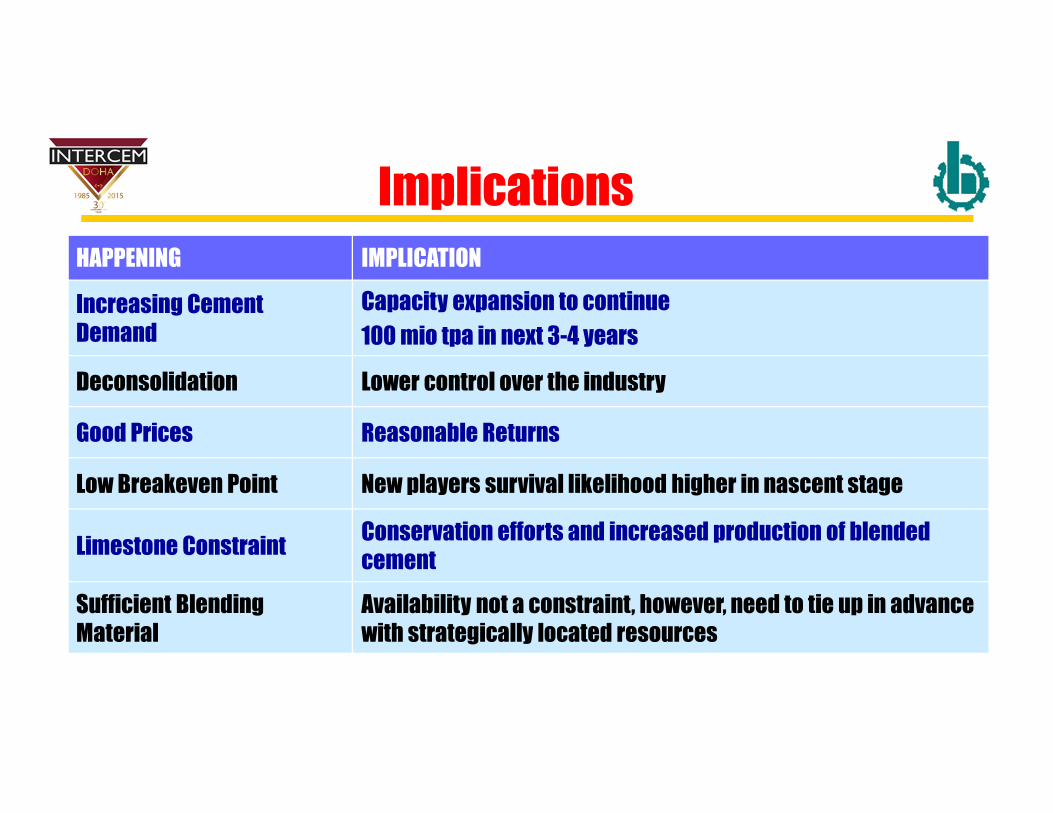

Implications

HAPPENING IMPLICATION

Increasing Cement Demand

Capacity expansion to continue

100 mio tpa in next 3-4 years

Deconsolidation Lower control over the industry

Good Prices Reasonable Returns

Low Breakeven Point New players survival likelihood higher in nascent stage

Limestone ConstraintConservation efforts and increased production of blended cement

Sufficient Blending Material

Availability not a constraint, however, need to tie up in advance with strategically located resources

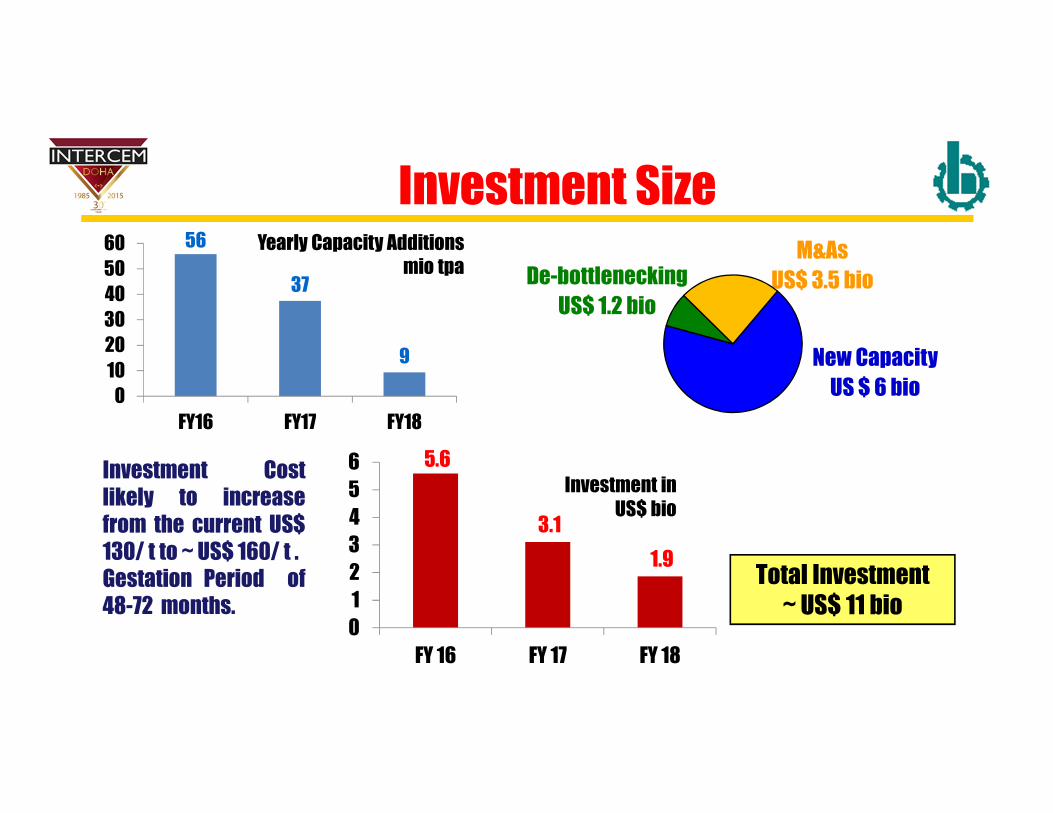

56

37

9

0

10

20

30

40

50

60

FY16 FY17 FY18

5.6

3.1

1.9

0

1

2

3

4

5

6

FY 16 FY 17 FY 18

Investment Size

Investment Costlikely to increasefrom the current US$130/ t to ~ US$ 160/ t .Gestation Period of48-72 months.

Total Investment ~ US$ 11 bio

De-bottlenecking

US$ 1.2 bio

M&As

US$ 3.5 bio

New Capacity

US $ 6 bio

Investment in US$ bio

Yearly Capacity Additions mio tpa

262 282 307 335

365 398 432

468

337 358402

444 459 463 463 463

-

100

200

300

400

500

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

Demand Supply Capability

Investment Timing

Demand exceeds Supply.

New expansion plans should be underway by FY 2016/ 17.

Substantial surplus capacity seen in FY 2016 - FY 2018… Valuation could be lower!

M&A could see 15-25 mio tpa exchanging hands.

Mio t Supply-Demand Comparison

Indian Cement Market – FY 2021

World’s 2nd Largest Cement Market

Consumption Growth7-10 % pa

PCC334 kgs

Supply ≈ Demand35-45 mio tpa

required annually FY22 onwards

GDP to remain robust

M&A 15-25 mio tpaUS$ 3.5 bio CAPEX Investment

~ US$ 7 bio

Cement Consumption468 mio t

Web : www.holtecnet.com

E-Mail : [email protected]

Address : Holtec Centre, A Block, Sushant Lok,

Gurgaon 122001 – India

Telephone : +91 - 124 - 238 5095, 404 7900

Facsimile : +91 - 124 - 238 5114, 238 5116

Thank youThank youThank youThank you