The Impact of The Sarbanes-Oxley Act of 2002: The ... · PDF fileThe Impact of The...

18

Financial Decisions, Summer 2007, Article 4 1 The Impact of The Sarbanes-Oxley Act of 2002: The Perspective of CFOs Zhuoming “Joe” Peng,* William P. Dukes ** and Ronald Bremer ** Western Oregon University * Rawls College of Business, Texas Tech University ** Abstract A survey that describes the impact of The Sarbanes-Oxley Act of 2002 from the perspective of CFOs of US publicly traded firms is summarized and discussed. The test result suggests that steeper costs of regulatory filings due to the compliance with the Act are the most likely reason for a firm to consider deregistering its shares with the SEC. The results of the survey indicate that some proper corporate governance practices envisioned by the Act were largely in place before its enactment. The very purpose of the Act is to restore and maintain investor confidence after the recent corporate scandals, and the cost of compliance with the Act is ongoing and considerable. The results of the survey should be of interest to individual investors, the investing public, the academic community, as well as policymakers. We thank an anonymous referee, Ronnie Clayton (the editor), Dean Crawford, William R. Pasewark, and seminar participants at the 2005 International Business and Economy Conference (IBEC) meetings, the 2005 Financial Management Association (FMA) meetings for comments and suggestions. All remaining errors are our own. This paper was initiated while the first author was at SUNY Oswego. 1. Introduction Congress passed the Sarbanes-Oxley Act of 2002 (SOX) in response to a wave of corporate scandals. The Act contains the most significant securities law changes since passage of the original federal securities laws in 1933 and 1934 in the wake of the Great Depression. Hence, SOX is the most comprehensive financial regulation reform in recent U.S. history and the most comprehensive legislation ever in the field of corporate governance. Before SOX, corporate governance was primarily the purview of state governments; however the enactment of the Act has made the governance structure of corporate America a matter of federal law. Many SOX provisions were aimed at solving specific deficiencies in corporate governance. Among other features, SOX created the Public Company Accounting Oversight Board (the PCAOB), an independent, non-profit body, funded by mandatory fees on public companies. It is the Chief Financial Officers (CFOs) who are on the firing line on a daily basis to strive for compliance with SOX. The Act has a profound impact on the structure of corporate governance of a public companies and how CFOs perform their duties. It increases the responsibility of the Chief Executive Officers (CEOs) and CFOs of public companies by requiring them to certify the

Transcript of The Impact of The Sarbanes-Oxley Act of 2002: The ... · PDF fileThe Impact of The...

Financial Decisions, Summer 2007, Article 4

1

The Impact of The Sarbanes-Oxley Act of 2002: The Perspective of CFOs

Zhuoming “Joe” Peng,* William P. Dukes** and Ronald Bremer**

Western Oregon University*

Rawls College of Business, Texas Tech University**

Abstract A survey that describes the impact of The Sarbanes-Oxley Act of 2002 from the perspective of CFOs of US publicly traded firms is summarized and discussed. The test result suggests that steeper costs of regulatory filings due to the compliance with the Act are the most likely reason for a firm to consider deregistering its shares with the SEC. The results of the survey indicate that some proper corporate governance practices envisioned by the Act were largely in place before its enactment. The very purpose of the Act is to restore and maintain investor confidence after the recent corporate scandals, and the cost of compliance with the Act is ongoing and considerable. The results of the survey should be of interest to individual investors, the investing public, the academic community, as well as policymakers. We thank an anonymous referee, Ronnie Clayton (the editor), Dean Crawford, William R. Pasewark, and seminar participants at the 2005 International Business and Economy Conference (IBEC) meetings, the 2005 Financial Management Association (FMA) meetings for comments and suggestions. All remaining errors are our own. This paper was initiated while the first author was at SUNY Oswego.

1. Introduction

Congress passed the Sarbanes-Oxley Act of 2002 (SOX) in response to a wave of corporate scandals. The Act contains the most significant securities law changes since passage of the original federal securities laws in 1933 and 1934 in the wake of the Great Depression. Hence, SOX is the most comprehensive financial regulation reform in recent U.S. history and the most comprehensive legislation ever in the field of corporate governance. Before SOX, corporate governance was primarily the purview of state governments; however the enactment of the Act has made the governance structure of corporate America a matter of federal law. Many SOX provisions were aimed at solving specific deficiencies in corporate governance. Among other features, SOX created the Public Company Accounting Oversight Board (the PCAOB), an independent, non-profit body, funded by mandatory fees on public companies.

It is the Chief Financial Officers (CFOs) who are on the firing line on a daily basis to strive for compliance with SOX. The Act has a profound impact on the structure of corporate governance of a public companies and how CFOs perform their duties. It increases the responsibility of the Chief Executive Officers (CEOs) and CFOs of public companies by requiring them to certify the

Financial Decisions, Summer 2007, Article 4

2

quarterly and annual financial statements submitted to the Securities Exchange Commission (SEC). It institutes criminal penalties that include significant monetary fines and/or imprisonment of up to 20 years for any CEO or CFO who knowingly and falsely certifies financial statements. Compliance with SOX appears to require expenditure of significant resources. According to one recent study released by the Financial Executives International (FEI) (2004), the cost to comply with SOX is estimated to be $2 million annually for some large companies. On one hand, the very purpose of SOX is to restore and maintain investor confidence after recent corporate scandals. On the other hand, the cost of compliance is ongoing for public companies. As indicated in Block (2004), the passage of SOX may cause more firms to become or remain private due to increased costs of regulatory filings pursuant to compliance with the Act. One major disadvantage of the separation of ownership and management in a corporation is that it may lead to agency conflicts between shareholders’ and managers’ objectives (Smith (1937) and Jensen and Meckling (1976)). How effective is the Act at preventing looting by corporate executives who manage a publicly traded company on behalf of its owners, the shareholders? Do the benefits that SOX provides outweigh the costs? The goal of this paper is to understand CFO perceptions of SOX in terms of their companies’ compliance with the Act and its impact on their businesses. The results should be of interest to individual investors, the investing public, the academic community, and policymakers. 2. An Overview of Major Provisions of Sox Pertaining to Corporate Governance1 The provisions to be investigated are primarily contained in Title III and Title IV of SOX. Sections 302, 404, and 906, establish specific and detailed financial reporting requirements for each public company. Section 302 requires that CEOs and CFOs personally certify that they have reviewed all the quarterly and annual reports filed with the SEC, and that in any of these reports (a) financial information is materially accurate and complete, (b) disclosure controls and procedures are maintained, and (c) adequacy of internal control over financial reporting is maintained. In addition, Section 302 requires both CEOs and CFOs to certify that the company discloses to its audit committee and external auditors any material weaknesses in internal controls and procedures that could adversely affect financial reporting, and publicly report any fraud involving management or internal control employees. Complementing Section 302, Section 404 requires that any annual report of a public company to include an internal control report which shall (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures for financial reporting; and (2) contain an assessment, as of the end of the company’s fiscal year, of the effectiveness of the internal control structure and procedures of the company for financial reporting.2 Section 906 amends the U.S. Criminal Code and adds a criminal provision. Under Section 906, the CEO and the CFO must certify that the financial statements and disclosures fully comply with provisions of the Securities Exchange Act and that they fairly present, in all material respects, the operations and financial condition of the company. Unlike Sections 302 and 404, Section 906 is within the jurisdiction of the Justice Department. Under Section 906, maximum penalties are a fine of not more than $5 million and/or imprisonment of up to 20 years of the CEO or the CFO for willful certification of the financial statements knowing that they do not fully comply with the requirements. However, the law has never been clear on the difference between a “knowing”

Financial Decisions, Summer 2007, Article 4

3

violation (up to $1 million fine and/or 10 years in prison) and a “willful” violation (up to $5 million fine and/or 20 years in prison.) Section 407 of the Act requires that publicly traded firms have audit committees composed entirely of independent directors and disclose whether at least one of the audit committee members is a financial expert.3 In addition, SOX requires that audit committees (i) have the authority to select, evaluate, compensate, and terminate their firms’ outside auditors, (ii) receive communications from auditors about key accounting issues, and (iii) establish procedures to process the complaints of whistleblowers. Section 406 of the Act requires that a public company disclose in its filings with the SEC whether the company has adopted a written code of ethics for its senior management, including the CEO, CFO, and principal accounting officer or controller. Section 403 of SOX amends Section 16(a) of the Securities Exchange Act of 1934 Act so that most insider trading transactions need to be filed electronically with the SEC within two business days.4 Any company maintaining a corporate website must post these filings on their sites by the end of the business day the filings are submitted to the SEC. 3. Data Descriptions The primary source of information for this paper is from an Internet-based survey. An email was sent on May 24, 2005 to 1,312 members of the Financial Executives International (FEI) requesting the CFOs’ participation in the survey. CFOs’ email addresses within the FEI database were found using the following three criteria: (1) the FEI member belongs to one local chapter of the FEI within the US; (2) the job title of the FEI member is either “Chief Financial Officer” or “CFO”; and (3) the FEI member is the CFO of a publicly traded company in the US. A generic username and password were provided in the email so that each CFO could complete the survey anonymously. A hyperlink was embedded in the email directing the CFO to a web page containing the survey. A beta test of the survey was conducted among MBA students and finance doctoral students before the email was sent. It took these students an average of 15 minutes to complete the survey. To maximize the response rate the recommendation of Graham and Harvey (2001) was followed and a second email was sent to the same FEI members on June 21, 2005.5

Eighty-three CFOs completed the survey giving a response rate of over 6 percent. Given that traditionally the response rate of any survey targeted to FEI members is low, a formal test of “nonresponse bias” of the sample is critical before any conclusion may be drawn from the survey results. The Global Industry Classification Standard (GICS) was used in the survey, and each CFO was asked to choose an industry sector in the GICS that best fits his/her company. Chi-Square goodness-of-fit tests were performed to determine whether the responses obtained in the sample represent the industry sectors and the market capitalizations in roughly the same proportion as those found in the Standard and Poor’s Research Insight population. Table 1 summarizes the counts for the number of industries represented in the sample and the Research Insight population. There is no significant difference in these distributions at the 5 percent level. Table 2 summarizes the counts for the number of companies in market capitalization categories represented in the sample and the Research Insight population. The Chi-Square goodness-of-fit test is significant due mainly to the firms with the smallest market capitalizations (less than $75 million) being under represented in the sample. There are 38.43 percent of the companies with

Financial Decisions, Summer 2007, Article 4

4

market capitalization less than $75 million in the Research Insight population, while only 14.46 percent in the sample. If the smallest firms are dropped from the test, the Chi-Square test is no longer significant (p-value = 0.156).

Financial Decisions, Summer 2007, Article 4

5

Table 1. Industries of the Survey Companies, the Corresponding Research

Insight Population, and Chi-Square Goodness of Fit Test

Which of the following industries best fits your company?

GICS Sectors Number of Firms in the Sample

Number of Firms in Research Insight Population

Consumer Discretionary 7 1287 Consumer Staples 2 282 Energy 4 371 Financials 18 1413 Health Care 8 1029 Industrials 11 950 Information Technology 15 1527 Materials 6 374 Telecommunication Services 3 170 Utilities 3 288 Other 6 752 Total 83 8443

Chi-Square test statistic = 7.444, DF = 10, p-value = 0.683

Table 2. Market Capitalization of the Survey Companies, the Corresponding Research Insight Population, and Chi-Square Goodness of Fit Tests

What is the best estimate of the market capitalization of your company?

Market Capitalization Number of Firms in the Sample

Number of Firms in Research Insight

Population < $75 million 12 2850 between $75 million and $700 million 34 2704 between $700 million and $1 billion 9 370 between $1 billion and $3 billion 13 806 between $3 billion and $10 billion 9 421 between $10 billion and $20 billion 5 143 > $20 billion 1 122 Total 83 7416

Chi-Square Test Including the Smallest Firms, Test statistic = 31.004, DF = 6, p-value < 0.01

Chi-Square Test without the Smallest Firms (< $75 million), Test statistic = 7.997, DF = 5, p-value = 0.156

One focus of the research is to assess CFOs’ opinions regarding whether the benefits provided by SOX to the investing public outweigh the ongoing cost of compliance to corporate America. If

Financial Decisions, Summer 2007, Article 4

6

larger firms have complaints about the added financial burden of the compliance, it is reasonable to infer that smaller firms may feel the burden even more. For instance, Greifeld (2006) argues that it is time to fix SOX so that small companies (with less than $128 million in market capitalizations) could be exempted from Section 404 of the Act. Even if larger firms feel the costs of compliance are reasonable, the smaller firms may not have the same opinion. Furthermore, it was a series of business scandals that occurred in large firms such as Enron, Tyco, WorldCom/MCI, and Adelphia that prompted Congress to pass the Act. As such, the fact that larger firms are represented more in the sample is not problematic. Graham and Harvey (2001, P. 189) states “large-sample studies often have weaknesses related to variable specification and the inability to ask qualitative questions.” Survey-based analysis appears to be an appropriate alternative if the sample fairly represents the underlying population. The discussion above motivates why the sample is unbiased and why it should give a meaningful picture of CFOs’ opinions and industry’s reaction to SOX.6 4. Survey Results 4a. Summary Statistics for Background Information on the Sample Firms

Table 3 presents background information on the companies in the sample. More than 80 percent of the firms are “accelerated filers,”7 and most of the firms use the calendar year-end as their fiscal year-end. According to SEC Rule 12g5-1, a public company with less than 300 shareholders as defined by the rule may be deregistered very easily if it chooses to do so. In the survey sample, only 12.05 percent (10 out of 83) of the firms have less than 300 shareholders. Most of the firms’ common stocks are listed either on NYSE or NASDAQ National Market.

Table 3. Background Information the Firms

Question: Is your company considered as an “accelerated filer” by the SEC? Response Yes No Missing Number of responses 66 16 1 Question: The ending date of your company’s fiscal year is ________. Ending Month: March April May June July September November December Count 5 2 2 3 3 3 1 63 Question: Your company’s common stock is listed on ______. Exchange: NYSE NASDAQ NASDAQ AMEX Other National Market Small Cap Market Count 39 36 3 2 3

Financial Decisions, Summer 2007, Article 4

7

4b. The Functions of the Audit Committees before the Enactment of SOX Section 301 of SOX requires that each member of the audit committee be a member of the board of directors and be independent of the management. It also requires that the audit committee be responsible for pre-approving all audit services provided by the auditor. As shown in Table 4, with 95 percent confidence, the true proportion of US firms that had an audit committee whose authority included hiring or firing the auditor or that the management needed the committee’s approval for auditor’s selection was between 44.10 percent and 66.34 percent before the enactment of SOX. After the Enron era’s financial debacle, there may have been a perception in the investing public that board members (at least those on an audit committee) had not been given the authority to guard shareholders’ wealth properly. The survey results do not support this perception. On the other hand, it could be the case that board members had the authority but failed to perform their fiduciary duty effectively.

Table 4. Some Summary Statistics of the Functions of the Audit

Committees before the Enactment of SOX

Yes No Total

The committee hired/fired the auditor. 46 37 83 A 95% confidence interval for the proportion of Audit Committees that hired/fired auditors is (0.4410, 0.6634)

The management needed the committee’s approval for auditor’s selection.

46 37 83

A 95% confidence interval for the proportion that indicated that management needed the committee’s approval for auditor’s selection is (0.4410, 0.6634)

The committee was involved in coordinating the audit or audit fee negotiation.

40 43 83

A 95% confidence interval for the proportion of audit committees that were involved in coordinating the audit or audit fee negotiation is (0.3708, 0.5944)

The committee was involved in other capacities. 34 49 83 A 95% confidence interval for the proportion of audit committees that were involved in other capacities is (0.3028, 0.5231)

4c. The Act’s Impact on Corporate America’s Governance Practices8

As summarized in Table 5, there is not a significant change in the following aspects of corporate governance practices due to the enactment of SOX:

(i) The size of the board of directors after the enactment compared to before. The average size of the boards is 8.43 before the enactment and it is 8.38 after.

(ii) The board’s independence in terms of the percentage of executive directors on the board after compared to before the enactment. The average is 20.46 percent before and it is 19.13 percent after.

Financial Decisions, Summer 2007, Article 4

8

(iii) The board’s independence in terms of the number of executive directors on the board after compared to before the enactment. The average is 1.65 before and it is 1.49 after.

(iv) The size of the audit committee after compared to before the enactment. The average is 3.56 before and it is 3.64 after.

Table 5. Makeup of the Board of Directors and Audit Committees

Number of Firms Before After Difference (After-Before)

Mean Std. Mean Std. Mean Std. P-value Paired t

Board Members 80 8.43 2.86 8.38 3.12 -0.04 1.58 0.805 Executive Directors on the Boards 80 1.65 1.02 1.49 0.66 -0.16 0.75 0.057*

Audit Committee Members 78 3.55 0.85 3.64 0.90 0.09 0.43 0.07 Note:

1. *Equivalent result when the proportion of the board of directors is considered. 2. An equivalent nonparametric test is performed for each corresponding paired t-test, and the results are

consistent with those reported in this table.

As summarized in Table 6, there is a significant change in the following aspects of corporate governance after the enactment of SOX compared to before:

(i) Sixty-eight of seventy-nine CFOs indicate that his/her company had an entirely independent audit committee before the enactment. With 95 percent confidence, the true proportion of US firms having an entirely independent audit committee before the enactment is between 76.45 percent and 92.84 percent. The Act requires that publicly traded firms have audit committees composed entirely of independent directors. The results suggest that more than two-thirds of the US firms were doing what SOX requires regarding audit committee independence before its enactment.

(ii) The SEC’s final rule pursuant to Section 407 of SOX requires that a company to disclose whether it has at least one "audit committee financial expert" serving on its audit committee. A company that does not have an audit committee financial expert must disclose this fact and explain why it has no such expert. The number of financial experts on the audit committee in the sample has significantly increased, at the 5 percent level, after the enactment compared to before. The average is 1.47 before and it is 1.70 after. It appears that the Act is effective in this regard, or, perhaps it would be more cumbersome for companies to explain to the SEC why they do not have an expert on the audit committee. One word of caution on our survey finding is appropriate. Before the enactment of SOX, a public company was not required to have a financial expert on the audit committee of its board. When we asked in the questionnaire how many financial experts were on the board before SOX, many CFOs might have reported the “official” number which would have been zero, however, companies may have “acquired” financial experts by coming across some board members who had the appropriate skills. As such, the statistically significant difference of the number of financial experts on the audit committee before and after the enactment reported in Table 6 is likely overstated.

(iii) The percentage of financial experts on the audit committees has significantly increased after compared to before the enactment. The average is 41.88 percent before and it is 47.84 percent after.

Financial Decisions, Summer 2007, Article 4

9

(iv) After the enactment, the SEC requires that each publicly traded company disclose whether it has adopted a code of ethics for its senior management, including the CEO, CFO, and principal accounting officer or controller. Eighty of the eighty-three CFOs answered the question and indicated that they have adopted a code of ethics. Out of these eighty CFOs fifty-seven of them (71.25%) indicated that his/her company had such a code of ethics in place before the enactment of SOX. With 95 percent confidence, the true proportion of US firms having a code of ethics for its senior management before the enactment is between 60.05 percent and 80.82 percent. This suggests that most of the US firms were doing what SOX expects with regard to the adoption of a code of ethics before its enactment.

Table 6. Audit Committee Independence, Code of Ethics Availability,

and Number of Financial Experts on the Audit Committee Panel A: Audit Committee Independence before the Enactment

Yes No Total Did the company have an entirely independent audit committee? 68 11 79

A 95% confidence interval for the proportion of US firms with an entirely independent audit committee before SOX is (0.7645, 0.9284)

Panel B: Code of Ethics Availability before the Enactment

Yes No Total Did the company have a written code of ethics that applied to senior management, including the CEO, CFO, and principal accounting officer or controller?

57 23 80

A 95% confidence interval for the proportion of US firms with a written code of ethics before SOX is (0.6005, 0.8082).

Panel C: Number of Financial Experts on the Audit Committee

Number of Firms Before After Difference (After-Before)

Mean Std. Mean Std. Mean Std. P-value Paired t

79 1.47 0.97 1.71 0.99 0.24 0.54 <0.01* Note:

1. *Equivalent result when the proportion of the financial experts on the audit committee is considered. 2. An equivalent nonparametric test is performed for the paired t-test, and the result is consistent with that

reported in the table.

4d. The Non-audit Services Provided by a Company’s Auditor before and after the Enactment Section 301 of SOX requires that any non-audit services provided by the auditor, for example, tax services, that are not prohibited by the Act and the SEC rules be pre-approved by the company’s audit committee. The results in Table 7 suggest that SOX is binding in this regard. There has been a significant decrease in proportion of American companies that ask its auditor to perform tax services (78.31 percent before and 57.83 percent after). With 95 percent confidence,

Financial Decisions, Summer 2007, Article 4

10

the percentage before the enactment minus the percentage after is between 6.64 percent and 34.32 percent. There is also a significant decrease of US firms that use its auditor to perform other non-audit services (40.96 percent before and 21.69 percent after). With 95 percent confidence, the percentage before the enactment minus the percentage after is between 5.47 percent and 33.08 percent.

Table 7. The Non-audit Services Provided by a Company’s

Auditor Before and After the Enactment

Before the Enactment After the Enactment

Tax Service

Other Non-Audit Service Tax

Service Other Non-

Audit Service

No Yes Total No Yes Total No 12 6 18 No 31 4 35 Yes 37 27 65 Yes 34 14 48

Total 49 34 83 Total 65 18 83 A 95% confidence interval of the proportion of the U.S. firms using the auditor for tax services Before the enactment minus the proportion After is (0.0664, 0.3432).

A 95% confidence interval of the proportion of the U.S. firms using the auditor for other non-audit services Before the enactment minus the proportion After is (0.0547, 0.3308).

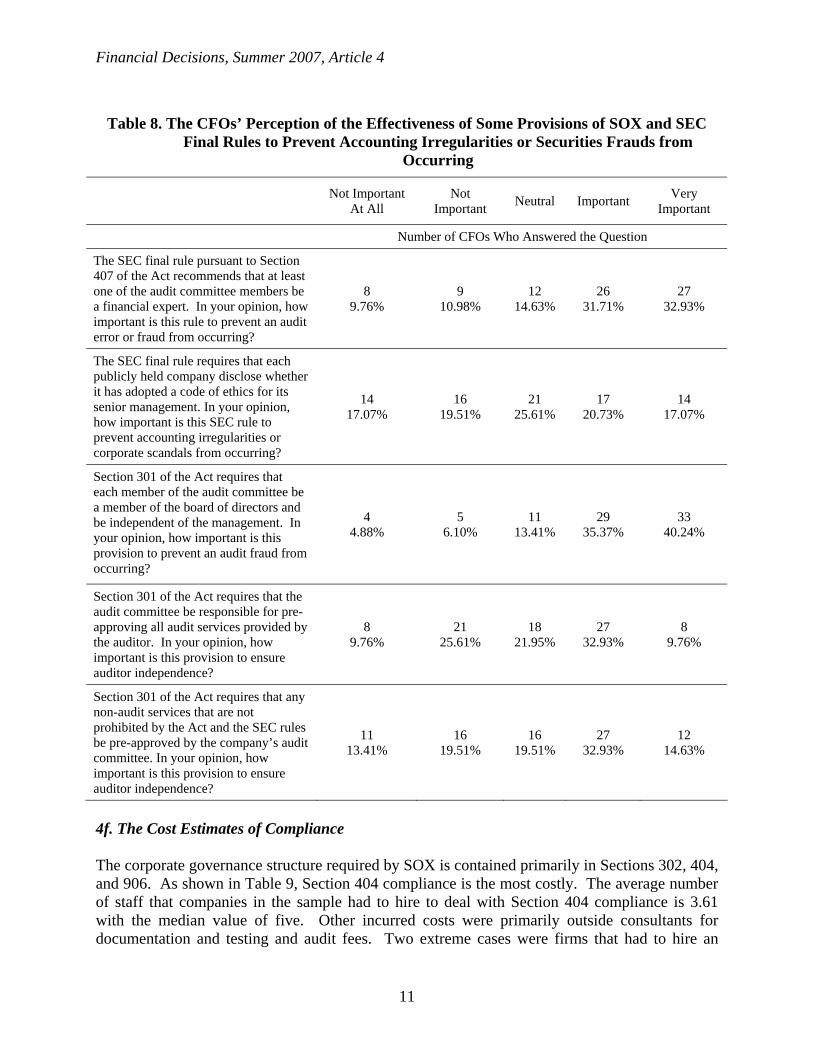

4e. The CFOs’ Perception of the Effectiveness of Some Provisions of SOX and SEC Final

Rules to Prevent Accounting Irregularities or Securities Frauds from Occurring Table 8 summarizes the results concerning questions regarding the CFOs’ perception of the effectiveness of some provisions of the Act and SEC final rules to prevent accounting irregularities or securities fraud from occurring. Over seventy-five percent of the CFOs in the sample indicated that an entirely independent and very powerful audit committee is an important or very important provision of the Act. Only 42.70 percent of the CFOs considered it important or very important that the audit committee pre-approve all audit services provided by the auditor. Sixty-four percent of the CFOs felt it was important or very important that at least one of the audit committee members be a financial expert as defined in Section 407 of SOX. The CFOs were equally split on the effectiveness of adopting codes of ethics for a company’s senior management to prevent accounting irregularities or securities frauds from occurring. That is, approximately 37 percent felt it was important or very important and 37 percent felt it was not important or not important at all. It should come as scant surprise that not many CFOs consider having codes of ethics important. For example, Peters (2004) indicated that there was a code of ethics for senior financial officers in Enron before its collapse. Verschoor (2004) and Bradford (2007) contend that having codes of ethics, the mainstay of the so-called “best practices”, is inadequate by itself to induce companies to be corporate good citizens.

Financial Decisions, Summer 2007, Article 4

11

Table 8. The CFOs’ Perception of the Effectiveness of Some Provisions of SOX and SEC

Final Rules to Prevent Accounting Irregularities or Securities Frauds from Occurring

Not Important At All

Not Important Neutral Important Very

Important

Number of CFOs Who Answered the Question

The SEC final rule pursuant to Section 407 of the Act recommends that at least one of the audit committee members be a financial expert. In your opinion, how important is this rule to prevent an audit error or fraud from occurring?

8 9.76%

9 10.98%

12 14.63%

26 31.71%

27 32.93%

The SEC final rule requires that each publicly held company disclose whether it has adopted a code of ethics for its senior management. In your opinion, how important is this SEC rule to prevent accounting irregularities or corporate scandals from occurring?

14 17.07%

16 19.51%

21 25.61%

17 20.73%

14 17.07%

Section 301 of the Act requires that each member of the audit committee be a member of the board of directors and be independent of the management. In your opinion, how important is this provision to prevent an audit fraud from occurring?

4 4.88%

5 6.10%

11 13.41%

29 35.37%

33 40.24%

Section 301 of the Act requires that the audit committee be responsible for pre-approving all audit services provided by the auditor. In your opinion, how important is this provision to ensure auditor independence?

8 9.76%

21 25.61%

18 21.95%

27 32.93%

8 9.76%

Section 301 of the Act requires that any non-audit services that are not prohibited by the Act and the SEC rules be pre-approved by the company’s audit committee. In your opinion, how important is this provision to ensure auditor independence?

11 13.41%

16 19.51%

16 19.51%

27 32.93%

12 14.63%

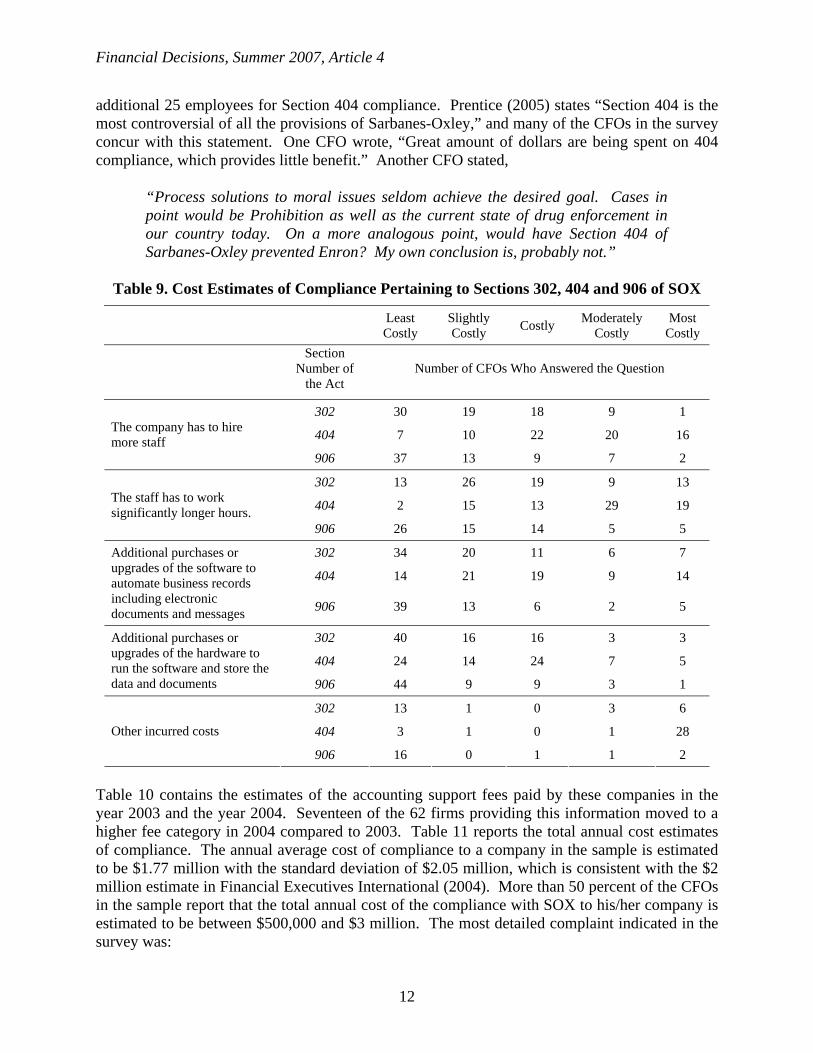

4f. The Cost Estimates of Compliance

The corporate governance structure required by SOX is contained primarily in Sections 302, 404, and 906. As shown in Table 9, Section 404 compliance is the most costly. The average number of staff that companies in the sample had to hire to deal with Section 404 compliance is 3.61 with the median value of five. Other incurred costs were primarily outside consultants for documentation and testing and audit fees. Two extreme cases were firms that had to hire an

Financial Decisions, Summer 2007, Article 4

12

additional 25 employees for Section 404 compliance. Prentice (2005) states “Section 404 is the most controversial of all the provisions of Sarbanes-Oxley,” and many of the CFOs in the survey concur with this statement. One CFO wrote, “Great amount of dollars are being spent on 404 compliance, which provides little benefit.” Another CFO stated,

“Process solutions to moral issues seldom achieve the desired goal. Cases in point would be Prohibition as well as the current state of drug enforcement in our country today. On a more analogous point, would have Section 404 of Sarbanes-Oxley prevented Enron? My own conclusion is, probably not.”

Table 9. Cost Estimates of Compliance Pertaining to Sections 302, 404 and 906 of SOX

Least Costly

Slightly Costly Costly Moderately

Costly Most

Costly

Section

Number of the Act

Number of CFOs Who Answered the Question

302 30 19 18 9 1

404 7 10 22 20 16 The company has to hire more staff

906 37 13 9 7 2

302 13 26 19 9 13

404 2 15 13 29 19 The staff has to work significantly longer hours.

906 26 15 14 5 5

302 34 20 11 6 7

404 14 21 19 9 14

Additional purchases or upgrades of the software to automate business records including electronic documents and messages 906 39 13 6 2 5

302 40 16 16 3 3

404 24 14 24 7 5

Additional purchases or upgrades of the hardware to run the software and store the data and documents 906 44 9 9 3 1

302 13 1 0 3 6

404 3 1 0 1 28 Other incurred costs

906 16 0 1 1 2

Table 10 contains the estimates of the accounting support fees paid by these companies in the year 2003 and the year 2004. Seventeen of the 62 firms providing this information moved to a higher fee category in 2004 compared to 2003. Table 11 reports the total annual cost estimates of compliance. The annual average cost of compliance to a company in the sample is estimated to be $1.77 million with the standard deviation of $2.05 million, which is consistent with the $2 million estimate in Financial Executives International (2004). More than 50 percent of the CFOs in the sample report that the total annual cost of the compliance with SOX to his/her company is estimated to be between $500,000 and $3 million. The most detailed complaint indicated in the survey was:

Financial Decisions, Summer 2007, Article 4

13

“This Act was horribly overreaching. It is costly, and there is very little/absolutely no cost benefit relationship. The Act and, specifically, the Section 404 requirements, will do little, if anything, to deter the "crimes"/"irregularities" it was intended to deter/preclude. Management override is the biggest issue, and the Section 404 requirements hardly address that issue. It is a complete waste of time and money. PCAOB is ineffective, at best. Their "investigations" of the Big 4 firms is a joke, and the Big 4 firms do not know what to do or how to do it in complying with the Section 404 audits. They (the Big 4 firms) gouged "corporate America" in the purported "audits" of the control environments, using no/very little professional judgment in the conduct of their examinations. And I spent over 30 years with a Big 4 firm, including over 20 as a partner.”

Table 10. Accounting Support Fees Paid in 2003 and 2004 2004

2003 $0 $1-$500 $501-$1,000

$1,001-$5,000

$5,001-$10,000

$10,001-$50,000 >$50,000 Total Counts

in 2003 $0 2 0 1 1 1 0 0 5 $1-$500 0 8 1 1 0 0 0 10 $501-$1,000 0 0 5 2 0 0 0 7 $1,001-$5,000 0 0 0 16 1 1 0 18 $5,001-$10,000 0 0 0 0 6 1 0 7 $10,001-$50,000 0 0 0 0 0 13 1 14 >$50,000 0 0 0 0 0 0 1 1 Total Counts in 2004 2 8 7 20 8 15 2 62

Table 11. The Total Annual Cost Estimates of Compliance

Total Annual Cost Number of Firms

Percentage of Firms

< $100,000 2 2.56% between $100,000 and $500,000 20 25.64 between $500,000 and $1 million 24 30.77 between $1 million and $3 million 17 21.79 between $3 million and $5 million 10 12.82 between $5 million and $10 million 4 5.13 > $10 million 1 1.28

Total 78 100%

The approximate average and standard deviation is $1.77 million and $2.05 million, respectively.

The CFOs were asked to rank the likelihood of each of a list of items as a possible reason for the company to consider delisting its common stock, that is to say, to terminate its stock registration with the SEC. Most of the items on the list are given in Brigham and Ehrhardt (2005, P. 651-652) as disadvantages of operating the business as a public company. The results of nonparametric comparison of median rankings, summarized in Table 12, indicate that Item f), “steeper costs of regulatory filings pursuant to compliance with the Act,” has a median response

Financial Decisions, Summer 2007, Article 4

14

that is statistically larger than the median response of the other items, making it the reason with the largest likelihood for a publicly traded firm to terminate its stock registration with the SEC. Publicly traded firms need to pay for D&O insurance,9 stock exchange listing fees, audit fees, and legal fees. It appears that the ongoing cost of the compliance with SOX may constitute another financial burden of being a public company.

Table 12. Possible Reasons of Terminating the Stock Registration with the

SEC

Five-Point Likert Scale

Least Likely 1 2 3 4

Most Likely 5

Total Number of Rankings a) Unexpected early debt repayment request 65 6 2 0 1

b) Self-dealings 65 5 2 2 0 c) Inactive market/low stock price 38 7 10 6 14 d) Control 40 7 13 7 7 e) Investor relations 44 12 13 2 2 f) Steeper costs of regulatory filings pursuant to compliance with the Act 18 7 5 20 20

Wilcoxon Signed Rank Test: f-a, f-b, f-c, f-d, f-e Test of median = 0.000 versus median > 0.000

N N* Test Wilcoxon Statistic

Estimated P-value

Median

f-a 73 10 54 1480.5 0.000 2.000 f-b 73 10 54 1473.0 0.000 2.000 f-c 74 9 48 1005.0 0.000 1.000 f-d 73 10 52 1226.0 0.000 1.000 f-e 72 11 47 1121.5 0.000 1.500

* denotes for missing values.

4g. Do the Benefits of SOX Outweigh the Cost?

The CFOs were asked whether they agree that the benefits of SOX outweigh the cost to corporate America. The results are summarized in Table 13. Approximately 60 percent of the CFOs either strongly disagree or disagree, and approximately 27 percent of the CFOs either agree or strongly agree. It is noteworthy that each of the 32 CFOs who strongly disagree provided an explanation as to why he/she held such a view, but none of the seven CFOs who strongly agree provided any explanation at all.

Financial Decisions, Summer 2007, Article 4

15

Table 13. CFOs’ Overall Perception of SOX

Do the benefits of SOX provided to the investing public outweigh the cost to corporate America?

Number of Firms

Percentage of the Firms

Strongly Disagree 32 40.51% Disagree 17 21.52 Neutral 9 11.39 Agree 14 17.72 Strongly Agree 7 8.86 Total 79 100%

5. Conclusions

A survey that describes the impact of The Sarbanes-Oxley Act of 2002 from the perspective of CFOs of US publicly traded firms is summarized and discussed. The results indicate that the true proportion of US firms that had an audit committee whose authority included hiring or firing the auditor or that the management needed the committee’s approval for auditor’s selection was between 44.10 percent and 66.34 percent before the enactment of the Act. After the Enron era’s financial debacle, there may have been a perception in the investing public that board members (at least those on an audit committee) had not been given the authority to guard shareholders’ wealth properly. The results tend not to support this perception. However, it could be the case that board members had the authority but failed to perform their fiduciary duty effectively. Furthermore, it is found that there is not a significant change in the following aspects of corporate governance practices due to the enactment of the Act: (i) The size of the board of directors after the enactment compared to before; (ii) The board independence in terms of the percentage of executive directors on the board after SOX compared to before the enactment; (iii) The board independence in terms of the number of executive directors on the board after SOX compared to before the enactment; and (iv) The size of the audit committee after the enactment compared to before. The results of the research indicate that some of the proper corporate governance practices envisioned by SOX were largely in place before the enactment. What is unknown is the reason why they had been in place.

The estimated annual average cost of the compliance with SOX to a company is estimated to be $1.77 million with the standard deviation of $2.05 million. More than 50 percent of the CFOs reported that the total annual cost of the compliance with SOX to his/her firm is estimated to be between $500,000 and $3 million. The most likely reason, indicated by the CFOs, that a publicly traded firm would consider deregistering its shares with the SEC was steeper costs of regulatory filings pursuant to compliance with SOX. The ongoing cost of compliance with the Act constitutes another financial burden placed on public companies. Approximately 60 percent of the CFOs either strongly disagree or disagree that the benefits provided by the Act outweigh the cost, while approximately 27 percent of them either agree or strongly agree.

Financial Decisions, Summer 2007, Article 4

16

On the one hand, the very purpose of SOX is to restore and maintain investor confidence after the recent corporate scandals. On the other hand, the cost of compliance with SOX is ongoing and considerable to public companies. Do the benefits provided by SOX outweigh the costs? The results of this paper shed light on CFOs’ view with regard to this question indicate that the benefits are perceived to fall far short of the costs.

Financial Decisions, Summer 2007, Article 4

17

References Block, S. B. (2004). The latest movement to going private: An empirical study. Journal of

Applied Finance, 14(1), 36-44. Bradford, W. C. (2007). Because That’s Where the Money Is: Toward a Theory and Strategy of

Corporate Legal Compliance. SSRN Working Paper. Available at http://ssrn.com/abstract=955428.

Brigham, E. F., and Ehrhardt, M., C. (2005). Financial management: Theory and practice, 11th

edition. Mason, Ohio: South-Western. Financial Executives International. (2004). Various commentaries regarding the Sarbanes-Oxley

Act of 2002 on the organization’s website. Available at http://www.fei.org and accessible with membership ID and password.

Geiger, M. A., and Taylor, P. L. (2003). CEO and CFO certifications of financial information.

Accounting Horizons, 17(4), 357-368. Graham, J. R., and Harvey, C. R. (2001). The Theory and Practice of Corporate Finance:

Evidence from the Field. Journal of Financial Economics, 60, 187-243. Greifeld, B. (2006). “It’s Time to Pull Up Our SOX.” Wall Street Journal, March 6, A14, col. 2. Jensen, M. C., and Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency

costs and ownership structure. Journal of Financial Economics, 3, 305-360. Peters, A. (2004). Will the New Rules Guarantee “Good” Governance and Avoid Future

Scandals? Nova Law Review 28, 283-292. Prentice, R. (2005). Student Guide to the Sarbanes-Oxley Act. Mason, Ohio: Thomson

Publishing. Smith, A. (1937). The wealth of nations. New York: Random House, Modern Library Edition. Trahan, E. A., and Gitman, L. J. (1995). Bridging the Theory-Practice Gap in Corporate Finance:

A Survey of Chief Financial Officers. Quarterly Review of Economics and Finance, 35, 73-87.

U.S. House of Representatives, Committee on financial services. (2002). Sarbanes-Oxley Act of

2002. Public Law No. 107-204. Washington, D.C.: Government Printing Office. Verschoor, C. C. (2004). Will Sarbanes-Oxley Improve Ethics? Strategic Finance, 85(9), 15-16.

Financial Decisions, Summer 2007, Article 4

18

Endnotes 1 Some of the discussions in this section draw from Prentice (2005) and Geiger and Taylor

(2003). 2 The Foreign Corrupt Practices Act of 1977 (FCPA) required public companies to institute

effective internal accounting control systems to prevent these companies from paying bribes to foreign government officials. Section 404 of the SOX focuses on internal financial controls so that the information presented in the financial statements of public companies is reliable.

3 The SEC’s final rule regarding the definition of an “Audit Committee Financial Expert” is

available on its website at http://www.sec.gov/rules/final/33-8177.htm#footnote_14. 4 Section 16(a) of the Securities Exchange Act of 1934 required insiders, which includes officers,

directors, and holders of 10 percent of a company’s common stock, file reports with the SEC regarding their insider trading transactions. Most of these transactions did not have to be filed until the tenth day of the month following the month when the transactions had occurred.

5 For individuals interested in reading the questionnaire and/or the two emails sent to the FEI

members, please contact the first author. 6 Not every empirical study using the data obtained from survey methodologies tests the

“nonresponse bias” of the data. For example, in Trahan and Gitman (1995, P. 75) they stated, “As is typical of descriptive surveys, the grant of anonymity to respondents was deemed more important than testing for nonresponse bias.”

7 The SEC considers a firm (among other factors) as an “accelerated filer” if its market

capitalization is greater than $75 million. 8 The Act was enacted in June 2002. However, it is likely that some companies might have

changed their corporate governance practices or structures ahead of the Act’s enactment in anticipation that the legislation would become law. Therefore, in the survey’s questionnaire, we ask CFOs to provide the information regarding the pertinent changes made either before or after, whichever is applicable, of the enactment of SOX.

9 D&O insurance protects directors and officers of a corporation from liability claims arising out

of alleged errors in judgment, breaches in duty and wrongful acts related to the company’s activities.

![Impact Sarbanes Oxley Act Security 1344[1]](https://static.fdocuments.us/doc/165x107/577d33c11a28ab3a6b8ba601/impact-sarbanes-oxley-act-security-13441.jpg)