The impact of the EU ETS on European energy and carbon markets · The impact of the EU ETS on...

34

The impact of the EU ETS on European energy and carbon markets David Newbery Danish Environmental Economic Conference Skodsborg Hotel 23 August 2010 http://www.eprg.group.cam.ac. uk

Transcript of The impact of the EU ETS on European energy and carbon markets · The impact of the EU ETS on...

The impact of the EU ETS on European energy and carbon markets

David Newbery

Danish Environmental Economic ConferenceSkodsborg Hotel 23 August 2010

http://www.eprg.group.cam.ac. uk

D Newbery Copenhagen 2010 2

Outline• Climate Change Challenge

– more carbon underground than we should release

– Kyoto then ETS sets targets

• The logic of EU targets

• GHG targets and the EU ETS

• EU 20-20-20 Directive and ETS

• R&D andEU SET Plan

D Newbery Copenhagen 2010 3

Climate change challenges

• World should not release all C from fossil fuels

• Climate policy risks depressing fossil fuel prices– unless CCS on major scale?

• How best to limit cumulative GHG release?– Limits on annual emissions or scarcity GHG price

related to remaining absorptive capacity?

– Kyoto sets emissions targets not a carbon price

• EU ETS as response to emissions targets

Ambitious target of 80% reduction by 2050

MR Allen et al. Nature 458, 1163-1166(2009)doi:10.1038/nature08019

Peak CO2-warming vs cumulative emissions 1750–2500

Now

Proven L H

Unconventional oil +gas

Resource

If we want a 50% chance of lessthan 2oC rise we can only useanother 500 Gt C ever!

D Newbery Copenhagen 2010 5

The logic of EU targets

• easy to determine “fair” allocation– and can buy off opponents with free allocations

• does not impinge on sovereign tax powers– EU carbon tax failed

• easier to give impression of leadership/action– without spelling out costs

– ETS => electricity prices ⇑ unanticipated by voters

Targets should be translated into sensible policy

6

EUA price October 2004-April 2010

0

5

10

15

20

25

30

35

Oct-04 Apr-05 Sep-05 Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09 Mar-10

Eur

o/t

CO

2

Futures Dec 2007OTC IndexSecond period Dec 2008Second period next DecCER 09

start of ETS

Second period

CO2 prices are volatile and now too low

Actual emissions revealed

D Newbery Copenhagen 2010 7

Effect of quota driven ETS

• Scarcity of EUAs determines EUA price– rather than long-run view of required carbon price

• Fuel cost + EUA of marginal plant sets electricity price

• When coal and gas competitive in electricity market

– EUA price set by coal-gas relative price

=> coal and gas-fired plant costs move together

Lax quantity target keeps coal competitive

Discourages greater CO2 reduction

D Newbery Copenhagen 2010 8NETA\Pxdata\fuel_choice

Fuel choices in UK electricity generation, 2000-10

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

0 2 4 6 8 10 12 14 16 18 20 22

Coal price Euros/MWht

Gas

pric

e E

uros

/MW

ht

Fuel post ETS

fuel pre-ETS

fuel +EUA cost Phase I

fuel + EUA Phase II

Gas cheaper than coal

Coal cheaper than gas

Coal 38%, gas 50%

Coal 34%, gas 55%

EUAs can make coal and gas competitive in GB

D Newbery Copenhagen 2010 9

UK price movements: 2007 to 2009 in €

0

20

40

60

80

100

120

1-Ja

n-07

1-Apr-

07

1-Ju

l-07

1-Oct

-07

1-Ja

n-08

1-Apr

-08

1-Ju

l-08

1-O

ct-0

8

1-Jan

-09

€/M

Wh

e

Electricity forward 2010 (€/MWh)

Gas cost forward (2010) + EUA

Coal cost forward (2010) + EUA

EUA price in €/tCO2

Correlation of coal+EUA on gas+EUA high at 96%Source: Bloomberg data

D Newbery Copenhagen 2010 10

Collapse in EUA price impacts electricity pricesForward base year contracts - France and Germany Aug 2005-May 2006

0

10

20

30

40

50

60

70

29-Aug-05

13-Sep-05

28-Sep-05

13-Oct-05

28-Oct-05

12-Nov-05

27-Nov-05

12-Dec-05

27-Dec-05

11-Jan-06

26-Jan-06

10-Feb-06

25-Feb-06

12-Mar-06

27-Mar-06

11-Apr-06

26-Apr-06

11-May-

06

Eur

os/M

Wh

FR base 2007

DE base 2007

EUA coalcost

EUA gas cost

Source: EEX

D Newbery Copenhagen 2010 11

But not price less EUA cost => EUA directly feeds through to electricity price

Forward 2007 annual prices - France and Germany 2006

0

10

20

30

40

50

60

70

80

90

1-Ja

n-06

16-Ja

n-06

31-Ja

n-06

15-F

eb-06

2-Mar

-06

17-M

ar-06

1-Apr-0

6

16-A

pr-06

1-May

-06

16-M

ay-06

Eur

os/M

Wh

FR peak less gasEUA

DE peak less gasEUA

FR base less gasEUA

DE base less gasEUA

DE base less coalEUA

coal EUA cost

EUA cost inCCGT

Source: EEX

D Newbery Copenhagen 2010 12

Rise in gas price shifts generation into coalWeekday moving 24 hr av coal and gas generation Britain 1 Oct-9 Dec 05

0

100

200

300

400

500

600

700

800

900

3-Oct-

055-

Oct-05

6-Oct-

0510

-Oct-

0512

-Oct-

0514

-Oct-

0517

-Oct-

0519

-Oct-

0521

-Oct-

0525

-Oct-

0526

-Oct-

0528

-Oct-

051-

Nov-0

53-

Nov-0

54-

Nov-0

58-

Nov-0

510

-Nov

-05

14-N

ov-0

515

-Nov

-05

17-N

ov-0

521

-Nov

-05

23-N

ov-0

524

-Nov

-05

28-N

ov-0

530

-Nov

-05

2-Dec

-05

5-Dec

-05

7-Dec

-05

9-Dec

-05

GW

h/24

hou

rs

0

10

20

30

40

50

60

70

80

90

£/M

Whe

gas output

coal output

gas cost + EUA

Source: NGT

D Newbery Copenhagen 2010 13

Impact on gas market

• Suppose gas price increases– initially: demand falls (fuel switch gas => coal)

=> demand for EUAs rises => EUA price ⇑

=> partially offsets advantage of coal

=> offsets some demand reduction for gas

=> reduces elasticity of demand for gas, ε– Lerner Index (p-c)/p = 1/ε=> increases market power of gas suppliers

• Gazprom, and suppliers with protected markets

Bad idea

D Newbery Copenhagen 2010 14

Demand for gas

Demand for gas in ESI

Priceof Gasg

Price rise

Initial demand fall (gas-coal)

EUA price rise induces someswitch back to gas

Demand for gas if EUA price constant

Demand for gas if EUA price varies

D Newbery Copenhagen 2010 15

Policy implications

• Imposing extra constraint on market reduces demand elasticities, amplifies market power

• If the price of EUAs is independent of gas demand then there is no multiplier effect=> banking over longer periods helps

• Other reasons for fixing C-price, not quantity:

Prices vs Quantities (Weitzman, 1974)

D Newbery Copenhagen 2010 16

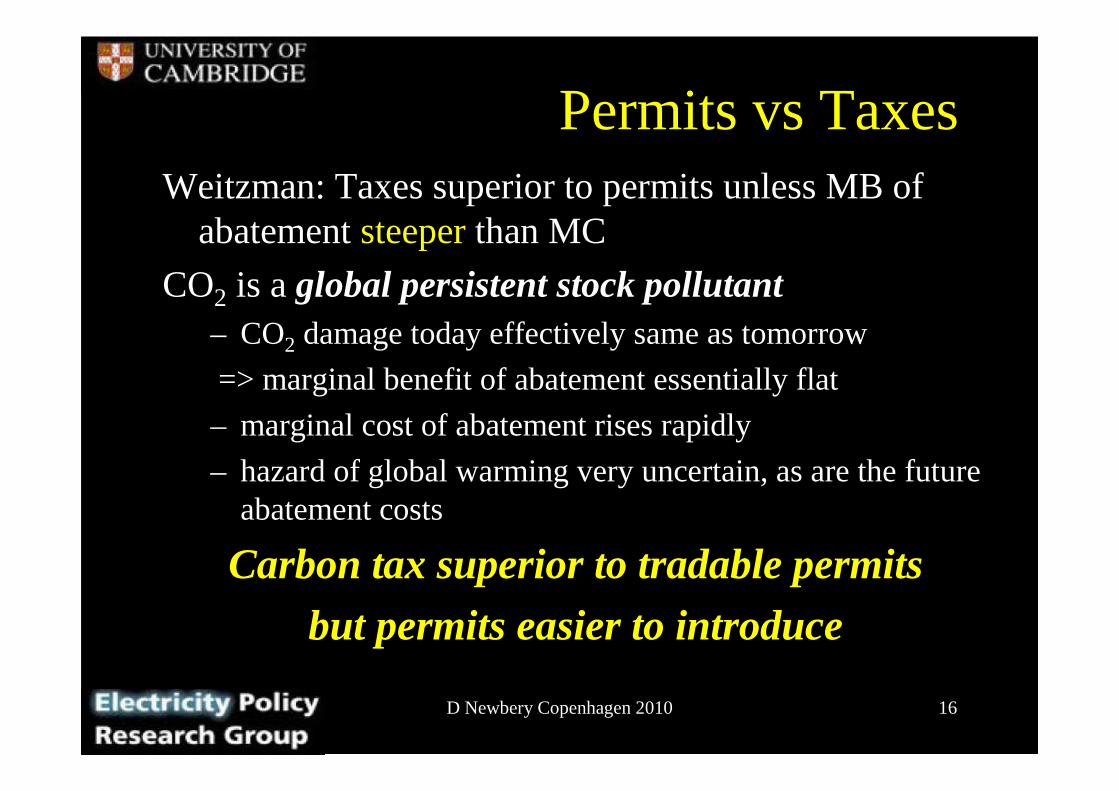

Permits vs TaxesWeitzman: Taxes superior to permits unless MB of

abatement steeperthan MC

CO2 is a global persistent stock pollutant– CO2 damage today effectively same as tomorrow

=> marginal benefit of abatement essentially flat

– marginal cost of abatement rises rapidly

– hazard of global warming very uncertain, as are the future abatement costs

Carbon tax superior to tradable permits

but permits easier to introduce

D Newbery Copenhagen 2010 17Newbery IIB 1 17

Start of ETS

Costs of errors setting prices or quantities

Reductions in emissions

Correct MC

MC

Best estimate of Marginal cost of abatement

MB, Marginal benefit from abatement

£/tC

efficiency lossfrom charge

efficiency lossfrom quota

t

Q* Q

t*

D Newbery Copenhagen 2010 18

Reforming ETS

• Reform EU ETS to provide rising price floor– sufficient for nuclear or on-shore wind or CCS

• Commitment to raise CO2 price at 3% p.a. over life of plant may suffice– €25/EUA 2010 => €34 in 2020, €61 in 2040 ...

• Making it credible: write CfD on this path– offer CfD at €45/EUA for 20y from commissioning?

makes extra carbon savings additional

D Newbery Copenhagen 2010 19

Carbon tax alternative

• Each Member State imposes a Carbon tax – tax bads not goods as part of fiscal adjustment

– rebated by EUA price for covered sector

– can start low: €20/t CO2 and escalate at 5% p.a. above RPI = €34/t by 2020

• Tax or full EUA auctioning to finance SET-Plan and RES, avoid taxing electricity

D Newbery Copenhagen 2010 20

Supporting RD&D

• 80% GHG reduction => decarbonising electricity

• Zero-C electricity requires renewables– and CCS + nuclear

• RES is not yet commercial (except in niches)– requires support now to drive down future costs

• R&D + deployment drives innovation and learning

• But RD&D is a public good benefiting the whole world

So how to gain collective support for RD&D?

D Newbery Copenhagen 2010 21

ETS and Renewables

• Aim: deliver low-C solutions for world

• Need to explore a portfolio of possible solutions– Then select those which show most promise

• Danger with RES target – choose cheapest– Fortunately MS have differing resources to explore

– And differing aspirations to industrial leadership

20-20-20 Directive: least bad feasible solution?

D Newbery Copenhagen 2010 22

Experience curves justify deployment support

Source: IEA

D Newbery Copenhagen 2010 23

2050 projected CO2 price

0

10

20

30

40

50

60

70

with 12.5% renewables with 20% renewables 2009 projections

Eur

os/to

nne

CO

2

Source: Committee on Climate Change, 2008 and 2009

2008 projections 2009 projections

after Renewables Directive andrecessionRenewables

depressesC-price

D Newbery Copenhagen 2010 24

Failures of ETS

• Current ETS sets quota for total EU emissions

• Renewables Directive increases RES=> increased RES does not reduce CO2

=> but does reduce price of EUAs

=> prejudices other low-C generation like nuclear

• Risks undermining support for RES

Solved by fixing EUA price instead of quota

D Newbery Copenhagen 2010 25

Reforming 2020 Directive• Not to reduce CO2 - ETS ensures no impact

– ETS intended to price CO2– but fails to give credible signals

• not to support low-C generation, only RES

=> support to RD&D to drive down costs of RES

• How? Support investment or generation?

• Learning comes from:– design (cost, reliability, controllability, etc)

– production, installation, siting/planning, grid integration

but not from operation (provided reliable)

D Newbery Copenhagen 2010 26

Implications for RES support• No RES should bid below SRMC

– Given that it can rapidly reduce output=> support should be for availability, not output

• RES should not have automatic priority– merit order should be based on avoided costs

=> if RES is more costly than alternatives (including balancing, redispatch), back it off=> foregone RES generation should count to RES

target (as it has no CO2 credit)– unless ETS reformed to support CO2 price

D Newbery Copenhagen 2010 27

Conclusions• ETSto price CO2

– but volatile, price too low, impacts gas market power• RES Directiveto support deployment and learning

=> Well defined MS funding in place through obligations• But RES Directive undermines ETS

– risks bringing ETS into disrepute=> Reform ETS – provide floor price

– de-links gas and coal markets– reduces risk of low-C generation investment– makes Renewables contribute to reduced emissions

• Failing which encourage MS to impose C tax– With rebates for EUA’s surrendered

The impact of the EU ETS on European energy and carbon markets

David Newbery

Danish Environmental Economic ConferenceSkodsborg Hotel 23 August 2010

http://www.eprg.group.cam.ac. uk

Spare slides on SET-Plan

D Newbery Copenhagen 2010 30

SET Low-C Plan

• Strategic Energy Technology (SET) Plan• Promising technology benefits from LbD

– Supported by 20-20-20 Directive and national deployment

• Many obstacles require R&D and perhaps pilots⇒ need efficient collective action to increase low-C R&D⇒ IPR benefits made widely available, contrary to MS interests

• But R&D collapsed at end of 1980s– liberalisation and resulting pessimism over nuclear future?

• SET plan to leverage MS’s R&D, steer choices

Ensure adequate size and diversity of portfolio

D Newbery Copenhagen 2010 31

UK Electricity R&D intensity

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

perc

ent e

lect

ricity

rev

enue

ROCs

other power

hydrogen and fuel cell

nuclear fission and fusion

Renewables

fossil fuels

Source: IEA

D Newbery Copenhagen 2010 32

UK Renewables R&D intensity (3-yr moving average)

0.00%

0.05%

0.10%

0.15%

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

perc

ent e

lect

ricity

rev

enue

geo-thermal

bio-energy

ocean

wind

solar

Source: IEA

D Newbery Copenhagen 2010 33

SET support schemes

• 2007 SET R&D non-nuclear ∼ €2.4bn (Nuclear €0.94)– 70:30 private:public; 80:20 MS:EC

• SET plan to 2020 total €70 bn or double current rate– Grid: €2bn; fuel cells + H2: €5bn; Wind: €6bn;

– nuclear fission €7bn; bio-energy € 9bn;

– smart cities €11 bn; CCS €13 bn; Solar: €16bn;

• Joint programming to amplify MS R&D– CCS as an example

ETS auction revenues as funding source?

D Newbery Copenhagen 2010 34

Three pillars of EU low-C policy

• ETSto price CO2

– for mature low-C investments - reform needed

• 20-20-20 Directive: demand pull for renewables– justified by learning spillovers and burden sharing

– induces near-commercial low-C deployment

• EU SET-Plan to treble R&D spend– to support less mature low-C options

Ensure they work together not in conflict