The European livestock market, with emphasis on pig ...€¦ · The European livestock market, with...

32

The European livestock market, with emphasis on pig production, and also a success story of Norwegian exports

Transcript of The European livestock market, with emphasis on pig ...€¦ · The European livestock market, with...

The European livestock market, with emphasis on pig

production, and also a success story of Norwegian exports

Outline

• Introduction – Myself and the Topigs – Norsvin merger

• Global macro trends & European trends • European market • My European view of Norway and Norsvin

Norwegian

Profession

• Farmer– Netherlands and Germany

• Food Producer– Frievar. www.frievar.com– Friberne. www.friberne.nl

• TOPIGS NORSVIN– Chairman at Dutch Cooperative Topigs– Chairman at Supervisory Board of Topigs Norsvin

TOPIGS (Netherlands) and Norsvin (Norway) launched a joint company on 4th of June 2014.

A farmers deal

TOPIGS

Norsvin

Ownership: Farmer owned companies

1

Strong R&D focus

2

High‐end combinedproduct portfolio

3Complementary geographical presence

4

Topigs Group BV

Top Pi N‐Line

Tempo Z‐line

Talent A & B‐line

Terminal Maternal

Norsvin Duroc

Norsvin Landrace

NorsvinYorkshire

Norsvin SA

Terminal Maternal

TOPIGS and Norsvin is a strategic fit

Simple overview of the Topigs Norsvin corporate structure

Topigs Norsvin Holding BV

Norsvin International Holding AS

Germany Russia

…all other original TOPIGS

international subsidiaries

Brazil Canada USA

Topigs Group BV

• Ownership • Dutch: 66,5%• Norwegian: 33,5%

• Supervisory Board • Dutch: 4 seats • Norwegian: 4 seats

• Board of Directors:• Martin Bijl (CEO)• Cor van Hertrooij

(CFO)• Bjarne Holm (CDO)• Hans Olijslagers

(CTO)

Vion Food Group

CoöperatieTopigs Group

UANortura SA Felleskjøpet

Agri SANorsvin SA

(cooperative)

33,5% 66,5%

Topigs Norsvin with strong global presence in all key markets.

R&D budget

1,6 million crossbred gilts/year

100 million slaughter pigs

9 million doses of semen

million

545454

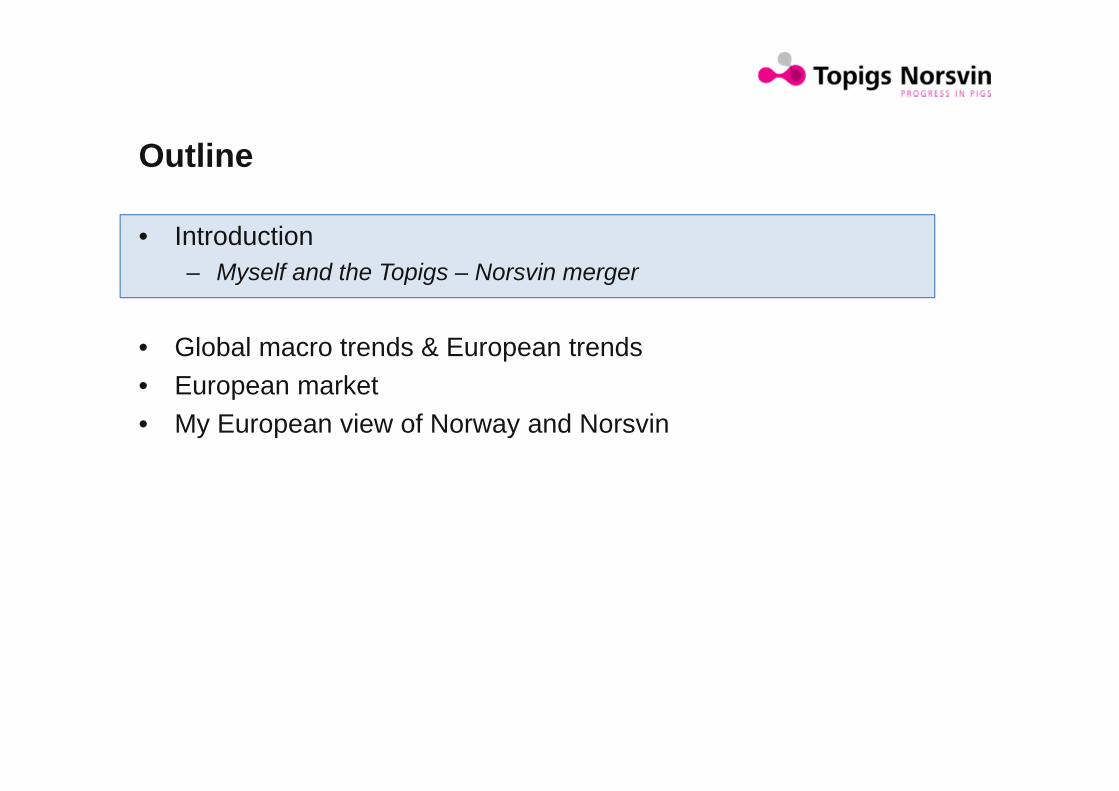

All over the world

We serve the Professional Pig Producers around the world

We know the local needsand circumstances

Present in 54countries

Progress in pigs. Everyday

Tailored offerings

based on a complete product portfolio

Stringent bio-security

focus

Partnership AmbitionInnovationSustainability

Excellent support

through local presence

World class applied R&D

Integrated solutions

focusing on the entire

value chain

Topigs Norsvin – Value Proposition

Outline

• Introduction • Global macro trends & European trends • European market • My European view of Norway and Norsvin

• World population is growingvery fast

• Agriculture production is alsogrowing very fast

• Surplus– Milk– Sugar– Pigmeat– ….

• Speculation agriculturecommodeties

• Commodety?– Quality– Food safty– Health

• Free market?– GMO– Antibiotics– MRSA– Manipulation of DNA

• Cloning– Tax – Subsidies

Trends

Market environment and trends

Global strategic environment and key trends

Consolidation and professionalization among customers. More integrated

Lean meat yield more important, to yet higher weights. Technifiedfarming precision farming

Animal and consumer health, animal welfare and environmental impact

increasingly important

Growing global pork meat demand:2010 – 2030 growth of ~45 %

Total feed cost is the major economic concern of professional pork

producers

Qualified labor is limited costs & quality

Consolidation among swine genetics players: 3‐4 global players in ~7

years time

95 % of pork meat is consumed where it is produced

The global swineindustry & swine genetics industry

• 5 markets - 95% of the market within the continent

• Asia– FC/ efficiency– China Decrease with 10 Mln Sows

• South America- FC/efficiency/sustainability- Stable number of sows

• North America– FC/Efficiency/ sustainability/welfare– 6 % more production

World Market

• Western Europe– FC/efficiency, but more

consumer demands like quality/taste/welfare

– Self sufficiency 115 %– Price below cost price– European pig farmers

suffering– Does the classical pig cycle

still work?– Spain is the only country with

growth– Netherlands/France/Germany

/Italy -5 to -10 %– Denmark?– A lot of bankruptcy

• Eastern Europe– FC/efficiency– Lots of politics– Good opportunities– Growing markets– Political situation stays

uncertain

European market

EU –Purketetthet i 2013

Development pig farms in The Netherlands(Source: Centraal bureau voor de Statistiek (CBS))

0

500

1000

1500

2000

2500

0

50

100

150

200

250

30019

50

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

*

Num

bero

f pigs(x 10.000)

Num

bero

f pigsp

er farm

(x1.00

0)

Num

ber o

f farms (x1.00

0)

Year (inventory date: April

Number of farms (x 1.000) Number of pigs (x 10.000) Pigs per farm (x 1.000)

Prices the NetherlandsAll prices are excl. VAT. Used sources: - * Agrimatie.nl – Wageningen UR - ** Landelijk biggenprijzenschema – Wageningen UR (new release every year in July)

1,00

1,10

1,20

1,30

1,40

1,50

1,60

1,70

1,80

1,90

25,00

30,00

35,00

40,00

45,00

50,00

55,00

60,00Jan‐2014

Feb‐2014

Mrt‐2014

Apr‐2014

Mei‐2014

Jun‐2014

Jul‐2

014

Aug‐2014

Sep‐2014

Okt‐2014

Nov

‐2014

Dec‐2014

Jan‐2015

Feb‐2015

Mrt‐2015

Apr‐2015

Mei‐2015

Jun‐2015

Jul‐2

015

Aug‐2015

Sep‐2015

Okt‐2015

Prices pig m

eat (€/kg)

Prices piglets (€

/piglet)

Aksetittel

Cost price piglets** ‐ NL Piglet price* ‐ NL Cost price meat** ‐ NL Meat price* ‐ NL

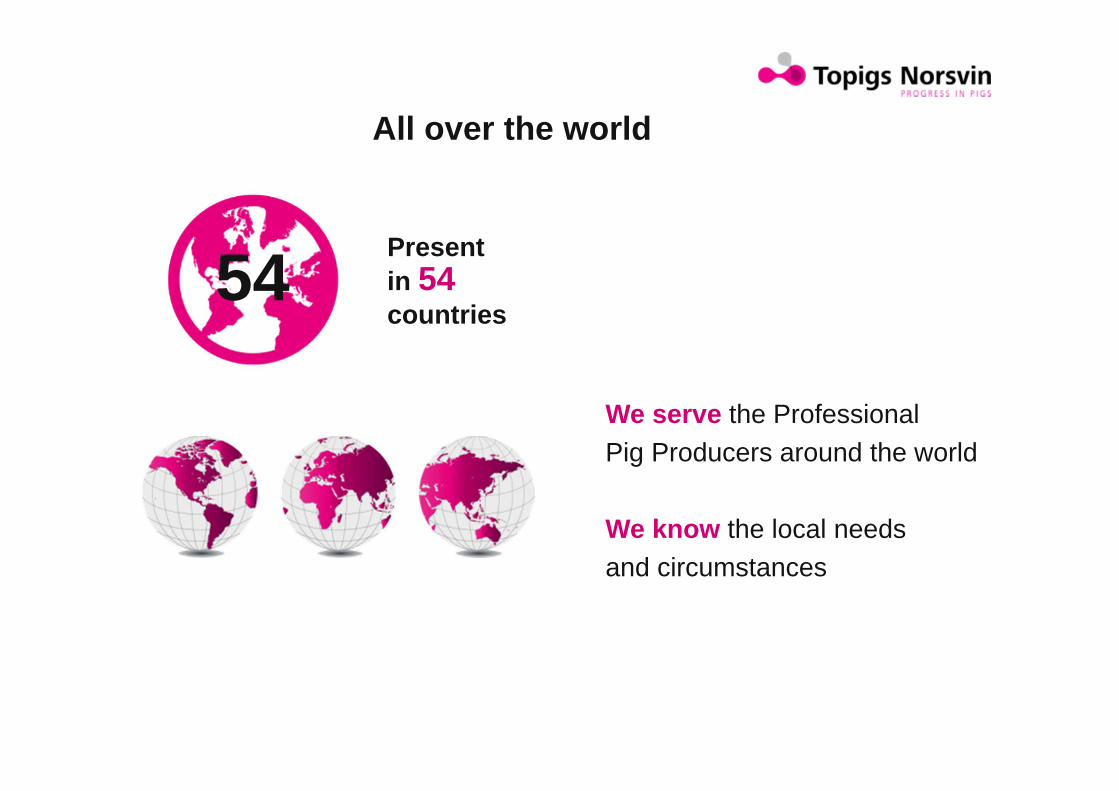

Market history slaughter swine

Outline

• Introduction • Global macro trends & European trends • European market • My European view of Norway and Norsvin

My view on Norway

– Beautiful country– Farmers important in the society– Working very well together in the whole value chain– System seems to be in balance– Good quality products

• Good taste• Healty• Fair price

– Something the rest of the world is looking for?

BONDENS SJØLBESTEMMELSESRETTThe farmers right to make decisions

VITENSKAPENS LANDEVINNINGERProgress through Science

FRAMGANG FOR DE MANGEProgress for all

Norsvin: CT scanning of pigs since 2008

• Leading in innovations within pig breading globally

• 3,000 purebred boars on-test annually

• 1200 pictures/animal

• In-house Matlab script (Dr. Kongsro)

• Fully automatic calculation of in vivo carcass quality

• High value for the breeding program:• High heritabilities• Data on the selection candidate• Large # animals tested

Computed tomography (CT)

Norsvin Delta Station

1958Start of selection as Norsvin. AI introduced as tool

1960Ultrasonic back fat evaluation implemented

1970Start of central testing stations

1992BLUP, FIRE stations, # live born piglets etc.

1997Carcass dissection and Meat Quality protocol

2001Piglet weighing and mortality protocol implemented

2008Computer Tomography implemented as off-test tool

2014Genomic selection incorporated in breeding program

Norsvin Landrace

Since the beginning:Bred for terminal efficiency and productivity

A UNIQUE PRODUCT GLOBALLY

Background

Do it on their own …

The first joint product Innovation - Progress - Balance

TN70

Sustainable genetic progressto an integrated industry usingstate of the art technology in a vast global population structure securing high health supply

We shall double annual genetic progress

Breeding Program

PROGRESS IN PIGS. EVERY DAY.