THE EFFECT OF CORPORATE GOVERNANCE ON WORKING CAPITAL...

69

THE EFFECT OF CORPORATE GOVERNANCE ON WORKING CAPITAL OF MANUFACTURING FIRMS LISTED AT THE NAIROBI SECURITIES EXCHANGE HENRY KURUGA KARANI A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF MASTERS DEGREE IN BUSINESS ADMINISTRATION (MBA), UNIVERSITY OF NAIROBI OCTOBER, 2013

Transcript of THE EFFECT OF CORPORATE GOVERNANCE ON WORKING CAPITAL...

THE EFFECT OF CORPORATE GOVERNANCE ON WORKING

CAPITAL OF MANUFACTURING FIRMS LISTED AT THE NAIROBI

SECURITIES EXCHANGE

HENRY KURUGA KARANI

A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF

THE REQUIREMENTS FOR THE AWARD OF MASTERS DEGREE IN

BUSINESS ADMINISTRATION (MBA), UNIVERSITY OF NAIROBI

OCTOBER, 2013

ii

DECLARATION

I declare that this is my original work and has not been presented for a degree in any other university.

Signature …………………………………….. Date ……………………………

H. Karani D61/63370/2011

SUPERVISOR

This project has been submitted for examination with my approval as the University Supervisor:

Signature …………………………………….. Date …………………………….

Mr C. Iraya

Lecturer, Department of Finance and Accounting, University of Nairobi

iii

ACKNOWLEDGEMENTS

My special and sincere thanks go to my Wife Carolyne and my son Lemuel who gave me the

moral support and had to sacrifice a lot to enable me complete this research project. I cannot

forget to thank my supervisor Mr. Cyrus Iraya and moderator Mrs. Nyamute, for their guidance,

support, suggestions, useful comments and constructive critique which were all instrumental to

the successful completion of this research project.

I also wish to appreciate the support and encouragement from my friends during the tough time

that I had to balance between the demands of a rigorous academic program and an equally

demanding work environment. My gratitude to God Almighty who renewed my strength at every

Single stage of this study.

God bless you all.

iv

DEDICATION

This research project is dedicated to my family for their inspiration, encouragement,

understanding and prayers towards the successful completion of this course. I also would wish to

thank the Almighty God who has given me the wisdom and knowledge to undertake this course.

v

ABSTRACT

Effective corporate governance practices in an organization ensure that its resources are managed

in a manner that will lead to a better performance. The management of working capital is such a

resource that effective corporate governance has an effect since when a business does not

manage its liquidity well; it will have cash shortages and as a result experience problems paying

its obligations when they fall due. Towards this end, the research sought to examine the effect of

corporate governance on the working capital management efficiency of manufacturing firms

listed at the Nairobi securities exchange.

This study adopted a co-relational research design. The firms that were analyzed after the

screening process finally became 15 of which their financial statements for the period 2008-2012

were studied. A regression model was determined to establish the relationship between various

working capital parameters and the corporate governance practices. The control variables that

were used included the firm size and sales growth.

The results of the study show that adoption of corporate governance practices plays an important

role in improving the efficiency of working capital management. By the study adopting a co-

relational design and not necessarily a causal relationship between the two, this finding may only

be generalized to firms similar to those that were included in this research. This study contributes

to the literature on the factors that improve the efficiency of working capital management, and in

particular on the association between several features of corporate governance and the efficiency

of working capital management. The findings may be useful for financial managers, investors,

financial management consultants, and other stakeholders.

vi

TABLE OF CONTENT

DECLARATION ............................................................................................................................ ii

ABSTRACT .................................................................................................................................... v

LIST OF TABLES……………………………………………………………………………………………………………………………….ix

LIST OF ABBREVIATIONS ......................................................................................................... x

CHAPTER ONE:INTRODUCTION .......................................................................................... 1

1.1 Background of the Study .......................................................................................................... 1

1.1.1 Corporate Governance .................................................................................................... 2

1.1.2 Working capital Management ........................................................................................ 3

1.1.3 Relationship between Corporate Governance and Working Capital Management ........ 4

1.1.4 Manufacturing Industry in Kenya................................................................................... 5

1.2 Research Problem ..................................................................................................................... 7

1.3 Research Objective ................................................................................................................... 9

1.4 Value of the Study……………………………………………………………………………….………………………………………..10

CHAPTER TWO: LITERATURE REVIEW .......................................................................... 12

2.1 Introduction ............................................................................................................................. 12

2.2 Theoretical Framework ........................................................................................................... 12

2.2.1 Matching Approach ...................................................................................................... 12

2.2.2 Aggressive Approach ................................................................................................... 13

2.2.3 Conservative Approach ................................................................................................ 15

vii

2.3 Empirical Review.................................................................................................................... 17

2.4 Summary of Literature Review ............................................................................................... 20

CHAPTER THREE: RESEARCH METHODOLOGY ......................................................... 23

3.1 Introduction ............................................................................................................................. 23

3.2 Research Design...................................................................................................................... 23

3.3 Population of the Study ........................................................................................................... 23

3.4 Data Collection ....................................................................................................................... 24

3.5 Data Analysis .......................................................................................................................... 24

CHAPTER FOUR:DATA ANALYSIS, RESULTS AND DISCUSSION ............................. 27

4.1 Introduction ............................................................................................................................. 27

4.2 Descriptive Statistics ............................................................................................................... 27

4.3 Inferential Analysis ................................................................................................................. 30

4.4.1 Corporate governance and accounts receivable management efficiency ..................... 30

4.4.2 Corporate Governance and Inventory Management ..................................................... 32

4.4.3 Corporate governance and accounts payable management .......................................... 35

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS….……38

5.1 Introduction…......……………………………………….......……………………………….38

5.2 Summary………………………...……………………..…………………………………….38

5.3 Conclusions and Recommendations…………………………......…………………………..39

viii

5.4 Limitation of the study……………….………………………………………………………40

5.5 Suggestions for further research…………………………………………………….……….41

REFERENCES..............................................................................................................................42

APPENDICES..........................................................................................................................................49

APPENDIX 1: MANUFACTURING FIRMS LISTED AT THE NSE ...................................... 49

APPENDIX II: CORRELATION…..………………………………………..…………………51

APPENDIX III: SOURCE DATA………..……………….……………………………………….…………………..54

ix

LIST OF TABLES

Table 4.1: Descriptive statistics of independent, dependent, and control variables ..................... 27

Table 4.2: Corporate governance and accounts receivable management ..................................... 31

Table 4.3: Model Summary for Account receivable with corporate governance ......................... 32

Table 4.4: Corporate Governance and Inventory Management .................................................... 34

Table 4.5: Model Summary for INV with Control Variables ....................................................... 34

Table 4.6: Corporate Governance and accounts payable Management ........................................ 36

Table 4.7: Model Summary for accounts payable with Control Variables................................... 36

x

LIST OF ABBREVIATIONS

AGOA: African Growth and Opportunity Act

CEO: Chief Executive Officer

COMESA: Common Market for Eastern and Southern Africa

EAC: East African Community

GDP: Gross Domestic Product

KAM: Kenya Association of Manufacturers.

NSE: Nairobi Securities Exchange

R & D: Research and Development

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

Within the context of globalization, almost all organizations around the world are currently

undergoing significant changes. One of the major dimensions of these changes within these

organizations is corporate governance. Corporate governance has indeed become the focus of

increased attention of not only directors, investors and stakeholders, but also regulators, who are

all watching more, and more carefully whether organizations are ―governed‖ efficiently,

effectively and ethically (Ganesan, 2007). In particular, corporate governance scholars have

come to the conclusion that companies across the world need to adopt commonly accepted

corporate governance standards to be able to attract foreign capital, to become internationally

more competitive and to deal with corporate governance problems in today‘s economy.

The observance of corporate governance tenets by a firm is believed to bring about different

types of benefits to a firm. Solomon et al. (2003) emphasize the importance of good corporate

governance and claim that corporate governance involves a set of relationships between a

company‘s management, its board, its shareholders and other stakeholders, with increasingly

accepted ―good‖ corporate governance practices. They point that by adopting good corporate

governance principles, co-operation will continue to play a crucial role in our economies with

high economic efficiency, our personal savings will be well managed with investor confidence

and our pensions will be secured with monitored performance. In much more economic terms,

Pistor (2006) and Meharey (2006) define good corporate governance as an economic function of

2

the firm, which knows how to maximize its residuals. What they mean by the firm‘s residuals is

wealth generation by the firm through real operations and distribution of wealth to shareholders

on a pro rata basis in the case of investor-owned firms. In contrast, bad corporate governance is

just the failure of a firm to meet one or both of these conditions. According to Fox and Heller,

(2006), managers should operate their firms in order to meet these good corporate governance

conditions (wealth generation by real operations and distribution of the wealth to shareholders)

that entirely depend on the structure of constraints and incentives in which they operate, and a

structure that depends on the prevailing legal system.

1.1.1 Corporate Governance

A number of definitions have been given to corporate governance. Mayer (1997) assert that

corporate governance is concerned with ways of bringing the interests of (investors and

managers) into line and ensuring that firms are run for the benefit of investors. It therefore

follows that corporate governance is concerned with the relationship between the internal

governance mechanisms of corporations and society‘s conception of the scope of corporate

accountability (Deakin and Hughes, 2007). It has also been defined by, Keasey et al. (2005) to

include ‗‗the structures, processes, cultures and systems that engender the successful operation of

the organizations‘‘. Corporate governance is also seen as the whole set of measures taken within

the social entity that is an enterprise to favour the economic agents to take part in the productive

process, in order to generate some organizational surplus, and to set up a fair distribution

between the partners, taking into consideration what they have brought to the organization

(Maati, 1999).

3

In the literature, Solomon et al. (2003) emphasize the importance of good corporate governance

and claim that corporate governance involves a set of relationships between a company‘s

management, its board, its shareholders and other stakeholders, with increasingly accepted

―good‖ corporate governance practices. By adopting good corporate governance principles, co-

operation will continue to play a crucial role in our economies with high economic efficiency,

our personal savings will be well managed with investor confidence and our pensions will be

secured with monitored performance.

1.1.2 Working capital Management

Working capital management involves planning and controlling current assets and current

liabilities in a manner that eliminates the risk of the inability of firm to pay its short term

obligations when they fall due and to avoid the excessive investment in these assets on the other

hand (Eljelly, 2004). This is because too much working capital reduces risk and return, while too

little working capital increases risk and return. Managers spend considerable time on day to day

problems that involve working capital decisions (Rehaman & Nasr, 2007). This is because

current assets are short term investment that is continually being converted to other forms of

assets. With regard to current liabilities, a firm is responsible to paying these debts on timely

basis. Taken together, decisions on current assets and liabilities become frequent, repetitive and

time consuming (Appuhami, 2008). Working capital management involves the decision on the

amount of current assets and the financing of these assets. Current assets involve those classes of

assets that can be converted to cash easily and normally within a period of one year and such

temporary investment that can be converted to cash upon need (Rehaman & Nasr, 2007).

4

Management of working capital is essential for most firms. The management of working capital,

in the context of this study, refers to the management of current assets and of current liabilities.

Working capital components include receivables, inventory, payables, and using cash efficiently

for day-to-day operations. The optimization of working capital balances helps minimize working

capital requirements, which in turn, increase firms‘ free cash flow (Ganesan, 2007). Inefficient

working capital management policy, induced by poor corporate governance, has a negative

impact on shareholders‘ wealth. Effective corporate governance serves as a check on the

management of the firm‘s resources, including working capital.

1.1.3 Relationship between Corporate Governance and Working Capital Management

Corporate governance plays an important role in controlling the management of working capital

by formulating sound policies. The role of CEO duality, board size, and audit committee in

working capital management cannot be ignored since the CEO duality and board size help in

maintaining an appropriate level of working capital in the organization (Gill and Shah, 2012).

CEO tenure also helps in improving working capital management. The dual-responsibility, CEOs

serve the interests of the management team and one way to protect the team‘s position is to hold

excessive corporate liquidity. In addition, the CEO together with the board of directors

formulates policies, including policy related to working capital management.Audit committee

represents another internal governance mechanism whose impact is to improve the quality of

financial management of a company and therefore encouraging the firm not to take unnecessary

risk in maintenance of their working capital level (Kyereboah-Coleman, 2007). Working capital

management falls under the area of financial management. Kyereboah-Coleman (2007) suggests

that audit committees should have a minimum size of three members to enhance independence.

An independent audit committee enhances the efficiency of working capital by auditing cash

5

accounts, accounts receivable, accounts payable, and inventory accounts, which in turn,

minimizes agency problems and agency costs. According to Yermack (1996) and Lipton and

Lorsch (1992), a small board of directors is more effective in the decision-making process than a

larger board of directors and the small board sizes should be encouraged to promote effective

communication and decision-making.

Inadequate policies regarding accounts receivable, accounts payable, and inventory management

have a negative impact on the cash conversion cycle. The policy to maintain high cash balances

may reflect management‘s own risk aversion and that may cause an agency problem because the

board of directors and the CEO may maintain balances that do not maximize shareholders‘

wealth (Gill and Shah, 2012). By managing working capital effectively, shareholders can get

maximum return on their invested capital. Weak corporate governance might have adverse

consequences for cash management, accounts receivable, inventory, accounts payable, and cash

conversion. In light of these considerations, the purpose of this study is to empirically document

the Effect of corporate governance on working capital management.

1.1.4 Manufacturing Industry in Kenya

Kenya manufacturing sector is the fourth biggest sector after agriculture, transport and

communication, and wholesale and retail trade. The sector, which is dominated by subsidiaries of

multi-national corporations, contributed approximately 18% of the Gross Domestic Product

(GDP) in 2012. Improved power supply, increased supply of agricultural products for agro

processing, favorable tax reforms and tax incentives, more vigorous export promotion and liberal

trade incentives to take advantage of the expanded market outlets through AGOA, COMESA and

6

East African Community (EAC) arrangements, have all resulted in a modest expansion in the

sector of 1.5 per cent in 2008 as compared to 1.2 per cent in 2007.

Although initially developed under the import substitution policy, Kenya‘s manufacturing sector

is now export based in line with the country‘s policy of emerging as a mid-sized economy in the

year 2030. The sector is loosely classified into 12 sub-categories based on the raw materials the

companies import and or the products they manufacture. The individual firm members are

organized under the membership of Kenya Association of Manufacturers (KAM) to give them a

platform for negotiating common position with the relevant government authorities.

Challenges facing the sector include shrinking demands for locally manufactured goods due to

rising poverty levels and reduced exports resulting from general economic slump after the recent

global recession. In addition, the high cost of inputs resulting from poor infrastructure has led to

high prices for final products leading to under-utilization of capacity. The erratic and high cost of

energy has also had a negative impact. Other challenges include security issues, arbitrary

charges levied by regulatory and local authorities and high cost of securing financial facilities

from the banks. However opportunity for growth exists with the rollout of common tariff under

the newly integrated EAC custom union, because Kenya‘s manufacturing sector is the largest in

the region. As at the end of 2012, there were Seventeen (17) manufacturing firms listed in the

Nairobi Securities Exchange with the price movement of 5 of them being used to determine the

daily average NSE index.

7

1.2 Research Problem

Corporate governance is seen as the process and structure used to direct and manage the business

affairs of the company towards enhancing business prosperity and corporate accountability with

the ultimate objective of realizing long-term shareholder value, whilst taking into account the

interest of other stakeholders. Claessens et al. (2002) maintain that better corporate frameworks

benefit firms through greater access to financing, lower cost of capital, better performance and

more favourable treatment of all stakeholders. Effective corporate governance practices in an

organization ensure also that its resources are managed in a manner that will lead to a better

performance. The management of working capital is such a resource that effective corporate

governance has an effect. When a business does not manage its liquidity well, it will have cash

shortages and as a result experience problems paying its obligations when they fall due. Indeed,

working capital starvation has generally been credited as a major cause, if not the main cause of

small business failure in many developed and developing countries (Rafuse, 2006). The

importance of an effective management of working capital is further necessitated by the present

unpredictable business environment.

Inefficient working capital management policy, induced by poor corporate governance, has a

negative impact on shareholders‘ wealth. Effective corporate governance serves as a check on

the management of the firm‘s resources. Although accounts receivable, inventory, and accounts

payable are important parts of working capital management, cash is one of the most vulnerable to

wanton behavior by management (Isshaq et al. 2009).For Borsch-Supan and Koke (2002),

understanding corporate governance is important not only because eliminating these agency

costs potentially increases productivity at firm level, but because macro level policy decisions

8

also boost economic growth, since policy makers are now more aware of the good corporate

governance.

The Kenyan manufacturing sector is considered as one of the key segments of the economy.

According to the Kenya Association of Manufacturers (KAM), the manufacturing sector

employs more than 1.5 million employees. In addition, the Kenyan vision 2030 blue print

identifies as one of the key pillars of the attainment of the objectives of the strategy the need for

the manufacturing sector to grow at the rate of 10% over a period of 20 years. This can only be

achieved if there is growth in the profits of the sector and this will be dependent upon the

management identifying all the variables that can influence profits of a firm including the

observance of good corporate governance. The board of directors and the CEO are responsible

for formulating policies regarding cash management, accounts receivable, inventory purchases

and maintenance, accounts payable, and all other policies in the organization. By managing

working capital effectively, shareholders can get maximum return on their invested capital.

Weak corporate governance therefore, might have adverse consequencesfor cash management,

accounts receivable, inventory, accounts payable, and cash conversion. There is need therefore to

establish the effect that corporate governance will have in the management of working capital.

There is enormous amount of research studies on corporate governance code and rules existing in

various countries. Research findings documented greater investor protection through strict

corporate governance provisions (La Porta et al. 2008). Gompers et al. (2003) developed a

corporate governance index for the US firms and found that the index is highly correlated with

better operating performance and higher market valuation. Drobetz and Gru¨ninger (2007) tested

9

the relationships between board size, CEO duality, and cashholdings by collecting data from

Switzerland. Gill and Mathur (2011) and Gill and Shah (2012) investigated the impact of CEO

duality and board size on cash holdings and corporate liquidity by collecting data from Canadian

firms.

In Kenya, Nganga (2009) studied the relationship between working capital and profitability of

listed companies at the NSE. The study found out that managers can create value if they adopt a

conservative approach towards working capital investment and working capital financing

policies. It was also found out that investors have a positive opinion on those firms that adopt an

aggressive approach to managing their short-term liabilities. Muthuva (2010) pointed that

effective management of working capital in a firm should aim at ensuring that the firm has the

ability to continue operating with sufficient cash flow for payment of both maturing short-term

debt and impending operational expenses. This process will require further that cash collection

from customers is made in time so that the firm has no difficulty in paying its current liabilities.

Therefore in the issue of corporate governance and its relationship with firms performance has

been investigated in depth as well as working capital. However, the effect of corporate

governance in the management of working capital in Kenya has not been investigated. This gap

therefore lead to the following research question: what is the effect of corporate governance on

the working capital of manufacturing firms listed at the Nairobi Securities Exchange?

1.3 Research Objective

To establish the effect of corporate governance on working capital of manufacturing firms listed

at the Nairobi Securities Exchange.

10

1.4 Value of the Study

The understanding of the effect that corporate governance has on working capital management is

of help to policy makers – governments and other stakeholders – to design targeted policies and

programs that will actively stimulate the growth and sustainability of the manufacturing firms in

the country, as well as helping those policy makers to support, encourage, and promote the

establishment of these firms. Regulatory bodies such as KAM, Capital Markets Authority and

the Kenya Revenue Authority can use the study findings to improve on the framework for

regulation.

The study findings are of benefit to management and staff of manufacturing firms who can gain

insight into how their institutions can effectively manage their working capital. This study offers

an understanding on the importance of maintaining an optimal working capital and postulating

the relationship that exist between the existing level of working capital and the profit level.

Several policies on the management of working capital that various manufacturing firms can

adopt are also addressed. This is because manufacturing firms need to adapt to the changing

needs of the current business set up and requirement of various suppliers and providers of

services. As a result, manufacturing firms in the country and other affiliated firms can derive

great benefit from the study.

This study creates a monograph which could be replicated in other sectors of the economy. Most

importantly, this research contributes to the literature on the relationship between working

capital management and profitability. It is hoped that the findings are valuable to the

academicians, who may find useful research gaps that may stimulate interest in further research

in future. Recommendations have been made on possible areas of future studies. This study is

11

further justified since it is of value to those interested in setting up manufacturing firms in the

country since they are be able to understand what to do right to succeed and what if done wrong

would bring the business down.

12

CHAPTER TWO: LITERATURE REVIEW

2.1 Introduction

This chapter reviews literature relating to corporate governance and a firms working capital

management. The literature review has been organized in the following sections. First section

covers the theories underlying the study, corporate governance and firm‘s working capital. The

second section covers the empirical studies on the subject area covered and summary of the

section.

2.2 Theoretical Framework

Firms usually come to the conclusion that there is a need for an appropriate mixture of debt finance with

regard to the length of time to maturity; some short term borrowing is desirable alongside some long-term

borrowing (Brigham and Ehrhardt, 2004). This is because there is always a minimum level of current

assets which is continuously required by a firm to carry on its business operations. This forms the

permanent or fixed working capital. The extra working capital needed to support the changing production

and sales activities is the variable or temporary working capital. Both are necessary to facilitate

production and sales through the operating cycle. The major factors to be considered in achieving the

right balance between the permanent and variable working capital include cost (interest rate, arrangement

fee etc.) and risk of not being able to renew borrowings, of the yield curve shifting or not being able to

meet sudden outflow if the maturity is bunched (Weinraub and Visscher, 1998).

2.2.1 Matching Approach

According to Gitman (2005), some firms follow the matching principle, in which the maturity

structure of finance matches the maturity period of the project or asset. Here, the fixed assets and

current assets which are needed on permanent basis are financed through long term sources,

while current assets whose financing needs vary throughout the year are financed by short term

13

borrowings. A firm that is taking the maturity approach is considered to be adopting a moderate

stance. Under such an approach, a rising level of total assets is financed principally through

increases in long-term finance applied to fixed assets and permanent current assets. The

fluctuating current assets such as those related to seasonal variations are financed with short-term

funds (Gitman, 2005).

The theory implies that excessive cash in corporate accounts is not necessarily in favor of the

firm.Unnecessary cash may be built up because of poor corporate governance. Tradeoff theory,

pecking order theory, and free cash flow theory usually explain the pattern of cash holdings.

Firms, according to tradeoff theory and by extension the matching approach, set their optimal

level of cashholdings by weighting the marginal costs and marginal benefits of holding cash

(Afza and Adnan, 2007). The benefits of cash holding are reduction in the likelihood of financial

distress; allowing the pursuance of investment policy when financial constraints are met; and

minimization of the costs of raising external funds or liquidating existing assets (Ferreira and

Vilela, 2004). According to Afza and Adnan (2007), maintaining an appropriate level of liquidity

within the organization is fundamental for smooth operations of a firm. The level of cash a firm

maintains is characterized by its policies regarding working capital requirements, cash flow

management, dividend payments, investment, and asset management.

2.2.2 Aggressive Approach

This approach is considered more risky because of the frequent need to refinance to support

permanent current assets as well as fluctuating current assets. Moyer et al. (2005) observe that if

a firm relied on overdraft for this, it will be vulnerable to a rapid withdrawal of that facility and if

stocks and cash are reduced to pay back the overdraft the firm may experience severe

14

disruptions, loss of sales and output, and additional costs because of a failure to maintain the

minimum required working capital to sustain optimum profitability. Thus, Bringham and

Ehrhardt (2004) posit that this working capital policy will be associated with higher return and

risk.

Audit committee represents another internal governance mechanism whose impactis to improve

the quality of financial management of a company and therefore encouraging the firm not to take

unnecessary risk in maintenance of their working capital level (Kyereboah-Coleman, 2007).

Working capital management falls under the area of financial management. Kyereboah-Coleman

(2007) suggests that audit committees should have a minimum size of three members to enhance

independence. An independent audit committee enhances the efficiency of working capital by

auditing cash accounts, accounts receivable, accounts payable, and inventory accounts, which in

turn, minimizes agency problems and agency costs.

According to Smith (1980), a firm may adopt an aggressive working capital management policy

with a low level of current assets as a percentage of total assets, or it may also be used for the

financing decisions of the firm in the form of high level of current liabilities as a percentage of

total liabilities. Working capital management is important because of its effects on the firms‘

profitability and risk, and consequently its value (Smith, 1980). The greater the investment in

current assets, the lower the risk, but also the lower the profitability obtained. However, contrary

to this, Carpenter and Johnson (1983) provided empirical evidence that there is no linear

relationship between the level of current assets and revenue systematic risk of the US firms;

however, some indications of a possible nonlinear relationship were found, which were not

highly statistically significant.

15

According to Jensen (1993), a lack of independent leadership creates difficulty forboards to

respond to failure in top management. He argues thatconcentration of decision management and

decision control in one individual hindersboards‘ effectiveness in monitoring top management.

However, when a CEO doubles as board chair, it affords the CEO the opportunity to carry out

decisions and projectswithout undue influence of bureaucratic structures (Kyereboah-Coleman,

2007).

2.2.3 Conservative Approach

Under the conservative approach, the firm finances its permanent assets and also a part of

temporary current assets with long term financing. When there are times in the course of the year

when surplus cash is available, this will be invested in short-term instruments. Most of the

managers feel much happier under the conservative approach because of the lower risk of being

unable to pay bills as they arise. The low-risk is to make sure that long term financing covers the

total investment of the assets. However, such a policy may not be to the best interest of the

owners of the firm. The short term funds invested in the short term securities is unlikely to earn

satisfactory return relative to the cost of the long term funds. In all likelihood, shareholders

would be better off if the firm reduced its long term financing, by returning cash to shareholders

or paying off some long term loans.

The holding and increasing of net working capital tie up money used for financing net working

capital. If net working capital increases, the firm must utilize and tie up more money, and this

decreases free cash flows. Production level growth necessitates increased levels of cash,

inventories, and accounts receivable (Michalski, 2008).Although having some cousin of cash and

inventory help firms‘ smoothing operations,building unnecessary working capital backfires.

16

Paying accounts payable after the duedate also hurts the firm because of the penalty charged by

suppliers. Building unnecessary working capital is also not in favor of the firm because it has a

negative impact on shareholders‘ wealth. Therefore, an optimal working capital management

policy is necessary for the firm.Corporate governance plays an important role in controlling the

management ofworking capital by formulating sound policies. The role of CEO duality, board

size, and audit committee in working capital management cannot be ignored. CEO duality and

board size help in maintaining an appropriate level of working capital in the organization (Gill

and Shah, 2012).

VanHorne and Wachowicz (2004) further observe that excessive levels of current assets as

advocated by the conservative working capital may have a negative effect on the firm‘s

profitability, whereas a low level of current assets may lead to a lower level of liquidity and

stock-outs, resulting in difficulties in maintaining smooth operations. More aggressive working

capital policies are associated with higher return and risk, while conservative working capital

policies are associated with lower risk and return (Weinraub and Visscher, 1998).

By managing working capital effectively, shareholders can get maximum return ontheir invested

capital. Weak corporate governance might have adverse consequences for cash management

(Harford et al. 2008), accounts receivable, inventory, accounts payable, and cash conversion. In

light of these considerations, the purpose of this study is to empirically document the impact of

corporate governance on working capital management efficiency.

17

2.3 Empirical Review

According to Jensen (1993), a lack of independent leadership creates difficulty for boards to

respond to failure in top management. He argues that concentration of decision management and

decision control in one individual hinders boards‘ effectiveness in monitoring top management.

However, when a CEO doubles as board chair, it affords the CEO the opportunity to carry out

decisions and projects without undue influence of bureaucratic structures (Kyereboah-Coleman,

2007). Therefore, CEO duality can improve the efficiency of working capital. Dittmar et al.

(2003) collected a sample of more than 11,000 firms from 45 countries and found that

corporations in countries where shareholders‘ rights are not well protected hold up to twice as

much cash as corporations in countries with good shareholder protection. They also found that

when shareholder protection is poor, factors that generally drive the need for cash holdings, such

as investment opportunities and asymmetric information, actually become less important. In

addition, the study found that firms hold larger cash balances when access to funds is easier.

Dittmar et al. (2007) explain that agency problems are important determinants of corporate cash

holdings. Therefore, strong corporate governance is necessary. They sampled 297 French firms

over the period 1998-2002 using tradeoff theory and pecking order theory. The author found that

growth companies hold higher cash levels than mature companies. Drobetz and Gru¨ninger

(2007) investigated the determinants of cash holdings for a comprehensive sample of 156 Swiss

non-financial firms between 1995 and 2004. They found a positive relationship between: CEO

duality and corporate cash holdings; and a non-significant relationship between board size and

corporate cash holdings. That is, CEO duality leads to significantly higher cash holdings and

larger board size has no impact on corporate cash holdings.

18

Narware (2004) in his empirical study on Indian National Fertilizer Limited, for 1990-91 to

1999-2000 signify that working capital management and profitability of the company disclosed

both negative and positive association. He also found evidence that increase in the profitability

of a company was less than the proportion to decrease in working capital. However, the study

done by Raheman and Nasr, (2007) on a sample of 94 Pakistani firms listed on Karachi Stock

Exchange for a period of 6 years from 1999 – 2004, demonstrate a strong negative relationship

exists between variables of the working capital management represented by liquidity and debt

with profitability of the firm.

Kuan et al. (2011) examined the association between corporate governance and cash policy of

family-controlled firms. The authors found that the impact of corporate governance, with its

separation of control rights and cash flow rights, director-ownership-in-pledge ratio and

proportion of independent directors on cash policy, differs between family-controlled and non-

family-controlled firms. The authors also found that the separation of seat control rights and cash

flow rights, as well as chair duality, significantly affects the cash policy within different levels of

cash holdings in firms.

According to Padachi (2006), high investment in inventories and receivables is associated with

lower profitability. He used return on total assets as a measure of profitability for a sample of 58

small manufacturing firms in Mauritius for the period 1998–2003. His findings reveal an

increasing trend in the short-term component of working capital financing. Similar to most recent

study by Christopher and Kamalavalli, (2009) which focus on 14 corporate hospitals in India for

19

the period 1996-97 to 2005-06. Their correlations and regression analysis signifying that

working capital component namely current ratio, cash turnover ratio, current assets to operating

income and leverage negatively influence profitability.

The holding and increasing of net working capital tie up money used for financing net working

capital. If net working capital increases, the firm must utilize and tie up more money, and this

decreases free cash flows. Production level growth necessitates increased levels of cash,

inventories, and accounts receivable (Michalski, 2008). Although having some cousin of cash

and inventory help firms‘ smoothing operations, building unnecessary working capital backfires.

Paying accounts payable after the due date also hurts the firm because of the penalty charged by

suppliers. Building unnecessary working capital is also not in favor of the firm because it has a

negative impact on shareholders‘ wealth. Therefore, an optimal working capital management

policy is necessary for the firm.

Lau and Block (2012) collected data from Standard and Poor 500 and the Edgar database to

investigate whether the presence of controlling founders and families had significant impact on

the level of cash holdings, and their implications on firm value. The authors found that founder

firms hold a significantly higher level of cash than family firms. In addition, they found a

positive interaction effect between founder management and cash holdings on firm value,

suggesting the presence of founders as managers helps to mitigate the agency costs of cash

holdings. Gill and Mathur (2011) collected data from Canadian service firms from 2009 to 2011

and found that sales growth positively impacts corporate liquidity.

20

On his part, Nazir (2009) analyzed the impact of aggressiveness of working capital investment

and financing policies in Pakistan for a sample of 204 non-financial firms listed at Karachi Stock

Exchange for the period of 1998-2005. They evaluated on firm returns i.e. return on assets and

Tobin‘s Q to represent market performance and indicates that firms adopting an aggressive

approach towards working capital financing policy give more value to the firms while inverse

relationship between the aggressiveness of working capital investment policies on firms

performance exist. These results are consistent with Afza and Nazir (2007) that using Tobin‘s Q

to represent stock market performance of Karachi Securities Exchange. According to Irene and

Lee (2007) who researched on the prevailing working capital management practices of some

well-performed Malaysian public firms listed on Bursa Malaysia, they examined the correlation

between profitability and the level of working capital of the sample firms and found out that

profitability and working capital are linearly related positively to a certain extent.

Gill and Shah (2012) sampled Canadian firms from 2009 to 2011 and found that CEO duality

and board size positively impact corporate cash holdings. The findings also suggest that CEO

duality and board size negatively impact net working capital. Valipour et al. (2012) took a

sample of 83 Iranian firms listed in the Tehran Security Exchange for the period of 2001-2010

and found a negative relationship between sales growth and cash conversion cycle. In summary,

the limited availability of literature review indicates that corporate governance influences the

efficiency of working capital management.

2.4 Summary of Literature Review

The importance of the corporate governance and its effect on management of working capital in

a firm has been expounded in detail both in the literature as well as from the empirical studies

done on the subject area. A firm‘s working capital is found to affect a firm‘s liquidity and

21

profitability and thus the objective of managing working capital is to ascertain that a firm has the

ability to continue operating with sufficient cash flow for payment of both maturing short-term

debt and impending operational expenses. Efficient working capital management involves

planning and controlling the current assets and current liabilities in a manner that eliminates the

risk of inability of a firm to meet due short term obligations and at the same time to avoid

excessive investment in these assets on the other hand. The level of managing the working

capital is affected by the corporate governance practices adopted by a firm.

A review of prior literature reveals that there exists a significant relation between corporate

governance and working capital management of a firm by using different variable selection for

analysis. In addition, it has been found out that different corporate governance practices have

different levels of working capital and they will always strife to maintain the level of working

capital in the short term. The risk behaviour preference of the firms‘ management was also found

to have an effect in the level of current assets and current liabilities that is held by a firm. For

risk averse managers, it was found out that such firms will hold a high proportion of current

assets compared to the current liabilities and vice versa for risk seeking managers. In effect

therefore, the level of risk preference characteristics of firm‘s managers will affect the level of

performance and profitability of the organization.

However, the studies have tended to examine a restricted subset of corporate governance

mechanisms such as director ownership, board size, and board composition. By examining both

internal and external factors, the present research will support Grandmont et al.’s (2004) claim

that financial performance depends on a full and comprehensive examination of corporate

governance practices, which reduces the endogeneity problem evident in some studies. Further,

the data will extend over five years from 2008 to 2006 and this will allow the researcher to

22

investigate dynamic aspects with regard to the changing information impacts of corporate

governance.

23

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction

This chapter sets to explain the research design, the population of interest, the basis of sample

selection, the type of secondary data that was used, the sources of data, the techniques of analysis

to be used and the data analysis. A multivariate model is estimated using the SPSS.

3.2 Research Design

This study employed correlation research design. According to Albright et al. (2011) a

correlation research is a procedure in which subjects‘ score on two variables are simply

measured, without manipulation of any variable, to determine whether there is a relationship.

The study also adopted a cross-sectional study in which data was gathered just once over the

period 2008 to 2012 and as such, a causal study will be undertaken in a non-contrived setting

with no researcher interference. A cross sectional study was used to determine the

interrelationship between the variables under consideration among the different firms in the

study and this will permit the researcher to make statistical inference on the broader population

and generalize the findings to real life situations and thereby increase the external validity of the

study.

3.3 Population of the Study

The population of interest in this research was of composed of all manufacturing firms listed at

the NSE that have operated in Kenya between 2008 and 2012. As of 31st

Dec, 2012, there were

17 listed Manufacturing firms at the NSE with 13 of them in the Main Investment Market

Segment (MIMS) and 4 of them in the alternative investment market segment (AIMS) and this

24

constituted the requisite population (Appendix I). The reason as to why these markets were

chosen is primarily due to the availability and the reliability of the financial statements in that

they are subject to the mandatory audit by internationally recognized audit firms and also listed

firms have an incentive to manage their working capital efficiently and thus increase their share

prices. Most of the firms have their headquarters in Nairobi and its environs and it was

convenient in terms of time and accessibility to the researcher. Since the number of the firms is

limited, then the study was a census survey.

3.4 Data Collection

Data was collected from annual reports submitted to the NSE and Capital Markets Authority. All

the manufacturing firms that had continually operated between 2008 and 2012 were included to

ensure that the sampling frame is current and complete. From the financial statements, the

researcher collected information on level of account receivables, inventory, account payables,

sales, total assets and also establish the cash conversion cycle. From the notes to the accounts,

the CEO tenure and duality, board size and Audit committee composition was established.

3.5 Data Analysis

Multiple regression analysis was applied to the data to examine the effect of the corporate

governance tenets on the working capital management elements in manufacturing firms. The

regression models was run from the financial reports of the firms that had been in operation since

2008 and whose annual reports were available for the periods. The balance sheets, income

statements and their notes was studied to get the data for the variables mentioned in the model.

The regression was adapted from the one used by Gill and Biger (2012) when they did a similar

research on Canadian firms.

25

The equation specifically took the form;

Regression equation (A): AR = βо+ β1TNt+ β2BSt+ β3ACt+ β4FSt + β5GROWt + α

Regression equation (B): INV =βо+ β1TNt+ β2BSt+ β3ACt+ β4FSt + β5GROWt+ α

Regression equation (C): AP =βо+ β1TNt+ β2BSt+ β3ACt+ β4FSt + β5GROWt + α

Dependent Variable Measurement

Accounts receivables (ARt) (Accounts receivables/sales) × 365 days

Accounts Payable (APt) (Accounts payables/cost of goods sold) × 365 days

Inventory (INVt) (Inventory/cost of goods sold) × 365 days

Independent (explanatory) variables

CEO tenure (TNt ) Number of years serving as a CEO

Board size (BS,t ) Number of directors serving on board

Audit committee (AC,t ) Number of audit committee members

26

Control Variables

Sales growth (GROWt ) (Current year sales 2 previous year sales)/previous

year sales

Firm size (FSt ) Log of average assets

27

CHAPTER FOUR

DATA ANALYSIS, RESULTS AND DISCUSSION

4.1 Introduction

This chapter presents the results and findings of the study based on the research objectives. The

results are presented in the form of summary tables. In addition a regression analysis is used to

analyse the data to answer the research objective.

4.2 Descriptive Statistics

Table 4.1 below summarizes the descriptive statistics of the variables included in the regression

models as presented. It represents the variables of the 15 manufacturing firms operating in Kenya

in the financial results years 2008-2012.

Table 4.1: Descriptive statistics of independent, dependent, and control variables

Variable Mean Median SD

AR 0.445 0.414 0.2231

IT 1.235 0.628 0.582

AP 0.567 0.237 0.410

CCC 9.269 5.965 1.724

TN 1.476 .898 0.725

BS 1.667 1.257 0.584

AC 3.785 1.548 0.965

SG 0.345 0.124 0.102

FS 2.876 1.652 0.46

28

Source: Calculations based on Annual reports of firms from 2008-2012

Notes: SD – standard deviation; CD – CEO tenure; BS – board size; AC – audit committee; SG –

firm growth; AR – accounts receivables (in days); IT – inventory holding (in days); AP –

accounts payables (in days); CCC – cash conversion cycle (in days); FS – Firm Size;

The mean value of the account receivable is 44.5% of the working capital and the standard

deviation 22.3%. It means that value of the account receivable can deviate from the mean to

both sides by 22.3 %. The traditional measures of liquidity (cash conversion cycle) for the

manufacturing firms in Kenya is 9.269 with the standard deviation of 1.724.

To check the size of the firm and its relationship with working capital, natural logarithm of total

assets is used as a control variable. The mean value of log of total assets is 1.621917 while the

standard deviation is 1.02345. The cash conversion cycle is used as a proxy to check the

efficiency in managing working capital which influences the firms liquidity level is on average

2.876 while its standard deviation is 0.346.

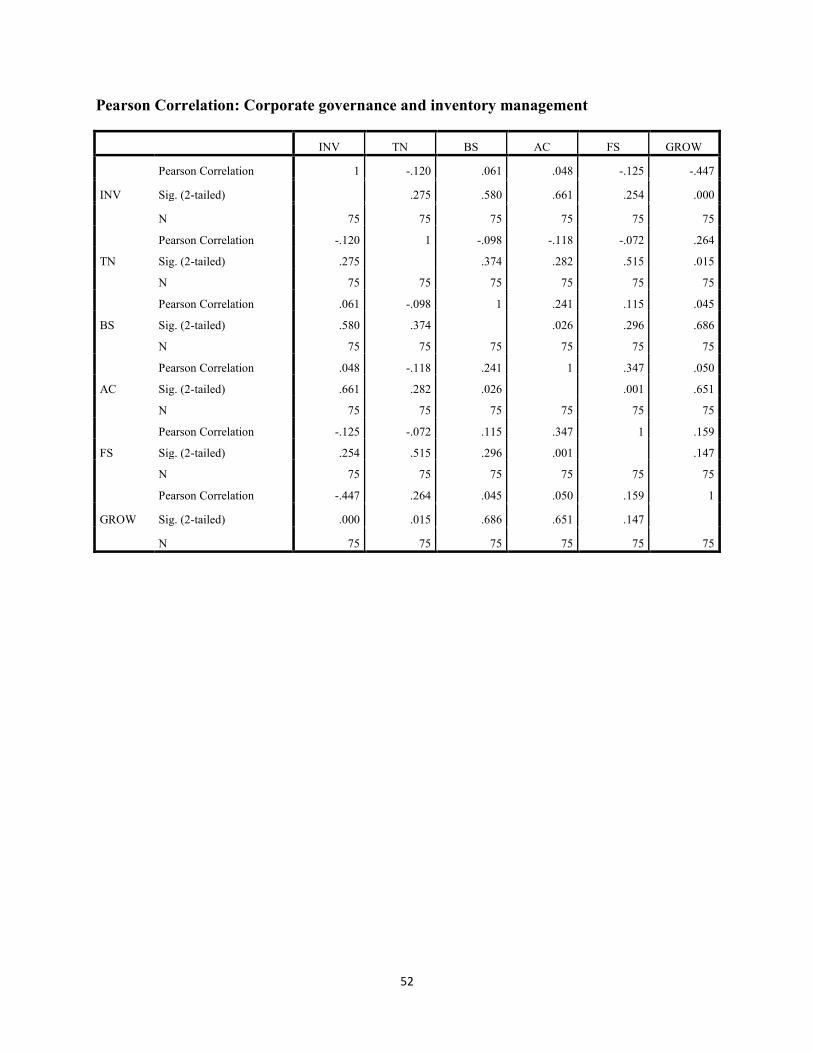

From Appendix II, the bivariate correlation analysis shows that; Accounts receivable

management efficiency is positively correlated with the CEO tenure, audit committee, firm size

and sales growth. The accounts payable management efficiency is positively correlated with the

audit committee while the cash conversion cycle is positively correlated with CEO tenure, and

audit committee. The results also show that inventory management is positively correlated with

CEO tenure, board size and audit committee.

29

The results from the descriptive statistics above show that, generally, observance of corporate

governance tenets such as establishment of the audit committee, constituted of a board that has

the oversight role of the workings of the managers will help in the maintenance of optimal

working capital by a firm. Audit committee represents internal governance mechanism whose

impact is to improve the quality of financial management of a company including the working

capital level. Hence, a firm should consider increasing the role of the audit committee to

determination of optimal working capital. This finding is in line with that of Kyereboah-Coleman

(2007) who argued for a small board size to promote a faster and effective communication and

decision-making. They further pointed that audit committee should have a minimum size of three

members to enhance independent.

An independent audit committee enhances the efficiency of working capital by auditing cash

accounts, accounts receivable, accounts payable, and inventory accounts, which in turn,

minimizes agency problems and agency costs as suggested by Jensen (1993). The CEO tenure

had also a positive correlation with the level of working capital held. This could be because that

when a CEO serves longer in a firm, it serves as an added incentive to promote the interests of

shareholders due essentially to the fact that apart from job security, the CEO is afforded the

opportunity to witness the results of decisions taken. This is the same view that Kyereboah-

Coleman (2007) pointed out though it contradicts the conclusion made by Drobetz and

Gru¨ninger (2007) who found an insignificant relationship between board size and corporate cash

holdings.

30

4.3 Inferential Analysis

For inferential analysis the study used several regression models. These models were used to

identify important variables influencing the dependent variable. The regression analysis is used

to investigate the impact of corporate governance on the working capital position of the firm.

The determinants of working capital were estimated using pooled least squares and general least

squares method with cross section weights.

As pointed out by Raheman and Nasr (2007), when using pooled data and cross sections there

may be a problem of heteroskedasticity (changing variation after short period of time) and to

counter this problem, the general least square with cross section weights approach was adopted.

In the regression, the common intercept was calculated for all variables and assigned a weight.

Further as Gill and Beger (2012) noted, when using multiple regression analysis, there is a

possibility of endogeneity occurring whereby when certain variables are omitted, it leads to

measurement errors. To minimize endogeneity issues, the most important variables that impact

the working capital management efficiency (Account receivable, inventory, cash and account

payables) are used.

4.4.1 Corporate governance and accounts receivable management efficiency

The results show that there exist positive relationships between CEO duality and accounts

receivable; audit committee and accounts receivable and also the firm size and account

receivable. This means that CEO duality and audit committee of the firm improve the efficiency

of accounts receivable management, which in turn, helps reduce working capital requirements.

These results give credence to the findings of Saddour (2006) who found that internationalization

of the CEO and board composition enhances the level of management of the working capital.

31

From Table 4.2 below, the established multiple linear regression equation becomes:

AR = 34.835 + 15.052TN – 5.313 BS + 0.726AC + 9.961FS – 3.487GROW

The coefficient of intercept C has a value (34.835) and is significant. The coefficient of CEO

duality is high and also significant and this means that a unit increase in the CEO duality

increases the efficiency of account receivable management and highly significant at ά. = 5%, and

implies that the increase or decrease in the corporate governance, significantly affects the

efficiency of account receivable management.

Table 4.2: Corporate governance and accounts receivable management

Model Unstandardized

Coefficients

Standardized

Coefficients

t Sig. Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1

(Constant) 34.835 40.878 0.940 0.350

TN 15.052 16.435 0.094 0.916 0.363 0.902 1.109

BS -5.313 5.324 -0.100 -0.998 0.321 0.934 1.071

AC 0.726 8.469 0.009 0.086 0.932 0.833 1.201

FS 9.961 13.902 0.075 0.717 0.476 0.854 1.171

GROW -3.487 0.693 -.516 -5.028 0.000 0.896 1.116

a. Dependent Variable: AR

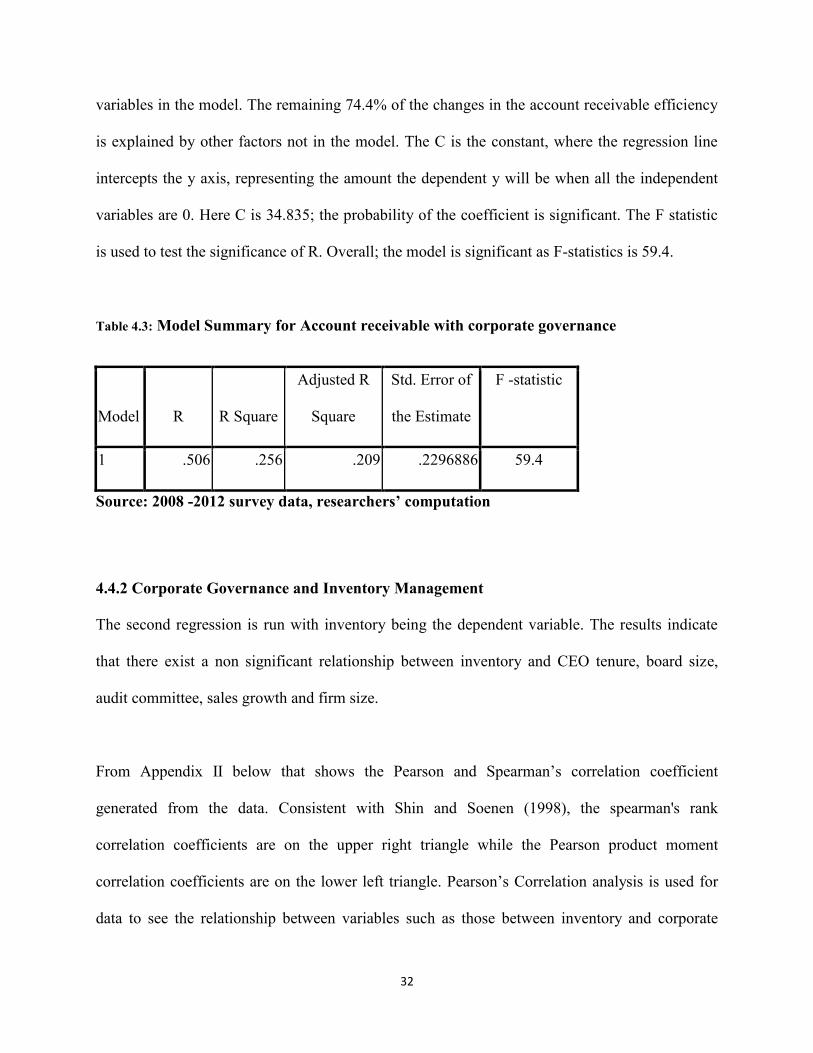

From table 4.3, the adjusted R2, also called the coefficient of multiple determinations, is the

percent of the variance in the dependent explained uniquely or jointly by the independent

variables and is 25.6%. This means that 25.6% of the changes in the account receivable

efficiency will be explained by the changes in the corporate governance variables and control

32

variables in the model. The remaining 74.4% of the changes in the account receivable efficiency

is explained by other factors not in the model. The C is the constant, where the regression line

intercepts the y axis, representing the amount the dependent y will be when all the independent

variables are 0. Here C is 34.835; the probability of the coefficient is significant. The F statistic

is used to test the significance of R. Overall; the model is significant as F-statistics is 59.4.

Table 4.3: Model Summary for Account receivable with corporate governance

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate

F -statistic

1 .506 .256 .209 .2296886 59.4

Source: 2008 -2012 survey data, researchers’ computation

4.4.2 Corporate Governance and Inventory Management

The second regression is run with inventory being the dependent variable. The results indicate

that there exist a non significant relationship between inventory and CEO tenure, board size,

audit committee, sales growth and firm size.

From Appendix II below that shows the Pearson and Spearman‘s correlation coefficient

generated from the data. Consistent with Shin and Soenen (1998), the spearman's rank

correlation coefficients are on the upper right triangle while the Pearson product moment

correlation coefficients are on the lower left triangle. Pearson‘s Correlation analysis is used for

data to see the relationship between variables such as those between inventory and corporate

33

governance tenets. If the presence and practice of different corporate governance principles leads

to an efficient management of inventory, then one should expect a positive relationship. There is

a negative relationship between efficient management of inventory and the measures of corporate

governance specifically CEO tenure, firm size and sales growth of the firm. However, there

exists a positive relationship between size of the board and audit committee. This result will be

consistent with the results of Gill and Shah who found that CEO duality and board size positively

impact corporate cash holdings and also that CEO duality and board size negatively impact net

working capital.

The effect of corporate governance on efficient management of inventory is investigated for all

75 firm-year observations. From Table 4.4 below, the established multiple linear regression

equation becomes:

INV = 223.325 + 1.769TN +5.924BS + 10.772AC - 19.292FS – 4.689GROW

The coefficient of intercept C has a value (223.325) and is significant. The CEO tenure, Board

size and audit committee improve the efficiency of inventory management. This means that an

organization should endeavor to set up an audit committee such that the more the board size and

consequently the audit committee size the better managed the inventory of the firm. It is further

interpreted however that if the firm size increases or the growth increases, the level of inventory

management efficiency declines. This finding however is puzzling as it contradicts that made by

Gill and Biger (2012) found on American Manufacturing firms.

34

Table 4.4: Corporate Governance and Inventory Management

Model Unstandardized

Coefficients

Standardized

Coefficients

t Sig. Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1

(Constant) 223.325 162.642 1.373 0.174

TN 1.769 26.498 0.007 0.067 0.947 0.902 1.109

BS 5.924 8.583 0.071 0.690 0.492 0.934 1.071

AC 10.772 13.654 0.086 0.789 0.433 0.833 1.201

FS -19.292 22.413 -0.093 -0.861 0.392 0.854 1.171

GROW -4.689 1.118 -0.441 -4.194 0.000 0.896 1.116

With an R2 of 13.2% is low and this model explains only 13.2% of the variability in the

independent variables

Table 4.5: Model Summary for INV with Control Variables

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate F -statistic

1 .465 .216 .186 .1568003 31.603

Source: 2008 -2012 survey data, researchers’ computation

The adjusted R2, also called the coefficient of multiple determinations, is the percent of the

variance in the dependent explained uniquely or jointly by the independent variables and is

35

21.6%. The C is the constant, where the regression line intercepts the y axis, representing the

amount the inventory when all the independent variables are 0. The F-statistic also reflects the

highly significance of the model as its value is 31.603.

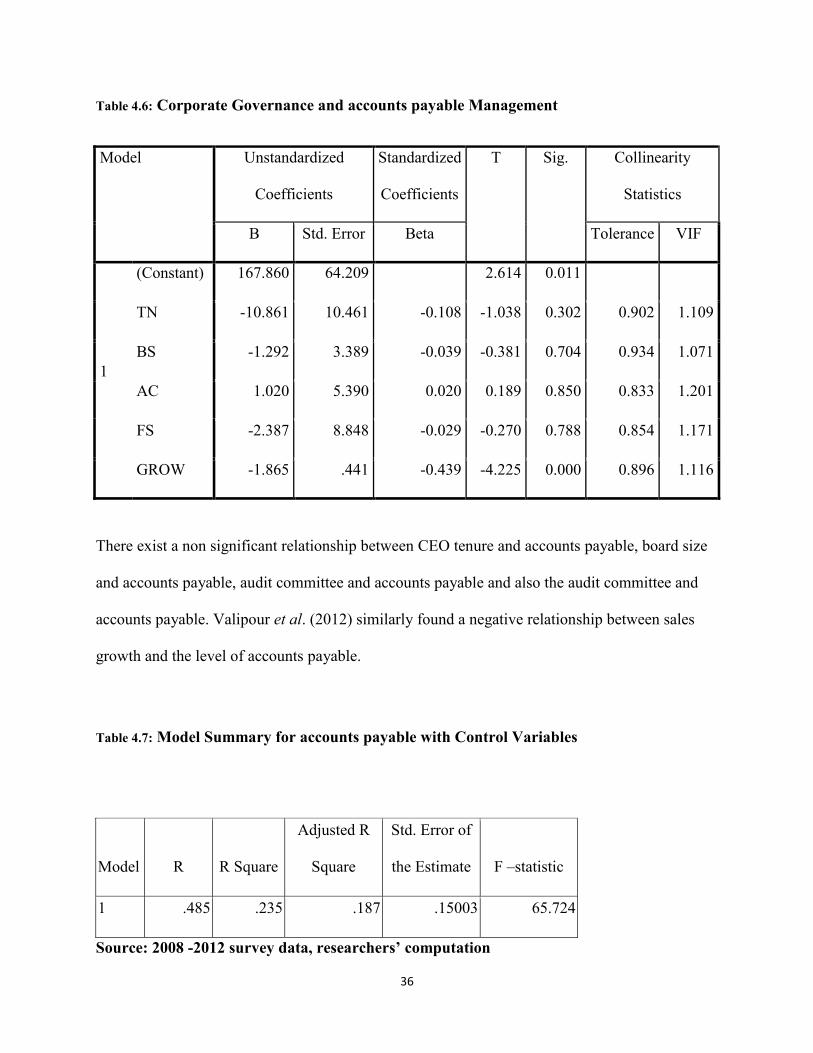

4.4.3 Corporate governance and accounts payable management

The third regression is run with accounts payable being the dependent variable. The results from

table 4.6 indicate that there exist a positive relationship between accounts payable and audit

committee only. Otherwise a negative relationship exists between CEO tenure, board size, firm

size and the growth of the firm. This result shows that as the corporate governance practices are

implemented by a firm, the level of accounts payable of the firm is minimized. This is a positive

result since the intentions of the firm is not to increase the level of accounts receivable to sub

optimal level since it is going to lead to the erosion of the firm credit rating.

From Table 4.6 below, the established multiple linear regression equation becomes:

INV = 167.860 – 10.861TN - 1.292BS + 1.02AC - 2.387FS – 1.865GROW

36

Table 4.6: Corporate Governance and accounts payable Management

Model Unstandardized

Coefficients

Standardized

Coefficients

T Sig. Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1

(Constant) 167.860 64.209 2.614 0.011

TN -10.861 10.461 -0.108 -1.038 0.302 0.902 1.109

BS -1.292 3.389 -0.039 -0.381 0.704 0.934 1.071

AC 1.020 5.390 0.020 0.189 0.850 0.833 1.201

FS -2.387 8.848 -0.029 -0.270 0.788 0.854 1.171

GROW -1.865 .441 -0.439 -4.225 0.000 0.896 1.116

There exist a non significant relationship between CEO tenure and accounts payable, board size

and accounts payable, audit committee and accounts payable and also the audit committee and

accounts payable. Valipour et al. (2012) similarly found a negative relationship between sales

growth and the level of accounts payable.

Table 4.7: Model Summary for accounts payable with Control Variables

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate F –statistic

1 .485 .235 .187 .15003 65.724

Source: 2008 -2012 survey data, researchers’ computation

37

The adjusted R2, also called the coefficient of multiple determinations, is the percent of the

variance in the dependent explained uniquely or jointly by the independent variables and is

18.7%. The F statistic is used to test the significance of R. Overall; the model is significant as F-

statistics is 65.724

38

CHAPTER FIVE

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

5.1 Introduction

This chapter presents a summary of the key findings of the study as well as the conclusions,

limitations of the study, and recommendations for further research.

5.2 Summary

The secondary data in this analysis covered a period of 5 years from 2008 to 2012. The

population of study was manufacturing firms listed at the NSE and was in operation during the

study period. After the screening process firms whose accounts were not available in all the years

of study or were not listed in the full were eliminated and from this screening process 2 firms

were eliminated leaving 15 to be studied in the research.

A test for multi collinearity was performed. All the variance inflation factor (VIF) coefficients

are less than 2 and tolerance coefficients are greater than 0.50. CEO tenure, board size, sales

growth, audit committee, and firm size explain 25.6% percent of the variance in accounts

receivable management efficiency of listed manufacturing firms in Kenya. CEO tenure, board

size, sales growth, audit committee, and firm size explain 6.70 percent of the variance in

inventory management efficiency of American manufacturing firms. The random and fixed

effects of independent variables on the dependent variables indicate that the efficiency of

working capital management differs from sector to sector and from year to year. The changes in

the measures of working capital management may be due to the changes in economic situations,

39

changes in the general level of interest rates that affect the opportunity cost of holding cash, and

changes in working capital management policies.

An independent audit committee enhances the efficiency of working capital by auditing cash

accounts, accounts receivable, accounts payable, and inventory accounts, which in turn,

minimizes agency problems and agency costs. The CEO tenure had also a positive correlation

with the level of working capital held and this could be due essentially to the fact that apart from

job security, the CEO is afforded the opportunity to witness the results of decisions taken

There is a negative relationship between efficient management of inventory and the measures of

corporate governance specifically CEO tenure, firm size and sales growth of the firm. However,

there exists a positive relationship between size of the board and audit committee. Further, there

existed a positive relationship between accounts payable and audit committee only. Otherwise a

negative relationship exists between CEO tenure, board size, firm size and the growth of the

firm. This result shows that as the corporate governance practices are implemented by a firm, the

level of accounts payable of the firm is minimized. This is a positive result since the intentions of

the firm is not to increase the level of accounts receivable to sub optimal level since it is going to

lead to the erosion of the firm credit rating.

5.3 Conclusions and Recommendation

The present study found that corporate governance improves the efficiency of working capital

management Kenyan manufacturing firms. Larger board size may not be in favor of Kenyan

manufacturing firms because it does not improve working capital management efficiency. The

40

positive correlation between corporate governance and inventory, account receivable and

payable means that foe efficient management of these working capital, there is need for the

establishment of an active audit committee and also the CEO tenure need to be enhanced to

achieve optimality of the working capital components. Further, the results suggest that managers

can create value for their shareholders by working positively with the audit committee and also

through establishment of the appropriate oversight over their actions.

Shareholders should also view the board of directors as a good corporate governance practice

and support the improvements and government controls to maintain the independence of the

board of directors. Outside directors should exist and they are useful tools for the independence

of the board. The members of the board of directors should realise that the structure of the board

is directly related to corporate performance and eventually the way working capital is managed

in the organization. There is need also for harmonization of corporate governance across all the

firms since some of the all the firms had different nature of corporate governance practices and

therefore leading to the difference in the management of performance of working capital

management.

5.4 Limitation of the study

This study is limited to the sample of Kenyan manufacturing firms. The findings of this study

could only be generalized to firms similar to those that were included in this research. In

addition, sample size is small. The scope of further research may be extended to other

components of working capital including cash, marketable securities, cash conversion cycle as

well as incorporation of more control variables.

41

There is also a potential inter relations between corporate governance practices and contextual

variables that were not taken into account. Recent studies have shown that certain corporate

governance practices are interconnected, and may be more effective in certain contexts. For

example, the results of Boujenoui and Zeghal (2006) tend to demonstrate that the ownership

structure, might possibly affect the governance mechanisms put in place by the companies.

Likewise, the corporate size might also affect the CEO tenure or board size. This relationship

was not considered in this study.

5.5 Suggestions for Further Research

Future research should investigate generalizations of the findings beyond the Kenyan firms.

Important control variables such as industry sectors from different countries, board composition,

etc. should also be used.

42

REFERENCES

Afza, T., & Adnan, S.M. (2007). Determinants of corporate cash holdings: A case study of

Pakistan. Proceedings of Singapore Economic Review Conference (SERC) 2007, August

01-04, Organized by Singapore Economics Review and The University of Manchester

(Brooks World Poverty Institute), Singapore 164-165.

Albright, S.C., Winston, W.L. and Zappe, J. (2011) Data Analysis And Decision

Making, Mason OH: South-Western Cengage Learning.

Appuhami, B.A.R., (2008). The impact of firms‘ capital expenditure on working capital

management: An empirical study across industries in Thailand. International

Management Review, 2008, 1, 8-21.

Brigham, E. F., and Ehrhardt, M. C. (2004). Financial Management: Theory and Practice. 11th

Edition, South-Western College Publishing, New York.

Borsch-Supan, A. and Koke, J. (2002), ―An applied econometrician‘s view of empirical

corporate governance studies‖, German Economic Review, 3 3, 295-326

Carpenter, M. D., and Johnson, K. H. (1983), ―The Association between Working Capital

Policy and Operating Risk‖, Financial Review, 18, 3, 106-107.

Christopher, S. B., and Kamalavalli, A. L. (2009). Sensitivity of profitability to working capital

management in Indian corporate hospitals.

43

Claessens, S., Djankor, S., Fan, J.P.H. and Lang, L.H.P. (2002), ‗‗Disentangling the incentive

and entrenchment effects of large shareholders‘‘, The Journal of Finance, 57 6, 2741-71

Dittmar, A., Mahrt-Smith, J. and Servaes, H. (2003), ―International corporate governance and

corporate cash holdings‖, Journal of Financial and Quantitative Analysis, 3, 1,

Drobetz, W. and Gru¨ninger, M.C. (2007), ―Corporate cash holdings: evidence from

Switzerland‖, Financial Markets Portfolio, 21, 293-324.

Eljelly, A. M. A. (2004). ―Liquidity-Profitability Tradeoff: An Empirical Investigation in an

Emerging Market‖, International Journal of Commerce and Management, 14, 2,

48-61.

Ferreira, M.A., & Vilela, A.S. (2004). Why do firms hold cash? Evidence from EMU countries.

European Financial Management, 10(2), 295-319.

Fox, M. and Heller, M. (2006), Corporate Governance Lessons from Transition Economy

Reforms, Princeton University Press, Princeton, NJ.

Ganesan, V. (2007), ―An analysis of working capital management efficiency in