“THE GLOBAL UNIFIED PAYMENT NETWORK” · “THE GLOBAL UNIFIED PAYMENT NETWORK ... Nilson Report...

30

“THE GLOBAL UNIFIED PAYMENT NETWORK” Building real economic value for Payment Market Participants

Transcript of “THE GLOBAL UNIFIED PAYMENT NETWORK” · “THE GLOBAL UNIFIED PAYMENT NETWORK ... Nilson Report...

“THE GLOBAL UNIFIED PAYMENT NETWORK”

Building real economic value for Payment Market Participants

www.hazza.network Not to be copied/distributed without express permission

This document is an overview (“Overview”) of HAZZA. The Octo3 Foundation Limited (“Octo3 Foundation”) reserves the right to amend or replace any or all of the Overview at any time and

undertakes no obligation to update the Overview or to provide the recipient with access to any additional information.

Recipients are notified as follows:

Eligible purchasers: the information in this Overview is for prospective purchasers and is not intended to be received or read by anyone else.

No offer of securities: the HAZZA Token (as described in this Overview) is not intended to constitute securities in any jurisdiction. This Overview does not constitute a prospectus nor offer

document of any sort and is not intended to constitute an offer or solicitation of securities or any other investment or other product in any jurisdiction. Any offer or agreement in relation to any sale

and purchase of HAZZA Tokens is to be governed solely by a separate document setting out the terms and conditions of such agreement and may not be available to all persons.

No advice: this Overview does not constitute advice to purchase any HAZZA Tokens nor should it be relied upon in connection with, any contract or purchasing decision.

No representations: the Foundation makes no representation or warranty to the recipient or it advisers as to the accuracy or completeness of the information, statements, opinions or matters

(express or implied) arising out of, contained in or derived from this Overview or any omission from this document or of any other written or oral information or opinions provided now or in the future

to any interested party or their advisers. This Overview contains forward-looking statements that are based on the beliefs of the Foundation, as well as assumptions made by and information

available to the Foundation. No representation or warranty is given as to the achievement or reasonableness of any plans, future projections or prospects and nothing in this document is or should

be relied upon as a promise or representation as to the future. The Foundation expressly disclaims all liability for any loss or damage of whatsoever kind (whether foreseeable or not) which may

arise from any person acting on any information and opinions contained in this Overview or any information which is made available in connection with any further enquiries, notwithstanding any

negligence, default or lack of care.

Risk warning: potential purchasers should assess the risks and their own appetite for such risks independently and consult their advisors before making a decision to purchase any HAZZA Tokens.

Translations: this Overview and related materials are issued by the Foundation in English. Any translation is for reference purposes only and is not certified by any person. If there is any

inconsistency between a translation and the English version of this Overview, the English version prevails.

Property of the Octo3 Foundation: this Overview is the property of Octo3 Foundation and, by receiving it, the recipient agrees to not copy or distribute without the express permission of the Octo3

Foundation.

Unless otherwise stated, all references to “$” and “dollars” in this Overview pertain to United States dollars.

This Overview has not been reviewed by any regulatory authority in any jurisdiction. References in this Overview to specific companies and platforms are for illustrative purposes only. Other than

Octo3 Limited and Octo3 Foundation, the use of any company and/or platform names and trademarks does not imply any affiliation with, or endorsement by, any of those parties.

DISCLAIMER

2

• Total payment transaction value is expected to be $70TN by 2025(1)

• The way it is managed is highly fragmented and complex causing

friction for consumers, merchants, market participants

(transaction fees could amount to $1.7TN by 2025)(2)THE CHALLENGE

• We have a proven, secure, enterprise payment platform

• The founders collectively have 60+ years of payments and

technology experience

• We are creating a unified global payment network to drive a

seamless experience for all participants at a lower cost THE SOLUTION

• Technology disruptions such as blockchain are revolutionizing

the industry – levelling the playing field through creating inclusion

and accessibility

• We have entered a ‘convenience-first’ era, creating huge

demand for a global unified payment networkTHE OPPORTUNITY

Note: (1) Electronic transactions consist of online and offline payments by credit card, debit card, pre-paid card, eWallets

Note: (10and mobile payments, etc.

Note: (2) Total transaction value multiplied by estimated transaction fees captured by intermediaries (2.5%) = $1.7 TN

Source: Nilson Report (2016-2017), Persistence Market Research (2016)3

• Tokens will be created to ‘access’ and ‘pay’ for services on this

global payments network through a Token Sale

• At the end of the Token Sale, there will be a fixed supply of

tokens available in the marketTHE PARTICIPATION

TABLE OF CONTENTS

The Challenge

The Opportunity

The Solution

HAZZA Senior Team

Octo3 Foundation

The Participation

Project Timetable

Summary

Glossary4

THE CHALLENGE

5

www.hazza.network Not to be copied/distributed without express permission

CONSUMERS MERCHANTS

$23.4TN $22.8TN

TERMINAL PROVIDERS (POS)

(in 2016) (1) (in 2016) (2)

Payments is a highly complex and fragmented market with

many intermediaries…

THE CHALLENGE

Note: (1) Total electronic transaction value paid by consumers in 2016. Total electronic transaction value paid by consumers is a projection based on current trends.

Note: (2) Total electronic transaction value received by merchants in 2016, after the intermediary fees charged by payment companies. Total electronic transaction value received by merchants is also a projection.

Source: Nilson Report (2016-2017), Persistence Market Research (2016)

Current State Inefficiencies: $585 BN

6

ISSUERS

ONLINE PROVIDERS

TECH SOLUTIONS

ALTERNATIVE PAYMENT METHODS

ACQUIRERS PAYMENT SERVICE

PROVIDERS

PAYMENT METHOD

PROVIDERS

www.hazza.network Not to be copied/distributed without express permission

…Caused by …

THE CHALLENGE

Typical physical

and online shopsCASH

Lack of Universal Acceptance

…resulting in the lack of universal acceptance for consumers

and merchants

Inefficient Layers of

Intermediaries

Fragmented

Technology Standards

Complex Multichannel

Implementation

Current State Inefficiencies: $585 BN (average 2.5% fees)

only 5 accepted

only 2-3

accepted

7

A leading global

eCommerce platform

CONSUMERS MERCHANTS

$23.4TN $22.8TN(in 2016) (1) (in 2016) (2)

Note: (1) Total electronic transaction value paid by consumers in 2016.

Note: (2) Total electronic transaction value received by merchants in 2016, after the intermediary fees charged by payment companies.

Source: Nilson Report (2016-2017), Persistence Market Research (2016)

www.hazza.network Not to be copied/distributed without express permission

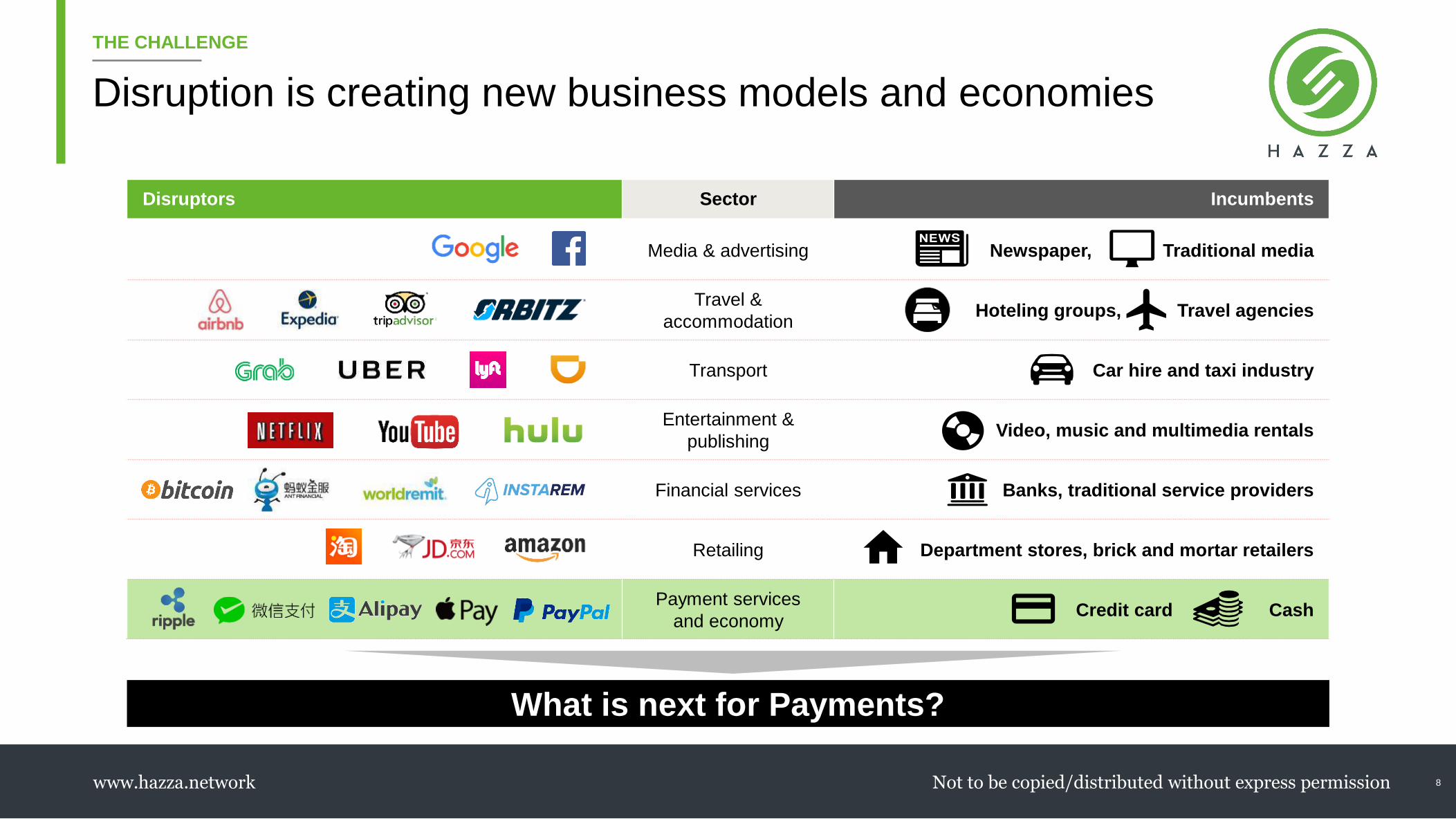

Disruption is creating new business models and economies

THE CHALLENGE

Disruptors Sector Incumbents

Media & advertising Newspaper, Traditional media

Travel &

accommodationHoteling groups, Travel agencies

Transport Car hire and taxi industry

Entertainment &

publishingVideo, music and multimedia rentals

Financial services Banks, traditional service providers

Retailing Department stores, brick and mortar retailers

Payment services

and economyCredit card Cash

What is next for Payments?

8

www.hazza.network Not to be copied/distributed without express permission

The birth of

The birth of the

Alliance

The birth of the

Association

First card

issuance in

China

Visa becomes

For-Profit

MasterCard

becomes For-Profit

The birth ofThe birth of

Issuance of

first bitcoin

Release of

THE NEXT EVOLUTION

New technologies can breathe new life into a historically

proven model

9

HISTORY

First credit card

issued by

The birth of

1950 1970 1980 2000 2010

FUTURE

Membership models have been successful,

however they:

• Are private alliances with expensive

membership fees

• Are an exclusive club for large players,

excluding market participants

• Result in a fragmented market, with high

barriers to entry

Emerging APMs and innovations are

mostly point solutions

• For B2C: Alipay, Wechat Pay or ApplePay

• For Inter-bank: Ripple

• Do not address: ecosystem and

interoperability

The birth of

SELECTED EXAMPLES

Payments market will need:

An open & transparent

payment network – driving

global decentralization

Run by members for

members – for anyone

and everyone

Leveraging internet and

blockchain technology

////

THE OPPORTUNITY

10

SECTOR MOMENTUM • Aggressive acquisition of merchants and customers by

alternative payment methods (APMs)

• Ant Financial spent $4 BN in the last two years on

market entry

2 BN BY 2036

GLOBAL PENETRATION – Alipay aims to reach a

global customer base of

• 77% increase from 2016 enabling digital payments

• PMPs are going omni-channel with different

underlying technologies (e.g. Visa payWave,

MasterCard Paypass, etc.)

6.8 BN USERS GLOBALLY

DIGITAL ADOPTION – By 2022, smartphone

penetration is expected to reach

Sources: Goldman Sachs (2017), Nilson Report (2016-2017), Persistence Market Research (2016), Euromonitor (2017), McKinsey (2016), Ripple Insights

(2016), Boston Consulting Group (2015), eMarketer (2016), China Daily (2016), Ericsson (2017), iResearch Global (2016), Boston Globe (2017), CNBC

(2017), Economic Times (2017), TechCrunch (2017), Reuters (2017)

OF ALL CONSUMER

TRANSACTIONS (2016)

• High barriers to entry for merchants, consumers

and APMs

• New technologies enabling financial inclusion

FINANCIAL INCLUSION – Third world economies,

cash is used for

70%

• China’s mobile payment transaction value grew by

145x in the last 5 years

• Payment intermediaries is a $585 BN business and

estimated to grow to $1.7 TN by 2025

$70 TN BY 2025

CASHLESS PAYMENTS – The non-cash transaction

value is expected to exceed

Harnessing the

explosive growth and

innovation in the

payments industry

11

www.hazza.network Not to be copied/distributed without express permission

Universal acceptance could be realized through a democratized

payment platform

THE OPPORTUNITY

12

…to an open payments economy

From a closed payments economy…

Consumers Merchants

PMPs/APMs PSPsIssuers Acquirers

Chinese tourists

with WeChat Pay

• Direct and hassle-free payments enabled by smart contract

Go to Tesco

Express in

London

Accept WeChat Pay with

the use of HAZZA

Customer will be charged

FX conversion and

transaction fees (~1%)

Merchants are charged

2.5% on average by

payments intermediaries

SELECTED EXAMPLES

ILLUSTRATIVE

Scenario: Chinese tourist

spends £20 in Tesco

Express in London with

credit card

£20 + £0.2 £20 – £0.5

THE SOLUTION

13

SOLUTION OVERVIEW

Migrating an existing proven

payment platform to

blockchain Revolutionizing the payment ecosystem

Optimizing business engagement

Leading financial inclusion

Enhancing global acceptance of all payment methods

The HAZZA network concept was born with this thinking…

BENEFITS

14

HAZZA

• We plan to migrate a proven Fintech payment platform to

blockchain technology

• Creating an open access, global, unified payment network

• Through a not-for-profit foundation governed by the

community through a decentralized structure (DAO)

PROVEN PLATFORM

Using a proven omni-

channel, certified and

secure solution

15

CERTIFIED

REAL TIME

OMNI-CHANNEL

PROVEN

SECURE

• Certified processor of Visa, MasterCard,

Discover Card, Diners Club, and American

Express

• BASE I and BASE II capable

• Fully functional ISO 8583 Payment Switch

• Fully compliant local/global instances

• E-commerce, Physical PoS, mPoS,

MOTO, coupon, loyalty on a single

integrated platform

• All major Card Brands and comprehensive

coverage of global APMs

• Processing in 130+ currencies

• Proprietary, cloud-based technology with

simple API integration

• Intelligent routing & switching for cost

optimization

• Real-time consolidated reporting and

dashboards

• Unlimited scalability

• Web-based, secure portal for transactions

management

• Comprehensive audit trail & access

control

• Encrypted payment card data

• PCI-DSS Level 1 compliant

www.hazza.network Not to be copied/distributed without express permission

TECHNOLOGY POSSIBILITIES

Leveraging blockchain technology

Independently verified

transactions Smart contracts

Peer-to-peer network Decentralized and

Immutable Ledger

Increased security

• Independent transaction verification

• Encrypted transactions and identities

• No single point of failure

Reduced cost

• Significant savings from disintermediation

• Minimal infrastructure costs

Increased transparency

• Accessible source of truth

• Effective governance and audit by participants

Reduced transaction time

• Near real-time transaction (sec/min)

• Smart contracts triggered once conditions are met

• Public, write-once ledger

• All transaction activities in the

network are encrypted

• No central control of network

• No intermediaries

• Close to real time settlement

• All transactions require verification

and confirmation by majority of the

network participants

• Key application of blockchain

technology

• Automatically facilitate, verify or

enforce the terms of a contract

KEY FEATURES KEY BENEFITS

16

www.hazza.network Not to be copied/distributed without express permission

IMPLEMENTATION

Existing solution proposed to be migrated to blockchain

technology in 3 phases…

HAZZA token-enabled smart contract functions

HAZZA Core Platform

HAZZA network leveraging blockchain

Phase IDecentralize Business Engagement

Phase IIBuild Engagement Marketplace

Phase IIIDecentralize Payment Processing

HAZZA Open API (decentralized)

HAZZA Core Platform

Merchants PSPs PMPs Other participants

HAZZA PAYMENT

ROUTE OPTIMIZER

HAZZA

Smart

Contracts

Participant

Registry

Service

Publishing

Discovery

KYC

Participant

VerificationMerchant

Service

Channel

Adaptor

Rating

On-chain Transactions

(Migrated to Blockchain)

HAZZA Open API (decentralized)

HAZZA Core Platform

Merchants PSPs PMPs

HAZZA

Smart

Contracts

Off-chain

Transactions &

Negotiations

(State Channel

Technology)

• Faster

• Private to 2

parties only

• Posted upon

completion of

business rules

Roles of blockchain:

• Identity verification

• Contest judge

• Record distribution

Other participants

Off-chain

Smart

Contract

s

Off-chain

Smart

Contracts

HAZZA Open API (decentralized)

Merchants PSPs PMPs Other participants

On-chain Transactions

(Migrated to blockchain)

Off-chain Transactions

& Negotiations

(Migrated to blockchain)

• Evaluate new blockchain

technology readiness

(e.g. Lightning Network,

Raiden)

• Leverage blockchain in

core processing when

ready

I.I

I.II

II

III

17

Exis

ting F

inte

ch

so

lution

to

mig

rate

www.hazza.network Not to be copied/distributed without express permission

GLOBAL UNIFIED PAYMENTS NETWORK

An open access, all-to-all

payments network enabled by

blockchain technology

Decentralizing participation

Eliminating inefficiencies

Driving innovation & new economies

Enabling Financial Inclusion

All Payment Methods

Service Providers

and IssuersNew Use Cases and

Value Added Services

All Merchants

THE HAZZA NETWORK

…resulting in an open global unified payment network

Note: HAZZA will have a local instance in jurisdictions where in-country payment networks are required.

Companies shown above are for illustrative purpose only.

18

Potential Benefits:

• Greater access to

merchants

• Lower customer

acquisition costs

Potential Benefits:

• New business model

• New job opportunities

for new products /

services

Potential Benefits:

• Higher transaction volume

• Lower technology costs

Potential Benefits:

• Lower customer

acquisition costs

• Greater access to

merchants

ILLUSTRATIVE

www.hazza.network Not to be copied/distributed without express permission

Smart contract technology will be utilized to revolutionize and

optimize business model

USE CASE

19

Expected to be completed automatically within minutes on the HAZZA network

Potential benefits for merchants

Potential benefits for payments participants

• Open and transparent marketplace – access to all

payment participants

• Real-time discovery – complete automation by

smart contract

• Significant time savings – PMP / PSP engagement

completed within minutes (vs. months)

• No downtime – auto-switching to best payment

option available

• Minimized merchant acquisition cost – automated

business engagement

• Greater merchant access with high scalability –

exposed to global merchants with one connection

• Minimized operational risks – all rules pre-set on

smart contracts

I am looking for…

• PMP

• Accept CNY/IDR/THB

• Service in all Asian

countries

• Full KYC

• Above average rating

• Lowest price available

I am a…

• PMP

• Accept CNY/IDR/THB

• Services all Asian

countries

• Full KYC

No rating

requirement

High rating

only

POS

Provider

Average

rating

MERCHANTS PAYMENT INTERMEDIARIES

HAZZA-enabled

smart contract

with

self-discoveryHigh rating

only

POS

provider

Smart

Contract

Building a marketplace leveraging smart contracts

www.hazza.network Not to be copied/distributed without express permission

Founders: 60+ years collectively of payments and fintech

experience

AJMAL SAMUEL HANS WONGFounder & Chairman

of OCTO3 Limited

Founder and Chief Technical Officer (CTO)

of OCTO3 Limited

HAZZA SENIOR TEAM

TYRONE LYNCHChief Executive Officer (CEO)

of OCTO3 Limited

20

• 20+ years of financial infrastructure, payments, clearing

houses, regulatory, IT and management experience

• Ex-President and CEO – Cityline, Founder and CEO –

ASAP Transaction Processing Corporation Limited

• Fellow of the Hong Kong Institute of Directors

• Member of the Institute for Electrical and Electronic

Engineers (IEEE), International Computer Society, and

Association for Computing Machinery (ACM).

• Board member, Sir David Trench Fund (HKSAR

Government)

• 20+ years of industry experience in large-scale mission

critical financial infrastructure and payments systems

development, deployment and management

• Comprehensive working knowledge of the banking

regulatory framework applicable to financial technology

• Previously led the technical direction, development and

operation of mass transaction systems and designs and

implementation of mission-critical messaging solutions at

International Messaging Associates for US government

organizations and many large international corporations

• 20+ years of P&L management experience for global

multinationals in the payments and technology sectors

• Expertise in international market entry and

commercialization of new businesses (Recently created

and managed NTT Group’s new global payments

service line)

• Former CEO of NTT DATA Hong Kong’s global payment

business, Senior VP at NTT Communications Asia and

Senior Executive for Atos Origin and Schlumberger

Japan

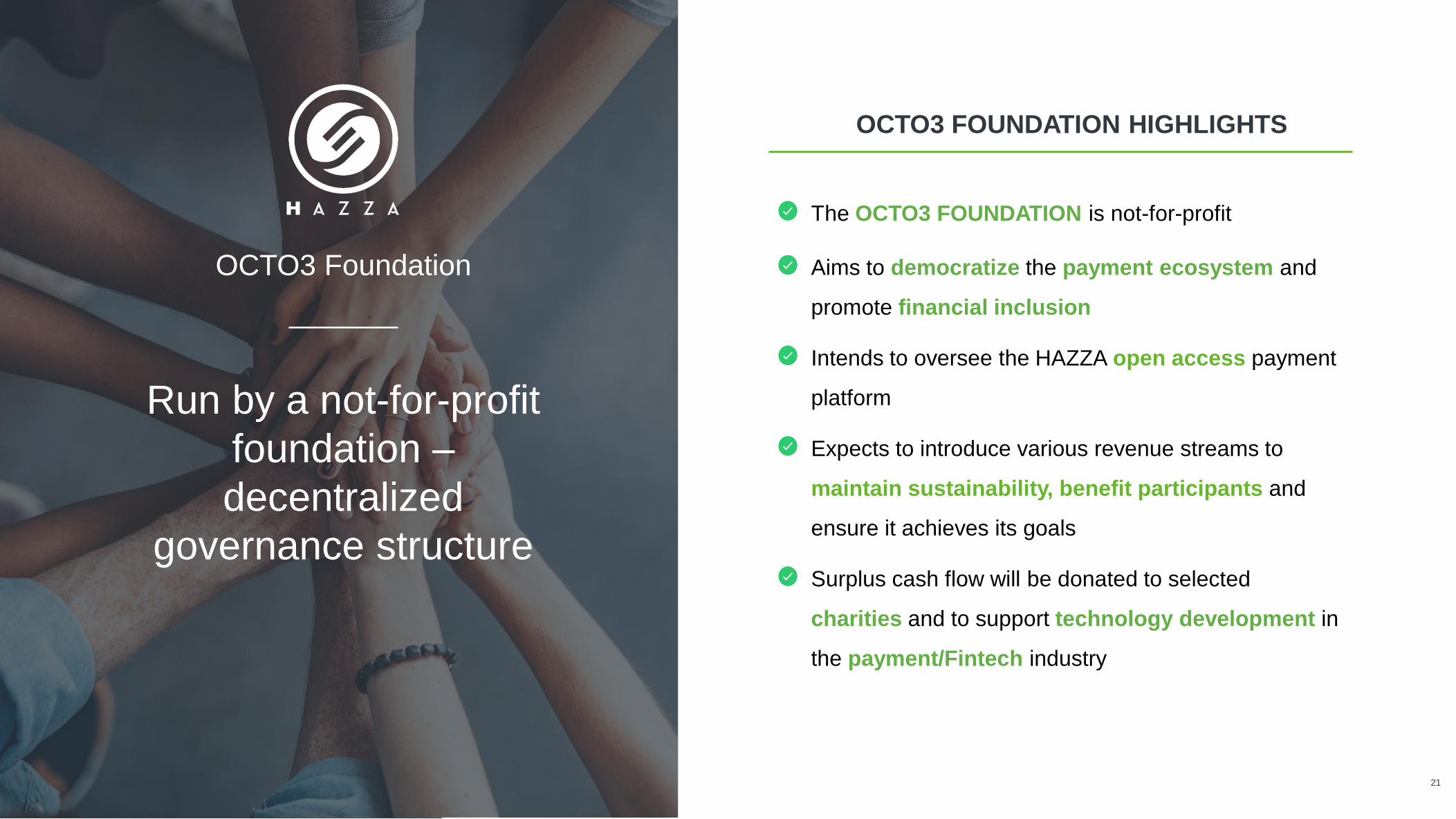

Run by a not-for-profit

foundation –

decentralized

governance structure

21

The OCTO3 FOUNDATION is not-for-profit

Aims to democratize the payment ecosystem and

promote financial inclusion

Intends to oversee the HAZZA open access payment

platform

Expects to introduce various revenue streams to

maintain sustainability, benefit participants and

ensure it achieves its goals

Surplus cash flow will be donated to selected

charities and to support technology development in

the payment/Fintech industry

OCTO3 FOUNDATION HIGHLIGHTS

OCTO3 Foundation

www.hazza.network Not to be copied/distributed without express permission

GOVERNANCE

Governed by the community for the community

• Subject matter

experts

• Regulatory/Legal

• Technology

• Others

ADVISORS PARTNERS

Composition – 7 Directors

• 3 Founding Directors

• 4 Independent Directors: elected by the Foundation members

Guidance

• Key decisions

• Review strategic and material decisions

• Committee setup: Remuneration, Nomination and Audit Committee

BOARD OF DIRECTORS

Key Responsibilities

• Oversee Token Sale and HAZZA

network development

• Promote HAZZA network

awareness

Executive Management Team

• Day-to-day operation

• To be appointed by Board of

Directors

Foundation Members

• Vote for Independent Directors

and key decisions

• A portion of members to be

elected by HAZZA participants

OCTO3 FOUNDATION

COMMUNITY

• Governed by the community and not-for-profit

22

Issuers Acquirers

Financial

Services

Industry

Associations

MerchantsConsumer

Groups

PMPs

Participants

Coaches /

TrainersKYC Services Data Analytics

Tax ServicesCredit Services

3rd party service providers

Other

participants

Other service

providers

A token sale will be launched to raise required proceeds to build

the HAZZA network

‘The HAZZA Token will be the KEY to the HAZZA Economy’

THE PARTICIPATION

www.hazza.network Not to be copied/distributed without express permission

HAZZA TOKEN GOALS

The HAZZA token sale (ticker: HAZ)

Our vision is for the HAZZA Tokens to be the digital

currency that will underpin the HAZZA network and will

enable participants to:

• Pay for accessing the HAZZA network and its services

• Govern the technological development of the HAZZA

network

• Contribute their efforts to developing the HAZZA network

• Utilize future token functionalities of the HAZZA Token

once online

24

Levelling the

Play field

• Facilitate opening up of proprietary technology

to a not-for-profit foundation for the benefit of the

payments community

• Allow transparency of the HAZZA network and the

various participants interests

“To Democratize the Payments Market”

Global

Accessibility

• Access a wide pool of contributors and

participants

• Allows 24/7 token sales

• Strong and efficient engagement with the

community of users

• Bootstrap network effectExpedite

Adoption

WHY A TOKEN SALE?HAZZA TOKEN OVERVIEW

www.hazza.network Not to be copied/distributed without express permission

VALUE CREATION

Using HAZZA tokens to access a potential $700+BN economy

ESTIMATED VALUE CREATION FOR THE PAYMENT COMMUNITY ($ BN)

• New job opportunities for society (re-

skilling)

• Creating sub-economies around HAZZA

– new financial products/services

• Open for innovation to shape payment

system and drive adoption

• Lowering barrier of entries for small-to-

medium enterprises

• Faster adoption of new payment

methods

OTHER POTENTIAL

BENEFITS TO THE

COMMUNITY

25

$500+BNPotential other benefits

Potential savings on

transaction costs (2)

Benefiting 40+ MN merchants

Potenial economic

value of greater

access (3)

15% expansion of payments

market

Potential savings on

technology costs (1)

Benefiting PSPs & 15+ MN

merchants

2018 2020 2021 … 2025

50

110

200

730

3.7x

2019

20

10x

Potential

Token Utilities

Phase IIPhase I Phase III

Access Govern Access Govern

Develop

Access Govern

Develop TBD

• Method of payment

• Identify Verification

• Other utilities

HAZZA

Roadmap

$2500BN(2.5 BN unbanked spending <US$100 per month)

Note: (1) PSPs could save transaction fees paid to technology providers per transaction

Note: (2) Merchants could save an estimated 1% of the projected non-cash transaction value due to disintermediation

Note: (3) The additional interchange revenue of PMPs and issuers benefiting from the use of HAZZA network

Source: Nilson Report (2016-2017), Persistence Market Research (2016), Pew Global (2015)

FINANCIAL INCLUSION

www.hazza.network Not to be copied/distributed without express permission

HAZZA TOKEN GOALS

Sale structure and token distribution

26

KEY DATESTOKEN DISTRIBUTIONSALE STRUCTURE

US$0.38 token

price

MARKET DETERMINED

OUTCOME

FIXED token

quantity

determined at

end of sale

FIXED proportion

to the public &

private sale

UNCAPPED

until completion

of token sale

FIXED token

supply

Private-sale

Whitepaper Release

Public

Sale

Token Activation

Sept 1

Oct 3

Oct 31

On or after

Nov 8

HAZZA Website Go-LiveAug 25

Note: 1) The Foundation reserve the right to end the Token Sale at any

time before Oct 31 without prior notice; 2) Token activation is subject to

completion of AML / CTF requirements as may be required by Octo3

Foundation.

www.hazza.network Not to be copied/distributed without express permission

PROJECT TIMETABLE

Aiming to launch the HAZZA network within 8 months

27

2017 2018

Q3 Q4 Q1 Q2 Q3 Q4

Jul Aug Sep Oct Nov Dec

To

ken

Sale

Sch

ed

ule

Project Kick-off

HA

ZZ

A R

oad

map

Whitepaper Release

Token Sale Mobilization

Private sale

Public

Sale

Oct 3 – Oct 31

Sept 1 – Oct 31

HAZZA Phase I Development

Phase II Development

Participant

Register

HAZZA Go-live

HAZZA Token Activation (Nov 8)

Milestones

Legend

Phases

Key activities

Octo3

Foundation

Registration

Octo3 Foundation Org Setup

API Development & Release

Pilot

Smart

Contract

Development

Smart

Contract

Activation

(Oct 3)Service

Publishing

Discovery KYC Participant

Verification

Merchant

Service

Rating

Sandbox

Release

Disruption is inevitable

Timing is perfect

HAZZA is positioned to harness this potential to benefit you

HAZZA has the solution and the team to realize this opportunity

SUMMARY

28

www.hazza.network Not to be copied/distributed without express permission

APPENDIX

Glossary

Term Definition

Acquirer Financial institution which provides merchant accounts and related services to merchants

APIs Application programming interfaces

APMs Alternative payment methods

B2C Business to consumer

BASE I VisaNet’s authorization system

BASE II VisaNet’s settlement system

DAO Decentralized autonomous organization

FX Foreign Exchange

HAZZA Token ERC20-compliant token issued using the ethereum network

HAZZA network The technology network that all payments players can connect to for global unified payments

ISO 8583The international standard for financial transaction card originated interchange messaging issued by the International Organization for

Standardization

Issuer A financial institution which issues a card and in some cases a line of credit to the consumers

KYC Know-your-customer

mPOS Mobile point-of-sale

MOTO Mail order/telephone order

29

www.hazza.network Not to be copied/distributed without express permission

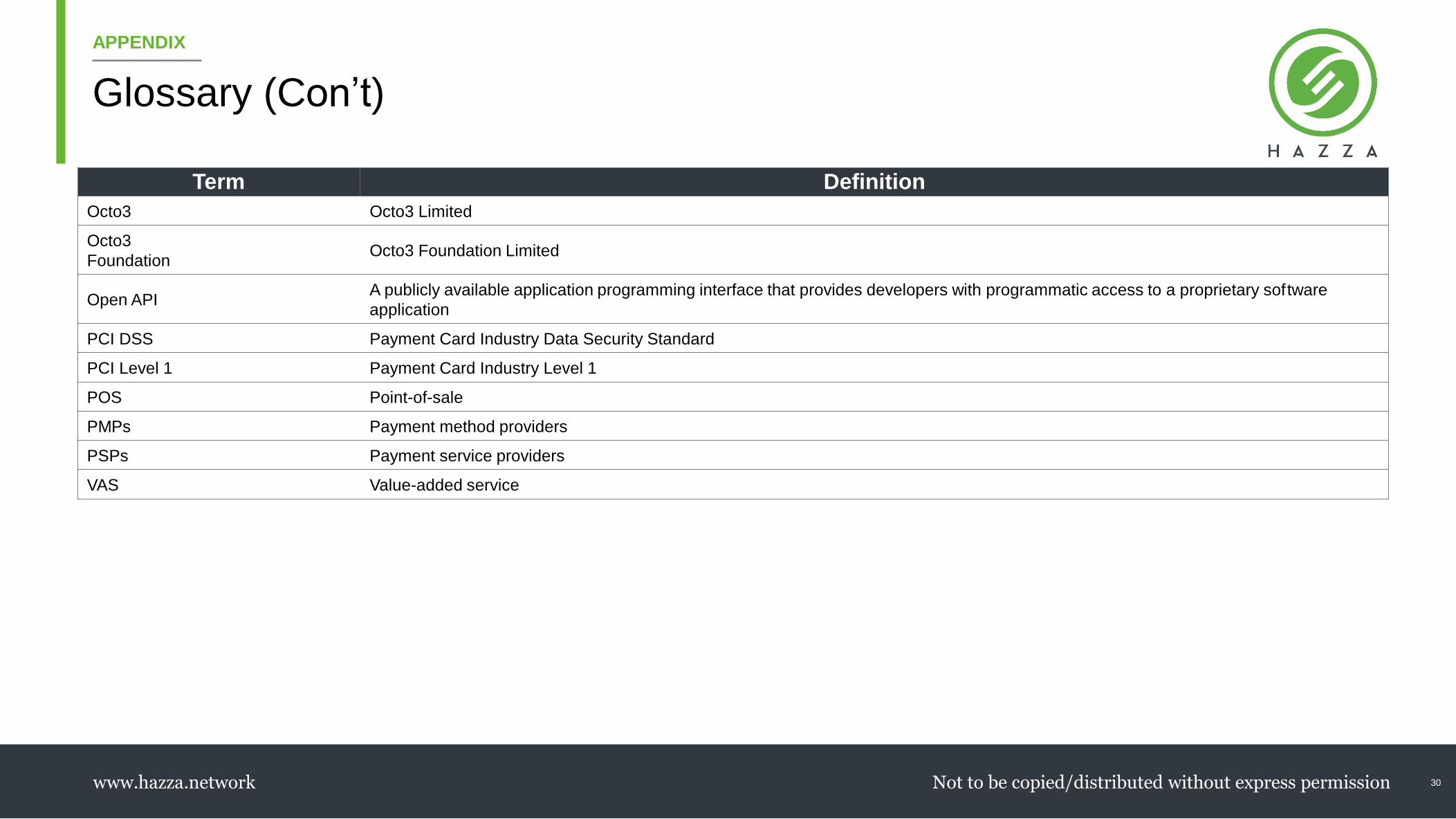

APPENDIX

Glossary (Con’t)

Term Definition

Octo3 Octo3 Limited

Octo3

Foundation Octo3 Foundation Limited

Open APIA publicly available application programming interface that provides developers with programmatic access to a proprietary software

application

PCI DSS Payment Card Industry Data Security Standard

PCI Level 1 Payment Card Industry Level 1

POS Point-of-sale

PMPs Payment method providers

PSPs Payment service providers

VAS Value-added service

30