The Devil is in the Details Insurance Hell … The Devil is in the Details Presenters: Judy...

47

Insurance Hell … The Devil is The Devil is in the Details in the Details Presenters: •Judy Thomson-Torosian, Service & Sales Manager for the MML Insurance Programs •John Thomas, Account Executive for the MML Insurance Programs Moderator: Mike Forster Director of Risk Management Michigan Municipal League

-

Upload

kristian-holt -

Category

Documents

-

view

224 -

download

2

Transcript of The Devil is in the Details Insurance Hell … The Devil is in the Details Presenters: Judy...

Insurance Hell … The Devil is in the DetailsThe Devil is in the Details

Presenters:

•Judy Thomson-Torosian, Service & Sales Manager for the MML Insurance Programs

•John Thomas, Account Executive for the MML Insurance Programs

Moderator:

Mike Forster

Director of Risk Management

Michigan Municipal League

WHAT IS RISK MANAGEMENT?

The process of making and

implementing decisions that will

minimize the adverse effects of

accidental and business loss on an

operation.

Standard PracticeStandard Practice

In municipal operations, In municipal operations, riskrisk

managementmanagement is often a is often a

reaction to an event reaction to an event

… … it seldom includes analysis it seldom includes analysis

and and

pre-planning.pre-planning.

GOAL: Meeting responsibility to taxpayers and employees

27 5

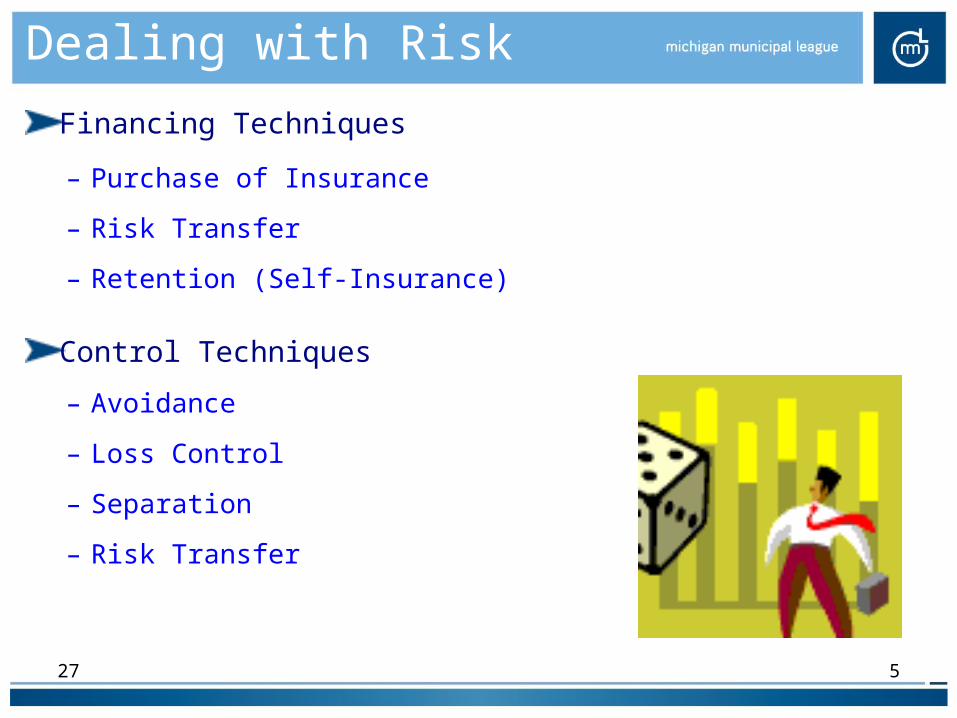

Dealing with Risk

Financing Techniques

– Purchase of Insurance

– Risk Transfer

– Retention (Self-Insurance)

Control Techniques

– Avoidance

– Loss Control

– Separation

– Risk Transfer

What to look for when purchasing insurance:

What coverages are included in the quote?

What type of coverage form is offered?

Is there an aggregate limit during the policy period?

Is property coverage provided on a blanket basis?

Is there a coinsurance factor on property?

What services are included in the quote?

Who will be providing service: claims, loss control, policy issuance and endorsements, answering questions, etc.

Experience of provider

Price

What coverages are included?

Liability:Public Officials E&OGeneral LiabilityMedical PaymentsPersonal & Advertising Injury

Property (buildings and contents)Inland MarineCrime

Automobile

Special EventsFireworksLiquor Liability

Underground Storage Tanks

Fiduciary Liability

Workers’ Compensation

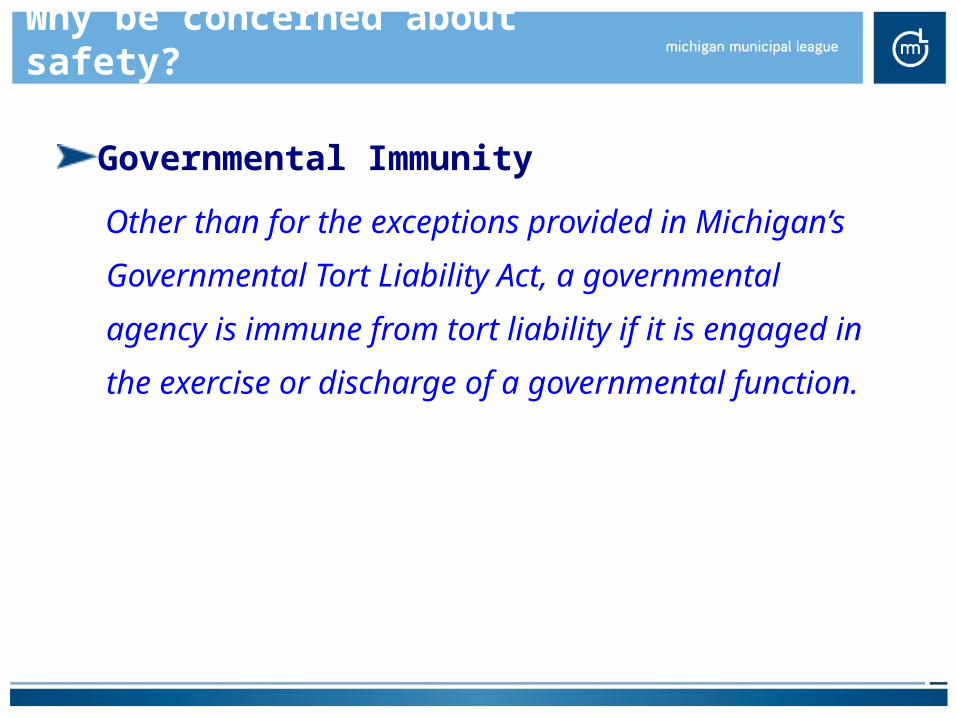

Why be concerned about safety?

Governmental Immunity

Other than for the exceptions provided in Michigan’s

Governmental Tort Liability Act, a governmental

agency is immune from tort liability if it is engaged in

the exercise or discharge of a governmental function.

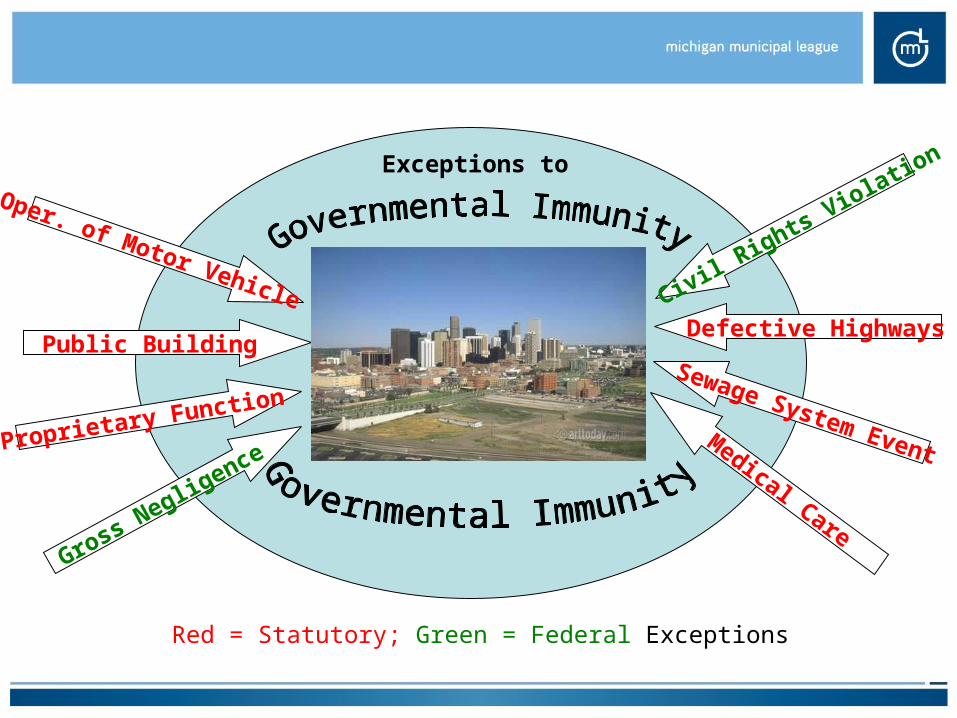

Defective Highways

Sewage System Event

Civil Rights Violatio

n

Proprietary Function

Public Building

Oper. of Motor Vehicle

Gross Negligence

Medical Care

Exceptions to

Red = Statutory; Green = Federal Exceptions

Operation of a Motor Vehicle

Governmental agencies shall be liable for bodily injury and property damage resulting from the negligent operation by any officer, agent, or employee of the governmental agency, of a motor vehicle of which the governmental agency is owner.

Defective Highway

Each governmental agency having jurisdiction over a highway shall maintain the highway in reasonable repair so that it is reasonably safe and convenient for public travel.

The duty of the state and county road commissions to repair and maintain highways … extends only to the improved portion of the highway designed for vehicular travel and does not include sidewalks, trailways, crosswalks …

Public Buildings

Governmental agencies have the obligation to repair and maintain public buildings under their control when open for use by members of the public.

Civil Rights Violation

Federal civil rights laws prohibit (among other things) discrimination based on race, color or national origin. They also prohibit police excessive force.

Gross Negligence

Public EmployeesEach officer, employee, volunteer, or member of a board is immune from tort liability for injury to a person or damage to property while in the course of employment if he/she:

Reasonably believes he or she is acting within the scope of his or her authority; and

The governmental agency is engaged in the exercise of a governmental function; and

The employee’s conduct does not constitute gross negligence that was the proximate cause of the injury or damages.

Gross Negligence is defined as conduct so reckless as to demonstrate a substantial lack of concern for whether an injury or property damage results.

Sewage System Event

Claimant must prove:

The governmental agency was an appropriate governmental agency,

The sewage disposal system had a defect,

The governmental agency knew, or should have known, about the defect,

The governmental agency failed to take reasonable steps to repair, correct or remedy the defect, and

The defect was a substantial proximate cause of the event.

Proprietary Function

The immunity of the governmental agency shall not apply to actions to recover for bodily injury or property damage arising out of the performance of a proprietary function.

Proprietary Function shall mean any activity which is conducted primarily for the purpose of producing a monetary profit excluding however any activity supported by taxes. In Hyde v University of Michigan, the Michigan Supreme Court established two tests to determine whether a proprietary function exists: 1) the activity must be conducted primarily for the purpose of producing a pecuniary* profit and 2) the activity cannot be normally supported by taxes and fees.

* pecuniary – monetary or financial.

Medical Care

No immunity to a governmental agency or an employee or agent of a governmental agency with respect to:

providing medical care or treatment to a patient, except medical care or treatment provided to a patient in a hospital owned by the Dept. of Community Health or operated by the Dept. of Corrections.

Liability Concerns

What is the type of Coverage Form?

Is the policy subject to Aggregate Limits?

Is Legal Coverage within or outside of the Liability Limit?

What is the deductible?

Is there a Self-Insured Retention?

How broad is the coverage? (i.e., Back & Future Wages for Employment, Sewer Back-up, Land Use)

What type of Liability Coverage Form is offered?

Occurrence (Claim can be filed at any time)

Claims-Made (Claim must be filed during the policy term, or no coverage)

Liability Concerns

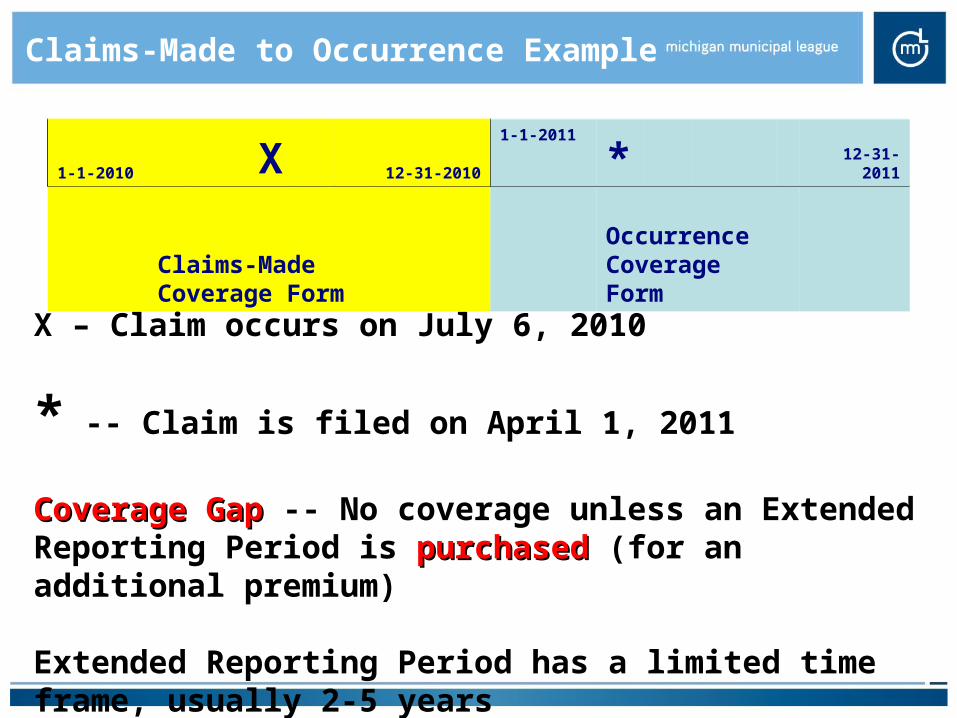

Claims-Made to Occurrence Example

1-1-2010 X 12-31-20101-1-2011 * 12-31-2011

Claims-Made Coverage Form

Occurrence Coverage Form

X – Claim occurs on July 6, 2010

* -- Claim is filed on April 1, 2011

Coverage GapCoverage Gap -- No coverage unless an Extended Reporting Period is purchasedpurchased (for an additional premium)

Extended Reporting Period has a limited time frame, usually 2-5 years

1-1-2010 X 12-31-20101-1-2011 * 12-31-2011

Claims-Made Coverage Form

Occurrence Coverage Form

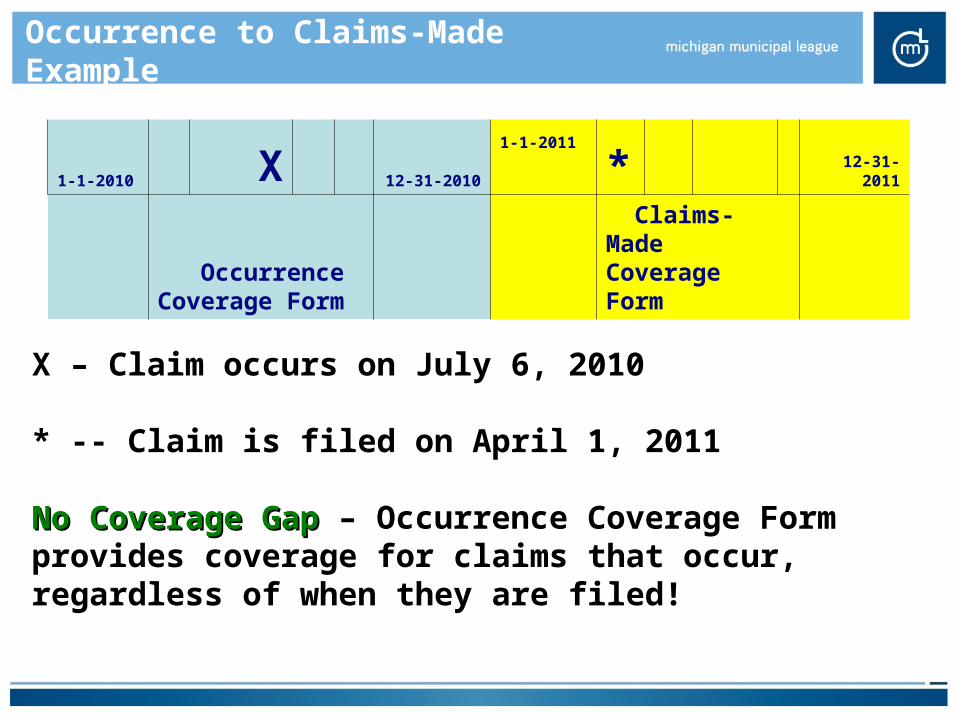

Occurrence to Claims-Made Example

1-1-2010 X 12-31-20101-1-2011 * 12-31-2011

Occurrence Coverage Form

Claims-Made Coverage Form

X – Claim occurs on July 6, 2010

* -- Claim is filed on April 1, 2011

No Coverage GapNo Coverage Gap – Occurrence Coverage Form provides coverage for claims that occur, regardless of when they are filed!

Is there an aggregate limit during the policy period?

May apply to one line of coverage or to the entire liability policy

If claims reach aggregate limit, coverage stops

Per occurrence limits with no aggregate are best!

i.e., Aggregate Limit -- $5,000,000

Additional Claims:

(No Coverage)

$1,000,000

$250,000

$15,000

$5,000,000 Aggregate

$5,000,000 in Claims

Actual Claim #1-- $5,000,000

Rotted tree was scheduled to be removed

Tree was not removed as scheduled

Woman went for a walk during a storm

Tree came down and landed on woman

Woman was left as a quadriplegic

Cost of Claim -- $5,000,000

City’s total incurred for the 10 claims for this policy period -- $5,022,858.02

If $5,000,000 Aggregate Limit -- $22,858.02 with no coverage

But there was No Aggregate and all claims paid!

Actual Claim #2 -- $10,000,000

Police restrained and arrested large disturbed man

Man died in custody

Cost of Claim -- $10,000,000

City’s total cost for the 298 Claims for this policy period -- $10,764,394.29

If $10,000,000 Aggregate Limit -- $764,394.29 with no coverage

But there was No Aggregate and all claims paid!

Liability Concerns

Is Legal Coverage within or outside of the Liability Limit?– Legal within the liability limit reduces the amount

available to pay “Damages” (Awards)

Liability Concerns

Deductibles -- A portion of a covered loss that is not paid by the insurer. These add to your cost, whenever you have a claim.

Self Insured Retention -- A dollar amount specified in an insurance policy (usually a liability insurance policy) that must be paid by the insured before the insurance policy will respond to a loss.

Some policies include both!

Property Concerns

Is property coverage provided on a blanket basis or per location basis?

Is property insured with a Coinsurance Factor?

How is Property in the Open Covered?

How is Boiler & Machinery Covered?

Property Concerns

Is property coverage provided on a blanket basis or per location basis?

A blanket limit covers all scheduled buildings and contents under one combined per occurrence limit

If coverage is written per location (or per building) … this increases the chance of under-insuring a piece of property! If a building is scheduled for $500,000, is destroyed and costs $750,000 to replace, coverage is $500,000. You pay the difference of $250,000.

Is property insured with a Coinsurance Factor?

Premium credit for agreeing to insure-to-value (80%, 90%, 100%)

Formula: Did/Should x Coinsurance %

Example: Building is insured for $1,000,000 with a 100% Coinsurance Factor … the carrier determines that building’s replacement cost value is $2,000,000

$1,000,000/$2,000,000 X 100% (1/2) = only ½ of the claim is actually paid … you pay the rest!

Property Concerns

Property Concerns

Property in the Open (PIO) – not a building

Examples of property in the open – fences, street lights, traffic lights, playgrounds, tennis courts, barbeques, outdoor clocks, fountains

Many policies require that coverage for PIO is dependent on proximity to scheduled property – i.e., within 100 or 1,000 feet

If not scheduled … no coverage

Property Concerns

Boiler & Machinery (or mechanical breakdown) – This coverage encompasses much more than just boilers and pressure vessels. It also can include refrigeration equipment, air conditioning equipment, various types of piping, turbines, engines, pumps, compressors, blowers, gearing, shafting, electric motors, generators, transformers and assorted other types of mechanical and electrical equipment.

Many policies provide only a $1,000,000 limit for this exposure rather than the full blanket limit!

Property Concerns

Is there a limit on Glass or is it covered in total as part of the property blanket?

Many carriers include a dollar limit or maximum for glass. It is better to have glass included in the property blanket limit.

Automobile Concerns

Physical Damage

– What are deductibles?

– Are fire vehicles insured for an Agreed Amount Valuation?

Michigan No-Fault

Who is driving your vehicles?

Crime Concerns

What can you do to protect public entity money?

– Zero Balance Accounts

– Check with your bank before a loss to see what they protect and what they do not

– Maintain Accountability within your organization

Other Considerations

Service

Pools

Terrorism

Fiduciary Liability

Pollution

Workers’ Compensation (too big a topic to discuss in detail)

What service will be provided and by whom?

Claims (Is it local? Do they understand MI Governmental Immunity? Are claims handled by carrier or farmed out? What percentage of their clients are public entities?)

Loss Control (The knowledge of OSHA without the fines)

Policy Issuance and Endorsements

Answering Questions

Resolving Differences

Pools

If they are 100% reinsured, they are not a Pool

What is the average size of their Members?

Some Pools have the potential to assess Members to pay for the claims of other Members (the MML Liability & Property Pool does not)

How are sales people compensated? (The MML Pool does not pay sales commissions. Coverage suggestions are made to assist Members.)

Terrorism

What is TRIA?

What are the exposures?

Fiduciary Liability

Once money is paid by a public entity into an Employee Retirement account, the money no longer belongs to the public entity and that account needs its own Crime coverage.

Pollution – an Exclusion

This exposure needs a separate policy

Assess your exposure?– Do you have USTs or ASTs?– Do you have a Sewage Treatment Plant?– Is there potential for spillage into local waterways?– Do you separate your storm water and sewage?

Workers’ Compensation

Coverage A – Statutory Coverage that pays for an injured workers’:

Lost Time Benefits

Medical Expenses

Vocational Rehabilitation

Burial Expenses

Coverage B – Employers Liability

What You Need to Know:

Exclusive Remedy

Consider designating a medical clinic/facility for the initial treatment of workers who are not seriously injured. In most instances, the employee should treat with the employer’s designated medical clinic/facility for the first ten days following the injury.

– This ensures consistent quality of care, allows proper monitoring and controls your costs.

– Contact a local clinic to set up a relationship and establish procedures

What You Need to Know:

Investigate and report claims promptly

Report all claims – Michigan requires all WC medical bills to be processed through a fee schedule, reducing bills to per procedure maximum.

What to Look for on a Certificate of insurance:

Carrier’s Rating *

Limits (How much remains?*) – if applicable, request “per event” coverage

Deductibles

Reputation of Named Insured *

Cancellation Notice Requirements

Are Medical Payments Included?

* (typically not on the Cert. – you have to ask – If you are additional insured, ask for a copy of the endorsement.)

Certificate of Insurance

Agency

Insured

Insurance Carrier

Policy Term & Limits

Additional Insured?

Certificate HolderAgent’s Signature

Is Med. Pay Included?

Cancellation Notice

Questions