Rock of AGIS: The Foundation for Oracle R12 Intercompany ...

The Future of Cash2012

AGISCONSULTING

3

. Foreword

Every day, consumers and businesses engagein transactions, which fuel the growth of local,national and global economies. In today’sglobalized and digital societies, cash plays aprominent role in enabling these transactions.For most people, paying has become aphysiological need in the sense of Maslow’shierarchy of needs as it has become necessaryto pay for even the most basic needs such asfood, water or shelter. For some, cash is theonly available payment mechanism. Othershave a variety of instruments at their disposalbut cash remains a strong and viable optionfor both consumers and businesses alike.

As key stakeholders in the cash cycle, our aimis to ensure it continues to support economicdevelopment. We believe it is our responsibilityto bring awareness to its importance in ourdaily life so that all stakeholders can effectivelycontribute to the availability of and access tocash and to ensure that it remains a secure,trusted and efficient payment mechanism.

Therefore, we commissioned this fourth editionof the Future of Cash study to shed light onthe status of cash in four distinct and differentmarkets namely; Brazil, the euro-zone, SouthAfrica and the United States of America.Participants in the study represent seven centralbanks; six commercial banks and twologistics/cash-in-transit (CIT) companies.

In addition to recognizing the wealth ofknowledge we acquired from our referencesources, we gratefully acknowledge and thankour participants for their invaluable time andcontributions and the ATMIA Cash Council, forits valued support. With much gratitude, wewould like to also thank Mr. Dan Littman ofthe Federal Reserve Bank of Cleveland, whograciously agreed to review and edit our reportfor content and clarity.

Eric BoissonasGeneral Manager

KBA-Notasys

Jean-Yves RayMarketing Director

SICPA

Christopher GeorgeChief Operating Officer

iCVn

4 THE FUTURE OF CASH 2012

. About us

www.kba-notasys.com

KBA-NotaSys is regarded as the main driver ofinnovation and excellence within the high-securityprinting industry. Working hand in hand with ourclients and partners, we have continuously elevatedthe art of banknote printing to new levels. Bylistening to our clients' needs we have expandedour range of products and services to meet theever-changing challenges of our market.

Today we offer a unique range of products andservices to authorised securtiy printers and centralbanks enabling them to design, produce andissue banknotes according to their specific andindividual needs.

www.sicpa.com

Leading global provider of security inks andintegrated security systems for governments, centralbanks, security printers and brand owners, SICPA isthe trusted partner in matters of currency, securitydocuments and the protection of governmentrevenues and brand products against illicit trade.

Established in 1927, the company has expandedto a multi-national group with headquarters andresearch centres in Switzerland with offices andmanufacturing facilities in 26 locations on fivecontinents. SICPA believes in the power of knowledgeand innovations, and its continued success is builton talents coming from a wide range ofcompetencies, notably chemistry, engineering,computer and material science.

www.icvn.com

iCVn, a Maryland USA company, has patented andimplemented the world's first cash tracking andvalidation network. Our proprietary CashTrakker™desktop software and mobile application allow forthe validation and tracking of curency banknotes,negotiable instruments, wire transfers and prepaidcards using our dynamically updated proprietarydatabases that reside in a global network. iCVn iscurrently tracking multiple currencies worldwideand has sold sytems to law enforcement, intelligenceagencies and financial institutions, domesticallyand internationally. iCVn's next generation cashtracking solutions will target the retail and gamingindustries. We are honored to sponsor thisinternational study on the Future of Cash.

5

FOREWORD 3

ABOUT US 4

TABLE OF CONTENTS 5

1. EXECUTIVE SUMMARY 6

INTRODUCTION 8

2. DEMAND FOR CASH 10

2.1 Cash in Circulation 10

2.2 Understanding Cash Usage 13

2.3 The Impact of the 2008 Financial Crisis on Cash Demand 16

2.4 The Share of Cash in Retail Payments 17

2.5 Why is Cash Used 19

3. THE EVOLUTION OF THE CASH CYCLE 21

3.1 The Four Cash Cycles 21

3.2 Key Trends Impacting the Cash Cycle 24

4. LONG-TERM PERSPECTIVES 33

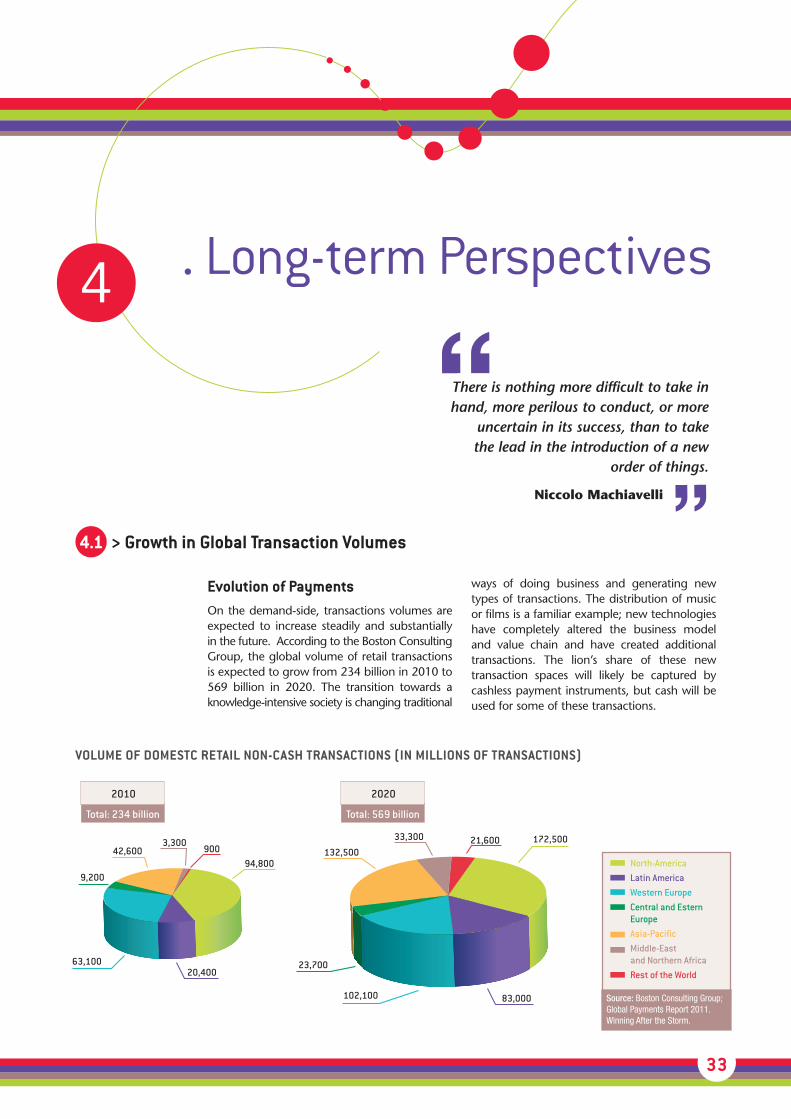

4.1 Growth in Global Transaction Volumes 33

4.2 Adapting to Changes 36

4.3 Winning the Efficiency Battle 37

4.4 Long-term Scenarios 41

APPENDICES 44

List of Participants 44

Bibliography 45

. Table of contents

AGISCONSULTING

www.agis-consulting.com

AGIS Consulting is an independent strategyconsulting firm, specializsed in retail payments,including cash, cards and other paymentinstruments. AGIS was founded in 2001 in Parisand has since developed a worldwide network ofpartners.

The European retail payments market is facingtremendous change, under the combined pressuresof the evolving regulatory market and Europeanintegration, technological innovation and socio-economic factors. AGIS aims at providing itsclients with out-of -the box thinking, in order toanticipate the changes in the market and developcustomized value-added solutions.

Clients range from financial institutions, to paymentservice providers, to soft and hardware vendors.

www.asi-consulting.com

ASI Management Consultancy provides businesdevelopment and strategic consulting to financialinstitutions, gaming enterprises and technologycompanies serving these industries. Additionalareas of focus and expertise include productdevelopment as well as marketing and salessupport. Leveraging the experience and knowledgeof a network of consultants throughout the world,ASI provides its strategic consulting services inNorth and Latin America and EMEA.

6 THE FUTURE OF CASH 2012

. Executive Summary1

Cash Demand is GrowingDuring the past decade, cash in circulation hasbeen growing at exceptional rates in all fourmarkets covered by this research – Brazil, theeuro-zone, South Africa, and the United States.In Brazil and South Africa, this has been drivenprimarily by transactional cash, fuelled by sustainedgrowth of GDP and consumer expenditure. Inthe euro-zone and the US, the larger part of thisgrowth results from hoarding, both at domesticand international levels; nonetheless, transactionalcash has been growing as well.

The 2008 financial crisis and ensuing debtcrisis have demonstrated the fundamentalcontingency role of cash. The crisis has led tosignificant peaks in cash demand, as consumersreallocate their savings in times of instability. Ithas also changed spending behaviors as manyconsumers have shifted away from electronicpayment instruments to cash in order totighten their control over their budget. Thecrisis has reminded us that cash is far morethan a payment instrument; it is the foundationof the modern financial system.

Cash remains, and by far, the most widelyused payment instrument; it is used to settlebetween 8 and 9 transactions out of 10.Nonetheless, the relative share of cash isdeclining with the development of alternativepayment instruments, but in most countries,this is compensated by growth in transactionvolumes. A reduction in cash usage at thepoint of sale leads to lower demand fortransactional banknotes but does not impactdemand for banknotes used for hoarding.Consequently, a reduction in transactional cash

would only have a moderate impact on theoverall value of cash in circulation.

The Cash Cycle is ChangingThe role of central banks in the cash cycle ischanging. Strong developments in fitnesssorting technology have led to significantproductivity gains and have enabled centralbanks to consolidate their infrastructure.Furthermore, central banks have evolved theircash distribution models to facilitate commercialrecirculation of banknotes. The level ofinvolvement of central banks in fitness sortingvaries significantly between countries; somecentral banks mainly process unfit banknotesprior to destruction – e.g. South Africa, theNetherlands; others continue to play animportant role in the processing alongside thecommercial sector – US, France, Germany… Inall cases, central banks are increasing theirsupervisory and monitoring role to ensure thequality and authenticity of cash in circulation.

Commercial recirculation has developed indifferent ways in different markets.

• Some markets have implemented ’industrial’or cash centre recirculation; this is particularlythe case where central banks offer someform of balance sheet relief to the commercialsector to compensate the opportunity costof holding additional cash inventories. It alsoenables commercial processors to mergestocks from different customers and thereforeachieve economies of scale. This is the casein the US, in the Netherlands, in South Africaand Brazil.

7

• Other markets have opted to recirculate atthe bank branch either at the front-officeusing recirculating ATMs or teller cash recyclers,or in the back-office. This includes but is notlimited to Belgium, France, Germany, andSpain. Local recirculation contributes toshorten the cash cycle.

The increase in commercial processing has ledcommercial banks to rethink their owninfrastructure and achieve the optimal balancebetween in- and outsourcing. One modelwhich has been developing recently is the’interbank utility’ where banks pool their cashcenters into a single entity. This model ispresent in Austria with GSA, in the Netherlandswith GSN, in South Africa with SBV. Somecountries have opted to pool their ATM estatesinto a single jointly-owned company such asAutomatia in Finland. For commercial banks,this model is aimed at reducing the cost of thecash infrastructure. For the central bank, itcontributes to a more robust cash cycle, byreducing the number of entities involved, thuseasing the oversight and enforcementresponsibilities.

Another trend is emerging in several markets:cash is being processed closer to the point ofsale. This has been driven by technology, as arange of new solutions has been emerging:smart safes, self check-out devices for notes andcoins, end-to-end automated solutions… It hasalso benefited from lower interest rates whichreduce the opportunity cost of holding cash andlimit the need to transport cash back to thecentral bank. Commercial banks have beenreplicating the strategies of the central bank asthey in turn have been pushing processingdown the food chain towards their customersand crediting cash which is still held on thecustomer’s premises.

Long-term ProspectsThere is strong consensus that the overallvolume of payments will increase in the future.The evolution towards knowledge-intensive

societies will change traditional ways of doingbusiness and create new business models, newdistribution channels, more tailored andsegmented products and services. This willresult in the emergence of new transactionspaces. Cash will face increasing competitionfrom new payment instruments in thisenvironment. Nonetheless, cash will continueto play an essential role. On the one hand, theresilience of cash is such that the substitutionof cash would be a very slow process. On theother hand, the fundamental attributes of cash– universality, trust and anonymity – willcontinue to play key societal roles in thefuture.

The diversification of payment instruments willaccelerate the competitive pressures on cash,which faces a significant efficiency challenge.The societal cost of cash is widely used as anargument in favor of cash substitution, butthere are significant opportunities to furtheroptimize the efficiency of cash. Key levers tofurther reduce the cost of cash are:

• Incremental productivity gains through newtechnology and process improvements

• Further integration of the cash cycle throughstandardization

• Optimization of cash inventories by industry-wide management information systems

However, the real question is not the actualcost but rather how and by whom it is funded.Today, the costs are split between thestakeholders – central banks, commercial banks,retailers, consumers – and this balance is basedon a high level of cash usage.

Innovation will benefit cash. It is often assumedthat new technologies will foster alternativepayment instruments and cash substitution.Historically, cash has largely benefitted fromnew technologies; the ATM and the paymentcard have largely improved the availability andaccess to cash. We believe new technologieswill further increase the availability of cash,broaden the range of uses and improve itsefficiency and convenience.

8 THE FUTURE OF CASH 2012

. Introduction

In this fourth edition of the Future of Cashreport, we endeavor to understand the ongoingforces which are driving change in the cashcycle, affecting the fundamentals as well asaccommodating weak signals from the marketplace. It is not our intention to provide all theanswers but we hope to inspire innovativethinking and new responses to the challengesfaced by the stakeholders.

The previous editions of the Future of Cashwere focused on the euro-zone following theintroduction of the euro, which represented anunprecedented logistical operation. This editioncovers four markets: Brazil, the euro-zone,South Africa and the United States of America.

The first section analyses the evolution ofdemand for cash both in quantitative andqualitative terms. The second section addresseshow the cash cycle has been changing andcompares the evolutions across different markets.The third section looks at the long–termprospects.

This report has been authored by GuillaumeLepecq of AGIS Consulting and HamletAmbarsoom of ASI Management Consultancy.It is based on desktop research as well as aseries of interviews with key stakeholders inthe cash cycle - including central banks,commercial banks, and third-party cash logisticsand processing companies in all four markets.The list of organizations interviewed appears inappendix 1.

The information and opinions included in thisreport have been gathered to the best of ourknowledge, but the authors do not acceptliability for any loss arising from its use.

Before we begin, for comparison purposes,here we present some relevant data across thefour markets of the study.

When I was young I thought thatmoney was the most important thing in life; now that I am old

I know that it is.

Oscar Wilde

“”

9

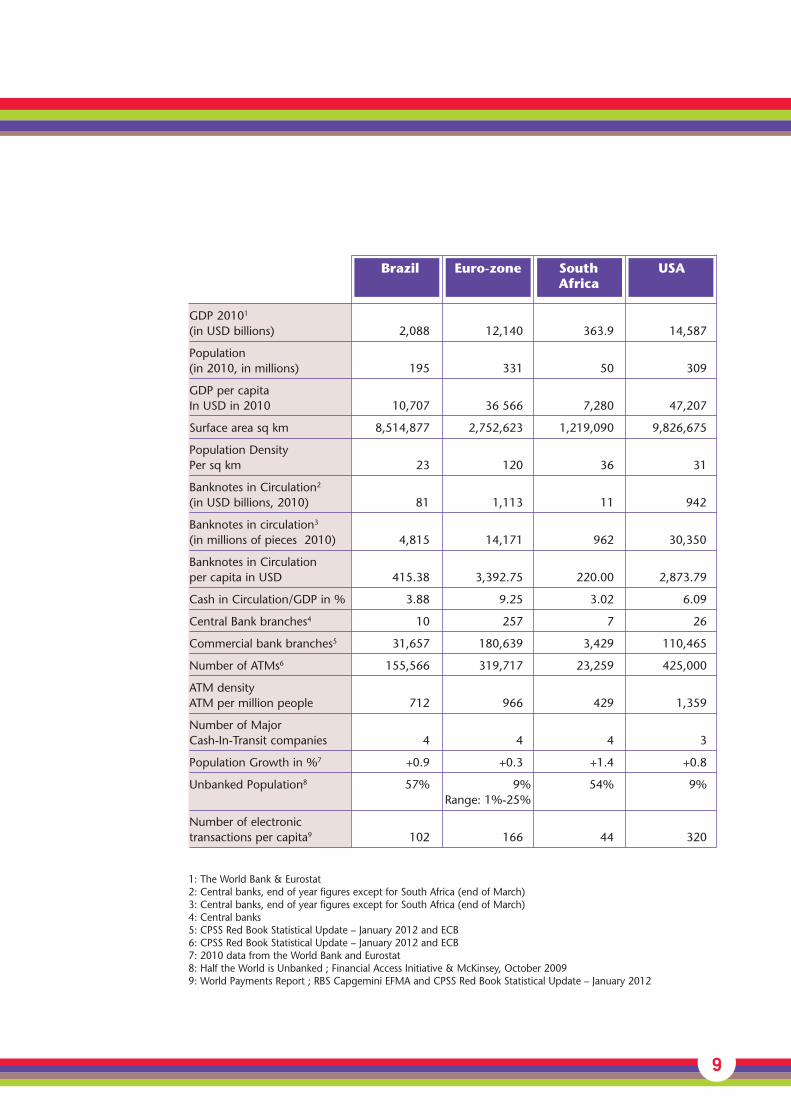

Brazil Euro-zone South USAAfrica

GDP 20101

(in USD billions) 2,088 12,140 363.9 14,587

Population(in 2010, in millions) 195 331 50 309

GDP per capitaIn USD in 2010 10,707 36 566 7,280 47,207

Surface area sq km 8,514,877 2,752,623 1,219,090 9,826,675

Population DensityPer sq km 23 120 36 31

Banknotes in Circulation2

(in USD billions, 2010) 81 1,113 11 942

Banknotes in circulation3

(in millions of pieces 2010) 4,815 14,171 962 30,350

Banknotes in Circulation per capita in USD 415.38 3,392.75 220.00 2,873.79

Cash in Circulation/GDP in % 3.88 9.25 3.02 6.09

Central Bank branches4 10 257 7 26

Commercial bank branches5 31,657 180,639 3,429 110,465

Number of ATMs6 155,566 319,717 23,259 425,000

ATM densityATM per million people 712 966 429 1,359

Number of Major Cash-In-Transit companies 4 4 4 3

Population Growth in %7 +0.9 +0.3 +1.4 +0.8

Unbanked Population8 57% 9% 54% 9%Range: 1%-25%

Number of electronic transactions per capita9 102 166 44 320

1: The World Bank & Eurostat2: Central banks, end of year figures except for South Africa (end of March)3: Central banks, end of year figures except for South Africa (end of March)4: Central banks5: CPSS Red Book Statistical Update – January 2012 and ECB6: CPSS Red Book Statistical Update – January 2012 and ECB7: 2010 data from the World Bank and Eurostat8: Half the World is Unbanked ; Financial Access Initiative & McKinsey, October 20099: World Payments Report ; RBS Capgemini EFMA and CPSS Red Book Statistical Update – January 2012

10 THE FUTURE OF CASH 2012

. Demand for Cash2

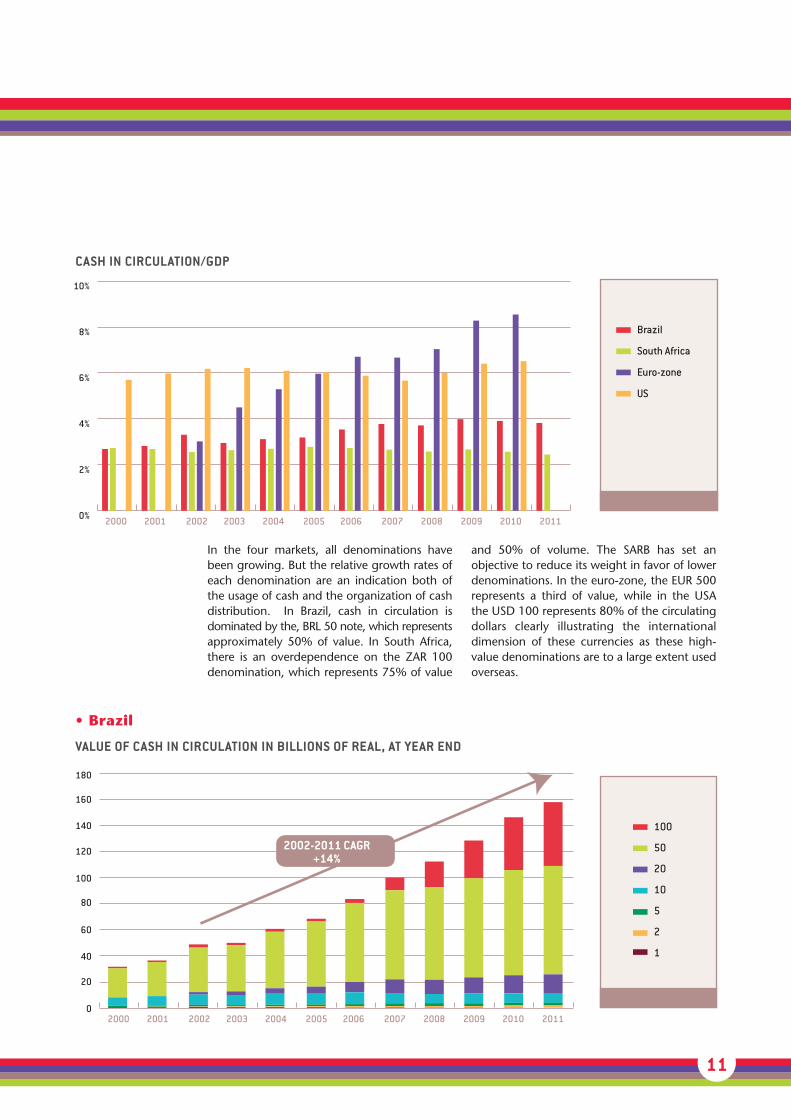

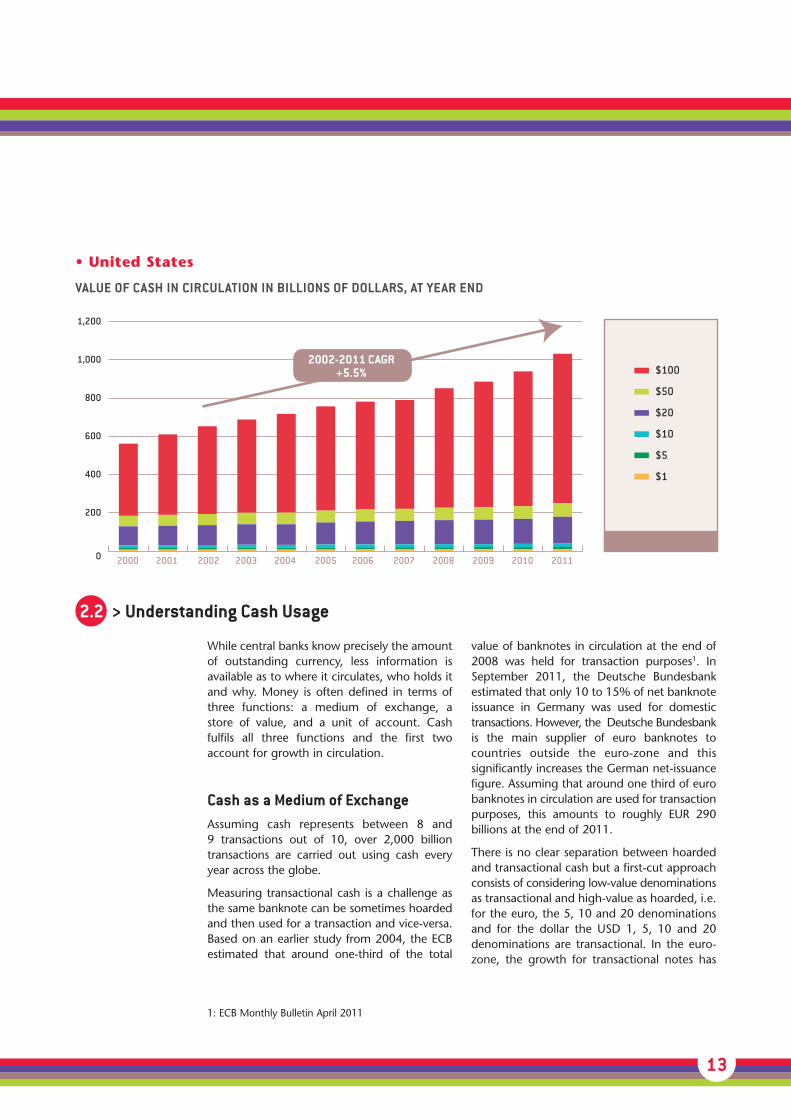

Currency in circulation refers to the numberand value of banknotes issued by the monetaryauthority, regardless of who holds it: consumers,businesses or financial institutions. It is the mostwidely used metric to measure cash demand. Inthe four markets studied in this report, the2002-2011 Compound Annual Growth Rate ofthe value of banknotes in circulation was 14%in Brazil, 10.6% in the euro-zone, 9.5% inSouth Africa and 5.5% in the US. The value ofbanknotes in circulation in these markets exceedsUSD 2,000 billion.

During this period, the transition economies ofBrazil and South Africa have experiencedsustained growth; however, cash in circulationhas exceeded GDP growth. In both countries,demographics have had a positive impact oncash in circulation, as the economically activepopulation has been increasing and movingup the social ladder. In the case of the euro-zone exceptional growth rates followed theeuro changeover as the reserves of hoardedcash in the legacy currencies of the euro whichhad disappeared, prior the changeover, werereconstituted; also, the international demandfor euro has fuelled growth over the period.However, following the changeover, annualgrowth rates have constantly fallen to between4 and 7% per annum in the course of theyears. In the US, the cash-in circulation toGDP ratio has remained remarkably stable overthe period, with a slight increase since 2007.

At a macro-economic level, cash demand istraditionally related to GDP growth, privateconsumption and inflation as well as theexchange rate, which drives internationaldemand. In more mature economies such asthe USA or the euro-zone, there are alternativesto cash both as a store of value and as apayment instrument and this could in theorychallenge historic models. However, duringthe last decade the weight of cash in theeconomy has been stable in the US and hasalmost trebled in the euro-zone, fromapproximately 3% in 2002 to 8.5% in 2010. Itis likely that the euro has challenged the dollaras an international reserve currency, especiallyin the countries surrounding the euro-zoneand this explains the growth differential betweenthe two currencies. Low interest rates since the 2008 financial crisis have reduced theopportunity cost of holding cash.

2.1 > Cash in Circulation

11

Brazil

South Africa

Euro-zone

US

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110%

2%

4%

6%

8%

10%

100

50

20

10

5

2

1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

2002-2011 CAGR+14%

0

80

60

40

20

100

120

140

160

180

CASH IN CIRCULATION/GDP

• Brazil

VALUE OF CASH IN CIRCULATION IN BILLIONS OF REAL, AT YEAR END

In the four markets, all denominations havebeen growing. But the relative growth rates ofeach denomination are an indication both ofthe usage of cash and the organization of cashdistribution. In Brazil, cash in circulation isdominated by the, BRL 50 note, which representsapproximately 50% of value. In South Africa,there is an overdependence on the ZAR 100denomination, which represents 75% of value

and 50% of volume. The SARB has set anobjective to reduce its weight in favor of lowerdenominations. In the euro-zone, the EUR 500represents a third of value, while in the USAthe USD 100 represents 80% of the circulatingdollars clearly illustrating the internationaldimension of these currencies as these high-value denominations are to a large extent usedoverseas.

12 THE FUTURE OF CASH 2012

2. Demand for Cash

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

2002-2011 CAGR+10.6%

1,000

900

800

700

600

500

400

300

200

100

0

500

200

100

50

20

10

5

• South Africa

VALUE OF CASH IN CIRCULATION IN BILLIONS OF RAND, AS OF END OF MARCH

• Euro-zone

VALUE OF CASH IN CIRCULATION IN BILIONS OF EUROS, AT YEAR END

R 200

R100

R 50

R 20

R 10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

2002-2011 CAGR+9.5%

100

90

80

70

60

50

40

30

20

10

0

While central banks know precisely the amountof outstanding currency, less information isavailable as to where it circulates, who holds itand why. Money is often defined in terms ofthree functions: a medium of exchange, astore of value, and a unit of account. Cashfulfils all three functions and the first twoaccount for growth in circulation.

Cash as a Medium of ExchangeAssuming cash represents between 8 and 9 transactions out of 10, over 2,000 billiontransactions are carried out using cash everyyear across the globe.

Measuring transactional cash is a challenge asthe same banknote can be sometimes hoardedand then used for a transaction and vice-versa.Based on an earlier study from 2004, the ECBestimated that around one-third of the total

value of banknotes in circulation at the end of2008 was held for transaction purposes1. InSeptember 2011, the Deutsche Bundesbankestimated that only 10 to 15% of net banknoteissuance in Germany was used for domestictransactions. However, the Deutsche Bundesbankis the main supplier of euro banknotes tocountries outside the euro-zone and thissignificantly increases the German net-issuancefigure. Assuming that around one third of eurobanknotes in circulation are used for transactionpurposes, this amounts to roughly EUR 290billions at the end of 2011.

There is no clear separation between hoardedand transactional cash but a first-cut approachconsists of considering low-value denominationsas transactional and high-value as hoarded, i.e.for the euro, the 5, 10 and 20 denominationsand for the dollar the USD 1, 5, 10 and 20denominations are transactional. In the euro-zone, the growth for transactional notes has

2.2 > Understanding Cash Usage

13

• United States

VALUE OF CASH IN CIRCULATION IN BILLIONS OF DOLLARS, AT YEAR END

1: ECB Monthly Bulletin April 2011

$100

$50

$20

$10

$5

$1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110

200

400

600

800

1,000

1,200

2002-2011 CAGR+5.5%

14 THE FUTURE OF CASH 2012

2. Demand for Cash

been higher than private consumption, withan average annual growth of 3.6% between2002 and 2010. In the US, these denominationsrepresent 17% of the total value of cash incirculation and 70% of the volume.

It should be noted that there are significantseasonal variations of transactional cash, whichreflect the variations in consumer spendingacross the week, the month or the year. Typically,in all four markets analyzed cash in circulationwill peak towards the end of the year asconsumers prepare for Christmas.

Cash as a Store of ValueAs cash is a non-interest bearing asset, there isan opportunity cost of holding cash equal toshort-term interest rates. Theoretically, thisshould limit the attractiveness of cash as astore of value. Nonetheless, cash presents anumber of attractive features for those whohoard it:

• Liquidity: by definition, cash is a liquid assetwhich can be immediately transformed forconsumption purposes or to acquire otherassets.

• Availability: cash is available to all, includingthose who do not have access to bankingservices or who do not understand or trustother assets.

• Trust: currencies which are hoarded areperceived as strong stable currencies. As anillustration, in spite of the recent debt criseswhich have hit both the USA and the euro-zone, there has been little impact on currencydemand.

In Brazil and South Africa, little information isavailable with respect to hoarding. However,given the relatively high interest rates it isunlikely that people who have access to bankingservices would hoard cash. This leaves theunbanked and under-banked, who have limitedalternatives, but while hoarding is naturallyimportant for these groups it is unlikely torepresent a significant share in value.

International and/or Regional Use Both the dollar and the euro are prominentinternational currencies and they are usedextensively outside of their borders. In the caseof the dollar, it is estimated that between 55 and 66% of the value of US currency is heldin foreign countries, primarily in USD 50 andUSD 100 denominations.

In the case of the euro, the ECB has estimatedthat, at the end of 2008, between 20% and25% of the euro banknotes in circulation wereheld abroad, essentially in neighboring countriessuch as Russia. However, this estimate isbased on essentially on registered bulk bankshipments outside the euro area and we expectthat the real figure is closer and possiblyhigher than the the upper band.

The Rand is emerging as a regional currency; itis legal tender in the Common Monetary Areawhich links South Africa, Lesotho and Swazilandinto a monetary union and it is also increasinglyused in bordering countries such as Namibiaand Zimbabwe. The Real on the other handcannot be considered as a regional currencybut it is used marginally in the borderingcountries namely Argentina and Paraguay.

Supply-chain InventoriesThe smooth functioning of the cash cyclerequires a certain amount of cash: retailersrequire change in their tills before accepting acash payment at the beginning of each day;ATMs are stocked with cash in order to fulfillcash withdrawals.

As described in the next section of this paper,there has been a decentralization of the cashcycle over the past decade. Ten years ago, cashwas essentially counted and sorted in cashcenters, as banks were reducing processing attheir branches; today, cash is increasinglyprocessed and recirculated closer to the point ofsale. The multiplication of cash delivery pointsand the increase in automation have led to anincrease in cash inventories throughout the cashsupply chain. The growth in the installed base ofATMs is a clear illustration of this process. Whilethe number of bank branches has remained

15

stable in the four markets during the past fiveyears, the installed base of ATMs has grown.However, a recent study1, predicts that by 2020,in America and Europe, the number of bankbranches will be as much as 50% less than thecurrent count, attributing this reduction to

technological advancements and higher levelsof financial sophistication amongst consumers.

More recently, there has been growth in retaildevices such as smart safes, recycling units, self-check-outs… which also lead to additionalinventories.

€-zone

USA

Left Hand Scale

Right Hand Scale

2006 2007 2008 2009 2010

Brazil

South Africa

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

50,000

100,000

150,000

200,000

250,000

2006

2007

2008

2009

2010

USA Brazil South Africa Euro-zone

Source: CPSS Red Book - January 2012 and ECB

0

100,000

200,000

300,000

400,000

500,000

NUMBER OF BANK BRANCHES

NUMBER OF ATMs

1: Global Retail Banking 2020 – Key trends and implications for retail banking real estate; James Brown, Lee Elliott, Colin Burnet; Jones Lang LaSalle

16 THE FUTURE OF CASH 2012

2. Demand for Cash

The financial crisis which shook the world in2008, has had a considerable impact on cashdemand across the globe. The most visibleconsequences in the mature economies of the US and the euro-zone, have been a loss ofconfidence in global finance and a significantincrease in demand for cash. The crisis actuallyhad multiple and complex impacts on cashdemand.

Increase in HoardingThe first and most visible impact has been anincrease in hoarding, in the wake of the collapseof Lehman Brothers in October 2008, as anxiouscustomers withdrew their money from theirbank accounts. The ECB has measured thatthe additional demand for euro banknotesresulting from the financial crisis representedEUR 35 billion during the months of Septemberand October 20081, a large part of which camefrom abroad. Two thirds of this demand wasfor EUR 500 banknotes.

Increase in Transactional CashBut the financial crisis has also led to anincrease in transactional denominations asconsumers moved away from credit cards todebit cards and cash. Part of this shift ismechanical: with the economic slowdown,consumers have been reducing their spendingand consequently the average transactionvalues have dropped. And cash is more widelyused for lower-value transactions. The 2010FRB Boston Survey of Consumer PaymentChoice (SCPC) shows that consumers shiftedtoward cash payments in 2009 and reducedtheir use of payment cards. As a result, the

share of cash in consumer payments increasedfrom 20.8 percent in 2008 to 28.2 percent in2009 and nearly 29% in 2010. And eventhough the cause is not clear, a survey of theBritish Retail Consortium shows that cash usagehas increased by 5.7% in the United Kingdomin 20112.

Budget Control It also appears that some consumers havereturned to envelope budgeting; in order tobetter control their monthly budget theyprepare cash envelopes for their main expenses.This process illustrates another key function ofcash – the unit of account. More than anyother payment instruments, cash enablesconsumers to understand and measure thevalue of goods and services and control theirbudgets. This becomes critical at a time whenconsumers need to de-leverage.

The financial crisis has clearly demonstratedthe contingency role of cash, which becomesa refuge value in times of crises. Besides the2008 financial crisis several other crises haveunfortunately reminded us of this importantrole: the earthquake and tsunami in Japan in2011, Hurricane Katrina in New Orleans in2005, the September 2001 terrorist attacks inthe US, not to mention the Y2K changeover.In the US, cash in circulation grew by 20% in1999, in anticipation of the Y2K changeover.At the time of writing of this report, the Greekdebt crisis led to a sharp increase in cashdemand in May 2012. Large outflows of cashduring all these events have contributed tokeep the financial system afloat by enablingtransactions in times of instability.

2.3 > The Impact of the 2008 Financial Crisis on Cash Demand

1: ECB Monthly Bulletin, April 20112: Cost of Collection Survey, British Retail Consortium

17

One key question remains: how long will theimpact of this crisis last? Will consumers goback to their pre-crisis payments and savingshabits as soon as the economy recovers or willthis have a long-term impact? It is worthmentioning that the Great depression shapedthe saving behavior of an entire generation. In

the USA, consumers rate cash highest invirtually every payment characteristic (acceptance,convenience, cost, and security) and therankings have strengthened between 2009ans 2008. This suggests that consumer demandfor cash is unlikely to disappear any timesoon1.

Measuring the Share of CashThe value of cash in circulation is not directlyrelated to the share of cash as a retail paymentinstrument, essentially because cash is alsoused for other purposes than transactions.

Unlike other payment instruments, cashtransactions are not registered and monitoredindividually by banks and payment schemes.Accurate data on the volume and value of cashtransactions is not available and surveys arerequired to estimate these figures. Two mainapproaches are used. The first is a top-downapproach, which consists in measuring privateconsumption and deducting the value ofcashless payments; the difference gives anapproximation of the value of cash payments.The second is the diary method whereby arepresentative sample of consumers is invitedto register all their transactions during a givenperiod of time. Both methods however onlyprovide estimates and the margins of error canbe significant; one survey carried out in theNetherlands2 indicated that the volume ofcash transactions ranges from 3 to 7 billiontransactions.

In Europe, the ECB’s company survey on theuse of cash estimated that the value oftransactions paid in cash in 2008 amounted to

around EUR 1,400 billion in the sectors ofactivity covered by the survey. This exceedsthe transactions paid with debit and creditcards which amounted to just below EUR1,000 billion.

In South-Africa, the reserve bank has estimatedthat 86% of retail transactions volumes and56% of value were settled in cash in 2011.

In the United Sates, the Federal Reserve Bankof Boston conducts an annual survey ofconsumer payment choice1. In 2009, the surveyconcluded that the average consumer made64.5 payments in a typical month. Debit cardswere the most commonly used instrumentwith 29.3% of payments, followed by cashwith 28.2% and credit cards with 11.2%.These figures include all types of payments, i.e.bill payments, online payments, retail, serviceand person-to-person payments; if we look atretail, service and person-to-person payments– then cash is first with 25.2% followed bydebit cards with 19.8%.

In Brazil, for 72% of the population, cash wasthe most frequently used payment instrumentin 2010. Nonetheless, the figure dropped from82% in 2007. On average, 59% of consumerspending was paid in cash in 2010, downfrom 77% in 20073.

2.4 > The Share of Cash in Retail Payments

1: The 2009 Survey of Consumer Payment Choice, by Kevin Foster, Erik Meijer and Michael A. Zabek; Federal Reserve Bank of Boston.

2: Explaining cash usage in the Netherlands: the effect of electronic payment instruments; DNB Working paper N° 136, March 2007.

3: O brasileiro e sua relac�a�o com o dinheiro – III; Banco Central do Brasil, 2010.

18 THE FUTURE OF CASH 2012

2. Demand for Cash

The rational arguments for selection of cash asa payment instrument are well known – budgetcontrol, convenience, anonymity… - but thereare also subconscious reasons which will triggerthis decision and which are less well known.Payment behavior differs according to thepayment instrument used: e.g. people spendmore in coins than in banknotes; in NYC, taxisreceive larger tips with cards than with cash;card issuers often argue that card usageincreases spending… Research from the DNB1

has shown for instance, that Dutch residentsoriginating from countries which are morecash intensive are likely to use more cash inthe Netherlands as well.

The Relative Share of Cash at the Point of Sale is DecliningIn the long-run, cash has been challenged andsubstituted by other payment instruments andthe debit card in particular. The competitionfirst came from checks, followed by credit anddebit cards. The competition is intensifyingwith the multiplication of alternative paymentsinstruments, many of which are specificallytargeting low-value transactions – pre-paidcards, contactless cards, mobile phones….While the share of cash within all paymentshas declined, in most cases this has been offsetby the growth in transaction volumes.

One country which has seen a stronger declinein cash usage than most is the Netherlands,where DNB research shows a decline both inthe number of transactions and in value between2007 and 2010. A major driver for this cashsubstitution has been a joint campaign in2008-2009 from banks and retailers to promotecard payments. Following an agreement withretailers, banks agreed to stabilize the cost ofinterchange fees if retailers promoted electronictransactions. This resulted in growth in cardtransaction volumes. The effect of the campaignstabilized in 2010. This could be a signal thatthere is a threshold below which it is difficult orcostly to reduce the level of cash usage.

In the case of the Netherlands, the decline incash usage has been driven by an industryinitiative to promote card payments ratherthan by consumer preferences. Nordic countrieshave also seen a decline in cash usage; in thesecases banks have rendered access to cashmore difficult and costly by reducing theirATM fleets and closing down cash services intheir branches. As a result, ATMs in Finlandand Sweden have the highest usage rate in theEuropean Union with 8,500 and 5,000withdrawals per month, respectively.

A finer analysis shows that cash is crucial insome segments. This is the case for example inrestaurants and bars, in convenience stores aswell as many service providers. In Brazil, bakeriesreceive 95% of their revenue in cash, andpublic utilities 83%2. As stated earlier, in general,cash is more widely used for low-value payments.

Cash usage is very much influenced by lifestylefactors, and in particular where people shop.Typically, smaller stores tend to be more cashintensive, whereas large retailers see more cardusage. If online shopping increases, then cashusage is likely to decline. However, in recentmonths major on-line shopping sites and on-line stores of major retailers have indicatedthey accept cash for on-line purchases. Forexample, shoppers in the United States cannow make on-line purchases at Walmart andmake a cash payment at a local store. Twofactors are driving this new convenience. One,this form of payment allows the unbanked andor the under-banked with no access to creditor debit cards to make on-line purchases.Two, retailers can offer products and serviceson-line, which are not available at their stores.One potential long-term benefit for the retailersis their ability to reduce the store size byoffering larger products on-line only.

1: Choosing how to pay: the influence of home country habits; Anneke Kosse and David-Jan Jansen, DNB working paper n° 328, December 2011

2: O brasileiro e sua relac�a�o com o dinheiro – III; Banco Central do Brasil, 2010

19

The success of cash is based on three keyvalues: universality, trust and anonymity.

UniversalityUniversality means that cash is widely accepted,in a variety of situations. It does not requiretechnology to pay or be paid. It can be usedby all, young or old, rich or poor and acceptedby all. For some segments of the population itis the only available payment instrument e.g.the unbanked, children… For other groups, itis the most convenient payment instrumente.g. the blind, those suffering from mentalillnesses, the illiterate… as it provides ease ofuse. Banknote printers have invested in thedesigns to facilitate the use of notes by thesegroups. The fact that cash does not require aninfrastructure means that it is the preferredpayment instrument for those who do notprocess large volumes of transactions. Cash isalso available for a broad range of transactions;face-to-face transactions, peer-to-peertransactions. Cash is suitable for microtransactions – e.g. parking meters; it is themost common instrument for low-valuetransactions (under USD 20) but it is also usedfor high-value transactions, which exceed credit-card limits. It is widely used for remittanceseither through formal or informal systems,such as ’Hawala’ (meaning transfer, also

known as hundi) which is an informal valuetransfer system based on the performance andhonor of a huge network of money brokers,primarily located in the Middle East, NorthAfrica, the Horn of Africa, and South Asia. It isbasically a parallel or alternative remittancesystem that exists or operates outside of, orparallel to traditional banking or financialchannels.

TrustThe second core value of cash is trust and thisis based on a combination of factors. As legaltender, cash is issued by a public monetaryauthority and is perceived as public money,with the backing of the state. Ever since thegold standard was abandoned in 1971, cash isfiat money i.e. derives its value from agovernmental – or in the case of the euro –inter-governmental mandate. Trust also appliesto the technology developed on the banknotesto ensure the quality and security of thebanknotes as well as the infrastructure andprocesses in place to ensure counterfeitdetection.

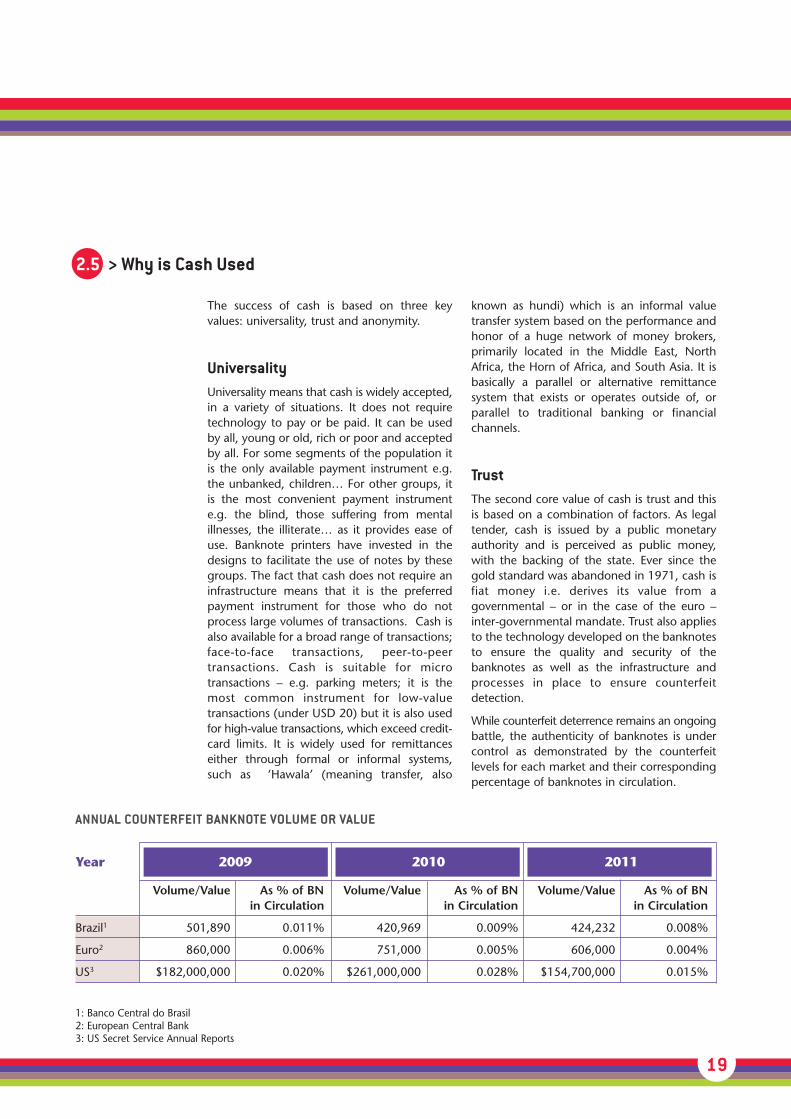

While counterfeit deterrence remains an ongoingbattle, the authenticity of banknotes is undercontrol as demonstrated by the counterfeitlevels for each market and their correspondingpercentage of banknotes in circulation.

2.5 > Why is Cash Used

1: Banco Central do Brasil2: European Central Bank3: US Secret Service Annual Reports

Year 2009 2010 2011

Volume/Value As % of BN Volume/Value As % of BN Volume/Value As % of BNin Circulation in Circulation in Circulation

Brazil1 501,890 0.011% 420,969 0.009% 424,232 0.008%

Euro2 860,000 0.006% 751,000 0.005% 606,000 0.004%

US3 $182,000,000 0.020% $261,000,000 0.028% $154,700,000 0.015%

ANNUAL COUNTERFEIT BANKNOTE VOLUME OR VALUE

20 THE FUTURE OF CASH 2012

AnonymityAnonymity is a value which is specific to cashas it is the only payment instrument whichdoes not require the transmission of identitydata between the payer and the payee. Thetransfer of identity represents the risk of identitytheft but also with the development of loyaltyschemes, data mining and one-to-one marketingan increasing invasion of one’s privacy. It islegitimate to ask whether it is necessary anddesirable, from a societal point of view, tocommunicate one’s identity when you make atransaction. And it raises a number of questions:how is the information stored? How is it used?Is it passed on to other parties? Who owns theinformation? etc…

The anonymity of cash is restricted. Firstly it islimited by the sheer bulk of cash. Secondly, itis restricted by regulations which imposereporting obligations to payment institutionsand other exposed persons (casinos, real-estatedealers, lawyers and accountants) as establishedby the Financial Action Task Force and laiddown in the Anti-Money Laundering andCounter-Terrorist Financing standards. Thirdly,many countries have restricted cash usage toavoid tax evasion.. In the wake of the Europeandebt crisis several countries have established acap for cash transactions: in Spain a limit ofEUR 2,500 has been set on cash transactionsfor business owners and independent contractorsand in Italy, the government reduced themaximum permissible payment in cash fromEUR 2,500 to 1,000 in December 2011. Lastly,anonymity is also restricted by technology,e.g. serial number tracking systems are in useby law enforcement agencies to combat criminalactivity.

2. Demand for Cash

21

Let us first review the current cash cycle foreach of the four markets and the factors thathave influenced change over the years.

THE BRAZILIAN CASH CYCLEAs the socio-economic landscape of the countryhas evolved, so has the role of the BancoCentral do Brasil (BACEN) in managing thecash cycle of Brasil. With cash in circulationincreasing at an average annual rate of 14%over the last ten years coupled with theproliferation of automation solutions that haveincreased consumer access to cash, BACEN hashad to increase processing capacity and enhanceits infrastructure to keep pace with this growth.

Given the changing dynamics of the country,in 2006 BACEN decided to outsource all cashprocessing and recirculation to Banco do Brasil(BdB), which is the largest bank by assets andcontrolled by the government, under a custodialinventory scheme. Under this program, allcommercial banks make deposits to andwithdrawals from their reserve account withBACEN operated and managed by BdB at over140 cash centers and almost 1,400 bankbranches throughout the country. The cost ofthe services is covered by the users (commercialbanks). A Custody Council, with BACEN, BdBand commercial bank members was created tohelp manage this system.

BACEN remains the exclusive entity thatmanages the introduction, distribution anddestruction of cash and through its 10 cashcenters around the country, BACEN maintainssupervisory oversight over the performance ofBdB by checking the compliance with custodyregulations, the quality and authenticity ofcash in circulation as well as conducting allbanknote destruction. The transportation isshared: BACEN is responsible for transportationfrom the print works to the main cities whileBdB are responsible for the other stages, fromthe main cities to other distribution points.BACEN periodically conducts research studieswith the public to assess the perception that ithas about the quality of money in circulationand the use of banknotes and coins.

In support of its continued role in the Braziliancash cycle, the 10 BACEN cash centers haveundergone several modernization projectsincluding a new IT Cash Operation ControlSystem introduced in 2009, new high-speedbanknote sorting machines installed in 2010and on-line and off-line destruction systemsintroduced in 2011.

In the last quarter of 2010, the two higherdenominations of a new banknote series werelaunched, updating the design and securityfeatures. The medium denominations werelaunched in July 2012 and the last twodenominations will be launched in 2013. Thereplacement of the current series will begradual and the banknotes will not lose theirlegal tender.

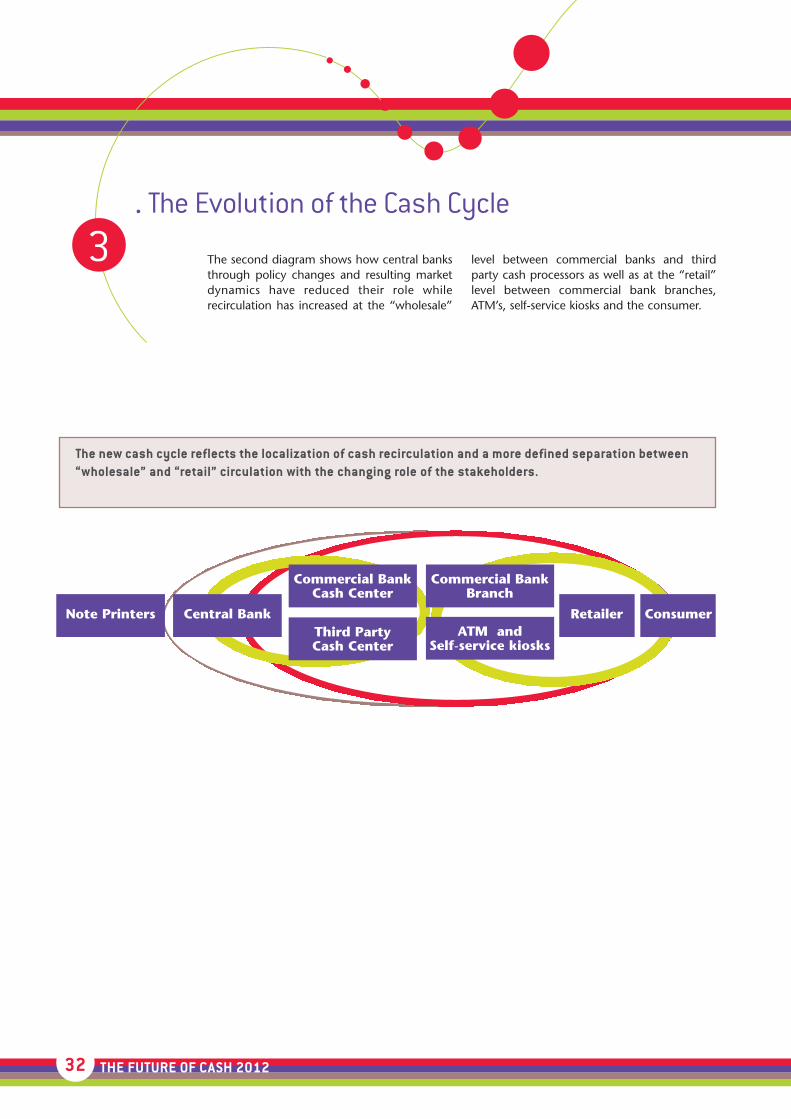

. The Evolution of the Cash Cycle3

3.1 > The Four Cash Cycles

22 THE FUTURE OF CASH 2012

3. The Evolution of the Cash Cycle

THE EURO-ZONE CASH CYCLESThe Eurosystem, which comprises the EuropeanCentral Bank (ECB) and the national centralbanks of the Member States whose currency isthe euro, is the monetary authority of the euroarea. The ECB has the exclusive right toauthorize the issuance of banknotes within theeuro area and is responsible for maintaining itsintegrity. The Eurosystem is responsible fordefining certain common principles such asthe recirculation of banknotes, the free-of-charge services provided by the national centralbanks… The Eurosystem consists of severalnational cash cycles. Cross Border cash transportsonly takes place on a very limited scale. Due todifferent circumstances and historicaldevelopments in the euro area countries, eachof these cash cycles has its own characteristicsand peculiarities. Each national central bank isresponsible for the physical distribution andprocessing of banknotes within their territoriesand for defining their cash distribution models.For this purpose, each central bank maintainsa network of cash centers. There are currently257 central bank branches in the euro zone,which is half the number at the moment of theintroduction of euro banknotes and coins inJanuary 2002. As for cash distribution models,some countries have Largely delegatedprocessing to the commercial sector – Finland,the Netherlands, Spain – while in othercountries, the central banks process the majorityof banknotes– Germany, France, Italy… andare continuing to consolidate their footprint.

The euro area established a banknote recyclingframework in 2004, following complaints fromthe market that in some countries, banks hadto lodge all banknotes received by them withthe National Central Bank, while in othercountries banks could recirculate banknotes.Following the recycling framework, which wascast in an ECB Recirculation Decision in 2010,some National Central Banks have stimulatedbanks and cash processing companies torecirculate fit banknotes received by them, byintroducing some form of balance sheet relief– Cyprus, Finland Greece, Ireland, Malta, the

Netherlands, Slovenia, Spain. These marketshave seen the development of industrial orcash center recirculation. In other markets, therecirculation takes place closer to the point ofuse, either through recirculating ATMs, as inBelgium or in branch back offices as in Franceor Germany. The implementation of banknoterecirculation as of 2005 has led to thestabilization of the volume of banknotes whichare fitness sorted at the central bank facilitieswhich fluctuates between 2.5 and 3 billionpieces per month.

In 2007, the ECB Governing Council adopteda roadmap towards medium-term convergenceof the cash services of the national centralbanks. The Eurosystem does not envisage a“one-size-fits-all” model and has provided forflexibility and a transition period for thisconvergence process. Some measures havebeen implemented such as: remote access tonational central bank services in the wholeeuro area; harmonization of basic services suchas coin lodgements from professional clients,common free-of-charge services; commonminimum opening hours. One importantmeasure currently being implemented in theharmonization of the electronic data exchangebetween national central banks.

THE SOUTH AFRICAN CASH CYCLEThe South African cash cycle is undergoingfundamental changes.

The South African Reserve Bank (SARB) used toprocess a third of the banknotes; cash centersowned by commercial banks or SBV the bank-owned wholesale processor would processanother third. The rest was processed at theretail locations. Fitness standards were introducedin 2006.

In 2010, the SARB introduced changes to itsdistribution policy and established fees forlodgements and withdrawals which has ledcommercial banks to develop recirculation. In2012, the central bank has indicated that itwill reduce its role as a processor and eventually

23

only process unfit notes i.e. between 20 and25% of cash in circulation. The SARB willmaintain a network of 6 branches with onlineshredding; the current processing capacity isbeing transferred to the commercial sector.The SARB will increase it monitoring of thefitness sorting and will conduct an annualinspection of equipment.

The existing Notes Held To Order (NHTO)system which offers overnight relief will becapped and eventually phased out to bereplaced by a Custodial Inventory System (CIS)which aims at compensating intra-monthvolatility of cash flows. This model will requirean improved forecasting and inventorymanagement system which is currently beingdeveloped.

In the last quarter of 2012, a new banknoteseries bearing the portrait of Nelson Mandelawill be launched. The five denominations will becirculated simultaneously and a 12-month co-circulation period is expected. The new seriesare expected to have an increased lifespan thanthe current one which is 18 months for the ZAR100 denomination and 6 for the ZAR 10.

The objective of the new cash distributionmodel is to improve the efficiency of theholistic value chain. The introduction of centralbank fees will incentivize banks to seek forefficiencies and will encourage recirculation ofbanknotes both at wholesale and at point ofsale level. SBV will play a central role as it is thesole entity entitled to operate the NHTO andCIS mechanisms.

THE US CASH CYCLE“The Federal Reserve’s mission and fundamentalobjectives in providing cash services have beenconstant over the years, but its approach tomeeting these objectives has evolved steadily totake advantage of advances in technology andto respond to changes in the way depositoryinstitutions (DIs) use the Fed’s cash services.Advances in currency processing equipmentand sensor technology have increased productivity

and improved note authentication and fitnessmeasurement, thereby reducing the prematuredestruction of fit currency while maintainingthe quality and integrity of currency in circulation.

The Federal Reserve has significantly altered its cash operations “ footprint” over the past 15 years. These changes have balanced theincreased (societal) cost of transporting currencyfarther to and from the market where it isneeded, on the one hand, and the efficiencygains and cost savings associated with leveraginggreater economies of scale through consolidationof processing volumes and elimination ofredundant (fixed cost) support and overheadexpenses, on the other. As a result, the FederalReserve has opened one additional cashprocessing operation in 2001 and closed tenprocessing operations in the past 15 years.However, the Fed has not closed any operationswithout establishing a “cash depot” in thatmarket. Cash depots are operated underoutsourcing arrangements by a third‐partyvendor that acts as a secure collection pointfor Federal Reserve currency deposits from aregion’s DIs, and as a secure distribution pointfor currency orders that DIs have placed withthe servicing Reserve Bank located in anothercity. The work of verifying deposits andpreparing orders is performed by the servicingReserve Bank. The currency is transportedbetween the depot and the Reserve Bank insealed containers. The Federal Reserve pays forthe transportation between the depot and theservicing Reserve Bank. Credit for deposits ispassed to the DI upon receipt and bulkverification at the depot, and the charge fororders does not occur until the day that ordersare picked up from the depot.

Policy changes in recent years have alsocontributed to the evolution of the FederalReserve’s role in providing cash services. Withimplementation of the Custodial Inventory (CI)Program in 2006 and the cross-shipping fee in2007, the Federal Reserve significantly alteredthe costs faced by some DIs in processing and recirculating currency, and as a result,encouraged significant changes in their behavior.

24 THE FUTURE OF CASH 2012

3. The Evolution of the Cash Cycle

Provided they could meet the operating andfinancial requirements, DIs that coulddemonstrate the ability to recirculate a significantvolume of currency on a weekly basis becameeligible to participate in the CI Program, whichafforded them “balance sheet relief” by enablingthem to hold $10 and $20 notes in their vaultsthat are accounted for on the Fed’s books.About 16 DIs currently operate 92 CI vaults.Coupled with the cross-shipping fee, DIs

responded strongly and quickly to theseincentives by reducing their cross-shipping of$10 and $20 notes. Within a span of less thaneighteen months, the Fed saw a 50% decreasein cross-shipping and a 20% decline in ordersand deposits, accounting for most, but not allof the decline in total FRB volumes in 2007and 2008.”1

The cash cycles in the four markets haveundergone an evolution resulting from changesin regulations, improved technologies, growthand sophistication of their consumers,distribution and availability of cash, and pressurefrom non-cash payment alternatives.

3.2 > Key Trends Impacting the Cash Cycle

REGULATORY• Banknote Recirculation• Central bank footprint

• Cash distribution models• Balance sheet relief mechanisms

SOCIO-ECONOMIC• GDP growth

• Demographics• Interest rates• “Black swans”

MARKET FACTORS• Bank disintermeditation

• Cash substitution• Change in lifestyle factors

• Growing transaction volumes

TECHNOLOGY• High-speed sorters• Local recirculation

• Inventory management systems• Retail cash-office technology

CASH CYCLE

1: Federal Reserve Cash Product Office

25

While the cash cycle in the four markets aresimilar in terms of representative stakeholders,the role and function of each stakeholdergroup is different indeed. It could be arguedthat the primary factors influencing thesedifferences are the model of the central bankand the business strategy of the otherstakeholders in the cash cycle. Needless tosay, the higher up the cash cycle food chain,the more the business strategy of the stakeholdergroup influences the what, where, when andhow further down the chain! One key changein this evolution has been the functional andoperational changes in the central bank profile,which have pushed cash processing functionsto commercial entities thus resulting in a new “wholesale” (central bank + commercialprocessors) and “retail” (financial institutions +retailers + consumers) recirculation cycle.

Central Bank FootprintOne key trend impacting the cash cycle is thereduction of central banks’ footprint. Theconsolidation of central bank cash centers hasfirst resulted from improvements in technologies,which have led to the increase in the throughputof high-speed banknote sorters. This has resultedin the emergence of a new generation oflarger, more industrialized cash centers, oftenlocated in the vicinity of communication hubs,to facilitate and expedite logistics. Thanks toimproved sensor technology, central bankshave also reduced the volumes of banknotesshredded prematurely.

Technology and improvements throughoperational best practices have been instrumentalin the reduction of the brick-and-mortarinfrastructure in the four markets studied.While central and commercial banks and thirdparty processors will continue to look for thistype of infrastructure improvements, these willprimarily represent consolidations in the industry.Regardless of the technological improvements,there will remain a need to sort and recirculatecash at both the “wholesale” and “retail” levelfor the foreseeable future so a physical

infrastructure is a necessary components of thecash cycle.

In the US, in addition to the recirculationpolicy the introduction of the “Check 21”(check truncation) policy eliminated the needto move the physical checks from the processingbank to the domiciling bank and eliminatedthe Federal Reserve’s role as the check clearing-house for their member banks. Assuch, Federal Reserve branch offices thatsupported both cash and check processingwere faced with increased costs for cashprocessing since the fees from check clearingswere eliminated. Therefore, the Federal Reserveundertook a study to reduce their cash operationsfootprint through closures and redistributionof their incoming and outgoing volumes from36 to 26 locations.

As more central banks shift their role from asovereign entity, (controlling) overseeing allaspects of cash processing and cash circulationto an administrative role, (involved anddelegated) that participates in and monitorsthe industry’s performance, they have pursueda consolidation effort to reduce their footprint.Whereas the controlling model forces thecentral bank to remain active and maintainprocessing centers in all regions of their country,the changing model has allowed central banksto consolidate further and close operationcenters where commercial entities have takenon the role of local processing and recirculation.

The introduction of technology platforms thatallowed commercial entities to closely emulatethe fitness sorting and recirculation as well ascounterfeit detection functions historicallyperformed by central banks has enabled centralbanks to reduce their infrastructure. Thesetechnologies include high-speed sorters,intelligent (smart) safes; multi-function andrecirculating ATMs and teller and retailer cashrecyclers.

High speed sorters entered the commercialsector some fifteen years ago and while theyenabled non-central bank entities to effectivelyand efficiently perform verification, fitness

26 THE FUTURE OF CASH 2012

3 sorting and suspect counterfeit detection, theirprice point made them cost prohibitive formost commercial cash processors to adopt thetechnology. Even today, these high-speedsorters remain the domain of cash processorswith operations in metropolitan areas wherethe density of clients and their associatedvolumes of cash justifies the expenditure.However, as the “retail” cash cycle hasprogressively gotten shorter, and thus closer tothe consumer, smaller and less expensivesorters have closed the gap between the largeand small commercial operators.

The assumption of cash processing andrecirculation functions by commercial banksand other third-party service providers hasresulted in policy and profile changes and orenhancements to existing policies. However,budgetary constraints and improved technologieshave contributed to the closures and consolidationof central bank operation centers, as well.

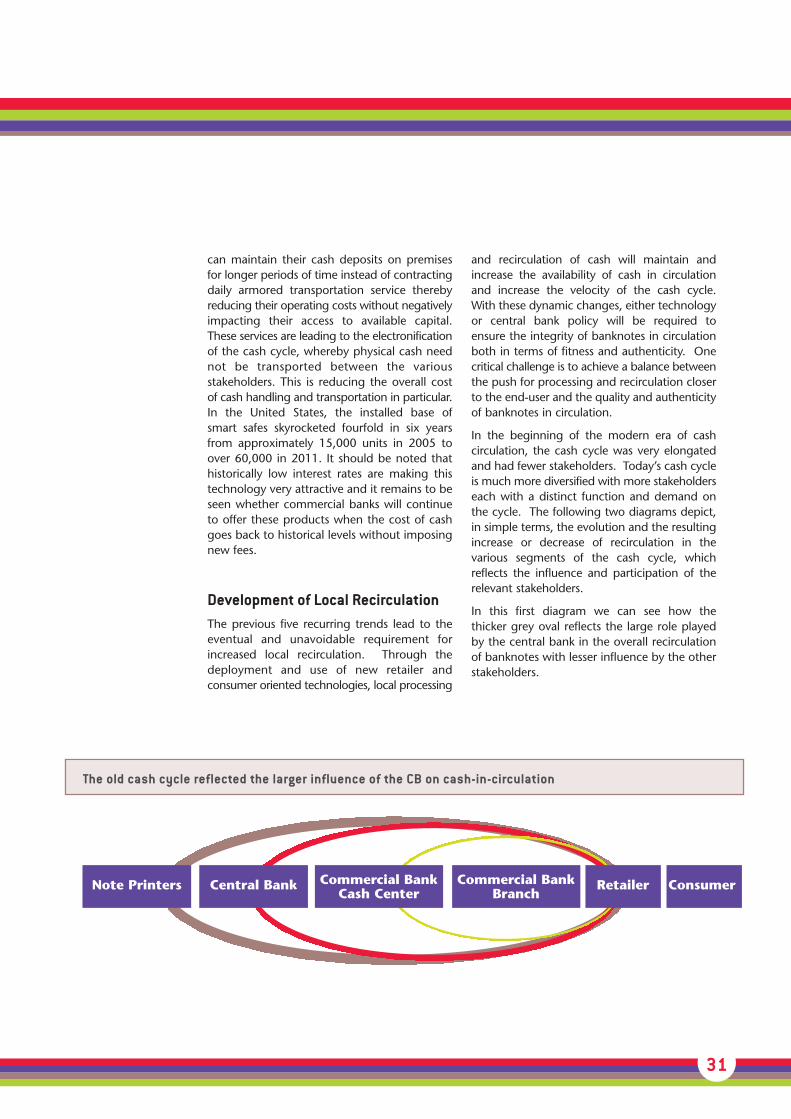

The availability of cash has been enhancedthrough the deployment of existing and newdevices (ATM, recyclers, multi-function kiosks,etc.) that have introduced more cash accesspoints for consumers. The continual migrationof the cash cycle from a centralized (wholesale,central bank controlled and facilitated) to adiversified (retail, expansion of recirculation tostakeholders down the cash supply chain)model will continue to increase the availabilityof cash.

Changing Cash Distribution Policiesof Central Banks While many factors have influenced the evolutionof cash in circulation, the smooth functioningof the cash cycle is primarily the responsibilityof the central bank. As such, central bankmodels and policies determine the flow andexchange of cash in the cycle. To betterunderstand the changing role of central banks,it is important to review the prevailing centralbank profiles. There are currently three modelsemployed by nearly all central banks around

the world.

• “Controlling” – the central bank exclusivelyperforms banknote authentication, fitnesssorting, recirculation and destruction.

• “Involved” – the central bank allows orrequires commercial banks to performauthentication, fitness sorting and recirculation.

• “Delegated” – the central bank effectivelydelegates all cash processing related activities,except for initial distribution and finaldestruction, to commercial banks.

As recently as twenty years ago, the “Delegated”model was non-existent and few central banksemployed the “Involved” model. Today, mostcentral banks have adopted the “Involved”model - US, France, Germany, Italy, Spain…-and several have completely delegated – Brazil,South Africa, the Netherlands… - the cashprocessing and recirculation function to thecommercial sector. The “Controlling” modelis the dinosaur of the industry and thus nearlyextinct.

Regardless of the model, the central bankestablishes the criteria for fitness sorting anddefines what constitutes a “fit” banknote.Furthermore, by its nature, the central bank isthe only entity in the entire cash cycle that caneffectively cull out all counterfeits fromcirculation.

One of the most important functions of a

Involved Delegated

Belgium Brazil

France The Netherlands

Germany South Africa

Italy

Spain

US

. The Evolution of the Cash Cycle

27

central bank, whether as a sovereign or anadministrator, is to ensure the integrity andavailability of cash. The effectiveness of thecash cycle is determined by two key factors.The first being the volume of cash in circulationthat at some point or another must be processed(verified, authenticated and fitness sorted) andthe second is the velocity with which the cashis processed and made available to the cycle.Both of these factors are critical in determiningthe processing bandwidth requirements withina specific geography. Therefore, delegatingand involved central banks have introducedrecirculation policies that encourage participationby and organizational commitment fromfinancial institutions.

In the euro zone, the ECB have enacted policychanges that permit banks to process andrecirculate cash deposited with their institution.There are no incentives or penalties associatedwith the ECB policy. The velocity of cash isincreased if recirculation is done locally. However,in other cases, such as the US and SouthAfrica, the recirculation policy is more of amandate to encourage banks to perform theirown sorting and recirculation or pay a fee forthe same functions to be performed by thecentral bank. In the US, the Federal Reservemaintains an involved profile but has delegatedcash recirculation of the USD 10 and USD 20to commercial banks through a RecirculationPolicy introduced in 2007.

Balance Sheet Relief MechanismsRecirculation may lead to an increase in thevolume of vault cash as banks process cash intheir facilities rather than returning it to thecentral bank, thus resulting in additionalinventories and consequently higher opportunitycosts. Some central banks have introducedpolicies to incentivize recirculation andcompensate the cost of funding these additionalcash inventories through balance sheet reliefmechanisms. The most notable and frequentlyused policies are “Notes Held to Order” (NHTO)and “Custodial Inventory” (CI).

The Bank of England was the first central bankto introduce a Notes Held To Order schemeand the following is an excerpt from “Managingthe Circulation of Banknotes” by the Bank ofEngland’s Notes Division published in 2010.

“A significant development came in 1982when the Bank introduced the Notes Held toOrder (NHTO) scheme to address the risks andcosts associated with excessive volumes ofnotes being transported to and from the Bank.Before the 1980s, financial institutions wouldphysically return large volumes of surplus notesto the Bank (including its regional branches)for storage, then collect them when requiredto fulfill public demand. This was because thealternative — of holding the surplus notesthemselves — would mean that a financialinstitution would incur the cost of funding anon interest bearing asset on its balance sheet.Over time, the volumes being transportedeach day grew in size and the associated risksand costs rose commensurately. The principalfeature of the NHTO scheme was that itallowed scheme members (the major financialinstitutions handling large quantities of notes)to be paid the face value for selling surplusnotes to the Bank, but without physicallyreturning those notes to the Bank. They couldhold these notes — with no balance sheetfunding cost — securely in their own cashcenters until demanded by the public. Thisremoved the financial incentive for physicalmovements of notes to and from the Bank. Asa result, the NHTO scheme substantially reducedthe transport costs and associated risks ofcommercial note distribution. By 2001, notesorting was established as an activity wholly inthe commercial sector and the NHTO schemewas replaced by the Note Circulation Scheme(NCS). The NCS incentivized greater efficiencyin members’ processes and improved the riskmanagement of the overall scheme. Importantly,it retained as a central principle the mechanismfor relieving members of the funding cost ofholding notes that are being sorted, or held assurplus to current demand.”

28 THE FUTURE OF CASH 2012

3 While balance sheet relief mechanisms all aimat reducing the funding costs of cash inventories,the actual models vary significantly from countryto country: some offer overnight relief whileothers compensate intra-month variations indemand; in some cases, they are solely anincentive; in others, the central banks introducedfees for lodgements and/or withdrawals.Custodial Inventory in various forms has beenin existence for decades as well. However, inrecent years these policies have been undertakento influence the behavior and function of thecommercial banking sector. Custodial Inventoryworks much like the NHTO program and thefollowing is an excerpt from the US FederalReserve’s “Cash Services Custodial InventoryProgram”, which was introduced in March of2006.

“A custodial inventory enables an institution totransfer currency to the Federal Reserve Bank’sbooks, but physically hold the currency withintheir secured facility, thereby reducing theinvestment cost of holding currency longenough to recirculate it to customers. TheCustodial Inventory program is applicable onlyto USD 10 and USD 20 notes. Under theprogram, an institution may hold in a CustodialInventory up to four days average dailypayments in USD 10 and $20 notes, providedit holds one day of average daily payments onits own books.”

Balance sheet relief mechanisms are available- in different forms – in Brazil, Cyprus, Finland,Greece, Ireland, Malta, the Netherlands, Slovenia,Spain, South Africa and the US. These systemssupport the large scale recirculation of banknotesbetween banks and other commercial parties.They also enable the clearing of cash betweenparticipants.

Changing Business Model ofCommercial Banks The physical handling of cash is an industrialprocess, far away from the perceived corecompetencies of banks. Cash is also generallyperceived as a cost center and cost reduction

has been the driving strategic focus. In thepast, the main response has been outsourcing.In all markets, transportation has been fullyoutsourced to cash-in-transit companies. Thepicture is far more heterogeneous for bothcash center operations and ATM servicing:some banks are fully outsourced while otherscontinue to run both their cash centers andtheir ATM networks. The trend however hasbeen to increase outsourcing. Our observationsand feedback from participating commercialbanks indicate a strong desire on their part toexit cash processing as independent operators.Outsourcing to third-party vendors has becomea norm throughout the world over the lastdecade or more.

The development of recirculation has alteredthis evolution. On the one hand, recirculationhas pushed processing towards the bank branchand therefore led banks to re-insource somelevel of processing. On the other hand, it hasenabled banks to reduce their dependency onthird-party providers.

As with any business, the lower the fixed costs,the more efficient and cost effective theendeavor. Therefore, some central banks arereducing their national footprint and pushingthe responsibility down the food chain throughrecirculation and other polices. Since the cashcycle requires processing centers, commercialbanks have been forced to establish or expandtheir own centers and or outsource their workto third party processors. This cost reductionacross the industry is another factor contributingto the localization of cash in circulation thusreducing transportation and storage costs.

With governments and commercial entitiesunder constant pressure to reduce costs andincrease their efficiency, cash recirculation inmost markets has separated into the “wholesale”and “retail” sectors. This shortening of thecash cycle has allowed many stakeholders toachieve cost reductions. Some would arguethat localization is as a direct result of thesebudget cuts while others are convinced thatlocalization was inevitable and cost reductionsare the positive by-product.

. The Evolution of the Cash Cycle

29

Additionally, as an alternative to outsourcing inorder to create economies of scale and toreduce the cost and increase the efficiency ofcash processing, some countries areexperimenting with various consortium modelsthat represent a partnership between commercialbanks and/or cash-in-transit companies – thelater as either service providers and or full-fledged partners.

SBV in South Africa is an illustration of thismodel. SBV was established in 1986 by thethree major banks at the time in order tooptimize operational savings through co-operation between the banks in respect ofprocessing and secure transportation of bulkcash. Retail cash processing and ATM serviceswere later added to service offerings. SBV hassince evolved into an independent commercialcompany, now equally owned by the fourmajor banks in South Africa, with a focus oncash risk management. SBV is the sole entityauthorized and approved by the South AfricaReserve Bank to operate the Notes Held ToOrder (NHTO) and Custodial Inventory System(CIS) mechanisms.

In addition to SBV in South Africa, some otherexamples include:

Geld Service Nederland (GSN) a partnershipbetween the three major banks – ABN Amro,ING and RABO with the Dutch National Bank(DNB) as a Supervisor Board observer – handlingmore than 90% of cash flow in the bankingcenters serving its member banks as well asother financial institutions.

GSA, a subsidiary of the Austrian Central Bank(OeNB) in cooperation with commercial bankswhere cash processing is outsourced to theGSA while the OeNB maintains its core centralbank functions of banknote issuance, counterfeitdetection, etc... The OeNB bears the initialcapital investment requirement and is thereforecompensated through rental payments by theGSA consortium as part of its cost structure.Through its participation, the OeNB ensurethe quality of the banknotes in circulation.

Automatia Pankkiautomaatit Oy (Auto-matia), founded in 1994 operates Finland’snationwide ’Otto’ ATM network and performsall circulation of cash. Automatia is ownedjointly by the 3 largest banks in Finland namely,Nordea, OP-Pohjola Group and Sampo Bank.The high usage through this cooperative (vs.the typical competitive approach) has reducedcosts for all member banks and its services areavailable to all banks operating in Finland.

In Brazil, Banco do Brasil (a public-privatebank) is the official Custodial Bank of thenation contracted by the Banco Central doBrasil to perform cash processing andrecirculation functions as well as managing acustodial inventory program.

In a few countries, the central banks have orare undertaking projects to evaluate andpossibly roll-out new concepts such as theshared infrastructure initiative in Belgium. Thepurpose is to improve the efficiency of thecash cycle by co-hosting the central bank andthe CIT in the same facility. This reduces theoverall number of cash centers, eliminatestransportation between the central bank andthe commercial cash centers and enablesstraight-through processing as the central bankwill continue to perform the fitness sortingwhereas the CIT will carry out the pre- andpost processing. This initiative is well on itsway and should be operational in early-2014so the final impact and whether it’s successfulor not remains to be seen. A similar projectwas undertaken by the Federal Reserve bankand several financial institutions a few yearsago but it never became operational becauseduring the analysis phase it was determinedthat the different security policies of the centralbank would unnecessarily increase the unitcost of the financial institutions. Therefore,the co-location project was abandoned but amore robust custodial inventory program wasimplemented by the Federal Reserve.

However, it should be noted that most ofthese initiatives are taking shape in smaller andtechnologically advanced countries with ahighly concentrated banking sector.

30 THE FUTURE OF CASH 2012

3 While indications are that cash in physicalform will be with us for years to come, somebanks in some markets are attempting toaccelerate cash substitution by restricting theaccess to cash. Regardless of their preference,it is possible that in some countries, such asSweden, Finland and the Netherlands, at somepoint in time, consumers may not have theoption of using cash for transactional purposesin some locations and even be unable to utilizetheir bank for cash-based transactions. Thiscould lead to the disintermediation of banksfrom the cash cycle and the emergence ofspecialized players as has been the case withindependent ATM deployers in the US.

One natural outcome of reduced cash usage isthe increased unit costs of processing banknotesdue to the fixed costs of the cash infrastructure.This will inevitably lead to increased costs toconsumers for any cash transactions in anysegment of the cash cycle. While the consortiumsmentioned above endeavor to reduce the costburden for the entire cash cycle, thesephenomena will force a behavioral change inthe average consumer who will not be willingto bear the increasing costs for transacting incash, which could inevitably lead to theexpanded use of non-cash payment instruments.

The Expanding Role of Retailers As far as availability of cash is concerned, longgone are the days when consumers andmerchants had to make a trip to their localbank branch for cash deposits and orwithdrawals. With the introduction of ATM’sin the late 1970’s and the ubiquity of thesedevices in today’s world, cash is now readilyavailable to consumers. Over the last five years,countries in emerging markets are experiencingsubstantial growth in ATM installations. At theend of 2011 there were a total of 2.3 millionATM devices installed worldwide. This numberis projected to exceed 3.1 million by the year2015, which represents a 37% increase in fouryears time or nearly 10% per annum.

In addition to traditional ATM devices, whichprimarily serve the banked and underbanked,over the last few years, multi-function kiosksare making ATM type transactions available toeven the unbanked. Therefore, the infrastructurenecessary to make cash readily available toaverage banked and unbanked consumerscontinues to grow each year.

Needless to say, technology enablers of anexpanded infrastructure of cash in circulationforce more “retail” recirculation and thusreduction at the “wholesale” level. Over time,this dynamic will undoubtedly lead to furtherreduction and consolidation of physicalprocessing infrastructure in the cash cycle.

While ATMs and bank branches were the onlyplaces to withdraw cash in the past, anincreasing number of alternatives are nowbecoming more established. It is possible,under certain circumstances, to withdraw cashwhen paying for shopping in certain storeswith cashback. Other companies also offer theopportunity to withdraw cash in cooperationwith banks. For example, in Germany, customersof Postbank can withdraw cash free of chargefrom Shell petrol stations. In addition tocreating greater flexibility when it comes towithdrawing cash, such partnerships alsofacilitate the recirculation of sales revenues forthe retail companies involved. Several largeretailers have been piloting combined depositand withdrawal devices in large shoppingcenters. Most shopping centers already haveATMs, which provide a cost-effeicient way forretailers to recirculate their cash

The most recent technology to help with costreduction and cash cycle contraction has beenretail automation, including intelligent safes,recirculation devices, self-service paymentterminals and end-to-end closed loop systems.While smart safes were introduced in the early1990’s as a solution to address security problemsassociated to internal theft and robberies, theyhave evolved into solutions that allow banks tooffer “Remote Cash Capture” (RCC) and“provisional credit” products where merchants

. The Evolution of the Cash Cycle

31

can maintain their cash deposits on premisesfor longer periods of time instead of contractingdaily armored transportation service therebyreducing their operating costs without negativelyimpacting their access to available capital.These services are leading to the electronificationof the cash cycle, whereby physical cash neednot be transported between the variousstakeholders. This is reducing the overall costof cash handling and transportation in particular.In the United States, the installed base ofsmart safes skyrocketed fourfold in six yearsfrom approximately 15,000 units in 2005 toover 60,000 in 2011. It should be noted thathistorically low interest rates are making thistechnology very attractive and it remains to beseen whether commercial banks will continueto offer these products when the cost of cashgoes back to historical levels without imposingnew fees.