THE IMPACT OF AUTOMATED TELLER MACHINES (ATMs) ON CUSTOMER ...

45

KAMPALA INTERNATIONAL UNIVERSITY DEPARTMENT OF BUSINESS AND MANAGEMENT THE IMPACT OF AUTOMATED TELLER MACHINES (ATMs) ON CUSTOMER SATISFACTION. -A CASE STUDY OF CRANE BANK. UGANDA Submitted by: NAKAYISO ESEZA Reg. No.: BBA/4195/31 I DV Supervisor: Dr. SUNDAY NICHOLAS A Research Report Submitted To the School Of Business & Management in Partial Fulfillment for the Award of the Degree in Business Administration . Kampala International University P.O. Box 20000, Kampala, Uganda. August2006

Transcript of THE IMPACT OF AUTOMATED TELLER MACHINES (ATMs) ON CUSTOMER ...

KAMPALA INTERNATIONAL UNIVERSITY DEPARTMENT OF BUSINESS AND MANAGEMENT

THE IMPACT OF AUTOMATED TELLER MACHINES (ATMs) ON

CUSTOMER SATISFACTION. -A CASE STUDY OF CRANE BANK.

UGANDA

Submitted by: NAKA YISO ESEZA Reg. No.: BBA/4195/31 I DV

Supervisor: Dr. SUNDAY NICHOLAS

A Research Report Submitted To the School Of Business & Management in Partial Fulfillment for the Award of the Degree in

Business Administration .

Kampala International University P.O. Box 20000, Kampala, Uganda.

August2006

ACKNOWLEDGEMENT

I wish to express my deepest gratitude to Dr. Sunday Nicholas my supervisor, for his interest and support throughout the study.

I owe my warmest thanks to my brother Mr. Golooba Edward for the financial suppmi especially paying my tuition fees throughout the entire course. I also wish to thank my mother Mrs. Nnalongo Saben Mukasa Kayiso for the help, assistance, support and advice. I also thank all my brothers and sisters for all their support and encouragement.

Special thanks go to Crane Bank especially the General Manager Operations and to all my respondents, without whom this study would not have materialized.

I wish to also thank Sr. Sarto Mukasa for her support especially through prayers. I also thank Mr. Kimuli Paul and all the rest who supported me in any way that may the good Lord reward you abundantly.

APPROVAL

"I declare that this research is my original work and has not been published or submitted for any Degree or award to any University\ Institution."

SIGNED: ..N~(f~ _______ fu i~1.,_0.,_~------------ Date: ___ L~~-A~~.:L: __ 2,0'l)b · NAKA YISO ESEZA STUDENT

SIGNED~R. SUND~ :;/&8

-------------- Date: K{ ti: Pb __ _ SUPERVISOR.

11

DEDICATION

This research project is dedicated to my parents, Ssalongo and Nnalongo Pontian Kimbugwe Kayiso ofKansanga, Mr. and Mrs. Golooba ofNajjera, Mukutoggumu Road, and to all my brothers and sisters.

iii

LIST OF TABLES Page

Table 1 Table 2 Table 3 Table 4

Table 5 Table 6 Table 7 Table 8

Graph 1 Graph 2 Graph3 Chart 1 Chart 2

Bio data of the respondents:-------------------------------------------- l 8 occupations of the respondents:---- --------------·---------19 the age brackets of the respondents---·---- •---------------------19 accounts that customers utilize in Crane Bank ----------20

level of satisfaction due to the ATMs---------------------------21 the rate at which the customers are coping up with the new developments---21 reveals al the problems encountered-----------------------------------------------22

the solutions that were given by the customers to the above problems---23

LIST OF GRAPHS AND CHARTS

customer satisfaction in the use of ATMs------------------------------------23 Is it easy to make mistakes----------------------------------·--------------24 Who explained how ATMs work to you--------------·--------------24 The changes realized by the bank due to customer satisfaction -----------25 Other modem facilities that Crane Bank should installl----------------25

ABBREVIATIONS ICT-------------------Information and Communication Technology ATMs----------Automated Teller Machines

IV

TABLE OF CONTENTS Page

Acknowledgement---------------------------------·-----------------------------------1 Approval---------------------- --------------------------11 Dedication-----------------------------------·------------------------------m List of tables------------------- ----------------- -------1v Abbreviations----------------------------------------------------------------1v Tab I e of contents--------------------------- ------------------------------v-v1 Abstract-------------------------------------------------------------------------------v11

CHAPTER ONE

1.0 Introduction 1.1 Background of the study-------------------------------------------------1 1.2 Statement of the problem-------------------------------------------------2 1.3 purpose of the study----------------------------·--------------------------------2 1.4 Objectives of the study----------------------------------------------------------------3 1.5 Research questions------·--- ---------------------------·---3 1.6 Scope of the study·--- -----------------------------------------------------3 1. 7 Significance of the study--------------------------------------------------3

CHAPTER TWO

2.0 Literature review 2.1 introduction------------------------------------------------------------------------4 2.2 Definitions-----------------------------------------------------------------------4 2.3 Role of ICT in bank performance---------------------------------------------------5 2.4 Concept of Automation-----•--- -----------------------6 2.4.1 Computerization and Management----------------------------------------7 2.4.2 ATMs and employees--------------------------------------------------8 2.4.3 ATMs and customers-------------------------------------------------------------9-10 2.4.4 ATMs and bank performance-----------------------------------------------------1 l 2.5 Challenges faced in introducing ICT in banks----------------------------------11 2.6 How the challenges are handled --------------------------------------------------12 2. 7 Safety to ATMs----------------------------------------------------------------------12 2.8 Relationship between customer satisfaction and ATMs-----------------------13 2.9 Conclusion---------------------------------------------------------------------------14

CHAPTER THREE

3.0 Methodology

V

3 .1 Introduction------------------------------- -----------------------------15 3 .2 Research design---------·---------------------------------------------15 3.3 Study population------- •------------------------------------------15 3.4 Sample design-----------------·-- •---------------------------------15 3 .5 Sources of data----------- ------------------------------------------15 3. 6 Data collection instruments------------------·--------------------------------16 3. 7 Data processing, analysis and presentation-·-----------------------· -------16 3. 8 limitations of the study---·-------------------------------------16 3.9 Budget estimates for research proposal and report-------------------------------17 3 .9 .1 Time frame-------------- --- ---------------------------------17

CHAPTER FOUR

4.0 Presentation, analysis and Interpretation of findings 4. I Introduction-----------·--- -------------------------------------------------------18 4.2 Bio data of the respondents--------·-------------------------------------------18 4.2.1 Customer service and satisfaction--------·--- --------------------------19 4.2.2 Customer satisfaction due to the use of ATMs-----------------------------20-21 4.3 Problems encountered at the ATMs---------------------------------------------22 4.4 Changes associated with ATMs that improve Customer satisfaction-------23 4.5 Is it easy to make mistakes ?----------------------------------------0 -------24 4.5.1 Who explained how ATMs work to you?--------------------------------24 4.6 The changes realized by the bank due to customer satisfaction-------------25 4.7 Other modem facilities that Crane Bank should install-----------------------25 4.8 Conclusion---------------------------------------------------------------26

CHAPTER FIVE

5.0 Summary, conclusions and recommendations of the study 5 .1 Introduction------------------------------------------·-- --------------------------2 7 5 .2 Summary of findings--------------·--- •--------------------------------27 5 .2.2 ATM and customer satisfaction--------------------------------------------27 5.2.3 Relationship between customer satisfaction and the ATMs----------------28 5.3 Conclusion -------------------------------------------------------------28 5 .4 Recommendations---------------------------------------------------------29 5.5 Issues for future research---------------------------------------------------29

APP END IX A-------------------------------------------·-------Reference APPENDIX B--------------------------------------------- ---Questionnaire

VI

ABSTRACT

The research was can-ied out with the main objective of finding out the impact of ATMs on customer satisfaction in Crane Bank Uganda. This study focused don four research questions.

1. To find out the impact of ATMs on Customer Satisfaction 2. To find out the relationship between ATMs and customer satisfaction. 3. To find out the challenges faced by the banks when installing the ATMs 4. To find out how the challenges can be handled.

Data was collected using self-administered questionnaires to forty ATM customers. Key informants included the banking staff. Data was entered and analyzed using statistical means. The results of the study revealed the following:

The majority of the customers have used ATMs since the Bank introduced them, access the ATMs often (weekly) and find it easy to use them.

The findings also revealed that most of the customers prefer to use the ATMs, although most of them consider them located far away. Therefore, there is a need by the bank to further strengthen the benefits of the ATM and to address the problems related to using them, in order to have high customer satisfaction.

Vil

CHAPTER ONE

INTRODUCTION

1.1 Background of the study

Technology has always been the mechanism through which human kind has leveraged its

efforts, both individually and collectively to improve its quality of life. Technology

management is the ultimate battleground that will determine which companies and

owners will be the winners and losers in the wealth creation game. Technology has

become a key factor in defining competitive advantage in the modem business world and

it is likely to become an even more pervasive factor of production in the future (Norma

H& Danny S 2002, pg2)

Most countries have employed technology to accelerate economic growth pace. Foreign

capital and technology have played an important role in economic rejuvenation of

countries. It helps to increase productivity and hence provision of higher wages.

Information and communication technology (JCT) involves planned application of

integrated information handling tools and methods to improve the productivity of people

in office operations. The invention of information and communication technology in the

past century brought vast amounts of energies in scope of its usage and ATM's are part of

it.

Crane Bank is one of the commercial banks that exist in Uganda. There motto is

"Growing to serve and serving to grow". It started operating in 1995. It has got very

many customers and the presence of ATM's has drastically changed the culture in

Uganda, with Crane Bank at the forefront of it's development. Long hours and long

queues are history. The first ATM was introduced in May 2002, 32 ATM's in Kampala

and the main access account is the Crane Access account. In order not to inconvenience

the customers, the bank started the Crane Access account and customers don't have to go

to the bank to open an account and collect their ATM cards. All this can be done at the

ATM centre. With the ATM's, they have.been able to offer services at lower.costs. The

1

minimum balance is 10,000\=, there are no account maintenance charges, through

ATM's; you can top up airtime, change money, pay school fees or utility bills. A contract

was also made with the National Water and Sewerage Corporation to collect water bills.

Crane Bank also launched last year in October bank master software in order to enable

them fasten the ATM work. This software is able to store data at a faster rate.

Its usage has become diversified, and computers affect the greater part of our working

life. Automation is the act of implementing the control of equipment with advanced

technology; usually involving electronic hardware; "automation replaces human workers

by machines". It is also the condition of being automatically operated or controlled;

"automation increases productivity. The equipment used to achieve automatic control or

operation is advanced. Automation can also be called computerization or cybernation.

Business process automation (BPA) is the process of integrating enterprise applications,

reducing human intervention wherever possible, and assembling software services into

end-to-end process flows. As a significant part of business process reengineering, BPA

improves operational efficiencies and reduces risks.

1.2 Statement of the problem

Customers want a quick and faster delivery of services and this poses a challenge to the

banks to continue updating their services _to satisfy customers and work efficiently. This

involves quick services to reduce on the queuing customers in the bank. Therefore it is in

this perspective that the use of ATMs as part of ICT to improve on their services and

performance is important. As the banking industry keeps on growing, it also employs

more people. However despite the availability of the modem services, no initiative has

been taken to find the impact of ATMs on customer satisfaction.

1.3 Purpose of the study

The purpose of the study is to find out the impact of ATMs on customer

satisfaction that has possibly led to greater customer care and profitability of the banks.

2

1.4 Objectives of the study

The study was guided by the following objectives.

I. To find out the role of ATMs on customer satisfaction.

2. To establish the relationship between ATMs and customer satisfaction.

3. To find out the associated challenges faced in installing ATMs in Crane bank.

4. To find out how the challenges can be handled.

1.5 Research questions

The study was guided by the following questions.

I. What is the impact of ATMs on customer satisfaction?

2. What is the relationship between ATMs and customer satisfaction?

3. What are the associated challenges faced in installing ATMs in banks?

4. How can the challenges be handled?

1.6 Scope of the study

The study focused on the impact of ATMs on customer satisfaction and it was

conducted in Crane bank, at Crane chambers on Kampala Road and different ATMs were

also visited. The study considered ATM's as the independent variable and customer

satisfaction as the dependent variable, with much emphasis on the ICT department and

operations in the bank.

1. 7 Significance of the study

1. The research was to help management on how weII to use ATM's to have

customer satisfaction.

2. The research was to help future researchers to add on the existing body of

knowledge.

3. The research was to help the banking industry to know whether to instaII more

ATM's for customer satisfaction.

3

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter set out some of the main issues about the existing literature on

the subjects carried out by the scholars. It containsliterature on ATM's and there

impact on customer satisfaction.

2.2 Definitions

According to C.S. French (1993 pg.3), a computer is a device that works under control

of stored programs automatically accepting, storing and processing data to produce

information as a result of that processing ..

Technology is a collection of practices, procedures, techniques and devices used in

collecting, storing, retrieving, processing, distributing and delivering information and

knowledge that foster speed and accuracy in doing things.

Information Technology (ICT) is the technology which supports the activities involving

the creation, storage, manipulation and communication of information together with their

related methods, management and application (Norma H& Danny S, 2002 pg.3)

Computerization. According to French (1993, pg 7) it is a system used to convert data

from internal and external services by used of computer's information system and to

communicate that inforn1ation in an appropriate form to manage at all levels in all

functions to make timely and effective decisions for planning, directing and controlling

the activities for which they are responsible

4

A bank is a financial institution that accepts deposits, withdrawals and makes loans.

Banks operate with charging interests on money got and lending out money by making

loans.

Automated Teller Machines (ATMs) are specialized computer terminals, which are

connected online to the bank's Central Computer.

A TMs are sometimes known as Auto-banks or cash dispensers. They are normally

located outside the bank building, so that they can be accessed outside normal banking

hours (ATM magazine.comFeb. 19, 1999 by John Kennish).

2.3Role of ATMs to banks.

a) Time Saver. Saves time on data processing and transactions. ATMs have helped to

save time. This is because you can easily enter and retrieve data

b) Paperless office. ATMs have improved bank perfonnance through the reduction of

paper work. Data can easily be entered and stored in large amounts.

c) Accurate and updated transaction. According to Dr. Hamm Mukasa (2001 pg.16-

17), banks have become more accurate since several calculations can be done in a short

time with fewer mistakes. Computers are very accurate and can easily identify an en-or.

d) Greater volumes of data handled and processed. Large volumes of data can be

handled by computers due to ATMs. This has helped banks to store and easily look for

data hence overcoming the risk involved in the manual system.

e) Elongated banking hours. With manual systems, the banking hours were limited as

more time was needed to cru.Ty out the bank-office accounting functions after the counters

were closed for customers. With the introduction of computer systems, the banks could

offer longer hours for their customers. ·

f) Multi-tasking. Possibility of carrying out several activities at the sru.ne time.

Automation enabled any teller to caJ.Ty out more than one transaction type, if not all.

g) Any where banking. With the presence of ATMs, customers can can-y out their

transactions from any place.

5

h) Any time banking. The ATMs have also enabled the customers to carry out there

transactions at anytime. This is because the automatic generated machines are efficient 24

hours.

i) Deviation from the "branch" concept. Customers can get all their queries and

problems answered away from the bank branches. This can be done with the use of

ATMs.

j) Increased job satisfaction. With ICT in existence, this involves giving bonuses to

faster work done (Royal & Hughes 1991). The employees can enter data in a faster way

that ensures accuracy.

k) Budgetary control. Computers have benefited a lot through checking out several

business expenses that can get out of hand if not checked at regular intervals. A computer

can easily identify errors faster and can signal; warnings when things are not in order

(Royal & Hughes 1991).

2.4 The concept of Automation

Information technology has been hailed .to play a major role in development of most

economic paiis of the world. Automation through the use of computers provides an

opportunity for less developed countries to increase their development efforts. This new

technology has great potential but should be determined differently by a country or

economy. Info1mation management and handling in organizations involves much more

than the technologies utilized.

Bank customers use a special key that contains a magnetic strip along one side. The strip

is what contains data about the cardholder. The card is entered into the slot in the

machine, and account details from the strip are read by the ATM which then makes

contact with the central computer inside the bank. Next the customer enters a secret PIN

which provides the authorization to access the account. The facilities provided include;

withdrawing cash, finding out the account balance, top up airtime, change money, pay

school fees or pay utility bills, printing a mini statement, making deposits and

transferring money between accounts, (Nulurnansi, 2001).

6

ATMs offer a new alternative way in our daily banking affairs (Njuki, 2001). Over 70%

of the bank services provided by the banks could be automated or handled on self-service

basis.

ICT is important because it shows which businesses are winners and losers. The concept

also ensures a faster way of delivering services. This is because customers hate making

long queues for services, and they will always go for that bank, that can easily meet their

demands efficiently and effectively. Due to this call, all banks therefore are faced with a

challenge of installing ICT facilities given that it is a computerized era.

In almost every organization, people go for work and they are scheduled to perform

certain tasks to encourage efficiency and effectiveness, the only fancy way of describing

such events is division of labour, technology and its automation has by further greatest

impact in easing such events more as that of information system and all its speed in

organization, (Farbey, Land, Targett, 1995).

Some analytical scholars like Daniel Hertzberg (I 984) have already appreciated the

impact of computerization in the banking industry. He particularly highlights the

contribution of the modem innovations in the banking services such as the use of

automated teller machines (ATMs). The emergency of Internet banking and automated

teller machines (ATMs) networks has reduced the need for physical or direct contacts

between customers and their respective bankers.

John Kateeba Nyakahuma, Uganda Institute of Bankers -The New Vision 25th October

2001, further asserted that the combination of the computer and modem

telecommunications technology is changing the internal configuration of financial

intermediaries. It is further noted that allover the world the way business is conducted is

changing with the use of inf01mation technology. In virtually every industry from

banking and securities trading to manufacturing and design sectors, business managers

are striving to harness the power of information technology. The computer arrived in the

banking scene to stay during the 1960s.

7

2.4.1 Computerization and the management

The use of computers extends to several departments of the bank. The adaptation to

change is a managerial problem and this creates strategic advances or competitive edge

links. Top management is expected to handle situations where in major changes in

technology will affect the employees. This is ample scope to improve organizational

efficiency and effectiveness using ICT innovatively (Dr. Hamm Mukasa, 2003 pg 14-15).

Management has to work very hard to satisfy the customers. This will involve trying to

keep up the standards with the new ICT. This enables faster communication among

management and hence improves on Crane bank performance. The every day progress

made in infonnation technology has a significant impact on handling of transactions

because it has been made easier.

Automation enhances corporate adherence formation among several or even internally

between departments for the purpose of sharing infonnation which at that particular

moment is the major resource needed to gain strategic advantages.

Pierre Simon of Uganda Institute of Bankers further pointed out clearly that this

adherence (networking) could operate best for commercial banking networks, offering

services to cooperate, professional and individual customers. These banks could be of any

size given that small banks can also cool their resources or outsource the provision to

service sector companies. He further noted that progress made in information technology

over the past years has a significant impact on the handling of transactions.

2.4.2. ATMs and employees

ICT systems are numerous and can be like a bomb explosion, causing wide spread panic

and confusion in the organization. This requires the top executives to identify the areas of

impact properly in advance and precautions taken to cushion the shock. Some of the

impact areas are new inputs/ output equipment, organizational structural changes, fast,

efficient and h·ansparent operations (Dr. Ham Mukasa, 2003 pg 16).

8

Employees normally show reactions like; will it affect salary earning? Will it erode ones

authority? Will it mean change of job description? among others. Therefore, for the

perfo1mance not to change, the top executives should choose the employees who learn

faster to teach them. It is only after they realize that ICT relives them from the drudgery

of routine work that they start to appreciate the positive impact.

The banking personnel is always worried about losing their jobs, because one of the most

common duties was dispensing cash to customers. However such fear was unnecessary.

Instead of decreases of human resources in the bank offices, personnel found them to be

re-trained for managing the problems created by ATMs. The lines were reduced, cards

retained, notes filled in by machines and users claimed not to receive all the money they

specified. These are some of the problems that personnel had to handle on a day-to-day

basis.

2.4.3 ATMs and customers

Computers are being introduced to direct customer service in banks. Customers will

appreciate the speed at which services will be delivered. The customer is also

increasingly having to become a part of the transaction processing and therefore requires

knowing how to operate the ICTs. This leads to the new applications and services, which

can be offered, by banks to their customers through electronic banking, Internet banking

andATMs.

Good customer service leads to the growth of a sustainable customer base. A customer is

a person who enables a business to exist. He is not an outsider on air business, but part of

us. We are not doing him a favor by serving him; he is doing us a favor by allowing us to

serve him (Mahatma Ghandi, 1983).

Customer service is all about ending a transaction or interaction so that the customer feels

better than before it began. To the banking industry, great customer service pleased a

customer according to his or her individual preference so much so that the customer feels

9

special and remembers the interactions with the bank. According to Devendra (1983), to

bring services closer to a customer and to guarantee the opportunity to use them anytime,

a customer want to have the most important target in banking during the last twenty

years.

Computers have become the most important factor behind the decreasing amount of

working places (Lehti, 1996). This new information technology innovation, with

emphasis on ATMs, has greatly enhanced customer service (De Wit, 1990).

The most impmiant aspect of customer service should be viewed in terms of delivery and

should be availed when and where customer delivery should be seen as a product and like

any other product, it where to be developed, packaged, priced, provided, communicated,

distributed and marketed (Katz, 1998).

Customer service was further defined as an administrative process whereby· customers

expectations, orders and inquiries in addition to a wide variety of "before and after" sales

service and quickly, effectively, handled to meet customer needs and satisfaction,

(Kitimbo, 1994).

There is no doubts that customers are faced with similar offers from similar or related

funds and have consequently become very sophisticated hence if banks are to gain and

hold on to their customers, then they must offer good customer service that is attractive to

satisfy customers as a reward for their support of the firm, or else the banks are bound to

loose out (Chattered Bankers, 1997).

Providing a good service on a consistent basis implies that customers will continuously

be satisfied and return to the same service and perhaps recommend the service to their

colleagues. Eventually good customer service can become a good promotional tool for

the bank, consequently drawing and satisfying more customers, (Rendall and Senor,

1992).

10

A company's failure to provide the desired level of service quality may mean

dissatisfaction of customers and thus lead to loss of customers. Computerization such as

ATMs in several banks helps to improve customer service and satisfaction as well.

2.4.4 ATMs and bank performance

Most organizations have taken up computers as a form of ICT to handle their day-to-day

activities. The banking industry to date has a number of computer-aided programmers

developed to ease banking transactions. The introduction of ATM's and electronic

transfer system, currently in use is an example of an ICT programmed. According to Dr.

Ham Mukasa (2003 pg 17), customers and staff may be able to increase efficiency, with

which they make and receive payments and enjoy greater convenience. Electronic

banking may also increase access to financial systems for customers who have previously

found access limited. Electronic banking could also reduce operating costs for banks.

This allows more profits for the bank and hence favoring expansion. This also favors

credit extension activities and hence providing significant opportunities for the banks.

Management will realize a lot of improvement in their banking services if computers are

used to facilitate such activities (Simon, 1991). Management should adopt a

computerized system in order to reach customers the faster way and easily. The bank

performance will be shown by the customers available and the services that are offered.

Banks will work faster and efficiently to meet more customers in a given period of time.

The banks therefore should involve highly advanced technologies like ATMs in order to

hold on to their customers and ease their performance to higher productivity.

2.5 Challenges faced in introducing ICTs in banks

In the world of banking, it is often so, that as long as the old and familiar bank

service are easily available, interest in new technology in form of automatic services are

strongly Iimited,(Lehti and Kari,1996). It was difficult for old people to accept this new

technique and these new advantages of them. It wasn't easy to trust a new technology.

When a new product often enters the market, it is expensive, (Utterback, 1994). A lot of

11

money is spent on installing just a single ATM. This therefore means that there has got to

be a return on investment, otherwise the bank is bound to make losses.

a) The employees' adaptation to the technology takes time but after a while; they learn

to appreciate it.

b) Most employees think of losing their jobs. The introduction of Automation in any

organization inevitably leads to some jobs being made redundant alongside the people

who perform those tasks. But ICTs also create new and different jobs, new skills and new

challenges (Dr. Ham Mukasa, 2003 pg 17)

c) At times, banks meet a high cost of acquiring the A TM facilities and also stationing

them in different locations. Most banks are concentrated in the city center where they can

easily meet the facilities and upgrade them. They ignore other parts of the country and at

times not get enough customer response.

d) Repairing, maintaining and upgrading the facilities are also a challenge. The presence

of different computer viruses and also breakdown of operation by the A TM machines is a

big problem.

2.6. How the challenges are handled?

It is possible to balance the effect of job redundancy with re-skilling where, possible and

staff takes on new jobs and duties. Actions such as group discussions, training and post

implementation reviews assist during the transaction from manual to ICT based

operations through allying the fears of staff.

However all the fears that customer had about ATMs are gradually erased. The whole

system has become so much better, that popularity of ATMs has grown rapidly. Due to

A TMs attracting more and more customers, queues in the bank offices shortened

dramatically.

2.7 Safety to ATMs

ATM crime has continued to disturb the facility. It is hard to get a hand on how many

ATM crimes are committed, as they are generally tracked separately, (Westbrook.com).

12

Many corrective measures regarding ATM security cost money. So every time the idea of

breaking out ATM crime comes up, the bankers go into a cardiac aiTest and lobby against

it, (Kennish, 2000).

The American Bankers Association puts the number at an even lower crime rate, for

every 3.5 million transactions, or about 3000 a year. However, the biggest problem is that

consumers do not seem to be reassured by the statistics.

'Our customers seem to be satisfied with the service so far and we hope that none of

those terrible crimes affects us, (Byarugaba, 2001).

2.8Relationship between Customer Satisfaction and ATMs

An excellent customer satisfaction leads to growth of customer base. Customer base can

never grow with poor services. Crane Bank Uganda intends to become a low cost

provider, where all services will be made cheap through ATMs. Crane Bank has opened

32 ATMs in order to serve their customers better. Before introduction of these machines,

the bank had about 10,000 customers but to date, it boasts of a 70,000-customer base.

The managing director of Crane Bank is optimistic that the growth of customer base is as

a result of the service being offered to their customers.

Introduction of ATMs, improvement in customer service, this builds customer loyalty

that in turn erects a firm customer base_ leading profitability to the bank. This trend shows

a positive return on investment, to (Kakuru, 2000).

Customer service is a philosophy, which employees feel, and act accountable for creating

satisfied customers (Tom Reilly, Value Added Customer Service). Ferreul (1989) tries to

bring out what a company can do to satisfy its clients. He states that customers require

variety of services and at most basic levels, they need fair prices, acceptable services and

product quality, and dependable deliverances.

13

Pierre (1998) further noted that with computerization and presence of ATMs the

provision of home banking services is highly possible although they have to undergo

standardization at the remote banking service stations in order to be offered merely by

telephone. He cited the home banking services offered in Europe vial Automated Teller

Machines as an example that can be applied in Uganda as well as in other developing

countries. He stated that a survey in the European banking industry revealed that most

clients changed from their bankers because of the poor quality of the services offered to

them. The study thus seeks to investigate the situation and try to figure out probable

solutions where possible, say by devising avenues, capable of enhancing or instilling

loyalty in the customers depending on high quality service delivery, then can in turn

boost customer satisfaction. Financial institutions therefore need to computerize their

production facilities in order to develop a cooperate culture based on superior quality

service delivery.

Computerization of information system by any organization especially a financial

institution would enable it to maintain a high degree of flexibility and openness in their

information systems and operation as well as it brings about product customization and

benefits that accrue to it, (Giehira, 1997).

2.9 CONCLUSION

The banking industry has witnessed a positive invasion of technology used in today's

banks. Particular interest is focused on computerization of the bank's operations through

the introduction of ATMs. It is evident today that no bank will keep a customer if the

bank cannot serve the customer better and faster through computerization. ATMs have a

yardstick of self-service banking, and the customers' perception is very positive as far as

t5his facility is concerned. The ATM has further enhanced customer loyalty, because the

customers can access their cash 24 hours a day, due to the fact that the bank is open for

only a few hours a day.

14

CHAPTER THREE

METHODOLOGY

3.1. Introduction

This chapter presented the research design, procedure of the study, the sources of

data collection, data analysis, presentation and limitations of the study.

3.2. Research Design

The researcher used a descriptive and explanatory design in a way that it involved

in-depth interviews with the people themselves. The in-depth interviews were under the

qualitative data. The quantitative and qualitative data , WCU'., collected using semi

structured questioners. There was use of both numerical and non-numerical data. The

exploratory design included visiting the IO of the ATM locations in Kampala region and

recording what was on ground.

3.3. Study population

The researcher targeted forty ( 40) respondents and this sample was selected from

the management and customers. This was intended to facilitate the attainment of more

objective results. Ten ATM locations were used and the main branch at Crane Chambers.

3.4 Sample design

The management, staff and customers was selected using random sampling

technique. This technique involved the use of probability sampling for better results. The

population was sub-divided into sub-populations. A total of three strata were selected and

from each stratum, the fourth respondent was selected.

3.5. Sources of data

The data that was used for the purpose of the study included both primary and

secondary data.

15

(i) Primary data

This was obtained directly from the bank records and individual persons include staff and

the bank customers. Questionnaires and personal interviews w_e,r-e, used for that effect.

(ii) Secondary data

This was collected from already available data and literature. It involved the use of

external and internal sources.

a) Intemal sources

-ATM reports by Crane bank

-Company financial statements (balance sheets and income statements)

b) External sources

-Commercial journals

-Government Publications

-Text books

-Periodicals by the Bank

-Research reports

3.6. Data collection instruments

The research instruments were self-administered questionnaires. It also involved

personal interviews.

3.7. Data processing, analysis and presentation

The data obtained was edited, coded, and arranged in percentages and frequencies. It l,vi;i.s

then be analyzed by use of pie cha1is and graphs as a statistical test.

3.8. Limitations of the study

These included problems that the researcher faced during the research study.

I. Financial resources. The researcher was faced with a problem of limited funds to

facilitate the study for example collecting data.

16

2. Time constraint. There was also limited by time since the researcher had to beat the

deadline.

3. Revealing of information. Some respondents were reluctant to provide the required

infonnation for the fear of revealing their business secrets to competitors in the same

industry.

3.9 Budget estimates for research proposal and report

Activity Description Amount in shillings

A Proposal writing and printing 60,000

B. Proposal review 40,000

C. Data Collection 60,000

D. Data analysis 40,000

E Dissertation write up 80,000

F Contingences 50,000

TOTAL 330,000

3.9.1 Time frame

Activity Description Expected Period (Weeks)

1. Proposal writing and review 5

2. Data collection 2

3. Data analysis 5

4. Dissertation write up 6

17

CHAPTER FOUR

4.0 PRESENTATION, ANALYSIS AND INTERPRETATION OF FINDINGS

4.1 INTRODUCTION

The purpose of the study was to find out the impact of ATMs on customer

satisfaction. This chapter comprises of the presentation, discussion, analysis and

interpretation of findings.

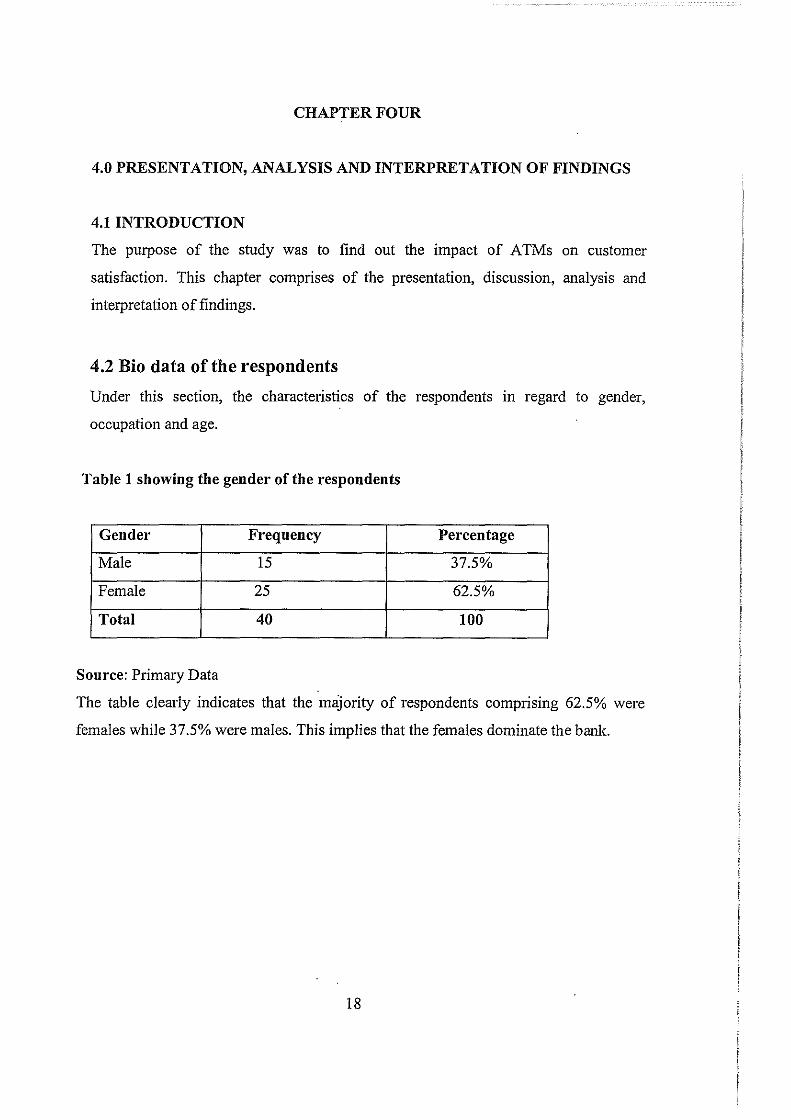

4.2 Bio data of the respondents

Under this section, the characteristics of the respondents m regard to gender,

occupation and age.

Table I showing the gender of the respondents

Gender Freqnency Percentage

Male 15 37.5%

Female 25 62.5%

Total 40 100

Source: Primary Data

The table clearly indicates that the majority of respondents comprising 62.5% were

females while 37.5% were males. This implies that the females dominate the bank.

18

Table 2 occupations of the respondents

Occupation Frequency Percentage

Students 20 50%

Bankers 5 12.5%

Business men 10 25%

Accountants 3 7.5%

Others 2 5%

Total 40 100

Source: Primary Data

From the above, 50% of the clients were students, 12.5% were bankers, .25% were

businessmen, 7.5% were Accountants and others were only 2%.

Table 3 showing the age brackets of the respondents

Age Frequency Percentages

15-25 10 25%

26-35 20 50%

36-45 5 12.5%

46-55 3 7.5%

55+ 2 5%

Total 40 100

Source: Primary Data

From the above table, 25% are between 15-25, the majority of the bank customers are

between 26-35 with 50%, 12.5% are between 26-45years, 7.5% are between 46-55years

and the least number of customers who are above 55 are only 5% of the clientele.

4.2.1 Customer service and Satisfaction in Crane Bank

The study findings showed that Crane Bank Uganda has a variety of services it offers to

its customers in a bid to meet their customer demands satisfactorily. The bank has got

accounts like current account, Ordinary savings account, Crane access account, Regular

19

Monthly Savings account, Crane access debit Account, Fixed Deposit account and

Children's Savings account. It was also noted that different customers utilize various

services as shown in the table below;

Table 4 of the accounts that customers utilize in Crane Bank

Service Frequency Percentage

Current account 10 25%

Ordinary savings account 3 7.5%

Crane access account 3 7.5%

Regular monthly savings account 5 12.5%

Crane access debit card 12 30%

Fixed deposit account 5 12.5%

Children's savings account 2 5%

Total 40 100

Source: Primary data

The table above illustrates that all the bank accounts are utilized by the customers,

current account 25%, ordinary savings account 7.5%, crane access account 7.5%,

regular monthly savings account 12.5%, the crane access debit card that is for the ATM

is the one that it highly utilized with 30%, fixed deposit account 12.5% and the children

savings account with 5%. This implies that the customers are more interested in the

Crane access debit account with the ATM card.

4.2.2 the level of Customer Satisfaction due to the presence of ATMs

The study also intended to establish the ATMs as part of computerization adopted by

the bank to foster customer satisfaction.

The findings revealed that Crane bank installing more ATMs and having bank master

software to make the work faster.

20

Table 5 the level of satisfaction due to the ATMs

Statement Frequency Percentage

Very good 25 62.5%

Good 10 25%

Poor 5 12.5%

Very poor - -

Total 40 100

Source: Primary Data

It is evident that the bank has attained improvement due to the presence of ATMs. The

table above reveals that 62.5% find the ATMs highly satisfying, 25% find them good and

only 12.5% find them poor. There was no client who was not getting satisfaction among

all the respondents.

Table 6 the rate at which the customers are coping up with the new

developments

Statement Frequency Percentage

Fast rate 20 50%

Fairly fast rate 10 25%

Slow rate 10 25%

Very slow rate - -

Total 40 100

Source: Primary Data

The above table revealed that most customers are coping up with the new developments

at a faster rate 50%, the other customers at a fairly faster rate 25%, only 25% are coping

up at a low rate and no customer is very slow at catching up with the developments.

The results of the work are in line with the work of Herman Gichira, in the East African

21

Newspaper of August, 1997, where he lamented that in the banking industry today, it is

seen as the most fmtunate trend that technological advancement has brought in place.

4.3The problems encountered at the ATMs

Customers encounter many problems when operating or waiting to be served at the

ATMs. These problems can be explained below;

Table 7 reveals al the problems encountered

Statement Strongly Agree Strongly

agree Disagree

Long queues 25 10 5

(62.5%) (25%) (12.5%)

Disruption of 21 6 13

automated services

(52.5%) (15%) (32.5%)

Power failures 17 14 9

(42.5%) (35%) (22.5%)

Limited ATMs 17 13 10

(42.5%) (32.5%) (15%)

Source: Primary data

From the table above, it was revealed that the highest problem encountered at ATMs is

the presence of the long queues with 62.5%, followed by the disruption of the automated

services 52.5%, and then also the presence of fewer ATMs 42.5% and lastly power

failures with 32.5% since most of the tenninals have got standby generators.

22

Table 8 shows some the solutions that were given by the customers to

the above problems.

Statement Freqnency Percentage

Increase the ATM 25 62.5%

terminals

Servicing and 7 17.5%

maintaining the facilities

Open more branches Ill 3 7.5%

busy centers

Others 5 12.5%

4.4 The changes associated with ATMs in improving the level of

customer Satisfaction

Customer Satisfaction from ATMs

80% 70%

~ 60% .13 50% ; 40% ~ 30% if 20%

10% 0%

Yes No

Customer response

From the above graph, ATMs have improved the level of customer satisfaction

and 75% of the customers agree that they have derived better satisfaction through

the use of ATMs and only 25% did not agree.

23

4.5 Is it easy to make mistakes?

70 60

fil 50 C)

.fl 40 C

~ 30 if 20

10

0 Yes No

Customer Response

70% of the customers find ATMs convenient because they cannot easily make

mistakes when operating them. Only 30% of the customers find it hard.

4.5.1 Who explained how ATMs work to you?

50 45 40

fil 35 C) .fl 30 C 25 ~ 20 a, 15

D. 10

5 0

Banking staff Friends Bronchures None

Customer Response

According to the customers the bank staff is the one that explains more onhow

ATMs work with the percentage of 50%, followed by friends, with 30% then the

brochures provided by the bank offer only 12.5% of the explanation and lastly

some customers claimed that no one explained to the how the A TMs work.

24

4.6The changes realized by the bank due to customer satisfaction.

II Increase in customer base

Ill Efficiency

□Others

According to the research from the bank, it has been proved that A TMs have led

to increase in the customer base 270° (74%), bank efficiency has also increased by

45° (13%) and others by 45° (13%).

4. 7 Other modern facilities that Crane Bank should install.

25

IIIIMoreATMs

fill Others

Majority of the customers still want more ATMs to be installed especially in busy

centers in order to avoid inconveniences.

4.8 Conclusion

According to the research findings, most customers have got more satisfaction

through the use of ATMs and therefore Crane Bank should always focus on their

development to have a higher customer base and satisfaction hence high

profitability.

26

CHAPTER FIVE

5. SUMMARY, CONCLUSIONS AND RECOMMENDATIONS OF THE STUDY

5.1 INTRODUCTION

1. ATM and Customer Satisfaction

ii. Relationship between Customer satisfaction and ATMs.

m. Challenges faced in installing ATMs

1v. How are the challenges handled?

5.2 SUMMARY OF FINDINGS

ATMs have greatly improved customer satisfaction, and this can be cited in the

following ways;

1. 90% of the customers find it easy to use ATMs.

11. 78% of the customers, use ATMs at least once a week

5.2.2 ATMs and Customer Satisfaction

Customer base has grown as a result of introducing ATMs. The majority of the

respondents are satisfied with the present functions of ATMs. However, other functions

recommended by the respondents included acceptance of coins, giving legally accepted

notes and detailed bank statements.

27

5.2.3 Relationship between Customer Satisfaction and ATMs

1. 80% of the customers prefer the ATM to the Bank to make withdrawals or

deposits.

11. 85% feel safe using ATMs

m. 87% would like to have more ATMs especially in their villages

rv. 78% of the customers would like to have more A TMs within reasonable reach of

their homes, work place or schools.

v. Customers have found ATMs to be convenient, fast and accessible.

5.3 CONCLUSIONS

The numbers of customers who have used ATMs for a period greater than one

year are more currently than they used to be before 2001.

i. Crane Bank Staff only contribute 20% towards transfusing information about

ATMs to customers. Friends told majority of their customers about ATMs.

ii. 50% of Crane Bank staff explained to their customers how ATMs work.

iii. 78% oft/ze customers access ATMs at least once a week.

28

5.4 RECOMMENDATIONS

There is a need for further improvement of customer service by making the following

interventions;

1. Increasing the number of ATM service points and hence reducing queuing time

and also making the services more accessible.

2. Increasing available ATM functions so that customers have a wider an-ay of

transactions that they can perform at the ATM service points.

3. Reduce on failure of machines by creating better ICT connections and also

can-ying out regular maintenance.

4. Avoid putting forged notes at ATM terminals.

5. Improving security for customers at the ATM service points.

6. There is need for the Bank to further market the ATM as a useful utility in order

to increase the customer base. Sensitization can be done through brochures,

radios, Television and personal communication.

5.5 ISSUES FOR FUTURE RESEARCH

The researcher is of the view that further studies can be conducted to assess the impact of

A TMs on customer satisfaction for higher customer base, growth and profitability.

29

APPENDIX A: REFERENCE

1. Chartered Institute of Bankers (Vol. No.3 March (1997)

2. C.S.French (1993, 1995) Computer Science

3. Devendre (1983): Indian Banking and Automation.

4. De Wit,G.R (1990): The Character of Technological Change and Employment in

Banking: A Case study of Dutch Automated Clearing House(BCG)

5. Donald A. Marchand, William J. Kettinger & John.D, Rollins (2001) Information

Orientation. The link to Business Performance

6. Donald H.S (1983) Computer today MC Graw-Hill,Inc

7. Farbey B. L & Target.F(1995) How to assess your I.T Investment Management

Today

8. Herman Gichira (1997) Financial Institution and Information Technology,

Internet.

9. Kakuru J.(2000): Financial Management. Makerere University Press.

10. Kennish (2000): Technological advance in Banking. ATM Magazine.com.

I 1. Lehti-Kari(l996): Pankkitoiminta tietoyhteiskunnassa.

Suunta2002,Kustarmusyhtio. Otava, Keuruu.

12. Mahatma Ghandi(l983): Banking and Customer Service. Vajpayee press.

13. Mark.L& Louise K.(2000). E- Commerce. Doing business Electronically

14. Njuki A,(2001): Alternative ways in daily BankingAffairs. Capital Markets

Authority, Vol.4 110.8.

15. Norma Harrison and Danny Samson (2002) Technology Management. Text and

International cases.

16. Pierre Simon, New Technology and Coperative Advantage. (UIB) Journal

17. Scott Basham& Stephenson College (1995) Chartered Institute of Bankers in

Scotland. Information Technology

18. Stephen P. Robbins (2001) Organizational theory. Structure, Design &

Applications

19. The Institute of bankers of Sri-Lanka 2003. Bankers' Journal Vol 22 No.3

20. The New Vision Contract Publishing, August 18'\ 2005, Crane Bank 10th

30

Anniversary

21. Utterback, James M(l994): Mastering the Dynamics of Innovations; How

Companies can seize opportunities in the Face of Technological change.

31

APPENDIX A

RESEARCH INTERVIEW GUIDE ON THE IMPACT OF ATMS ON

CUSTOMER SATISFACTION

Please kindly fill these forms completely. They are for academic purposes only.

Tick the suitable alternative.

PART 1: PERSONAL PROFILE

I. Gender for the respondent

a) Female b)male ~I-~

2. Occupation of the respondent-----------------------------------------------------------

3. Age

a) 15-25

b) 26-35

c) 36-45

d) 46-55

e) 55+

PART2: GENERAL DATA

I. What services does Crane Bank offer to you?

Cunent account

Ordinary savings account

Crane access account

Regular monthly savings account

Crane access debit card

Fixed deposit account

Children's savings account .

Others specify--------------------------------------------------------

2. For how long have you worked for/been a customer of Crane Bank?

1-2

2-4

4-6

6-8

8-10

Others specify----------------------- ----------------------------

3. Is it believed that ATMs play a major role in customer satisfaction?

Strongly agree

Strongly disagree

Agree

Not agree

4. What problems do you encounter when withdrawing money?

Long queues

Power failures

Limited counters

Limited working hours

Disruption of automated services

Others specify-----------------------------

5. What solutions would best deal with the above problem?

Increase the ATM terminals ·

Servicing and maintaining the facilities

Open more branches in busy centers

Others

6. Have the changes associated with ATMs improved the level of customer

satisfaction?

a) Yes b)No

7. How would you describe the performance of your bank as a result of

computerization?

Very good C=:J Goodc:=:J Poorc:=:J Very poor C=:J

8. At what rate are you copping up with the new developments associated with

Computerization?

Fast rate C=:J Fairly fast ratec:=:J Slow ratec:=:J Very slow rateCJ

9. Are the employees satisfied with how reliable the A TM facilities are?

Very satisfied C=:J Satisfied CJ Dissatisfied CJ Very dissatisfied CJ

10. Are you satisfied with how flexible the system is?

Very satisfied C=:J Satisfied C=:J Dissatisfied C=:J Very dissatisfied CJ

11. What new changes have you realized in your bank that has been due to customer

satisfaction?

12. Which other modern facilities would you like to install for a better performance?

13. Who explained how ATMs work?

Banking staff C=::J Friends

Brochures None

14. Is it easy to make mistakes?

No C=::J Yes

Thank you for your corporation.

KAMPALA INTERNATIONAL UNIVERSITY

Ggaba Road, Kansanga • PO BOX 20000 Kampala, Uganda Tel: +256 (0) 41 • 266 813 • Fax: +256 (0) 41 · 501 974

E-mail: [email protected] • Website: http://W1Nw.kiu.ac.ug

Office of the Dean School of Business and IVIanagement

THE HEAD THE HUMAN RESOURCE DEPARTMENT CRANE BANI< LTD l<AMPALA,UGANDA

Dear Sir/Madam,

Date: 27TH July,2006 ·

RE: MISS. NAKAYISO ESEZA REG.NO BBA\4195I31\DU This is to confirm and inform you that the above referenced lady is a bonafide student of Kampala International University pursuing a Bachelor of Business Administration Degree programme(banking and Finance option) in the school of Business and Management of this University.

Her title of the Research Project is "THE IMPACT OF AUTOMATED TELLER MACHINES ON CUSTOMER SATISFACTION" A CASE STUDY OF CRANE BANK LIMIED.

As part of her studies (research work) she has to collect relevant information through questionnaires, interviews and reading materials from your place.

In this regard, I request that you kindly assist her by supplying/furnishing her with the required information and data she might need for her research project and also by filling up the questionnaire.

Any assistance rendered to her in this regard will be highly appreciated.

Yours Sincerely,

DR. Y. NYAB GA ASSOCIATE DEAN - SCHOOL OF BUSINESS AND MANAGEMENT TEL.NO. 0752 843 919

"Exploring the Heights"