The feedback loop: Ireland’s retail banks, regulation & real economy supply and demand Fiona...

16

The feedback loop: Ireland’s retail banks, regulation & real economy supply and demand Fiona Muldoon Director, Credit Institutions & Insurance Supervision 11 April 2013

-

Upload

liliana-cannon -

Category

Documents

-

view

221 -

download

2

Transcript of The feedback loop: Ireland’s retail banks, regulation & real economy supply and demand Fiona...

The feedback loop: Ireland’s retail banks, regulation & real economy supply and demand

Fiona MuldoonDirector, Credit Institutions & Insurance Supervision 11 April 2013

2

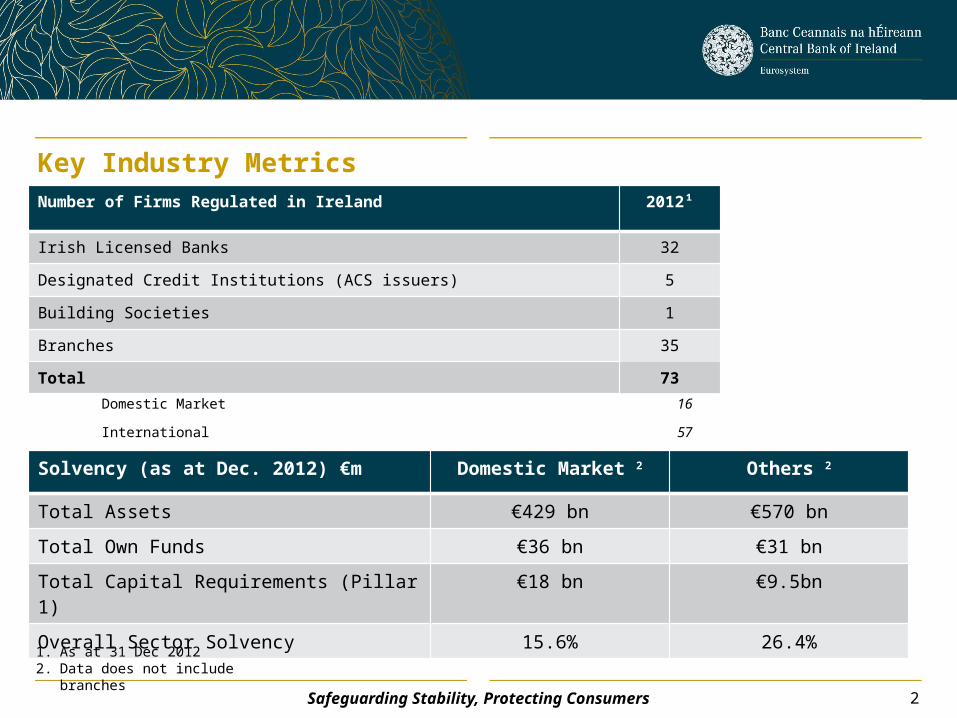

Key Industry MetricsNumber of Firms Regulated in Ireland 2012¹

Irish Licensed Banks 32

Designated Credit Institutions (ACS issuers) 5

Building Societies 1

Branches 35

Total 73

Solvency (as at Dec. 2012) €m Domestic Market 2 Others 2

Total Assets €429 bn €570 bn

Total Own Funds €36 bn €31 bn

Total Capital Requirements (Pillar 1) €18 bn €9.5bn

Overall Sector Solvency 15.6% 26.4%

1. As at 31 Dec 20122. Data does not include branches

Safeguarding Stability, Protecting Consumers

Domestic Market 16

International 57

3Safeguarding Stability, Protecting Consumers

TO BE UPDATED FOR 31 DECMBER DATA in EARLY APRIL

Snapshot of Irish Banking as of 31 December 2012

Domestic Market Credit Retail InstitutionsTotal Assets: €429b

Business Lines1. Retail Deposits and Loans2. Corporate Deposits and Loans3. Commercial Lending4. Mortgage Lending5. SME Lending6. Credit Cards

Other Credit InstitutionsTotal Assets: €570b

Business Lines1. Corporate Loans2. Structured Products/Lending3. Corporate Trust Services4. Custody Services5. Wealth Management6. Debt Securities

4

Key Industry Metrics: Balance SheetKey Balance Sheet Statistics as at 31 December 2012

Retail Institutions

Others

Total Assets €429b €570b

Of which

Loans and Advances €299b €122b

Debt Securities €93b €84b

Derivatives €11b €353b

Asset Quality

Non-performing Assets €98b €0.8b

Impairment Provisions €52b €0.9b

Coverage (Provs/Non-Perf) 52% 108%

Safeguarding Stability, Protecting Consumers

5

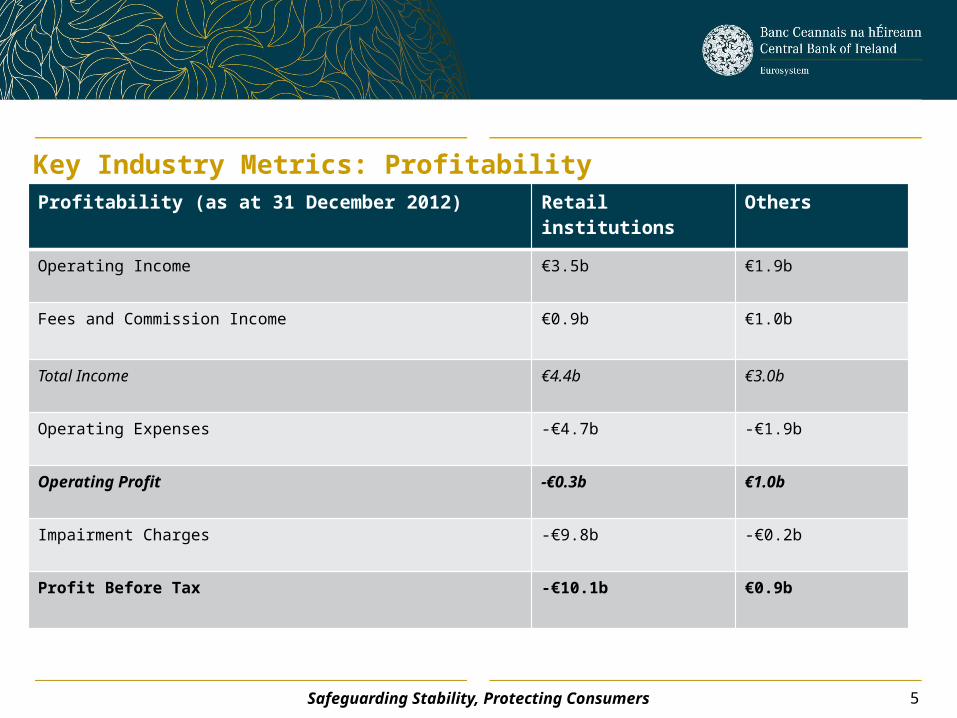

Key Industry Metrics: ProfitabilityProfitability (as at 31 December 2012) Retail

institutionsOthers

Operating Income €3.5b €1.9b

Fees and Commission Income €0.9b €1.0b

Total Income €4.4b €3.0b

Operating Expenses -€4.7b -€1.9b

Operating Profit -€0.3b €1.0b

Impairment Charges -€9.8b -€0.2b

Profit Before Tax -€10.1b €0.9b

Safeguarding Stability, Protecting Consumers

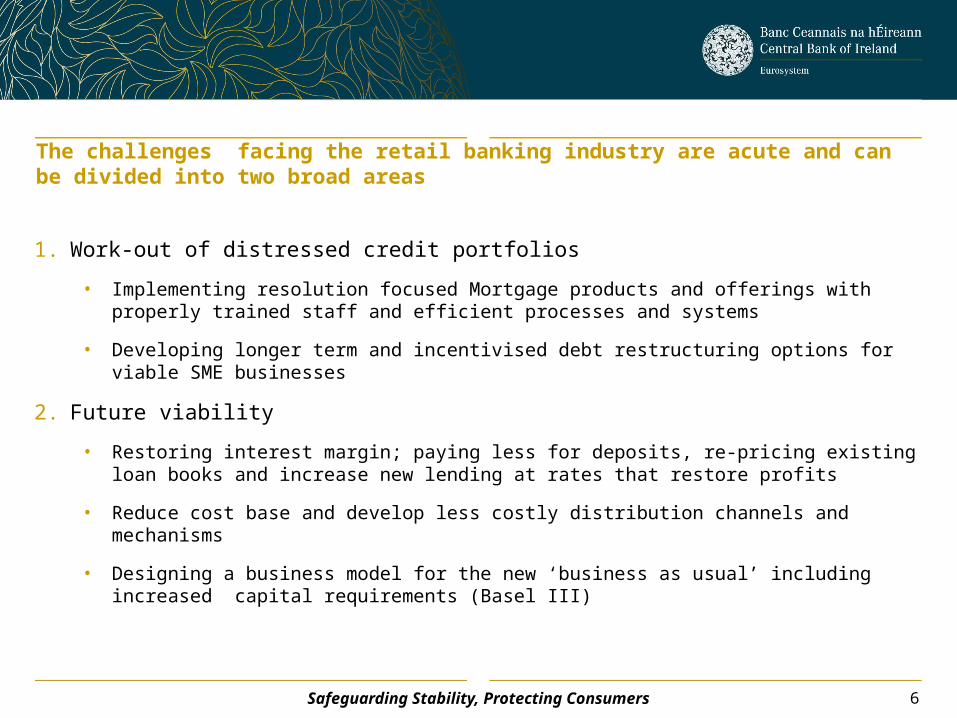

The challenges facing the retail banking industry are acute and can be divided into two broad areas

1. Work-out of distressed credit portfolios

• Implementing resolution focused Mortgage products and offerings with properly trained staff and efficient processes and systems

• Developing longer term and incentivised debt restructuring options for viable SME businesses

2. Future viability

• Restoring interest margin; paying less for deposits, re-pricing existing loan books and increase new lending at rates that restore profits

• Reduce cost base and develop less costly distribution channels and mechanisms

• Designing a business model for the new ‘business as usual’ including increased capital requirements (Basel III)

6Safeguarding Stability, Protecting Consumers

7

Economic contraction

Domestic demand

SME capacity to pay

Distressed Loans

Bank profitability

Bank capacity to lend

Consumer & SME

confidence

The challenges faced by the domestic banks matter in a real way to ‘ordinary’ SME borrowers and to consumers

Safeguarding Stability, Protecting Consumers

8

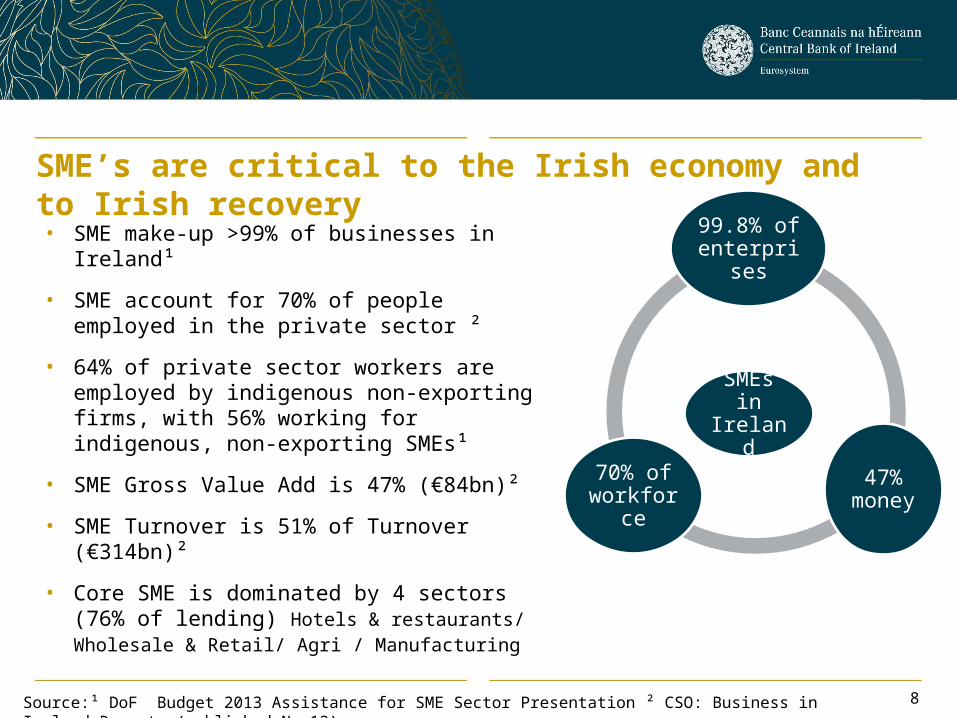

SME’s are critical to the Irish economy and to Irish recovery

SMEs in Ireland

99.8% of enterprises

47% money

70% of workforce

• SME make-up >99% of businesses in Ireland¹

• SME account for 70% of people employed in the private sector ²

• 64% of private sector workers are employed by indigenous non-exporting firms, with 56% working for indigenous, non-exporting SMEs¹

• SME Gross Value Add is 47% (€84bn)²

• SME Turnover is 51% of Turnover (€314bn)²

• Core SME is dominated by 4 sectors (76% of lending) Hotels & restaurants/ Wholesale & Retail/ Agri / Manufacturing

Source:¹ DoF Budget 2013 Assistance for SME Sector Presentation ² CSO: Business in Ireland Report (published Nov12)

9

SME

Personal guarantees 70% employer : repayment capacity for mortgages

Cross guarantees on collateral

No single definition of SME

Cashflow supports direct trading & “indirect” debt

Business property is part of a larger

premises

PDH debt serviced through drawings

Multi-banking

SME Arrears: Complex issues and a high level of inter-connectedness

Safeguarding Stability, Protecting Consumers

1. Governance & Execution framework of SME Support Unit organisation

2. Quality of Implementation plan and progress made

3. Restructuring – assessing and distinguishing viable and non-viable borrowers

4. Re-underwriting – disentangling viable debt from unsustainable property-

related debt

5. Credit Assessment Tools & Policies (Debt/ Financial/ Collateral)

6. MI/ KPIs/ key milestones and timelines

7. Operational plans/Skills/ Resources and Training/Execution ability

8. Level of external assistance / sectoral/ restructuring expertise

10

SME Arrears: Central bank areas of regulatory focus for 2013

Safeguarding Stability, Protecting Consumers

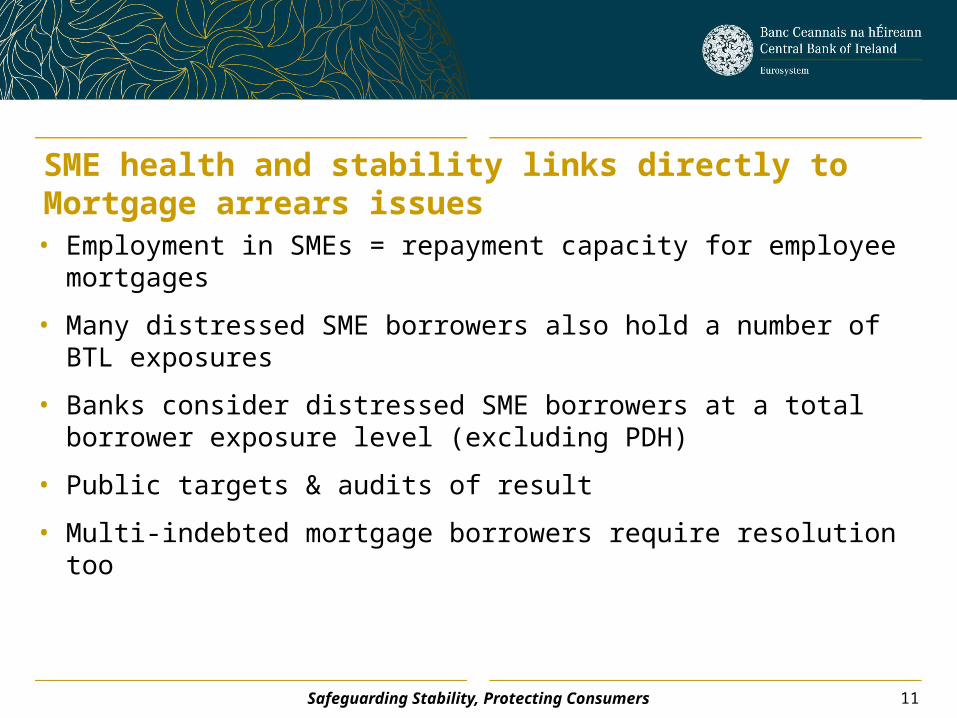

SME health and stability links directly to Mortgage arrears issues

• Employment in SMEs = repayment capacity for employee mortgages

• Many distressed SME borrowers also hold a number of BTL exposures

• Banks consider distressed SME borrowers at a total borrower exposure level (excluding PDH)

• Public targets & audits of result

• Multi-indebted mortgage borrowers require resolution too

11Safeguarding Stability, Protecting Consumers

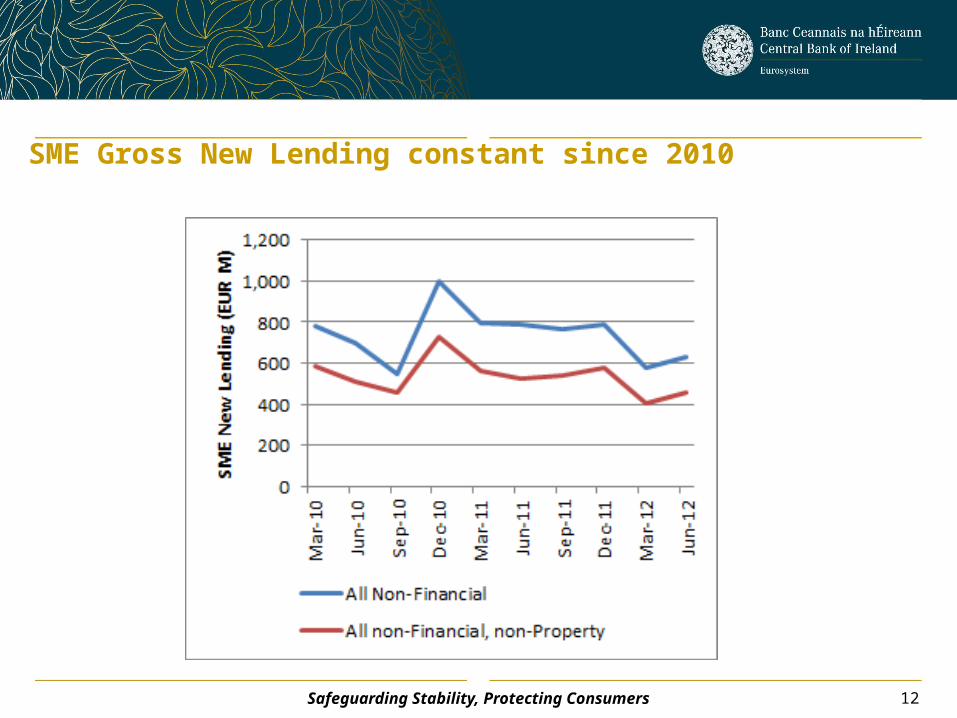

SME Gross New Lending constant since 2010

12Safeguarding Stability, Protecting Consumers

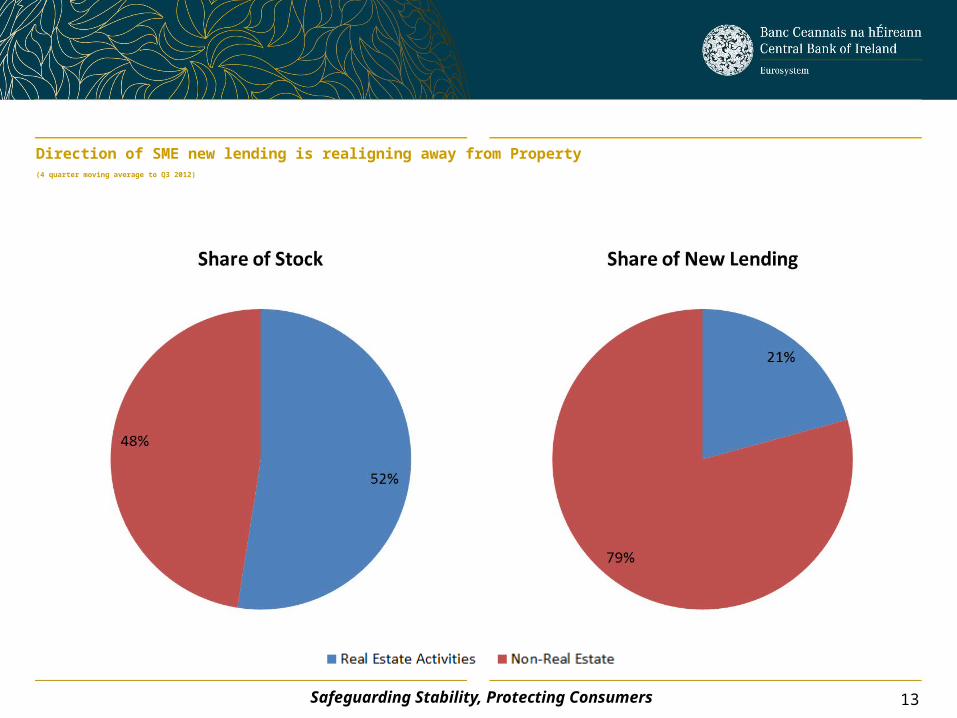

Direction of SME new lending is realigning away from Property(4 quarter moving average to Q3 2012)

13Safeguarding Stability, Protecting Consumers

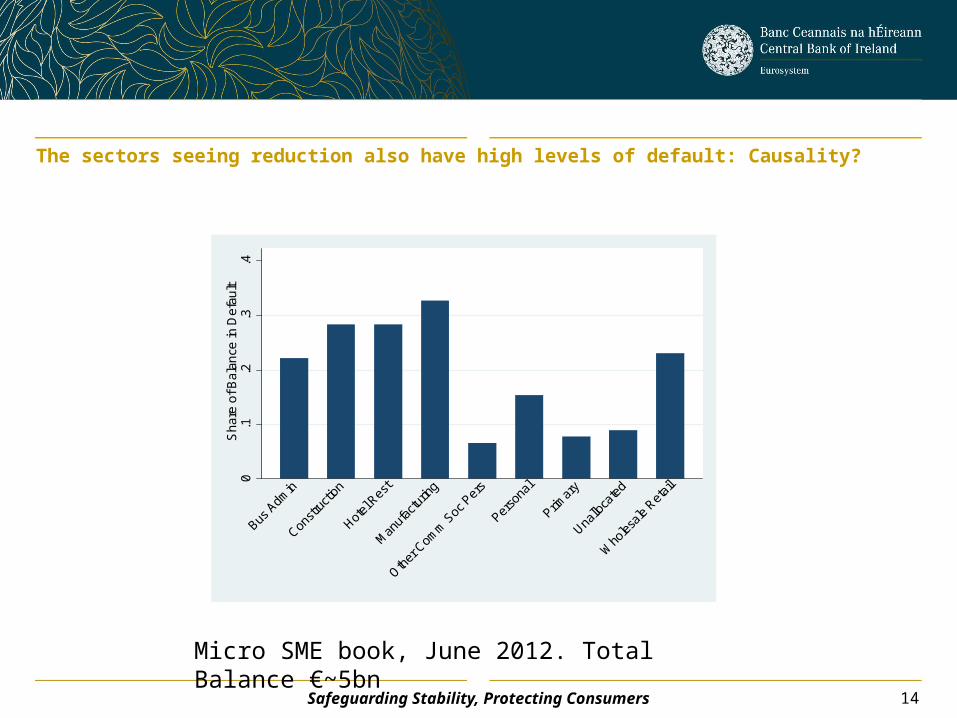

The sectors seeing reduction also have high levels of default: Causality?

0.1

.2.3

.4S

har

e o

f Bal

ance

in D

efau

lt

Bus A

dmin

Constr

uctio

n

Hotel

Rest

Man

ufac

turin

g

Other

Com

m S

oc P

ers

Perso

nal

Primar

y

Unallo

cate

d

Who

lesale

Ret

ail

Micro SME book, June 2012. Total Balance €~5bn

14Safeguarding Stability, Protecting Consumers

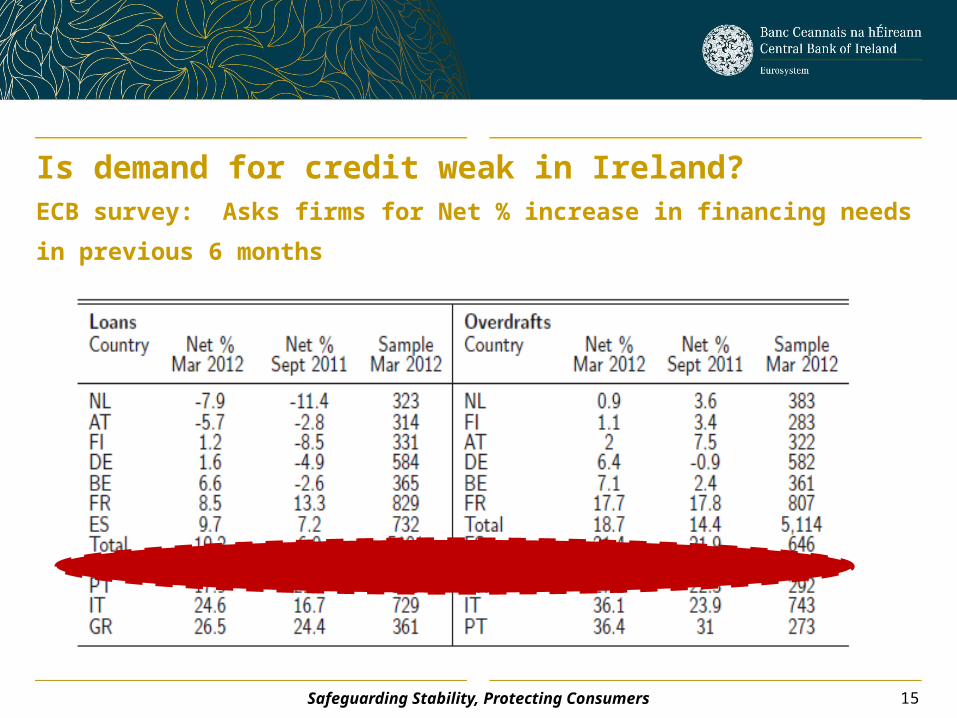

Is demand for credit weak in Ireland? ECB survey: Asks firms for Net % increase in financing needs in previous 6 months

15Safeguarding Stability, Protecting Consumers

16

Economic growth

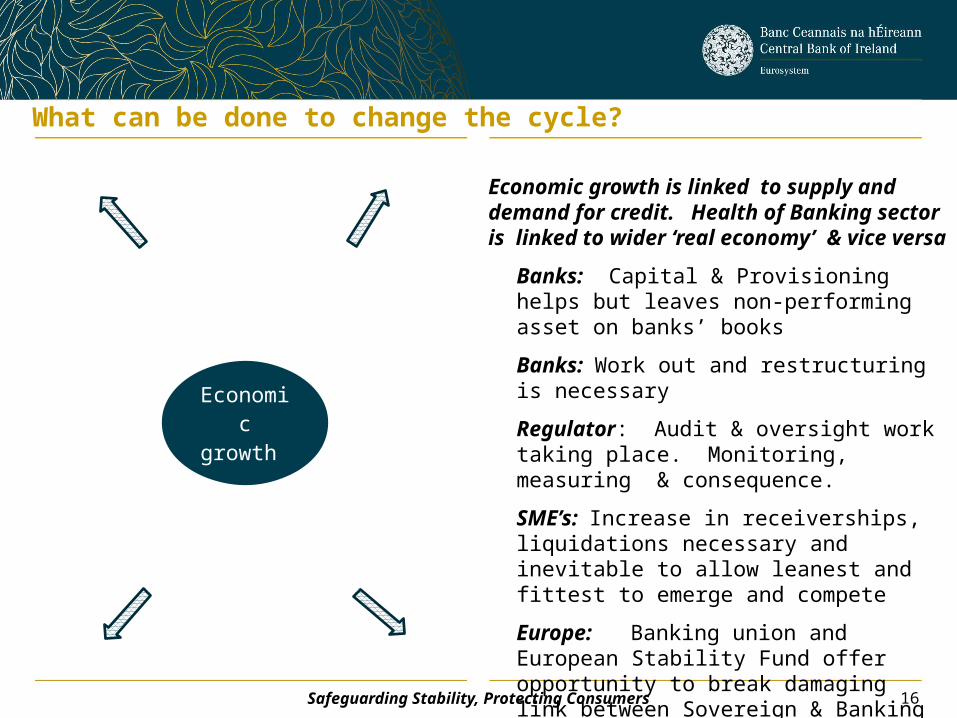

Economic growth is linked to supply and demand for credit. Health of Banking sector is linked to wider ‘real economy’ & vice versa

Banks: Capital & Provisioning helps but leaves non-performing asset on banks’ books

Banks: Work out and restructuring is necessary

Regulator: Audit & oversight work taking place. Monitoring, measuring & consequence.

SME’s: Increase in receiverships, liquidations necessary and inevitable to allow leanest and fittest to emerge and compete

Europe: Banking union and European Stability Fund offer opportunity to break damaging link between Sovereign & Banking Sector

Ireland: Better oversight, better regulation, safer banks prevent recurrence of past mistakes

What can be done to change the cycle?

Safeguarding Stability, Protecting Consumers