The Growth Imperative. I wanna be a billionaire… I wanna be on the cover of Forbes magazine…

55

The Growth Imperative

-

Upload

kierra-newlon -

Category

Documents

-

view

223 -

download

4

Transcript of The Growth Imperative. I wanna be a billionaire… I wanna be on the cover of Forbes magazine…

The Growth Imperative

I wanna be a billionaire…I wanna be on the

cover of Forbes magazine…

What we will discuss

• Shift happens/change occurs

• How might it impact us?

• What can we do about it?– Three strategies to “future-proof” you business

The growth imperative

Shift happens

• clients are demanding more value from you

• new regulations are making the industry more transparent

• rising number of do-it-yourselfers

• other advisors are improving their game

The growth imperative

Shift happens

The growth imperative

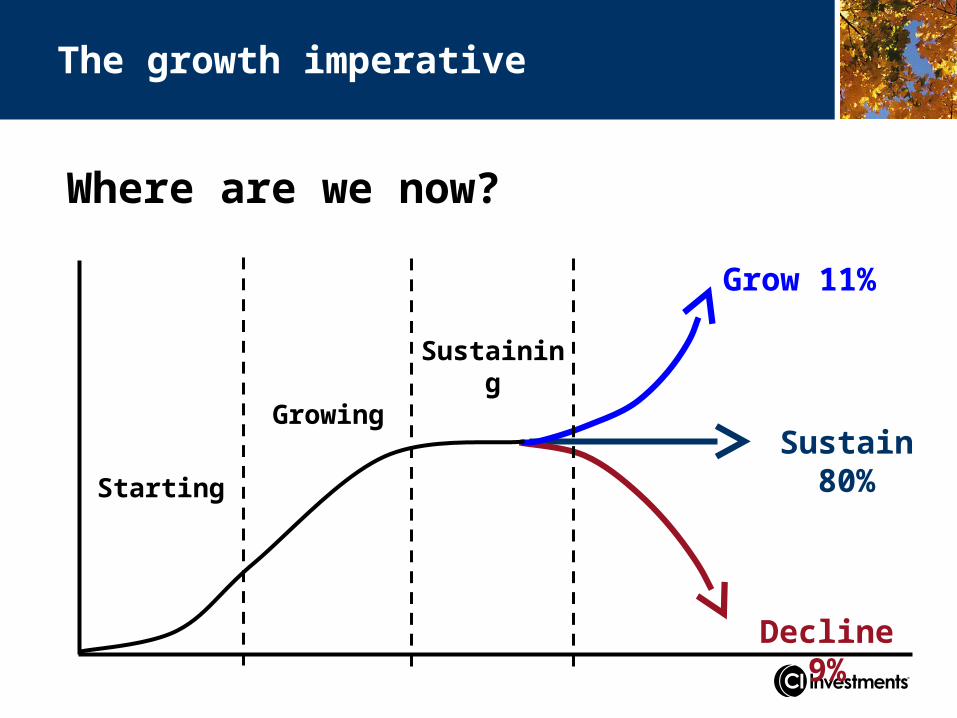

Where are we now?

Grow 11%

Decline 9%

Sustain 80%Starting

Growing

Sustaining

The growth imperative

Maybe I just don’t “wanna” build a really huge business.

Is there something wrong with that?

The growth imperative

GREATNESS doesn’t depend on

SIZE

The growth imperative

CAPABILITY

The growth imperative

What your business

does now could doPROCESSES CAPABILITY

The growth imperative

you use a recipe

you follow a blueprint

The growth imperative

To build a business:

• clearly define what you are trying to accomplish

• carefully think through the unique service you are going to provide to your chosen target market

• organize all the elements you need to meet that objective

• continually improve your offering

• stay ahead of competitive threats and meet evolving customer needs

The growth imperative

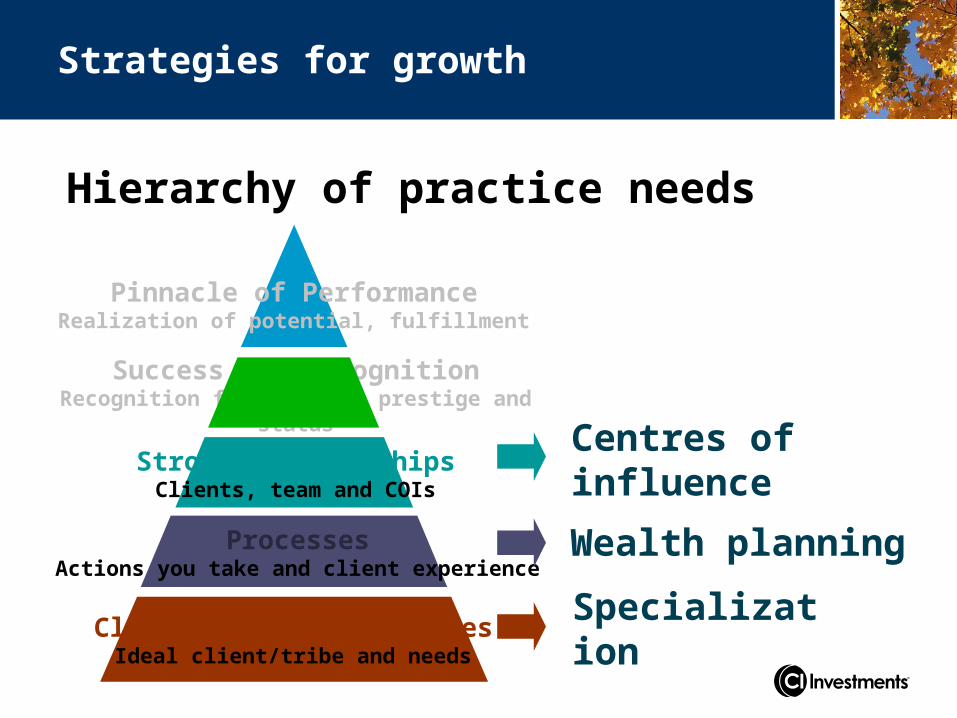

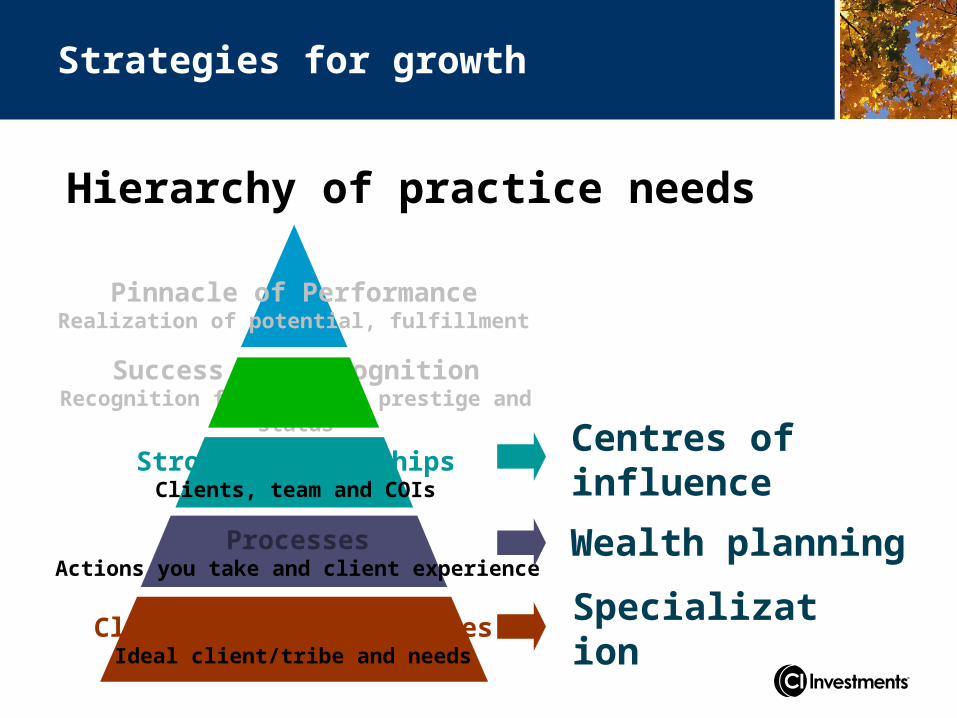

Hierarchy of practice needs

Success and RecognitionRecognition from others, prestige and status

Strong RelationshipsClients, team and COIs

ProcessesActions you take and client experience

Client Base and ResourcesIdeal client/tribe and needs

Pinnacle of PerformanceRealization of potential, fulfillment

Centres of influence

Wealth planning

Specialization

Strategies for growth

Hierarchy of practice needs

Success and RecognitionRecognition from others, prestige and status

Strong RelationshipsClients, team and COIs

ProcessesActions you take and client experience

Client Base and ResourcesIdeal client/tribe and needs

Pinnacle of PerformanceRealization of potential, fulfillment

Centres of influence

Wealth planning

Specialization

Strategies for growth

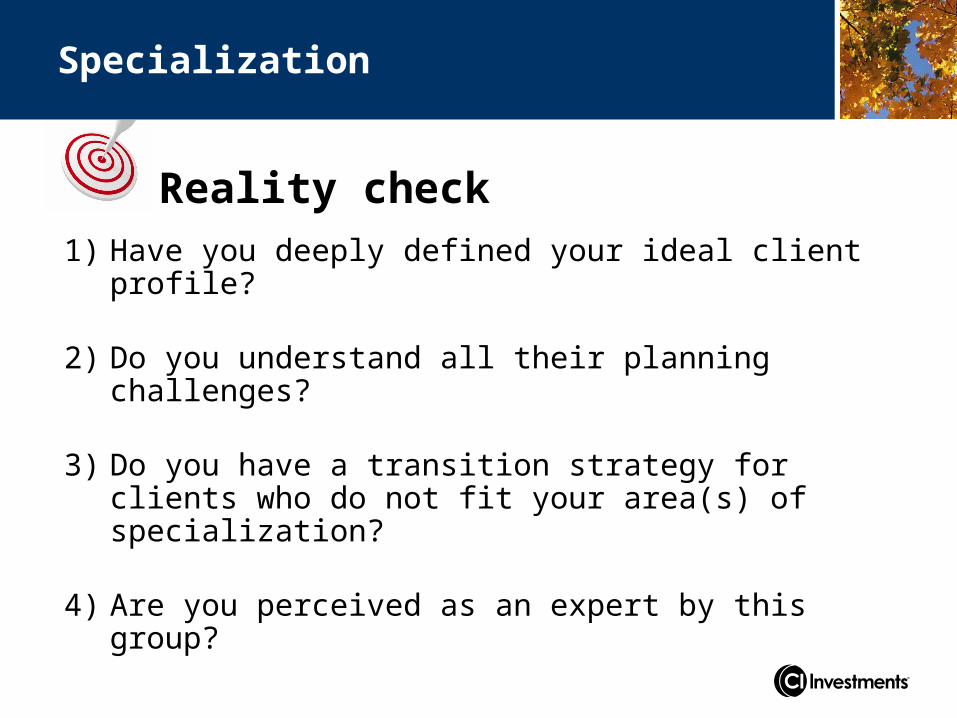

Specialization

Reality check

Specialization

1) Have you deeply defined your ideal client profile?

2) Do you understand all their planning challenges?

3) Do you have a transition strategy for clients who do not fit your area(s) of specialization?

4) Are you perceived as an expert by this group?

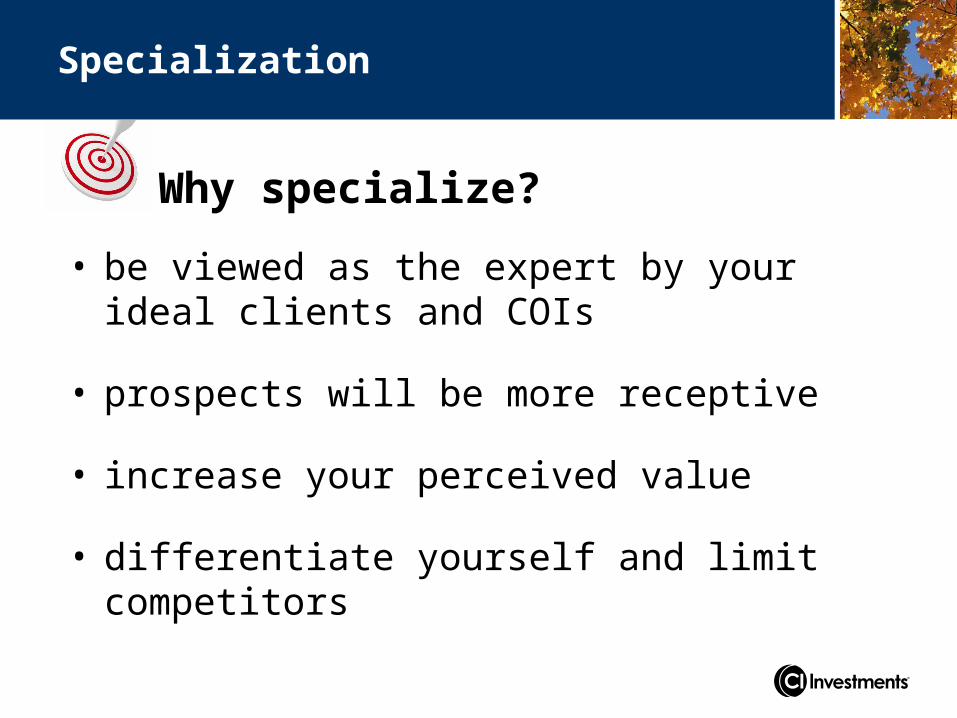

Why specialize?

Specialization

• be viewed as the expert by your ideal clients and COIs

• prospects will be more receptive

• increase your perceived value

• differentiate yourself and limit competitors

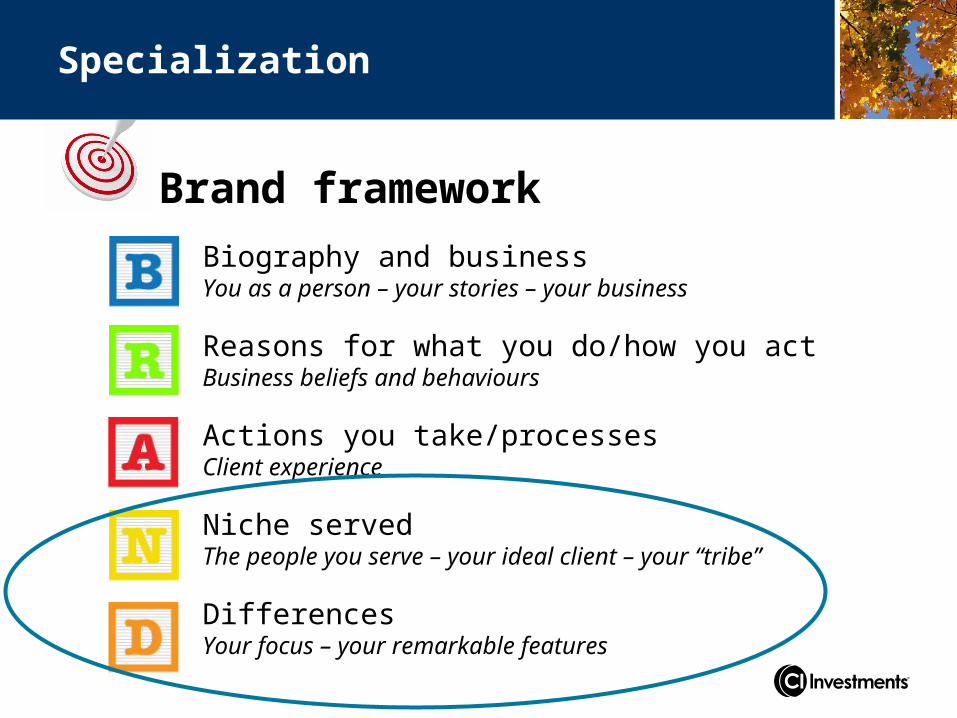

Brand framework

Specialization

Biography and businessYou as a person – your stories – your business

Reasons for what you do/how you actBusiness beliefs and behaviours

Actions you take/processesClient experience

Niche servedThe people you serve – your ideal client – your “tribe”

DifferencesYour focus – your remarkable features

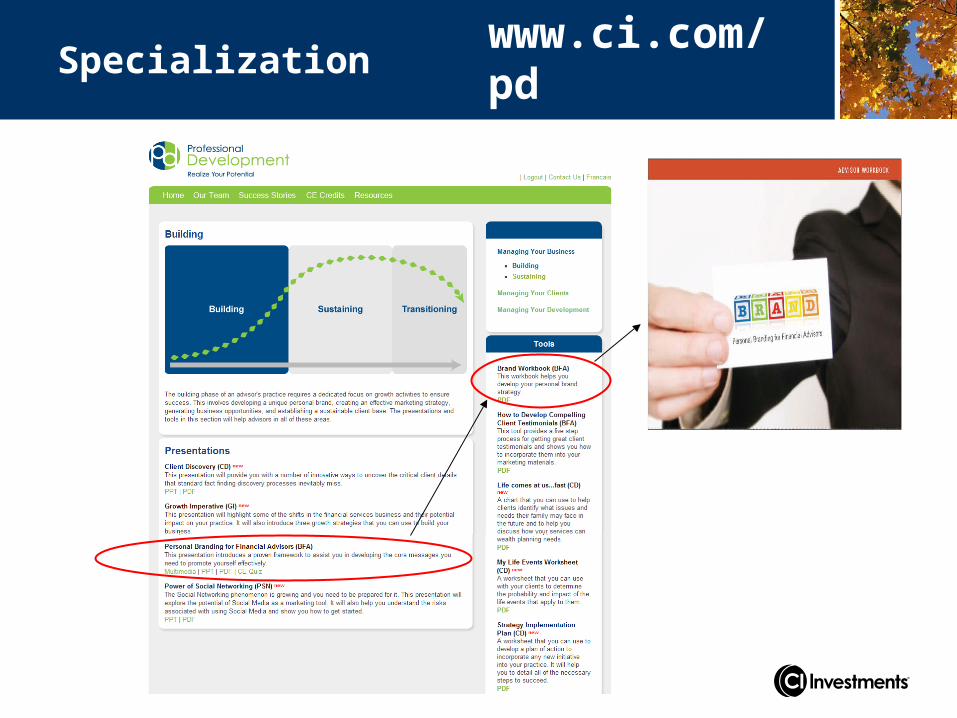

www.ci.com/pdSpecialization

Not your niche…

Specialization

their “tribe”

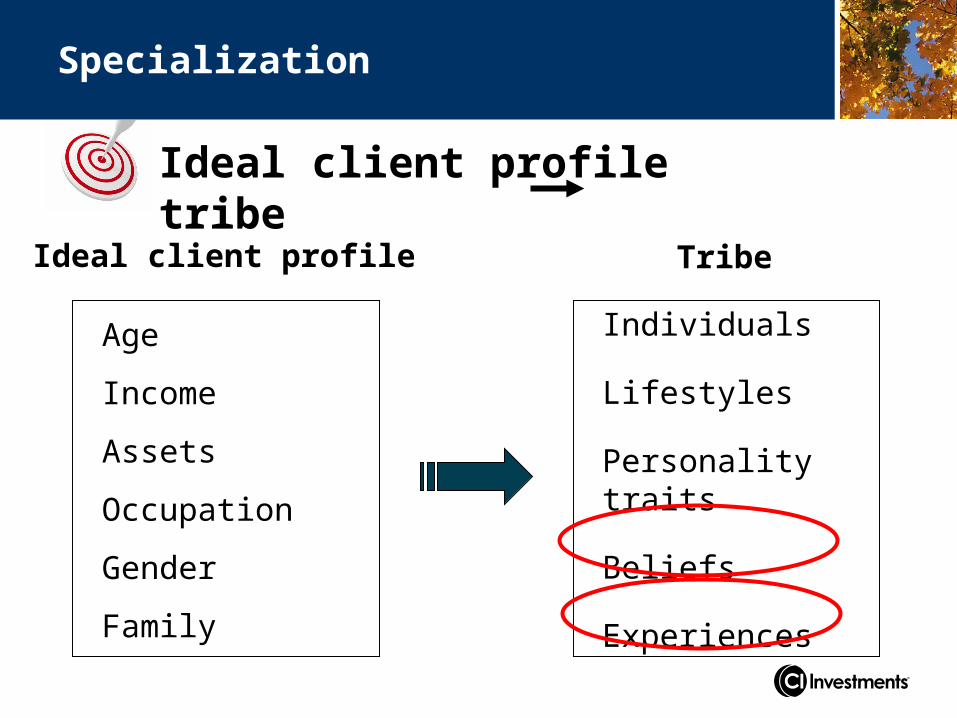

Ideal client profile tribe

Specialization

Ideal client profile

Age

Income

Assets

Occupation

Gender

Family

Individuals

Lifestyles

Personality traits

Beliefs

Experiences

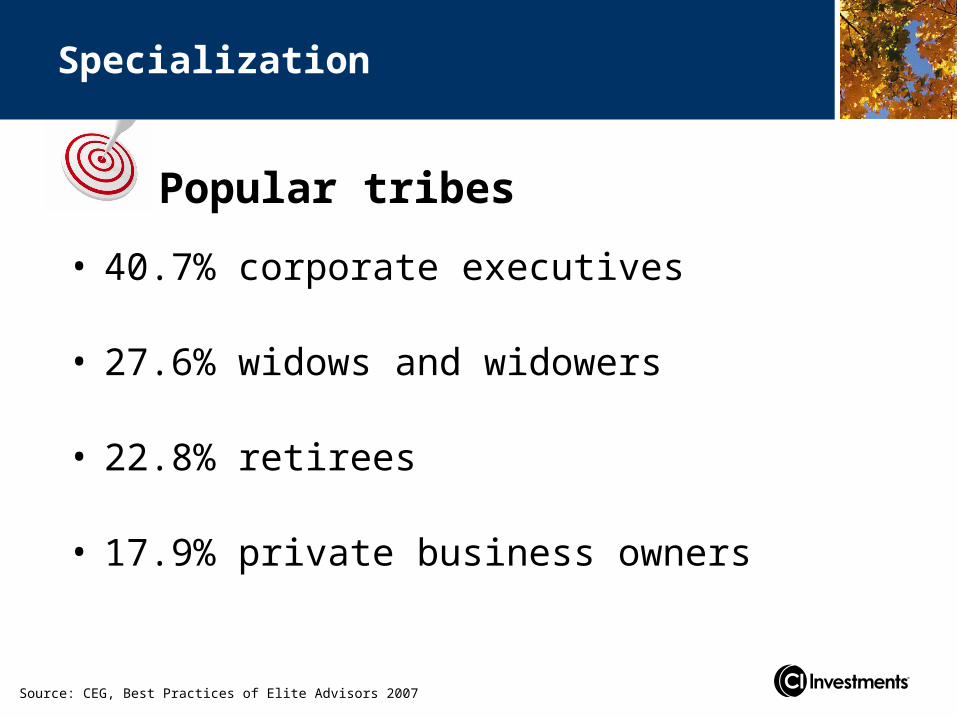

Tribe

• 40.7% corporate executives

• 27.6% widows and widowers

• 22.8% retirees

• 17.9% private business owners

Popular tribes

Specialization

Source: CEG, Best Practices of Elite Advisors 2007

Travel and leisure

Health and recreation

Specialization

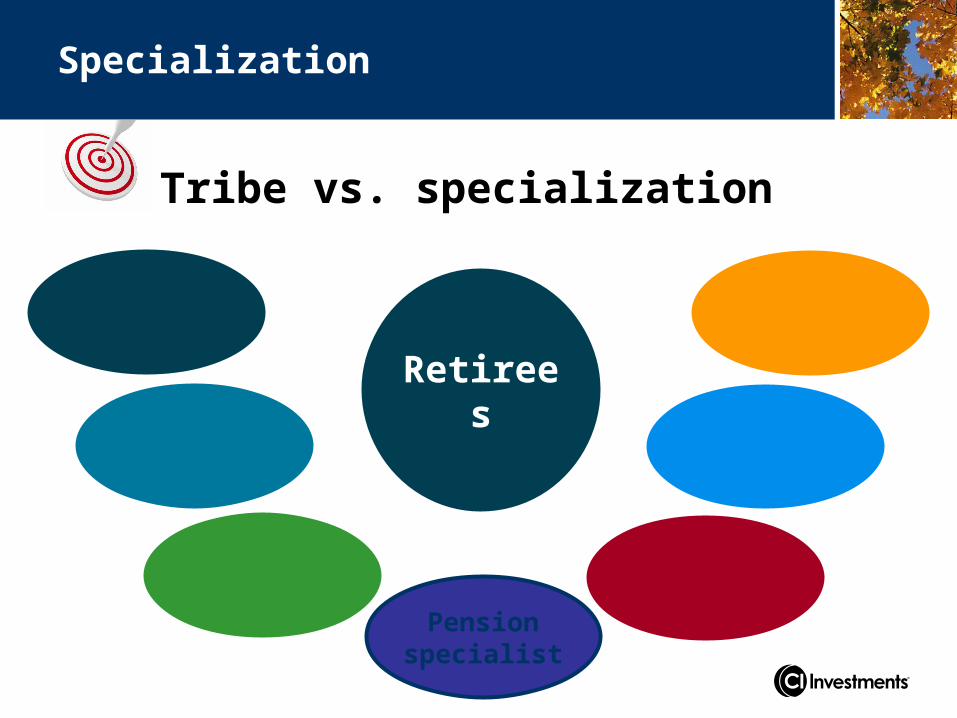

Retirees

Long-term care

Establishing trusts

Real estate downsizing

Charitable donations

Tribe vs. specialization

Pension specialist

Specialization

Long-term care

How to specialize

Nursing home

At home care

Insurance

Becoming part of a tribe

Specialization

• has a tribe already selected you?

• locate their “watering holes”

– regular meetings

– common periodicals/publication

– COI’s

– websites

• package your entire offering to be uniquely attractive to this group

Hierarchy of practice needs

Success and RecognitionRecognition from others, prestige and status

Strong RelationshipsClients, team and COIs

ProcessesActions you take and client experience

Client Base and ResourcesIdeal client/tribe and needs

Pinnacle of PerformanceRealization of potential, fulfillment

Centres of influence

Wealth planning

Specialization

Strategies for growth

Wealth planning

Reality check

Wealth planning

1) Are you going beyond investments?

2) Do you know what both spouses/family are concerned about?

3) Do you know what assets your clients may hold elsewhere?

4) Do you know if your clients have proper insurance in place?

5) Do you know when your clients last reviewed their wills?

Why provide true planning?

Wealth planning

• if you don’t, someone else will!

• a deeper relationship with your clients and their families will:– protect you and your practice

– help you help them

• become your clients’ single and most-valued resource for all their financial advice

• higher income as a wealth manager

• increase referrals from client and COIs

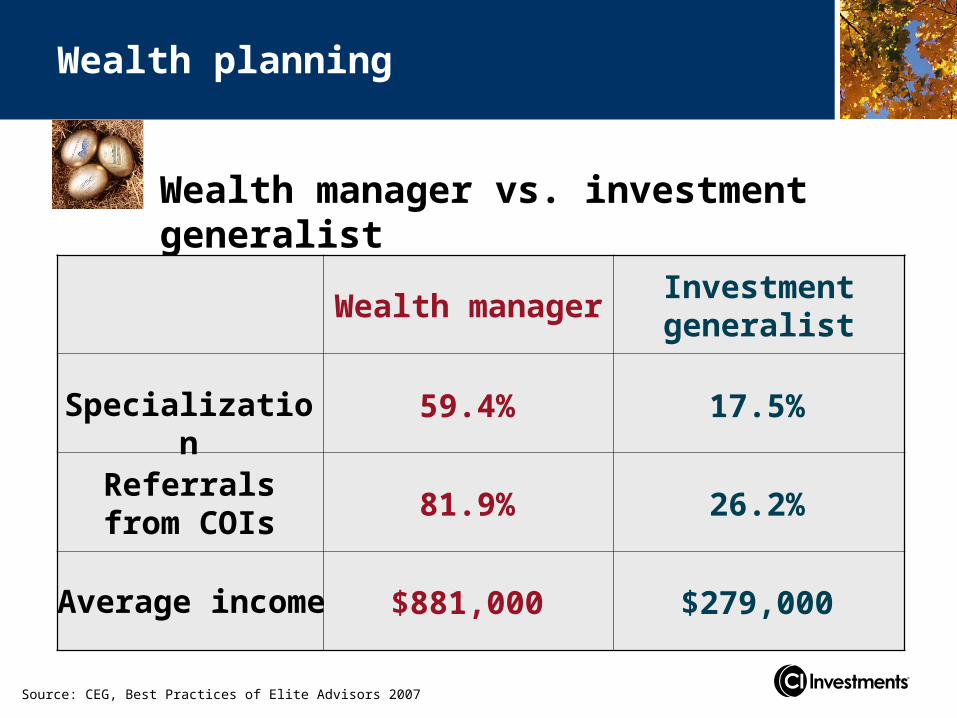

Wealth planning

Wealth manager vs. investment generalist

Source: CEG, Best Practices of Elite Advisors 2007

Wealth managerInvestment generalist

Specialization

Referrals from COIs

Average income

59.4% 17.5%

81.9% 26.2%

$881,000 $279,000

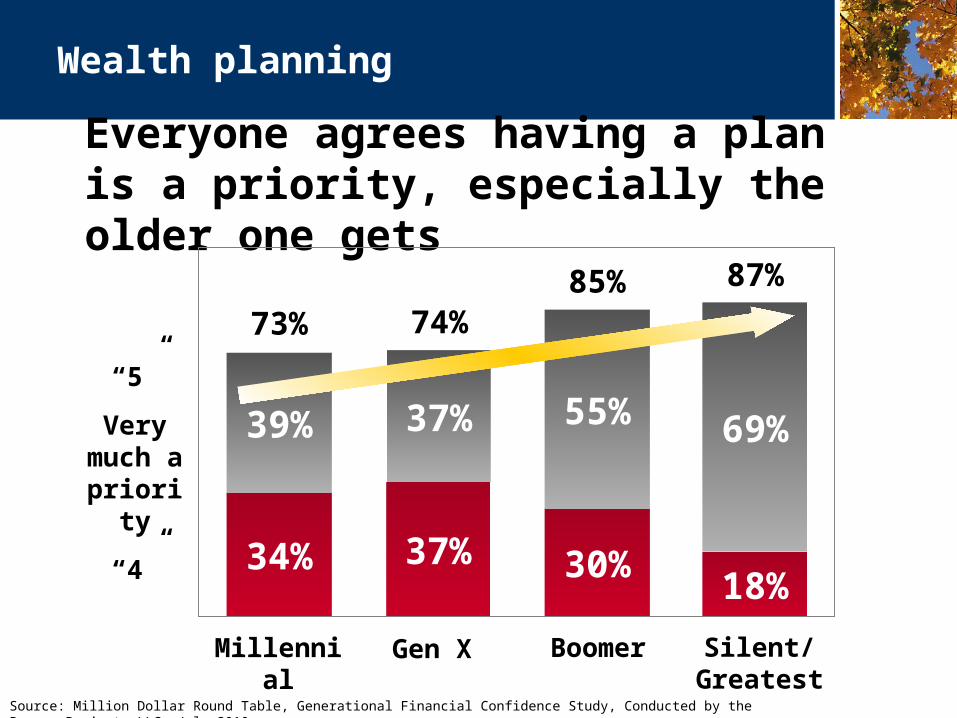

Everyone agrees having a plan is a priority, especially the older one gets

Source: Million Dollar Round Table, Generational Financial Confidence Study, Conducted by the Boomer Project, LLC, July 2010.

73% 74%85% 87%

34% 37% 30%18%

39% 37% 55% 69%

“5”

Very much a priority

“4”

Millennial Gen X Boomer Silent/Greatest

Wealth planning

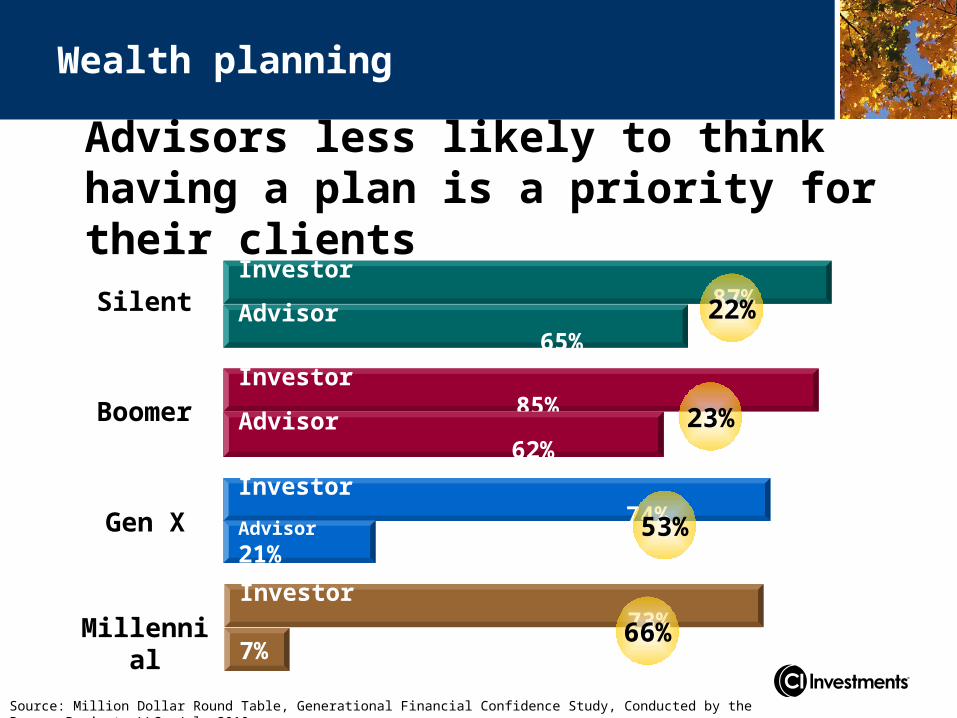

Advisors less likely to think having a plan is a priority for their clients

Source: Million Dollar Round Table, Generational Financial Confidence Study, Conducted by the Boomer Project, LLC, July 2010.

Millennial

Gen X

Silent

Boomer

Investor 87%

Investor 85%

Investor 74%

Investor 73%

Advisor 65%

Advisor 62%

Advisor 21%

7%

23%

53%

66%

22%

Wealth planning

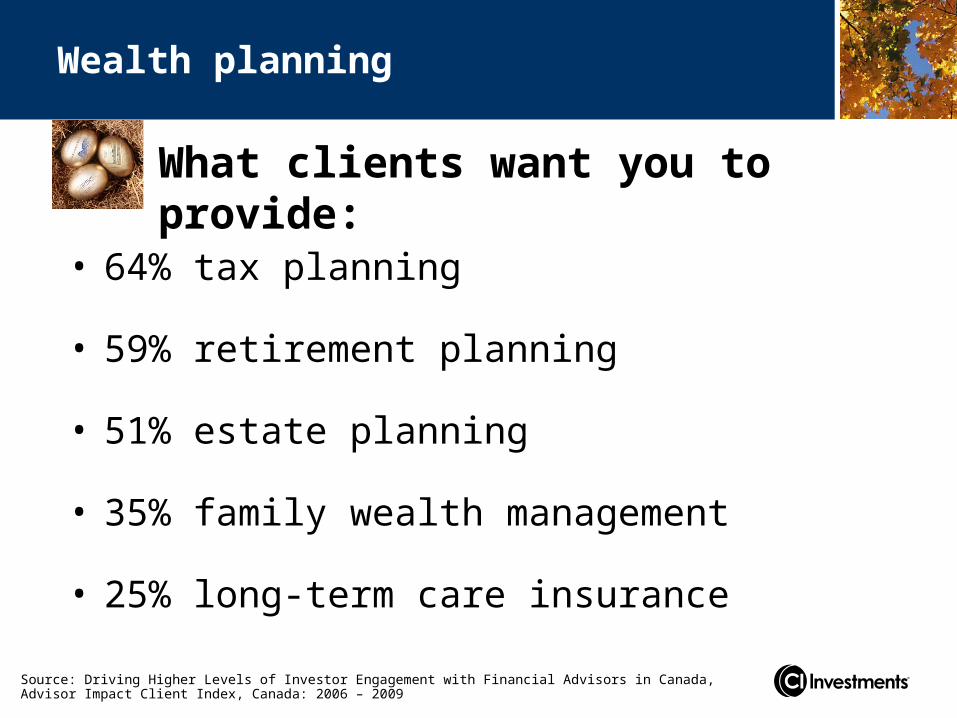

What clients want you to provide:

Wealth planning

• 64% tax planning

• 59% retirement planning

• 51% estate planning

• 35% family wealth management

• 25% long-term care insurance

Source: Driving Higher Levels of Investor Engagement with Financial Advisors in Canada, Advisor Impact Client Index, Canada: 2006 – 2009

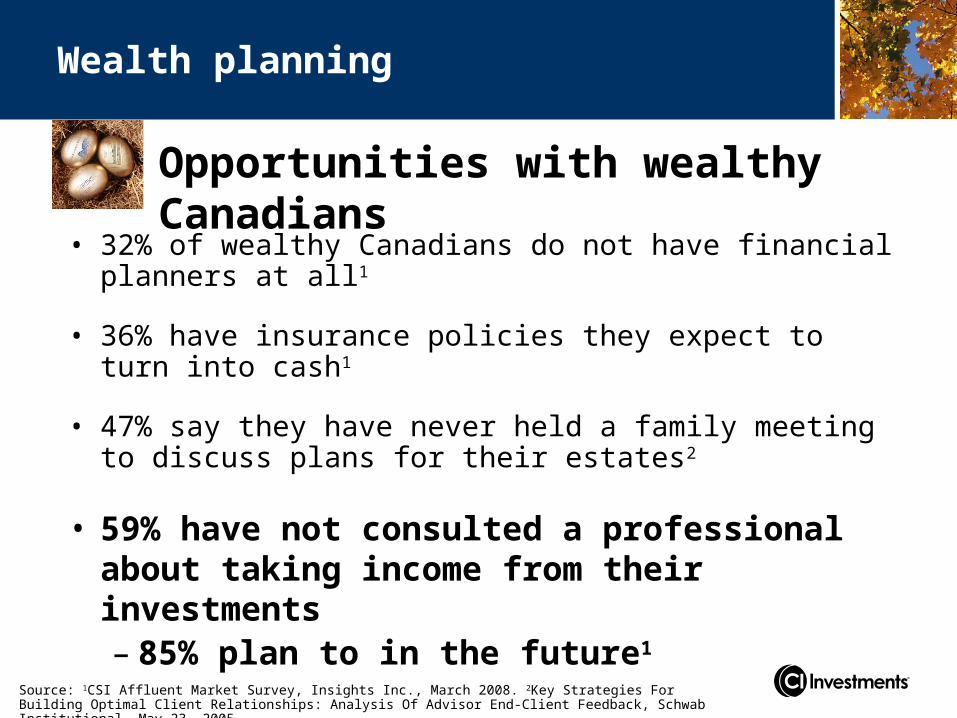

Opportunities with wealthy Canadians

Wealth planning

• 32% of wealthy Canadians do not have financial planners at all1

• 36% have insurance policies they expect to turn into cash1

• 47% say they have never held a family meeting to discuss plans for their estates2

• 59% have not consulted a professional about taking income from their investments– 85% plan to in the future1

Source: 1CSI Affluent Market Survey, Insights Inc., March 2008. 2Key Strategies For Building Optimal Client Relationships: Analysis Of Advisor End-Client Feedback, Schwab Institutional, May 23, 2005.

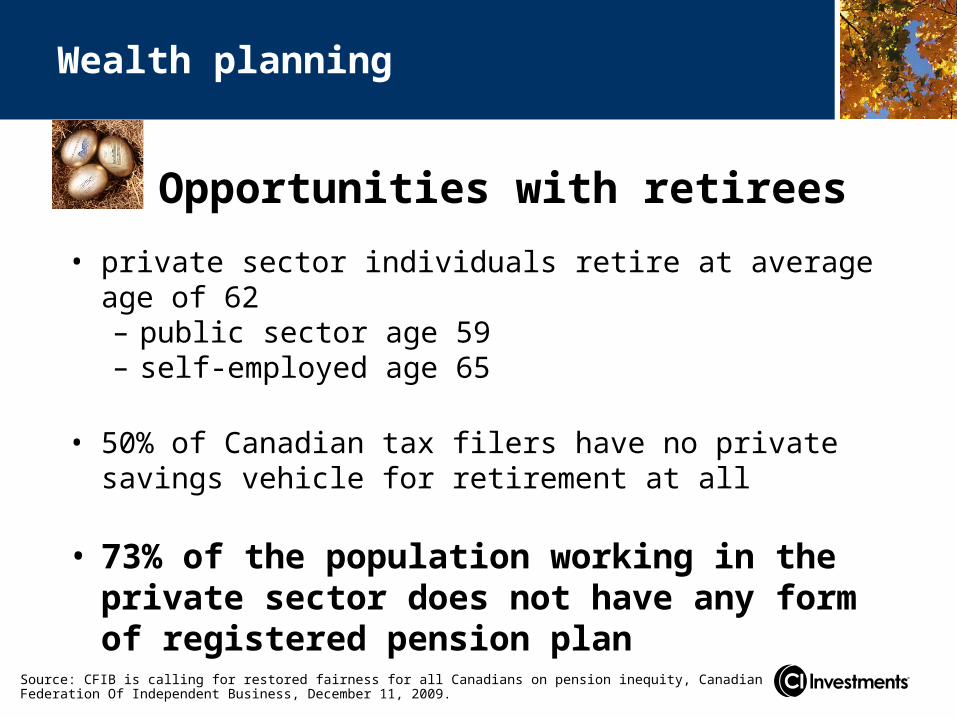

Opportunities with retirees

Wealth planning

• private sector individuals retire at average age of 62– public sector age 59– self-employed age 65

• 50% of Canadian tax filers have no private savings vehicle for retirement at all

• 73% of the population working in the private sector does not have any form of registered pension plan

Source: CFIB is calling for restored fairness for all Canadians on pension inequity, Canadian Federation Of Independent Business, December 11, 2009.

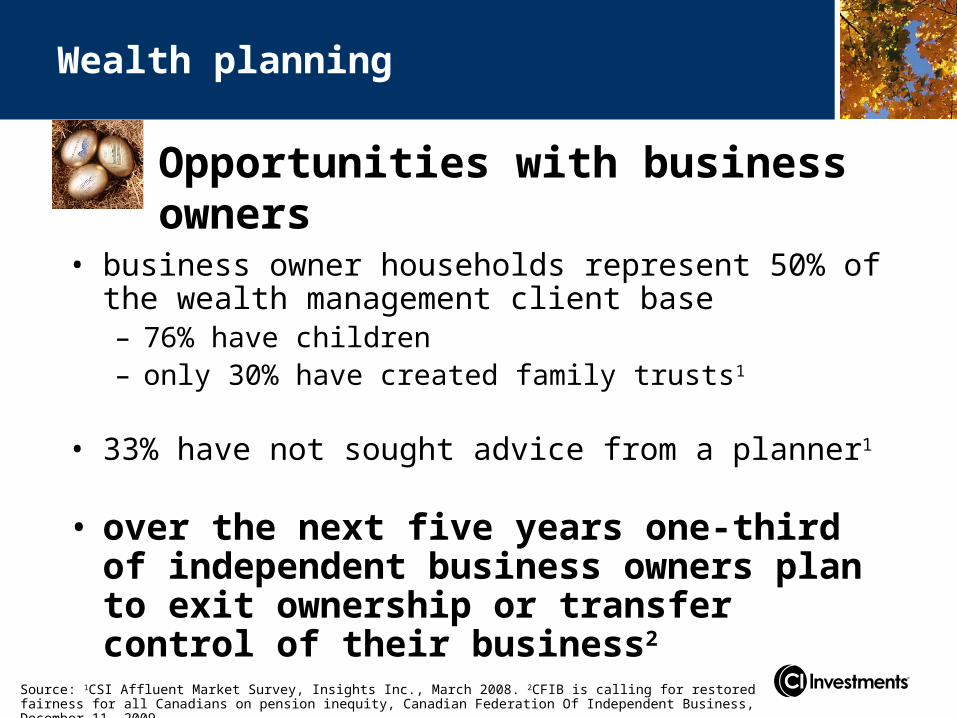

Opportunities with business owners

Wealth planning

• business owner households represent 50% of the wealth management client base– 76% have children– only 30% have created family trusts1

• 33% have not sought advice from a planner1

• over the next five years one-third of independent business owners plan to exit ownership or transfer control of their business2

Source: 1CSI Affluent Market Survey, Insights Inc., March 2008. 2CFIB is calling for restored fairness for all Canadians on pension inequity, Canadian Federation Of Independent Business, December 11, 2009.

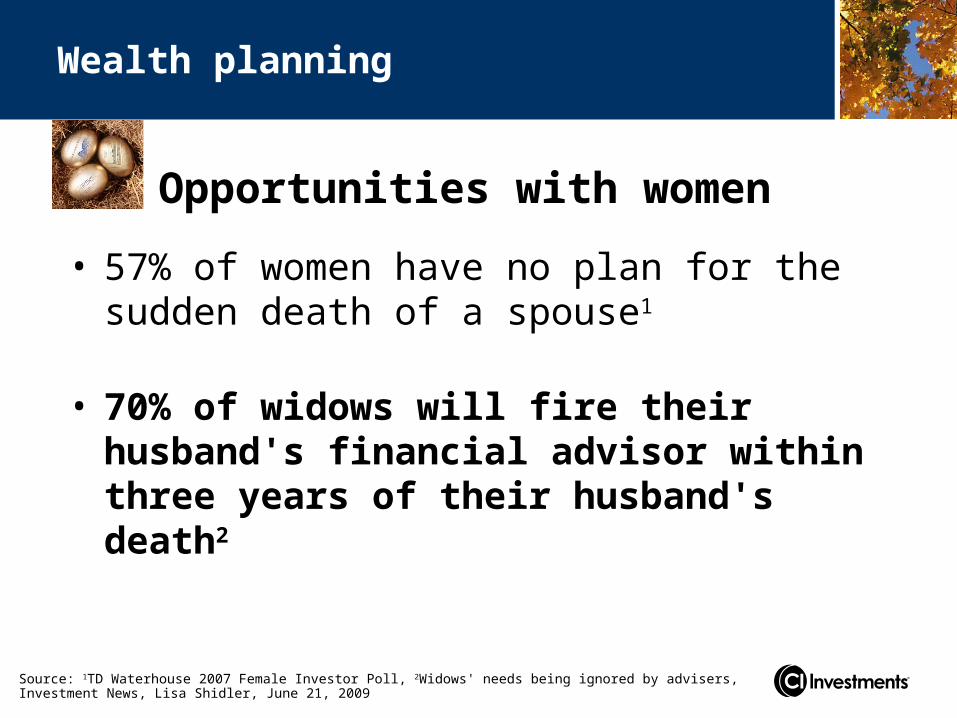

Opportunities with women

Wealth planning

• 57% of women have no plan for the sudden death of a spouse1

• 70% of widows will fire their husband's financial advisor within three years of their husband's death2

Source: 1TD Waterhouse 2007 Female Investor Poll, 2Widows' needs being ignored by advisers, Investment News, Lisa Shidler, June 21, 2009

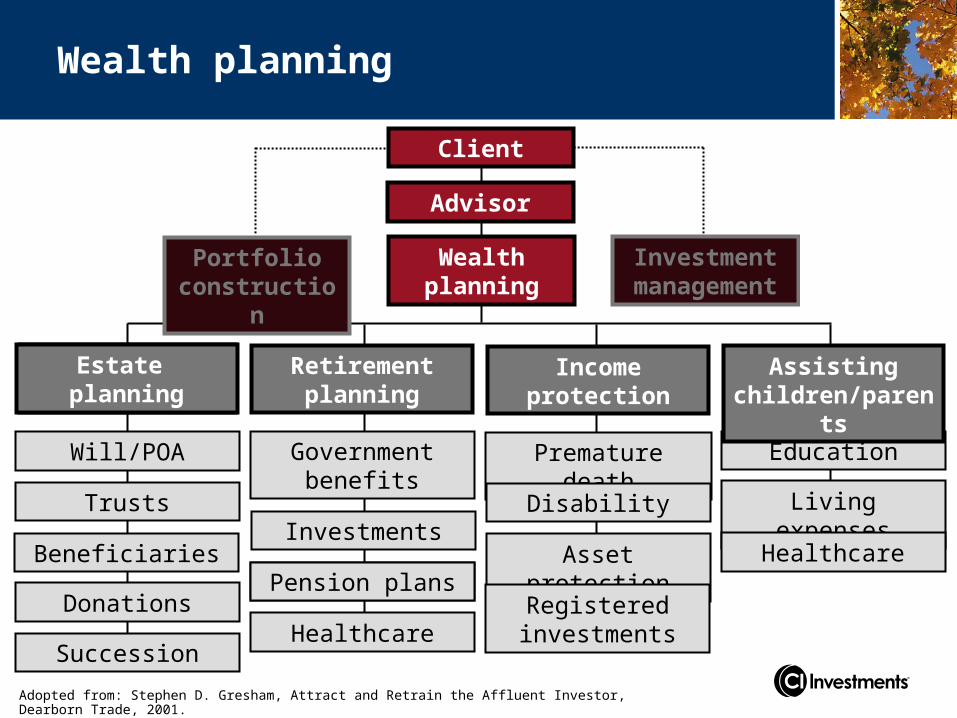

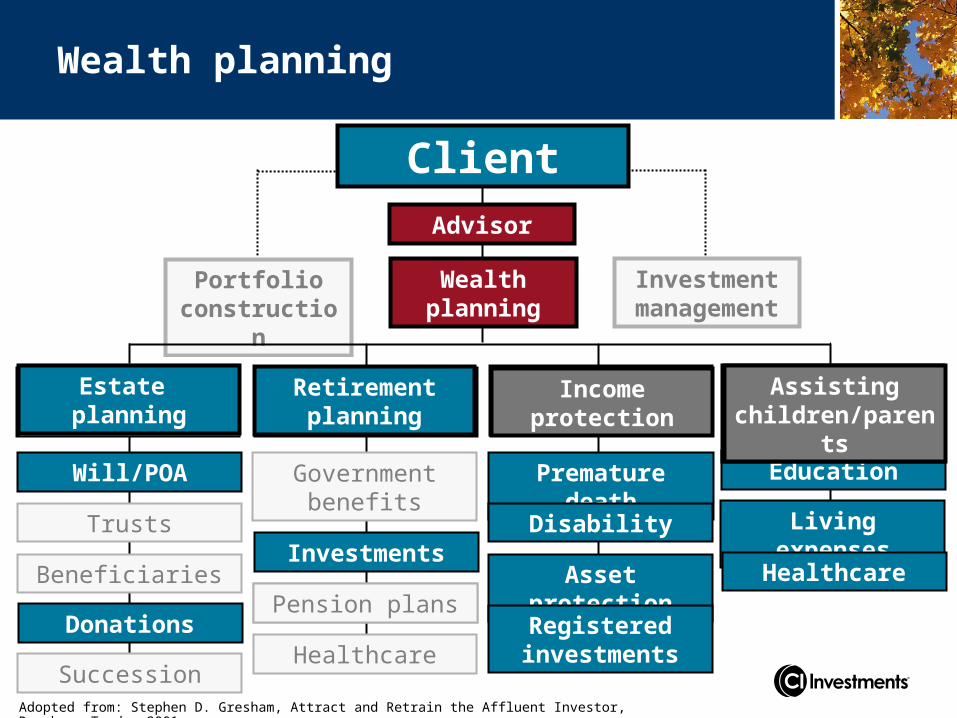

Wealth planning

Adopted from: Stephen D. Gresham, Attract and Retrain the Affluent Investor, Dearborn Trade, 2001.

Client

Portfolio construction

Wealth planning

Investment management

Estate planning

Will/POA

Trusts

Beneficiaries

Donations

Government benefits

Investments

Pension plans

Healthcare

Premature death

Disability

Asset protection

Registered investments

Education

Living expenses

Healthcare

Retirement planning

Income protection

Estate planning

Assisting children/parents

Pension plans

Advisor

Succession

Education

Living expenses

Healthcare

Assisting children/parents

Premature death

Disability

Asset protection

Registered investments

Income protection

Wealth planning

Adopted from: Stephen D. Gresham, Attract and Retrain the Affluent Investor, Dearborn Trade, 2001.

Advisor

Client

Portfolio construction

Wealth planning

Investment management

Retirement planning

Income protection

Estate planning

Assisting children/parents

Government benefits

Investments

Pension plans

Healthcare

Pension plans

Retirement planning

Will/POA

Trusts

Beneficiaries

Donations

Succession

Estate planningEstate planning

How to become a wealth manager

Wealth planning

• build the support team – identify other professionals you want to work with based on specific needs of target clients you want to address

• control the process – you are at the centre of the relationships to facilitate the process

• make the move – be patient, the full transition can take up to 18 months

Source: Become the center of your boomer client's wealth management team 2007

Hierarchy of practice needs

Success and RecognitionRecognition from others, prestige and status

Strong RelationshipsClients, team and COIs

ProcessesActions you take and client experience

Client Base and ResourcesIdeal client/tribe and needs

Pinnacle of PerformanceRealization of potential, fulfillment

Centres of influence

Wealth planning

Specialization

Strategies for growth

Centres of influence

Reality check

Centres of influence

1) Has your COI referred a prospect to you within the last year?– Have you?

2) Did that prospect fit your ideal client profile?– Did the prospect fit theirs?

3) Can your COI articulate what you do and how you are different?– Can you articulate what they do and how they are

different?

Why work with COIs?

Centres of influence

• best way to increase high-quality referrals

• bring their expertise to your existing clients and prospects

• foster communication with your clients’ outside advisors and ensure strategies are aligned

Broken trust

Source: TrustedAdvisor Associates 2008

Centres of influence

INMATE# 61727054

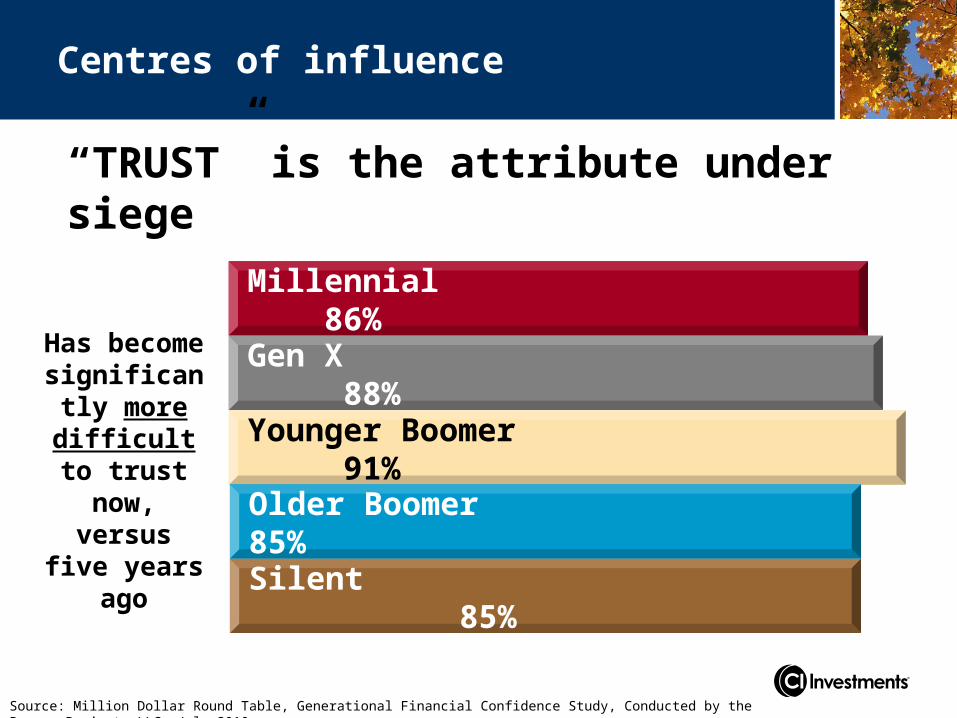

“TRUST” is the attribute under siege

Source: Million Dollar Round Table, Generational Financial Confidence Study, Conducted by the Boomer Project, LLC, July 2010.

Has become significantly

more difficult to trust now, versus five years ago

Millennial 86%

Gen X 88%

Younger Boomer 91%

Older Boomer 85%Silent 85%

Centres of influence

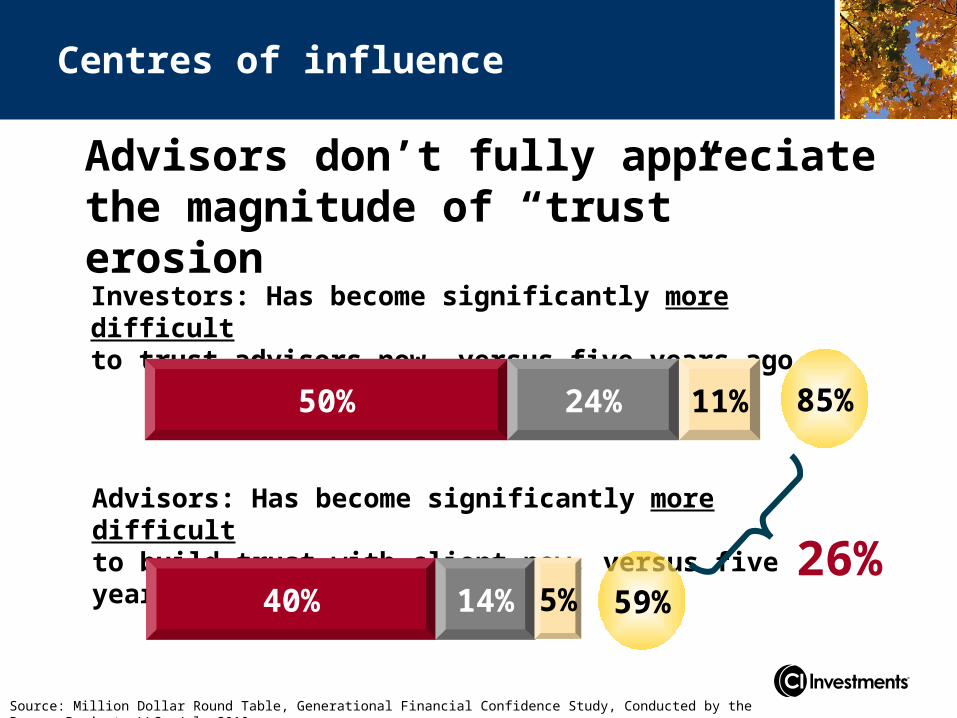

Advisors don’t fully appreciate the magnitude of “trust” erosion

Source: Million Dollar Round Table, Generational Financial Confidence Study, Conducted by the Boomer Project, LLC, July 2010.

Investors: Has become significantly more difficult to trust advisors now, versus five years ago

Advisors: Has become significantly more difficult to build trust with client now, versus five years ago

50%

40%

24%

14%

11%

5%

85%

59%26%

Centres of influence

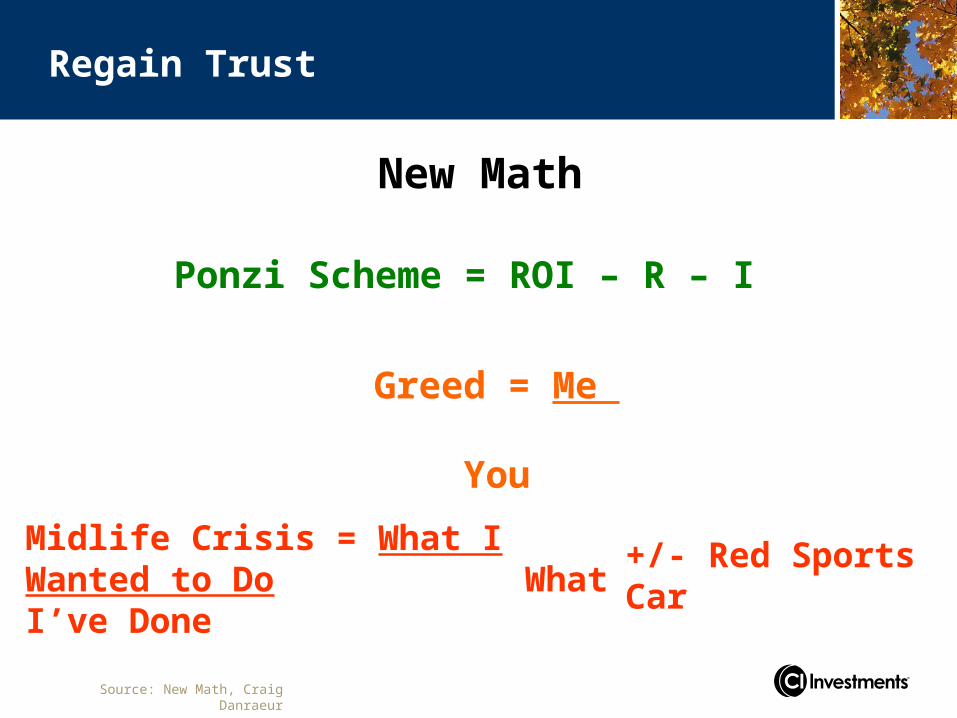

Greed = Me You

Ponzi Scheme = ROI – R – IPonzi Scheme = ROI – R – I

Greed = Me You

Source: New Math, Craig Danraeur

+/- Red Sports Car

New Math

Midlife Crisis = What I Wanted to Do What I’ve Done

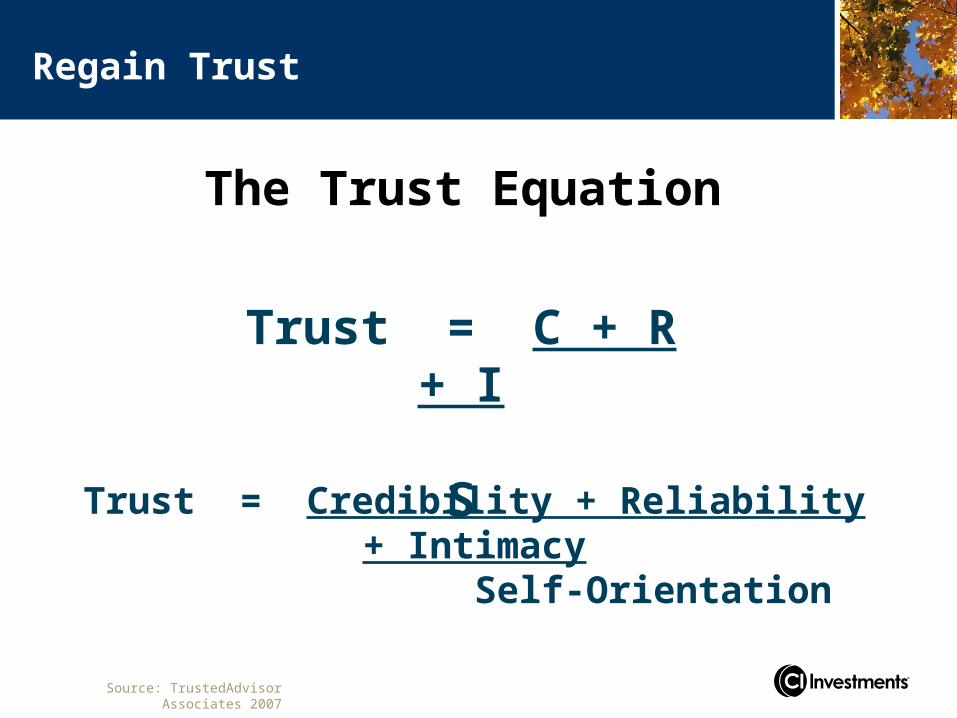

Regain Trust

The Trust Equation

Trust = C + R + I S

Trust = Credibility + Reliability + Intimacy Self-Orientation

Source: TrustedAdvisor Associates 2007

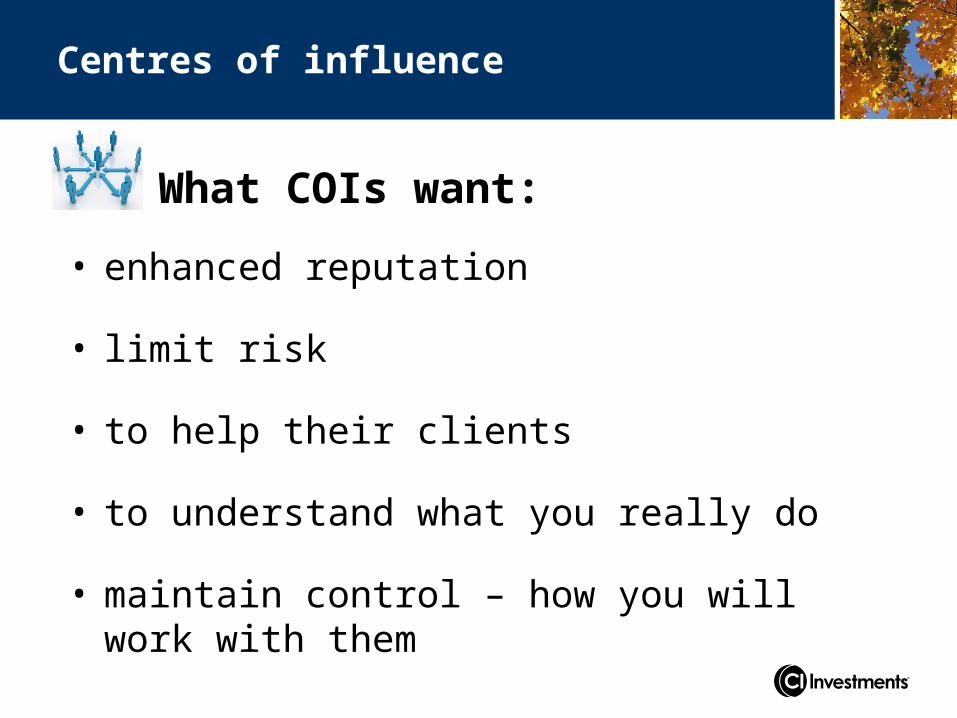

Regain Trust

What COIs want:

Centres of influence

• enhanced reputation

• limit risk

• to help their clients

• to understand what you really do

• maintain control – how you will work with them

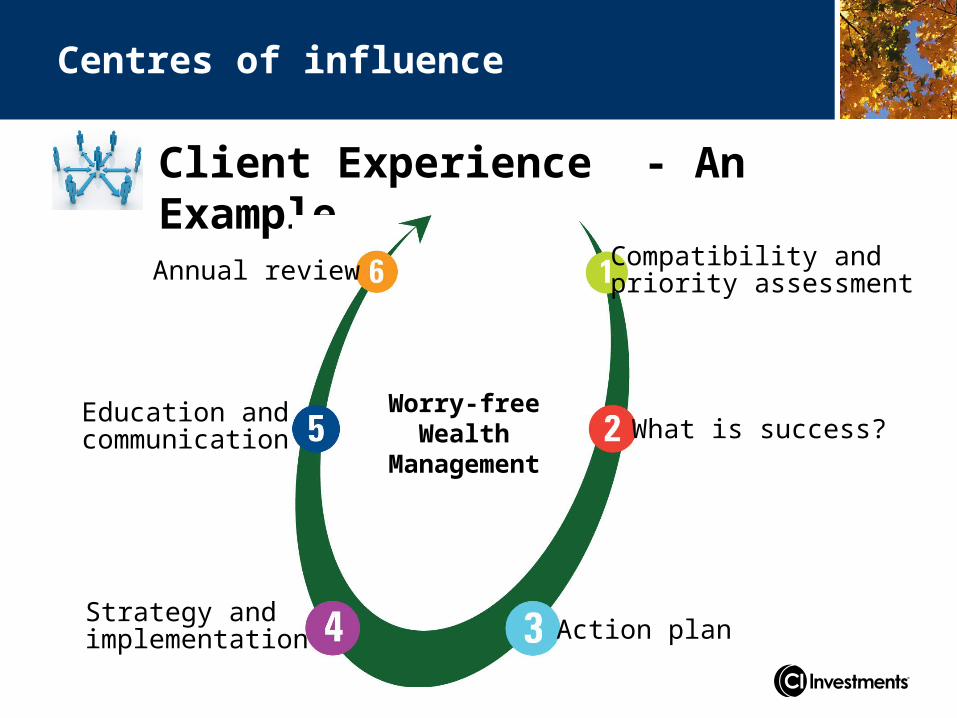

Client Experience - An Example

Annual review

Education andcommunication

Action planStrategy andimplementation

What is success?

Compatibility andpriority assessment

Worry-free Wealth

Management

Centres of influence

How to work with COIs

Centres of influence

• qualify them up front – discovery meetings

• help them with their business challenges

• recognize it will take time to develop the relationship

• differentiate yourself from other advisors

Hierarchy of practice needs

Success and RecognitionRecognition from others, prestige and status

Strong RelationshipsClients, team and COIs

ProcessesActions you take and client experience

Client Base and ResourcesIdeal client/tribe and needs

Pinnacle of PerformanceRealization of potential, fulfillment

Centres of influence

Wealth planning

Specialization

Strategies for growth

Thank you

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. ®CI Investments the CI Investments design, Harbour Advisors, Harbour Funds, Signature and Signature Global Advisors are registered trademarks of CI Investments Inc.

www.ci.com/pd