Budget -Revenues: $47.66 billion -Expenditures: $65.05 billion *Budget deficit.

THE IMPACT OF A BUDGET DEFICIT ON TRANSPORT INFRASTRUCTURE

INVESTMENT IN SOUTH AFRICA

BY

APHIWE NANTO

A DISSERTATION SUBMITTED IN FULFILMENT OF THE REQUIREMENTS

FOR THE DEGREE

MASTER OF COMMERCE

(TRANSPORT ECONOMICS)

DEPARTMENT OF ECONOMICS

FACULTY OF COMMERCE AND MANAGEMENT

UNIVERSITY OF FORT HARE

SOUTH AFRICA

SUPERVISOR: PROF. R. NCWADI

2013

brought to you by COREView metadata, citation and similar papers at core.ac.uk

provided by South East Academic Libraries System (SEALS)

i

ABSTRACT

Persistent government budget deficits and government debt have become major concerns in

both developed and developing countries. This study investigates the impact of a budget

deficit on transport infrastructure investment in South Africa. Quarterly time series data,

covering the period 1990q1- 2009q4, was used in this project. The study tests for stationarity

using the Augmented Dickey- Fuller and Phillips Perron; it tests for cointegration using the

Johansen (1991, 1995) methodology. A vector error correction model is used as an estimation

technique. The results of this study show that a budget deficit has a negative impact on

transport infrastructure investment in South Africa.

Keywords: Budget deficit, transport infrastructure investment, VECM, South Africa.

ii

DECLARATION

I, the undersigned, Aphiwe Nanto, hereby declare that this dissertation is my own original

work and that all sources have been accurately reported, acknowledged and referenced.

Moreover, I declare that this document has not previously been submitted at any university

for a similar or any other academic qualification.

Signature …………………………

Date ………/………/………….

iii

ACKNOWLEDGEMENTS

Firstly, I thank my savior the Lord Jesus Christ for his love and strength that he has given me

to make all things possible. Secondly, I thank the National Department of Transport and the

Govan Mbeki foundation for their financial assistance; none of this would have been possible

without your support. I also express my sincere gratitude to my supervisor, Prof. R. Ncwadi,

for his unlimited advice, encouragement and guidance. Finally, I thank my family and

friends who gave me the much needed words of encouragement and advice throughout the

years, it is highly appreciated.

iv

DEDICATION

This thesis is dedicated to my parents, my brothers and my daughter.

v

LIST OF ACRONYMS

ADF: Augmented Dickey Fuller

ARDL: Auto regression distribution lags

AIC: Akaike Information Criterion

ASGISA: Accelerated Shared Growth Initiative for South Africa

BBBEE: Broad Based Black Economic Empowerment

CGC: Classical Growth Cycles

CPI: Consumer Price Index

DF: Dickey Fuller

DTI: Department of Trade and Industry

ECM: Error Correction Model

FDI: Foreign Direct Investment

FPE: Final Prediction Error

GDP: Gross domestic Product

GEAR: Growth, Employment and Redistribution

GFSY: Government Financial Statistics Yearbook

HQ: Hannan-Quinn

IMF: International Monetary Fund

IRF: Impulse Response Functions

JB: Jarque- Bera

KPSS: Kwiatkowski Phillips Schmidt Shin

LM: Lagrange Multiplier

LR: Likelihood Ratio

MTEF: Macro Transport Infrastructure Forum

NEER: Nominal Effective Exchange Rate

NGP: New Growth Path

OECD: Organisation for Economic Co-operation and Development

OLG: Overlapping Generations

OLS: Ordinary Least Squares

PIMS: Political Information and Monitoring Services

PP: Phillips-Perron

R&D: Research and Development

RDP: Reconstruction and Development Programme

vi

RGDP: Real Gross Domestic Product

SAIIA: South African Institute of International Affairs

SARB: South African Reserve Bank

SC: Schwarz Criterion

STATSSA: Statistics South Africa

SUR: Seemingly Unrelated Regression

TII: Transport Infrastructure Investment

TVP-VAR: Time Varying Parameter -Vector Auto Regression

UNCTAD: United Nations Conference on Trade and Development

US: United States

VAR: Vector Auto regression

VECM: Vector Error Correction Model

vii

Table of Contents

ABSTRACT ............................................................................................................................................. i

DECLARATION .................................................................................................................................... ii

ACKNOWLEDGEMENTS ................................................................................................................... iii

DEDICATION ....................................................................................................................................... iv

LIST OF ACRONYMS .......................................................................................................................... v

LIST OF TABLES .................................................................................................................................. x

LIST OF FIGURES ............................................................................................................................... xi

CHAPTER ONE ................................................................................................................................... 1

INTRODUCTION ................................................................................................................................. 1

1.1 Background and Problem Statement ............................................................................................. 1

1.2 Objectives of the study .................................................................................................................. 3

1.3 Hypothesis of the study ................................................................................................................. 4

1.4 Significance of the study ............................................................................................................... 4

1.5 Organisation of the study .............................................................................................................. 4

CHAPTER TWO .................................................................................................................................. 5

LITERATURE REVIEW .................................................................................................................... 5

2.1 Introduction ................................................................................................................................... 5

2.2 Theoretical Literature .................................................................................................................... 5

2.2.1 Harrod-Domar Model ................................................................................................................ 5

2.2.2 Robert Solow Model .................................................................................................................. 6

2.2.2.1 Limitations of the neo-classical growth model ....................................................................... 8

2.2.3 Endogenous Growth Model ....................................................................................................... 9

2.2.3.1 The Lucas Endogenous Growth Model ................................................................................ 10

2.2.3.2 The Romer Model of Endogenous Growth ........................................................................... 11

2.2.3.3 Limitations of the endogenous growth model ....................................................................... 13

2.2.4 Assessment of the Theories...................................................................................................... 13

2.3 Empirical Literature .................................................................................................................... 14

2.3.1 Empirical Evidence from Developed Countries ...................................................................... 14

2.3.2 Empirical Evidence from Developing Countries ..................................................................... 22

2.3.3 Empirical Evidence from South Africa .................................................................................... 29

2.4 Conclusion .................................................................................................................................. 34

CHAPTER THREE ............................................................................................................................ 36

viii

AN OVERVIEW OF THE SOUTH AFRICAN BUDGET DEFICIT AND TRANSPORT

INFRASTRUCTURE INVESTMENT ............................................................................................. 36

3. 1 Introduction ................................................................................................................................ 36

3.2 Historical overview ..................................................................................................................... 36

3.2.1 South African Public Transport Infrastructure Investment 1980-2011 .................................... 37

3.3 Government Revenue 1980-2011 ............................................................................................... 39

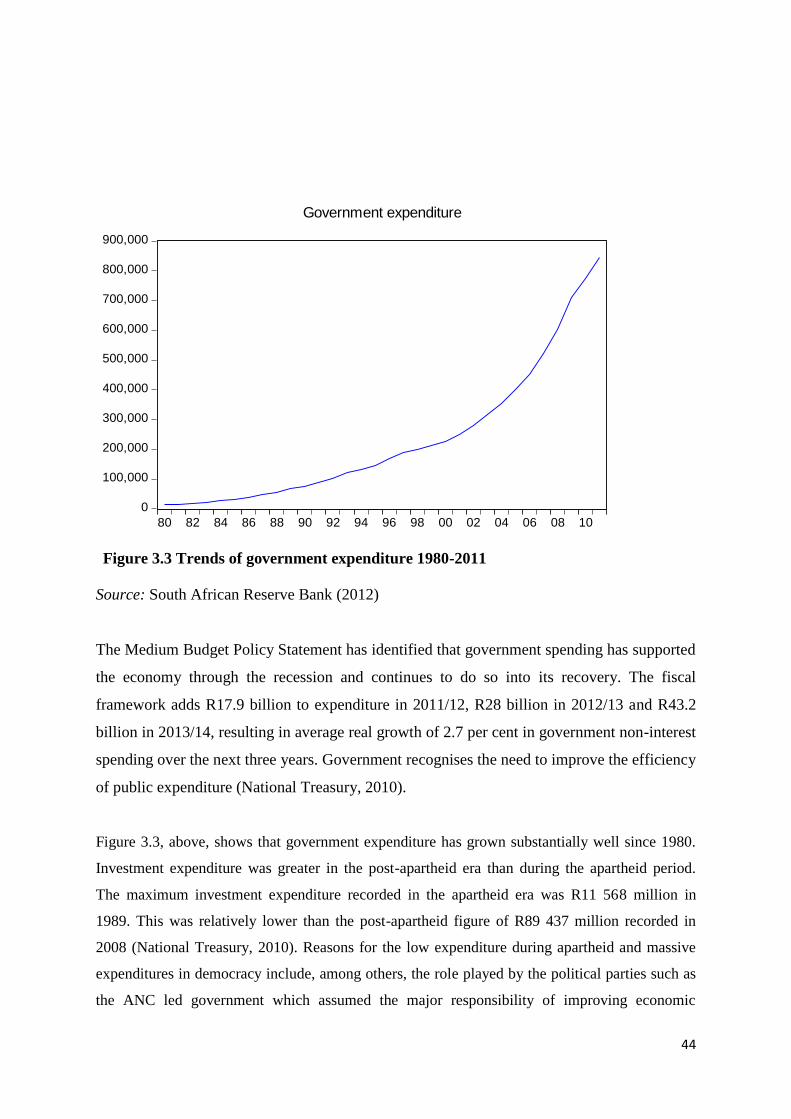

3.4 Government Expenditure 1980-2011 .......................................................................................... 41

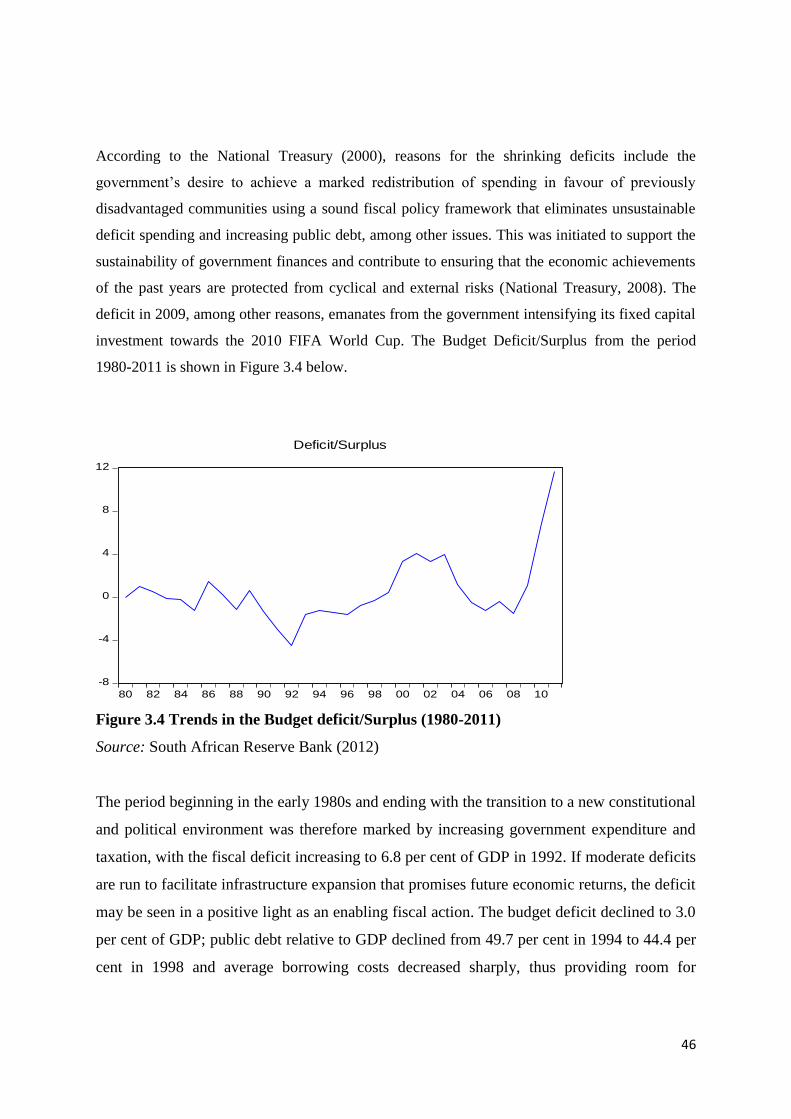

3.5 Budget Deficit/Surplus 1980-2011 ............................................................................................. 45

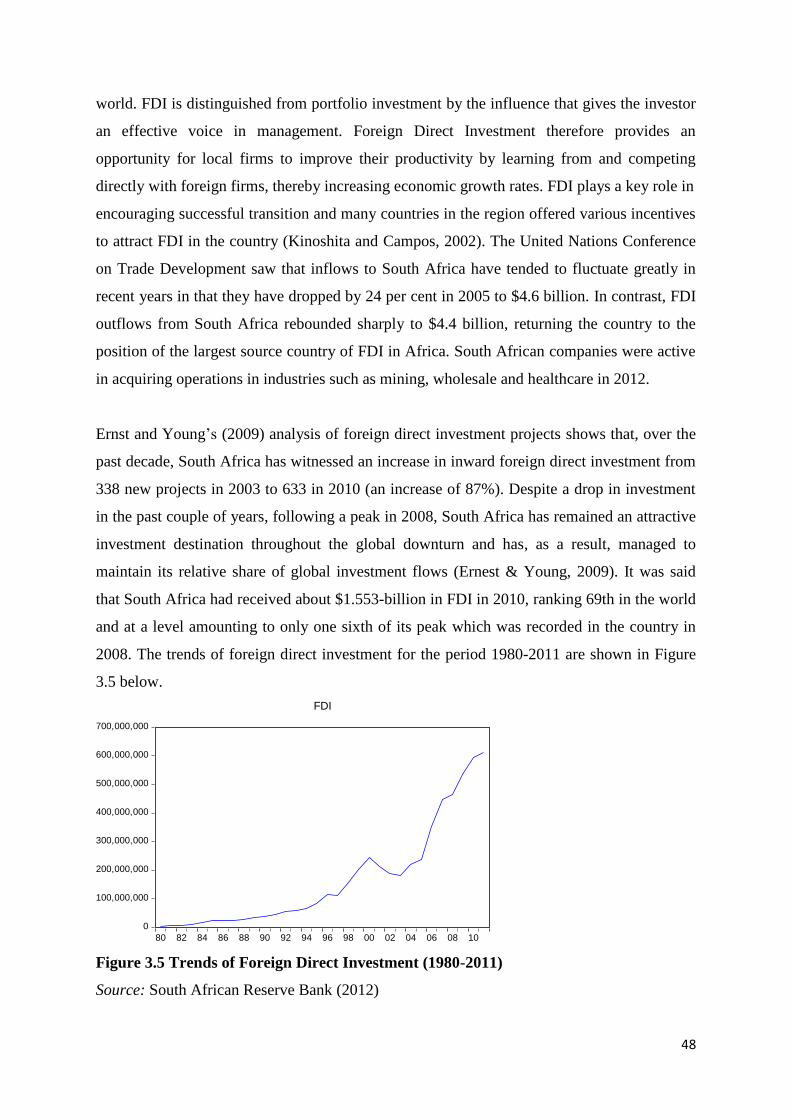

3.6 Foreign Direct Investment 1980-2011 ........................................................................................ 47

3.7 Real Gross Domestic Product 1980-2011 ................................................................................... 49

3.8 Conclusion .................................................................................................................................. 52

CHAPTER FOUR ............................................................................................................................... 53

RESEARCH METHODOLOGY ...................................................................................................... 53

4.1 Introduction ................................................................................................................................. 53

4.2 Model specifications ................................................................................................................... 53

4.3 Definition of the variables and data sources ............................................................................... 54

4.4 Expected Priori ............................................................................................................................ 54

4.5 Estimation Techniques ................................................................................................................ 55

4.5.1 Testing for Stationarity/Unit Root ........................................................................................... 55

4.5.2 The Augmented Dickey–Fuller test and Phillips Perron test ................................................... 56

4.5.3 Cointegration and vector error correlation modeling (VECM) ................................................ 57

4.5.4 Diagnostic Tests ....................................................................................................................... 60

4.5.4.1 Autocorrelation LM Test ...................................................................................................... 61

4.5.4.2 Heteroscedasticity test........................................................................................................... 61

4.5.4.3 Residual normality test.......................................................................................................... 61

4.5.5 Impulse response and variance decomposition ........................................................................ 61

4.5.5.1 Impulse response ................................................................................................................... 62

4.5.5.2 Variance Decomposition ....................................................................................................... 62

4.6 Conclusion .................................................................................................................................. 63

CHAPTER FIVE ................................................................................................................................ 64

PRESENTATION OF EMPIRICAL RESULTS ............................................................................. 64

5.1 Introduction ................................................................................................................................. 64

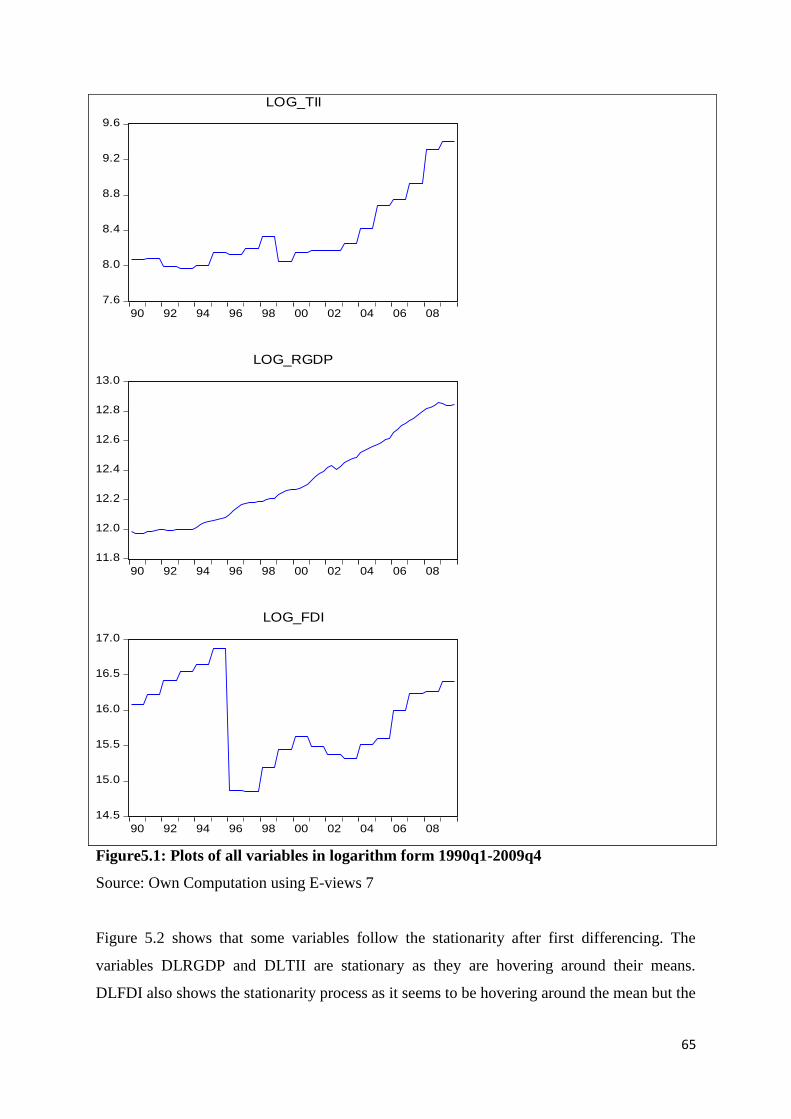

5.2 Stationarity/unit root test ............................................................................................................. 64

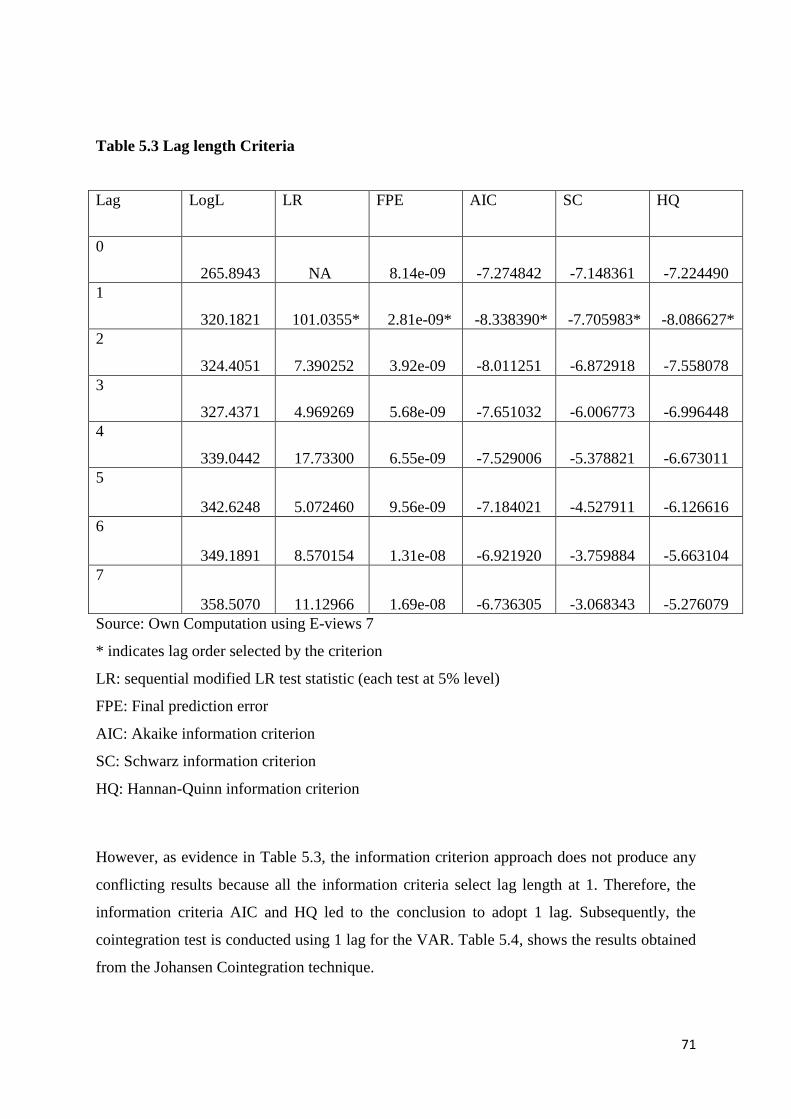

5.3 Cointegration............................................................................................................................... 70

ix

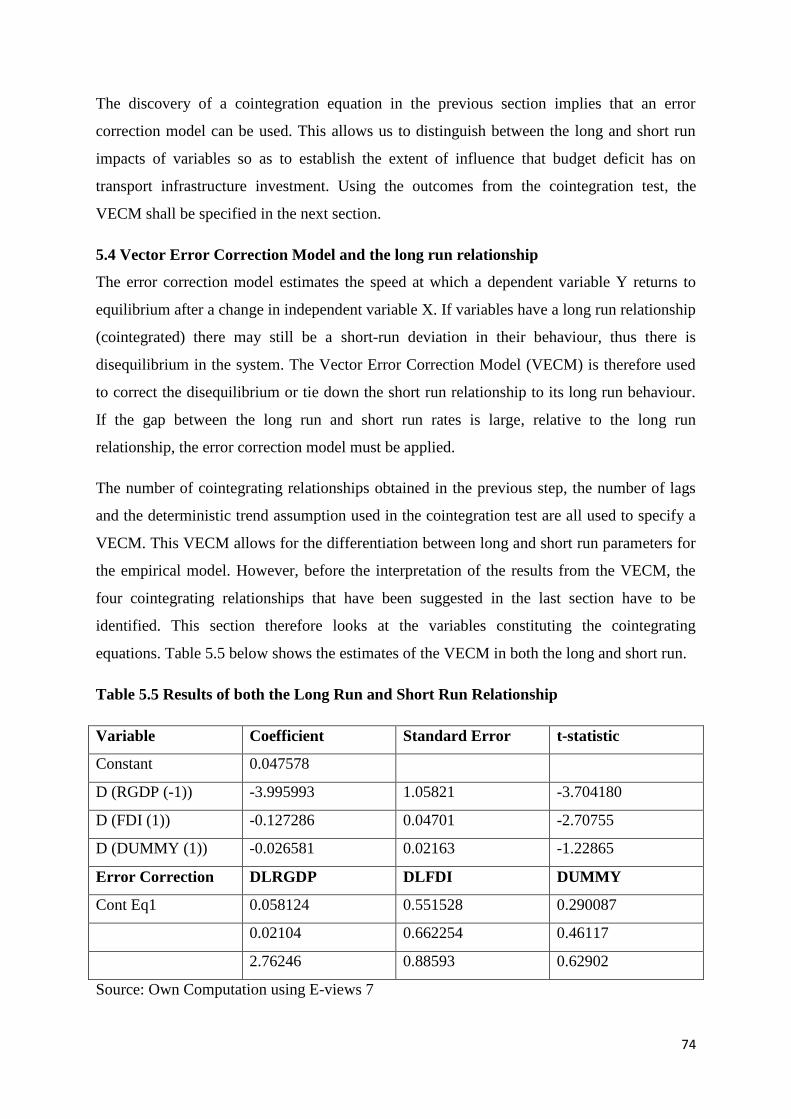

5.4 Vector Error Correction Model and the long run relationship .................................................... 74

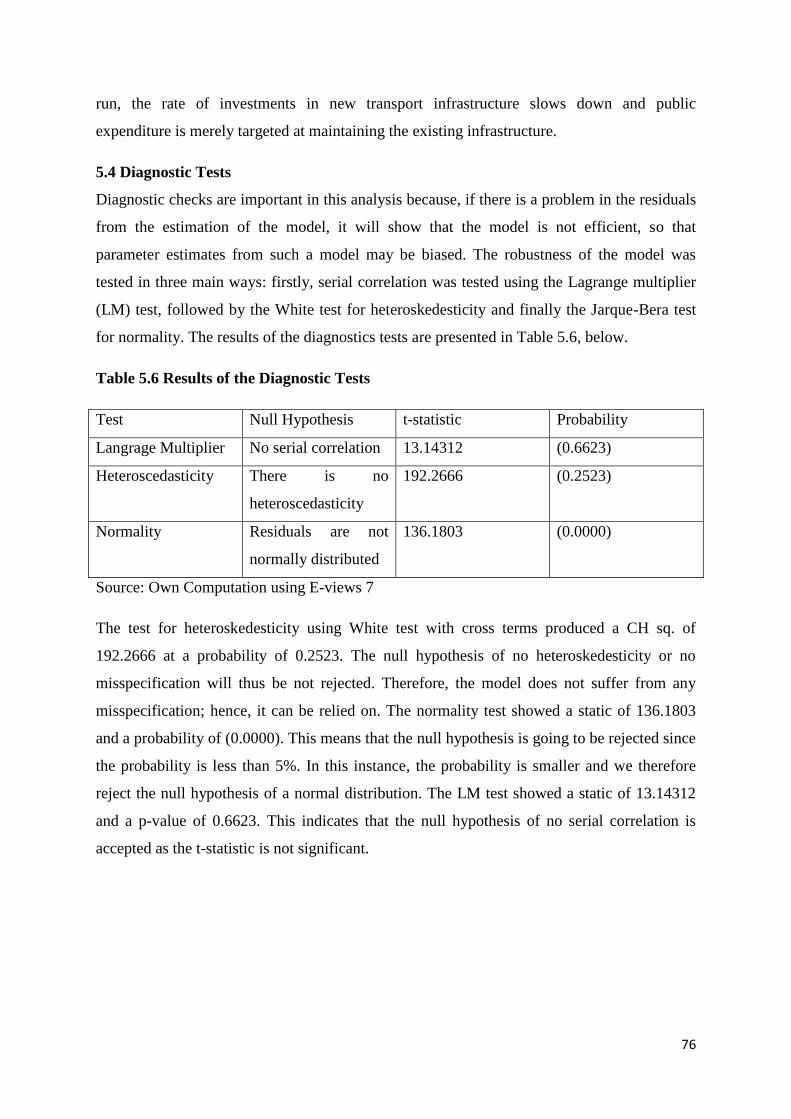

5.4 Diagnostic Tests .......................................................................................................................... 76

5.5 Impulse response and Variance decomposition .......................................................................... 77

5.6 Variance Decomposition ............................................................................................................. 78

5.7 Conclusion .................................................................................................................................. 80

CHAPTER SIX ................................................................................................................................... 81

SUMMARY OF THE MAIN FINDINGS, CONCLUSIONS, IMPLICATIONS AND

RECOMMENDATIONS .................................................................................................................... 81

6.1 Summary of the study and conclusions ....................................................................................... 81

6.2 Conclusions ................................................................................................................................. 82

6.3 Recommendations ....................................................................................................................... 82

6.4 Delimitations and recommendations for future research ............................................................ 82

REFERENCES .................................................................................................................................... 83

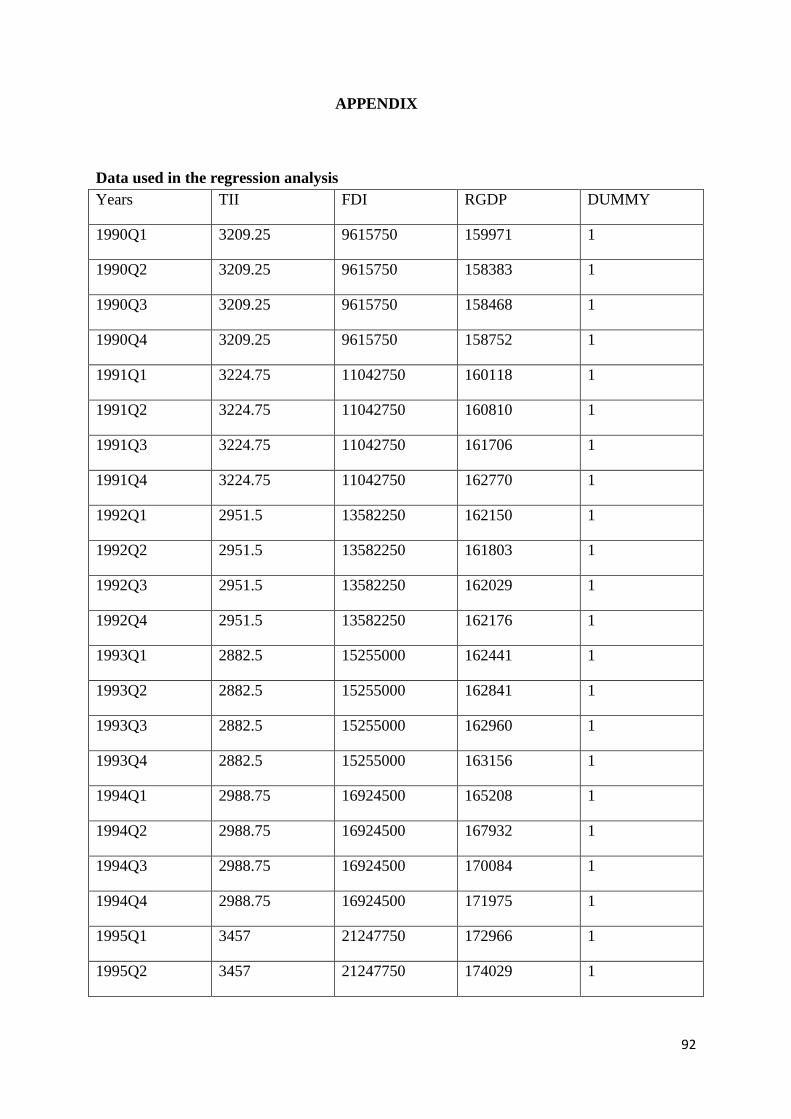

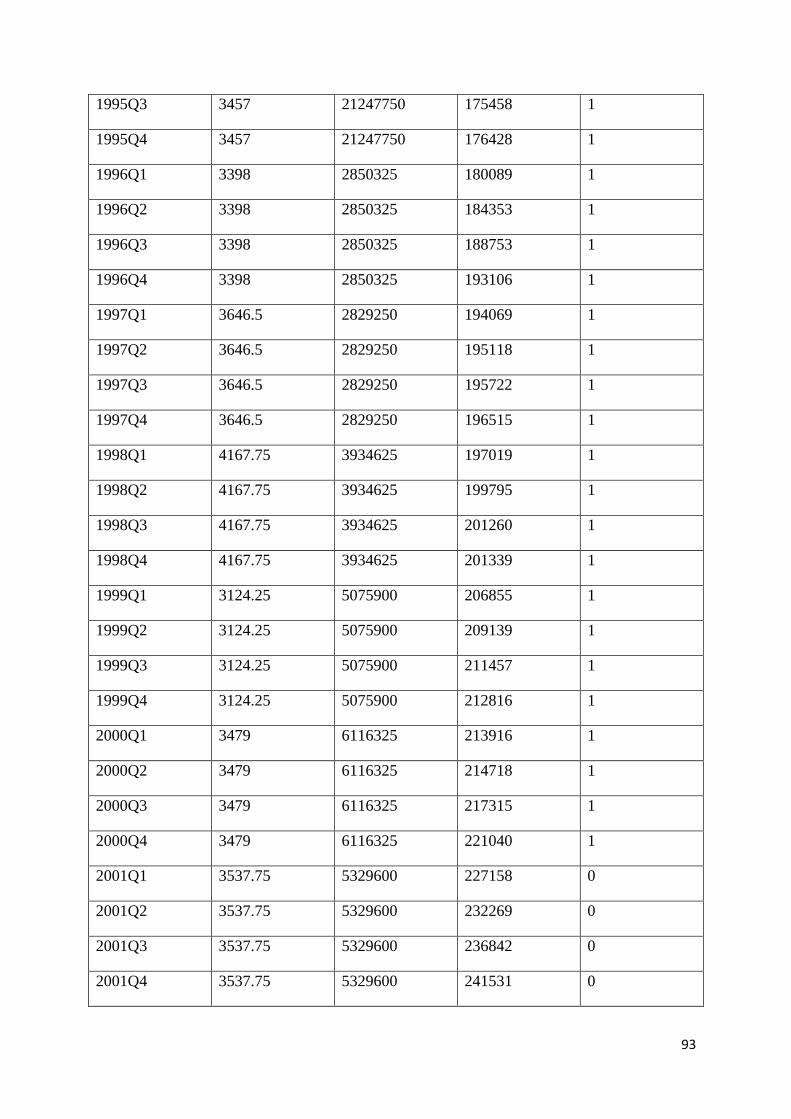

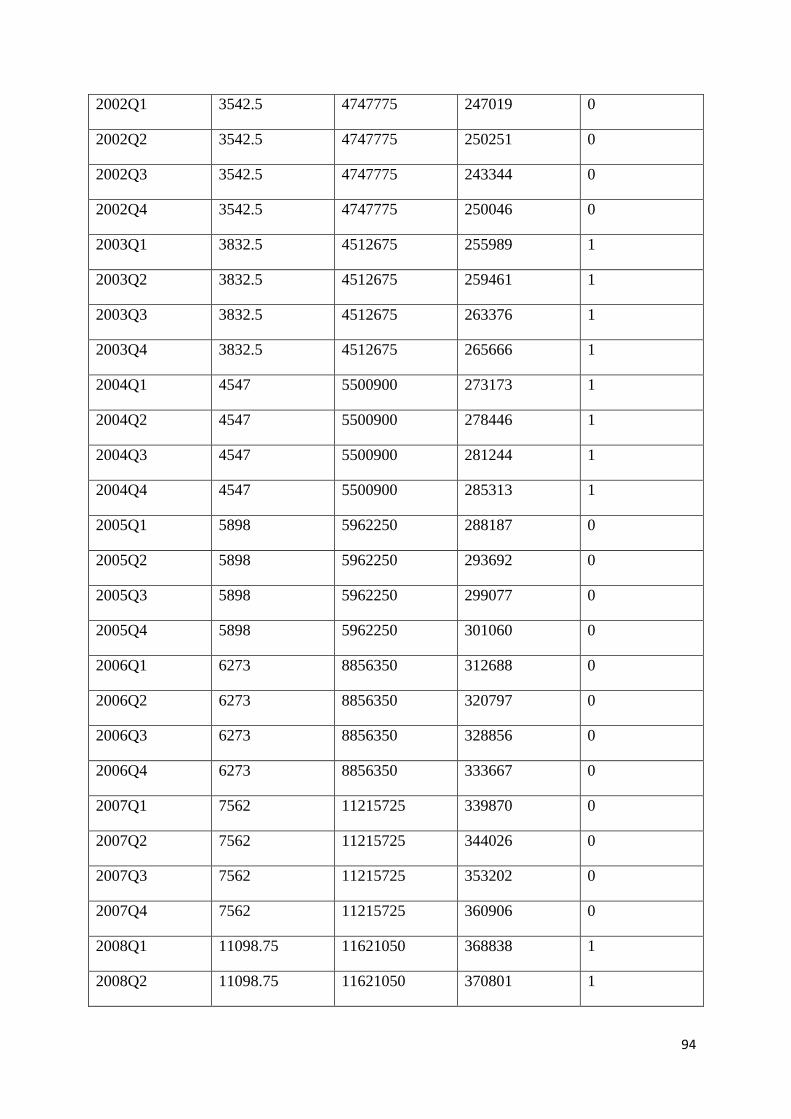

APPENDIX .......................................................................................................................................... 92

Data used in the regression analysis ..................................................................................................... 92

x

LIST OF TABLES

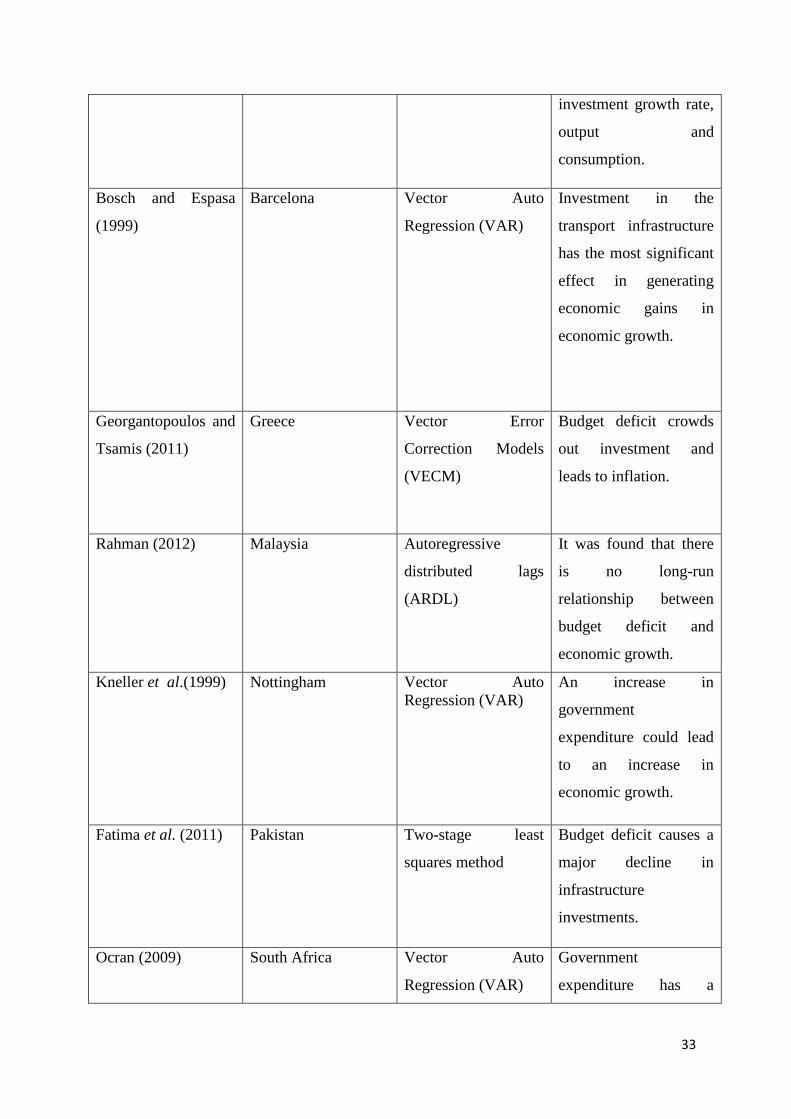

Table 2.1: Summary of selected empirical literature on the budget deficit and transport

infrastructure investment……………………………………………………………………..33

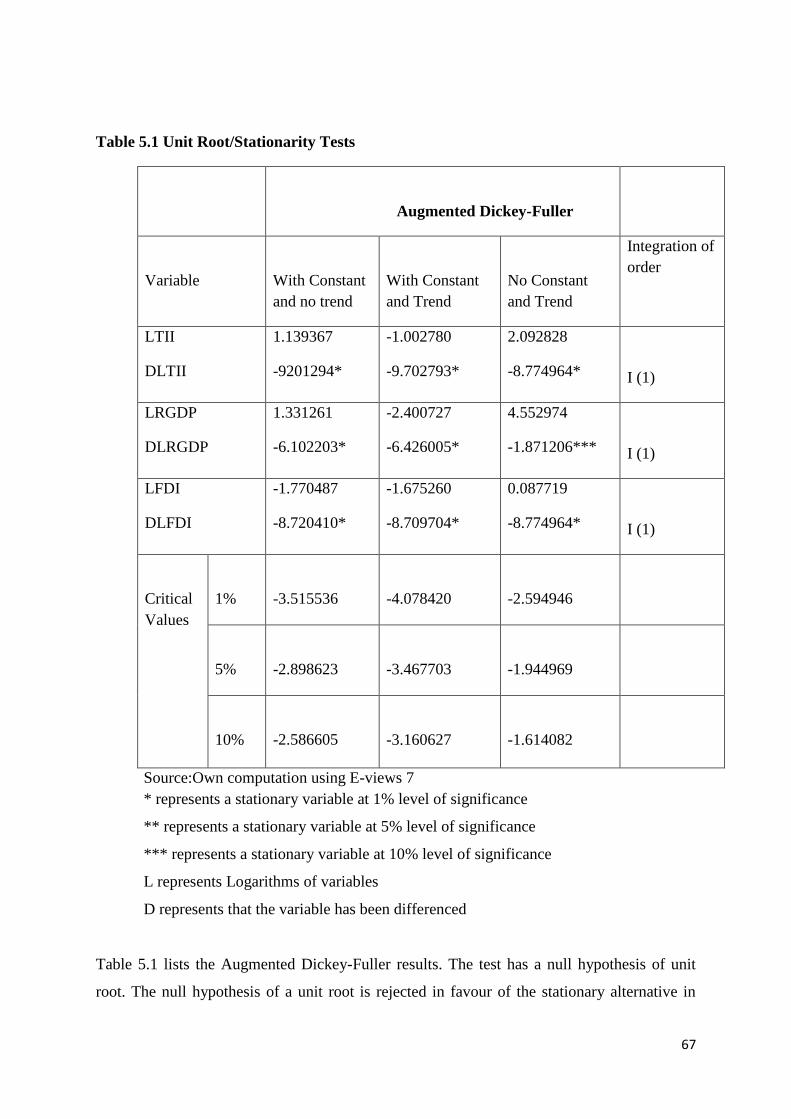

Table 5.1: Unit root/Stationarity Tests……………………………………………………….68

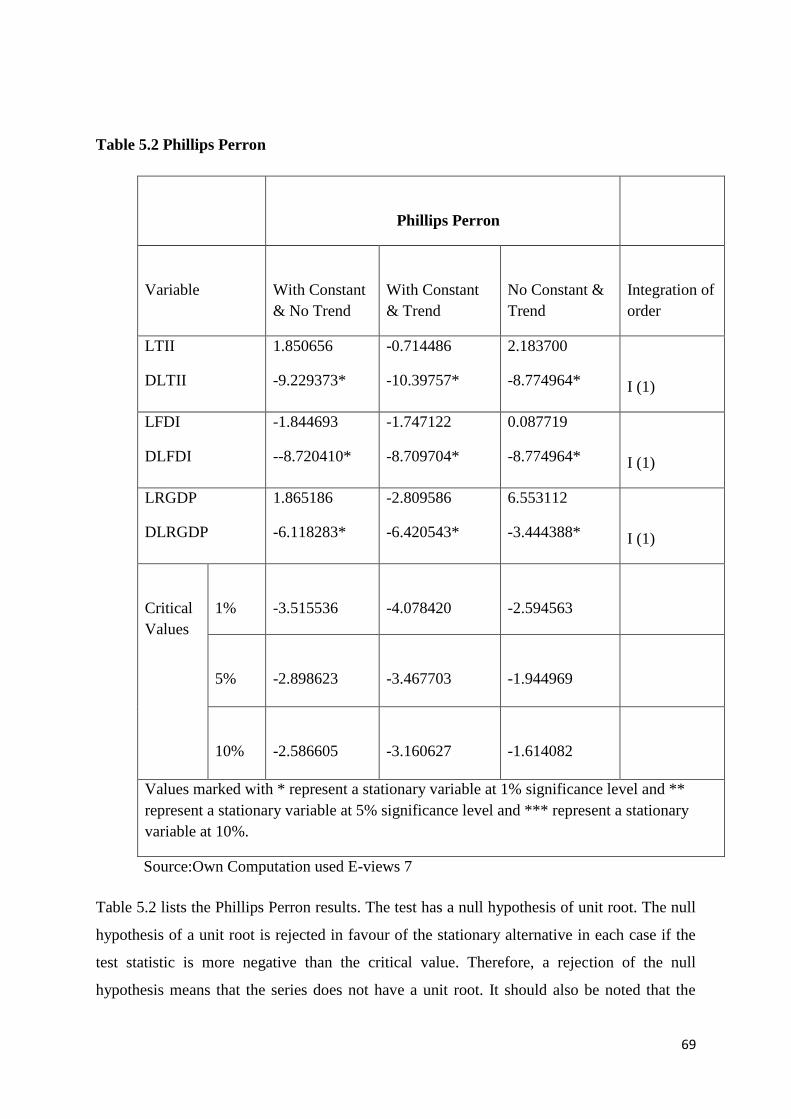

Table 5.2: Phillips-Perron……………………………………………...…………………….70

Table 5.3: Lag Length Criteria……………………………………………………………….72

Table 5.4: Johansen cointegration rank test results………………………………………….73

Table 5.5: Results of both the Long run and Short run Relationship………………………..75

Table 5.6: Results of the Diagnostic Tests…………………………………………………...77

Table 5.7: Variance Decomposition………………………………………………………….80

xi

LIST OF FIGURES

Figure 2.1: Solow Growth Model……………………………………………………………..7

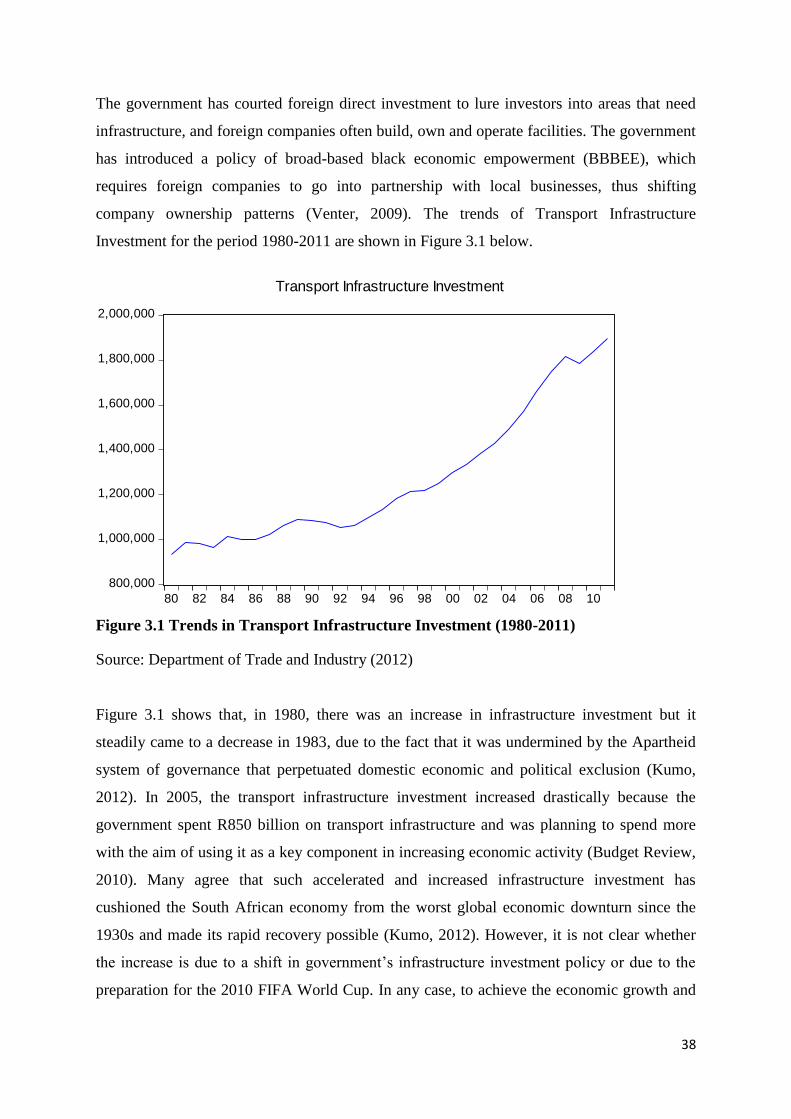

Figure 3.1: Trends in Transport Infrastructure Investment (1980-2011)..…………………...38

Figure 3.2: Trends in Government Revenue (1980-2011)…………………………………...40

Figure 3.3: Trends in Government Expenditure (1980-2011)……………………………….44

Figure 3.4: Trends in the budget deficit/surplus (1980-2011)………………………….…...46

Figure 3.5: Trends in foreign direct investment (1980-2011)………………………………..48

Figure 3.6: Trends in RGDP (1980-2011)…………………………………………………...51

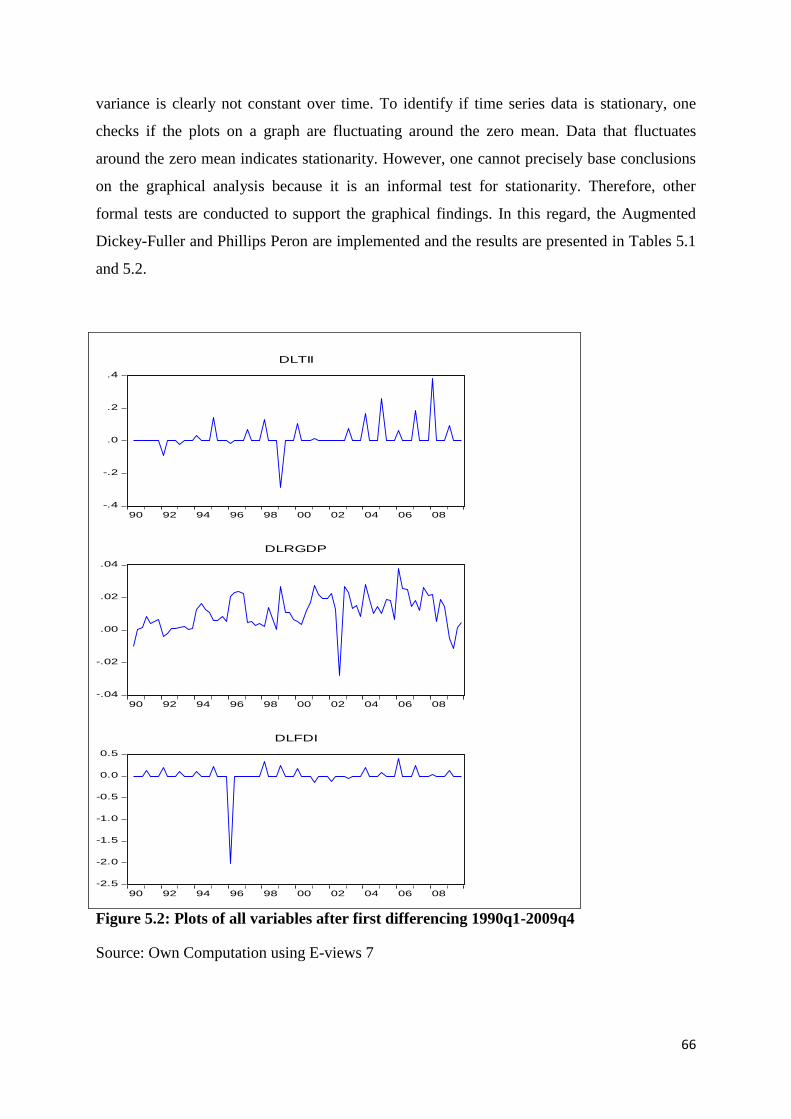

Figure 5.1: Plots of all variables in logarithm form 1990q1-2009q4………………………...66

Figure 5.2: Plots of all variables after differencing 1990q1-2009q4………………………...67

Figure 5.3: Johansen Cointegration Vector…………………………………………………..74

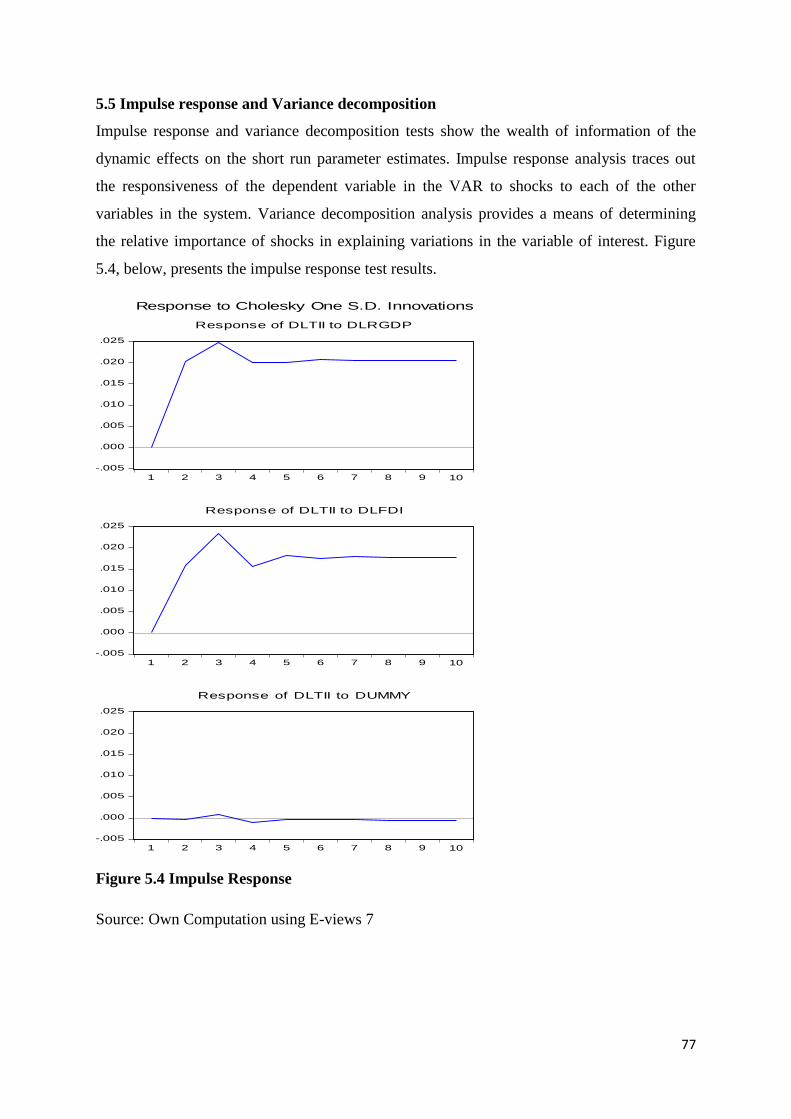

Figure 5.4: Impulse Response………………………………………………………………..78

1

CHAPTER ONE

INTRODUCTION

1.1 Background and Problem Statement

The term ‘budget deficit’ is described as the negative budget surplus whereby government

expenditure exceeds government revenue. Budget revenue includes three important

components, which are: tax revenue, tax exempt revenue and private revenues. The most

important component of the budget revenue is tax revenue. However, budget expenditure

involves four important elements, which are: current expenditure, investment expenditure,

real expenditure and transfer payments (Mwakalikamo, 2011). Current expenditure is the

kind of expenditure related to nondurable goods and services like the payment of wages and

salaries, and it is used for short term expenses. Investment expenditure is related to

investment and capital development, such as the construction of infrastructure and purchasing

of capital goods like tractors and other machines for production (Mwakalikamo, 2011).

Transfer payment includes grants and subsidies which have an indirect impact to the GDP. If

the budget expenditure exceeds budget revenue, which are both important components of the

budget, then it is stated to be a budget deficit.

Persistent government budget deficits and computing government debt have become major

concerns in both developed and developing countries. Extensive theoretical and empirical

literature has been developed to examine the relationship between budget deficits and

macroeconomic variables (Akinbobola and Oladipo, 2011). The monetarists share the view

that fiscal deficits are harmful to an economy. While some of the increases in the deficits

have been associated with declining tax revenue, resulting from the recession, others relate to

the increase in debt service payments on public debt. The development of a budget deficit is

often traced to the Keynesian inspired expenditure-led growth theory of the 1970s (Olomola

and Olagungu, 2004). Most countries of the world adopted the theory that the government has

to spend more in order to stimulate economic growth. However, its consequences on

macroeconomic variables cannot be underestimated in most countries of the world.

The South African government recognises the importance of transport infrastructure in

economic growth in South Africa. In South Africa, the improvement in public transport

infrastructure has served to link undeveloped and developed regions, such as towns and rural

2

areas, and it has been seen as the most valuable policy tool because it acts as a stimulus

during economic downturns (Negota, 2001). The improved transport infrastructure has also

improved trade, to a large extent, since goods can now be delivered without any transport

infrastructure complications (Negota, 2001). Public transport infrastructure investment in the

form of seaports, airports, rail and roads causes South Africa to move towards a sustained and

growing development (Fourie, 2006). This enables all South Africans, especially the poor, to

enjoy greater access to economic empowerment through job creation.

The Minister of Finance, Gordhan, in his budget speech stated that South Africa’s investment

in infrastructure gives impetus to growth in the economy (National Treasury, 2012). An

improvement in economic growth contributes towards the reduction of inequality, poverty

and the creation of decent work for people, especially for those who are not skilled (National

Treasury, 2012). In this regard, the New Growth Path which is currently a South African

macroeconomic strategy creates a way of making the South African economy more

developed and equitable for sustained growth. This strategy encourages stronger investments

in infrastructure, by both the public and private sectors, in order for the country to create the

necessary employment opportunities and at the same time reduce poverty.

Given these objectives of the government to stimulate the economy towards a higher growth

path, there are two primary instruments, amongst others, that a country can use, namely:

fiscal policy and monetary policies. A monetary policy is used mainly to regulate money

supply through interest rates (Mollentze & Van der Merwe, 2010). A fiscal policy on the

other hand, deals with government revenue through tax and expenditure (Nattrass, 2000 and

Ajam and Aron, 2007).

A budget is considered a useful tool of control utilised by companies. It can help set

developmental policies in the country. Budget is a record of the earning and spending of an

organization. When the actual expenditures are in conformity with the planned expenditure,

then planning becomes useful for that unit. Budget can either be a deficit or surplus. A budget

deficit results in situations where the expenditures of the country exceed its revenues, earned

from taxes and other sources. According to Sill (2005), the expenditure of an entity, which

exceeds its earning or income, has been termed a budget deficit. In the absence of financing

from external sources the deficit is carried forward to the next financial year. The deficit can

be a result of delays in the collection of revenues i.e. sales, taxes or other sources of revenues.

Budget revenues decrease due to erosion of the tax base, while expenditures most often rise

3

due to an increase in transfers to the population such as unemployment benefits, social

welfare, etc. (Anušić , 1994). The country entered a recession in 2008 with the government

already spending more than it was taking in tax. However, in any recession, the budget deficit

increases because of the automatic stabilizers that kick in where tax receipts fall and welfare

spending increases. That deficit will not last longer; it will change as soon as the country

experiences increasing returns in the economy.

South Africa reported a government budget deficit equal to 4.80 percent of the country's

Gross Domestic Product in 2011 (National Treasury, 1995). During this period 1989 until

2011, South Africa’s Government Budget averaged -3.03 percent of GDP reaching an all-

time high of 0.90 percent of GDP in December 2007 and a record low of -7.40 percent of

GDP in December 1992. Government Budget is an itemized accounting of the payments

received by government (taxes and other fees) and the payments made by government

(purchases and transfer payments).

Given this scenario of a budget deficit, if not funded by foreign aid and/or increased taxes,

the government may not invest in infrastructure. A lack of infrastructural investment may

lead to a decline in growth as well as job opportunities. However, given these large figures of

a budget deficit on GDP, the question at hand is: does the budget deficit have an effect on

infrastructure investments? How has the budget deficit affected the infrastructure investment

over the years, both in the long and short run? Lastly, what policy recommendations could be

implemented to reduce budget deficits?

1.2 Objectives of the study

The primary objective of this study is to investigate the impact of a budget deficit on public

transport infrastructure investment in South Africa. This broad objective is explored through

the following sub objectives:

To review the trends of both public transport infrastructure investments and budget deficit

from 1990-2009.

To investigate the short run and the long run response of the public transport

infrastructure investment to changes in the budget deficit from the period 1990-2009.

To make policy conclusions and recommendations based on the findings.

4

1.3 Hypothesis of the study

H0: Government budget deficit has a significant negative relationship with transport

infrastructure investment in South Africa.

HA : Government budget deficit does not have a significant negative relationship with

transport infrastructure investment in South Africa.

1.4 Significance of the study

The relationship between the budget deficits on transport infrastructure investment has

attracted a vast amount of literature from both theoretical and empirical fronts in recent years.

Many researchers investigated the relationship between the two, but they have reached

conflicting results. There is still a debate as to whether there is a positive relationship or a

negative relationship, if any, between budget deficit and transport infrastructure investment.

Therefore, this study seeks to fill in that gap by examining the relationship between the two

in South Africa.

1.5 Organisation of the study

Following this introduction, Chapter two reviews both the theoretical and empirical literature

pertaining to the relationship between public transport infrastructure investment and budget

deficit. The chapter made use of the following theories: the Harrod-Domar growth theory;

Robert Solow’s theory and the Endogenous Growth model. The empirical evidence

conducted was from developed and developing countries as well as South Africa specifically.

Chapter three provides an overview of trends in the relationship between public transport

infrastructure investment and budget deficit in South Africa. Chapter four discusses the

methodology and sources of data used in this study. Chapter five estimates the regression

model and interprets the results. Chapter six presents a summary of the study and policy

recommendations. The last chapter points out some limitations associated with the study.

5

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

The purpose of this chapter is to explore the various theories of infrastructure investment.

The Harrod-Domar growth theory, Robert Solow’s theory and the Endogenous growth theory

are discussed in this chapter. These theories are important in that they provide the

determinants and fundamental dynamics of infrastructure investment and economic growth.

This chapter is divided into three sections. The first section presents growth theories. The

second section deals with the empirical literature on infrastructure investment and budget

deficit from developed, developing countries and from South Africa. The last section

provides the concluding remarks of this chapter.

2.2 Theoretical Literature

This section is aimed at investigating the determinants of infrastructure investments.

Traditional theories of infrastructure investment, namely; the Harrod-Domar growth theory,

Robert Solow’s theory and Endogenous Growth Models are discussed herein.

2.2.1 Harrod-Domar Model

The Harrod-Domar model stipulates that growth depends on the quality of labour and

investment leads to capital accumulation which later affects the economic growth of a

country (Jones, 2013). This theory has the following assumptions:

1. Output is a function of capital stock i.e.

Y= f (K)

Where Y = Gross Domestic Product and K = Level of Capital Stock

2. The marginal product of capital is constant. This means that marginal and average products

of capital are equal.

3. The product of the savings rate and output equals investment.

sY= S= I

4. The change in the capital stock is equal to investment less depreciation of the capital stock.

6

ΔK= I- δ K

This theory states that in order for the country to grow it solely depends on government

expenditure on investments and savings. The development of a country includes the rate of

output growth solely the rate of infrastructure investment being made in which the

government has enough capital. The main strength of this theory is that the absence of the

economic shocks predicts economic growth in the short run.

2.2.2 Robert Solow Model

The neoclassical growth theory was developed by Robert Solow (1956), a prominent

economist of the twentieth century (Uwasu, 2006). In a nutshell, the Solow model predicted

that a country may experience growth accelerations and growth slowdowns. This model

consists of both a supply and demand side, but it focuses primarily on the supply side. With

reference to this study, this means that it focuses on government expenditures that tend to

have an effect on the public transport infrastructure investment which later affects the

economic growth of a country.

The Solow model states that an increase in the labour supply results in a larger output. This

can only happen if a lot of people take part in a country’s production (for example, if those

who are not part of the labour force start working); when the transport infrastructure takes

place, real output increases. Solow stated that a productivity increase can, for example, take

place when investments in equipment like computers and machinery reduce labour hours.

Productivity increases explain the increase in output that cannot be explained by labour and

capital (inputs), called the productivity of an input, and is affected by a lot of factors.

According to this model, the productivity of an input is affected by technological factors such

as differences in capital per worker and differences in knowledge (Burda and Wyplosz,

2001).

The theory starts with a simplified assumption that there is no technological progress in the

economy; that is, output is a function of the capital-labour ratio and is expressed as follows,

Y= f (K)………………………………………………………………………………….…..2.1

Y = output per head

K = capital per head

The Solow growth model is illustrated in Figure 2.1 below.

7

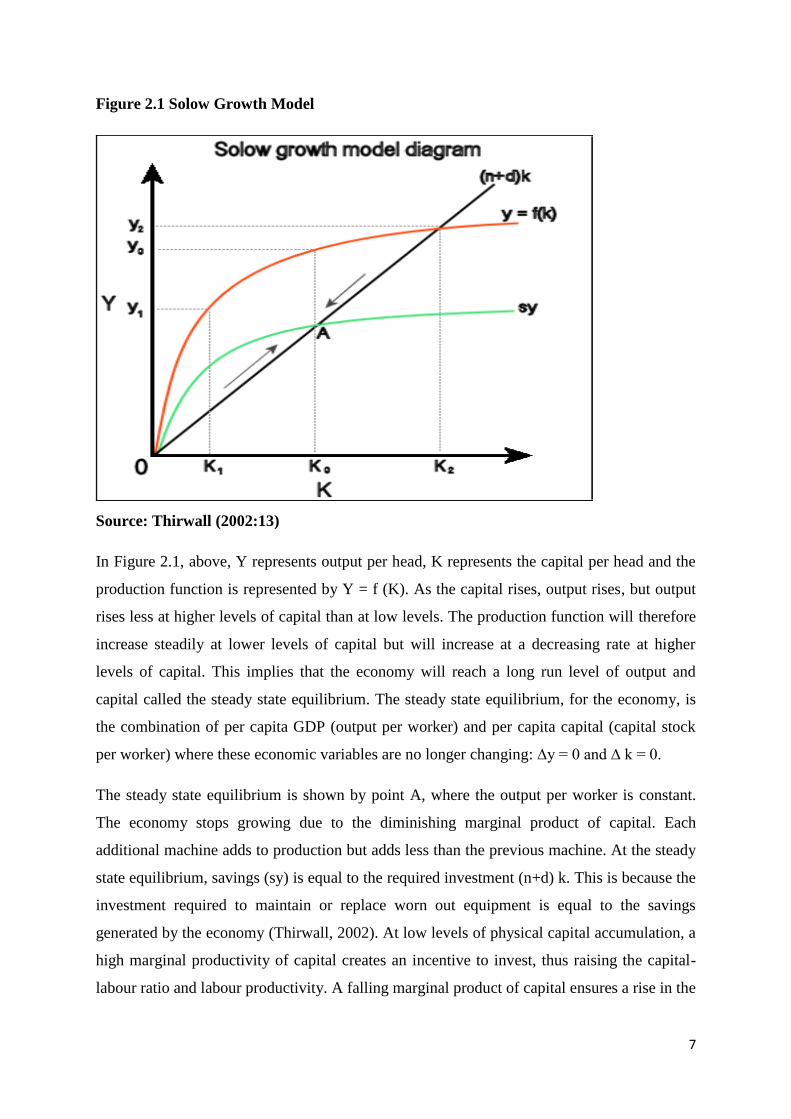

Figure 2.1 Solow Growth Model

Source: Thirwall (2002:13)

In Figure 2.1, above, Y represents output per head, K represents the capital per head and the

production function is represented by Y = f (K). As the capital rises, output rises, but output

rises less at higher levels of capital than at low levels. The production function will therefore

increase steadily at lower levels of capital but will increase at a decreasing rate at higher

levels of capital. This implies that the economy will reach a long run level of output and

capital called the steady state equilibrium. The steady state equilibrium, for the economy, is

the combination of per capita GDP (output per worker) and per capita capital (capital stock

per worker) where these economic variables are no longer changing: ∆y = 0 and ∆ k = 0.

The steady state equilibrium is shown by point A, where the output per worker is constant.

The economy stops growing due to the diminishing marginal product of capital. Each

additional machine adds to production but adds less than the previous machine. At the steady

state equilibrium, savings (sy) is equal to the required investment (n+d) k. This is because the

investment required to maintain or replace worn out equipment is equal to the savings

generated by the economy (Thirwall, 2002). At low levels of physical capital accumulation, a

high marginal productivity of capital creates an incentive to invest, thus raising the capital-

labour ratio and labour productivity. A falling marginal product of capital ensures a rise in the

8

capital-output ratio and a declining incentive to invest until a point is reached at which the

full savings (and hence investment) generated by the economy are employed in order to

supply new labour hours entering the workforce with the same capital intensity as existing

previous labour hours available for production.

The only way for the economy to grow or move from the steady state equilibrium is for the

economy to raise its savings level and maintain a lower labour force growth rate. This can

only happen if savings have risen relative to investment requirements and therefore more is

saved than required to maintain the capital per head constant. This higher savings rate implies

that there will be an incentive to invest, thus increasing the capital-labour ratio and labour

productivity. A high population growth rate leads to a decline in labour productivity

(Thirwall, 2002). A lower growth rate of the labour force allows the use of investment for the

purposes of capital deepening rather than capital widening; again, the consequence is a rising

capital-labour ratio and higher labour productivity. Both changes in the savings rate and

changes in the growth rate of the labour force result in a temporary change in the growth rate

of output as the economy moves towards a new steady state defined by the new savings rate

and labour force growth rate. In a steady state the natural growth rate of the economy would

again prevail (Fedderke & Simkins, 2006). With constant-returns-to-scale production, in the

short run, savings tend to increase the growth rate of output but they do not affect the growth

rate of output in the long run. The implication here is that a higher savings rate initially

increases output or growth but the economy will reach new steady state equilibrium in the

long run.

2.2.2.1 Limitations of the neo-classical growth model

The neo-classical growth model assumes that economies reach long run steady state

equilibrium and the only way for the economy to grow is through technological progress. It

however leaves the determinants or sources of this exogenous variable unexplained. The

model assumes that in the absence of shocks or technological change all economies will

diverge to zero growth. Rising per capita incomes are only a temporary phenomenon

resulting from a change in technology. Any increase in per capita income that cannot be

attributed to labour or capital is ascribed to what is known as the Solow residual. In his

empirical studies, Solow showed that approximately 50 percent of historical growth in

industrialised nations is attributed to the residual (Fedderke & Simkins, 2006). However, it is

impossible to analyse the determinants of technological advances because it is completely

independent (exogenous) of the decisions of economic agents. Another weakness of the

9

Solow growth model is that it fails to explain large differences in residuals across different

countries. The conception that poor countries will eventually catch up with developed

countries, if technological progress is the same, is not effective if there is no explanation of

the determinants of these technological advances (Fedderke & Simkins, 2006). In view of the

weaknesses of the Solow growth model, the new growth theory (endogenous) emerged;

hence, it is discussed in the next sub section.

2.2.3 Endogenous Growth Model

The main purpose of the endogenous growth model is to explain the existence of increasing

returns to scale and contradictory long term growth patterns. The endogenous growth theory

was formed by (Romer, 1986) and (Lucas, 1988). The endogenous growth model outlines

how human capital development as well as research and development (R&D) contribute to

long run economic growth. The endogenous growth model is based on two approaches taken

by the (Romer, 1986) and (Lucas, 1988) models. The theory assumes that there are positive

externalities associated with human capital formation (education and training, for example)

and research and development that prevent marginal product from declining (Thirwall, 2002).

The theory begins with the assumption that there are constant returns in production.

The endogenous growth theory is an extension of the Solow growth model, expressed as

follows:

Y = AK…………………………………………………………………………………..…2.2

Where Y = output

A = total factor productivity (technology)

K = physical and human capital

Equation 2.2 shows that output is proportional to capital. Total factor productivity represents

the marginal product of capital which is constant. The above formula of the endogenous

growth theory proposes that there is no decreasing marginal product of capital and

endogenises technological progress. Therefore, the production function has a constant

marginal product of capital. To prevent the decrease of marginal product of capital it was

proposed that the concept of capital be increased to include human capital (Lucas, 1988). The

concept of human capital, as outlined by Lucas (1988), is explained in the next subsection.

10

2.2.3.1 The Lucas Endogenous Growth Model

The Lucas (1986) approach of endogenous growth introduces the concept of human capital as

opposed to physical labour in the production function. Human capital refers to the knowledge

accumulation or skills gained by workers through learning by doing. The Lucas (1986) model

states that the growth rate of the economy will be determined by the rate of growth of human

capital creation. The Lucas (1986) model of endogenous growth is expressed as follows:

Y = AF (Kα, H

1-α)………………………………………………………………………….2.3

Where: Y = output

A = total factor productivity

K = capital

H= human capital

α and 1-α = output elasticities of the factor inputs. (α and 1-α=1).

Equation 2.3 above illustrates human capital as a component of the production function.

Capital not decreasing and human capital displaying positive externalities, such as education

and training, enables the economy to reach long run economic growth (Todaro and Smith,

2009). Firms and consumers invest in human capital by gaining knowledge. All inputs of the

production function can thus be accumulated. The growth of capital generates new

knowledge about production in the economy as a whole. Growth is then created by assuming

that the motivation to invest in human capital is non-decreasing in human capital (Todaro and

Smith, 2009). The Lucas model of endogenous growth suggests a production function of

human capital which has constant returns to scale in human capital but with the possibility of

increasing returns to scale. Hence, the marginal product of human capital that determines the

incentive to invest in knowledge accumulation is constant. The Lucas model assumes that

human capital relates to the skills and experience gained by the labour force. Investment in

human capital has a positive impact on the growth process. The second approach to

endogenous growth, by Romer (1986, 1990), is discussed in the ensuing subsection.

11

2.2.3.2 The Romer Model of Endogenous Growth

The second aspect of the new endogenous growth theory is in line with research and

development (R&D). The path that a country could take in order to not experience

diminishing returns in the long run would be technological progress. Spending on research

and development (R&D) is considered an investment in knowledge that translates into new

technologies as well as using the resources of physical and human capital that are already in

existence more efficiently. Romer (1986) focuses on research and development as an

important tool to knowledge accumulation. The model adds R&D to the original production

function. This is expressed as follows:

Y = A (R) f (Ri, Ki, Li)............................................................................................................2.4

Where: Y = output

A = total factor productivity

Ki = capital

Li = labour

Ri = stock of results from expenditure on R&D in firm i and where spill over from private

research efforts lead to improvements in the public stock of knowledge.

Equation 2.4, above, shows an augmented production function that includes R&D. In this

model, output is not only a function of capital and labour but also R&D efforts by firms.

Economies of scale are external to firms as technology will move across to other firms

resulting in an improvement in public knowledge. The Romer model of endogenous growth

through technological progress has characteristics of a public good, which states that it is

non-rivalry and partially-excludable. The creation of new knowledge by one firm is assumed

to have a positive external effect on the production possibilities of other firms because

knowledge cannot be perfectly patented or kept secret. With spill-over effects, knowledge

production is an inadvertent side-product of all production and investment activity, and

would take place whether firms wish to undertake it or not, as long as they are engaged in

their standard productive activity (Fedderke & Simkins, 2006). The marginal cost of using

new knowledge is assumed to be zero or close to zero. The low cost of using existing

knowledge is also assumed to lower the cost of producing new knowledge, this results in

dynamic scale economies in knowledge accumulation.

12

The effect of knowledge spill-over is to ensure that the efficiency of the labour input at the

social level improves. The consequence of this is that the production function shows

increasing returns to scale at the social level (because of constant social returns to capital).

Once social returns to scale in capital are constant, it immediately follows that the marginal

product of capital also becomes constant. Consequently, the incentive to invest does not

change with a rising capital labour ratio, since the marginal product of capital and hence the

profit rate is constant. The source of the non-declining incentive to invest in Romer’s (1986)

model arises due to knowledge spill-over, which ensures a non-declining marginal product of

capital (Fedderke & Simkins, 2006). To illustrate how a firm can internalize economies of

scale, Romer (1990) developed a new production function as illustrated below.

The production function is augmented to endogenize technological progress (Romer, 1990).

Y = f (K, L, H, A)……………………………………………………………………….…...2.5

Where: Y= output

K = capital

L = labour

H = human capital

A = stock of knowledge about technological progress

The above equation includes human capital in the production function and technology is no

longer exogenous. This is because technology occurs as a result of R&D. In conducting

R&D, human capital and knowledge of capital stock are used which make technology

endogenous to the firm. In conducting R&D, the firm obtains increasing economies of scale

due to the non-declining nature of capital stock and human capital. Long run growth depends

on the human capital devoted to research and on the effectiveness of the human capital

engaged in the research.

With R&D, there seems to be stronger consent that R&D may have a persistent effect on

growth. As R&D expenditure gets higher, the growth rates tend to be higher. To the end,

overall expenditure on R&D as a share of GDP has increased since the 1980s, in most

countries, mainly as a result of increases in R&D activity in the business sector. The

endogenous growth theory emphasizes that the long-run rate of growth is not explained by

population growth, as in the Solow model, but rather by knowledge accumulation (Foss,

1998). Romer (1986) and Lucas (1988) argue that technological progress is an effect of

13

targeted research and development. Research and development results in improvement in

technological progress which, in turn, attracts more investment and leads to increased

productivity.

2.2.3.3 Limitations of the endogenous growth model

The assumption of decreasing marginal product of capital and changing the shape of the

production function to the extent that it exhibits constant marginal product of capital, violates

economic principles. The changed assumption implies that a firm with twice as much

machinery will produce twice as much output. If doubling capital doubles output, then

doubling all factors including labour will more than double output; this suggests increasing

returns to scale. The issue here is that larger and larger firms become more efficient and there

would eventually be one firm dominating the entire economy. This possibility of this

occurring is lost and therefore, increasing returns to scale to all factors is ruled out (Thirwall,

2002). The assumption that a non-declining marginal product of capital occurs as a result of

knowledge spill-over is difficult to defend. This is because the knowledge spill-over may be

difficult to internalize but it takes time for the knowledge to move across to other sectors,

regions or countries. The public good characteristic of technology, on which the theory relies,

is therefore doubtful. Another weakness of the model is the approach of technological

advancement. Even though the development theory has proven that technology has an

explicit origin (investment in capital stock) it still remains unexplained as an internal activity

on the part of economic factors. Technology continues to happen unexpectedly as it is a by-

product of intentional activity directed not at technological change itself, but at a quite

different productive activity. The expectation is of a reward from the act of investment in

physical capital rather than from technological change (Fedderke & Simkins, 2006).

2.2.4 Assessment of the Theories

A number of growth theories have been reviewed; however, the traditional neo-classical and

endogenous growth theories become relevant for the study. The neoclassical and endogenous

growth theories use a production function based approach in identifying factors that

contribute to economic growth (transport infrastructure investment). The neoclassical growth

theory assumes that capital and labour are the fundamental determinants of economic growth.

Nevertheless, the theory predicts that an economy will reach a steady state equilibrium due to

the diminishing marginal product of capital and technology (exogenous) which is the only

source of economic growth. The weakness of the neoclassical theory is that it fails to explain

the determinants of this exogenous variable. The prediction of absolute convergence, where

14

developing countries with the same access to technology as developed countries will catch

up, is another weakness. It would be very hard for developing countries to catch up if

technological determinants are not known. The endogenous growth theory is also reviewed

due to these weaknesses.

The endogenous growth model endogenises technological progress. The theory outlines that

positive externalities, such as human capital development and R&D, prevent marginal

product from declining. Technological progresses, unlike the neoclassical theory, are

attributed to these positive externalities. Human capital development through knowledge

accumulation and skills development contributes positively to growth in output. Human

capital development results in non-declining marginal product of labour and the possibility of

increasing returns to scale in production. The endogenous growth theory also attributes

technological progress to R&D activities. The endogenous growth becomes relevant because

it attributes long run economic growth to positive externalities gained through activities such

as human capital and R&D.

2.3 Empirical Literature

2.3.1 Empirical Evidence from Developed Countries

Moudud (1998), in the Jerome Institute, used the Classical Growth Cycles model (CGC) in

the study of government spending and growth cycles. The investigation was to reveal the

different situations in which government expenditure can lead to both crowding-in and

crowding-out of output and employment. It was found that an increase in government budget

deficit lowers the savings rate, investment growth rate, output and consumption. Higher

government budget deficits stimulate the demand for bank credit, thus negatively affecting

the finance charges of firms to accumulate to their cash flows. Increases in government

deficit tend to lead to a decline in investments which result in crowding out effects.

Therefore, an expansionary government deficit lowers the bond prices, raises the interest rate

of bonds, increases the demand for consumption and, lastly, raises the demand for money. A

rise in a budget deficit leads to a crowd-out effect because it increases the interest rate which

later negatively affects investment and economic growth.

Cohen and Percoco (2003) examined the fiscal implications of infrastructure developments in

Washington. The objective of this paper was to discuss government’s fiscal management with

infrastructure investments and advance a policy proposal in that regard for the Latin

15

American Region. The empirical results showed that both developing and developed

countries have faced a budget deficit which led to a debt crisis resulting in most of the

infrastructure investment being delayed or cancelled. By doing this, legislations were passed

in order to attract new investors (such as foreigners) to support infrastructure development

programs that could no longer be implemented by the government. An increase in private

infrastructure spending is associated with higher or more public spending on infrastructure.

More infrastructure spending does eliminate poverty and contributes to the improvement of

economic performance.

Bosch and Espasa (1999), in their working paper in Barcelona, saw that transport

infrastructure is one of the direct measures used to make an impact in the growth rate and the

geographical distribution of economic activity. The study used the VAR method to see how

the changes in infrastructure investment affect economic growth; it uses marginal product

calculation to check the intensity of infrastructure investment towards GDP. The data

analyzed is from the period 1991-2008 and is taken from the Department of Economy and

Finance. In order for transport infrastructure to have a significant effect on the growth rate it

depends on the availability of public capital. Transport infrastructure is an important tool in a

country as it brings opportunities such as trade and interpersonal relations between countries.

Spending on infrastructure stimulates the U.S economy and investing in infrastructure goes

beyond improvements to the quality of roads, sewers, highways and power plants. These

investments not only generate significant economic returns but also generate an increase in

the tax revenue for the government. It was found that investment in the transport

infrastructure has the most significant effect in generating economic gains in economic

growth.

The research conducted by Copeland, Levine and Mallet (2011) has as its main objective a

discussion of policy issues associated with how infrastructure can be used as a mechanism to

benefit economic recovery. The report showed that, when the government has enough

resources to spend on infrastructure investments to stimulate a sluggish economy in the short

run it leads to positive returns on the productivity of the country. It is found that the returns

are larger than the cost with spending in infrastructure and that, with more investment, there

is an increase in productivity growth. An increase in infrastructure spending stimulates labour

demand when the labour market is underutilized because workers are hired to accept

construction projects. Higher deficits slow down economic growth in the long run because

16

the government’s borrowing of funds tends to crowd out private investments. The data used

was obtained from Sweden, during a study which explored whether there is a negative

relationship between the budget deficit and the exchange rate.

Aschauer (1989) conducted a study regarding the relationship between aggregate productivity

and the flow of government spending. He found very high estimates of the elasticity of

private output with respect to public capital: 0.35 to 0.45. He argued that having the

government spend more on military variables, meaning core infrastructure such as airports,

seaports, roads, railways and sewers, brings more productivity and growth to the economy.

Aschauer (1990) stated that under certain circumstances, public capital and private factors of

production of labour and private capital may be balancing factors of production so that an

increase in the stock of public capital increases the productivity of private factors of

production. However it thereby generates increased demand for labour and private capital

investment goods. Aschauer postulates that public capital can have both a direct and indirect

effect on private output. The direct effect occurs because public capital changes the level of

output by making private labour and capital inputs more or less productive. However, an

indirect effect occurs because an increase in public capital will have an influence on marginal

product of labour or capital. He stated that the government implementing an effective fiscal

policy is a good and correct way in which the government could manage its expenditure and

could be an efficient strategy.

Moudud (1999) investigated the effect of government spending in a growing economy. A rise

in the budget deficit increases the growth rate of output and employment. By increasing

effective demand, the rise in the budget deficit raises potential business profits, thereby

stimulating investment spending. The positive effect of the budget deficit can be augmented

by expansionary monetary policies that maintain low interest rates. This has the dual effect of

providing greater monetary stimulus from the deficit and keeping financial charges on

business debt low.

Barro (1990), in his article “Government Spending in a Simple Model of Endogenous

Growth”, explored the relationship between government spending and economic growth. It

stipulates that in order to remain with a positive growth rate of output per capita, in the long

run, there must be advanced technologies in the form of new investments being made and

new processes. This theory assumes that all resources such as labour and capital are being

17

fully utilized. It states that fiscal policy measures can have an effect on the long run of the

economy. The capital used by the government to finance infrastructure investment increases

only if the capital stock also increases. Barro (1990) identifies the existence of a positive

correlation between government spending and long-run economic growth. Barro (1990)

believed that expenditure on investment and productive activities is expected to contribute

positively to economic growth, while government consumption spending is expected to retard

growth.

Georgantopoulos and Tsamis (2011) explored the Macroeconomic Effects of Budget Deficits.

This paper examined the causal links between budget deficit (BD) and other macroeconomic

variables such as Consumer Price Index (CPI), Gross Domestic Product (GDP) and Nominal

Effective Exchange Rate (NEER) in Greece. The study employed the Cointergration test,

Granger-causality using Vector Error Correction Models (VECM) and Variance

Decomposition analysis for the period 1980-2009. Data figures are calculated by employing

data obtained from the World Development Indicators (i.e. the World Bank database) and

UNCTAD (United Nations database). The Augmented Dickey-Fuller (ADF) test has been

used to test the unit roots of the concerned time series variables. It was found that the printing

of more money due to the budget deficit resulted in inflation. Budget deficit reduces the

supply of loanable funds, driving up the interest rates, crowds out investment and causes

other currencies to appreciate the domestic currency and further deteriorate the trade deficit.

Higher interest rates attract foreign investors, who want to earn higher returns. Hence, budget

deficits raise interest rates (both domestic and foreign) causing net foreign investment to fall.

The research conducted by Rutkowski (2009) in Poland found that improvements in the

quantity and quality of public infrastructure can have a positive impact on growth in Poland;

this is in line with the theory and empirical literature on the subject. A significant effort has

been made in recent years to increase public capital spending and this has contributed

towards smoothening the economic downturn during the crisis. The study employed the

vector auto regression model on quarterly variables over the period 1999-2007. Impulse

response functions point to a positive relationship between public investment, private

investment and GDP growth.

18

Tien-Ming and Yuli (2003) used Hakkio’s (1996) model in regards to seven Asian countries

and eight Euro-currency countries over the years 1951 to 2001. The Time-Series Cross-

Section Regression was applied with the Seemingly Unrelated Regression (SUR) approach to

data from 15 countries, in investigating the relationship between fiscal deficits and exchange

rates. The empirical relationship between deficit reduction and exchange rate is unclear

because the theoretical relationship is ambiguous. Deficit reduction has different effects on

the exchange rate, with some effects leading to a stronger exchange rate and other effects

leading to a weaker exchange rate. Budget deficit reduction may affect interest rates and

exchange rates both directly and indirectly. Direct effects decrease the exchange rate, while

indirect effects increase exchange rates. Theory and evidence both warn that large budget

deficits pose real threats to macroeconomic stability and, consequently to economic growth

and development. An increase in the budget deficit will result in a reduction in investment

and an increase in the current account deficit. A public sector deficit could lead to an external

debt crisis because of foreign borrowing, while borrowing domestically could result in higher

real interest rates.

Adam and Bevan (2004) studied the relationship between fiscal deficits and the economic

growth for a panel of 45 developing countries over the period 1970–1999. The OLG model is

employed. The evidence found was that of a threshold effect at a level of the deficit around

1.5% of GDP. It was also found that there is an interactive effect between deficits and debt

stocks, with high debt stocks exacerbating the adverse consequences of high deficits. The

impact of the deficit is likely to be complex, depending on the financing mix and outstanding

debt stock. In particular, deficits may encourage growth if financed by limited seigniorage;

they are likely to discourage growth if financed by domestic debt; and to have opposite flow

and stock effects if financed by external loans at market rates.

Anušić (1994) looked at the impact of the budget deficit and inflation in Croatia. The study

made use of the Keynesian economic theory which states that the increase in budget deficit

will cause ceteris paribus, the increase in real interest rate reason being due to budget deficit

occurrence the aggregate national demand increases as well. He found that the budget deficit,

along with its potential increase and its impact on the economy can cause a decrease in real

gross investment, which is called the crowding-out effect.

19

Kneller, Bleamey and Gemmell (1999) investigated the effects of a fiscal policy on growth in

Nottingham. The outcome was that an increase in government expenditure, namely investing

in public transport infrastructure, could lead to an increase in economic growth. Using the

vector auto regression method, the study stipulated that government spending or investing in

transport infrastructure constitutes benefits such as time saving and reducing the costs of

congestions. The data used was collected from a panel of 22 OECD countries from 1970 until

1995. Government budget data come from the Government Financial Statistics Yearbook

(GFSY) and from the World Bank Tables.

Zhan (2009) shows that public investments boost aggregate demand which boosts

employment and utilizes flexibility on low income countries, especially during economic

downturns. The fiscal policy can affect the investment in public transport infrastructure

negatively in such a way that some countries are not always aware of the economic downturn

that will take place during times of recession. This results in badly designed projects being

implemented during a crisis because the country failed to plan in advance, or implement

policy goals effectively. This could be problematic for an economy because the infrastructure

investments take time to be designed and evaluated.

Chmura (2011) used qualitative research to determine the long term benefits of the

government investing in public transportation infrastructure. The increase in government

expenditure does have an economic impact that is positive because it benefits the regional

industries supporting the infrastructure being developed such as trucks and site development

and later the people employed to do the infrastructure work spend their income on goods and

services resulting in regional businesses benefiting from government expenditure; all this

encourages economic growth. The economic impact of government expenditure increases the

country’s capacity of its public transportation network which provides time savings for

businesses and residents travelling using public transport. The time saving leads to higher

productivity for the country and it halves the unemployment rate.

Spoehr, Burgan and Molloy (2012) found that government expenditure on public transport

infrastructure investment does increase productivity, competitiveness and the capacity of

business to deliver high quality services. This affects the economy positively in the short run

but, in the long run, it affects it negatively. This tends to be negative in the long run because

the country is in public debt through financing the transport infrastructure.

20

Cata (2004) investigated the relationship between investment, growth and budget deficit

ceilings and found that a budget deficit crowds out the net exports of goods and services

causing an appreciation of the exchange rate and increasing the country’s debt. This budget

deficit would also force the government to raise taxes and reduce public expenditure, thus

affecting infrastructure investment negatively.

In a report submitted by Yongding (2010) in China, about the impact of the global financial

crisis on the economy, it has been shown that government surplus or a deficit can affect

investment in that the higher the national deficit, the less money there is available for

investment. It will not necessarily be negative if the total amount of money available is still

adequate for investment. In the case of the United States, a large part of the government

deficit is offset by net imports with foreigners lending the U.S. government money. In this

case, foreign loans can be used to boost the investment which would have been reduced by

the deficit spending. Each year’s deficit adds to the cumulative deficit, the total of which

would be the outstanding government debt. If government debt becomes very large, as a

proportion of an economy’s size, investors in the government debt may begin to fear that the

government may simply print money. Such a solution to reduce debt would lower the value

of that government’s money, resulting in high inflation and high interest rates, as lenders

would demand higher returns to account for the decrease of the money. Such an event might

also lead to the government’s money being worth less in relation to money from other

countries.

Pereira and Andraz (2010) explored the economic and fiscal effects of investments in road

transport infrastructure by using the vector auto regression model VAR. They made use of

impulse responses and found that investment in transport infrastructure has been a powerful

tool to increase private investments, to create new permanent jobs and to promote long term

economic growth in all countries. Policies such as a budget deficit that would reduce

investments will result in lower long term economic growth as well as worse budgetary

conditions in the future. Pereira showed that changes in public investment in road

infrastructure in the U.S. are positively correlated with lagged changes in output and

negatively correlated with lagged changes in employment. The study used annual data from

the period 1980-1998 which was obtained from the regional accounts published by the

National Institute of Statistics.

21

Srivyal and Venkata (2004) investigated the budget deficits and other macroeconomic

variables using the cointegration approach and Variance Error Correction Models (VECM)

for the annual period 1970-2002. The study tries to reveal the effects of a budget deficit with

other macroeconomic variables such as nominal effective exchange rate, GDP, Consumer

Price Index and money supply (M3). The Phillips Perron (PP) that allows weak dependence

and heterogeneity in residuals was employed, as well as the Engle and Granger (1987) and,

lastly, the maximum-likelihood test procedure established by Johansen and Juselius (1990)

and Johansen (1991). The empirical results reveal that the variables under study are

cointegrated and there is a bi-directional causality between budget deficit and nominal

effective exchange rates. However, it has not observed any significant relationship between

budget deficit and GDP, money supply and Consumer Price Index. It is also observed that the

GDP Granger causes budget deficit whereas budget deficit does not.

Chakraborty (2002) examined the real or direct and financial crowding out of investments.

An asymmetric vector autoregressive (VAR) model was employed. Data was drawn from the

new series of National Account Statistics published by the Central Statistical Organisation,

the Handbook of Statistics on Indian Economy, Reserve Bank of India. The period of analysis

is 1970–7 to 2002-03. The empirical results found that fiscal deficit does not put upward

pressure on the interest rate and high fiscal deficit affects capital formation in the economy

both by reducing private investment through an increase in the interest rate and through

reduction in the public sector’s own investment arising out of ever-increasing consumption

expenditure.

Goyal (2004), using monthly data, argues that there is a two-way causality between fiscal

deficit and interest rates. It was outlined that interest rates did not rise in recent years in spite

of high fiscal deficits because of larger liquidity available to the system. The Reserve Bank of

India has noted that raising public sector investment to boost aggregate demand in the

economy crowds-out both private consumption and investment with no long-lasting impact

on output. On the other hand, infrastructure investment by the public sector crowds-in private

investment while public investment in manufacturing crowds-out private investment.

Schäuble (2012), the Minister of Finance, stated that Germany's 2010 federal budget shows

that the country experienced a record-high deficit of well above €50 billion. Public-sector

debt surpassed €1.7 trillion, approaching 80% of GDP. The financial crisis and the ensuing

22

recession only went so far as explaining the high levels of indebtedness. The results show that

once a government's debt burden reaches a threshold perceived to be unsustainable more debt

will only stunt, not stimulate, economic growth.

Ball and Mankiw (1995) explored the case of the United States from 1960 to 1994. They

came to the same conclusion as that of research conducted on the pattern of government

expenditures for 30 developing countries. Huge budget deficits had significantly reduced the

level of national savings and private investment. Apart from that, high budget deficits will

signal to the citizens that the government has lost control in managing its funds. It was found

that the countries that faced budget deficits have a lower growth rate in comparison to

countries that faced a budget surplus. A continuous rise in budget deficits will also lead to the

problem of bankruptcy. As a result, the investors will have less confidence to invest in a

country and it will further reduce the economic growth of a country. Apart from that, the

budget deficit can also reduce the economic growth of a country based on the perspective of

politics and the election process.

Cogito (2010) found that there were large deficits in Canada which resulted in a rapidly

growing federal government debt. There has been a fierce debate over how the federal and

provincial budget deficit affected long-term growth. The supply of available funds for

investment decreases. This will result an increase in interest rates because of scarcity of

available funds. This higher interest rate then alters the behavior of firms that participate in

the loan market. Many demanders of loanable funds are discouraged by the higher interest

rate. Fewer families buy new homes and fewer firms choose to build new factories. The fall

in the investment, because of government borrowing, is called crowding out.

2.3.2 Empirical Evidence from Developing Countries

The Organisation for Economic Co-operation Development (OECD) (2002), using the cost

benefit analysis, found that investing in public transport infrastructure causes the resources to

be allocated and used efficiently in a country. Government expenditure increasing to invest in

transport infrastructure improves the accessibility of economic activities leading to an

increase in the market size for manufacturing, tourism and competitiveness. Investment in

transport infrastructure does encourage economic development in underdeveloped regions by

generating employment and improved environmental outcomes.

23

A study by Raju and Mukherje (2010) of fiscal deficit, crowding out and the sustainability of

economic growth in India from 1980-2009 shows that there is no long run relationship

between the variables. The study applied unit root tests and cointegration techniques that

allow for endogenously determined structural breaks. It was found that there is either

crowding in or crowding out of public spending and investment and the findings are in line

with the ricardian equivalence theory that implies that it does not matter whether a

government finances its spending with debt or tax increases. The convergence in fiscal deficit

and debt has helped to accelerate the rate of investment in the economy in the medium run.

Bose, Harque and Osborn (2007) investigate the relationship between budget deficit and

economic growth for 30 developing countries, from 1970 to 1990. By using panel data

analyses, they found that the budget deficit helps the economy to grow provided that the

deficits were due to productive expenditures such as education, health and capital

expenditures. The same conclusion is derived based on the research done by Fischer. A huge

budget deficit helps Morocco and Italy to grow since the excessive spending helps to increase

the level of private consumption in the short-run. It was due to the deficits which were used

to reduce the burden of taxation from the consumers’ perspective. In the long-run, huge

budget deficits ruined the level of economic growth for these two countries since they have to

struggle in paying back all the national debts.

Ramzan, Saleem and Butt (2013) explored the impact of budget deficit on economic growth

in Pakistan. Time series data was used for the period 1980 to 2010 and the study used

regression analysis. The Pearson Correlation test was also applied to check the relationship

among independent variables. The analysis reveals that the model was a good fit. The results

showed that there is moderate correlation between budget deficit and investment.

Odhiambo, Momanyi, Frederick and Othuon (2013) investigated the relationship between

fiscal deficits and economic growth in Kenya. The study used both exploratory and causal

research designs and employed time series secondary data for a period of 38 years (1970-

2009) and was estimated using the OLS method as well as the Johansen Cointegration test.

The study also performed various econometric tests such as the Dickey Fuller (DF) and

Augmented Dickey Fuller (ADF) unit root test as well as the error correction model.

Diagnostic tests, like multicollinearity, were also performed. The study found a positive

relationship between budget deficits and economic growth, in line with the Keynesian

24

assumptions and hence recommends prudent financial management and enhanced revenue

collection by revenue authorities so as not to crowd-out private sector investment by

borrowing domestically.

Kukk (2004), in a working paper about the effect of fiscal policy on economic growth in both

the short run and the long run, found that government revenue and government expenditure

have a significant effect on GDP because public investments are positively related to growth.

With the government improving its expenditure when it is needed the best results in GDP

growth can be achieved. By raising taxes and increasing investments the government could

experience accelerated growth rates. Using the cost function modelling approach and

augmented dickey fuller test for checking the unit roots it was found that underinvestment in

transport infrastructure was largely responsible for low levels of growth rates in output.

Roy, Heuty and Letouze (2006) investigated the fiscal space for public investment in

Singapore; they found that public investment has been declining since the 1980s especially in

public investment in infrastructure due to fiscal conditions such as the country experiencing a

fiscal deficit. A fiscal deficit is an important cause for the decline of public investments and

slows down economic growth. Public investments such as infrastructure have an important

role in kick starting economic growth, reducing the unemployment rate and, in turn, reducing

poverty. They used time series data from the period 1970-2000 that was obtained from the

International Monetary Fund.

Rahman (2012) explored the relationship between budget deficit and economic growth from

Malaysia’s perspective. Four variables were used, namely: real GDP, government debt,

productive expenditures and non-productive expenditures. The ARDL approach is used to

analyse the long-run relationship between all series since it can cater for a small sample size.

By using quarterly data from 2000 to 2011, it was found that there is no long-run relationship

between budget deficit and economic growth in Malaysia. However, productive expenditure

has a positive long-run relationship with the economic growth.

Hadiwibowo (2010) finds significant relationships between fiscal policy variables such as

government expenditure and government revenue and investments. In this study, the vector

error correction model was employed to investigate fiscal policy, investments and economic

growth in Indonesia. The study uses data obtained from Statistics Indonesia, Ministry of

25

Finance, world development indicators; it uses quarterly time series data from 1969-2008.