The Global Financial Crisis: Implications for Debt...

39

The Global Financial Crisis: Implications for Debt Implications for Debt Management 1 Leonardo Hernández PRMED May 2009

-

Upload

doannguyet -

Category

Documents

-

view

215 -

download

0

Transcript of The Global Financial Crisis: Implications for Debt...

The Global Financial Crisis:Implications for DebtImplications for Debt

Management

1

Leonardo HernándezPRMED

May 2009

Presentation Outline

• The ongoing crisis in a nutshell

• Debt Sustainability: a summary

• Debt sustainability &• Debt sustainability &management in the currentenvironment

• The crisis: a protracted one?

• Room for improving the DSF?

2

Presentation Outline

• The ongoing crisis in a nutshell

• Debt Sustainability: a summary

• Debt sustainability & management

3

• Debt sustainability & managementin the current environment

• The crisis: a protracted one?

• Room for improving the DSF?

The Crisis in a nutshell

• Antecedents of the crisis:– Boom-bust credit boom, fueled by lax

monetary policy in developed countries

– Financial innovations (securitization, assetstriping, etc.)

– Poor assessment of risks

– Poor corporate governance

– Macroeconomic imbalances (low savings insome developed countries,...)

• Led to an asset price bubble and excessinvestment in real estate

4

US Residential Mortgage Backed Securitiesversus Other Securitized Assets (% GDP)

Source: Blundell-Wignall and Atkinson (2008), Federal Reserve,Datasteam, OECD.

The Crisis in a nutshell

Three Main Contagion Channels

• Liquidity squeeze and lower riskappetite higher financial costs

• Lower commodity prices and tradevolumes lower export proceeds andgovernment revenues

• Reduction in capital flows andremittances tightened financial sources

6

Drastic fall in commodity prices andexport volumes

Selected Commodity Price Indices

300

350

400

450

500

Energy

Metals

January 2003=100

World Trade Volume

(Annual Percent Change)

0

5

10

7

Source: IMF staff. Latest projections correspond to April 2009.

50

100

150

200

250

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Food

-15

-10

-5

2007 2008 2009 Projection

World trade volume (goods and services)

All Types of Private Capital Flows toEmerging Economies Plunging

U.S. dollars, billions, net 2006 2007 2008 2009

Private Flows 565 929 466 165

• Equity investment 222 296 174 195

• Direct 171 304 263 198

• Portfolio 52 -8 -89 -3• Portfolio 52 -8 -89 -3

• Private Creditors 343 632 292 -30

• Commercial Banks 212 410 167 -61

• Nonbanks 131 222 125 31

Official Flows, net -58 11 41 29

• IFIs -30 3 17 31

• Bilateral -27 9 24 -2

Capital Flows to Emerging Economies

Source: Institute for International Finance: “Capital Flows toEmerging Market Economies.” 01/27/09.

Potential Decline in Remittances

10

15

20

25

Baseline Low Case

(% change)

-10

-5

0

5

10

2005 2006 2007 2008 2009 2010

Source: World Bank data and staff estimates.

Remittance Flows to Developing Countries

The Crisis in a nutshell

• Countries reactions to the crisis:– Loose monetary policy

– Recapitalization of financial systems

– Bail out of household and corporate– Bail out of household and corporatesectors

– Fiscal stimulus packages

– Financial systems regulatory overhaul

• And IFIs are stepping in byintermediating more funds

10

G20 Countries – Discretionary FiscalStimulus in 2009 (% of GDP)

Australia

CanadaFrance

Germany

Italy

JapanSpain

U.K.

U.S.A

Advanced Economies -

Simple average = 1.2%

of GDP

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Argentina

Brazil

China

IndiaIndonesia

Korea

MexicoRussia

Saudi Arabia

South Africa

Turkey

Australia

Emerging Economies -

Simple average = 1.3%

of GDP

11

Source: IMF Staff Note to G20 Deputies Jan. 31, 2009

Bottom line: outlook for LICs in 2009has deteriorated sharply

GDP Growth

(In percent)

6

8

10

WEO Spring 2008

Latest projections

Current Account Deficit

(In percent of GDP)

12

14

16

18

20

WEO Spring 2008

Latest projections

12

Source: IMF Staff. Latest projections correspond to April 2009.

0

2

4

All LICs Sub-

Saharan

Africa

Asia Middle East

and Europe

Latin

America

0

2

4

6

8

10

All LICs Sub-

Saharan

Africa

Asia Middle East

and Europe

Latin

America

Global growth: -1.3% in 2009

The Crisis in a nutshell

Impacts and responses

• Higher financial costs, although benchmark interest rates

will remain low for a while;

• New intermediation channels, although financing gaps

remain significant;remain significant;

• Renewed focus on fiscal stimulus: fiscal space

considerations.

Bottom line

• Full impact depends on countries’ initial conditions

(fundamentals) and exposure to shocks;

• Final outcome depends on the depth and length of the crisis.

13

Presentation Outline

• The ongoing crisis in a nutshell

• Debt Sustainability: a summary

• Debt sustainability & management

14

• Debt sustainability & managementin the current environment

• The crisis: a protracted one?

• Room for improving the DSF?

Debt sustainability: a summary

• Debt is sustainable as long as it can beserviced without resorting toexceptional financing and/or majorcorrections in the balance ofincome and expenditures.income and expenditures.

• Analyses focuses on indicators such as:

– PV of Debt in percent of: (i) Exports,(ii) GDP, and (iii) GovernmentRevenues;

– Debt Service in percent of (i)Exports, (ii) Government revenues.

15

Debt sustainability: a summary

• Debt sustainability indicators willdeteriorate due to the fall in exports andgovernment revenues, and the increase indebt service.

• For some countries rollover and acceleratedrepayment may be an issue.

• Debt sustainability indicators maydeteriorate even further as governmentsimplement fiscal stimulus packages.

16

Debt sustainability: a summary

• A critical issue is how long the crisiswill last.

• A short lived crisis will have a small effecton debt sustainability as relevanton debt sustainability as relevantindicators are of a long term nature(forward looking, 20 yrs).

• In contrast, a protracted crisis will have amore lasting effect on debt sustainability.

17

Presentation Outline

• The ongoing crisis in a nutshell

• Debt Sustainability: a summary

• Debt sustainability &

18

• Debt sustainability &management in the currentenvironment

• The crisis: a protracted one?

• Room for improving the DSF?

Financial crisis: issues to consider

• Initial conditions (resilience):• Domestic financial sector (including links to international

markets through private and sovereign borrowing)• Fiscal imbalances (taking account of official financing

commitments)• External imbalances (including reliance on portfolio flows)

• Crisis impact:• Crisis impact:• Growth prospects (dependence on commodities whose prices

are falling or sectors where external demand is falling)• Fiscal revenues (dependence on commodity exports)• External account (terms of trade shocks)• Remittances• Domestic financial sector (links to international markets)• Financing – official and private (new borrowing and rollover in

private markets, aid)• Volatility and uncertainty (interest rates; exchange rates)

19

Issues to consider … taxdependence on commodity exports

AngolaNigeria

ChadCongo, Republic of

Commodity Revenues to Total Revenue, 2008

(Ratio, in percent of total revenue)

20

0 20 40 60 80 100

VietnamGuinea

MongoliaMauritania

Papua New GuineaSudan

AzerbaijanYemen, Republic

Angola

Source: IMF staff estimates.

Implications for Debt Management

• Borrowing environment is increasingly complex - madeeven more challenging by the evolving financial crisis

• Potential for rollover risk // sudden reversal is high

• Need to avoid costly mistakes, accumulation of unsustainabledebts (due to new borrowing or arrears accumulation)

• Exchange and interest rate uncertainty is high

• Current situation underscores importance of having a• Current situation underscores importance of having astrong debt management capacity, institutions andpractices

• To address concerns about the growing risk of debt distress, and

• Contribute to improved public financial management in developing countries

• Scaling up in provision of technical assistance andcapacity building efforts if lacking the capacity

• Need for coordinated work programs to provide concerted capacitybuilding and TA

21

List of Heavily Indebted PoorCountries (as of end March 2009)

24 Post Completion Point Countries

Benin Ethiopia Honduras Mauritania Rwanda Tanzania

Bolivia Ghana Madagascar MozambiqueSão Tomé and

PríncipeUganda

Burkina Faso Guyana Malawi Nicaragua Senegal Zambia

Cameroon Gambia, The Mali Niger Sierra Leone BurundiCameroon Gambia, The Mali Niger Sierra Leone Burundi

11 Interim Countries

AfghanistanCentral African

RepublicCongo, Dem. Rep.

of theGuinea Haiti Togo

CôteCôte d’Ivoired’Ivoire Chad Congo, Rep. of Guinea-Bissau Liberia

7 Pre-Decision Point Countries

ComorosComorosEritreaEritrea SomaliaSomalia

SudanSudan KyrgyzKyrgyzRepublicRepublic

5

HIPC: Debt burdens have beenreduced markedly….

In billions of U.S. dollars, in end-2008 NPV terms

50.6

100

120

140

160

87.373.6

35.6 30.3

6.8

40.7

21.421.4

17.1

0

20

40

60

80

100

Before traditional

debt relief

After traditional debt

relief

After HIPC Initiative

debt relief

After additional

bilateral debt relief

After MDRI

24 Completion-Point Countries 11 Interim Countries

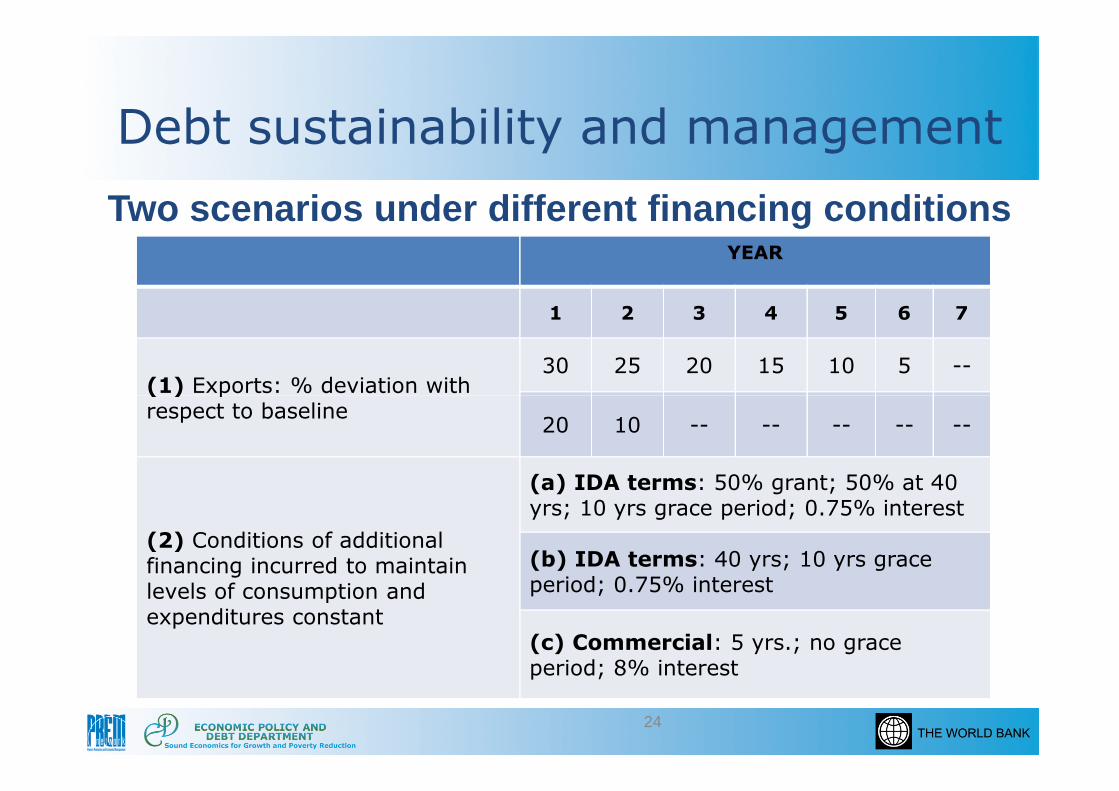

Debt sustainability and management

YEAR

1 2 3 4 5 6 7

(1) Exports: % deviation with30 25 20 15 10 5 --

Two scenarios under different financing conditions

24

(1) Exports: % deviation withrespect to baseline

20 10 -- -- -- -- --

(2) Conditions of additionalfinancing incurred to maintainlevels of consumption andexpenditures constant

(a) IDA terms: 50% grant; 50% at 40yrs; 10 yrs grace period; 0.75% interest

(b) IDA terms: 40 yrs; 10 yrs graceperiod; 0.75% interest

(c) Commercial: 5 yrs.; no graceperiod; 8% interest

Debt sustainability and management

25

Debt sustainability and management

26

Debt sustainability and management

27

Debt sustainability and management

28

Debt sustainability and management

29

Debt sustainability and management

30

Presentation Outline

• The ongoing crisis in a nutshell

• Debt Sustainability: a summary

• Debt sustainability &

31

• Debt sustainability &management in the currentenvironment

• The crisis: a protracted one?

• Room for improving the DSF?

A protracted crisis?

• Short-term responses/effects

– Fiscal stimulus packages substitute for thefall in aggregate demand

– Government’s and IFI’s lending replace– Government’s and IFI’s lending replacebanks and other financial intermediaries

– Recapitalization/lending to banks allowthem to stay in business

32

A protracted crisis?

• Long-term issues:

– Global imbalance: large deficits andaccumulation of debt in some countries(and reserve accumulation in others) needsto be reversed, a costly and difficultto be reversed, a costly and difficultadjustment.

– Further balance sheet effects may resultfrom this adjustment as some currenciesappreciate/depreciate.

– Allocation of losses among stake holders: acomplex economic and political process.

33

What will provide the next locomotivefor global growth?

8.0

12.0

United States: Personal Savings Rate and Current

Account Balance 1950 - 2008

34

-8.0

-4.0

0.0

4.0

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

Current Account Balance - % of GDP

Personal Saving Rate

Presentation Outline

• The ongoing crisis in a nutshell

• Debt Sustainability: a summary

• Debt sustainability &

35

• Debt sustainability &management in the currentenvironment

• The crisis: a protracted one?

• Room for improving the DSF?

Room for improving DSF?

• Bottom line:– DCs need growth and trade to resume

quickly (the sooner the better)

– Need cheap financing to muddle through(the more and cheaper the better)(the more and cheaper the better)

• What relaxing the DSF and relatedpolicies would accomplish?– It would allow countries greater access to

borrowing (with implications for non-concessional), but that is not necessarilythe remedy under the current conditions.

36

Room for improving DSF?

• Broadly speaking, the term “DSF” isused to address two distinct issues:

– Measurement of debt sustainability usingCPIA, DSA (“medical check up”)

– IDA/IMF policies on borrowing, including– IDA/IMF policies on borrowing, includingnon concessional (“treatment”)

– Currently the treatment allows forflexibility (the IMF is revising its ownpolicy to make it more flexible and theBank does a case by case analysis)

37

Room for improving DSF?• Is there room for improving the tests run

on the patient (“change the thermometer”)to ensure accurate prognosis? YES, work ison the pipeline for Annual Meetings,including the investment-growth nexus;

• Is there room for more flexible treatments?YES, carefully administered (family doctoris still the best suited to do this);

• Bottom line: let’s not mix up the medicaltests with the treatments (now, more thanever, LICs don’t need expensive loans).

38

The Global Financial Crisis:Implications for DebtImplications for Debt

Management

39

Leonardo HernándezPRMED

May 2009