THE EFFECT OF FINANCIAL TECHNOLOGY ON FINANCIAL INCLUSION ...

57

i THE EFFECT OF FINANCIAL TECHNOLOGY ON FINANCIAL INCLUSION IN NIGERIA BY USMAN MUHAMMAD USMAN BU/17C/BS/2885 DEPARTMENT OF ACCOUNTING FACULTY OF MANAGEMENT AND SOCIAL SCIENCES BAZE UNIVERSITY, ABUJA

Transcript of THE EFFECT OF FINANCIAL TECHNOLOGY ON FINANCIAL INCLUSION ...

i

THE EFFECT OF FINANCIAL TECHNOLOGY ON FINANCIAL

INCLUSION IN NIGERIA

BY

USMAN MUHAMMAD USMAN

BU/17C/BS/2885

DEPARTMENT OF ACCOUNTING

FACULTY OF MANAGEMENT AND SOCIAL SCIENCES

BAZE UNIVERSITY, ABUJA

ii

September, 2020

THE EFFECT OF FINANCIAL TECHNOLOGY ON FINANCIAL

INCLUSION IN NIGERIA

BY

USMAN MUHAMMAD USMAN

BU/17C/BS/2885

DEPARTMENT OF ACCOUNTING

FACULTY OF MANAGEMENT AND SOCIAL SCIENCES

BAZE UNIVERSITY, ABUJA

SEPTEMBER, 2020

iii

EFFECT OF FINANCIAL TECHNOLOGY ON FINANCIAL INCLUSION

IN NIGERIA

BY

USMAN MUHAMMAD USMAN

BU/17C/BS/2885

A DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE

REQUIREMENTS FOR THE AWARD OF BACHELOR OF SCIENCE

DEGREE IN ACCOUNTING

TO THE

DEPARTMENT OF ACCOUNTING

FACULTY OF MANAGEMENT AND SOCIAL SCIENCES

BAZE UNIVERSITY, ABUJA

iv

SEPTEMBER, 2020

DECLARATION

I hereby declare that this project entitled “THE EFFECT OF FINANCIAL

TECHNOLOGY ON FINANCIAL INCLUSION IN NIGERIA” has been

undertaken by me under the supervision of (MRS JOSEPHINE ENE). I further

certify this work has not been previously submitted for the award of a degree or

certificate elsewhere. All ideas and views are products of my research. Where the

views of others have been expressed, they have been duly acknowledged.

___________________ __________________

Usman Muhammad Usman 15/09/2020

BU/17C/BS/2885

v

CERTIFICATION

This is to certify that this research work ‘’ EFFECT OF FINANCIAL

TECHNOLOGY ON FINANCIAL INCLUSION’’ by USMAN MUHAMMAD

USMAN, BU/17C/BS/2885 has been approved by the Department of

ACCOUNTING, Faculty of Management and Social Sciences, Baze University,

Abuja, Nigeria

____________________ __________________

Mrs Josephine C. Ene

Supervisor

15/09/2020

____________________ __________________

Dr Adamu Garba Zango

Head of Department

15/09/2020

____________________ __________________

Prof. Osita Agbu

Dean, Faculty of Management

and Social Sciences

15/09/2020

____________________ __________________

Prof. Aliyu Kantudu 15/09/2020

External Examiner

vi

DEDICATION

I respectfully dedicate this project to my parents. Alhaji Muhammad Usman and

Hajiya Hafsat Muhammad Usman for their endless support and prayers. I appreciate

every effort put in shaping me into the man I have become today and I can only

celebrate every milestone with your prayers. Thank you for encouraging me to

dream, and for providing a platform for me to achieve my dreams.

vii

ACKNOWLEDGEMENT

After giving much gratitude to Almighty Allah (SWT), I direct my appreciation to

my parents, Muhammad Usman and Hafsat Usman for their prayers, understanding

and for instilling the quest for success at a young age. I will like to appreciate my

supervisor, Mrs Josephine Ene for her time, understanding, guidance,

encouragement and patience. I cannot fail to appreciate my lecturers who impacted

endless knowledge from their wide skills and experience especially my HOD, Dr

Adamu Zango. I want to thank my family members, grandparents and guardians for

their endless support, patience and well wishes. I also want to thank my amazing

siblings, Adda Nana, Adda Nafisa, Aisha, Idi, Maryam, Asmau, Alamin and

Maisaratu ; thank you for your support and prayers. I want to especially thank

Maryam for burning the midnight candle with me. I cannot fail to thank Kawu

Hammanga, Ibrahim Bello, Ahmed Iya and Abubakar Raji for their continuous

support and assistance rendered throughout the course of my degree. I would also

like to acknowledge my roommate and long-time friend turned brother Adil. My

classmates, thank you for extending your warm acceptance, healthy competition and

wonderful memories built. To other persons who contributed to this project Ahmad

Shafi’i, Qasim, Maryam, Zainab, Rasheedat, Salihu, Bashir, Safwan, Baffa, and

Hayatu, thank you for giving me multiple reasons to continue believing in myself.

viii

TABLE OF CONTENTS

TITLE PAGE........................................................................................................i

DECLARATION.................................................................................................ii

CERTIFICATION..............................................................................................iii

DEDICATION....................................................................................................iv

ACKNOWLEDGMENT...................................................................................v

TABLE OF CONTENTS..................................................................................ix

LIST OF TABLES..............................................................................................x

LIST OF FIGURES............................................................................................x

ABSTRACT.......................................................................................................xii

CHAPTER I: INTRODUCTION

1.1 Background to the Study.................................................................. 1

1.2 Statement of the Problem................................................................. 3

1.3 Objectives of the Study.......................................................................... 5

1.4 Research Questions.......................................................................... 5

1.5 Research Hypotheses........................................................................ 6

1.6 Scope of the Study.................................................................................. 6

1.7 Significance of the Study……………………….…………………….…. 6

ix

CHAPTER II: LITERATURE REVIEW

2.1 Introduction……………………………………………………… 7

2.2 Conceptual Framework ………………………..………………… 10

2.3 Empirical Analysis........ …………………………………………… 15

2.4 Theoretical Framework...................................................................... 20

CHAPTER III: RESEARCH METHODOLOGY

3.1 Introduction...................................................................................... 24

3.2 Research Design............................................................................... 24

3.3 Population of Study.......................................................................... 24

3.4 Sample of Study................................................................................ 24

3.5 Types and Sources of Data…............................................................ 25

3.6 Instrument of Data collection............................................................ 25

3.7 Definition of Variables…………………………………………..… 25

3.8 Model Specification........................................................................... 25

3.9 Method of Data Analysis...................................................................

CHAPTER IV: DATA PRESENTATION AND ANALYSIS

25

4.1 Introduction........................................................................................... 27

4.2 Presentation of Descriptive Statistics..................................................... 27

x

4.3 Analysis of Data ………………………………………...................... 29

4.4 Discussion of Findings ………………………………………………. 33

CHAPTER V: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

5.1 Introduction............................................................................................... 36

5.2 Summary ………............................................................................... 36

5.3 Conclusion................................................................................................ 36

5.4 Recommendations..................................................................................... 37

5.5 Limitations of the Study………………………………………………… 38

5.6 Suggestions for Further Studies.................................................................. 38

REFERENCES……………………………………………………………… 39

APPENDICES

CONTACT INFORMATION

xi

ABSTRACT

The concept of financial inclusion has been gradually accepted in the global world

since it is known as one of the key driver of economic growth and development. The

Central Bank of Nigeria’s cashless policy introduced in Nigeria in the year 2011

has in its objective, the financial inclusion. In view of this, the researcher seeks to

assess the impact of electronic banking on financial inclusion in Nigeria. The study

utilized the total number of automated teller machines, point of sale devices and

internet banking operation in Nigeria to represent electronic banking for the period

under review. The study used Statistical Package for Social Study with the aid of

linear regression analysis. The finding revealed that both internet banking and

automated teller machines have insignificant impact on financial inclusion while the

point of sale devices significantly impact financial inclusion in Nigeria. Based on

the findings as revealed by the study, it is recommended that all the deposit money

banks in Nigeria should work on the challenges that hinder the successful operation

of automated teller machines and internet banking and strive to meet international

best practice. Moreover, the number of point of sales should be increase and made

available with easy accessibility to the users.

KEYWORDS Financial Inclusion, Electronic Banking, Automated Teller Machine,

Point of Sale and Internet Banking.

1

CHAPTER I

INTRODUCTION

1.1 Background to the Study

Poverty with its debilitating effects have always had important implication on global development.

However, with COVID-19 taking its toll on the world, causing deaths, illnesses and economic

despair resulting to estimates that suggests that 49 million people will be pushed into extreme

poverty in 2020 (World bank, 2020), its relevance in global discourse has become apparently

prominent. To reduce the vulnerability to poverty, the global community has overtime deployed

several mechanisms with a marked inclination towards the pursuit of inclusiveness. The thrust of

this predilection being that poverty does not exist because of insufficient money in any economy,

but rather exists because of inequality in the distribution of national income. With this reasoning,

measures of inclusiveness such as financial inclusion have continued to generate a lot of research

and policy attention.

Financial inclusion is defined the availability of finance and financial services for all in fair,

transparent and equitable manner at an affordable cost. It also refers to the situation whereby basic

banking services are delivered at an affordable cost to all section of the society. These definitions

summarily portray financial inclusion as the incorporation of all citizens of a nation in formal

banking transactions. The involvement of the citizens in financial mainstream is expected to fuel

investment, create jobs and stimulate growth.

In Nigeria, the government through the Central Bank of Nigeria has tried to achieve a financial

inclusion as an integral part for promoting sustainable and inclusive growth by formulating policies

that are expected to encourage country wide access to financial services at affordable cost

particularly to the less privilege and vulnerable group Olatunji, (2015). The intent of these policies

2

and mechanisms is to reduce the number of persons excluded from organized financial system by

getting more people involved in the organized financial system. These consistent attempts to

sustain and deepen financial inclusion have included the deployment of technological innovations

in the financial sector.

Technological innovation in financial services is broadly referred to as financial technology.

Financial technology involves any new technology or innovation that disrupts traditional ways of

conducting financial transactions. Even more specifically, financial technology includes all

software and other modern technologies used by businesses that provide automated and improved

financial service delivery. Such technology in financial service delivery is expected to eliminate

barriers to access to banking services, encourage the use of bank services and ultimately contribute

to national economic growth (Asian Development Bank, 2016). Furthermore, ADB stated that

such innovations essentially serve as adequate means of providing opportunities to promote

financial inclusion through reduction of costs of providing these services.

Undoubtedly, the introduction of digital technology has greatly transformed the Nigerian financial

sector nevertheless; the extent to which it has increased participation and accessibility of the

financial services activities remains debatable. Therefore, this study attempts to determine the

impact of digitalization of financial services on financial inclusion.

1.2 Statement of the Problem

Financial technology, as observed by Villasenor, Darrell and Lewis (2015), has significantly

influenced the delivery of financial services. Villasenor, Darrell and Lewis further expounded that

such technologies have improved security and comfort in cash handling. However, the study

3

posited that though technology may have had a positive effect on quality of financial services, its

effect on financial inclusion remains to be adequately established.

The recent global focus is motivated by the increased recognition of the relevance of financial

inclusion as an important element of economic development consequently creating the need for

concerted efforts to eliminate or at least reduce obstacles and barriers to access to formal

banking services. The extent to which financial technology has facilitated financial inclusion

especially in developing economies has therefore continued to attract the attention of

researchers.

According to the study by Radcliffe and Voorhies (2012), financial technology created an

expansion of digital payment platforms that have offered the opportunity to link poor people with

providers of savings, credit, and insurance products. In the same vein, Nyamongo and Ndirangu

(2013), McKee, Kaffenberger and Zimmerman (2015) posited that financial technology has

facilitated access for lower-salary individuals with deficient financial related services choices.

Fanta and Makina (2019) also reported that technology fostered both access to and usage of

financial services thereby improving financial inclusion. The study specifically identified the

positive effect of internet access and Automated teller machines.

Contrariwise, Arenaza (2019) argued that the provision of technology in finance services involves

the participation and interactions of different players and the conditions of the regulatory

environment which pose complexities to all participants and thus negate their role in financial

inclusion. Buckley and Malady (2015) also argued that the constraints on the uptake and use of

financial technology in developing markets limit the effect of financial technology on financial

4

inclusion. Further probing the effectiveness of financial technology in improving financial

inclusion in developing economies, World Bank (2020) reported that technology interference

mechanisms required a foundation of dependable and productive bases that ensure that such

services are user-friendly, secure and cost-effective manner. Such required dependable and

productive bases are typically deficient in many developing economies and could potentially

diminish the participation of citizens.

Invariably, financial technology has the potential to activate the scope for better achievement of

inclusion and integration; however its effect in developing economies still remains to be

sufficiently validated. Furthermore, technology is a versatile and ever-changing phenomenon and

hence requires continuous reevaluation to ensure relevance of empirical evidence. Therefore, this

study examined the effect of financial technology on financial inclusion in Nigeria, a developing

economy, using current data.

1.3 Objective of the Study

The overall objective of the study is to determine the effect of financial technology on financial

inclusion in Nigeria. The specific objectives include the following:

i. To ascertain the effect of internet banking on financial inclusion in Nigeria.

ii. To examine the effect of Automated Teller Machines on financial inclusion in Nigeria.

iii. To assess the impact of Point of Sales on financial inclusion in Nigeria.

1.4 Research Questions

From the aforementioned objectives, the following research questions are formulated.

5

i. What is the effect of internet banking on financial inclusion in Nigeria?

ii. What is the effect of Automated Teller Machines on financial inclusion in Nigeria?

iii. What the impact of Point of Sales on financial inclusion in Nigeria?

1.5 Research Hypothesis:

The study tested the following the following hypotheses:

HO1: Internet banking has no significant effect on financial inclusion in Nigeria.

HO2: Automated Teller Machines has no significant effect on financial inclusion in Nigeria.

HO3: Point of Sales has no significant effect on financial inclusion in Nigeria.

1.6 Scope of the Study

The focus of this study is on effect of financial technology on financial inclusion in Nigeria. The

study is a time series study covering the period from 2010 to 2018. This includes the most current

data available on the variables understudied. Furthermore, the range of the years ensures the

provision of sufficient data for the tool of analysis chosen.

In this work, financial technology is proxies using internet banking, Automated Teller Machines

and Point of Sales while financial inclusion is estimated using the number of banked people.

1.7 Significance of the Study:

The study will provide current empirical evidence on the relationship between financial technology

and financial inclusion in Nigeria, thereby contributing significantly to the body of knowledge.

The research will also be helpful as a reference material for other researchers who chose to write

on the subject matter.

6

Furthermore, the findings of this study will assist the government and its agencies particularly the

Central Bank of Nigeria in policy formulation and implementation on the unbanked population.

The study will also provide a guide on moral suasion and directives to deposit money banks to

enhance financial inclusion through financial technology.

7

CHAPTER II

LITERATURE REVIEW

2.1 Introduction

In this chapter, literature in relation to financial technological innovation and financial inclusion

were reviewed to establish their existing conceptual, theoretical and empirical frameworks.

2.2 Conceptual Framework

2.2.1 Financial Inclusion

Raghuram Committee (2003) in India defined financial inclusion as the process of ensuring access

to financial services and timely and adequate credit where needed by vulnerable groups such as

the weaker sections and low income groups at an affordable cost. This definition clearly identified

the focus of financial inclusion on the vulnerable member of the society. It also captures ease of

accessibility to credit. According to Akingbola (2006) financial inclusion is the extension of the

benefits of banking to the have-nots. The study further explained that it simply means banks will

offer a basic account to anyone who want to have. The concept of financial inclusion explains how

the financial excluded, unbanked and under-banked people in the society are made to be accessible

and uses the affordable, quality financial services and product in convenience manner (CBN,

2009). Comprehensively, Ene (2019) outlined financial inclusion as a delivering of basic banking

services at an affordable cost to all sections of the society, especially the vast disadvantaged and

low-income groups who tend to be excluded from formal banking system. Financial inclusion

requires that attention is given to human and institutional issues, such as quality of access,

affordability of products, provider sustainability, and outreach to the most excluded populations.

8

Financial inclusion can therefore be defined as access to finance and financial services for all in

fair, transparent and equitable manner at an affordable cost.

Financial inclusion is widely considered as a right of all citizens to social inclusion, better quality

of life and a tool for strengthening the economic capacity and capabilities of the poor in a nation

BCB, (2010). Such submissions and obvious increasing importance of financial inclusion as a

catalyst for economic growth and development has motivated policymakers to view financial

inclusion as catalyst for the achievement of developmental goals by ensuring basic access to formal

banking system for all citizens.

Even though, the problem is more acute in the developing and African countries in particular, such

that achieving a higher financial inclusion level has become a global challenge Ardic et al, (2019).

This is proven by the evidence that only 46 per cent of the world adults have access to financial

services. Hence, the global target has been to remove all the barriers, including education, gender,

age, irregular income, regulation and geographical locations that have together contributed to the

dearth of access to financial services by billions of adults all over the world.

The Benefit of Financial Inclusion

Mohan (2018), noted that, once access to financial services improves, inclusion affords several

benefits to the consumer, regulator and the economy alike. The author explained that the

establishment of an account relationship can pave the way for the customer to avail the benefits of

a variety of financial products, which are not only standardized, but are also provided by

institutions that are regulated and supervised by credible regulators that ensures safety of

investment. In addition, Mohan expounded that bank accounts can also be used for multiple

purposes, such as, making small value remittances at low cost and purchases on credit. In

summary, access to a bank account does provide the account holder not only a safer means of

9

keeping his/her fund but also provides access to use of other low cost and convenient means of

transaction. For the regulator, the transparency in the flow of transactions makes monitoring and

compliance easier, while for the economy, increased financial inclusion makes capital

accumulation easier and more transparent. Mohan (2018) concluded therefore that “the single

gateway of a banking account can be used for several purposes and represents a beneficial situation

for all the economic units in the country.

Saddam (2019) stated that inclusion of this segment of the society would generate multiple

economic activities, cause growth in national output and eventually reduce poverty. The study

attributed the rise in poverty level in Nigeria to the challenges of financial exclusion. According

to him, achieving optimal level of financial inclusion in Nigeria means empowering 70.0 per cent

of the population living below poverty level, and this would boost growth and development.

Financial inclusion also guarantees improved ability of poor people to save, borrow, and make

payments throughout their lifetime. Summarily, financial inclusion will maximize the scale of

economic activities that can be financed and hence, energizing the potentials for higher economic

growth.

Dimensions of Financial Inclusion

Okorie (2017) explained that financial inclusion extended beyond the regular form of financial

intermediation. The study stated that it involved:

i. Basic no frills banking account for making and receiving payments;

ii. Savings products suited to the pattern of cash flows of a poor household;

iii. Money transfer facilities

iv. Insurance (life and non-life)

10

v. A platform for the mobilization of savings in the rural area through the diffused network of

branches in all parts of the society;

vi. The encouragement of banking habits among the largely agrarian rural population

vii. Provision of credit for the growth of the small scale industries and entrepreneurs and

viii. Promotion of balanced development and eventual reduction in the rural-urban migration

Issue and Challenges of Financial Inclusion

According to Moghalu, (2019), the dearth of access to financial services by billions of adults all

over the world poses serious challenges to global economic growth and development. The

challenge of inadequate financial inclusion is not just for the developing economies alone, from

the emerging to high-income countries, government conceive and implement policies that seek to

ensure majority of the population become financially included. Therefore improving the global

average level of financial inclusion has, therefore, become a global challenge. Moghalu observed

that beyond the non-robustness and inefficiencies of the financial system which contributes to the

act of being excluded or included, the more fundamental issue of suboptimal macroeconomic

environment in the form of low income capacity and pervasive poverty level among the populace

has played a more critical role of eroding the eligibility of the bulk of the financially excluded.

Specifically, the study noted that in Nigeria, the major challenges within the general economic

conditions have manifested in the forms of:

i. A major challenge in the financial inclusion process is how to ensure that the poor rural

dwellers are carried along considering the lack of financial sophistication among this segment

of the Nigerian society due to the general low level of financial literacy. Majority of the

estimated 40 million financially excluded Nigerians lack knowledge of the services and

benefits derivable from accessing financial services, while staff of the service providers often

11

display lack of adequate understanding of the services and so unable to educate effectively. In

fact sub-optimal outcome from attempts to increase customer awareness is reflected in the

lack of appreciable progress in the literacy level of the populace. This has remained a major

impediment to the progress of the financial inclusion as a result process.

ii. There is also the challenge of increasing poverty. Though the economy has been reported to

have grown at an average of 7.0 per cent between 2009 and 2011, unemployment rate continue

to increase while progress on many of the poverty reducing Millennium Development Goals

has been slow.

iii. The uncompetitive wage levels, particularly in the public sector where a large number belong

to the low-cadre means that these groups are excluded financially. Though their salaries are

paid into the bank but the personnel only visit the bank once in a month to collect their salaries

with little or nothing to save

To surmount these challenges, in 2010, a national financial inclusion target was instituted having

these five priorities as being most crucial to increasing financial inclusion in Nigeria:

i. Create an enabling environment for the expansion of DFS.

ii. Enable the rapid growth of agent networks with nationwide reach.

iii. Harmonize KYC requirements for opening and operating accounts/mobile wallets on all

financial services platforms.

iv. Create an enabling environment to serve the most excluded.

v. Improve the adoption of cashless payment channels, particularly in government-to-person and

person-to-government payments

12

The major goal of this revised Strategy is to reduce the proportion of adult Nigerians that are

financially excluded to 20% in year 2020 from its baseline figure of 46.3% in 2010.

2.2.2 Financial Technology (FinTech)

Financial technology is perhaps the best innovation that has happened in the banking industry in

the 21st Century. It has made banking possible away from banking premises. Banking can now

take place anywhere using various electronic devices like mobile phones, automated teller

machines, point-of-sale systems, smart televisions, computers, tablets, among others. Today,

different baking transactions can be completed or initiated from different locations outside banking

premises such as transfer and receipts of funds, balance enquiry, purchase of airtime, payment of

bills and account opening.

The concept of Financial Technology has been defined in many ways by researchers. Daniel (2005)

defines the concept as the delivery of information and services by banks to customers via different

delivery platforms that can be used on different electronic devices such as personal computers,

mobile phones or digital televisions with browsers or desktop software. As good as this definition

appears, it does not take into cognizance other platforms for financial technology such as

automated teller machines, internet banking and point-of-sales which are the focus of this study.

Similarly, Abid and Noreen (2006) defined financial technology as any use of information and

communication technology and other electronic means by a bank to conduct transactions and have

interaction with stakeholders. This definition is however broader than that of Daniel as it focuses

on information and communication technology. Abid and Noreen also posited that financial

technology is a system of payment whereby transaction takes place electronically without the use

13

of cash. Ayman and Poul (2007) defined financial technology as provision of banking and financial

services with the help of telecommunication devices such as mobile telecommunication devices.

Succintly, Basel committee on Banking Supervision (2003) defined financial technology as

nothing but e-business in the banking industry. From these definitions therefore, financial

technology may be viewed as a generic term for describing delivery of banking services and

products through electronic channels, such as mobile phones, the internet, automated teller

machines and point-of-sales facilities. In simple words, financial technology implies provision of

banking products and services through electronic delivery channels.

Financial technology has been around for quite some time in the form of automated teller machines

and mobile phone transactions, however, in more recent times, it has been transformed by the

internet—a new delivery channel that has facilitated banking transactions for both customers and

banks Moddibo, (2018).

The scope of offered services offered by financial technology may include facilities to conduct

bank transactions, to administer accounts and to access customized information. In the broader

sense financial technology enables the execution of financial services in the course of which—

within a technological procedure the customer uses communication techniques in conjunction with

telecommunication devices.

i. Automated Teller Machine (ATM)

ATM is a machine where cash withdrawal and deposits can be made over the machine without

going into the banking hall. It also provides other quick teller services including airtime purchase,

funds transfer, balance enquiry and bills payment, among others. These machines usually operate

24 hours/7 days and may be accessed with or without a card Al-Sukkar, (2005)

14

ii. Point-of-Sale (POS)

POS also referred to as point of purchase (POP) or checkout is the location where payment is made

in respect of a transaction an electronic device and card. A POS terminal manages the selling

process by a salesperson accessible interface Chitokwindo, (2014). The same system allows the

creation and printing of the receipt. POS systems record sales for business and tax purposes.

Chitokwindo however noted that an illegal software dubbed "zappers" is increasingly used on them

to falsify these records with a view to evading the payment of taxes.

iii. Internet Banking

Internet banking allows customers of a financial institution to conduct financial transactions on a

secure website operated by the institution, which can be a retail or virtual bank, credit union or

society. It also referred to as on-line banking. Banks increasingly operate websites and transaction

portals through which customers are able not only to inquire about account balances, interest and

exchange rates but also to conduct a range of transactions. Internet banking however is prone to

internet fraudsters and hackers if carried out over an unsafe platform Alabar, (2012).

Internet banking extends the opportunity to create another alternative method of banking beyond

the bank branch and ATM network through which vast section of the population, including people

who live in remote areas, will have easier and faster access to formal financial services Abid &

Noreen, (2006). Thus, internet banking, is simply defined as carrying out banking transactions via

mobile devices such as cell phones or personal digital assistant(s). The offered services may

include transaction facilities such as checking account balances, transferring funds and accessing

other banking products and services from anywhere, at any time as well as other related services

that cater primarily for financial information and communication needs revolving around bank

activities Ensor, Montez & Wannemacher, (2012). According to World Bank (2010), internet

15

banking refers to a system which enables people to conduct financial transactions using a mobile

device against a bank account accessible from that device. Since, compared to traditional banking,

with the internet banking system, an account holder can conduct banking transactions without

visiting a bank branch, thus it increases the efficiency of the individual account holder by saving

time as well as eliminating space shortcomings Sanusi, 2010; Ahmed, Rayhman, Islam &

Mahjabin, 2011). According to the central bank of Bangladesh, “Mobile Financial Services (MFS)

is an approach to offering financial and banking services via internet wireless networks which

enables for user to execute banking transactions. That is, any internet account holder can make

deposits, withdraw, and to send or receive funds from their internet account

2.3 Empirical Framework

Empirical literatures on the impact of financial technology on financial inclusion and related topics

have produced inconclusive arguments.

Christopher, Mike and Amy (2006) undertook a survey of four hundred and seven bank customers

in thirty-three organizations in Ekiti state of Nigeria. Their objective was to analyze the effects of

availability of financial technology facilities among other factors on the bank customers’ choice

of a banking institution. The study revealed that the availability of financial technology facilities

such as automated teller machine, internet banking and telephone banking do not have a significant

influence on customer’s bank choice decision. It could be observed however that the study is not

primarily focused on the impact of financial technology on financial inclusion and moreover, they

employed primary data for the study which may not be as reliable as secondary data.

16

In another related study, Mansur (2002), adopted qualitative research method to study the role of

technology in achieving financial inclusion in rural India. The paper attempted to examine the

contributions of information and communication technology towards achieving financial inclusion

and reducing financial exclusion in the country and analyzed different application of information

and communication technology which banks are adopting. In his finding, it was revealed that

information and communication technology play a significant role in achievement of financial

technology.

Dayadhar, (2019).posited that this would directly or indirectly reflect the effectiveness of the

financial institution’s efforts to bring-in underprivileged people to the mainstream financial

system, especially in rural area support in achieving inclusive growth. The study concluded that

modern information and communication technology can act as a tool to develop a platform which

helps to extend financial services to remote areas. The study specifically identifies internet banking

and automated teller machines as two promising options for achieving financial inclusion. Thus,

the technology of internet banking and automated teller machines are adding new avenues in

providing banking services to the unbanked population who are financially excluded. However,

the study is qualitative and relied on previous empirical findings and conclusions which makes it

prone to bias and subjectivity.

Ene (2019) carried out a study on the impact of electronic banking on financial inclusion with an

effort to fetch out the key drivers of financial inclusion in the wake of Central Bank of Nigeria’s

cashless policy. Regression analysis was adopted using ordinary least square in his data analysis.

However he argued that electronic banking has significant effect on financial inclusion by

specifically pointing out the point of sale as major driver of the financial inclusion in Nigeria.

Although he attribute the ineffectiveness of automated teller machine to the contribution of

17

financial inclusion as much as PoS is as a result of network problem that the out of service report

from machine is often thereby keeping the customers waiting till the services restored. He also

point out other technical issue such as dispense error and withholding the customers` cards after

the uses of machine as a major problem that hindered its performance in driving the financial

inclusion

Mago and Chitokwindo. (2014) examined the impact of financial technology on financial inclusion

in Zimbabwe, with a focus on mobile banking in the Masvingo province. The research adopted a

qualitative research methodology and a survey design. They argued that electronic banking

significantly impacts financial inclusion in Zimbabwe. Their results show that low income people

are willing to adopt mobile banking, thereby enhancing financial inclusion. The reason they argued

in this line is that internet banking is easily accessible, convenient, cheaper, easy to use and secure.

Although they adopted an admissible methodology, it could be observed that the scope of their

study is too narrow since they under understudied only a province as against the entire country

which would have produced a more robust analysis.

Asare and Sakoe (2015) examined the effects of financial technology on financial services in

Ghana using qualitative research method. The study found out that the advent of financial

technology in Ghana has enhanced accessibility to a wide range of banking products and also

delivery of banking services has been made increasingly faster to cover a wide range of customers

or people referred by existing customers. Therefore, the study concluded that financial technology

has fundamentally changed the business of banking in Ghana from a financial intermediary to a

financial shopping mall providing a one-stop-shop for various financial services.

18

In a similar study carried out by Asare and Sakoe (2015) on the effects of electronic banking on

financial services in Ghana, it was established that electronic banking has affected financial

services by empowering banking customers, improving the standard of service delivery and

making banking more competitive and complex. It was established that electronic banking has a

positive effect on bank productivity, banking transactions, cashier’s output, bank patronage, bank

services delivery, customers’ services and bank services. Electronic banking has affected

positively the number of people who have access to financial services in Ghana and has enabled

banks to reduce cost and banking services to be delivered faster, efficiently and with less staff.

In another related study, Dymski and Gary (2015) observed that today almost all banks are

adopting information and communication technology as a means to enhance service quality. They

are providing information and communication technology-based e-service to their customers in

form of financial technology such as internet banking or online banking. It brings convenience and

customer centricity, enhances service quality and cost effectiveness in banking and increases

customer satisfaction in banking services. Thus, in line with Mago and Chitokwindo (2014), they

agreed that financial technology positively impacts financial inclusion.

Akhisar, Tunay and Tunay (2015) carried out a study on the impacts of electronic base system

on the fbank performance in Egypt by adopting the execution of electronic-based managing an

account system in twenty three advance nations and developing countries` electronic financial

services in 2005 utilizing dynamic board information techniques. The result of the study set up

that bank productivity of advance and developing countries was influenced by the proportion of

the quantity of branches to the quantity of ATMs and were profoundly critical and electronic

managing an account services in a large form. The concentrate likewise found that a few variables

had a negative relationship, due to differing qualities in the level of advancement

19

Of the nations, the socio-social structure and electronic managing an account base.

Monyoncho (2018) carried out as study to find out the relationship between E-Banking and

financial inclusion as executed by the deposit money banks in Kenya utilizing optional data for

the period of five years. The discoveries of the study uncovered that ATM developments, and

Mastercards, offered convenience for the customers to access formal financial services in large

proportion. The study presumed that selection of E-Banking has positive effect to the financial

inclusion in Kenya and prescribed that deposit money banks ought to keep putting resources into

the development of automated teller machines for efficiency.

Andrianaivo and Kpodar (2019) in their study found evidence that, in Africa, large share of the

population are financially excluded and therefore resort to the use of informal financial services.

They also found a relatively high propensity to save, but financial expansion and deepening was

constrained by lack of access to financial services and absence of depth of financial technology.

The problem is apparently accentuated by insufficient financial technology; coupled with the fact

that the number of ATMs and bank branches are low in this region. Evidences from the study not

only revealed that the interaction between mobile phone penetration and financial inclusion is

positive and significant in the growth regression, but also that people in Africa consider investment

in mobile technology as a necessity as it constitutes a large portion of their earnings (Andrianaivo

and Kpodar (2019). It therefore means that mobile financial service platform could be the answer

to bridge the gap in financial technology

2.4 Theoretical Framework

20

Different theories have been used to explain financial inclusion by researchers. Some of these

theories are the financial innovation theory, the technology acceptance theory and the diffusion of

innovation theory.

2.4.1 Technology Acceptance Model

This model was originally put forward by Davis (1986) to expound on the attitude behind the urge

to employ technological knowhow (Monyoncho, 2015). TAM deals with perceptions and not

systems real usage and argues when new technological advancement is introduced to the

customers, either one of this occurs that is, Perceived Ease of Use (PEOU) and Perceived

Usefulness (PU) influence their decision (Lule, Omwansa & Waema, 2012). PEOU is the level of

confidence that people put on a system and if users perceive a new technology to be beneficial in

support of both short and long-run, there is that encouragement to use the system. Further, the level

by which an individual consider a system will boost performance in the short and long-run is the

PU (Mojtahed, Nunes & Peng, 2011). The TAM affirms that the systems real utilization is

established by each user's behavioral intention for usage and is inspired by an individual’s

perception to the system. The theory also explains that the perception towards new technology has

a direct relation to its functionality as well as the simplicity of the system Lim and Ting, 2012).

TAM considers that acceptance of technology and functionality is influenced by consumer’s

intentions that establish the customer’s perception towards system (Mojtahed, Nunes & Peng,

2011). The theory also supports that the recognitions or suspicions about the advancement are

instrumental in the improvement of states of mind that will in the long run result in system usage

conduct (Lim & Ting, 2012).

TAM also explores the attitude of individuals towards particular system Lule, Omwansa and

Waema, 2012). The TAM gives details and clarifies and portrays the reasons why clients

21

acknowledge or dismiss an advancement or data framework. TAM is important both as a prescient

strategy, considering the objective to evaluate the probability of individuals and associations to

receive a specific innovation Mojtahed, Nunes and Peng, (2011). TAM can be used to explain the

digital financial services which can be applied in clarifying the existence of variations in consumer

behaviors especially when it comes to use of related digital financial services (Lim & Ting, 2012)

The theory is an adaptation of the Reasoned Action Theory specifically tailored for modeling user

acceptance of information systems. The goal of the theory is to provide an explanation of the

determinants of computer acceptance that is general, capable of explaining user behavior across a

broad range of end-user computing technologies and user populations, while at the same time being

both parsimonious and theoretically justified. Thus, this study believes that the acceptance of

contemporary banking technology by customers is fundamental to the performance of these banks

as well as the realization of financial.

2.4.2 Diffusion of Innovation Theory

The Diffusion of Innovations (DOI) theory was proposed by Rogers (1995) to explain the approach

through which innovation can be passed via different ways over certain period among different

users (Sarker & Sahay, 2004). DOI theory explores the ways in which innovative ideas are passed

from one generation to the other. According to DOI theory, an innovation is conveyed through

various channels continually among individuals of the same social beliefs (Echchab &

Hassanuddeen, (2013).The dispersion of Innovation hypothesis looks at the rate at which new

advancement are spreading, how the new development is spreading and reasons why it is spreading

with a specific end goal to research the elements influencing the selection of new data innovation

advancement (Monyoncho, 2015). The diffusion of innovations theory explains that innovationists

22

apply normal distribution curve which can be partitioned into five segments to categorize users in

terms of innovativeness. Diffusion theory explains that the crucial aspect in establishing

implementation of innovation is: absolute advantage, companionable, simplicity, trial ability as

well as ease to be detected (Monyoncho, 2015). DOI also classifies users as modernizer, early

modernizers, and timely mass, late mass and stragglers (Echchab & Hassanuddeen, 2013). DOI

theory perceives innovations to be passed on via several ways several in a span of time as well as

a certain system (Sarker & Sahay, 2004). DOI theory tries to explicate as well as illustrate the

approaches in which innovations that are digital financial services are adopted and becomes

successful.

Innovation Diffusion theory considers a set of attributes as

Triability: The degree to which an innovation may be experimented with on a limited basis

Complexity: The degree to which an innovation is perceived as relatively difficult to understand

and use.

Relative Advantage: “The degree to which an innovation is perceived to be better than the idea it

supersedes”.

Compatibility: “The degree to which an innovation is perceived as consistent with the existing

values, past experiences and needs of potential adopters.

Observability: “The degree to which the results of an innovation are visible to others”.

Among these attributes, only relative advantage, compatibility and complexity are consistently

related to innovation adoption (cheu et al., 2000).

Rogers reviewed nearly 1500 studies where variants of IDT are used to investigate the adoption of

technological innovations in an array of settings including, agriculture, health care, city planning,

and economic development. A smaller set of studies focus on, how these attributes influence

23

behavioral intention and use. Rogers developed his IDT constructs by identifying the product

attributes that most greatly influenced adoption.

Since Nigeria is a developing nation with several challenges associated with technology

acceptance, the theoretical framework that closely explains this study is the technology acceptance

theory and hence is the theory that underpins this study.

Summary of Literature Review

The subject of financial technology and financial inclusion has been a point which has pulled in

the consideration of researchers all inclusive with blended outcomes. A few of the investigation

endeavors utilized data that are primary in nature to analyze which could be distorted by bias as

such data are inclined to control towards the analyst's ideal goals and ends. While a portion of the

revealed that there was no connection between the financial technology and the financial inclusion,

some other found a significant and positive effect of financial technology on financial inclusion.

To provide further clarification to the existing discourse, the present examination utilizes optimal

information got from exceptionally legitimate establishments in Nigeria to explore the relationship

existing among the variables.

24

CHAPTER III

RESEARCH METHODOLOGY

3.1 Introduction

This section explains the methodology used to carry out this study. The chapter discussed the

research design, population, source of data, variable measurement, model specification and

technique of analysis of the study.

3.2 Research Design

This study used descriptive research design to examine the impact of financial technology on

financial inclusion by assessing how the various proxies of financial technology influence access

to financial product and services. The period understudied from 2010 to 2018 (9years) is

considered sufficient for the examination of the relationship while isolating the influence of other

factors. Furthermore, the use of population growth rate as a control variable will eliminate the

potential effect of increase in population.

3.3 Population and Sample of the Study

The study considered all the understudied financial technology variables offered by all the

financial banks in Nigeria from 2010 to 2018. Specifically, internet banking, automated teller

machine and point of sale were selected to assess their impact on financial inclusion.

3.4 Type and Source of Data

Secondary data on all the variables were extracted from Central Bank of Nigeria Statistical Bulletin

2018.

25

3.5 Definition of Variables

S/N Type Variable Measure/Proxy

1 Independent Financial Technology Internet banking (IB)

Automated Teller Machines

(ATMs)

Point of Sales (POS)

2 Dependent Financial Inclusion No of Bankable Population (FIN)

3 Control Population growth Population growth rate (POP)

3.6 Model Specification

The below stated model was used for this study

FIN= β 0 + β1ATMt-1 + β2POS t-1 + β3IBt-1 + β4POP t-1 + ξt-1

Where:

FIN represents the bankable population for the period

ATM represents the number of automated teller machine in Nigeria

POS represents the population that used point of sale in Nigeria

IB represents population that engaged in internet banking in Nigeria for the period under

consideration

POP represents the population that used point of sale in Nigeria for the period in consideration

β0 to β4 represent coefficient of the variables

ξ represent error term

3.8 Method of Data Analysis

26

The extracted data were analyzed utilizing descriptive and regression analysis techniques. The

Statistical Package for Social Science (SPSS) version 20.0 was used to generate the outputs.

27

CHAPTER IV

Data Presentation and Analysis

4.1 Introduction

This section of the research work presented and analyze all the relevant data concerned which

include: the internet banking, Automated Teller Machine and Point of Sales. The presented data

basically focused on financial inclusion to know the level of adopting banking as a means of

transaction among the populace through the stated variables listed above.

4.2 Presentation of Descriptive Statistic

The table 4.2.1 below stated the result obtained via descriptive measure with the variables

employed

The Table 4.1 below presented the descriptive result of the variables employed in this study.

Table 4.1: Descriptive Statistics of the variables employed

N Minimum Maximum Mean Std. Deviation Skewness Kurtosis

Statistic Statistic

(000,000)

Statistic

(000,000)

Statistic

(000,000)

Statistic

(000,000)

Statistic

(000,000)

Std.

Error

Statistic Std.

Error

Financial

Inclusion

7 1454.96 1851.83 1665.1114 163.79838 -.365 .794 -1.781 1.587

Internet

Banking

7 31567364087.00 184596629926.57 88909986491.1372 53352358917.94969 1.033 .794 .468 1.587

28

Automate

Teller

Machine

7

1568949120387.

82

6437592402748.4

0

39842089.7143 51661460.44785 .497 .794 -.373 1.587

Point of Sale 7 2367891.00 146267156.00

3637690158422.60

30

1704858208818.94460 1.827 .794 3.346 1.587

Valid N

(listwise)

7

The table above discussed the roles play by various variables employed in this study to encourage

the numbers of bankable individual in Nigeria banking sector. From the result, one can observed

that the Point of Sales plays a significant role to financial inclusion. At this point, the researched

agreed that the introduction of PoS in the Nigeria banking industry as a variable within the period

under the study encourage the bankable populace to engage in the formal financial services. In all,

the study showed that all the variables employed in this study had positive mean return which

shows a positive increase in the numbers of individual that use banking services.

In assessing the consistency of the variables in term of their contribution to the increase in the

customers of the bank, the above table also showed that the Point of Sales is more consistent than

other variables. This is because of its standard deviation of 1704858208818.94460 from a means

performance of 3637690158422.6030. This is follow by internet banking with the standard

deviation of 53352358917.94969 with the means value at 88909986491.1372. This has shown the

said variables experience a consistent contribution for the time under the study.

It is also shows in the table that the selected variables for this investigation were positively skewed

29

4.3 Data Analysis

Table 4.2 Regression Result for the Variables Employed

Coefficients

Model Unstandardized Coefficients Standardized

Coefficients

T

Sig.

B

(000,000)

Std. Error

Beta

1

(Constant) 1153.788 148.431 7.773 .004

Internet Banking 8.319E-010 .000 .271 .315 .774

Automate Teller Machine 1.595E-010 .000 1.660 2.680 .075

Point of Sale -3.584E-006 .000 1.130 1.433 0.0247

a. Dependent Variable: Financial Inclusion

The result in the table above demonstrates that positive relationship exist between financial

inclusion, internet banking, automated teller machine and point of sale. The implication of this is

that, any changes in the financial inclusion as dependent variable will cause an increase in the other

explanatory variables. The analysis explain further that keeping the variables at constant level, the

financial inclusion will only decrease by 12% (1153.788) ..

The t-result shows that all the explanatory variables used in this study with the exception of Point

of Sale were statistically insignificant to explain their contribution to financial inclusion. The

reason is that the t (sig) were greater than 0.05 level of significant and on this basis, null hypothesis

is accepted to the study that internet banking and automatic teller machine were not significant to

explain the contribution to the financial inclusion.

30

Table 4.3 Summary of the Regression Result for the Variables Employed

Model Summary

Model R R Square Adjusted R

Square

Std. Error of the

Estimate

1 .936a .876 .752 81.63282

a. Predictors: (Constant), Point of Sale, Automatic Teller Machine, Internet

Banking

The approximate R square of 88% as contained in the table above is an indication that change in

the financial inclusion were as a result of the contribution of the explanatory variables used, while

the remaining 12% will be as a result of other variables that are excluded in the model.

Table 4.4. The Regression result

ANOVAa

Model Sum of Squares Df

Mean Square

F Sig.

1

Regression 140987.706 3 46995.902 7.052 .071b

Residual 19991.753 3 6663.918

Total 160979.458 6

a. Dependent Variable: Financial Inclusion

b. Predictors: (Constant), Point of Sale, Automatic Teller Machine, Internet Banking

.The probability value of f, 0f 0.071 as shown in the table above is an indication that not all the

explanatory variables used in the course of this study are statistically insignificant to explain the

contribution to financial inclusion in the Nigeria banking sector. The reason is that F (sig) of 0.071

31

is greater than 0.05 significant level and in this case, the null hypothesis is accepted that the model

is statistically insignificant.

Testing of Hypotheses

The null hypotheses for this study are as follows

HO1 There is no significant relationship between internet banking and financial inclusion in

Nigeria.

HO2: There is no significant relationship between Automated Teller Machines and financial

inclusion in Nigeria.

H3: There is no significant relationship between Point of Sales and financial inclusion in Nigeria

Hypothesis One Testing

HO There is no significant relationship between internet banking and financial inclusion in Nigeria

H1 There is significant relationship between internet banking and financial inclusion in Nigeria

Table 4.5

Variable t-statistic Sig

Internet Banking .315 0.774

32

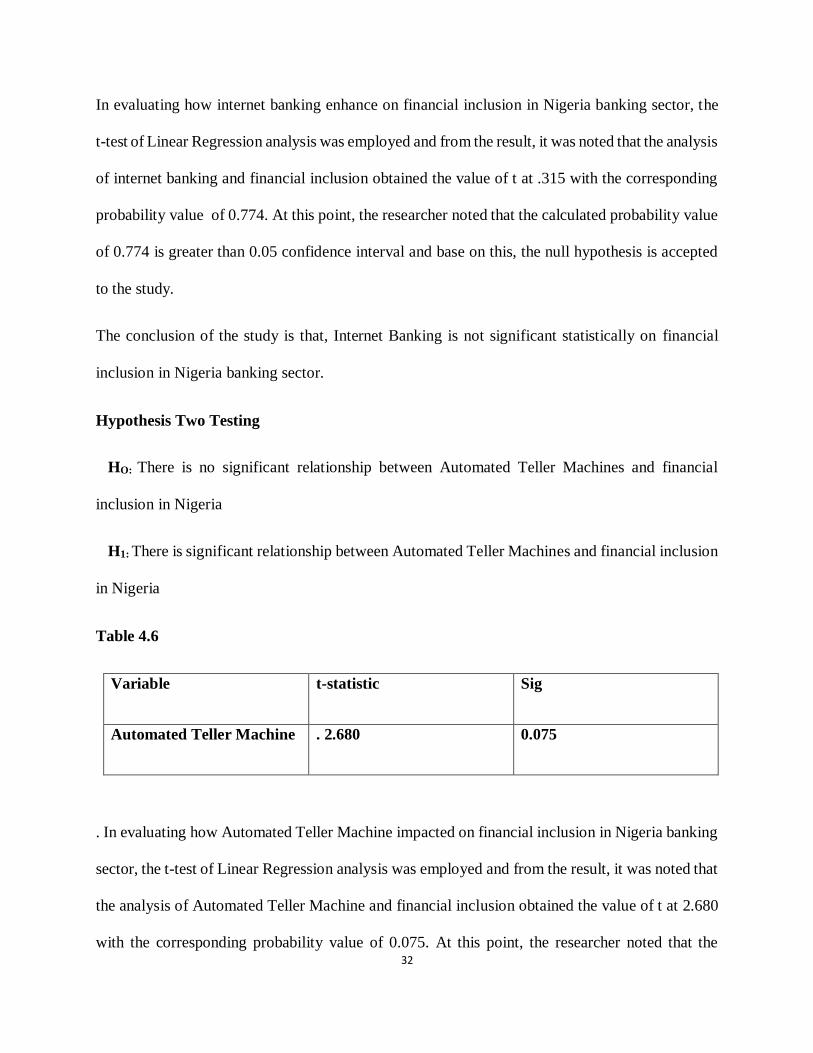

In evaluating how internet banking enhance on financial inclusion in Nigeria banking sector, the

t-test of Linear Regression analysis was employed and from the result, it was noted that the analysis

of internet banking and financial inclusion obtained the value of t at .315 with the corresponding

probability value of 0.774. At this point, the researcher noted that the calculated probability value

of 0.774 is greater than 0.05 confidence interval and base on this, the null hypothesis is accepted

to the study.

The conclusion of the study is that, Internet Banking is not significant statistically on financial

inclusion in Nigeria banking sector.

Hypothesis Two Testing

HO: There is no significant relationship between Automated Teller Machines and financial

inclusion in Nigeria

H1: There is significant relationship between Automated Teller Machines and financial inclusion

in Nigeria

Table 4.6

Variable t-statistic Sig

Automated Teller Machine . 2.680 0.075

. In evaluating how Automated Teller Machine impacted on financial inclusion in Nigeria banking

sector, the t-test of Linear Regression analysis was employed and from the result, it was noted that

the analysis of Automated Teller Machine and financial inclusion obtained the value of t at 2.680

with the corresponding probability value of 0.075. At this point, the researcher noted that the

33

calculated probability value of 0.075 is greater than 0.05 confidence interval and based on this, the

null hypothesis is accepted to the study.

The conclusion in this study is that, Automated Teller Machine is not significant statistically on

financial inclusion in Nigeria banking sector.

Hypothesis Three Testing

H0: There is no significant relationship between Point of Sales and financial inclusion in Nigeria

H: There is significant relationship between Point of Sales and financial inclusion in Nigeria

Table 4.7

Variable t-statistic Sig

Point of Sale 1.433 0.0247

In assessing how Point of Sale affect financial inclusion in Nigeria, the t-statistic of Linear

Regression analysis was employed and from the result, it was noted that the analysis of Point of

Sale and financial inclusion obtained the value of (t) at 1.433 with the corresponding probability

value of 0.0247. At this point, the researcher noted that the calculated probability value of 0.0247

is less than 0.05 confidence interval and based on this, the null hypothesis is therefore rejected...

The conclusion in this study is that, Point of Sale has positive effect to the financial inclusion in

Nigeria banking sector.

4.4 Discussion of Finding

34

According to the number one objective of this study, which target at assessing the impact of

Internet Banking on Financial Inclusion in Nigeria. As observed from the result obtained in

regression analysis, although the coefficient is positive and insignificant and this prompt the

researcher to conclude that, positive relationship exist but Internet Banking has no significant

effect on Financial Inclusion in Nigeria. The finding is indeed contrary to the view of Dayadhar,

(2019) and Mago and Chitokwindo. (2014) It is expected that the introduction of Internet Banking as

a financial technology to ease the banking transaction should have impacted positively on the

Financial Inclusion. The suspicious here is that, the poor internet service in the country and cost

of data purchase might have hinder the progress thereby discouraging people to use this medium

Moddibbo M. (2019).

The second objective of the study is to assess the impact of Automated Teller Machine on Financial

Inclusion in Nigeria. The regression result however shows that this machine has no significant

impact on Financial Inclusion despite positivity in their relationship. The ineffectiveness to impact

as expected can be trace to its non-availability in the rural area and inability to dispense all the

denomination in naira. This finding is in line with the view of Ener (2019), as well contrary to the

research finding of Rose & Paul ((2019) and disagree with the view of Monyoncho (2018).

Finally, the last objectives is to find out the effect of Point of Sale on Financial Inclusion in Nigeria.

Recently Point of Sale has become a common tool in the hand of individuals and businesses as a

means of transaction without necessary going to banking hall. This development ease way of doing

business as well as job creation in the country. With role play out by Point of Sale in the economy,

it is expected to have positive effect on Financial Inclusion in Nigeria of which this study is in

agreement with. This finding also agreed with the views of E. Ene (2019), who confirmed it`s

positive and significant effect on financial inclusion in Nigeria.

35

Moreover, three hypotheses were tested and the study showed that all except one explanatory

variable within the period covered by the study had no significant impact on the Financial Inclusion

in Nigeria.

36

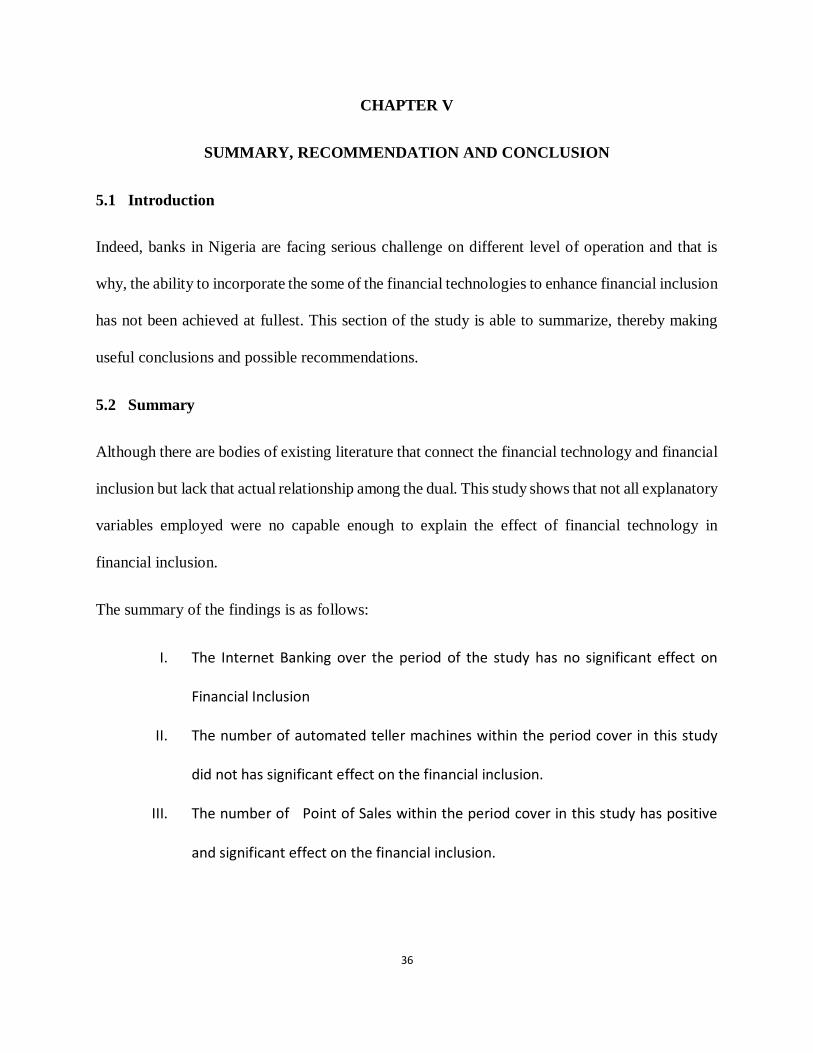

CHAPTER V

SUMMARY, RECOMMENDATION AND CONCLUSION

5.1 Introduction

Indeed, banks in Nigeria are facing serious challenge on different level of operation and that is

why, the ability to incorporate the some of the financial technologies to enhance financial inclusion

has not been achieved at fullest. This section of the study is able to summarize, thereby making

useful conclusions and possible recommendations.

5.2 Summary

Although there are bodies of existing literature that connect the financial technology and financial

inclusion but lack that actual relationship among the dual. This study shows that not all explanatory

variables employed were no capable enough to explain the effect of financial technology in

financial inclusion.

The summary of the findings is as follows:

I. The Internet Banking over the period of the study has no significant effect on

Financial Inclusion

II. The number of automated teller machines within the period cover in this study

did not has significant effect on the financial inclusion.

III. The number of Point of Sales within the period cover in this study has positive

and significant effect on the financial inclusion.

37

5.3 Conclusion

The target of every government across the globe particularly underdeveloped and developing

nation is to achieve the financial inclusion. Financial inclusion is term as a key element to drive

the economic growth and development and this is what called for this research as an area of

interest. In my addition to the existing knowledge in this subject matter, the study seek to find out

which of the variables of financial technology that drive the financial inclusion in Nigeria. As such

the study discovered that positive relationship exist between the financial technology and financial

inclusion particularly the contribution of Point of Sales as a driver of financial inclusion is

commendable. The other two variables such as Automated Teller Machine and Internet Banking

are facing major challenges thereby hindering their contribution to financial inclusion in Nigeria.

5.4 Recommendations

Following the specific objectives outline in this study, the following have been recommended for

system improvement.

I. Effort should be made by the government through the network provider to improve in

networking for effective uses of internet banking. There should be a campaign by the banks

to their customers to educate them on how to use the services.

38

II. The policy maker should design a strategy toward enhancing the automated teller machines

in term of its availability not only the cities also in the rural areas, improve on its

networking and its ability to dispense different Naira denomination.

III. The campaign on the uses and the convenience of financial technology for transaction

should be intensify by the regulators since it is capable to drive the financial inclusion.

IV. As such Point of Sale instrument have been found to be significant to drive the financial

inclusion, the Central Bank of Nigeria should make it more accessible to all businesses in

Nigeria,

5.5 Limitations of the Study

In the course of this study, the researcher encountered many challenges such as time constraints,

finance, unavailability of needed documents/data and the restriction of movement as a result of

pandemic situation in the country. All these were the limitations to this study.

5.6 Suggestion for Further Study

This study has contributed significantly to the argument on the impact of financial technology on

financial inclusion in Nigeria. The study is restricted to only three variables namely internet

banking, automated teller machine and point of sale. How other financial technology such as

mobile banking on financial inclusion. Therefore, the impact of this variable on financial inclusion

can be considered for further study.

39

References

Thingalaya, N.K., Moodithaya, M.S. and Shetty, N.S. (2010), Financial Inclusion.

Schumpeter, J. A. (1934). Theorie derwirtschaftlichenEntwicklung. Leipzig: Duncker and

Humblot. English translation published in 1934 as The Theory of Economic Development.

Cambridge, MA: Harvard University Press.

Mansur L., (2002), “Do Efficient Banking Industries Accelerate Economic Growth in Transition

Countries” (December 19, 2002). BOFIT Discussion Paper No. 14/2002.

Ahmed, Rayhman, Islam & Mahjabin, 2011), “Management of Nigeria’s Domestic Debt”, Keynote

Address at the 7thMonetary Policy Forum Organized by the Central Bank of Nigeria at the

CBN Conference Hall, Abuja.

Banco Central Do Brazil (2010)’’Report on Financial Inclusion’’ a report of the financial inclusion

project in Brazil.

Raghuram Committee (2008), A Hundred Small Steps—A Report of the Committee on Financial

Sector, India.

Based committee on Banking Supervision (2003), “Risk Management Principle for Electronic

Banking “Switzerland Bank for International Settlements, Retrieved 10th July, 2010 from

http://www.bis/pub/bcbs/pdf.

Oluyemi, N (2004), The Economic Effects of Technological Progress: Evidence from the

Banking Industry”. Journal of money, Credit and Banking.

Chitokwindo, L. B. (2014), Inclusive Growth—Role of Financial Sector. National Finance

Conclave, Bhubaneswar, 27 November 2010, 23-39.

40

Babalakins and Daniel, M.A (2010),.financial services and the internet: what does cyberspace

means for the financial service industry? Internet research: electronic networking

application and policy, 7(2): 120-128’

Abid and Noreen, (2006), Banking and the internet. Past, Present, and possibility. Retrieved

March 2, 2011.From http.//.www.-db. Stanford. Edu/pub/gio/cs991 banking. Html

Chakrabarty K.C (2010), Inclusive Growth-Role of Financial Sector. Paper presented at the

National Finance conclave, Bhubaneswar-Orissa, India, 27th November.

Boyes, G and Stone, M (2003), E-business opportunities in financial services, journal of financial

services marketing, vol. 8: 176-189.

Moghalu, P. Z. (2019),), Economic Growth, Financial Deepening and Financial Inclusion. Annual

Bankers Conference, Hyderabad, 3 November 2006, 72-95.

Kama, U. and Adigun, M. (2013) Financial Inclusion in Nigeria: Issues and Challenges. Central

Bank of Nigeria, Abuja, Occasional Paper No. 45. https://doi.org/10.2139/ssrn.2365209

Sanusi, L. S. (2010), “The Nigerian Banking Industry: What Went Wrong and the Way Forward”

Being a Convocation Lecture Delivered at the Convocation Square, Bayero University,

Kano.

Sanusi, L. S. (2012). “Banking Reforms and its Impact on the Nigerian Economy” CBN Journal

of Applied Statistics, 2(2), 115-122.

Ensor, Montez & Wannemacher,( 2012), Financial Inclusion: Issue and Challenges. Economic and

Political Weekly, 41, 4310-4313

Ene, E E (2019) The Impact of Electronic Banking on Financial Inclusion in Nigeria.

41

Ayman, A and Poul, T.(2007) “The Impact of Electronic Banking on the Performance of Jordanian

Bank” Journal of Internet Banking and Commerce Vol. 16 No 2

Daniel, E. (2005) Provision of Electronic Banking in the UK and the Republic of Ireland.

International Journal of Bank Marketing

Al-Sukkar, H. (2005): “Toward a Model for the Acceptance of Internet Banking in Developing

Countries”, Information Technology for Development, 11(4): 381-398 4.

Amit R &Schoemaker P (1993), Strategic Assets and Organizational Rent. Strategic

Management Journal,14:33-46.

Alabar, N. (2012). Research methodology in the behavoiured sciences, Lagos: Longman.Awe J.

(2006),’’ don’t open an account, if it isn’t an e-bank’’ (http www. Jida.com) retrieve

9thSeptember 2014.

Mago, S. and Chitokwindo, S (2014), The Impact of Mobile Banking on Financial Inclusion in

Zimbabwe: A Case for Masvingo Province. Mediterranean Journal of Social Sciences, 5,

221-230.

Abid, H. and Noreen, U.C. (2006) Ready to E-Bank: An Exploratory Research on Adoption of E-

Banking and E-Readiness in Customers among Commercial Banks in Pakistan. Working

Paper Series

CBN (2003) Guidelines on Electronic-Banking in Nigeria, available at http/www.cenbank.org

Charity-Commission (2003), Guidelines On Electronic Banking, available at

http/www.charity-commission.gov.uk

Central Bank of Nigeria (2013) Financial Inclusion Strategy. Abuja

42

Central Bank of Nigeria. (2009) Centre for History and New MediaZotero version

2.0.9.http://www.zotero.org

Moddibo, H. M. (2003) E-Banking: Challenges and Opportunities. Economic and Political

Weekly, 38, 5377-5381

Asare, M. and Sakoe, J.(2015), Understanding Adoption and Continual Usage behavior Towards

Internet banking Services in Hong Kong, (Unpublished Master of PhilosophyThesis),

Lingnan University, Hong Kong. Commerce/Jibc/01030.htm

Christopher, G. C., Mike, L. and Amy, W. (2006): “A Logit Analysis of Electronic Banking in

New Zealand”, International Journal of Bank Market, 24: 360-383 5.

Akingbola (2006), The Benefits of Information Technology, at http/www.ebusinessforum.com

Fagbuyi, T (2003): “New Security Requirements For E-Banking System”, In Business

Times, August 25-31:36

Dymski, P and Gary, A. (2005) Financial Globalization, Social Exclusion and Financial Crises

’International Review of Applied Economics,19 (4): 439-457.

Mojtahed, E. & Nunes, K & Peng, L. M (2011), Financial Inclusion, Regulation and Stability:

Kenyan

Experience and Perspective. A paper presented at the UNCTAD's Multi-Year

Expert Meeting on Trade, Services and Development held in Geneva, Switzerland

World bank, (2020), Access to Financial Services in Nigeria 2019 Survey.

Olatunji S. (2015), Supply Side: The Impact of Financial Inclusion Policies on Deepening

Financial Inclusion in Nigeria. Retrieved on 17th August 2016

43

Danis, F. D (1989) Perceived usefulness perceived ease of use, and user acceptance of information

technology MIS quarterly, 13(3): 319-340.

Raghuram Committee (2003), Major role of technology in financial inclusion, The Hindu,

Retrieved from:

http://www.thehindu.com/business/Industry/major-role-of-technology-in-financial

inclusion/article2216563.ece

Asian Development Bank, (2016), Better policy Series” India Sustaining high and inclusive

growth, Retrieved from:

http://www.oecd.org/india/IndiaBrochure2012

Upahi, S ,& Omuya, O, (2019), Taking Banking Services to the Common Man - Financial

Inclusion, Reserve Bank of India Bulletin. Retrieved from:

http://rbidocs.rbi.org.in/rdocs/ Bulletin

Arenaza, (2019), Financial Innovation and Poverty Reduction: Evidence from Rural

Northern Nigeria. MFW4A Working Paper No. 1. African Development Bank

World Bank. (2015). Innovative Digital Payment Mechanisms Supporting Financial