Convert your car to electric, homemade electric car conversion, converting to electric car

Upload

nguyenthienCategory

view

213download

0

NOVEMBER 2, 2017

The Electric Car Tipping Point

Research highlights

2 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

This research underlies our fourth report on automotive propulsion and electric car adoption (out soon)

Focus

areas

• Potential of ICE

technologies

• Consumer perspective

• Updated volume forecasts

• Go-to-market challenges

• Carbon-cost tradeoffs

• Total costs of ownership

(TCO)

• Volume forecasts

• Battery technology and

industry overview

• Battery cost analysis

• Total costs of ownership

(TCO) revisited

• Evolution of battery costs

• Total costs of ownership by

powertrain

• Impact of shared mobility

• 2030 volume forecast

2009 2010 2011 2017

The Electric Car Tipping Point

Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

3

Battery costs have been declining at a rapid pace since 2009, at ~20% annually

We should reach an inflection point for a viable economic proposition for consumers

between 2025 and 2030 without incentives

Until that time, regulation, rather than consumer demand, will still drive the

electrification of cars

Until 2020, advanced internal combustion engines (ICEs) will be sufficient to meet

regulations. After that, electrification will be required

In 2025, most cars will still have an ICE. The average cost per car sold to meet

regulatory requirements will be ~$500 per unit above ICE costs

Electrification will manifest in different ways around the world. In the US, it will be

driven by mild hybrids or 48-volt hybrids (MHEVs) and battery-operated electric

vehicles (BEVs); in the EU and China, by BEVs; and in Japan and the rest of the world,

by mainly full hybrids (HEVs) and MHEVs

The shared economy (taxis and car sharing) will spur HEV and BEV adoption before

individual customers, given higher mileage. Autonomous vehicles will boost shared

mobility and therefore demand for HEVs and BEVs

Globally, we expect the share of electrified vehicles (xEVs) to be ~30% by 2025 and

~50% by 2030. The share of BEVs is projected to be 6% in 2025 and 14% in 2030

Executive summary

Source: BCG analysis

4

Our approach

Energy price

(oil, electricity)

Government

incentives

Battery & ICE tech.

cost/benefit

Regulatory

standards

Regulation-driven

output

Consumer-driven

output

Total miles driven

(mobility, consumer)

OEM economics

(lowest-cost solution)

TCO for consumer

(breakeven expectations)

Battery & ICE tech.

cost/benefit

No

Does consumer output meet

regulation standards?

Yes

Fa

cto

rs a

ffe

cti

ng

co

ns

um

ers

Fa

cto

rs a

ffe

cti

ng

OE

Ms

OutputAnalysisDriver

BCG view of

powertrain

evolution and

xEV market

forecast to 2030

OEM vehicle options

Key

5 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

• Starting in 2021, emission of

passenger car fleets in Europe

limited to max. 95g CO2/km

• Starting in 2025, max. 78g CO2/km

• Optimization of combustion engines

reaches economical limits

• CO2 targets in EU and US can be

achieved only with xEV

technologies

200

150

100

0

2120

115

117

95

191817151413

172

127

165

121110

139

Proposed 78

CO2 (g/km)

97

242322 2516

Governments have set aggressive CO2 targets

Today

ChinaEU JapanUSA

Ambitious CO2 targets... ...with strong implications

Note: China limits only include combustion engines (limits lower if alternative drive technologies included); US limits show NHTSA's efficiency standards and do not include credits for low-GWPcooling according to the EPA's GHG standards; regulations apply for passenger carsSources: BCG analysis; ICCT December 2014; AMS – Spagat zwischen Effizienz und Emission, 21.09.2015; EU-Study "CO2-Emissionsreduktion bei Pkw und leichten Nutzfahrzeugen nach 2020"

Alternative drive technologies

6 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

ICEs will be sufficient to meet regulations until 2020, not beyond

-1,000

0

-500

500

2025

CAFE credits

-398

2024

-543

Industry CAFE credits (M)

2023

-262

2022

-135

2021

-23

2020

43

2019

46

2018

40

2017

41

2016

123

108 106 104 102 100 98 96 93 91 87

95100106112119125

7881858895

0

50

100

150

Industry CO2 emissions EU (g/CO2)

20252020 2021 20242022 20232016 2017 2018 2019

Proposed

Regulatory requirements

CO2 projected

emissions

US and EU regulation not met after 2020

US

pro

jecti

ons

EU

pro

jecti

ons

7 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Countries have set various ways to incentivize xEV sales

• $7.5K per purchase

of full BEV, credits

are less for PHEV

(~5K), federal tax

credit

• ~$2.5K additional

vary by state

• Up to €4K rebate

for BEV and €3K for

PHEV

• €1B fund for

rebates/chargers

• Up to €6.3K for CO2

20g emissions or

less

• Up to €10K for BEV

when scrapping old

diesel

• BEVs exempt from

purchase tax (up

to 100%) and VAT

• Pay far lower

circulation tax,

pay 50% company

car tax

• Exempt from

parking, ferry,

bridge, toll fees

• ~$17K (RMB ~55K)

national rebate,

RMB 30K for a

PHEV

• Municipal

government

offering

additional RMB

~55K

• License plate

exempt from

charge and xEVs

avoid 6-to 12-

month wait

• Up to $8.5K

subsidy based on

purchase price

and benefit from

ICE alternative

• Exemption from

tonnage,

ownership and

acquisition tax

• Formerly had

subsidy of $700-

$1K on HEVs

USA Germany France Norway China Japan

8 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Global penetration of electrified vehicles has been limited to datexEVs are expected to account for 5% of total production this year

0

85

80

75

60

70

65

90

95

90.4

77.4%

18.8%

2015

71.3

79.2%

2.1%

19.3%76.1%

18.9%

2.4%

0.7%

0.9%

F 2017

91.2

73.7

78.2%

20.3%

2010

86.6

78.1%

19.1%

2014

84.3

79.0%

2013

81.6

2012

78.5

18.3%

78.3%

19.3%

2011

78.8%

18.6%

0.2%

1.0%

0.1%

0.2%

2016

Annual Vehicles Produced (M)

Source: 2017 August IHS Data

MHEVHEVPHEVBEV

Diesel

Gasoline

BEV 0.0% 0.1% 0.1% 0.2% 0.3% 0.4% 0.6% 0.9%

PHEV 0.0% 0.0% 0.1% 0.1% 0.2% 0.3% 0.4% 0.7%

HEV 1.4% 1.3% 2.0% 2.1% 2.2% 1.9% 2.2% 2.4%

MHEV 0.1% 0.0% 0.2% 0.2% 0.1% 0.3% 0.6% 1.0%

Total xEV 1.5% 1.5% 2.4% 2.5% 2.8% 2.9% 3.8% 5.0%

HEV ICEPHEV DieselMHEVBEV

9 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Battery costs for BEVs and PHEVs, however, are declining fastPotential evolution of battery cell costs by 2030

2018

180

150

120

90

0

2030202920282027202620252024202320222021202020192017

173

152

Cell level ($/kWh)

145

159

143

70

9097

106

80

106

120128135128

147

Note: TAR report D segment battery cell cost used at ~65 kWH to 2025

Sources: BCG analysis and forecast; TAR report; JP Morgan Global xEV Components report; UBS Future of Powertrain report; expert interviews; GM annual global conference

LG/GMUBSTAR JP MorganBCG low case projectionsBCG base case projections

Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

10

Key parameters Cost curve from

$150 per cell to

$90 per cell

$60 a barrel Incentives are

not included

Regulations are

assumed to

remain in place

Battery costs Oil costs

Incentives/

Regulations

11 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Comparison of TCO across powertrains: US 5-year TCOC-segment cost of ownership year-over-year change for different xEVs

Source: BCG analysis

In 2020, purchasing a PHEV will cost consumer

$35,541 over life of 5 years from 2020-2025

In 2027, purchasing a BEV will

cost consumer $30,678 over life

of 5 years from 2027-2032 35,541

191817 3015

40,000

35,000

30,000

25,000

2928272625242322212016

Year

30,678

5-year TCO, C segment ($)

PHEV BEVHEVMHEVICE

12 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Comparison of TCO across powertrains: US 10-year TCOC-segment cost of ownership year-over-year change for different xEVs

41,434

2027202620252024202320222021202020192018201720162015

50,000

45,000

40,000

35,000

30,000

203020292028

35,705

10-year TCO, C segment ($)

Source: BCG analysis

BEVPHEVHEVMHEVICE

In 2020, purchasing a PHEV will cost consumer

$41,434 over life of 10 years from 2020-2030

In 2025, purchasing a BEV will cost consumer

$35,705 over life of 10 years from 2025-2035

13

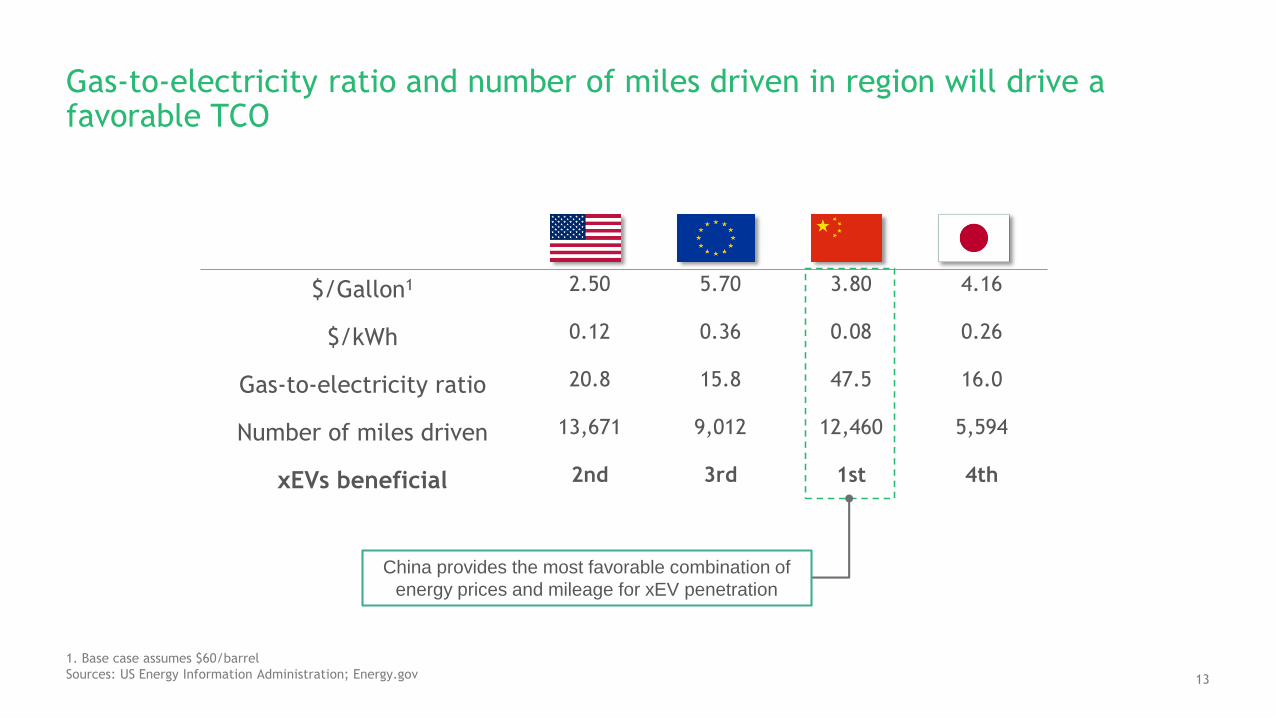

Gas-to-electricity ratio and number of miles driven in region will drive a favorable TCO

$/Gallon1 2.50 5.70 3.80 4.16

$/kWh 0.12 0.36 0.08 0.26

Gas-to-electricity ratio 20.8 15.8 47.5 16.0

Number of miles driven 13,671 9,012 12,460 5,594

xEVs beneficial 2nd 3rd 1st 4th

1. Base case assumes $60/barrel

Sources: US Energy Information Administration; Energy.gov

China provides the most favorable combination of

energy prices and mileage for xEV penetration

14 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Electrified vehicles are increasingly attractive at high mileage rates

2017 payback period, HEV versus ICE (years)1 2017 payback period, BEV versus ICE (years)1

Miles/yr USA China EU

25,000 6 4 3

50,000 3 2 2

75,000 2 2 1

100,000 2 1 1

Miles/yr USA China EU

25,000 11 5 6

50,000 6 3 3

75,000 4 2 2

100,000 3 2 2

1. Based on 2017 prices without incentives

Source: BCG analysis

15 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Cost-per-mile difference will be ~40% for urban shared vehicles in 2030Comparison: 2030 annual cost by category

0.0

0.5

1.0

1.5

1.22

Conventional ICE (10K yearly miles) 2030 Shared Autonomous

Vehicle (HEV)

(60K yearly passenger miles)

0.77

2030 Shared Autonomous

Electric Vehicle (BEV)

(60K yearly passenger miles)1

0.74

-40%

$/passenger mile per category

-37%

Car type and mileage

1. Corresponds to ~90K total miles, when passenger-less miles driven are added

Source: Upcoming BCG report, The Reimagined Car: Shared, Autonomous, and Electric

Cleaning

Tickets

Replacement (covers, mats, etc.)

Fleet Tax

Fleet Markup

Fleet Mgmt.

Data

Battery Replacement

Tires

Taxes/Fees

Software Upgrades

Financing

Fuel/Electric

Maintenance

Insurance

Depreciation

Parking

Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

16

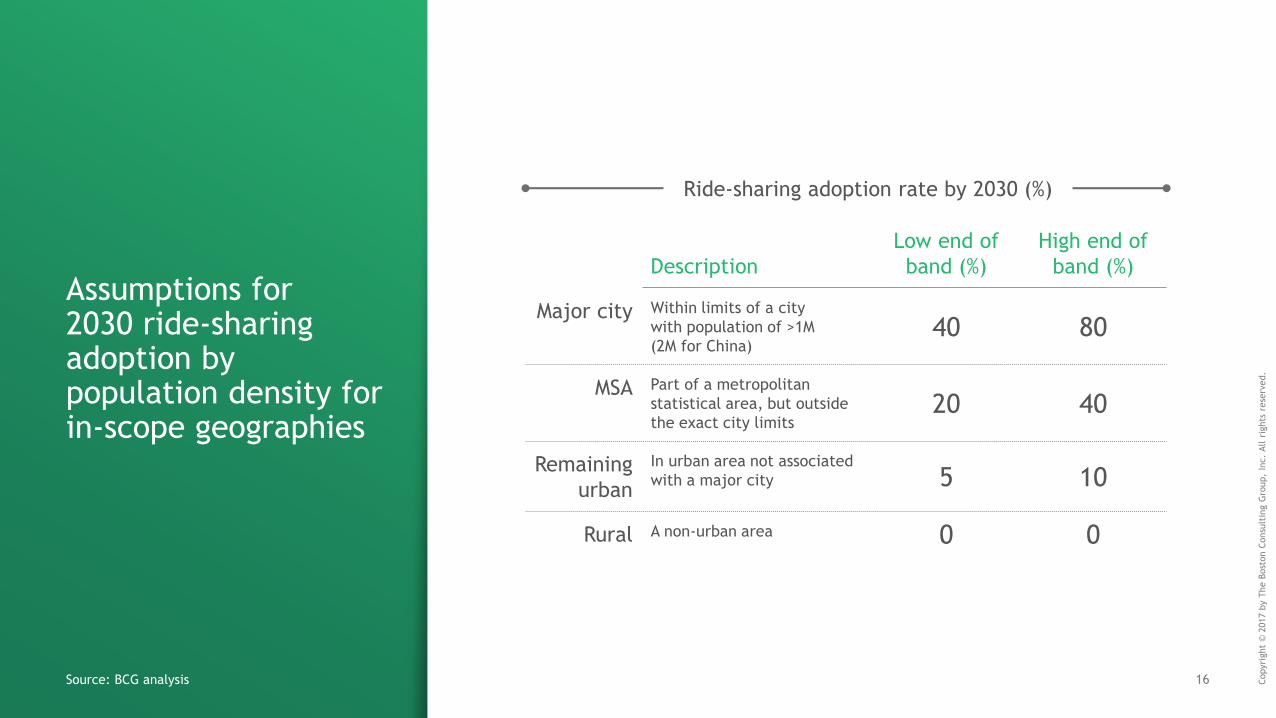

Assumptions for2030 ride-sharing adoption by population density for in-scope geographies

Source: BCG analysis

Description

Low end of

band (%)

High end of

band (%)

Major city Within limits of a city

with population of >1M

(2M for China)40 80

MSA Part of a metropolitan

statistical area, but outside

the exact city limits20 40

Remaining

urban

In urban area not associated

with a major city 5 10

Rural A non-urban area 0 0

Ride-sharing adoption rate by 2030 (%)

17 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Autonomous mobility varies by region and can have a range of outcomes

China Japan EU USA Global

12

5

20

15

10

5

0

30252015

1

4

9

4

20

15

10

5

0

30252015

2

6

2

14

6

20

15

10

5

0

30252015

10

4

19

5

0

30252015

10

15

20

7 8

20

10

0

30252015

15

5 431

Autonomous mobility veh.

as a % of vehicles sold

Autonomous mobility veh.

as a % of vehicles sold

Autonomous mobility veh.

as a % of vehicles sold

Autonomous mobility veh.

as a % of vehicles sold

Autonomous mobility veh.

as a % of vehicles sold

Note: Growth based on 2005-2017 adoption rate of smartphones (used from 2022 onwards)

Source: BCG analysis

High end of band Low end of band

18 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

BCG market forecast to 2030 (global view)

100

80

0

90

110

60

70

64%

8%

10%

1%

2016

90

2015

87

13%

3%

7%

2025

105

67%

9%

8%

8%

2%

6%

2024

104

70%

10%

8%

7%

2%

4%

2023

104

2022

102

2021

100

2020

98

78%

14%

2%

3%

1%

1%

2019

96

2018

93

2017

91

76%

Volume (M)

1%

2%

1%

2030

109

47%

5%

15%

13%

6%

14%

2029

108

53%

6%

12%

5%

12%

9%

2028

107

57%

6%

12%

11%

4%

10%

2027

106

61%

7%

11%

10%

3%

8%

2026

105

19%

DieselMHEVHEVPHEVBEV Gasoline

Source: BCG analysis

Regulation-driven Consumer-driven

Mobility impact

19 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

US market will see increased growth in MHEVs beginning in 2021; EUR market growth in BEVs will occur between 2023 and 2025

Source: BCG analysis

US

pro

jecti

ons

EU

pro

jecti

ons

15

10

0

20

32%

12%

16%

3%

48%

13%

2024

19

20232022 202520212020 2026

19

58%

2027

36%

1%

2028

2%

1%

2029

Volume (M)

8%

22%

2030

19

6%

21%

7%

11%

2019201820172016

19

2015

18

20

15

10

0

17

2020 2021 2022 2023 2024

8%

1%

10%

16%

3%

63%

17

2025 2026 2027 2029

20%

2%

12%

16%

3%

48%

17

20302028

Volume (M)

4%

91%

0%

3%

1%

1%

2019201820172016

17

2015

17

MHEV DieselHEVPHEVBEV Gasoline

20 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Volume in China will be driven by BEVs and PHEVs; in Japan, by HEVs and MHEVs owing to different driving patterns and OEM focus

Source: BCG analysis

Chin

a

pro

jecti

ons

Japan

pro

jecti

ons

6

0

4

202720262025

5

51%

3%

18%

20%

3%

4%

202420232015 20212020

5

64%

6%

12%

14%

2%

2019

5

Volume (M)

2016

5

2017 2018 2030

5

34%

2%

23%

24%

6%

12%

202920282022

0

35

25

30

20262025

32

81%

1%

5%

4%

6%

202420232022

3%28

Volume (M)

2030

35

55%

1%

2020

11%

7%

10%

17%

20292021 20282027

92%

2%

1%

1%

2%

2019201820172016

25

2015

22

GasolineDieselMHEVHEVPHEVBEV

21 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Incentives and lower battery costs could increase the share of BEVs

Source: BCG analysis

Impact on powertrain technologies Δ to base case

(% of global market 2030)

Base case Sensitivity ICE Diesel MHEV HEV PHEV BEV

High oil price Oil at $60/barrel Oil at $90/barrel (3.4) 0.6 1.0 0.4 0.6 0.9

Low battery

costs

Costs for TAR cost curve:

$90 per cell cost in 2030

Costs follow BCG cost curve:

$70 per cell cost in 2030 (1.5) 0.0 (1.4) 0.0 0.7 2.2

Government

incentives

No subsidies used, pure

economics forecasted

With current subsidies

for each region sustained

to 2030

(6.0) 0.0 (1.4) 0.0 2.5 4.8

Regulatory

rollback

Current CAFE regulations

remain in place in US

US administration reduces

CAFE/GHG regulations 3.4 0.0 (2.7) 0.0 0.0 (0.6)

22 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.Devise a pricing strategy to

incentivize customers to buy

xEVs to meet regulations

Make or buy new powertrain

modules and components

Manage differentiation in a

BEV environment

Invest in a charging network

Identify the highest areas of

value and key OEMs to

partner with

Manage the profitability of

manufacturing ICE

components

Adjust the level and timing of

investment

Support the development of a

charging infrastructure in

urban centers

Determine the level of incen-

tives to sustain momentum

until a breakeven TCO

Manage the shift in energy

source and the associated

shift in tax revenues

OEMs Suppliers Government

Key implications

23 Copyri

ght

© 2

017 b

y T

he B

ost

on C

onsu

ltin

g G

roup,

Inc.

All r

ights

rese

rved.

Author team and regional experts Selected publications and research

Xavier MosquetSenior partner

BCG Detroit

Hadi Zablit Senior partner

BCG Paris

Aakash Arora Principal

BCG Detroit

Andreas DingerSenior partner

BCG Munich

Gabe Rodriguez-GarrigaProject leader

BCG Detroit

Gang XuPartner

BCG Shanghai

Chris LaChanceProject leader

BCG Detroit

Michelle AndersenPartner

BCG Detroit

Eric GruskinAssociate

BCG Detroit

Kazutoshi TominagaPartner

BCG Tokyo

Making Autonomous Vehicles a Reality:

Lessons from Boston and BeyondA report by BCG and the World Economic Forum

October 2017

Self-Driving Vehicles, Robo-Taxis, and the

Urban Mobility RevolutionA report by BCG and the World Economic Forum

July 2016

Revolution in the Driver’s Seat: The Road

to Autonomous VehiclesA report by BCG

April 2015

To request more information on this research, please contact [email protected].

To request a media interview, please contact Eric

Gregoire at [email protected].

To discuss the findings with a BCG expert, please

contact Irene Perzylo at [email protected].

Revolution Versus Regulation: The Make-

or-Break Questions About Autonomous

VehiclesA report by BCG and the World Economic Forum

September 2015