the GovernmentofPakistan Pakistan ShelterResource ...pdf.usaid.gov/pdf_docs/PNABU491.pdf ·...

68

Prepared for the Government of Pakistan bytM Pakistan Shelter Resource Mobilization Program United States Agency for International Development Mission to Pakistan and Afghanistan BEST AVAILABLE DOCUMENT

Transcript of the GovernmentofPakistan Pakistan ShelterResource ...pdf.usaid.gov/pdf_docs/PNABU491.pdf ·...

Prepared for the

Government of PakistanbytM

Pakistan Shelter Resource Mobilization ProgramUnited States Agency for International Development

Mission to Pakistan and Afghanistan

BEST AVAILABLE DOCUMENT

Pakistan Shelter Resource Mobilization ProgramGcwemmeat olPekbtan I u.s. Alency lor international Development

Fourth Floor, 30 West Blue Area, Islamabad, PakistanTelephone: (92-51) 818463/826226 Fax: (92-51) 217131

Staff:

Jon Wegge, ChiefTechnical AdvisorJavaid I. Qureshi, Program Management SpecialistJaved Akthar, Project Management SpecialistJeanne Russell, Publications EditorTahir. Younis, Secretary

This report relies heavily on research carried out by Planning andDevelopment Collaborative, Inc. (pADCO) ofWashington, D.C., undercontract with the U.S. Agency for International Development Mission toPakistan and Afghanistan. In particular, recognition is due to the principalauthor, Mr. Daniel S. Coleman.

Except where otherwise indicated, photographs in this document were takenby Ms. Samina Rizvi of21st Century Consult~ncyand Management Services(Pvt.) Ltd. of Karachi.

This report is dedicated to the memory of the late James Wright Ladd, aconsultant to PADCO for this study. Mr. Ladd developed the financialmodels that appear in this report.

At the time this report was written, 31 Pakistani rupees (Rs. 31) wereequivalent to one US dollar (US 51).

The views expressed herein are those ofthe authors and do not necessarilyreflect those ofthe United States Agencyfor International Development, t/'eUSAJD Mission to Pakistan and Afg/,anistan, or the Government ofPakistan.

June, 1994

Contents

Introduction 1

Executive Summary 7

Background 13Housing Finance in Pakistan 13Economic Benefits ofa Housing Finance System 14The Missing Ingredient: A Housing Finance System 15

Structuring the Housing Finance Sector 21Key Elements 21TI,e Regulatory Environment 22Housing Policy 22A Housing Constituency 23

Resource Mobilization Issues 27Resource Mobilization Worldwide 27Resource Mobilization in Pakistan 30

Specific Remedies 31Government Incentive Measures 34

The Housing Refinance Facility 39HRF Operations 39HRF Terms and Conditions 41Financial Impact on tl,e HFCs 42Risks to the SBP 44Foundationfor a National Mortgage Market 45ClosureoftheHRF 45

An Apex Bank 49What an Apex Bank Is 49Examples in Developed Countries 50Examples in Developing Countries 51An Apex Bankfor Pakistan? 54

Next Steps for Pakistan's Housing Finance Sector 59Conclusions 59Immediate Actions 60

Appendix A - Financial Models 63Appendix B - Comparison ofHousing Finance Systems 69Appendix C - The Impact ofInflation on Housing Finance 75

SRMP Page;

Introductio...,

Housingfinance offers greatpromise to become the most dynamic part ofPakistan's housing sector. The vitality it can bring to the housing economy hasdeveloped only in the past severalyears, with the introduction ofmarket-orientedlending. Whether it canfuljill the promise it holds dePends largely on thecontinuation ofpolicy reform to create an environment that not only enableshousingfinance to grow, butpermits it to flourish.

There is ample reason to have titled this paPer '~ Blueprintfor the DevelopmentofHousing Finance in Pakistan. "Housingfinance, like housing itse{f, must bebuilt on a solidfoundation,' only then can a plannedstructure be built.Market-oriented housingfinance now has a solidfoundation in Pakistan; thepurpose ofthe paper is to set out a I 'blueprint' 'for completing tlie structure ofanefficient and capable housingfinance system.

This paper has been prepared by the Shelter Resource Mobilization Program(SRMP) ofthe U.S.A.LD. Mission to Pakistan andAfghanistan. Since the SRMPhas now come to an end, the report is, in many respects, an attempt by the staffofthe SRMP to "Ieave behind" suggestions and recommendationsfor future actionsin the housingfinance sector and to provide a context that promotes greaterunderstanding ofthe housingfinance and urban sectors.

Housing Finance and Economic Growth

In countries where policy-makers have valued the housing sectorfor itscontributions to the economy, housingfinance has been an engine ofeconomicgrowth. A well-functioning housing finance system offtrs incentivesforhouseholds to save, provides investors with opPOrtunites to gain stable,long-term retums, creates large numbers ofjobsfor skilled and unskilledworkers in construction and ancillary industries, enables homeowners toleverage their physical assets intofinancial assetsfor investment, andcontributes greatly to the d.eePening and broadening ofthe finance sector.

A well-functioning housingfinance system provides credit to households,inherently broadening access to credit by individuals,' it adds SPecialized newinstitutions and creates new financial instruments to enable longer-terminvestments and stabilize loan portfolios, inherently deepening the finance sector.Evidencefrom many countries suggests that housingfinance plays a major rolein economic growth and is particularly vital to development offinancial sectorcapacity. When policy environments enablefinance sectors to movefrom

. primitive levels ofdevelopment to more sophistit:ated capabilities, housing

SRMPPageJ

finance appears to almost always be a major - ifnot the single greatest growth area infinance.

Housing and Housing Finance Policy in Pakistan

In Pakistan, policy-makers havefor far too long viewed the housing sector as apurely social sector. The policy outlook is that housing is a basic need, butpeople are poor,' therefore the housing sector requires subsidizedplots,subsidizedfinance, subsidized infrastructure, and subsidized services. The realityofexperience, however, shows poignantly that housing hasfar less priority thandefense or debt service, and rarely arefunds available in the quantity needed. Italso shows that byputting housing on a non-market basis, the formal privatesector can play only an extremely limited role, and that housing and urbandevelopmentfall almost totally within the preserve ofinefficient andfrequentlyincapable public sector agencies.

Put simply, the policy which hasflowedfrom this outlook is one that has becomeself-defeating. The private sector is "shut out, ~, but the public sector has neitherthe resources or capabilities to meet the minimum needs ofthe housing andurhan sectors. Pakistan's population is rapidly expanding and rapidlyurbanizing. Most housing construction is informally constructed,' most urhangrowth is unplanned and unserviced. Housing contributes little to the economyand virtually nothing to the finance sector.

Until very recently, the private sector had not been permitted to operate housingfinance companies that specialize in providing housing credit. Because there islittle credit availablefor housing, people must save the entire amount in advance,or informally borrow the savings ofothers, usually otherfamily members. Sinceeveryone needs housing, the total quantity ofsuch savings is probably very large.Yet, sincefew people save withformal sectorfinancial institutions, little ofthisvolume ofsavingsfinds its way into the finance sector. In essence, people do, ofnecessity, have a long-term view offinancing housing, but the economy lacks theinstitutions and savings mechanisms to permitpeople's housing resources toflowthrough theformal financial sector.

To see that such institutions do rise andflourish, strong leadership is requiredfrom both the private andpublic sectors. In Pakistan, people have leamedfromexperience thatfinancial institutions are not always trustworthy and that rarelydo financial institutions actually offer services to households. They approachthem with caution. At the same time, the public sector has inadequately regulatedthe institutions ofthe finance sector. Leadership is required to establish acollegial relationship that will enable housingfinance to flourish. Ifhousingfinance can not succeed, it is unlikely that otherforms oflong-term lending candevelop.

SRMPPag.2

A lack oflong-term lending is a mark ofan undeveloped economy. In Pakistan,the structure ofalmost all debt is short-term. Such debt is inherently volatile,with negative consequencesfor the economy and itsfinancial institutions. Thereis a ''mis-match'' between the need to develop the fundamental infrastructurenecessaryfor economic growth and the finance sector's ability to structureinstruments and modalities to provide the long-term credit necessary to createsuch infrastructure.

The ,Urban Context

Much ofthe impact ofthis mis-matchfalls on the urban sector. Evidencefrommany countries shows that most new economic growth takes place in urbanareas, which already contribute more to GNP than does agriculture. Finance isnot the only area ofthe housing sector that needs reform and growth. Even acasual glimpse ofPakistan's urban centers reveals severe shortfalls ininvestment in roads, water, sewerage, power, transportation,telecommunications, and maintenance ofinfrastructure. Pakistan's urban sectorfunctions poorly and is an extremely weakframeworkfor economic growth.

Although the focus ofthe SRMP was on housingfinance, the linkages betweenthe housingfinance sector and the broader urban sector are obvious and strong.Infrastructure is the skeletonfor urban development; housing provides much ofthe visible physical environment ofthe urban setting. Because the SRMP was afinance program with a strong interest in housing, it documented urbanconditions at the same time that it attempted to stimulate housingfinance.Throughout this report, a number, ofphotographs are presented to illustratePakistan's urban setting and provide an urban context in which housingfinancewill develop.

Improving the conditions in which people live requires creating awell-functioning urban sector. A well-functioning housingfinance sector willstimulate housing improvement, but, ultimately, expansion ofhousingfinance tothe point where it can meet the needs ofthe vast majority ofPakistanis mandatesthat urban planning, administration, andfinance be strengthened greatly.

The table that follows, adaptedfrom the World Bankpolicypaper titled''Enabling Housing Markets to Work, "presents a series ofpolicy strategies thatshould be adopted to make Pakistan's housing sector perform adequately andmeet the housing needs ofthe country. Taken together, the strategies make up anoverall policy that would enable Pakistan to develop a well-functioning housingsector.

SRMPPage3

'I...

Enabling Pakistan'sThe DO's and DON'Ts

Po/icy Area: Mortgage Finance

DO:

• Allow the private &ector to lend.

• Encourage competition in mortgagelending.

• Ensure lending i& at po&itivelmarket rate&.

• Enforce foreclo&ure law& and debtrecovery mechani&ms.

• Ensure prudential regulation.

• Introduce appropriate and&tandardizedloan in&trument&.

DON'T:

• Allow interest·rate &ubsidies.

• Neglect or disadvantage resourcemobilization.

• Allow high default rate:;.

• Di&criminate again&t rental housinginvestment.

DO:

Policy Area: Property Rights

DON'T:

• Regularize land tenure.

• Expand land regi&tration.

• Privatize public hou&ing &tock.

• E&tabli&h effective property taxation.

• Make land titling expensive.

• Di&courage land transactions.

• Engage in mQ3& eviction.

• Nationalize land.

DO:

• Make &ub&idie& transparent.

• Target &ub&idie& to the poor.

• Sub&idize people, not hou&e&.

• Regularly review sub&idie&.

SRMPPage4

Policy Area: Subsidies

DON'T:

• Build&ubsidized houses.

• Allow hidden &ub&idies.

• Let &ubsidies di&tort prices.

• Use rent control tu a sub&idy.

Housing Market to Workof Housing Policy

Policy Area: Infrastructure

-

DO: DON'T:

• Neglect infrastructure investment.

• Use environmental concerns as a reaSonta clear slums.

• Coordinate land development.

• Emphasize cost recovery.

• Ba.~e provision on demand.

• Improve slum infrastructure.

Policy Area: Land and Building Regulation

DO:

• Reduce regulatory complexity.

• Assess the cost o/regulation.

• Remove price distortions.

• Remove artificial shortages.

DON'T:

• Impose unaffordable standards.

• Maintain unenforceable rules.

• Design projects without links toregulatory and institutional refoml.

DO:

Policy Area: Building Industry

DON'T:

• Eliminate Monopoly practices.

• Encourage small-firm entry.

• Reduce import controls.

• Support building research.

• A ilow long permit delays.

• Inhibit competition.

• Create or maintain public monopolies.

• Delay p'o\';.rion ofinfrastructure.

DO:

Policy Area: Housing Policy and Institutions

DON'T:

• Balance public and private roles.

• Create aforum/or managing the housingsector as a whole.

• Develop enabling strategies.

• Monitor sector performance.

.' Engage in direct public housing delivery.

• Neglect a role for local government

• Retain financially unsustai,.al,leinstitutions.

SRMPPage5

Executive SummaryThe Government ofPakistan has authorized theestablishment ofa private sector housing financesystem. As a contribution to the new system, the StateBank of Pakistan (SSP) will set up a Housing RefinanceFacility within tht') SSP to provide liquidity in theamount ofRs. 450 million to the housing financecompanies (HFCs). The provision of these funds to theHFCs will permit them to make more mortgage loans,which in turn will improve their financial condition andgive them room to grow and profit over the short run.

It is not intended, however, that the HousingRefinance Facility will resolve all the HFC'sfinancial resource problems. In the long run,only through the mobilization of savings,coupled with the development oflocal capitalmarkets, will adequate resources be generatedto meet the housing finance need. •

The purpose of this report is to assess the needand prospects for the growth and developmentof the nascent housing finance sector inPakistan. It discusses the resource mobilizationissues and the problems the sector mustovercome to ensure a sufficient flow offinancial resources to meet the overwhelmingneed for housing.

The ramifications of the State Bank ofPakistan's approval to use $IS million inHousing Guaranty funds to establish a HousingRefinance Facility within the SBP arediscussed and suggestions are made on howthis Facility would operate to provide someneeded liquidity to the sector.

The report takes into consideration theconcerns of the monetary authorities and thehousing fmance companies, particularly as

regards the integrity of the system and themobilization of resources.

Finally, the paper explains how the sectormight be structured to ensure its success,including the possible role of a centralorganization to regulate as well as provideliquidity to the sector.

The structure of the new private housingfmance sector in Pakistan is predicated on thefollowing principles:

• that the propensity to save within thedomestic economy is enhanced as a resultof an increase in the flow of fmancialresources and a concomitant increase inmortgage loans;

• that the increase in resources reflect realmark.up rates, and that governmentsubsidies will not be required to mobilizethese resources; and

• that the instruments and institutionsthrough which these resources flow will laythe groundwork for a capital market insecondary mortgages.

In the longrun, onlythrough themobilizationofsavings,coupled withthedevelopmentoflocalcapitalmarkets, willadequateresources begenerated tomeet thehousingfinance·need.

SRMP Page 7

I

J

.. :~'

A refinancefacility atthe State

Bank isafirst step

towardeventual

developmentofa

secondarymarket in

housingfinance.

Similarly, the State Bank of Pakistan needsassurances:

• that the companies comprising the housingfmance system be fonned of individualsand groups of the highest integrity, so as toassure the public and the monetaryauthorities that the companies will fulfillhonestly their commitments to the savingand borrowing public;

• that the companies are properly managed,and are taking necessary safeguards toassure that assets and liabilities arereasonably matched and that depositors'funds are protected.

The State Bank ofPakistlUl recognizes theimportance of housing fmance in the overalleconomic context. It understands the need tonurture these housing finance companies sothat they can fulfill the promise of providinghousing finance to the people. Moreover, theSBP is aware that the development of thehousing fmance system offers a uniqueopportunity to demonstrate how a newfmancial group should be organized, regulatedand supported, since the very newness of theHFCs pennits the SBP to start out with a cleanslate. Thus, this learning experience can benefitthe entire fmancial sector.

ike propensity to save withinthe domestic economy isenhanced as a result ofanincrease in the flow offinancial resources and aconcomitant increase inmortgage loans.

This communality of interests between thecompanies and the SBP presupposes a closeand almost collegial relationship. Thecompanies must be open with the SBP, eveninsisting that the SBP make on-site inspectionsof the companies so that they will be betterable to comply fully with the PrudentialRegulations. The SBP should assign at leastone full-time agent to regulate the companies,who would spend time with the companies

SRMPPage8

learning about their problems and theirbusiness operations.

There should be periodic and, in fact, frequentmeetings and exchanges of wfonnationbetween the State Bank and the HFCs,recognizing that the more they know abouteach otht1', the more they will understand theother's needs and problems. An environmentof trust must be created. But if this newdirection is not taken, then an "us versusthem" attitude will prevail, with the resultbeing similar to the strained relationship thatappears to exist between the SBP and otherfinancial institutions in Pakistan.

The communality ofinterestsbetween the HFCs and theState Bank presupposes aclose and almost collegialrelationship.

An environment oftrust mustbe created-without this trustan "us versus them" attitudewillprevaiL

It is important for the HFCs to recognize thatthe Government of Pakistan is in the process ofmodifying and refming its tiscal and monetal)'policies. These changes are due in large part toa need to refonn its fmancial sector to fulfillcommitments to the IMF and the World Bank,as well as a recognition that the governmentdeficit has to be restrained. As a result, the oldsystem offmancial advances, subsidies,guarantees and outright favors are beingcurtailed and in some cases eliminated. Thismeans essentially that the HFCs will not be thebeneficiaries of the same kind of treatment thatother financial institutions had when theyinitiated operations. This does not mean thatthe HFCs are being treated unfairly; it is justthat the rules have changed. The HFCs mustrecognize and accept this fact.

The immediate next step to enhance the growthof the housing finance system in Pakistan is for

the State Bank to activate the HousingRefinance Facilitv, which is discussed in detaillater in this paper. The SBP must fonnallyissue the rules and regulations for the HFCs togain access to this Facility. At the same time,the Ministry of Finance must enter the UScapital market to borrow the Housing Guarantyfunds. The State Bank should aim to open thisFacility no later than July I, 1994.

Government regulations now pennit housingfmance companies to accept savings accounts,essentially Certificates of Investment with a 30day or more maturity date. Concurrently, theState Bank should consider the question of theHFCs being authorized to accept foreigncurrency accounts, and if approved, it should

. issue a circular to this effect, again no laterthan July I, 1994.

These two actions by the State Bank will give areal as well as a psychological boost to thehousing fmance sector. It will show that theGovernment supports the sector, and just asimportantly, it will not result in any cost to theGovernment. In fact it will be a benefit to theGovernment insofar as it will allow theGovernment to tap a very inexpensive sourceof foreign currency, the Housing Guarantyfunds. In addition, this action will encourage

the other groups to carry on with the necessarysteps to obtain their licenses to do business ashousing fmance companies. Finally, theGovernment should consider a number of taxrelated incentives to encourage savings, topromote home lending and to strengthen andenhance the financial soundness of the HFCs.

While the State Bank goes ahead with its plansto open the Refmance Facility, the HFCsshould continue with their efforts to mobilizefinancial resources utilizing those avenues nowavailable to them. Either individually orjointly, they should explore the possibility ofdesigning and utilizing some sort of specializedsavings-linked mobilization program such as aContract Savings Scheme. This woulddemonstrate to the State Bank that the HFCsare very serious about the need to mobilizedomestic savings and are fully aware of theirresponsibilities in this matter.

These schemes would include both the use offoreign currency accounts and rupee basedaccounts. The HFCs should committhemselves to devising at least onecomprehensive savings-linked scheme by JulyI, 1994. At the same time, one or more HFCshould begin to issue Certificates of Investmentto mobilize domestic savings.

A vibranthousingsector isessential tothe economyand criticalto people'ssocial andeconomicwell-being.

A well-functioning housingfinance system requires:

• An operational and regulatory framework

• Financially soundprimary lending instiuRons

• Ready access to capital and sources ofliquidity

• A government that supports and nurtures the system

• A free market environment with real mark-ups

• A legal system that enforces lender rights

• Financialprograms to provide housing to the poor

• A realistic and dynamic housing policy

• A well-organized and active housingfinance constituency

• A levelplayingfield with otherfinancial institutions

SRMPPage9

Housing: The Good, the Poor,

Katchl Abadl••/onlla/ow river bank In K.,.chl. Condemned to lIfe In fir. "ood plain, low·lncomepeople f.ce dl...,.,when rite river .we". with .the .nnual ,.In..

".'eIJ., hou...0' the prlveleged In la/em~bad. ".,." dlacemabl. In tit. foreground a,. tlte mud andtltatch huta 0' tlte I... fotfUnete (photo coul'te8y of"aul 8. Mecerllley).

SRMP Page /0

and the Ugly

11

'.:'.',.,' ",'

A housing conatructlon proj.ct of th. Kar.chlDevelopmentAuthority. TIre pUblic aector's directInvolv.ment In I.nd d.v./opment h.. thw.rted thedevelopment of th. prlv.te a.ctor, consum.dsc.rc. public sector ...aouree., .nd I.d to highlysp.cul.tiv.'.nd marle.ta.

N.w multJ-atory "ata In th. poah Clifton SNcha,.. ofKa,.chl.

A Katchl Abadla/onga main ,./lway trackIn Ka,.chl. Th.s.a.ttI.m.nD .,. aP'Oduct of",pldurlJan growth and apubllc...ctordominated houa/ngd.llveryayatem that "la unabla to m.etd.mand•. Although '"th... encroachm.ntaa,. tacitly to/ereted'by GovWnrn.nt~n'· '.' .th. a.na. th.t th.ya,. gen.,.IIy I.ftund!aturbed-m.,.,y

,do.not,hav. ,cc",ato"'th. ",un,ti,,,., .a.tv/caa- g..,electric, water, .mlunltatlon-that the....t of th. community,

.. ...iiiiiii iiiiiiiiiiiiiiiiiiiiii_iiiii_iiiiiiiiiiiii =~ at la",• • njoya.

• I· ~:.. ' ...~.-, •••

~. I.t :. ~\. "'~"'.

. .'~::." .',

" .••• ~! :;'...

SRMP Page 11

Background

Housing Finance in Pakistan

Over the last several years, Pakistan has been In theprocess of establishing a market-based housingfinance system. The potential economic and socialInfluence of this system Is enormous and Is closelylinked to Pakistan's capability for economic success.Many Issues face housing finance In Pakistan; noneare more Important, more critical, or more Immediatethat the development ofmortgage lending as anIntegral component and substantial feature of thefinance sector.

,After years of gestation, in a quiet, persistentand deliberate fashion, a new type of privatefmancial institution was born in PakistaJi. Itwas created in a time of turmoil, whengovernments were changing, fmancialinstitutions were failing, and there wasincreasing doubt as to whether another type offmancial institution was really necessary.

But there were a few business people-lookingto the future and willing to take a chance-whorealized that Pakistan desperately neededhousing and needed to look at new ways tofmance that housing. Similarly, there werethose in government who realized that acounby like Pakistan could not afford to let thehousing situation continue as it had been.

What was it that drove these business peopleand government officials to join forces increat~g this new fmancial system? First, it wasclear that the supply of standard, affordablehousing was not meeting an overwhebningdemand, and that in fact, the housing situation

was deteriorating. While financial assistance inthe fonn ofsubsidized loans was beingprovided through the House Building FinanceCorporation (HBFC) and developed plots weresupplied by local development authorities andprovincial bodies, this was far from sufficient.In light of the reduction and eventual cut-off inthe supply offresh funds to the HBFC, homelending from the public sector was drying up.Accordingly, most families were still forced toaccumulate sufficient cash in hand to purchaseor build a home in private sector developments.Long-tenn housing fmance, the key to awell-developed housing sector everywhere inthe world, was still not available to the vastmajority ofPakistanis, regardless of income.

The huge gap between the supply and thedemand for housing, they realized, was dueessentially to the chronic shortfall in theavailability of sufficient fmancing at affordabletenos. Only the private sector could mobilizethe necessary fmancial resources to meet thedemand for housing. The creation of a new and

Benefits ofastrongmarket-orientedhousingfinancesystem:

• more andbetterhousing

• astrongerconstructionindustry

• improvedsavings rateand greaterinvestment infIXed capital

• creditflowingat market ratesand accordingto demand

• a broader anddeeperfinancialsector

..

.Previous Page BialikSRMP Page J3

Economic Benefits ofa Housing Finance System

A rupeeinvested in

housinggenerates

two rupees ofinvestment in

relatedsectors. A

job createdin housinggenerates

twojobs inrelated

sectors.

viable housing finance system that could meetthis demand was the right way to proceed;further delays would only exacerbate thehousing situation. The time to act wasripe-and they acted.

A private sector housing fmance system is nowfun<;tioning mPakistan. Two oompanies arelicensed and making mortgage loans, a thirdcompany is expected to start-up in a matter ofweeks, while four other groups are waiting inthe wings.

Yet as these companies have becomeimmersed in resource mobilization efforts and

The benefits to be derived from an active andvibrant housing sector are clearly evidentbecause investments in this important sectorgive rise to multiplier effects throughout theeconomy.

Studies in a number of countries have shownthat for each unit ofcurrency-in this caserupees-invested in housing, about two rupeesof additional economic activity are generatedin other sectors. While this multiplier effect inhousing is not much different from investmentsin other sectors, benefits from the housingsector are spread throughout theC('.()nomy-nearly all economic sectors arcaffected by investments in housing.

A second major argument for housing is itseffect on employment. In all countries,regardless of the level ofdevelopment, theemployment ofone worker in the constructionsector, including housing, will generate abouttwo additional jobs in other sectors. Byinvesting in the housing sector, thecombination of these twolinkages-investment andemployment-provide a broad stimulus to theeconomy. But the reverse is also true.Continuing to neglect the housing sector wiDhave a lingering and negative impact on theeconomy ofPakistan which wiD be felt weDbeyond the sector itself.

SRMPPageU

mortgage lending operations, the magnitudeand complexity of the task they haveundertaken has become clearer. A housingfmance operation, which requires hugeamounts of funds to be loaned for thelong-tenn, is quite unlike IlIlY other type offmancial activity.

The Oovernment, which supports the newhousing fmance system, has also begun torealize the uniqueness ofhousing fmance. It isin this context that a blueprint is presentedwhich both the housing companies and thegovernment can make use of to guide thehousing fmance system to success.

The housing sector has a significant impact onsavings in a variety of ways. Without doubt,the possibility ofpurchasing or building ahome is a major incentive for nearly allfamilies to save. This is particularly trueamong large segments of gainfully employedmiddle income workers, whose prospects forever purchasing Ii home are limited due to lackofmortgage fmance, high prices, and littleincentive to save.

Ifhousing fmance is made available ataffordable prices, then it has been shown inmost countries of the world that families willincrease their savings in order to accumulatethe required up-front capital contribution toqualify for a mortgage loan. There is no reasonto believe that the situation is any different inPakistan.

Proofof this propensity to save for housing isreflected by comparing different bousingfmance systems. In Oennany and France,where contract savings schemes arcresponsible for a large percentage of funds forhousing fmance, mortgage loans as apercentage of OOP are 33 and 35 percentrespectively, which reflects the need for apotential borrower to save a large amount ofthe price of a house to qualify for a mortgageloan. Often families in those two countriesmust save about one-third of the cost of the

--:;

The Missing Ingredient: A Housing Finance System

home, with the remaining two-thirds consistingof a mortgage loan.

In the US and Denmark, however, wherecontract savings schemes do not exist, and highloan-to-value mortgages are common,mortgage loans as a percentage of GDP aremuch higher, 47 and 44 percent respectively.In these two counbies, 80 percent and higherloan-ta-value mortgages are standard,indicating that savings is a less importantfactor in purchasing a home (see Appendix Bfor country comparisons ofhousing financesystems). This analysis clearly shows howsavings can actually increase when there is theopportunity or the requirement to save in orderto purchase a home.

Another aspect of savings relates to therelationship between savings and the price ofhousing. Although empirical evidence islimited, it has been argued that as the price ofhousing rises, savings decline, and visa versa.Housing prices frequently rise because thesupply ofhousing does not meet the demand ofa growing population with increasing means toacquire that housing. And the reason why thesupply is not increasing is because of a lack ofhousing fmance resources to facilitate the ..purchase ofhousing. Thus, an adequate supplyofhousing finance will lead to an increase in

"l

Pakistan's private sector housing fmanceindustly is clearly in its infancy. Over the pastfive years, The U.S. Agency for InternationalDevelopment, through its Shelter ResourceMobilization Program, has assisted theGovernment to begin establishing amarket-based housing (mance system. To date,two housing finance companies (lIFC) havebeen licensed and begun operations.

But even as these companies start to makemortgage loans, it is obvious that there are stillmany hurdles to overcome if they and thecompanies to folJow are to succeed asspecialized housing (mance institutions, muchless meet the needs of millions ofPakistanisfor housing finance.

the production ofhousing, lower prices and aconcomitant increase in the rate of savings.

The llvailability ofhousing finance willfrequently lead to better use of personalsavings by fllQilitating alternative investmentsin other (r.()nomic sectors. The argument here,which is clearly relevant to Pakistan, is thataccess to a long-term mortgage loan willpermit the borrower to make an alternativeinvestment in a business opportunity ratherthan use savings to fmance a home. In thisway, new investment and employment aregenerated, which is beneficial for both thepeople and the economy ofPakistan.

Access to housing (mance will lead not only toan increase in the rate of savings and in theproduction ofhousing, but it will result in thegrowth ofhome ownership. Over time, theequity accumulated in a personal residence willbe the 1I0urce of capital many entrepreneurs useto initiate new businesses, many ofwhich willbe small businesses, which are the incubatorsofemployment. While this general use of homeequity for business pwposes is probably someyears away in Pakistan, the creation of ahousing (mance system today will acceleratethe time when enterprising business people canseize this unique fmancing opportunity.

The institutional framework for housing(mance in Pakistan consists essentially of twoand. shortly, three privately owned housing(mance institutions and a sector regulatoryfunction which is housed in the State Bank ofPakistan. The Ministry ofFinance licenses thehousing (mance companies, although thisiunction is expected to be transferred to theState Bank ofPakistan at a later date.

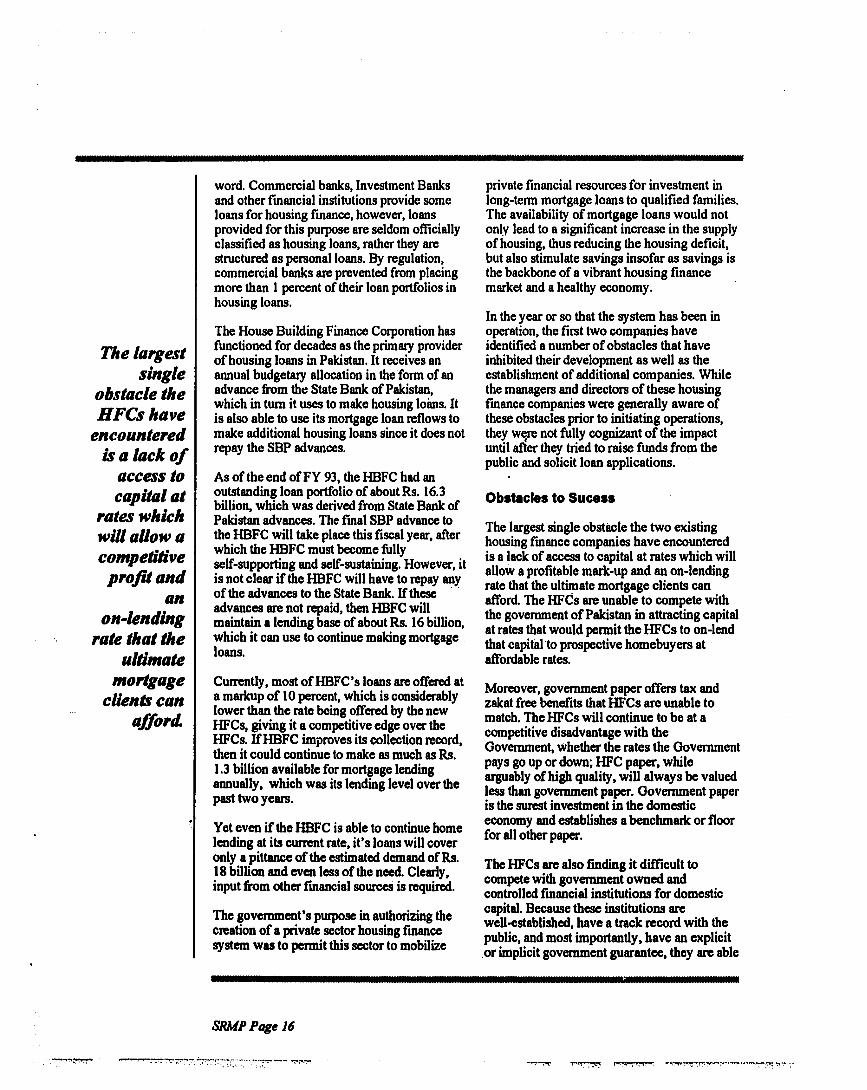

The HBFC

A state-owned financial institution, the HouseBuilding Finance Corporation, makes housingloans with funds channeled from the StateBank ofPakistan, but it is not a housing(mance institution in the true sense of the

SRMP Page 15

An adequatesupply of'sousingfinance willlead to anincreoseintheproduction ofI,ous;ng,more valuefor price, awider rangeofchoice,and aconcomitantincrease inthe rate ofsavings.

The largestsingle

obstacle theHFCshave

encounteredisa lack o!

access tocapital at

rates whichwillaUowacompetitive

projitandan

on-lendingrate that the

uldmatemortgage

clients canafford.

word. Commercial banks, Investment Banksand other fmancial institutions provide someloans for housing finance, however, loansprovided for this purpose are seldom officiallyclassified as housing loans, rather they arestructured as personal loans. By regulation,commercial banks are prevented from placingmore than I percent of their loan portfolios inhousing loans.

The House Building Finance Corpomtion hasfunctioned for decades as the primary providerofhousing loans in Pakistan. It receives anannual budgetaIy allocation in the fonn of anadvance from the State Bank ofPakistan,which in tum it uses to make housing lolms. Itis also able to use its mortgage loan reflows tomake additional housing loans since it does notrepay the SBP advances.

As of the end ofFY 93, theHBFC had anoutstanding loan portfolio of about Rs. 16.3billion, which was derived from State Bank ofPakistan advances. The fmal SBP advance tothe HBFC will take place this fiscal year, afterwhich the HBFC must become fullyself-supporting and self-sustaining. However, itis not clear if the HBFC will have to repay anyof the advances to the State Bank. If these .advances are not repaid, then HBFC willmaintain a lending base of about Rs. 16 billion,which it can use to continue making mortgageloans.

Currently, most ofHBFC's loans are offered ata markup of 10 percent, which is considerablylower than the rate being offered by the newHFCs, giving it a competitive edge over theHFCs. IfHBFC improves its collection record,then it could continue to make as much as Rs.1.3 billion available for mortgage lendingannually, which was its lending level over thepast two years.

Yet even if the HBFC is able to continue homelending at its current rate, it's loans will coveronly a pittance of the estimated demand ofRs.18 billion and even less of the need. Clearly,input from other fmancial sourceS is required.

The government's purpose in authorizing thecreation of a private sector housing fmancesystem was to pennit this sector to mobilize

SRMPPageJ6

private financial resources for investment inlong-tenn mortgage loans to qualified families.The availability of mortgage loans would notonly lead to a significant increase in the supplyof housing, thus reducing the housing deficit,but also stimulate savings insofar as savings isthe backbone of a vibrant housing financemarket and a healthy economy.

In the year or so that the system has been inoperation, the first two companies haveidentified a number ofobstacles that haveinhibited their development as well as theestablishment of additional companies. Whilethe managers and directors of these housingfmance companies were generally aware ofthese obstacles prior to initiating operations,they were not fully cognizant of the impactuntil afier they tried to raise funds from thepublic and solicit loan applications.

Ob.taeles to Sue•••

The largest single obstacle the two existinghousing fmance companies have encounteredis a lack of access to capital at rates which willallow a profitable mark-up and an on-lendingrate that the ultimate mortgage clients canafford. The HFC:s are unable to compete withthe government ofPakistan in attracting capitalat rates that would pennit the HFCs to on-lendthat capital'to prospective homebuyers at .affordable rates.

Moreover, government paper offers tax andzakat free benefits that HFCs are unable tomatch. The HFCs will continue to be at acompetitive disadvantage with theGovernment, whether the rates the Governmentpays go up or down~ HFC paper, whilearguably ofhigh quality, will always be valuedless than government paper. Government paperis the surest investment in the domesticeconomy and establishes a benchmark or floorfor all other paper.

The HFCs are also fmding it difficult tocompete with government owned andcontrolled fmancial institutions for domesticcapital. Because these institutions arewell-established, have a track record with thepublic, and most importantly, have an explicitor implicit government guarantee, they are able

to attract fmancial resources at more favorableterms than the new HFCs.

It can be said that the new housing fmancesystem is paying the price for the failure of theGovernment ofPakistan to regulate and controlother fmancial ore.anizations, which, in thepast, have frequently mismanaged their fundsand or defrauded the public. the latest being thefmance cooperatives. The public is rightlywary to put their trust once again in a new typeof institution. Thus the HFCs are unable tocompete for funds from the "pure" savers, thatis, savers that are simply looking for thehighest return while at the same time seekingto place their money in the safest institution.

The NewHFCs

On the other hand, the pedigree of the newhousing fmance companies is impeccable. TheMinisby ofFinance chose to authorize only themost credible of the applicants to completeapplications for a housing fmance license,ultimately authorizing only seven of the 24groups to proceed. The result has been theincorporation and licensing ofa stellar groupofhousing finance companies, headed by thetwo institutions now operating. Citibank .Housing Finance. owned fully by its worldrenowned parent, and Intemationll1 HouliingFinance Limited, among whose owners areInternational Finance Corporation,Commonwealth Development Corporation,PICIC and Cresbank, represent the highest typeof institutional credibility.

It is clear that these institutions typify the levelof integrity so necessary to provide the generalpublic and government regulators withconfidence in the system. Yet they still havebeen unable to devise instruments which wouldpennit them to compete effectively with otherparts of the banking sector. To use a commoncliche, the playing field is still not level.

To date, the two operating institutions aremaking some housing loans, utilizing theirequity capital as the source of lending funds.When this source has been fully committed tomortgage lending, they may be able to accesstheir parent companies for additional funding,either in the fonn ofequity or loans.

However, these funds are expensive, since theparent compames must on-lend at rates thatthey would ordinarily make for competinguses. They are a limited resource since theparent companies are not set up to providelong-tenn loans to subordinate companies.

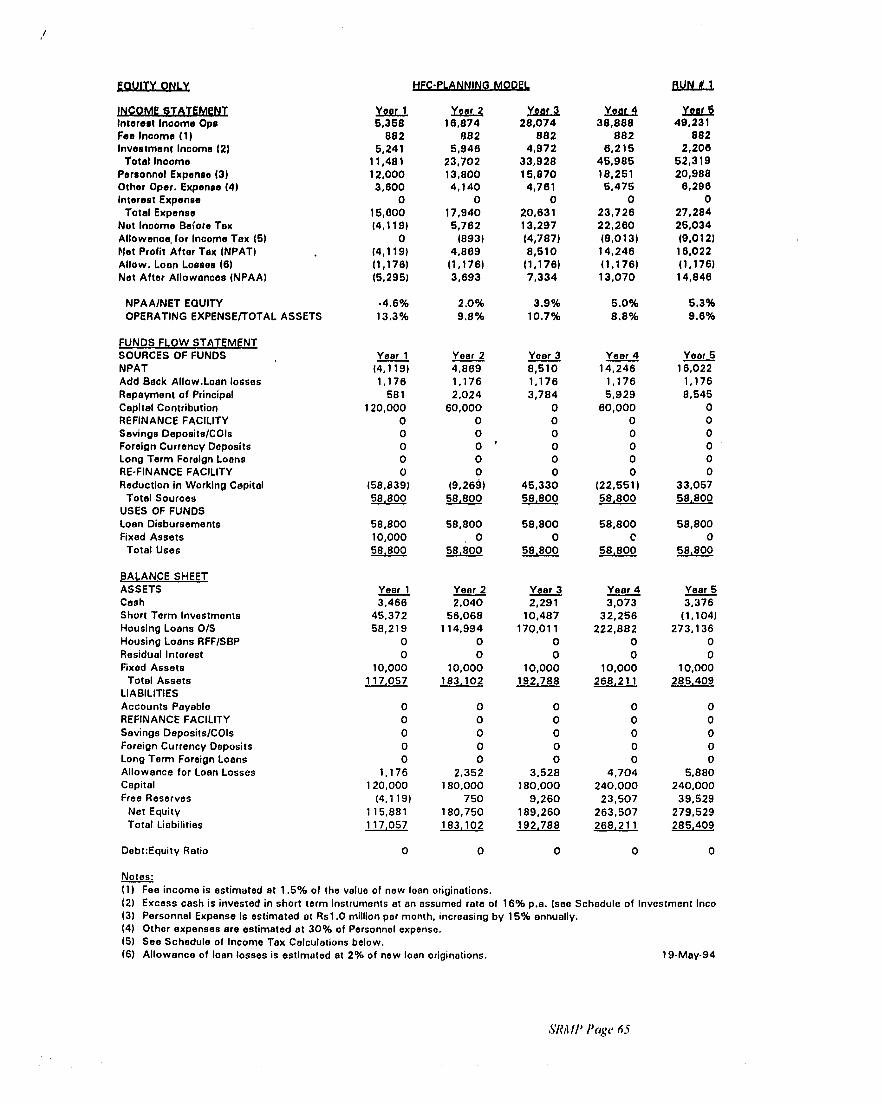

Besides. this defeats the purpose for creatingthe housing fmance system in the flI'st place:remember that the purpose was to mobilizenew financial resources from domestic marketsfor on-lending for housing. Moreover, lendingfrom an equity base alone is not a viablebusiness. as illustrated in the computer-basedsimulations in Appendix A.

Housing Afford.bUlly

A limited amount offunds coupled with theirhigh cost means that the market is restricted toborrowers in the higher income. brackets. A Rs.300,000 mortgage loan at 20 percent for 12years requires a monthly payment of about Rs.5,500, a payment that only a small percentageoffamilies can afford to make. To qualify forthis mortgage loan, which is sufficient tofmance the purchase or construction of a basichousing unit, a family must have a monthlyincome in the Rs. 16,500 range.

But, quoting a 20 percent markup on long-termloans appears to discourage prospectiveborrowers. The HFCs have been dismayed tosee highly qualified borrowerswalk away fromloan application interviews either because theycannot afford the high markup loans or becausethey are reluctant to take on relatively high costdebt.

There are a number ofways to mitigate thedamage high markups have on the mortgagemarket, not least being the use of adjustablerate mortgages. One of the most successful inrecent years is the Dual Index Mortgage, whichis very effective in countries with moderateinflation.

While such mortgages are not allowed inPakistan now, the continuation of highmarkups would warrant future consideration ofthe problem of affordability. The use of DualIndex Mortgages in inflationary economies isdiscussed in Appendix C.

SRMP Page 17

The presentHFCstypifythe level ofintegritynecessary toprovide thegeneralpublic andgovernmentregulatorswithconfidencein thehousingfi~lance

system.

1MW'

Children and

. ,-'

Children pIe"ngln nlbbl.h hNp. along theRiverL.,." In K.rachl.

A boy In a Katchl Abedl..t In ",.h.rtof.",.cap'.' city of"'amabad. Approx/me"'y 1100child,." undera". five dl••ve". dey.l" "a".n .~. .(World Benlf. 1"'). lIajor ifill ofyoungchIld,." .,.die"".., dl Immunlzebl.dl....... ecute rupI...toty Infect/OM .nd' m.'nuttlt#on (photo cou"'yof".u/8.lIacartn.y).

A hom wom.n and herchild,." Iy/"gln a.... .. K....chl Th.y recently m/greted from

A child,.,,'. petit, pattof. privete club In Defenc. punjab Provine. In tit. hope of findIng work.Houelng 'oclely In K.NeItI. lloat child,." hw. Rapid populet/on IIfOwth .nd I.c/( ofemploymentno acceu to fflcllHl. oftitle eort. opportunHl. hev. contributed to 'nc",.'ng urbe"

dec.y.

; ..."' ••.. ,,..:r ...... -.•

"'~':":''''I>:' :.

the Urban Environment

Young boys In en Oren'" Town engln.erlngworlcahop. Deaplte laws to the confrll'Y, childlebor Is ".,.,..lve/n Pald_n.

Th. grip ofpovertyend ./e~1e ofhousingfore.. "'mlll.. toIlv• ..sque"'n Inmale..hlff110m...TIl... lIuta» tucleedbehind upper-e/...lloualngln Kanchl,eiw med. frOm palmfrond.. reed

. matl/ng, cloth,dlscerded cnta,

;end othwselvegfKl ..meterle/.. Leclc of .educetlorr end theconaumlngatnJlIfiII. of.y~aysurvlvelI...,.th...children with IIttl.hope or opportunityfore b.tter "fe.

Fortunete children ofmlddle/ncom. femlll••running hom. from school. In 1885, the Gro..Enrollment Retlo In Prlmery School. was..tlmeted et..." (World Senle, 1882). "enyconalder .ven th... /ow "gu,.. to b. Inflated.

SRMPPageJ9

...

, ' ....... ,:.

Structuring the Housing FinanceSector

To gain the economic, financial, and social benefitsrelated to having a vigorous housing sector thatproduces the housing people can afford, the housingfinance system in Pakistan must have awell-functioning regulatory environment, a supportivepolicy environment, and a strong housing constituency.

The structure ofPakistan's housing fmancesector is predicated on the following principles:

• that the propensity to save in the domesticeconomy is enhanced by an increase in theflow of fmancial resources and aconcomitant increase in mortgage loans;

• that the increase in resources reflect realmark-up rates, and that governmentsubsidies are not required to mobil~e

these resources; and

• that the instruments and institutionsthrough which these resources flow willlay the groundwork for a capital market insecondary mortgages.

Similarly, the State Bank ofPakistan and theMinistry ofFinance need assurances:

• that the companies comprising the housingfmance system be formed of individualsand groups of the highest integrity, so as toassure the public and the monetaryauthorities that the companies will fulfillhonestly their commitments to the savingand borrowing public.

• that the companies are properly managed,and are taking necessary safeguards toassure that assets and liabilities arereasonably matched and that depositors'funds are protected.

Finally, the housing fmance companies needthe support and the intervention of Governmentto fulfill their mandate. The HFCs cannotoperate in an environment where they do nothave equal access to resources and the equalopportunity to compete for those resources. Ifthey do not have this access, then theGovernment must intervene in the market toassure the flow of resources to the HFCs. Thisassumes, further, that the Government wishesto have a viable housing finance sector and theHFCs meet the Government's standards ofperformance. Specific industry-wide incentivesthat the Government ofPakistan may wish toconsider are discussed in further detail later inthis paper.

_____K......ey Elements

SaVings Aspects

Earlier in this paper, the importance of housingwithin the economy and the relevance of astrong housing fmance sectoT in generatingdomestic savings was discussed. While there isno assurance that domestic savings will growthrough the development of the housingfinance sector, there is enough evidence todemonstrate that there is a strong relationshipbetween a buoyant housing finance system andthe rate of domestic savings. It is also clear that

II

HFCsneedasupportivei,olicyenvironmentwhere theyhave equalaccess toresources andthe equalopportunity tocompete/orthoseresources.

Previous Page Blank SRMP Page2!

There is noreal

guidance ordirection ofthe housing

sector, muchless the

housingfinancesector.

There is nowritten

nationalpolicy, nor is

there ancentral

agency thatis

articulatinghousing

policy,written orotherwise.

as long as the housing fmance sector remainsin its infant stage of development, noappreciable increase in domestic savingsgenerated by this industry will oecur. Onlythrough the overa11 growth of the housingfmance industry witt savings increase and onlythe State Bank of Pakistan, with the blessingof the Ministry of Finance, has the capacity toensure the growth of the system.

Real Market Rate Tenns

Specific resource mobilization techniquessuggested in this paper wilt in no way requirethe SBP or any other government institution tosubsidize the HFCs in their efforts to attractfmancial resources (this does not preclude theHFCs from acting as conduits for funds orsubsidies that the Government of Pakistanmight direct exclusively to poor families whoare not the usual HFC clients).

If a saving mobilization program, such as aContract Savings Schemes as suggested in thenext section, is deemed feasible, savers may bepaid a lower markup on their savings becausein return they are being offered the opportunityofobtaining a housing loan at a predeterminedtime. This is not a subsidy.

HFC lending rates are determined principa11yby their cost of funds. Companies cannot makea decent return on capital if they do not lend atterms in excess of the cost of capital andoperating expenses. Thus it is not in thescheme of things for the private sectorfmancial institution to subsidize theirborrowers, nor as private sector institutions dothey intend to request subsidies to do so.

Secondary Markets

The development of the Housing RefmanceFacility (HRF) within the State Bank ofPakistan sets the stage for the eventual creationof a secondlUY market. It is impossible todetermine how this secondlUY market willdevelop or function. Nevertheless, thedevelopment of the Housing Refmance Facilitywithin the SBP is a necesSlU}' precondition forthe creation of a viable secondlU)' market. It isthrough the development of the HRF that the

SRMP Page 22

.iII

S9P and the housing finance system will gainthe necesslU)' experience to establish a truecapital market for mortgages.

The Regulatory Environment

The State Bank of Pakistan is rightlyconcerned about the safety of any funds itmakes available to refmance loans originatedby the HFCs, as is currently contemplated.However, this risk can only be mitigatedthrough a strong and we11-functioningregulatory process, which is the responsibilityof the SBP itself. The SBP has, or will haveshortly, the responsibility for:

• Licensing new housing finance institutions(The licensing function is now theresponsibility of the Ministry of Finance;however, the SBP will assumeresponsibility at a future date);

• Writing the Prudential Regulations forthese same institutions; and

• Enforcing the Prudential Regulations.

If the Non-Bank Financial Institutions Division(NBFI) of the SBP undertakes its responsibilityproperly, then the twin risks associated withinstitutional failure and mortgage default willbe minimal. Normally, it is when a regulatoryinstitution is lax, incompetent or subject togovenunent interference that problems arisewithin the regulatory system.

It is important, moreover, that the SBP be strictbut fair in carrying oUf. its regulatory functions.It should not be arbitrary in the licensing ofnew institutions. Instead it should let themarket determine how many and whichinstitutions the market can support. Ifattritionoccurs, it will not affect the operation of theHousing Refinance Facility in as long as theSBP holds a flfSt lien on the mortgagesprovided as security for its loans.

Housins PoI/cy__

There is no real guidance or direction of thehousing sector, much less the housing fmancesector. There is no written national housing

policy, nor is there an central agency that isarticulating housing policy, written orotherwise,

The National Housing Authority of theMinistry of Housing and Works is chargedwith the responsibility of preparing a nationalhousing policy. Apparently, such a policy hasbeen drafted, but it has not been approved orenacted by the Government. This policy dearthis being filled by what could be called animplicit housing policy, which could bedefined as follows:

• ~ousing assistance, such as subsidies, isdirected mainly to selected groups inPakistani society, such as the civil servantsand militarj' rersonnel;

• Minimal housing assistance is provided tothe segments of societ3' which are too poorto provide themselves with standardhousip:-'

• The putJli" :,' ~ . r :.., -i.,l1l; <;nance agencycontinues ") F. ' .;te 1'. "l: ,J thosesegmentr. ~ . SOl" ;t}. t!:&t • ,('; able to obtainhousing loans tiL'(i"~ ~nfh. Ice;

• Private sector hou;;;.ng fmalice institutionsare permitted, however barriers are put inthe way of mobilizing financial resources;

• Transfer and registration ofproperty,which inhibit the development ofmortgage markets, are discouraged

. through the imposition ofonerous fees andstamp duties;

• And fmally, a clear, concise housingpoli~y has not been articulated.

A more plausible and explicit policy, and onethat is generally in force :n countries that havevibrant housing sectors, include the followingelements, written or otherwise:

• Subsidies are only directed to groups thatare too poor to afford adequate housingsolutions;

• Adequate land regularization and propertytitling and transfer systems are in place tofacilitate housing development and are agovernmental priority;

• Mortgage f'nance is the responsibility ofthe privat~ sector, and the role ofgovernment is to facilitate the flow ofresources to the sector.

• The major role of government in theproduction of housing is to ensure that costrecoverable infrastructure is madeavailable to the populace at large;

• The government will articulate a housingpolicy that promotes the concept of freemarkets as the most effective way to meetthe housing need.

Both the implicit Pakistani housing policy andthe suggested explicit housing policy asdescribed above are too simplistic, however,they are representative enough to indicate thatwhat Pakistan does in the policy arena is farremoved from policies in countries withsuccessful housing programs. The problemsfacing the young housing fmance sectorprimarily result from an inadequate policy

.. environment in which they can functioneffectively. In the long run, the Government ofPakistan will have to develop a housing policy,including the fmancial elements within thatpolicy, that will create an environment wherehousing production blossoms. Until that day,the housing fmance sector faces an uphillstruggle.

. A Housing Const/tuencl!-The hOUStJlg iir.I!.!lI:·11 sector suffers from a lackoforgan!7..ed groups actively supportingimprovements in and the development ofhousing. This missing constituency sorelyhampers any efforts by the indi'/;dulll HFCsand their shareholders to bring about thenecessBJY legislative and regulatory reformsthat they deem to be neccssBJY for thewell.being of the sector. An important endrecent step in rectifying this situation was thenaming of a full-time SecretBJY General of theHousing Finance Trade Group. Through thisgroup and its SecretBJY General, the industrywill be able to speak with a single voice. Theindividual HFCs must strongly support thiseffort. The history of trade associations inPakistan and throughout the world shows thatthey wode for the good of all their membership.

SRMPPage23

The historyoftradeassociationsin Pakistanandthroughoutthe worldshows thatthey work forthe good ofall theirmemhership.

Urban Roads, Traffic

Children retumlng hm .chooletop • erowd.bu.. Serore th,. bu. I. con8ldwed full...ve,.,more P8a..g.,. will be h.nfllng 0" the ,..,ledd.,. Thl. I. P8rt1eul.rly huerdou. In thebumper to bumpe, ".me ofK.,.chl. Leho,.••ndP••hew.,.

F.lalR08d.the meln

ro.dto theQu.'d-e-Az.m

In,.",.tJonelAirport, .nd

one of theb••tfOMI.In

K.,.chl.

SRMPPage24

A cem.' ce" e.".,Ing. hNVy lo.d In the Defence.,.. ofKe'.chl. Sleycl... rlck.hew•••nd • v.,'eryof.nlmel driven c.". .h.re the roed with. wide.".y ofmotorized vehlel.. ".vellng.' high.pHd.. T'eme ,.,.IItJ.. In P.kl."n .,e .mungthe hlgh..t In the world.

,S4~:~ .:0;''::::• . .. III"

.-..,:'n":.... . , " .... '. • • t •

.: :! .::: .... ~....,

and Transportation

The condition ofmany roed.l. poor. Thl. photow.. teken n..r the Con.u/ate ofBang/ad..h InKarachi.

The a"'."ce ofem/u/on.tendard. and lack ofenforcement of motorvehicle regu/atJon. ha.re.ulted In Incr,,"nglevel. ofair pollutJon Inurb.n centeno The.verege vehicle InPalfl.ten emltll 20 tJm..more hydrocarbon., 25tim..more carbonmonoxide, and 3.8 tim..a. much nltrou. oxide asthe average vehicle Inthe United Ste,..(pakl.ten NatJonalCon.ervatlon Strategy,1882).

..:. ::',

With the e"ceptlon of'./amabad, where they areprohibited, motorized rlclcshaws are Ubiquitousf..ture. of the ur"'n landscape. Re/atJve top...enger carrying capaclty-among thelowe.t, and vehicle em/sslons-among thehighest, they a,. the most Inefficient vehicle. onthe road.

SRMP Page 25

Resource Mobilization Issues

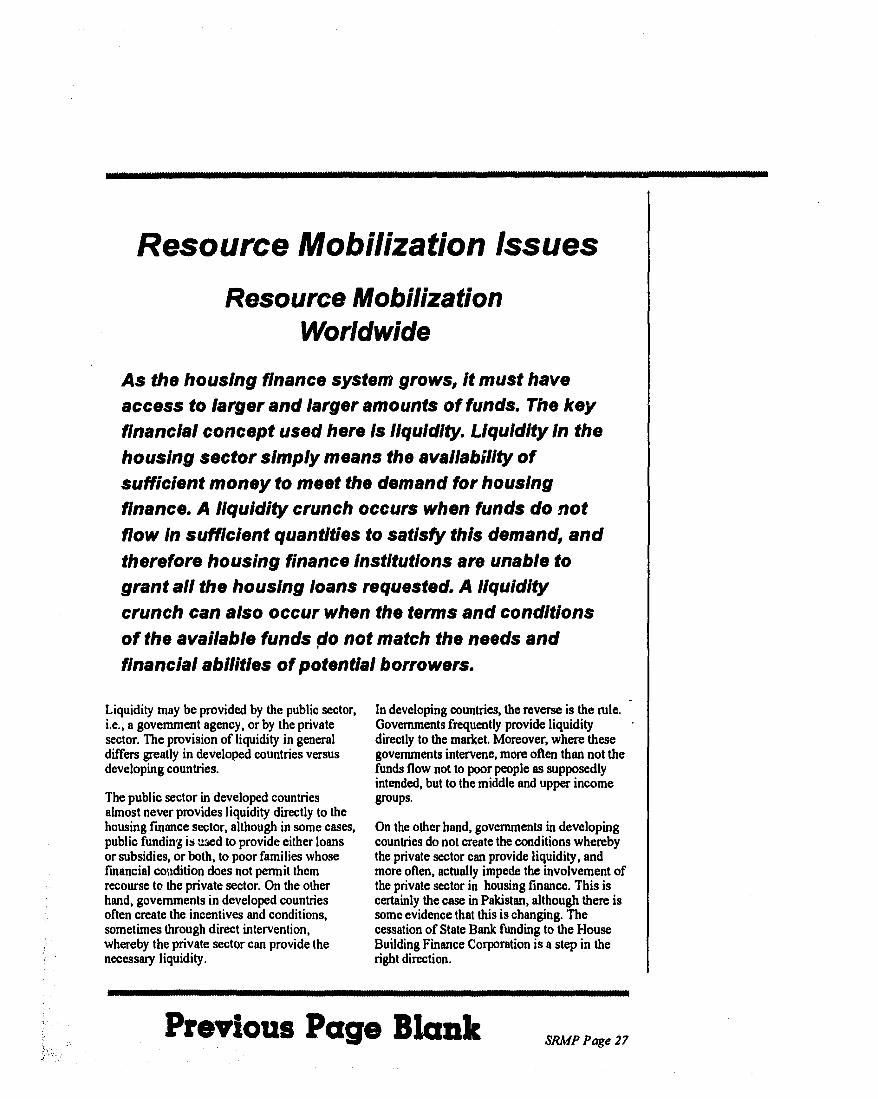

Resource MobilizationWorldwide

As the housing finance system grows, it must haveaccess to larger and larger amounts of funds. The keyfinancial concept used here Is liquidity. Liquidity In thehousing sector simply means the avallabUlty ofsufficient money to meet the demand for housingfinance. A liquidity crunch occurs when funds do notflow in sufficient quantities to satisfy this demand, andtherefore housing finance Institutions are unable togrant all the housing loans requested. A liquiditycrunch can also occur when the terms and conditionsof the available funds ,:10 not match the needs andfinancial abilities of potential borrowers.

Liquidity may be provided by the public sector,i.e., a government agency, or by the privatesector. The provision of liquidity in generaldiffers greatly in developed countries versusdeveloping countries.

The public sector in developed countriesalmost never provides liquidity directly to thehousing fmance sector, although in some cases,public fundin'~ ilt u:>ed to provide either loansor subsidies, or both, to poor families whosefmancial cO\ldition does not permit themrecourse to the private sector. On the otherhand, governments in developed countriesoften create the incentives and conditions,sometimes through direct intervention,whereby the private sector can provide thenecessBJY liquidity.

In developing countries, the reverse is the rule.Governments frequently provide liquiditydirectly to the market. Moreover, where thesegovernments intervene, more often than not thefunds flow not to poor people as supposedlyintended, but to the middle and upper incomegroups.

On the other hand, governments in developingcountries do not create the conditions wherebythe private sector can provide liquidity, andmore often, actually impede the involvement ofthe private sector in housing finance. This iscertainly the case in Pakistan, although there issome evidence that this is changing. Thecessation of State Bank funding to the HouseBuilding Finance Corporation is a step in theright direction.

Previous Page Blank SRMPPage27

Liquiditymaybe

provided bythe public

sector or theprivate

sector. Theprovision of

liquidityvaries greatlyin developed

countriesversus

developingcountries.

Although the public sector indeveloped countries r"relyprovides liquidity directly tothe housingfinance sector, itoften creates the incentivesand conditions- sometimesthrough direct interventionwhereby the private sectorcan provide the necessaryliquidity.

Financial resources for housing purposes arederived from a variety of sources. Indeveloping countries, loans and grants fromexternal donors can be a major resource,however, funding from this source can neverbe sufficient to meet more than a fraction ofthe fmancing needs. For this reason, externalfunding has been found to be more effective toan individual fmancial institution rather than anentire system.

In recent years, foreign donor funding has beenused more often to leverage change in thehousing sector, rather than as a solution to thephysical housing need. In addition, foreigncommercial loans are being viewed as apossible source ofhousing fmance.

All countries, to some degree, allocate fundsdirectly from the Central Government. Indeveloped countries, direct governmentfunding generally takes the fonn of subsidiesfor low-income families. But, in developingcountries, it more often consists ofdirectlending through a government-owned orcontrolled fmancial institution to selectedsegments of the market.

Government Housing Bank in Thailand isconsidered a good example of an institutionthat is generally free of governmentinterference, provides loans based on need, andoperates on market principles. A bad example

SRMPPage28

is when a housing fmance institution is used topromote a political agenda, provides loansbased on influence, and operates at a loss,requiring constant injections of capital.

Sources of Housing Finance

The major portion of financial resources orliquidity, particularly for the private sectorinstitutions, is derived from two basic sources:

• Deposits in home lending institutions, inthe fonn ofpassbook and time depositsfrom individuals and businesses; and

• Capital Markets, in the form of loans,bonds, securitized debt, and a wide varietyof financial instruments issued by housinglenders or specialized fmancialintermediaries.

Financial institutions mobilize deposits ingeneral by focusing on two distinct savingsmarkets: the pure savers who are seeking aninvestment vehicle, and the linked savers whoare seeking to utilize their savings for aspecific purpose.

On the other hand,governments in developingcountries do not create theconditions whereby theprivate sector can provideliquidity, and more often,actually impede theinvolvement ofthe privatesector in housingfinance.

Pure savers are always attracted by the yield ontheir savings, commensurate with the risk, andfor that reason, savings deposits from thismarket segment can be very mobile as the

depositor is constantly seeking the highestreturn. Moreover the potential market is largesince most people in the middle or higherincome bmckets do have some disposableincome to be saved.

A housingfinance systemmust attract deposits from"pure" savers as well asfrom"linked" savers. Pure saversare primarily interested in thereturn on their savingsdeposits, while linked savel'smake deposits to generateboth savings and the incomeon savings to acquire a home.

Linked savings is more stable, however thissavings universe is probably much smaller.The initial concept ofBuilding Societies in theUK and Savings and Loan Associations in theUS were for all practical purposes attuned tosavers who used their savings to access ahousing loan, although there was no formalcontract or agreem~nt to that effect.

Most developed countries utilize both depositsand the capital market to mobilize resources,although the proportion will vary depending ona number offactors. For example, primarymortgage lenders in the UK mobilize over 90percent of their housing resources fromdeposits, while in Denmark, specialized creditinstitutions generate 80 percent of theirhousing resources through the capital markets.

In the US, the proportion has been changingrapidly since the I970s when deposits from thesavings and loan associations funded 55percent of all housing loans while by 1991,deposits fell to only 33 percent. The trend inthe US as well as in many other countries hasbeen towards growth in the capital markets asthe principal supplier offmaneial resources forhousing, at the expense ofdeposits.

Resource Mobilization In India

The housing fmance sector in India has alsoexperienced a change in the composition of itsfmancial resources. The farst, and still India'slargest housing fmance institution, the HousingDevelopment Finance Corporation, initiallymobilized resources by tapping, the capitalmarkets, principally loans from other fmancialinstitutions. To complement these domesticsources, HDFC relied on international donoragencies, the largest being a USAID HousingGuaranty loan ($12~ million) and an IBRDloon ($250 million), which were instrumentalin not only providing large amounts ofliquidity, but also helped to provide credibilityto the institution. HDFC has now expanded itsoutreach by utilizing a variety of ways togenerate resources. In partlcular, it has focusedon individual and company deposits byoffering a variety of instruments with varyingmaturities to appeal to different investmentobjectives.

Today, 3S percent ofHDFC resources arederived from deposits. Capital marketresources include long-term bonds purchasedby trusts, insurance companies, corporationsand banlcs, as well as shorter term loansprovided principally by commercial banks.

The establishment of the National HousingBanIc (NHB) in India was supposed to open upa new source of liquidity for the growingnumber ofhousing fmance companies in India.However, a securities market scandal hasaffected the ability of the NHB to mise capitalfor on-lending to primary sector housingfmanee companies and it has been unable tofunction completely as a secondary housingfmance institution so far. Whether itwillovercome its managerial credibility problemsto fulfill its financial mandate is still open toquestion.

Resource Mobilization In Indonesia

Indonesia has addressed the liquidity issue in amanner similar to Pakistan. A state savingsbank, Bank Tebungan Negara (BTN). providesalmost 90 percent of all housing loans. Itreceives funding from the Bank of Indonesia(the Central Bank) and interest-free loans from

SRMPPage29

HDFCinIndia hasexpanded itsoutreach byutilizing avariety ofways togenerateresources. Ithasfocusedon individualand companydeposits byoffering anarray ofinstrumentswith varyingmaturities toappeal todifferentinvestl,tlentobjectives.

:.....~..... _ .......~.---:',._4 .._ ..• ~ ~

The newlyemerging

housingfinance

companies inPakistan

have little orno access to

the capitalmarkets.

the Ministry ofFinance. However, it also hashad access to large IBRD low-eost housingloans. These sources contribute abouttwo-thirds ofBTN's lending resources, withinternal resources consisting mainly of depositsand savings contributing the rest. BTN isexperimenting with a contract saving plan,although to date its success has been limited.

Another state institution, P.T. Papan Sejahtera,provides some housing loans, generating itsfunds from Bank of Indonesia credits, but alsoraises funds through bond placements thatcany below-market interest rates. Finally,commercial banks provide relativelyshort-term mortgage loans only toupper-income Indonesians. To date, Indonesia,like Pakistan, has been able to tap only aminimal portion of domestic savings and localcapital markets for home lending purposes. Ithas relied instead on direct governmentfunding and external funding as the majorfunding sources.

The Indonesian Government has not pennittedthe establishment of specialized fmanceinstitutions, as has Pakistan, nor has it put in

place those conditions which would permitcommercial banks, which can make housingloans, to maximize use of the capital markets.The result is that the condition of Indonesia'shousing is clearly sub-standard and, in fact,they are quite similar to the housing conditionsin Pakistan.

The consensus among housing finance expertsis that there is no right way to mobilizeresources for the housing sector. Nor is there afonnula for determining the proportion of usebetween different resource instruments.

Institutions in most countries experiment witha variety of instruments and techniques,selecting those that work best at the time theyare being tried and used. Moreover, thoseinstitutions understand the economic andpolitical realities under which they are workingand design resource mobilization programsaccordingly.

However, it is clear that until domestic savingsare mobilized and the capital markets freed up,no country will be able to generate sufficientfunds for housing fmance purposes.

Resource Mobilization in PakistanI

The ability of the HFCs in Pakistan to gainaccess to domestic capital markets and/orattract deposits is very limited at this time. TheGovenunent taps the domestic capital marketextensively to fmance its deficit. although thepressure on Government to reduce its relianceon debt for this purpose is constant. It isvirtually impossible for private sector fmancialinstitutions to compete with the govenunent aslong p.s the latter's markup on deposits remainsat today's high levels.

Recently, a blue chip textile company had topay a markup of 19.68 percent on a 5 year termloan from the capital market. Even a largepublic agency such as Water and PowerDevelopment Authority (WAPDA) has tried,so far unsuccessfully, to borrow up to Rs. 15billion at a 19 percent markup, even thoughthese bonds can be treated as approved security

SRMP Page 30

for the purpose of investment by trusts andinsurance companies to the same extent asprime government securities. The lack of anexplicit government guaranty has been themain reason why WAPDA has had difficultymarketing this issue. These high ratescontribute to the HFcs inability to attract thepure savers.

For a fledgling HFC to obtain a similar loan, itwould have to pay a higher rate on deposits.which would require the HFC to makemortgage loans at a markup of around 25percent, which is clearly too steep for even thewealthier Pakistanis.

The limited experience to date in the HFCsindicates that the market for mortgage loansappears to dry up at 17 percent, and even atthat rate it reaches only a tiny fraction of the

market. However, these high markups, drivenby inflation, arc a relatively new development,and it is still unclear what impact such rateswill have on the market over the long run (seeAppendix C for a brief discussion of the impactof inflation on the housing fmance sector).

Deposits are an even less likely prospect as alending resource. HFCs are not permitted tooffer demand or passbook savings, although30-day time or term savings deposits areallowed. Nevertheless, the HFCs believe that itis very difficult for these time deposits, calledCertificates of Investment, to compete withsimilar instruments being offered bygovernment institutions, such as the StateBank's rate d Ij percent on 6 month T Bills.

However, an HFC must be very careful inutilizing short-tenn deposits to fmancelong-term loans. The danger of mismatchingassets and liabilities is well-known even to themost casual observer of housing financesystems. Yet this danger can be mitigated, butnot eliminated, by the existence ofwell-functioning capital markets which offerliquidity for long-tenn mortgage instruments.

In the long run, the solution is simple. Thegovernment must step aside and stop

competing with the private sector in the pursuitof financial resources while at the same time,place a high priority on the creation of along-term bond market. It must also permit theHFCs more leeway in the mobilization ofresources.

Accordingly, Government must work withHFCs to create an environment whereby theHFCs can compete successfully with the rest ofthe financial market for resources. In the shortrun, however, there are some immediate steps,discussed later in this section, that thegovernment could take to bolster the HFCs andpermit them to carry out their assignedmandate to provide housing finance to allPakistanis.

__Specific Remedies

The State Bank appears to support the newhousing fmance companies. Yet, it is clear thatthe SBP is very concerned about the capacityand the capability of the HFCs to carry outtheir objectives, that is to mobilize resourcesand make mortgage loans, while demonstratingto the public and the government that they willnot wreak havoc on the economy in the sameway as have other fmancial institutions.

Untildomesticsavings aremobilized andthe capitalmarketsfreedup, nocountry willbe able togeneratesufficientfunds forhousingfinancepurposes.

In the long run, the solution is simple. Government must stepaside and stop competing with the private sector in the pursuitoffinancial resources while at the same time placing a highpriority on the creation ofa long-term bond market It mustalso permit the HFCs more leeway in the mobilization ofresources. Accordingly, Government must work with HFCsto create an environment whereby the HFCs can competesuccessfully with the rest ofthe financial marketfor resources.

SRMP Page3}

Thert:areample

examplesworldwide

where the useofa linked,

savingsscheme has

beensllccessful as

one toolamong a

variety ofsavings and

loanincentives.

The government is demonstrating itswillingness to support the housing sector byactivating the Housing Refinance Facility in anefficient and expeditious manner. Additionalassistance will depend on the HFCsperformance, but there is no assurance fromGovernment that more assistance, other thanthat deriving from the new facility, will beforthcoming.

The HFCs should initiate several resourcemobilization activities that would fit within thecurrent SBP authoritative and regulatoryframework. In the case where SBP approvalwould be required for a particular activity, theState Bank might have to issue a circular toclarify its approval. It should not be necessaryto change the NBFI Prudential Regulations forany ofthe activities listed below.

Other Funding

Additional funding to the SBP HousingRefinance Facility (HRF), possibly through theSBP Housing Credit Fund, should beconsidered at an appropriate time, althoughSBP's current policy will not permit it toprovide any more funding. Further, anyadditional funding should be in the form ofloans, not advances or grants, to the HFCs,under similar terms and conditions as theproposed HRF. '

Such funding should be contingent on theHFC's overall performance and theirsuccessful utilization of their quota under theHRF. Consideration of new funding should betaken up only when at least two of the HFCshave exhausted their quotas of Rs. 7S millionin initial loan refinancing from the HRF.

The housing fmance companies do not requiredirect funding from the Government ofPakistan or its specialized agencies, rather theyrequire the opportunity to compete with otherfinancial institutions in the mobilization offinancial resources. To accomplish this, theGovernment might have to resort to some sortof direct intervention in the form of guaranties,insurance, or tax benefits, as is found in mostcountries that have vibrant housing financeindustries.

SRMP Page 32

A fun or partiall guarantee would permit theHFCs to tap the domestic capital market for theadditional funds as discussed above. To repeat,this sort of Government intervention does notrequire direct financial contributions to thecompanies, which is neither recommended nordesirable. In all instances, these types ofinterventions should be enacted only within thecountry macroeconomic context and policy.

Savings Schemes

The HFCs should consider devising some sortof linked savin!>.s plan, such as a ContractSavings Scheme, which would tie the openingand maintenance of a personal savings accountto an opportunity to obtain a mortgage loan at apredetermined ratio. This type of scheme couldstrongly promote savings in general inPakistan, but more importantly, could possiblygenerate large amounts of funds for mortgagelending.

The cost of marketing such a scheme is likelyto be relatively high, therefore the HFCsshould focus now on designing a scheme andthen market it when their mortgage loanportfolios increase. Schemes should bedeveloped for Foreign Currency as well asRupee accounts.

The HFCs do not requiredirectfunding from theGovernment ofPakistan or itsspecialized agencies; rather,they require the opportunityto compete with otherinstitutions in themobilization offinancialresources.

There are ample experiences worldwide, inboth developed and developing countries,where the use of a linked savings scheme hasbeen successful as one tool amon'g a variety ofsavings and loan incentives. It should be

pointed out that this sort of scheme has notbeen very successful in India because thegroup targeted by this program has a limitedcapacity to save. For it to work in Pakistan, ascheme would have to be addressedspecifically to those income groups that theHFCs have identified as having sufficientincomes to participate in a linked savingprogram.

The real advantage ofanylinked savings scheme is thatnormally savers will accept alower mark-up than thatoffered by other savingsprograms-because at theend ofa specifiedperiod thesaver will be eligiblefor amortgage loan equal to afIXed percentage oftheamountsaved.

The real advantage of any linked savingsscheme is that normally savers will accept alower markup than that offered by other savingprograms because at the end of a specifiedperiod the saver will be eligible for a mortgageloan equal to a fixed percentage of the amountsaved. The saving must be constant over anumber ofyears to demonstrate to the lendinginstitution that the saverlborrower iscreditworthy. Usually, there is a significantpenalty if the saver withdraws from thescheme.

It should be pointed out that the lendinginstitution must structure the scheme in such away that borrowings do not exceed theavailable lending funds in the institution. InGermany, for example. the ratio is 2: I,meaning each Mark saved under their schemewill permit two Marks to be borrowed over a 7year term, which has been sufficient to meetthe borrowing demand. In Pakistan, the ratio

might be as little as I: I, at least in the initialstages of a scheme.

Foreign Currency Deposits

The HFCs are permitted to accept localcurrency savings accounts. Therefore the HFCsshould also be allowed to accept foreigncurrency deposits as one way to promote themobilization of savings. Investment Banks andModllJ'abas, which are also Non-BankFinancial Institutions, are currently permittedto set up foreign currency accounts.

Since HFCs have to meet the same reserverequirements as those two fmancialinstitutions, they shouldbe permitted to acceptand maintain foreign currency deposits. Thisrecommendation might very well be moot if,within the near future, the Government permitsfull convertability of the Rupee coupled withadoption of market rates for foreign exchangecover.

Certificates of Investment

The HFCs should utilize Certificates ofInvestment (COl) to generate short-termresources for mortgage lending. To overcomethe disadvantage ofcompeting with theGovernment of Pakistan for funds, the HFCsshould utilize the COls to mobilize savingsdeposits in conjunction with a linked savingsscheme. .