The Hong Kong Institute of Chartered Secretaries - Table of … · 2019-08-09 · in position for...

49

Guide Directors’ Induction: An Overview A practical guide to good governance The Hong Kong Institute of Chartered Secretaries

Transcript of The Hong Kong Institute of Chartered Secretaries - Table of … · 2019-08-09 · in position for...

Guide

Directors’ Induction:

An Overview

A practical guide to good governance

The Hong Kong Institute of Chartered Secretaries

Table of Contents

A. DIRECTORS’ INDUCTION ........................................................................................................................................ 1

1. WHAT INDUCTION IS REQUIRED ............................................................................................................... 3

2. BASIC DIRECTORS’ DUTIES .......................................................................................................................... 4

3. TYPES OF DIRECTORS AND COMMITTEES .............................................................................................. 6

4. THE LISTING AND OTHER RULES ............................................................................................................... 9

5. DISCLOSURES OF INTERESTS (DI) ........................................................................................................... 10

6. INSIDER DEALING ....................................................................................................................................... 11

7. INSIDE INFORMATION AND RECENT REFORMS ................................................................................ 13

8 NOTIFIABLE TRANSACTIONS .................................................................................................................... 17

9. CONNECTED TRANSACTIONS .................................................................................................................. 19

10. TAKEOVERS CODE ....................................................................................................................................... 21

11. BOARD PRACTICES ...................................................................................................................................... 23

12. LIAISON WITH MANAGEMENT ................................................................................................................ 24

13. BUSINESS FAMILIARIZATION .................................................................................................................. 25

Appendix A – Checklist on Directors’ Induction ......................................................................................... 26

Appendix B – Overview of Procedures Relating to Appointment of Director ................................... 29

Appendix C – Biography..................................................................................................................................... 31

Appendix D – Disclosure of Interests ............................................................................................................. 33

Appendix E – Questionnaire for Directors’ Interview ............................................................................... 34

Appendix F – Confirmation ............................................................................................................................... 37

Appendix G – Confirmation of Independence (INED) ............................................................................... 38

Appendix H – Publicity Guidelines ................................................................................................................. 41

B. RESOURCES ............................................................................................................................................................ 42

A. DIRECTORS’ INDUCTION

Guide on Directors’ Induction

A.1 In August of 2006, The Hong Kong Institute of Chartered Secretaries (HKICS) issued its first Guidance Note on Directors’ Induction. During the past seven years, there have been successive revisions to the Listing Rules (Rules) and the Corporate Governance Code (Code) thereunder.

A.2 It was in 2012, through a combination of Rule 3.28 and section F to the Code that the

status of the company secretary of listed issuers was fully recognized, with their appointment and termination requiring physical Board meetings of listed issuers. The company secretary is now truly regarded as a member of the senior management team.

A.3 This Guide on Directors’ Induction (Guide) relates to the company secretary’s roles and

responsibilities under Section F to “facilitate induction and professional development of

directors”. A.4 As our members have organised various inductions for directors, we have canvassed their

views as to what they feel as important to share with the profession. The result is the non-exhaustive checklist in Appendix A.

A.5 Directors’ induction session could take the form of one or more sessions. What is important

is that directors should have an understanding of relevant topics prior to their appointment in accordance with the suggested procedures in Appendix B.

A.6 During the induction process, there is the need to be practical and deferential to the

particular circumstance of directors being appointed. For example, a directors’ induction session in the context of an IPO candidate, for compliance reasons, may very well be much different from one for an experienced director being appointed over an existing listed issuer.

A.7 Listing Rules provisions are mandatory. Code provisions operate under the “comply or

explain” regime. That is, whilst most listed issuers would seek to fully comply with Code provisions for good corporate governance, deviation is acceptable where listed issuers consider this to be warranted, subject to explanation. For example, the Code provides for the Chairman and the CEO to be different persons. However, certain listed issuers may see an advantage in having the same person act as Chairman and CEO, and they could explain the rationale behind the deviation. Recommended best practices (RBP) are aspirations of good practices which may eventually become Code or Listing Rules provisions. For example, Board evaluation which is an RBP is a developing topic.

Page 2

A.8 The materials herein are applicable to a Main Board issuer. For a GEM Board issuer, necessary modifications could be made to refer to the appropriate GEM Board rules. The rules and regulations herein are updated to 1 March 2013.

A.9 Special gratitude is extended to the following persons for their significant contributions in

guiding the preparation of this Guide: Edith Shih FCIS FCS (PE), President of HKICS

April Chan FCIS FCS (PE), Immediate Past President and Chairman of Technical Consultation

Panel of HKICS

Brian Lo FCIS FCS, Member, Technical Consultation Panel & Education Committee & Ex-

Chairman Assessment Review Panel

David Ng FCIS FCS, Member, Professional Development Committee & Technical

Consultation Panel

Edwin Ing FCIS FCS, Interim Chief Executive and Past President of HKICS

Jack Chow FCIS FCS, Treasurer of HKICS

Keith Stephenson, Member, Technical Consultation Panel

Paul Mok FCIS FCS, Member, Technical Consultation Panel

Polly Wong FCIS FCS (PE) Chairman of Professional Development Committee

Mohan Datwani LLB LLM MBA (Iowa)(Distinction)

Solicitor & Accredited Mediator Director, Technical and Research The Hong Kong Institute of Chartered Secretaries

Page 3

1. WHAT INDUCTION IS REQUIRED

1.1 Under Rule 3.09, every director of a listed company is required to have the necessary

character, competence, experience and integrity to serve as a director of a listed company. The Stock Exchange of Hong Kong Limited (Exchange) has wide discretion to ask for information on a director being fit and proper to be appointed as a director of a listed issuer.

1.2 Assuming that such fit and proper director is identified, under Code A6.1, “every newly

appointed director of an issuer should receive a comprehensive, formal and tailored induction on appointment”. What precisely does “comprehensive, formal and tailored” mean? This is by no means an easy question to answer. What could be gauged from the statement is that no two induction sessions should be identical, because otherwise they would not be tailor made. Nevertheless, there could be some elements of commonality as set out under the checklist contained in Appendix A.

1.3 Returning to Code A6.1, the provision goes on to state that after the induction, directors

should receive subsequent briefings and professional development necessary to ensure that they have a proper understanding of the “issuer’s operations and business, and is fully aware of their responsibilities under statute and common law, the Exchange Listing Rules, legal and other regulatory requirements and the Issuer’s business and governance policies.”

1.4 Given the wide array of topics which directors should have knowledge as set out under

Code A6.1, it makes sense that the directors’ induction would cover a broad range of topics. Following induction, directors should keep themselves abreast of business, legal and compliance developments and acquire other enhanced governance and soft skills.

1.5 The process of advancing one’s skill sets while acting as director is a process of continuous

professional development (CPD). The purpose is much more than the motion of sitting through classes to “tick a box” of having done so to satisfy disclosure requirements under the annual and other corporate governance reports. Rather, it is for the directors’ own benefit and the skill sets acquired are transferrable.

1.6 The following chapters discuss the various topics as they appear under the checklist in

Appendix A.

Page 4

2. BASIC DIRECTORS’ DUTIES

2.1 A company is a creation of law. It needs someone to represent it, namely its directors, in its

day-to-day business and other functions. The shareholders invest into the company and their rights and obligations are governed by the constitutional documents which represents a binding contract amongst them. For private companies, the number of shareholders is limited to 50 and shares are not freely transferrable under the Companies Ordinance. For publicly listed companies, transfer restrictions are not present.

2.2 The liability of the shareholders is limited where they invest in a limited liability company. However, directors do not have such limited liabilities. They are regarded as fiduciaries with heightened fiduciary responsibilities and related liabilities. While there could be differences in position for overseas companies listed in Hong Kong, nevertheless, all directors have to comply with the Listing Rules, which adopts Hong Kong law standards for directors’ duties.

2.3 In accordance with Code A6., the induction session should start by providing directors with

an understanding of their common law responsibilities. Section 174 of the 2006 UK Companies Act., which partially codifies the common law position, is instructive in this regard. It states that “a director of a company must exercise reasonable care, skill and diligence” and then defines that this as “the care, skill and diligence that would be exercised by a reasonably diligent person with (a) the general knowledge, skill and experience that may reasonably be expected of a person carrying out the same functions carried out by the director in relation to the company, and (b) the general knowledge, skill and experience that the director has”.

2.4 In summary, directors should know that their responsibilities should be commensurate with persons with their knowledge and skill sets and they should make the effort to attend Board and committee meetings. In the absence of suspicion or other grounds, the day-to-day exigencies of the business may be delegated.

2.5 In Hong Kong, the duties of directors have not yet been codified under any statute, although the new Companies Ordinance would contain provisions similar to the UK’s Companies Act for partial codification. In any event, directors should also be asked, prior to the induction session, to read the constitutional documents of the listed issuer; the literature from the Companies Registry (CR), “A Guide on Directors’ Duties”; and The Hong

Kong Institute of Directors’ (HKIOD) “Guidelines for Directors” and “Guide for Independent Non-Executive Directors”, where relevant, for a high level summary of directors’ duties as these would remain relevant. Please refer to Section B “Resources” for the relevant links.

2.6 Also, Rule 3.08 summarizes that directors are required, at common law, to act honestly and

in good faith for the company as a whole, for proper purpose and to be answerable for misapplication of assets and conflict of interests. They are required to make disclosures of interests and to exercise proper skill, care and diligence.

Page 5

2.7 Rule 3.08 then goes on to state obligations, which, in a number of instances are over and

above the common law. For example, a director must take an active interest in the issuer’s affairs and obtain a general understanding of its business. This means that simply attending formal meetings is insufficient.

2.8 In accordance with Rule 3.08 business briefings should be provided to new directors for

their general understanding. This should be a straightforward exercise for a listed issuer, as previous published financial reports would be sufficient. However, for new initial public offering (IPO) applicants, similar information should be provided against publicity guidelines, and if required, non-disclosure agreement. This is because premature disclosures could delay or prevent the IPO altogether. Please refer to Appendix H herein for the scope of the publicity guidelines.

Page 6

3. TYPES OF DIRECTORS AND COMMITTEES

3.1 There are generally three types of directors, executive directors (EDs), non-executive

directors (NEDs) and independent non-executive director (INEDs) (that is NEDs satisfying the independence requirements under Rule 3.13 and designated as such).

3.2 Prior to the appointment of any director, the company secretary should conduct background due diligence, including bankruptcy and litigation searches, and seek the director’s confirmation of other business interests for checking conflicts.

3.3 After induction, depending on the practice of individual companies, a director candidate would be asked to complete a questionnaire modelled around questions under Appendix E. In case of an IPO candidate, in addition to completing the questionnaire, sponsors would require attendance of directors at formal interviews on their replies and other matters they deem appropriate to comply with Practice Note 21 of the Listing Rules on sponsors’ due diligence.

3.4 In many cases, new NEDs (including INEDs) may feel that their responsibilities are much

lower than that of EDs, as they are not part of the executive team. Thus, after explaining the common law duties as heightened by the Listing Rules, directors should be referred to Code A.6.

3.5 Code A.6 states that a listed issuer has a unitary Board. This means that directors

collectively must discharge their fiduciary duties to the listed issuer. Codes A6.7 and 6.8 specify that all directors should make a contribution to the development of the issuer’s strategy and policies through independent, constructive and informed participation. They should regularly and actively attend Board and committee meetings on which they serve. They should also attend general meetings of shareholders for a balanced view of shareholders’ concerns.

3.6 In fact, NEDs have an important role in enhancing the corporate governance of listed

issuers under the various specialized committees as follows:

Audit Committee. Rule 3.21. This is a committee of NEDs only (with no EDs). It

must have a majority of INEDs and one of the INEDs must have the appropriate

professional qualifications or accounting or related financial management expertise.

Under Code C.3, it is explained that the Board should have formal and transparent

arrangements to consider how it will apply financial reporting and internal control

principles and maintain an appropriate relationship with the issuer’s auditor. These

form the basis of the Audit Committee’s terms of reference which needs to be

published on the Exchange’s and the listed issuer’s websites. Normally, the listed

issuer would draft these for the approval of the Audit Committee prior to adoption

Page 7

by the Board of Directors. For some issuers, their Audit Committees are also tasked

with monitoring their company or group’s risk management process if neither a

separate risk committee nor the Board itself has taken up the primary role. The

Hong Kong Institute of Certified Public Accountants (HKICPA) has “A Guide for

Effective Audit Committees” with the sample of the terms of reference of an Audit

Committee which must be approved by the Board of Directors of the listed issuer.

Please refer to Section B “Resources” for the relevant link.

Remuneration Committee. Rule 3.25. This is a committee with a majority of INEDs

and chaired by an INED. Under Code B.1, it is explained that an issuer should

disclose its directors’ remuneration policy and other related matters. The

procedures for setting policies on directors’ remuneration should be formal and

transparent to attract and retain directors. These form the basis of the

Remuneration Committee’s terms of reference which needs to be published on the

Exchange’s and the listed issuer’s websites. Normally, the listed issuer would draft

these for the approval of the Remuneration Committee prior to adoption by the

Board of Directors. As an RBP, in the event the Board approves any remuneration or

compensation arrangements that the Remuneration Committee disagrees with, the

Board should disclose the reasons for its resolution in the next Corporate

Governance Report.

Nomination Committee. Code A5. This is a committee with a majority of INEDs and

chaired by the chairman of the Board or an INED. Under Code A5, it is explained

that the Nomination Committee should review the structure, size and composition

of the Board and where warranted, propose changes to the Board to complement

the issuer’s strategy, identify Board members, select or make recommendations on

potential directors, assess independence of INEDs and make recommendations on

Board appointments and succession planning for directors, in particular the

chairman and chief executive. These form the basis of the Nomination Committee’s

terms of reference which needs to be published on the Exchange’s and issuer’s

websites. Normally, the listed issuer would draft these for the approval of the

Nomination Committee prior to adoption by the Board of Directors.

Corporate Governance Committee. This is optional. It is up to the listed issuer to

determine if there is a need for a committee to take charge of corporate governance

matters or the Board would directly discharge such responsibilities.

Page 8

There are also various business committees that the Board may establish depending on business needs which may include participation by EDs and NEDs. For example, there could be business development, strategy, finance, risk, management and other committees.

3.7 Given the importance of NEDs, under Code A2.7, the chairman of the Board of Directors

should hold meetings with NEDs at least once a year and under Code A2.9, promote a culture of openness and debate and facilitate the effective contributions of NEDs.

3.8 As from 1 January 2013, every listed issuer must have at least one-third of its Board

members as INEDs, subject to a minimum of three INEDs. Further, under Rule 3.10(2), at least one of the INEDs must have appropriate professional qualifications or accounting or related financial management expertise. From a recent HKICS research report, accountants are the preferred choice to act as INEDs for listed issuers.

3.9 Under Code A4.3, INEDs should not normally serve for more than 9 years unless their re-

election is supported by an explanation of their continued independence and suitability for re-election in the AGM circular and approved by shareholders. To safeguard independence, INEDs could at most be granted during a 12-month period, the lesser of 0.1% options and an aggregate in value of the underlying shares at HK$5 million, based on the closing price on the date of grant. Any further grant during the period requires approval of the independent shareholders at a general meeting under Rule 17.04.

3.10 Directors should be in the position to request independent professional advice on matters

they deem necessary at the expense of the listed issuer.

Page 9

4. THE LISTING AND OTHER RULES

4.1 As set out under Rule 2.01, the principal function of the Exchange is to provide a “fair,

orderly and efficient market for trading of securities” which reflects Section 21 of the Securities and Futures Ordinance’s (SFO) statutory obligation to maintain an orderly, informed and fair market for the trading of securities. This principal function underlies the rationale of many of the rules and regulations of the Exchange and the Securities and Futures Commission (SFC), including those relating to minority protection. Directors’ understanding of the principal function during the induction would assist them to more readily appreciate the rationale behind the rules and regulations from both the Exchange and the SFC.

4.2 Directors should be made aware that after the induction session they are required to sign a

directors’ undertaking (Undertaking), in the form of Appendix 5B of the Listing Rules. This certifies that directors would, in the exercise of their powers and duties as a director of the listed issuer, comply to the best of their abilities with the Listing Rules, and also use their best endeavours to procure that the issuer and any of their alternates (who by the way are not even counted towards directors’ attendance at Board and other committee meetings) to comply with the Listing Rules.

4.3 Under the Undertaking, directors are also required to undertake to comply with part XV of

the SFO, the Code on Takeovers and Mergers (“Takeovers Code”), the Code on Share Repurchase and all other securities laws and regulations, and to procure that the listed issuer would comply with these rules and regulations.

4.4 In accordance with the Undertaking, in addition to personal compliance by directors of

applicable rules and regulations, directors should be concerned with compliance by the listed issuer under proper internal control procedures. The written procedures should be made available to directors prior to the induction to allow them to raise relevant questions during induction.

4.5 The emerging better practice would be for directors to be briefed on the issuer’s risk management processes during the induction session. Directors should understand that compliance with applicable rules and regulations is ultimately their responsibility.

Page 10

5. DISCLOSURES OF INTERESTS (DI)

5.1 As set forth under the Undertaking, all directors are required to comply with Part XV of the

SFO. The provisions of Part XV are complex. 5.2 Section 308 of Part XV of the SFO refers to the “duty of disclosure” arising under Divisions

7 to 10 of the part in respect of dealings in securities by directors and certain other insiders, which includes a director’s family interests, spouse, minor child, controlled corporation, and trusts interests amongst others. The definition of securities is also extended to dealings in structured products and derivatives by directors and other insiders.

5.3 Under section 347, where directors come under a duty of disclosure, they should notify the

listed issuer and the Exchange of their interests. The notification should be provided to the listed issuer and The Exchange contemporaneously, or as close in time as possible. The obligation to notify generally has to be effected, in accordance with section 348, within three business days of the relevant event occurring or coming to the knowledge of the director, and ten business days upon the appointment of a director to an existing listed issuer for an initial disclosure of interests.

5.4 The failure to comply with Part XV entails serious consequences. These include a fine of up

to HK$100,000 and two years’ imprisonment, or on summary conviction a fine of up to HK$10,000 and 6 months’ imprisonment. The SFC is serious as to enforcement of disclosure obligations which is important for an orderly market in trading of securities and to prevent market manipulation. A director’s violation of disclosure could also trigger investigations into other regulatory infractions depending on the seriousness of the breach and the relevant circumstances.

5.5 Directors should seek their own professional advice they require in case of doubt. The link

to the SFO is set out under Section B “Resources” for directors’ reference.

Page 11

6. INSIDER DEALING 6.1 On the topic of the SFO, directors should then be made aware of the concept of market

misconduct under the SFO with specific focus on insider dealing. 6.2 Under the SFO, there are dual, but exclusive, civil and criminal regimes for the following

market misconducts (1) insider dealing, (2) false trading, (3) price rigging, (4) disclosure of information about prohibited transactions, (5) disclosure of false or misleading information including transactions, and (6) stock market manipulation under Parts XIII and XIV of the SFO respectively. That is, the SFC could choose either to pursue a civil case under the Market Misconduct Tribunal (MMT) established under section 251 of the SFO for breaches of Part XIII, or recommend the Department of Justice to pursue a criminal case under Part XIV of the SFO. The SFC also has wide remedial powers under section 213 whether it pursues a civil or criminal case.

6.3 In relation to the market misconduct of insider dealing under Parts XIII and XIV of the SFO,

directors are regarded as persons “connected” with the listed issuer. As a connected person, if a director has “relevant information” and either deals with, or counsels or

procures another person to deal in securities and derivatives of the listed issuer, with knowledge or reasonable cause to believe that the person would so deal in the shares and derivatives that would amount to insider dealing with civil or criminal consequences.

6.4 As to what constitutes “relevant information” to trigger insider dealing, the SFO has a

definition. Basically, there has to be (1) specific information which is (2) not generally known and (3) would be likely to materially affect the price of listed securities.

6.5 Relevant information, as defined, excludes information that is generally known. Thus,

directors could respond to any questions from any persons seeking information on the company by asking the person to read the listed issuer’s disclosures on its website disseminated for the purpose of keeping the market informed of the listed issuer’s developments. Further, the person might seek professional advice on such information, as required.

6.6 Directors should understand that where the SFC investigates potential market misconduct,

including insider dealing, the process in itself would be costly, stressful and time consuming for directors and others involved, even if the SFC chooses not to proceed with the case. Directors should not put themselves in a position of being investigated.

6.7 Assuming for the purposes of discussions, the SFC pursues an insider dealing case as a civil

case, and prevails at the MMT, the MMT could then disqualify, without leave of court, the insider dealer from being a director (disqualification) or from dealing in securities for up to 5 years (cold shoulder), and not to perpetrate the market misconduct (cease or desist) amongst its other powers. Any contravention of the MMT’s order could lead to a fine of up to HK$1 million and imprisonment for 2 years. Also, the MMT could order payment of the

Page 12

relevant costs of the Government and SFC for the investigations and proceedings, and recommend that relevant disciplinary proceedings be initiated where the insider dealer is a professional. The insider dealer could be asked to pay the Government for the gain made or loss avoided under section 257 of the SFO (disgorgement order) and is exposed to recovery by third parties for their pecuniary losses under section 281 of the SFO. In this connection, the MMT is under current jurisprudence not required to reconcile the profits with the losses for a net position.

6.8 If the SFC chooses to recommend the Department of Justice to pursue a criminal

prosecution, the court could, on indictment, fine the convicted insider dealer up to HK$10 million and impose a prison sentence of up to 10 years, or on a summary conviction, up to HK$1 million and a prison term of up to 3 years under section 303 of the SFO. The Court could also order disqualification, cold shoulder and recommend discipline against the person. The conviction could also open up the convicted person to civil liability under section 305 of the SFO.

6.9 Directors should be provided with the Model Code and be reminded that under the Model

Code, they could not deal in the securities of their listed issuers where they are in possession of unpublished inside information at any time, or during the black-out period of 30 days immediately preceding the publication date of the quarterly or interim results and 60 days immediately preceding the publication date of the annual results. Irrespective, directors should in general not deal in the listed issuer’s securities without prior notification to the chairman. There are also other matters set out under the Model Code which directors should be asked to familiarise themselves with relating to takeovers and disclosure obligations under the SFO.

Page 13

7. INSIDE INFORMATION AND RECENT REFORMS 7.1 “Inside information” under Part XIVA of the SFO, effective as from 1 January 2013, is

defined in the same way as relevant information for the purposes of insider dealings. A listed issuer has the obligation to disclose as soon as practicable any inside information which comes to its knowledge (section 307B of SFO) for equal, timely and effective access by the public (section 307C of SFO). A director as an officer of the listed issuer, must take all reasonable measures from time to time to ensure that proper safeguards exist to prevent a breach of the disclosure requirement (section 307G(1) of SFO). Further, the disclosure must not be false or misleading as to a material fact or omission that is known or ought to have been known (section 307B(3)).

7.2 These mean that subject to certain safe harbours, the listed issuer must announce the

inside information on the Exchange’s website (section 307C) prior to or at the same time as other forms of public dissemination of the information. The safe harbours are contained under Section 307D and aimed to prevent premature disclosures which could affect the listed issuer’s legitimate business. Thus, where confidentiality is preserved, disclosure is not required for incomplete negotiations or trade secrets. Further, disclosure is not required where there is a law or court order restricting such disclosure, and in case of a foreign law, court order or enforcement agency restriction, upon the grant of a waiver by the SFC.

7.3 Prior to Part XIVA of the SFO being effective, under Rule 13.09 of the Listing Rule which did

not have statutory backing, breaches of general disclosure obligations normally only attracted public censure of directors and attendance at corporate governance courses. As from 1 January 2013, in case of a breach of the disclosure requirements, the SFC could institute “disclosure proceedings” before the MMT, with sanctions similar to insider dealings, that is disqualification, cold shoulder, ceases and desist, and additionally for directors (and the chief executive), a regulatory fine of not exceeding HK$8,000,000 could be imposed by the MMT. Also, it opens up civil liabilities to the director (and chief executive) to pay compensation by way of damages for pecuniary loss as a result of the breach of the general disclosure obligations. Other ancillary orders include an order recommending discipline, internal control review of the listed issuer’s compliance procedures and directors’ attendance at corporate governance courses.

7.4 Directors need to be familiar with the SFC’s “Guidelines on Disclosure of Inside Information”

of June 2012, effective 1 January 2013, the link (under Section B “Resources”) of which should be provided to directors. In the guidelines, the SFC specified that it is for the listed issuer to make a prompt assessment of the likely impact of events and circumstances on its share price and decide consciously whether disclosure is required. The SFC also listed some 34 common events, which were not intended to be exhaustive, with possible inside information implications.

7.5 The following is the list of the 34 circumstances:

Page 14

changes in performance, or the expectation of the performance, of the business changes in financial condition, e.g. cash flow crisis, credit crunch changes in control and control agreements changes in directors and (if applicable) supervisors changes in directors’ service contracts changes in auditors or any other information related to the auditors’ activity; changes in the share capital, e.g. new share placing, bonus issue, rights issue, share

split, share consolidation and capital reduction issue of debt securities, convertible instruments, options or warrants to acquire or

subscribe for securities takeovers and mergers (corporations will also need to comply with the Takeovers Codes

that include specific disclosure obligations purchase or disposal of equity interests or other major assets or business operations formation of a joint venture; restructurings, reorganizations and spin-offs that have an effect on the corporation’s

assets, liabilities, financial position or profits and losses; decisions concerning buy-back programmes or transactions in other listed financial

instruments; changes to the memorandum and articles (or equivalent constitutional documents); filing of winding up petitions, the issuing of winding up orders or the appointment of

provisional receivers or liquidators; legal disputes and proceedings; revocation or cancellation of credit lines by one or more banks;

changes in value of assets (including advances, loans, debts or other forms of financial assistance);

insolvency of relevant debtors; reduction of real properties’ values; physical destruction of uninsured goods; new licenses, patents, registered trademarks; decrease or increase in value of financial instruments in portfolio which include

financial assets or liabilities arising from futures contracts, derivatives, warrants, swaps protective hedges, credit default swaps;

decrease in value of patents or rights or intangible assets due to market innovation; receiving acquisition bids for relevant assets; innovative products or processes; changes in expected earnings or losses; orders received from customers, their cancellation or important changes; withdrawal from or entry into new core business areas; changes in the investment policy; changes in the accounting policy; ex-dividend date, changes in dividend payment date and amount of dividend; changes

in dividend policy;

Page 15

pledge of the corporation’s shares by controlling shareholders; and changes in a matter which was the subject of a previous announcement. The SFC will provide an initial consultation service for two years as from 1 January 2013 to the market with a view to compliance in the form of verbal discussions, but views are non-binding in nature.

7.6 As discussed, Part XIVA requires a director to take all reasonable measures to ensure proper safeguards exist to prevent a breach of the general disclosure obligation (section 307G(1) of the SFO). Directors would be in breach where they intentionally, recklessly, negligently or otherwise failed to take reasonable measures to ensure that the proper safeguards exist (section 307G(2)).

7.7 The SFC is of the view that while there is a unitary Board, the NEDs are not involved in day-

to-day business and they have to rely on the internal control procedures of the listed issuer amongst other matters. Thus, the Board’s responsibility for establishing and monitoring key internal control procedures is of particular significance for NEDs in view of their reliance.

7.8 NEDs accordingly have to be especially concerned with proper internal control procedures being in place in view of the serious consequences of Part XIVA with the regulatory penalty of HK$8,000,000 and follow-on civil penalties. In accordance with Code A1.8 directors should be provided insurance cover in respect of legal actions, which the listed issuer should seriously consider extending to its officers (D&O insurances).

7.9 As suggested by the SFC under the Guide, and for which the company secretary has a facilitative role, the listed issuer should:

establish controls for monitoring business & corporate developments & events establish periodic financial reporting procedures maintain and regularly review a sensitivity list identifying factors or developments

which are likely to give rise to the emergence of inside information authorise one or more officers or an internal committee to be notified of any potential

inside information and to escalate any such information to the attention of the Board maintain an audit trail of meetings and discussions for assessment of inside

information restrict access to inside information to a limited number of employees on a need-to-

know basis

ensure appropriate confidentiality agreements are in place when entering into significant negotiations

designate a small number of officers to speak on behalf of the company develop procedures to review presentation materials in advance before releasing the

same at media briefings record briefings and discussions with analysts or the media develop procedures for responding to market rumours, leaks and inadvertent disclosures

Page 16

provide regular training to relevant employees to help understand the company’s policies, procedures and disclosure duties

document the disclosure policies and procedures in writing disseminate inside information via electronic publication system before information is

released via other channels publish the disclosure policies and procedures.

7.10 Rule 13.09 would focus on the issue of false market as from 1 January 2013. When the Exchange learns of possible market misconduct by a listed issuer, the matter is to be referred to the SFC. Only where the SFC decides not to pursue the matter would the Exchange pursue the matter.

Page 17

8 NOTIFIABLE TRANSACTIONS

8.1 In addition to the general disclosure obligation for inside information, directors should be

concerned that the listed issuer discharges its disclosure obligation relating to notifiable transactions under Chapter 14 of the Listing Rules.

8.2 Under Rule 14.04, the list of what amounts to notifiable transactions includes (1)

acquisition or disposal of assets (2) deemed disposals (3) writing, accepting, transferring, exercising or terminating an option (4) entering or terminating finance leases (5) grant of an indemnity or guarantee (6) providing financial assistance to a listed issuer and (7) a list of other transactions. In addition, it also includes certain disposal of assets.

8.3 Directors have to ensure that the system of procedures is in place for the listed issuer to

notify the investing public of notifiable transactions, as part of the day-to-day compliance of the listed issuer.

8.4 The Exchange, under Rule 14.08, has helpfully summarized the different types of notifiable

transactions in a matrix. The transaction types are (1) share transaction (involving securities and not cash) (2) discloseable transaction (3) major transactions (disposal) (4) major transaction (acquisition) (5) very substantial disposal and (6) very substantial acquisition. The transactions are to be considered against certain applicable tests, or what is commonly known as “five tests”. Instead of 30 types of transactions (six types of transactions x five tests), there are 28 types of transactions, as the test of equity capital ratio is not applicable to major and very substantial disposals.

8.5 The five tests relate to certain financial ratios of the listed issuer. These are (1) asset ratio

(2) consideration ratio (3) profits ratio (4) revenue ratio and (5) equity capital ratio respectively. Rule 14.07 explains the details of these percentage ratios further. In certain cases, the listed issuer could propose alternative tests to the Exchange where the five tests are not applicable.

8.6 In determining the disclosures applicable for notifiable transactions, there is need to

consider the transaction type against the applicable test ratio. There are thus (1) share transactions within a 5% test ratio (2) discloseable transactions within a 5% to 25% test ratio (3) major transactions (disposal) within a 25% to 75% test ratio (4) major transactions (acquisition) within a 25% to 100% test ratio (5) very substantial disposal with over 75% test ratio and (6) very substantial acquisition with over 100% test ratio.

8.7 Rule 14.33 then sets out the matrix for the various disclosure requirements. Directors

should be aware that as a minimum, in relation to notifiable transactions, there is need to (1) notify the Exchange and (2) the public by way of announcement under Rule 2.07C. Depending on the transaction type and applicable test ratio, there may be need for (3) explaining the transaction in a circular to shareholders (4) obtaining shareholders’ approval and (5) providing accountants’ reports. If the transaction amounts to a reverse takeover, the Exchange could deem this to be a new listing.

Page 18

8.8 There are various rules relating to the contents of announcements (Rule 14.58), circulars

(Rule 14.63) and other matters. It is probably sufficient to inform directors that the company secretary would be the first point of contact for them to deal with these issues.

Page 19

9. CONNECTED TRANSACTIONS

9.1 Under Chapter 14A of the Listing Rules, where a transaction of the listed issuer is regarded

as a “connected transaction”, there are additional compliance requirements. These are to ensure that the interests of shareholders as a whole are taken into account by the listed issuer when it enters into a connected transaction.

9.2 Under Rule 14A.02, where a transaction is a connected transaction, a circular has to be

sent to shareholders providing information as to the transaction. Further approval of the shareholders will be required before the transaction could proceed. Any person with a material interest in the transaction would not be permitted to vote. That is, the connected transaction has to be approved by independent shareholders’ vote albeit there are certain exemptions.

9.3 Directors, for the purposes of connected transactions, are “connected persons” for the

duration they serve as directors and for a period of 12 months thereafter. The definition of a connected person extends to a director’s “associates” which includes (1) any person cohabiting with the director as a spouse (2) child (3) step-child (4) parent (5) step-parent (6) brother (7) sister (8) step-brother (9) step-sister (10) father-in-law (11) mother-in-law (12) son-in-law (13) daughter-in-law (14) grandparent (15) grandchild (16) uncle (17) aunt (18) cousin (19) brother-in-law (20) sister-in-law (21) nephew and (22) niece, and (23) any company of which the director or any such associates control 50% of the vote at general meeting or the right to appoint a majority of directors. It also includes (24) any other person or entity that the director has entered or proposes to enter into any agreement, arrangement, understanding or undertaking, whether formal or informal on whether express or implied, in respect of the transaction which in the opinion of the Exchange should be regarded as a connected person.

9.4 Rule 14A.13 defines what amounts to a “connected transaction”. This includes any (1)

transaction between a listed issuer and a connected person (2) certain deemed transactions relating to acquisition or disposal of interest in a company (3) the provision of certain financial assistance by or to a listed issuer and related granting of indemnity, guarantee or security (4) options and (5) joint ventures. There are certain connected transactions which are regarded as “continuing connected transaction”. These usually involve provision of goods, services, or financial assistance over a period of time in the ordinary course of business of the issuer. For example, where a director buys premises and leases it out to the listed issuer for an office, this would be a continuing connected transaction.

9.5 Rule 14A.16 then provides for certain exemptions for connected transactions and

continuing connected transactions. Depending on the nature of the exemption it could exempt all requirements in relation to reporting, announcement, independent shareholders’ approval and annual review (for continuing connected transactions) or independent shareholders’ approval requirement only.

Page 20

9.6 The connected transactions with full exemption include certain (1) intergroup transactions

(2) issue of new securities (3) stock exchange dealings (4) purchase of own securities (5) director services contract (6) consumer goods or consumer services (7) sharing of administrative services (8) transaction with persons connected at the level of subsidiaries (9) transactions with associate of a passive investor and (10) de minimis transactions based on certain applicable thresholds and monetary value of up to a maximum of HK$1 million when aggregated for all connected transactions over a 12-month period.

9.7 The continuing connected transactions with full exemption include certain (1) consumer

goods or consumer services (2) sharing of administrative services and de minimis transactions based on certain applicable thresholds and monetary value of up to a maximum of HK$10 million when aggregated for all continuing connected transactions over a 12-month period.

9.8 The rules are complex and company secretary should be the first point of contact for

directors to deal with connected, including continuing connected transactions related issues. There is the “Guide on Connected Transaction Rules” issued by the Exchange the link of which is set out under Section B “Resources” and there would likely be market consultation on the topic.

Page 21

10. TAKEOVERS CODE

10.1 The Takeovers Code, as explained in paragraph 1.2 of the “Introduction” thereto, relates to

takeovers, mergers and share repurchases and is intended to achieve equality of treatment of shareholders, mandating disclosure of timely and adequate information to enable shareholders to make an informed decision as to the merits of an offer, and for there to be a fair and informed market in the shares of the affected listed issuer.

10.2 The Takeovers Code does not have the force of law. This means that directors should not

simply read the Takeovers Code and assume it is complete. Directors need to understand that the SFC retains the ultimate interpretation and would consider the spirit and intent of the Takeovers Code as a whole. The SFC would, where a ruling is sought, consider not simply the strict provisions of the Takeovers Code, but the spirit and intent of the code from the facts presented.

10.3 Under paragraph 1.5 of the Introduction of the Takeovers Codes, directors have

responsibilities along with people seeking to gain or consolidate control of listed issuers, their professional advisers and persons connected with the transaction and persons actively engaged in the securities market under the Takeovers Code. In case of doubt, the director could seek rulings from the Executive Director of the Corporate Finance Division (Executive) of the SFC. There would be detailed review of the issues and the Executive may find it necessary to convene an informal meeting to hear the views of interested parties before making a ruling.

10.4 Rule 26 of the Takeovers Code states that where a person or persons acting in concert

acquires or consolidates 30% of the voting rights of the listed issuer then there is a need to make a mandatory general offer to all shareholders. The exceptions to such mandatory general offer obligations include (1) the “creeper”, that is, where less than 2% of the voting rights of the listed issuer are acquired within a 12-month period (2) where the persons already own over 50% of the voting rights of the listed issuers and (3) where the SFC grants a whitewash waiver.

10.5 When a mandatory offer is triggered, the acquirer would have to prove its financial capability to acquire the shares in the hands of the public and the standby facilities and arrangement fees could be substantial. The acquirer also needs to appoint a placement agent to place down shares to maintain a free float for the shares in the hands of the public and the financial advisory and placement fees would also be substantial. Thus, no one would desire to inadvertently trigger the obligation to make a mandatory general offer. For example, on 22 May 2012 the Executive publicly censured Capital VC Limited and Yau Chung Hong, executive director, substantial shareholder and member of investment committee of Capital VC Limited (an investment company under Chapter 21 of Listing Rules) for breach of the mandatory offer obligation requirement in Rule 26.1 of the Takeovers Code and imposed a cold shoulder denying Yau direct or indirect access to the Hong Kong

Page 22

securities markets for 18 months until 22 November 2013 for inadvertently consolidating control to 30.19% of Longlife Group Holdings limited, a GEM Board listed company, thereby triggering the mandatory obligation, but failing to do so (source: Takeovers Bulletin, Issue

No. 21, June 2012). 10.6 Where two or more persons who are not parties acting in concert become parties in concert

and they hold between 30% to 50% of the voting rights of the listed issuer, the mandatory general obligation would not normally be triggered, even though when they come into concert, this exceeds 30% of the voting rights of the listed issuer. Further, they could collectively acquire no more than the creeper of 2% of the voting rights within a 12-month period.

10.7 The SFC notes that the majority of questions which arise are whether parties are parties

“acting in concert”. The definition of acting in concert is contained under Chapter 2 of the Takeovers Code. It generally refers to persons, who pursuant to an agreement or understanding (whether formal or informal) actively co-operate to obtain or consolidate “control” of a listed issuer through the acquisition by any of them of voting rights of the listed issuer. The definition then specifically refers to various classes of persons who are deemed to act in concert. These include directors of the listed issuer, their close relatives and related trusts and companies controlled by them. “Close relatives" is defined to mean a person's spouse, de facto spouse, children, parents and siblings. With such wide definition, the scope of the Takeover Code is extensive.

10.8 The SFC has the right to grant a whitewash waiver, where the person or persons acting in

concert acquire or consolidate in excess of 30% voting rights from an issue of new shares and securities sanctioned by a vote of the independent shareholders. The INEDs would advise the independent shareholders based on advice from an independent financial adviser. Also, in many instances, investors may use convertible loan notes, and it is up to the professional advisers of the offeror and offeree to advise upon the takeovers implication under the Takeovers Code, in consultation with the Executive, as necessary.

10.9 The Takeovers Code are complex and that directors should be aware that when they act in concert and seek to actively co-operate with others to gain or consolidate control over a listed issuer, that there are potential Takeovers Codes issues.

Page 23

11. BOARD PRACTICES

11.1 Under Section F of the Code, the company secretary has the supporting role to “ensure

good information flow within the Board and that Board policy and procedures are followed.” Thus, the various aspects of Board practices are also part of the company secretary’s advisory roles on “governance matters”, referred to under Section F of the Code.

11.2 When Board meetings are called, directors should make an effort to attend such meetings

and all records of attendance, would be disclosed in the next annual report or corporate governance report. In many companies, it is now permissible to have telephone meetings. Also, there are technologies available to assist in distribution of Board papers for the listed issuer to adopt, as appropriate.

11.3 The NEDs should especially be concerned with there being sufficient internal control

procedures with the listed issuer. They should add to the discussions and deliberations with their knowledge and experiences as part of their active interest in the affairs of the listed issuer. They should also offer their learning and expertise.

11.4 Directors during Board meetings should be mindful of their independence in relation to the

transactions in question. Any material interests need to be disclosed, and there may be situations where they may have to abstain from voting on matters where, for example, there is a conflict of interests.

11.5 Directors, where they are involved in various committees, should realize that they perform

an important function in keeping a proper check and balance on various Board functions including audit, nomination and remuneration matters, and where there is a governance committee, governance matters.

11.6 The Chairman of the Board should meet with the NEDs at least once a year to evaluate any

issues that might be raised by them and to take into account their views on matters pertaining to the strategy of the company and other matters. Directors should understand that this does not prevent them from raising issues from time to time directly with the Chairman, even prior to such meetings.

11.7 In terms of the conduct of the meetings, it is important that there are proper notices of

meetings and agendas. Directors should offer their views without inhibition, and for a proper deliberation by directors present, with courtesy and respect for each other. Any proposed items for discussions should be communicated beforehand in as much as possible.

11.8 It is the company secretary’s duty to ensure that Board policy and procedures are followed.

There is need to prepare, circulate and keep all notices of meetings, agendas, Board resolutions in good order, and depending on the requirements of the listed issuer, records of implementation of the Board resolutions. In addition, there is need to coordinate management and experts to attend meetings upon request of the Chairman and directors.

Page 24

12. LIAISON WITH MANAGEMENT

12.1 In theory, the day-to-day business of the listed issuer is carried out by the unitary Board.

In practice, the Board sets the strategy and directions for implementation by management. The senior management for most listed issuers include the CEO, CFO and COO, or the three 3 Cs. There could also be the CLO (Chief Legal Officer) and CCO (Chief Compliance Officer) etc. depending on the organisation.

12.2 The Code provides that the Chairman of the Board and the CEO should be separate persons.

There are various listed issuers with a common Chairman and CEO. The listed issuer has to decide what is the best Board and management structure to comply or explain the reasons for the Chairman and the CEO being the same person.

12.3 Under Code D1, the Board should give clear directions to the management on matters that

must be approved by the Board before decisions are executed. There should thus be a list of matters which are specifically reserved for Board approval. Directors should take an active interest in the list as part of the internal control of the listed issuer.

12.4 Also, when the Board delegates aspects of its management and administration functions

to management, it must, at the same time, give clear directions as to the power of management, in particular, where management should report back and obtain prior Board approval before making decisions or entering into any commitments on behalf of the issuer.

12.5 The Board should not delegate matters to a Board committee, executive directors or management to an extent that would significantly hinder or reduce the ability of the Board as a whole to perform its functions.

12.6 The Code also provides that an issuer should formalize the functions reserved to the

Board and those delegated to management. It should review those arrangements periodically to ensure that they remain appropriate for the issuer’s needs.

12.7 An issuer should disclose the respective responsibilities, accountabilities and contributions

of the Board and management. Also, directors should clearly understand delegation arrangements in place. Issuers should have formal letters of appointment for directors setting out the key terms and conditions of their appointment.

12.8 The terms of reference of the Board (or a committee) should include at least the

provisions: (1) to develop and review an issuer’s policies and practices on corporate governance and make recommendations to the Board (2) to review and monitor the training and continuous professional development of directors and senior management (3) to review and monitor the issuer’s policies and practices on compliance with legal and regulatory requirements (4) to develop, review and monitor the code of conduct and compliance manual (if any) applicable to employees and directors, and (5) to review the issuer’s compliance with the Code and disclosure in the Corporate Governance Report.

Page 25

13. BUSINESS FAMILIARIZATION

13.1 The listed issuer is in the business of maximizing the return to its shareholders.

Accordingly, directors should be familiar with the business operations of the listed issuer. It is only with such understanding that directors should be able to make a real contribution to the listed issuer’s strategy and offer their perspectives from their learning and experiences.

13.2 The company secretary should work with management to prepare a proper business briefing

prior to the appointment of directors. If the company is already listed, the latest annual reports, business plans and budgets, and an opportunity for the new director to discuss the business aspects with the management should be arranged for directors. Where the company is an IPO candidate, then, a business briefing should be provided against publicity guidelines, and if required, non-disclosure agreement, and discussions with management should be arranged.

13.3 The listed issuer should consider if there should be visits by directors to the business

locations where the business of the listed issuer is being carried out. Directors should know of the operating environment, including the local community and culture where the business operates. They should be able to talk to those in charge on the front line and to conduct their own SWOT analysis under wider regulatory concerns like environmental policies, anti-competitive issues and corrupt practices, along with any other issues they deem appropriate.

13.4 If the business is being carried out in a foreign jurisdiction, the listed issuer should balance

the cost benefits and with technology could replace site visits with telephone or video conferences, etc. The long term advantages, in terms of real contribution of directors from business familiarization, should be considered.

Page 26

Appendix A – Checklist on Directors’ Induction

A. Directors’ Induction: o Listing Rules, Ordinances & Takeovers Code

1. What Induction is Required:

o Comprehensive Induction Session o Continuous Professional Development (CPD)

2. Basic Directors’ Duties:

o Unlimited Liabilities & Common Law Duties o Heightened Listing Rules Responsibilities

3. Types of Directors and Committees:

o ED, NED & INED (Confirmation of Independence) o Concept of Unitary Board & Roles o Audit, Remuneration & Nomination o Governance Committee (Optional) o Other Issues

4. The Listing and other Rules: o Directors’ Undertaking o Explain Internal Control Procedures o Management to answer questions

5. Disclosure of Interest (DI):

o Part XV of SFO, Divisions 7 to 10 o Extended Reach o Penalties for Failure to Comply o Professional Advice when in Doubt

6. Inside Dealing:

o Model Code for Securities Transaction o Market Misconducts: Mutually Exclusive Civil and Criminal Regimes o Market Misconduct Tribunal (MMT) or Court o Extended Reach o Meaning of Inside Information o Black Out Periods

7. Inside Information and Recent Reforms:

o Part XIVA, Securities and Futures Ordinance o Statutory Backing to Inside Information

Page 27

o MMT Regulatory Fine & Civil Liabilities o Guidelines on Disclosure of Inside Information o NEDs & Internal Control Procedures o Exchange & False Market

8. Notifiable Transactions:

o Definition of Notifiable Transactions o The Transaction Types/Matrix o The Five Tests o Disclosure Requirements

9. Connected Transactions:

o Definition of Connected Transactions o Director as Connected Person o Extended Definition o Continuing Connected Transactions o Exceptions o HKEx “Guide on Connected Transaction Rules

10. Takeovers Code:

o Informed Decision for Fair and Informed Market o Mandatory General Offer o Creeper o Concert Parties o Whitewash Waiver o Role of INEDs

11. Board Practices:

o Directors to attend Board Meetings o Attendance Records & Contribution o NEDs & Internal Control Procedures o Directors’ Independence & Disclosures/Voting o Managed Communication o Company Secretary Roles

12. Liaison with Management:

o Unitary Board & Senior Management o Chairman and CEO Roles o Directors & Internal Control o Delegation of Administration Functions o Terms of References for Appointment

13. Business Familiarization:

o Maximizing Return to Shareholders

Page 28

o Business Familiarization & Real Contribution o Publicity Guidelines for IPO Candidates o Site Visits & SWOT analysis

Page 29

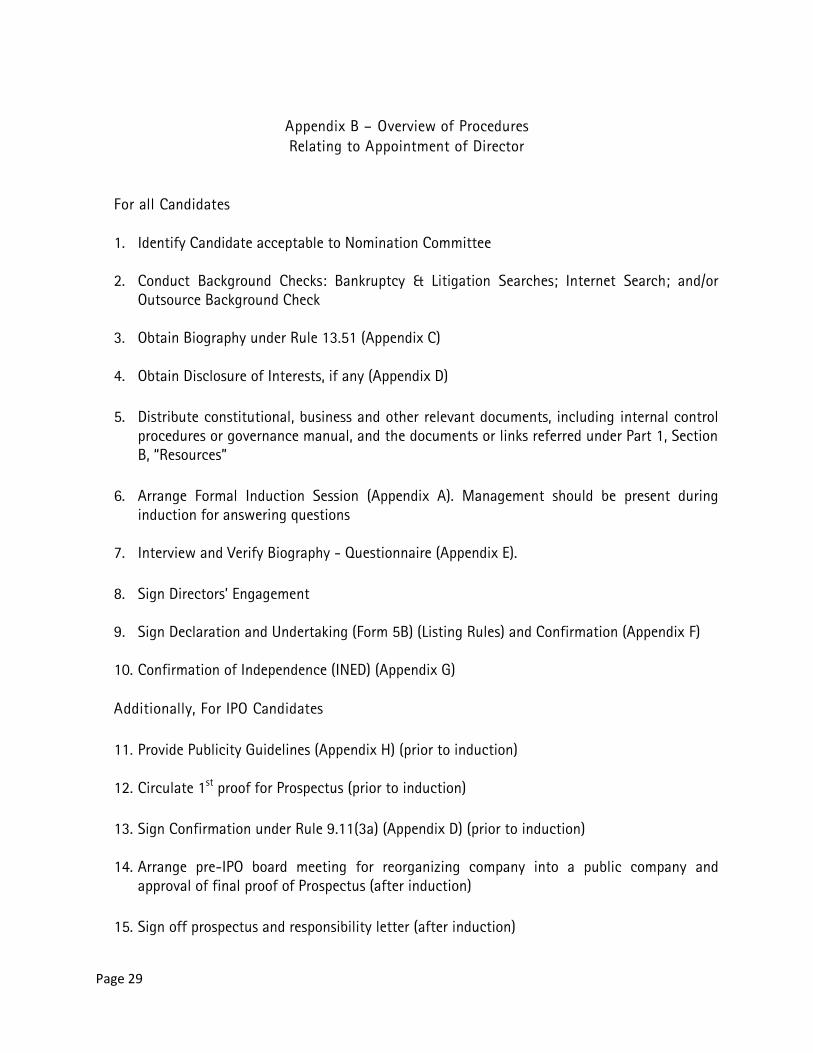

Appendix B – Overview of Procedures

Relating to Appointment of Director

For all Candidates

1. Identify Candidate acceptable to Nomination Committee

2. Conduct Background Checks: Bankruptcy & Litigation Searches; Internet Search; and/or Outsource Background Check

3. Obtain Biography under Rule 13.51 (Appendix C)

4. Obtain Disclosure of Interests, if any (Appendix D)

5. Distribute constitutional, business and other relevant documents, including internal control procedures or governance manual, and the documents or links referred under Part 1, Section B, “Resources”

6. Arrange Formal Induction Session (Appendix A). Management should be present during induction for answering questions

7. Interview and Verify Biography - Questionnaire (Appendix E).

8. Sign Directors’ Engagement

9. Sign Declaration and Undertaking (Form 5B) (Listing Rules) and Confirmation (Appendix F)

10. Confirmation of Independence (INED) (Appendix G)

Additionally, For IPO Candidates

11. Provide Publicity Guidelines (Appendix H) (prior to induction)

12. Circulate 1st proof for Prospectus (prior to induction)

13. Sign Confirmation under Rule 9.11(3a) (Appendix D) (prior to induction)

14. Arrange pre-IPO board meeting for reorganizing company into a public company and approval of final proof of Prospectus (after induction)

15. Sign off prospectus and responsibility letter (after induction)

Page 30

Announcement

16. Announce appointment generally or in IPO Prospectus

Note: The procedures may change according to the requirements of the listed issuer. The form of

documents would change according to the requirements and advice from professional advisors

Page 31

Appendix C – Biography

[NAME OF COMPANY]

Biography

[Name of ED/NED / INED]

[Biographical Details]*

Save as disclosed above, [Name] has not held any directorship in other public companies, the securities of which are listed on any securities market in Hong Kong or overseas in the last three years, and any other positions with the Company and other members of the Group in the past three years immediately preceding the date of this document/prospectus. Save as disclosed herein, there are no other matters in relation to [Name] which are required to disclose pursuant to Rule 13.51(2) of the Listing Rules.

Confirmed by:

_____________________

[Name]

Date:

*Note: Need to verify with documents and interview

Page 32

[Additionally, for IPOs] [The Exchange] Dear Sirs, Re: [The Company] Rule 9.11(3a) Listing Rules I am [ED/NED/INED] of the [Company]. I confirm that the [1st] proof of the listing documents contain all my biographical details under Rule 13.51(2), which are true and accurate, and complete and undertake prior to dealing of the securities of the [Company], to inform you of any changes. I also undertake to lodge with you, as required under Rule 9.11(38) my declaration and undertaking under Form B, Appendix 5 of the Listing Rules. Yours faithfully, _____________________

[Name]

Date:

Page 33

Appendix D – Disclosure of Interests

[NAME OF COMPANY] Disclosure of Director’s Interests

[Name of ED/NED / INED]

I and my associates (as defined under the Listing Rules) have discloseable interests in the following

businesses:

Business: (1) Company (2) Partnership (3) Sole Proprietorship (4) Others (Specify)

Description: Changes from Previous Disclosures:

Interest: (1) Director (2) Substantial Shareholder (over 10% vote at general meeting) (3) Partner (4) Sole Proprietor (5) Others (Specify)

The above are the complete information and I undertake to inform the Company of any changes

and additional interests from time to time.

_____________________

[Name]

Date:

Page 34

Appendix E – Questionnaire for Directors’ Interview

Invariably, each company may have matters which it requires to be covered under the questionnaire.

We will only set out some basic questions under the questionnaire:

[NAME OF COMPANY]

Questionnaire

Date: Time: Location: In Attendance: Please review the following questions prior to the interview and bring along all supporting

documents to verify the biography and answers to the following questions. Documents should be

original or properly certified copies:

1. Experience as a director of any listed issuer (1) in Hong Kong, or (2) elsewhere? 2. Date and reason for cessation as director, if applicable?

3. Current committee or sub-committee appointments with the Company (and its Group)?

4. Other roles in any listed issuers or the Company (and its Group)?

5. Other business interests?

6. Knowledge of Listing Rules, including roles and responsibilities and corporate governance?

7. Any censures or disciplines by regulators of disciplinary bodies?

8. Education and professional qualifications?

9. Previous employment and work experience?

10. Other competencies to be director of the Company?

11. Address of Residence?

Page 35

12. Nationality? 13. Who introduced you to the Group? 14. With your other commitments, can you allocate time to serve as director to take an active

interest in the affairs of the Company (and its Group)?

15. How will you manage conflicts of interest with directors and controlling shareholders?

16. How would you act in the interest of the independent shareholders, as a whole?

17. What is good corporate governance and what does it entail?

18. What is your experience in implementing and dealing with corporate governance?

19. Have you ever been bankrupted?

20. Any litigation, regulatory or disciplinary proceedings or actions against you?

21. Any litigation, regulatory or disciplinary proceedings or actions against a company, or entity controlled by you, which you are or were director?

22. Any investigations by any professional bodies or authorities?

23. Are there any disputes with any Company (and its Group)

24. Do you know if the Company (and its Group) has sound internal control system?

25. Do you know if the CFO of the Company (and its Group) has financial knowledge including in the preparation of financial statements?

26. How can you be effective in supervising the performance of the executive and senior management relating to the strategy and policies of the Company (and its Group)?

27. Do you directly or indirectly have competing interests with the Company (and its Group) businesses?

28. Your interest in the Company (and its Group) top clients or supplier?

29. Any relationship with any shareholder or directors of the Company and its Group?

Page 36

30. Any other information you believe to be relevant to your role with the Company (and its Group)?

Please note that in terms of timing, the questions are intended to review background information

and your intentions and should not be limited to current matters. Please feel free to add to the

questions and any issues that you deem appropriate.

Page 37

Appendix F – Confirmation

[NAME OF COMPANY] Confirmation

[The Company]

Dear Sirs,

Re: [Name of Company]

This is to confirm and acknowledge that all applicable requirements and procedures for making and

completing the Declaration and Undertaking, Part 1 of Form B under the Listing Rules and the

possible consequences of a false declaration have been explained to me, [by the solicitors for the

Company/Sponsors] which is understood.

I also acknowledge attending the induction session where relevant extracts of the Listing Rules and

other regulations were provided to me with relevant explanation.

_____________________

[Name]

Date:

Page 38

Appendix G – Confirmation of Independence (INED)

[The Listing Division The Exchange] [The Sponsors] Dear Sirs Re: [The Company] I am proposed independent non-executive director of the Company under the proposed listing application, and permission to deal with the shares of the Company’s on the main Board of The Stock Exchange of Hong Kong Limited (the “Exchange”). Terms and expressions used herein shall have the meaning under the Listing Rules, unless the context requires otherwise. I confirm my independence for the purposes of Rule 3.13 of the Listing Rules: 1. I do not hold more than 1% interest of the total issued share capital of the Company.

2. I have not received any interest in any securities of the Company as gift, or by means of

other financial assistance, from the Company or a connected person thereof. 3. I am not director, partner, principal of a professional adviser which currently, or has within

one year immediately prior to my proposed appointment as independent non-executive director provided services, and I am not employee of such professional adviser who is or has been involved in providing such services during such period to:

(a) the Company, its holding company or any of their respective subsidiaries or

connected persons; or (b) any person who was a controlling shareholder of the Company within one year

immediately prior to the date of my proposed appointment as an independent non-executive director of the Company, or any of their associates.

4. I do not have a material interest in any principal business activity of and am not

involved in any material business dealings with the Company, its holding company or their respective subsidiaries or with any connected persons of the Company.

5. I am not on the Board of Directors of the Company specifically to protect the interests

of an entity whose interests are not the same as those of the shareholders of the Company as a whole.

Page 39

6. I am not and was not connected with a director, the chief executive or a substantial

shareholder of the Company within two years immediately prior to the date of my proposed appointment as an independent non-executive director of the Company.

7. I am not, and have not at any time during the two years immediately prior to the date

of my proposed appointment as an independent non-executive director of the Company been, an executive or director (other than an independent non-executive director) of the Company, of its holding company or any of their respective subsidiaries or of any connected persons of the Company.

8. I am not financially dependent on the Company, its holding company or any of their

respective subsidiaries or connected persons of the Company. 9 I do not have any past or present financial or other interest in the business of the

Company, or any past or present connection with any connected person of the Company, that, in either case, might affect my exercise of independent judgment.

10 I have no management function in the Company and its subsidiaries. 11 I am not aware of any factor which may affect my independence from the Company, its

holding company or any of the respective subsidiaries or connected persons of the Company.

Furthermore, I understand that as part of the application documents to be submitted to the Stock Exchange for the Proposed Application, a written confirmation must be provided by each of the independent non-executive directors or proposed independent non-executive directors of the Company on the understanding of the obligations and duties of an independent non-executive director. I confirm that I understand the obligations, duties and responsibilities of an independent non-executive director of a company listed on the Stock Exchange and I undertake to comply with such obligations, duties and responsibilities under the Listing Rules, and other applicable laws and provisions as an independent non-executive director of the Company. I believe that I have a standard of competence and commercial or professional experience to ensure that the interests of the general body of shareholders (present and future) of the Company will be represented.

Page 40

I understand that you may rely on the confirmations and undertakings provided in the confirmation letter in connection with the proposed listing application. I undertake that if there is any subsequent change of circumstances which may affect my independence, I shall inform you in writing as soon as practicable. Confirmed by: _____________________ [Name] Date:

Page 41

Appendix H – Publicity Guidelines

Invariably, for an IPO, there will be counsels for the sponsors and the company and they will come up

with the publicity guidelines. We will only set out some basic elements of the guidelines:

1. It applies to all parties involved in the IPO, the company, sponsors, others and their staff.

2. Publicity includes electronic communications, websites and public or press enquiries.

3. The IPO should be kept confidential prior to its announcement.

4. Sponsors and legal advisers should be consulted prior to release of publicity information.

5. All publicity must be true, accurate and consistent with, and must not be misleading or

contradict the prospectus.

6. All publicity materials must be legended “Application has been or will be made to The Stock

Exchange of Hong Kong Limited for listing of and permission to deal in the securities of the

company”.

7. Any release of publicity before the Listing Committee hearing could lead to delay or the

application not being considered.

8. Other promotional activities could also lead to issues and there is need to consult sponsors

on the promotional activities and potential impact.

9. The prospectus must contain verifiable information for investors to make an informed

investment decision. Otherwise, the Company and directors could become liable.

10. Under the SFO, any fraudulent or reckless misrepresentation to induce another to subscribe

for securities is an offence.

11. There should be a working group, with experience to deal with publicity, to pre-clear all

publicity information.

12. There should be no discussions of historical or projected results with brokers, banks or

analysts other than members of the sponsors.

13. The company may pre-clear factual business information and developments to customers

for business purposes.

14. The company may require the entry of non-disclosure agreement with various parties.

15. The procedures should remain in place until such time determined by the company after the

IPO share distribution

Page 42

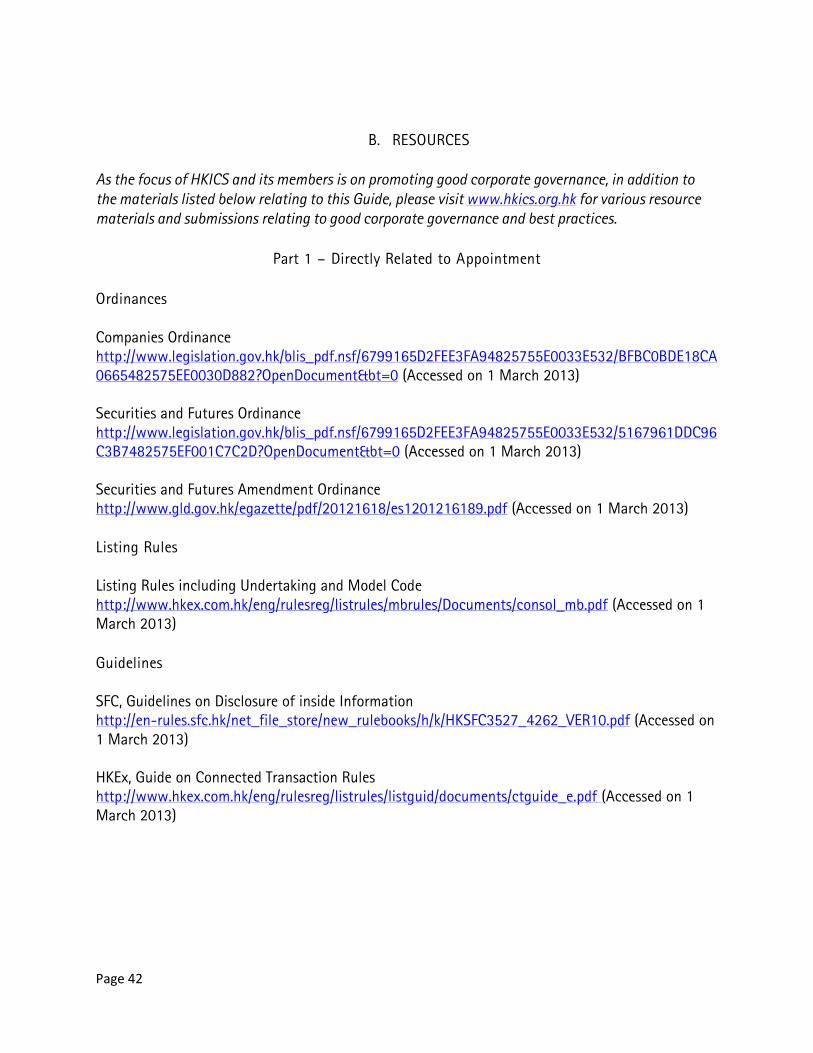

B. RESOURCES

As the focus of HKICS and its members is on promoting good corporate governance, in addition to