The great bubble tranfer

5

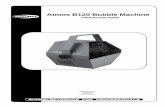

Stephanie Pomboy 212.989.3311 1 April 3, 2002 Housing Wealth vs. Stock Market Wealth $Billions 500 1500 2500 3500 4500 5500 6500 7500 8500 9500 10500 11500 12500 13500 14500 Q1-1980 Q1-1981 Q1-1982 Q1-1983 Q1-1984 Q1-1985 Q1-1986 Q1-1987 Q1-1988 Q1-1989 Q1-1990 Q1-1991 Q1-1992 Q1-1993 Q1-1994 Q1-1995 Q1-1996 Q1-1997 Q1-1998 Q1-1999 Q1-2000 Q1-2001 q1-2022 85000 88500 92000 95500 99000 102500 106000 109500 113000 116500 120000 123500 127000 The Great Bubble Transfer Either by simple serendipity or in yet another flawlessly orchestrated performance by the Maestro, the U.S. has quietly undergone the greatest ‘Bubble Transfer’ in history. The $3 trillion in wealth that was so abruptly lopped off the top of the Wilshire since its peak in March 2000 has miraculously resurfaced in the real estate market where homeowners have seen the value of their homes appreciate $2-3 trillion over the same timeframe. Like the bubble in financial assets, the new real estate bubble has its own distinctly disturbing characteristics. For example, one could argue, and quite cogently, that the home has become the new ‘margin account’ as consumers through popular programs like ‘cash-out’ Refi increasingly leverage against unrealized gains in their single largest asset.

-

Upload

claudio-santos -

Category

Documents

-

view

214 -

download

1

description

America Bubble

Transcript of The great bubble tranfer

Stephanie Pomboy 212.989.3311

1 April 3, 2002

Housing Wealth vs. Stock Market Wealth $Billions

500

1500

2500

3500

4500

5500

6500

7500

8500

9500

10500

11500

12500

13500

14500

Q1-

1980

Q1-

1981

Q1-

1982

Q1-

1983

Q1-

1984

Q1-

1985

Q1-

1986

Q1-

1987

Q1-

1988

Q1-

1989

Q1-

1990

Q1-

1991

Q1-

1992

Q1-

1993

Q1-

1994

Q1-

1995

Q1-

1996

Q1-

1997

Q1-

1998

Q1-

1999

Q1-

2000

Q1-

2001

q1-2

022

85000

88500

92000

95500

99000

102500

106000

109500

113000

116500

120000

123500

127000

The Great Bubble Transfer Either by simple serendipity or in yet another flawlessly orchestrated performance by the Maestro, the U.S. has quietly undergone the greatest ‘Bubble Transfer’ in history. The $3 trillion in wealth that was so abruptly lopped off the top of the Wilshire since its peak in March 2000 has miraculously resurfaced in the real estate market where homeowners have seen the value of their homes appreciate $2-3 trillion over the same timeframe. Like the bubble in financial assets, the new real estate bubble has its own distinctly disturbing characteristics. For example, one could argue, and quite cogently, that the home has become the new ‘margin account’ as consumers through popular programs like ‘cash-out’ Refi increasingly leverage against unrealized gains in their single largest asset.

Stephanie Pomboy 212.989.3311

2 April 3, 2002

Perhaps the most disturbing hallmark of this Refi mania is the corresponding plunge in homeowners’ equity stake, especially in an environment where secular lows in both the Unemployment Rate and Mortgage Rates would suggest just the opposite would occur.

Homeowners Equity % Home Value

52

54.5

57

59.5

62

64.5

67

69.5

72

Q1-

1980

Q1-

1981

Q1-

1982

Q1-

1983

Q1-

1984

Q1-

1985

Q1-

1986

Q1-

1987

Q1-

1988

Q1-

1989

Q1-

1990

Q1-

1991

Q1-

1992

Q1-

1993

Q1-

1994

Q1-

1995

Q1-

1996

Q1-

1997

Q1-

1998

Q1-

1999

Q1-

2000

Q1-

2001

The cash-out Refi numbers reveal a ‘speculative fervor’ that makes the Nasdaq mania look tame. According to estimates by Fannie Mae, the average cash-out Refi is $34,000. This sounds like a lot to me, particularly considering that the median home price is just $150,000…e.g., the average Joe is extracting 20% of his home value! In total, Fannie Mae estimates that $75 to $80b will be drawn out of homes this year with about 60% of that cash being spent with the remainder being used to pay down high interest debt. (The Fed expects over 70% to be spent). Either way, this translates to about $50-55b increase in consumption, or one full month’s worth of annual Personal Consumption Expenditures. So the impact on consumption is both real and largely quantifiable.

Stephanie Pomboy 212.989.3311

3 April 3, 2002

Moreover, there is evidence to suggest that the housing wealth effect may be significantly larger than the stock market wealth effect we’ve become so obsessed with. Based on a recent study by Robert Shiller (of “Irrational Exuberance” fame) housing has always been a more important driver for consumers than the stock market. In his rigorous state-by-state and 14 country analysis, he found housing to have TWICE the correlation with consumption than the stock market has. So, with housing in the driver’s seat of the great consumption rig, it bears considering what the future holds for the sector. As to the demand side, it’s essentially a factor of employment and demographics. Given the remarkable strength in employment, it’s hard to envision it getting much better from here. And household formations, having peaked in 1998 and are headed steadily downward as the baby-boom bulge moves into retirement. So, the outlook for demand would appear to be stagnant, at best. Meanwhile, the supply picture looks considerably less favorable. Like the real estate boom of the mid-1980s, the recent run up in prices has invited an enormous amount of new construction. Some of this new supply is already being reflected in the Inventory of Unsold Homes, which has started to trend higher.

New Residential Construction

50

100

150

200

250

300

350

400

Jan-

1980

Jan-

1981

Jan-

1982

Jan-

1983

Jan-

1984

Jan-

1985

Jan-

1986

Jan-

1987

Jan-

1988

Jan-

1989

Jan-

1990

Jan-

1991

Jan-

1992

Jan-

1993

Jan-

1994

Jan-

1995

Jan-

1996

Jan-

1997

Jan-

1998

Jan-

1999

Jan-

2000

Jan-

2001

Jan-

2002

Stephanie Pomboy 212.989.3311

4 April 3, 2002

With all this supply coming on, it’s just a matter of time before prices get smacked…

And this is where things get ugly… With homeowners’ equity near all-time lows, any softening in home prices could engender the risk of a cascade into negative equity. But even more immediately, the increase in mortgage debt service (again, despite new lows in mortgage rates) does not bode well for consumption as the Fed prepares to reverse course.

Inventory of Unsold Homes vs. Median Home Price

1250000

1500000

1750000

2000000

2250000

2500000

2750000

3000000

3250000

Sep

-198

2

Sep

-198

3

Sep

-198

4

Sep

-198

5

Sep

-198

6

Sep

-198

7

Sep

-198

8

Sep

-198

9

Sep

-199

0

Sep

-199

1

Sep

-199

2

Sep

-199

3

Sep

-199

4

Sep

-199

5

Sep

-199

6

Sep

-199

7

Sep

-199

8

Sep

-199

9

Sep

-200

0

Sep

-200

1

-2.50

0.00

2.50

5.00

7.50

10.00

Stephanie Pomboy 212.989.3311

5 April 3, 2002

Mortgage Debt Service % DPI

4

4.2

4.4

4.6

4.8

5

5.2

5.4

5.6

5.8

6

6.2

6.4

6.6

Q1-

1980

Q1-

1981

Q1-

1982

Q1-

1983

Q1-

1984

Q1-

1985

Q1-

1986

Q1-

1987

Q1-

1988

Q1-

1989

Q1-

1990

Q1-

1991

Q1-

1992

Q1-

1993

Q1-

1994

Q1-

1995

Q1-

1996

Q1-

1997

Q1-

1998

Q1-

1999

Q1-

2000

Q1-

2001

LET’S TWIST AGAIN… ? Aware that the underpinnings of the current recovery are rooted in this housing bubble, Greenspan will surely make no haste in raising rates. But, should inflation pressures (like the recent increase in energy prices) force his hand, we would not be surprised, in fact we would expect to see the Fed try to tinker with the shape of the yield curve to keep mortgage rates down. (Like they did last winter in their coordinated ‘Operation Twist’ with Treasury). In light of the recent revelation that the Fed discussed employing ‘unconventional measures’, should their standard tools be rendered impotent, we must surely be alert to what they may be doing behind the curtain.