The Global automotive market: Back on four wheels

24

Economic Outlook no.1210 August September 2014 Special Report www.eulerhermes.com The global automotive market Back on four wheels Economic Research

Transcript of The Global automotive market: Back on four wheels

Economic Outlookno.1210 August September 2014

Special Reportwww.eulerhermes.com

The globalautomotive marketBack on four wheels

Economic Research

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

2

Economic ResearchEuler Hermes Group

Economic Outlookno. 1210 Special Report

Contents

The Economic Outlook is a monthlypublication released by the EconomicResearch Department of Euler HermesGroup. This publication is for the clientsof Euler Hermes Group and available onsubscription for other businesses andorganisations. Reproduction is authorised,so long as mention of source is made.Contact the Economic Research Depart-ment Publication Director and Chief Eco-nomist: Ludovic Subran Macroeconomic Research and CountryRisk: David Semmens (Head), FrédéricAndres, Andrew Atkinson, Ana Boata,Mahamoud Islam, Dan North, DanielaOrdóñez, Manfred Stamer (Country Econ-omists)Sector and Insolvency Research:Maxime Lemerle (Head), Farah Allouche,Yann Lacroix, Marc Livinec, Didier Moizo(Sector Advisors) Support: Lætitia Giordanella (Office Man-ager), Sarah Bosse-Platière, Simon GerardsIglesias, Claudia Huisman, Ibrahim Touré,Sergey ZuevEditor: Martine Benhadj Graphic Design: Claire Mabille Photo credit: AllianzFor further information, contact theEconomic Research Department ofEuler Hermes Group at 1, place desSaisons 92048 Paris La Défense Cedex– Tel.: +33 (0) 1 84 11 50 46 – e-mail:[email protected] > EulerHermes Group is a limited companywith a Directoire and SupervisoryBoard, with a capital of EUR 14 509 497,RCS Paris B 388 236 853 Photoengraving: Imprimerie Adelinet –Permit August September 2014; issn1 162–2 881 ◾ September 5, 2014

3 EDITORIAL

4 OVERVIEW

8 AUTOMOTIVE MANUFACTURING RISKS IN 2014

10 CHINAGetting hot under the hood

12 UNITED STATESLike new!

13 JAPANAutomatic door closure

14 EUROPEA market at several different speeds

15 Spain: Fresh bodywork

15 Italy: Time to change engine(s)

16 France: In search of a higher gear

16 Germany: Solid!

17 United Kingdom: Top speed

17 Belgium: At a standstill

18 NEW PLAYERSTechnical breakdown

18 Brazil, Russia, India: Where’s the exit?

19 Thailand and Argentina: In need of repair

20 OUR PUBLICATIONS

22 SUBSIDIARIES

3

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

EDITORIAL

Fasten your seatbelt,the engine is revving up

LUDOVIC SUBRAN

Amid geopolitical crises, confidence shocks, and false startsfor growth, the disarray seems to be undermining the timidrecoveries in most economies since the start of the year. Andyet the automotive market seems to be getting its color back.When we look at global production, it seems the crisis has(finally) been erased and auto makers are returning to pre-2009 annual growth rates of around +4%. Also, the presagedend of the car has not eventuated. Despite an apparent socialpreference for usage over ownership, the emergence – al-though slowed – of middle classes continues to fuel car sales.After all, with a little more wealth people always do the samething, and this since the industrial revolution. First, they eatbetter, then they buy a first or replacement TV, then a wash-ing machine, a mobile phone, and eventually, with a littlemore money (and often a loan), we buy our first car (or tradein the old one) before thinking of buying a house. This rathersimple – but no less true – summary of the wealth effect(which does not take into account the wellbeing effect as-sociated with a car, etc.) shows, if needed, that the health ofthe automotive market remains an important factor in un-derstanding the growth dynamics of a given country. Looking at ten or so markets, including the United States,Europe, and the BRICs, the opportunities and economic risks

facing these countries are quite clear. With tumbling marketsin Thailand, Brazil, Russia, and Argentina, poor profitabilityamong European players and excessive profitability in theChinese market, the automotive sector corroborates thebroad macroeconomic trends and provides a glimpse ofwhat is to come, which is actually quite positive. In fact, look-ing at market potential, we see that the reindustrializationof the United Kingdom and the United States is being con-firmed by the return of automotive production, albeit partial;that Spain, France, and Germany are battling to save the au-tomotive sector for the political symbolism it entails, andthat Italy and Belgium are continuing to suffer. We also seethat Japan is doing wonders in its automotive market thanksto an aggressive economic policy, and that the Chinese mar-ket needs to consolidate and revise its pricing to shift up agear. There is both good news and more to be done, whilethe Paris Motor Show in a few weeks will continue to piqueour imagination between innovation, design, and hedonism.

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

4

OVERVIEW

The global automotive marketBack on four wheels

Growth in global automotiveproduction is likely to remainat around +4% per year in2014 and 2015, with anincrease in production inChina, India, and Mexico at theexpense of Europe. Productionis even expected to exceed100 million vehicles by 2017.The major componentmanufacturers, which areessential for auto makers,have relocated to followproduction and registerhealthy levels of profitability.

YANN LACROIX, THE LEAD AUTHOR OF THIS REPORT

5

On the other hand, car sales by marketreflect the economic difficulties facingvarious countries: the recovery issluggish in Europe; in the United Statesit is more pronounced, but “jobless”; inJapan it is underpinned by publicpolicies; in emerging countries it islagging behind, despite highexpectations. Euler Hermes’ forecaststhe following outlook:

1 > China. The market is soaring (+10% in2014 and +8% in 2015) but is perhaps becomingtoo profitable: selling prices will have to fall tomaintain this pace.

2 > United States. The market has finally re-turned to its pre-crisis sales level, with a -20%reduction in the workforce and renewed prof-itability. We expect the market to grow +4% in2014 and +3% in 2015, i.e. 17 million units sold.

3 > Japan. Despite its accommodating mone-tary policy and flagrant protectionism (94% ofcars sold are Japanese), the VAT hike is expectedto dent sales by -5% in 2014 and -2% in 2015.

4 > Europe. The automotive market is ex-pected to recover by +5% in 2014 and 2015, butis still a long way from its pre-crisis level. Thecannibalism among European auto makers con-tinues to rage, eating away at margins alreadysuffering from overcapacity.◾ France: the market is showing early signs ofa recovery, and sales are expected to grow +3%in 2015, but production, which continues tomove offshore and is positioned mainly in en-try-level products, has more than halved since2005. ◾ Italy: the market is still depressed (sales areexpected to come in at 1.3 million units, i.e. halftheir pre-crisis level) and production capacitycontinues to be underutilized with no hope of arapid turnaround.◾ Germany: auto makers are seeking to absorbthe increase in operating costs and investmentsvia efficiency gains and internal synergies. The

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

▶

6

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

market is expected to grow +3% in 2014 and2015.◾ Spain: automotive production is expected togrow +10% and contribute strongly to the coun-try’s trade surplus (EUR 12.5 billion in 2013)after the wage adjustments and the increase inworking hours. The market, although at half itspre-crisis level, is set to register an increase of+10% in 2014, bolstered by scrappage incen-tives.◾ United Kingdom: lthe pre-crisis level of reg-istrations, at 2.4 million units, has been regained,and the market is expected to grow +10%.◾ Belgium: The market should remain stablewhile production faces a chronic crisis (halvedby the crisis) and there is no prospect for growth.

5 > New players. The hoped-for El Dorado inemerging automotive markets has been under-mined by the series of economic and politicalcrises. For 2014, we expect registrations to fall -10% in Brazil, grow a meager +2.5% in India, andcontract -14% in Russia. A few new markets suchas Saudi Arabia, Turkey, and Malaysia are step-ping forth, but as Thailand and Argentina haveshown, economic and political risks have a directimpact on the automotive market.

Global car production hasregained cruising speed

The global market has returned to amedium-term growth rate of +4% per year and production is set to exceed 100 million ve-hicles (passenger cars and commercial vehicles)by 2017. While it is well known that the indus-trialized countries, such as the United States (ow-nership rate of 80%), Europe (ownership rate ofmore than 55%), and Japan (ownership rate of60%), do not offer great growth potential, theyremain renewal markets. With lower and, insome cases, very low ownership rates in placeslike China (5%), India (2%) or Africa, the rest ofthe world offers obvious long-term growth pros-pects. However, new, ever-cheaper and harder-wearing products will have to be invented toadapt to still-limited infrastructures and services:manufacturers are working on it.

Production has already started to switch tonew economies, as illustrated by the majorshifts between 2007 and 2013The playing field has been overturned, withstrong growth in production in some countries,chief among which China (+149%) and India(+72%), and a steep decline in industrializedcountries, with contractions of -42% in Franceand -49% in Italy. Despite the decrease in salesin Europe, production of entry-level models has

55

60

65

70

75

80

85

90

95

15f14e1312111009080706050403020100

94

World vehicle productionin millions of units

Sources: OICA, Euler Hermes forecasts

-60 -30 0 30 60 90 120 150China

India

Mexico

Brazil

South Korea

United States

Germany

United Kingdom

Japan

Spain

France

Italy -49%

-42%

-25%

-17%

-9%

-8%

2%

11%

26%

46%

72%

149%

World vehicle productioncountry change, in million of units

Sources: OICA, Euler Hermes

▶

7

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

been shifted to low-cost countries such as Slo-vakia, Slovenia, the Czech Republic, or Poland,to preserve a decent level of profitability. Therehas been strong growth in production notablyin Mexico, which in a few years has become theproduction factory for the United States; invest-ment flows in Mexico are massive and manyprojects are afoot, while domestic sales are stag-nant. Last, new zones of production are emerg-ing in Southeast Asia and North Africa.

For car sales, the economiccrisis is not yet out of rearview

Four main markets dominate global carsales: China, the United States, Europe, andJapan. China has been the largest market since2009, and its lead over the United States is

growing with each passing day. Behind thesefour dominant markets in terms of passengercar sales, emerging markets are yet to imposethemselves in terms of sales volumes. Thehoped-for El Dorado is struggling to materializeas economic and political crises slow householdvehicle ownership rates.

Car sales by market reflect the economicdifficulties facing various countries: therecovery is sluggish in Europe; in the UnitedStates it is more pronounced, but “jobless”; inJapan it is underpinned by public policies; inemerging countries it is lagging behind, despitehigh expectations. Car registrations are also amajor indicator of a country’s economic health.This report sheds light on their expectedtrends.◾

Others

India

Russia

Brazil

Japan

Europe

United States

China15%

27%

23%

17%

8%

4%

4%

2%

World sales by geographical region

Change in activity and profitability for car-part manufacturers

Sources: OICA, Euler Hermes

The major parts manufacturers havemanaged to gain from this growth inauto makers’ production movementsby massively restructuring in regions indecline and investing in growthregions.

European groups, which have posted steady growth inactivity and profits, provide the most emblematic exampleof this globalization among car-part makers and of the endof their reliance on their home market. Their operatingmargin has been much higher since 2010 than in the early2000s, thanks to greater negotiating power with automakers. We expect stable growth in this margin (ofaround 0.1pp per year) on expected sales growth of 6%per year. ◾

The big winners? Car-part manufacturers,with an operating margin of 7.5%in 2015 YANN LACROIX

FOCUS

▶

Sources: Continental, Faurecia, Valeo, Autoliv, Plastic Omnium, consensus, Euler Hermes forecasts(1) Change in revenue compared with the previous year (2) Operating profit rate = profit from operations overrevenue

Europe 2007 2008 2009 2010 2011 2012 2013 2014e 2015f

RevenueChange (1) 8.6 % 12.0 % -17.8 % 34.7 % 16.9 % 7.0 % 3.3 % 5.0 % 6.0 %

OperatingProfit Rate (2) 5.7 % 0.7 % -0.5 % 7.0 % 7.4 % 7.2 % 7.3 % 7.4 % 7.5 %

75%of global salesconcentrated in4 regions

8

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

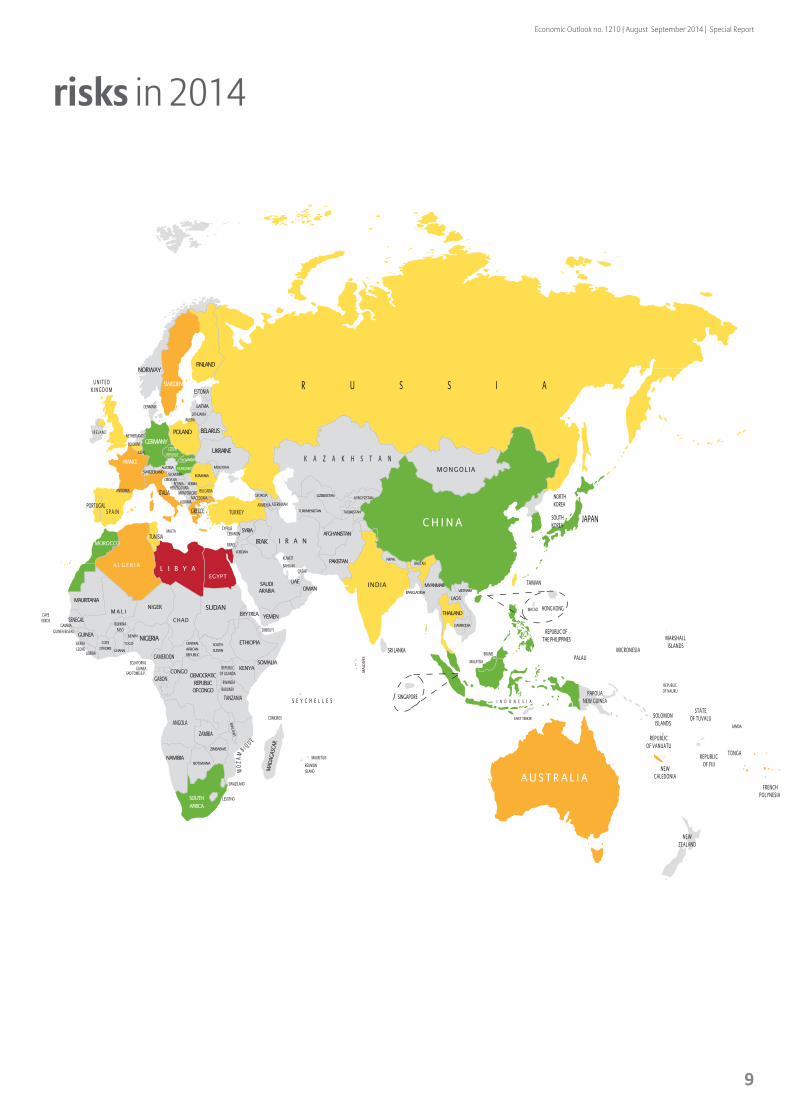

Automotive manufacturing Overall riskin the automotivesector

2014SECTOR RESEARCH TEAM

Source Euler Hermes, as of July 16, 2014

Sound fundamentals; veryfavorable or fairly good outlook.

Signs of weaknesses; possibleslowdown.

l

l

l

l

Structural weaknesses;unfavorable or fairly bad outlook.

Imminent or recongnised crisis.

9

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

risks in 2014

10

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

CHINAGetting hot under the hood

0

5

10

15

20

25United StatesChina

15f14e1312111009080706

21

17

Trend in registrations12 rolling months (in millions of units)

Sources: national statistics, Euler Hermes forecasts

China became theworld's largestmarket in 2009,surpassing theUnited States

With growth of +10% in 2014 and +8%expected for 2015, the Chinese market isextending its lead after having surpassed over-taken the US market in 2009. At nearly 20million units sold in 2014, it now accounts for27% of global sales. Moreover, with an owner-ship rate of close to 5%, it offers all auto makersvery attractive prospects for long-term growthof around +8% to +10% per year. It is a vehiclemarket whose role is growing: with 21 millionunits sold in 2015, it will be 25% larger than theUS market.

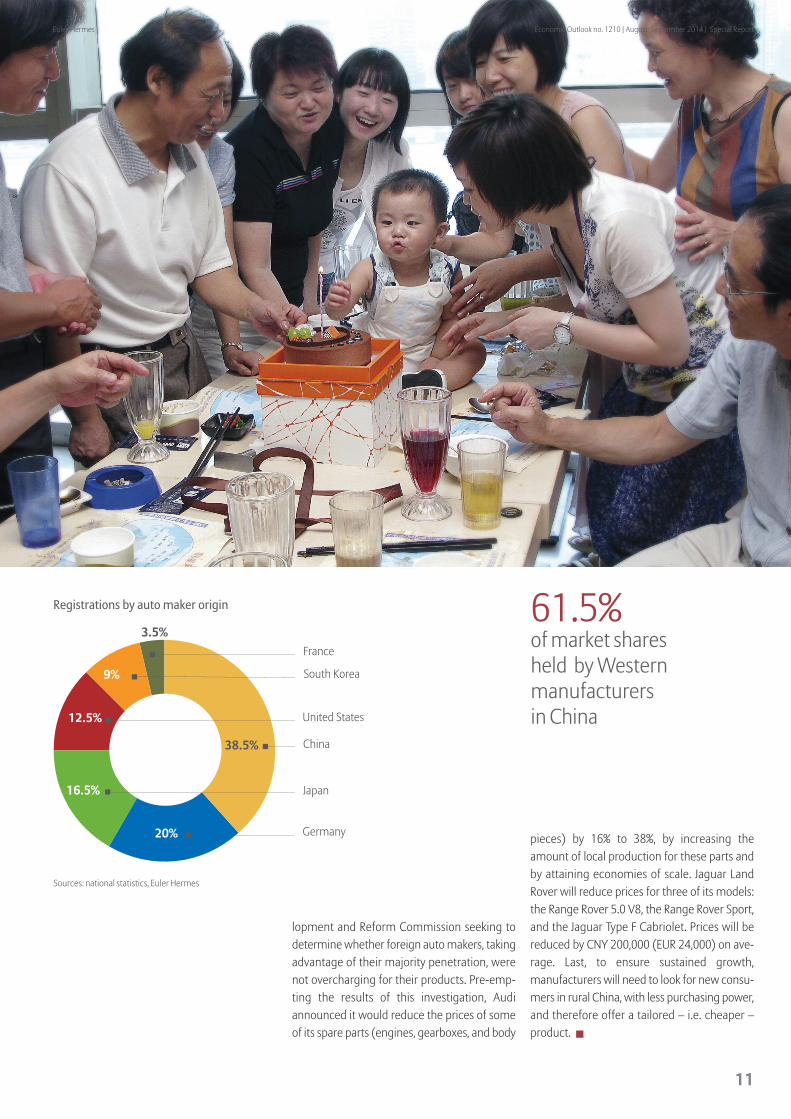

The market remains dominated by Westernmanufacturers via joint ventures with localmanufacturersThe market shares of Chinese brands, which stilllack brand power, have been declining steadily.

The difficulties of Chinese brandsAlthough the China Association of AutomobileManufacturers (CAAM) lists more than 80 pri-vate and state-owned automotive makers, onlyaround 15 of them produce more than 100,000vehicles per year. After the seven state-ownedcompanies and their joint ventures, a few privateplayers appear. The three largest private manu-facturers are Geely (owner of Volvo Cars), Great

Wall, and BYD. They produce less than 1 millionunits, which remains very little compared withinternational manufacturers. Altogether, thereare 96 Chinese brands, which produce 524 dif-ferent models, whereas in the United Statesthere are only 45 brands and 294 different mo-dels. This atomization generates low levels ofproduction per manufacturer and therefore lowmargins that impede investment in R&D. Chi-nese manufacturers invest 2% of their sales inR&D, while the corresponding figure for theirWestern counterparts is between 4% and 6%.The result is an eroding global sales perfor-mance year after year.

The market is very (too?) profitable For the Volkswagen group for example, Chinaaccounts for 30% of sales but nearly 50% of ear-nings. Selling prices may be much higher therethan elsewhere, to the benefit of manufacturerswith a sound local footing, but for how long?Audi and Jaguar Land Rover are revising theirpricing strategy in China, in response to aninvestigation carried out by the National Deve-

21 millionunits

sold in 2015

11

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

France

South Korea

United States

Japan

Germany

China

3.5%

38.5%

9%

16.5%

12.5%

20%

Registrations by auto maker origin

Sources: national statistics, Euler Hermes

lopment and Reform Commission seeking todetermine whether foreign auto makers, takingadvantage of their majority penetration, werenot overcharging for their products. Pre-emp-ting the results of this investigation, Audiannounced it would reduce the prices of someof its spare parts (engines, gearboxes, and body

pieces) by 16% to 38%, by increasing theamount of local production for these parts andby attaining economies of scale. Jaguar LandRover will reduce prices for three of its models:the Range Rover 5.0 V8, the Range Rover Sport,and the Jaguar Type F Cabriolet. Prices will bereduced by CNY 200,000 (EUR 24,000) on ave-rage. Last, to ensure sustained growth,manufacturers will need to look for new consu-mers in rural China, with less purchasing power,and therefore offer a tailored – i.e. cheaper –product. ◾

61.5% of market sharesheld by Westernmanufacturersin China

12

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

The US market represents 23%of global sales of passengervehicles (PV) and light commer-cial vehicles (LCV), or 16.5million unitsIt has become very profitable onceagain, after the deep restructuringscarried out in 2009-2010. The USautomotive industry has thus re-gained the competitiveness it hadpreviously lost: for an unchangedlevel of production, the workforcehas been reduced by -20% andmany production sites have beenshut down. Armed with a renewedand completely restructured prod-uct range, US groups have returned

to being profitable, although forGeneral Motors 2014 will be largelytarnished by massive callbacks ofits vehicles (nearly 25 million) forsafety reasons.

The US market remains verylucrative, dominated by largepickups and SUVs (the latteraccount for half of registrations)Ford generates almost all its profitsin the United States, and is the mar-ket leader with its Ford F-seriespickup (the case for many yearsnow). Nevertheless, this marketdoes not have high growth poten-tial, with an ownership rate in ex-cess of 80%. We expect growth of+4% in 2014 followed by +3% in2015. This would put the numberof registrations at around 17 millionunits in 2015. It is a renewal marketdominated by US and Japanesebrands, which represent more than83% of registrations.

2014 has been marked by bigmovements in exchange rates,affecting both consolidatedsales and profitabilityIn 2014, the average profitability ofUS car manufacturers is expectedto decrease by -1pp to 2.7% beforereturning to 3.5% in 2015. Thereare ongoing efforts to turn aroundtheir European operations, whichwill record losses yet again this year.The South American markets, inparticular the very downbeat Bra-zilian market, are also hitting pro-fits. Last, 2014 will be tough for Ge-

neral Motors due to the scale ofcallbacks following a number of ac-cidents, some fatal, which will im-pose considerable extra costs andprovisions.◾

3,000,000

6,000,000

9,000,000

12,000,000

15,000,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

1,300,000Headcount(right axis)Production (left axis)

f1514e131211100908070605

936,000

12 million

Production and workforce in the United Statesannual average

Sources: national statistics, Euler Hermes forecasts

0

10

20

30

40

50

2014

2013

GermanySouth KoreaJapanUnited States

Market share by originof auto makers in the United Statesin %

Sources: national statistics, Euler Hermes estimate

UNITED STATESLike new !

Change in activity and profitability

Sources: companies, Ford and General Motors, consensus, Euler Hermesforecasts(1) Change in revenue compared with the previous year(2) Operating profit rate = profit from operations over revenue

United States 2011 2012 2013 2014e 2015f

Revenue Change (1) 8.3 % 0.3 % 5.8 % -1.9 % 5.0 %

Operating ProfitRate (2) 5.3 % 0.9 % 3.7 % 2.7 % 3.5 %

The workforcehas beenreduced by

20%

13

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.8

6.0

15f14e131211100908070605

5

Registrations in Japan12 rolling months (in millions of units)

Sources: JAMA, Euler Hermes forecasts

Non-domestic

Japan

6%

94%

Market share by origin of automakersin Japan

Sources: national statistics, Euler Hermes

6

7

8

9

10

11

15f14e131211100908070605

9

Production in Japan12 rolling months (in millions of units)

Sources: JAMA, Euler Hermes forecasts

Foreign brandsaccount for only

6%of registrations

JAPANAutomatic door closure

Change in activity and profitability

Sources: companies, Toyota, Honda, Nissan, Mazda, Mitsubishi, consensus,Euler Hermes forecasts(1) Change in revenue compared with the previous year(2) Operating profit rate = profit from operations over revenue

Japan 2011 2012 2013 2014e 2015f

RevenueChange(1) 5.7 % -2.6 % 14.6 % 15.8 % 3.2 %

Operating Profit Rate (2) 4.0 % 2.9 % 5.5 % 7.3 % 7.3 %

Japan has cumbersome technicalbarriers in place that limit the pre-sence of Western manufacturers.As a result, foreign brands accountfor only 6% of registrations. Its mar-ket is quite closed, to the benefit ofJapanese auto makers and theirmargins.

In terms of registrations, theimpact of the VAT hike (from5% to 8%) will be seen in thesecond half of 2014, and to alesser degree in 2015Registrations are expected to fall inthe second half of 2014, for a -5%annual contraction in the volumeof sales, followed by anotheralthough smaller decrease of -2%in 2015 (the base effect of H1 2014on H1 2015 will be negative).

Japan is, however, a large pro-ducer country, where monetarypolicy and exchange rates havea big impact on producers’ prof-itabilityGrowth in volumes will be weakerthis year (+2%) due to the slow-down in the domestic market, butwill pick up to +4% in 2015. Almosthalf of production is exported, inparticular to the United States(33%), Asia and the Middle East(26%), and Europe (18%), with therest shared among South America,Africa, and Oceania.

The three largest manufactur-ers, namely Toyota, Honda, andNissan, regained a healthy levelof profitability at +7.3% in 2014,thanks to their solid presence inthe highly profitable US market,but also in China and worldwide.

They also benefit from a highlyprotected local market, whereprice competition is, accordingly,limited, and from a particularlyaggressive monetary policy. Sincethe end of 2012, the yen hasdepreciated nearly -30% againstthe euro and -20% against the dol-lar, which gives them anautomatic gain in competitivenessand therefore in profitability. Ano-ther source of profitability for thethree main Japanese manufactu-rers is their premium subsidiaries– Lexus for Toyota, Infiniti for Nis-san, and Acura for Honda – whichhave been successful in the USmarket and are beginning topenetrate the Chinese market.These subsidiaries are still strug-gling to gain a foothold in Europe,however, in the face of Germancompetition.◾

14

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

EUROPEA market at several different speeds

The European market represents more than17% of global sales, with 12.9 million unitssold. It is expected to grow by +5% in 2014and 2015It is one of the most crowded markets, whereconsiderable production overcapacity makesprofitability uncertain. Despite a few site shut-downs, mainly at Ford, Opel, and PSA, excesscapacity is still estimated at nearly 6 million units.As a result, profitability remains very low or, inthe case of some volume auto makers, negative.The automotive industry has a long way to goto complete its industrial revolution, which limitsprofitability on European soil.

Despite the recovery in sales that began in2014 and which looks set to continuethrough 2015, sales will remain 15% belowtheir pre-crisis levelsWhile the United Kingdom has regained its pre-crisis level of registrations of 2.4 million units,up +10%, the crisis continues to cast a longshadow over a number of Eastern Europeancountries, such as Romania, where sales of new

cars are six times lower than in 2007; Hungary,where they are almost three times lower; andBulgaria, where they have halved. Althoughthese three markets are extremely small (only1% of the European market), they are sympto-matic of the intensity of the crisis from whichthe European automotive industry is yet toemerge. That said, the recovery in these markets,with growth rates in excess of +10%, also showsthat the worst appears to be well behind us.

Price competition is eroding the margins ofoperators, which have had to reduce theircosts European volume auto makers have done this,and now it is the Germans’ turn.◾

Others

Italy

South Korea

Japan

United States

4%

37%

6%

15%

12%

20%

6%

Germany

France

Market share by manufacturer origin in Europe

Sources: AAA, Euler Hermes

11

12

13

14

15

16

15f14e131211100908070605

13.5

Registrations in Europe12 rolling months (in millions of units)

Sources: ACEA, Euler Hermes forecasts

Excess capacity isestimated at

6 millionsunits

15

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

◾ In 2011, Spain took the decision to in-crease the number of working hours and toadjust wages downwards to pave the wayfor an upturn in production and hiring: pro-duction is growing again at +10% in 2014 (1.9million units) and we expect +8% in 2015 (atclose to 2.05 million units). The sector has be-come a large contributor to the country’s tradesurplus, which reached EUR 12.5 billion in 2013.

The domestic market is still being stimulatedby aid programs , including a EUR 2,000 scrap-page premium on purchases of new cars. Des-pite growth in sales of +10% in 2014, at 800,000units, sales remain at half their pre-crisis level.With no support in 2015, the market can be ex-pected to stabilize at best.

◾ Italy has taken action but the main problemis the ever-decreasing supply produced by Italianauto makers, which have lost considerable mar-ket shares in Europe. Italy’s five factories aremarkedly underutilized, although productionlooks set to stabilize at around 400,000 vehiclesin 2014, up +3%. We do not see any tangiblerecovery in the short term, with growth of only+4% in 2015 to 416,000 units. The new produc-tion plan announced by FIAT’s management,for, in particular, Alfa Romeo (targeted annualsales volume of 400,000 in 2018 compared with74,000 at present) and Maserati brands will taketime before new models are launched.

Domestic demand remains in the doldrumsand shows no sign of improvement. Sales havestabilized at 1.3 million units in 2013 and 2014,with an uptick of around +5% expected in 2015.This will nevertheless keep the market a longway off pre-crisis levels, which peaked at 2.5million units. With an ageing fleet, the Italiangovernment is also considering tax measuresto boost the market.◾

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

15f14e131211100908070605

0.4

Production in Italy12 rolling months (in millions of units)

Sources: ANFIA, Euler Hermes forecasts

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

2

15f14e131211100908070605

2

Production in Spain12 rolling months (in millions of units)

Sources: ANFAC, Euler Hermes forecasts

Spain: Fresh bodyworkItaly: Time to change engine(s)

In 2014, Spanish productionis growingagain at

+10%Annual Italian

production

400,000vehicles

16

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

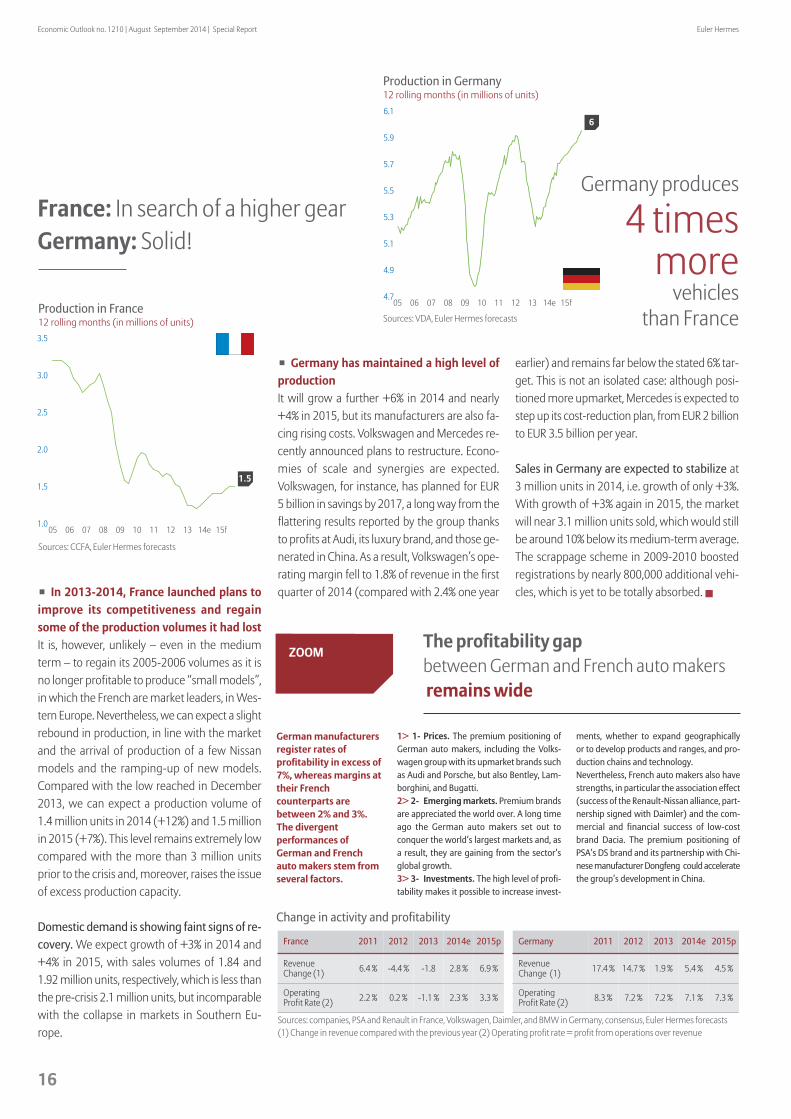

France: In search of a higher gearGermany: Solid!

◾ In 2013-2014, France launched plans toimprove its competitiveness and regainsome of the production volumes it had lostIt is, however, unlikely – even in the mediumterm – to regain its 2005-2006 volumes as it isno longer profitable to produce “small models”,in which the French are market leaders, in Wes-tern Europe. Nevertheless, we can expect a slightrebound in production, in line with the marketand the arrival of production of a few Nissanmodels and the ramping-up of new models.Compared with the low reached in December2013, we can expect a production volume of1.4 million units in 2014 (+12%) and 1.5 millionin 2015 (+7%). This level remains extremely lowcompared with the more than 3 million unitsprior to the crisis and, moreover, raises the issueof excess production capacity.

Domestic demand is showing faint signs of re-covery. We expect growth of +3% in 2014 and+4% in 2015, with sales volumes of 1.84 and1.92 million units, respectively, which is less thanthe pre-crisis 2.1 million units, but incomparablewith the collapse in markets in Southern Eu-rope.

◾ Germany has maintained a high level ofproductionIt will grow a further +6% in 2014 and nearly+4% in 2015, but its manufacturers are also fa-cing rising costs. Volkswagen and Mercedes re-cently announced plans to restructure. Econo-mies of scale and synergies are expected.Volkswagen, for instance, has planned for EUR5 billion in savings by 2017, a long way from theflattering results reported by the group thanksto profits at Audi, its luxury brand, and those ge-nerated in China. As a result, Volkswagen’s ope-rating margin fell to 1.8% of revenue in the firstquarter of 2014 (compared with 2.4% one year

earlier) and remains far below the stated 6% tar-get. This is not an isolated case: although posi-tioned more upmarket, Mercedes is expected tostep up its cost-reduction plan, from EUR 2 billionto EUR 3.5 billion per year.

Sales in Germany are expected to stabilize at3 million units in 2014, i.e. growth of only +3%.With growth of +3% again in 2015, the marketwill near 3.1 million units sold, which would stillbe around 10% below its medium-term average.The scrappage scheme in 2009-2010 boostedregistrations by nearly 800,000 additional vehi-cles, which is yet to be totally absorbed.◾

Change in activity and profitability

Sources: companies, PSA and Renault in France, Volkswagen, Daimler, and BMW in Germany, consensus, Euler Hermes forecasts(1) Change in revenue compared with the previous year (2) Operating profit rate = profit from operations over revenue

1.0

1.5

2.0

2.5

3.0

3.5

15f14e131211100908070605

1.5

Production in France12 rolling months (in millions of units)

Sources: CCFA, Euler Hermes forecasts

4.7

4.9

5.1

5.3

5.5

5.7

5.9

6.1

15f14e131211100908070605

6

Production in Germany12 rolling months (in millions of units)

Sources: VDA, Euler Hermes forecasts

German manufacturersregister rates ofprofitability in excess of7%, whereas margins attheir Frenchcounterparts arebetween 2% and 3%.The divergentperformances ofGerman and Frenchauto makers stem fromseveral factors.

The profitability gap between German and French auto makersremains wide

1> 1- Prices. The premium positioning ofGerman auto makers, including the Volks-wagen group with its upmarket brands suchas Audi and Porsche, but also Bentley, Lam-borghini, and Bugatti.2> 2- Emerging markets. Premium brandsare appreciated the world over. A long timeago the German auto makers set out toconquer the world’s largest markets and, asa result, they are gaining from the sector’sglobal growth.3> 3- Investments. The high level of profi-tability makes it possible to increase invest-

ments, whether to expand geographicallyor to develop products and ranges, and pro-duction chains and technology.Nevertheless, French auto makers also havestrengths, in particular the association effect(success of the Renault-Nissan alliance, part-nership signed with Daimler) and the com-mercial and financial success of low-costbrand Dacia. The premium positioning ofPSA’s DS brand and its partnership with Chi-nese manufacturer Dongfeng could acceleratethe group’s development in China.

ZOOM

Germany produces

4 timesmore

vehiclesthan France

France 2011 2012 2013 2014e 2015p

RevenueChange (1) 6.4 % -4.4 % -1.8 2.8 % 6.9 %

Operating Profit Rate (2) 2.2 % 0.2 % -1.1 % 2.3 % 3.3 %

Germany 2011 2012 2013 2014e 2015p

RevenueChange (1) 17.4 % 14.7 % 1.9 % 5.4 % 4.5 %

Operating Profit Rate (2) 8.3 % 7.2 % 7.2 % 7.1 % 7.3 %

17

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

◾ The United Kingdom has regained its pre-crisis levelsIn terms of production, the market will reacharound 1.6 million passenger vehicles in 2015,i.e. the level produced in 2005, after a very toughperiod during which historic manufacturers di-sappeared. Who still remembers British groupLeyland, which comprised the Jaguar, Rover andLand Rover, Austin Morris, and Wolseley brands?In its day it accounted for 40% of the market. To-day the factories are labelled Nissan, Honda,Toyota, Ford, Vauxhall (subsidiary of General Mo-tors), Mini (subsidiary of BMW), and Jaguar LandRover (subsidiary of Indian conglomerate Tata).Nevertheless, thanks to the flexibility of its labormarket and to its increasingly attractive corporatetax regime, the United Kingdom has once againbecome a true producer of cars, with annual pro-duction growth of around +3%.

It also benefits from a buoyant domestic de-mand, with the market forecast to grow +8%in 2014 and a further +3% in 2015, to 2.5 millionunits. It is one of the few markets to have sur-passed, albeit just, its pre-crisis level.

◾ The European automotive crisis has takena heavy toll on Belgium with the closure of theOpel site in Antwerp in 2010 and the scheduledshutdown of Ford’s site in Genk by the end of2014. After 900,000 passenger vehicles were pro-duced in 2006, production collapsed to less than450,000 units in 2013. Its marked decline conti-nues. 2015 production is thus expected to fallbelow 400,000 units. Without a national auto

maker, Belgium has been a loser in trade-offsbetween location and production costs.Its domestic demand has stabilized on the wholeunder 500,000 units. This should also be the casefor 2014 and 2015, which, ultimately, makes Bel-gium a small European market.◾

United Kingdom: Top speedBelgium: At a standstill

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

15f14e131211100908070605

0.4

Production in Belgium12 rolling months (in millions of units)

Sources: FEBIAC, Euler Hermes forecasts

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

15f14e131211100908070605

1.6

Production in the United Kingdom12 rolling months (in millions of units)

Sources: SMMT, Euler Hermes forecasts

2015 productionUnited Kingdom

1.6 millionBelgium

fell below

400,000units

◾ While India seems to be gradually awak-ening from its slumber, sales volumes re-main confined to 1.8 million units, in a popu-lation of more than 1 billion inhabitants. Itsmarket remains ten times smaller than the Chi-nese market, with a very low ownership rate ofaround 2%. The weak purchasing power and in-frastructure deficiencies continue to hold backstrong growth, although the long-term potentialremains. For 2014 we expect weak growth ofaround +2.5%. A new type of ultra-low-cost ve-hicle will need to be developed, in keeping withthe country’s needs and means.

◾ The Brazilian market is more of a concernWhereas it was thought it would be the mo-ney-spinner of South America, the country hasbeen in recession since the spring of 2013, andits auto market looks set to register an annualcontraction of around -10% in 2014 followed bya slight recovery of +3% in 2015. After havingreached 3 million units, sales are expected tolabor to 2.5 million at end-2014. A number ofmanufacturers have increased their productioncapacity in the country and therefore currentlyface a shortfall in profitability in this market.

18

NEW PLAYERSTechnical breakdown

Brazil, Russia, India: Where’s the exit?

◾ Finally, the Russian market remainschaotic, which has hit local investmentWhile the government wants to develop the lo-cal automotive industry and has put in placeimport taxes and requirements for auto makersto increase their local content rate, the recentgeopolitical developments are jeopardizing thisindustrialization. Here again, a number of ma-

nufacturers have registered losses, such as localleader Avtovaz (Lada brand), a subsidiary of Re-nault-Nissan.

In a context of economic crisis (including aninterest rate at 12%) and under the effect ofthe sanctions announced, we expect a slumpof -14% in 2014, after a fall of nearly -6% in2013. Sales are expected to begin to recover byaround +5% over the course of 2015 to 2.5 mil-lion units, which is still a long way from their2013 level of nearly 3 million units. However,there is a need to consider the effects of financialsupport for the sector and of a possible borderclosure to vehicle imports depending on the se-verity of the sanctions (27% of sales in the firsthalf of 2014 were imported vehicles). This wouldmainly affect the premium auto makers that donot have local production sites. Last, note the in-troduction on September 1 2014 of a scrappagepremium (EUR 825 per vehicle) until 31 Decem-ber 2014 to curb the market’s fall and perhapsreduce the stocks of manufacturers, which haveall announced production cutbacks.◾

0.5

1.0

1.5

2.0

2.5

3.0 ProductionRegistrations

15f14e131211100908070605

2

2.5

Registrations and production in India12 rolling months (in millions of units)

Sources: SIAM, Euler Hermes forecasts

1.0

1.5

2.0

2.5

3.0

3.5

4.0 ProductionRegistrations

15f14e131211100908070605

3.2

2.6

Registrations and production in Brazil12 rolling months (in millions of units)

Sources: ANFAVEA, Euler Hermes forecasts

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

15f14e13121110090807

2.5

Registrations in Russia12 rolling months (in millions of units)

Sources: OAR, Euler Hermes forecasts

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

Registrationsin 2014

Brazil -10 %Russia -14 %India +2.5 %

19

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

Thailand and Argentina: In need of repair

The large automotive groups will have to turnto new emerging countries over the next fewyears if they want to sustain their globalgrowth. Some countries offer real growth op-portunities, albeit still modest in size. Not toomuch should be expected for Western auto ma-kers, as these countries could be firmly in thesights of Chinese manufacturers whose deve-lopment in mature markets still seems fraughtwith difficulty owing to the technical and envi-ronment constraints imposed in Europe and theUnited States. Thailand, Indonesia, Malaysia, Tur-key, and Saudi Arabia form the last opportunitiesfor growth in a world where markets are eithermature or underdeveloped and where the keypositions have already been taken. But cautionis called for, as national markets can fluctuatewildly, as illustrated by the cases of Thailand andArgentina.

◾ The Thai market appeared to offer brightprospects, albeit bolstered by scrappage in-centives in 2012 and early 2013 after the 2011floods in the country. However, the market hasfallen drastically under the effect of the political

crisis since late 2013 and the military coup. Thestill-uncertain situation points to a bad 2014,with a possible -36% fall in sales to 410,000 units,followed by a rebound of around +10% in 2015,which would return the market to its 2005 level.Pending better days, Thailand, which had alsobecome a production zone for Southeast Asia,has seen its activity contract sharply and its in-vestment prospects dry up.

◾ Argentina: A fall in 2014 (-30%) followedby the beginnings of a recovery (+10%) in2015Under the weight of the economic and financialcrisis afflicting Argentina, sales have collapsedsince January 2014 following the 18% devalua-tion of the Argentine peso, leading to a spike inprices and the introduction of a 50% tax on pur-chases of high-end vehicles. To boost sales andproduction, in June the government launcheda plan to facilitate car purchases on credit, whichnational association ADEFA hopes will have animpact towards the end of the year. Neverthe-less, 2014 will be marked by a fall of -30%, follo-wed by an incipient recovery in 2015, up +10%.

In addition to the collapse in its domestic market,Argentina is also affected by difficulties in itslargest export market: Brazil. The situation re-presents a direct threat for French auto makers,which have a more than 25% share of the Ar-gentine automotive market. Other manufactu-rers, such as Volkswagen, FIAT, Ford, GM, andToyota are also exposed to an economic down-turn in this country.◾

0.2

0.4

0.6

0.8

1.0 ProductionRegistrations

15f14e131211100908070605

0.6

0.5

Registrations and production in Argentina12 rolling months (in millions of units)

Sources: ADEFA, Euler Hermes forecasts

A fall in salesin Thailand

-36%in 2014

0.2

0.3

0.4

0.5

0.6

0.7

0.8

15f14e131211100908070605

0.4

Registrations in Thailand12 rolling months (in millions of units)

Sources: TAIE, Euler Hermes forecasts

Argentina

-30%in sales in 2014

20

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

Economic ResearchEuler Hermes Group

Economic Outlookand otherpublications

Already issued:

no. 1191 ◽ Global Sector Outlook Now where did global demand go?

no. 1192 ◽ Special Report Trade Routes: What has changed, what will change

no. 1193 ◽ Macroeconomic, Risk and Insolvency Outlook Europe: Still looking for a second wind

no. 1194 ◽ Business Insolvency Worldwide Corporate insolvencies:The true nature of the eurozone crisis

no. 1195-1196 ◽ Macroeconomic, Risk and Insolvency Outlook The world at a crossroads

no. 1197 ◽ Global Sector Outlook Reconciling economic (dis)illusions and financial risks

no. 1198 ◽ Special Report The Mediterranean: Turning the tide

no. 1199 ◽ Macroeconomic and Country Risk Outlook Half-baked recovery

no. 1200-1201 ◽ Business Insolvency Worldwide Patching things up: Fewer insolvencies, except in Europe

no. 1202-1203 ◽ Macroeconomic and Country Risk Outlook Top Ten Game Changers in 2014: Getting back in the game

no. 1204 ◽ Global Sector Outlook All things come to those who wait: Green shoots for one out of four sectors

no. 1205-1206 ◽ Macroeconomic and Country Risk Outlook Hot, bright and soft spots: Who could make or break global growth?

no. 1207 ◽ Business Insolvency Worldwide Insolvency World Cup 2014: Who will score fewer insolvencies?

no. 1208-1209 ◽ Macroeconomic, Country Risk and Global Sector Outlook Growth: A giant with feet of clay

no. 1210 ◽ Special Report The global automotive market: Back on four wheels

To come:

no. 1211 ◽ Special Report

Macroeconomic, Country Riskand Global Sector Outlook

Economic Outlookno. 1208-1209June-July 2014

www.eulerhermes.com

Growth: A giantwith feet of clay10 industry short stories exposemacroeconomic fragility

Economic Research

Macroeconomicand Country Risk Outlook

EconomicOutlook no. 1205-1206March-April 2014

www.eulerhermes.com

Hot, brightand soft spots:Who could make or breakglobal growth?

Economic Research

Global Sector Outlook

Economic Outlookno.1204 February 2014

www.eulerhermes.com

All things cometo those who waitGreen shoots for one out of four sectors

Economic Research

1 :

Business Insolvency Worldwide

Economic Outlookno. 1207May 2014

www.eulerhermes.com

InsolvencyWorld Cup 2014: Who will score fewer insolvencies?

Economic Research

21

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

https://www.youtube.com/watch?feature=player_detailpage&v=EhZaQnqR3TE

◽Non-payments in Italy: It’s not over… yet! > 2014-09-04 (En)◽Don’t cry too much for Argentina > 2018-08-08 (En)◽ Fertilizer: The seed growing secretly > 2014-08-05 (En, Fr)◽ Road transport: Labor costs explain the large gap in profitability inEurope > 2014-07-08 (En, Fr)◽The European electricity market under strong pressure > 2014-07-05(En, Fr)◽Thailand: Another coup challenges the country’s economicresiliencel > 2014-06-06 (En)◽2014 World Cup : more inflation than growth in Brazil > 2014-06-06(En)◽Tire industry on a roll >2014-04-17(En, Fr)◽Putinomics: Tightrope walking > 2014-04-10(En)◽Renzimania: Will charm survive tough reforms? >2014-04-09 (En)◽The reindustrialization of the U.S.: A 2014 update > 2014-04-02 (En)◽Fewer non-payments in 2013for Italian companies, but moresevere > 2014-02-19(En)

EconomicInsight

◽Belgium > 2014-06-30◽Burkina-Faso > 2014-06-30◽Chile > 2014-06-30◽China > 2014-06-30 ◽Colombia > 2014-06-30◽Cote d'Ivoire > 2014-06-30◽Croatia > 2014-06-30 ◽Czech Republic > 2014-06-30◽France > 2014-06-30◽Germany > 2014-06-30◽Greece > 2014-06-30◽Hungary > 2014-06-30◽India > 2014-06-30 ◽Ireland > 2014-06-30◽Italy > 2014-06-30◽Malaysia > 2014-06-30◽Morocco > 2014-06-30◽Namibia > 2014-06-30

◽Nicaragua > 2014-06-30◽Nigeria > 2014-06-30◽Panama > 2014-06-30◽Peru > 2014-06-30◽Poland > 2014-06-30◽Portugal > 2014-06-30◽Senegal > 2014-06-30◽Serbia > 2014-06-30◽Singapore > 2014-06-30◽South Africa > 2014-06-30 ◽Spain > 2014-06-30◽Tanzania > 2014-06-30◽Thailand > 2014-06-30◽Turkey > 2014-06-30◽United Arab Emirates> 2014-06-30◽United Kingdom > 2014-06-30◽United States > 2014-06-30

CountryReport

WeeklyExport RiskOutlook

◽Construction in Germany: Betongold at a turning point? > 2014-08-07 (En)◽Construction in South Korea: not out of the woods yet > 2014-08-07 (En)◽Machinery andEquipment in Italy: Preparing its comeback > 2014-06-23(En)◽Pharmaceuticals in China: At full volume > 2014-06-24 (En, Fr)◽High-Tech in the Netherlands: A gem at the heart of Europe > 2014-04-29 (En)◽Pharmaceuticals in Russia: A high-growth market mainly benefiting Western laboratories (untilnow) > 2014-04-18 (En, Fr)◽The chemicals industry in Germany: Challenging times ahead despite a recent gasp of relief> 2014-04-15 (En)◽The Italian wine industry: In vino veritas, leading the way out of the crisis > 2014-04-15 (En, It)◽Baumärkte Deutschland: 2014 - noch ein verregnetes Jahr ? > 2014-04-18 (De)◽ Secteur de la construction en France : valoriser un potentiel de croissance en accélérant la sortiede crise > 2014-03-26 (Fr)

IndustryReport

http://www.eulerhermes.com/economic-research/economic-publi-NN

TheEconomicTalk

22

Economic Outlook no. 1210 | August September 2014 | Special Report Euler Hermes

> ArgentinaSolunionAv. Corrientes 299 C1043AAC CBA,Buenos AiresPhone: + 54 11 4320 9048

> AustraliaEuler Hermes Australia Pty LtdLevel 9, Forecourt Building2 Market StreetSydney, NSW 2000Phone: + 61 2 8258 5108

> AustriaAcredia Versicherung AGHimmelpfortgasse 291010 ViennaPhone: + 43 5 01 02-1111

Euler Hermes Collections GmbHZweigniederlassung ÖsterreichHandelskai 3881020 ViennaPhone: + 43 1 90 227 14000

> BahrainPlease contact United Arab Emirates

> BelgiumEuler Hermes Europe SA (NV) Avenue des Arts — Kunstlaan, 56 1000 BrusselsPhone: + 32 2 289 3111

> BrazilEuler Hermes Seguros de Crédito SAAvenida Paulista, 2,421 — 3° andarJardim PaulistaSão Paulo / SP 01311-300Phone: + 55 11 3065 2260

> CanadaEuler Hermes North America InsuranceCompany1155, René-Lévesque Blvd WestBureau 2810Montréal Québec H3B 2L2Phone : +1 514 876 9656 / +1 877 509 3224

> ChileSolunion Av. Isidora Goyenechea, 3520SantiagoPhone: + 56 2 2410 5400

> ChinaEuler Hermes Consulting (Shanghai) Co.,Ltd. Unit 2103, Taiping Finance Tower, N°488 Middle Yincheng Road, Pudong New Area, Shanghai, 200120Phone: + 86 21 6030 5900

> ColombiaSolunionCalle 7 Sur No. 42-70Edificio Fōrum II Piso 8MedellinPhone : +57 4 444 01 45

SubsidiariesRegistered office:Euler Hermes Group 1, place des Saisons 92078 Paris La Défense - FranceTel.: + 33 (0) 1 84 11 50 50

www.eulerhermes.com

> Czech RepublicEuler Hermes Europe S.A. organizacni slozkaMolákova 576/11186 00 Prague 8Phone: + 420 266 109 511

> DenmarkEuler Hermes Danmark, filial ofEuler Hermes Europe S.A. BelgienAmerika Plads 192 100 Copenhague OPhone: + 45 88 33 33 88

> EstoniaPlease contact Finland

> FinlandEuler Hermes Europe SASuomen sivuliikeMannerheimintie 10500280 HelsinkiPhone: + 358 10 850 8500

> FranceEuler Hermes France SAEuler Hermes CollectionsEuler Hermes World Agency1, Place des SaisonsF-92 048 Paris La DéfensePhone: + 33 1 84 11 50 50

> GermanyEuler Hermes Deutschland AGFriedensallee 25422763 HamburgPhone: + 49 40 8834 0

Euler Hermes AktiengesellschaftGaastraße 2722761 HamburgPhone: + 49 40 8834 9000

Euler Hermes Collections GmbHZeppelinstr. 4814471 PostdamPhone: + 49 331 27890 000

Euler Hermes Rating GmbHFriedensallee 25422763 HambourgPhone: + 49 40 8 34 640

Euler Hermes Liaison Office at AGCSAllianz Global Coroporate & Specialty AGFritz-Schäffer-Straße 981737 MünchenPhone: + 49 89 38 00 12 159

> GreeceEuler Hermes HellasCredit Insurance SA16 Laodikias Street & 1-3 Nymfeou StreetAthens Greece 11528 Phone: + 30 210 69 00 000

> Hong KongEuler Hermes Hong Kong Services LtdSuites 403-11, 4/F - Cityplaza 412 Taikoo Wan Road Island EastHong KongPhone: + 852 3665 8901

> HungaryEuler Hermes Europe SAMagyarrorszagi FioktelepeEuler Hermes Magyar Követeléskezelõ Kft.(trade debt collection)Kiscelli u. 1041037 BudapestPhone: +36 1 453 9000

> IndiaEuler Hermes India Pvt.Ltd5th Floor, Vaibhav Chambers Opposite Income Tax OfficeBandra Kurla ComplexBandra (East)Mumbai 400 051Phone: +91 22 6623 2525

> IndonesiaPT Asuransi Allianz Utama IndonesiaSummitmas II. Building, 9th FloorJl. Jenderal Sudirman Kav 61-62Jakarta 12190Phone: +62 21 252 2470 ext. 6100

> IrelandEuler Hermes IrelandAllianz HouseElm ParkMerrion RoadDublin 4Phone: +353 (0)1 518 7900

> IsraelICIC2, Shenkar Street68010 Tel AvivPhone: +97 23 796 2444

> ItalyEuler Hermes Europe SARappresentanza generale per l’ItaliaVia Raffaello Matarazzo, 1900139 RomePhone: + 39 06 8700 1

> JapanEuler Hermes Deutschland AG, Japan BranchKyobashi Nisshoku Bldg 7th floor8-7, Kyobashi, 1-chome,Chuo-KuTokyo 104-0031Phone: + 81 3 35 38 5403

> KuwaitPlease contact United Arab Emirates

> LatviaPlease contact Sweden

23

Euler Hermes Economic Outlook no. 1210 | August September 2014 | Special Report

> LithuaniaPlease contact Denmark

> MalaysiaEuler Hermes Singapore Services Pte Ltd.,Malaysia BranchSuite 3B-13-7, Level 13, Block 3BPlaza Sentral, Jalan Stesen Sentral 550470 Kuala LumpurPhone: +603 2264 8556 (or 8599)

> MexicoSolunionTorre PolancoMariano Escobedo 476, Piso 15Colonia Nueva Anzures11590 Mexico D.F.Phone: +52 55 52 01 79 00

> MoroccoEuler Hermes Acmar37, bd Abdelatiff Ben Kaddour20 050 CasablancaPhone: + 212 5 22 79 03 30

> The NetherlandsEuler Hermes NederlandPettelaarpark 20P.O. Box 707515201CZ’s-HertogenboschPhone: + 31 (0) 73 688 99 99 / 0800 385 37 65

Euler Hermes BondingDe Entree 67 (Alpha Tower)P.O. Box 124731100 AL AmsterdamPhone: +31 (0) 20 696 39 41

> New ZealandEuler Hermes New Zeland LtdLevel 1, 152 Fanshawe StreetAuckland 1010Phone: + 64 9 354 2995

> NorwayEuler Hermes NorgeHolbergsgate 21 P.O. Box 6 875St. Olavs Plass0130 OsloPhone: + 47 2 325 6000

> OmanPlease contact United Arab Emirates

> PhilippinesPlease contact Singapore

> PolandTowarzystwo Ubezpieczen Euler Hermes SAul. Domaniewska 50 B02-672 VarsawPhone: + 48 22 363 6363

> PortugalCOSEC Companhia de Seguro deCréditos, S.A.Avenida da República, nº 581069-057 LisbonPhone: + 351 21 791 3700

> QatarPlease contact United Arab Emirates

> RomaniaEuler Hermes Europe SA BruxellesSucursala BucurestiStr. Petru Maior Nr.6Sector 1 011264 BucarestPhone: + 40 21 302 0300

> RussiaEuler Hermes Credit Management OOOOffice C08, 4-th Dobryninskiy per., 8,Moscou, 119049Phone: + 7 495 9812 8 33 ext.4000

> Saudi ArabiaPlease contact United Arab Emirates

> SingaporeEuler Hermes Singapore Services Pte Ltd12 Marina View#14-01 Asia Square Tower 2Singapore 018961Phone: + 65 6297 8802

> SlovakiaEuler Hermes Europe SA, pobokapoist’ovne z ineho clenskeho statu2012: Plynárenská 7/A82109 BratislavaPhone: + 421 2 582 80 911

> South AfricaPlease contact Italy

> South KoreaEuler Hermes Hong Kong ServicesKorea Liaison OfficeRm 1411, 14/F, SayongPlatinum Bldg156, Cheokseon-dong,Chongro-ku,Seoul 110-052,Phone: + 82 2 733 8813

> SpainSolunionAvda. General Perón, 40Edificio Moda ShoppingPortal C, 3a planta28020 MadridPhone: +34 91 581 34 00

> Sri LankaPlease contact Singapore

> SwedenEuler Hermes Sverige filialKlarabergsviadukten 90P.O. Box 729101 64 StockholmPhone: + 46 8 5551 36 00

> SwitzerlandEuler Hermes Deutschland AG,Zweigniederlassung ZürichRichtiplatz 1Postfach8304 WallisellenPhone : + 41 44 283 65 65Phone : + 41 44 283 65 85 (Reinsurance)

> TaiwanPlease contact Hong Kong

> ThailandAllianz C.P. General Insurance Co., Ltd323 United Center Building30 th FloorSilom Road.Bangrak, Bangkok 10500Phone+ 66 2638 9000

> TunisiaPlease contact Italy

> TurkeyEuler Hermes Sigorta A.S.Buyukdere Cad. No :100-102Maya Akar Center Kat: 7 Esentepe34394 Şișli/ IstanbulPhone: +90 212 2907610

> United Arab EmiratesEuler Hermesc/o Alliance Insurance (PSC)Warba Centre, 4th Floor Office 405PO Box 183957DubaiPhone: + 971 4 211 6005

> United KingdomEuler Hermes UK1 Canada SquareLondres E14 5DXPhone: + 44 20 7 512 9333

> United StatesEuler Hermes North AmericaInsurance Company800 Red Brook BoulevardOwings Mills, MD 21117Phone: + 1 877 883 3224

> VietnamPlease contact Singapore

Euler Hermes Economic Outlookis published monthly by the Economic Research Departmentof Euler Hermes Group1, place des Saisons, F-92048 Paris La Défense Cedex e-mail: [email protected] - Tel. : +33 (0) 1 84 11 50 50

This document reflects the opinion of the Economic Research Department of Euler Hermes Group.

The information, analyses and forecasts contained herein are based on the Department's current

hypotheses and viewpoints and are of a prospective nature. In this regard, the Economic Research

Department of Euler Hermes Group has no responsibility for the consequences hereof and no

liability. Moreover, these analyses are subject to modification at any time.

www.eulerhermes.com

EconomicOutlook