The Future of High-Carbon Assets The Triple Bottom Line: TBH ...

20

CrimsonFinancier The Future of High-Carbon Assets By Morgan Bui & Carolin Schellhorn, Ph.D. The Triple Bottom Line: TBH about the TBL By Robert A. Jankiewicz Why People Should Embrace Sustainable Investing By Audrey Rusnak Spring 2016

Transcript of The Future of High-Carbon Assets The Triple Bottom Line: TBH ...

CrimsonFinancier

The Future of High-Carbon

Assets

By Morgan Bui & Carolin

Schellhorn, Ph.D.

The Triple Bottom Line: TBH

about the TBL

By Robert A. Jankiewicz

Why People Should Embrace

Sustainable Investing

By Audrey Rusnak

Spring 2016

2

Editor-in-Chief

Lisa Aquino, 2016

Junior Editor

Bianca Luscher, 2018

President of the

Finance Society

Joseph Wutkowski, 2016

Contributors

Rachael Ranieri, 2016

Audrey Rusnak, 2016

Morgan Bui, 2017

Andrew Chirichella, 2017

Peter Golish, 2017

Michael Baldini, 2018

Robert Jankiewicz, 2018

Patrick Michael, 2018

Faculty

Contributor

Carolin Schellhorn, Ph. D.,

Department of Finance

Faculty Advisor

Carolin Schellhorn, Ph. D.,

Department of Finance

Letter from the Editor

Crimson Financier is an academic journal created and edit-ed by students at Saint Joseph’s University (SJU), a Jesuit institu-tion. This publication provides a platform for both students and faculty to publish their written works. Crimson Financier explores the next wave of financial and investing trends and connects them to Ignatian values. Cura personalis (care for the whole person) is more than a phrase written in an ancient language; it promotes the desire to live greater in all aspects of life, including business careers.

The Finance Society is proud to present the second issue of Crimson Financier. While the first issue of our publication fo-cused on the trend of impact investing, this issue highlights com-panies practicing impact investing and the effect on their triple bot-tom lines.

The articles within this issue will explore the meaning be-hind the triple bottom line and the reasons supporting stakeholder-focused strategies. It will also shed light on the sustainable pro-grams and efforts of various companies as well as various sus-tainable investment instruments that have arisen in recent years.

We are pleased to have Dr. Carolin Schellhorn from the SJU Department of Finance contribute another article to this is-sue. Dr. Schellhorn and 2015 Summer Scholar, Morgan Bui, dis-cuss the impact of the December 2015 Paris conference (COP21) in regards to climate change, sustainability and high-carbon as-sets.

Crimson Financier would like to take this opportunity to sin-cerely thank Dr. Schellhorn for her unwavering support in the pro-cess of creating this publication.

The encouragement of the Pedro Arrupe Center for Busi-ness Ethics has been unparalleled. We are grateful as the Arrupe Center continues to promote this journal and partner with us to sponsor events that educate students about sustainable investing. Congratulations to the Arrupe Center on 10 years of making ethics a priority for the Haub School of Business.

We also greatly appreciate the time and effort of each of the journal’s contributors. Creating a foundation for a new publica-tion is not an easy task, and Crimson Financier would not exist

without them. ♦

Lisa Aquino, 2016

Spring 2016

ISSUE 2

3

Title

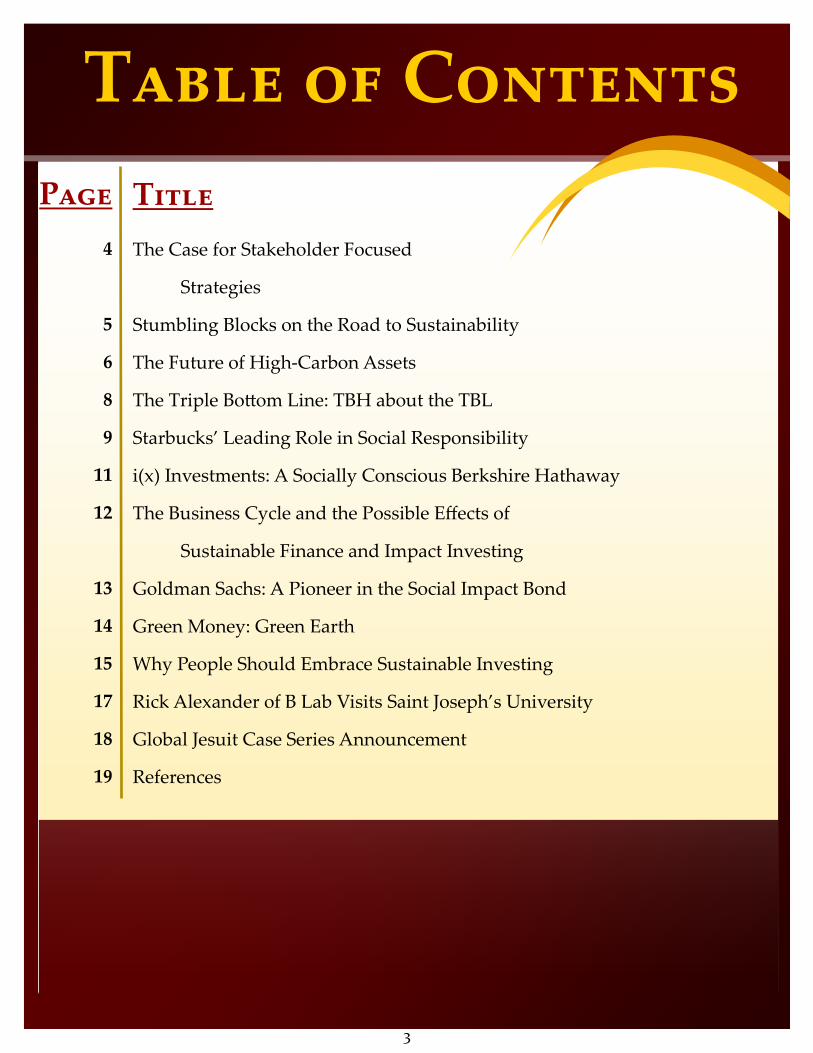

The Case for Stakeholder Focused

Strategies

Stumbling Blocks on the Road to Sustainability

The Future of High-Carbon Assets

The Triple Bottom Line: TBH about the TBL

Starbucks’ Leading Role in Social Responsibility

i(x) Investments: A Socially Conscious Berkshire Hathaway

The Business Cycle and the Possible Effects of

Sustainable Finance and Impact Investing

Goldman Sachs: A Pioneer in the Social Impact Bond

Green Money: Green Earth

Why People Should Embrace Sustainable Investing

Rick Alexander of B Lab Visits Saint Joseph’s University

Global Jesuit Case Series Announcement

References

Table of Contents

Page

4

5

6

8

9

11

12

13

14

15

17

18

19

4

The Case for Stakeholder Focused Strategies Andrew Chirichella & Peter Golish, 2017

The traditional belief and culture of publicly owned com-

panies is to drive shareholder value up as much as possible, with a

tendency to focus on short term profits. This has led to an explosion

in shareholder value which has helped drive the wealth of people

who are heavily invested in publicly traded equities.

Stakeholder Theory

However, there are more groups of people, besides the

shareholders, that can benefit from a company’s success. They are

the stakeholders, which include groups such as the customers, em-

ployees, local economy and even the shareholders; pretty much

anyone affected by that company and the decisions that they

make. When a company looks to increase stakeholder value, it is

applying the stakeholder theory to its strategies.

The stakeholder theory is that a company that manages

its stakeholder relationships effectively will have a longer life span

and have better performance compared to companies that do

not engage their stakeholders effectively. To put it in simpler terms,

the more that firms factor in all of the people and groups affected

by a corporate strategy or decision, the greater their long term

profits will be.

Companies should implement certain strategies that will

help to manage stakeholder relationships. Making a commitment

to monitoring stakeholder interests allows a company to ensure that

they are keeping track of the kinds of strategies that stakeholders

would like the company to follow. They should develop strategies to

deal with the concerns of stakeholders and make the interests and

concerns into manageable strategies that can be implemented.

The Purpose of Stakeholder Strategy

A way to entice people to follow this strategy initially is to

promote it as a huge part of impact investing, the triple bottom

line, and part of corporate social responsibility. Without the stake-

holder strategy, it is impossible to really follow any of these princi-

ples. As Jack Springman wrote in his Harvard Business Review Article

about the stakeholder strategy, “No system can thrive if one mem-

ber group continually benefits at the expense of others.”1

Using this strategy also leads to more sustainable business

strategies and even lowers the potential risks for companies, such

as environmental risks and interest rate risks. This leads to safer in-

vestments for both the company and the areas and people affect-

ed by a firm’s decisions.

Benefits

According to Michael Porter of HBR, while critics may not

like the idea of no longer maximizing short term profits, focusing on

all stakeholders will cause a maximization of profits in the long run.1

Along with the possibility of maximizing long run profits, a

firm that applies a focused stakeholder strategy will also be able to

implement social

change much quicker

and more effectively.

Firms will be able to

help solve many social

issues like poverty and

income inequality.

This can also

lead to healthier fami-

lies, reduce employee

absences, encourage

more environmentally

friendly investments,

and improve production to become more efficient.

The (Triple) Bottom Line

While it may be a common strategy for firms simply to fo-

cus on shareholder value above all else, many companies are

changing their strategies, such as Deutsche Bank and Coca Cola. If

these major companies have analyzed the benefits and costs of a

focused stakeholder decision-making strategy and proceed to use

it, then many more firms are likely to closely follow suit, making it

something that could be extremely beneficial for the world and

businesses as a whole. ♦

According to Michael

Porter of HBR, while

critics may not like the idea

of no longer maximizing

short term profits, focusing

on all stakeholders will

cause a maximization of

profits in the long run.

5

Stumbling Blocks on the Road to Sustainability Lisa Aquino, 2016

Few would argue against the theory behind impact invest-

ing. After all, who would have issues with the growth of philanthropy,

sustainability and an overall better world?

Then, what is the problem? Why isn’t everyone enthusiastic

about impact investing? The answer is simple enough: execution.

Like all things in their relative infancy, impact investing still

has some hurdles to overcome. According to Kevin Starr of the Stan-

ford Social Innovation Review, impact investing is in trouble for a

handful of reasons. Starr claims that impact investors will not receive

the market rate of return for a long time due to the nature of the

investments.1 It is generally difficult to make money from unsubsi-

dized “rural livelihoods,

basic health care, basic

education solutions,

clean water” and other

solutions that “meet the

fundamental needs of

the poor.”1 There are

impact businesses that

generate profits but not

necessarily large im-

pact, and businesses

that generate the most

impact while managing

to lose the least amount

of money (yet still lose

money). Additionally,

some investors assume

that the existence of a

revenue stream signals

future revenue growth,

and therefore profit

growth.1

With the focus

on profit and returns,

the presence of inves-

tors can drive organiza-

tions away from their missions. Starr argues that the demands of

investors can influence an impact business to shift away from its

target population toward a more affluent market. Once the busi-

ness achieves stable figures, it can return its focus to the target pop-

ulation. However, the numbers do not often hit the trigger mark.1

With all of these roadblocks, how can one effectively sup-

port impact companies? Starr believes that investors should worry

more about the level of impact the companies achieve as op-

posed to profit because “[i]n the real world of the poor, real

change still means step-

ping up with money that

you don’t expect to get

back, while demanding

maximum returns in the

form of impact.”1

On the other

hand, maybe the answer

does not lie with the investor, but with the companies themselves.

Impact Makers is a social-impact IT consulting firm based in Rich-

mond, VA and operates

under a hybrid business

structure. It is a registered

B Corporation that is

owned by two public

charities: The Community

Foundation Serving Rich-

mond and Central Virgin-

ia (TCF) and Virginia

Community Capital

(VCC). TCF and VCC

both supply funds that

support charities and

invest in companies with

social missions, but this

structure means that Im-

pact Makers handed

over all its equity to the

Richmond community.

With 70% of its equity held

by TCF and 30% by VCC,

Impact Makers receives

funds from these two

charities and focuses on

delivering its “pro bono

consulting services to

local nonprofit organizations.”2 This structure allows business profits

to directly benefit local charitable nonprofits, which in turn benefit

the community. The business model manages to accomplish this

goal and even simultaneously meets market returns.2

Although impact investing has its pros and cons, no one

ever said creating impact would be easy. Impact investors and

companies might have to get a little creative, but there is hope for

the future of sustainability. ♦

On the other hand, maybe

the answer does not lie with

the investor, but with the

companies themselves.

6

The Future of High-Carbon Assets Morgan Bui ’17, Board of Trustees Scholar and 2015 Summer Scholar Carolin Schellhorn, Ph.D., Department of Finance

Introduction

The climate-negotiating parties in Paris in December

2015 (COP21) created an agreement strong enough to lead ob-

servers to believe it may serve as a market signal that the world

will decarbonize significantly over the next couple of decades.

Whether global decarbonization will be sufficient to keep the

global temperature increase below two degrees Celsius by mid-

century is currently unknown, but it has become a possibility. Ad-

herence to a carbon budget consistent with the Paris agreement

means that the coal, oil and natural gas sectors will be able to use

only a fraction of their currently identified reserves. As a result, their

assets and related industries are worth less than currently record-

ed, thus creating concerns about the existence of a “carbon

bubble.” Our investigation, as part of a summer scholar’s project,

focused on the reasons that assets associated with the fossil fuel

industry are at risk of becoming “stranded,” which means that

they may lose market value or turn into liabilities before the ends

of their expected economic lives. We discovered two likely areas

of origin for these risks to the stability of our economic and finan-

cial systems: corporate governance blind spots and climate

change.

Corporate Governance Blind Spots and Climate Change

Until about the mid1970s, there was no single pur-

pose associated with the corporate form of enterprise

ownership. It was whatever the shareholders and their

representatives considered relevant and included, among

other things, the provision of benefits to employees, the

community or the larger society. This changed with the

free-market framework introduced by Milton Friedman and

other Chicago economists who asserted that the overrid-

ing goal of corporate managers should be the creation of

shareholder wealth measured as the dollar value of equity

a s d e t e r -

mined in the

s tock mar -

ket. The fo-

cus on mon-

etary value

a b o v e a l l

else diverted

a t t e n t i o n

from qualita-

tive and oth-

er quantitative measures associated with value creation,

such as measures of human and animal health and well-

being, pollution and greenhouse gas emissions.

Among the four greenhouse gases emitted by

human activities, the largest in quantity by far is carbon

dioxide. For the first time in recorded history, this gas has

reached a level of 400 parts per million (ppm) in the at-

mosphere up from 280 ppm in pre-industrial times. If busi-

ness continues as usual, it may reach 450 ppm in a couple

of decades. At current carbon dioxide levels, climate

change has already been documented as a contributing

factor in changing global average temperatures,

droughts, floods, heavier storms and extreme weather,

leading to changes in ecosystems including oceans that

threaten food supplies and livelihoods. The four economic

sectors that emit the most carbon are energy and electric-

ity, agriculture and forestry, industry, and transportation.

Any efforts to decarbonize the economy would have to

focus first on these sectors.

Given the gravity of what is at stake for humanity,

civilizations, and our ecosystems, one would have ex-

pected that coordinated climate change mitigation and

adaptation would have become the top cultural priorities

as soon as the science had become publicly available.

Yet governments are acting hesitantly and sporadically.

Corporations also in the agriculture, food, and energy sec-

tors continue their focus on short-term shareholder wealth

creation measured in dollar amounts at the expense of our

atmosphere and ecosystems. As the realization is sinking in

that we, as a global society, are going to pay a price that

could be disturbingly high, some market participants have

begun to assess the risks to our asset values and to the sta-

bility of our economic and financial systems.

Given the gravity of what is at

stake for humanity, civilizations,

and our ecosystems, one would

have expected that coordinated

climate change mitigation and

adaptation would have become

the top cultural priorities as soon

as the science had become publicly

available.

7

The Risks

There are obvious physical risks associated with extreme

energy exploration and production in difficult locations such as

the deep oceans and the Arctic. The BP Gulf oil spill of 2010 is a

relatively recent example. In the face of increasing opposition

from conservation and native groups, companies operate in an

unpredictable regulatory environment. And in the age of social

networking, there are significant reputational risks associated with

energy production that is harming our ecosystems and the atmos-

phere, especially as the millennials mature and move into posi-

tions of responsibility. As renewable energy sources are becoming

increasingly available and energy producers worldwide respond,

large fluctuations in the market prices of oil and gas make it al-

most impossible to assess the eventual profitability of new fossil

fuel projects with any accuracy. All of these risks combine to cre-

ate financial risks that are very difficult to assess and manage.

Moody’s In-

vestor Service has re-

cently addressed this

issue with two reports

published in November

a n d De c e m be r o f

2015, respectively. Of

86 sectors analyzed, 11

sectors with around $2

trillion in rated debt are

c l a s s i f i e d a s

“immediate, elevated

r i sk” or “emerging,

elevated risk” in terms

of their credit exposure

to environmental is-

sues. Moody’s inter-

prets this as “material

credit impacts” that these sectors are experiencing now or that

are expected to arise in the next three to five years. At about the

same time, the Carbon Tracker Initiative estimated that about $2

trillion of capital expenditures in the coal, oil and gas sectors need

to be forestalled over the next ten years, if we are to have a

chance of staying within a carbon budget that may limit a global

temperature increase to about two degrees Celsius by mid-

century. The international agreement forged by the recent con-

ference (COP21) in Paris in December 2015 provides, at a mini-

mum, global support for federal and municipal regulatory action

to help advance a large-scale decarbonization of our economy.

Opportunities and the Way Forward

How do we respond to these unprecedented busi-

ness and societal challenges in a responsible way? A first

step is to acknowledge the situation, become informed,

and discuss possible solutions by engaging with business

managers, investors, consumers, donors, scientists and poli-

ticians. Several opportunities for an effective effort to

meet these challenges exist, but a constructive way for-

ward requires informed collaboration and consensus on

how to proceed. There are currently several issues that

require resolution, such as: Can we stay within our carbon

budget by switching to all renewable sources of energy, or

must we rely on nuclear power as well? As responsible

investors, should we shun all nuclear power and/or fossil

fuel assets, or should we select the “best-in-class” or ex-

clude “worst-in-class?” Should we engage with compa-

nies in which we invest, or become politically active and

demand bi-partisan action on climate change? Should

we ask for the removal of subsidies that are becoming in-

creasingly difficult to justify for fossil fuels? Should we ask

for carbon pricing in the form of a (potentially revenue-

neutral) carbon tax?

Guidance and initiatives to address these and

related issues abound.

An interesting organiza-

tion, for instance, is the

Carbon Pricing Leader-

ship group consisting of

government and busi-

ness leaders who are

collaborating to devel-

o p c a r b o n p r i c i n g

methods and practices.

Strong academic lead-

ers, providing research

and educational pro-

gram support, include

the University of Ox-

ford’s Smith School of

Enterprise and the Environment, and the University of Cam-

bridge’s Institute for Sustainability Leadership. Last but not

least, Goldman Sachs, Mercer and BlackRock are among

several institutional investors who have begun to assess

climate change risks and consider them in their asset allo-

cation decisions. The sooner more of us become informed

and involved in the transition to a low-carbon economy,

the more smoothly this transition is likely to unfold, and the

better the outcome is likely to be for the triple-bottom line

of businesses and asset portfolios as well as for our well-

being as individuals, families, and communities. ♦

How do we respond to these

unprecedented business and

societal challenges in a

responsible way?

8

The Triple Bottom Line: TBH about the TBL Robert A. Jankiewicz, 2018

Whether through our own observations or through the

lessons taught in our business schools, we know that business mod-

els worldwide have evolved astoundingly. Companies are con-

stantly trying to figure out ways to increase sales and cut expenses

in order to add an extra digit to that one number on the bottom of

the income statement. It’s true, the bottom line can sometimes be

a strong determinant of a company’s performance but let’s face it,

there is more to a company’s profitability than simply the digits be-

hind the dollar sign.

In the mid-1990s, John Elkington, the founder of SustainA-

bility, created the idea of “the triple bottom line,” or TBL for short.2

The TBL is an accounting framework that shifts the concept of profit-

ability to include social and environmental impact, which can be

summarized using what is known as the “three Ps”: Profit, People,

and Planet.3 Each of these three pillars should be considered as

separate “accounts” that can be used

to measure profitability.3 Essentially,

companies should not only be con-

cerned with the monetary profit they

earn, but also take into account the

impact that their businesses have on the

environment and any stakeholders that

can be affected by their actions.3

So, what is the big deal about

the triple bottom line anyway? Why

should companies be concerned with

it? First, one of the main reasons organizations should embrace

that TBL is due to corporate social responsibility.3 Other than raising

shareholder value, businesses have a commitment to acting in a

manner that can positively impact the quality of life in communities

where they operate.1 Additionally, following the TBL framework

offers companies competitive advantages and bona fide reputa-

tions.3 The benefits that arise from the TBL can impact companies

from both internal and external standpoints. For example, an exter-

nal benefit could be the creation or expansion of new markets,

especially since the positive characteristics of the triple bottom line

can be highly attractive to a diversified group of consumers.3 More

importantly, from an internal perspective, when companies follow

the “People” pillar, they will be able to reap the benefits of employ-

ee retention and engagement, leading to improved productivity.3

Overall, it is obvious that the triple bottom line can have

very important effects on businesses, but

sometimes difficulty arises in trying to

measure the positive outcomes of the

three pillars in terms of cash.2 Despite this

slight impediment, there are still many

rewards that come from the triple bottom

line. Therefore, the act of simply under-

standing and trying to improve the impact

that organizations have on society and

the environment truly places companies in

a position for sustainable profitability. ♦

Essentially, companies should not

only be concerned with the

monetary profit they earn, but

also take into account the impact

that their businesses have on the

environment and any

stakeholders that can be affected

by their actions.

9

Sustainable investing not only involves environmental

improvement as the primary goal; it also involves social good.

Companies are turning to sustainable investing programs that

benefit society as well. Starbucks has taken up the torch as one of

these companies. It started what is known as the “College

Achievement Plan.” The program began recently in June 2014.

Aiming to encourage the pursuits of young college dreamers who

are hoping to achieve the “American Dream,” Starbucks wants its

employees to never give up on their hearts’ desires and greatest

a m bi t i on s .

With about

70% of the

employees

being stu-

dents, Star-

bucks under-

stands that

sadly only

about half of

the college students in world will actually finish their academic

aspirations.5 Financial distress and the daunting and tiring aspects

of life can sometimes hinder them from being able to focus entire-

ly on what they want to do. As a result, Starbucks has made edu-

cation a primary investment.

So, how did Starbucks take on this rather altruistic en-

deavor, knowing that it would have to allocate a huge chunk of

money towards this plan in order to make it a success? Well, un-

fortunately, the downside is that

this program can only be found

at Arizona State University. Star-

bucks chose this college be-

cause it believed it was the only

university that shared its vision

and fully supported the compa-

ny’s goal to give every student a

high-quality education, within

reason. This college wears its gold

sticker as the most innovative

school in the country, according

to the News & World Report.5 It

also has the reputation of serving

as 5th in the United States to educate and develop graduates

who are best-qualified for and prepared for their career choices.

Arizona State University stands out with its higher-educational

goals, resilient drive for innovation, and strong belief in the free-

dom to pursue dreams and passions.

How can someone be a part of this program? Well, the

company provides the tools needed through the College Plan

Welcome Tool, which introduces any hopeful applicant to this

program. The second step is to apply to Arizona State University

and meet the acceptance criteria. Once accepted, Starbucks

employees are encouraged to speak to a counselor who will

guide them as they face the formidable reality of paying for the

ridiculously high cost of college. Students can choose any course

of study they want, any class they want to take. They immediately

receive an upfront scholarship that partially pays for tuition costs.

Financial aid advisors, like any other college, are there to assist

with applying for FAFSA, grants, or any other type of financial aid.

The beauty of this program is that each time a student completes

21 credits, he or she is reimbursed for the full cost of the tuition and

any mandatory fees, including any additional credits he or she

may have earned—as long as he or she stays enrolled and is on

the road to graduation, of course. Another cool aspect is that this

reimbursement appears right in the student’s paycheck, which I’m

sure is extremely self-gratifying after working hard and spending

hours studying and serving drinks to customers.

Originally, only partial scholarships and the sheer oppor-

tunity of higher education was made available to freshmen and

sophomores. Juniors and seniors have always been rewarded with

full tuition reimbursements for their hard work and dedication.3

Conveniently, the program allows students to transfer to ASU and

take advantage of the program at any point in time, even if they

want to spend the first two years at a different college and then

transfer to take advantage of the full tuition reimbursement. This

program was extended to freshmen and sophomores in April 2015

and has proven to be a huge

success.

The “College Achieve-

ment Plan” is specially made

available in the United States only,

and for a very good reason. Mil-

lennials and the generation be-

hind are part of a new wave of

people who start and never finish

their education due to skyrocket-

ing costs that turn into an over-

whelmingly huge pile of debt. This

debt overshadows every dream

and prevents many students from ever achieving their ambitions,

forcing them to relinquish their aspirations and the lives they de-

sire. This inequality that is occurring in the United States is a huge

problem, the next financial bubble, and Starbucks is making a

statement with this program. This problem is the biggest challenge

young people face, and graduating with debt and student loans

to pay off only hinders them from moving out, having more mon-

ey in their pockets, and following their career goals.

With about 70% of the employees

being students, Starbucks

understands that sadly only

about half of the college students

in world will actually finish their

academic aspirations.

Starbucks’ Leading Role in Social Responsibility

Audrey Rusnak, 2016

10

Starbucks values work/life balance, family, aca-

demics and learning, skills development, and financial sta-

bility—all values that young students hold near and dear to

their hearts as well. ASU is there to help facilitate this

change.

The program has soared. Starbucks has a goal of

reaching 25,000 graduates by 2025, and it is already off to

an incredible start. As of October

2015, more than 4,000 students

have enrolled through Starbucks

and the number of enrollees is only

expected to grow.2 More than 200

graduates are projected to earn

degrees in May 2016. In November

2015, Starbucks announced that it

will honor military men and women

who have served or are currently

serving by offering them free tuition. Not only that, but Star-

bucks is also willing to offer free tuition to their spouses and

children. As of this announcement, it has already hired 5,500

military men and women and their spouses and plans to

reach 10,000 by 2018.6 Starbucks’ chief executive chairman

made the statement that the company views offering a

helping hand to military men and women as an important

moral responsibility of the nation.1 Instead of simply offering

words of thanks, Starbucks is taking action and directly im-

pacting their lives in a positive way and rewarding them for

their sacrifices. Most people share the belief that military

men and women should be rewarded in some way. This

aspect of the program epitomizes the altruistic intentions of

impact investing and serves as one

example of how it promotes social

responsibility and corporate govern-

ance.

With goals of limiting stu-

dent loan debt and reaching out to

military men and women, Starbucks

has taken the wheel in delivering

palpable results through sustainable

investing. Will Starbucks partner with other universities to

help bring about this social change? I’m hoping that other

colleges will see the benefits that the “College Achieve-

ment Plan” reaps and join Starbucks in making an influential

difference in society. ♦

In November 2015, Starbucks

announced that it will

honor military men and

women who have served or are

currently serving by offering

them free tuition.

11

i(x) Investments: A Socially Conscious

Berkshire Hathaway Lisa Aquino, 2016

Most people are familiar with the name Berkshire Hath-

away, or with one of its many holdings. This conglomerate earns

its money by holding complete and partial stakes in attractive

operating businesses and stocks. According to Chairman and

CEO Warren Buffett, Berkshire Hathaway is structured to maxim-

ize long-term capital growth by allowing the tax-free movement

of large sums of money from one business

to another within the conglomerate.2

Well, what if there were a social-

ly responsible version of Buffett’s Berkshire

Hathaway?

That is exactly what Warren Buf-

fett’s grandson, Howard W. Buffett, is

building with co-founder, Trevor Neilson. i(x) Investments mimics

Berkshire Hathaway’s structure, but the similarities end there. This

firm’s name reflects its goal to invest in companies that are work-

ing on sustainable and environmental issues. People who see “i

(x)” usually think back to their math classes…and occasionally

shudder. Regardless of a person’s reaction to the subject of

mathematics, an equation is exactly what this firm wants people

to picture when they hear its name. An equation is also a ques-

tion, and the question that i(x) Investments believes everyone

should consider is whether or not they

will use their investments to leave an impact on the world and

change it for the better.

i(x) Investments “invests in the pillars of human needs…

in a multi-strategy investment approach

throughout the entire capital structure.”1

Potential ventures for i(x) tend to be in

their early stages, undervalued, and likely

to exhibit hyper-growth. In addition to

i(x)’s “expertise in creating and measuring

social impact,” these potential compa-

nies receive the benefit of total reinvest-

ment, unlike with Berkshire Hathaway.1 i(x)

Investments believes that this structure is the most effective

method for impact investing, as opposed to the “finite life cy-

cle” and returns-driven mentality of funds.1

With a long-term focus, i(x)’s goal is to improve world

issues through sustained impact investing while also ushering in a

new potential for capitalism. With the combination of millennial

values and a financially successful bloodline, it would come as

no surprise if Howard W. Buffett succeeds in changing the face

of investing. ♦

What if there were a socially

responsible version of Warren

Buffett’s Berkshire Hathaway?

12

The Business Cycle and the Possible Effects of

Sustainable Finance and Impact Investing Patrick Michael, 2018

What is the Business Cycle?

What do economic expansions and recessions have in

common? They must both end. My thought to this commonality is,

why? Why do expansions have to end and why do recessions

have to start?

The process of having many expansions and recessions

in a cyclical entity is called the business cycle. The National Bu-

reau of Economic Research (NBER) states that the economic busi-

ness cycle is a series of expansions and recessions that occur over

many years.1 The average economic expansion lasts about fifty-

eight months and the average recession lasts only an average of

eleven months. If this is the case, why have we not been able to

eliminate the negative side of the business cycle?

While NBER does not give a definitive answer for why

recessions happen, it does give its best educated guess. It is gen-

erally accepted by economists that, “There is a clear pattern of

excessive speculative activity evident in latter stages of economic

expansion.”2 What are these speculative

activities that cause recessions? In the

recession of 2001, the cause was the

overvaluation and speculation of many

technology companies during the dot-

com boom. In addition to the dot-com

bust, the Great Recession of 2007 was

caused by the unsustainable speculation

involving the U.S. housing market. If the

two recessions in recent memory were

caused by the same basic mistake, why do we, as rational

investors, repeat our missteps?

Why Sustainable Finance and Impact Investing are

the Answer

The ultimate goal of most individuals and firms within

the world’s financial structure is to generate immediate profit

while sustaining long-term growth. Of course there are a few

exceptions, but not many would say that making money now

and making money for many years to come is a bad thing.

Sustainable finance is an avenue many companies are elect-

ing to take in order to cut costs, create a better public im-

age, and increase their revenue all while attracting a new

type of investor, the Impact Investor. This new breed of inves-

tors is not only concerned with its ultimate return, but also in

the sustainability and moral standing in which its returns are

achieved. This is not to say that these investors expect lower

returns for their selectivity, when in fact, they should expect

the same percentage returns as non-Impact Investors. Im-

pact Investing can help keep firms accountable for when

they are financially irresponsible, financially unsustainable, or fi-

nancially immoral. For example, let’s say a firm wants to cut cost,

so it decides to outsource most of its manufacturing jobs to other

countries. Outsourcing in itself is not immoral or financially irrespon-

sible and can actually be a smart business decision in certain cas-

es. It would be an issue for an Impact Investor, however, if this firm

in question did not pay its outsourced workers fair wages for their

work. This lower labor cost would give the investor a greater return

but would actually be against the moral code of the Impact In-

vestor. So instead of the firm paying its workers unfair wages, it is

forced to cut costs in some other way. These cost savings have to

be achieved in a way that is not socially or environmentally harm-

ful. The lowering of costs will likely lead to better and more effi-

cient production, which would give Impact Investors a larger re-

turn on their investment. Imagine if every company had to take

into account the social and environmental implications of its busi-

ness practices. Many would be forced to find a different source of

revenue. They would have to use meth-

ods that generate profit without the need

to destroy the environment or pay their

workers sixty cents an hour. I believe that

if there are real ramifications (less capital

from investors) for companies that per-

form business practices that are detri-

mental to society or our planet, we would

see a healthier, more stable, and sustain-

able economy. ♦

Sustainable finance is an avenue

many companies are electing to

take in order to cut costs, create

a better public image, and

increase their revenue all while

attracting a new type of

investor, the Impact Investor.

13

Goldman Sachs: A Pioneer in the

Social Impact Bond Michael Baldini, 2018

[Goldman Sachs] was a pio-

neer in impact investing

with the creation of its

“social impact bond”....

Goldman Sachs Cares

As most people already know, Goldman Sachs is one of

the most historically influential investment banks and one of the top

valued brands in the world. However, did you know that Goldman

Sachs is not only improving its financial bottom line, but the social

and environmental bottom line, which benefits the lives of others? It

was a pioneer in impact investing with the creation of its “social

impact bond,” which continues to serve as a unique financial tool

to leverage private capital to support social programs in necessi-

tous communities.

What Is a Social Impact Bond

and How Does It Work1

At the heart of the social

impact bond are the social chal-

lenges that federal, state and city

governments face. Due to the

amount of social challenges,

budgets might be too tight to cov-

er all of them adequately. These

governments will turn to social im-

pact bonds to help relieve the

strict budget constraints due to the

various conflicts in the communi-

ties. Therefore, private investors

step up to loan the money, which

finances the costs and funds the

service provider’s program. The

overall goal of the Goldman Sachs

social impact bond is to enable this

private-public partnership to deliv-

er proactive social programs to

underprivileged living communities. If Goldman Sachs meets this

goal through measurable evaluation, the government pays private

investors back. It helps the community by making a difference in

the quality of life for the citizens, the government by addressing a

policy priority and achieving long-term savings, and the investors by

providing returns.

Early Childhood Education2

Alongside J.B. Pritzker and the United Way of Salt Lake,

Goldman Sachs created the first ever social impact bond for the

financing of early childhood education in 2013. This partnership

committed around $7 million to finance a high quality preschool

program in Utah that focuses on increasing academic achieve-

ment and school preparedness for at risk children aged 3 and 4

years old. This program also opened 600 more slots for students who

were subjected to a school district that did not have the funds to

expand classrooms. Data released in 2015 shows that the social

impact bond was a major success because fewer children needed

special education or remedial pro-

grams, which in result saved the school

districts a significant amount of money.

In addition, these students signify much

promise and receive an early start to

their school careers. Investors were paid

as well which made it the first social

impact bond in the country that yielded

a return.

“This is an issue of national concern. People all over the country are

really talking about the importance of our early childhood educa-

tion yet, we’re all in a moment in

time where there are really dimin-

ished government resources to be

able to fund those programs.”

– Andi Phillips of the Urban Invest-

ment Group at Goldman Sachs2

Urban Progress3

The Brooklyn Navy once

stood as the US Navy’s greatest

shipyard, housing some of our na-

tion’s most honored naval ships

and employing around 70,000

workers. However, through a peri-

od of disuse from the 1970s to the

early 1980s the shipyard rotted

away and employment numbers

dropped to around 10,000 workers.

Thus, Goldman Sachs pledged to

rejuvenate the shipyard through a

series of investments in 2012. These investments not only preserved

the historic infrastructure of the site, but also introduced innovative

and sustainable business practices. The project led to a $7.3 million

New Markets Tax Credit equity investment by Goldman Sachs,

which resulted in changing three vacant buildings into a modern

industrial facility.

The investment has also yielded an extra 215,000 square

feet of construction space, which will house Crye Precision, a de-

signer and manufacturer of uniforms for all branches of the U.S.

Military. Another main tenant that is being housed under the addi-

tional space is a project called Macro Sea, a lab for manufactur-

ing, prototyping and 3-D printing.

This commitment has resulted in job creation for low in-

come earners in an area that has been punctuated with unem-

ployment and poverty. Goldman Sachs sought to bring a new

home for industrial growth and did so successfully through the so-

cial impact bond, which created 6,400 jobs and created an annual

economic impact of $2 billion.4 ♦

[Goldman Sachs]

was a pioneer in

impact investing

with the creation of

its “social impact

bond.”

14

Green Money: Green Earth

Rachael Ranieri, 2016

Due to the

issuance of green

bonds, both the pub-

lic and private sector

worlds have collided.

This specific type of

asset class is a confla-

tion of fixed income securities and sustainability efforts. Besides

investing in a triple-A rated fixed income product, investors are

able to contribute toward environmental solutions.

Within the past ten years, our world has endured dev-

astating natural disasters. Many argue that these occurrences

are a direct effect of climate change. This vast, beautiful plan-

et requires viable efforts toward stewardship. Comprehensive

efforts toward energy efficiency, prevention of greenhouse

gas emissions, and investment in new

technology will further enhance envi-

ronmental sustainability.

Luckily, the innovative nature

of green bonds allows clean energy

initiatives to tap into the capital mar-

kets. This asset class has tremendous

potential to provide the capital that is

needed to work towards sustainability.

The funds generated from the issuance

of green bonds are allocated to envi-

ronmental projects. Since the World

Bank issued the first green bond in

2008, the demand for this instrument

has not caught much resistance. In

2014, $36.6 billion of these debt instru-

ments were issued, more than triple the

amount in 2013.5

In addition to its uniqueness,

this security is fundamentally structured

to provide a financial and social yield.

According to the World Bank, one of its

green bond-funded projects is improv-

ing energy efficiency in factories in

China and is expected to cut green-

house gases by 4 million tons a year.2

The ability to quantify a sustainability

project’s net impact, such as the

amount of green-

house gas reduction,

could be one of the

components creating

a tailwind behind

green bonds. This

asset class has not

only provided funding for sustainability projects, but it has also

sparked dialogue about the need for climate solutions. The

pressures of rising global temperatures and extreme weather

patterns have a compounding effect on developing coun-

tries. The aggregate impact of climate change put a devel-

oping country’s GDP, food, and water supply in harm’s way.

Through this asset class, more capital will hopefully be readily

available to work toward preserving our planet. ♦

Luckily, the innovative nature of green bonds allows clean

energy initiatives to tap into the capital markets.

15

To many potential and experienced

investors, sustainable investing still merely means

risky business. Not only is it a concept that has

only recently been planted in people’s minds

and newly discussed, but the enigmatic idea of

investing this way also constitutes uncharted wa-

ters. Environmental change and social good

primarily fuel the fire of sustainable investing, but

many fear they might get burned by the flames

of risk and potential loss.

People argue that sustainable investing

is too much of a risk, a waste of money, and

quite frankly not as good of a deal or much of a

guarantee compared to

other investments. So, why

should they embrace this

concept and partake in this

venture? There are many

reasons why individuals and

businesses together should

jump on this bandwagon

that are more than just long-

term financial rewards.

For individual inves-

tors, sustainable investing is more of a risk than it is

to corporate leaders. Their futures are potentially

on the line. Addressing one of the primary con-

cerns about impact investing, the Global Impact

Investing Network, or GIIN, has taken the lead on

educating people who are interested in putting

their money towards a good cause. GIIN pro-

vides people with the resources necessary to

research and make decisions regarding incorpo-

rating funds that promote environmental change

or social responsibility into their portfolios. Be-

cause of growing interest, organizations and

companies are giving people what they need in

order to engage in this increasingly ubiquitous

trend.

Businesses should engage in sustainable

investing practices for a myriad of reasons, all of

which encompass a single one: people demand

and expect businesses and corporations to be

socially responsible. As a trend, sustainability con-

tinues to surface into daily lives, and people are

becoming more and more attentive to environ-

mental and social changes and needs. As a re-

sult, many people, especially millennials, look to

invest in companies that support sustainable

practices and work to implement sustainable

change. About 85% of employees want to work

for companies that support

charities and nonprofits,

and/or that value improving

the environment or creating

social good.9 If companies

want to make a profit, they

need to assimilate sustaina-

bility into their business strat-

egies to even draw consum-

er demand. When most

people look for jobs, they

are seeking positions with companies that are

sustainable and socially responsible. Studies have

shown that corporate social responsibility im-

pacts how companies’ employees thrive in terms

of their productivity and morale, and influences

whether or not they will stay with their compa-

nies. If companies want the best talent, they

need to have these values to attract and keep

the talent. Essentially, being socially responsible

constitutes the key to success, serves as a cata-

lyst for opportunity and innovation and gives

companies a competitive advantage. In the

end, social responsibility allows businesses to es-

tablish long-term growth and advancement.

About 85% of employees

want to work for

companies that support

charities and nonprofits,

and/or that value

improving the

environment or creating

social good.9

Why People Should Embrace Sustainable Investing Audrey Rusnak, 2016

16

Millennials lead the way in

impact investing.

Individuals and businesses both know that the demographical

transitions taking place have a major impact on investing trends as well.

Millennials lead the way in impact investing. This generation took impact

investing by the reins and rode with it. In terms of savings, millennials and

future generations will have to rely more on their own investments and re-

tirement funds and less on Social Security. Millennials care most about the

type of ends their means will create. With global warming on the rise, social

issues being in the spotlight, and sustainability and philanthropy being hot

topics, millennials want the money they invest to not only produce strong

financial returns, but also want go towards a good cause. This frame of

mind controls how they think as well as the decisions they make. Millennials

hope to influence future generations, impress upon them this form of think-

ing and emphasize its importance. Millennials are currently earning college

degrees, embarking on their careers, and looking for ways to finance their

futures. So this method of investing, where one can earn strong returns while

simultaneously making a positive impact, is extremely important to them.

Because it lacks a tangible long-term track record, impact invest-

ing often means taking a leap of faith. However, with the right resources,

coupled with people’s increased interest and participation, impact invest-

ing will continue to grow and boom as people’s returns are maximized. Tak-

ing an increased interest in environmental change and corporate govern-

ance strategies that positively benefit society will ensure investors that their

investments will be worth it, both financially and societally. Since sustainable

investing is the way of the future and the hottest rising trend in investments,

it’s good to strike the iron while it’s hot. ♦

17

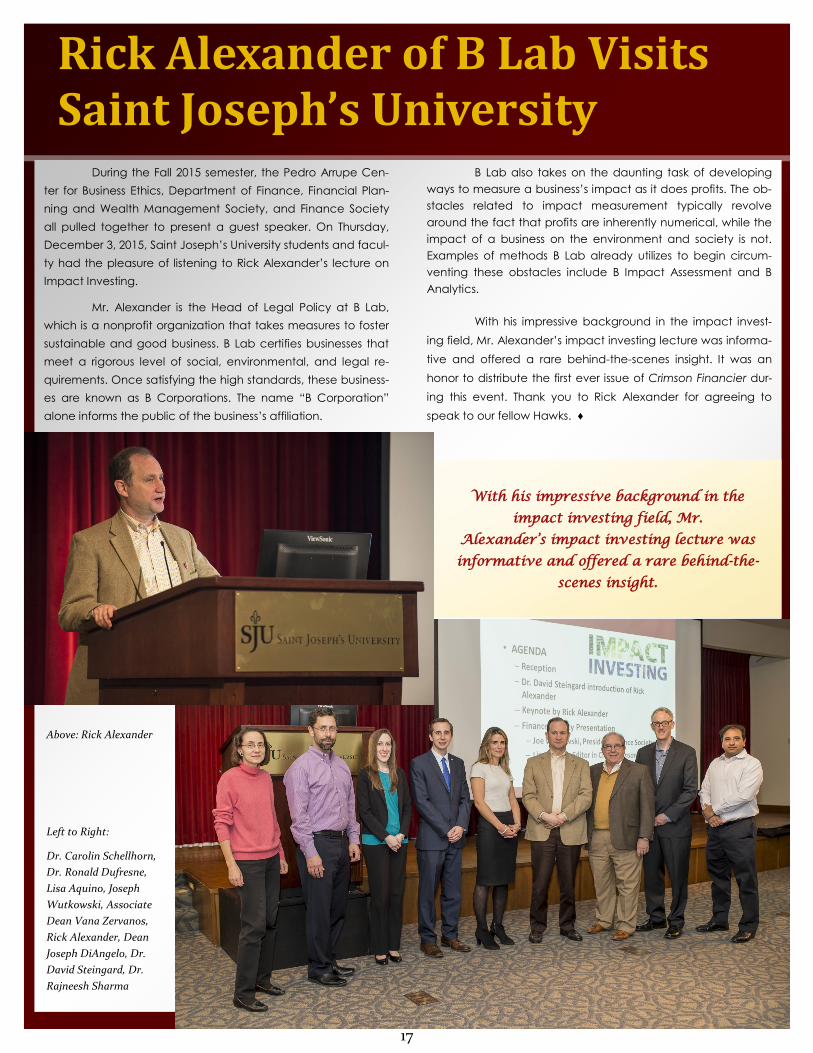

Rick Alexander of B Lab Visits Saint Joseph’s University

During the Fall 2015 semester, the Pedro Arrupe Cen-

ter for Business Ethics, Department of Finance, Financial Plan-

ning and Wealth Management Society, and Finance Society

all pulled together to present a guest speaker. On Thursday,

December 3, 2015, Saint Joseph’s University students and facul-

ty had the pleasure of listening to Rick Alexander’s lecture on

Impact Investing.

Mr. Alexander is the Head of Legal Policy at B Lab,

which is a nonprofit organization that takes measures to foster

sustainable and good business. B Lab certifies businesses that

meet a rigorous level of social, environmental, and legal re-

quirements. Once satisfying the high standards, these business-

es are known as B Corporations. The name “B Corporation”

alone informs the public of the business’s affiliation.

B Lab also takes on the daunting task of developing

ways to measure a business’s impact as it does profits. The ob-

stacles related to impact measurement typically revolve

around the fact that profits are inherently numerical, while the

impact of a business on the environment and society is not.

Examples of methods B Lab already utilizes to begin circum-

venting these obstacles include B Impact Assessment and B

Analytics.

With his impressive background in the impact invest-

ing field, Mr. Alexander’s impact investing lecture was informa-

tive and offered a rare behind-the-scenes insight. It was an

honor to distribute the first ever issue of Crimson Financier dur-

ing this event. Thank you to Rick Alexander for agreeing to

speak to our fellow Hawks. ♦

With his impressive background in the

impact investing field, Mr.

Alexander’s impact investing lecture was

informative and offered a rare behind-the-

scenes insight.

Above: Rick Alexander

Left to Right:

Dr. Carolin Schellhorn,

Dr. Ronald Dufresne,

Lisa Aquino, Joseph

Wutkowski, Associate

Dean Vana Zervanos,

Rick Alexander, Dean

Joseph DiAngelo, Dr.

David Steingard, Dr.

Rajneesh Sharma

18

Global Jesuit Case Series Announcement

We are excited to announce our partnership

with the Global Jesuit Case Series (GJCS). The GJCS is

a network of individuals across the globe that uses

Jesuit tradition and values to shape the next genera-

tion of leaders through unique case studies and its

annual Inner Compass magazine.

At the end of the Fall 2015 semester, members

of the GJCS met with faculty and students from the

Pedro Arrupe Center for Business Ethics and the Fi-

nance Society. The GJCS recognized Saint Joseph’s

University for the work it has been doing to incorpo-

rate business ethics in all fields.

The fact that Crimson Financier is a student-

run organization impressed the GJCS representatives,

who offered to post the Fall 2015 issue, as well as any

future issues, on the GJCS website. They can be

viewed at http://www.gjcs.org/crimson-financier.

We at Crimson Financier are thankful for this

opportunity and extend our gratitude to the repre-

sentatives of the Global Jesuit Case Series for coming

to Saint Joseph’s University. We greatly appreciate

Dr. Brent Smith, Dr. David Steingard and Dr. Carolin

Schellhorn’s work in helping facilitate this meeting.

Crimson Financier looks forward to growing

this relationship with the Global Jesuit Case Series. ♦

We are excited to announce our partnership

with the Global Jesuit Case Series.

19

References The Case for Stakeholder Focused Strategies—

Andrew Chirichella & Peter Golish, 2017

1. Springman, Jack. "Implementing a Stakeholder Strat-egy." Harvard Business Review. Harvard Business Review, 28 July 2011. Web. 14 Jan. 2016. <https://hbr.org/2011/07/implementing-a-stakeholder-str> .

Stumbling Blocks on the Road to Sustainability—

Lisa Aquino, 2016

1. Starr, Kevin. "The Trouble With Impact Investing: P1 (SSIR)." Stanford Social Innovation Review. Stanford University, 24 Jan. 2012. Web. 16 Jan. 2016. <http://ssir.org/articles/entry/the_trouble_with_impact_investing_part_1>.

2. Hanau, Lori. "7 Guideposts for Leading Conscious Growth." Conscious Company Jan.-Feb. 2016: 7-9. Print.

The Triple Bottom Line: TBH about the TBL—Robert

A. Jankiewicz, 2018

1. Colquitt, Jason, Jeffery A. LePine, and Michael J. Wesson. Organizational Behavior: Improving Perfor-mance and Commitment in the Workplace. New York: McGraw-Hill Irwin, 2011. Print.

2. Hindle, Tim. "Triple Bottom Line." The Economist. The Economist Newspaper, 17 Nov. 2009. Web. 29 Nov. 2015.

3. Scott, Ryan. "The Bottom Line of Corporate Good." Forbes. Forbes Magazine, 14 Sept. 2012. Web. 29 Nov. 2015.

Starbucks’ Leading Role in Social Responsibility—

Audrey Rusnak, 2016

1. Agrawal, Nadya. “Starbucks Offers Free College Tuition

To Military Spouses and Children.” Huffington Post. The Huffington Post Inc., 9 November 2015. Web. 4 January 2016. <http://www.huffingtonpost.com/entry/starbucks-college-achievement-plan_5640dd1ee4b0b24aee4b1b4d>.

2. “Starbucks College Achievement Plan Passes 4,000

Mark.” QSR. Journalistic Inc., 14 October 2015. Web. 4 January 2016. <https://www.qsrmagazine.com/news/starbucks-college-achievement-plan-passes-4000-mark>.

3. EPR Retail News Editors. “43 Starbucks Partners Re-

ceived Their Degrees Through The Starbucks College Achievement Plan In December.” EPR Retail News. EPR News, 18 December 2015. Web. 4 January 2016. <http://eprretailnews.com/2015/12/18/43-starbucks-partners-received-their-degrees-through-the-starbucks-college-achievement-plan-in-december-8765432123456790/#>.

4. 3P Contributor. “The Key to Improving Career Readi-

ness Among College Graduates.” TriplePundit. Triple Pundit, 5 January 2016. <http://www.triplepundit.com/2016/01/public-private-partnerships-the-key-to-improving-career-readiness-among-college-graduates/>.

5. “Starbucks College Achievement Plan.” Starbucks.

Starbucks Corporation. Web. 4 January 2016. <http://globalassets.starbucks.com/assets/39415f5a386a47259479e9f553246eef.pdf>.

6. “Starbucks Hires 5,500 Veterans and Military Spouses;

Extends College Benefit.” Starbucks Newsroom. Star-bucks Corporation, 9 November 2015. Web. 4 January

2016. <https://news.starbucks.com/news/starbucks-hires-5500-veterans-and-military-spouses> .

i(x) Investments: A Socially Conscious Berkshire

Hathaway—Lisa Aquino, 2016

1. "i(x) Investments." I(x) Investments. I(x) Investments, 2015. Web. 17 Jan. 2016. <http://www.ix-investments.com>.

2. Das, Anupreeta. "Warren Buffett Defends Berkshire Hathaway's Conglomerate Structure." MarketWatch. MarketWatch, Inc, 28 Feb. 2015. Web. 17 Jan. 2016. <http://www.marketwatch.com/story/warren-buffett-defends-berkshire-hathaways-conglomerate-structure-2015-02-28>.

The Business Cycle and the Possible Effects of Sus-

tainable Finance and Impact Investing—Patrick

Michael, 2018

1. "The National Bureau of Economic Research." The National Bureau of Economic Research. National Bu-reau of Economic Research, 2015. Web. 17 Dec. 2015. <http://www.nber.org/>.

2. "Investopedia." Investopedia. Investopedia, LLC, 2015. Web. 17 Dec. 2015. <http://www.investopedia.com/> .

Goldman Sachs: A Pioneer in the Social Impact

Bond—Michael Baldini, 2018

1. "Social Impact Bonds." goldmansachs.com. Goldman Sachs, Oct. 2014. Web. 5 Jan. 2016. <http://www.goldmansachs.com/our-thinking/pages/social-impact-bonds.html>.

2. Phillips, Andi. "Impact Investing Social Impact Bond for Early Childhood Education." goldmansachs.com. Goldman Sachs, 2015. Web. 5 Jan. 2016. <http://www.goldmansachs.com/what-we-do/investing-and-lending/impact-investing/case-studies/salt-lake-social-impact-bond.html>.

3. "Impact Investing Brooklyn Navy Yard, New York City." goldmansachs.com. N.p., 2015. Web. 5 Jan. 2016. <http://www.goldmansachs.com/who-we-are/progress/brooklyn-navy-yard/index.html>.

4. "A Story of Urban Progress." goldmansachs.com. Goldman Sachs, 2015. Web. 5 Jan. 2016. <http://www.goldmansachs.com/who-we-are/progress/brooklyn-navy-yard/index.html>.

Green Money: Green Earth—Rachael Ranieri, 2016

1. "World Bank Green Bonds." World Bank Green Bonds. World Bank Treasury, 2009. Web. 20 Jan. 2016. <http://treasury.worldbank.org/cmd/htm/WorldBankGreenBonds.html>.

2. "Green Bonds Attract Private Sector Climate Fi-nance." World Bank. The World Bank Group, 10 June 2015. Web. 20 Jan. 2016. <http://www.worldbank.org/en/topic/climatechange/brief/green-bonds-climate-finance>.

3. "Green Bond Fact Sheet." World Bank Green Bonds. The World Bank Group, July 2015. Web. 20 Jan. 2016. <http://treasury.worldbank.org/cmd/pdf/WorldBank_GreenBondFactsheet.pdf>.

4. "A Bad Climate for Development." The Economist. The Economist Newspaper Limited, 17 Sept. 2009. Web. 04 Apr. 2016. <http://www.economist.com/node/14447171>.

5. Field, Anne. "$36.6B In Green Bonds Issued Last Year." Forbes. Forbes Magazine, 15 Jan. 2015. Web. 20 Jan. 2016. <http://www.forbes.com/sites/annefield/2015/01/15/36-6b-in-green-bonds-issued-last-year/#2715e4857a0b5cb84dab31fa> .

Why People Should Embrace Sustainable Invest-

ing—Audrey Rusnak, 2016

1. Hale, Jon. “Does Sustainable Investing Deliver Sus-tainable Profits?” Morningstar. Morningstar, 7 Decem-ber 2015. Web. 4 January 2016. <http://www.morningstar.co.uk/uk/news/145330/does-sustainable-investing-deliver-sustainable-profits.aspx>.

2. “Five Companies that Typify Sustainable Investment.” The Week. The Week Ltd, 13 March 2015. Web. 4 January 2016. <http://www.theweek.co.uk/sustainable-investment/62934/five-companies-that-typify-sustainable-investment>.

3. Ostrowski, Greg. “The Rise of Sustainable Investing.” U.S. News & World Report: Money. U.S. News & World Report, 15 September 2015. Web. 4 January 2016. <http://money.usnews.com/money/blogs/the-smarter-mutual-fund-investor/2015/09/15/the-rise-of-sustainable-investing>.

4. Hurley, Brad. “Complement Your Giving With Impact Investing.” Huffington Post. Huffington Post, 5 May 2015. Web. 4 January 2016. <http://www.huffingtonpost.com/brad-hurley/complement-your-giving-wi_b_7217764.html>.

5. Taft, John G. “The Warren Buffet Effect: Investing in Our World.” Huffington Post. Huffington Post, 12 July 2014. Web. 4 January 2016. <http://www.huffingtonpost.com/john-g-taft/the-warren-buffett-effect_b_5577685.html>.

6. Davidson, Alex. “A Guide to Sustainable Investing.” The Wall Street Journal. Dow Jones Company Inc., 8 November 2015. Web. 4 January 2016. <http://www.wsj.com/articles/a-guide-to-sustainable-investing-1447038115>.

7. Chamberlain, Michael. “Socially Responsible Invest-ing: What You Need to Know.” Forbes. Forbes, 24 April 2013. Web. 4 January 2016. <http://www.forbes.com/sites/feeonlyplanner/2013/04/24/socially-responsible-investing-what-you-need-to-know/#2715e4857a0b2fb74fef5863>.

8. Heyns, Gerrit. “Companies that Invest in Sustainability Do Better Financially.” Harvard Business Review. Harvard Business Review, 19 September 2012. Web. 4 January 2016. <https://hbr.org/2012/09/sustainable-investing-time-to/>.

9. Horoszowski, Mark. “5 Reasons Your Business Should Be Socially Responsible.” Movingworlds. Moving-Worlds.Org, 3 December 2011. Web. 4 January 2016. <http://blog.movingworlds.org/5-reasons-your-business-should-be-socially-responsible/>.

10. Steverman, Ben. “Sustainable Investing Is Booming. Is it Smart?” Bloomberg Business. Bloomberg LP, 21 October 2015. Web. 4 January 2016. <http://www.bloomberg.com/news/articles/2015-10-21/sustainable-investing-is-booming-is-it-smart-> .

20

A Publication by the

Finance Society

of Saint Joseph’s University

“A student-led organization”