the Grocer - Global 50

2

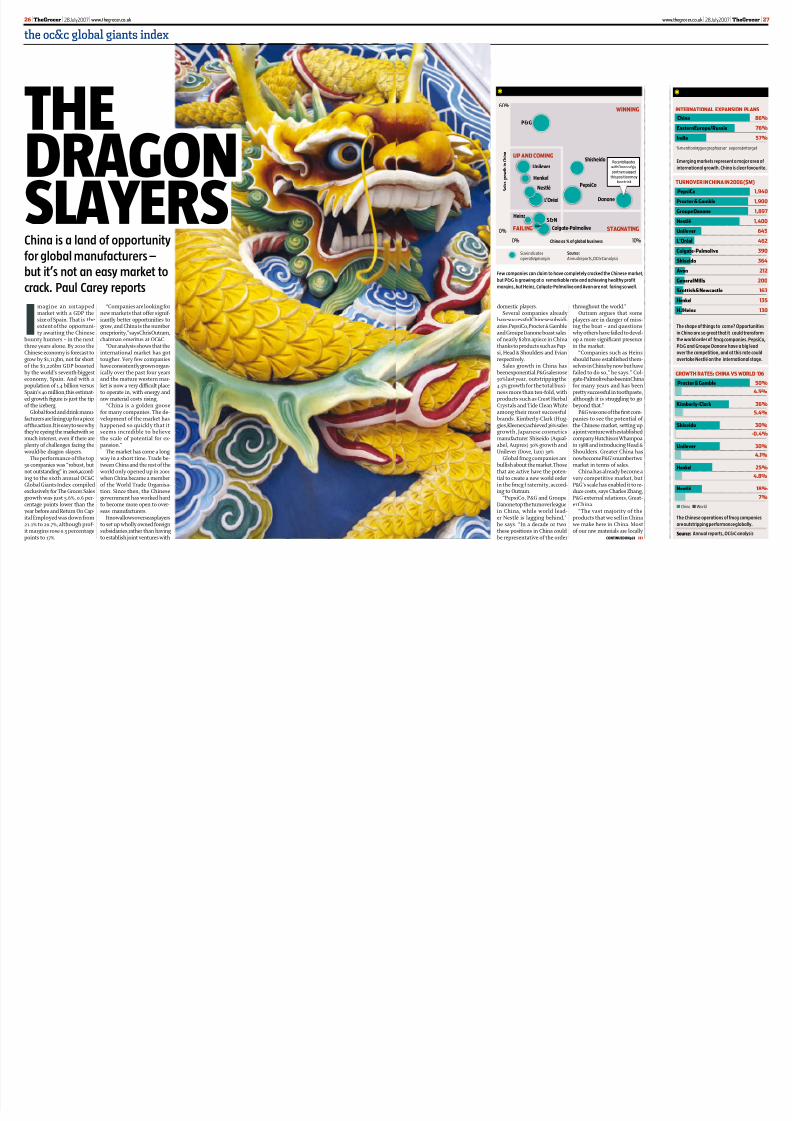

Few companies can claim to have completely cracked the Chinese market, but P&G is growing at a remarkable rate and achieving healthy profit margins, but Heinz, Colgate-Palmolive and Avon are not faring so well. 26l TheGrocer l 28July2007 l www.thegrocer.co.uk www.thegrocer.co.uk l 28July2007 l TheGrocer l 27 the oc&c global giants index the dragon slayers the growing market international expansion plans C 86% ee/r 76% id 57% %mentionin ggeographyasan expansi ontarget Emerging markets represent a major area of international growth. China is clear favourite. turnover in China in 2006 ($m) pC 1,940 pc& Gb 1,900 GD 1,897 né 1,400 u 645 l’oé 462 Cg-p 390 sd 364 a 212 Gm 200 sc&nc 163 hk 135 hJhz 130 The shape of things to come? Opportunities in China are so great that it could transform the world order of fmcg companies. PepsiCo, P&G and Groupe Danone have a big lead over the competition, and at this rate could overtake Nestlé on the international stage. Growth rates: China vs worlD ‘06 pc& Gb 50% 4.5% Kb-Ck 36% 5.4% sd 30% -0.4% u 30% 4.1% hk 25% 4.8% né 18% 7% n China n World The Chinese operations of fmcg companies are outstripping performance globally. source: Annual reports, OC&C analysis ✱ i magine an untapped market with a GDP the size of Spain. That is the extent of the opportuni- ty awaiting the Chinese bounty hunters – in the next three years alone. By 2010 the Chinese economy is forecast to grow by $1,113bn, not far short of the $1,226bn GDP boasted by the world’s seventh-biggest economy, Spain. And with a population of 1.4 billion versus Spain’s 40 million,this estimat- ed growth gure is just the tip of the iceberg. Global food and drink manu- facturers are lining up for a piece of the action.It is easy to see why they’re eyeing the marketwith so much interest, even if there are plenty of challenges facing the would-be dragon slayers. The performance of the top 50 companies was “robust, but not outstanding” in 2006,accord- ing to the sixth annual OC&C Global Giants Index compiled exclusively for The Grocer.Sales growth was just 5.6%, 0.6 per- centage points lower than the year before and Return On Cap- ital Employed was down from 21.1% to 20.7%, although prof- it margins rose 0.5 percentage points to 17%. China is a land of opportunity for global manufacturers – but it’s not an easy market to crack. Paul Carey reports “Companies are looking for new markets that offer signif- icantly better opportunities to grow, and China is the number onepriority,”saysChrisOutram, chairman emeritus at OC&C. “Our analysis shows that the international market has got tougher. Very few companies have consistently grown organ- ically over the past four years and the mature western mar- ket is now a very difcult place to operate in, with energy and raw material costs rising. “China is a golden goose for many companies. The de- velopment of the market has happened so quickly that it seems incredible to believe the scale of potential for ex- pansion.” The market has come a long way in a short time. Trade be- tween China and the rest of the world only opened up in 2001 when China became a member of the World Trade Organisa- tion. Since then, the Chinese government has worked hard to become more open to over- seas manufacturers. Itnowallowsoverseasplayers to set up wholly owned foreign subsidiaries,rather than having to establish joint ventures with China: winnersandlosers ✱ Sizeindicates operatin gmargin Source: Annua lreports,OC&Canalysis S a l e s g r o w t h i n C h i n a 60% 0% 0% 10% China as % of global business P&G Unilever Henkel Nestlé L’Oréal Shisheido PepsiCo Danone Heinz S&N Colgate-Palmolive winninG staGnatinG Failin G up anD CominG Recentdisputes withDanone ’sjv partnersugges t thispositionmay beatrisk Avon domestic players. Several companies already havesuccessfulChinesesubsidi- aries.PepsiCo,Procter & Gamble and Groupe Danone boast sales of nearly $2bn apiece in China thanks to products such as Pep- si, Head & Shoulders and Evian respectively. Sales growth in China has beenexponential.P&Gsalesrose 50% last year, outstrippin g the 4.5% growth for the total busi- ness more than ten-fold, with products such as Crest Herbal Crystals and Tide Clean White among their most successful brands. Kimberly-Clark (Hug- gies,Kleenex) achieved 36% sales growth, Japanese cosmetics manufacturer Shiseido (Aqual- abel, Aupres) 30% growth and Unilever (Dove, Lux) 30%. Global fmcg companies are bullish about the market.Those that are active have the poten- tial to create a new world order in the fmcg f raternity, accord- ing to Outram. “PepsiCo, P&G and Groupe Danone top the turnover league in China, while world lead- er Nestlé is lagging behind,” he says. “In a decade or two these positions in China could be representative of the order throughout the world.” Outram argues that some players are in danger of miss- ing the boat – and questions why others have failed to devel- op a more signicant presence in the market. “Companies such as Heinz should have established them- selves in China by now but have failed to do so,” he says.” Col- gate-PalmolivehasbeeninChina for many years and has been pretty successful in toothpaste, although it is struggling to go beyond that.” P&G was one of the rst com- panies to see the potential of the Chinese market, setting up a joint venture with established company Hutchison Whampoa in 1988 and introducing Head & Shoulders. Greater China has nowbecomeP&G’snumbertwo market in terms of sales. China has already become a very competitive market, but P&G’s scale has enabled it to re- duce costs, says Charles Zhang, P&G external relations, Great- er China. “The vast majority of the products that we sell in China we make here in China. Most of our raw materials are locally Continuedonp28

-

Upload

iordachencristina1889 -

Category

Documents

-

view

221 -

download

0

Transcript of the Grocer - Global 50

8/8/2019 the Grocer - Global 50

http://slidepdf.com/reader/full/the-grocer-global-50 1/2

Few companies can claim to have completely cracked the Chinese market,

but P&G is growing at a remarkable rate and achieving healthy profit

margins, but Heinz, Colgate-Palmolive and Avon are not faring so well.

26 l TheGrocer l 28July2007 l www.thegrocer.co.uk www.thegrocer.co.uk l 28July2007 l TheGrocer l 27

the oc&c global giants index

thedragonslayers

the growing market

international expansion plans

C 86%

e e/r 76%

id 57%

%mentioninggeographyasan expansiontarget

Emerging markets represent a major area of

international growth. China is clear favourite.

turnover in China in 2006 ($m)

pC 1,940

pc & Gb 1,900

G D 1,897

né 1,400

u 645

l’oé 462

Cg-p 390

sd 364

a 212

G m 200

sc & nc 163

hk 135

hJ hz 130

The shape of things to come? Opportunities

in China are so great that it could transform

the world order of fmcg companies. PepsiCo,

P&G and Groupe Danone have a big leadover the competition, and at this rate could

overtake Nestlé on the international stage.

Growth rates: China vs worlD ‘06

pc & Gb 50%

4.5%

Kb-Ck 36%

5.4%

sd 30%

-0.4%

u 30%

4.1%

hk 25%

4.8%

né 18%

7%

n China n World

The Chinese operations of fmcg companies

are outstripping performance globally.

source: Annual reports, OC&C analysis

✱

imagine an untappedmarket with a GDP thesize of Spain. That is theextent of the opportuni-ty awaiting the Chinese

bounty hunters – in the nextthree years alone. By 2010 theChinese economy is forecast togrow by $1,113bn, not far shortof the $1,226bn GDP boastedby the world’s seventh-biggesteconomy, Spain. And with apopulation of 1.4 billion versusSpain’s 40 million,this estimat-ed growth gure is just the tipof the iceberg.

Global food and drink manu-facturers are lining up for a pieceof the action.It is easy to see whythey’re eyeing the marketwith somuch interest, even if there areplenty of challenges facing thewould-be dragon slayers.

The performance of the top50 companies was “robust, butnot outstanding” in 2006,accord-ing to the sixth annual OC&CGlobal Giants Index compiledexclusively for The Grocer.Salesgrowth was just 5.6%, 0.6 per-centage points lower than theyear before and Return On Cap-ital Employed was down from21.1% to 20.7%, although prof-it margins rose 0.5 percentagepoints to 17%.

China is a land of opportunityfor global manufacturers –

but it’s not an easy market tocrack. Paul Carey reports

“Companies are looking fornew markets that offer signif-icantly better opportunities togrow, and China is the numberone priority,” says Chris Outram,chairman emeritus at OC&C.

“Our analysis shows that theinternational market has gottougher. Very few companieshave consistently grown organ-ically over the past four yearsand the mature western mar-ket is now a very difcult placeto operate in, with energy andraw material costs rising.

“China is a golden goose

for many companies. The de-velopment of the market hashappened so quickly that itseems incredible to believethe scale of potential for ex-pansion.”

The market has come a longway in a short time. Trade be-tween China and the rest of theworld only opened up in 2001when China became a memberof the World Trade Organisa-tion. Since then, the Chinesegovernment has worked hardto become more open to over-seas manufacturers.

It now allows overseas playersto set up wholly owned foreignsubsidiaries,rather than havingto establish joint ventures with

China:winners and losers✱

Sizeindicatesoperatingmargin

Source:Annualreports,OC&Canalysis

S a l e s g r o w t h i n C h i n a

60%

0%

0% 10%China as % of global business

P&G

Unilever

Henkel

Nestlé

L’Oréal

Shisheido

PepsiCo

Danone

HeinzS&N

Colgate-Palmolive

winninG

staGnatinGFailin

G

up anD CominGRecentdisputes

withDanone’sjvpartnersuggest

thispositionmaybeatrisk

Avon

domestic players.Several companies already

have successful Chinese subsidi-aries.PepsiCo,Procter & Gambleand Groupe Danone boast salesof nearly $2bn apiece in Chinathanks to products such as Pep-si, Head & Shoulders and Evianrespectively.

Sales growth in China hasbeen exponential.P&G sales rose50% last year, outstripping the4.5% growth for the total busi-ness more than ten-fold, withproducts such as Crest HerbalCrystals and Tide Clean White

among their most successfulbrands. Kimberly-Clark (Hug-gies,Kleenex) achieved 36% salesgrowth, Japanese cosmeticsmanufacturer Shiseido (Aqual-abel, Aupres) 30% growth andUnilever (Dove, Lux) 30%.

Global fmcg companies arebullish about the market.Thosethat are active have the poten-tial to create a new world orderin the fmcg f raternity, accord-ing to Outram.

“PepsiCo, P&G and GroupeDanone top the turnover leaguein China, while world lead-er Nestlé is lagging behind,”he says. “In a decade or twothese positions in China couldbe representative of the order

throughout the world.”Outram argues that some

players are in danger of miss-ing the boat – and questionswhy others have failed to devel-op a more signicant presencein the market.

“Companies such as Heinzshould have established them-selves in China by now but havefailed to do so,” he says.” Col-gate-PalmolivehasbeeninChinafor many years and has beenpretty successful in toothpaste,although it is struggling to gobeyond that.”

P&G was one of the rst com-panies to see the potential of the Chinese market, setting upa joint venture with establishedcompany Hutchison Whampoain 1988 and introducing Head &Shoulders. Greater China hasnow become P&G’s number twomarket in terms of sales.

China has already become avery competitive market, butP&G’s scale has enabled it to re-duce costs, says Charles Zhang,P&G external relations, Great-er China.

“The vast majority of theproducts that we sell in Chinawe make here in China. Mostof our raw materials are locally

Continuedonp28

8/8/2019 the Grocer - Global 50

http://slidepdf.com/reader/full/the-grocer-global-50 2/2

drinkers were persuaded to mixit with green tea and it has beena success.

“When P&G introduced nap-pies to China it had to educatemothers about their purpose.They had never seen them be-fore and needed to be taughthow they worked.”

Trying too hard to meet theneeds of the local market canhave unanticipated consequenc-es for other parts of the businessas Tesco discovered when Brit-ish newspapers reacted withmoral outrage to the discoveryit was selling live turtles in itsChinese stores.

Western companies thatmakethe most of the opportunitiesChina offers, however, will beable to offset the impact of anyweaker markets they are oper-ating in.

“Companies need to findways of taking a bigger shareof the growth in developed mar-kets,” says Outram. “There isevidence of a strategic shift to-wards top-line growth. Theyare splashing out on advertis-ing and being more aggressiveat driving sales.”

Those that continue to focuson more established marketswill need to increase their spend

on research and developmentand many are already doing so,says Outram, often by buyingin the NPD.

“Instead of spending timecoming up with new ideas them-selves, companies such as P&Gare buying innovation in theform of smaller companies.They have adopted a ‘proud-ly found elsewhere’ mentality,which is paying off.It gets prod-ucts to market rapidly, reducesthe failure rates and is likely tobe copied by a range of com-panies.”

Elsewhere, acquisitions re-vealed a greater level of caution,

Continuedfromp27

28 l TheGrocer l 28July2007 l www.thegrocer.co.uk

cex

www.thegrocer.co.uk l 28July2007 l TheGrocer l 29

the oc&c global giants index

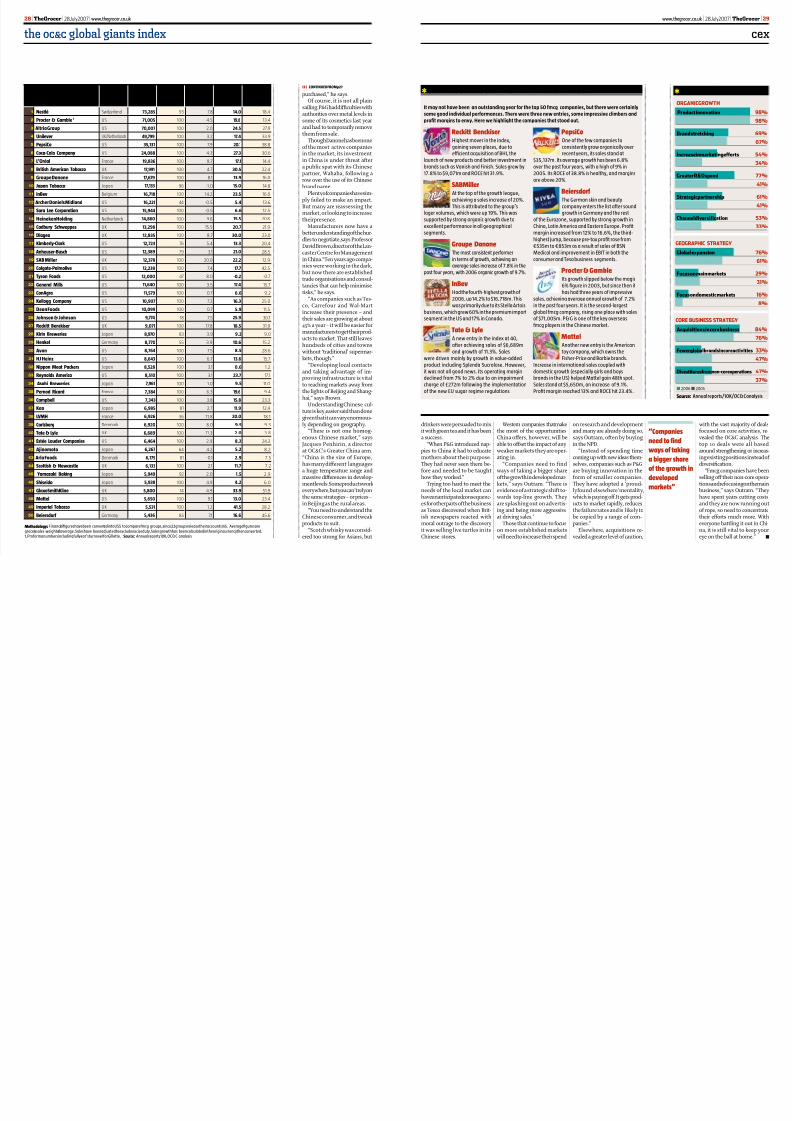

key strategiC direCtions

orGaniC Growth

pdc 98%

98%

Bd cg 69%

67%

increasenmarketngefforts 54%

34%

G r&D d 77%

41%

sgc 61%

41%

C dfc 53%

33%

GeoGraphiC strateGy

Gb 76%

61%

Fc k 29% 31%

Fc dc k 16%

8%

Core Business strateGy

acq c b 84%

76%

Fewerglobalbrandsncoreactvtes 33%

47%

Dvestturesfromnon-coreoperatons 47%

37%

n 2006n 2005

source: Annual reports/10K/OC&C analysis

✱

Reckitt BenckiserHighest mover in the index,gaining seven places, due toefcient acquisition of BHI, the

launch of new products and better investment inbrands such as Vanish and Finish. Sales grew by17.8% to $9,071m and ROCE hit 31.9%.

SABMillerAt the top of the growth league,achieving a sales increase of 20%.This is attributed to the group’s

lager volumes, which were up 19%. This wassupported by strong organic growth due toexcellent performance in all geographicalsegments.

Groupe DanoneThe most consistent performerin terms of growth, achieving anaverage sales increase of 7.8% in the

past four years, with 2006 organic growth of 9.7%.

InBevHad the fourth-highest growth of 2006, up 14.2% to $16,718m. Thiswas primarily due to its Stella Artois

business, which grew 60% in the premium importsegment in the US and 17% in Canada.

Tate & LyleA new entry in the index at 40,after achieving sales of $6,689mand growth of 11.3%. Sales

were driven mainly by growth in value-addedproduct including Splenda Sucralose. However,it was not all good news. Its operating margindeclined from 7% to 2% due to an impairmentcharge of £272m following the implementationof the new EU sugar regime regulations.

PepsiCoOne of the few companies toconsistently grow organically overrecent years, its sales stand at

$35,137m. Its average growth has been 6.8%over the past four years, with a high of 9% in2005. Its ROCE of 38.8% is healthy, and marginsare above 20%.

Beiersdorf The German skin and beautycompany enters the list after soundgrowth in Germany and the rest

of the Eurozone, supported by strong growth inChina, Latin America and Eastern Europe. Protmargin increased from 12% to 16.6%, the third-highest jump, because pre-tax prot rose from€535m to €853m as a result of sales of BSNMedical and improvement in EBIT in both theconsumer and Tesa business segments.

Procter & GambleIts growth slipped below the magic6% gure in 2003, but since then ithas had three years of impressive

sales, achieving average annual growth of 7.2%in the past four years. It is the second-largestglobal fmcg company, rising one place with salesof $71,005m. P&G is one of the key overseasfmcg players in the Chinese market.

MattelAnother new entry is the Americantoy company, which owns theFisher-Price and Barbie brands.

Increase in international sales coupled withdomestic growth (especially girls and boysbrands in the US) helped Mattel gain 48th spot.Sales stand at $5,650m, an increase of 9.1%.Prot margin reached 13% and ROCE hit 23.4%.

star performers companies that impressed this year✱

with the vast majority of dealsfocused on core activities, re-vealed the OC&C analysis. Thetop 10 deals were all basedaround strengthening or increas-ing existing positions instead of diversication.

“Fmcg companies have beenselling off their non-core opera-tionsandrefocusingonthemainbusiness,” says Outram. “Theyhave spent years cutting costsand they are now running outof rope, so need to concentratetheir efforts much more. Witheveryone battling it out in Chi-na, it is still vital to keep youreye on the ball at home.” n

“Companies

need to find

ways of taking

a bigger share

of the growth in

developed

markets”

Company & ranking Country ofdomiCile

groCery sales 2006

($m)

groCery sales in

total sales(%)

groCery sales

growth2005-06 (%)

Profitmargin

2006 (%)roCe 2006

(%)

1 né Switzerland 73,285 93 7.8 14.0 18.4

2 Pc & gb 1 US 71,005 100 4.5 19.8 13.4

3 a gp US 70,007 100 2.0 24.5 27.9

4

uv UK/Netherlands 49,799 100 3.2 17.4 33.95 PpC US 35,137 100 7.9 20.1 38.8

6 Cc-C Cp US 24,088 100 4.3 27.3 30.6

7 l’oé France 19,836 100 8.7 17.1 14.4

8 B ac tbcc UK 17,991 100 4.7 30.5 22.4

9 gp d France 17,679 100 8.1 13.9 16.0

10 Jp tbcc Japan 17,133 96 -1.0 15.0 14.8

11 iBv Belgium 16,718 100 14.2 23.5 16.0

12 ac d m US 16,221 44 -0.5 5.4 13.6

13 s l Cp US 15,944 100 -0.5 6.6 12.5

14 hk h Netherlands 14,860 100 9.6 15.5 20.8

15 Cb scpp UK 13,298 100 15.5 20.7 21.9

16 d UK 12,835 100 8.7 30.0 23.0

17 Kb-Ck US 12,723 76 5.4 13.3 20.4

18 a-Bc US 12,389 79 3.1 21.0 28.5

19 saB m UK 12,378 100 20.0 22.2 12.9

20 C-Pv US 12,238 100 7.4 17.7 42.5

21 t f US 12,000 47 8.0 -0.2 -0.7

22 g m US 11,640 100 3.5 17.4 15.7

23 Ca US 11,579 100 0.7 6.6 9.2

24 K Cp US 10,907 100 7.2 16.3 25.0

25 d f US 10,099 100 -0.7 5.9 11.5

26 J & J US 9,774 18 7.5 25.9 30.1

27 rck Bck UK 9,071 100 17.8 18.5 31.9

28 K B Japan 8,970 83 3.9 9.2 9.0

29 hk Germany 8,770 55 3.9 10.6 15.2

30 av US 8,764 100 7.5 8.5 28.6

31 hJ hz US 8,643 100 6.7 13.6 15.7

32 npp m Pck Japan 8,528 100 3.1 0.6 1.2

33 r ac US 8,510 100 3.1 23.7 17.1

34 a B Japan 7,961 100 1.0 9.5 11.0

35 P rc France 7,384 100 6.3 19.6 9.4

36 Cpb US 7,343 100 3.8 15.8 23.3

37 K Japan 6,985 81 2.7 11.9 12.4

38 lVmh France 6,926 36 11.8 20.0 18.1

39 Cb Denmark 6,920 100 8.0 9.5 9.3

40 t & l UK 6,689 100 11.3 2.0 3.8

41 eé l Cp US 6,464 100 2.9 8.2 24.3

42 aj Japan 6,267 64 4.2 5.2 8.2

43 a f Denmark 6,175 81 -0.1 2.9 7.5

44 sc & nc UK 6,133 100 2.1 11.7 7.2

45 yzk Bk Japan 5,949 92 2.0 1.5 2.9

46 s Japan 5,938 100 4.9 4.2 6.0

47 gxsK UK 5,800 14 4.9 33.9 51.9

48 m US 5,650 100 9.1 13.0 23.4

49 ip tbcc UK 5,531 100 1.2 41.5 28.2

50 B Germany 5,436 85 7.1 16.6 45.6

Methodology: Financialgureshavebeen convertedintoUS$ tocomparefmcg groups,since22groupsreleasetheiraccountsin$. Averageguresaregrocerysales weightedaverage.Saleshave beenadjustedtoexcludeexciseduty.Salesgrowthhas beencalculatedintheorigincurrencythenconverted.1.Proformanumbersincludingfullyear’sturnoverforGillette.Source: Annualreports,10K,OC&C analysis

purchased,” he says.Of course, it is not all plain

sailing.P&G had difculties withauthorities over metal levels insome of its cosmetics last yearand had to temporarily removethem from sale.

Though Danone has been oneof the most active companiesin the market, its investmentin China is under threat aftera public spat with its Chinesepartner, Wahaha, following arow over the use of its Chinesebrand name.

Plentyofcompanieshavesim-ply failed to make an impact.But many are reassessing themarket, or looking to increasetheir presence.

Manufacturers now have abetter understanding of the hur-dles to negotiate,says ProfessorDavid Brown,director of the Lan-caster Centre for Managementin China.“Ten years ago compa-nies were working in the dark,but now there are establishedtrade organisations and consul-tancies that can help minimiserisks,” he says.

“As companies such as Tes-co, Carrefour and Wal-Martincrease their presence – andtheir sales are growing at about45% a year – it will be easier formanufacturers to get their prod-ucts to market. That still leaveshundreds of cities and townswithout ‘traditional’ supermar-kets, though.”

“Developing local contactsand taking advantage of im-proving infrastructure is vitalto reaching markets away fromthe lights of Beijing and Shang-hai,” says Brown.

Understanding Chinese cul-

ture is key,easier said than donegiven that it can vary enormous-ly depending on geography.

“There is not one homog-enous Chinese market,” says

Jacques Penhirin, a directorat OC&C’s Greater China arm.“China is the size of Europe,has many different languages,a huge temperature range andmassive differences in develop-mentlevels.Someproductsworkeverywhere,but you can’t rely onthe same strategies – or prices –in Beijing as the rural areas.

“You need to understand theChinese consumer, and tweakproducts to suit.

“Scotch whisky was consid-ered too strong for Asians, but

It may not have been an outstanding year for the top 50 fmcg companies, but there were certainlysome good individual performances. There were three new entries, some impressive climbers andprot margins to envy. Here we highlight the companies that stood out.