The Hybrid Domestic Asset Protection Trust By Steven J. Oshins ...

22

The Hybrid Domestic Asset Protection Trust By Steven J. Oshins, Esq., AEP (Distinguished) i This article was adapted and updated from a previously published article cited as “Steve Oshins & The Hybrid Domestic Asset Protection Trust,” LISI Asset Protection Newsletter #200 (May 10, 2012). Background Asset protection has become one of the hottest areas of law and has become the ideal complement to estate planning. Consequently, the Domestic Asset Protection Trust (“DAPT”) has become one of the most popular asset protection tools in the planner’s toolbox. As more states have enacted DAPT legislation, practitioners have started doing more DAPTs for their clients. After approximately 16 years since the first DAPT legislation passed, no non- bankruptcy creditor has challenged a DAPT all the way through the court system and been able to access any DAPT assets. Most likely this is because such a large supermajority believes that if tested the DAPT will work to protect its assets from a creditor of the settlor. However, despite the very high likelihood of protection, if there is a way to increase the odds of success even more, then such a strategy should be utilized whenever possible. The Hybrid Domestic Asset Protection Trust The Hybrid Domestic Asset Protection Trust (“Hybrid DAPT”) is a strategy that should increase the probability that the trust assets will be protected. And it is very simple. The Hybrid DAPT is just like a regular DAPT except that the settlor isn’t an initial discretionary beneficiary of the trust, but can be added later. Thus, the trust is initially set up for the benefit of the settlor’s spouse and descendants, for example, but not for the settlor. By not including the settlor as a beneficiary of the trust, the Hybrid DAPT is by definition a third-party trust and therefore almost certainly avoids the potential risk of uncertainty of a regular DAPT. The Hybrid DAPT strategy can be used either with a completed gift or incomplete gift version of the DAPT technique. Especially where the settlor is married and has a strong, trusting relationship with his or her spouse, is there any good reason that the settlor must have his or her name in the trust agreement as a beneficiary? It is very simple to indirectly access the trust assets through the spouse. And the trust agreement should define the “spouse” using a “floating spouse provision” that says that the spouse is the person the settlor is married to and living with from time to time. This gives the settlor the ability to access the trust assets through a subsequent spouse in the event of a divorce or the death of the settlor’s current spouse.

Transcript of The Hybrid Domestic Asset Protection Trust By Steven J. Oshins ...

The Hybrid Domestic Asset Protection Trust

By Steven J. Oshins, Esq., AEP (Distinguished)i This article was adapted and updated from a previously published article cited as “Steve Oshins & The Hybrid Domestic Asset Protection Trust,” LISI Asset Protection Newsletter #200 (May 10, 2012). Background

Asset protection has become one of the hottest areas of law and has become the ideal complement to estate planning. Consequently, the Domestic Asset Protection Trust (“DAPT”) has become one of the most popular asset protection tools in the planner’s toolbox. As more states have enacted DAPT legislation, practitioners have started doing more DAPTs for their clients.

After approximately 16 years since the first DAPT legislation passed, no non-bankruptcy creditor has challenged a DAPT all the way through the court system and been able to access any DAPT assets. Most likely this is because such a large supermajority believes that if tested the DAPT will work to protect its assets from a creditor of the settlor. However, despite the very high likelihood of protection, if there is a way to increase the odds of success even more, then such a strategy should be utilized whenever possible.

The Hybrid Domestic Asset Protection Trust

The Hybrid Domestic Asset Protection Trust (“Hybrid DAPT”) is a strategy that should increase the probability that the trust assets will be protected. And it is very simple. The Hybrid DAPT is just like a regular DAPT except that the settlor isn’t an initial discretionary beneficiary of the trust, but can be added later. Thus, the trust is initially set up for the benefit of the settlor’s spouse and descendants, for example, but not for the settlor. By not including the settlor as a beneficiary of the trust, the Hybrid DAPT is by definition a third-party trust and therefore almost certainly avoids the potential risk of uncertainty of a regular DAPT. The Hybrid DAPT strategy can be used either with a completed gift or incomplete gift version of the DAPT technique.

Especially where the settlor is married and has a strong, trusting relationship with his or her spouse, is there any good reason that the settlor must have his or her name in the trust agreement as a beneficiary? It is very simple to indirectly access the trust assets through the spouse. And the trust agreement should define the “spouse” using a “floating spouse provision” that says that the spouse is the person the settlor is married to and living with from time to time. This gives the settlor the ability to access the trust assets through a subsequent spouse in the event of a divorce or the death of the settlor’s current spouse.

If the settlor has no spouse, then it becomes more difficult to access the assets. However, since a good asset protection planner will be sure to leave sufficient wealth outside of the client’s asset protection trust, in most cases the settlor won’t have to work through this issue anytime soon.

If the Settlor is added as a Beneficiary

In case the settlor needs to be a discretionary beneficiary of the Hybrid DAPT sometime in the future (i.e., if the settlor has no spouse or child that will “share” a distribution with the settlor and the settlor now needs a distribution), the trust agreement provides that the trust protector can add additional beneficiaries, including the settlor. However, if the settlor is added, then the Hybrid DAPT becomes a regular DAPT and thus risks that the law is still unsettled on DAPTs (even though most people believe that they work).

What happens if the settlor suspects that a creditor attack may be forthcoming? Or what if the settlor is considering filing bankruptcy? In either case, very far in advance of the problem occurring, the settlor would ask the trust protector to remove him or her as a discretionary beneficiary.

§548(e) of the 2005 Bankruptcy Act It is extremely unlikely that a DAPT settlor will file for bankruptcy, especially if the settlor has an “old and cold” DAPT that is past the applicable state’s statute of limitations period. In fact, of the hundreds of DAPTs created by the author of this article, not one of those clients has gone through bankruptcy. However, in maintaining the philosophy of this article that it is important to build into the structure every safeguard available, it is interesting to note that the Hybrid DAPT most likely does not fit the definition required by §548(e) of the 2005 Bankruptcy Act that would otherwise potentially claw back the assets of a traditional DAPT. The requirements of §548(e) are as follows: (1) In addition to any transfer that the trustee may otherwise avoid, the trustee may avoid any transfer of an interest of the debtor in property that was made on or within 10 years before the date of the filing of the petition, if— (A) such transfer was made to a self-settled trust or similar device; (B) such transfer was by the debtor; (C) the debtor is a beneficiary of such trust or similar device [emphasis added]; and (D) the debtor made such transfer with actual intent to hinder, delay, or defraud any entity to which the debtor was or became, on or after the date that such transfer was made, indebted.

Unless the settlor is added as a discretionary beneficiary of the Hybrid DAPT, Subsection (C) doesn’t apply. Also, arguably Subsection (A) doesn’t apply either

since the Hybrid DAPT isn’t a “self-settled trust or similar device” at the time the provisions are applied.

The Completed Gift Hybrid DAPT

Many DAPTs are designed as Incomplete Gift DAPTs where the sole objective is asset protection. However, many DAPTs are designed as Completed Gift DAPTs where the settlor is a discretionary beneficiary of a trust designed with the following attributes:

(i) It’s a completed gift for gift tax purposes, (ii) The settlor is a discretionary beneficiary, (iii) The trust assets are protected from the settlor’s beneficiaries, and (iv) The trust assets are outside of the settlor’s estate for estate tax

purposes at the settlor’s death.

The Completed Gift DAPT strategy was approved by the Service in PLR 200944002 where a resident of a DAPT jurisdiction established the DAPT using the laws of that DAPT jurisdiction.

However, with respect to a resident of a non-DAPT jurisdiction, although most practitioners are comfortable that this strategy works, whether the trust assets are open to creditors of the settlor is still uncertain since it is unclear which state law will apply for creditor purposes. The DAPT will be includible in the settlor’s estate at death if the trust assets are open to the settlor’s creditors. If this were the case, this would occur under IRC §2036(a)(1) since the settlor would be treated as retaining the ability to run up creditor debts which can be paid out of the trust at the settlor’s death.

IRC § 2036(a)(1) provides that the value of the gross estate shall include the value of all property to the extent of any interest therein of which the decedent has at any time made a transfer (except in the case of a bona fide sale for an adequate and full consideration in money or money's worth), by trust or otherwise, under which the decedent has retained for life or for any period not ascertainable without reference to the decedent's death or for any period that does not in fact end before death the possession or enjoyment of, or the right to the income from, the property.

The Completed Gift Hybrid DAPT reduces this risk significantly since the settlor isn’t a discretionary beneficiary of the trust and, thus, it isn’t a self-settled trust. In an ideal scenario, the settlor will never need to be added as a discretionary beneficiary by the trust protector. However, if the settlor does need to be added at a later date, since the Completed Gift Hybrid DAPT also gives the trust protector the power to remove beneficiaries, as long as the settlor is removed as a discretionary beneficiary more than three years prior to death, there is no

estate tax inclusion since IRC §2035 (the three-year contemplation of death rule) won’t apply.

Down and Dirty

To this date, no non-bankruptcy creditor has challenged a DAPT all the way through the court system and been able to access any DAPT assets. Although the cases have settled or the creditors have decided not to sue, the estate or asset protection planner must still consider how to plan if the law does go the wrong way. Unfortunately, although there will ultimately be case law in a non-bankruptcy scenario, whether good or bad, unless the case law goes through the appeal process and is ultimately decided by the highest court, we still won’t have any certainty. So it is prudent to plan for this uncertainty.

If the settlor has set up a Hybrid DAPT, whether as an Incomplete Gift Hybrid DAPT or as a Completed Gift Hybrid DAPT, if the settlor wants to be sure to preserve a portion of the Hybrid DAPT’s assets if the settlor is being added in as a discretionary beneficiary, the trustee can split the Hybrid DAPT into two separate trusts and the trust protector can add the settlor as a discretionary beneficiary of only one of the two trusts so as not to taint the other trust.

For example, if there are $10 million of assets in the Hybrid DAPT, the trustee might divide the trust into two trusts – the “Clean Hybrid DAPT” which doesn’t include the settlor as a discretionary beneficiary and has $8 million of assets, and the “Dirty Hybrid DAPT” which includes the settlor as a discretionary beneficiary and has $2 million of assets. Thus, the risk has been transferred away from the Clean Hybrid DAPT to the Dirty Hybrid DAPT (which, again, should be protected, but is potentially being sacrificed in the interests of not tainting the assets in the Clean Hybrid DAPT). This is nothing more than a risk management decision.

Summary

It is imperative that the asset protection planner create a plan with the highest probability of success. In most cases, it is possible to significantly increase the protection by simply using a Hybrid DAPT rather than a traditional DAPT. This article describes this structure and also creates a further structure where the Hybrid DAPT can be divided into a Clean Hybrid DAPT and a Dirty Hybrid DAPT so that even if the Dirty Hybrid DAPT is unsuccessful, it doesn’t taint the Clean Hybrid DAPT.

i Steven J. Oshins, Esq., AEP (Distinguished) is an attorney at the Law Offices of Oshins & Associates, LLC in Las Vegas, Nevada, with clients throughout the United States. He is listed in The Best Lawyers in America®. He was inducted into the NAEPC Estate Planning Hall of Fame® in 2011 and was named one of the 24 Elite Estate Planning Attorneys in America by the Trust Advisor. He has authored many of the most valuable estate planning and asset protection laws that have been enacted in Nevada.

Steve Oshins is a member of the Law Offices of Oshins & Associates, LLC in Las Vegas, Nevada. He is rated AV by the Martindale-Hubbell Law Directory and is listed in The Best Lawyers in America®. He was inducted into the NAEPC Estate Planning Hall of Fame® in 2011 and has been named one of the 24 “Elite Estate Planning Attorneys” by The Trust Advisor and one of the Top 100 Attorneys in Worth. He can be reached at 702-341-6000, ext. 2 or [email protected]. His law firm’s website is www.oshins.com.

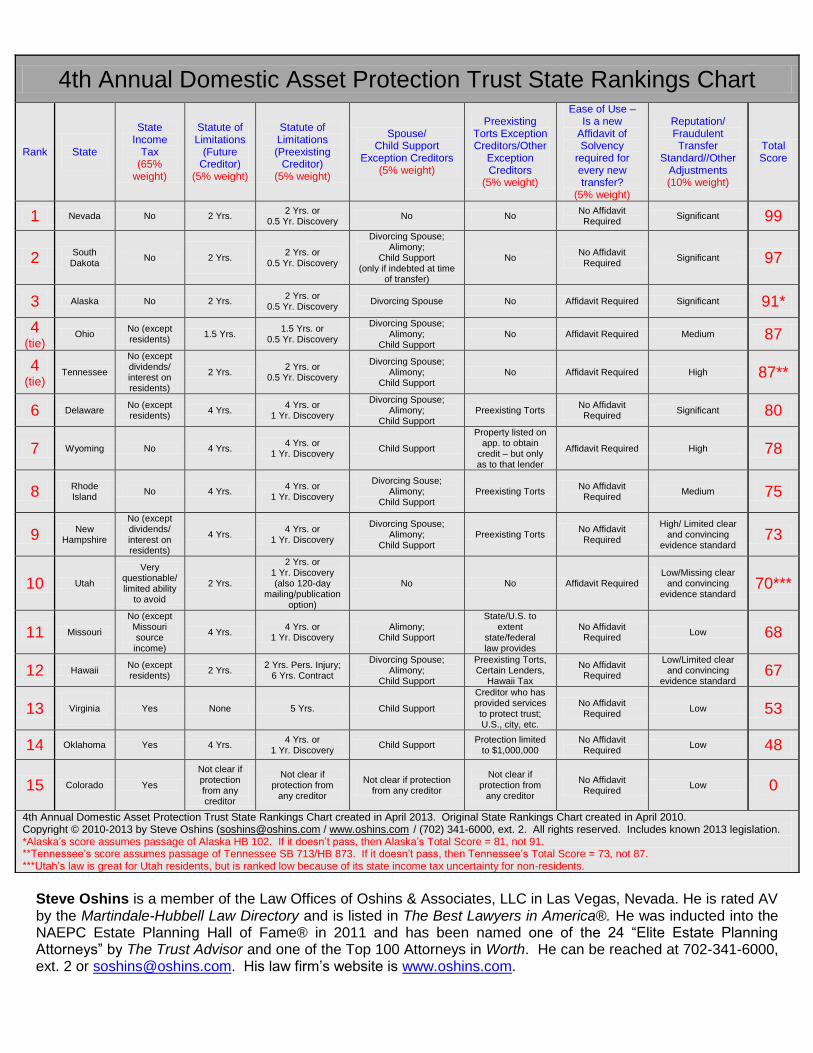

4th Annual Domestic Asset Protection Trust State Rankings Chart

Rank

State

State Income

Tax (65%

weight)

Statute of Limitations

(Future Creditor)

(5% weight)

Statute of Limitations (Preexisting

Creditor) (5% weight)

Spouse/ Child Support

Exception Creditors (5% weight)

Preexisting Torts Exception Creditors/Other

Exception Creditors

(5% weight)

Ease of Use – Is a new

Affidavit of Solvency

required for every new transfer?

(5% weight)

Reputation/ Fraudulent Transfer

Standard//Other Adjustments (10% weight)

Total Score

1 Nevada No 2 Yrs. 2 Yrs. or

0.5 Yr. Discovery No No

No Affidavit Required

Significant 99

2 South Dakota

No

2 Yrs.

2 Yrs. or 0.5 Yr. Discovery

Divorcing Spouse; Alimony;

Child Support (only if indebted at time

of transfer)

No No Affidavit Required

Significant 97

3 Alaska No 2 Yrs. 2 Yrs. or

0.5 Yr. Discovery

Divorcing Spouse

No Affidavit Required Significant 91*

4 (tie)

Ohio No (except residents)

1.5 Yrs. 1.5 Yrs. or

0.5 Yr. Discovery

Divorcing Spouse; Alimony;

Child Support No Affidavit Required Medium 87

4 (tie)

Tennessee

No (except dividends/ interest on residents)

2 Yrs. 2 Yrs. or

0.5 Yr. Discovery

Divorcing Spouse; Alimony;

Child Support No Affidavit Required High 87**

6 Delaware No (except residents)

4 Yrs. 4 Yrs. or

1 Yr. Discovery

Divorcing Spouse; Alimony;

Child Support Preexisting Torts

No Affidavit Required

Significant 80

7 Wyoming No 4 Yrs. 4 Yrs. or

1 Yr. Discovery Child Support

Property listed on app. to obtain

credit – but only as to that lender

Affidavit Required High 78

8 Rhode Island

No 4 Yrs. 4 Yrs. or

1 Yr. Discovery

Divorcing Souse; Alimony;

Child Support Preexisting Torts

No Affidavit Required

Medium 75

9 New

Hampshire

No (except dividends/ interest on residents)

4 Yrs. 4 Yrs. or

1 Yr. Discovery

Divorcing Spouse; Alimony;

Child Support Preexisting Torts

No Affidavit Required

High/ Limited clear and convincing

evidence standard 73

10 Utah

Very questionable/ limited ability

to avoid

2 Yrs.

2 Yrs. or 1 Yr. Discovery (also 120-day

mailing/publication option)

No No Affidavit Required Low/Missing clear

and convincing evidence standard

70***

11 Missouri

No (except Missouri source income)

4 Yrs. 4 Yrs. or

1 Yr. Discovery Alimony;

Child Support

State/U.S. to extent

state/federal law provides

No Affidavit Required

Low 68

12 Hawaii No (except residents)

2 Yrs. 2 Yrs. Pers. Injury;

6 Yrs. Contract

Divorcing Spouse; Alimony;

Child Support

Preexisting Torts, Certain Lenders,

Hawaii Tax

No Affidavit Required

Low/Limited clear and convincing

evidence standard 67

13

Virginia

Yes None 5 Yrs. Child Support

Creditor who has provided services to protect trust; U.S., city, etc.

No Affidavit Required

Low 53

14 Oklahoma Yes 4 Yrs. 4 Yrs. or

1 Yr. Discovery Child Support

Protection limited to $1,000,000

No Affidavit Required

Low 48

15 Colorado Yes

Not clear if protection from any creditor

Not clear if protection from

any creditor

Not clear if protection from any creditor

Not clear if protection from

any creditor

No Affidavit Required

Low 0

4th Annual Domestic Asset Protection Trust State Rankings Chart created in April 2013. Original State Rankings Chart created in April 2010. Copyright © 2010-2013 by Steve Oshins ([email protected] / www.oshins.com / (702) 341-6000, ext. 2. All rights reserved. Includes known 2013 legislation. *Alaska’s score assumes passage of Alaska HB 102. If it doesn’t pass, then Alaska’s Total Score = 81, not 91. **Tennessee’s score assumes passage of Tennessee SB 713/HB 873. If it doesn’t pass, then Tennessee’s Total Score = 73, not 87. ***Utah’s law is great for Utah residents, but is ranked low because of its state income tax uncertainty for non-residents.

Enduring Strategies for Same-Sex Couples in an Evolving Landscape

Gail E. Cohen, Esq. Erin Gilmore Smith, Esq.

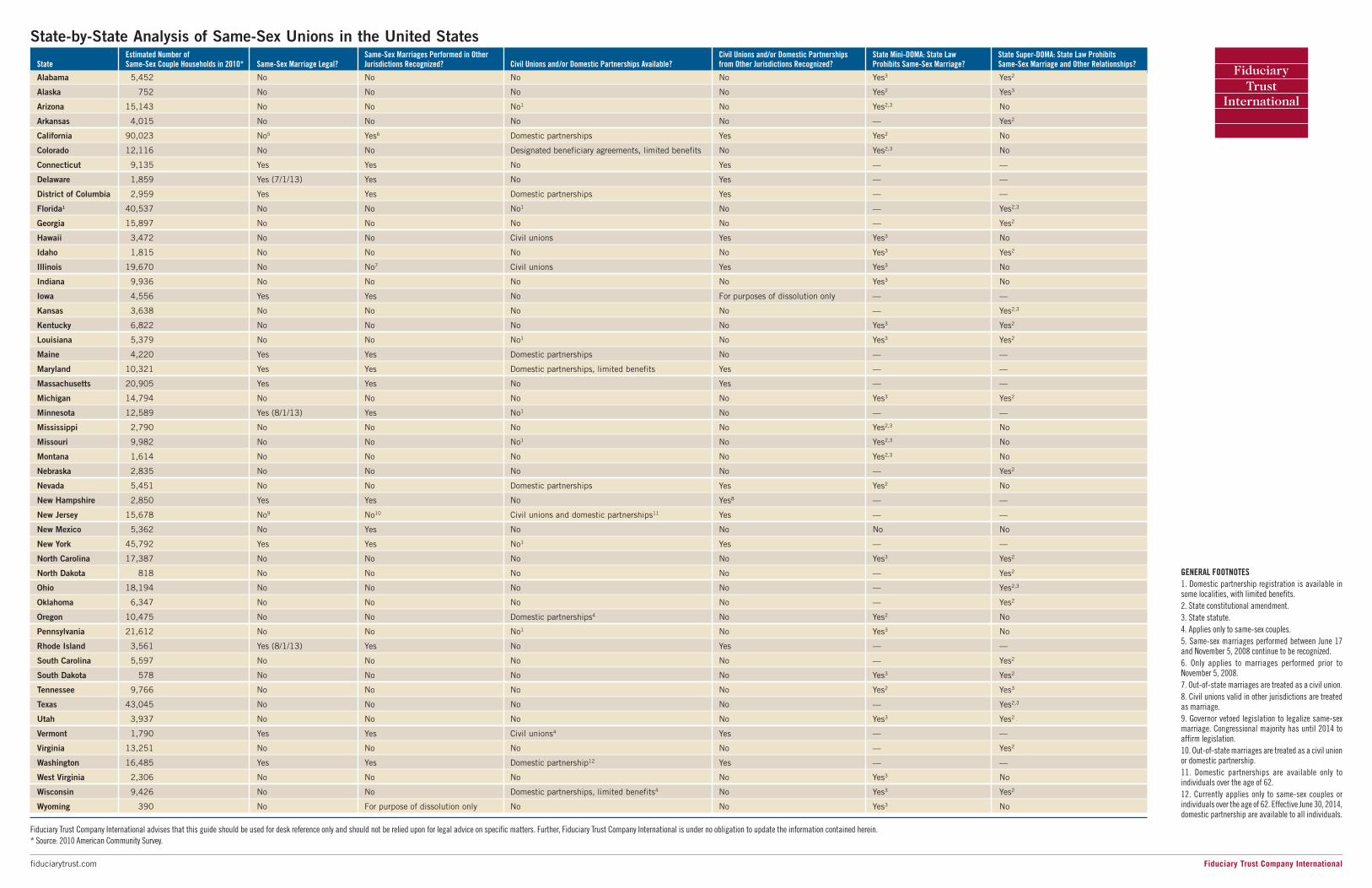

Fiduciary Trust Company International Estate planning goals of same-sex couples are no different from the goals of opposite-sex couples. For married couples, however, federal and often state laws treat same-sex couples as if they were strangers. Two cases are currently before the U.S. Supreme Court that could dramatically change the landscape for same-sex couples. Regardless of the rulings, there are timely and enduring estate planning strategies same-sex couples should consider today to minimize transfer taxes, protect assets, provide for future incapacity, and ensure their estate plans leverage benefits that might ultimately become available. A Rapidly-Evolving Landscape for Same-Sex Spouses On the state level, same-sex marriage is recognized in New York, Massachusetts, Connecticut, Iowa, Vermont, New Hampshire, Maine, Maryland, Washington, and the District of Columbia. Beginning July 1, 2013, Delaware will also recognize same-sex marriage; Minnesota and Rhode Island will join the list beginning August 1. New Mexico recognizes the validity of out-of-state marriages, but does not itself allow same-sex marriage. In addition, civil unions offering broad protections are available in Hawaii, Illinois and New Jersey. Domestic partnerships are available in California, Nevada and Oregon. Colorado and Wisconsin offer domestic partnerships with more limited benefits. Domestic partnership registries, conveying limited benefits, are available locally in some cities. View a state-by-state analysis of same-sex unions. On the federal level, the 1996 Defense of Marriage Act (“DOMA”) provides that no state is obligated to recognize same-sex marriages from other states and, for federal purposes, defines “marriage” as a legal union only between one man and one woman.1

Section 2: Powers Reserved to the States No state, territory or possession of the United States, or Indian Tribe shall be required to give effect to any public act, record, or judicial proceeding of any other state, territory, possession or tribe respecting a relationship between persons of the same sex that is treated as marriage under the laws of such

other state, territory, possession or tribe, or a right of claim arising from such relationship. Section 3: Definition of “Marriage” and “Spouse” In determining the meaning of any Act of Congress, or of any ruling, regulation, or interpretation of the various administrative bureaus and agencies of the United States, the word “marriage” means only a legal union between one man and one woman as husband and wife, and the word “spouse” refers only to a person of the opposite sex who is a husband or a wife.

Since its enactment, DOMA has been found to impact more than 1,100 federal laws and regulations.2 In recent years, there have been a number of challenges to the constitutionality of Section 3 of DOMA.3 The Obama Administration In February 2011, the Obama Administration announced that it would no longer defend Section 3 of DOMA, as applied to same-sex couples who are legally married under state law. In a letter addressed to Speaker of the House John Boehner, Attorney General Eric Holder announced the Administration determined that Section 3 violates the equal protection clause of the Fifth Amendment. The Attorney General also stated he believes that classifications based on sexual orientation warrant a heightened level of scrutiny and that Section 3 fails this heightened standard of review. The Legislative Branch, through its Bipartisan Legal Advisory Group of the U.S. House of Representatives (“BLAG”), intervened in many pending court cases to defend the law. Although the Obama Administration no longer defends Section 3 of DOMA, it continues to enforce the law. Windsor v. United States The Second Circuit is the most-recent court to rule Section 3 of DOMA to be unconstitutional.4 The Supreme Court heard oral arguments on the case in March and a ruling is expected by late June.

Details – Windsor v. United States Edie Windsor and Thea Spyer were New York residents, together for more than forty years before marrying in Canada in 2007. Beginning in 2004, New York recognized same-sex marriages performed in Canada and other jurisdictions. Thea died in 2009; Edie was the beneficiary and executrix of Thea’s estate. In 2010, Edie filed a claim for refund of the more than $363,000 in federal estate taxes paid by Thea’s estate and a ruling that Section 3 of DOMA violates the equal protection clause of the Fifth Amendment. But for DOMA, it was argued, the federal marital deduction would have applied and no federal estate tax would have been due. In June 2012, the District Court for the Southern District of New York reviewed the equal protection claim under an enhanced rational basis test, noting that laws that “exhibit a

desire to harm a politically unpopular group require a more searching form of rational basis review.” BLAG raised four governmental interests advanced by Section 3 of DOMA: (1) caution and the traditional institute of marriage, (2) child rearing and procreation, (3) consistence and uniformity of federal benefits, and (4) conserving the public fisc. The Court found that none of these interests met the enhanced rational basis test and granted Windsor’s motion for summary judgment. BLAG appealed to the Second Circuit, which heard the case on an expedited basis in October 2012. The Second Circuit concluded that gay men and lesbians constitute a quasi-suspect class and that Section 3 of DOMA must therefore be reviewed under heightened scrutiny. In determining this classification, the Court looked to four factors: (1) history of discrimination against the class, (2) ability of the class to contribute to society, (3) immutability of characteristic defining the class, and (4) minority status and political powerlessness. Further, the Court did not find the law to be substantially related to an important government interest (or, in the words of the Court, the justifications were not “exceedingly persuasive”). BLAG offered four justifications for Section 3 of DOMA, each of which was rejected. 1. Maintaining a uniform federal definition of marriage: the Court noted that defining marriage

has traditionally been an exclusive matter of state regulation and that DOMA not only breaches a “longstanding deference to federalism”, but it does not create uniformity in the definition of marriage because it leaves standing other inconsistences in the marriage laws between states such as age requirements and consanguinity.

2. Protecting the public fisc: the Court found that while maintaining the public fisc may be an

important government interest, DOMA is so broad and has such far-reaching effects beyond the legislative intent to conserve public resources that it is not substantially related to fiscal matters.

3. Preserving a traditional institution of marriage: the Court did not recognize tradition to be an

important government interest and found that, in the alternative, even if the preservation of the traditional institution of marriage was an important government interest, DOMA is not a means to achieve this interest because the law does not prevent same-sex couples from marrying under state law. It merely prohibits a federal recognition of that union.

4. Encouraging responsible child rearing: the Court noted that although the promotion of

procreation can be an important government interest, there is no substantial relationship between DOMA and this interest because DOMA offers no incentives to opposite-sex couples to have children

On the State Level: several states have adopted so-called “mini-DOMAs” that define marriage as a union between one man and one woman. California’s Proposition 8 is an example of a mini-DOMA. Other states have adopted “super-DOMAs” that, in addition to defining marriage as a union between one man and one woman, prohibit the recognition of civil unions, domestic partnerships and other similar relationships.

Currently thirty-eight states have legislation or constitutional amendments (or both) prohibiting same-sex marriage to some degree.5 Hollingsworth v. Perry The second case currently before the Supreme Court is a challenge to California’s prohibition on same-sex marriage.6 As with Windsor, a decision is expected by late June.

Details – Hollingsworth v. Perry In 2000, California voters adopted an initiative statutory enactment known as Proposition 22, providing: Only marriage between a man and a woman is valid or recognized in California.7 In 2008, Proposition 22 was stuck down as unconstitutional under state equal protection and due process challenges by the California Supreme Court, which held that the California constitution guaranteed same-sex couples the right to use the designation “marriage.”8 Following this ruling, California issued more than 18,000 marriage licenses to same-sex couples. A few months later, in November 2008, California voters adopted Proposition 8, the California Marriage Protection Act.9 Unlike Proposition 22, which was a statutory initiative, Proposition 8 was a constitutional initiative, the language of which was the same as Proposition 22. However, Proposition 8 did not affect the status same-sex marriages performed prior to its enactment in November 2008.10 In 2009, after being denied marriage licenses, two same-sex couples challenged the constitutionality of Proposition 8 under the Fourteenth Amendment’s due process and equal protection clauses. In the District Court proceeding, California’s Governor Arnold Schwarzenegger and Attorney General Jerry Brown declined to defend Proposition 8, and the official proponents of Proposition 8 intervened. The District Court applied a rational basis review and found Proposition 8 to be unconstitutional under due process and equal protection grounds. Only the official Proposition 8 proponents appealed the decision. Upon the Proposition 8’s proponents’ appeal to the Ninth Circuit, the plaintiffs raised a third issue: Proposition 8 violates the equal protection clause by eliminating the right to marry, which had previously been guaranteed to gay men and lesbians under the California state Constitution. The Ninth Circuit found that Proposition 8 did not affect any of the rationales proffered by the amendment’s proponents – furthering the interest of reasonable procreation and childbearing, reducing the threat of irresponsible procreation, protecting religious freedom and preventing children from being taught same-sex marriage in school - and, as a result, the Court did not address whether any of the justifications were reasonable under a rational basis review. The Court concluded that the only rationales it could infer for the enactment of Proposition 8 was tradition, which is not a justification for taking away a right that has

already been granted, and moral disapproval of gays and lesbian women, which is prohibited under equal protection and does not withstand rational basis scrutiny. Estate Planning Strategies for Same-Sex Couples As with opposite-sex couples, much of estate planning for same-sex couples is centered upon protecting assets for the surviving spouse and ensuring each spouse’s wishes are carried out. Depending on how the Supreme Court rules in Windsor and Perry, DOMA and state-based legislation may not necessarily go away. However, there are enduring estate-planning strategies to consider for same-sex couples that are effective regardless of marital status. Strategy One: Plan for a Federal Marital Deduction The marital deduction is easily one of the most important and powerful benefits available to married couples. Since this deduction allows spouses to transfer unlimited assets to each other gift- and estate-tax free, it can offer significant savings upon the death of the first spouse. The 2013 federal estate tax rate is 40%, with an exemption of $5.25 million. Currently, under Section 3 of DOMA, same-sex married couples cannot take advantage of this unlimited federal marital deduction. Same-sex married couples should consider drafting their estate planning documents to provide flexibility in the event that the federal marital deduction becomes available. Disclaimer planning should also be considered. For surviving spouses paid estate taxes at the death of the first spouse, the executor should consider filing a protective claim for refund, if available. Strategy Two: Consider These Drafting Strategies Estate tax allocation clauses in existing documents should be reviewed to ensure that any estate taxes that are ultimately due will be paid as the testator intends. The drafting attorney should consider defining “marriage” in estate planning documents. For example, a “spouse” may be defined as someone who has married or entered into a civil union or domestic partnership in a jurisdiction that recognizes such, regardless of what law governs the document. The document may also define who constitutes a “marital child.” Strategy Three: Leverage Trusts to Minimize Gift and Estate Taxes Lifetime Credit Shelter Trust Utilizing an individual’s lifetime exemption amount to create a lifetime credit shelter trust may be an attractive planning strategy for same-sex couples who do not wish to make outright gifts. Unlike a QTIP trust, there is no requirement that the donor and beneficiary be married. For same-sex married couples whose

marriage is later recognized for federal purposes or for unmarried couples who later wed, the terms of the trust and its effectiveness remain the same. The grantor may name his or partner as the beneficiary for the partner’s lifetime. The beneficiary-partner may be granted a power of appointment over the assets or the trust agreement may control the disposition of the assets upon the death of the beneficiary-partner. Distributions to the beneficiary-partner can indirectly benefit the grantor, as each is part of the same household. To hedge against divorce or separation, the trust agreement may define the beneficiary as the current spouse or domestic partner. If the grantor’s lifetime exclusion amount is utilized to create the trust, no gift tax is due and the assets in the trust - including the appreciation on the initial contribution - will likely not be includable in the grantor’s estate for estate tax purposes. A word of caution: Couples who wish to each create a credit shelter trust for the other partner should exercise caution to avoid the reciprocal trust rule and the inclusion of the trusts in each grantor’s estate for estate tax purposes. The reciprocal trust rule holds that substantially identical trusts (for example, same terms, similar asset values, contemporaneous execution) created by two grantors for the benefit of each other are considered interrelated and will be included in the each grantor’s estate for estate tax purposes. Grantor Retained Income Trust (“GRIT”) A GRIT is an irrevocable inter vivos trust into which the grantor transfers assets and receives all net income from the trust, at least annually, during the term. At the expiration of the trust term, the remaining assets pass to a named beneficiary (or a trust for that person’s benefit). The funding of a GRIT is a taxable event. However, for gift tax purposes, the value of the assets contributed to the GRIT may be discounted to reflect the present value of the grantor’s retained income interest. To take advantage of the valuation discount, IRC § 2702 requires that the beneficiary of a GRIT be a non-family member. Under Section 3 of DOMA, same-sex married couples are not deemed to be spouses under the tax code. The grantor may therefore name his or her same-sex spouse as a beneficiary and still receive a valuation discount on the transfer. If the grantor dies during the GRIT term, the assets will likely be includable in his or her estate for estate tax purposes. However, the grantor is in no worse position for having created the GRIT. Since it is unclear how a repeal of Section 3 of DOMA would affect existing GRITs, caution should be exercised by same-sex married couples. If Section 3 is DOMA is found to be unconstitutional by the Supreme Court, the discount for

the retained interest may be disregarded. Of course, unmarried couples may still take advantage of a GRIT. Grantor Retained Annuity Trust (“GRAT”) Similar to a GRIT, the grantor retains the right to receive a fixed annuity amount for the term of the trust. At the end of the trust’s term, any remaining assets pass to a named beneficiary, such as a partner or spouse (or a trust for that person’s benefit). Unlike a GRIT, there is no restriction on a family member being a beneficiary of a GRAT. The IRS assumes that a GRAT will grow at a rate equal to the IRC Section 7520 rate in effect at the time of the transfer (1.2% for May 2013). Any growth in excess of the 7520 rate passes to the beneficiaries tax free; and the lower the 7520 rate, the more likely the trust’s growth will surpass this hurdle rate. The creation of a GRAT is a taxable event, and unlike a GRIT, no discount is available on the valuation of the assets contributed to the trust. However, the annuity amount can be structured so that the present value of the annuity payments equals or nearly equals the value of the property contributed to the GRAT. This “zeroing out” results in little or no gift tax paid. The grantor’s death during the term of the GRAT will likely cause the assets of the trust to be includable in the grantor’s estate for estate tax purposes. However, the grantor is in no worse position for having created the GRAT. Now may be the time to act to create a GRAT. In recent years, several bills have been introduced in Congress intended to quash the tax benefits of a GRAT by prohibiting a zeroing- out of the trust and requiring a 10-year term (making growth in excess of the 7520 rate over the term of trust more difficult). President Obama’s Green Book for 2014 also contains a similar proposal. Charitable Lead Trust (“CLT”) & Charitable Remainder Trust (“CRT”) For couples who are charitably inclined, CLTs and CRTs may be attractive planning vehicles. As with a GRAT, there are no restrictions on family members being beneficiaries. Thus, the fate of DOMA does not impact these trusts. A CLT is structured and operates in a similar way to a GRAT, except that the annuity payment is made to a charity rather than the grantor. At the end of the trust’s term, any remaining assets pass to a non-charitable beneficiary, such as a partner or other family member. As with a GRAT, the annuity amount is calculated using the 7520 rate in effect at the time of the transfer (or, if lower, the 7520 rate in effect in either of the two preceding months). Any growth in excess of the 7520 rate will pass to the beneficiary tax free at the end of the trust’s term. A CRT is structured so that the income beneficiary receives either an annual annuity amount or a unitrust amount from the trust, with the remainder passing to

a charitable beneficiary at the end of the trust’s term. The distribution from a CRT must be between 5% and 50%, calculated either upon the initial value of the trust assets (for an annuity) or the fair market value of the trust assets (for a unitrust). A CRT may be especially attractive for donors with appreciated assets. If the CRT is funded with appreciated assets which are later sold in the trust, because the remainder person of the trust is a charity, no tax is due on the capital gain. The donor may also receive an income tax deduction in the year the CRT is created, based on the value of the charity’s remainder interest in the trust. Generally, the older the donor, the greater the deduction. The creation of a CRT triggers a taxable gift. However, if the donor is the income beneficiary, the CRT is not considered a gift and no tax is due. Additionally, a CRT is generally not subject to estate tax at the death of the grantor. Strategy Four: Consider the Benefits of Life Insurance Properly structured, life insurance can provide liquidity for surviving same-sex spouses or partners to offset the payment of federal and state estate taxes that may be due upon the death of the first spouse. Individuals may wish to consider leveraging the $5.25 million lifetime exclusion amount to create and fund an irrevocable life insurance trust (“ILIT”). The grantor may gift assets to the trust for the purchase of a life insurance policy on his or her life or an existing life insurance policy may be transferred into the trust. The trust owns the policy and the death benefit is payable into the trust, with the beneficiary of the trust generally being the surviving same-sex spouse (or other beneficiary who will bear the burden of estate taxes). Unlike life insurance owned by the insured, a life insurance policy owned by an ILIT is generally not includable in the insured’s estate for estate tax purposes. An ILIT can be drafted in such a way to provide for flexibility if a marital deduction is available at the death of the first spouse. If life insurance is owned outside of an ILIT, caution should be exercised to document that the spouse or partner owning the policy has an insurable interest in the life of the other. Strategy Five: Be Mindful of Property Ownership It is important to consider state homestead laws and the rights of decedents to devise homesteads. In addition to protecting a primary residence from creditors and exemptions from property taxes, some state homestead laws also place limits on an owner’s ability to devise the property. For example, in Florida, if a homeowner is survived by minor children, he cannot devise his property outside of his spouse and children. As same-sex marriage is not recognized in Florida, if a homeowner is survived by minor children, the partner would have no rights to

the residence, even if devised under the decedent’s Will. An unmarried surviving partner would be subject to the same restrictions. Strategy Six: Ensure Ancillary Estate Planning Documents Are in Place Prenuptial or Domestic Partnership Agreement Prenuptial and domestic partnership agreements (sometimes referred to as cohabitation agreements) are private contracts that set forth each spouse’s or partner’s rights and responsibilities if their union should end, including rights (such as spousal support) that are not otherwise available under state law. The requirements for and enforceability of domestic partnership agreements vary from state to state. California and Florida courts, for example, have recognized the enforceability of these agreements; courts in Georgia, Louisiana and Illinois have not. Health Care Proxy A health care proxy (sometimes referred to as an advance health care directive or a power of attorney for health care) permits an individual designated by the principal to make health-related decisions on his or her behalf. In California, the statutory advance health care directive form also permits the principal to make end-of-life decisions. Other jurisdictions, such as New York, require a separate living will. In the absence of a health care proxy, state law varies as to whom, if anyone, can make health care decisions on behalf of an incapacitated patient. In New York, spouses and domestic partners have priority to make health care decisions in the absence of a designated health care agent or guardian. For these purposes, a domestic partner is defined as a registered domestic partner in any jurisdiction, a person recognized as a beneficiary or covered person under the patient’s employee benefits or health insurance, or an individual otherwise dependent or mutually interdependent on the other under a totality of the circumstances test. In Florida, in the absence of a guardian, a spouse has priority to make health care (not end-of-life) decisions for an incapacitated individual. However, Florida does not recognize same-sex marriages legal in other jurisdictions. Burial Instructions Same-sex couples should consider executing burial instructions, expressing their wishes or naming their spouse or partner as the individual authorized to make burial decisions. In the absence of burial instructions, state law governs the disposition of remains. In New York, priority over the disposition of remains is given to an agent appointed in writing by the decedent. In the absence of an appointed agent, priority is given to an individual’s spouse or domestic partner. The definition of a

domestic partner for these purposes is the same as the definition of a domestic partner for health care decisions. In other states, however, priority does not extend to domestic partners. For example, in Florida, in the absence of written instructions, a decedent’s surviving spouse, children, parents and siblings (in that order) have the authority to make burial arrangements. A same-sex spouse or partner (same-sex or otherwise) has no authorization under Florida law, absent the decedent’s written instructions. Conclusion Until parity is granted to these couples, their estate plans will require special strategies and attention. If executed property, these enduring techniques may mitigate or even eliminate the disparate treatment same-sex spouses currently face.

1 Pub. L. No. 104-199 (1996), codified at 28 U.S.C. §1738(C), 1 U.S.C. §7. 2 Pederson v. U.S. Office of Personnel Management, 881 F. Supp, 2d 294, 299 (D. Conn. 2012). 3 Gill v. Office of Personnel Management, 699 F. Supp. 2d 374 (D. Mass, 2010), affirmed by, 682 F.3d 1 (1st Cir. 2012) & Massachusetts v. U.S. Department of Health and Human Services, 698 F. Supp. 2d 234 (2010), affirmed by, 692 F.3d 1 (1st Cir. 2012), Windsor v. United States, 833 F. Supp. 2d 394 (S.D.N.Y. 2012), 2012 U.S. App. LEXIS 21785 (2nd Cir. 2012), Golinski v. U.S. Office of Personnel Management, 824 F. Supp. 968 (N.D. Cal. 2012), Dragovich v. U.S. Dept. of Treasury, 872 F. Supp. 2d 944 (N.D. Cal. 2012), Pedersen v. U.S. Office of Personnel Management, supra, note 2, 4 Windsor v. United States, 833 F. Supp. 2d 394 (S.D.N.Y. 2012), 699 F.3d 169 (2nd Cir. 2012) . 5 See Appendix for a survey of the same-sex union laws of each state. 6 Perry v. Schwarzenegger, 704 F. Supp. 2d 921 (N.D. Cal. 2010), aff’d sub nom., Perry v. Brown, 671 F.3d 1052 (9th Cir. 2012). 7 CAL. FAM. CODE §308.5. 8 In re Marriage Cases, 183 P. 3d 384 (Cal. 2008). 9 CAL. CONST., art. I, §7.5. 10 Strauss v. Horton, 207 P. 3d 48 (Cal. 2009).

Alabama 5,452 No No No No Yes3 Yes2

Alaska 752 No No No No Yes2 Yes3

Arizona 15,143 No No No1 No Yes2,3 No

Arkansas 4,015 No No No No — Yes2

California 90,023 No5 Yes6 Domestic partnerships Yes Yes2 No

Colorado 12,116 No No Designated beneficiary agreements, limited benefits No Yes2,3 No

Connecticut 9,135 Yes Yes No Yes — —

Delaware 1,859 Yes (7/1/13) Yes No Yes — —

District of Columbia 2,959 Yes Yes Domestic partnerships Yes — —

Florida1 40,537 No No No1 No — Yes2,3

Georgia 15,897 No No No No — Yes2

Hawaii 3,472 No No Civil unions Yes Yes3 No

Idaho 1,815 No No No No Yes3 Yes2

Illinois 19,670 No No7 Civil unions Yes Yes3 No

Indiana 9,936 No No No No Yes3 No

Iowa 4,556 Yes Yes No For purposes of dissolution only — —

Kansas 3,638 No No No No — Yes2,3

Kentucky 6,822 No No No No Yes3 Yes2

Louisiana 5,379 No No No1 No Yes3 Yes2

Maine 4,220 Yes Yes Domestic partnerships No — —

Maryland 10,321 Yes Yes Domestic partnerships, limited benefits Yes — —

Massachusetts 20,905 Yes Yes No Yes — —

Michigan 14,794 No No No No Yes3 Yes2

Minnesota 12,589 Yes (8/1/13) Yes No1 No — —

Mississippi 2,790 No No No No Yes2,3 No

Missouri 9,982 No No No1 No Yes2,3 No

Montana 1,614 No No No No Yes2,3 No

Nebraska 2,835 No No No No — Yes2

Nevada 5,451 No No Domestic partnerships Yes Yes2 No

New Hampshire 2,850 Yes Yes No Yes8 — —

New Jersey 15,678 No9 No10 Civil unions and domestic partnerships11 Yes — —

New Mexico 5,362 No Yes No No No No

New York 45,792 Yes Yes No1 Yes — —

North Carolina 17,387 No No No No Yes3 Yes2

North Dakota 818 No No No No — Yes2

Ohio 18,194 No No No No — Yes2,3

Oklahoma 6,347 No No No No — Yes2

Oregon 10,475 No No Domestic partnerships4 No Yes2 No

Pennsylvania 21,612 No No No1 No Yes3 No

Rhode Island 3,561 Yes (8/1/13) Yes No Yes — —

South Carolina 5,597 No No No No — Yes2

South Dakota 578 No No No No Yes3 Yes2

Tennessee 9,766 No No No No Yes2 Yes3

Texas 43,045 No No No No — Yes2,3

Utah 3,937 No No No No Yes3 Yes2

Vermont 1,790 Yes Yes Civil unions4 Yes — —

Virginia 13,251 No No No No — Yes2

Washington 16,485 Yes Yes Domestic partnership12 Yes — —

West Virginia 2,306 No No No No Yes3 No

Wisconsin 9,426 No No Domestic partnerships, limited benefits4 No Yes3 Yes2

Wyoming 390 No For purpose of dissolution only No No Yes3 No

Estimated Number of Same-Sex Marriages Performed in Other Civil Unions and/or Domestic Partnerships State Mini-DOMA: State Law State Super-DOMA: State Law Prohibits State Same-Sex Couple Households in 2010* Same-Sex Marriage Legal? Jurisdictions Recognized? Civil Unions and/or Domestic Partnerships Available? from Other Jurisdictions Recognized? Prohibits Same-Sex Marriage? Same-Sex Marriage and Other Relationships?

Fiduciary Trust Company International advises that this guide should be used for desk reference only and should not be relied upon for legal advice on specific matters. Further, Fiduciary Trust Company International is under no obligation to update the information contained herein.

* Source: 2010 American Community Survey.

GENERAL FOOTNOTES

1. Domestic partnership registration is available insome localities, with limited benefits.

2. State constitutional amendment.

3. State statute.

4. Applies only to same-sex couples.

5. Same-sex marriages performed between June 17and November 5, 2008 continue to be recognized.

6. Only applies to marriages performed prior toNovember 5, 2008.

7. Out-of-state marriages are treated as a civil union.

8. Civil unions valid in other jurisdictions are treated as marriage.

9. Governor vetoed legislation to legalize same-sexmarriage. Congressional majority has until 2014 toaffirm legislation.

10. Out-of-state marriages are treated as a civil unionor domestic partnership.

11. Domestic partnerships are available only toindividuals over the age of 62.

12. Currently applies only to same-sex couples orindividuals over the age of 62. Effective June 30, 2014,domestic partnership are available to all individuals.

State-by-State Analysis of Same-Sex Unions in the United States

Fiduciary Trust Company Internationalfiduciarytrust.com

1

Deadline To Send ACA Summary of Benefits & Coverage (SBC) Adds Pressure For Employers To Finalize 2014 Plan Designs As Agencies Add

MEC & MV Disclosures To SBC

By Cynthia Marcotte Stamer1

Employer and union group health plan sponsors and insurers of group and individual health plans (Health Plans) agonizing over 2014 health plan design decisions need to keep in mind that impending deadlines to update and deliver required Summary of Benefits and Communications (SBC) disclosures mandated by the Patient Protection and Affordable Care Act (Affordable Care Act) shorten the time to finalize decisions including new requirements to disclose whether the Affordable Health Plan-covered Health Plans provide “minimum essential coverage” (MEC) and “minimum value” within the meaning of the Affordable Care Act. The Affordable Care Act’s requirement that Health Plans distribute updated SBCs before the beginning of the enrollment period for coverage to be provided in 2014 creates added urgency and pressure for Health Plans and their employer and other sponsors to finalize and implement their decisions on their Health Plans 2014 plan designs and coverages to allow adequate lead time to prepare and deliver the required SBCs for 2014. The Departments of Health & Human Services (HHS), Labor (DOL) and Treasury (IRS)(collectively, the Agencies) announced April 23, 2013 that SBCs for periods of coverage after December 31, 2013 must disclose if the Health Plans provide MEC and minimum value. Health Plans, their sponsors, fiduciaries, and insurers generally will need to update their Health Plans’ SBCS to include these disclosures as well as to incorporate other changes necessary to accurately disclose other plan design changes made to post-December 31, 2013 coverage before the enrollment period begins. Plan sponsors planning changes to their health plans must allow sufficient lead time to both finalize plan designs and contracts, amend plan documents, make MEC and minimum value determinations, and then timely update and distribute the SBC in accordance with the SBC rules. This means that most plan sponsors of Health Plans have much less time than historically used to finalize their decisions. ACA SBC Mandate Overview As amended by the Affordable Care Act amended the Public Health Services Act (PHS) § 2715, Employee Retirement Income Security Act (ERISA) § 715 and the Internal Revenue Code (Code) §§ 9815 require that Health Plans provide a SBC and a “Uniform Glossary” that “accurately describes the benefits and coverage under the applicable plan or coverage” in a way that meets the format, content and other detailed SBC standards set for the Affordable Care Act as implemented by the Departments regulatory guidance. The Summary of Benefits and Coverage and Uniform Glossary Final Regulation (Final Regulation) implementing this requirement published February 14, 2012 generally requires Health Plans at specified times including before the first offer of coverage under the Plan as well as following certain material changes to the Plan. For Health Plans providing group health plan coverage, FAQs About Affordable Care Act Implementation (Part VII)[*] set the deadline for Health Plan to deliver a SBC as follows, while at the same time indicating that the Departments would not impose penalties on plans and issuers “working diligently and in good faith” to provide the required SBC content in an appearance consistent with the Final Regulations:

2

• To covered persons enrolling or re-enrolling in an open enrollment period (including late enrollees and re-enrollees) as the first day of the first open enrollment period that begins on or after September 23, 2012; and

• For individuals enrolling in coverage other than through an open enrollment period (including individuals who are newly eligible for coverage and special enrollees) as the first day of the first plan year that begins on or after September 23, 2012. See FAQs About Affordable Care Act Implementation (Part VIII).

The Final Regulation and other existing guidance generally dictates that Health Plans follow a required template for providing the SBC and accompanying glossary. When publishing the Final Regulation, the Departments also published the required SBC template form (2013 SBC Template) and instructions for Health Plans to use to prepare and provide the required SBC for coverage beginning before January 1, 2014 and promised updated guidance and templates for use in providing SBCs for post-2013 coverage. While the Agencies clarified certain other details about the SBC rules, they did not materially change the required content or form of the 2013 SBC Template until their April 23, 2013 release of FAQs About Affordable Care Act Implementation (Part XIV). See e.g. FAQs About Affordable Care Act Implementation Part IX and Part X. FAQ Part XIV Requires MEC and Minimum Value Disclosures In SBC FAQs About Affordable Care Act Implementation (Part XIV) published April 23, 2013 announces the updated required 2014 SBC Template that the Agencies are requiring to SBCs for periods of health coverage from January 1, 2014 to December 31, 2014. Along with the 2014 SBC Template, the Agencies also published 2014 Sample Completed SBC, which provides an example of a SBC completed for a hypothetical health plan prepared by the Agencies. The 2014 SBC Template updates the 2013 SBC Template and Sample Completed Template to add information the Agencies believe individuals eligible for Health Plan coverage should know in light of the impending implementation of the individual shared responsibility requirements of Internal Revenue Code (Code) § 5000A and the employer shared responsibility rules of Code § 4980H commonly called the Affordable Care Act’s “pay-or-play” rules. These were the "penalty" provisions that the Supreme Court ruled are taxes last Summer. Rationale For SBC Changes Beginning in 2014, Code § 4980H generally requires employers of 50 or more full-time employees to pay a penalty if the employer fails to offer a group health plan providing MEC and meeting the “minimum value” requirements of the Affordable Care Act. Code § 36B(c)(2)(C)(ii) provides that an employer-sponsored Health Plan provides MV if the ratio of the share of total costs paid by the Health Plan relative to the total costs of covered services is no less than 60% of the anticipated covered medical spending for covered benefits paid by a group health plan for a standard population, computed in accordance with the plan’s cost-sharing, and divided by the total anticipated allowed charges for covered benefits provided to a standard population is no less than 60%. See Patient Protection and Affordable Care Act: Standards Related to Essential Health Benefits, Actuarial Value, and Accreditation Regulation. HHS has published a MV Calculator for use in calculating this percentage. Meanwhile, Code § 5000A generally imposes a penalty tax on individuals that fail to maintain enrollment in “minimum essential coverage” (MEC) within the meaning of Code § 5000A(f) and not otherwise exempt under Code § 5000A(d).

3

SBC Changes Required By FAQs XIV In Response To Pay-Or-Play Rules Since choosing to enroll in an employer-sponsored health plan providing MEC is one of the options that individuals can choose to avoid incurring the individual penalty under Code § 5000A, the Agencies feel that the SBC should disclose whether the offered Health Plan provides MEC and provides the requisite Minimum Value. Accordingly, the 2014 SBC Template requires that the SBC disclose if the Health Plan provides MEC and meets Minimum Value. The Agencies did not make any changes to the uniform glossary, Instructions for Completing the SBC, “Why This Matters” language, or to the coverage examples for the SBC. In general, the SBC requires that Health Plans update their existing SBCs to make the following disclosures for post-December 31, 2013 periods of coverage:

Does this Coverage Provide Minimum Essential Coverage? The Affordable Care Act requires most people to have health care coverage that qualifies as “minimum essential coverage.” This plan or policy [does/does not] provide minimum essential coverage. Does this Coverage Meet the Minimum Value Standard? In order for certain types of health coverage (for example, individually purchased insurance or job-based coverage) to qualify as minimum essential coverage, the plan must pay, on average, at least 60 percent of allowed charges for covered services. This is called the “minimum value standard.” This health coverage [does/does not] meet the minimum value standard for the benefits it provides.”

Health Plans will need to finalize plan designs and conduct the necessary analysis to decide the correct way to complete this language, then update SBCs to be provided for post-December 31, 2013 periods of coverage to include the required language appropriately completed based on the findings. Where the design of the 2014 SBC is too advanced already to do this, the Guidance allows Health Plans to provide the required language by sending the language in a supplemental SBC communication. However, most Health Plans will want to avoid the added cost and expense of the printing and distribution of this notification. Other SBC Requirement Clarifications in FAQs XIV While the 2014 SBC Template remains unchanged other than for the additional required statements about the MEC and minimum essential coverage, FAQs XIV does provide various other helpful clarifications about how to complete the 2014 SBC Template about the applicability of lifetime and annual limits in light of the Affordable Care Act’s restrictions on these limitations. In addition, FAQs XIV also continues for another year the guidance in:

• Affordable Care Act Implementation FAQs Part VIII, Q2 (regarding the Departments’ basic approach to implementation of the SBC requirements during the first year of applicability) for another year;

• Affordable Care Act Implementation FAQs Part IX, Q1 regarding the circumstances in which an SBC may be provided electronically and associated enforcement relief;

• Affordable Care Act Implementation FAQs Part IX, Q8 (regarding penalties for failure to provide the SBC or uniform glossary);

4

• Affordable Care Act Implementation FAQs Part IX, Q9 (regarding the coverage examples calculator); and related information related to use of the coverage examples calculator;

• Affordable Care Act Implementation FAQs Part IX, Q10 (regarding an issuer’s obligation to provide an SBC with respect to benefits it does not insure); and

• Affordable Care Act Implementation FAQs Part IX, Q13 (regarding expatriate coverage);

• Current enforcement relief about the Special Rule contained in the Instruction Guides for Group and Individual Coverage and about Medicare Advantage Plans contained in Affordable Care Act Implementation FAQs Part X, Q1

• Continues Affordable Care Act Implementation FAQs Part VIII, Q5 regarding use of carveout arrangements “until further guidance is issued.”

• Extends to September 23, 2014 existing relief for plans and issuers with respect to an insured health insurance product is not being actively marketed where the health insurance issuer has not actively marketed the product at any time on or after September 23, 2012 provided the SBC is provided for that product no later than September 23, 2014; and

• The anti-duplication rule for student group health coverage in the Final SBC regulations.

SBC Delivery Deadline Means Time Short To Finalize 2014 Plan Designs Employer and other health plan sponsors, insurers, administrators and others involved in 2014 Health Plan decisions and preparations must take into account the deadline for distributing the SBC before the enrollment period begins and allow adequate lead time to properly finalize their Health Plan design decisions and the analysis required to accurately prepare and deliver the SBC. Since Health Plan design decisions must be finalized to properly prepare the newly added MEC and minimum value and other required SBC disclosures, the need to prepare and distribute the SBC by the beginning of enrollment periods for post-December 31, 2013 periods of coverage means time running short to finalize 2014 plan designs. Employer and other Health Plan sponsors and others involved in 2014 Health Plan decision-making must take into account the SBC requirements and deadlines to ensure that they allow adequate time to complete the analysis and other preparations necessary timely to prepare and distribute SBCs in respond to the design decisions ultimately elected. This includes the careful preparation of the SBC to accurately reflect Health Plan design and terms, the review and coordination of the language of existing Health Plan documents and summary plan descriptions to identify and address potential discrepencies between the government-mandated terms and language in the Glossary and SBC and those documents, proper structuring and formatting of all of these documents and timely distribution in accordance with applicable regulations to participants and beneficiaries entitled to receive these documents in a manner that positions the Health Plan to show compliance. In regard to distributions, Health Plans and others involved in the planning and execution of these processes also need to ensure that any electronic or other methods of distribution meet applicable requirements and that copies are distributed to all entitled parties – employees and dependents – in accordance with the applicable rules.

5

For Help or More Information If you need help with the SBC or other 2014 health plan decision-making or preparation, or with reviewing and updating, administering or defending your group health or other employee benefit, human resources, insurance, health care matters or related documents or practices, please contact the author of this update, Cynthia Marcotte Stamer. THE FOLLOWING DISCLAIMER IS INCLUDED TO COMPLY WITH AND IN RESPONSE TO U.S. TREASURY DEPARTMENT CIRCULAR 230 REGULATIONS. ANY STATEMENTS CONTAINED HEREIN ARE NOT INTENDED OR WRITTEN BY THE WRITER TO BE USED, AND NOTHING CONTAINED HEREIN CAN BE USED BY YOU OR ANY OTHER PERSON, FOR THE PURPOSE OF (1) AVOIDING PENALTIES THAT MAY BE IMPOSED UNDER FEDERAL TAX LAW, OR (2) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY TAX-RELATED TRANSACTION OR MATTER ADDRESSED HEREIN. ©2013 Cynthia Marcotte Stamer, P.C. Nonexclusive license to republish granted to eReport.com. All other rights reserved.

1 A Fellow in the American College of Employee Benefit Council, immediate past Chair of the American Bar Association (ABA) RPTE Employee Benefits & Other Compensation Group and current Co-Chair of its Welfare Benefit Committee, Vice-Chair of the ABA TIPS Employee Benefits Committee, a council member of the ABA Joint Committee on Employee Benefits, and past Chair of the ABA Health Law Section Managed Care & Insurance Interest Group, Ms. Stamer is recognized, internationally, nationally and locally for her more than 25 years of work, advocacy, education and publications on cutting edge health and managed care, employee benefit, human resources and related workforce, insurance and financial services, and health care matters. A board certified labor and employment attorney widely known for her extensive and creative knowledge and experienced with these and other employment, employee benefit and compensation matters, Ms. Stamer continuously advises and assists employers, employee benefit plans, their sponsoring employers, fiduciaries, insurers, administrators, service providers, insurers and others to monitor and respond to evolving legal and operational requirements and to design, administer, document and defend medical and other welfare benefit, qualified and non-qualified deferred compensation and retirement, severance and other employee benefit, compensation, and human resources, management and other programs and practices tailored to the client’s human resources, employee benefits or other management goals. A primary drafter of the Bolivian Social Security pension privatization law, Ms. Stamer also works extensively with management, service provider and other clients to monitor legislative and regulatory developments and to deal with Congressional and state legislators, regulators, and enforcement officials concerning regulatory, investigatory or enforcement concerns. Recognized in Who’s Who In American Professionals and both an American Bar Association (ABA) and a State Bar of Texas Fellow, Ms. Stamer serves on the Editorial Advisory Board of Employee Benefits News, HR.com, Insurance Thought Leadership, Solutions Law Press, Inc. and other publications, and active in a multitude of other employee benefits, human resources and other professional and civic organizations. She also is a widely published author and highly regarded speaker on these matters. Her insights on these and other matters appear in the Bureau of National Affairs, Spencer Publications, the Wall Street Journal, the Dallas Business Journal, the Houston Business Journal, Modern and many other national and local publications. You can learn more about Ms. Stamer and her experience, review some of her other training, speaking, publications and other resources, and register to receive future updates about developments on these and other concerns from Ms. Stamer here.

What Duties do Trustees owe the Remainder Beneficiaries of Revocable Trusts?

ABA RPTE Non-Tax Estate Planning Considerations Group

In a trilogy of new cases, courts in three states have addressed the issue of whether the

trustee of a revocable trust has a duty to account to, and can be held liable to, the

remainder beneficiaries of the trust for a period during which the trust was revocable.

The three cases are: (i) the Iowa Supreme Court case of In the Matter of Trust # T-1 of

Mary Faye Trimble, 86 N.W. 2d 474 (Jan. 2013); the California Supreme Court case of

In re Estate of Giraldin, 290 P.3d 199 (Dec. 2012); and the Arizona Court of Appeals

case of Pennell v. Alverson, 2012 WL 4088679 (Ariz. App. Div 1, Sept. 18, 2012).

Based on these three cases, as well as the previously decided Missouri case of In re

Stephen M. Gunther Revocable Living Trust, 350 S.W. 3d 44 (Mo. Ct. App. 2011), it is

clear that, while a trust is revocable, the trustee has a duty only to the settlor, and that

even after the death of the settlor when the interests of the remainder beneficiaries has

vested, the trustee continues to have no duty to the remainder beneficiaries for any

actions taken while the trust was revocable. In other words, based on these cases, it

appears that during the life of the settlor, the trustee has a fiduciary duty only to the

settlor, even after the death of the settlor, so that the remainder beneficiaries cannot

bring claims against the trustee for any breach of fiduciary duty to themselves. On the

other hand, the remainder beneficiaries may have standing to bring claims against the

trustee for a breach of fiduciary duty to the settlor that occurred during the settlor’s life,

other than any such breach consented to (actually or implicitly) or directed by the settlor,

if such breach adversely affects the interests of the remainder beneficiaries.