The Financing of Illinois K-12 Education 1998-2007 Dr. Michael Jacoby Executive Director, Illinois...

28

The Financing of Illinois K-12 Education 1998-2007 Dr. Michael Jacoby Executive Director, Illinois ASBO Chair, Illinois Education Roundtable

-

Upload

rosalind-hamilton -

Category

Documents

-

view

220 -

download

0

Transcript of The Financing of Illinois K-12 Education 1998-2007 Dr. Michael Jacoby Executive Director, Illinois...

The Financing of Illinois K-12 Education 1998-2007

Dr. Michael JacobyExecutive Director, Illinois ASBOChair, Illinois Education Roundtable

Topics, Documents Revenue/Expenditure Data

2008 AFR Rev and Exp Summary Data 1998-2008 Rev and Exp Graphs 1998-2008

Historical Review of Funding Reform Proposals Legislative Research Unit Report

Annual Financial Report How Data is Collected: (See 2007 AFR)

Illinois Program Accounting Manual (IPAM) Revenue (by Fund [9] and Source):

Local:TaxesCPPRTTuitionFeesInterest EarningsFood ServicePupil ActivitiesOther

State:GSASpecial EdVocationalBilingualTransportationOther

Federal:UnrestrictedRestrictedTitle VFood ServiceTitle ITitle IVSpecial EdVocational

Annual Financial Report Expense (by Fund [9], Function & Object):

Fund:Operating Funds: - Education - Operation & Maintenance - Transportation - IMRFBond & InterestSite & ConstructionWorking CashRent (Tort in 2009)Life Safety

Function:InstructionSupport ServicesCommunity ServicesNon-Programmed ChargesDebt Service

Object:SalaryBenefitsPurchased ServicesCapital OutlayOther ObjectsTransfersTuition

ADA = Average Daily AttendanceIllinois School District ADA Growth 1998-2007

0.0%

0.4%

2.0%

2.9%

4.8%

6.7%

5.8%

6.2%6.2%

7.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

% G

row

th

Operating Fund Data – 10 Year Summary

Source = ISBE Analysis of AFR Data 1998 - 2007

Revenue and Expense Growth 1998-2007

49.4%

45.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

% G

row

th

Revenue

Expense

Inflation Adjusted

Inflation measured by the Consumer Price Index indicates that $1.00 in 1998 is equivalent in purchasing power to $1.27 in 2007.

Inflation Adjusted Revenue Increase 1998 to 2007 = 22.4% Expense Increase 1998 to 2007 = 18.5%

Policy Implication CPI is not a reliable inflation index for education. “ECI is a more accurate measurement of the

inflationary spending pressures that school districts face” (EFAB 2005)

Operating Fund Revenue Per ADA

4,58

02,

240

501

4,75

72,

497

553

4,93

92,

578

609

5,11

32,

654

650

5,15

12,

637

676

5,27

82,

595

761

5,67

22,

843

819

6,00

92,

880

857

6,49

92,

952

866

6,85

03,

232

863

0

2,000

4,000

6,000

8,000

10,000

12,000

Per ADA

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

Illinois School Revenues per ADA (by Source)

Federal Sources

State Sources

Local Sources

Operating Fund Revenue Per ADA Illinois School District Revenue (by Source)

62.5% 62.5%

30.6% 29.5%

6.8% 7.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

% o

f R

ev Local Sources

State Sources

Federal Sources

Local vs State Revenue – Operating Funds

(2 Axis)

62.5%

60.8%60.7% 60.6%

60.8%

61.0%

60.7%

61.6%

62.9%

62.5%

30.6%

31.9%

31.7%

31.5%

31.1%

30.0%

30.4%

29.5%

28.6%

29.5%

60.0%

61.0%

62.0%

63.0%

64.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 200728.5%

29.5%

30.5%

31.5%

32.5%

Lo

cal R

even

ue

Sta

te R

even

ue

Operating Fund Expenditures Per ADA by Function

4,07

22,

916

4,38

53,

078

4,51

03,

257

4,75

13,

478

4,92

03,

603

5,08

93,

696

5,27

83,

748

5,42

33,

903

5,62

54,

129

5,86

84,

305

0

2,000

4,000

6,000

8,000

10,000

12,000

Per ADA

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

Illinois School Expenditures per ADA (by Function)

Debt Services

Nonprogrammed Charges

Community Services

Support Services

Instruction

Operating Fund Expenditure Per ADA Illinois School District Expense (by Function)

Instruction and Support Service Only = 95.9% of Expenses

55.3%55.9%

40.6%40.0%

35.0%

45.0%

55.0%

65.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

% o

f E

xp Instruction

Support Services

Operating Fund Expenditures Per ADA by Object

4,50

9

628

794

532363235

4,76

9

724

894

537369249

5,01

7

706

910

579385260

5,25

5

783

953

648

399273

5,45

6863

978

612407319

5,63

0

923

1,018

631364331

5,77

4

1,061

1,057

632300321

5,93

9

1,076

1,158

650281333

6,11

6

1,144

1,237

701310352

6,36

7

1,187

1,315

722315376

0

2,000

4,000

6,000

8,000

10,000

12,000

Per ADA

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

Illinois School Expenditures per ADA (by Object)

Tuition

Transfers

Other Objects

Capital Outlay

Supplies

Purchased Services

Benefits

Salary

Operating Fund Expenditure Per ADA Illinois School District Expense (by Object)

Major Objects Only = 99% of Expenses

63.09% 61.35%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

% o

f E

xp

Salary

Benefits

Purchased Services

Supplies

Capital Outlay

Tuition

See Next Chart for

Detail

Operating Fund Expenditure Per ADA Illinois School District Expense (by Object)

Not Including Salary = ~38% of Expenses

11.43%

8.78%

12.67%

11.12%

6.96%7.45%

3.04%

5.08%

3.62%3.29%

0.72% 0.83%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fiscal Year

% o

f E

xp

Benefits

Purchased Services

Supplies

Capital Outlay

Tuition

Capital Outlay

Transfers

Expense Per ADA – Change from 1998 by Function

Function $ Inc from 1998

% Inc from 1998

Instruction 1,796 44%

Support Services 1,387 48%

Community Services

11 20%

Non Programmed Charges

85 37%

Debt Services 34 240%

Denotes potential policy implication or budget trend

Local Budget Trends

An increase in Debt Services within the Operating Funds suggests an increased reliance upon Tax or GSA Anticipation Warrants, or non-referendum debt (i.e. performance contracts).

Both principal and interest for these types of borrowing must be paid directly from the fund that receives the revenue.

Total Warrants/Notes issued or outstanding FY 2007 = $268M

Total principal/interest paid from Operating Funds in FY 2007 = $90.2M

An increase from 1998 of $63.6M

Expense Per ADA – Change from 1998 by Function

Object $ Inc from 1998

% Inc from 1998

Salary 1,858 41%

Benefits 559 89%

Purchase Services

520 65%

Supplies 190 36%

Capital Outlay -48 -13%

Other Objects 34 67%

Transfers -23 -69%

Tuition 140 60%Denotes potential policy implication or budget trend

Local Budget Trends

Employee benefit increases over 10 years have had a significant impact on school budgets.

This is primarily associated with health insurance premiums.

Total expense from Operating Funds in FY 2007 = $2.2B

An increase from 1998 of $1.05B

Benefit Cost Per ADA % Change from 1998

Fiscal Yr $ Inc from 1998

% Inc from 1998

1999 96 15.3%

2000 78 12.4%

2001 155 24.8%

2002 236 37.6%

2003 295 47.0%

2004 434 69.1%

2005 449 71.5%

2006 517 82.4%

2007 559 89.1%

Total Cost Inc = $1.052 Billion

Local Budget Trends

Purchased Service increase suggests more external contracting by schools for various functions Custodial Services + $211M or 76% over 1998 Transportation Services + $224M or 82% over 1998

Capital Outlay decrease suggests schools purchased less equipment or equipment at lower costs. Education Fund down $74M or 25% decline over

1998 Instruction down $30M or 21% decline over 1998

Local Budget Trends

Transfers decrease is difficult to discern and AFR data is not sufficient to make an evaluation.

IPAM Definition: “This object category does not represent a purchase; rather, it shows that funds have been transferred in some manner. Included here are transactions for moving money from one fund to another and for transmitting flow-through funds to another LEA.”

Local Budget Trends Tuition increase is summarized below:

Regular program increase suggests more districts paying tuition to other districts for programming.

Sp Ed increase is within expectations when compared with total expense increase 1998 to 2007

Increase in CC tuition suggests more dual credit programs.

Function Per ADA $ Inc from

1998

Per ADA % Inc from

1998

Regular 13 150%

Special Ed 70 49%

Vocational 2 15%

Community College .05 108%

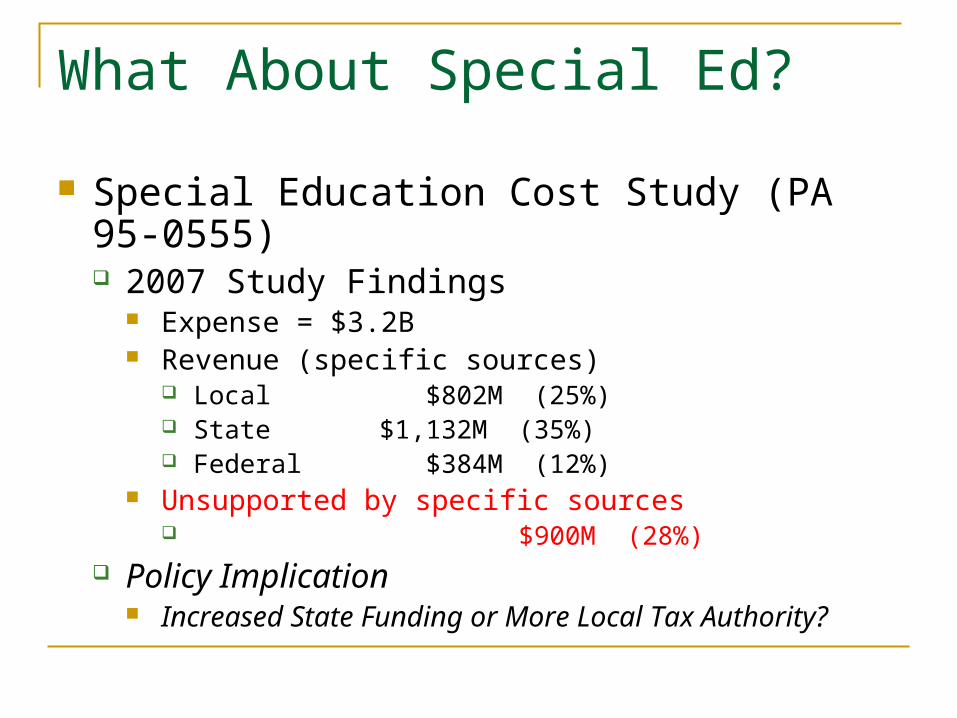

What About Special Ed?

Special Education Cost Study (PA 95-0555) 2007 Study Findings

Expense = $3.2B Revenue (specific sources)

Local $802M (25%) State $1,132M (35%) Federal $384M (12%)

Unsupported by specific sources $900M (28%)

Policy Implication Increased State Funding or More Local Tax

Authority?

What About Special Ed?

1998 to 2007 per ADA (select *Function #s)

Function1998 per

ADA2007 per

ADA $ Inc % Inc1200 Sp Ed 647.32 1,051.55 404 62%2110 Social Work 70.40 113.76 43 62%2140 Psych 34.27 57.40 23 67%2150 Speech 36.50 85.48 49 134%4120 Tuition 165.45 253.91 88 53%

953.94 1,562.10 608 64%

The PA 95-0555 Expense methodology is preferred, however comparable 1998 data is not currently available.

Local Budget Trend

Special Education expenses per ADA from 1998 to 2007 increased 64% compared to the total Education Fund increase of 45%.

Speech and Hearing expenses represented the largest increase at 134%.

As a % of the total Education Fund Budget, Special Ed increased from 16% in 1998 to 18% in 2007. This 2% proportional increase = $334M

Illinois Funding Proposals

Handout Historical Review of Selected Education

Funding and Reform Proposals-Illinois Legislative

Research Unit December 20, 2006